The Volterra Stein-Stein model with stochastic interest rates

Abstract

We introduce the Volterra Stein-Stein model with stochastic interest rates, where both volatility and interest rates are driven by correlated Gaussian Volterra processes. This framework unifies various well-known Markovian and non-Markovian models while preserving analytical tractability for pricing and hedging financial derivatives. We derive explicit formulas for pricing zero-coupon bond and interest rate cap or floor, along with a semi-explicit expression for the characteristic function of the log-forward index using Fredholm resolvents and determinants. This allows for fast and efficient derivative pricing and calibration via Fourier methods. We calibrate our model to market data and observe that our framework is flexible enough to capture key empirical features, such as the humped-shaped term structure of ATM implied volatilities for cap options and the concave ATM implied volatility skew term structure (in log-log scale) of the S&P 500 options. Finally, we establish connections between our characteristic function formula and expressions that depend on infinite-dimensional Riccati equations, thereby making the link with conventional linear-quadratic models.

Keywords: Gaussian Volterra processes, volatility, interest rate, memory, Fredholm resolvents and determinants, Fourier pricing, Riccati equations.

1 Introduction

Modeling the joint dynamics of interest rates and equity is crucial for pricing and hedging hybrid derivatives. These products, which include equity-linked interest rate derivatives, callable hybrid structures, and quanto options, depend on the interaction between stock prices, interest rates, and their volatilities. A realistic model must capture the well-documented stylized facts of each underlying as well as accurately describe their dependency structure to ensure consistent pricing and risk management across asset classes.

Empirical evidence reveals persistent memory effects in historical time series of interest rates and asset volatility and slow decay of their autocorrelations structures, see Cont (2001); Dai and Singleton (2003); McCarthy, DiSario, Saraoglu, and Li (2004).

Beyond historical data, robust and universal patterns emerge in the term structures of option prices across a broad range of maturities. Specifically,

- (i)

-

(ii)

for stock indices such as the S&P 500: the term structure of the At-The-Money (ATM) skew of the implied volatility of call and put options, when plotted in log-log scale, exhibits typically a concave shape. In addition, the ATM skew displays an approximately linear decrease at long maturities suggesting a power-law decay, though only for sufficiently large maturities, see Abi Jaber and Li (2024); Bayer, Friz, and Gatheral (2016); Bergomi (2015); Delemotte, De Marco, and Segonne (2023); Guyon and El Amrani (2023).

Various approaches have been developed to jointly model equity and interest rate dynamics, often by extending stochastic volatility frameworks to include stochastic interest rates. For instance, Singor, Grzelak, van Bragt, and Oosterlee (2013); Grzelak, Oosterlee, and Van Weeren (2011) incorporated stochastic rates into the Heston (1993) model, while van Haastrecht et al. (2009); van Haastrecht and Pelsser (2011) adapted the Stein and Stein (1991) and Schöbel and Zhu (1999) volatility models with multi-factor Hull and White (1993) interest rates. However, these frameworks rely on Markovian dynamics with a single characteristic time scale for at least one of the two risk factors, and fail to capture the complex shapes of term structures observed on the market: they lead either to term structures of cap/floor implied volatilities that decrease monotonically - at odds with the empirically observed hump-shaped patterns - or ATM skews that decay too quickly for longer maturities. While such models offer analytical tractability, their inability to align with empirical data highlights the need for alternative approaches that incorporate more flexibility.

To address these limitations, we propose a flexible yet analytically tractable model based on Volterra processes, capable of accurately reproducing these empirical term structure features while remaining computationally efficient for option pricing and model calibration. Our motivation for incorporating Volterra processes stems from their proven ability to capture key stylized facts of volatility (Abi Jaber and Li (2024); Bayer, Friz, and Gatheral (2016); Gatheral, Jaisson, and Rosenbaum (2018); Guyon and Lekeufack (2023)) and interest rates (Abi Jaber (2022b); Benth and Rohde (2019); Corcuera, Farkas, Schoutens, and Valkeila (2013); Hainaut (2022)).

We propose a hybrid equity-rate modeling framework where both volatility and interest rates are driven by (possibly correlated) Gaussian Volterra processes, unifying a broad class of Markovian and non-Markovian models. Building on the Volterra Stein-Stein model with constant interest rates studied by Abi Jaber (2022a), we extend the framework to incorporate stochastic interest rates, capturing key market features more effectively. Our main contributions can be summarized as follows:

-

•

Mathematical tractability and pricing: Despite the non-Markovian nature of the processes, we derive explicit pricing formulas for zero-coupon bonds and call and put options on zero-coupon bonds, see Propositions 2.1 and 2.2. We obtain a semi-explicit expression for the characteristic function of the log-forward index in terms of Fredholm (1903) resolvents and determinants, enabling Fourier-based pricing methods, see Theorem 3.1. This result extends the formula derived by Abi Jaber (2022a) for constant interest rates.

-

•

Flexibility and joint calibration: We calibrate our model to market data and achieve excellent fits for: (i) the humped-shaped term structure of ATM implied volatilities for cap options by incorporating in interest rates mean reversion as well as long-range memory with a fractional kernel, see Figure 3, and (ii) the concave ATM implied volatility skew term structure (in a log-log plot) of S&P 500 options using a shifted fractional kernel, see Figure 8. On the selected calibration date, our estimated parameters yield a negative implied correlation between short rates and the index, aligning with historical observations. Furthermore, we compare the impact of a singular power-law kernel for volatility (rough volatility) and demonstrate that rough models underperform our non-rough counterparts in capturing the entire volatility surface, confirming within our framework the findings of Abi Jaber and Li (2024); Delemotte, De Marco, and Segonne (2023); Guyon and Lekeufack (2023).

-

•

Link with conventional linear-quadratic models: We establish connections between our characteristic function formula and expressions that depend on infinite-dimensional Riccati equations, see Proposition 5.1 for general kernels and Proposition 5.2 for completely monotone convolution kernels. The latter formula establishes the link with conventional linear-quadratic models (Proposition 5.3), allows us to recover closed-form solutions in specific cases such as in van Haastrecht, Lord, Pelsser, and Schrager (2009) (Corollary 5.1), and leads to another numerical approximation method based on multi-factor approximations in the spirit of Abi Jaber and El Euch (2019), see Section 5.3.

The paper is outlined as follows. In Section 2, we introduce the Volterra Stein-Stein model with stochastic rates, derive pricing formulas for zero-coupon bonds, and analyze the forward index dynamics. Section 3 provides a semi-explicit expression for the characteristic function of the log-index. In Section 4, we validate the Gaussian Volterra framework by calibrating the interest rate and volatility models to market data. Finally, Section 5 establishes connections with conventional linear-quadratic models, derives simplified forms for Markovian volatility models, and introduces a multi-factor approximation for the characteristic function for completely monotone kernels.

2 The Volterra Stein-Stein and Hull-White model

We fix a finite horizon and a filtered probability space where stands for one risk-neutral probability measure and the filtration satisfies the usual conditions. We consider a financial market with a financial index denoted by that depends on both stochastic interest rate and volatility with dynamics

In order to incorporate memory effects, we model the two risk factors by general Gaussian Volterra processes, combining a Volterra Stein-Stein model for , as studied by Abi Jaber (2022a), with a Volterra Hull-White model for :

| (2.1) | ||||

| (2.2) |

where are correlated Brownian motions such that

with , , , and the kernels and satisfy the following definition.

Definition 2.1.

A kernel is a Volterra kernel of continuous and bounded type in if for and

Finally, is a time-dependent function used to perfectly fit the initial term-structure of market bond prices, see Remark 2.1, and is such that

| (2.3) |

Under Definition 2.1 and for locally square integrable, it can be shown there exists a strong solution to (2.1) and (2.2), such that

this follows from an adaption of (Abi Jaber, 2022a, Theorem A.3). In particular, the joint process is a Gaussian process.

This class of models encompasses well-known Markov and non-Markovian Volterra processes. For an introduction to Volterra processes, we refer among others to (Hainaut, 2022, Chapter 9). Several kernels satisfy Definition 2.1 such as:

-

•

the constant kernel: , then we obtain Markovian models such as the classical Stein and Stein (1991) or Schöbel and Zhu (1999) model for volatility and the Hull and White (1993) model for short-term interest rate, such models have been studied by van Haastrecht, Lord, Pelsser, and Schrager (2009); Grzelak, Oosterlee, and Van Weeren (2012),

-

•

the exponential kernel: with , then we also obtain Markovian models but with modified mean-reversion level and reversion speed,

-

•

the fractional kernel: with a Hurst index then we obtain non-semimartingale and non-Markovian long or short memory fractional processes whenever . For the kernel is singular at , we get rough models as for example the rough Stein-Stein model studied by Abi Jaber (2022a) and for , we obtain long-memory processes as, for example, the fractional version of the Hull and White model,

-

•

the shifted fractional kernel: with and , then we obtain path-dependent processes that are semi-martingales but non-Markovian processes. Compared to the fractional kernel, the shifted fractional kernel has no singularity as , and can achieve faster decays than the fractional kernel for larger with coefficients .

2.1 Pricing Zero-Coupon bonds and interest rate derivatives

Let us now consider the pricing of zero-coupon bond as well as interest rate derivatives in our framework. The price at time of a maturity zero-coupon bound is denoted by and defined by

We now show that even considering a general Volterra Hull and White model for interest rate dynamics, the zero-coupon bond price admits an analytic expression. To this end, we introduce the concept of resolvent associated to a kernel and give some examples in Table 1. Note that we consider the resolvent definition of Abi Jaber (2022a), which may differ from other papers.

Definition 2.2.

| Kernel | Resolvent | |

|---|---|---|

Proposition 2.1.

Let us define, for by

| (2.4) |

with the resolvent associated to with the convention if . The price of the zero-coupon bond at time is given by

| (2.5) |

with the time-dependent function given by

Moreover, the dynamics of ( are given by

with

| (2.6) |

Proof.

Using the resolvent associated to the kernel and using (Abi Jaber, 2022a, Theorem A.3), we have that is the strong solution of the following equation

with the convention if In this case, we have that, for

Using the definition of given by (2.4) together with an application of stochastic Fubini’s theorem, we obtain that

Thus, for conditional on , the random variable is Gaussian with mean

and variance

Therefore, we readily deduce that

and we finally obtain that

∎

Remark 2.1.

Proposition 2.1 provides a natural way to estimate the function such that the interest rate model matches perfectly the initial term-structure of market bond prices. In fact from (2.5), we deduce that

Thus, if we assume that, for some given maturities , we have the initial term-structure of market bond prices , and that is piecewise constant such that

| (2.7) |

then

Based on the expression for the pricing of zero-coupon bonds, we can now easily deduce explicit expressions for the pricing of zero-coupon bond call and put options.

Proposition 2.2.

Let us consider maturity zero-coupon bond call option and put option with and the strike of the option. The arbitrage-free price at time of the call option is given by

and the price of the put option is given by

where is the cumulative function of a normal distribution and

| (2.8) |

| (2.9) |

where

| (2.10) |

Proof.

Let us consider the call option. We know that the arbitrage-free price of a call on zero-coupon bond satisfies

From Proposition 2.1, we know that under the risk-neutral measure

Therefore, for we obtain that under the forward measure 111We introduce the forward measure in Section 2.2., the zero-coupon bond dynamics is given by

Moreover, under we have that

and we deduce that

where is the cumulative function of a normal distribution and are given by (2.8)-(2.9). Finally, using the call/put parity, we easily deduce the form of the put price. ∎

Based on zero-coupon bonds call or put options, we can price cap and floor options since, as explained in Brigo and Mercurio (2006), cap and floor options can be decomposed into a sum of zero-coupon bonds options. In fact, the cap and floor payoffs are of the form

where is the reference rate and are the payment date. Using Brigo and Mercurio (2006), we have that the price at time , of cap and floor options is given by

This enable us to calibrate our Gaussian Volterra model for interest rate to the market data of cap and floor options for any Volterra kernel .

2.2 Forward measure and pricing of derivatives on the index

Let us now focus on the pricing financial derivatives on the index in our framework. Standard arguments imply that the arbitrage-free price of financial derivatives is obtained by taking the discounted value of the payoffs under a risk-neutral measure . In this case, if we consider a general maturity derivative of the form

where is a continuous positive function, the arbitrage-free price at time is given by

| (2.11) |

In the presence of stochastic interest rates, it is impossible to obtain a more explicit form of the price if we consider the formulation under the risk-neutral measure. One technique for dealing with this problem is to switch from the risk-neutral measure to the forward neutral measure. Thus, let us introduce the forward neutral measure denoted by which is equivalent to the risk-neutral measure . The change of measure from the risk-neutral measure to the forward measure satisfies

We can now introduce the forward index denoted by and defined as, for

Since under the forward measure the financial index divided by the zero-coupon bond is a martingale, we obtain that the process has the following dynamic

| (2.12) |

with

| (2.13) |

where is a dimensional correlated Brownian motion under the forward measure and

By combining the forward measure and the forward financial index, we obtain that the arbitrage-free price of a derivative (2.11) satisfies

By switching from the risk-neutral measure to the forward measure, we get a simpler framework for pricing financial derivatives. In the following, we will show that the characteristic function of the log-forward index admits an explicit form. This opens the way to a fast pricing of financial derivatives using Fourier methods. Moreover, using hedging approaches developed in several papers Abi Jaber and Gérard (2024); El Euch and Rosenbaum (2018); Motte and Hainaut (2024), some hedging strategies can also be deduced by Fourier methods for contingent claims that admit a Fourier representation.

3 The characteristic function of the log-forward index

The aim of this section is to derive an analytical form of the characteristic

function of the log-forward index with dynamics

(2.12) under and apply it for Fourier pricing of derivatives on the index.

We start by recalling some results on operator theory in Hilbert spaces as well as introducing some notations. Let be a linear compact operator acting on . Then, is a bounded operator i.e. there exists such that, for all , and for , the closure of is compact in . is an integral operator if a linear operator induced by a kernel such that, for and

Moreover, if is a integral operator, then is a Hilbert-Schmidt operator on into itself and is in particular compact. The trace of an operator, denoted by , is defined for operators of trace class where a compact operator is said to be of trace class if

for a given orthonormal basis . For more details about the trace of an operator, we refer to (Abi Jaber, 2022a, Section

A) and the references therein.

Let us now introduce some notations and properties:

-

•

denotes the following product on

Note that is the inner product in but not in .

-

•

For any kernels the product is defined by

-

•

For a kernel denotes the adjoint kernel such that, for

and is the operator induced by

-

•

id denotes the identity operator such that , .

3.1 Semi-explicit expression

We now derive a semi-explicit form for the characteristic function of

the log-forward index in our framework.

To this end, we consider an approach similar to Abi Jaber (2022a) which deduces the explicit form of the log-price characteristic function in equity markets with a Volterra Stein-Stein volatility model. Here, we show that this result can be extended to a framework where interest rates are also stochastic. As in Abi Jaber (2022a), we consider the expression of the adjusted conditional mean of and then we define a linear operator in that will be useful for the expression of the characteristic function. The adjusted conditional mean of denoted by is given by

and we can easily show that reduces to

Definition 3.1.

For such that the operator acting on is defined by

| (3.1) |

where:

-

•

is the integral operator induced by and the adjoint operator,

-

•

and

-

•

is the adjusted covariance integral operator such that

with the integral operator associated with the covariance kernel given by

Note that using similar arguments than in the proof of (Abi Jaber et al., 2021a, Lemma 5.6.), we can prove that is well defined and is a bounded linear operator acting on .

Based now on and , we deduce a semi-explicit expression of the characteristic function. The methodology used in Abi Jaber (2022a) to deduce the analytical expression of the characteristic function can be extended to a framework with stochastic interest rates. Nevertheless, to extend these results, we need to consider the process defined, for such that as

in order to take account of the correlations between the processes, recall the definition of in (2.6). In particular when , reduces to and we recover the framework of Abi Jaber (2022a).

Theorem 3.1.

-

•

given by (3.1),

-

•

where is the strong derivative of induced by the kernel

-

•

Proof.

The proof is given in Section 6. ∎

3.2 Numerical implementation and Fourier pricing

For a practical perspective, we propose a natural way of approximating

the expression of the characteristic function when we consider general

Volterra kernels that lead, for example, to non-Markovian models such

as the fractional or shifted fractional kernels. This approximation is

based a natural discretization of the inner product .

In this section, for sake of simplicity, we fix .

As proposed by Abi Jaber (2022a), we can approximate the explicit

expression of the characteristic function (3.2)

by an approximate closed form solution using a simple disctretization

of the operator à la Fredholm. To

this end, for fixed we consider a partition of

with for Then,

for such that

we can approximate the operator by a

matrix denoted and defined by

| (3.3) |

where is the identity matrix, is the lower triangular matrix such that

| (3.4) |

and

with the discretized covariance matrix given by

| (3.5) |

When we consider kernels of the form

with for and for , we observe that the matrix (3.4)-(3.5) can be computed in closed form

where and is the Appell hypergeometric function of the first kind given by

with the Pochhammer symbol such that

Based on the approximate operator, we now deduce a closed form approximate solution to the characteristic function. Relying on Abi Jaber and Guellil (2025), we have that , that appears in (3.2), can be rewritten in term of the Fredholm determinant such that

where is the net number of times crosses the negative real axis between and . The reason we have rewritten is that this enables us to use the Fredholm determinant to calculate , instead of having to discretize the trace-dependent expression which would require the computation of for several values of . In this case, if for and for such that we consider the dimensional vector with , a natural approximation of the characteristic function is given by

| (3.6) |

with:

-

•

the approximate operator defined by (3.3),

-

•

-

•

Remark 3.1.

To compute , we need to compute the integral of the form , where is defined by (2.6) and admits an explicit expression for some well-known kernels as revealed by Table 1. However, except for the indicator or exponential kernels, the integral does not have an explicit expression and needs to be computed numerically.

Let us now discuss the pricing of equity derivatives. From Section 2.2, we know that the arbitrage-free price, at time , of a financial derivative is given by

where is the price of a zero-coupon bond of maturity . Exploiting the Fourier link between the density function and the characteristic function, we can easily deduce how to efficiently compute the price of vanilla options such as call and put options using a Fourier method. For , let us consider defined by

then, from Lewis (2001), the price at time of a call option is given by

| (3.7) |

where . Using a numerical integration

of (3.7), we can efficiently price call options

as well as calibrate the model to equity market data. In this paper,

we use the Gauss-Laguerre quadrature numerical integration which has

been demonstrated to be efficient in the context of option pricing

(see Abi Jaber and Gérard (2024)). In practice, for a general kernel function ,

such as the fractional or path-dependent kernels, we have to approximate

the expression of the characteristic function of

that appears in the integral (3.7). To this

end, we use the discretization approach detailed above.

Note that such approximation procedure is not always necessary. In

fact, as we will see later in Section 5.2,

if we consider the Stein-Stein volatility model i.e. ,

the analytic expression of the characteristic function is more explicit

as shown by Corollary 5.1.

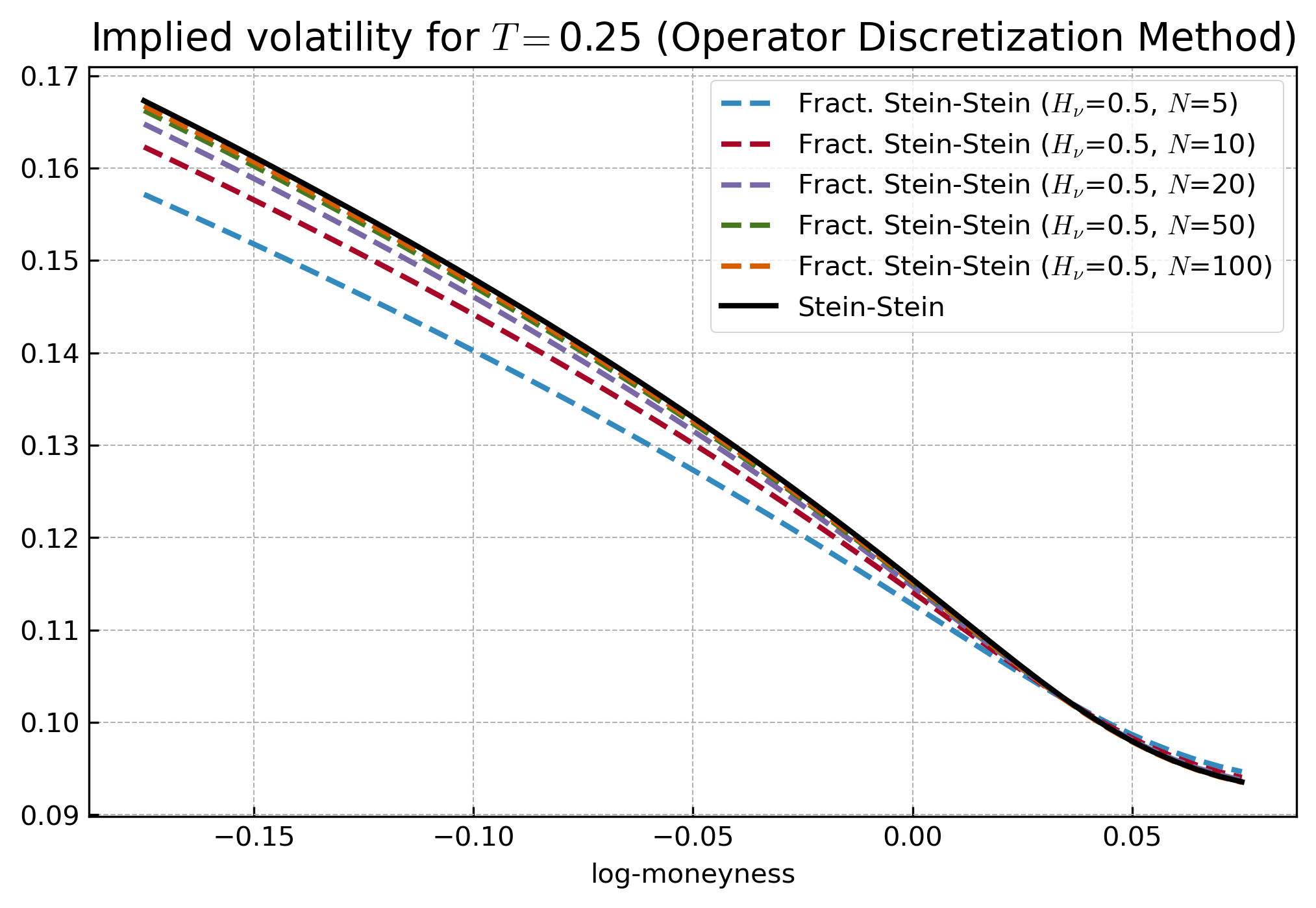

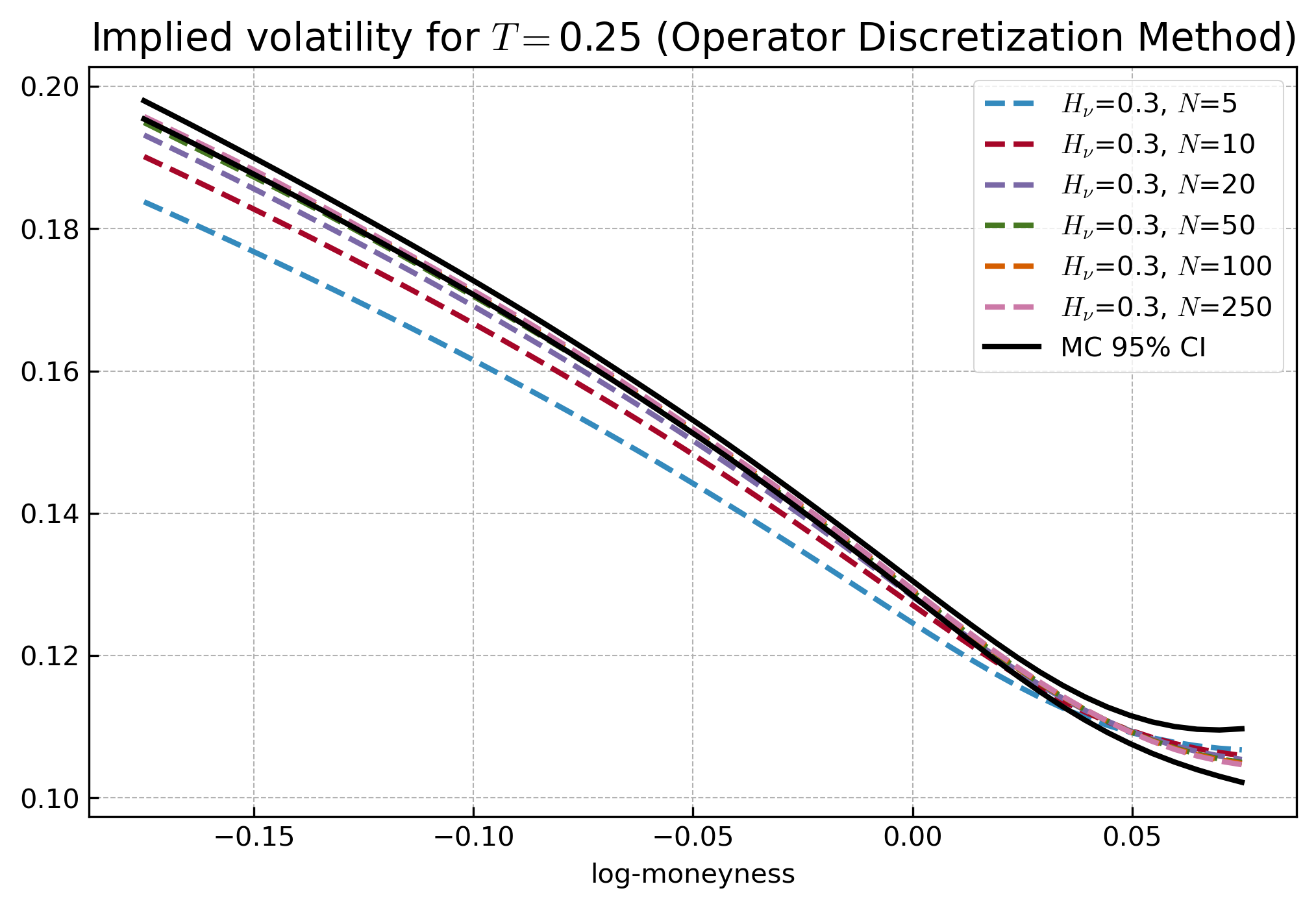

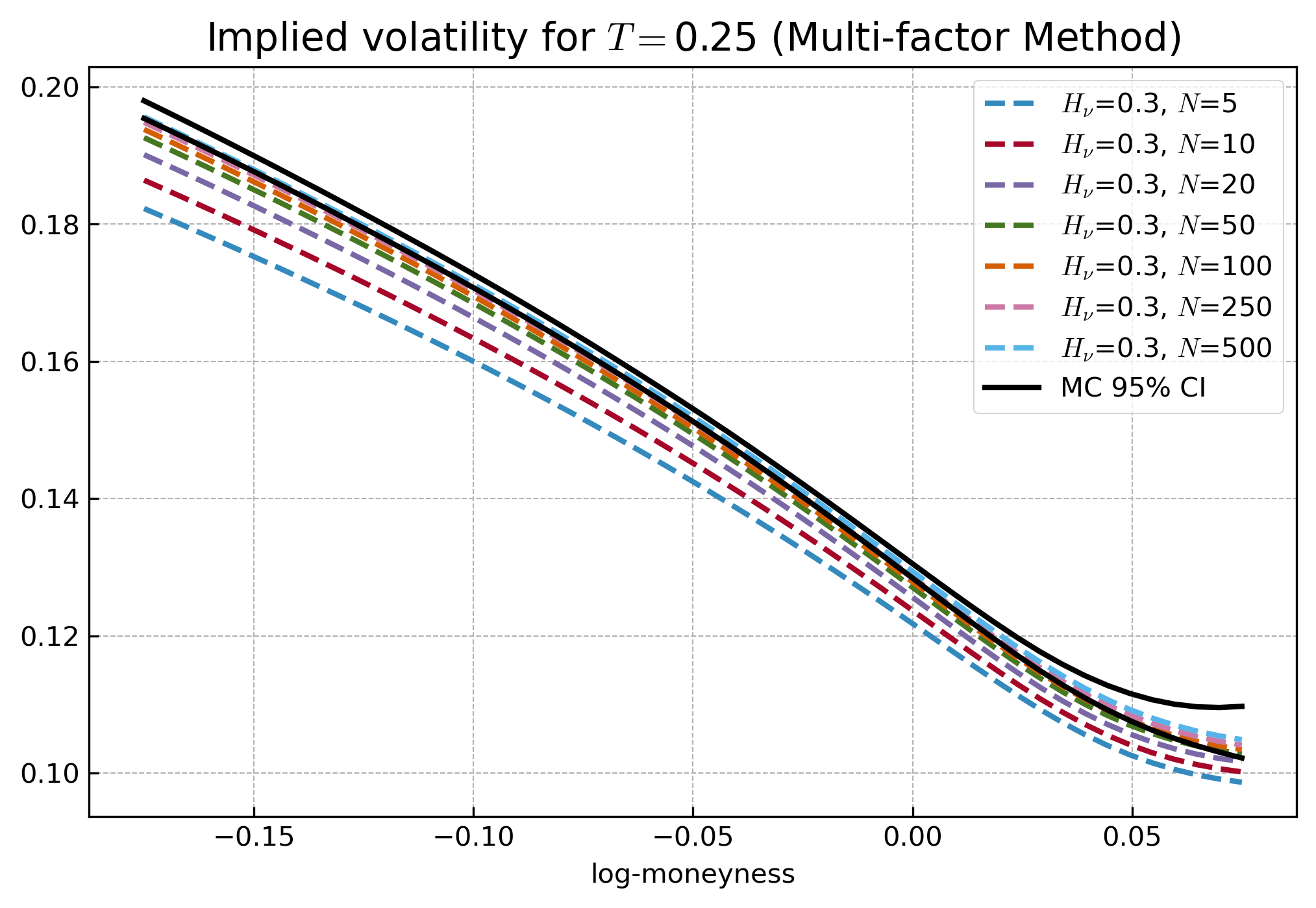

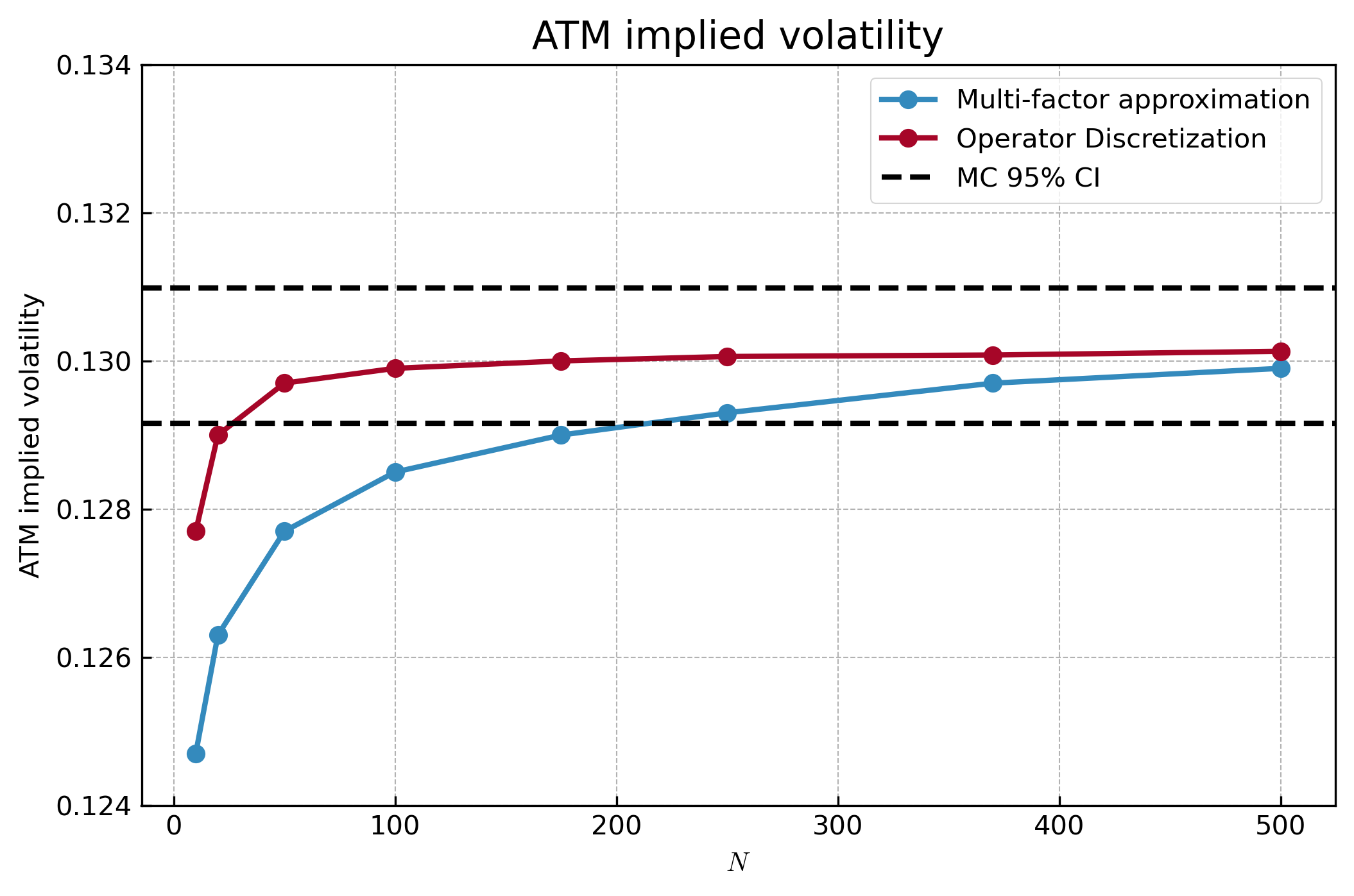

The closed form approximate solution of the characteristic function (3.6) has been proposed in different papers Abi Jaber (2022a, b). However, it is important to note that theoretically, a general convergence result when tends to infinity has not yet been demonstrated. We nevertheless verify empirically the convergence of this approximation method as . For this purpose, we restrict ourselves to a one-factor Hull and White model for the interest rate i.e. and we consider the fractional kernel for the volatility . Without loss of generality, we fix arbitrarily the model parameters to

Figure 1 presents the implied volatility dynamics generated by the operator discretization as well as . As expected, we observe a relative fast convergence as the number of discretization factors increases.

4 Calibration to market data

In this section, we highlight the relevance of our framework for calibration on

market data. To this end, we place ourselves in an equity market context

where the process represents an equity

stock index. Our calibration instruments from market data, are interest rate options, caps and floors,

as well as equity vanilla call and put options. Let us now calibrate the models to the market data in order to validate

the relevance of the introduced framework. To this end, we consider

market data of 25/08/2022 consisting of USD 3M Libor yield curve and

ATM USD cap implied volatility data from Bloomberg, and S&P500 implied

volatility data purchased from the CBOE website222https://datashop.cboe.com/..

The calibration procedure takes place in two stages. First we calibrate

the interest rate parameters using the USD 3M Libor yield curve and

ATM cap data. Then, using these calibrated interest rate parameters,

we calibrate the volatility and correlation parameters based on S&P500

implied volatility data.

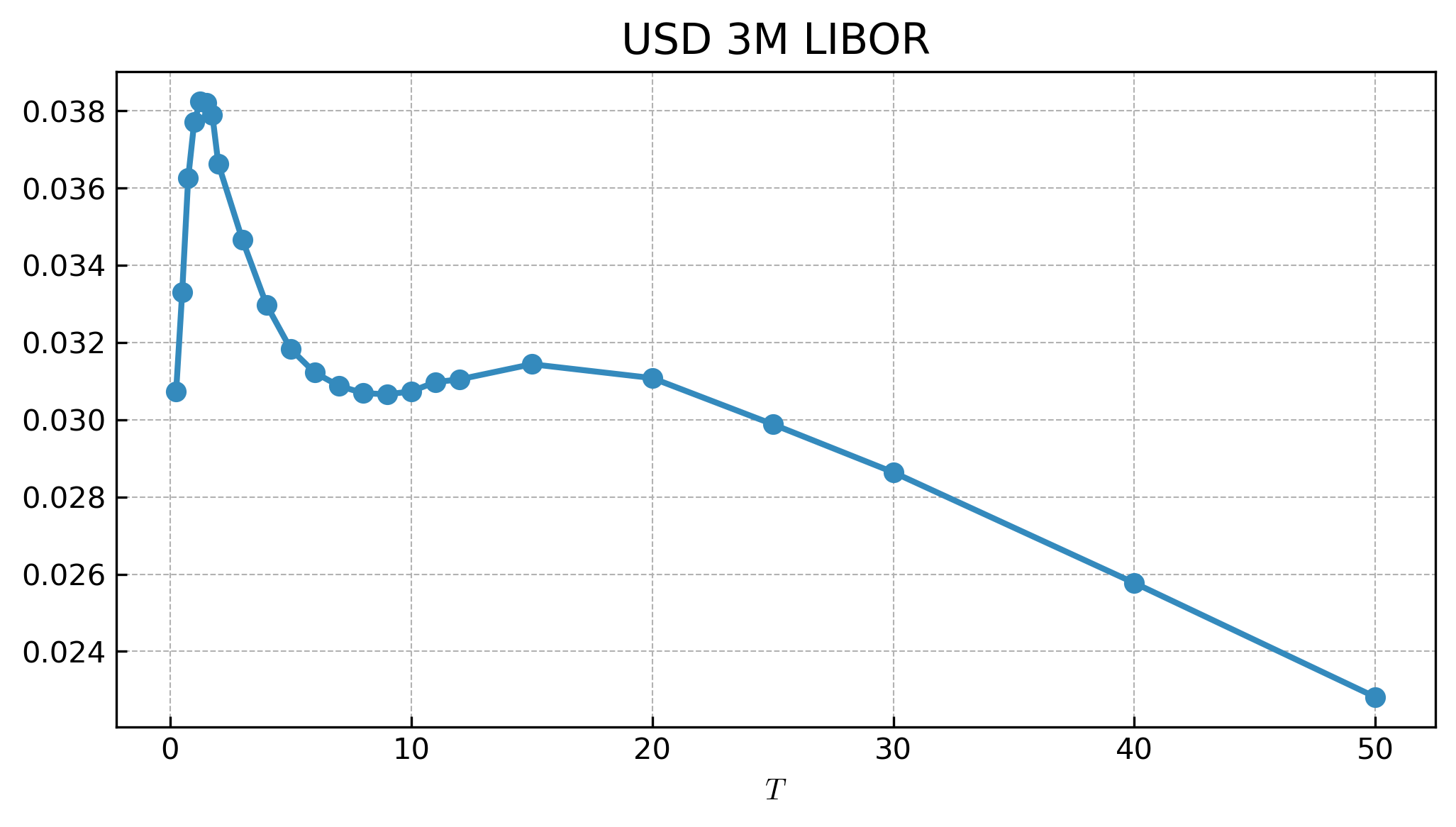

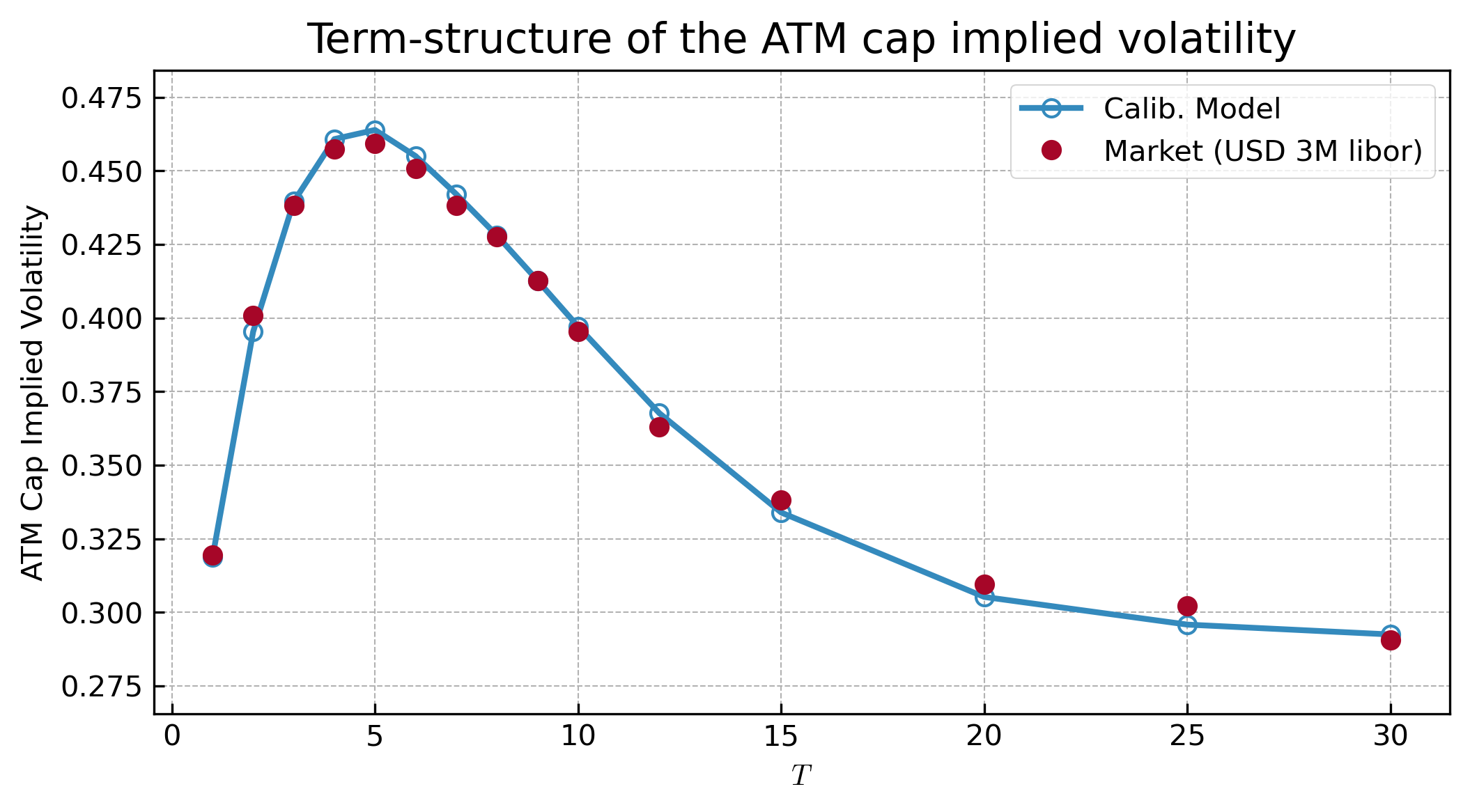

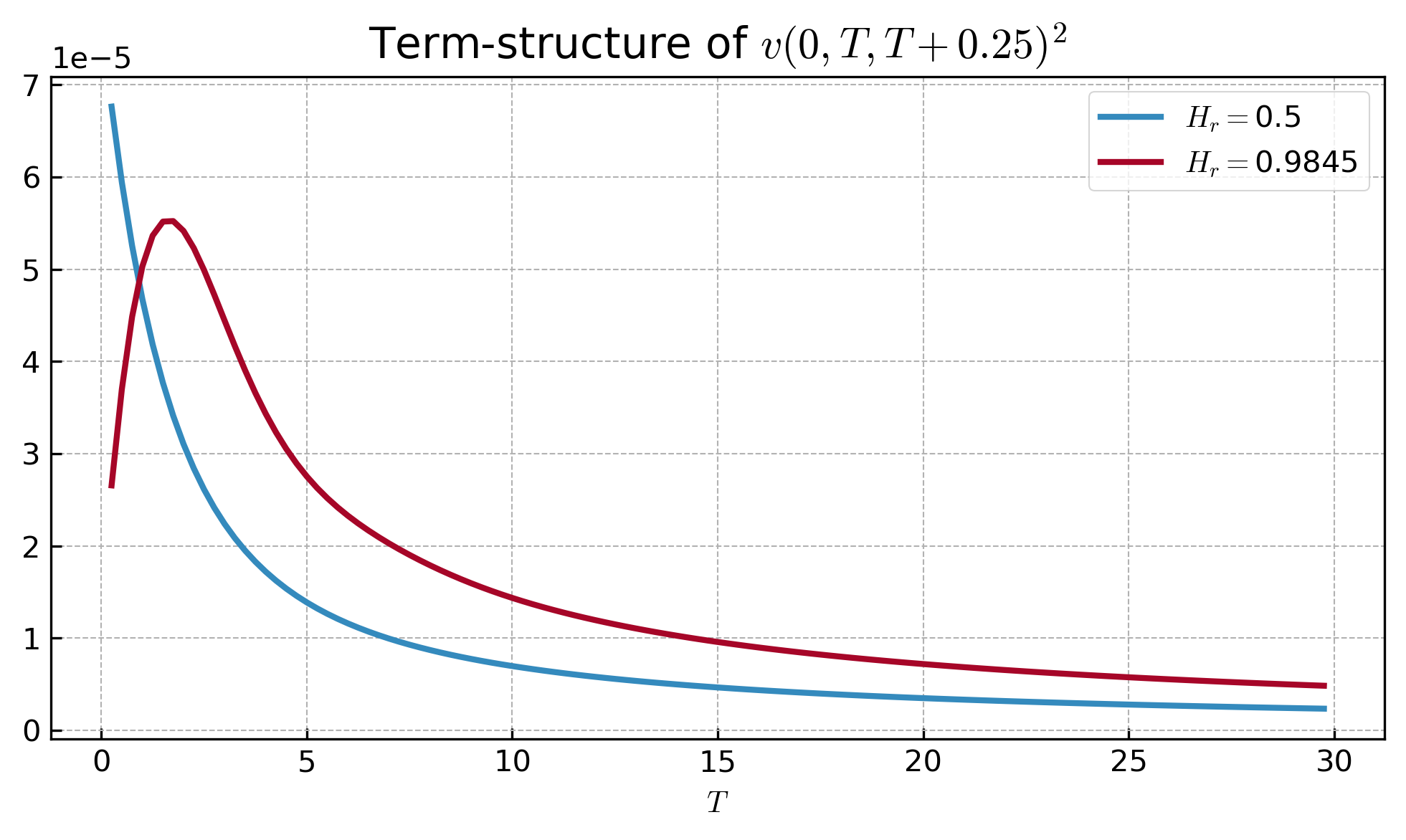

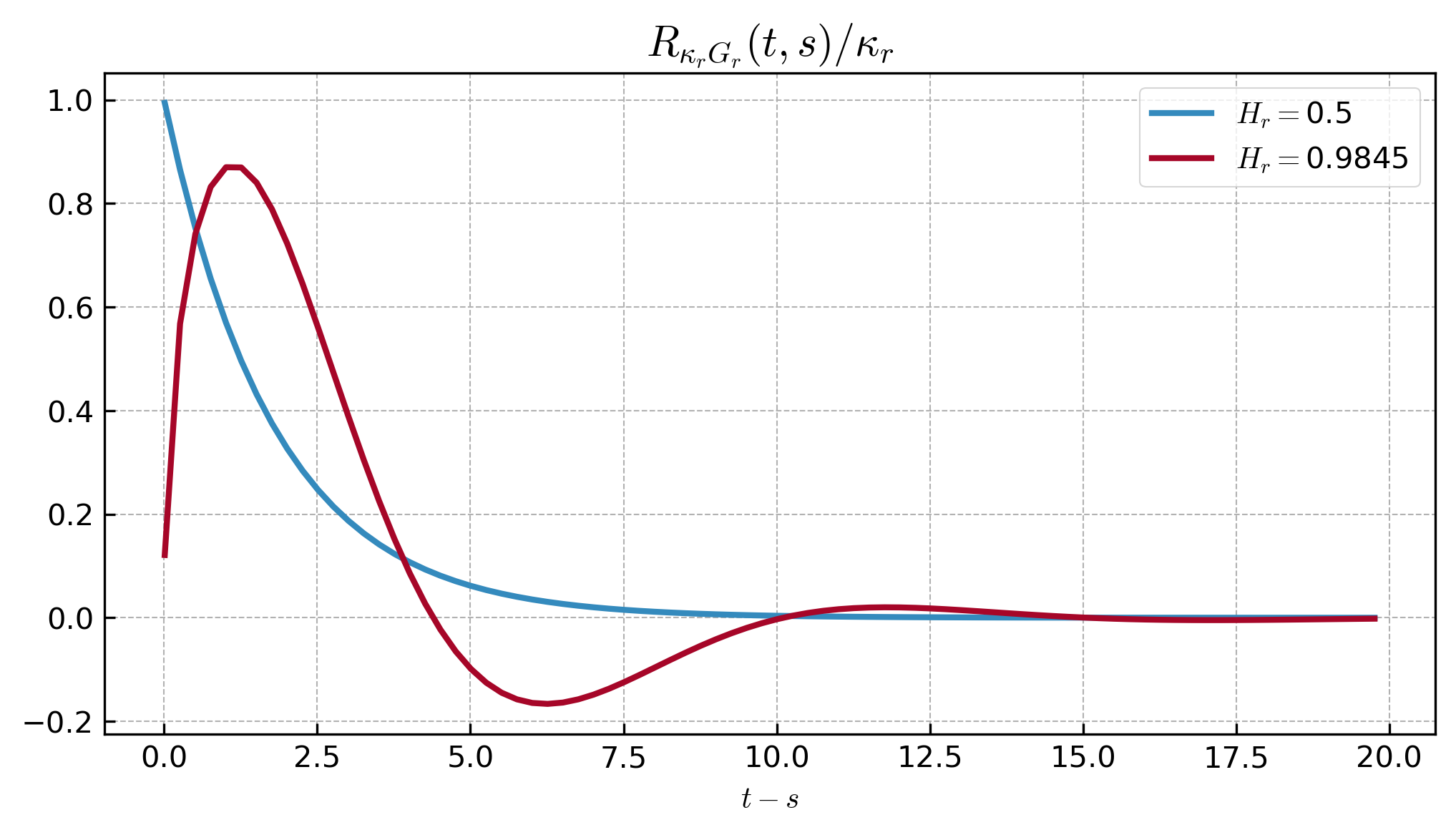

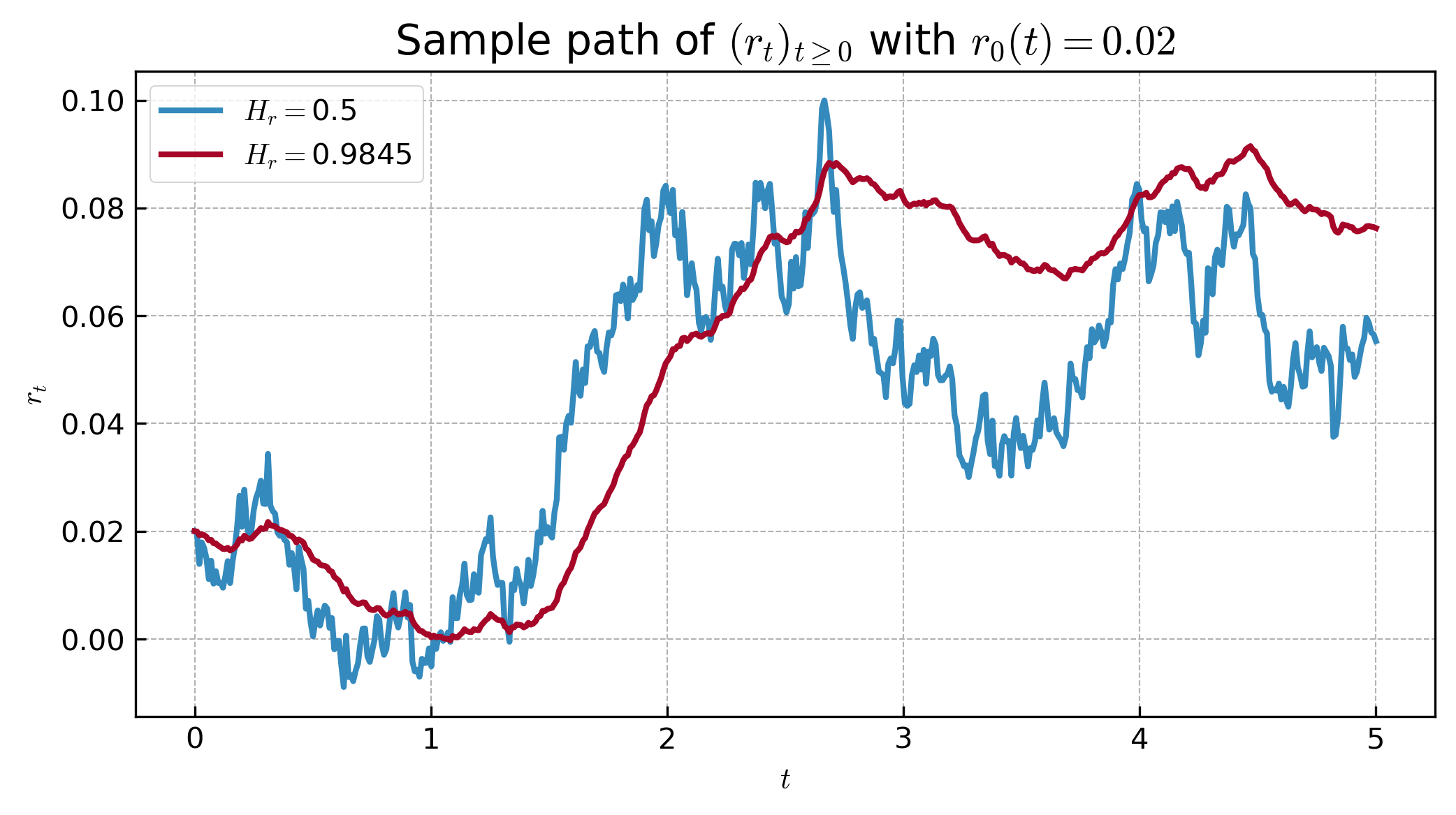

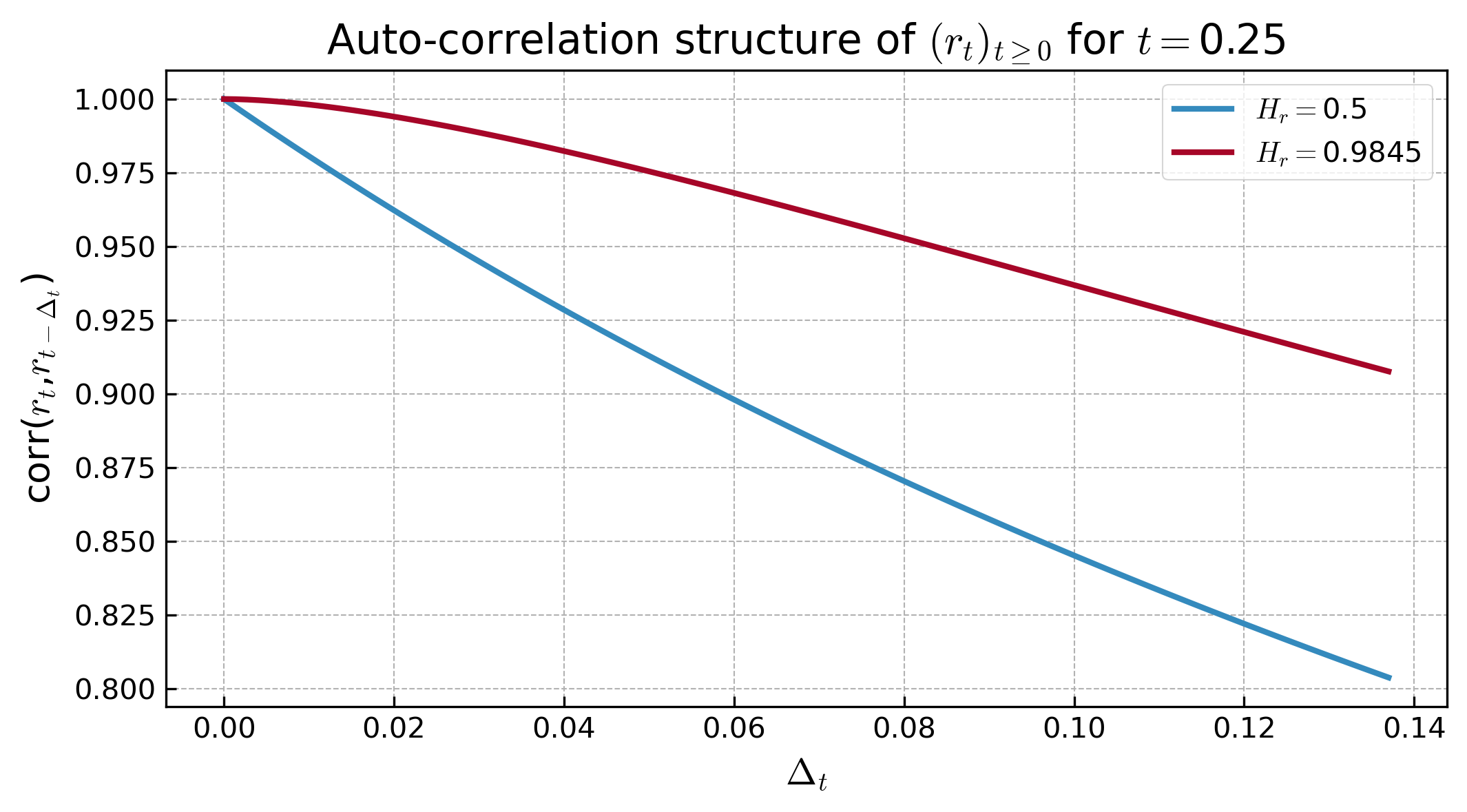

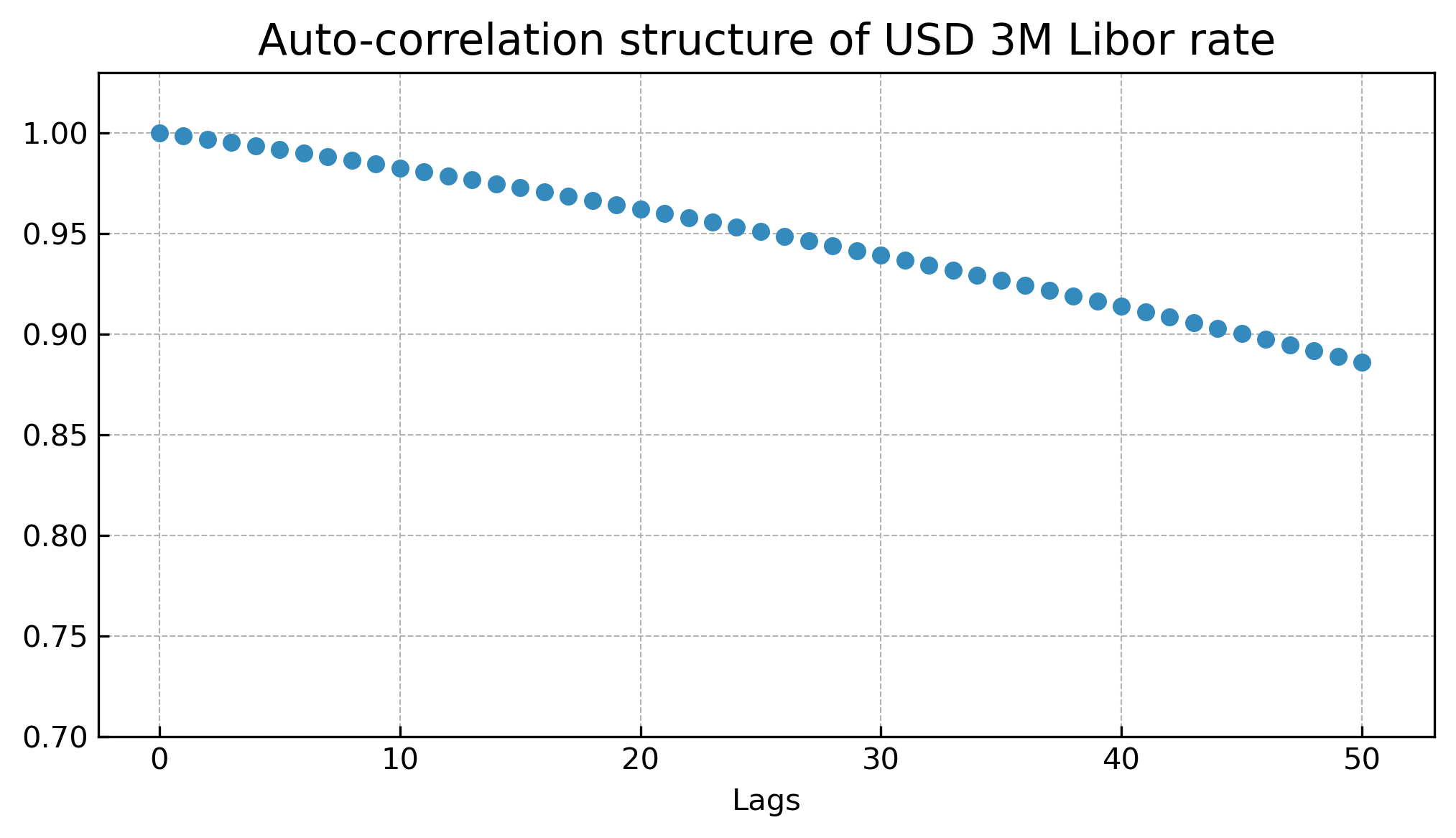

For the interest model, we consider the fractional kernel of the form The data we have for the calibration are the USD 3M Libor yield curve and the ATM USD cap implied volatility for annual maturities ranging from 1 year to 30 years. Firstly, using (2.7) and the USD 3M Libor yield curve (Figure 2), the input curve can deduced such that Then, since cap options are sum of zero-coupon bond options, we use Proposition 2.2 and calibrate the interest rate parameters by minimizing the root square error (RMSE) between model and market ATM cap implied volatility. Results of this calibration are displayed on Figure 3 with the corresponding calibrated parameters. The RMSE is 0.3663% and we observe an excellent fit of the data with as the calibrated model perfectly reproduces the humped shape of the market ATM cap implied volatility term-structure with only three parameters. As revealed by Figure 3, this can be explained by the fact that the term-structure of the ZC bond options pricing variance (2.10), with produces a humped shape333Due to humped behavior of the resolvent that drives and thus the pricing variance. when and , which is totally not the case when considering the Hull-White model (i.e. . Moreover, as expected and revealed in Figure 4, generates a smoother sample path than , and exhibits long-range dependencies. To check that long-term dependence makes sense, we consider historical data on the USD 3M Libor rate (daily close values) from 01/06/2021 to 30/09/2024, and examine the empirical auto-correlation structure. As we can see in Figure 4, the USD rate exhibits strong persistence, which is perfectly in line with previous studies (see Dai and Singleton (2003); McCarthy et al. (2004)), and emphasizes that considering long-range dependence models seems appropriate for modeling the dynamics of short rates.

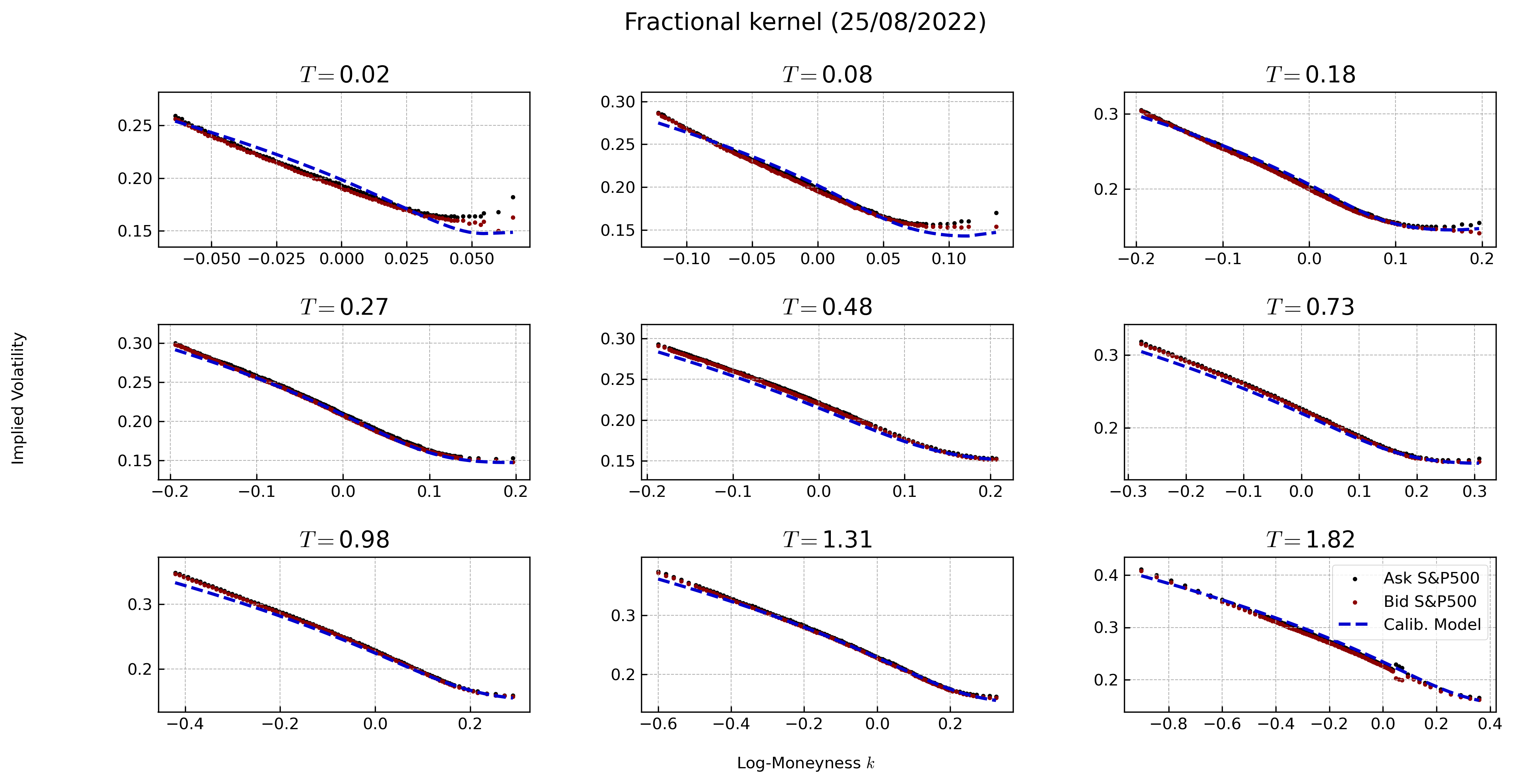

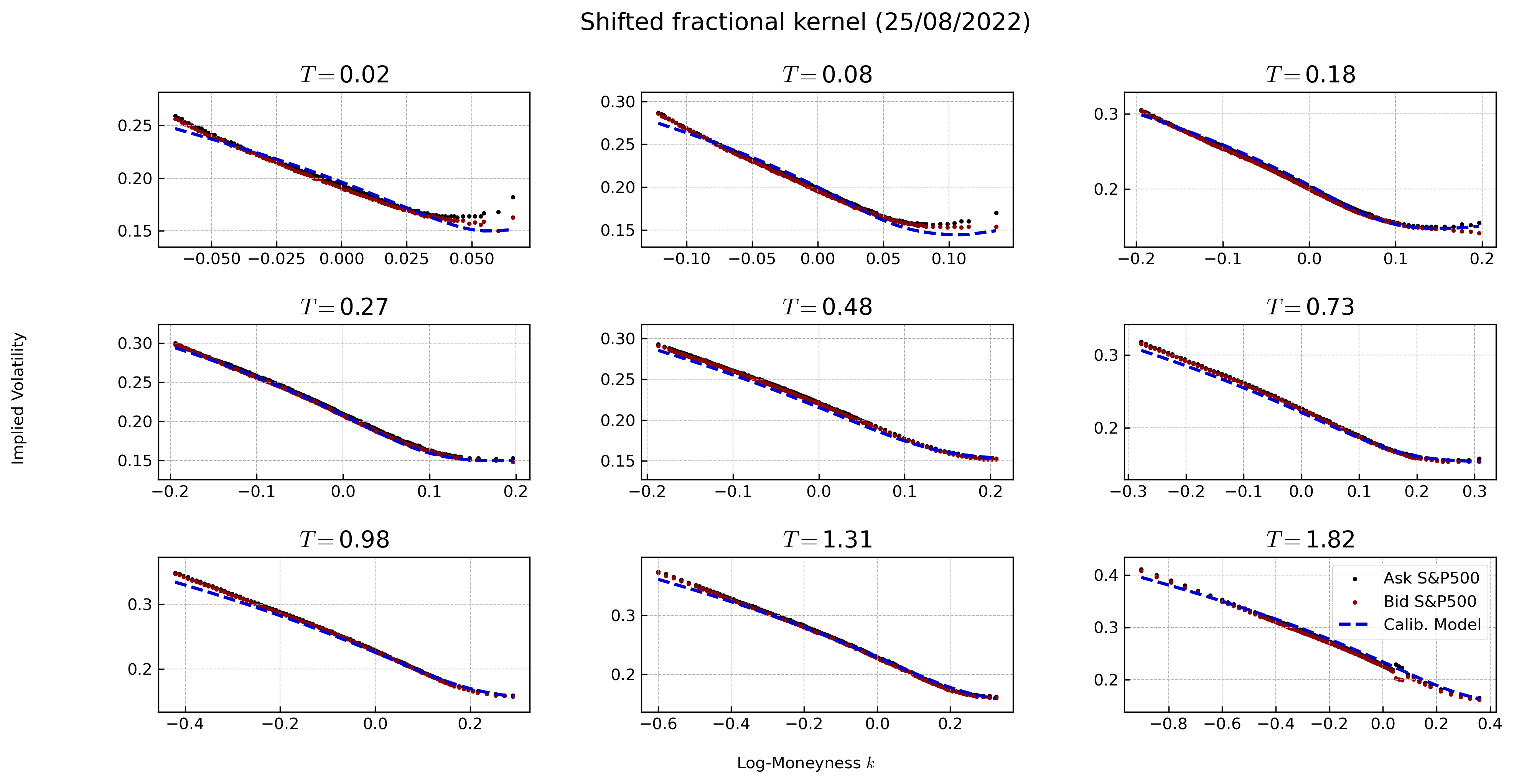

Let us now consider the calibration of the volatility and correlation

parameters. To this end, we consider the fractional kernel of the

form as

well as the shifted fractional kernel of the form

with The data we have for the calibration are

the S&P500 implied volatility data for different maturities ranging

from 1 week to 1.82 years and different strikes. Using the operator

discretization method with to approximate the characteristic

function of the log-forward index and a Fourier method, we can price

efficiently call options. Therefore, we calibrate the volatility and

correlation parameters by minimizing the RMSE between model and S&P500

implied volatility. To have a more parsimonious model, we decide to

fix and . We prefer to capture the

correlation between the index and the interest rate rather

than the correlation , but we have a leverage of flexibility

if we decide to calibrate as well.

Results of this

calibration are displayed on Figure 5, 6 and 7, we

observe that, for both kernels, . The RMSE are

0.4912% for the fractional kernel and 0.4204% for the shifted fractional

kernel. Overall, the calibration is good for both kernels, especially

around the ATM, yet the shifted fractional kernel outperforms the fractional

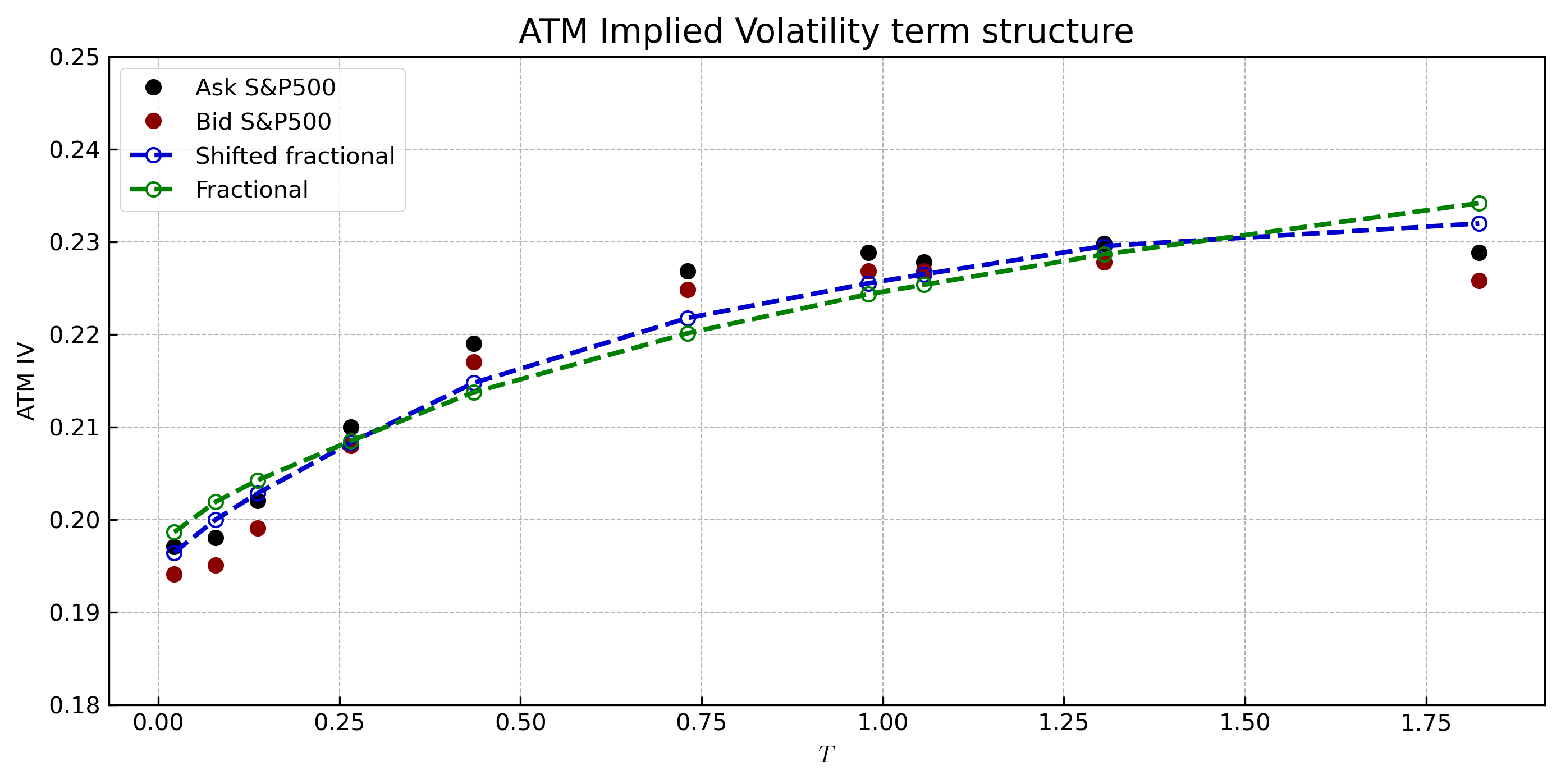

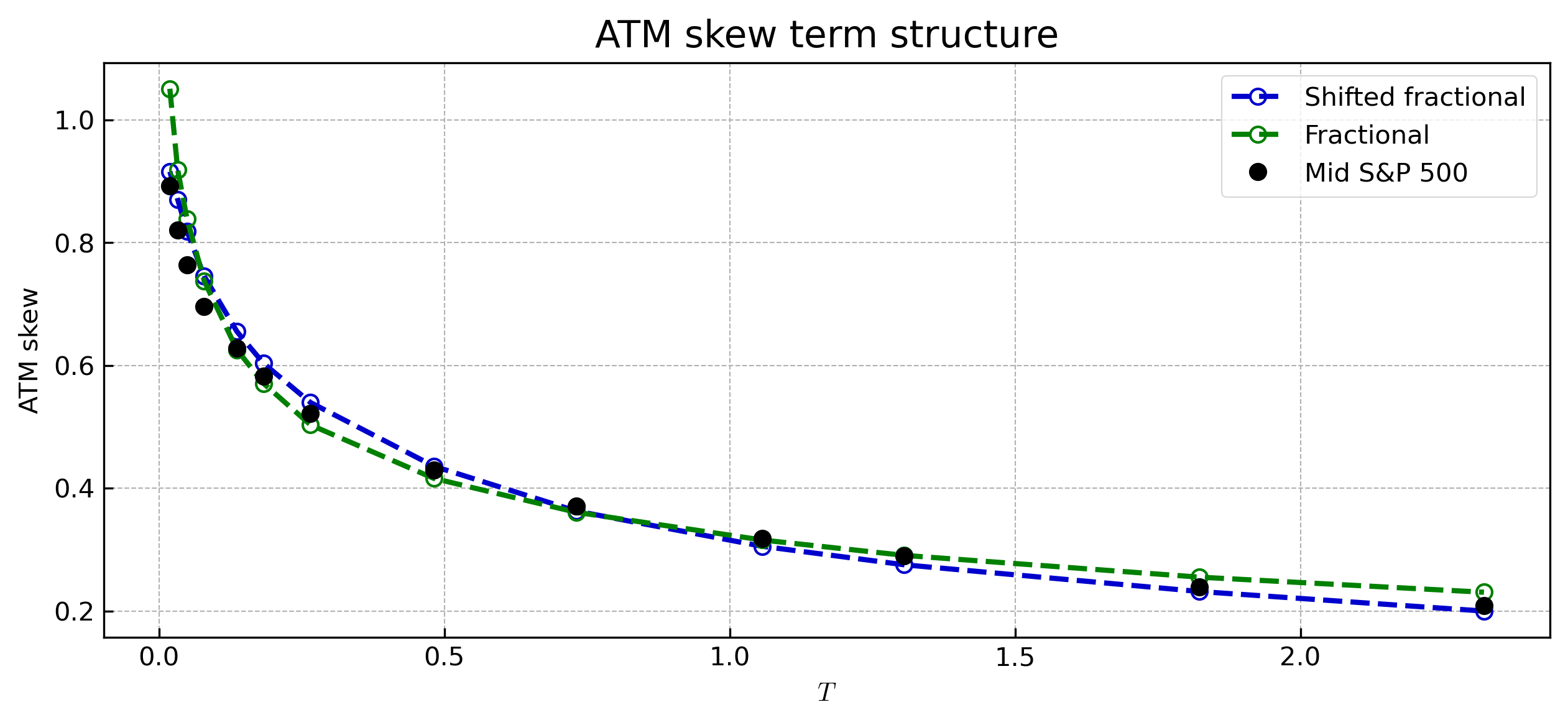

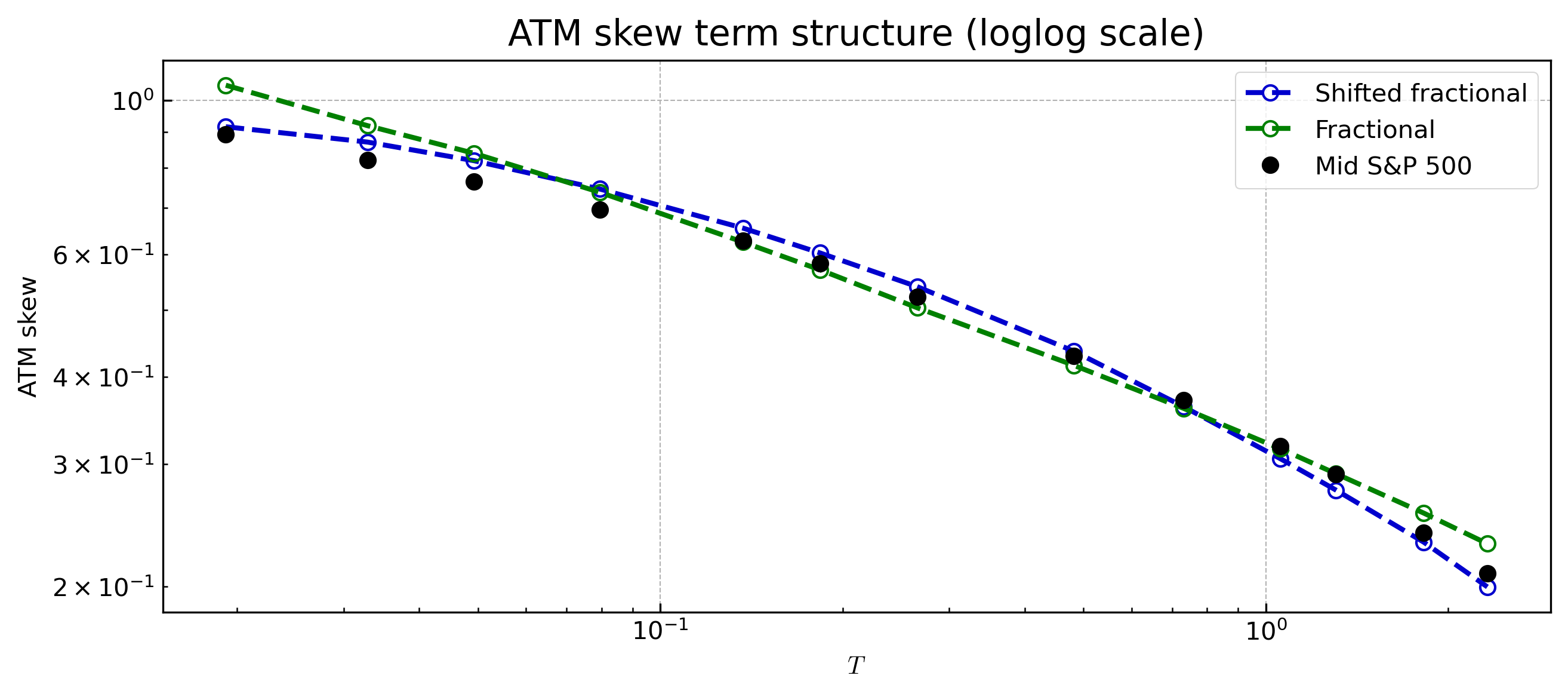

kernel. Moreover, as we can observe on Figure 8,

the shifted fractional kernel reproduces the term-structure of the ATM skew with a concave shape on the log-log scale for the chosen date, which is less the case for the fractional kernel. We observe that , indicating that the shifted kernel exhibits a faster decrease for longer maturities while prevents it from having an exploding skew for shorter maturities, allowing it to better capture the concave shape of the skew (in log-log scale). Our results demonstrate that the rough model underperforms the non-rough model associated with the shifted fractional kernel in capturing the entire volatility surface, confirming the findings of Abi Jaber and Li (2024); Delemotte, De Marco, and Segonne (2023); Guyon and Lekeufack (2023).

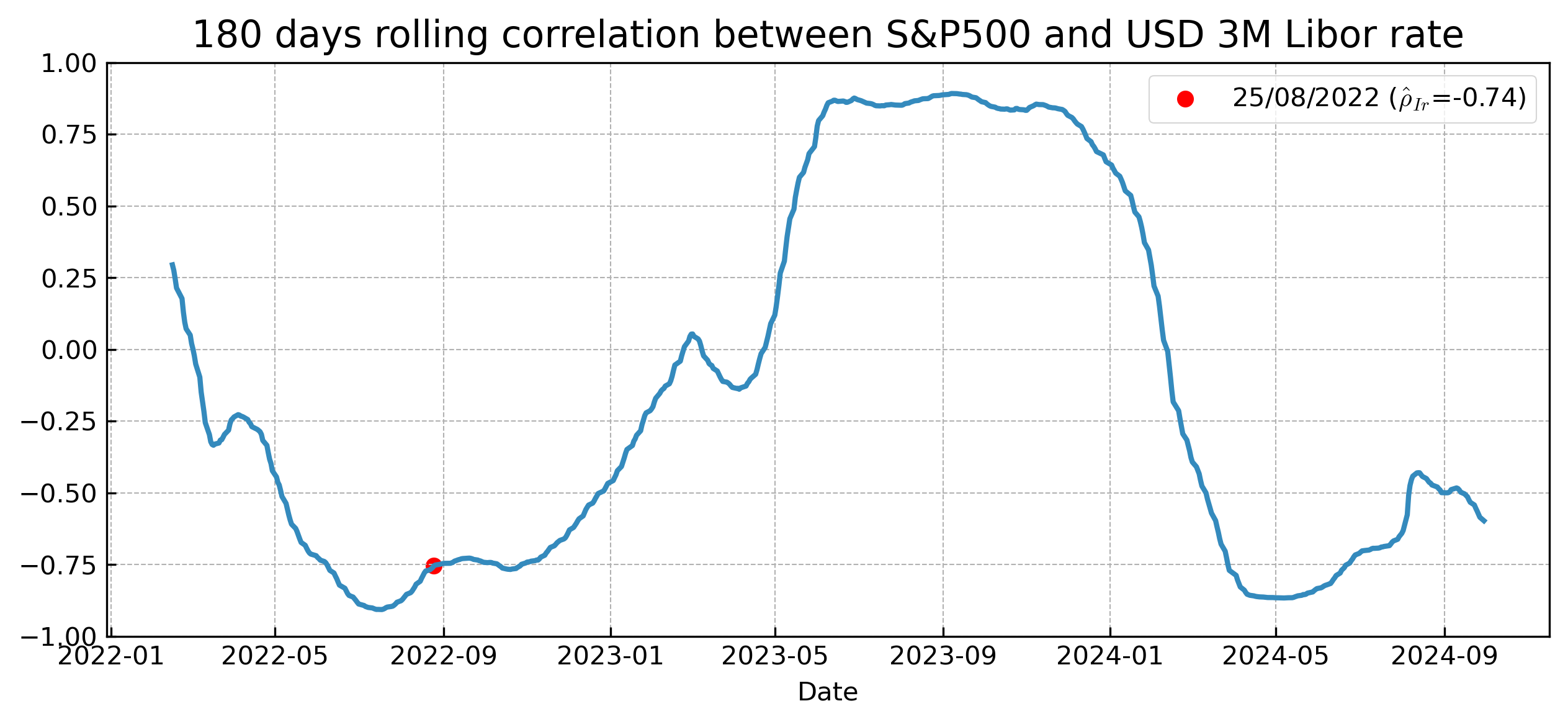

We also observe that the calibrated correlations between interest rate and index processes are significant. To ensure that these estimated values make sense, we looked at the empirical 180 days rolling correlation between the S&P500 index and the USD 3M Libor rate (daily close values). The results are displayed on Figure 9. We first observe that the correlation is not constant and almost never zero. Secondly, we notice that, for the calibration date we have chosen, the empirical rolling correlation is negative. This seems in line with the correlation values obtained during calibration on the implied volatility surface of the S&P500, and thus assuming correlation between processes appears coherent with market data.

5 Link with conventional quadratic linear models

5.1 Link with operator Riccati equations

In this section, we provide the link between the analytic expression of the characteristic function (3.2) and expression that depends on Riccati equations.

Proposition 5.1.

Proof.

From Lemma 6.1, we have that , where is an integral operator induced by a symmetric kernel such that

In this case, we have that

Moreover, we also know from Lemma B.1. in Abi Jaber (2022a) that

and by the definition, we also have that

As is composed of integral operators, it is also an integral operator induced by the following kernel

with the kernel induced by the identity operator such that Thus, using the dominated convergence theorem, we obtain that solves a Riccati equation given, for and by

More explicitly, since for we also have, for ,

Thus, using the integral operator we obtain that, for ,

In addition, from Theorem 3.1, we know that satisfies the following ODE

with ∎

We go now a step further and deduce more explicit Riccati equations by considering completely monotone Volterra kernels.

Definition 5.1.

A kernel is a completely monotone Volterra kernel if it satisfies Definition 2.1 and admits a Laplace representation of the form

| (5.3) |

where is a positive measure.

Proposition 5.2.

Proof.

The proof is given in Section 6. ∎

5.2 Riccati equations for Markovian volatility models

In this section, we consider some particular completely monotone kernels associated to Markovian volatility models. For those models, we derive a simplified version of the characteristic function based on Riccati equations. In particular, for the indicator and exponential kernels, we obtain closed form expressions similar to the characteristic functions deduced in van Haastrecht et al. (2009).

Proposition 5.3.

Suppose that and with and , then, for such that

| (5.8) |

with solution of the following SDEs

on with , such that, almost surely,

and , and time-dependent functions satisfying Riccati equations of the form

| (5.9) |

| (5.10) |

| (5.11) |

with for

Proof.

The proof is given in Section 6. ∎

Corollary 5.1.

Suppose that and with , and . Then, for such that

| (5.12) |

with , and time-dependent functions given by

| (5.13) |

| (5.14) |

5.3 Multi-factor approximation for completely monotone Volterra kernels

In this section, we propose another alternative to approximate the characteristic function when considering completely monotone Volterra kernels in the sense of Definition 2.1. The approximate method is based on a Laplace representation of completely monotone kernels and expression of the characteristic function in terms of Riccati equations. Unlike the approach proposed in Section 3.2, a convergence result is deduced for this multi-factor approximate approach. Using a Laplace transform representation, we have that completely monotone kernels can be rewritten such that

| (5.16) |

with a positive measure. Hence a natural approximation of the kernel is given by

| (5.17) |

where are the weights and the mean reversion terms that should be appropriately defined. Under suitable choice, converges in to the completely monotone kernels. Therefore, based on Proposition 5.3, we can propose another approximate solution of the characteristic function associated to completely monotone Volterra kernels.

Lemma 5.1.

Suppose that for all , and are such that

such that and

as goes to infinity. For fixed, there exists a function such that the following inequality holds

| (5.18) |

and converges in to when goes to infinity i.e.

as goes to infinity.

Proof.

We refer to the proof of (Abi Jaber and El Euch, 2019, Proposition 3.3.). ∎

Remark 5.2.

Proposition 5.4.

Let be the solution of (2.12) with the completely monotone kernel (5.16) and solution of (2.12) with the approximate kernel (5.17). Suppose that the assumptions of Lemma 5.1 are satisfied and that, for such that the sequence is uniformly integrable, then

where is the solution of Riccati equation (5.9) with and , for

Proof.

Based on Proposition 5.4,

we can deduce a second approximate solution of the characteristic

function for which a theoretical convergence result is established.

However, it is a semi-closed solution in the sense that it requires

solving Riccati equations.

Finally, we decide to compare this “multi-factor” approximate

method with the “operator discretization” method proposed

in Section 3.2.

For this purpose, we consider the same kernels and model parameters

as in Section 3.2.

Figure 10 presents

the implied volatility generated for different by the multi-factor

method where the system of Riccati equations (5.9)-(5.10)-(5.11)

is solved numerically using an implicit method. We observe a convergence

as the number of factors increases. However,

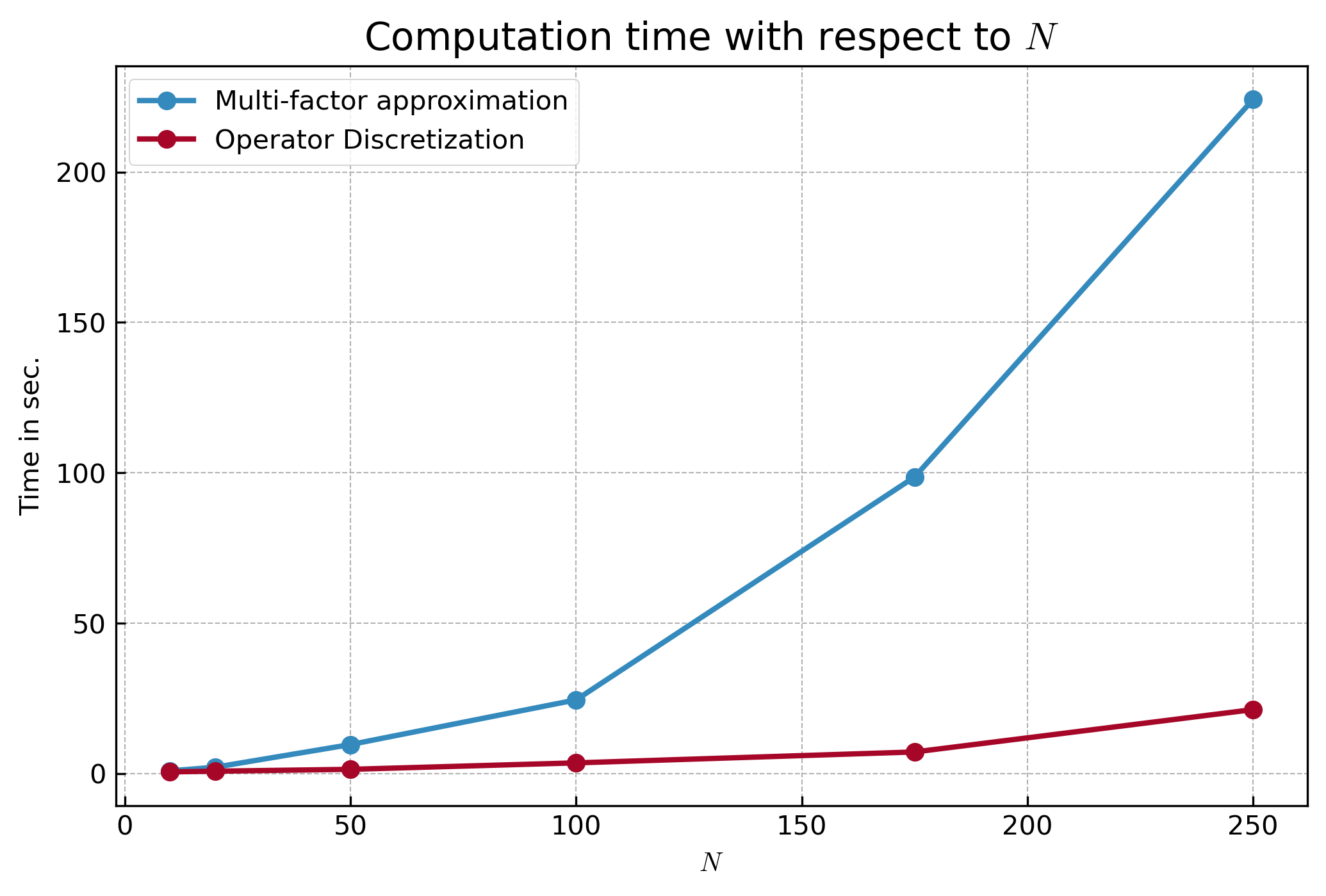

the speed of convergence differs between the methods. As revealed by Figure

11, the operator discretization

approach converges much faster than the multi-factor approach, either

with respect to or in terms of computation time. Nevertheless, it

should be noted that the speed of convergence of the “multi-factor”

method depends strongly on the choice of multi-factor parameters

, as well as the numerical method used to solve the system of Riccati equations and other choices than those used in this paper could

give a faster speed of convergence. The aim of this comparison is

above all to illustrate that the “operator discretization” method

converges quickly and is fairly simple to implement compared with

the “multi-factor” method.

6 Proofs

6.1 Proof of Theorem 3.1

We first consider two useful lemmas before proving Theorem 3.1.

Lemma 6.1.

For such that there exists an integral operator induced by a symmetric kernel such that

| (6.1) |

and for any

| (6.2) |

with Moreover, the kernel satisfies

| (6.3) |

Proof.

From (Abi Jaber, 2022a, Lemma B.1.), we know that in our setting there exists an integral operator induced by a symmetric kernel such that (6.1) and (6.2) are satisfied. Moreover, from (6.2), since is an integral operator and is symmetric, we deduce that, for any ,

Moreover, since is a symmetric integral operator, we also have that

We conclude that, for any ,

and thus, for

almost everywhere. ∎

Lemma 6.2.

For such that and let us define such that

Then the dynamics of is given by

| (6.4) |

Proof.

First, we set

and using Lemma 6.1, we have that

Using the Leibniz rule, we deduce that

For fixed let us now deduce the dynamics of and Since we have that

an application of Ito’s lemma yields to

Moreover, an application of the Leibniz rule combined with the fact that yields to

The quadratic variation is given by

Take it all together, we have that

Therefore, we obtain that

Finally, using the fact that and (see Lemma 6.1), we obtain that

∎

Proof.

As explained in Abi Jaber (2022a), it is sufficient to make the proof for such Fix and consider the processes and defined, for by

| (6.5) |

and

If we prove that is a martingale under , then the proof is complete since, in this case, we have that

and thus

Let us prove that is a (true) martingale under . First, we can prove that is a local martingale by showing that the drift of the dynamic of is null. Using the dynamic of given by (2.12), the dynamic of given by (6.4) and the fact that , we observe that

Moreover, the quadratic variation of satisfies

As the dynamic of can be written such that

we easily obtain that

but as

we have that

and since, from (Abi Jaber, 2022a, Lemma B.1.),

we have that is a local martingale. It remains to show that this is a true martingale. Since and , from (6.5), it follows that

Furthermore, we observe that

and, as we deduce that

Then, we define the process such that

This process is a true martingale (see arguments in (Abi Jaber et al., 2021b, in Lemma 7.3)). Therefore, we finally have that

and as is a local martingale upper bounded by a true martingale, this a true martingale and it completes the proof. ∎

6.2 Proof of Proposition 5.2

We first consider a lemma before proving Proposition 5.2.

Lemma 6.3.

Assume that the kernel function is completely monotone and can be represented as (5.3). Then,

with

| (6.6) |

Moreover, for such that

with

| (6.7) |

Proof.

Proof.

We divide the proof into two steps. The first step is to show that

with such that

| (6.8) |

| (6.9) |

and

| (6.10) |

with a time-dependent function given by

| (6.11) |

Then, the second step is to deduce the equations satisfied by .

Step 1

Step 2

Let us now deduce the equations satisfied by . First, we have that

A direct differentiation of with respect to leads to

Using the form of we obtain that

Moreover, using (6.3) in Lemma 6.1 and once again the Fubini’s theorem, we have that

Using the same arguments, we also obtain that

Thus, we deduce that

Let us consider now the ODE satisfied by . We have that

Using the same argument than for we have that

Using the form of we obtain that

and, using similar arguments than previously, we also have that

Moreover, as

we have that

Therefore, as , we obtain that

Finally, let us consider the equation satisfied by . We know that

Therefore, we have that

Using once again the form of we deduce that

Also, we have that

and

Moreover, as

and , we finally obtain that

and that concludes the proof. ∎

6.3 Proof of Proposition 5.3

Proof.

Assuming that and , with the volatility process reduces to

Let us introduce some auxiliary processes solution of the following SDEs

Then, we can deduce that, almost surely,

Also, we observe that

and

with

We also have that, for

with Therefore, using Proposition 5.2, we have that

with

Using Proposition 5.2, we have that

Moreover, after fastidious calculus, we end up with

and

∎

Acknowledgments

Eduardo Abi Jaber is grateful for the financial support from the Chaires FiME-FDD, Financial Risks, Deep Finance & Statistics and Machine Learning and systematic methods in finance at Ecole Polytechnique. Edouard Motte was financially supported by the Fonds de la Recherche Scientifique (F.R.S. - FNRS) through a FRIA grant.

References

- Abi Jaber (2022a) E. Abi Jaber. The characteristic function of gaussian stochastic volatility models: an analytic expression. Finance and Stochastics, 26(4):733–769, 2022a.

- Abi Jaber (2022b) E. Abi Jaber. The Laplace transform of the integrated volterra Wishart process. Mathematical Finance, 32(1):309–348, 2022b.

- Abi Jaber and El Euch (2019) E. Abi Jaber and O. El Euch. Multifactor approximation of rough volatility models. SIAM Journal on Financial Mathematics, 10(2):309–349, 2019.

- Abi Jaber and Gérard (2024) E. Abi Jaber and L. A. Gérard. Signature volatility models: pricing and hedging with fourier. 2024. Available at SSRN.

- Abi Jaber and Guellil (2025) E. Abi Jaber and M. Guellil. Complex discontinuities of in the Volterra Stein-Stein model. Working Paper, 2025.

- Abi Jaber and Li (2024) E. Abi Jaber and S. Li. Volatility models in practice: Rough, path-dependent or Markovian? Path-Dependent or Markovian, 2024.

- Abi Jaber et al. (2021a) E. Abi Jaber, E. Miller, and H. Pham. Markowitz portfolio selection for multivariate affine and quadratic volterra models. SIAM Journal on Financial Mathematics, 12(1):369–409, 2021a.

- Abi Jaber et al. (2021b) E. Abi Jaber, E. Miller, and H. Pham. Integral operator Riccati equations arising in stochastic Volterra control problems. SIAM Journal on Control and Optimization, 59(2):1581–1603, 2021b.

- Bayer et al. (2016) C. Bayer, P. Friz, and J. Gatheral. Pricing under rough volatility. Quantitative Finance, 16(6):887–904, 2016.

- Benth and Rohde (2019) F.E. Benth and V. Rohde. On non-negative modeling with carma processes. Journal of Mathematical Analysis and Applications, 476(1):196–214, 2019.

- Bergomi (2015) L. Bergomi. Stochastic volatility modeling. CRC press, 2015.

- Brigo and Mercurio (2006) D. Brigo and F. Mercurio. Interest rate models-theory and practice: with smile, inflation and credit. Springer, Berlin, 2006.

- Cont (2001) R. Cont. Empirical properties of asset returns: stylized facts and statistical issues. Quantitative finance, 1(2):223, 2001.

- Corcuera et al. (2013) J.M. Corcuera, G. Farkas, W. Schoutens, and E. Valkeila. A short rate model using ambit processes. In Malliavin calculus and stochastic analysis: A festschrift in honor of David Nualart, pages 525–553. Springer, 2013.

- Dai and Singleton (2003) Q. Dai and K. Singleton. Term structure dynamics in theory and reality. The Review of Financial Studies, 16(3):631–678, 2003.

- De Jong et al. (2004) F. De Jong, J. Driessen, and A. Pelsser. On the information in the interest rate term structure and option prices. Review of Derivatives Research, 7:99–127, 2004.

- Delemotte et al. (2023) J. Delemotte, S. De Marco, and F. Segonne. Yet another analysis of the sp500 at-the-money skew: Crossover of different power-law behaviours. Available at SSRN 4428407, 2023.

- El Euch and Rosenbaum (2018) O. El Euch and M. Rosenbaum. Perfect hedging in rough heston models. The Annals of Applied Probability, 28(6):3813–3856, 2018.

- Fredholm (1903) I. Fredholm. Sur une classe d’équations fonctionnelles. 1903.

- Gatheral et al. (2018) J. Gatheral, T. Jaisson, and M. Rosenbaum. Volatility is rough. Quantitative Finance, 18(6):933–949, 2018.

- Grzelak et al. (2011) L.A. Grzelak, C.W. Oosterlee, and S. Van Weeren. The affine Heston model with correlated gaussian interest rates for pricing hybrid derivatives. Quantitative Finance, 11(11):1647–1663, 2011.

- Grzelak et al. (2012) L.A. Grzelak, C.W. Oosterlee, and S. Van Weeren. Extension of stochastic volatility equity models with the Hull–White interest rate process. Quantitative Finance, 12(1):89–105, 2012.

- Guyon and El Amrani (2023) J. Guyon and M. El Amrani. Does the term-structure of equity at-the-money skew really follow a power law? Risk Magazine, Cutting Edge section, 2023.

- Guyon and Lekeufack (2023) J. Guyon and J. Lekeufack. Volatility is (mostly) path-dependent. Quantitative Finance, 23(9):1221–1258, 2023.

- Hainaut (2022) D. Hainaut. Continuous time processes for finance: Switching, self-exciting, fractional and other recent dynamics. Bocconi and Springer Series, 2022.

- Heston (1993) S.L. Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The review of financial studies, 6(2):327–343, 1993.

- Hull and White (1993) J. Hull and A. White. One-factor interest-rate models and the valuation of interest-rate derivative securities. Journal of financial and quantitative analysis, 28(2):235–254, 1993.

- Lewis (2001) A. L. Lewis. A simple option formula for general jump-diffusion and other exponential levy processes, 2001. Available at SSRN 282110.

- McCarthy et al. (2004) J. McCarthy, R. DiSario, H. Saraoglu, and H. Li. Tests of long-range dependence in interest rates using wavelets. The Quarterly Review of Economics and Finance, 44(1):180–189, 2004.

- Motte and Hainaut (2024) E. Motte and D. Hainaut. Partial hedging in rough volatility models. SIAM Journal on Financial Mathematics, 15(3):601–652, 2024.

- Schöbel and Zhu (1999) R. Schöbel and J. Zhu. Stochastic volatility with an ornstein–uhlenbeck process: an extension. Review of Finance, 3(1):23–46, 1999.

- Singor et al. (2013) S.N. Singor, L.A. Grzelak, D.D. van Bragt, and C.W. Oosterlee. Pricing inflation products with stochastic volatility and stochastic interest rates. Insurance: Mathematics and Economics, 52(2):286–299, 2013.

- Stein and Stein (1991) E.M. Stein and J.C. Stein. Stock price distributions with stochastic volatility: an analytic approach. The Review of Financial Studies, 4(4):727–752, 1991.

- van Haastrecht and Pelsser (2011) A. van Haastrecht and A. Pelsser. Generic pricing of fx, inflation and stock options under stochastic interest rates and stochastic volatility. Quantitative Finance, 11(5):665–691, 2011.

- van Haastrecht et al. (2009) A. van Haastrecht, R. Lord, A. Pelsser, and D. Schrager. Pricing long-dated insurance contracts with stochastic interest rates and stochastic volatility. Insurance: Mathematics and Economics, 45(3):436–448, 2009.