Bayesian estimation of Unit-Weibull distribution based on dual generalized order statistics with application to the Cotton Production Data

Qazi J. Azhada, Abdul Nasir Khanb111Corresponding Author: A. N. Khan (nasirgd4931@gmail.com ), Bhagwati Devic, Jahangir Sabbir Khand, Ayush Tripathie

aDepartment of Mathematics, Shiv Nadar Institution of Eminence, Dadri, India

bDepartment of Mathematics and Statistics, Dr. Vishwanath Karad MIT World Peace University, Pune, India

cDepartment of Statistics, Central University of Jharkhand, Jharkhand, India

dDepartment of Statistics and Operations Research, Aligarh Muslim university, India

eDepartment of Mathematics, Jaypee Institute of Information Technology, , India

Abstract

The Unit Weibull distribution with parameters and is considered to study in the context of dual generalized order statistics. For the analysis purpose, Bayes estimators based on symmetric and asymmetric loss functions are obtained. The methods which are utilized for Bayesian estimation are approximation and simulation tools such as Lindley, Tierney-Kadane and Markov chain Monte Carlo methods. The authors have considered squared error loss function as symmetric and LINEX and general entropy loss function as asymmetric loss functions. After presenting the mathematical results, a simulation study is conducted to exhibit the performances of various derived estimators. As this study is considered for the dual generalized order statistics that is unification of models based distinct ordered random variable such as order statistics, record values, etc. This provides flexibility in our results and in continuation of this, the cotton production data of USA is analyzed for both submodels of ordered random variables: order statistics and record values.

Keywords: Unit-Weibull distribution, Lindley approximation, Tierney-Kadane approximation, MCMC.

1 Introduction

A two parameter distribution was proposed by Mazucheli et al. (2018) known as unit-Weibull (UW) distribution. This distribution is obtained by making the transformation , where random variable Y follows Weibull distribution. Authors shows that this distribution performed better than Kumaraswamy, Beta and other well known distributions. The probability density function (pdf) of UW distribution with parameters and is

with corresponding cumulative distribution function (cdf) as

where and are shape parameters.Pdf of this transformed model exhibits characteristics such as increasing, decreasing, bathtub-shaped, unimodal, and anti-unimodal. This distribution encompasses a variety of sub-distributions, including instances such as the standard uniform distribution which spans the interval with parameters and , the power function distribution with , as well as the unit Rayleigh distribution with .

For further insights into additional characteristics and properties associated with the UW distribution, interested readers are encouraged to explore the comprehensive study conducted by Mazucheli et al. (2018). Following its emergence, different researchers have studied this distribution in diverse scenarios. For instance, Mazucheli et al. (2019) presented a quantile regression model by considering UW distribution. Iliev et al. (2019) conducted study on the one-side Hausdorff approximation of the Heaviside step function by employing UW, Unit-logistic and Topp Leone cumulative sigmoid functions. Menezes et al. (2021) presented corrected biased maximum likelihood estimators for the parameters of UW distribution using different methods like Cox-Snell, Parametric bootstrap, and Firth. Alotaibi et al. (2020) delved into the analysis of multicomponent stress strength reliability using both classical and Bayesian approaches, focusing on the UW distribution. Alotaibi et al. (2021) obtained estimates of system reliability under known and unknown parameters using classical and Bayesian approaches when the data were observed as progressively type II censored. The authors also constructed asymptotic intervals using the Fisher information matrix, boot-p, and boot-t intervals for system reliability. Almetwally et al. (2023) conducted the study on UW distribution for the progressive Type-II censored data. The authors presented estimates for the unknown parameters of UW distribution using two classical methods like MLE and the maximum product of spacing. In the Bayesian estimation paradigm, authors incorporated both the likelihood function and the product of spacing function to estimate the parameters of UW distribution.

In this article, we have broadened the study on UW distribution within a dual generalized order statistics (dgos) paradigm. The dgos was presented as a model containing sub-model of ordered random variable like, reverse order statistics, lower record values, generalized lower record values, and so on. By taking into account the order statistics of component lifetimes, these models may be used to study the reliability of complex systems, which aids in comprehending how the failure of a single component affects the reliability of the entire system. On the other hand the dgos can be utilized in designing redundancy and safety measures in critical system. For example, Consider that it is important to identify and evaluate the most severe failures in decreasing order of severity for a critical system, such as nuclear power plants. This makes it easier to plan safety and redundancy measures appropriately. In this study we provide the practical applicability of UW distribution under the more generalized framework of ordered random variable known as dgos. Pawlas and Szynal (2001) first established dgos as a lower generalized order statistic. Following that Burkschat et al. (2003) presented various distributional properties of dgos and their sub-models. Also established the connection between gos and dgos.Numerous authors have addressed the estimation problem for various distributions within the context of the dgos framework. We will delve into some of the prominent research in this area. Jaheen and Al Harbi (2011) utilized the dgos model for Bayesian estimation of parameters of exponentiated Weibull distribution. They have also utilized the MCMC algorithm to calculate Bayes estimators by considering both symmetric and asymmetric loss functions. Abd Al-Fattah et al. (2021) have estimated the parameters of Exponentiated Generalized Inverted Kumaraswamy Distribution using the Bayesian approach under the dgos framework.

2 Mathematical Formulation of Problem

Let , , be sequence of independent identically distributed random variables with absolutely continuous distribution function (df) and probability density function (pdf) . Let , , and , , such that . Then , ,, are called dual generalized order statistics (dgos) with joint pdf

for . The dgos is an unified approach that contains several models of ordered random variable arranged in descending order of magnitude. Taking different values of parameters, can be reduced to different-different models of ordered random variables. For example, when we set and , then the obtained model from is known as reversed order statistics, when set , then the obtained model from is known as or generalized lower record values and when we set along with , then the obtained model is known as ordinary lower record values, etc. To know more about models of ordered random variables readers are advised to go through the articles/books: David and Nagaraja (2004), Ahsanullah (2004), Arnold et al. (2008). Let us suppose that be the dgos taking from UW(, ) then the likelihood function written as

| (2.1) |

Now we have considered two parameter gamma distributions as independent informative priors for the shape parameters and

| (2.2) |

The square error loss function (SELF) is defined as

The posterior mean is the Bayes estimator under SELF. The LINEX loss function is defined as

and Bayes estimator corresponding to LINEX loss function is given as

The general entropy (GE) function defined as

The Bayes estimator corresponding to GE is given as

Now, the joint posterior density of and is obtained by using (2.1) and (2.2), and is given as

3 Bayesian Estimation of the Problem

For finding the Bayes estimators of , and , we employ Tierney and Kadane’s approximation, Lindley Approximation and Markov chain Monte Carlo methods. The reason for opting these approximation technique is due to the complex form of posterior joint density function.

3.1 Lindley Approximation

Here, we have used Lindley approximation method to approximate the ratio of integrals which was proposed by Lindley (1980). The Bayes estimator for a parameter in presence of any loss function can be represented in the form as given below

| (3.1) |

where is the logarithm of likelihood function and is the logarithm of prior distribution of . In our case , thus (3.1) can be written as

where and . Thus, using this method, the approximated value of is given as

where,

| (3.4) |

where is the element of the inverse matrix . We have obtained the Bayes estimator for the parameters and using the quantities represented in (3.4) and by replacing with their respective MLEs.

For the UW distribution, the terms as given in (3.4) are reduced in the form as:

| (3.5) |

Utilizing quantities given in (3.5), The Bayes estimators for unknown parameters can be obtained. Here, all quantities except and its derivative, are same for each of the Bayes estimator. For example in the case of SELF, the quantity for Bayes estimator of can be represented as,

For the Bayes estimator ,

For the Bayes estimator of ,

Similarly following the same idea for LINEX and GE loss function and for given in Table [1], the Bayes estimators and their derivatives can easily be found as discussed for SELF.

| Parameter | LINEX | GE |

|---|---|---|

3.2 Tierney and Kadane’s approximation

The Tierney and Kadane’s approximation (T-K) method is an another approach to evaluate the ratio integral, which was introduced by Tierney and Kadane (1986). Under this method, The posterior expectation can be written as

where, and

Here, and same as defined in the last section.

Thus, the approximate value of posterior expectation of using T-K approximation method can be written as

| (3.6) |

where, and maximizes and respectively. and are the inverse hessian matrices of and at and , respectively. In our case, we have

where is a constant independent of parameters , . Further, obtain and then equate both of these quantities to 0. We get

| (3.7) | |||

| (3.8) |

Now and can be obtained by solving (3.7) and (3.8). Thus, the determinant for the negative of the inverse Hessian of evaluated at is as:

where

The determinant of , i.e., will be same for estimates of parameters under all loss functions while determinant of , i.e., will not be same as it contains the term which is different for each parameter and loss function.

First we will find the Bayes estimators for , and under SELF. For Bayes estimator of , we have this implies

| (3.9) |

Now, differentiating (3.9) with respect to , , we get

Thus, the solution of first derivatives given above produces the MLE’s for and . Now, determinant for the negative of the inverse hessian matrix of obtained at and is . The quantities and can be obtained by taking derivatives of as in the case of Using the quantity and in equation (3.6), we get the Bayes estimate of

For the Bayes estimator of , we have , this implies

| (3.10) |

Now, differentiating (3.10) with respect to , , we get

Thus, the solution of first derivatives given above produces the MLE’s for and . Now, determinant for the negative of the inverse hessian matrix of obtained at and is . Using the same idea of Bayes estimator of , we find the Bayes estimator of .

Following in the same steps, we can find the Bayes estimator of . For the Bayes estimator of , we have , this implies

| (3.11) |

Now, differentiating (3.11) with respect to , , we get

Thus, the solution of first derivatives given above produces the MLE’s for and . Now, determinant for the negative of the inverse hessian matrix of obtained at and is , where

The quantities given in Table [2] are used for finding the Bayes estimators under LINEX and GE loss functions. The steps involved for obtaining the Bayes estimators are similar to SELF.

| Parameter | LINEX | GE |

|---|---|---|

3.3 Markov Chain Monte Carlo

Now, we use Markov Chain Monte Carlo (MCMC) method to obtain the Bayes estimators of the unknown parameters of UW distribution. The idea behind this to approximate the posterior distribution of parameters in the context of Bayesian analysis. The MCMC method is used to generate random sample from the posterior distribution and then use the generated data to obtain the Bayes estimator across the considered loss functions. For this, first we calculate the marginal densities of unknown parameters using the likelihood function and prior distribution. The marginal densities of and as

| (3.14) |

From (3.14) we observe that the generation of random sample for is easy as it has a nice closed form of gamma distribution (Geman and Geman (1987)). But for it is not easy as it does not have a nice analytical form of any known probability distribution. So for this, we employ the idea of Metropolis Hasting (MH) algorithm with normal distribution (see Gelman et al. (2013)) as the proposal density. The readers are referred to Arshad et al. (2023) to see the algorithm. Once we generate the random data of size say , we can obtain the Bayes estimators in the following manner. For the squared error loss function , LINEX loss function and GE loss function

4 Simulation Study

This section comprises of studying the behavior of the derived estimators on the simulated model. Various configurations of the parameters, sample sizes and priors have been used and reported in this section. Since dgos is an umbrella term containing several ordered random variable based models so we have obtained the results for two sub models that is, order statistic and lower record values. We have seen that for and the dgos model reduces to lower record value and for and the dgos model reduces to order statistics. The performance of Bayes estimators (order statistics and lower record values) are measured using the criteria of risk function. In order to calculate the risk, first we need to generate the random sample of dgos. For this purpose the algorithm discussed by Arshad et al. (2023) is considered here. Now, after generating the random sample for the both the submodels, we calculate Bayes estimators for Lindley approximation, T-K method and MCMC techniques and then the respective risks for each estimator are obtained for 1000 replications. The risks of estimators are calculated for the different configurations of parameters. Two configurations of priors are considered for calculation of Bayes estimators i.e., Prior I and Prior II The calculation is performed using R software(R Core Team (2023)). In addition to this, the convergence behaviour of generated Markov chain is tested with the aid of Gelman Rubin (GR) diagnostic (See Gelman et al. (2013)). With GR diagnostic we find that as we increase the number of iterations, the value of shrink reduction factor is getting close to 1. Hence, we conclude that convergence is achieved. The risks of various estimators are reported in Table [3-8]. From these tables, the following observations are made.

-

(i)

The Table [3] reports risks of Bayes estimates obtained using Lindley Approximation method for lower record values. From the table, it is observed that risks based on asymmetric loss functions (LINEX and GELF) are much smaller than symmetric loss function.

-

(ii)

The Table [4] reports risks of Bayes estimates obtained using T-K method for lower record values. From the table, it is observed that risks based on asymmetric loss functions (LINEX and GELF) are much smaller than symmetric loss function. It is also observed that risks of estimators based on T-K method are smaller than risk of estimators based on Lindley method.

-

(iii)

The Table [5] reports risks of Bayes estimates obtained using MCMC method for lower record values. From the table, it is observed that risks based on asymmetric loss functions (LINEX and GELF) are much smaller than symmetric loss function. It is also observed that mostly risks of estimators based on MCMC method are not smaller than risk of estimators based on T-K method.

- (iv)

-

(v)

From all the tables, it is observed that the risks of all estimators are decreasing as we increase the sample size irrespective of ordered random models. Also, Prior I seems to have shown lesser risk that Prior II.

-

(vi)

From these observations it is evident that Bayes estimators based on asymmetric loss functions (LINEX and GELF) are performing better based on their risks. So, In practical scenarios where the underlying assumptions considered in this study are satisfied, it is recommended to use asymmetric loss functions as it provides more flexibility to the model. Also, estimators based on T-K and MCMC methods are performing better than Lindley estimators.

| SELF | LINEX | GELF | ||||||||

| (1,1) | 5 | 0.2420 | 0.1380 | 0.0500 | 0.0343 | 0.0207 | 0.0087 | 0.0378 | 0.0125 | 0.0101 |

| 10 | 0.1123 | 0.0804 | 0.0171 | 0.0129 | 0.0074 | 0.0024 | 0.0203 | 0.0030 | 0.0053 | |

| 15 | 0.0717 | 0.0377 | 0.0086 | 0.0053 | 0.0019 | 0.0011 | 0.0114 | 0.0011 | 0.0031 | |

| (1.5,1) | 5 | 0.4072 | 0.1651 | 0.0468 | 0.0360 | 0.0210 | 0.0065 | 0.0616 | 0.0116 | 0.0123 |

| 10 | 0.3535 | 0.0888 | 0.0301 | 0.0261 | 0.0085 | 0.0035 | 0.0414 | 0.0066 | 0.0072 | |

| 15 | 0.3027 | 0.0416 | 0.0234 | 0.0230 | 0.0044 | 0.0028 | 0.0300 | 0.0044 | 0.0046 | |

| (1,1.5) | 5 | 0.3699 | 0.3627 | 0.0830 | 0.0333 | 0.0596 | 0.0122 | 0.0437 | 0.0387 | 0.0097 |

| 10 | 0.2016 | 0.2756 | 0.0285 | 0.0351 | 0.0179 | 0.0045 | 0.0261 | 0.0109 | 0.0058 | |

| 15 | 0.1219 | 0.1457 | 0.0145 | 0.0142 | 0.0059 | 0.0019 | 0.0166 | 0.0041 | 0.0040 | |

| (1.5,1.5) | 5 | 0.3586 | 0.2523 | 0.0524 | 0.0278 | 0.0387 | 0.0065 | 0.0665 | 0.0249 | 0.0122 |

| 10 | 0.2338 | 0.1606 | 0.0190 | 0.0177 | 0.0089 | 0.0025 | 0.0337 | 0.0057 | 0.0061 | |

| 15 | 0.1848 | 0.0749 | 0.0118 | 0.0110 | 0.0038 | 0.0014 | 0.0200 | 0.0034 | 0.0036 | |

| (1,1) | 5 | 0.3207 | 0.1897 | 0.0572 | 0.0340 | 0.0243 | 0.0069 | 0.0500 | 0.0226 | 0.0126 |

| 10 | 0.2641 | 0.1302 | 0.0451 | 0.0296 | 0.0163 | 0.0055 | 0.0419 | 0.0149 | 0.0098 | |

| 15 | 0.2398 | 0.0838 | 0.0369 | 0.0275 | 0.0103 | 0.0045 | 0.0350 | 0.0095 | 0.0076 | |

| (1.5,1) | 5 | 0.5144 | 0.1920 | 0.0718 | 0.0537 | 0.0241 | 0.0089 | 0.0881 | 0.0211 | 0.0164 |

| 10 | 0.4083 | 0.1354 | 0.0529 | 0.0438 | 0.0171 | 0.0067 | 0.0710 | 0.0158 | 0.0121 | |

| 15 | 0.3602 | 0.0973 | 0.0460 | 0.0394 | 0.0117 | 0.0058 | 0.0613 | 0.0110 | 0.0099 | |

| (1,1.5) | 5 | 0.2984 | 0.1138 | 0.0488 | 0.0322 | 0.0142 | 0.0058 | 0.0496 | 0.0169 | 0.0108 |

| 10 | 0.2634 | 0.0842 | 0.0398 | 0.0302 | 0.0104 | 0.0047 | 0.0415 | 0.0113 | 0.0082 | |

| 15 | 0.2532 | 0.0693 | 0.0370 | 0.0289 | 0.0087 | 0.0044 | 0.0367 | 0.0090 | 0.0070 | |

| (1.5,1.5) | 5 | 0.5417 | 0.1179 | 0.0683 | 0.0559 | 0.0142 | 0.0083 | 0.0907 | 0.0169 | 0.0155 |

| 10 | 0.4180 | 0.0855 | 0.0513 | 0.0449 | 0.0107 | 0.0064 | 0.0728 | 0.0115 | 0.0116 | |

| 15 | 0.3510 | 0.0705 | 0.0413 | 0.0381 | 0.0089 | 0.0052 | 0.0596 | 0.0094 | 0.0089 | |

| SELF | LINEX | GELF | ||||||||

| (1,1) | 5 | 0.1054 | 0.0937 | 0.0117 | 0.0122 | 0.0105 | 0.0014 | 0.0569 | 0.0000 | 0.0177 |

| 10 | 0.0992 | 0.0397 | 0.0120 | 0.0116 | 0.0046 | 0.0015 | 0.0291 | 0.0000 | 0.0161 | |

| 15 | 0.1127 | 0.0260 | 0.0130 | 0.0131 | 0.0031 | 0.0017 | 0.0323 | 0.0001 | 0.0161 | |

| (1.5,1) | 5 | 0.2304 | 0.1645 | 0.0315 | 0.0292 | 0.0188 | 0.0037 | 0.1231 | 0.0000 | 0.0273 |

| 10 | 0.2245 | 0.0721 | 0.0300 | 0.0297 | 0.0085 | 0.0036 | 0.0299 | 0.0034 | 0.0251 | |

| 15 | 0.2122 | 0.0472 | 0.0272 | 0.0277 | 0.0057 | 0.0033 | 0.0434 | 0.0067 | 0.0218 | |

| (1,1.5) | 5 | 0.1194 | 0.1189 | 0.0089 | 0.0126 | 0.0130 | 0.0011 | 0.0001 | 0.0044 | 0.0115 |

| 10 | 0.1064 | 0.0551 | 0.0093 | 0.0114 | 0.0063 | 0.0012 | 0.0036 | 0.0004 | 0.0124 | |

| 15 | 0.1152 | 0.0431 | 0.0108 | 0.0125 | 0.0051 | 0.0014 | 0.0025 | 0.0062 | 0.0136 | |

| (1.5,1.5) | 5 | 0.1611 | 0.1671 | 0.0181 | 0.0204 | 0.0173 | 0.0021 | 0.0000 | 0.0116 | 0.0210 |

| 10 | 0.1647 | 0.1124 | 0.0185 | 0.0214 | 0.0129 | 0.0022 | 0.0420 | 0.0096 | 0.0201 | |

| 15 | 0.1772 | 0.0692 | 0.0185 | 0.0227 | 0.0080 | 0.0023 | 0.0067 | 0.0023 | 0.0188 | |

| (1,1) | 5 | 0.2199 | 0.1413 | 0.0188 | 0.0277 | 0.0149 | 0.0030 | 0.0041 | 0.0247 | 0.0523 |

| 10 | 0.1894 | 0.0601 | 0.0190 | 0.0236 | 0.0062 | 0.0030 | 0.0044 | 0.0011 | 0.0321 | |

| 15 | 0.2063 | 0.0416 | 0.0209 | 0.0246 | 0.0046 | 0.0031 | 0.0122 | 0.0003 | 0.0295 | |

| (1.5,1) | 5 | 0.3543 | 0.2689 | 0.0400 | 0.0440 | 0.0302 | 0.0050 | 0.0607 | 0.0057 | 0.0623 |

| 10 | 0.3198 | 0.1056 | 0.0350 | 0.0416 | 0.0121 | 0.0045 | 0.0013 | 0.0081 | 0.0423 | |

| 15 | 0.3022 | 0.0609 | 0.0300 | 0.0371 | 0.0073 | 0.0038 | 0.0004 | 0.0004 | 0.0274 | |

| (1,1.5) | 5 | 0.2283 | 0.2136 | 0.0159 | 0.0261 | 0.0223 | 0.0024 | 0.0249 | 0.0043 | 0.0421 |

| 10 | 0.1949 | 0.1042 | 0.0165 | 0.0224 | 0.0110 | 0.0026 | 0.0527 | 0.0016 | 0.0249 | |

| 15 | 0.2344 | 0.0770 | 0.0191 | 0.0260 | 0.0085 | 0.0028 | 0.0193 | 0.0004 | 0.0288 | |

| (1.5,1.5) | 5 | 0.3220 | 0.3650 | 0.0285 | 0.0379 | 0.0375 | 0.0034 | 0.0738 | 0.0060 | 0.0523 |

| 10 | 0.3013 | 0.1695 | 0.0272 | 0.0375 | 0.0186 | 0.0035 | 0.0274 | 0.0182 | 0.0336 | |

| 15 | 0.3002 | 0.1018 | 0.0248 | 0.0356 | 0.0116 | 0.0032 | 0.2057 | 0.0260 | 0.0297 | |

| SELF | LINEX | GELF | ||||||||

| (1,1) | 5 | 0.1460 | 0.1129 | 0.0159 | 0.0166 | 0.0113 | 0.0023 | 0.0285 | 0.0079 | 0.0255 |

| 10 | 0.1386 | 0.0468 | 0.0162 | 0.0153 | 0.0054 | 0.0020 | 0.0268 | 0.0044 | 0.0219 | |

| 15 | 0.1193 | 0.0272 | 0.0158 | 0.0150 | 0.0036 | 0.0021 | 0.0234 | 0.0028 | 0.0193 | |

| (1.5,1) | 5 | 0.2543 | 0.1895 | 0.0327 | 0.0342 | 0.0189 | 0.0043 | 0.0368 | 0.0109 | 0.0297 |

| 10 | 0.2507 | 0.0810 | 0.0327 | 0.0326 | 0.0092 | 0.0043 | 0.0365 | 0.0061 | 0.0272 | |

| 15 | 0.2452 | 0.0480 | 0.0303 | 0.0319 | 0.0074 | 0.0043 | 0.0363 | 0.0051 | 0.0262 | |

| (1,1.5) | 5 | 0.1878 | 0.1280 | 0.0159 | 0.0180 | 0.0138 | 0.0018 | 0.0181 | 0.0076 | 0.0161 |

| 10 | 0.1629 | 0.0772 | 0.0144 | 0.0176 | 0.0080 | 0.0017 | 0.0177 | 0.0036 | 0.0157 | |

| 15 | 0.1346 | 0.0475 | 0.0124 | 0.0169 | 0.0058 | 0.0018 | 0.0171 | 0.0027 | 0.0155 | |

| (1.5,1.5) | 5 | 0.2183 | 0.1804 | 0.0222 | 0.0266 | 0.0175 | 0.0029 | 0.0259 | 0.0079 | 0.0223 |

| 10 | 0.2041 | 0.1096 | 0.0208 | 0.0250 | 0.0131 | 0.0027 | 0.0231 | 0.0044 | 0.0208 | |

| 15 | 0.1997 | 0.0787 | 0.0199 | 0.0246 | 0.0099 | 0.0025 | 0.0218 | 0.0033 | 0.0189 | |

| (1,1) | 5 | 0.5205 | 0.4258 | 0.0508 | 0.0584 | 0.0497 | 0.0064 | 0.1505 | 0.0236 | 0.1609 |

| 10 | 0.5178 | 0.1950 | 0.0481 | 0.0424 | 0.0228 | 0.0058 | 0.1290 | 0.0125 | 0.1296 | |

| 15 | 0.4821 | 0.0969 | 0.0438 | 0.0435 | 0.0115 | 0.0051 | 0.0920 | 0.0079 | 0.0842 | |

| (1.5,1) | 5 | 0.7781 | 0.6158 | 0.0741 | 0.0766 | 0.0699 | 0.0080 | 0.1052 | 0.0293 | 0.1078 |

| 10 | 0.5823 | 0.1947 | 0.0579 | 0.0687 | 0.0274 | 0.0075 | 0.0973 | 0.0144 | 0.0884 | |

| 15 | 0.5694 | 0.1114 | 0.0547 | 0.0645 | 0.0161 | 0.0072 | 0.0895 | 0.0095 | 0.0758 | |

| (1,1.5) | 5 | 0.6265 | 0.6602 | 0.0473 | 0.0669 | 0.0790 | 0.0054 | 0.1184 | 0.0205 | 0.1458 |

| 10 | 0.5195 | 0.3003 | 0.0396 | 0.0498 | 0.0367 | 0.0051 | 0.1066 | 0.0109 | 0.1199 | |

| 15 | 0.4970 | 0.1991 | 0.0402 | 0.0460 | 0.0268 | 0.0046 | 0.0911 | 0.0079 | 0.0982 | |

| (1.5,1.5) | 5 | 0.7412 | 0.7977 | 0.0575 | 0.0874 | 0.0960 | 0.0070 | 0.0899 | 0.0235 | 0.1076 |

| 10 | 0.6611 | 0.3901 | 0.0516 | 0.0687 | 0.0396 | 0.0060 | 0.0780 | 0.0106 | 0.0824 | |

| 15 | 0.5900 | 0.2081 | 0.0454 | 0.0706 | 0.0274 | 0.0060 | 0.0725 | 0.0079 | 0.0708 | |

| SELF | LINEX | GELF | ||||||||

| (1,1) | 5 | 0.0399 | 0.0642 | 0.0079 | 0.0052 | 0.0079 | 0.0010 | 0.0077 | 0.0103 | 0.0017 |

| 10 | 0.0626 | 0.0643 | 0.0083 | 0.0078 | 0.0081 | 0.0011 | 0.0087 | 0.0078 | 0.0013 | |

| 15 | 0.0621 | 0.0449 | 0.0075 | 0.0075 | 0.0055 | 0.0009 | 0.0076 | 0.0053 | 0.0011 | |

| (1.5,1) | 5 | 0.2937 | 0.0861 | 0.0284 | 0.0404 | 0.0111 | 0.0032 | 0.0419 | 0.0150 | 0.0034 |

| 10 | 0.0903 | 0.0572 | 0.0107 | 0.0105 | 0.0070 | 0.0014 | 0.0133 | 0.0067 | 0.0017 | |

| 15 | 0.0764 | 0.0424 | 0.0079 | 0.0097 | 0.0052 | 0.0010 | 0.0108 | 0.0050 | 0.0012 | |

| (1,1.5) | 5 | 0.0339 | 0.2035 | 0.0058 | 0.0046 | 0.0153 | 0.0006 | 0.0070 | 0.0172 | 0.0019 |

| 10 | 0.0533 | 0.0656 | 0.0069 | 0.0065 | 0.0080 | 0.0008 | 0.0070 | 0.0088 | 0.0009 | |

| 15 | 0.0567 | 0.0538 | 0.0063 | 0.0068 | 0.0068 | 0.0008 | 0.0069 | 0.0071 | 0.0009 | |

| (1.5,1.5) | 5 | 0.3050 | 0.2407 | 0.0198 | 0.0424 | 0.0248 | 0.0023 | 0.0422 | 0.0313 | 0.0025 |

| 10 | 0.1020 | 0.0778 | 0.0078 | 0.0096 | 0.0090 | 0.0010 | 0.0121 | 0.0093 | 0.0013 | |

| 15 | 0.0691 | 0.0535 | 0.0067 | 0.0089 | 0.0067 | 0.0009 | 0.0104 | 0.0071 | 0.0010 | |

| (1,1) | 5 | 0.1728 | 0.1628 | 0.0347 | 0.021 | 0.0203 | 0.0044 | 0.0236 | 0.0188 | 0.0057 |

| 10 | 0.1131 | 0.1015 | 0.0172 | 0.0142 | 0.013 | 0.0021 | 0.0149 | 0.0121 | 0.0025 | |

| 15 | 0.0851 | 0.063 | 0.0112 | 0.0103 | 0.0079 | 0.0014 | 0.0102 | 0.0075 | 0.0016 | |

| (1.5,1) | 5 | 0.2026 | 0.1493 | 0.0329 | 0.024 | 0.0197 | 0.0042 | 0.0302 | 0.0187 | 0.0051 |

| 10 | 0.1116 | 0.0889 | 0.0158 | 0.0136 | 0.0114 | 0.002 | 0.0155 | 0.0107 | 0.0022 | |

| 15 | 0.0874 | 0.0581 | 0.0104 | 0.0108 | 0.0073 | 0.0013 | 0.0117 | 0.0069 | 0.0014 | |

| (1,1.5) | 5 | 0.1714 | 0.0996 | 0.0302 | 0.0215 | 0.0121 | 0.0038 | 0.0241 | 0.0142 | 0.005 |

| 10 | 0.1181 | 0.0705 | 0.0164 | 0.0147 | 0.0088 | 0.002 | 0.0149 | 0.0092 | 0.0024 | |

| 15 | 0.0868 | 0.0597 | 0.0111 | 0.0108 | 0.0075 | 0.0014 | 0.0109 | 0.0077 | 0.0016 | |

| (1.5,1.5) | 5 | 0.1872 | 0.0975 | 0.0307 | 0.0224 | 0.0126 | 0.0039 | 0.0287 | 0.0149 | 0.005 |

| 10 | 0.1157 | 0.0696 | 0.0168 | 0.0143 | 0.0087 | 0.0021 | 0.0163 | 0.0091 | 0.0024 | |

| 15 | 0.0879 | 0.0597 | 0.0111 | 0.0109 | 0.0073 | 0.0014 | 0.0119 | 0.0075 | 0.0015 | |

| SELF | LINEX | GELF | ||||||||

| (1,1) | 5 | 0.1565 | 0.1548 | 0.0141 | 0.0164 | 0.0178 | 0.0017 | 0.0083 | 0.0119 | 0.0132 |

| 10 | 0.1109 | 0.0850 | 0.0113 | 0.0131 | 0.0104 | 0.0014 | 0.0003 | 0.0073 | 0.0088 | |

| 15 | 0.0868 | 0.0505 | 0.0092 | 0.0107 | 0.0062 | 0.0012 | 0.0009 | 0.0083 | 0.0062 | |

| (1.5,1) | 5 | 0.1547 | 0.1471 | 0.0179 | 0.0168 | 0.0168 | 0.0022 | 0.0079 | 0.0033 | 0.0115 |

| 10 | 0.1452 | 0.0749 | 0.0118 | 0.0164 | 0.0090 | 0.0015 | 0.0000 | 0.0185 | 0.0057 | |

| 15 | 0.1131 | 0.0484 | 0.0080 | 0.0132 | 0.0059 | 0.0010 | 0.0039 | 0.0030 | 0.0034 | |

| (1,1.5) | 5 | 0.1245 | 0.1593 | 0.0110 | 0.0128 | 0.0170 | 0.0014 | 0.0017 | 0.0055 | 0.0114 |

| 10 | 0.1038 | 0.1304 | 0.0096 | 0.0121 | 0.0153 | 0.0012 | 0.0000 | 0.0115 | 0.0083 | |

| 15 | 0.0745 | 0.0843 | 0.0073 | 0.0091 | 0.0102 | 0.0009 | 0.0113 | 0.0002 | 0.0058 | |

| (1.5,1.5) | 5 | 0.1298 | 0.1371 | 0.0124 | 0.0145 | 0.0147 | 0.0015 | 0.0002 | 0.0169 | 0.0097 |

| 10 | 0.1310 | 0.1156 | 0.0095 | 0.0145 | 0.0136 | 0.0012 | 0.0018 | 0.0170 | 0.0058 | |

| 15 | 0.1069 | 0.0785 | 0.0075 | 0.0125 | 0.0094 | 0.0009 | 0.0008 | 0.0006 | 0.0039 | |

| (1,1) | 5 | 0.4364 | 0.3500 | 0.0246 | 0.0414 | 0.0419 | 0.0030 | 0.0002 | 0.0846 | 0.0224 |

| 10 | 0.1841 | 0.1339 | 0.0144 | 0.0220 | 0.0173 | 0.0018 | 0.0091 | 0.0206 | 0.0119 | |

| 15 | 0.0893 | 0.0670 | 0.0101 | 0.0109 | 0.0084 | 0.0013 | 0.0100 | 0.0298 | 0.0074 | |

| (1.5,1) | 5 | 0.8246 | 0.3618 | 0.0247 | 0.0598 | 0.0436 | 0.0030 | 0.0454 | 0.0114 | 0.0170 |

| 10 | 0.3987 | 0.1218 | 0.0149 | 0.0425 | 0.0151 | 0.0018 | 0.0113 | 0.0004 | 0.0069 | |

| 15 | 0.2270 | 0.0694 | 0.0095 | 0.0268 | 0.0086 | 0.0012 | 0.0108 | 0.0003 | 0.0038 | |

| (1,1.5) | 5 | 0.4085 | 0.7131 | 0.0226 | 0.0385 | 0.0823 | 0.0028 | 0.0093 | 0.0237 | 0.0408 |

| 10 | 0.1834 | 0.2342 | 0.0141 | 0.0219 | 0.0291 | 0.0017 | 0.0001 | 0.0011 | 0.0158 | |

| 15 | 0.0997 | 0.1414 | 0.0096 | 0.0123 | 0.0176 | 0.0012 | 0.0098 | 0.0023 | 0.0088 | |

| (1.5,1.5) | 5 | 0.7049 | 0.5513 | 0.0242 | 0.0513 | 0.0608 | 0.0030 | 0.0843 | 0.0011 | 0.0216 |

| 10 | 0.3847 | 0.2198 | 0.0135 | 0.0414 | 0.0265 | 0.0017 | 0.0043 | 0.0057 | 0.0083 | |

| 15 | 0.2394 | 0.1348 | 0.0103 | 0.0281 | 0.0166 | 0.0013 | 0.0014 | 0.0000 | 0.0053 | |

| SELF | LINEX | GELF | ||||||||

| (1,1) | 5 | 0.1697 | 0.1478 | 0.0145 | 0.0188 | 0.0167 | 0.0019 | 0.0178 | 0.0105 | 0.0136 |

| 10 | 0.0953 | 0.0894 | 0.0102 | 0.0108 | 0.0108 | 0.0012 | 0.0102 | 0.0071 | 0.0074 | |

| 15 | 0.0737 | 0.0511 | 0.0087 | 0.0087 | 0.0058 | 0.0010 | 0.0079 | 0.0045 | 0.0051 | |

| (1.5,1) | 5 | 0.1812 | 0.1342 | 0.0176 | 0.0228 | 0.0125 | 0.0026 | 0.0194 | 0.0097 | 0.0128 |

| 10 | 0.1645 | 0.0758 | 0.0121 | 0.0156 | 0.0086 | 0.0013 | 0.0098 | 0.0064 | 0.0053 | |

| 15 | 0.1290 | 0.0478 | 0.0073 | 0.0130 | 0.0072 | 0.0011 | 0.0073 | 0.0052 | 0.0039 | |

| (1,1.5) | 5 | 0.1376 | 0.1662 | 0.0122 | 0.0137 | 0.0157 | 0.0014 | 0.0132 | 0.0094 | 0.0108 |

| 10 | 0.0911 | 0.1104 | 0.0092 | 0.0122 | 0.0120 | 0.0012 | 0.0106 | 0.0053 | 0.0085 | |

| 15 | 0.0753 | 0.0783 | 0.0080 | 0.0077 | 0.0105 | 0.0009 | 0.0071 | 0.0046 | 0.0060 | |

| (1.5,1.5) | 5 | 0.1699 | 0.1259 | 0.0141 | 0.0192 | 0.0179 | 0.0017 | 0.0152 | 0.0100 | 0.0099 |

| 10 | 0.1257 | 0.1164 | 0.0097 | 0.0147 | 0.0134 | 0.0012 | 0.0091 | 0.0062 | 0.0058 | |

| 15 | 0.0988 | 0.0765 | 0.0061 | 0.0119 | 0.0095 | 0.0010 | 0.0069 | 0.0039 | 0.0043 | |

| (1,1) | 5 | 0.3344 | 0.4099 | 0.0273 | 0.0562 | 0.0549 | 0.0036 | 0.0462 | 0.0224 | 0.0412 |

| 10 | 0.2050 | 0.1222 | 0.0177 | 0.0254 | 0.0201 | 0.0021 | 0.0195 | 0.0106 | 0.0148 | |

| 15 | 0.1101 | 0.0629 | 0.0110 | 0.0118 | 0.0087 | 0.0014 | 0.0117 | 0.0059 | 0.0087 | |

| (1.5,1) | 5 | 0.5720 | 0.3512 | 0.0252 | 0.0649 | 0.0412 | 0.0037 | 0.0300 | 0.0198 | 0.0211 |

| 10 | 0.4530 | 0.1176 | 0.0161 | 0.0408 | 0.0137 | 0.0019 | 0.0149 | 0.0088 | 0.0070 | |

| 15 | 0.2642 | 0.0599 | 0.0111 | 0.0242 | 0.0071 | 0.0012 | 0.0093 | 0.0056 | 0.0038 | |

| (1,1.5) | 5 | 0.4867 | 0.5031 | 0.0253 | 0.0403 | 0.0676 | 0.0031 | 0.0403 | 0.0167 | 0.0466 |

| 10 | 0.1473 | 0.2134 | 0.0137 | 0.0239 | 0.0366 | 0.0019 | 0.0185 | 0.0100 | 0.0188 | |

| 15 | 0.1315 | 0.1739 | 0.0120 | 0.0107 | 0.0158 | 0.0012 | 0.0099 | 0.0056 | 0.0088 | |

| (1.5,1.5) | 5 | 0.5585 | 0.5337 | 0.0258 | 0.0606 | 0.0552 | 0.0032 | 0.0266 | 0.0162 | 0.0238 |

| 10 | 0.3194 | 0.2301 | 0.0138 | 0.0433 | 0.0271 | 0.0018 | 0.0148 | 0.0082 | 0.0086 | |

| 15 | 0.2483 | 0.1506 | 0.0117 | 0.0265 | 0.0170 | 0.0013 | 0.0098 | 0.0056 | 0.0055 | |

5 Numerical Illustration: Cotton Production Data

To see the real world applicability of the developed results, we have taken the data of production of cotton in the United States of America. USA is among the top producers of cotton worldwide. U.S cotton production varies annually depending on weather trends, market preferences and governmental regulations.

| Year | Production |

|---|---|

| 2013-14 | 2.81 |

| 2014-15 | 3.55 |

| 2015-16 | 2.81 |

| 2016-17 | 3.74 |

| 2017-18 | 4.56 |

| 2018-19 | 4 |

| 2019-20 | 4.34 |

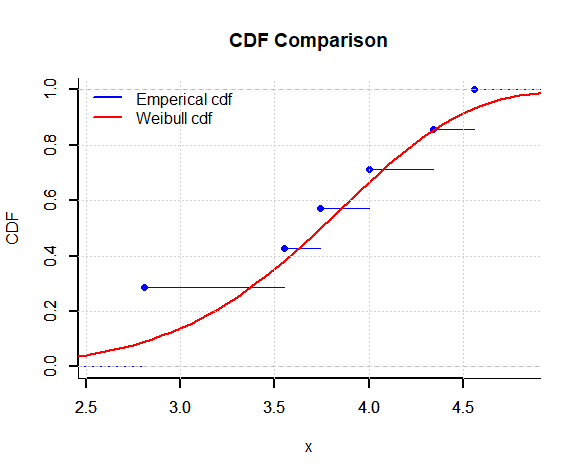

As it is mentioned clear in the Introduction (Section [1]) that the transformation follows UW distribution when follows Weibull distribution. So the authors decided that first its best to see the support of the data with respect to Weibull distribution and then by taking the transformation we will check the fitting for the UW distribution. In this direction, we frame hypotheses as against where represents cdf of Weibull distribution and represents empirical distribution of data. Using Kolmogorov-Smirnov (KS) test, we find that , p-value , which supports that weibull is a good fit.This claim is being supported by the visualization given in Figure [1]. To ensure that this distribution provides best fit among other distribution then we will commpare the fitting of the distribution with some well known distributions (See Table [10]). For this purpose, we are using the criteria of Akaike Information Criterion (AIC), Bayesian Information Criterion (BIC) and log likelihood. The estimates are obtained using maximum likelihood techniques.

| Distribution | Estimates | -log likelihood | AIC | BIC |

|---|---|---|---|---|

| Weibull | -6.643325 | 17.28665 | 17.17847 | |

| Gamma | -6.866839 | 17.73368 | 17.6255 | |

| Normal | -6.783007 | 17.56601 | 17.45783 | |

| Exponential | -16.13396 | 34.26793 | 34.21384 |

Now, we will show that the transformed data supports UW distribution. For this we apply KS test and it is found that for the KS statistics is 0.1958 with value 0.9525. As this article provides generalized nature of results for ordered random variables. Now we will present our results in the context of order statistics. From the data given in Table [9], the order statistics can easily be found. Based on order statistics, the Bayes estimates (for and ) of the unknown parameters are calculated and reported in Table [11].

Now, we show the application of lower record values in the context of the same application. For this purpose, we first extract lower record values from the transformed dataset. The obtained lower record values are 0.0602, 0.0287, 0.0238, 0.0183, 0.0130, 0.0105. Based on record values, the Bayes estimates (for and ) of the unknown parameters are calculated and reported in Table [12].

| Method | SELF | LINEX | GELF | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Lindley | 0.4876 | 1.2564 | 0.2134 | 0.4981 | 1.6754 | 0.2806 | 0.4129 | 1.6987 | 0.1659 |

| T-K | 0.5969 | 1.8678 | 0.2615 | 0.5354 | 1.8043 | 0.2513 | 0.4293 | 1.7724 | 0.1840 |

| MCMC | 0.2508 | 2.9533 | 0.1057 | 0.2183 | 2.7360 | 0.0989 | 0.0563 | 2.6828 | 0.0156 |

| Method | SELF | LINEX | GELF | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Lindley | 0.1231 | 1.5871 | 0.0876 | 0.1023 | 1.6251 | 0.0871 | 0.1104 | 1.6326 | 0.0611 |

| T-K | 0.1461 | 1.8000 | 0.0797 | 0.1269 | 1.7078 | 0.0629 | 0.1004 | 1.6811 | 0.0482 |

| MCMC | 0.2340 | 2.9930 | 0.1049 | 0.2038 | 2.6531 | 0.0982 | 0.0302 | 2.5683 | 0.0074 |

Statements and Declarations

-

•

Conflict of Interest: On behalf of all authors, the corresponding author states that there is no conflict of interest.

-

•

Funding Information: There is no funding available.

-

•

Data availability: The authors confirm that the data supporting the findings of this study are available in the article (See Table 9).

-

•

Ethics approval: Not Applicable

References

- Abd Al-Fattah et al. (2021) Abd Al-Fattah, A., Abd El-Kader, R., El-Helbawy, A., and Al-Dayian, G. (2021). Bayesian Estimation and Prediction for Exponentiated Generalized Inverted Kumaraswamy Distribution Based on Dual Generalized Order Statistics. Journal of Advances in Mathematics and Computer Science, 36(1):94–111.

- Ahsanullah (2004) Ahsanullah, M. (2004). Record values–theory and applications. University Press of America.

- Almetwally et al. (2023) Almetwally, E. M., Jawa, T. M., Sayed-Ahmed, N., Park, C., Zakarya, M., and Dey, S. (2023). Analysis of unit-Weibull based on progressive type-II censored with optimal scheme. Alexandria Engineering Journal, 63:321–338.

- Alotaibi et al. (2020) Alotaibi, R. M., Tripathi, Y. M., Dey, S., and Rezk, H. R. (2020). Bayesian and non-Bayesian reliability estimation of multicomponent stress–strength model for unit Weibull distribution. Journal of Taibah University for Science, 14(1):1164–1181.

- Alotaibi et al. (2021) Alotaibi, R. M., Tripathi, Y. M., Dey, S., and Rezk, H. R. (2021). Estimation of multicomponent reliability based on progressively Type II censored data from unit Weibull distribution. WSEAS Trans. Math, 20:288–299.

- Arnold et al. (2008) Arnold, B. C., Balakrishnan, N., and Nagaraja, H. N. (2008). A first course in order statistics. SIAM.

- Arshad et al. (2023) Arshad, M., J. Azhad, Q., Gupta, N., and Pathak, A. K. (2023). Bayesian inference of Unit Gompertz distribution based on dual generalized order statistics. Communications in Statistics-Simulation and Computation, 52(8):3657–3675.

- Burkschat et al. (2003) Burkschat, M., Cramer, E., and Kamps, U. (2003). Dual generalized order statistics. Metron-International Journal of Statistics, 61(1):13–26.

- David and Nagaraja (2004) David, H. A. and Nagaraja, H. N. (2004). Order statistics. John Wiley & Sons.

- Gelman et al. (2013) Gelman, A., Stern, H. S., Carlin, J. B., Dunson, D. B., Vehtari, A., and Rubin, D. B. (2013). Bayesian data analysis.

- Geman and Geman (1987) Geman, S. and Geman, D. (1987). Stochastic relaxation, Gibbs distributions, and the Bayesian restoration of images. In Readings in computer vision, pages 564–584. Elsevier.

- Iliev et al. (2019) Iliev, A. I., Rahnev, A., Kyurkchiev, N., and Markov, S. (2019). A study on the unit-logistic, unit-Weibull and Topp-Leone cumulative sigmoids. Biomath Communications, 6(1):1–15.

- Jaheen and Al Harbi (2011) Jaheen, Z. and Al Harbi, M. M. (2011). Bayesian estimation based on dual generalized order statistics from the exponentiated Weibull model. Journal of Statistical Theory and Applications, 10(4):591–602.

- Lindley (1980) Lindley, D. V. (1980). Approximate Bayesian methods. Trabajos de estadística y de investigación operativa, 31:223–245.

- Mazucheli et al. (2018) Mazucheli, J., Menezes, A., and Ghitany, M. (2018). The unit-Weibull distribution and associated inference. J. Appl. Probab. Stat, 13(2):1–22.

- Mazucheli et al. (2019) Mazucheli, J., Menezes, A. F., and Dey, S. (2019). Unit-Gompertz distribution with applications. Statistica, 79(1):25–43.

- Menezes et al. (2021) Menezes, A., Mazucheli, J., Alqallaf, F., and Ghitany, M. (2021). Bias-corrected maximum likelihood estimators of the parameters of the unit-weibull distribution. Austrian Journal of Statistics, 50(3):41–53.

- Pawlas and Szynal (2001) Pawlas, P. and Szynal, D. (2001). Recurrence relations for single and product moments of lower generalized order statistics from the inverse Weibull distribution. Demonstratio Math, 34(2):353–358.

- R Core Team (2023) R Core Team (2023). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Tierney and Kadane (1986) Tierney, L. and Kadane, J. B. (1986). Accurate approximations for posterior moments and marginal densities. Journal of the american statistical association, 81(393):82–86.