assumption

Prediction-Powered Inference

with Imputed Covariates and Nonuniform Sampling

Abstract

Machine learning models are increasingly used to produce predictions that serve as input data in subsequent statistical analyses. For example, computer vision predictions of economic and environmental indicators based on satellite imagery are used in downstream regressions; similarly, language models are widely used to approximate human ratings and opinions in social science research. However, failure to properly account for errors in the machine learning predictions renders standard statistical procedures invalid. Prior work uses what we call the Predict-Then-Debias estimator to give valid confidence intervals when machine learning algorithms impute missing variables, assuming a small complete sample from the population of interest. We expand the scope by introducing bootstrap confidence intervals that apply when the complete data is a nonuniform (i.e., weighted, stratified, or clustered) sample and to settings where an arbitrary subset of features is imputed. Importantly, the method can be applied to many settings without requiring additional calculations. We prove that these confidence intervals are valid under no assumptions on the quality of the machine learning model and are no wider than the intervals obtained by methods that do not use machine learning predictions.

Keywords: prediction-powered inference, prediction-based inference, missing data, measurement error, two-phase sampling designs, internal validation, bootstrap

1 Introduction

With increasingly rich data collection and a surge in open science initiatives, investigators now frequently rely on machine learning algorithms to predict quantities of interest based on large collections of related but indirect measurements. For example, in remote sensing studies, land cover is predicted from satellite images with computer vision algorithms. Similarly, millions of protein structures have been predicted from their amino acid sequences, but such structures are rarely measured directly because it is costly and difficult. This situation is pervasive—investigators are now often faced with large data sets that partially consist of machine learning outputs. However, using error-prone predictions from machine learning models as input data for statistical analysis (e.g., calculating regression coefficients) can lead to considerable biases and misleading conclusions. This has led to a flurry of recent works that develop methods to resolve the conundrum of how to use machine-learning predictions in a statistical analysis. In particular, when the analyst has access to data in which the predictions and the ground truth measurements are jointly available, it is possible to correct the bias of the machine learning model without assumptions on the quality of the predictions. In such settings, we develop methods to construct confidence intervals that account for errors in the machine learning predictions.

1.1 Problem setup

We first introduce our setting and two simple baselines. We assume a distribution over data points . The features are always observed, but measuring is costly (e.g., it requires expert human labeling). As such, few complete data points are available. In addition, we also have access to a much larger data set of machine-learning predictions of , which we denote by . The reader should interpret as a reasonably accurate but imperfect proxy of . Formally, we have access to a small complete () sample and a much larger incomplete () sample , adding up to data points total. Here, and are disjoint sets of indices such that . We denote by the size of the complete sample, .

Our goal is to estimate some quantity describing the distribution of . As our primary example in this work, we may wish to estimate the coefficients in a generalized linear model (GLM), obtained by regressing one component of on the remaining components. Note that the population regression coefficient vector for a GLM is still a well-defined estimand of interest even when a GLM does not accurately describe the distribution of . Typically an investigator will have access to a function (implemented in software) which takes a sample of data as input and returns an estimate of as an output. They can, therefore, readily deploy two natural and simple approaches to estimating :

-

1.

The naive approach: Act as if and apply to all available samples imputed with machine learning predictions: .

-

2.

The classical approach: Ignore the machine learning predictions and apply to the small complete sample only: .

Both approaches have both advantages and limitations. In particular, targets the correct parameter , but it does not leverage the potential power of machine-learning predictions. Meanwhile, the naive approach uses the abundant machine-learning predictions, but it targets the wrong parameter; even with infinite data, will be biased, unless the proxy comes from the exact same distribution as . Consequently, confidence intervals based on the naive approach are invalid. We observe in our real-data experiments (Section 4) that the naive estimator is sometimes biased by a factor of or more.

Given the limitations of the classical and naive approaches and the growing prevalence of machine-learning-imputed datasets, there is a growing interest in developing methods that leverage all available data, aiming for the best of both worlds. In this paper, we build on an easy-to-implement estimator proposed in Chen and Chen, (2000) and recently promoted in Tong et al., (2019), Yang and Ding, (2020), Kremers, (2021), Zrnic, (2024), Miao and Lu, (2024), and Gronsbell et al., (2024), which we will call the Predict-Then-Debias (PTD) estimator.

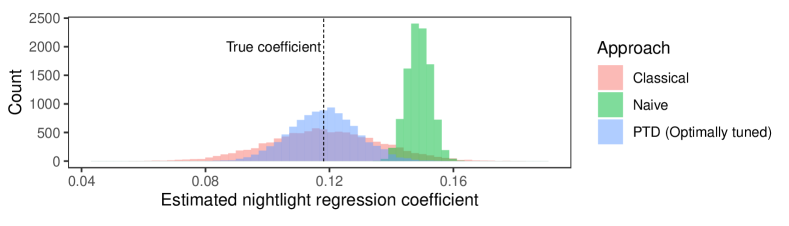

Preview example.

Figure 1 previews a real-data example, in which the goal is to estimate the regression coefficient for nightlights in a regression of housing price on population, nightlights, and road density. The complete sample had accurate measurements of all variables, while the incomplete sample had accurate measurements of housing price and population, but used predictions of nightlights and road density based on daytime satellite imagery to impute the missing covariates. The figure shows histograms for the three estimators across simulations. In each simulation, a random sample of size was drawn (with replacement) from the dataset of Rolf et al., 2021a , and of these samples were randomly assigned to the complete sample. The key takeaway is that the PTD estimator is approximately unbiased, unlike the naive estimator, and has a lower variance than the classical estimator. The naive approach was biased and consistently overestimated the nightlight regression coefficient. Meanwhile, the classical approach, which ignored the samples with proxy nightlight and road density measurements, had large variance—so much so that it sometimes produced estimates that were even less accurate than those of the naive approach.

1.2 A flexible solution: Predict-Then-Debias (PTD) estimator

The PTD estimator takes the naive estimator based on the incomplete sample—which is biased—and then adds a bias correction term based on the complete sample. In particular, let , , and ; the first estimator is similar to the previously defined naive estimator and the second estimator is the classical estimator. The basic Predict-Then-Debias estimator is then defined as

To study properties of , we presume standard regularity conditions, namely that will converge to as the sample size grows, and that and converge to some limit that we will denote by . Under such assumptions, is consistent: it converges to as . Meanwhile, the variance of this estimator has the potential to be quite small when . In particular, when the samples are independent, the variance of the th coordinate of is given by

The first term should be small, or even negligible, because is estimated from a large sample. If , then will tend to be near zero, implying the second variance is also small.

We can reduce the variance further by considering a matrix-valued tuning parameter—for any (possibly data-dependent) tuning matrix , define

If converges to some , is again consistent, meaning it will converge to in the large-sample limit. One can check that is minimized for each when . This optimal tuning matrix is unknown a priori but can be estimated with data. We refer to as the tuned PTD estimator (or sometimes just the PTD estimator for short).

While the PTD estimator is straightforward to compute and has desirable consistency and efficiency properties, streamlined approaches for constructing confidence intervals for the PTD estimator are less well-developed. One approach is to derive a central limit theorem for as well as a formula for its asymptotic variance, and then use the normal approximation to construct a confidence interval. In the context of GLM coefficient estimators, this approach was taken by Chen and Chen, (2000), among others, but to generalize to other estimation problems requires additional mathematical calculations.

An alternative approach to constructing confidence intervals for is to use the bootstrap. In particular, one can fix the tuning matrix , resample the data with replacement times, recalculate on each resampled version of the dataset, and return the interval given by the -th and -th largest obtained estimates. This easy-to-generalize approach is presented explicitly in Algorithm 1 when the complete and incomplete datasets are IID. Notably, implementation of this algorithm merely requires software to evaluate on various resamplings of the input data. We highlight that these confidence intervals are asymptotically valid no matter how accurate the machine-learning predictions are, making them an appealing choice for use with complex machine-learning models. Moreover, when estimating regression coefficients, the confidence intervals are valid even when the regression is misspecified. This manuscript discusses the validity of this algorithm and its extensions to cases with weighted, cluster, and stratified sampling.

1.3 Our contribution

We develop bootstrap-based approaches to construct confidence intervals for the PTD estimator, generalizing to new settings and providing precise technical conditions under which the intervals have theoretical guarantees of validity. Building off Algorithm 1, the contributions of our paper are as follows:

-

•

In Algorithm 2, we use inverse probability weighting to generalize Algorithm 1 to handle weighted two-phase sampling designs, where the complete sample is a weighted random subsample of all data points. We provide sufficient conditions under which this algorithm returns asymptotically valid confidence intervals.

- •

-

•

In Section B we present a cluster bootstrap (e.g., Davison and Hinkley, , 1997) modification of Algorithms 2 and 3. In many applications of interest it is of practical importance to select entire geographical clusters within which all units will be measured. Similarly, we present modifications of Algorithm 2 that can be used when the data is obtained via stratified sampling; such settings are common when the data comes from statistical surveys.

In addition, we discuss the efficiency of the PTD estimator and compare it to the PPI++ estimator. We show a situation where the latter is more efficient than the former, a first in the literature.

Finally, in Section 4 we show with real-data experiments that our bootstrap-based approaches achieve the desired coverage, while providing confidence intervals that are narrower than simply using the complete sample. Notably, these simulations include cases where the covariates—not the response variables—are imputed via machine learning, a setting that has received little attention in the literature on prediction-powered inference. R implementations of the methods and our experiments can be found at https://github.com/DanKluger/Predict-Then-Debias_Bootstrap.

1.4 Related work

Because the literature on methods for using proxies in a statistical analysis is vast, we restrict our attention to discussing methods that use a small complete subsample, sometimes called internal validation data, where all variables of interest, including the proxies, are jointly measured. This has historically been investigated in the literature on measurement error (Carroll et al., , 2006), missing data (Little and Rubin, , 2019), and survey sampling (Särndal et al., , 2003).

Measurement error and missing data:

Measurement error techniques such as regression calibration and SIMEX (e.g., Carroll et al., , 2006) are generally designed for cases where internal validation data is unavailable, so they rely on assumptions about the prediction error. Such methods are sometimes used even when there is an internal validation sample (Spiegelman et al., , 2001; Fong and Tyler, , 2021), but they still rely critically upon the nondifferential measurement error assumption, unlike the present work. Multiple imputation methods (e.g., Little and Rubin, , 2019) are often used when internal validation data is available (Carroll et al., , 2006; Guo and Little, , 2011; Proctor et al., , 2023). Multiple imputation does not require the nondifferential measurement error assumption, but it instead requires Bayesian modelling assumptions about the distribution of the missing data (in our case the ground truth values) given the observed data (in our case the predictions and other widely available variables). As a result, confidence intervals for parameters of interest given by multiple imputation-based approaches do not have frequentist guarantees. This is a critical limitation in practice—data-based experiments in Proctor et al., (2023) show that multiple imputation confidence intervals with nominal level 95% have coverage of less than 80% in some cases.

Semiparametric and semisupervised inference:

Approaches from the semiparametrics literature (Robins et al., , 1994; Tsiatis, , 2006), give a broad class of estimators for the setting of internal validation with asymptotically valid confidence intervals. As discussed in Chen and Chen, (2000), the PTD estimator is a special case of the semiparametric estimator from Robins et al., (1994), and therefore the semiparametric estimator, with an optimal estimate of the nuisance function, can be more efficient than the PTD estimator. A recent body of work on semi-supervised inference considers methods for leveraging a large unlabeled dataset and a small labeled dataset and focuses on efficiency in high-dimensional and semiparametric regimes for specific types of estimators. In particular, recent works studied efficient estimation of means (Zhang et al., , 2019; Zhang and Bradic, , 2021; Zhang et al., , 2023), linear regression parameters (Chakrabortty and Cai, , 2018), quantiles (Chakrabortty et al., , 2022), and quantile and average treatment effect estimates (Chakrabortty and Dai, , 2022). While their efficiency is appealing, the complexity of semiparametric methods (which require estimating a nuisance function) makes them less accessible to users who do not have extensive statistical training.

Loss-debiasing approaches:

More recently, prediction-powered inference (PPI) (Angelopoulos et al., 2023a, ), and other works that build upon or extend it (Angelopoulos et al., 2023c, ; Miao et al., , 2023; Gan et al., , 2024; Zrnic and Candès, 2024a, ; Zrnic and Candès, 2024b, ), propose more streamlined methods for leveraging internal validation data for convex M-estimation tasks that use few tuning parameters. The estimators from these works have some conceptual similarities to the PTD estimator but have important technical differences: instead of debiasing the naive estimator directly they debias the empirical loss based on predictions. Such methods lead to valid confidence intervals, however they do not easily generalize to many use cases of interest. For example, the debiased empirical loss in PPI++ (e.g., Angelopoulos et al., 2023c, ) can be nonconvex when using predicted covariates in a regression, violating the conditions under which valid coverage holds. See (Ji et al., , 2025) for a further discussion of the connections between the PTD and PPI estimators, and their semiparametrically efficient variants.

Several works in this space have considered nonuniform sampling (e.g., Fisch et al., , 2024; Zrnic and Candès, 2024a, ), however they do not rely on the PTD estimator or bootstrap confidence intervals, and thus require case-by-case calculations to form valid confidence intervals. Lastly, we note that there are methods for the same setting as PPI that use modeling assumptions (Wang et al., , 2020; McCaw et al., , 2023)—see Motwani and Witten, (2023) for a comparison with the PPI approach.

Predict-Then-Debias approaches:

A simple alternative to approaches that use the validation sample to debias the empirical loss is to use the PTD approach, which readily generalizes to a broad class of estimators. PTD-type estimators have been studied for GLMs (Chen and Chen, , 2000; Tong et al., , 2019; Kremers, , 2021), Cox regression models (Kremers, , 2021), treatment effect estimators (Yang and Ding, , 2020), and more (Miao and Lu, , 2024; Gronsbell et al., , 2024; Zrnic, , 2024). However, some of these works (Chen and Chen, , 2000; Tong et al., , 2019) use asymptotic variance calculations to construct confidence intervals, but generalizing to estimators beyond GLMs requires bespoke asymptotic variance calculations.

Resampling approaches offer a different path forward that may bypass such calculations. Kremers, (2021) and Miao and Lu, (2024) propose jackknife-based and bootstrap-based approaches, respectively, for estimating the covariance of the debiased estimator. However, neither work proves the consistency of the covariance estimators. Yang and Ding, (2020) do provide theoretical guarantees for a bootstrapped-based approach, but that work proposes bootstrapping the asymptotic linear expansion terms rather than the estimator itself. This requires the calculation of the linear expansion for the estimator at hand. By contrast, our approach does not require such calculation, and we prove that the confidence intervals are valid under weak conditions.

Lastly, a critical practical challenge is that internal validation samples are often weighted, stratified, or clustered random samples. To our knowledge, only Yang and Ding, (2020) (and a brief remark in Kremers, (2021)) address the case where the validation sample is weighted and existing work does not address the cases where it is a clustered or stratified sample.

2 Properties of the PTD estimator

We formalize the key properties of the tuned PTD estimator . Moreover, we present a couple of strategic ways to choose the tuning matrix and discuss the efficiency of the optimally tuned relative to the classical estimator , the PPI++ estimator (Angelopoulos et al., 2023c, ), and a commonly considered variant of the PTD estimator. Readers not interested in the theoretical development may prefer to skim the next two sections other than the algorithm definitions and then turn to the experiments in Section 4.

2.1 Formal setting and assumptions

We start by introducing the formal setting, notation, and some assumptions. Let be a random vector drawn from a distribution denoting the actual data and be a random vector drawn from a distribution denoting the machine-learning-imputed proxy for . The reader should think of the case where only a subset of the components of are imputed with predictions— and . The investigator has proxy samples , and for a subset of these samples the corresponding vector of actual data, , is also available.

The goal is to use the small number of samples of and the larger number of samples of to estimate some parameter , where is a function that maps probability distributions to a summary statistic of interest. Note that can be any quantity describing the joint distribution of the entries of . For example, can be the population mean or quantile of a component of , the population correlation between two components of , the population regression coefficient in a generalized linear model (GLM) relating one component of to other components of . We denote by the corresponding parameter of the joint distribution of the proxy .

We now introduce assumptions about the sampling of that are analogous to the missing-at-random and positivity assumptions commonly seen in the missing data and sample survey literatures, respectively. Let be the indicator taking on the value if is observed and otherwise. We assume the following:

Assumption 1 (Sampling and missingness assumption).

-

(i)

IID assumption: ;

-

(ii)

Missing at random assumption: ;

-

(iii)

Known sampling probability: is known;

-

(iv)

Overlap assumption: For some , almost surely.

For two-phase labeling designs, where an investigator first starts with and subsequently chooses the subset of samples where is measured (i.e where ), the investigator can easily ensure by design that parts (ii)–(iv) of Assumption 1 hold. Note that when and , this means that is allowed to depend on the observable features .

We consider settings where and can be estimated using standard statistical software and an appropriate choice of weights. Specifically, let be the data matrix of the proxies whose ’th row is and let be the data matrix of the actual data whose ’th row is (which is observed only when ). Further, define the weights

typically used for inverse probability weighted estimators, and let Let be a function that takes a data matrix and a weights vector and estimates . For many choices of targets , there are statistical software packages that implement such , allowing a data matrix and a sample weight vector as inputs. Finally, we use the following shorthand notation

to describe the weighted estimator for based on the true data from the complete sample, the weighted estimator for based on the proxy data from the complete sample, and the weighted estimator for based on the proxy data from the incomplete sample, respectively. We remark that, even though many rows of are unobserved, can still be evaluated because the missing rows of are given zero weight according to the vector .

We study the tuned PTD estimator:

| (1) |

where is a tuning matrix. Recall its key property: it converges to regardless of the quality of the proxy samples. Formally, provided , , , and for some fixed , then

In words, this means the PTD estimator is targeting the parameter , which is the value that the algorithm would output with an infinitely large complete sample.

2.2 Asymptotic normality of the PTD estimator

We now show that the tuned PTD estimator can be well approximated by a normal distribution under certain regularity conditions. We begin with an assumption that holds for a large class of estimator functions .

Assumption 2 (Asymptotic weighted linearity of , , and ).

There exist functions and such that each component of the random vector has mean and finite variance, and such that, as ,

-

(i)

,

-

(ii)

,

-

(iii)

.

While Assumption 2 is stated in an abstract form, it holds for a broad class of common statistical estimators and there is often a mathematical formula that can be used to derive the functions and . For example, under certain regularity conditions, and can be found by calculating the influence function of with respect to the distributions and , respectively (Hampel, , 1974; van der Vaart, , 1998). Assumption 2 also holds for M-estimators under fairly mild regularity conditions. M-estimators include a broad class of estimators of interest such as sample means, sample quantiles, linear and logistic regression coefficients, and regression coefficients in quantile regression or robust regression, among others. See Appendix E.1, particularly Proposition E.1 and Assumptions 5 and 6, for further details justifying Assumption 2 for M-estimation.

Under Assumptions 1 and 2, the following proposition shows that is asymptotically normally distributed. Let denote a random vector with the same distribution as and let and denote the functions guaranteed by Assumptions 2. We let , , and denote covariance matrices of interest, with , , and being the asymptotic covariance matrices of , , and , respectively.

We defer all proofs of the results from the main text to the appendix.

2.3 Optimal tuning matrix

Ideally, the tuning matrix is chosen to minimize the (asymptotic) variance of each component of . In Equation (2), note that for each , only depends on the th row of , which we denote by . Further, is a quadratic function in that is minimized when , where is the th canonical vector. Hence, setting , where

| (3) |

simultaneously minimizes each diagonal entry of . If one uses the tuning matrix

| (4) |

and , , and , then and, by Proposition 2.1, we have a tuned PTD estimator with minimal asymptotic variance.

Because has tuning parameters, estimating can be unstable in small sample sizes. To address this, we also consider the optimal tuning matrix among the class of diagonal tuning matrices, reducing the number of tuning parameters from to . Note that, by minimizing univariate quadratic equations, the asymptotic variance in Equation (2) is minimized across all diagonal choices of when letting , where is the diagonal matrix with

| (5) |

Therefore, selecting such that minimizes the asymptotic variance of among all possible diagonal choices of .

2.4 Efficiency of the tuned PTD estimator

We next state that is more efficient than the classical estimator : for each coordinate , the asymptotic variance of is smaller than that of . This result has been established in similar settings (e.g., Chen and Chen, (2000); Gronsbell et al., (2024)).

To build intuition about the asymptotic efficiency of and how it compares to that of other estimators, we consider the case where is univariate (i.e., ) and where the complete sample is a uniform random subsample (i.e., for some , always). In this case, the following holds

This reveals two natural facts. First, has a larger gain over the classical approach when , the probability of observing the real data, is small. This is intuitive: if most real samples are observed, then there is little to be gained from machine learning imputations and is a good estimator. Second, the greater the correlation between and , the greater the efficiency of relative to the classical approach. If , we expect and that would be large.

Next, we can compare the variance of the optimally tuned PTD estimator to that of the optimally tuned PPI++ estimator (Angelopoulos et al., 2023c, ), which we call in the same setting. We prove in Appendix F.2 that

This is of interest because it shows that recent proposals in the prediction-powered inference literature that involve debiasing the loss function (e.g., Angelopoulos et al., 2023c ) are not necessarily less efficient than the PTD approach. Indeed, in Appendix F.2 we present examples where and other examples where . The latter is the first such case exhibited in the literature.

Lastly, the reader might wonder about the efficiency of a PTD-type estimator that uses all samples (rather than just incomplete samples) to calculate . It turns out this variant has the same asymptotic variance as the PTD estimator herein, provided the complete sample is a uniform random subsample and the optimal tuning matrices are used; see Appendix F.3.

3 Bootstrap confidence intervals

We now develop bootstrap algorithms that construct confidence intervals based on . Algorithm 2 generalizes Algorithm 1 to non-uniformly weighted settings. We then introduce a computational speedup in Algorithm 3. We prove that both algorithms provide asymptotically valid confidence intervals under suitable assumptions. Finally, we discuss generalizations of these bootstrap approaches to clustered and stratified sampling settings.

The bootstrap approaches presented in this section are more flexible than CLT-based approaches for constructing confidence intervals in the sense that they do not require the mathematical calculation of the asymptotic variance terms. Nonetheless, for completeness, we present a CLT-based approach in Appendix A.

3.1 Main bootstrap algorithm and its validity

We first introduce the necessary notation. Let for each . Further, let be the empirical distribution of from the samples, where assigns a point mass of at and elsewhere. Next, define a single bootstrap draw of , , , and to be the version of that quantity with a starred superscript in the following procedure:

-

1.

Draw and set for each .

-

2.

Set , and such that the ’th rows of and are and , respectively.

-

3.

Evaluate , , and .

-

4.

Set .

With this in hand, Algorithm 2 computes confidence intervals at level for each component of by first taking independent draws from the bootstrap distribution and returning the and empirical quantiles of each coordinate.

To show that Algorithm 2 leads to asymptotically valid confidence intervals, we must first introduce some further notation and an assumption. Let

| (6) |

Under a fixed realization of the data (i.e., for a fixed ), we call the distribution of generated by the above 4-step empirical bootstrap procedure the bootstrap distribution of , and we use to denote the probability that an event occurs under the bootstrap distribution of . Below we introduce a bootstrap consistency assumption for that heuristically says the random bootstrap distribution of uniformly converges to the distribution of . The below consistency assumption is not trivial to check; however, because much literature has been devoted to proving the bootstrap consistency for a large variety of settings and estimators of interest (Shao and Tu, , 1995; Kosorok, , 2008; van der Vaart and Wellner, , 2023), we state bootstrap consistency of as an assumption and then give precise technical conditions where the assumption will be met for example use cases of interest.

Assumption 3 (Bootstrap consistency and limiting distribution of ).

For each fixed ,

-

(i)

and

-

(ii)

converges in distribution to some random variable with a symmetric distribution and a continuous, strictly increasing CDF.

This assumption holds in a variety of use cases of interest. For many common statistical estimands of interest, such as Z-estimators (including linear or logistic regression coefficients), quantiles, and L-statistics, among others, Assumption 3 will hold, provided that Assumption 1 and mild regularity conditions (that are specific to the estimand) are met.

Remark 1 (Bootstrap Consistency for Z-estimators).

Z-estimators are estimators that solve for the zero of estimating equations, and include M-estimators with differentiable loss functions. When , , and are Z-estimators, is also a Z-estimator. Many works in the theoretical bootstrap literature (e.g., Chapters 10.3 and 13 of Kosorok, (2008)) show that under certain standard and fairly mild regularity conditions, Z-estimators satisfy the bootstrap consistency criteria in Assumption 3 or a stronger version of it. In Appendix E.2.1, by direct application of such results, we present some sufficient (although not necessary) conditions under which Assumption 3 holds for Z-estimators.

Remark 2 (Hadamard differentiable estimators).

As another route toward verifying Assumption 3 holds, when , , and , are each Hadamard differentiable functions of the empirical distributions of or , will also be a Hadamard differentiable function of a particular empirical distribution. In Appendix E.2.2 and Theorem E.1, we characterize precisely when and how Hadamard differentiability of the component estimators implies Assumption 3. A number of estimators including quantiles and trimmed means are Hadamard differentiable functions of the empirical distribution function.

The following theorem shows that Algorithm 2 provides asymptotically valid confidence intervals under certain conditions.

3.2 A faster bootstrap procedure

Algorithm 2 can be slow if the incomplete sample is large because it requires computing for different bootstrap draws, which requires evaluating on a large data set with each draw. (For the percentile bootstrap it is often recommended to choose or larger (e.g., Little and Rubin, (2019)).) Next, we propose a convolution-based speed-up (Algorithm 3) that replaces the computation of with a Gaussian approximation. We show that this is valid when is asymptotically Gaussian and when a consistent estimator of its asymptotic variance is readily available. This convolution-based speed-up exploits the fact that is asymptotically uncorrelated with and .

Implementation of the speed-up for Algorithm 2 merely requires a consistent estimator of . Under Assumptions 1 and 2, standard statistical software can typically be used to return a matrix estimating such that as (e.g., see Remark 3). Letting be such a readily computable estimate of , our proposed algorithm is as follows:

The following theorem shows that under certain conditions, Algorithm 3 gives asymptotically valid confidence intervals.

Theorem 3.2.

We note that while standard software can often be used to return a consistent estimator of (which is all that is required for Algorithm 3), it cannot typically be used to find a consistent estimator for (which is required for constructing CLT-based confidence intervals via Algorithm 4 in Appendix A). Therefore, Algorithm 3 is easier to generalize to new estimators than the purely CLT-based Algorithm 4 while having faster runtime than Algorithm 2.

3.3 Subroutines for estimating optimal tuning matrix

In this subsection, we present subroutines for Algorithms 2 and 3 to compute the tuning matrix . The subroutines are designed to have the same computational complexity as the corresponding algorithm. The subroutines can easily be modified such that estimates the optimal tuning matrix rather than the optimal diagonal tuning matrix by modifying the last line to return ; see Equation (4).

3.4 Cluster and stratified bootstraps

In many applications of interest, it is more economical to measure for entire clusters of samples (e.g., all samples in a geographical unit) and forgo measuring entirely on the remaining clusters. Such cases will violate Assumption 1 and can render the confidence intervals from Algorithms 2 and 3 too narrow. These algorithms can readily be extended using a cluster bootstrap scheme to appropriately construct confidence intervals in such settings. The cluster bootstrap modification involves resampling entire clusters with replacement as opposed to resampling individual samples with replacement—see Section B.1 and Algorithm 5 for details.

Another common setting is stratified sampling, which can often reduce the number of samples needed. In the stratified sampling that we consider, the population is partitioned into strata and a fixed number of incomplete samples and complete samples are drawn from each strata. In Appendix B.2 we present a modification of Algorithm 2 (Algorithm 6) that constructs confidence intervals for the PTD estimator that account for the stratified sampling scheme. We caution readers that Algorithm 6 is only designed to work in regimes where there is a small number of large strata and instead point readers to Section 6.2.4 of Shao and Tu, (1995) for variants of the bootstrap for stratified samples that are designed to work in other regimes. Theoretical justifications of Algorithms 5 and 6 are out of scope for the current work, but we refer the reader to Davison and Hinkley, (1997); Shao and Tu, (1995) and references therein for details on these methods and Cheng et al., (2013) for a theoretical justification of the cluster bootstrap.

4 Experiments

In this section, we present a variety of experiments using four different real datasets to validate our method and compare it to the classical approach (i.e., only using the gold-standard data from the complete sample). We also consider a number of variations of the PTD approach that involve different algorithms for constructing confidence intervals (see Section 4.4) and different tuning matrix choices (see Section 4.5).

Our experiments focus on regression tasks such as linear regression, logistic regression, and quantile regression, and some of them involve weighted, stratified, or clustered labelling schemes. Let and be the subvectors of corresponding to the response variable and covariate vector, respectively, and define and as the analogous subvectors of . Our regression experiments fall into 3 main categories:

-

1.

Error-in-response regressions: In an error-in-response regression, the investigator has access to a large incomplete sample with measurements of and and can obtain access to a much smaller complete sample with measurements of , and .

-

2.

Error-in-covariate regressions: In an error-in-covariate regression, the investigator has access to a large incomplete sample with measurements of and and can obtain access to a much smaller complete sample with measurements of , , and .

-

3.

Error-in-both regressions: In an error-in-both regression, the investigator has access to a large incomplete sample with measurements of and and can obtain access to a much smaller complete sample with measurements of , , , and .

Recent works on prediction-powered inference (Angelopoulos et al., 2023a, ; Angelopoulos et al., 2023c, ; Miao and Lu, , 2024; Zrnic, , 2024) only test their methods for error-in-response regressions, so we focus on error-in-covariate and error-in-both regressions.

The experiments conducted are summarized in Table 1. We describe the experimental setup and datasets in more detail the following subsections.

| Exp # | Dataset | Model | Error Regime | Sampling Scheme | Algorithms | ||

| 1 | AlphaFold | Logistic Reg | Error-in-response | Weighted | 2,3,4 | ||

| 2 | Housing Price | Linear Reg | Error-in-covariate | Uniform | 2,3,4 | ||

| 3 | Housing Price | Quantile Reg | Error-in-covariate | Uniform | 2,3 | ||

| 4 | Tree cover | Linear Reg | Error-in-both | Uniform | 2,3,4 | ||

| 5 | Tree cover | Linear Reg | Error-in-both | Clustered | 5, 3/5 | ||

| 6 | Tree cover | Logistic Reg | Error-in-both | Uniform | 2,3,4 | ||

| 7 | Census | Linear Reg | Error-in-covariate | Stratified | 6 |

4.1 Experimental setup

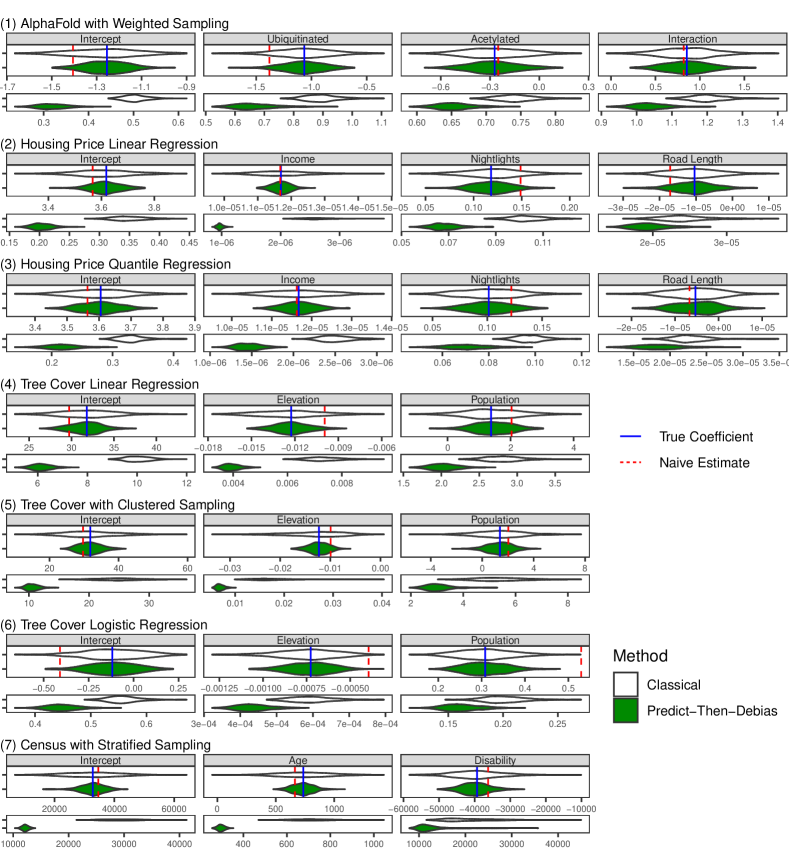

For each experiment we use the following validation procedure. We start with samples where and are jointly measured, where and . We calculate the “ground truth” regression coefficients by regressing on using all samples (blue lines in Figure 2) and the “naive” regression coefficients by regressing on using all samples (red lines in Figure 2). Even if the samples are drawn from a superpopulation, we can treat estimated from the samples as our estimand of interest because all simulations are based on these empirical samples. We then conduct 500 simulations in which we

-

1.

Randomly select a subsample of the samples of size . A subset of the samples are randomly assigned to the complete sample, where all variables are observed. For all samples not assigned to the complete sample, the values are withheld.

-

2.

Compute the classical estimator of and the corresponding 90% confidence interval using only data from the complete sample. Confidence intervals are calculated using the sandwich estimator for .

-

3.

Run various PTD-based approaches using from the complete sample and from the remaining samples to estimate and a corresponding 90% confidence interval. In particular, we consider a number of choices of tuning matrices and Algorithms 2– 4, to construct 90% confidence intervals for . In some cases, we forgo Algorithm 4 or both Algorithms 3 and 4 because of lack of implemented analytic expressions.

Unless otherwise specified, step 1 is done by uniform random sampling without replacement; however, in some of our experiments we use a weighted, stratified, or cluster sampling scheme. Finally, we calculate the coverage for each method by calculating the percentage of the simulations in which the 90% confidence intervals contained (estimated from regressing on using all samples).

4.2 Datasets

We briefly describe the datasets used and experiments conducted. Further details are presented in Appendix G.

AlphaFold Experiments:

We used a dataset of samples that originated from Bludau et al., (2022) and was downloaded from Zenodo (Angelopoulos et al., 2023b, ). Each sample had indicators of whether there was acetylation and ubiquatination, and an indicator of whether the protein region was an internally disordered region (IDR) coupled with a prediction of based on AlphaFold (Jumper et al., , 2021). We test Algorithms 2–4 when the estimands are the regression coefficients for a logisitic regression of on . was withheld on all samples outside from a randomly selected complete sample. The complete sample was selected according to a weighted sampling scheme such that for each of the 4 possible combinations of and , there were 250 complete samples in expectation.

Housing Price Experiments:

We used a dataset of gold-standard measurements and remote sensing-based estimates of economic and environmental variables from Rolf et al., 2021a ; Rolf et al., 2021b that was used in Proctor et al., (2023) to study multiple imputation methods. Each of the samples corresponded to a distinct grid cell, and included grid cell-level averages of housing price, income, nightlight intensity, and road length. We considered settings where the estimand was the regression coefficient of housing price on income, nightlight intensity, and road length, and where outside of a small complete sample, gold-standard measurements of nightlights and road length were unavailable (but proxies based on daytime satellite imagery were available for all samples). In Experiment 2 the estimands were regression coefficients from a linear regression, and the estimands in Experiment 3 were regression coefficients for a quantile regression with .

Tree Cover Experiments:

We used a dataset of samples of grid cells taken from the previously mentioned data source (Rolf et al., 2021a, ; Rolf et al., 2021b, ). The variables included the percent of tree cover and grid cell-level averages of population and elevation. We considered settings where the estimands were the regression coefficients of tree cover on elevation and population, and where outside of a small complete sample, gold-standard measurements of tree cover and population were unavailable (but satellite-based proxies were available for all samples). In Experiments 4 and 5 the estimands were regression coefficients from a linear regression, while in Experiment 6 the estimands were regression coefficients from a logistic regression where the tree cover was binarized according to a meaningful threshold from a forestry perspective (Oswalt et al., , 2019). In Experiment 5, the data and the complete samples were sampled via cluster sampling (where each cluster corresponded to a 0.5° 0.5° grid cell), and the cluster bootstrap method (Algorithm 5) was tested.

Census Experiments:

We used a dataset of income, age, and disability status of individuals from California taken from the 2019 US Census survey and downloaded via the Folktables interface (Ding et al., , 2021). We considered a setting where the estimands are the regression coefficients of income on age and disability status, and where disability status was only measured on a small complete sample. Outside the complete sample we used predictions of disability status based on a machine learning model that we trained using the previous year’s census data. In Experiment 7 the incomplete sample and complete sample were taken according to stratified random sampling (with strata based on age buckets), and we tested Algorithm 6.

4.3 Point estimates and confidence interval size

For each experiment and regression coefficient, Figure 2 gives a violin plot across the 500 simulations of the point estimates and widths of the 90% confidence intervals for the classical approach and for the PTD approach. In this figure, we only present the results for the PTD approach when the tuning matrix is chosen to estimate the asymptotically optimal diagonal tuning matrix given in Equation (5) and when confidence intervals are calculated using the fully bootstrap approach (e.g., Algorithm 2). Figure 2 shows that in a fair number of cases the naive estimator has substantial bias, and that consistent with cautionary notes in the literature (van Smeden et al., , 2019; Kluger et al., , 2024) the bias is often not attenuation towards zero. Meanwhile the classical and PTD estimators are consistently unbiased (they are centered on the blue line). The PTD estimator consistently has lower variance and narrower confidence intervals than the classical estimator as guaranteed by Proposition 2.2.

Section 4.4 and Figure 3 present the empirical coverages and confidence interval widths for the faster alternatives to constructing confidence intervals for the PTD estimator. Meanwhile, Section 4.5 and Figure 4 presents the empirical coverages and confidence interval widths for other choices for the tuning matrix besides those estimating the asymptotically optimal diagonal tuning matrix.

4.4 Comparing different confidence interval methods

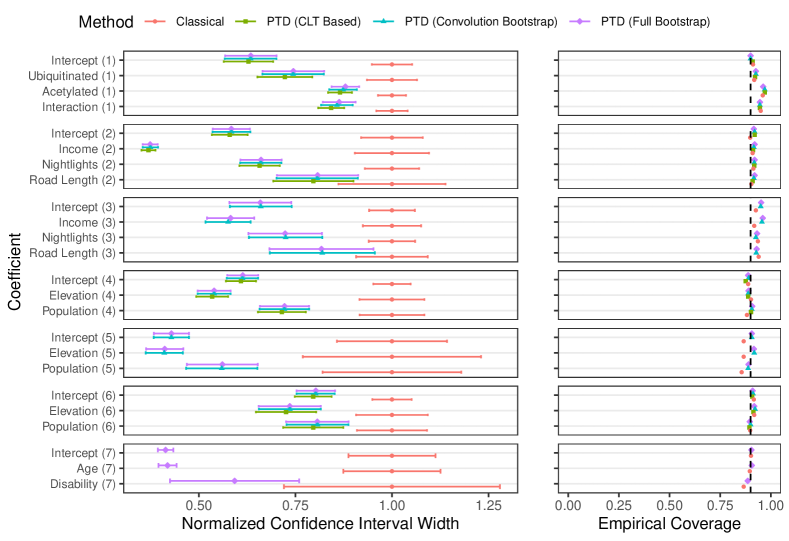

In Figure 3, we present how the confidence interval widths and empirical coverage varied with the algorithm used to construct confidence intervals for . With the exception of the AlphaFold and the quantile regression experiments, in which mild overcoverage was observed, the confidence intervals for had empirical coverages (across 500 simulations) that were close to the target coverage of . The overcoverage in the AlphaFold experiment can be explained by the fact that each simulation involved sampling points without replacement from a dataset with points. Had we instead sampled with replacement or used a larger dataset, our superpopulation inference approach would not substantially overestimate the simulation scheme-specific variance of .

The 3 different approaches for constructing confidence intervals yielded similar empirical coverages and confidence interval widths across the 7 experiments. Therefore, we recommend that investigators mainly consider runtime and ease-of-implementation when choosing between constructing CLT-based, convolution bootstrap-based, and fully bootstrap approaches to constructing confidence intervals for . Of these 3 approaches, CLT-based approaches are hardest to implement and generalize (requiring asymptotic variance calculations or an existing software implementation) but have the lowest runtime. On the other end of the spectrum, fully bootstrap approaches can be implemented in a few lines of code and require no asymptotic variance calculations but have the longest runtime. The convolution bootstrap approach is a compromise that leverages existing software that calculates asymptotic variance approximations and has intermediate runtime.

4.5 Comparing different tuning matrix choices

The results presented in Figures 2 and 3 all use a tuning matrix that estimates the optimal diagonal tuning matrix given in Equation (5). We next present additional results when using the tuning matrix given in Equation (4) (which estimates the optimal tuning matrix among all matrices) and also when using the untuned PTD estimator (which has ). In Figure 4, for each regression coefficient, experiment, and tuning matrix choice we show the average and standard deviation of the 90% confidence interval widths across the 500 simulations. For ease of comparison across coefficients and experiments, the confidence interval widths are only presented for full percentile bootstrap approaches (e.g., Algorithms 2, 5, and 6) and are normalized by the average confidence interval width of the classical estimator across the 500 simulations. Figure 4 also shows the empirical coverage for each tuning matrix choice.

The confidence intervals when using the optimal diagonal tuning matrix are typically similar in size to those when using the optimal tuning matrix. Moreover, the slightly narrower confidence intervals of the optimal tuning matrix comes at a cost of slightly poorer coverage, particularly in the stratified and clustered sampling experiments, which we suspect is driven by the high number of tuning parameters relative to the effective sample size. Meanwhile, the untuned PTD estimator sometimes has confidence intervals of comparable size to those of the optimally tuned PTD estimator, but it can also have confidence intervals that are much larger even than those of the classical estimator. Overall, this suggests that using a diagonal tuning matrix is enough to give intervals that are nearly as small as the full tuning matrix, while an untuned PTD estimator is best avoided. Since the diagonal tuning is in general more stable because it has fewer parameters, we recommend this as the default choice.

Acknowledgments

This work was supported by the MIT Institute for Data Systems and Society Michael Hammer Postdoctoral Fellowship, by the U.S. Department of Energy Computational Science Graduate Fellowship under Award Number DE-SC0023112, and by a Stanford Data Science postdoctoral fellowship. The authors also wish to thank Lihua Lei for helpful discussions.

References

- (1) Angelopoulos, A. N., Bates, S., Fannjiang, C., Jordan, M. I., and Zrnic, T. (2023a). Prediction-powered inference. Science, 382(6671):669–674.

- (2) Angelopoulos, A. N., Bates, S., Fannjiang, C., Jordan, M. I., and Zrnic, T. (2023b). Prediction-powered inference: Data sets. 10.5281/zenodo.8397451.

- (3) Angelopoulos, A. N., Duchi, J. C., and Zrnic, T. (2023c). PPI++: Efficient prediction-powered inference. arXiv preprint arXiv:2311.01453.

- Bludau et al., (2022) Bludau, I., Willems, S., Zeng, W.-F., Strauss, M. T., Hansen, F. M., Tanzer, M. C., Karayel, O., Schulman, B. A., and Mann, M. (2022). The structural context of posttranslational modifications at a proteome-wide scale. PLoS biology, 20(5):e3001636.

- Carroll et al., (2006) Carroll, R. J., Ruppert, D., Stefanski, L. A., and Crainiceanu, C. M. (2006). Measurement Error in Nonlinear Models: A Modern Perspective, Second Edition. Chapman and Hall/CRC, London, 2nd edition.

- Chakrabortty and Cai, (2018) Chakrabortty, A. and Cai, T. (2018). Efficient and adaptive linear regression in semi-supervised settings. The Annals of Statistics, 46(4):1541 – 1572.

- Chakrabortty and Dai, (2022) Chakrabortty, A. and Dai, G. (2022). A general framework for treatment effect estimation in semi-supervised and high dimensional settings. arXiv preprint arXiv:2201.00468.

- Chakrabortty et al., (2022) Chakrabortty, A., Dai, G., and Carroll, R. J. (2022). Semi-supervised quantile estimation: Robust and efficient inference in high dimensional settings. arXiv preprint arXiv:2201.10208.

- Chen and Chen, (2000) Chen, Y.-H. and Chen, H. (2000). A unified approach to regression analysis under double-sampling designs. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 62(3):449–460.

- Cheng et al., (2013) Cheng, G., Yu, Z., and Huang, J. Z. (2013). The cluster bootstrap consistency in generalized estimating equations. Journal of Multivariate Analysis, 115:33–47.

- Davison and Hinkley, (1997) Davison, A. C. and Hinkley, D. V. (1997). Further Ideas, page 70–135. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press.

- Ding et al., (2021) Ding, F., Hardt, M., Miller, J., and Schmidt, L. (2021). Retiring adult: New datasets for fair machine learning. In Advances in Neural Information Processing Systems.

- Fisch et al., (2024) Fisch, A., Maynez, J., Hofer, R. A., Dhingra, B., Globerson, A., and Cohen, W. W. (2024). Stratified prediction-powered inference for effective hybrid evaluation of language models. In The Thirty-eighth Annual Conference on Neural Information Processing Systems.

- Fong and Tyler, (2021) Fong, C. and Tyler, M. (2021). Machine learning predictions as regression covariates. Political Analysis, 29(4):467–484.

- Gan et al., (2024) Gan, F., Liang, W., and Zou, C. (2024). Prediction de-correlated inference: A safe approach for post-prediction inference. Australian & New Zealand Journal of Statistics, 66(4):417–440.

- Gronsbell et al., (2024) Gronsbell, J., Gao, J., Shi, Y., McCaw, Z. R., and Cheng, D. (2024). Another look at inference after prediction. arXiv preprint arXiv:2411.19908.

- Guo and Little, (2011) Guo, Y. and Little, R. J. (2011). Regression analysis with covariates that have heteroscedastic measurement error. Statistics in Medicine, 30(18):2278–2294.

- Hampel, (1974) Hampel, F. R. (1974). The influence curve and its role in robust estimation. Journal of the American Statistical Association, 69(346):383–393.

- Ji et al., (2025) Ji, W., Lei, L., and Zrnic, T. (2025). Predictions as surrogates: Revisiting surrogate outcomes in the age of ai. arXiv preprint arXiv:2501.09731.

- Jumper et al., (2021) Jumper, J., Evans, R., Pritzel, A., Green, T., Figurnov, M., Ronneberger, O., Tunyasuvunakool, K., Bates, R., Žídek, A., Potapenko, A., et al. (2021). Highly accurate protein structure prediction with alphafold. Nature, 596(7873):583–589.

- Kluger et al., (2024) Kluger, D. M., Lobell, D. B., and Owen, A. B. (2024). Biases in estimates of air pollution impacts: the role of omitted variables and measurement errors. arXiv preprint arXiv:2310.08831.

- Koenker, (2024) Koenker, R. (2024). quantreg: Quantile Regression. R package version 5.93.

- Kosorok, (2008) Kosorok, M. R. (2008). Introduction to Empirical Processes and Semiparametric Inference. Springer Series in Statistics. Springer.

- Kremers, (2021) Kremers, W. K. (2021). A general, simple, robust method to account for measurement error when analyzing data with an internal validation subsample. arXiv preprint arXiv:2106.14063.

- Lehmann and Romano, (2005) Lehmann, E. L. and Romano, J. P. (2005). Testing Statistical Hypotheses: Third Edition. Springer Series in Statistics. Springer.

- Little and Rubin, (2019) Little, R. J. A. and Rubin, D. B. (2019). Statistical Analysis with Missing Data: Third Edition. Wiley Series in Probability and Statistics. Wiley, Hoboken, NJ, 3rd edition.

- McCaw et al., (2023) McCaw, Z. R., Gaynor, S. M., Sun, R., and Lin, X. (2023). Leveraging a surrogate outcome to improve inference on a partially missing target outcome. Biometrics, 79(2):1472–1484.

- Miao and Lu, (2024) Miao, J. and Lu, Q. (2024). Task-agnostic machine-learning-assisted inference. In 38th Conference on Neural Information Processing Systems. NeurIPS. https://arxiv.org/abs/2405.20039.

- Miao et al., (2023) Miao, J., Miao, X., Wu, Y., Zhao, J., and Lu, Q. (2023). Assumption-lean and data-adaptive post-prediction inference. arXiv preprint arXiv:2311.14220.

- Motwani and Witten, (2023) Motwani, K. and Witten, D. (2023). Revisiting inference after prediction. Journal of Machine Learning Research, 24(394):1–18.

- Oswalt et al., (2019) Oswalt, S. N., Smith, W. B., Miles, P. D., and Pugh, S. A. (2019). Forest Resources of the United States, 2017: a technical document supporting the Forest Service 2020 RPA Assessment. U.S. Department of Agriculture, Forest Service.

- Proctor et al., (2023) Proctor, J., Carleton, T., and Sum, S. (2023). Parameter recovery using remotely sensed variables. Technical report, National Bureau of Economic Research.

- Robins et al., (1994) Robins, J. M., Rotnitzky, A., and Zhao, L. P. (1994). Estimation of regression coefficients when some regressors are not always observed. Journal of the American Statistical Association, 89(427):846–866.

- (34) Rolf, E., Proctor, J., Carleton, T., Bolliger, I., Shankar, V., Ishihara, M., Recht, B., and Hsiang, S. (2021a). A generalizable and accessible approach to machine learning with global satellite imagery. Nature Communications, 12(1):4392.

- (35) Rolf, E., Proctor, J., Carleton, T., Bolliger, I., Shankar, V., Ishihara, M., Recht, B., and Hsiang, S. (2021b). A generalizable and accessible approach to machine learning with global satellite imagery. https://www.codeocean.com/capsule/6456296/tree/v2.

- Särndal et al., (2003) Särndal, C.-E., Swensson, B., and Wretman, J. (2003). Model assisted survey sampling. Springer Science & Business Media.

- Schatzman, (2002) Schatzman, M. (2002). Numerical Analysis: A Mathematical Introduction. Numerical Analysis: A Mathematical Introduction. Clarendon Press.

- Shao and Tu, (1995) Shao, J. and Tu, D. (1995). The Jackknife and Bootstrap. Springer Series in Statistics. Springer.

- Spiegelman et al., (2001) Spiegelman, D., Carroll, R. J., and Kipnis, V. (2001). Efficient regression calibration for logistic regression in main study/internal validation study designs with an imperfect reference instrument. Statistics in Medicine, 20(1):139–160.

- Tong et al., (2019) Tong, J., Huang, J., Chubak, J., Wang, X., Moore, J. H., Hubbard, R. A., and Chen, Y. (2019). An augmented estimation procedure for ehr-based association studies accounting for differential misclassification. Journal of the American Medical Informatics Association, 27(2):244–253.

- Tsiatis, (2006) Tsiatis, A. A. (2006). Models and Methods for Missing Data, pages 137–150. Springer Series in Statistics. Springer.

- van der Vaart, (1998) van der Vaart, A. W. (1998). Asymptotic Statistics. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press.

- van der Vaart and Wellner, (2023) van der Vaart, A. W. and Wellner, J. A. (2023). Weak Convergence and Empirical Processes: With Applications to Statistics (2nd Edition). Springer Series in Statistics. Springer.

- van Smeden et al., (2019) van Smeden, M., Lash, T. L., and Groenwold, R. H. H. (2019). Reflection on modern methods: five myths about measurement error in epidemiological research. International Journal of Epidemiology, 49(1):338–347.

- Wang et al., (2020) Wang, S., McCormick, T. H., and Leek, J. T. (2020). Methods for correcting inference based on outcomes predicted by machine learning. Proceedings of the National Academy of Sciences, 117(48):30266–30275.

- Yang and Ding, (2020) Yang, S. and Ding, P. (2020). Combining multiple observational data sources to estimate causal effects. Journal of the American Statistical Association, 115(531):1540–1554. PMID: 33088006.

- Zhang et al., (2019) Zhang, A., Brown, L. D., and Cai, T. T. (2019). Semi-supervised inference: General theory and estimation of means. The Annals of Statistics, 47(5):2538 – 2566.

- Zhang and Bradic, (2021) Zhang, Y. and Bradic, J. (2021). High-dimensional semi-supervised learning: in search of optimal inference of the mean. Biometrika, 109(2):387–403.

- Zhang et al., (2023) Zhang, Y., Chakrabortty, A., and Bradic, J. (2023). Double robust semi-supervised inference for the mean: selection bias under mar labeling with decaying overlap. Information and Inference: A Journal of the IMA, 12(3):2066–2159.

- Zrnic, (2024) Zrnic, T. (2024). A note on the prediction-powered bootstrap. arXiv preprint arXiv:2405.18379.

- (51) Zrnic, T. and Candès, E. J. (2024a). Active statistical inference. arXiv preprint arXiv:2403.03208.

- (52) Zrnic, T. and Candès, E. J. (2024b). Cross-prediction-powered inference. Proceedings of the National Academy of Sciences, 121(15):e2322083121.

Appendix A Constructing confidence intervals using the CLT

To construct confidence intervals for based on Proposition 2.1, the investigator needs to have consistent estimates of , , , and . This is formalized in the following assumption, and remarks are given at the end of the section describing how an investigator can obtain consistent estimates of , , , and .

Assumption 4.

(Consistent asymptotic variance estimators) The investigator can use the data to construct matrices , , and such that as , , , , and .

Corollary A.1.

Proof.

Note that by Assumptions 1 and 2 as well as Proposition 2.1, , where

By Assumption 4 and since , if we let be the matrix returned by Algorithm 4, by the continuous mapping theorem.

Now fix . By the previous results and . Therefore by Slutsky’s lemma, Now let denote the CDF of a standard normal distribution, let be the quantile of a standard normal, and let be the confidence interval returned by Algorithm 4. Hence

Above the penultimate step holds by the definition of convergence in distribution and continuity of , since , and the last step holds by symmetry of the standard normal and the fact that is the quantile of a standard normal. ∎

The following remarks give some guidance on how investigators can readily construct covariance matrix estimators that satisfy Assumption 4.

Remark 3.

When calculating , , and via software that evaluates given a data matrix and weight vector as inputs, standard statistical software commonly also returns estimated covariance matrices , , and . Often, setting , , will give covariance matrices such that , , and . For example, if evaluates an M-estimator (such as a GLM or a sample quantile), under Assumptions 1, 2 and other fairly mild regularity conditions, the sandwich estimators , , and will be consistent for , , and after rescaling by . Moreover, for many common M-estimators, standard statistical software will compute sandwich estimators for given a data matrix and weight vector as input.

While , , and can often be consistently estimated using standard statistical software, most statistical software packages would not be equipped to estimate , because it is the asymptotic covariance matrix of two different estimators. That being said, in many cases it is possible for an investigator to derive a formula for that can then be used to construct a consistent estimator of . In the next remark, we describe how to construct a consistent estimator of for -estimation tasks (and a similar analytic approach can also be taken to construct consistent estimators of , , and ).

Remark 4.

(Estimating for M-estimation tasks) Using the same setup and notation as in Section E.1, and assuming the regularity conditions of Proposition E.1 and that the loss function is smooth enough for Hessians and expectations to be swapped, and . Moreover note that by Assumption 1 and the tower property , , and . Hence,

Setting

it follows that under additional regularity conditions beyond those in Proposition E.1 (e.g., if and are locally Lipschitz in a neighborhood of and ) . Therefore, under such regularity conditions, an investigator can consistently estimate with the above estimator provided that they have a formula for the gradient and Hessian of the loss function with respect to evaluated at and .

An alternative approach to estimating that does not require analytic calculations is to use the bootstrap. The method in Miao and Lu, (2024) proposes using the bootstrap to produce a consistent estimator of and subsequently applying (a uniform sampling version of) Algorithm 4. In this paper, we do not consider the approach of using the bootstrap-based estimator of for use in Algorithm 4 for two reasons. First, Algorithm 4 is intended to have fast runtime whereas the bootstrap can be time consuming to implement. Second, if users are confronting a setting where it is difficult to find an analytic formula for , Algorithms 2 and 3 will provide asymptotically valid confidence intervals in certain settings of interest where the method in Miao and Lu, (2024) could fail to provide asymptotically valid confidence intervals. In particular, in the settings of Theorems 3.1 (or Theorem 3.2), Algorithms 2 (or Algorithm 3) provides asymptotically valid confidence intervals; however, the method in Miao and Lu, (2024) uses a bootstrap-based estimator of the variance which requires an additional uniform integrability condition on the squared bootstrap pivots (e.g., see Chapter 3.1.6 of Shao and Tu, (1995)).

Appendix B Bootstrap for cluster or stratified sampling settings

B.1 Cluster bootstrap

Suppose that the samples are partitioned into clusters and that within each cluster, is either unobserved on all samples or is observed on all samples. In particular, let denote clusters which form a partition of (i.e., for each , satisfying and for all ). In the cluster labelling schemes that we consider, is originally unobserved on all samples and then subsequently measured via the following procedure:

-

1.

Draw for some .

-

2.

For each , if , collect observations of for each and if forgo collecting the observations for which .

According to the above sampling scheme, note that for each , the inverse probability weights are given by and for each . Letting and , Algorithm 5 gives a cluster bootstrap modification to Algorithm 2 that corrects confidence interval widths to account for the correlations induced by above sampling scheme.

We note that Algorithm 5 can also be sped up using the same convolution approach as in Algorithm 3 when is asymptotically normal. In particular one can replace the relatively slow step in Line 7 of Algorithm 5, by independently drawing , where is the estimated covariance matrix of that only needs to be calculated once outside of the for loop. To use this speedup, should appropriately account for the cluster sampling scheme (e.g., this can be done fairly quickly using the vcovCL function in R).

B.2 Bootstrap for stratified sampling

Suppose that the population of samples can be partitioned into disjoint strata . In particular, let denote strata which form a partition of (i.e., for each , satisfying and for all ). We consider stratified sampling schemes where initially none of the samples are observed and then subsequently for each the investigator:

-

1.

Obtains a random subsample without replacement of of size . For each let be an indicator of whether was observed in this subsample.

-

2.

Obtains a random subsample without replacement of of size and forgoes collecting observations on this subsample. For each let be an indicator of whether was observed in this subsample.

According to the above sampling scheme, note that for each , the inverse probability weights are given by and for each . Letting and , Algorithm 6 gives a stratified bootstrap modification to Algorithm 2 that corrects confidence interval widths to account for the above sampling scheme. We remark that this version of the stratified bootstrap is only designed to work in settings where there is a small number of large strata.

Appendix C Proofs of theoretical results from Section 2

In this appendix we prove the propositions displayed in Section 2. The proofs of those propositions, as well as those of many other theoretical results in the paper, rely on the following lemma that establishes asymptotic normality of . Before presenting this lemma and these proofs we display formulas from the main text that are regularly used in these proofs and we also present some helpful notation. In particular, recall that using Assumption 2, we let be functions such that each component of has mean and finite variance, and such that

Further define

| (7) |

where recall that each of the displayed blocks of is a matrix, and , , and

Proof.

Let , and let denote a random variable with the same distribution as . Note that by Assumption 2 and rearranging terms,

| (8) |

where denotes a vector of terms that converge to in probability as . Note that under Assumption 1,

Above the first equality holds by the tower property. The second equality above holds because (by the missing at random assumption in Assumption 1, and is a deterministic function of and ). The third equality above holds by linearity of conditional expectation and by our definitions that , , and . The final equality above holds by Assumption 2.

Since , by combining Equation (8), the multivariate CLT, and Slutsky’s lemma, it is clear that , where

Thus to complete the proof it remains to show defined in Equation (7). Letting and , and recalling the formulas for , ,, and it is clear that

Hence it suffices to show that and . To do this recall that since , , , and . Hence,

and

The last steps in the above two displays hold because always and therefore always.

∎

C.1 Proof of Proposition 2.1

C.2 Proof of Proposition 2.2

Appendix D Proofs of theoretical results from Section 3

In this appendix, we prove Theorems 3.1 and 3.2 which give guarantees that under certain assumptions, Algorithms 2 and 3 give asymptotically valid confidence intervals. Because the proofs are lengthy they are broken into 3 main parts:

-

1.

The first part is showing that the bootstrap is consistent for various pivots of interest. In particular, we refresh the reader with Assumption 3, which gives Bootstrap consistency for bootstrapped pivots of the form where , and we also introduce some helpful notation for studying bootstrap consistency (we point the reader to Section E.2 for sufficient conditions under which Assumption 3 holds). Subsequently, in Theorem D.1 we prove bootstrap consistency for pivots that arise in Algorithm 3 that are approximately drawn from the bootstrap distribution, which is a critical step in the proof of Theorem 3.2.

-

2.

The second part provides auxiliary lemmas, including Lemma D.2 that gives conditions under which the percentile bootstrap leads to asymptotically valid confidence intervals. A notable difference between Lemma D.2 and standard results about when the percentile bootstrap is valid (e.g., Theorem 4.1 in Shao and Tu, (1995)), is that Lemma D.2 allows terms to be ignored.

-

3.

The third part is proofs of asymptotic validity of the confidence intervals from Algorithm 2 (see Section D.3.1) and Algorithm 3 (see Section D.3.2). These proofs piece together the specific algorithms and assumptions by applying bootstrap consistency results and the auxiliary lemma about asymptotic validity of percentile bootstrap confidence intervals.

D.1 Bootstrap consistency notation and results

We now reintroduce the notions of the bootstrap distribution and of bootstrap consistency, using notation convenient to our setting. Recall that . We let denote the empirical distribution of from the samples, which can be thought of as a random distribution. Fixing , we draw and use to denote the probability of an event that depends on the values of . After drawing , we define to be the components of for each , we define

and we define

and . We call the distribution of generated by this procedure under a fixed the bootstrap distribution of . Note that even though many values of (and in turn rows of ) are unobserved, for any draw from the bootstrap distribution, is still observed and can be evaluated because whenever the th row of is missing, the corresponding weight .

We now introduce the notions of pivots and bootstrap consistency. Given a random variable (often called a pivot) which depends on samples of the data drawn from and a procedure to randomly generate that depends on the empirical distribution , the bootstrap distribution of is said to be consistent (with respect to the sup-norm) if

When proving and leveraging bootstrap consistency results it is convenient to define the metric on the collection of CDFs such that for any (possibly random) CDFs and ,

| (9) |

Therefore if and are the random CDF and CDF given by and , respectively, then equivalently the bootstrap distribution of is consistent if . Another way of restating Assumption 3(i) is that the bootstrap distribution is consistent for for any arbitrary (we defer sufficient conditions under which Assumption 3 holds to Section E.2).

Assumption 3 along with Lemma D.2, proved in the next subsection, can be used to show that Algorithm 2 provides asymptotically valid confidence intervals. While the bootstrap consistency claim from Assumption 3 involves quantities generated in Algorithm 2, is drawn from a Gaussian distribution rather than from the actual bootstrap distribution in Algorithm 3. In the next theorem, we prove a bootstrap consistency result for an approximate draw of the pivot from the bootstrap distribution (which is generated in Algorithm 3 up to terms).

Theorem D.1.

Proof.

Fix and . Define to be the th row of the matrix so that . Let

be the Random CDFs of the bootstrap pivot (and pivot component). Letting , also define

Let to be the expectation with respect to just the independent (which conditions on ), let for all , and let be the probability density function of a random vector. Then for each ,

Above the 2nd step holds by independence of and Fubini’s theorem, and recall that is defined at (9). Hence taking the supremum over all ,

Above the last step holds because letting such that ,

so by Assumption 3, .

We now show that . To do this note that since is independent of the data

Also note that by applying Proposition 2.1 to the case where for all ,

Further, letting and observing that , by Lemma C.1 and the continuous mapping theorem , where by Formula (7), . Since is independent of for all and , . Thus letting , it is clear that and also . Letting denote the CDF of , denote the CDF of and recalling that is the CDF of , by Polya’s theorem (Theorem 11.2.9 in Lehmann and Romano, (2005)), and both converge to , uniformly in . Combining these results,

where the last step holds from uniform convergence of and to . Finally combining this with a previous result

∎

D.2 Lemmas for showing validity of percentile bootstrap

In this section, we present two lemmas that, along with the bootstrap consistency results in the previous subsection, allow us to prove the validity of Algorithms 2 and 3. The next lemma shows that Assumption 3 implies that and , when viewed as sequences indexed by integers for some , are bounded in probability. Subsequently, Lemma D.2 gives sufficient conditions under which the percentile bootstrap gives asymptotically valid confidence intervals.

Lemma D.1.

Under Assumption 3, for any fixed , and , where denotes a sequence of random vectors indexed by that is bounded in probability for all larger than some .

Proof.

First we will show that if for is a sequence of random vectors such that such that for all , then . To see this, let for , where for all . Fix and note that since and since for all , by definition of bounded in probability, there exists , and such that for all . Letting and be such numbers and defining , and observe that for all ,

Above the 2nd step follows from monotonicity of probability measure and the third step follows from the union bound and the final step holds because for each . Since the above argument holds for all , we have found that . Hence we have shown that for any there exists an and such that , implying by definition that .

Now fix and let denote the th row of for . By Assumption 3(ii), for each , converges in distribution. Thus for each , so by the result of the previous paragraph, .

Fix , and using defined in the previous paragraph define and define . As argued in the previous paragraph . To show that fix . By Assumption 3(i),

Thus if we let be the event that

there exists an such that for all , . It is easy to check that under the event , for any ,

Since , there also exists an and such that for all , . Letting and be such numbers and observe that for all ,

Above the penultimate inequality holds because of the aforementioned upper bound on when the event occurs. Taking the supremum of the above inequality over all , . Thus we have shown that for any fixed , there exists numbers and such that , so by definition . Recalling our definition of it follows that for each , . Since each component of the sequence of vectors is , by the result of the first paragraph . ∎

In the following lemma, is a rescaling constant that depends on and satisfies as . In many applications of interest ; however, here we choose to state the lemma more generally.

Lemma D.2.

Suppose is a univariate pivot and that is the bootstrapped (or approximate bootstrapped) version of such that as ,

where has symmetric distribution with a continuous and strictly increasing CDF. Further suppose that and are an estimator and a bootstrap (or approximate bootstrap) draw of the estimator such that and . Then, letting be IID draws from the bootstrap (or approximate bootstrap) distribution , the empirical quantiles of this sequence provide asymptotically valid confidence intervals for in the sense that

Proof.

Let and and note that by assumption and . Also let and note that . Now define the following CDFs

where the first two CDFs are random CDFs that depend on the empirical data distribution . Letting denote the metric defined at (9), by assumption in the lemma statement . Also by assumption where has CDF and where, by assumption, has a continuous and strictly increasing CDF as well as a symmetric distribution. Letting be the CDF of , by Polya’s Theorem (Theorem 11.2.9 in Lehmann and Romano, (2005)) converges to uniformly in as and hence .

Now we will show for all . To do this fix and note

Above the last step holds because is continuous and and because as mentioned earlier . Thus we have shown that for all .

Now define for each . Since are IID draws from the bootstrap distribution , it is clear that are IID draws from the bootstrap distribution , which has CDF . Thus defining

it is clear that by the strong law of large numbers that as , for all . Letting denote a term that converges to zero almost surely as , combining this with the previous result we get that for all ,

Thus as for all . Since is continuous and strictly increasing, by Lemma 11.2.1 in Lehmann and Romano, (2005), as , for all .

To complete the proof, recall that , and . Thus if we let denote a terms that converge to in probability as ,

Above the third step follows from the previous result and the penultimate step follows from the assumption that is the CDF of a symmetric random variable. The final step above holds because by Slutsky’s lemma and since converges to a random variable whose CDF is as . A similar argument shows that . Combining this with the previous result

∎

D.3 Proofs of Theorems 3.1 and 3.2

D.3.1 Proof of Theorem 3.1