Private, Auditable, and Distributed Ledger for Financial Institutes

Abstract

Distributed ledger technology offers several advantages for banking and finance industry, including efficient transaction processing and cross-party transaction reconciliation. The key challenges for adoption of this technology in financial institutes are (a) the building of a privacy-preserving ledger, (b) supporting auditing and regulatory requirements, and (c) flexibility to adapt to complex use-cases with multiple digital assets and actors. This paper proposes a framework†††PADL-source-code . for a private, audit-able, and distributed ledger (PADL) that adapts easily to fundamental use-cases within financial institutes PADL employs widely-used cryptography schemes combined with zero-knowledge proofs to propose a transaction scheme for a ‘table’ like ledger. It enables fast confidential peer-to-peer multi-asset transactions, and transaction graph anonymity, in a no-trust setup, but with customized privacy. We prove that integrity and anonymity of PADL is secured against a strong threat model. Furthermore, we showcase three fundamental real-life use-cases, namely, an assets exchange ledger, a settlement ledger, and a bond market ledger. Based on these use-cases we show that PADL supports smooth-lined inter-assets auditing while preserving privacy of the participants. For example, we show how a bank can be audited for its liquidity or credit risk without violation of privacy of itself or any other party, or how can PADL ensures honest coupon rate payment in bond market without sharing investors values. Finally, our evaluation shows PADL’s advantage in performance against previous relevant schemes.

Keywords:

Distributed Ledger, Privacy, De-Fi, Zero-knowledge Proofs, Smart Contract, Blockchain, Multi-assets Ledger1 Introduction

Blockchain and distributed ledgers technology has opened-up a new form of financial interaction, to transact with no requirement of mediator bodies. The impact is clearly evident in the continuous growth of public blockchain domains such as Bitcoin [nakamoto2008], Ethereum [wood2014ethereum] and other ledgers based on smart contract platforms, notably HyperLedger [androulaki2018hyperledger]. For financial industry, which is originally centralized, adapting distributed ledger technology potentially offers several advantages, such as reducing efforts involved in settlement and post-trades processing, streamlining laborious auditing processes, shifting to cloud environments, and enabling nearly instant approval of transactions. However, the current public blockchain ecosystem does not necessarily match the needs of financial institutions that must comply with government regulations and laws. A specific example is that of privacy: public blockchains requires that all participants have access to the transaction for its validation. This is unacceptable (or even illegal) to majority of institutions that require their clients’ personal information or trading strategy be kept private and safe.

In recent years the focus on ‘private’ blockchains has increased to address concerns on privacy in public blockchain, which are considered only pseudo-anonymous. Privacy may be enhanced on blockchain by encrypting or anonymizing certain information, for example, the transaction’s values, participants addresses, type of assets, or transaction graph. Inevitably though, encryption of information adds to the complexity of transaction validation and auditing. While encryption may help with enabling private transaction, it makes it nearly impossible for financial institutions to meet trading requirements or answer auditor’s queries without revealing sensitive information.

Zero-knowledge proofs (ZKP) introduced as interactive [goldwasser2019knowledge] or non-interactive protocols (NIZK) [blum2019non] between a prover and verifier to convince the truth of a statement without revealing any further information. This technology can be used in private ledger to validate integrity of transactions and answer auditor queries without revealing sensitive information. ZKP systems have seen rapid advancements, particularly in terms of efficiency [groth2010short], succinctness, and general applicability. These developments build upon foundational frameworks such as zk-SNARKs [sasson2014zksnarks] and extend to transparent systems that do not require a trusted setup, such as zk-STARKs [sasson2018zkstarks], Ligero [bhadauria2020ligero++, ames2017ligero], and Bulletproofs [SP:BBBPWM18]. One of the primary advantages of modern proof systems is their ability to produce short proofs and facilitate the batching verification of range proofs, which demonstrate that a hidden value lies within a specified interval. Evidently, these frameworks can be combined with public blockchains to enhance the privacy of these blockchains with ZKP [sasson2014zerocash, sun2021survey]. However current efforts focused on public blockchains fail to address institutions or enterprise blockchain applications that have a different set of auditing and privacy requirements or constraints that are not the focus of public crypto-assets. In practice, it is also recognized that adapting to new cryptography tools may require far more time in a regulated environment where security vulnerability cannot be compromised. Finally, financial industry use-cases involve multiple actors and multiple assets or asset-type in the trade or transaction. Existing public blockchain hardly address the issue of maintaining or exchanging multiple assets, not to mention, inter-asset auditing or customizing privacy. Hence, a private distributed ledger for financial institutions must be considerate of the following requirements:

Auditing. Auditing inevitably requires disclosing information to assess and limit the financial and security risks institutes possess. Auditing in a private ledger can be divided into two types. First is privacy preserving auditing which does not require violating privacy of other participants (if they are not directly involved). In this optimal private auditing, a shares a ZKP to convince an auditor with the information encrypted to ensure; traceability, transaction integrity, or regulating trading requirements. This privacy preserving auditing would open-up in future the capability to audit financial institutes without laborious efforts or book disclosure, for example, maintaining level of capital at risk in a confidential multi-assets ledgers as we show here. Additionally, some regulations require opening all values. Hence ‘full’ auditing in essence, letting only a specified party, the capability to open an encrypted value. The requirement here is that this type of auditing should be limited to the specified party. We later discuss the case of a ‘settlement bank’, where tracing values can be done by a settlement bank for ‘full’ auditing.

Private Multi-Asset Ledger. Public blockchain ledgers, in their original implementation use anonymous accounts, but values, transactions graphs, balances, and assets are public. By private ledger, we consider this information fully or partially to be hidden with the combination of encryption and zero-knowledge proofs to create private blockchains. Note, that anonymity includes also the hiding of the transaction graph and their assets. Transaction graph can be an extremely resourceful information [alarab2020competence, zhi2022ledgit]. From trading perspective, even a small history of transaction can be sufficient to reveal its strategy or position, however, from auditing perspective, it is still required to maintain traceability, either in privacy preserving manner, with using ZKP, or with decryption of information by an auditor. Furthermore, majority of existing financial use-cases involve multiple assets and multiple actors. For example, existing trading applications support multiple equities, exchanges, loans or other complex financial instruments. Hence, confidential multi-asset and audit-able privacy between assets is a necessity in order to handle practical use-cases within financial institutions.

No-trust Setup. No trusted setup is highly desired in the context of external auditing using ZKP. Some distributed ledgers may offer auditing capabilities with the help of a trusted entity such as third-party auditors. This indeed does not provide data protection. Moreover, trusted setup or shared setup, using original zk-SNARK systems for example, would require the auditor to trust the setup. Hence, regulatory auditing would require transparent proofs, i.e. without verification or proving keys. Even if the auditor holds or trusts the holders of the keys, it makes auditing an issue when inter-banking applications may have several and different auditing bodies, where sharing the keys with the bodies, compromises the privacy of the data. The trusted setup, in the auditing context, is hence highly undesirable to most financial institutions as a pre-requirement.

In this paper, we propose PADL which follows a ‘table’ ledger scheme and combines encrypted commitments with audit-tokens and NIZK to support private peer-to-peer multi-asset transaction. It supports privacy preserving auditing of inter-asset balances to prove rates and liquidity risks of financial institutions with no trusted setup, and supports full auditing for provable traceability of transactions. We show that with PADL framework, it is straight-forward to build financial market ledger such as bond markets, confidential asset swap, settlement bank with customized privacy. The transaction scheme enables asynchronous proof generations amongst the participants, and provides a general transaction porpuse for various types of multi-asset transactions. Furthermore, PADL is an open-source package, compatible with smart-contract to showcase its integration to various blockchain integration. Finally, our performance evaluation shows that PADL, is not only more flexible, but outperforms other private ‘table’ ledgers without sacrificing privacy or auditing capabilities in any form. To summarize, our contributions are as follows:

-

•

PADL framework. We propose a complete and industry-ready distributed ledger for private and anonymous multi-asset transactions while supporting privacy-preserving and full auditing.

-

•

New privacy-preserving audits notions. We identified several core privacy preserving auditing proofs that enables operational risk control and are crucial for financial institution operations.

-

•

Evaluations. We provide a comprehensive theoretical and empirical evaluation of PADL. We evaluate the security and privacy properties, and show its practicality via performance evaluation.

-

•

Usecase Showcase. We showcase practical use-cases for financial institution ledgers that are enabled with PADL, thereby demonstrating the capability of PADL in constructing complex transaction scheme for financial applications.

2 Related Work

Our work is closest to zkLedger, that is also a table based private distributed ledger that combines NIZK based on -protocols [cramer1996modular] with Pedersen commitment to propose a private and audit-able transaction scheme. However, zkLedger is limited to single non-private asset and thus it cannot support complex multi-asset applications that are common within finance industry. PADL’s flexible transaction scheme supports confidential multi-asset transactions with inter-asset auditing, making it possible to use for different use-cases such as asset exchange, trading loan ledger, settlement ledger, bond market, or secondary markets. Not only this, as shown in our evaluation, PADL transaction scheme scales better with number of assets and participants compared to zkLedger’s transaction scheme.

Other private ledgers that offer privacy and auditing include Solidus [cecchetti2017solidus], PEReDi [aggelos2022peredi] Miniledger [chatzigiannis2021miniledger], Fabzk [kang2019fabzk], Azeroth [jeong2023azeroth], etc. Some of these ledger do not necessarily permit auditing while maintaining privacy [gao2019private], or that their auditing is possible only if the ledger is open to public or to a trusted third party, or a fixed auditor [Androulaki2019]. Furthermore, these ledgers are focussed and restricted to single asset transactions and auditing. Similarly, Platypus shows an ‘e-cash’ scheme for meeting regulations under privacy [Wust2021], but with the trust of a central bank. This can be a significant limitation of privacy, since auditor in such cases might be able to access private information related to banks and entities that are not the target of the audit or have different regulatory requirements. Miniledger [chatzigiannis2021miniledger], simply presents a different implementation of the zkLedger whilst losing some capabilities in order to simplify it, but does not offer additional privacy value. PEReDi [aggelos2022peredi] does not support multi-asset swaps and/or offline transactions. Many privacy preserving protocols based on membership proof, such as on Monero [noether2016ring] and ZCash [sasson2014zerocash] are intended for efficiency in much larger number of participants than in the case of enterprise blockchain. Therefore, they are concerned mostly with single asset/currency and (pseudo) anonymity without auditing or without multi-assets capability. However recent works investigate and offer Monero protocols with tractability [li2019traceable]. Here, we show that in a ‘table’ data structure, it is straight-forward to deal with privacy preserving or full auditing, and to introduce auditing between confidential assets. Similarly, ZCash which is based on succinct schemes, is also being studied for the propose of regulation enforcement protocols [xu2023regulation, li2019toward, xu2023regulation], or for the ability to introduce multi-assets for ZCash [Ding2020a, Xu2020]. These ledgers and others based on zk-SNARK [Ding2020a, Jia2024, Xu2020, Garman2016, Wust2021], however do not focus on enterprise blockchains use-cases where trust setup as with original zk-SNARK implementations is not practical for auditing context. Finally, there are also applications of privacy preserving ledgers that are in this work context, for example, [khattak2020dynamic, meralli2020] for dynamic pricing and securities market, respectively. We extend auditing capabilities, and add to these set of applications by applying PADL to private atomic swap exchanges and bond markets in a single framework and general transaction scheme.

The rest of the paper is structured as follows. Sec. 3 describes the PADL design and the transaction scheme informally. This is immediately followed by the application use-cases in Sec. 4. Sec. 5 describes formal treatment of our PADL followed by its security and performance analysis in Sec. LABEL:sec:eval. For supplementary, we add appendix providing detailed examples of transactions (LABEL:appendix:usecases), and further security analysis with complementary proofs (LABEL:appendix:security,D).

3 PADL - Ledger Design

This section describes PADL design and the proposed private transaction scheme informally. We postpone the formal definition of PADL transaction scheme to Sec. 5 but for clarity of this section, introduce essential components; Let be a cyclic group and let be two random generators of . Then in the setup of a ledger, each participant generates its public key, which is related to its secret key via the following relation: .

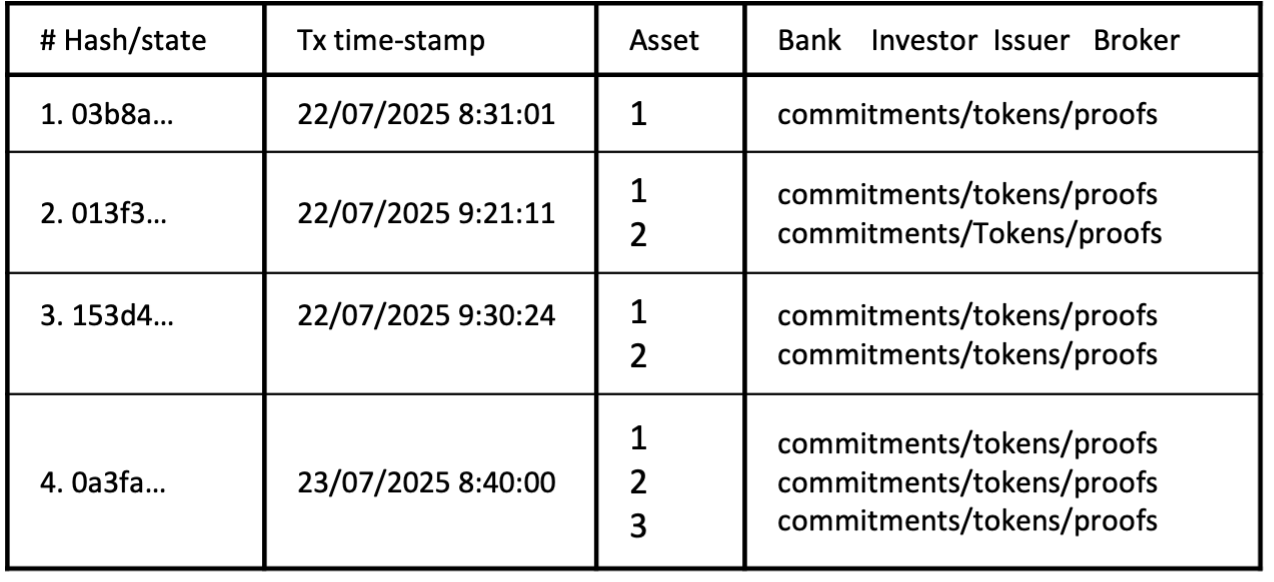

The PADL structure is an ‘append-only’ transaction ledger, where each transaction is added to a table in a synchronized manner. Figure 1 illustrates the different actors that can interact with the distributed ledger (a), the information stored in the encrypted ledger table (b) and high-level description of the transaction scheme (c). Asynchronous transactions is also possible in various ways, but out of scope at this stage. A transaction is sent to the host of the ledger by the ‘sender’. The sender knows and hides all participants’ values for a specific transaction. A multi-asset transaction, consisting of one or more assets, represents one row that may have several sub-rows depending on the number of assets in the transaction. Each transaction can possess multiple confidential assets, so the assets and their amounts in the transactions are encrypted using Pedersen commitment for each participant to hide their values. The commitments are accompanied with tokens and the proofs required to validate the integrity of the transaction scheme. Thus, for each transaction , each participant , and each asset , we associate a cell of a 3-dimensional and dynamical array, , where are the indices of the transaction, participant, and asset, respectively:

In the above , is Pedersen commitment, defined by . Here is the value participant wishes to hide and is a random blinding factor. The commitment is associated with a blinding factor as a token, . In order to prove the binding of the blinding factor in the token to the commitment, a proof of ‘consistency’ is always accompanied here (). To make sure that no asset is created or destroyed in a transaction, it is required that the product of commitments across participants for each asset is equal to 1, where . This ensures that the sum of blinding factors and the sum of values are equal to zero, and . Table LABEL:table:padl_algo provides the algorithms for PADL construction, and the generation of commits and blinding factors is detailed in the algorithm .

Additionally, a proof of asset is required to validate that no participant overspends, . In order for each participant to provide a proof of asset, we introduce a complementary commit , a complementary token , and proofs. The complimentary commit is a commitment to the same value but with a different blinding factor and the token is the public key raised to . The complimentary commits are required since the participants do not know the blinding factor in the original commitment, hence they re-commit their values. Finally, each participant starts with an initial cell for each asset that can be minted by the participants themselves and/or verified by other parties (Def. 3).

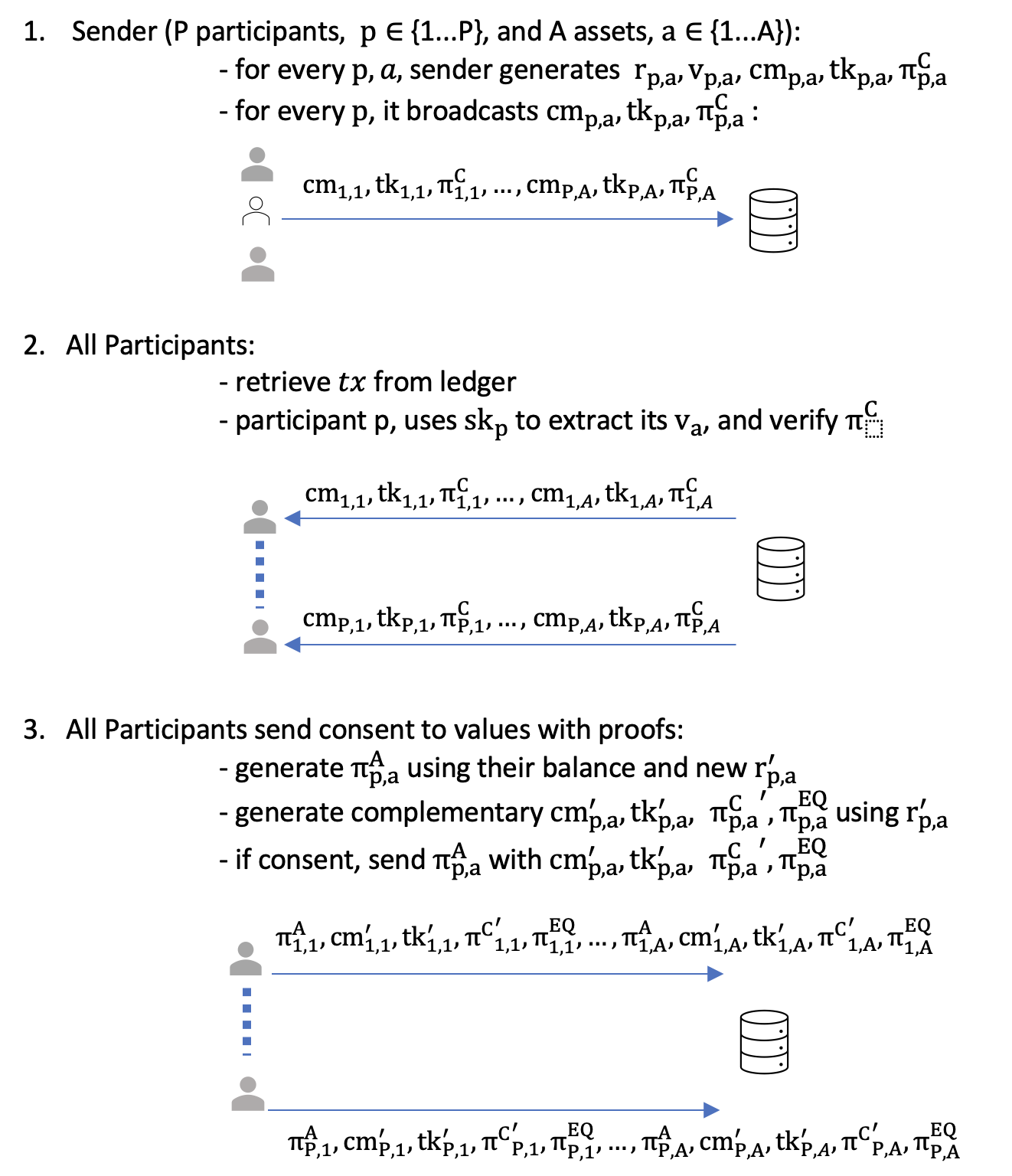

3.0.1 PADL Transaction.

The transaction scheme is designed for general purpose, confidential multi-assets transactions (Fig. 1c). A formal definition of the transaction scheme (Def. 3) is provided later at Sec. 5. Before the broadcasting step, a sender generates commitment-token pairs and proofs of consistency, for every asset and participant. It also hashes the commitment-token pairs to provide a unique identification of the transaction information. The transaction is then broadcast, without the proof of assets, allowing negative values for other participants, e.g. a broker, or in ‘atomic’ asset exchange. Subsequently, it also does not reveal who is the sender (traditionally known as spender), i.e. the sender is not the only participant who can commit to negative value (sends asset). After broadcasting the transaction, each participant, can extract the values committed, using their secret keys by calculating and use brute-force to solve the . Only the holder of the secret key can extract and be convinced with its value. This extraction is possible in practical cases where value belongs to a finite small set, and within a maximum range.

Next, the participants fill their proof of assets. Since is not known for the participant, participants provide also a complementary commit(), complementary token () and complementary consistency proof () for a new private . In order to verify that the same is used, the participant also generates an equivalence proof (). This proof is also sufficient to verify the identity, as it requires knowledge of its secret key, this proof is detailed in Sec. 5. The participant then adds a proof of asset for proving the sufficient balance in asset with the product of previous commits, .

This scheme has several advantages. First, the proving system is simpler than previously suggested [narula2018zkLedger, chatzigiannis2021miniledger], since it does not require generating the conditions of using a disjunctive proof.

Second and more importantly, it enables a single exchange with multi-assets, by committing minus values for other participants in a transaction. This offers practical flexibility when applying PADL to different use-cases where a trade-off between privacy, performance and future commitments/contracts is needed. Third, it hides the sender from the broadcaster or from the ledger. Fourth, generating the proof of asset is computationally expensive and likely the limiting step, and in this scheme, the participants generate the proof for themselves, asynchronously.

3.0.2 Extension to ‘injective tx’.

PADL transaction scheme requires other participants besides the sender to interact with the ledger to fill up the proof of assets. However, this is not necessarily a bottleneck since on any encrypted ledger, participants would need to consent to an encrypted value, even if it is a positive value, e.g. in loan assets, or where assets accrued interest. With that, our scheme can be easily changed to the simple case of an ‘injective’ transaction where consent is not required. In such case, the sender would provide range proofs to all transaction values to be positive, and proof of asset for itself. Along with another disjunctive proofs for everyone to conceal the sender [narula2018zkLedger]. Note that in any case the validation of proofs is required.

3.0.3 Validation and extension to dropping parties.

In order to validate transactions, each participant can verify the ZKP proofs at its own local node or machine, and also validate the hash declared in the transaction to ensure the commits and tokens corresponds to the number of participants and assets cells seen. An API can approve or reject the transaction. Alternatively, verification of the proofs for all broadcast cells can be obtained by a centralized service or with smart contract (which is also implemented in the PADL code). In case that some proof of assets are not valid, or not filled due to dropping parties, the sender can exclude these participants () and the transaction can be still validated. The exclusion is simply done by an extra step. The sender(), regenerates its own cell with a modified blinding factor, , that is the sum of the excluded participants and itself, . That makes the proof of balance valid again. In fact, the sender is able to remove any participant as long as the commit value is 0. Otherwise, the proof of balance would fail. The trade-off here, is anonymity of the transaction graph. The less participants involved in the transaction, the more information on the transaction graph can be extracted. The security of anonymity and integrity of the transaction scheme is defined in Sec. LABEL:sec:eval and formally analyzed in Appendix LABEL:appendix:security.

4 Use-Cases

We discuss several fundamental use cases for transactions and trading applications where PADL can provide privacy with audit-ability. Other uses cases can be built on top of the ledger components here. Concrete examples of transaction generation are also shown in Appendix LABEL:appendix:usecases.

4.1 Simple exchange ledger

We describe how PADL can be seamlessly used for exchange of confidential assets atomically. Assuming that two participants would like to exchange assets, with PADL it can be done in a single transaction. To do so, participant A creates a transaction consisting of commitments and tokens committing to transferring amount of asset to participant B. In the same transaction, participant A also writes a commitment on behalf of participant B, committing participant B to amount of . Then, participant A can broadcast this transaction, participant B can decide to either accept or reject this transaction. To accept the transaction, participant B simply writes its Cell’s proofs, which is then finalized and verified by participant A and the transaction is appended to the ledger. Note that by adding their proof of assets, they consent to the exchange. Next, the transaction is appended if validation passes. In the validation, the ZKPs are verified and the immutability of original broadcast transaction is checked by checking the hash of the final transaction. Finally, if a participants provides a ‘wrong’ or ‘bad’ cell in the transaction, it simply results in rejection of the transaction.

4.2 Settlement Trusted Bank ledger

Currently, bank payment systems are required a trusted party in order to be audit-able and follows ‘Know-Your-Costumer’, Anti-Money Laundering, specific rules, or keys recovery criteria. In such cases, the ledger contains a party that acts as a settlement bank, and would have access to the balance of some participants (’full’ auditing). In a distributed solution, we wish to avoid key management by the trusted parties, meaning parties would not share their private keys with any party. This scenario can be treated in PADL, by an additional token, ; signing by the public key of the trusted party. For many cases, the issuer can be defined as the ‘auditor’ or ‘trusted’ party, where its participant index is . The transaction cell structure is altered to facilitate this requirement:

Note that we also need to add consistency proof for the new added token. However, if in the committee consensus, the issuer is also designated as the approving entity (no need for consensus), the Cell structure can be reduced to:

The issuer can also check for any asset balance, by extracting the balance for each asset itself, and proof of asset can be avoided. This accelerates largely the ZKP system for a very typical and realistic use-case. In addition since, the token is designated to a single cell, it is flexible to define many audit tokens for a list of parties (s) and for any cell in a transaction.

4.3 Bond Market ledger

In this subsection we describe the application of PADL to a third and a more complex use case of trading bonds. The application of blockchain in the debt capital markets with arrival of ‘smart bonds’ is highly anticipated. However, in many cases, the bond issuers or investors might be reluctant to disclose their positions. We show how PADL is applied to make private transaction in the bond markets. For this case, we are mainly interested in exchange of two types of assets, bonds and a USD-backed digital token. The bond issuer would like to issue bonds and borrow USD-coin in return. The investors wish to lend USD-coin to buy bonds, however, the USD-coin for the investors are handled by another party, i.e. custodians. Also, the bonds are handled by brokers with fees, thereby interacting with the bond issuer and the investors. The privacy requirements in this scenario are as follows:

-

•

Only the broker knows the details of bond deals.

-

•

Custodian knows only the amount of money released to an investor.

-

•

The bond issuer does not need to know the individual investors’ contribution.

-

•

The investors does not know about other investors.

-

•

Coupon (or interest rate) payment by the issuer can be issued without the issuer learning about the distribution of the payment amongst the investors.

PADL allows the investors and bond issuer to make these transaction while maintaining privacy as described below (in brief). The entire transaction flow is described in Appendix.

We start by assuming all the participants: issuers, custodians, broker and the bond issuer are on PADL, and a ledger consists of two assets, a bond and a USD tokens. The ledger is initialized such that bonds are minted by the bond issuer and the USD coin asset by the custodians. The custodian can then issue USD token to the investors as requested by the investors, by creating a transaction on PADL. In order to exchange assets (buy bond for USD coin), the broker creates a transaction on behalf of both the investor and bond issuer. This transaction consists of commitments that are written in every participant’s columns. The bond issuer can open the commitments in its column to verify that it is committing to number of bonds in exchange for number of USD coins. Similarly, the investor can verify that it is committing to USD token in exchange for receiving bonds. Furthermore, the broker creates transactions for the bond issuer to pay the coupons to the investors. Again, the only value the bond issuer can verify is that it pays the correct coupon rate for the money it received for the bonds, however, it cannot decrypt the payments that each of the participants on PADL receive. Each investor however can verify that it receives the right amount of coupon payment as promised. Finally once the bond matures, the broker in a single transaction (see example in Appendix LABEL:appendix:usecases), can return the USD coins to the investors while taking its commission away from all participants, and the bond issuer can destroy the bond asset.

The use-cases above shows the applicability of PADL to develop various private and audit-able markets. We next discuss the cryptography and methods which define the transaction scheme, auditing, and ledger construction followed by security analysis.

5 Methods

5.1 Notations and Background

We denote by the execution of algorithm on input and produces . By , we denote an algorithm that has access to oracle . We use to denote that r is sampled uniformly at random from a set S.

Let be prime-ordered additive subgroup of the elliptic curve generated by some generator and some prime . For simplicity, we use multiplicative notation for group throughout the paper.

By , we denote the participant (with public key ) account’s commitment coin in the -th transaction row for a specific asset . Similarly, by , we denote the corresponding commitment coin value. We exploit the notation for

to mean the same for a specific transaction . We often omit if the context is clear.

Discrete Log (DLOG) Assumption: Given where and , no PPT adversary can output with non-negligible probability. This paper relies on the intractability of solving the discrete logarithm problem.

5.1.1 Commitment Scheme.

A commitment scheme consists of two steps: first the sender commits to a value as a commitment; later the sender may choose to reveal the committed value. A commitment scheme should satisfy the hiding and binding properties. Additionally, a commitment scheme has additive homomorphic property, if given two commitments, we have . We briefly recall notions for the Pedersen commitment scheme [C:Pedersen91] while hiding and binding definitions [EC:GroKoh15] are recalled in the Appendix. is omitted for the rest of the paper since it is clear from the context.

Definition 1 (Pedersen Commitment)

Pedersen (homomorphic) commitment scheme consists of the following set of algorithms:

-

•

: on input a security parameter , this algorithm computes where are generators and outputs .

-

•

: on input a commitment key , a message and a randomness , this algorithm parses , and outputs as the commitment .

5.1.2 Zero-Knowledge Proof.

A non-interactive zero-knowledge proof (NIZK) [EC:GroOstSah06] allows a prover to prove to a verifier of some statement in zero-knowledge. NIZK is defined as follows:

Definition 2 (Non-interactive Zero-Knowledge Argument System)

Let be an NP-relation and be the language defined by . A non-interactive zero-knowledge argument system for consists of the following algorithms:

- :

-

Takes as input a security parameter , and outputs a common reference string .

- :

-

Takes as input a common reference string , a statement and a witness , and outputs either a proof or .

- :

-

Takes as input a common reference string , a statement , and a proof , and outputs either a or .

5.2 Privacy Preserving Multi-Asset Transaction with Audit

In this section, we formally introduce the notion of a confidential transaction with privacy-preserving audit scheme () which is later used to show PADL construction. is based on the syntax from (ring) confidential transaction (Ring-CT) [ESORICS:SALY17, FC:YSLAEZG20] but additionally introduces notions that capture the requirements for a variety of privacy-preserving audits. Modifications are also made to the syntax of confidential transaction scheme, allowing the scheme to better capture the functionality of table-based multi-asset transaction rather than graph-based mono-asset transaction. The security and privacy of the transaction scheme are detailed in Appendix LABEL:appendix:security.

5.2.1 scheme.

In general, a scheme consists of algorithms that are used to make confidential transactions. It is assumed that the distributed ledger is properly maintained and updated at all time***A consensus protocol is used to manage the state of the distributed ledger. However, the exact details are considered outside the scope of this work.. Recipient accounts (accounts where the commitment coin is positive) and spending accounts (accounts where the commitment coin is negative) are implicitly captured by the transaction amount list . Note that the transaction considered here is a multi-asset transaction. We additionally introduce to capture the transaction flexibility of the proposed PADL scheme, which permits policy-based spending. Policy enforcement is flexible and can include rules such as always accepting positive deposits, only accepting negative amounts if the transaction is initiated by the account owner, only accepting negative amounts if it is an authorized scheduled direct debit, and other possible variations. In practice, the default policy, is configured to accept positive amounts and only accept negative amounts if the transaction is initiated by the same account.

Definition 3 ()

A privacy preserving-enabled confidential transaction

scheme is a tuple of algorithms,

:

-

•

: on input a security parameter , this algorithm outputs a public parameter . All algorithms defined will implicitly receive as part of their inputs.

-

•

: on input a security parameter , this algorithm outputs an account secret key and an account public key .

-

•

: on input a transaction amount , this algorithm outputs a commitment and a commitment blinding factor .

-

•

: on input a transaction amount , a transaction policy , an account secret key , and an auxiliary information , this algorithm outputs an endorsement data .

-

•

: on input a transaction amount list , a history transactions list , and a master account public key list , this algorithm outputs a new transaction , and a validity proof .

-

•

: on input a new transaction , a validity proof , a history transactions list , and an account public key list , this algorithm outputs a verification bit .

In the context of auditing distributed ledgers, it is often required that the auditor can open the transactions and trace their graph to make conclusions about the financial health of the organization. In Provisions [CCS:DBBCB15], more privacy-preserving auditing is considered whereby solvency is proved without revealing the entire transactions history. However, existing works do not consider a couple of fundamental audit information that is used in financial auditing landscape. We identified the following sets of privacy-preserving auditing concepts that would be of interest to the financial auditing of participants in the distributed ledger. should support the following set of privacy-preserving audit capabilities:

-

1.

Basic Asset Balance. Without revealing the transaction history, the verifier should be convinced of the asset balance of the ledger participant.

-

2.

Liquidity. Without revealing the transaction history and an asset balance, the verifier should be convinced of the liquidity or credit of the asset.

-

3.

Inter-transactions Rate. Without revealing the transaction history, the verifier should be convinced of the inter-transaction rate between two subset of transactions.

5.3 Final PADL construction

In this section, we lay out the cryptography setup and elements involved in the transaction scheme. As discussed in the preceding sections, is executed to obtain which are assumed to be public in the ledger. Each participant will generate their keypair using where will now be the participant’s identity and unique account address. Transactions with proofs are generated using while the transaction value list used could be prepared by any party. During the generation of a transaction, the sender contacts the broadcaster using (in PADL, broadcast is a functionality provided by the ledger) to obtains endorsements from all parties. Meanwhile, the transaction amount is committed using . Lastly, is used to verify the transaction with proofs generated by with respect to the latest ledger transaction state and participant list. Each participant maintains its internal state which records . The construction is summarised in Table LABEL:table:padl_algo and all the elements of PADL’s are listed as follows (indices , and are omitted whenever appropriate for fluency).

Commitment commits to the value in a transaction as defined in Def. 1: .

Token hides the blinding factor, with a public-key, . The token has two distinctive roles: to facilitate verification of proof and to enable extractability of the committed value without knowledge of , as long as the value belongs to a small set. For example, participant, , can take a commitment and token , and use its secret key to compute to obtain . The extractability is also used in assigning an auditor or a trusted party, as described in the settlement bank use-case. Note that the combined system (, ) makes the scheme computationally hiding because adversary could solve the Discrete Log Problem for to obtain and be able to open the and proof of consistency ensured that the correct is used to construct the token.

Proof of balancemaintains the conservation of all assets in a transaction , ensuring that the sum of each asset value in the transaction equals zero. Proof of balance is a proof for the language . In PADL, proof of balance is checked by multiplying the commitments together and checked for equality with . By the homomorphic property of Pedersen commitment and assuming is the additive sharing of zero, we have . The proof of balance is unforgeable due to the hardness of discrete log.

Proof of consistency () ensures that the randomness used in the commitment and token are consistent. The proof of consistency is a proof for the language .

The proof of consistency is a ZK--protocol where the prover chooses random , and sets , and generates a challenge with a hash function . The prover calculates .

It then outputs the transcript .

The verifier verifies: .

Proof of equivalence () is used to show that two commitments have the same commitment value. The proof of equivalence is a proof for the language .

Given a commitment-token pair () and their consistency-verified complementary counterpart (), we can compute and . If , the prover would need to compute discrete log where as the discrete log between and is not known.

Therefore, it is sufficient to check for the knowledge of secret key between the base and group element to check for the commitment coin value equivalency. In PADL, Schnorr protocol [C:Schnorr89] for knowledge of discrete log is used.

Let and .

The prover chooses random , sets , and generates a challenge with a hash function . The prover calculates .

It then outputs the transcript .

The verifier verifies: .

Proof of asset () asserts that after summing the commitment coin values of an asset for a particular account p, it holds that the balance of the account is positive. Positive for PADL is defined to be within some range .

Proof of asset is a proof for the language .

Proof of asset for some participant p is instantiated by first asserting that a complementary commitment has the same coin value as the aggregated commitment coin via proof of equivalence whereby the aggregated commitment coin is obtained by multiplying all the commitment coins ***Alternatively, by multiplying all the individual complementary commitment coins which is a re-committed commitment coin.. Then, a NIZK range proof for Pedersen commitment such as Bulletproofs [SP:BBBPWM18] is used to assert that the asset balance contained in the complementary commitment is positive.

Note that is instantiated directly from the generalized special honest-verifier proof of knowledge () -protocol for the preimage of a group homomorphism by Maurer [AFRICACRYPT:Maurer09]. The aforementioned theorem and the instantiation are shown in the Appendix LABEL:appendix:security. Additionally, interactive proofs are transformed into non-interactive zero-knowledge proofs (NIZK) using the Fiat-Shamir transform [C:FiaSha86] in the random oracle model and the transaction identifier is a part of the statement for all proofs.

In the algorithm, the challenger replaces all transaction amount values in (except values belonging to accounts in corrupted list ) with a random value while making sure entries in the modified transaction summed to zero and it does not spend over the account balance limit. Note that transaction values for adversary corrupted accounts in both and is the same to prevent trivial cases of distinguishing. Let be the sublist containing only the modified values and let be the set of assets in the transaction. The distribution of the resulting commitments is the same from ’s point of view. The game is indistinguishable from by the commitment hiding property, it follows that |Pr[_1()=1] - Pr[_0()=1]|≤(∑_a=1^|