Discrete approximation of risk-based prices under volatility uncertainty

Abstract.

We discuss the asymptotic behaviour of risk-based indifference prices of European contingent claims in discrete-time financial markets under volatility uncertainty as the number of intermediate trading periods tends to infinity. The asymptotic risk-based prices form a strongly continuous convex monotone semigroup which is uniquely determined by its infinitesimal generator and therefore only depends on the covariance of the random factors but not on the particular choice of the model. We further compare the risk-based prices with the worst-case prices given by the -expectation and investigate their asymptotic behaviour as the risk aversion of the agent tends to infinity. The theoretical results are illustrated with several examples and numerical simulations showing, in particular, that the risk-based prices lead to a significant reduction of the bid-ask spread compared to the worst-case prices.

Key words: risk-based pricing, indifference pricing, volatility uncertainty, nonlinear semigroup, Chernoff approximation.

MSC 2020 Classification: Primary 91G20, 47H20; Secondary 91G70, 91G60, 47J25.

1. Introduction

Computing the prices of financial derivatives strongly depends on the choice of the underlying model and the associated probability distributions. Since these distributions are, in general, not precisely known, robust finance takes into account model uncertainty by considering sets of possible transition probabilities. In this article, we start with a simple asset model in discrete time for which derivative prices can easily be computed by backward recursion and analyze the asymptotic behaviour of derivative prices as the number of intermediate trading periods tends to infinity. A classical example of this is the convergence of derivative prices in the binomial model to the Bachelier or Black–Scholes prices, see e.g. [43, Section 5.7]. Discrete financial models are generally straightforward from a modeling perspective and arise naturally since trading typically occurs at discrete time points. Nonetheless, continuous-time models are very popular since they allow for the use of stochastic calculus and PDE methods. Furthermore, it has recently been shown in [32] that superhedging prices of discrete-time models with uncertain Markovian transition kernels converge to superhedging prices of continuous-time models with drift and volatility uncertainty. Superhedging prices correspond to intervals of plausible prices which do not generate arbitrage opportunities, see for example [34]. Although such intervals can naturally be associated with an arbitrage-free bid-ask spread, these bounds are, in general, too wide to be informative about the prices of a contingent claim in incomplete markets. In fact, each agent operating in the market assigns a different subjective value to the same contingent claim which can violate the bounds prescribed by the superhedging or subhedging prices.

A classical approach to reduce the bid-ask spread observable in incomplete markets consists of taking the preferences of an agent into account by associating a utility function or a risk measure to the agent. A strand of literature has developed in this direction introducing so-called good deals bounds. Good deals bounds aim to reduce the no-arbitrage bounds by ruling out prices that can be hedged by strategies leading to a high expected utility, i.e., prices that represent a deal which is too good. Good deals have been measured by means of Sharpe ratios [31], gain-loss ratios [12] or utility functions [27, 15, 28]. Moreover, the setting in [42] allows for imperfect hedges as long as their level of risk is acceptable. Closely related to good deal prices are indifference prices which make the agent indifferent regarding her utility or risk between selling or keeping the derivative, see [82, 76, 55, 13, 14]. A connection between the two concepts was first established in [54], where it is shown that indifference prices based on coherent risk measures are equivalent to the good deal prices in [28]. Furthermore, every convex risk measure representing good deal prices is given by an indifference price, see [2]. An extensive collection of the literature on good deal and indifference prices can be found in [26]. So far, explicit solutions have only been given in dominated settings, where the asset process is given with respect to a physical measure and the absence of good deals translates into restrictions on the set of equivalent local martingale measures . However, since incompleteness in a market is naturally connected with model uncertainty and the inability to precisely estimate the distribution of the assets, a more general framework taking model uncertainty into account seems to be necessary. In addition, as pointed out in [79], classical indifference pricing often has the flavour of a one-period model.

In this article, we work in a non-dominated setting, where the uncertain distribution of the increments of the asset process is determined by a sublinear expectation . Moreover, we consider an agent who measures the risk associated to a random loss by means of a robust entropic risk measure

where is a risk aversion parameter. Since the entropic risk measure is the certainty equivalent of the exponential utility, our agent can also be seen as a robust exponential utility maximizer whose preferences belong to the class of multiple priors preferences which have been introduced and characterized in [46]. The term robust refers to the consideration of several plausible models which can be derived from the dual representation

of the sublinear expectation. For a brief introduction to sublinear expectations, we refer to Subsection 2.1 and the references therein. Following the previously mentioned work [46] and its extension [59], the problem of robust pricing has gained a great deal of attention. In particular, we refer to [10, 38, 23, 1, 11, 24] for arbitrage theory and superhedging dualities under model uncertainty and to [39, 30, 40] for similar results in the presence of transaction costs and trading constraints. The multiple priors problem has also been tackled in the context of utility maximization in dominated settings, see [73, 48, 67, 5] and in non-dominated settings, see [36, 66, 64, 65]. In the specific context of exponential utility, the authors of [44, 33] prove duality in a continuous-time non-robust setting. Furthermore, in [75, 51] the value function of the utility maximization problem is characterized via a quadratic BSDE and several properties of the pricing functional such as monotonicity and the asymptotic behaviour w.r.t. the risk aversion parameter are derived. These results have been extended in [60] and, for a non-dominated setting, in [61]. For unbounded claims, duality and the existence of maximizers have been established in [6] and, under the presence of transaction costs, in [35].

Starting from a -dimensional discrete-time market, we assume that the asset process has independent increments which are determined by the equation

where is a fixed step-size, is a deterministic drift and is a -dimensional random vector with mean zero. Given a claim with payoff function and maturity , the indifference ask price is uniquely determined by the relation

where the random variables take values in a set of available strategies such that is -measurable for all and

Under suitable conditions, one can show that , where consists of all bounded continuous functions . Hence, if we require the indifference ask prices to be time consistent, they are completely determined by the one-step pricing operator and the equation

| (1.1) |

Dynamic consistency has previously been imposed in [31] to solve the multi-period pricing problem by iterating the solution of the one-period model. Furthermore, in a continuous-time setting, the authors of [56] show that local conditions on the pricing kernels guarantee nice global properties of the pricing operator, included time-consistency. In Subsection 2.3, dynamically consistent pricing operators are discussed in more detail. We are now interested in the limit behaviour of the multi-step prices as the number of intermediate trading periods tends to infinity. For that purpose, let be a maturity and be a sequence of decreasing step-sizes. Then, if the limit

| (1.2) |

of the multi-step indifference prices exists, it defines the asymptotic risk-based price of a claim with payoff function and maturity . In order to prove that the previous limit exists and to uniquely characterize the global dynamics of the asymptotic risk-based prices by means of their infinitesimal bevahiour, we reformulate equation (1.2) as an approximation result of a nonlinear semigroup. This view point is motivated by the fact that the time consistency of the multi-period prices transfers to the limit, i.e.,

| (1.3) |

Equation (1.1) guarantees that the right-hand side of equation (1.2) is given by

where denotes the pricing operator for one period with step size . Furthermore, these operators have desirable properties such as convexity and monotonicity. The question whether a sequence of iterated operators on converges to a limit operator such that is a strongly continuous convex monotone semigroup has systematically been addressed in a series of recent articles, see [18, 21, 20, 22]. Applying these results to the present setting shows that the limit

exists for all and . Moreover, the family is a strongly continuous convex monotone semigroup which is uniquely determined by its infinitesimal generator

The asymptotic risk-based prices are then defined by

Note that, by equation (1.2) and (1.3), these prices are time consistent and given as the limit of multi-period prices in a discrete model. In addition, the prices have desirable properties such as convexity and monotonicity w.r.t. the payoff function. So far, we did not address the question whether the asymptotic risk-based prices depend on the particular choice of the discrete model. In case of the previously mentioned approximation of the Bachelier prices, the central limit theorem guarantees that the Bachelier prices only depend on the covariance of the discrete model but not on the particular choice of its distribution. This observation is a particular case of the more general statement that strongly continuous semigroups are uniquely determined by their generators. For linear semigroups the uniqueness is classical result and for convex monotone semigroups it has been proven in [18, 20]. In the present article, the generator can explicitly be computed as

for sufficiently smooth functions , where is a set of available trading strategies and the function

describes the covariance of the random factors. In particular, the asymptotic risk-based prices only depend on the covariance of the discrete model but not on the particular choice of its distribution. In Subsection 2.2, we explain the semigroup approach in more detail and fix the precise terminology used throughout the rest of this article. Furthermore, at the beginning of Section 5, we recall the precise statements from [18] on which the proofs of the main results in this article are based.

In the following, the main results of this article are described in more detail. In order to guarantee the well-posedness of the one-step pricing operators and to exlcude doubling strategies as the number of intermediate trading periods tends to infinity, we first impose a volume constraint on the set of available trading strategies, see Theorem 3.2. Since the asymptotic risk-based prices are uniquely determined by the covariance of the random factors, a non-degeneracy condition guarantees that the volume constraint can be arbitrarily large, see Theorem 3.3. This way, we can define asymptotic risk-based prices involving unbounded sets of trading strategies as limits of volume constrained prices. Modeling the set allows to impose constraints on the available trading strategies such as volume or short-selling constraints, non-tradable assets, etc. However, in the absence of trading constraints, the generator does not depended on the gradient and is given by

In particular, the risk-based prices taking into account the attitude of the agent towards risk are always dominated by the worst-case prices associated to the -expectation, see Corollary 3.4. So far, in the absence of trading constraints, we did not define the asymptotic risk-based prices as the limit of multi-step prices, but as the limit of volume constrained asymptotic prices. However, under additional conditions on the distribution, the asymptotic prices can be obtained as the limit of the unconstrained multi-step prices, see Theorem 3.5. Finally, we are interested in the asymptotic behaviour of the prices as the risk aversion of the agent tends to infinity. For a dominated continuous-time framework, it has been shown in [75, 60] that the value of the utility maximization problem converges to the superhedging price as the risk aversion tends to infinity. In a non-dominated discrete-time setting, the same result has later been obtained in [6, 35], see also [25, 16] for similar results. Moreover, for finite state spaces and for downside-sensitive preferences, it has been shown in [28] that the risk-based price bounds approach the no-arbitrage ones as the set of desirable claims gets smaller. In this article, we impose a uniform ellipticity condition on the covariance of the random factors to show that the asymptotic risk-based prices converge to the worst-case prices associated to the -expectation as the risk aversion tends to infinity, see Theorem 3.6.

Apart from the novel theoretical insights regarding the converge of the multi-step prices to the asymptotic risk-based prices, Chernoff-type approximations also provide a tool for numerical approximations which is illustrated in Section 4. For instance, since the asymptotic risk-based prices only depend on the covariance structure of the model but not on the particular choice of the distribution, it is sufficient to recursively compute the indifference prices in the binomial model for every trading period. This also works well in the presence of model uncertainty, see Subsection 4.2 and Subsection 4.4. Furthermore, the numerical simulations in Subsection 4.3 confirm that the asymptotic prices only depends on the covariance of the increments although the precise bounds for the difference between the multi-step prices and the asymptotic prices might depend on the choice of the model. Convergence rates for Chernoff-type approximations have been investigated in [19] but addressing this question in the present context is beyond the scope of this article. So far, we focused on ask prices derived from the view point of the seller. Similarly, from the perspective of the buyer, one can derive the corresponding bid prices which are related to the ask prices via the equation . In particular, the bid-ask spread for the risk-based prices is always smaller than the the bid-ask spread for the worst-case prices associated to the -expectation, see Subsection 4.5.

The rest of this article is organized as follows: in Section 2, we introduce the market model, the asset distribution given by a sublinear expectation, dynamically consistent pricing operators and the necessary terminology regarding strongly continuous convex monotone semigroups. Section 3 first introduces the agent’s preferences and indifference pricing relations before stating the main results. Section 4 contains several examples in order to illustrate the abstract results including numerical simulations. The proofs of the main results are given in Section 5. Finally, Appendix A contains a basic convexity estimates and elementary properties of sublinear expectations while Appendix B contains some exponential moment estimates.

2. Market model and pricing operators

We consider financial assets which are traded at discounted prices at discrete time-points for some trading period .111Here, the superscript denotes the transpose of a vector or a matrix. All prices/payoffs are discounted by expressing them in terms of a numéraire which is strictly positive in all possible states at all considered trading times, i.e., the discounted value of a random payoff at time is given by . Furthermore, the asset prices start at and follow the dynamics

| (2.1) |

where is a deterministic drift and are i.i.d. random vectors on a sublinear expectation space which will be specified in the following subsection.

2.1. Asset distribution and sublinear expectations

A sublinear expectation space consists of a set , a pointwise ordered linear space of random variables with and for all and and a sublinear expectation satisfying

-

(i)

for all ,

-

(ii)

for all with ,

-

(iii)

for all ,

-

(iv)

for all and .

The sublinear expectation is called continuous from above if for all sequences with . Note that the properties (i) an (iii) imply cash invariance, i.e., it holds for all and . Sublinear expectations were introduced by Peng to incorporate model uncertainty of the asset distribution, see [71] for a detailed discussion. Indeed, the formula

| (2.2) |

defines a sublinear expectation, where the supremum is taken over an uncertainty set of probability measures on . On the other hand, every sublinear expectation which is continuous from above admits such a representation, see [71, Theorem 1.2.2]. Sublinear expectations are also closely related to several other concepts such as coherent risk measures in mathematical finance [3], upper expectations in robust statistics [53] and upper coherent previsions in the theory of imprecise probabilities [80]. In a dynamic setting sublinear expectations are linked to BSDEs [41, 74, 77]. Instead of specifying the space , we rather assume that it is rich enough to guarantee that and that all the terms appearing in the following are again elements of . In particular, we assume that for all and , where denotes the space of all bounded Lipschitz-continuous functions . The random vectors are supposed to be independent and identically distributed (i.i.d.) meaning that

and that is independent of for all , i.e.,

Furthermore, the random vectors have no mean uncertainty, i.e.,

| (2.3) |

For the sake of illustration, we provide several examples for the uncertain asset distribution given by the functional , where the space consists of all bounded continuous functions . Since we have already assumed that for all , the term is also well-defined for all if the sublinear expectation is continuous from above. The latter is valid if the supremum in equation (2.2) is taken over a tight set of probability measures.

Example 2.1.

- (i)

-

(ii)

Let be a probability measure on and be a bounded set.222As usual, denotes the Borel -algebra on . Perturbing the values of by leads to a sublinear distribution incorporating parametric uncertainty given by

Condition (2.3) is satisfied if and for we recover the linear case without uncertainty. As a particular one-dimensional example of this parametrization, we choose the Dirac measure and , where is a reference volatility and is the level of uncertainty. Then, the sublinear expectation

describes a binomial model with uncertain volatility. We also want to mention that, for every , the distribution is transformed to the distribution

through the weak transport plan . For uncertainty sets based on weak optimal transport, we refer to [58] and the references therein.

-

(iii)

In recent years, non-parametric uncertainty has been becoming increasingly popular and has been explored extensively, for instance, in the field of distributionally robust optimization, see, e.g, [8, 17, 45, 62, 72, 81, 83]. The analytical tractability of transport distances such as the Wasserstein distance allows for dual representations and explicit sensitivity analysis, see [7, 9]. Let be a reference distribution with and for some . We define

where is the level of uncertainty and the transport distance is given by

with the infimum being taken over the set of all couplings between and satisfying for all symmetric -matrices . Alternatively, the set can be replaced by the set of all martingale couplings. For details, we refer to [21, Section 4.2].

2.2. Continuous time limits and Chernoff-type approximations

So far, we considered asset prices following the dynamics given by equation (2.1) in a discrete-time framework with fixed step-size . Now, we are interested in the limit behaviour of the asset dynamics as the number of intermediate trading periods tends to infinity. Let , and for all . We define and

| (2.4) |

It follows from Peng’s central limit theorem for sublinear expectations, see [50, 68, 69, 70], that

| (2.5) |

for all , where is -normally distributed with for all and . In the linear case , we simply obtain , where is normally distributed with covariance matrix . While Peng’s definition of the -normal distribution relies on the existence and uniqueness of viscosity solutions for the fully nonlinear PDE

| (2.6) |

by setting , in this article, we will take an equivalent semigroup perspective. In the linear case, the family is a Brownian motion whose linear transition semigroup is given by the heat semigroup

for all , and . The semigroup is uniquely determined by its generator

for all and , where the space consists of all bounded twice continuously differentiable functions with bounded first and second derivative. In the sublinear case, the operators

form a semigroup of sublinear operators which is uniquely determined by its generator

for all and , see [21, Theorem 4.1]. Furthermore, the unique viscosity solution of equation (2.6) is given by , see [47, Theorem 6.2]. Subsequently, we explain the semigroup approach in more detail.

Throughout this article, the space is endowed with the mixed topology between the supremum norm and the topology of uniform convergence on compact sets, i.e., the strongest locally convex topology on which coincides on -bounded sets with the topology of uniform convergence on compact sets. In particular, for every sequence and , it holds if and only if

for all compact subsets and , see [47, Proposition B.2]. In the following, if not stated otherwise, all limits in are taken w.r.t. the mixed topology and compact subsets are denoted by . Although the mixed topology is not metrizable, it has been observed in [63] that, for monotone operators , sequential continuity is equivalent to continuity which is further equivalent to continuity on norm-bounded sets. For more details on the mixed topology, we refer to [47, Appendix B] and the references therein. Since functions are ordered pointwise here, an operator is called monotone if for all and with for all and convex if for all , and . The following definition characterizes the semigroups which will be studied in this article.

Definition 2.2.

A family of operators is called strongly continuous convex monotone semigroup on if the following conditions are satisfied:

-

(i)

is convex and monotone with for all and ,

-

(ii)

and for all and ,

-

(iii)

for all ,

-

(iv)

for all .

Furthermore, the generator of the semigroup is defined by

where the domain consists of all such that the previous limit exists.

It has recently been shown by Blessing et al., see [18], that strongly continuous convex monotone semigroups are uniquely determined by their so-called upper -generators defined on their upper Lipschitz sets. While this result is convincing due to its generality, in many applications, the generator can only be determined for sufficiently smooth functions . However, under additional conditions, the semigroup is already uniquely determined by the evaluation of its generator at smooth functions or even only smooth functions with compact support, see [18, 21, 22]. A precise statement which is sufficient for the applications presented in this article is given in Theorem 5.4. The second main result about strongly continuous convex monotone semigroups is that they allow for Chernoff-type approximations of the form

| (2.7) |

Here, the starting point is a family of one-step operators from which we derive the iterated operators . Under suitable stability conditions, the limit in equation (2.7) exists and defines a strongly continuous semigroup on which is uniquely determined by the infinitesimal behaviour of . To be precise, it holds

for smooth functions and the previously mentioned comparison principle can be applied. Chernoff-type approximations have been studied in [21, 20, 18, 22] and in Section 5 we recall the precise statement on which the proofs of the main results of this article are based.

Example 2.3.

Let for all , and , where the constant drift and the random factors are the same as before. It follows from Taylor’s formula that

for all and . Furthermore, the stability conditions required for the Chernoff-type approximations are satisfied. Hence, for every and , the limit

exists and defines a strongly continuous convex monotone semigroup on which is uniquely determined by its generator

for all and . For details, we refer to [21, Theorem 4.1]333The result in [21] is only stated with but the argumentation remains valid when adding a constant drift.. Moreover, by using that the random factors are i.i.d., one can show that

| (2.8) |

for all , , and . Since [47, Theorem 6.2] guarantees that the unique viscosity solution of equation (2.6) is given by , a random variable is G-normally distributed with if and only if for all . In this way, we recover a variant of Peng’s central limit theorem as a particular case of a Chernoff-type approximation. In addition, the semigroup approach used in [21] allows to replace the sublinear expectation by a convex expectation without significantly changing the proof. In contrast, the earlier results in [50, 68, 69, 70] are only stated for the sublinear case. The same is true for the convergence rates in [19] based on the semigroup approach in comparison to the ones based on monotone schemes for viscosity solutions in [49, 52, 57, 78].

We conclude this brief illustration of the semigroup approach by picking up the two sublinear expectations from Example 2.1. In the sequel, we denote by the sublinear expectation from Example 2.1(ii) describing parametric uncertainty with and by the sublinear expectation from Example 2.1(iii) describing non-parametric uncertainty with the same parameter . We define

and denote by and the corresponding semigroups with generators and , respectively. An explicit computation shows that

with for all and . The linear part on the right-hand side is the generator of the reference model, i.e., a Bachelier model with covariance matrix and drift , whereas the supremum incorporates the model uncertainty. In particular, the generator does not depend on the specific type of uncertainty as long as the amount of uncertainty is the same. The comparison principle guarantees that this observation is also valid for the semigroups, i.e., it holds for all and . For details, we refer to [21, Subsection 4.2].

2.3. Dynamically consistent pricing operators

In this subsection, we identify desirable properties for the pricing operators and focus on the pricing of European options with payoffs . As before, we consider discrete trading times for some trading period and recall that all prices are discounted. For every , we denote by the price at time of the contingent claim in the state . For every with and , we assume that

-

(p1)

with ,

-

(p2)

and for all ,

-

(p3)

implies ,

-

(p4)

,

-

(p5)

.

The conditions (p1)-(p3) have a clear interpretation and are desirable for any pricing operator. Since the underlying dynamics is a homogeneous Markov process, we require in condition (p5) that the pricing operators are also homogeneous, i.e., conditioned that the market is at time and in the same state, the prices of and coincide. In the sequel, the operator is therefore simply denoted by . Furthermore, as we will discuss below, condition (p4) guarantees the consistency of the extended pricing operators which reduces to the semigroup property, i.e., for all and . In particular, the pricing operators are fully determined by the one-step pricing operators and by the equation

We next discuss an extension of pricing operators to path-dependent options. To do so, let , where denotes the space of all bounded continuous functions . Then, represents a path-dependent option for some . Suppose that, for every , there exists with

for all of the form for with and . In addition, for every with and , we assume that

-

(1)

and implies ,

-

(2)

implies ,

-

(3)

implies .

If condition (3) were violated, there would exist a time and a state where is priced strictly higher than , even though has a lower price than in all possible states at some future time. This would result in time inconsistencies in the prices. Moreover, it is well known that condition (3) implies the dynamic programming principle or Bellman’s principle, see e.g. [29] and the respective references after Definition 2.2. In our context, the following statement holds.

Lemma 2.4.

Under the assumption that conditions (1) and (2) are satisfied, condition (3) is equivalent to

-

(3’)

for all with and .

In particular, for all and .

Proof.

Suppose that condition (3) is satisfied. Let with and . Since condition (1) implies , we obtain from (3) that .

Conversely, suppose that condition (3’) holds. Let with and with . Using condition (2), we obtain .

As for the second part, let and . For , we have . Hence, it follows from condition (3’) that

where and therefore . ∎

Remark 2.5.

Let be a family of path-dependent pricing operators which satisfies (1)-(3). Then, its restriction given by

of homogeneous pricing operators for options with payoff functions , satisfy

-

(p1’)

,

-

(p2’)

and for all ,

-

(p3’)

implies ,

-

(p4’)

,

for all . Here, the conditions (p1’)-(p3’) follow directly from the definition, while (p4’) is a consequence of Lemma 2.4.

As a result of the previous discussion, we obtain that a homogeneous pricing operator , which allows for an extension of pricing operators for path-dependent options, necessarily has to satisfy the semigroup property (p4’). In this sense, the semigroup property is necessary to avoid time inconsistencies in the corresponding prices. In particular, the pricing operator is given by the one-step pricing operators .

We finally remark that an extension to path-dependent pricing operators exists under rather mild conditions. For instance, if the mapping is continuous for all and any bounded continuous function , see e.g. [37, Proposition 5.5], then for every for some , it follows that the operators given by the backward recursion

have the desirable properties.

3. Agent’s preferences and indifference pricing

We now introduce agent’s preferences by considering an agent who measures her risk exposition by the entropic risk measure with risk aversion parameter , i.e., the agent’s risk on the random loss is given by

where is a sublinear expectation space incorporating model uncertainty of the asset distribution. Here, we consider risk measures as functionals defined on losses rather than on positions, i.e., the risk of a position is given by . In order to develop our indifference pricing framework, we first focus on ask pricing operators representing the seller’s price of European contingent claims and the corresponding bid prices will then be derived in Section 4.5. Recall that the asset dynamics with trading period have already been specified at the beginning of Section 2. Hence, the ask price for the contingent claim given the asset price at time is determined by the indifference pricing relation

where contains all available trading strategies. This relation should be read in the following way: assuming that the agent can always trade on the market to reduce her risk exposure, the quantity makes the agent indifferent between selling the derivative at this price or keeping it. Furthermore, the set of available trading strategies can a priori model any type of constraint. For example, we could consider if the agent can trade without constraints all assets in the market or for some if, for any reason, the agent cannot trade some of the assets. The set could also be bounded if volume constraints are imposed. Note that, in principle, by modelling in a suitable way, not all the components of the asset process need to be assets on the market so that the derivative could also depend on some external factors.

Since the factors are i.i.d., we obtain that the ask prices for one trading period are fully determined by the equation

where the trading adjusted risk functional is given by

| (3.1) |

Furthermore, by applying the cash invariance on the deterministic number , it follows that the one-step pricing operator is given by

| (3.2) |

for all and . Under reasonable assumptions specified in Section 3.1, one can show that and therefore, as discussed in Subsection 2.3, the time consistent multi-step pricing operators are given by

| (3.3) |

Similar to the worst-case asset dynamics in Subsection 2.2, we are now interested in the limit behaviour of the ask prices as the number of intermediate trading periods tends to infinity. Let and for all . Then, the limit

| (3.4) |

defines the time-consistent asymptotic risk-based price of a claim with payoff function .

Before stating the main results, we want to explain the relation between local and global indifference pricing in the present framework. Our formalization of the indifference pricing relation might appear slightly different from classical indifference pricing because one usually starts from a risk measure that is defined globally on the entire path of the asset process and the hedging strategy. However, although the pricing operator here is defined locally by a one-step indifference pricing principle, its concatenation in equation (3.3) again satisfies an indifference pricing relation. Indeed, since the entropic risk measure is time-consistent, we obtain

where . Hence, equation (3.3) and the cash invariance of yield

| (3.5) |

Using that the random factors are i.i.d., we obtain the global indifference relation

where with and the infima are taken over all -valued processes such that is -measurable for all .

3.1. Main results

Recall that is a constant drift and that is an i.i.d. sequence of random variables defined on a sublinear expectation space . So far, we did not specify the space but assumed it to be rich enough to guarantee that all the appearing expectations are well defined. In order to state and prove the results in this section, we define and impose the following conditions.

Assumption 3.1.

Let be a closed convex set including zero. Suppose that contains all -measurable functions satisfying for some , where denotes the Euclidean norm. In addition, for every and ,

If the expectation is linear, one can choose and the previous conditions reduce to and for all . Furthermore, the condition states that the mean is not uncertain. When passing from the multi-step prices to the asymptotic risk-based prices the number of intermediate trading times tends to infinity. Hence, in order to exclude doubling strategies, we impose a volume constraint on the trading sets by considering , where for all and . This constraint also guarantees that the one-step pricing operators

are well defined for all , and . The next theorem shows that the asymptotic risk-based prices are well defined and fully determined by the covariance

of the random factors and the deterministic drift. We define

| (3.6) | ||||

for all , and . Moreover, we recall that contains all bounded twice continuously differentiable functions with bounded first and second derivative and that all limits in are taken w.r.t. the mixed topology.

Theorem 3.2.

Suppose that Assumption 3.1 is satisfied. Then, for every , the limit

of the volume constrained multi-step ask pricing operators exists for all and . Furthermore, the family is a strongly continuous convex monotone semigroup on which is uniquely determined by its generator satisfying and

| (3.7) |

for all and .

The proof is given in Subsection 5.1. Without additional conditions, the volume constraint is necessary to prevent the two infima in equation (3.7) from taking the value . However, in case that there exists with

| (3.8) |

one can always restrict the infima to a bounded set which might depend on . This allows to take the limit in equation (3.7) and the next theorem shows that this transfers to the semigroups . Hence, we can define asymptotic risk-based prices involving unbounded sets of trading strategies as limits of volume constraint prices. Moreover, for it is sufficient to require that there exists with

| (3.9) |

Theorem 3.3.

Suppose that Assumption 3.1 and condition (3.8) are valid. Then, the limit

of the volume constrained prices exists for all and . Furthermore, the family is a strongly continuous convex monotone semigroup on which is uniquely determined by its generator satisfying and

Moreover, for , it is sufficient to require condition (3.9) instead of condition (3.8).

The proof is given in Subsection 5.2. In the case , the asymptotic prices do not dependent on the first derivative and are dominated by the -expectation which has previously been introduced in Subsection 2.2. Hence, while pricing with a -expectation corresponds to pricing according the worst-case measure in the ambiguity set, the risk-based framework leads to a mitigation of the worst-case bounds by taking into account the attitude of the agent towards risk.

Corollary 3.4.

Proof.

Let and . Since , we can substitute by to obtain

In addition, for every , the sublinearity of implies

and therefore . Since the family is a strongly continuous convex monotone semigroup on with generator

it follows from Theorem 5.4 that for all and . ∎

In one dimension, condition (3.8) is valid if and only if or or . The first case is trivial and the second case corresponds to the -expectation. Moreover, writing , the third case occurs if there exists with . Hence, in one dimension, condition (3.8) is satisfied in all relevant examples. Furthermore, in multi dimensions, condition (3.9) means that the variance of the increment is non zero for any strategy which also non trivially invests in the drift. Since has mean zero and thus the chance of loosing the investment exists, this means that the agent can not use the drift in order to reduce her risk infinitely.

So far, we defined the asymptotic risk-based prices corresponding to the case that no trading constraints are imposed as the limit of asymptotic risk-based prices corresponding to the case that the trading strategies are restricted to a bounded set. The question arises whether, in the absence of trading constraints, the asymptotic risk-based prices can also be obtained directly as the limit of unconstrained multi-step indifference prices. In order to achieve this approximation, we assume that there exist and with

| (3.10) |

In addition, for every , there exist and with

| (3.11) |

In particular, applying condition (3.11) with yields such that

is well-defined for all , and . Previously, we only imposed conditions on the first and second moments of which uniquely determine the asymptotic risk-based prices. This is due to the fact that strongly continuous convex monotone semigroups are uniquely determined by their generators. In particular, the convergence in Theorem 3.3 is derived from the convergence of the generators which only depend on the covariance of but not on further information about its distribution. In contrast to the asymptotic prices, the one-step prices depend on the particular distribution of which explains the necessity of imposing additional conditions on the exponential moments.

Theorem 3.5.

The proof is given in Subsection 5.3 and it relies on the fact that doubling strategies are automatically excluded by the additional conditions on the risk measure. Furthermore, we show in Appendix B that the conditions (3.10) and (3.11) are satisfied for bounded symmetric distributions and for families of normal distributions. These distributions naturally appear in numerical implementations of the iterative scheme, see Section 4.

So far, the risk aversion of the agent has been described by a fixed parameter which did not appear in the notation. However, the generator and thus the corresponding semigroup clearly depend on the choice of this parameter. Subsequently, we denote by the semigroup from Theorem 3.3 previously denoted by and by its generator previously denoted by . Corollary 3.4 states that, in the absence of trading constraints and for any , the asymptotic risk-based prices are dominated by the worst-case prices corresponding to the -expectation. We now show that this upper bound is achieved as the risk aversion of the agent tends to infinity if there exists with

| (3.12) |

Condition (3.12) guarantees that condition (3.8) is also valid since Lemma A.2(iv) implies

In particular, Theorem 3.3 and Corollary 3.4 can be applied. For a linear expectation both conditions are clearly equivalent but the same is not true in the sublinear case.

Theorem 3.6.

Let and suppose that Assumption 3.1 and condition (3.12) are satisfied. Then, as the risk aversion of the agent tends to infinity, the limit

of the unconstrained asymptotic risk-based prices exists for all and . Moreover, the family is a strongly continuous convex monotone semigroup on which is uniquely determined by its generator satisfying and

In particular, the limit of the risk-based prices coincides with the worst-case prices, i.e.,

where the strongly continuous convex monotone semigroup on is given by

The proof is given in Subsection 5.4. We conclude this section with a brief discussion of the difference between the conditions (3.8) and (3.12) using the binomial model and the normal distribution as illustrative examples.

Remark 3.7.

First, we consider a one-dimensional uncertain binomial model

where are fixed parameters. Condition (3.8) is equivalent to meaning that the ambiguity set contains at least one non deterministic model and condition (3.12) is equivalent to meaning that all the models are non deterministic and their volatility is uniformly bounded from below.

Second, let be a bounded set of positive semi-definite symmetric -matrices and

where denotes the -dimensional standard normal distribution and is any matrix with . For every ,

Hence, condition (3.8) means that, for every , there exists with . However, none of the matrices has to be positive definite, i.e., none of the linear models has to satisfy condition (3.8). On the other hand, condition (3.12) is satisfied if and only if is a set of uniformly positive definite matrices, i.e., it holds . Hence, all the linear models have to satisfy condition (3.12) with a uniform parameter.

4. Examples and numerical illustrations

In this section, we illustrate the application of our pricing model to different market dynamics. Since the continuous-time pricing dynamics does not depend on the choice of the particular model apart from its covariance structure, we can use simple models for the approximation. For instance, the Bachelier model (or the Black-Scholes model in the geometric case), is obtained as scaling limit of the binomial model. Similarly, we can start from indifference prices defined in a binomial model with or without volatility uncertainty and recursively solve the optimal investing problem for every trading period. We further illustrate the dependence of the pricing dynamics on both the level of risk aversion and of uncertainty as well as the convergence of the risk-based prices to the worst-case prices as the risk aversion tends to infinity. We also compare different linear models with the same covariance structures leading to the same continuous-time pricing dynamics although the error bounds might be different. Finally, we observe that the bid-ask spread for the risk-based prices is clearly smaller the one for the worst-case ones.

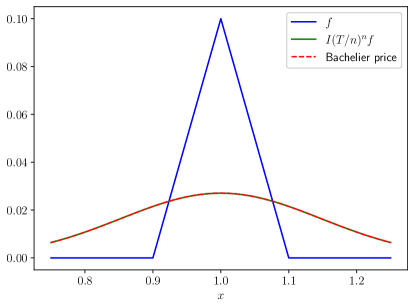

Throughout this section, we focus on pricing a butterfly option written on a single asset. Recall that a butterfly option with lower strike , middle strike and upper strike gives the holder of the contract the right to obtain at maturity the payoff

Usually, one requires .

In order to produce the numerical illustrations, we always implement444Source code and examples are available at https://github.com/sgarale/risk_based_pricing. the discrete-time approximation given by equation (3.4). Note that one could also exploit the characterization of the pricing dynamics as a non-linear PDE but working on the level of the generator poses additional difficulties when dealing with non smooth functions as it is mostly the case in financial contracts. Hence, we directly instead compute at each step of the iteration the trading strategy that optimally reduces the risk for the seller of the contract in the next trading period. We will only consider models satisfying the conditions (3.9)-(3.12) which allows us to choose and to consider the limit . In particular, we can perform an unconstrained optimization.

4.1. Implementation

For the iteration of the one-step operators, we have to find a suitable numerical representation of the resulting functions. Starting with a payoff function , which is known on its entire domain, we numerically compute the quantity on a finite set . In order to extend to its entire domain we then have to prescribe an interpolation method. The available possibilities include the following:

-

•

directly interpolate , e.g., linearly, using splines, etc,

-

•

save the optimizers corresponding to the points and interpolate them when computing on new points.

When testing these methods, the first one does not seem feasible: in order to obtain a good approximation of the value , which is then used for the next step of the iteration, one has to start from a very fine spatial grid. This is computationally expensive and becomes even more challenging in higher dimensions. We therefore choose the second option: first, we compute on a set of points covering the region of the domain we are interested in. The resulting optimizers are then interpolated to obtain a better approximation of on a finer grid. Furthermore, when the increments of the model are bounded, we can explicitly choose the bounds of the grid to guarantee that errors coming from the part of the domain that we disregard are avoided. For the sake of illustration, we consider a one-dimensional binomial model with volatility and suppose that we are interested in approximating the value on the interval by an -step iteration with step-size . Then, for the last step, the function coming from the -th step, will be evaluated on the region . Proceeding backwards, we obtain that it is sufficient to start the iteration with a grid contained in the interval

in order to avoid errors that might otherwise propagate to the interval . This also shows that a finer time discretization comes at the cost of enlarging the spatial grid.

4.2. Binomial model

We consider a one-dimensional binomial model with drift and volatility , i.e., the distribution of under the market expectation is given by

where . Assumption 3.1 and condition (3.12) are clearly satisfied. Hence, for and any risk aversion , Theorem 3.3 yields a strongly continuous convex monotone semigroup on which is uniquely determined by its generator satisfying and

for all and . Due to Theorem 5.4, the semigroup coincides with the linear heat semigroup corresponding to the pricing dynamics under the Bachelier model [4]. The risk aversion parameter does not appear in the generator of which is not surprising since the binomial model is complete. Hence, there is no reason for the prices to be sensitive to the risk aversion of an agent if the agent can replicate any payoff.

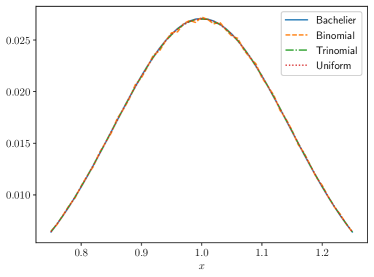

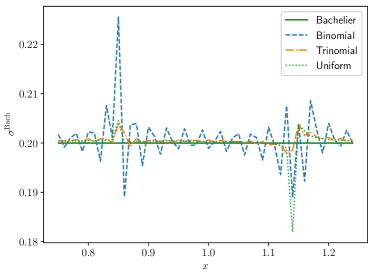

4.3. Several linear models

The observation that the risk aversion parameter does not affect the pricing dynamics extends to any linear model. Indeed, for and any linear expectation , Corollary 3.4 guarantees that the generator is given by

Furthermore, as long as the models share the same covariance structure given by the function for all , the semigroup does not depend on the particular choice of the distribution .

Figure 2 shows the approximation of the same risk-based prices with different linear models having the same volatility (). We compare the following models:

| (Binomial) | |||

| (Trinomial) | |||

| (Uniform) |

While all these models converge to the same Bachelier price, it seems that richer models convergence faster when using the same number of steps in the time discretization. This is particularly evident from the plot of the Bachelier implied volatilities.

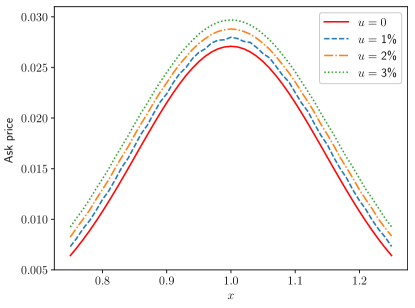

4.4. Uncertain binomial model

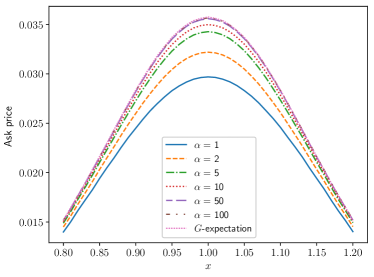

We consider a one-dimensional binomial model with drift and volatility uncertainty. Using the parametrization from Example 2.1(ii), we choose and , where is a reference volatility and is the level of uncertainty. This yields the sublinear expectation

Here, the risk averse agent fears the worst-case and increases the price as it can be seen in Figure 3.

Moreover, condition (3.12) is satisfied for any in which case Theorem 3.6 implies that the risk-based prices convergence to the -expectation as . Figure 4a displays the worst-case bound given by the -expectation and the risk-based prices for different levels of risk aversion. As shown in Corollary 3.4, the risk-based prices are always lower than the worst-case ones. Figure 4b shows more in detail how the risk-based prices approach the -expectation as the risk aversion parameter increases. Recall from Subsection 2.2 that the -expectation is obtained by a Chernoff-type approximation with one-step operator .

4.5. Bid-ask spread

Using the same arguments as in Section 3, we can additionally define bid pricing operators. Indeed, switching to the buyer position, we obtain that the one-step bid prices have to satisfy the indifference pricing relation

Hence, similarly to equation (3.2), we can define the one-step pricing operators

and the corresponding time consistent multi-step pricing operators

for all , and . Consequently, for every and , the limit

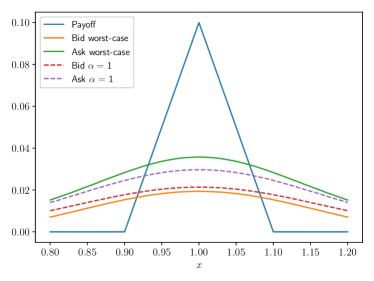

exists and satisfies for all and . Hence, in the absence of trading constraints, Corollary 3.4 implies that the bid-ask spread for the risk-based prices is smaller than the bid-ask spread for the worst-case prices associated to the -expectation. We now consider again the uncertain binomial model from Subsection 4.4 with reference volatility and uncertainty level .

Figure 5a shows the bid prices at different levels of risk aversion for a butterfly option5 while Figure 5b compares the risk-based bid-ask bounds with the worst-case ones corresponding to pricing with a -expectation. The risk-based approach, which considers the attitude of the agent towards uncertainty, clearly leads to a reduction of the bid-ask spread.

5. Proof of the main results

Definition 5.1.

Let be a family of operators . The Lipschitz set consists of all such that there exist and with

Moreover, for every such that the following limit exists, we define

Recall that all limits in are taken w.r.t. the mixed topology.

Assumption 5.2.

Let be a family of operators satisfying the following conditions:

-

(i)

.

-

(ii)

is convex and monotone with for all .

-

(iii)

There exists with

-

(iv)

For every , there exist and with

for all , , and .

-

(v)

The limit exists for all .

-

(vi)

For every , and with ,

-

(vii)

It holds for all .

The previous conditions guarantee that [18, Assumption 5.7] is satisfied since condition (vi) is equivalent to [18, Assumption 5.7(vi)], see [18, Lemma C.2]. Hence, the next theorem follows immediately from [18, Theorem 5.4, Theorem 5.9 and Corollary 5.11].

Theorem 5.3.

Let be a family of operators satisfying Assumption 5.2. Then, there exists a strongly continuous convex monotone semigroup on which is given by

| (5.1) |

In addition, the following statements are valid:

-

(i)

It holds and for all such that exists. In particular, this is valid for all .

-

(ii)

It holds for all and .

-

(iii)

For every , and , there exist and with

for all and .

-

(iv)

It holds and for all .

-

(v)

For every , there exists with

for all , and .

-

(vi)

It holds for all .

It follows from [18, Theorem 4.7] that semigroups which have been constructed this way are uniquely determined by their generators evaluated at smooth functions.

Theorem 5.4.

Let and be two strongly continuous convex monotone semigroups on with generators and , respectively, which satisfy the conditions (v) and (vi) of Theorem 5.3. Furthermore, we assume that and

Then, it holds for all and .

5.1. Proof of Theorem 3.2

Recall that

for all , and , where and . In the sequel, we fix and therefore simply write , , , and .

Proof of Theorem 3.2.

In order to apply Theorem 5.3, we have to verify Assumption 5.2. Furthermore, we have to show that

where is defined by equation (3.6). First, we verify Assumption 5.2(i)-(iv) and (vii). Condition (i) follows from . Regarding condition (ii), the monotonicity of yields the monotonicity of and holds by definition. Let , , and . Let be -optimizers of and , respectively, and define and . Then, by convexity of ,

Letting shows that is convex. For every , , and , the monotonicity and cash invariance of imply

Taking the infimum over and changing the roles of and yields

which shows that condition (iii) is satisfied with . Condition (iv) follows from

In order to verify condition (vii) with , we observe that

for all , and .

Second, we show that . Let . For every , and , applying Taylor’s formula on the function yields

| (5.2) |

It follows from Assumption 3.1 and Lemma A.2(vi) that

for all , and . Hence, there exist and with

for all , and . Dividing by , taking the supremum over and applying the previous estimate with shows that

Third, we verify condition (vi). Several sufficient conditions which guarantee that condition (vi) is valid have been systemically explored in [22, Subsection 2.5]. Here, we show that, for every , there exists with

| (5.3) |

for all and with and . Let , and with and . For every , and , applying equation (5.2) with yields

We apply Lemma A.1 with to obtain

for all and , where

The lower bound follows similarly and therefore taking the supremum over shows that, for every , there exists with

for all , with and and . Hence, we can apply [22, Corollary 2.14] with , and for all , and to obtain that condition (vi) is satisfied666The result in [22] is stated under a slightly stronger condition but a close inspection of the proof reveals that it is sufficient to verify inequality (5.3) instead of [22, Inequality (2.35)]..

Fourth, for every , we show that the limit exists and is given by

where for all , and . Let . Equation (5.2), Assumption 3.1 and Lemma A.2(i) and (vi) imply

| (5.4) |

for all , and , where

and . For every , and , we can estimate

and, by defining ,

| (5.5) |

Since for , we obtain

| (5.6) |

It remains to show that, for every ,

| (5.7) |

For every , and , Lemma A.2(viii) implies

Moreover, for every , by inequality (5.1) and Assumption 3.1, there exists with

| (5.8) |

Let and choose such that the previous inequality is valid. It follows from

that there exists with

for all , and . Let . Since the functions are equicontinuous with and converges uniformly to zero as , there exists with

| (5.9) |

Combining the inequalities (5.8) and (5.9) shows that equation (5.7) is valid. Hence, it follows from equation (5.4) that

By additionally applying this result on the constant function , we obtain that the limit exists and is given by

5.2. Proof of Theorem 3.3

The proof is based on the stability results for strongly continuous convex monotone semigroups in [22]. The basic idea is that, for a sequence of semigroups satisfying certain stability conditions, convergence of the generators implies convergence of the corresponding semigroups. In many applications, the generators can be determined explicitly for smooth functions and the same applies to their convergence. In contrast, showing the convergence of the semigroups directly is often not feasible.

Proof of Theorem 3.3.

In order to apply [22, Theorem 2.3], we have to verify [22, Assumption 2.2]. The conditions (i), (iii) and (iv) follow from Theorem 5.3 and the corresponding estimates in the proof of Theorem 3.2. In order to verify the conditions (ii) and (v), we show that, for every , there exist and with

| (5.10) |

for all , with and . Choose such that condition (3.8) is satisfied. For every , and , Lemma A.2(vii) implies

where and . This shows that equation (5.10) is valid and condition (v) follows immediately. For , we observe that, for every with ,

with equality for . Moreover, for every with , one can use condition (3.9) to estimate

for suitable constants . Hence, equation (5.10) is still valid for some . In order to verify condition (iii), we further show that there exists with

| (5.11) |

for all with . By equation (5.10), there exists with

for all , with and . For every with , and , it follows from Lemma A.2(viii) that

This shows that inequality (5.11) is satisfied. Furthermore, it holds

where denotes the space of all bounded twice differentiable functions such that the first and second are bounded and uniformly continuous. Indeed, for every and , the supremum in inequality (5.9) and therefore in inequality (5.7) can be taken over instead of . We obtain

and [20, Theorem 4.3] transfers the previous statement to the semigroup . It follows from [22, Corollary 2.16] that condition (iii) is satisfied for any sequence 777The result in [22] is stated under a slightly stronger condition but a close inspection of the proof reveals that it is sufficient to verify inequality (5.11).. The claim now follows from [22, Theorem 2.5] since Theorem 5.4 guarantees that the limit does not depend on the choice of the sequence . ∎

5.3. Proof of Theorem 3.5

The proof is similar to the one of Theorem 3.2 as soon as we can constrain the trading strategies to a bounded set.

Proof.

By condition (3.11), there exists such that is well-defined for all . Hence, since we are only interested in the limit behaviour of the iterated operators, we can replace by for all without affecting the result. We subsequently show that Assumption 5.2 is satisfied. The conditions (i)-(iv) and (vii) can be verified exactly as in the proof of Theorem 3.2, where we did not use that the set was bounded. In order to verify condition (v), let . We show that there exist and with

| (5.12) |

for all and . For every , and , Taylor’s formula implies

We choose and apply condition (3.10) to obtain and with

for all and . Furthermore, we apply condition (3.11) with

to obtain and with

for all , with and . Since is bounded, we have therefore verified equation (5.12). Now, one can proceed line by line as in the proof of Theorem 3.2 to show that the limit exists and is given by

where satisfies equation (5.12). Since the left-hand side does not depend on the particular choice of , we obtain

Finally, we observe that the choice of and in equation (5.12) only depends on and . Hence, again line by line as in the proof of Theorem 3.2, one can show that, for every , there exist and with

for all and with and . It follows from [22, Corollary 2.14] that condition (vi) is satisfied. Theorem 5.3 and Theorem 5.4 yield the claim. ∎

5.4. Proof of Theorem 3.6

This proof of also based on the stability results in [22] and thus very similar to the proof of Theorem 3.3. Recall that, for every , we now denote by the semigroup from Theorem 3.3 previously denoted by and by its generator previously denoted by .

Proof of Theorem 3.6.

In order to apply [22, Theorem 2.3], we have to verify [22, Assumption 2.2]. The conditions (i), (iii) and (iv) follow from Theorem 5.3 and the corresponding estimates in the proof of Theorem 3.2. In order to verify condition (v), we show that, for every , there exists with

| (5.13) |

for all , and , where

for all and . Let , and . Choosing yields

Furthermore, by condition (3.12) and Lemma A.2(ix), there exists with

for all with . Hence, for , we obtain

and Lemma A.2(viii) implies

It follows from as that inequality (5.13) is valid. Since Corollary 3.4 yields

and inequality (5.13) can also be applied on the constant function , we obtain

This shows that condition (v) is satisfied. It remains to verify condition (ii). For every risk aversion parameter and volume constraint , we denote by the semigroup from Theorem 3.2 corresponding to and by its generator. We show that there exists with

| (5.14) |

for all , and with . It follows from the proof of Theorem 3.3 that there exist and with

for all , with and . Hence, there exists with for all , and with . Corollary 3.4 and Lemma A.2(viii) now imply that inequality (5.14) is valid. Furthermore, we obtain from [22, Corollary 2.16] that, for every and with ,

The uniform continuity from above w.r.t. is preserved in the limit , i.e., condition (ii) is satisfied888The result in [22] is only stated for sequences of semigroups but it is actually valid for families of semigroups which are parameterized by an arbitrary index set. Here, we choose and .. The first part of the claim follows from [22, Theorem 2.5] since Theorem 5.4 guarantees that the limit does not depend on the choice of the sequence . Furthermore, as discussed in Subsection 2.2, the family is a strongly continuous convex monotone semigroup on with generator

Hence, the second part of the claim also follows from Theorem 5.4. ∎

Appendix A Basic convexity estimates

Lemma A.1.

Let be a vector space and be a convex functional. Then,

Proof.

For every and ,

The next lemma states some basic properties of convex and sublinear expectations. Convex expectations generalize sublinear expectations by relaxing the conditions (iii) and (iv) in the definition of a sublinear expectation to

Furthermore, convex expectations correspond to convex risk measures which are defined on losses rather than positions.

Lemma A.2.

For a convex expectation space the following statements are valid:

-

(i)

for all and .

-

(ii)

for all bounded .

-

(iii)

for all and .

-

(iv)

for all .

-

(v)

for all .

-

(vi)

Let with for all . Then, it holds

Moreover, if is sublinear, then the following statements are valid:

-

(vii)

for all .

-

(viii)

for all .

-

(ix)

for all .

Proof.

The properties (i)-(vi) coincide with [21, Lemma B.2]. Using the sublinearity of , property (vii) is obtained by rearranging the inequality

Property (viii) follows from property (vii) by changing the roles of and . Finally, the sublinearity of implies showing that property (ix) is valid. ∎

Appendix B Exponential moment estimates

Lemma B.1.

Proof.

Let . Regarding condition (3.10), we observe that

In order to verify condition (3.11), let and . For every , the dominated convergence theorem and Jensen’s inequality imply

Since hyperbolic cosine is a continuous function, we can choose a sequence with to obtain

| (B.1) |

It remains to show that, for every , there exist and with

| (B.2) |

For every , we consider the function . It holds

Since for , there exists with

In addition, since , there exists with

This shows that inequality (B.2) is valid with and . Hence, for every , it follows from inequality (B.1) and (B.2) that there exists and with

for all and . This shows that condition (3.11) is valid. ∎

Lemma B.2.

Proof.

Denote by the largest eigenvalue among all covariance matrices and choose . In particular, for every and , the matrix is invertible and satisfies . We obtain

for all and , where and is a symmetric matrix with . This shows that condition (3.10) is valid.

References

- [1] B. Acciaio, M. Beiglböck, F. Penkner, and W. Schachermayer. A model-free version of the fundamental theorem of asset pricing and the super-replication theorem. Math. Finance, 26(2):233–251, 2016.

- [2] T. Arai and M. Fukasawa. Convex risk measures for good deal bounds. Math. Finance, 24(3):464–484, 2014.

- [3] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath. Coherent measures of risk. Math. Finance, 9(3):203–228, 1999.

- [4] L. Bachelier. Théorie de la spéculation. Les Grands Classiques Gauthier-Villars. [Gauthier-Villars Great Classics]. Éditions Jacques Gabay, Sceaux, 1995. Théorie mathématique du jeu. [Mathematical theory of games], Reprint of the 1900 original.

- [5] J. D. Backhoff Veraguas and J. Fontbona. Robust utility maximization without model compactness. SIAM J. Financial Math., 7(1):70–103, 2016.

- [6] D. Bartl. Exponential utility maximization under model uncertainty for unbounded endowments. Ann. Appl. Probab., 29(1):577–612, 2019.

- [7] D. Bartl, S. Drapeau, J. Obłój, and J. Wiesel. Sensitivity analysis of Wasserstein distributionally robust optimization problems. Proc. R. Soc. A., 477(2256):Paper No. 20210176, 19, 2021.

- [8] D. Bartl, S. Drapeau, and L. Tangpi. Computational aspects of robust optimized certainty equivalents and option pricing. Math. Finance, 30(1):287–309, 2020.

- [9] D. Bartl and J. Wiesel. Sensitivity of multiperiod optimization problems with respect to the adapted Wasserstein distance. SIAM J. Financial Math., 14(2):704–720, 2023.

- [10] M. Beiglböck, P. Henry-Labordère, and F. Penkner. Model-independent bounds for option prices—a mass transport approach. Finance Stoch., 17(3):477–501, 2013.

- [11] M. Beiglböck, M. Nutz, and N. Touzi. Complete duality for martingale optimal transport on the line. Ann. Probab., 45(5):3038–3074, 2017.

- [12] A. E. Bernardo and O. Ledoit. Gain, loss, and asset pricing. Journal of Political Economy, 108(1):144–172, 2000.

- [13] S. Biagini, M. Frittelli, and M. Grasselli. Indifference price with general semimartingales. Math. Finance, 21(3):423–446, 2011.

- [14] J. Bion-Nadal and G. Di Nunno. Fully-dynamic risk-indifference pricing and no-good-deal bounds. SIAM J. Financial Math., 11(2):620–658, 2020.

- [15] T. Björk and I. Slinko. Towards a General Theory of Good-Deal Bounds*. Review of Finance, 10(2):221–260, 01 2006.

- [16] R. Blanchard and L. Carassus. Convergence of utility indifference prices to the superreplication price in a multiple-priors framework. Math. Finance, 31(1):366–398, 2021.

- [17] J. Blanchet and K. Murthy. Quantifying distributional model risk via optimal transport. Math. Oper. Res., 44(2):565–600, 2019.

- [18] J. Blessing, R. Denk, M. Kupper, and M. Nendel. Convex monotone semigroups and their generators with respect to -convergence. Preprint arXiv:2202.08653, 2022.

- [19] J. Blessing, L. Jiang, M. Kupper, and G. Liang. Convergence rates for Chernoff-type approximations of convex monotone semigroups. Preprint arXiv:2310.09830, 2023.

- [20] J. Blessing and M. Kupper. Nonlinear Semigroups Built on Generating Families and their Lipschitz Sets. Potential Anal., 59(3):857–895, 2023.

- [21] J. Blessing and M. Kupper. Nonlinear semigroups and limit theorems for convex expectations. To appear in Ann. Appl. Probab., 2024+.

- [22] J. Blessing, M. Kupper, and M. Nendel. Convergence of infinitesimal generators and stability of convex monotone semigroups. Preprint arXiv:2305.18981, 2023.

- [23] B. Bouchard and M. Nutz. Arbitrage and duality in nondominated discrete-time models. Ann. Appl. Probab., 25(2):823–859, 2015.

- [24] M. Burzoni, M. Frittelli, Z. Hou, M. Maggis, and J. Obłój. Pointwise arbitrage pricing theory in discrete time. Math. Oper. Res., 44(3):1034–1057, 2019.

- [25] L. Carassus and M. Rásonyi. Optimal strategies and utility-based prices converge when agents’ preferences do. Math. Oper. Res., 32(1):102–117, 2007.

- [26] R. Carmona, editor. Indifference pricing. Princeton Series in Financial Engineering. Princeton University Press, Princeton, NJ, 2009. Theory and applications.

- [27] P. Carr, H. Geman, and D. B. Madan. Pricing and hedging in incomplete markets. Journal of Financial Economics, 62(1):131–167, 2001.

- [28] A. Cerný and S. Hodges. The theory of good-deal pricing in financial markets. In Mathematical finance—Bachelier Congress, 2000 (Paris), Springer Finance, pages 175–202. Springer, Berlin, 2002.

- [29] P. Cheridito and M. Kupper. Composition of time-consistent dynamic monetary risk measures in discrete time. Int. J. Theor. Appl. Finance, 14(1):137–162, 2011.

- [30] P. Cheridito, M. Kupper, and L. Tangpi. Duality formulas for robust pricing and hedging in discrete time. SIAM J. Financial Math., 8(1):738–765, 2017.

- [31] J. H. Cochrane and J. Saa-Requejo. Beyond arbitrage: Good-deal asset price bounds in incomplete markets. Journal of Political Economy, 108(1):79–119, 2000.

- [32] D. Criens. Robust Market Approximations: From Discrete to Continuous Time. Preprint, arXiv:2402.16108 [math.PR] (2024), 2024.

- [33] F. Delbaen, P. Grandits, T. Rheinländer, D. Samperi, M. Schweizer, and C. Stricker. Exponential hedging and entropic penalties. Math. Finance, 12(2):99–123, 2002.

- [34] F. Delbaen and W. Schachermayer. The mathematics of arbitrage. Springer Finance. Springer-Verlag, Berlin, 2006.

- [35] S. Deng, X. Tan, and X. Yu. Utility maximization with proportional transaction costs under model uncertainty. Math. Oper. Res., 45(4):1210–1236, 2020.

- [36] L. Denis and M. Kervarec. Optimal investment under model uncertainty in nondominated models. SIAM J. Control Optim., 51(3):1803–1822, 2013.

- [37] R. Denk, M. Kupper, and M. Nendel. Kolmogorov-type and general extension results for nonlinear expectations. Banach J. Math. Anal., 12(3):515–540, 2018.

- [38] Y. Dolinsky and H. M. Soner. Martingale optimal transport and robust hedging in continuous time. Probab. Theory Related Fields, 160(1-2):391–427, 2014.

- [39] Y. Dolinsky and H. M. Soner. Robust hedging with proportional transaction costs. Finance Stoch., 18(2):327–347, 2014.

- [40] Y. Dolinsky and H. M. Soner. Convex duality with transaction costs. Math. Oper. Res., 42(2):448–471, 2017.

- [41] N. El Karoui, S. Peng, and M. C. Quenez. Backward stochastic differential equations in finance. Math. Finance, 7(1):1–71, 1997.

- [42] H. Föllmer and P. Leukert. Quantile hedging. Finance Stoch., 3(3):251–273, 1999.

- [43] H. Föllmer and A. Schied. Stochastic finance. De Gruyter Graduate. De Gruyter, Berlin, 2016. An introduction in discrete time, Fourth revised and extended edition.

- [44] M. Frittelli. The minimal entropy martingale measure and the valuation problem in incomplete markets. Math. Finance, 10(1):39–52, 2000.

- [45] R. Gao and A. Kleywegt. Distributionally robust stochastic optimization with Wasserstein distance. Math. Oper. Res., 48(2):603–655, 2023.

- [46] I. Gilboa and D. Schmeidler. Maxmin expected utility with nonunique prior. J. Math. Econom., 18(2):141–153, 1989.

- [47] B. Goldys, M. Nendel, and M. Röckner. Operator semigroups in the mixed topology and the infinitesimal description of Markov processes. J. Differential Equations, 412:23–86, 2024.

- [48] A. Gundel. Robust utility maximization for complete and incomplete market models. Finance Stoch., 9(2):151–176, 2005.

- [49] M. Hu, L. Jiang, and G. Liang. On the rate of convergence for an -stable central limit theorem under sublinear expectation. To appear in J. Appl. Probab., 2024+.

- [50] M. Hu, L. Jiang, G. Liang, and S. Peng. A universal robust limit theorem for nonlinear Lévy processes under sublinear expectation. Probab. Uncertain. Quant. Risk, 8(1):1–32, 2023.

- [51] Y. Hu, P. Imkeller, and M. Müller. Utility maximization in incomplete markets. Ann. Appl. Probab., 15(3):1691–1712, 2005.

- [52] S. Huang and G. Liang. A monotone scheme for G-equations with application to the explicit convergence rate of robust central limit theorem. J. Differential Equations, 398:1–37, 2024.

- [53] P. J. Huber. Robust statistics. Wiley Series in Probability and Mathematical Statistics. John Wiley & Sons, Inc., New York, 1981.

- [54] S. Jaschke and U. Küchler. Coherent risk measures and good-deal bounds. Finance Stoch., 5(2):181–200, 2001.

- [55] S. Klöppel and M. Schweizer. Dynamic indifference valuation via convex risk measures. Math. Finance, 17(4):599–627, 2007.

- [56] S. Klöppel and M. Schweizer. Dynamic utility-based good deal bounds. Statist. Decisions, 25(4):285–309, 2007.

- [57] N. V. Krylov. On Shige Peng’s central limit theorem. Stochastic Process. Appl., 130(3):1426–1434, 2020.

- [58] M. Kupper, M. Nendel, and A. Sgarabottolo. Risk measures based on weak optimal transport. arXiv preprint arXiv:2312.05973, 2023.

- [59] F. Maccheroni, M. Marinacci, and A. Rustichini. Ambiguity aversion, robustness, and the variational representation of preferences. Econometrica, 74(6):1447–1498, 2006.

- [60] M. Mania and M. Schweizer. Dynamic exponential utility indifference valuation. Ann. Appl. Probab., 15(3):2113–2143, 2005.

- [61] A. Matoussi, D. Possamaï, and C. Zhou. Robust utility maximization in nondominated models with 2BSDE: the uncertain volatility model. Math. Finance, 25(2):258–287, 2015.

- [62] P. Mohajerin Esfahani and D. Kuhn. Data-driven distributionally robust optimization using the Wasserstein metric: performance guarantees and tractable reformulations. Math. Program., 171(1-2, Ser. A):115–166, 2018.

- [63] M. Nendel. Lower semicontinuity of monotone functionals in the mixed topology on . To appear in Finance Stoch., 2024+.

- [64] A. Neufeld and M. Nutz. Robust utility maximization with Lévy processes. Math. Finance, 28(1):82–105, 2018.

- [65] A. Neufeld and M. Šikić. Nonconcave robust optimization with discrete strategies under Knightian uncertainty. Math. Methods Oper. Res., 90(2):229–253, 2019.

- [66] M. Nutz. Utility maximization under model uncertainty in discrete time. Math. Finance, 26(2):252–268, 2016.

- [67] K. Owari. Robust utility maximization with unbounded random endowment. In Advances in mathematical economics. Vol. 14, volume 14 of Adv. Math. Econ., pages 147–181. Springer, Tokyo, 2011.

- [68] S. Peng. -expectation, -Brownian motion and related stochastic calculus of Itô type. In Stochastic analysis and applications, volume 2 of Abel Symp., pages 541–567. Springer, Berlin, 2007.

- [69] S. Peng. Multi-dimensional -Brownian motion and related stochastic calculus under -expectation. Stochastic Process. Appl., 118(12):2223–2253, 2008.

- [70] S. Peng. A new central limit theorem under sublinear expectations. Preprint arXiv:0803.2656, 2008.

- [71] S. Peng. Nonlinear expectations and stochastic calculus under uncertainty, volume 95 of Probability Theory and Stochastic Modelling. Springer, Berlin, 2019. With robust CLT and G-Brownian motion.

- [72] G. Pflug and D. Wozabal. Ambiguity in portfolio selection. Quant. Finance, 7(4):435–442, 2007.

- [73] M.-C. Quenez. Optimal portfolio in a multiple-priors model. In Seminar on Stochastic Analysis, Random Fields and Applications IV, volume 58 of Progr. Probab., pages 291–321. Birkhäuser, Basel, 2004.

- [74] E. Rosazza Gianin. Risk measures via -expectations. Insurance Math. Econom., 39(1):19–34, 2006.

- [75] R. Rouge and N. El Karoui. Pricing via utility maximization and entropy. Mathematical Finance, 10(2):259–276, 2000.

- [76] A. Schied. Risk measures and robust optimization problems. Stoch. Models, 22(4):753–831, 2006.

- [77] H. M. Soner, N. Touzi, and J. Zhang. Wellposedness of second order backward SDEs. Probab. Theory Related Fields, 153(1-2):149–190, 2012.

- [78] Y. Song. Normal approximation by Stein’s method under sublinear expectations. Stochastic Process. Appl., 130(5):2838–2850, 2020.

- [79] J. Staum. Fundamental theorems of asset pricing for good deal bounds. Math. Finance, 14(2):141–161, 2004.

- [80] P. Walley. Statistical reasoning with imprecise probabilities, volume 42 of Monographs on Statistics and Applied Probability. Chapman and Hall, Ltd., London, 1991.

- [81] D. Wozabal. A framework for optimization under ambiguity. Ann. Oper. Res., 193:21–47, 2012.

- [82] M. Xu. Risk measure pricing and hedging in incomplete markets. Annals of Finance, 2(1):51–71, 2006.

- [83] C. Zhao and Y. Guan. Data-driven risk-averse stochastic optimization with Wasserstein metric. Oper. Res. Lett., 46(2):262–267, 2018.