Out-of-distribution Robust Optimization

‡Rotman School of Management, University of Toronto, hansheng.jiang@rotman.utoronto.ca )

Abstract

In this paper, we consider the contextual robust optimization problem under an out-of-distribution setting. The contextual robust optimization problem considers a risk-sensitive objective function for an optimization problem with the presence of a context vector (also known as covariates or side information) capturing related information. While the existing works mainly consider the in-distribution setting, and the resultant robustness achieved is in an out-of-sample sense, our paper studies an out-of-distribution setting where there can be a difference between the test environment and the training environment where the data are collected. We propose methods that handle this out-of-distribution setting, and the key relies on a density ratio estimation for the distribution shift. We show that additional structures such as covariate shift and label shift are not only helpful in defending distribution shift but also necessary in avoiding non-trivial solutions compared to other principled methods such as distributionally robust optimization. We also illustrate how the covariates can be useful in this procedure. Numerical experiments generate more intuitions and demonstrate that the proposed methods can help avoid over-conservative solutions.

1 Introduction

Contextual optimization considers a constrained optimization problem with the presence of covariates (context), and it can be viewed as a prediction problem under an optimization context where the output of the prediction model serves as the objective function for the downstream optimization problem. The goal is to develop a model (trained from past data) that prescribes a decision/solution for the downstream optimization problem using the covariates directly but without observation of the objective function. It has been extensively studied in recent years under various settings (Hu et al., 2022; Elmachtoub and Grigas, 2022; Bertsimas and Kallus, 2020; Ho-Nguyen and Kılınç-Karzan, 2022; Chen and Kılınç-Karzan, 2020; Wilder et al., 2019; Sun et al., 2023b; Huang and Gupta, 2024), and we refer to Sadana et al. (2024) for a survey on the topic. In this paper, we consider the problem of contextual robust optimization where the objective function of the optimization problem becomes a risk-sensitive one. Unlike all existing works, we consider a distribution shift/out-of-distribution setting where the test environment is different from the training environment that generates the training dataset. In this sense, the notion of robustness goes beyond the existing scope and it also covers robustness against the distribution shift. To summarize, our contributions are as follows:

First, we formulate the problem of out-of-distribution robust optimization and propose a method that utilizes a density ratio estimate to make inferences about the test environment with data from the training environment.

Second, we derive theoretical guarantees for the proposed method and use an analytical example to illustrate the values of shift structure in avoiding over-conservative solutions.

Third, we conduct numerical experiments to generate more intuitions for the setup and illustrate the effectiveness of the proposed method.

Related Literature. The study of robust optimization has a long history which considers risk-sensitive objectives and approximate solutions using the notion of uncertainty set (see Ghaoui et al. (2003); Chen et al. (2007); Natarajan et al. (2008) among others). A recent line of works considers the contextual formulation for robust optimization Chenreddy et al. (2022); Sun et al. (2023a); Patel et al. (2024) which can be viewed as the case of no distribution shift within our framework. A separate line of works concerns the problem of distributionally robust optimization for conditional or contextual stochastic optimization problems, and various techniques have been proposed, including Esteban-Pérez and Morales (2022); Kannan et al. (2020); Bertsimas and Van Parys (2022). Treatment of distributional shift in this context is very scarce except for recent work by (Wang et al., 2024), which proposed to treat covariate shift by combining two estimators. Duchi et al. (2023) considered distribution shift in the form of the latent mixture under a DRO framework, but their focus is on loss functions rather than optimization. As for the literature on distribution shift, there are several streams: (i) Classification (label shift): Lipton et al. (2018) propose to correct for label shift in any predictors, but their method only applies to the classification setting, i.e., a finite number of labels; (ii) Regression (label shift): Zhang et al. (2013) handle continuous labels with the kernel mean matching approach; (iii) Covariate shift: Reweighting is a fundamental idea to address covariate shift, dating back to Shimodaira (2000). Covariate shift is also considered in the causal inference literature, typically caused by unobserved confounders Jin and Candès (2023).

2 Problem Setup

2.1 Robust Contextual LP

Consider a standard-form linear program (LP)

| (1) | ||||

| s.t. |

where and are the inputs of the LP, and is the decision variable. A more data-driven setting of LP considers the presence of some covariates (contextual information or side information), where there is a feature vector that contains some information related to the objective vector . In this way, the LP can be described by the tuple .

The statistical setup of contextual optimization considers the tuple drawn from some (unknown) distribution . As the setup of a machine learning problem, there is an available (training) dataset consisting of i.i.d. samples from ,

One utilizes the dataset to develop a model so that in the test phase, one needs to recommend a feasible solution to a new LP problem using only the observation of but without observing the objective vector . Here is a new tuple independently sampled from the distribution In terms of the objective, contextual optimization usually adopts a risk-neutral objective and aims to optimize (in the test phase)

| (2) | ||||

| s.t. |

where the conditional distribution is not known exactly (due to the unknown ) and has to be learned from the training data. The recommended decision variables in the test phase can be viewed as a function of .

Alternatively, one can consider a risk-sensitive (robust) objective

| (3) | ||||

| s.t. |

where is a pre-specified constant. Here denotes the -quantile/value-at-risk of a random variable . Specifically, with being the inverse cumulative distribution function of . For the objective (2), it concerns the conditional expectation of , while (3) involves the quantile of the conditional distribution

From the literature of robust optimization (Ben-Tal et al., 2009), we know that the problem (3) can be equivalently written as the following optimization problem

| (4) | ||||

| s.t. |

where the decision variables become , , and the uncertainty set . The last constraint ensures the coverage guarantee and corresponds to the quantile level ; the probability is taken with respect to the conditional distribution Due to the intractability of (4), people usually consider the following problem as an approximation

| (5) | ||||

| s.t. |

where , instead of being a decision variable, is a fixed uncertainty set satisfying . The uncertainty set ideally covers the high-density region so that the approximation to (3) is tighter.

2.2 Distribution Shift

For both the risk-neutral (2) and the risk-sensitive (3) settings, the existing works on contextual optimization and robust context optimization mainly consider an in-distribution setting where the training data is sampled from some unknown distribution , and the distribution remains unchanged from training to test. In this spirit, the so-called robustness of the existing methods is achieved against either (i) the statistical gap between the realized samples and the unknown or (ii) the intrinsic uncertainty underlying the distribution that causes the randomness of In this paper, we re-examine this classic problem of robust optimization from the perspective of robustness against distribution shift or an out-of-distribution setting. While such a robustness guarantee can only be achieved in a very conservative manner in the worst case, we demonstrate (i) how the covariates can be useful and (ii) how additional structure on the distribution shift can reduce the conservativeness.

In the last subsection, we define a joint distribution on the tuple . Throughout the remainder of this paper, we omit describing the distribution of the constraint and focus on the joint distribution of the objective-covariates pair . This is without loss of generality because the constraint is revealed when solving the LP during the test phase. In general, a distribution shift or an out-of-distribution setting refers to the case in which the test data distribution differs from the training data distribution. Specifically, we consider a training data

sampled from some unknown distribution Different from the in-distribution case, the sample of the test phase

where may be different from The standard setup of contextual optimization (for both risk-neutral objective (2) and risk-sensitive objective (3)) considers the case of , whereas an out-of-distribution robust optimization allows a setting where

In context-free robust optimization, if one adopts the approximation formulation (5), the task reduces to characterizing the randomness of from the observed samples . For contextual robust optimization, the task accordingly becomes characterizing the randomness of the conditional distribution When it comes to the out-of-distribution setting, it uses the samples from the training distribution to obtain a characterization of the conditional distribution under the test distribution Hence, people usually assume an additional dataset is available

where it contains samples from but only has the covariates but no corresponding An alternative setting includes also in the dataset . We consider this weaker setting for the full generality.

It is imaginable and will be illustrated in the later sections that such distribution shift from and cannot be resolved in a worst-case sense. Specifically, if is allowed to be arbitrarily different from , there is no way we can learn anything meaningful from dataset . In this sense, we consider two common structures as in the distribution shift literature: covariate shift and label shift.

Notation-wise, let denote the marginal distribution of and , and denote the conditional distribution of and . In this notation, We define and analogously. Throughout this paper, we assume all the distributions have density functions. Let and denote the marginal density of and under distribution , and denote the conditional density of . The corresponding densities for are defined analogously.

-

•

Covariate shift: The distribution of the covariates differs between and , while the conditional distribution remains the same. In other words, but .

-

•

Label shift: The distribution of the objective vector differs between and , while the conditional distribution remains the same. In other words, but .

In the following, we first state our algorithm in general and then specialize it into these two cases.

3 OOD Robust Optimization

Following the setup in the previous section, the goal of robust optimization under the test distribution is

| s.t. |

where the quantile function VaR is with respect to the conditional distribution of under . If one adopts the approximation scheme, it reduces to solving the following problem

| (6) | ||||

| s.t. |

where the uncertainty set satisfies , i.e., gives a coverage guarantee for the conditional distribution under Compared to the in-distribution problem (5), the formulation (6) replaces the requirement on the uncertainty set from to Then the task reduces to constructing an uncertainty set for the distribution using the data and Consequently, suppose we have a perfect knowledge of the distribution , then it only needs an estimate of the density ratio to convert our knowledge of into an estimate of the test distribution .

We formally define the density ratio between and as

for all where and are the density functions for and , respectively. We assume the density ratio is well-defined everywhere. In particular, for the case of covariate shift, the density ratio concerns only the marginal distribution over , i.e., . Generally, we need to estimate the ratio function from the data and The following algorithm takes an estimate as its input, and later in Section 3.3, we show how it can be estimated under the two settings of covariate shift and label shift.

3.1 Algorithm

Algorithm 1 describes our main algorithm for OOD robust optimization. It takes the training data and the target quantile level as inputs. Also, it requires a prediction model for the conditional expectation and a density ratio estimate . The prediction model can be built based on some other available history data or using part of the training data . The predicted vector from this determines the center of the uncertainty set

The algorithm consists of two parts. The first part gives a coarse prediction of the quantiles of the conditional distribution It does not have to be accurate or even consistent. In the second part, we use both the expectation prediction model and the quantile prediction model to construct a variable-sized uncertainty set. The uncertainty set is box-shaped and it is controlled by a scalar variable Step 12 in Algorithm 1 is crucial for determining the size of the uncertainty set. In this step, it utilizes the estimated density ratio to re-weight the training samples in . The re-weighting adjusts the original uniform weight over all the training samples in and assigns a weight to each sample to reflect its density in the test distribution . Intuitively, step 8 ensures an empirical coverage of the samples over the test distribution pretending the density ratio estimate is precise.

| (7) |

| (8) |

We make a few remarks on the algorithm. First, the output uncertainty set from the algorithm is contextualized and depends on the covariates , with the benefits of contextual uncertainty set are illustrated in the existing literature (Goerigk and Kurtz, 2020; Chenreddy et al., 2022; Sun et al., 2023a). Second, we note that the algorithm utilizes the idea from the recent literature on conformal prediction to adjust the size of the uncertainty set. Such usage of conformal prediction in robust optimization and inverse optimization have appeared in several recent works (Sun et al., 2023a; Patel et al., 2024; Lin et al., 2024; Cao, 2024). The main advantage of using this conformal control is to obtain a coverage guarantee for the uncertainty set without imposing any assumptions/structures on the prediction models and Third, our re-weighting scheme (8) is a natural treatment and it mimics the existing literature on uncertainty calibration and conformal prediction (Tibshirani et al., 2019; Podkopaev and Ramdas, 2021). Moreover, we note that the inputs of the algorithm require only the training data but not the test data The test data contributes only to the construction of the density ratio estimate , while Algorithm 1 does not directly involve the test data. Lastly, we note the algorithm provides just a pipeline to solve the out-of-distribution robust optimization; many of its components, say, the density ratio estimate, the prediction model , and the learning of the quantile, are unrestricted in choice and can be substituted with other candidate methods.

3.2 Algorithm Analysis

Now we derive a guarantee for Algorithm 1 under the following assumption.

Assumption 1.

We assume that the estimated density ratio is uniformly bounded from below and above. That is, there exists and such that

for all .

We note this assumption is rather mild in that it concerns the estimated density ratio but not the true density ratio . Such a condition can always be met by truncating the estimated density ratio. Boundedness of the true density ratio is also a common assumption adopted in the literature (Kpotufe, 2017; Ma et al., 2023).

Theorem 1.

Theorem 1 considers the case when the density ratio estimate is precise. Under this condition, the performance guarantee holds and the right-hand side scales at a favorable rate as the number of samples in of Algorithm 1 increases. We emphasize that the algorithm utilizes samples from the training distribution to construct the uncertainty set but the performance guarantee is with respect to the test distribution This tells that the out-of-distribution robustness is well achievable under a perfect knowledge of density ratio.

When the density ratio estimate is not perfect, one can also obtain a slightly weaker guarantee. To proceed, let denote the estimated test distribution defined by the following density function

| (9) |

With this definition, the following corollary extends Theorem 1 to the case when the density ratio estimate is not fully accurate.

Corollary 1.

Let denote a distribution with a density function given by (9), then under Assumption 1, the uncertainty set generated by Algorithm 1 satisfies the following guarantee,

where the probability on the left-hand-side is with respect to and . Here denotes the total variation distance between two distributions.

Corollary 1 provides a natural extension that includes an extra term in the bound of Theorem 1. When the density ratio estimate is perfect, and this extra term disappears. At the other end of the spectrum, if one adopts a trivial density estimate where this term becomes which is the distance between the training distribution and the test distribution. In this light, the bound shows the benefits of having a good density ratio estimate; and any reasonable density estimate will always bring a better performance guarantee than the naive treatment of which ignores the distribution shift between and The two terms on the right-hand-side correspond to two “orthogonal” sources of errors: the first one captures the uncertainty calibration error when there is no distribution shift, and the second one captures the error of density ratio estimation.

We note that for the performance guarantees in both Theorem 1 and Corollary 1, they are in a marginal sense, not a conditional sense. In other words, they hold “on average” for all possible covariates . To obtain a conditional coverage guarantee that holds for each possible requires additional assumptions and treatments even for the in-distribution setting (see (Kannan et al., 2022; Sun et al., 2023a) among others). It will be accordingly more challenging for an out-of-distribution setting, which we leave for future investigation. Numerically, as the construction of the quantile prediction (in part 1 of Algorithm 1) is in a conditional sense, we usually observe a conditional coverage empirically.

3.3 Density Ratio Estimation for Covariate Shift and Lable Shift

Algorithm 1 takes a density ratio estimate as input. Here we describe how such estimate can be obtained under covariate shift and label shift.

Covariate Shift. We briefly describe the probabilistic classification approach proposed by Bickel et al. (2009). Intuitively, consider a random sample drawn from a mixture distribution of and . With equal probability, is either drawn from or from . If is drawn from , it is assigned a label , and if it is drawn from , it is assigned a label . Note that the following equation holds

This indicates that if we train a probability classifier that predicts the label based on , then the oracle classifier gives .

We can obtain a density ratio estimate based on this observation. First, we pool the covariates from both and . We assign a label if is from and if is from . Then, we learn a probability classifier (can be an ML model) so that . The density ratio can then be given by

Label Shift. Most of the existing literature on density ratio estimation under the label shift setting focuses on the classification task where the domain for the target variable is a discrete space. However, the cost vectors ’s in contextual optimization problems are continuous vectors. We can adopt the kernel mean matching approach introduced in Zhang et al. (2013). A brief introduction to the reproductive kernel Hilbert space (RKHS) and kernel mean match (KMM) is deferred to Appendix A.1. Let and be RKHS’s, with and denoting the respective feature maps. The kernel mean embedding operators are defined as

Define the conditional embedding operator as , where and denote the cross-covariance operators (Fukumizu et al., 2004). Based on the property that

the following equation holds under the label shift assumption: The main idea then is to estimate the density ratio with such that the estimated test distribution satisfies . Following the empirical estimators given in Appendix A.3, the loss to minimize can be written as

The estimate can then be chosen from a function family that minimizes the above loss.

4 Values of Shift Structure

In this section, we use an analytical example to show that the structure of covariates shift and label shift is helpful in avoiding over-conservative solutions. Consider the following linear program.

| (10) |

where . For the training distribution , with and independently sampled from and . Under this example, the ideal solution would be if the coverage guarantee can be met. An over-conservative solution will give . In the following, we analyze the problem under covariate shift and label shift.

Covariate Shift.

We introduce a scalar to represent the extent of the distribution shift. Under the covariate shift setting, the test distribution of follows , while the distribution of remains unchanged. Hence the conditional distribution of remains to be . The joint distribution of is shifted from to . We consider an idealized setting where the density ratio estimation is perfect and the distribution is known. Under this case, the solution of Algorithm 1 to (10) takes the following form

| (11) |

where is with respect to the test distribution . The probability of yielding a conservative solution can be calculated by

| (12) | ||||

where is the cumulative distribution function of a standard normal distribution.

Alternatively, one can take a worst-case approach by considering the following set of distributions which we call as worst-case ball:

where the set is centered at the training distribution Such a distribution set is commonly considered in distributionally robust optimization and we can accordingly formulate the robust optimization problem as

| (13) |

To make the set cover the test distribution , we need to have . Accordingly, we can solve (13) and obtain the following:

| (14) |

where for any we define

and the probability of an overly conservative solution under this worst-case ball framework (13) equals

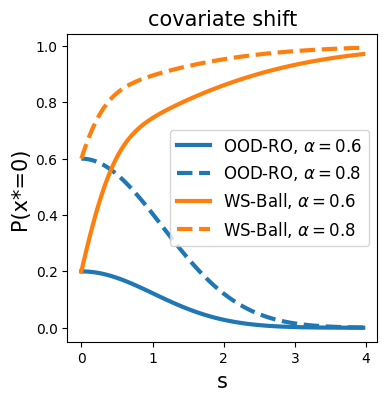

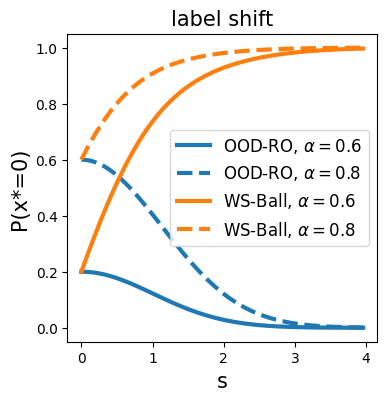

We can do the same calculation for the case of label shift, where the details are deferred to Appendix B. Figure 1 summarizes the two cases to compare our approach (which accounts for the shift structure) against the worst-case ball approach under two target quantile levels and . For both cases, as increases, the mean of the covariate and the objective becomes more and more positive. If we utilize this structure and also the information from the covariate, we should be able to take a more aggressive decision by setting ; this corresponds to the small probability of for our approach. However, if we do not take advantage of this shift structure, the worst-case ball has to be very large to cover the test distribution, and then a worst-case solution will result in a more and more conservative solution even as increases. This corresponds to the case in Corollary 1 if one adopts the naive density ratio , the right-hand-side will have a term of

5 Experiments

In this section, we illustrate the performance of our proposed algorithm via one simple example. More experiments are deferred to Appendix C. Continue with problem (10), but instead of considering a single-dimensional , set a multi-dimensional covariate . Let

and are independent. The training distribution of and are and respectively (let denote a zero vector of dimension , and an identity matrix of dimension ). Covariate shift occurs in the test phase, where the mean of is shifted from to (let denote a -dimensional vector with all components equaling ),

We study the performance of Algorithm 1 under different implementations of , , and , as listed below. All neural networks used in this experiment are feed-forward networks with one hidden layer of neurons. We consider the following setups. Prediction models : Lasso, random forest (“RF”), and neural network (“NN”). Quantile prediction models : linear quantile regression (“Linear”), gradient boosting regression (“GBR”), and neural network. Density ratio estimators : the trivial estimator (“Trivial”, ), the kernel mean matching method (“KMM”, (Gretton et al., 2008)), and the probabilistic classification method (“Cls-NN”, (Bickel et al., 2009)).

The risk level . The training dataset contains randomly generated samples, with of them used for learning , for learning , and for confidence adjustment. The test data contains samples from the shifted test distribution, with of them used to learn the density ratio estimator, and of them for evaluating the algorithm’s final performance. Unless otherwise stated, the default covariate dimension is . We present the main results of our experiment below, with further details and additional experimental results provided in Appendix C.

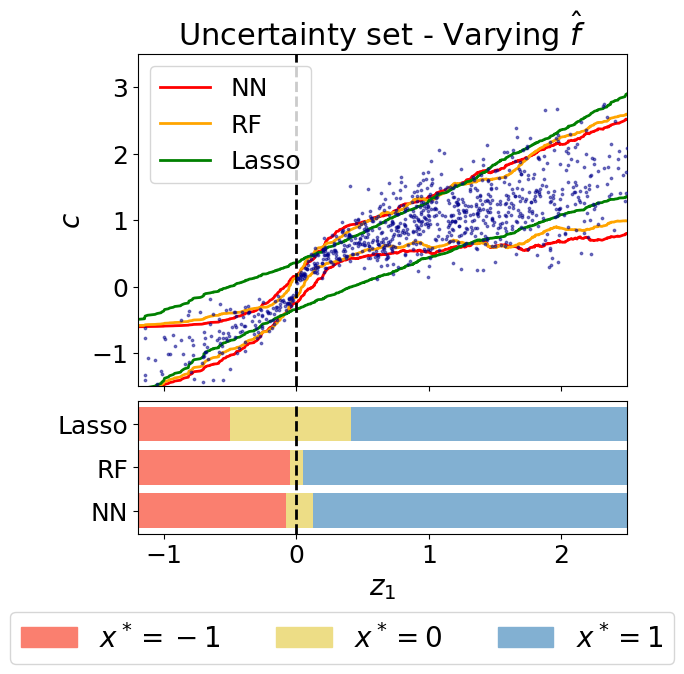

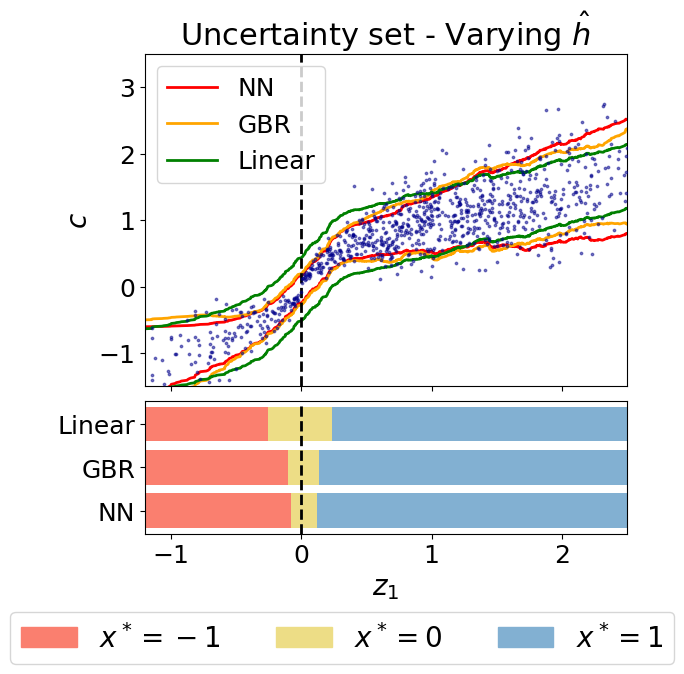

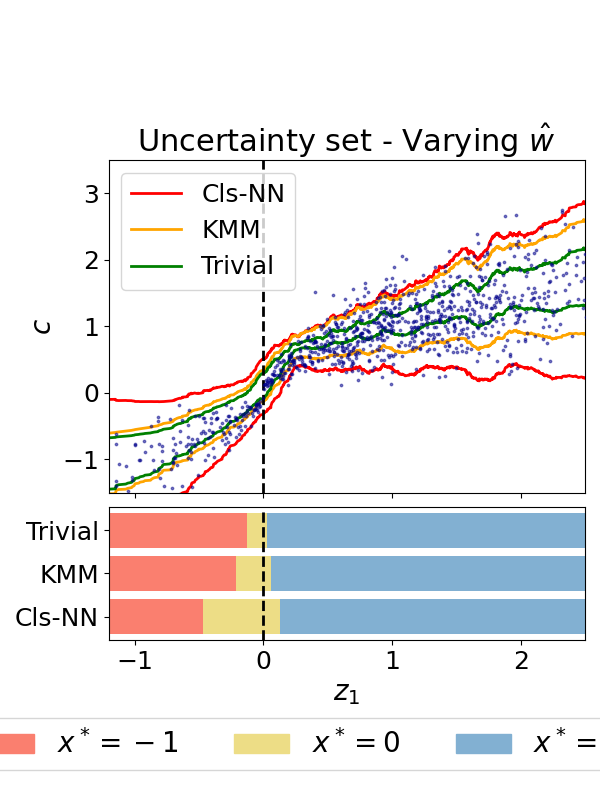

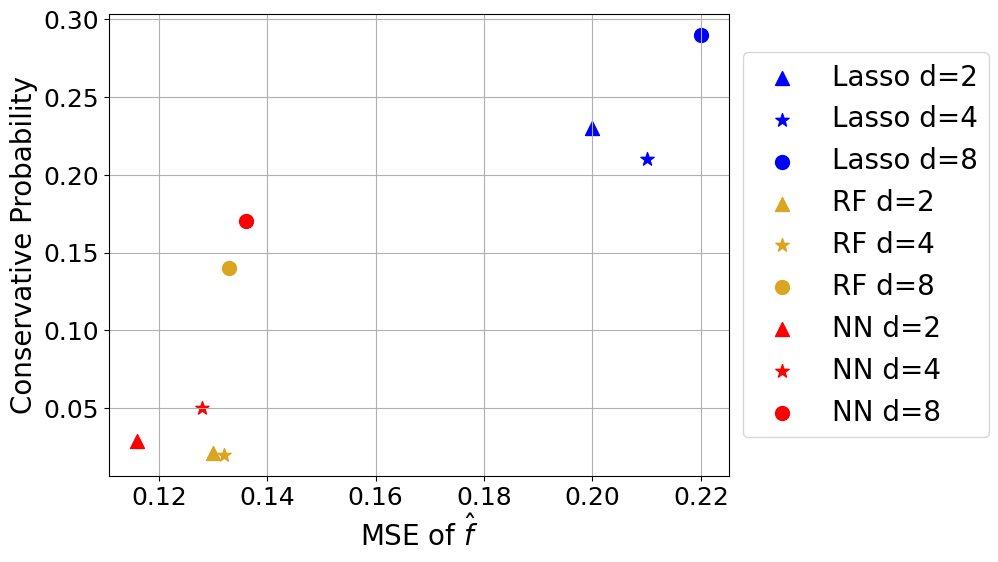

Prediction Models Boost Performance: In Figure 2, Algorithm 1 is evaluated under different implementations of and . The default configuration uses neural networks for and , and probabilistic classification for . Except for the function component explicitly studied in the experiment, all other components follow the default configuration. Compared to the rest of the benchmarks, the neural network usually gives a better prediction, and Figure 2 demonstrates that this reduces the probability of getting a conservative solution . In Appendix C, we further show that neural networks give more precise predictions and that the probability of being conservative is positively correlated with the mean squared error of the prediction models.

Density Ratio Estimator Avoids Mis-coverage: Now we illustrate the role of the density ratio estimator . The left panel of Figure 3 demonstrates the algorithm’s performance under different . The figure indicates that, if no reweighting is applied (i.e. “Trivially” estimate the density ratio to be ), the empirical coverage rate can significantly drop below . A potentially misleading observation from the bar chart is that a “Trivial” estimator appears to be less conservative than its counterparts. However, as discussed above, this deceptive advantage is achieved at the cost of violating the coverage guarantee. The table on the right panel of Figure 3 reinforces the importance of a reliable density ratio estimator. By observing the “Total” rows of KMM and Cls-NN under different settings of the covariate dimension, we point out that a reliable density ratio estimator maintains the empirical coverage rate to be close to , even when the prediction models are poor. Another observation is that the coverage guarantee is approximately achieved in a conditional sense: after splitting the domain of into two groups, with “” being a minority group and “” being major, the empirical coverage rate remains approximately for both groups.

| Trivial | KMM | Cls-NN | ||

|---|---|---|---|---|

| 0.80 | 0.77 | 0.79 | ||

| 0.78 | 0.75 | 0.77 | ||

| Total | 0.78 | 0.75 | 0.78 | |

| 0.56 | 0.72 | 0.79 | ||

| 0.54 | 0.86 | 0.81 | ||

| Total | 0.55 | 0.84 | 0.81 | |

| 0.53 | 0.71 | 0.86 | ||

| 0.4 | 0.76 | 0.81 | ||

| Total | 0.42 | 0.75 | 0.83 |

Discussions. In this paper, we study an out-of-distribution setting of robust optimization where the training distribution might be different from the test distribution Other than the method, the analysis, and the numerical experiments, we hope such a study calls for more attention to the meaning of robustness in the context of robust optimization. As noted earlier, existing works consider mainly (i) robustness against the statistical gap between the empirical distribution supported on and the true distribution or (ii) the robustness of a risk-sensitive objective such as VaR. Comparatively, the setting we study can be viewed as a robustness against distribution shift. Along this path, one may also consider the adversarial robustness where there might be a proportion of samples in the training data contaminated or adversarially generated from the other distributions than . We believe the study of such more general notions of robustness deserves more future works.

References

- Baker [1973] Charles R. Baker. Joint measures and cross-covariance operators. Transactions of the American Mathematical Society, 186:273–289, 1973. ISSN 00029947.

- Ben-Tal et al. [2009] Aharon Ben-Tal, Laurent El Ghaoui, and Arkadi Nemirovski. Robust optimization, volume 28. Princeton university press, 2009.

- Bertsimas and Kallus [2020] Dimitris Bertsimas and Nathan Kallus. From predictive to prescriptive analytics. Management Science, 66(3):1025–1044, 2020.

- Bertsimas and Van Parys [2022] Dimitris Bertsimas and Bart Van Parys. Bootstrap robust prescriptive analytics. Mathematical Programming, 195(1-2):39–78, 2022.

- Bickel et al. [2009] Steffen Bickel, Michael Brückner, and Tobias Scheffer. Discriminative learning under covariate shift. Journal of Machine Learning Research, 10(9), 2009.

- Cao [2024] Guyang Kevin Cao. Non-Parameteric Conformal Distributionally Robust Optimization. PhD thesis, University of Michigan, 2024.

- Chen and Kılınç-Karzan [2020] Violet Xinying Chen and Fatma Kılınç-Karzan. Online convex optimization perspective for learning from dynamically revealed preferences. arXiv preprint arXiv:2008.10460, 2020.

- Chen et al. [2007] Xin Chen, Melvyn Sim, and Peng Sun. A robust optimization perspective on stochastic programming. Operations Research, 55(6):1058–1071, 2007.

- Chenreddy et al. [2022] Abhilash Reddy Chenreddy, Nymisha Bandi, and Erick Delage. Data-driven conditional robust optimization. Advances in Neural Information Processing Systems, 35:9525–9537, 2022.

- Duchi et al. [2023] John Duchi, Tatsunori Hashimoto, and Hongseok Namkoong. Distributionally robust losses for latent covariate mixtures. Operations Research, 71(2):649–664, 2023.

- Elmachtoub and Grigas [2022] Adam N Elmachtoub and Paul Grigas. Smart "predict, then optimize". Management Science, 68(1):9–26, 2022.

- Esteban-Pérez and Morales [2022] Adrián Esteban-Pérez and Juan M Morales. Distributionally robust stochastic programs with side information based on trimmings. Mathematical Programming, 195(1-2):1069–1105, 2022.

- Fukumizu et al. [2004] Kenji Fukumizu, Francis R Bach, and Michael I Jordan. Dimensionality reduction for supervised learning with reproducing kernel hilbert spaces. Journal of Machine Learning Research, 5(Jan):73–99, 2004.

- Ghaoui et al. [2003] Laurent El Ghaoui, Maksim Oks, and Francois Oustry. Worst-case value-at-risk and robust portfolio optimization: A conic programming approach. Operations Research, 51(4):543–556, 2003.

- Goerigk and Kurtz [2020] Marc Goerigk and Jannis Kurtz. Data-driven robust optimization using unsupervised deep learning. arXiv preprint arXiv:2011.09769, 2020.

- Gretton et al. [2008] Arthur Gretton, Alex Smola, Jiayuan Huang, Marcel Schmittfull, Karsten Borgwardt, and Bernhard Schölkopf. Covariate shift by kernel mean matching. 2008.

- Ho-Nguyen and Kılınç-Karzan [2022] Nam Ho-Nguyen and Fatma Kılınç-Karzan. Risk guarantees for end-to-end prediction and optimization processes. Management Science, 68(12):8680–8698, 2022.

- Hu et al. [2022] Yichun Hu, Nathan Kallus, and Xiaojie Mao. Fast rates for contextual linear optimization. Management Science, 68(6):4236–4245, 2022.

- Huang et al. [2006] Jiayuan Huang, Arthur Gretton, Karsten Borgwardt, Bernhard Schölkopf, and Alex Smola. Correcting sample selection bias by unlabeled data. Advances in neural information processing systems, 19, 2006.

- Huang and Gupta [2024] Michael Huang and Vishal Gupta. Learning best-in-class policies for the predict-then-optimize framework. arXiv preprint arXiv:2402.03256, 2024.

- Jin and Candès [2023] Ying Jin and Emmanuel J Candès. Model-free selective inference under covariate shift via weighted conformal p-values. arXiv preprint arXiv:2307.09291, 2023.

- Kannan et al. [2020] Rohit Kannan, Güzin Bayraksan, and James R Luedtke. Residuals-based distributionally robust optimization with covariate information. arXiv preprint arXiv:2012.01088, 2020.

- Kannan et al. [2022] Rohit Kannan, Güzin Bayraksan, and James R Luedtke. Data-driven sample average approximation with covariate information. arXiv preprint arXiv:2207.13554, 2022.

- Kpotufe [2017] Samory Kpotufe. Lipschitz density-ratios, structured data, and data-driven tuning. In Artificial Intelligence and Statistics, pages 1320–1328. PMLR, 2017.

- Lin et al. [2024] Bo Lin, Erick Delage, and Timothy CY Chan. Conformal inverse optimization. arXiv preprint arXiv:2402.01489, 2024.

- Lipton et al. [2018] Zachary Lipton, Yu-Xiang Wang, and Alexander Smola. Detecting and correcting for label shift with black box predictors. In International conference on machine learning, pages 3122–3130. PMLR, 2018.

- Ma et al. [2023] Cong Ma, Reese Pathak, and Martin J Wainwright. Optimally tackling covariate shift in rkhs-based nonparametric regression. The Annals of Statistics, 51(2):738–761, 2023.

- Natarajan et al. [2008] Karthik Natarajan, Dessislava Pachamanova, and Melvyn Sim. Incorporating asymmetric distributional information in robust value-at-risk optimization. Management Science, 54(3):573–585, 2008.

- Ohmori [2021] Shunichi Ohmori. A predictive prescription using minimum volume k-nearest neighbor enclosing ellipsoid and robust optimization. Mathematics, 9(2):119, 2021.

- Patel et al. [2024] Yash P Patel, Sahana Rayan, and Ambuj Tewari. Conformal contextual robust optimization. In International Conference on Artificial Intelligence and Statistics, pages 2485–2493. PMLR, 2024.

- Podkopaev and Ramdas [2021] Aleksandr Podkopaev and Aaditya Ramdas. Distribution-free uncertainty quantification for classification under label shift. In Uncertainty in artificial intelligence, pages 844–853. PMLR, 2021.

- Sadana et al. [2024] Utsav Sadana, Abhilash Chenreddy, Erick Delage, Alexandre Forel, Emma Frejinger, and Thibaut Vidal. A survey of contextual optimization methods for decision-making under uncertainty. European Journal of Operational Research, 2024.

- Shimodaira [2000] Hidetoshi Shimodaira. Improving predictive inference under covariate shift by weighting the log-likelihood function. Journal of statistical planning and inference, 90(2):227–244, 2000.

- Song et al. [2009] Le Song, Jonathan Huang, Alex Smola, and Kenji Fukumizu. Hilbert space embeddings of conditional distributions with applications to dynamical systems. In Proceedings of the 26th Annual International Conference on Machine Learning, pages 961–968, 2009.

- Steinwart [2002] Ingo Steinwart. Support vector machines are universally consistent. Journal of Complexity, 18(3):768–791, 2002.

- Sun et al. [2023a] Chunlin Sun, Linyu Liu, and Xiaocheng Li. Predict-then-calibrate: A new perspective of robust contextual lp. Advances in Neural Information Processing Systems, 36:17713–17741, 2023a.

- Sun et al. [2023b] Chunlin Sun, Shang Liu, and Xiaocheng Li. Maximum optimality margin: A unified approach for contextual linear programming and inverse linear programming. In International Conference on Machine Learning, pages 32886–32912. PMLR, 2023b.

- Tibshirani et al. [2019] Ryan J Tibshirani, Rina Foygel Barber, Emmanuel Candes, and Aaditya Ramdas. Conformal prediction under covariate shift. Advances in neural information processing systems, 32, 2019.

- Wang et al. [2024] Tianyu Wang, Ningyuan Chen, and Chun Wang. Contextual optimization under covariate shift: A robust approach by intersecting wasserstein balls. arXiv preprint arXiv:2406.02426, 2024.

- Wilder et al. [2019] Bryan Wilder, Bistra Dilkina, and Milind Tambe. Melding the data-decisions pipeline: Decision-focused learning for combinatorial optimization. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 1658–1665, 2019.

- Zhang et al. [2013] Kun Zhang, Bernhard Schölkopf, Krikamol Muandet, and Zhikun Wang. Domain adaptation under target and conditional shift. In International Conference on Machine Learning, pages 819–827. PMLR, 2013.

Appendix A Reproductive Kernel Hilbert Space and Kernel Mean Matching

A.1 RKHS

Let the tuple denote a reproductive kernel Hilbert space (RKHS) on the sample space with kernel . The RKHS is a Hilbert space of functions , on which the inner product satisfies the reproducing property:

That said, the evaluation of function on a single point can be viewed as an inner product between function and the evaluation operator . We define the feature map by . Throughout this part, we will use the square bracket to denote mappings to functional spaces. Based on the reproducing property, the feature map satisfies for all .

The kernel mean embedding of a probability distribution [Zhang et al., 2013], denoted by , is a mapping from the space of all the probability distributions on to . The mapping is given by

The kernel is called characteristic if the kernel mean embedding is injective: for , it holds that . And following Huang et al. [2006], the operator is bijective if is a universal kernel in the sense of Steinwart [2002]. The core idea of the kernel mean matching is estimate with a satisfying .

A.2 Cross-covariance Operator

Consider the joint random variable . Define two RKHS’s by and respectively. Let denote the joint distribution of and their marginal distributions respectively, then the cross-covariance operator (with the dependency on omitted) is defined as [Baker, 1973]

In the following, we will omit the explicit distribution of the random variable in the subscript of and replace expressions like with . The operator can be viewed as a mapping from to in the following way: by noting that for any , we can define as

For any functions and , the cross-covariace operator has the following property:

which exactly corresponds to the covariance between and . The conditional embedding operator is a mapping from to such that, for any , the follow equation holds:

| (15) |

In other words, maps the feature map to the kernel mean embedding of the conditional distribution . Following Song et al. [2009], if the cross-covariance operator is invertible, by defining

the equation (15) is satisfied. To see this, it is sufficient to show that for all , and this holds following the derivations below,

Equation (15) directly implies the following property, which serves as the key step of the KMM procedure in the density ratio estimation method of Zhang et al. [2013]:

A.3 Empirical Estimations

In this section, we briefly outline how to estimate the quantities above using i.i.d. samples drawn from . By Mercer’s theorem, the feature map can be represented as a column vector in a (possibly infinite-dimensional) Hilbert space. We use to denote the outer product . Define the matrices and . Further define with and . The empirical estimators are indicated by adding a hat symbol to the original quantities, with their explicit expressions shown below:

Appendix B Illustrative Example

Consider the illustrative example:

| (16) |

where and . In the training distribution , the and are independent and respectively follow and . We list the explicit expressions for the following probability distributions:

We describe the explicit form of under the following two distribution shift scenarios:

-

•

Covariate shift: let represent the extent of covariate shift. The distribution of is shifted from to , while the conditional distribution of remains to be . The joint distribution of is shifted to .

-

•

Label shift: let represent the extent of label shift. The distribution of is shifted from to , while the conditional distribution remains to be . It follows that the distribution of in is shifted to , and the distribution of is shifted to . The joint distribution of is shifted to .

The solution to (16) admits a simple form under the idealized setting, as given in (11) and restated below:

| (17) |

The probability of yielding an over-conservative solution is

| (18) |

Specifically, in the covariate shift setting, the probability equals

and in the label shift setting, the probability also equals

Worst-case Approach

Alternative to our density ratio-based approach is the worst-case approach. Construct the worst-case ball:

Following the discussions in the main context, the objective of the worst-case approach is given by (13) and restated below:

The probability of yielding an over-conservative solution is

In the covariate shift setting, we have in order that covers . In the label shift setting, . The explicit form of the conservative probability is

for the covariate shift setting and

for the label shift setting.

Figure 1 is plotted by setting .

Appendix C More Experiments and Experiment Details

We consider several implementations of the three components: , and for our Algorithm 1. For the expectation predictor which predicts with , we consider using Lasso regression, random forest, and neural network. On different training datasets, the regularization parameter of the Lasso regression is selected as the optimal parameter in range ; for the random forest searches the best number of trees in range and the best depth in range ; the neural network has a single middle layer with neurons, with the learning rate set to and the training epochs set to . For the quantile predictor , we implement linear quantile regression, gradient boosting regression, and neural network, all trained by minimizing the quantile loss. For the density estimator, we mainly consider estimators for the covariate shift setting, including the trivial estimator, the kernel mean matching method introduced in Gretton et al. [2008], and the probabilistic classification method introduced in Bickel et al. [2009]. The computational complexity of the kernel mean matching method scales at least quadratically with the data size, so we only sample data from the training distribution and data from the test distribution to run the algorithm.

The performance metrics we consider include the coverage rate and the -quantile of the objective . Specifically, we evaluate the marginal and conditional coverage rates of the uncertainty sets generated from different implementations of our algorithm, and how different they are from the target coverage rate. The -quantile of the objective, denoted by , is evaluated by generating samples of from the underlying conditional distribution and then calculate the empirical -quantile of .

C.1 Additional Experiments on the Simple Example

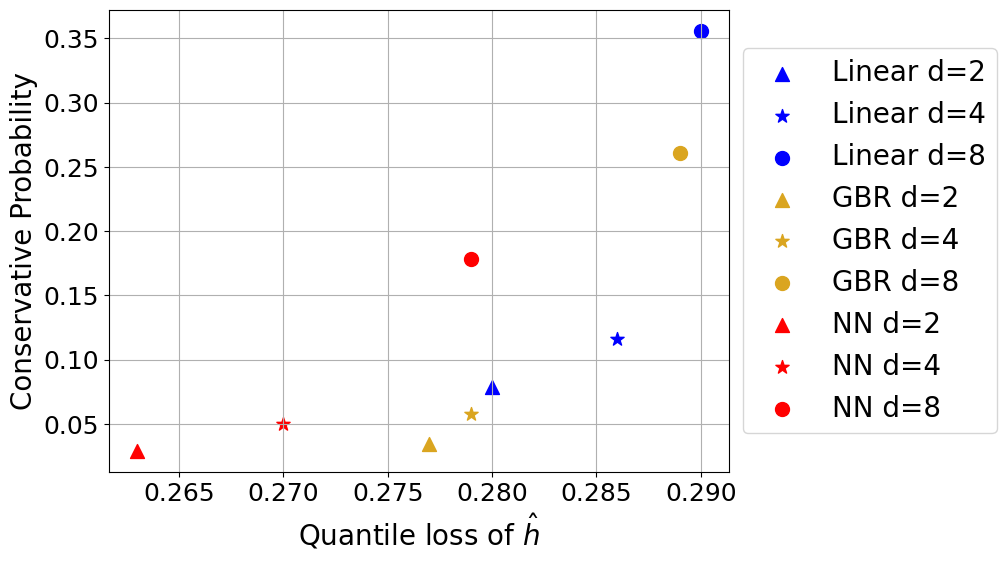

This section presents additional experimental results for the simple optimization problem discussed in Section 5. In Figure 4, we experiment with different choices of and , and different covariate dimensions . Specifically, the implementations of and follow the setup of Figure 2, and the ’s we consider include . Both the mean squared error and the quantile loss are evaluated on the test dataset, with the values known. The results indicate that the algorithm tends to perform better, as reflected by a lower conservative probability, when the prediction models and have lower prediction errors. Further, for both and , neural networks (NN) generally achieve strong predictive performance.

C.2 Shortest Path Problem and Fractional Knapsack Problem

We test our algorithm on two practical LP settings. The risk level is fixed to and we consider the covariate shift of the test distribution.

The shortest path problem seeks a path between two vertices in a weighted graph such that the total accumulated cost along the path’s edges is minimized. Specifically, we consider the shortest path problem on a grid with nodes and edges. The objective is to find the shortest path from the top-left node to the bottom-right node. For and , let denote the node on the -th row and -th column, with the top-left node located at the coordinate and the bottom-right node at the coordinate . The tuple denotes the edge between node and . Let denote the set of all nodes and denote all edges. For , use to represent the cost of the edge (for the undirected graph that we consider, set ). The decision variables are for all , where denotes a directed path segment from the node to the node . The shortest path problem then has the following risk-sensitive LP formulation:

| (19) | ||||

| s.t. |

Extending to the OOD robust formulation, we assume that the dynamic of the cost vector is controlled by the covariate (we fix in this experiment) through

where is a 0-1 matrix with each entry generated independently from a distribution. The matrix is fixed once it is generated. The symbol denotes an elementwise multiplication. Each element of the random vector is generated independently from . In the training data, the covariate is generated from , and in the test data is generated from . The objective of the OOD formulation replaces the part in (19) with .

The fractional knapsack problem models the case where customers select items that maximize their utility, under a budget constraint. We consider a simple setting with items. The decision variables denote the fractions (in range ) of items to purchase, denote the item utilities, denote the price of items, and the total budget. The fractional knapsack problem has the following risk-sensitive LP formulation:

| (20) | |||||

| s.t. | |||||

The OOD robust formulation considers covariate (with ) and assumes the conditional distribution of to be

where is a 0-1 matrix with each entry generated independently from a distribution. Each element of is generated independently from . The training distribution of the covariate is and the test distribution is .

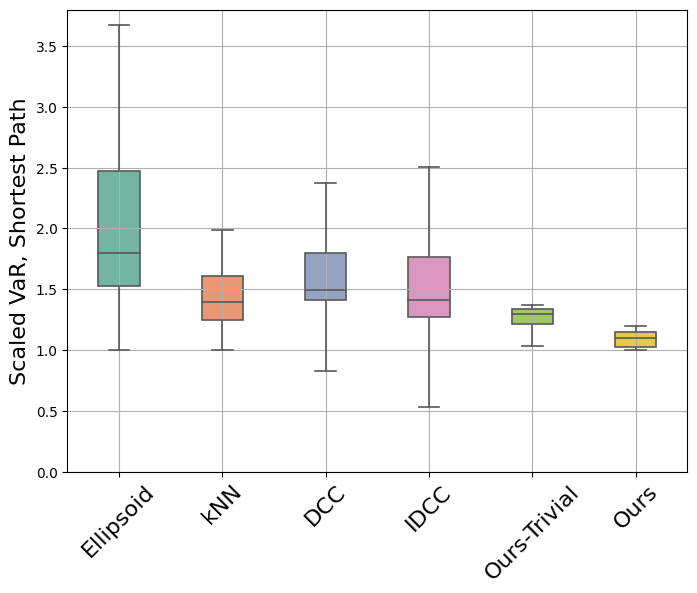

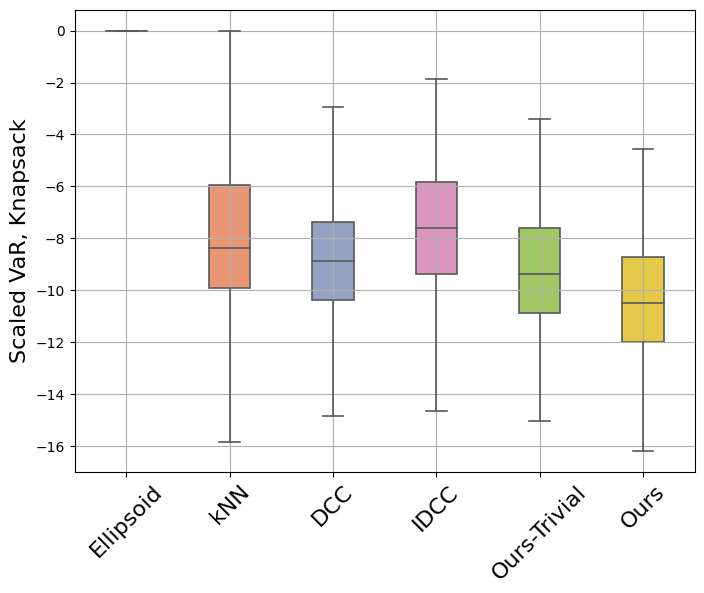

In Figure 5, we compare our algorithm against multiple benchmarks on the two LP settings above. As there is no existing algorithm that handles covariate shift in the risk-sensitive setting, we just implement the existing benchmark methods and evaluate them in the test environment. The “Ellipsoid” method ignores the contextual information and calibrates the ellipsoid to achieve an empirical coverage rate of on the training samples. The “DCC” and “IDCC” algorithms are proposed in Chenreddy et al. [2022]. The “NN” algorithm is a conditional robust optimization method proposed in [Ohmori, 2021]. The “Ours-Trivial” and “Ours” both implement our Algorithm 1 (with and being neural networks). “Ours-Trivial” sets a trivial density ratio estimator , while “Ours” uses the probabilistic classification method (which is shown to enjoy the best performance based on the previous experiments) to estimate . The result demonstrates that our algorithm generally outperforms the rest benchmarks, and leveraging the density ratio information further improves the performance on the test dataset.

Appendix D Proof of Theorems

D.1 Proof of Theorem 1

Let and define for . The final term produced from Algorithm 1 is a function of , which we define below as the function

For each , let denote the minimum such that covers . The function is formally defined below

Under this new notation, the form of can be formulated as

Further, if the density ratio estimate in Algorithm 1 is perfect, then the event is equivent to . We restate Theorem 1 below and provide a proof.

Theorem D.1.

Proof.

Since the distributions and are continuous, almost surely the samples are mutually distinct. Let denote an unordered set (e.g. denotes an unordered set containing distinct elements ). Then the following equation holds:

| (21) | ||||

The integration is over all possible sets of distinct elements, denoted by . The remaining part of the proof uniformly bounds the term for all sets .

Given a set , let denote the event that , and let denote the event that and . The term can be decomposed by the following chain of equations:

| (22) | ||||

where is from the fact that is invariant to the permutation of , and is by that

and .

We now characterize the terms . Without loss of generality, let , then

| (23) | ||||

The last line of (23) has the following bounds:

| (24) |

Combining (22), (23) and (24), the term is uniformly bounded:

Plugging the bounds above into (21) finishes the proof.

∎

D.2 Proof of Corollary 1

By defining the estimated test distribution as a distribution with the following density function:

we could directly apply Theorem 1 to see that

| (25) |

where the probability is with respect to and . From the definition of the total variation distance, the following inequality holds:

| (26) |

where is with respect to and . Combining (25) and (26) gives the result of Corollary 1, which we restate below: