An efficient numerical method for American options and their Greeks under the two-asset Kou jump-diffusion model

Abstract

In this paper we consider the numerical solution of the two-dimensional time-dependent partial integro-differential complementarity problem (PIDCP) that holds for the value of American-style options under the two-asset Kou jump-diffusion model. Following the method of lines (MOL), we derive an efficient numerical method for the pertinent PIDCP. Here, for the discretization of the nonlocal double integral term, an extension is employed of the fast algorithm by Toivanen [29] in the case of the one-asset Kou jump-diffusion model. For the temporal discretization, we study a useful family of second-order diagonally implicit Runge–Kutta (DIRK) methods. Their adaptation to the semidiscrete two-dimensional Kou PIDCP is obtained by means of an effective iteration introduced by d’Halluin, Forsyth & Labahn [7] and d’Halluin, Forsyth & Vetzal [8].

Ample numerical experiments are presented showing that the proposed numerical method achieves a favourable, second-order convergence behaviour to the American two-asset option value as well as to its Greeks Delta and Gamma.

1 Introduction

American-style options are widely traded derivatives in the financial markets due to their inherent flexibility of early exercise. For the evolution of the underlying asset prices, jump-diffusion processes constitute a principal class of models, see e.g. Cont & Tankov [6] and Schoutens [27]. Hence, it is of main importance to know the fair values of American-style options, together with their Greeks, under jump-diffusion models.

In this paper we shall deal with American-style options on two underlying assets. Here a direct generalization of the popular Kou jump-diffusion model for a single asset [22] to two assets is considered, where the finite-activity jumps in the two asset prices are assumed to occur simultaneously and the relative jump sizes possess log-double-exponential distributions.

In general, expressions in (semi-)closed analytical form are lacking in the literature for the fair values of American options and their Greeks. Accordingly, there is a big demand for effective approximation methods for these quantities. In the present paper, we shall consider their approximation via the numerical solution of the pertinent two-dimensional time-dependent partial integro-differential complementarity problem (PIDCP). Here the integral part stems from the contribution of the jumps and is nonlocal: the domain of integration is the whole first quadrant in the real plane.

For the numerical solution we follow the well-known and versatile method of lines (MOL). Here the two-dimensional time-dependent PIDCP is first semidiscretized in space (the asset price domain) and the resulting large semidiscrete PIDCP system is subsequently discretized in time. Key elements in the construction of an effective numerical method include the treatment of the double integral term, the selection of the temporal discretization scheme, and the handling of the early exercise constraint.

In the past two decades much interest has been devoted in the computational finance literature to the valuation of American options under jump-diffusion models via the numerical solution of PIDCPs. We give a brief overview of main references in this field, relevant to finite-activity jumps.

d’Halluin, Forsyth & Labahn [7] and d’Halluin, Forsyth & Vetzal [8] considered one-dimensional PIDCPs for the values of American options on a single asset under the Merton [24] and Kou [22] jump-diffusion models. The single integral term has been numerically evaluated by means of the fast Fourier transform, cf. also e.g. Almendral & Oosterlee [1], which avoids the computational burden of directly evaluating matrix-vector products with a large dense matrix stemming from the discretization of this term. For the temporal discretization, the Crank–Nicolson scheme is applied using variable step sizes. Here a fixed-point iteration on the integral part is effectively combined with a penalty iteration [9] to handle the early exercise constraint. Clift & Forsyth [5] extended the numerical solution approach from [7, 8] to two-dimensional PIDCPs for the values of American options on two assets under generalizations of the Merton and Kou jump-diffusion models.

Toivanen [29] considered the numerical solution of the one-dimensional Kou PIDCP and derived a simple and highly efficient algorithm for evaluating the integral term in this case. To deal with the early exercise constraint, a useful splitting technique is employed that has been introduced and studied by Ikonen & Toivanen [13, 15].

Salmi, Toivanen & von Sydow [26] proposed, for the temporal discretization of two-dimensional PIDCPs, the Crank–Nicolson Adams–Bashforth scheme. This is a second-order implicit-explicit (IMEX) method that conveniently treats the spatial differential part in an implicit manner and the integral part in an explicit manner.

Boen & in ’t Hout [3] considered the two-dimensional Merton PIDCP and studied, for the temporal discretization, a variety of second-order IMEX and alternating direction implicit (ADI) methods, using the Ikonen–Toivanen splitting technique to incorporate the early exercise constraint. Here the spatial differential part is again handled implicitly and the integral part explicitly.

Our aim in the present paper is to construct and investigate an efficient numerical method for the two-dimensional Kou PIDCP to approximate the fair values of American-style two-asset options together with their Greeks Delta and Gamma under the two-asset Kou model. An outline of the rest of our paper is as follows.

In Section 2, we formulate the pertinent two-dimensional Kou PIDCP.

In Section 3, we consider its semidiscretization. Here the spatial differential part is discretized in a common way, by applying second-order central finite differences on a smooth, nonuniform Cartesian grid. For the discretization of the double integral term, we employ the two-dimensional extension recently derived by in ’t Hout & Lamotte [18] of the fast algorithm by Toivanen [29] in the case of the one-asset Kou model. The number of elementary arithmetic operations of this algorithm is directly proportional to the number of spatial grid points, which is optimal.

For the temporal discretization of the semidiscrete two-dimensional Kou PIDCP, we investigate an interesting family of second-order diagonally implicit Runge–Kutta (DIRK) methods introduced by Cash [4]. These methods, containing a free parameter , are formulated in Section 4. For suitable values of , the method possesses a strong damping property (-stability). This property has been shown to be beneficial for the accurate and stable approximation of the Greeks Delta and Gamma for American options in the special case of the Black–Scholes model, see Ikonen & Toivanen [14], Le Floc’h [23] and in ’t Hout [17]. To our knowledge, the family of DIRK methods has not yet been considered in the literature for American options and their Greeks under more general, jump-diffusion models. In the present paper, we shall study its adaptation to the semidiscrete two-dimensional Kou PIDCP. Here the effective combination of the fixed-point and penalty iterations introduced by d’Halluin et al. [7, 8] is employed.

In Section 5, ample numerical experiments are presented that provide important insight into the convergence behaviour of the proposed numerical method for American option values as well as their Greeks Delta and Gamma under the two-asset Kou model.

In Section 6, conclusions are given.

2 American option valuation model

Let denote the fair value of an American-style option in the pertinent two-asset Kou jump-diffusion model if at time units before the given maturity time the two underlying asset prices are equal to and . Let denote the payoff of the option and consider the spatial integro-differential operator given by

| (2.1) |

Here is the risk-free interest rate, () is the instantaneous volatility for asset conditional on the event that no jumps occur, is the correlation coefficient of the two underlying standard Brownian motions, is the jump intensity of the underlying Poisson arrival process and () is the expected relative jump size for asset . The function is the joint probability density function of two independent random variables having log-double-exponential distributions [22],

| (2.2) |

The parameters , , , are all positive constants with and . It holds that

From financial option valuation theory it follows that the function satisfies the two-dimensional Kou PIDCP

| (2.3) |

valid pointwise for whenever , , . Boundary conditions are given by imposing (2.3) for and , respectively. The initial condition is provided by the payoff,

| (2.4) |

for , .

Along with the American option value function , we are interested in this paper in the Greeks Delta and Gamma. These important risk quantities are defined by

| (2.5) |

Clearly, all Greeks (2.5) appear in the function given by (2).

The three conditions in (2.3) naturally induce a decomposition of the -domain: the continuation region is the set of all points where holds and the early exercise region is the set of all points where holds. The joint boundary of these two regions is called the early exercise boundary or free boundary.

We shall deal in this paper with the well-known contract of an American put-on-the-average option, which has the payoff

| (2.6) |

with given strike price .

3 Spatial discretization

As the first step towards the numerical solution of the two-dimensional Kou PIDCP (2.3), we semidiscretize in the spatial variables . The semidiscretization is done in the same way as described in [18] for the case of a European put-on-the-average option.

For any given integer , a suitable smooth Cartesian grid is defined in a truncated spatial domain with fixed upper bound chosen sufficiently large. In each spatial direction, the mesh is uniform inside the interval and relatively fine. Outside, it is taken nonuniform and relatively coarse. Figure 1 shows a sample grid where , and .

Let denote the semidiscrete approximation to for and define the vector

where and the symbol T designates the transpose.

All five derivative terms in , given by (2), are approximated on the spatial grid in a common fashion using second-order central finite differences. The obtained semidiscretization of the relevant part of , including the term, can be written as , where is a given matrix that is sparse. Further details are given in [18, Sect. 3.1].

For the spatial discretization of the double integral term

we employ the two-dimensional extension [18] of the algorithm derived by Toivanen [29] for the case of the one-asset Kou model. A simple change of variables yields

whenever . Since the density function , given by (2.2), is defined on a partition of four sets of the first quadrant in the real plane, the integral is naturally decomposed into four integrals as , where

We shall consider the first integral above. For let denote its value at the spatial grid point . Write

and for define

Then can be expressed via a double cumulative sum,

| (3.1) |

The obvious but important fact holds that the are independent of the indices and . Consequently, if all values are given, then computing the double cumulative sums in (3.1) for all , can be performed, to leading order, in just additions.

For any given with an approximation to is obtained by using the bilinear interpolant that approximates on the -domain :

The approximation to is then defined by

| (3.2) |

It is easily verified that one arrives at the simple formula

| (3.3) |

with certain real coefficients for that are fully determined by the Kou parameters and the spatial grid (whenever ). These coefficients are independent of and they can therefore be computed upfront, before the time discretization. Since the values of in (3.2) can also be computed upfront, it readily follows that the number of elementary arithmetic operations to compute, for any given , all approximations () by (3.2) is, to leading order, equal to .

For the other three integrals , the discretization and efficient evaluation is performed completely analogous to that for . The favourable result is obtained that the number of elementary arithmetic operations to compute, for any given , the approximation to on the full spatial grid is, to leading order, directly proportional to the number of spatial grid points, which is optimal. For further details we refer to [18, Sect. 3.2].

For notational convenience, the approximation to the double integral on the full spatial grid will formally be denoted by , where is a given matrix. We emphasize that in our paper matrix-vector products in the case of are never evaluated directly, since this matrix is large and dense, but are always computed by the efficient algorithm described above.

Write . Then the spatial discretization gives rise to a large semidiscrete PIDCP system of the form

| (3.4) |

for with . Here vector inequalities are to be understood componentwise. The initial vector is given by pointwise evaluation of the payoff function on the spatial grid, except that cell averaging is used near the line segment , where is nonsmooth, see e.g. [16, 18].

Semidiscrete approximations to all Greeks Delta and Gamma are directly acquired by application of the pertinent second-order central finite difference formulas using the entries from the vector . Hence, as such, they form terms in the matrix-vector product .

4 Temporal discretization

For the temporal discretization of the semidiscrete PIDCP system (3.4), we shall investigate in this paper the adaptation of the diagonally implicit Runge–Kutta (DIRK) method given by the Butcher tableau

| (4.1) |

where denotes a given parameter. Method (4.1) possesses classical order of consistency222That is, for fixed systems of ordinary differential equations. equal to two for any value of and has the stability function given by

| (4.2) |

It is well-known that (4.1) is -stable333A Runge–Kutta method is called -stable if its stability function satisfies whenever , . If in addition , then the method is called -stable, see e.g. [10, 12]. for all and -stable if and only if .

The DIRK method (4.1) was introduced by Cash [4] and has been considered by various authors in the computational finance literature, notably for American option valuation. Khaliq, Voss & Kazmi [21] studied an adaptation of this method for the numerical valuation of American one- and two-asset options under the Black–Scholes model. Ikonen & Toivanen [14, 15] examined adaptations for the numerical valuation of American options under the one-asset Black–Scholes and Heston models. Recently, in ’t Hout [17] investigated an adaptation of (4.1) for the approximation of the Greeks Delta and Gamma in the case of American one- and two-asset options under the Black–Scholes model.

A common choice for the parameter value in (4.1) is , which yields both -stability and a relatively small error constant. This choice has been considered in all references above. It is worth mentioning that for this value of the stability function (4.2) is identical to that of the TR-BDF2 method, a familiar combination of the trapezoidal rule and the second-order backward differentiation formula introduced by Bank et al. [2] and subsequently studied by e.g. Hosea & Shampine [11]. The TR-BDF2 method has been advocated for the numerical approximation of one-asset American option values and their Greeks Delta and Gamma by Le Floc’h [23].

It is further interesting to note that (4.1) forms the underlying implicit method of both the Hundsdorfer–Verwer (HV) scheme and the modified Craig–Sneyd (MCS) scheme, two well-known alternating direction implicit (ADI) schemes that have first been studied for the temporal discretization of (semidiscrete) PDEs in finance by in ’t Hout and Welfert [19, 20]. For the MCS scheme, the value is often judiciously selected, cf. e.g. [17, 18]. Then the DIRK method (4.1) is -stable, but not -stable, since .

For the adaptation of (4.1) to (3.4), we shall adopt the popular penalty iteration. This has first been studied in the literature on American option valuation by Zvan, Forsyth & Vetzal [31, 32] and Forsyth & Vetzal [9] and has since then been widely considered in the computational finance literature. Along with it, a fixed-point iteration is employed on the integral part. This useful technique has first been proposed and analyzed in the literature on European option valuation under jump-diffusion models by Tavella & Randall [28] and d’Halluin, Forsyth & Vetzal [8], respectively. A simple and effective combination of the penalty iteration and the fixed-point iteration has been studied by d’Halluin, Forsyth & Labahn [7] and Clift & Forsyth [5] for American option valuation under jump-diffusion models. Following their approach, we acquire the adaptation of the DIRK method (4.1) under consideration in the present paper.

Let be a given, fixed large number and let be a given, fixed small tolerance. Let be any given sequence of temporal grid points with (constant or variable) step sizes () and set . Then the adaptation of method (4.1) to the semidiscrete PIDCP (3.4) generates approximations to successively, in a one-step manner, for by the DIRK-P method :

| (4.3) |

In each time step, two consecutive iteration processes are performed. Here , respectively , is defined as the diagonal matrix with -th diagonal entry equal to if , respectively , and zero otherwise (). For the first iteration process we consider the natural stopping criterion

and similarly for the second iteration process. For the solution of the large, sparse linear systems in (4.3), the BiCGSTAB iterative method444As implemented in Matlab version R2020b through the function bicgstab. is used with an ILU preconditioner.

Throughout this paper the common values and are selected. As starting vectors for the two iteration processes, the standard choice in the literature is . In the present paper, we shall consider linear extrapolation from the temporal grid points and to to define these vectors (whenever ) :

In our numerical experiments this choice is found to reduce the total number of iterations compared to the standard choice (which can be viewed as constant extrapolation).

Analogously to Section 3, fully discrete approximations to all Greeks Delta and Gamma are directly acquired by application of the pertinent second-order central finite difference formulas using the entries from the vector . Hence, they are constituents of the matrix-vector product .

We remark that the first two lines of (4.3) define the temporal discretization method that has been studied in [5, 7] and alluded to above (upon setting ). In this case, the underlying Runge–Kutta method is the classical -method.

It is well-known in the literature on American option valuation that suitable variable step sizes can lead to an improved convergence behaviour of temporal discretization methods compared to the use of constant step sizes, see e.g. Forsyth & Vetzal [9], Ikonen & Toivanen [15] and Reisinger & Whitley [25]. In this paper, we shall consider the nonuniform temporal grid defined by [15, 25]

| (4.4) |

Here, the variable step size is smallest for and grows linearly with .

5 Numerical study

In this section we consider four instances of the DIRK-P method (4.3):

DIRKa-P :

DIRKb-P :

DIRKc-P :

DIRKd-P :

For each of these four instances, the underlying Runge–Kutta method is -stable.

For DIRKa-P and DIRKd-P it is also -stable, whereas for DIRKb-P and DIRKc-P it

is not (then ).

In view of this, we apply the latter two methods with backward Euler damping, i.e.,

the first two time steps () are replaced by the BE-P method, which is defined

by the first two lines of (4.3) with and setting .

We shall investigate the temporal discretization errors555For this concept, see e.g. Hundsdorfer & Verwer [12]. of the above four DIRK-P methods at on a given region of interest ROI in the -domain, defined by

| (5.1) |

Here represents666A reference solution has been computed for each pertinent by applying the DIRKa-P method with time steps. the exact solution to the semidiscrete PIDCP system (3.4) at . Along with (5.1), the temporal discretization errors in the case of the Greeks Delta and Gamma will be studied. These errors are defined completely analogously to (5.1) and are denoted by and whenever . Notice that all temporal discretization errors are measured in the important maximum-norm.

For the numerical experiments we consider a typical parameter set, given by Table 1. It forms a blend of the parameter values for the Black–Scholes model in [17] and the Kou model in [5]. We take .

| 0.30 | 0.40 | 0.01 | 0.50 | 0.50 | 0.40 | 0.60 | 100 | 0.5 |

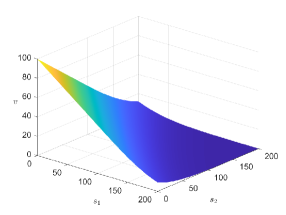

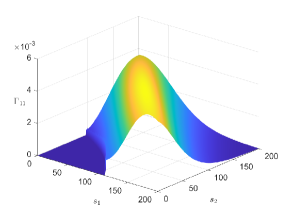

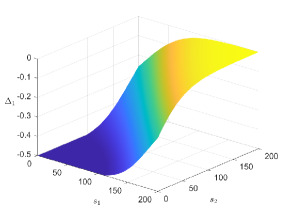

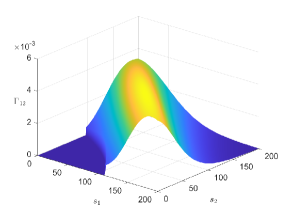

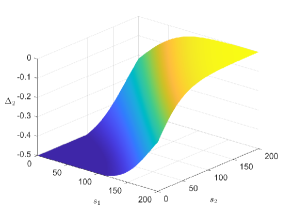

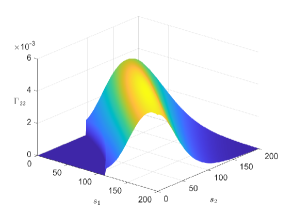

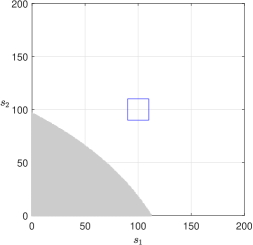

Figure 2 shows the approximated graphs of the American put-on-the-average option value function and the five Delta and Gamma functions (2.5) for on the -domain . Figure 3 shows in grey the corresponding early exercise region for . Here the blue square indicates the region of interest that we consider, given by . Clearly, this ROI lies well within the continuation region, at a significant distance from the early exercise boundary.

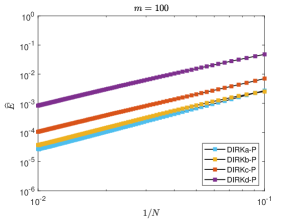

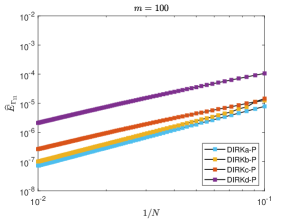

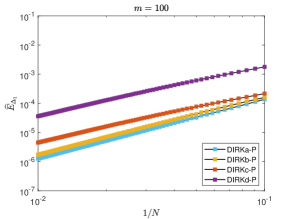

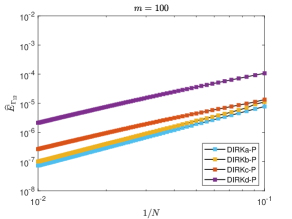

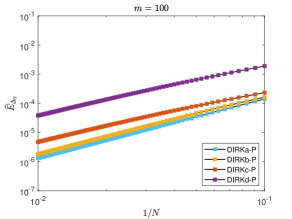

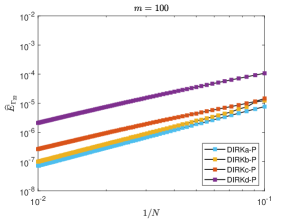

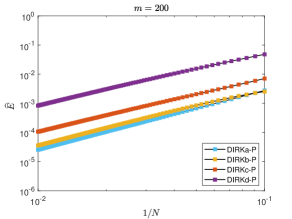

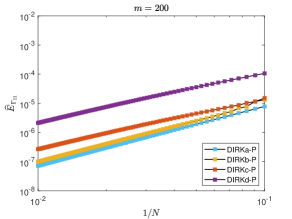

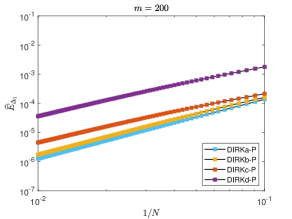

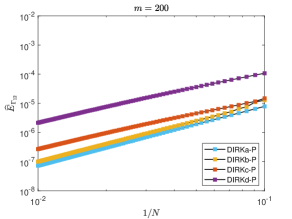

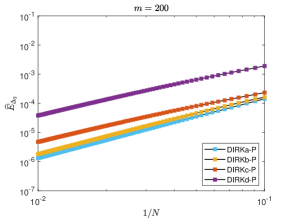

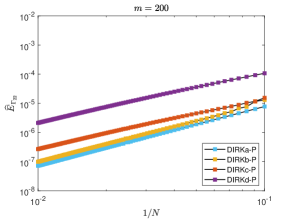

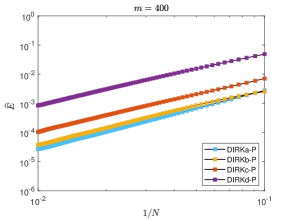

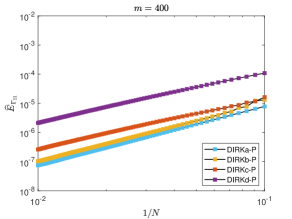

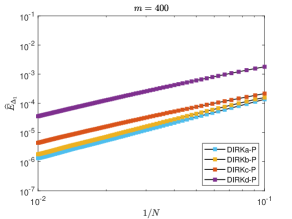

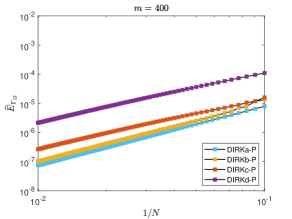

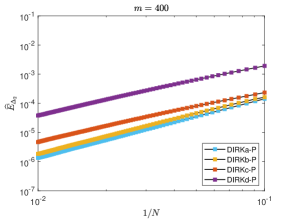

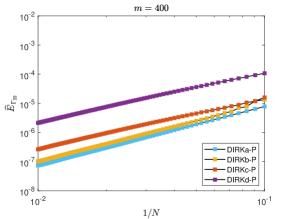

Figures 4, 5, 6 display, in double logarithmic scale, the temporal discretization errors versus for , respectively, and . The obtained results for the DIRKa-P, DIRKb-P, DIRKc-P and DIRKd-P methods are indicated by blue, orange, red and purple squares, respectively. In each figure, the left column shows the errors in the case of the option value (top), (middle) and (bottom) and the right column shows the errors in the case of (top), (middle) and (bottom).

A perusal of Figures 4, 5, 6 yields the positive result that all four DIRK-P methods under consideration possess a regular, second-order temporal convergence behaviour for the option value as well as all Greeks Delta and Gamma, with error constants that are essentially independent of , which is as desired. The error constant is found to be smallest for DIRKa-P and largest for DIRKd-P, with more than an order of magnitude difference. The error constant for DIRKb-P is close to that of DIRKa-P.

We next consider the DIRKa-P method and display in Tables 2, 3, 4 for , respectively, and the obtained777Spline interpolation is performed using neighbouring spatial grid points. approximations for the option value and all Deltas and Gammas for at five points of interest with . Computing, for each quantity and each point, the relative change in the difference between the approximations in Tables 2, 3 and in Tables 3, 4, directly leads to the numerical convergence orders given in Table 5. Clearly, a favourable second-order convergence behaviour is observed for the option value as well as all Deltas and Gammas when and increase simultaneously in a directly proportional way. For completeness, we mention that the numbers of iterations are modest; it always holds that .

6 Conclusions

In this paper, an efficient numerical method has been derived for the two-dimensional Kou PIDCP to approximate the fair values of American two-asset options together with their Greeks Delta and Gamma under the two-asset Kou jump-diffusion model. Here the nonlocal double integral is handled by the two-dimensional extension [18] of the fast algorithm by Toivanen [29] for the case of the one-asset Kou model. A useful family of DIRK methods, containing a free parameter , has been studied for the temporal discretization, applied with variable step sizes. The adaptation to the semidiscrete two-dimensional Kou PIDCP is obtained by employing the effective combination of the penalty iteration and the fixed-point iteration introduced by d’Halluin et al. [7, 8].

Four interesting values of have been considered. Numerical experiments reveal that for each value a favourable second-order temporal convergence behaviour is obtained. Among the four values, we deem to be preferable in view of a strong stability property (-stability) and a relatively small error constant of the method. The value is found to be a good alternative, provided the method is used with backward Euler damping.

An aim of future research is to investigate the numerical valuation of two-asset options under infinite-activity exponential Lévy processes. Here among others the ideas by Wang, Wan & Forsyth [30] are expected to be fruitful.

| 1.4410941 | 1.1383073 | 8.9582601 | 6.9719540 | 5.2348763 | |

| -3.2584818 | -2.7943724 | -2.3504777 | -1.9394994 | -1.5432873 | |

| -3.1100634 | -2.6572941 | -2.1988068 | -1.7831686 | -1.4158342 | |

| 4.5417553 | 4.6953152 | 4.5270544 | 4.1815685 | 3.7223616 | |

| 4.4658641 | 4.5400299 | 4.2998511 | 3.8964871 | 3.4317312 | |

| 4.7484932 | 4.7411556 | 4.3970553 | 3.8989366 | 3.3963788 |

| 1.4410326 | 1.1382366 | 8.9573323 | 6.9707384 | 5.2333520 | |

| -3.2587509 | -2.7945346 | -2.3505572 | -1.9394932 | -1.5431874 | |

| -3.1101373 | -2.6572752 | -2.1987284 | -1.7830391 | -1.4156498 | |

| 4.5418632 | 4.6951470 | 4.5270124 | 4.1818159 | 3.7229667 | |

| 4.4690948 | 4.5427646 | 4.3019622 | 3.8980510 | 3.4328213 | |

| 4.7484751 | 4.7408826 | 4.3969763 | 3.8991955 | 3.3969272 |

| 1.4410173 | 1.1382189 | 8.9571007 | 6.9704348 | 5.2329710 | |

| -3.2588183 | -2.7945753 | -2.3505774 | -1.9394920 | -1.5431629 | |

| -3.1101559 | -2.6572706 | -2.1987090 | -1.7830070 | -1.4156039 | |

| 4.5418893 | 4.6951043 | 4.5270008 | 4.1818764 | 3.7231174 | |

| 4.4699020 | 4.5434472 | 4.3024889 | 3.8984413 | 3.4330936 | |

| 4.7484710 | 4.7408145 | 4.3969563 | 3.8992599 | 3.3970642 |

| 2.0 | 2.0 | 2.0 | 2.0 | 2.0 | |

| 2.0 | 2.0 | 2.0 | 2.3 | 2.0 | |

| 2.0 | 2.0 | 2.0 | 2.0 | 2.0 | |

| 2.0 | 2.0 | 1.9 | 2.0 | 2.0 | |

| 2.0 | 2.0 | 2.0 | 2.0 | 2.0 | |

| 2.1 | 2.0 | 2.0 | 2.0 | 2.0 |

References

- [1] A. Almendral and C. W. Oosterlee. Numerical valuation of options with jumps in the underlying. Appl. Numer. Math., 53:1–18, 2005.

- [2] R. E. Bank, W. M. Coughran, W. Fichtner, E. H. Grosse, D. J. Rose, and R. K. Smith. Transient simulation of silicon devices and circuits. IEEE Trans. Comput.-Aided Design Int. Circ. Sys., 4:436–451, 1985.

- [3] L. Boen and K. J. in ’t Hout. Operator splitting schemes for American options under the two-asset Merton jump-diffusion model. Appl. Numer. Math., 153:114–131, 2020.

- [4] J. R. Cash. Two new finite difference schemes for parabolic equations. SIAM J. Numer. Anal., 21:433–446, 1984.

- [5] S. S. Clift and P. A. Forsyth. Numerical solution of two asset jump diffusion models for option valuation. Appl. Numer. Math., 58:743–782, 2008.

- [6] R. Cont and P. Tankov. Financial modelling with Jump Processes. Chapman & Hall/CRC Financial Mathematics Series. CRC Press, 2004.

- [7] Y. d’Halluin, P. A. Forsyth, and G. Labahn. A penalty method for American options with jump diffusion processes. Numer. Math., 97:321–352, 2004.

- [8] Y. d’Halluin, P. A. Forsyth, and K. R. Vetzal. Robust numerical methods for contingent claims under jump diffusion processes. IMA J. Numer. Anal., 25:87–112, 2005.

- [9] P. A. Forsyth and K. R. Vetzal. Quadratic convergence for valuing American options using a penalty method. SIAM J. Sci. Comp., 23:2095–2122, 2002.

- [10] E. Hairer and G. Wanner. Solving Ordinary Differential Equations II. Springer, 1991.

- [11] M. E. Hosea and L. F. Shampine. Analysis and implementation of TR-BDF2. Appl. Numer. Math., 20:21–37, 1996.

- [12] W. Hundsdorfer and J. G. Verwer. Numerical Solution of Time-Dependent Advection-Diffusion-Reaction Equations. Springer, 2003.

- [13] S. Ikonen and J. Toivanen. Operator splitting methods for American option pricing. Appl. Math. Lett., 17:809–814, 2004.

- [14] S. Ikonen and J. Toivanen. Pricing American options using LU decomposition. Appl. Math. Sc., 1:2529–2551, 2007.

- [15] S. Ikonen and J. Toivanen. Operator splitting methods for pricing American options under stochastic volatility. Numer. Math., 113:299–324, 2009.

- [16] K. J. in ’t Hout. Numerical Partial Differential Equations in Finance Explained. Palgrave Macmillan, 2017.

- [17] K. J. in ’t Hout. A note on the numerical approximation of Greeks for American-style options. Submitted for publication, arXiv:2401.13361, 2024.

- [18] K. J. in ’t Hout and P. Lamotte. Efficient numerical valuation of European options under the two-asset Kou jump-diffusion model. J. Comp. Finan., 26:101–137, 2023.

- [19] K. J. in ’t Hout and B. D. Welfert. Stability of ADI schemes applied to convection-diffusion equations with mixed derivative terms. Appl. Numer. Math., 57:19–35, 2007.

- [20] K. J. in ’t Hout and B. D. Welfert. Unconditional stability of second-order ADI schemes applied to multi-dimensional diffusion equations with mixed derivative terms. Appl. Numer. Math., 59:677–692, 2009.

- [21] A. Q. M. Khaliq, D. A. Voss, and S. H. K. Kazmi. A linearly implicit predictor-corrector scheme for pricing American options using a penalty method approach. J. Bank Finan., 30:489–502, 2006.

- [22] S. G. Kou. A jump-diffusion model for option pricing. Manag. Sci., 48:1086–1101, 2002.

- [23] F. Le Floc’h. TR-BDF2 for fast stable American option pricing. J. Comp. Finan., 17:31–56, 2014.

- [24] R. C. Merton. Option pricing when underlying stock returns are discontinuous. J. Finan. Econ., 3:125–144, 1976.

- [25] C. Reisinger and A. Whitley. The impact of a natural time change on the convergence of the Crank–Nicolson scheme. IMA J. Numer. Anal., 34:1156–1192, 2014.

- [26] S. Salmi, J. Toivanen, and L. von Sydow. An IMEX-scheme for pricing options under stochastic volatility models with jumps. SIAM J. Sci. Comp., 36:B817–B834, 2014.

- [27] W. Schoutens. Lévy Processes in Finance: Pricing Financial Derivatives. Wiley, 2003.

- [28] D. Tavella and C. Randall. Pricing Financial Instruments. Wiley, 2000.

- [29] J. Toivanen. Numerical valuation of European and American options under Kou’s jump-diffusion model. SIAM J. Sci. Comp., 30:1949–1970, 2008.

- [30] I. R. Wang, J. W. L. Wan, and P. A. Forsyth. Robust numerical valuation of European and American options under the CGMY process. J. Comp. Finan., 10:31–69, 2007.

- [31] R. Zvan, P. A. Forsyth, and K. R. Vetzal. Penalty methods for American options with stochastic volatility. J. Comp. Appl. Math., 91:199–218, 1998.

- [32] R. Zvan, P. A. Forsyth, and K. R. Vetzal. A finite volume approach for contingent claims valuation. IMA J. Numer. Anal., 21:703–731, 2001.