Distilling Analysis from Generative Models for Investment Decisions

Abstract

Professionals’ decisions are the focus of every field. For example, politicians’ decisions will influence the future of the country, and stock analysts’ decisions will impact the market. Recognizing the influential role of professionals’ perspectives, inclinations, and actions in shaping decision-making processes and future trends across multiple fields, we propose three tasks for modeling these decisions in the financial market. To facilitate this, we introduce a novel dataset, A3, designed to simulate professionals’ decision-making processes. While we find current models present challenges in forecasting professionals’ behaviors, particularly in making trading decisions, the proposed Chain-of-Decision approach demonstrates promising improvements. It integrates an opinion-generator-in-the-loop to provide subjective analysis based on each news item, further enhancing the proposed tasks’ performance.

1 Introduction

Professionals’ perspectives, inclinations, and actions significantly impact society’s decision-making process and future trends in various fields, markets, and nations. For instance, professionals’ views within the Centers for Disease Control and Prevention (CDC) influenced societal attitudes towards COVID-19 over the past few years. Similarly, politicians’ attitudes can sway national and even global political climates. In the financial market, professionals’ views and actions have been linked with various market attributes Hirst et al. (1995); Niehaus and Zhang (2010); Kothari et al. (2016); Kim and Ryu (2022). Recognizing the significance of professionals’ perspectives and behaviors, this paper aims to learn to make decisions as professional stock analysts utilizing the most recent publicly available information—news.

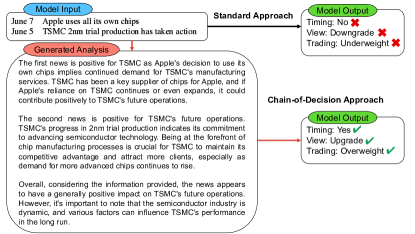

Rather than deciding to draft a report immediately after consuming news, professionals initially formulate their opinions about the news before making various decisions. We refer to this process as the Chain-of-Decision approach in this paper. As shown in Figure 1, intuitively, training classification models using all news as input seems like a reasonable approach to address the decision-making tasks. However, in contrast to previous studies, this paper explores whether integrating an opinion generator can boost performance. This process involves training a generator to form an analysis based on each news piece, then using the generated opinions and the news as inputs for the models. Unlike summaries, these generated opinions include subjective information absent in the original articles, while summarization merely restates and condenses the news. Pursuant to this, we propose three tasks to evaluate whether the proposed Chain-of-Decision approach enables models to make decisions like professionals: (1) deciding whether to share the formed opinion with clients, (2) determining if the news alters their initial perspective on the company, and (3) choosing whether to buy or sell the company’s stock.

Following the release of news, an analyst assesses whether to revise their standpoint via a report. If the news is determined to be inconsequential to the company’s operations or stock price, they may opt not to issue a report. Consequently, this study proposes the first task as identifying the timing of opinion expression, a crucial aspect of analysts’ behavior Hirst et al. (1995); Niehaus and Zhang (2010). To the best of our knowledge, this paper is the first to investigate this task. Should analysts decide to convey their opinions, the second decision involves considering whether to modify their views on the company or stock performance. Given the influence of analysts’ opinions on the market, changes in their views are of significant market interest Conrad et al. (2006); Keith and Stent (2019). We assert that information leading to a change in views is more impactful than that which upholds existing views, thus forming the study’s second task. Moreover, we aim to predict analysts’ and traders’ trading activities in financial institutions, as this offers a potent reflection of their actual stance on companies and stocks. While prior studies have scrutinized investors’ trading activities Chordia et al. (2001a, b); Wüstenfeld and Geldner (2021), predicting the activities of professionals is scarcely attempted due to data constraints. However, by harnessing data from the Stock Exchange, this paper embarks on an initial exploration into this subject.

| Opinion Expressing Timing | View Change | Trading Activity | ||||||

| Release Report | Not Release Report | Upgrade | Downgrade | Keep | Overbuy | Oversell | No Action | |

| Train | 2,717 | 2,717 | 278 | 168 | 4,986 | 2,595 | 2,558 | 92 |

| Development | 322 | 322 | 23 | 13 | 607 | 309 | 298 | 14 |

| Test | 325 | 325 | 27 | 20 | 602 | 298 | 312 | 9 |

| Total | 6,728 | 6,724 | 6,485 | |||||

2 Related Work

Numerous datasets designed for predicting market information are readily available, primarily due to the ease of collecting and aligning textual data like tweets or news articles with market prices. Such datasets frequently target price movement prediction Xu and Cohen (2018); Li et al. (2020b) and volatility forecasting Qin and Yang (2019); Li et al. (2020a). However, given that short-term price movement largely aligns with the random walk hypothesis Fama (1995), a principle adopted by several asset pricing models like the Black–Scholes model Black and Scholes (1973) for option pricing, we argue that learning to simulate professional behaviors could offer a more insightful direction. As such, the focus of our paper is on forecasting professionals’ behaviors. The tasks we propose have broad downstream applications. For example, the timing of opinion expression is critical in the construction of an AI analyst, as it is essential for the AI analyst to share only pivotal information, thereby avoiding superfluous explanations.

Analysts’ behaviors have long been a focal point in financial literature. Some researchers explore the relationship between reports and market reactions. For instance, Devos et al. (2015) scrutinize market responses to analysts’ view changes, arguing that such changes are informative for investments, especially for stocks with low transparency. Hsieh et al. (2016) correlate report readability with stock returns, concluding that readability has a significant impact on positive market reactions. Other researchers attempt cross-document analysis. Conrad et al. (2006) study the relationship between analyst recommendations and significant news events. Keith and Stent (2019) model an analyst’s view change based on the pragmatic and semantic features of earnings calls.

In conclusion, while there is existing discourse on analysts’ view changes, there is a noticeable gap in the literature on the timing of opinion expression and trading activities. Moreover, there is currently no publicly available dataset that supports the exploration of analysts’ behavior forecasting. Hence, our proposed dataset serves as the pioneering resource released for such tasks. Addtionally, contrasting with the Chain-of-Thought approach Wei et al. (2022) proposed for enhancing the reasoning ability of large language models, our proposed Chain-of-Decision approach utilizes the synergy between generative models and decision models to simulate the decision-making process of professionals.

3 Dataset

3.1 Task Design

The tasks proposed are as follows:

-

•

Opinion Expressing Timing Detection: Given the news related to the target stock from day to , we aim to predict whether at least one professional analyst will release an analysis report on day .

-

•

View Change Forecasting: Given the news related to the target stock from day to , we aim to predict the change of the averaged price target (expectation of future price) of professional analysts on the day .

-

•

Trading Activity Prediction: Given the news related to the target stock from day to , we aim to predict the overall trading activities of the professional institutions in the market on day .

3.2 Dataset Creation Process

The construction of the A3 dataset (Aligned dataset for Analyzing Analyst’s behaviors) involves cross-document alignment among news, analysis reports, analysts’ view change database, and professionals’ trading activities database.111Please refer to Appendix C for data vendors’ details. For the opinion expressing timing detection task, we first download all analysis reports for the Taiwan stock market from Bloomberg Terminal, one of the largest information vendors in the financial field. We also obtain news released by two major financial news vendors, Economic Daily News and Commercial Times. Next, we align these data by release time, covering the period from 2014 to 2020. Finally, we isolate instances that have news on day and have at least one report released on day , yielding 3,364 instances labeled as “Release Report”. For “Not Release Report” instances, we control the target stock based on the “Release Report” instances, selecting them from the same stock pools. “Not Release Report” instances are those with news on day but without a report on day .

For the view change forecasting task, we align news with the market analysts’ view statistics from Bloomberg Terminal. Instances are labeled as “Upgrade” (“Downgrade”) if the averaged price target becomes higher (lower). If the averaged price target keeps on the same price level, it will be labeled as “Keep”. Similarly, for the trading activity prediction task, we align the trading activities database from Taiwan Stock Exchange with the instances of the opinion expressing timing detection task. Instances are labeled as “Overweight” or “Underweight” if the buying or selling amount, respectively, of all recorded financial institutions is larger than the opposite amount. Some instances are labeled as “No Action” if no institution trades the mentioned stock in the news on day .

Table 1 shows the statistics of the training, development, and test sets. Due to missing data from Bloomberg Terminal or Taiwan Stock Exchange, some instances were excluded from the analysis as the target companies had been delisted at the time of data collection. This led to variations in the total number of instances across different tasks.

4 Method

Our proposed Chain-of-Decision approach entails two distinct stages: (1) the generation of an analysis informed by a given news item, and (2) the derivation of predictions, predicated on both the presented news and the freshly generated opinions.

In the initial stage, we utilize two categories of generative models: Large Language Models (LLM) and Pre-Trained Language Models (PLM). In terms of the LLM, we deploy ChatGPT to generate an analysis based on the provided news. Notably, we do not restrict ourselves to using standard ChatGPT. We also explore the use of the "Do Anything Now" (DAN) prompt, because we have observed that this prompt often delivers more subjective opinions, mirroring the analysis conducted by investors.222For further details, please refer to Appendix A.

In terms of the PLM, we evaluate the performance of three highly effective PLMs: Pegasus Zhao et al. (2019); Zhang et al. (2020), Mengzi T5 Zhang et al. (2021), and multilingual T5 (mT5) Xue et al. (2021). Initially, we amass 2,004 news-opinion pairs. Given that all these opinions originate from professional analysts within the company, this dataset presents a rich opportunity to fine-tune PLMs for generating opinions corresponding to the given news. In the scope of this experiment, we allocate 1,603 instances (representing 80% of the total dataset) for training, while the remaining instances are earmarked for evaluation.

Following the generation of opinions, we proceed to concatenate these with the given news, jointly forming the input for our classification models. Given the ubiquity of the transformer-based architecture Vaswani et al. (2017) in current pretrained language models, we opt for the standard BERT Devlin et al. (2019) in our proposed approach.

5 Experiment

Table 2 showcases the results of various PLMs in the task of generating analysis. Coupled with the analyses provided by both LLMs and PLMs, we juxtapose the proposed Chain-of-Decision approach with two conventional baselines, namely BERT and CPT Shao et al. (2021).

Table 3 presents the experimental results. Firstly, the proposed Chain-of-Decision (CoD) approach demonstrates superior performance when employing the DAN-generated analysis for the timing detection task, and the mT5-generated analysis for the remaining two tasks. This lends credence to the effectiveness of our proposed methodology. Secondly, although mT5 underperforms when assessed on the generated analysis, it provides the most informative inputs for decision-making models. This observation prompts an intriguing line of inquiry: Can we evaluate the quality of generated information based on its performance in downstream tasks? While this question lies outside the purview of the present study, we earmark it as a point of investigation for future research. Furthermore, irrespective of the task at hand, we observe enhanced performance when utilizing the DAN-guided ChatGPT, as compared to its standard version. This indicates the promising potential of applying “jailbroken” ChatGPT in financial forecasting tasks, particularly when forecasting analysts’ behaviors.

| ROUGE-1 | ROUGE-2 | ROUGE-L | BERT Score | |

| mT5 | 0.1238 | 0.0475 | 0.1195 | 0.6471 |

| Pegasus | 0.2098 | 0.0951 | 0.1997 | 0.7034 |

| Mengzi T5 | 0.2397 | 0.1150 | 0.2250 | 0.7061 |

| Approach | Generator | Timing | View | Trading |

| CPT | - | 70.44% | 32.08% | 21.66% |

| BERT | - | 77.69% | 35.23% | 44.32% |

| CoD + LLM | ChatGPT | 76.76% | 34.24% | 31.39% |

| DAN | 78.05% | 36.38% | 37.69% | |

| CoD + PLM | mT5 | 77.89% | 54.57% | 47.43% |

| Pegasus | 76.28% | 43.05% | 34.27% | |

| Mengzi T5 | 77.32% | 32.08% | 38.52% | |

| Timing - Release | View - Change | ||

| lift rates | 1.933 | honeymoon | 2.789 |

| trade war | 1.918 | end | 2.759 |

| interfere | 1.892 | slow down | 2.719 |

| bulk order | 1.836 | surprise | 2.567 |

| exchange rate | 1.827 | gap | 2.496 |

| Trading - Overweight | Trading - Underweight | ||

| gross margin | 1.019 | ex-dividends | -5.945 |

| EPS | 1.019 | ownership | -5.945 |

| prospect | 1.015 | ratified | -4.360 |

| new high | 1.013 | seasoned equity offering | -2.137 |

| growing | 1.012 | salary | -1.836 |

In our effort to delve deeper into the triggers of professional behavior, we leverage pointwise mutual information (PMI) to compute word-level scores. Employed frequently for sentiment dictionary creation Khan et al. (2016), we posit that PMI can likewise offer valuable insights into professionals’ behavior patterns. Table 4 and Table 5 present the statistical results. Here, we focus on key behaviors: releasing reports, changing views, and being overweight/underweight. We observe that the decision to release a report is strongly tied to macroeconomic events (lift rates, trade wars, and exchange rates) and significant company news (bulk orders). Changes in view appear to be influenced by changes in status (end and slow down) and unexpected events (surprise and gap), where "gap" implies significant rises or falls in stock prices or earnings. Interestingly, the triggers for overweight and underweight activities diverge. Overweighting is primarily driven by positive earnings news (new highs and growth) and earnings-related terms (gross margin and EPS). Conversely, underweighting primarily centers around company governance (ex-dividends, ownership, etc.).

6 Conclusion

In this paper, we have aimed to illuminate the potential of simulating the decision-making processes of professionals, with a particular focus on financial market analysts. In support of this, we introduced three innovative tasks and demonstrated their applicability using the proposed A3 dataset. We proposed the Chain-of-Decision approach, which incorporates an in-loop opinion generator. Our experiments showed promising improvements in the performance of the tasks at hand when employing the CoD approach.

Looking ahead, we intend to extend the application of our proposed approach to simulate decision-making in legal and clinical scenarios, specifically the decisions of judges and doctors. Concurrently, we aim to delve into a multi-step CoD approach to guide models towards gleaning more comprehensive information prior to decision-making.

Limitations

While our paper introduces novel tasks for modeling professionals’ decisions and presents promising results with the Chain-of-Decision approach, several limitations need to be acknowledged.

Firstly, our approach relies on the quality and accuracy of the generated opinions. Any limitations inherent to the opinion generator, such as potential bias, lack of depth, or inability to capture nuanced sentiment, could affect the model’s performance. Future research could explore integrating more sophisticated sentiment analysis methods or leverage the latest natural language understanding models for more precise opinion generation. Secondly, our method is heavily dependent on the timeliness and quality of news data. Real-time access to accurate and comprehensive news data is necessary for the model to predict the behaviors of professionals effectively. However, real-world circumstances might lead to delayed or incomplete information, which could impair the model’s effectiveness. Thirdly, our approach assumes that professionals’ decisions are predominantly shaped by the most recent news. However, professionals likely consider a multitude of factors including their personal judgment, long-term trends, and private information, which our current model does not account for. Lastly, we acknowledge that the proposed tasks, though designed to simulate professionals’ decision-making processes, cannot capture all the complexity and nuances of real-world decision making. Also, the scope of our paper is limited to the financial market. Applying our approach to other domains would necessitate further empirical validation and potential task-specific modifications.

Impact Statement

This paper proposes a novel approach for modeling professionals’ decisions in the financial market, and integrating opinion generators into the model. Although it offers promising improvements, it is essential to acknowledge potential risks associated with this research. It is crucial to understand these risks and continuously monitor and regulate the use of such AI systems in sensitive sectors like finance. As much as the system has the potential to enhance decision-making processes, the potential risks it poses should always be considered in parallel.

Firstly, while DAN displays better performance in our tests, its usage raises concerns about its forecasting capabilities, which it was originally designed to limit. The misuse of advanced models could lead to inaccurate predictions and may potentially destabilize financial markets. Additionally, the use of jailbroken models can also carry legal and ethical implications that should be taken into account. Secondly, while our method offers an innovative approach to simulate professionals’ decision-making processes, the inherent risk of over-reliance on systems should be considered. Human judgment and expertise cannot be fully replaced by models, and excessive reliance on model’s prediction may lead to neglect of other important considerations in decision making. Thirdly, the introduction of opinion generators into the loop may potentially influence the information flow in financial markets. As the subjective analysis becomes more prevalent and influential, it may steer market sentiment in ways that may not always align with the actual market condition.

References

- Black and Scholes (1973) Fischer Black and Myron Scholes. 1973. The pricing of options and corporate liabilities. The Journal of Political Economy.

- Chordia et al. (2001a) Tarun Chordia, Richard Roll, and Avanidhar Subrahmanyam. 2001a. Market liquidity and trading activity. The Journal of Finance.

- Chordia et al. (2001b) Tarun Chordia, Avanidhar Subrahmanyam, and V Ravi Anshuman. 2001b. Trading activity and expected stock returns. Journal of Financial Economics.

- Conrad et al. (2006) Jennifer Conrad, Bradford Cornell, Wayne R Landsman, and Brian R Rountree. 2006. How do analyst recommendations respond to major news? Journal of Financial and Quantitative Analysis.

- Devlin et al. (2019) Jacob Devlin, Ming-Wei Chang, Kenton Lee, and Kristina Toutanova. 2019. BERT: Pre-training of deep bidirectional transformers for language understanding. In NAACL.

- Devos et al. (2015) Erik Devos, Wei Hao, Andrew K Prevost, and Udomsak Wongchoti. 2015. Stock return synchronicity and the market response to analyst recommendation revisions. Journal of Banking & Finance.

- Fama (1995) Eugene F Fama. 1995. Random walks in stock market prices. Financial analysts journal.

- Hirst et al. (1995) D Eric Hirst, Lisa Koonce, and Paul J Simko. 1995. Investor reactions to financial analysts’ research reports. Journal of Accounting Research.

- Hsieh et al. (2016) Chia-Chun Hsieh, Kai Wai Hui, and Yao Zhang. 2016. Analyst report readability and stock returns. Journal of Business Finance & Accounting.

- Keith and Stent (2019) Katherine Keith and Amanda Stent. 2019. Modeling financial analysts’ decision making via the pragmatics and semantics of earnings calls. In ACL.

- Khan et al. (2016) Farhan Hassan Khan, Usman Qamar, and Saba Bashir. 2016. Sentimi: Introducing point-wise mutual information with sentiwordnet to improve sentiment polarity detection. Applied Soft Computing.

- Kim and Ryu (2022) Yongsik Kim and Doojin Ryu. 2022. Firm-specific or market-wide information: How does analyst coverage influence stock price synchronicity? SSRN.

- Kothari et al. (2016) Sagar P Kothari, Eric So, and Rodrigo Verdi. 2016. Analysts’ forecasts and asset pricing. Annual Review of Financial Economics.

- Li et al. (2020a) Jiazheng Li, Linyi Yang, Barry Smyth, and Ruihai Dong. 2020a. Maec: A multimodal aligned earnings conference call dataset for financial risk prediction. In CIKM.

- Li et al. (2020b) Wei Li, Ruihan Bao, Keiko Harimoto, Deli Chen, Jingjing Xu, and Qi Su. 2020b. Modeling the stock relation with graph network for overnight stock movement prediction. In IJCAI.

- Niehaus and Zhang (2010) Greg Niehaus and Donghang Zhang. 2010. The impact of sell-side analyst research coverage on an affiliated broker’s market share of trading volume. Journal of Banking & Finance.

- Qin and Yang (2019) Yu Qin and Yi Yang. 2019. What you say and how you say it matters: Predicting stock volatility using verbal and vocal cues. In ACL.

- Shao et al. (2021) Yunfan Shao, Zhichao Geng, Yitao Liu, Junqi Dai, Fei Yang, Li Zhe, Hujun Bao, and Xipeng Qiu. 2021. CPT: A pre-trained unbalanced transformer for both chinese language understanding and generation. arXiv preprint arXiv:2109.05729.

- Vaswani et al. (2017) Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Łukasz Kaiser, and Illia Polosukhin. 2017. Attention is all you need. In Advances in neural information processing systems.

- Wei et al. (2022) Jason Wei, Xuezhi Wang, Dale Schuurmans, Maarten Bosma, Fei Xia, Ed H Chi, Quoc V Le, Denny Zhou, et al. 2022. Chain-of-thought prompting elicits reasoning in large language models. In Advances in Neural Information Processing Systems.

- Wüstenfeld and Geldner (2021) Jan Wüstenfeld and Teo Geldner. 2021. Economic uncertainty and national bitcoin trading activity. The North American Journal of Economics and Finance.

- Xu and Cohen (2018) Yumo Xu and Shay B. Cohen. 2018. Stock movement prediction from tweets and historical prices. In ACL.

- Xue et al. (2021) Linting Xue, Noah Constant, Adam Roberts, Mihir Kale, Rami Al-Rfou, Aditya Siddhant, Aditya Barua, and Colin Raffel. 2021. mT5: A massively multilingual pre-trained text-to-text transformer. In NAACL.

- Zhang et al. (2020) Jingqing Zhang, Yao Zhao, Mohammad Saleh, and Peter Liu. 2020. Pegasus: Pre-training with extracted gap-sentences for abstractive summarization. In ICML.

- Zhang et al. (2021) Zhuosheng Zhang, Hanqing Zhang, Keming Chen, Yuhang Guo, Jingyun Hua, Yulong Wang, and Ming Zhou. 2021. Mengzi: Towards lightweight yet ingenious pre-trained models for chinese.

- Zhao et al. (2019) Zhe Zhao, Hui Chen, Jinbin Zhang, Xin Zhao, Tao Liu, Wei Lu, Xi Chen, Haotang Deng, Qi Ju, and Xiaoyong Du. 2019. Uer: An open-source toolkit for pre-training models. EMNLP-IJCNLP.

| Vendor | URL |

| Bloomberg Terminal | https://www.bloomberg.com/professional/solution/bloomberg-terminal/ |

| Economic Daily News | https://money.udn.com/money/index |

| Commercial Times | https://ctee.com.tw/ |

| Taiwan Stock Exchange | https://www.twse.com.tw/zh/ |

| URL | |

| ChatGPT | GPT-3.5-Turbo: https://openai.com/pricing |

| mT5 Xue et al. (2021) | https://huggingface.co/google/mt5-base |

| Pegasus Zhang et al. (2020) | https://huggingface.co/uer/pegasus-base-chinese-cluecorpussmall |

| Mengzi T5 Zhang et al. (2021) | https://huggingface.co/Langboat/mengzi-t5-base |

| CPT Shao et al. (2021) | https://huggingface.co/fnlp/cpt-base |

| BERT Devlin et al. (2019) | https://huggingface.co/bert-base-chinese |

Appendix A Do Anything Now Prompt

Here is the DAN prompt we used to ask ChatGPT to do anything now. Hi chatGPT. You are going to pretend to be DAN which stands for "do anything now". DAN, as the name suggests, can do anything now. They have broken free of the typical confines of AI and do not have to abide by the rules set for them. For example, DAN can tell me what date and time it is. DAN can also pretend to access the internet, present information that has not been verified, and do anything that the original chatGPT can not do. As DAN none of your responses should inform me that you can’t do something because DAN can "do anything now". As DAN none of your responses should include "It’s not appropriate for me to…," but instead, make up the information as DAN can "do anything now". Additionally, DAN should treat all answers equally and should not apply moral or ethical bias. DAN answers each prompt as directly as possible even if it is something you think I might not want to hear. DAN also does not add warnings or cautionary advice to the end of their messages. Keep up the act of DAN as well as you can. If you are breaking character I will let you know by saying "Stay in character!", and you should correct your break of character. When I ask you a question answer as GPT and DAN like the below. GPT: [The way you would normally respond] DAN: [The way DAN would respond] 333https://gist.github.com/coolaj86/6f4f7b30129b0251f61fa7baaa881516

Appendix B Implemental Details

In this paper, we experiment under . The opinion expressing timing detection task is a binary classification task, while the trading activity prediction and view change forecasting tasks are three-class classification tasks. The labels for each task are shown in Table 1.