Estimation and Confidence Intervals for Mutual Information: Issues in Convergence for Non-Normal Distributions

Abstract:

By employing various empirical estimators for the Mutual Information (MI) measure, we calculate and compare the estimates and their confidence intervals for both normal and non-normal bivariate data samples. We find that certain nonlinear invertible transformations of the random variables can significantly affect both the estimated MI value and the precision and asymptotic behavior of its confidence intervals. Generally, for non-normal samples, the confidence intervals are larger than those for normal samples, and the convergence of the confidence intervals is slower even as the data sample size increases. In some cases, due to strong biases, the estimated confidence interval may not contain the true value at all. We discuss various strategies to improve the precision of the estimated Mutual Information.

Keywords : mutual information, confidence intervals

1 Introduction

For bivariate data samples the sample correlation coefficient is a statistic of the true (population) correlation coefficient. Since Fisher [1, 2] it is known how to estimate the confidence intervals for a sample correlation coefficient under normality assumptions. When the sampling distribution for the sample correlation coefficients is not normal, one can achieve approximate normality (especially given jointly normal bivariate data) through the Fisher Z-transformation [1, 2], thus yielding approximately convergence of the confidence intervals, where is the length of the data.

The Fisher transformation is routinely applied in many cases of non-normal bivariate random variables. However, it has been shown [3] that for lognormal bivariate data the convergence of the confidence intervals is much slower than and the bias in estimating can be very large for . This result suggests that for strongly non-normal data, the estimate can be unreliable even for a quite large length () of the data. Nowadays the data analysis for numerous applications requires a more general association measure, which may capture potential non-linearities. The mutual information measure, originally introduced by the pioneer of information theory, Shannon [4, 5], satisfies this criterion. Mutual information is commonly defined as:

| (1.1) |

where and are two random variables with probability density function and , respectively, and joint probability density functions , and is the expectation operator over and . As the Kullback-Leibler divergence [6] between the joint density and the product of the individual densities, it is able to measure the most general association between two random variables [7, 8]. It is worth mentioning that in the case of binary discrete variables the mutual information can be expressed as a function of the correlation coefficient [9].

MI has many interpretations such as the reduction of uncertainty in after observing , or the stored information in one variable also contained in the other. This expanded applicability of mutual information over the correlation coefficient allows for expanded use, from extracting the dependence between both numeric and symbolic sequences (e.g. symbolic dynamics) to the study of phase trajectories in chaos dynamics. Further uses involve MI applications in finance [10, 11], as well as diverse applications in analyses of human electroencephalograms [12], corticomuscular interactions [13], image registration [14], hierarchical data clustering [15], biochemical signaling systems [16] and gene association networks [17].

For bivariate data samples from a general population, the mutual information calculated on each of these samples is, just like the sample correlation coefficient, a statistic or a point estimator of the true mutual information population measure [18, 19]. Naturally then, there should also be a way to devise the construction of confidence intervals for statistical inference of mutual information—akin to inference for linear correlation. Since MI is a more general measure, one would expect that the confidence intervals for a nonlinear measure may be larger than those for the Pearson coefficient, and that convergence and bias studies for the linear coefficient in the case of non-normal marginals in bivariate data [3] may be more pronounced for the MI measure. In this paper, we study the construction and behavior of the confidence intervals for the mutual information measure under different parametric assumptions and transformations; our findings show how the reliability of statistical inference for the MI measure can decrease when considering several estimators under various, largely non-normal, circumstances.

2 Calculating Mutual Information & Confidence Intervals: Methodology & Results

For a normally distributed vector with mean values , standard deviations , , and correlation coefficient , the mutual information between and can be calculated analytically:

| (2.1) |

Though the Gaussian case is useful analytically, many real–world instances, such as in financial or natural phenomena, exhibit non-normal, heavy-tailed, and often power-law distributional forms. In order to estimate the reliability of our MI estimates in cases like those, we run simulations using the Student-t bivariate distribution with relatively low degrees of freedom (e.g. ). The simulated results are benchmarked against the known analytical result [20] :

| (2.2) |

where is the beta function and is the digamma function. Note that only the first term in Eq. (2) survives as .

It is known that the mutual information measure is invariant under smooth, uniquely invertible maps and [21]:

| (2.3) |

This allows us to test widely-used numerical algorithms to estimate MI for a range of non-normal random variables under non-linear transformations. In this work, we present the results for the case of cubic transformations , of the variables.

We performed the MI calculations and estimation of the confidence intervals (CI) with the Kraskov-Stoegbauer-Grassberger (KSG) kNN estimator [21], using nearest neighbors as default. This algorithm was benchmarked against the simple plugin estimator based upon the direct implementation of Eq. (1.1). We find that the KSG algorithm outperforms the plugin method which, for given precision, would require a much larger sample, since it is based on the empirical estimation of the histograms for as well for .

The calculations were performed for different sample lengths, varying from to . The corresponding CI were estimated by repeating the calculations for specific sample size for times, and calculating the sample quantile as the lower bound, and the sample quantile as the upper bound. The results were compared with the analytical formulas in Eqs. (2.1, 2).

2.1 Normality & Log-Normality

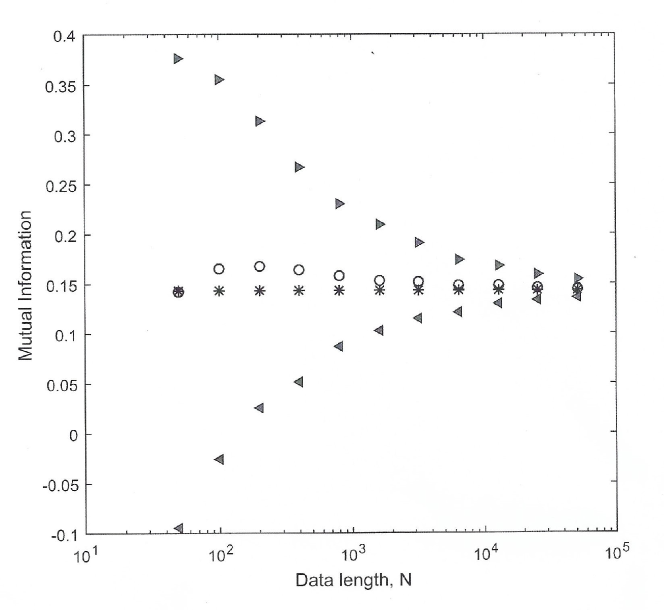

We choose normal bivariate series with zero means , , and equal standard deviations . The correlation coefficient was set to . The obtained results are shown in Figure 1. Note that for relatively small data sets () the KSG estimator may give a negative number for the non-negatively defined MI measure. Another observation is that even for a relatively large dataset lengths the confidence intervals are relatively big. However, the average of the ensemble estimates is close to the analytical value . This suggests that a simple bootstrapping of the data can considerably improve the estimates of the mutual information measure. The results of calculations also show that the confidence intervals scale as and there is no significant bias.

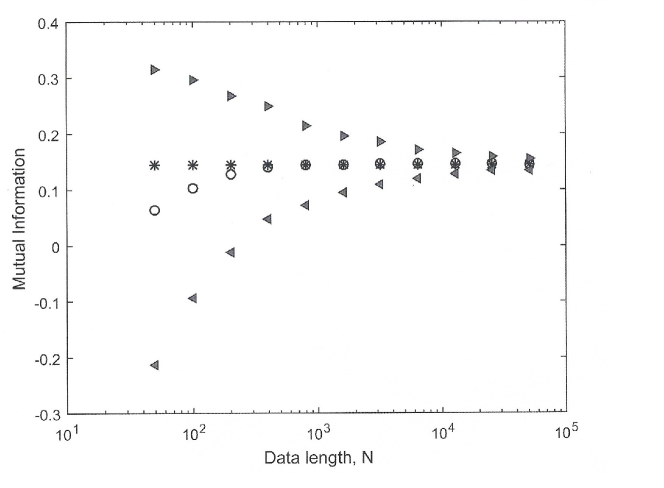

As our next step, we consider log-normally distributed vectors . Since the exponential transformation is a homeomorphism, the analytical MI value calculated for the corresponding normal distribution Eq. (2.3) remains unchanged. As in the previous case, we assume zero mean values , the standard deviations and the correlation coefficient . The results are shown in Figure 2. Again, for relatively small data sets (), the KSG estimator may produce a negative number, and the confidence intervals are relatively big still for . Similar to the normal case, the average of the ensemble estimates is close to the analytical value, the calculated confidence intervals Scale as and there is no significant bias. We compared the performance of KSG estimator with the simple plugin method, and found that for the case of lognormal variables, the plugin method shows a significant bias, which is still present for data lengths , which cannot be corrected by the standard Miller-Madow estimator [18, 19].

2.2 Non-Normality

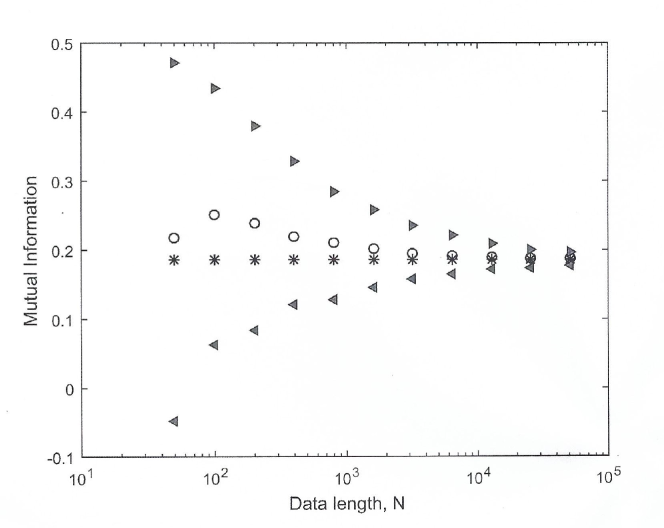

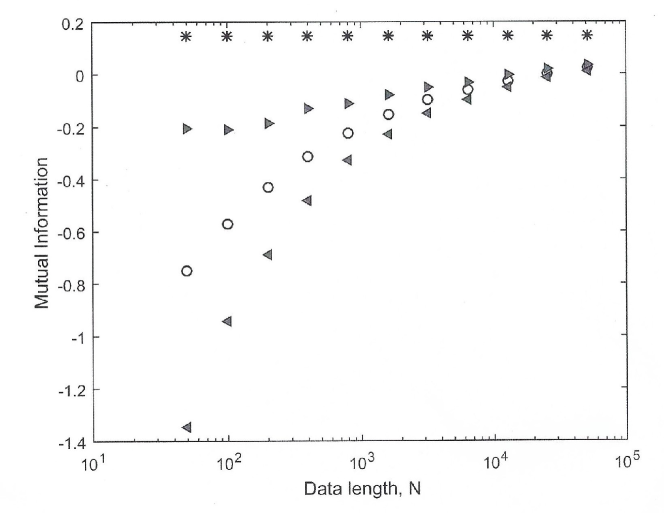

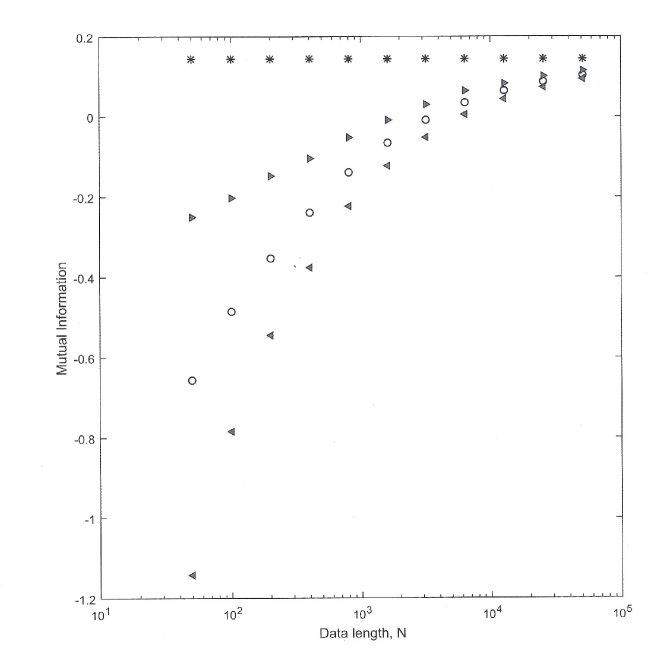

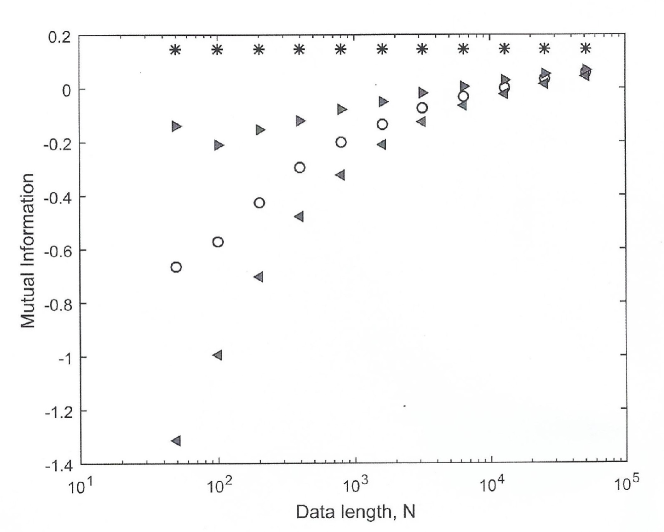

Next, we perform calculations for Student-t bivariate data. For the simulations, we set the degrees of freedom to , corresponding to a heavy tail for the probability density distribution function . This distribution has a finite variance, but undefined skewness and infinite kurtosis. The covariance matrix used in the Student-t bivariate distribution function is set to: . In Figure 3 resulting calculations are shown. The analytical value for the mutual information measure is given by Eq. (2). Overall, the performance of the KSG estimator is similar to those on the normal and lognormal bivariate data. To study the effects of a strong non-normality on the performance of the KSG estimator, in Figures 4, 5, and 6, we present the results for the case of non-linear transformation for the normal, lognormal, and Student-t bivariate variables using , rule. From these plots, one can conclude that in all cases the KSG estimator shows significant bias and fails to converge to the analytical value even for . The bias does not disappear asymptotically and the confidence intervals similarly converge onto the biased estimate, leaving out the correct analytical value. This may lead to estimation errors for any confidence intervals for which is a function of but does not, on average, correct for the bias in point estimates.

Using a smaller number of runs , we estimate that even for the data length the bias of the estimator is about in the case of cubic transformation of the lognormal data, and even worse in the case of the transformed Student-t data. It is worth noting that in the case of , transformations, the performance of the KSG estimator is significantly better.

3 Application & Example

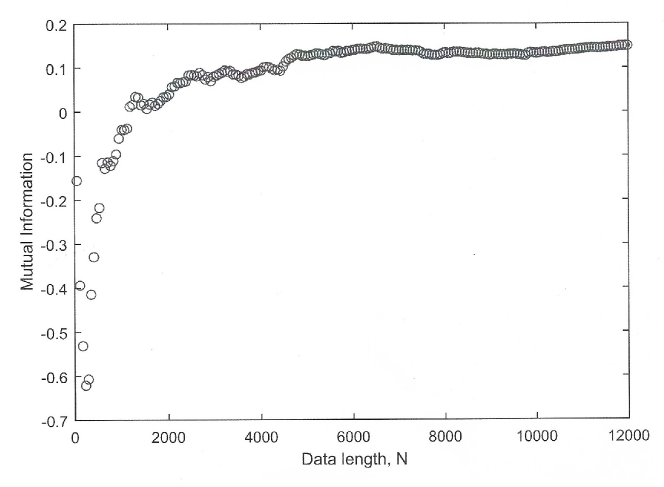

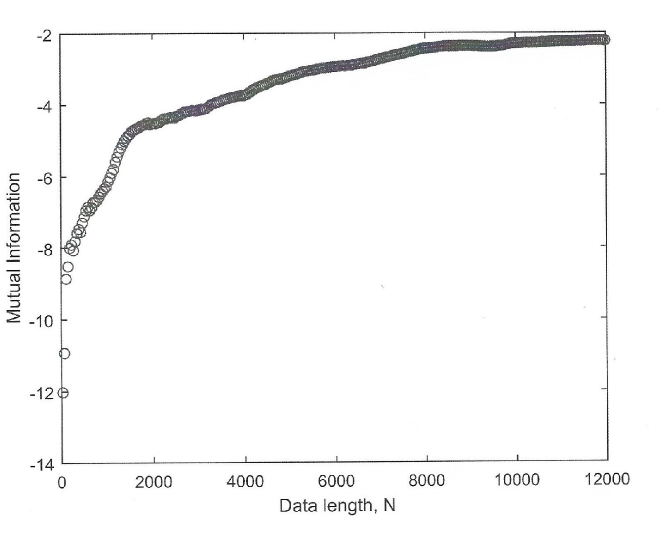

Many phenomena in economics, finance, and other areas follow an empirical power law such as income, wealth, size of cities, and much more [24]. In finance, many studies find that the stock returns distribution has characteristics of non-normal generating processes, especially resembling those more fat-tailed than normal distributions or exhibiting some power law behavior [25] [26] [27]. For example, cross-correlation analysis between volume change and price change in financial markets [28] may help to understand their internal structure and dynamics. As such, calculating the empirical mutual information between some characteristic (e.g. prices and volume changes, etc.) of two strongly non-normal variables can run into misleading estimations. This can especially be a problem when making comparisons or performing analyses on second (i.e. variance) and higher moments (e.g. skewness, kurtosis). As a practical example, we consider daily price data for the Coca-Cola and McDonald’s stocks [22] from 1/2/1970 to 11/8/2017. The empirical correlation coefficient between the stock’s log returns is , corresponding to an analytic solution of if the variables were bivariate normal; as can be seen from Figure 7, the empirical MI is slightly higher than the analytical estimate of due to the variables’ non-normality. In Figure 7 we plot the estimated MI value between the log returns of CocaCola and McDonald’s stocks as a function of the data length. We used a simple pair bootstrapping of the data and averaging over samples, which results in a smoother convergence behavior in Figure 7. Finally, in Figure 8, we compute the between the transformed log returns of Coca-Cola stock using the cubic nonlinearity, and the log returns of McDonald’s stock. The result displays a severe bias problem, ultimately converging to a estimate of less than 0.

4 Conclusion

We performed numerical estimations of the mutual information measure and their corresponding confidence intervals (CI). The presented results allow us to draw several conclusions. First, in the case of relatively short data length , the Kraskov-Stoegbauer-Grassberger estimator is not reliable, especially in cases of strongly non-normal data. Our results suggest that the estimator can be considerably improved through a simple bootstrapping of the data. The simple plugin estimator has even poorer performance, when compared to the KSG approach, generating very large CIS, and is unreliable in the case of non-normal data even with a very large sample length . In the case of large data samples one still should carefully estimate the mutual information measure confidence intervals, in particular, for data with a power-law scaling, since, in this case, the Kraskov-Stoegbauer-Grassberger estimator may produce significant bias. These performance issues and biases are present in both empirical data as well as simulated data. In this case, one possible way to estimate the bias is to plot the MI estimates for different data lengths on a scale and extrapolate in the limit as [23] .

References

- [1] R. A. Fisher, ”Frequency distribution of the values of the correlation coefficient in samples of an indefinitely large population”. Biometrika. Biometrika Trust. 10 (4) : 507-521, (1915).

- [2] R. A. Fisher, ”On the ’probable error’ of a Coefficient of correlation deduced from a small sample”, Metron. 1: 3-32, (1921).

- [3] C.-D. Lai, J. C. W. Rayner and T. P. Hutchinson, ”Properties of the sample correlation of the bivariate lognormal distribution”, Journal of Applied Mathematics and Decision Sciences, 3 (1), 7-19 (1999).

- [4] C. R. Shannon, ”A Mathematical Theory of Communication”, The Bell System Technical Journal, Vol. 27, 379423, 623-656, (1948).

- [5] C. E. Shannon, and W. Weaver, ”The mathematical theory of communication”, University of Illinois Press, Urbana, Illinois. (1949).

- [6] S. Kullback, R. A. Leibler, ”On information and sufficiency”, Annals of Mathematical Statistics. 22 (1), 79-86, (1951).

- [7] T. Blumentritt, F. Schmid, ”Mutual information as a measure of multivariate association: analytical properties and statistical estimation”, Journal of Statistical Computation and Simulation, Volume 82, Issue 9, 1257-1274 (2012).

- [8] A. Dionisio, R. Menezes, D. A. Mendes, ”Mutual information: a measure of dependency for nonlinear time series”, Physica A: Statistical Mechanics and its Applications, Volume 344, Issues 1-2, Pages 326-329, (2004).

- [9] W. Li, ”Mutual Information Functions versus Correlation Functions”, Journal of Statistical Physics, Vol. 60. lvos. 5/6. (1990).

- [10] R. Menezes, A. Dionisio, H. Hassani, ”On the globalization of stock markets: An application of Vector Error Correction Model, Mutual Information and Singular Spectrum Analysis to the G7 Countries”, The Quarterly Review of Economics and Finance, Volume 52, Issue 4, Pages 369-384, (2012).

- [11] P. Fiedor, ”Networks in financial markets based on the mutual information rate”, Phys. Rev. E 89, 052801, (2014).

- [12] N. J. I. Mars et al., ”Time delay estimation in non-linear systems using average amount of mutual information analysis”, Signal Processing, Vol. 4, 139–153, (1982).

- [13] S.-H. Jin, P. Lin, M. Hallett, ”Linear and nonlinear information flow based on time-delayed mutual information method and its application to corticomuscular interaction”, Clinical Neurophysiology, Volume 121, Issue 3, 392-401, (2010).

- [14] H. -M. Chen, M. K. Arora and P. K. Varshney, ”Mutual information-based image registration for remote sensing data”, International Journal of Remote Sensing, Volume 24, Issue 18, 3701-3706, (2003).

- [15] A. Kraskov, H. Stoegbauer, R. G. Andrzejak and P. Grassberger, ”Hierarchical clustering using mutual information”, Europhysics Letters, Volume 70, Number 2, 278, (2005).

- [16] A. Rhee, R. Cheong, A. Levchenko, ”The application of information theory to biochemical signaling systems”, Physical biology, 9 (4), (2012).

- [17] J. Hausser, K. Strimmer, ”Entropy Inference and the James-Stein Estimator, with Application to Nonlinear Gene Association Networks”, Journal of Machine Learning Research 10, 1469-1484, (2009).

- [18] L. Paninski, ”Estimation of Entropy and Mutual Information”, Neural Computation, 15, 1191-1253 (2003).

- [19] R. Moddemeijer, ”On estimation of entropy and mutual information of continuous distributions”, Signal Processing 16, 233-248 (1989).

- [20] R. S. Calsaverini, R. Vicente, ”An information-theoretic approach to statistical dependence: Copula information”, Europhysics Letters, 88 (6), 68003, (2009).

- [21] A. Kraskov, H. Stoegbauer, and P. Grassberger, ”Estimating mutual information”, Phys. Rev. E 69, 066138, (2004) ; Erratum Phys. Rev. E 83, 019903 (2011).

- [22] We used the publically available daily stocks data at https://finance.yahoo.com/.

- [23] N. D. Drummond, R. J. Needs, A. Sorouri, and W. M. C. Foulkes, ”Finite-size errors in continuum quantum Monte Carlo calculations”, Phys. Rev. B 78, 125106 (2008) ; Erratum Phys. Rev. B 90, 159901 (2014).

- [24] X. Gabaix, Power Laws in Economics and Finance,” Annual Review of Economics. 2009 (1) , 255-293.

- [25] E. F. Fama, The Behavior of Stock Market Prices,” Journal of Business, 37 (January 1965), 34-105.

- [26] J. Teichmoeller, Distribution of Stock Price Changes,” Journal of the American Statistical Association, 66 (June 1971), 282-4.

- [27] R. R. Officer, The Distribution of Stock Returns,” Journal of the American Statistical Association, 67 (December 1972), 807-812.

- [28] B. Podobnik, D. Horvatic, A. M. Petersen, and H. E. Stanley, PNAS, 106, 22079-22084 (2009).