Differentiable Discrete Event Simulation

for Queuing Network Control

Ethan Che Jing Dong Hongseok Namkoong

Columbia Business School

{eche25, jing.dong, namkoong}@gsb.columbia.edu

Abstract

Queuing network control is essential for managing congestion in job-processing systems such as service systems, communication networks, and manufacturing processes. Despite growing interest in applying reinforcement learning (RL) techniques, queueing network control poses distinct challenges, including high stochasticity, large state and action spaces, and lack of stability. To tackle these challenges, we propose a scalable framework for policy optimization based on differentiable discrete event simulation. Our main insight is that by implementing a well-designed smoothing technique for discrete event dynamics, we can compute policy gradients for large-scale queueing networks using auto-differentiation software (e.g., Tensorflow, PyTorch) and GPU parallelization. Through extensive empirical experiments, we observe that our policy gradient estimators are several orders of magnitude more accurate than typical -based estimators. In addition, we propose a new policy architecture, which drastically improves stability while maintaining the flexibility of neural-network policies. In a wide variety of scheduling and admission control tasks, we demonstrate that training control policies with pathwise gradients leads to a 50-1000x improvement in sample efficiency over state-of-the-art RL methods. Unlike prior tailored approaches to queueing, our methods can flexibly handle realistic scenarios, including systems operating in non-stationary environments and those with non-exponential interarrival/service times.

1 Introduction

Queuing models are a powerful modeling tool to conduct performance analysis and optimize operational policies in diverse applications such as service systems (e.g., call centers [1], healthcare delivery systems [6], ride-sharing platforms [9], etc), computer and communication systems [45, 76], manufacturing systems [86], and financial systems (e.g., limit order books [24]). Standard tools for queuing control analysis involve establishing structural properties of the underlying Markov decision process (MDP) or leveraging analytically more tractable approximations such as fluid [28, 18] or diffusion approximations [47, 89, 48, 68]. These analytical results often give rise to simple control policies that are easy to implement and interpret. However, these policies only work under restrictive modeling assumptions and can be highly sub-optimal outside of these settings. Moreover, deriving a good policy for a given queuing network model requires substantial queuing expertise and can be theoretically challenging.

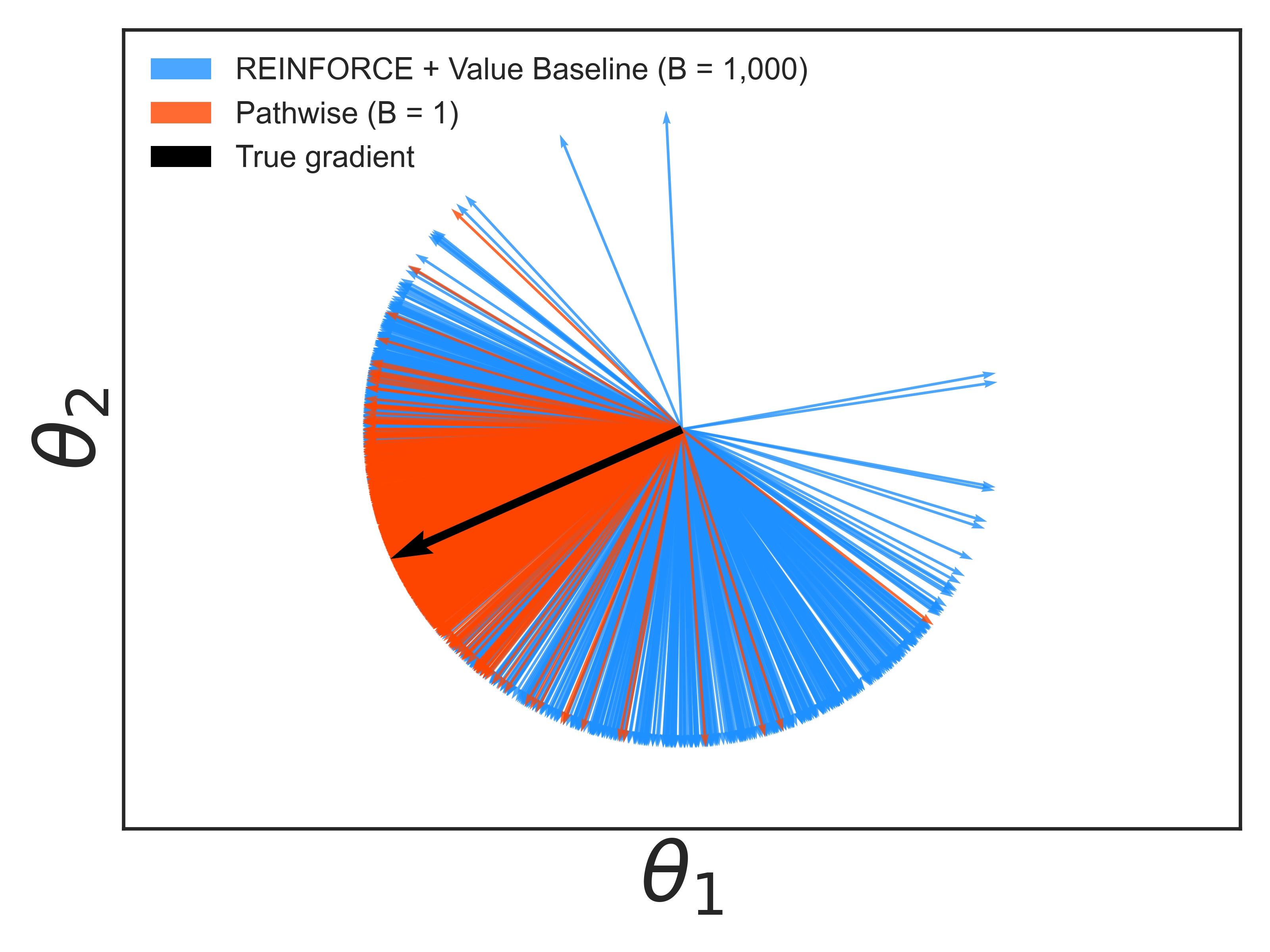

Recent advances in reinforcement learning (RL) have spurred growing interest in applying learning methodologies to solve queuing control problems, which benefit from increased data and computational resources [26, 98, 64]. These algorithms hold significant potential for generating effective controls for complex, industrial-scale networks encountered in real-world applications, which typically fall outside the scope of theoretical analysis. However, standard model-free RL algorithms [84, 82, 72] often under-perform in queuing control, even when compared to simple queuing policies [78, 64], unless proper modifications are made. This under-performance is primarily due to the unique challenges posed by queuing networks, including (1) high stochasticity of the trajectories, (2) large state and action spaces, and (3) lack of stability guarantees under sub-optimal policies [26]. For example, when applying policy gradient methods, typical policy gradient estimators based on coarse feedback from the environment (observed costs) suffer prohibitive error due to high variability (see, e.g., the estimators in Figure 1).

To tackle the challenges in applying off-the-shelf RL solutions for queuing control, we propose a new scalable framework for policy optimization that incorporates domain-specific queuing knowledge. Our main algorithmic insight is that queueing networks possess key structural properties that allow for several orders of magnitude more accurate gradient estimation. By leveraging the fact that the dynamics of discrete event simulations of queuing networks are governed by observed exogenous randomness (interarrival and service times), we propose a differentiable discrete event simulation framework. This framework enables the computation of a gradient of a performance objective (e.g., cumulative holding cost) with respect to actions.

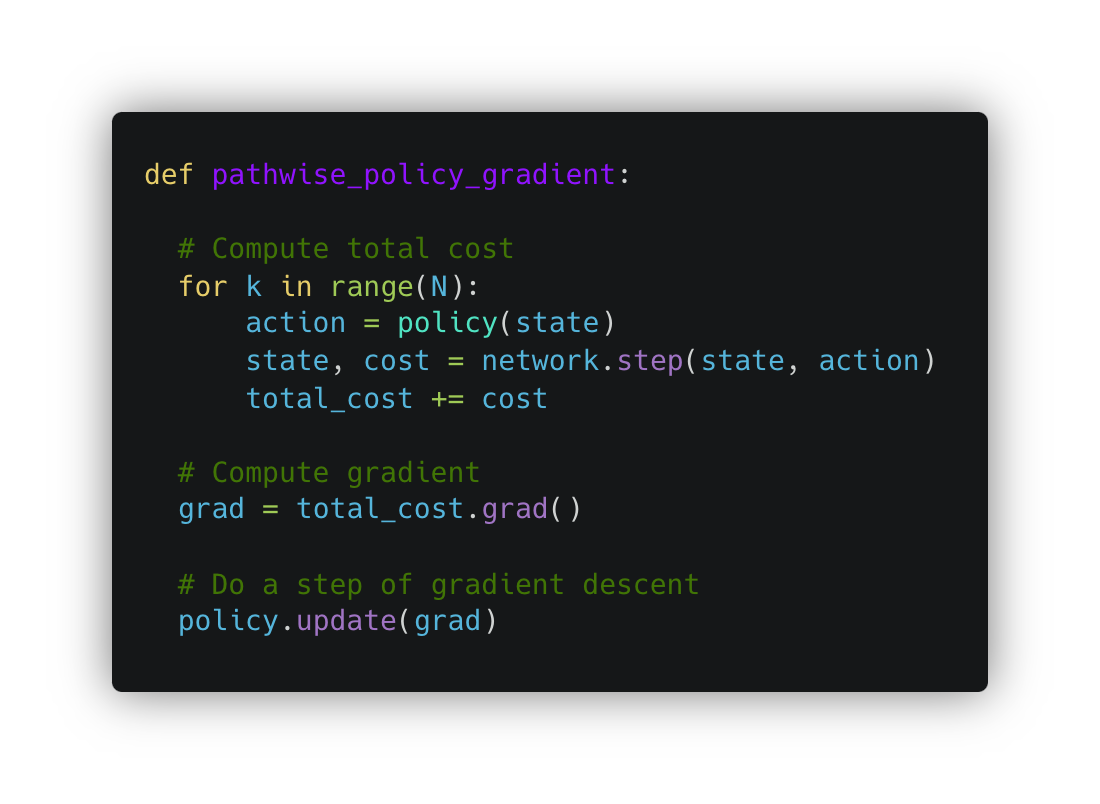

Our proposed gradient estimator, denoted as the estimator, can then be used to efficiently optimize the parameters of a control policy through stochastic gradient descent (SGD). By utilizing the known structure of queuing network dynamics, our approach provides finer-grained feedback on the sensitivity of the performance objective to any action taken along the sample path. This offers an infinitesimal counterfactual analysis: how the performance metric would change if the scheduling action were slightly perturbed. Rather than relying on analytic prowess to compute these gradients, we utilize the rapid advancements in scalable auto-differentiation libraries such as PyTorch [77] to efficiently compute gradients over a single sample path or a batch of sample paths. Our proposed approach supports very general control policies, including neural network policies, which have the potential to improve with more data and computational resources. Notably, our method seamlessly handles large-scale queuing networks and large batches of data via GPU parallelization. Unlike off-the-shelf RL solutions whose performance is exceedingly sensitive to implementation details [56, 58], our method is easy to implement (see e.g., Figure 2) and requires minimal effort for parameter tuning.

Across a range of queueing networks, we empirically observe that our estimator substantially improves the sample efficiency and stability of learning algorithms for queuing network control while preserving the flexibility of learning approaches. In Figure 1, we preview our main empirical findings which show that gradients lead to a 50-1000x improvement in sample efficiency over model-free policy gradient estimators (e.g., [101]). Buoyed by the promising empirical results, we provide several theoretical insights explaining the observed efficiency gains.

Our proposed approach draws inspiration from gradient estimation strategies developed in the stochastic modeling and simulation literature, particularly infinitesimal perturbation analysis (IPA) [35, 52, 60]. While IPA has been shown to provide efficient gradient estimators for specific small-scale queuing models (e.g., the queue), it is well-known that unbiased IPA estimates cannot be obtained for general multi-class queuing networks due to non-differentiability of the sample path [15, 32, 33]. Our framework overcomes this limitation by proposing a novel smoothing technique based on insights from fluid models/approximations for queues and tools from the machine learning (ML) literature. To the best of our knowledge, our method is the first to provide a gradient estimation framework capable of handling very general and large-scale queuing networks and various control policies. Our modeling approach is based on discrete-event simulation models, and as a result, it can accommodate non-stationary and non-Markovian inter-arrival and service times, requiring only samples instead of knowledge of the underlying distributions.

Our second contribution is a simple yet powerful modification to the control policy architecture. It has been widely observed that training a standard RL algorithm, such as proximal policy optimization [84] (PPO), may fail to converge due to instabilities arising from training with random initialization. To address this issue, researchers have proposed either switching to a stabilizing policy when instability occurs [64] or imitating (behavior cloning) a stabilizing policy at the beginning [26]. However, both methods limit policy flexibility and introduce additional complexity in the training process. We identify a key source of the problem: generic policy parameterizations (e.g., neural network policies) do not enforce work conservation, leading to scenarios where even optimized policies often assign servers to empty queues. To address this, we propose a modification to standard policy parameterizations in deep reinforcement learning, which we refer to as the ‘work-conserving softmax’. This modification is compatible with standard reinforcement learning algorithms and automatically guarantees work conservation. Although work conservation does not always guarantee stability, we empirically observe across many scenarios that it effectively eliminates instability in the training process, even when starting from a randomly initialized neural network policy. This modification not only complements our gradient estimator but is also compatible with other model-free RL approaches. We find that while PPO without any modifications fails to stabilize large queuing networks and leads to runaway queue lengths, PPO with the work-conserving softmax remains stable from random initialization and can learn better scheduling policies than traditional queuing policies.

Since rigorous empirical validation forms the basis of algorithmic progress, we provide a thorough empirical validation of the effectiveness of the differentiable discrete event simulator for queuing network control. We construct a wide variety of benchmark control problems, ranging from learning the -rule in a simple multi-class queue to scheduling and admission control in large-scale networks. Across the board, we find that our proposed gradient estimator achieves significant improvements in sample efficiency over model-free alternatives, which translate to downstream improvements in optimization performance.

-

•

In a careful empirical study across 10,800 parameter settings, we find that for 94.5% of these settings our proposed gradient estimator computed along a single sample path achieves greater estimation quality than with 1000x more data (see section 5.1).

-

•

In a scheduling task in multi-class queues, gradient descent with gradient estimator better approximates the optimal policy (the -rule) and achieves a smaller average cost than with a value function baseline and 1000x more data (see section 5.2).

- •

-

•

For large-scale scheduling problems, policy gradient with gradient estimator and work-conserving softmax policy architecture achieves a smaller long-run average holding cost than traditional queuing policies and state-of-the-art RL methods such as , which use 50x more data (see section 7). Performance gains are greater for larger networks with non-exponential noise.

These order-of-magnitude improvements in sample efficiency translate to improved computational efficiency when drawing trajectories from a simulator and improved data efficiency if samples of event times are collected from a real-world system.

Overall, these results indicate that one can achieve significant improvements in sample efficiency by incorporating the specific structure of queuing networks, which is under-utilized by model-free reinforcement learning methods. In section 8, we investigate the queue as a theoretical case study and show that even with an optimal baseline, has a sub-optimally large variance under heavy traffic compared to a pathwise policy gradient estimator. This analysis identifies some of the statistical limitations of , and illustrates that a better understanding of the transition dynamics, rather than narrowly estimating the value-function or -function, can deliver large improvements in statistical efficiency. Given the scarcity of theoretical results comparing the statistical efficiency of different policy gradient estimators, this result may be of broader interest.

Our broad aim with this work is to illustrate a new paradigm for combining the deep, structural knowledge of queuing networks developed in the stochastic modeling literature with learning and data-driven approaches. Rather than either choosing traditional queuing policies, which can be effective for certain queueing control problems but do not improve with data, or choosing model-free reinforcement learning methods, which learn from data but do not leverage known structure, our framework offers a favorable midpoint: we leverage structural insights to extract much more informative feedback from the environment, which can nonetheless be used to optimize black-box policies and improve reliability. Beyond queuing networks, our algorithmic insight provides a general-purpose tool for computing gradients in general discrete-event dynamical systems. Considering the widespread use of discrete-event simulators with popular modeling tools such as AnyLogic [94] or Simio [87] and open-source alternatives such as SimPy [69], the tools developed in this work can potentially be applied to policy optimization problems in broader industrial contexts.

The organization of this paper is as follows. In section 2, we discuss connections with related work. In section 3, we introduce the discrete-event dynamical system model for queuing networks. In section 4, we introduce our framework for gradient estimation. In section 5, we perform a careful empirical study of our proposed gradient estimator, across estimation and optimization tasks. In section 6, we discuss the instability issue in queuing control problems and our proposed modification to the policy architecture to address this. In section 7, we empirically investigate the performance of our proposed pathwise gradient estimation and work-conserving policy architecture in optimizing scheduling policies for large-scale networks. In section 8, we discuss the queue as a theoretical case study concerning the statistical efficiency of compared to estimators. Finally, section 9 concludes the paper and discusses extensions.

2 Related Work

We discuss connections to related work in queuing theory, reinforcement learning, and gradient estimation in machine learning and operations research.

Scheduling in Queuing Networks

Scheduling is a long-studied control task in the queuing literature for managing queues with multiple classes of jobs [48, 70]. Standard policies developed in the literature include static priority policies such as the -rule [25], threshold policies [80], policies derived from fluid approximations [7, 20, 71], including discrete review policies [46, 67], policies that have good stability properties such as MaxWeight [89] and MaxPressure [27]. Many of these policies satisfy desirable properties such as throughput optimality [93, 5], or cost minimization [25, 68] for certain networks and/or in certain asymptotic regimes. In our work, we aim to leverage some of the theoretical insights developed in this literature to design reinforcement learning algorithms that can learn faster and with less data than model-free RL alternatives. We also use some of the standard policies as benchmark policies when validating the performance of our policy gradient algorithm.

Reinforcement Learning in Queueing Network Control

Our research connects with the literature on developing reinforcement learning algorithms for queuing network control problems [73, 85, 79, 26, 64, 100, 78]. These works apply standard model-free RL techniques (e.g. -learning, , value iteration, etc.) but introduce novel modifications to address the unique challenges in queuing network control problems. Our work differs in that we propose an entirely new methodology for learning from the environment based on differentiable discrete event simulation, which is distinct from all model-free RL methods. The works [85, 64, 26, 78] observe that RL algorithms tend to be unstable and propose fixes to address this, such as introducing a Lyapunov function into the rewards, or behavior cloning of a stable policy for initialization. In our work, we propose a simple modification to the policy network architecture, denoted as the work-conserving softmax as it is designed to ensure work-conservation. We find empirically that work-conserving softmax ensures stability with even randomly initialized neural network policies. In our empirical experiments, we primarily compare our methodology with the algorithm developed in [26]. In particular, we construct a baseline with the same hyper-parameters, neural network architecture, and variance reduction techniques as in [26], although with our policy architecture modification that improves stability.

Differentiable Simulation in RL and Operations Research

While differentiable simulation is a well-studied paradigm for control problems in physics and robotics [50, 55, 90, 53, 81], it has only recently been explored for large-scale operations research problems. For instance, [66, 2] study inventory control problems and train a neural network using direct back-propagation of the cost, as sample paths of the inventory levels are continuous and differentiable in the actions. In our work, we study control problems for queuing networks, which are discrete and non-differentiable, preventing the direct application of such methods. To address this, we develop a novel framework for computing pathwise derivatives for these non-differentiable systems, which proves highly effective for training control policies. Another line of work, including [3, 4], proposes differentiable agent-based simulators based on differentiable relaxations. While these relaxations have shown strong performance in optimization tasks, they also introduce unpredictable discrepancies with the original dynamics. We introduce tailored differentiable relaxations in the back-propagation process only, ensuring that the forward simulation remains true to the original dynamics.

Gradient Estimation in Machine Learning

Gradient estimation [74] is an important sub-field of the machine learning literature, with applications in probabilistic modeling [61, 59] and reinforcement learning [101, 92]. There are two standard strategies for computing stochastic gradients [74]. The first is the score-function estimator or [101, 92], which only requires the ability to compute the gradient of log-likelihood but can have high variance [44]. Another strategy is the reparameterization trick [61], which involves decomposing the random variable into the stochasticity and the parameter of interest, and then taking a pathwise derivative under the realization of the stochasticity. Gradient estimators based on the reparameterization trick can have much smaller variance [74], but can only be applied in special cases (e.g. Gaussian random variables) that enable this decomposition. Our methodology makes a novel observation that for queuing networks, the structure of discrete-event dynamical systems gives rise to the reparameterization trick. Nevertheless, the function of interest is non-differentiable, so standard methods cannot be applied. As a result, our framework also connects with the literature on gradient estimation for discrete random variables [59, 65, 11, 96]. In particular, to properly smooth the non-differentiability of the event selection mechanism, we employ the straight-through trick [11], which has been previously used in applications such as discrete representation learning [97]. Our work involves a novel application of this technique for discrete-event systems, and we find that this is crucial for reducing bias when smoothing over long time horizons.

Gradient Estimation in Operations Research

There is extensive literature on gradient estimation for stochastic systems [35, 36, 39, 14, 33], some with direct application to queuing optimization [63, 42, 33]. Infinitesimal Perturbation Analysis (IPA) [35, 52, 60] is a standard framework for constructing pathwise gradient estimators, which takes derivatives through stochastic recursions that represent the dynamics of the system. While IPA has been applied successfully to some specific queuing networks and discrete-event environments more broadly [91], standard IPA techniques cannot be applied to general queuing networks control problems, as has been observed in [15]. There has been much research on outlining sufficient conditions under which IPA is valid, such as the commuting condition in [35, 36] or the perturbation conditions in [14], but these conditions do not hold in general. Several extensions to IPA have been proposed, but these alternatives require knowing the exact characteristics of the sampling distributions and bespoke analysis of event paths [33, 32]. Generalized likelihood-ratio estimation [39] is another popular gradient estimation framework, which leverages an explicit Markovian formulation of state transitions to estimate parameter sensitivities. However, this requires knowledge of the distributions of stochastic inputs, and even with this knowledge, it may be difficult to characterize the exact Markov transition kernel of the system. Finally, finite differences [31] and finite perturbation analysis [52, 15] are powerful methods, particularly when aided with common random numbers [41, 38], as it requires minimal knowledge about the system. However, it has been observed that performance can scale poorly with problem dimension [37, 41], and we also observe this in an admission control task (see Section 5.3).

Our contribution is proposing a novel, general-purpose framework for computing pathwise gradients through careful smoothing, which only requires samples of random input (e.g., interarrival times and service times) rather than knowledge of their distributions. Given the negative results about the applicability of IPA for general queuing network control problems (e.g., general queuing network model and scheduling policies), we introduce bias through smoothing to achieve generality. It has been observed in [29] that biased IPA surrogates can be surprisingly effective in simulation optimization tasks such as ambulance base location selection. Our extensive empirical results confirm this observation and illustrate that while there is some bias, it is very small in practice, even over long time horizons ( steps).

3 Discrete-Event Dynamical System Model for Queuing Networks

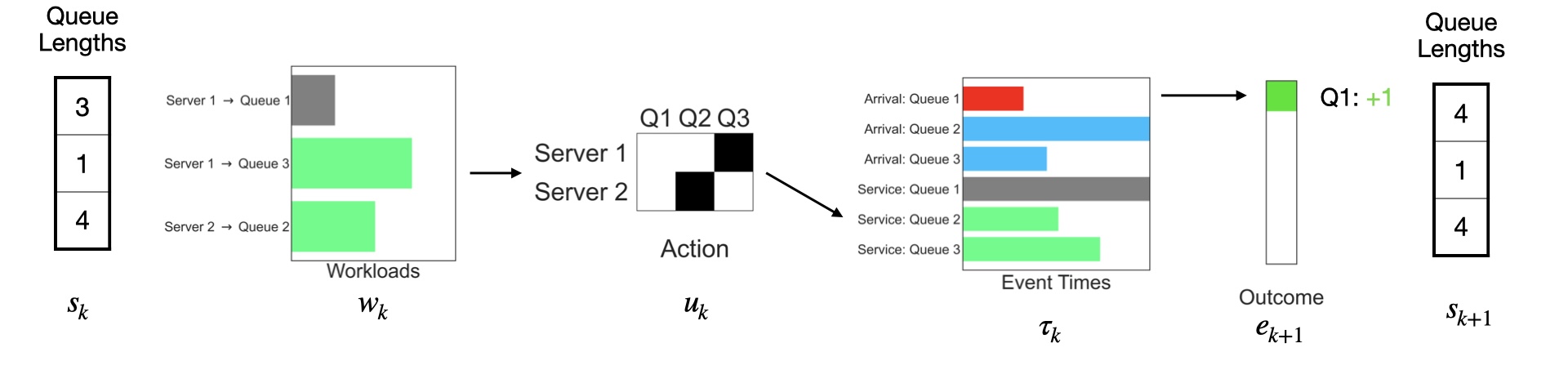

We describe multi-class queuing networks as discrete-event dynamical systems. This is different from the standard Markov chain representation, which is only applicable when inter-arrival and service times are exponentially distributed. To accommodate more general event-time distributions, the system description not only involves the queue lengths, but also auxiliary information such as residual inter-arrival times and workloads. Surprisingly, this more detailed system description leads to a novel gradient estimation strategy (discussed in Section 4) for policy optimization.

We first provide a brief overview of the basic scheduling problem. We then describe the discrete-event dynamics of multi-class queuing networks in detail and illustrate with a couple of well-known examples. While queuing networks have been treated as members of a more general class of Generalized Semi-Markov Processes (GSMPs) that reflect the discrete-event structure of these systems [40], we introduce a new set of notations tailored for queuing networks to elaborate on some of their special structures. In particular, we represent the discrete event dynamics via matrix-vector notation that maps directly to its implementation in auto-differentiation frameworks, allowing for the differentiable simulation of large-scale queueing networks through GPU parallelization.

3.1 The Scheduling Problem

A multi-class queuing network consists of queues and servers. The core state variable is the queue lengths associated with each queue, denoted as , which evolves over continuous time. As a discrete-event dynamical system, the state also includes auxiliary data denoted as — consisting of residual inter-arrival times and workloads at time —which determines state transitions but are typically not visible to the controller.

The goal of the controller is to route jobs to servers, represented by an assignment matrix , to manage congestion. More concretely, the problem is to derive a policy , which only depends on the observed queue lengths and selects scheduling actions, to minimize the integral of some instantaneous costs . A typical instantaneous cost is a linear holding/waiting cost:

for some vector . The objective is to find a policy that minimizes the cumulative cost over a time horizon:

| (1) |

Optimizing a continuous time objective can be difficult and may require an expensive discretization procedure. However, discrete-event dynamical systems are more structured in that is piecewise constant and is only updated when an event occurs. For the multi-class queuing networks, events are either arrivals to the network or job completions, i.e., a server finishes processing a job.

It is then sufficient to sample the system only when an event occurs, and we can approximate the continuous-time objective with a performance objective in the discrete-event system over events,

| (2) |

where is the queue lengths after the th event update. is an inter-event time that measures the time between the th and th event, and is chosen such that the time of the th event, a random variable denoted as , is “close” to .

The dynamics of queuing networks are highly stochastic, with large variations across trajectories. Randomness in the system is driven by the random arrival times of jobs and the random workloads (service requirements) of these jobs. We let denote a single realization, or ‘trace’, of these random variables over the horizon of events. We can then view the expected cost (2) more explicitly as a policy cost averaged over traces. In addition, we focus on a parameterized family of policies , for some , in order to optimize (2) efficiently. In this case, we utilize the following shorthand for the policy cost over a single trace and for the average policy cost under , which leads to the parameterized control problem:

| (3) |

We now turn to describe the structure of the transition dynamics of multi-class queuing networks, to elaborate how scheduling actions affect the queue lengths.

3.2 System Description

Recall that the multi-class queuing network consists of queues and servers, where each queue is associated with a job class, and different servers can be of different compatibilities with various job classes. Recall that denotes the lengths of the queues at time . The queue lengths are updated by one of two types of events: job arrivals or job completions. Although the process evolves in continuous time, it is sufficient to track the system only when an event occurs. We let count the th event in the system, and let denote the time immediately after the th event occurs. By doing so, we arrive at a discrete-time representation of the system. Given that we do not assume event times are exponential, the queue lengths alone are not a Markovian descriptor of the system. Instead, we must consider an augmented state , where is the vector of queue lengths and is an auxiliary state vector that includes residual inter-arrival times and residual workloads of the ‘top-of-queue’ jobs in each queue. The auxiliary state variables determine the sequence of events.

More explicitly, for each queue , the residual inter-arrival time keeps track of the time remaining until the next arrival to queue occurs. Immediately after an arrival to queue occurs, the next inter-arrival time is drawn from a probability distribution . When a job arrives to queue , it comes with a workload (service requirement) drawn from a distribution . We allow the distributions ’s and ’s to vary with time, i.e., the interarrival times and service requirements can be time-varying. For notational simplicity, we will not explicitly denote the time dependence here. We refer to the residual workload at time of the top-of-queue job in queue as , which specifies how much work must be done before the job completion. A job is only processed if it is routed to a server , in which case the server processes the job at a constant service rate . We refer to as the matrix of service rates. Under this scheduling decision, the residual processing time, i.e., the amount of time required to process the job, is .

The augmented state is a valid Markovian descriptor of the system and we now describe the corresponding transition function such that

where is an action taken by the controller and contains external randomness arising from new inter-arrival times or workloads drawn from ’s or ’s depending on the event type.

The transition is based on the next event, which is the event with the minimum residual time. The controller influences the transitions through the processing times, by deciding which jobs get routed to which servers. We focus on scheduling problems where the space of controls are feasible assignments of servers to queues. Let denote an -dimensional vector consisting of all ones. The action space is,

| (4) |

where is the topology of the network, which indicates which job class can be served by which server. Following existing works on scheduling in queuing networks [70], we consider networks for which each job class has exactly 1 compatible server.

Assumption A.

For every queue , there is 1 compatible server, i.e., .

Given an action , the residual processing time is when and when . This can be written compactly as

| (5) |

where extracts the diagonal entries of the matrix .

As a result, at time the residual event times consists of the residual inter-arrival and processing times,

We emphasize that depends on the action . The core operation in the transition dynamics is the event selection mechanism. The next event is the one with the minimum residual time in . We define to be a one-hot vector representing the of – the position of the minimum in :

| (Event Select) |

indicates the type of the th event. In particular, if the minimum residual event time is a residual inter-arrival time, then the next event is an arrival to the system. If it is a residual job processing time, then the next event is a job completion. We denote to be the inter-event time, which is equal to the minimum residual time:

| (Event Time) |

is the time between the th and th event, i.e. .

After the job is processed by a server, it either leaves the system or proceeds to another queue. Let denote the routing matrix, where the jth column, details the change in the queue lengths when a job in class finishes service. For example, for a tandem queue with two queues, the routing matrix is

indicating that when a job in the first queue completes service, it leaves its own queue and joins the second queue. When a job in the second queue completes service, it leaves the system.

We define the event matrix as a block matrix of the form

where is the identity matrix. The event matrix determines the update to the queue lengths, depending on which event took place. In particular, when the th event occurs, the update to the queue lengths is

| (Queue Update) |

Intuitively, the queue length of queue increases by when the next event is a class job arrival; the queue lengths update according to when the next event is a queue job completion.

The updates to the auxiliary state is typically given by

| (Aux Update) |

where is the element-wise product and are new inter-arrival times and are workloads . Intuitively, after an event occurs, we reduce the residual inter-arrival times by the inter-event time. We reduce workloads by the amount of work applied to the job, i.e., the inter-event time multiplied by the service rate of the allocated server. Finally, if an arrival occurred we draw a new inter-arrival time; if a job was completed, we draw a new workload for the top-of-queue job (if the queue is non-empty).

There are two boundary cases that make the update slightly different from (Aux Update). First, if a new job arrives at an empty queue (either an external arrival or a transition from a job completion), we also need to update to . Second, if a queue job completion leaves an empty queue behind, we set , indicating that no completions can occur for an empty queue.

Let denote exogenous noise in the environment, which consists of the sampled inter-arrival times and workloads for resetting the time of a completed event,

We finally arrive at the stated goal of describing the transition dynamics of in terms of a function . Notably, all the stochasticity is captured by ’s, which are independent of the states and actions.

It is worth mentioning a few features of this discrete-event representation.

-

•

While auxiliary data is necessary for to be a valid Markovian system descriptor, this information is typically not available to the controller. We assume the controller only observes the queue lengths, i.e., the control policy only depends on .

-

•

The representation can flexibly accommodate non-stationary and non-exponential event-time distributions, i.e., ’s and ’s can be general and time-varying.

-

•

This model enables purely data-driven simulation, as it only requires samples of the event times . One does not need to know the event time distributions ’s and ’s to simulate the system if data of these event times are available.

-

•

The matrix-vector representation enables GPU parallelism, which can greatly speed up the simulation of large-scale networks.

-

•

As we will explain later, this representation enables new gradient estimation strategies.

Queuing Network Examples

As a concrete illustration, we show how a few well-known queuing networks are described as discrete-event dynamical systems.

Example 1: The queue (see Figure 4) with arrival rate and service rate features a single queue and a single server , and exponentially distributed inter-arrival times and workloads, i.e., and respectively. The network topology is , the service rate is , and the routing matrix is , indicating that jobs leave the system after service completion. The scheduling policy is work-conserving, the server always serves the queue when it is non-empty, i.e. . The state update is,

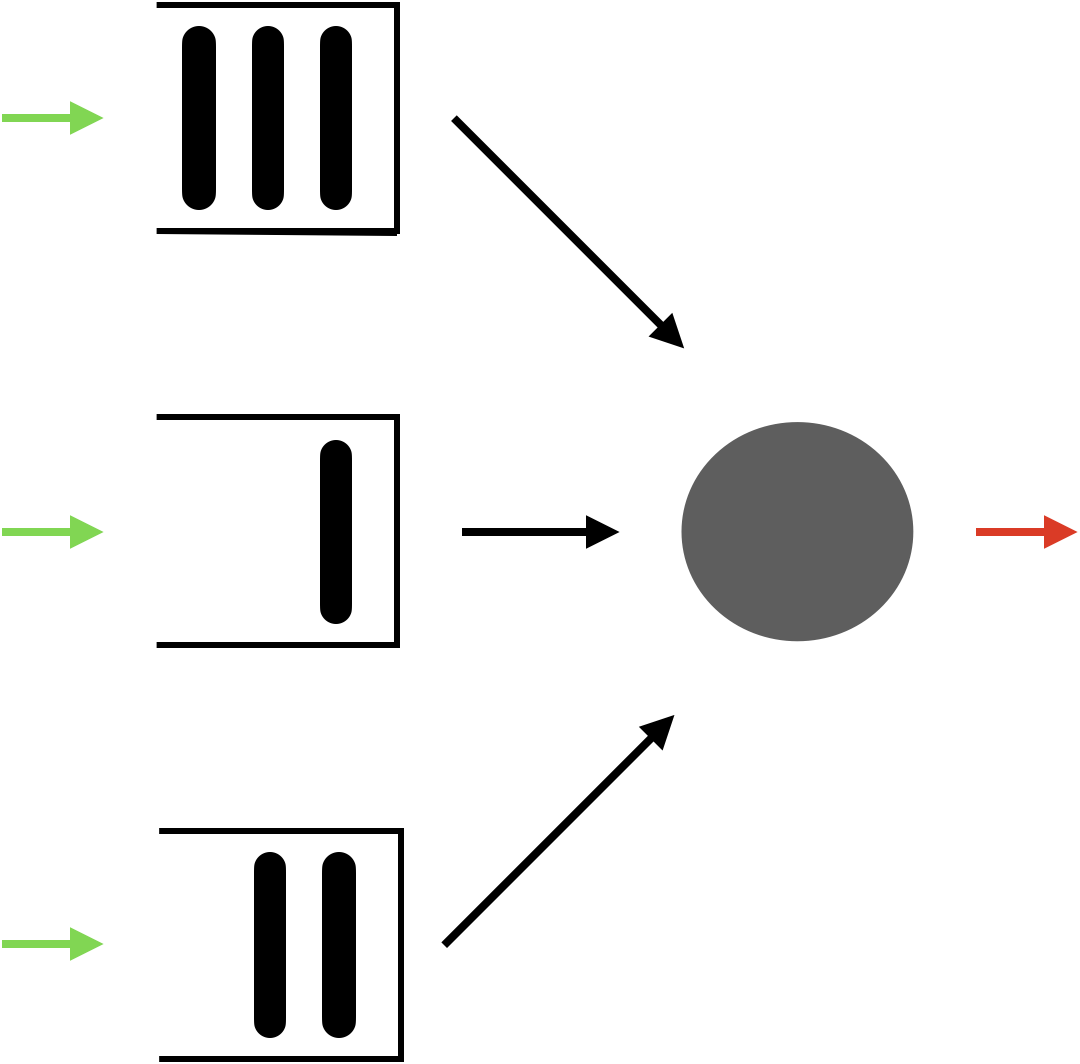

Example 2: The multi-class singer-server queue features an queues and a single server (see Figure 5). While the inter-arrival times and workloads, i.e., ’s are usually exponentially distributed, they can also follow other distributions. The network topology is , the service rates are , and the routing matrix is , indicating that jobs leave the system after service completion. A well-known scheduling policy for this system is the -rule, a static priority rule. Let denote the holding costs. The -rule sets

The state update is,

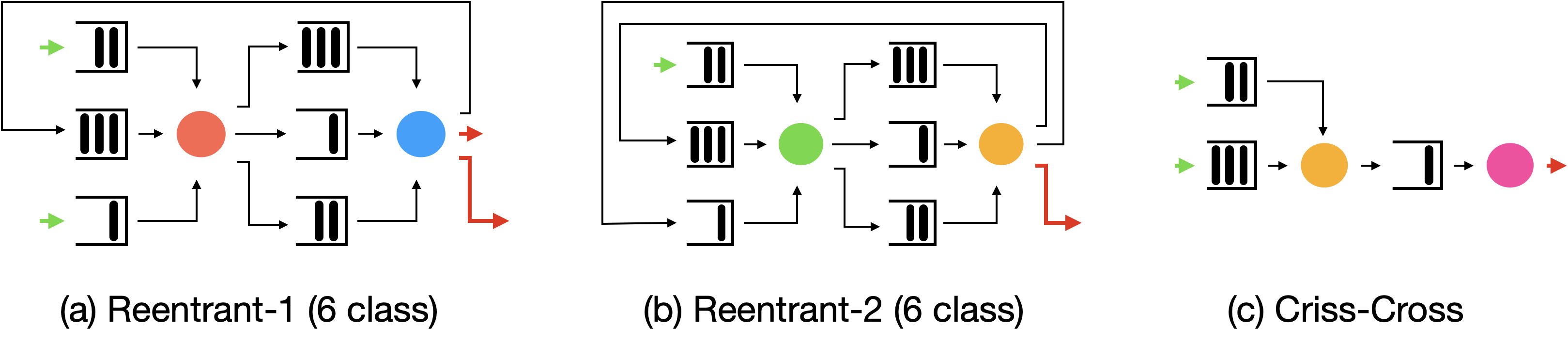

Example 3: The criss-cross network [49] features queues and servers (see Figure 13). External jobs arrive to queues 1 and 3. The first server can serve queues 1 and 3 with service rates and respectively, while the second server is dedicated to serving queue 2 with service rate . After jobs from queue 1 are processed, they are routed to queue 2; jobs from queues 2 and 3 exit the system after service completion. The inter-arrival times and workloads, i.e., ’s, can follow general distributions. The network topology , service rate matrix, and the routing matrix are:

Harrison and Wein [49] develop a work-conserving threshold policy for this system. For a threshold , server 1 prioritizes jobs in queue 1 if the number of jobs in queue 2 is below . Otherwise, it prioritizes queue 3. This gives the scheduling action

and the transition dynamics

Here, since queue 2 has no external arrivals.

4 Gradient Estimation

In this section, we introduce our proposed approach for estimating the gradient of the objective (3), . We start with a brief discussion of existing methods for gradient estimation, including their advantages and limitations. We then outline the main challenges for computing pathwise derivatives in multi-class queuing networks, and introduce our strategy for overcoming these challenges. Finally, we formally define our gradient estimation framework and discuss its computational and statistical properties. Later in section 5, we perform a comprehensive empirical study and find that our gradient estimation framework is able to overcome many of the limitations of existing methods in that (1) it is capable of estimating gradients for general queuing networks, (2) it provides stable gradient estimations over very long horizons ( steps), (3) it provides greater estimation accuracy than model-free policy gradient methods with 1000x less data, and (4) when applying to policy optimization, it drastically improves the performance of the policy gradient algorithm for various scheduling and admission control tasks.

Our goal is to optimize the parameterized control problem (3). A standard optimization algorithm is (stochastic) gradient descent, which has been considered for policy optimization and reinforcement learning [92, 8]. The core challenge for estimating policy gradient from sample paths of the queuing network is that the sample path cost is in general not differentiable in . As a consequence, one cannot change the order of differentiation and expectation, i.e.,

where is not even well-defined. The non-differentiability of these discrete-event dynamical systems emerges from two sources. First, actions are discrete scheduling decisions, and small perturbations in the policy can result in large changes in the scheduling decisions produced by the policy. Second, the actions affect the dynamics through the event times. The ordering of events is based on the ‘’ of the residual event times, which is not differentiable.

In the stochastic simulation literature, there are two popular methods for gradient estimation: infinitesimal perturbation analysis (IPA) and generalized likelihood ratio (LR) gradient estimation. To illustrate, consider abstractly and with a little abuse of notation a system following the dynamics , where is the state, is the parameter of interest, is exogenous stochastic noise, and is a differentiable function. Then, the IPA estimator computes a sample-path derivative estimator by constructing a derivative process via the recursion:

Likelihood-ratio gradient estimation on the other hand uses knowledge of the distribution of to form the gradient estimator. Suppose that is a Markov chain for which the transition kernel is parameterized by , i.e., . For a fixed , let

This allows one to obtain the following gradient estimator:

Despite their popularity, there are limitations to applying these methods to general multi-class queuing networks. While IPA has been proven efficient for simple queuing models, such as the queue through the Lindley recursion, it is well-known that unbiased IPA estimates cannot be obtained for general queuing networks [15, 32, 33]. The implementation of LR gradient estimation hinges on precise knowledge of the system’s Markovian transition kernel [39]. This requires knowledge of the inter-arrival time and workload distributions, and even with this knowledge, it is non-trivial to specify the transition kernel of the queue lengths and residual event times in generic systems. Modifications to IPA [32, 33] also require precise knowledge of event time distributions and often involve analyzing specific ordering of events which must be done on a case-by-case basis. As a result, none of these methods can reliably provide gradient estimation for complex queuing networks under general scheduling policies and with possibly unknown inter-arrival and service time distributions. Yet, the ability to handle such instances is important to solve large-scale problems arising in many applications.

Due to the challenges discussed above, existing reinforcement learning (RL) approaches for queueing network control mainly rely on model-free gradient estimators, utilizing either the estimator and/or -function estimation. As we will discuss shortly, these methods do not leverage the structural properties of queuing networks and may be highly sample-inefficient, e.g., requiring a prohibitively large sample for gradient estimation.

To address the challenges discussed above, we propose a novel gradient estimation framework that can handle general, large-scale multi-class queuing networks under any differentiable scheduling policy, requiring only samples of the event times rather than knowledge of their distributions. Most importantly, our approach streamlines the process of gradient estimation, leveraging auto-differentiation libraries such as PyTorch [77] or Jax [13] to automatically compute gradients, rather than constructing these gradients in a bespoke manner for each network as is required for IPA or LR. As shown in Figure 2, computing a gradient in our framework requires only a few lines of code. To the best of our knowledge, this is the first scalable alternative to model-free methods for gradient estimation in queuing networks.

4.1 The standard approach: the estimator

Considering the lack of differentiability in most reinforcement learning environments, the standard approach for gradient estimation developed in model-free RL is the score-function or estimator [101, 92]. This serves as the basis for modern policy gradient algorithms such as Trust-Region Policy Optimization (TRPO) [82] or Proximal Policy Optimization (PPO) [84]. As a result, it offers a useful and popular baseline to compare our proposed method with.

The core idea behind the estimator is to introduce a randomized policy and differentiate through the action probabilities induced by the policy. Under mild regularity conditions on and , the following expression holds for the policy gradient:

which leads to the following policy gradient estimator:

| () |

While being unbiased, the estimator is known to have a very high variance [99]. The variance arises from two sources. First, the cumulative cost can be very noisy, as has been observed for queuing networks [26]. Second, as the policy converges to the optimal policy, the score function can grow large, magnifying the variance in the cost term. Practical implementations involve many algorithmic add-ons to reduce variance, e.g., adding a ‘baseline’ term [99] which is usually (an estimate of) the value function ,

| () |

These algorithmic add-ons have led to the increased complexity of existing policy gradient implementations [57] and the outsized importance of various hyperparameters [56]. It has even been observed that seemingly small implementation “tricks” can have a large impact on performance, even more so than the choice of the algorithm itself [30].

4.2 Our approach: Differentiable Discrete-Event Simulation

We can view the state trajectory as a repeated composition of the transition function , which is affected by exogenous noise , i.e., stochastic inter-arrival and service times. If the transition function were differentiable with respect to the actions , then under any fixed trace , one could compute a sample-path derivative of the cost using auto-differentiation frameworks such as PyTorch [77] or Jax [13]. Auto-differentiation software computes gradients efficiently using the chain rule. To illustrate, given a sample path of states, actions, and noise , we can calculate the gradient of with respect to via

This computation is streamlined through a technique known as backpropagation, or reverse-mode auto-differentiation. The algorithm involves two steps. The first step, known as the forward pass, evaluates the main function or performance metric (in the example, ’s) and records the partial derivatives of all intermediate states relative to their inputs (e.g. ). This step constructs a computational graph, which outlines the dependencies among variables. The second step is a backward pass, which traverses the computational graph in reverse. It sequentially multiplies and accumulates partial derivatives using the chain rule, propagating these derivatives backward through the graph until the gradient concerning the initial input (in this example, ) is calculated. Due to this design, gradients of functions involving nested compositions can be computed in a time that is linear in the number of compositions. By systematically applying the chain rule in reverse, auto-differentiation avoids the redundancy and computational overhead typically associated with numeric differentiation methods.

However, as mentioned before, the dynamics do not have a meaningful derivative due to the non-differentiability of actions and the operation which selects the next event based on the minimum residual event time. Yet if we can utilize suitably differentiable surrogates, it would be possible to compute meaningful approximate sample-path derivatives using auto-differentiation.

4.2.1 Capacity sharing relaxation

First, we address the non-differentiability of the action space. Recall that are scheduling decisions, which assign jobs to servers. Since lies in a discrete space, a small change in the policy parameters can produce a jump in the actions. To alleviate this, we consider the transportation polytope as a continuous relaxation of the original action space (4):

| (14) |

The set of extreme points of coincide with the original, integral action space . For a fractional action , we can interpret it as servers splitting their capacity among multiple job classes motivated by the fluid approximation of queues [19]. As a relaxation, it allows servers to serve multiple jobs simultaneously. The effective service rate for each job class is equal to the fraction of the capacity allocated to the job class multiplied by the corresponding service rate.

As a result, instead of considering stochastic policies over discrete actions, we approach this problem as a continuous control problem and consider deterministic policies over continuous actions, i.e., the fractional scheduling decisions. Under this relaxation, the processing times are differentiable in the (fractional) scheduling decision. Finally, it is worth mentioning that we only use this relaxation when training policies. For policy evaluation, we enforce that actions are integral scheduling decisions in . To do so, we treat the fractional action as a probability distribution and use it to sample a discrete action.

Definition 1.

Under the capacity sharing relaxation, the service rate for queue under the routing decision is . Thus, given workload , the processing time of the job will be

| (15) |

Note that this is identical to the original definition of the processing times in (5). The only difference is that we now allow fractional routing actions, under which a server can serve multiple jobs at the same time.

For a concrete example, consider a single server compatible with two job classes 1 and 2 with service rates and respectively. Suppose it splits its capacity between job classes 1 and 2 according to and . Then for residual workloads and , the corresponding processing times are and . If and instead, then the corresponding processing times are and .

4.2.2 Differentiable event selection

To determine the next event type, the operation selects the next event based on the minimum residual event time. This operation does not give a meaningful gradient.

Pitfalls of ‘naive’ smoothing

In order to compute gradients of the sample path, we need to smooth the operation. There are multiple ways to do this. A naive approach is to directly replace with a differentiable surrogate. One such popular surrogate is . With some inverse temperature , applied to the vector of residual event times returns a vector in , which we use to replace the event selection operation :

| (Direct Smoothing) |

As , converges to . Thus, one may expect that for large , would give a reliable differentiable surrogate.

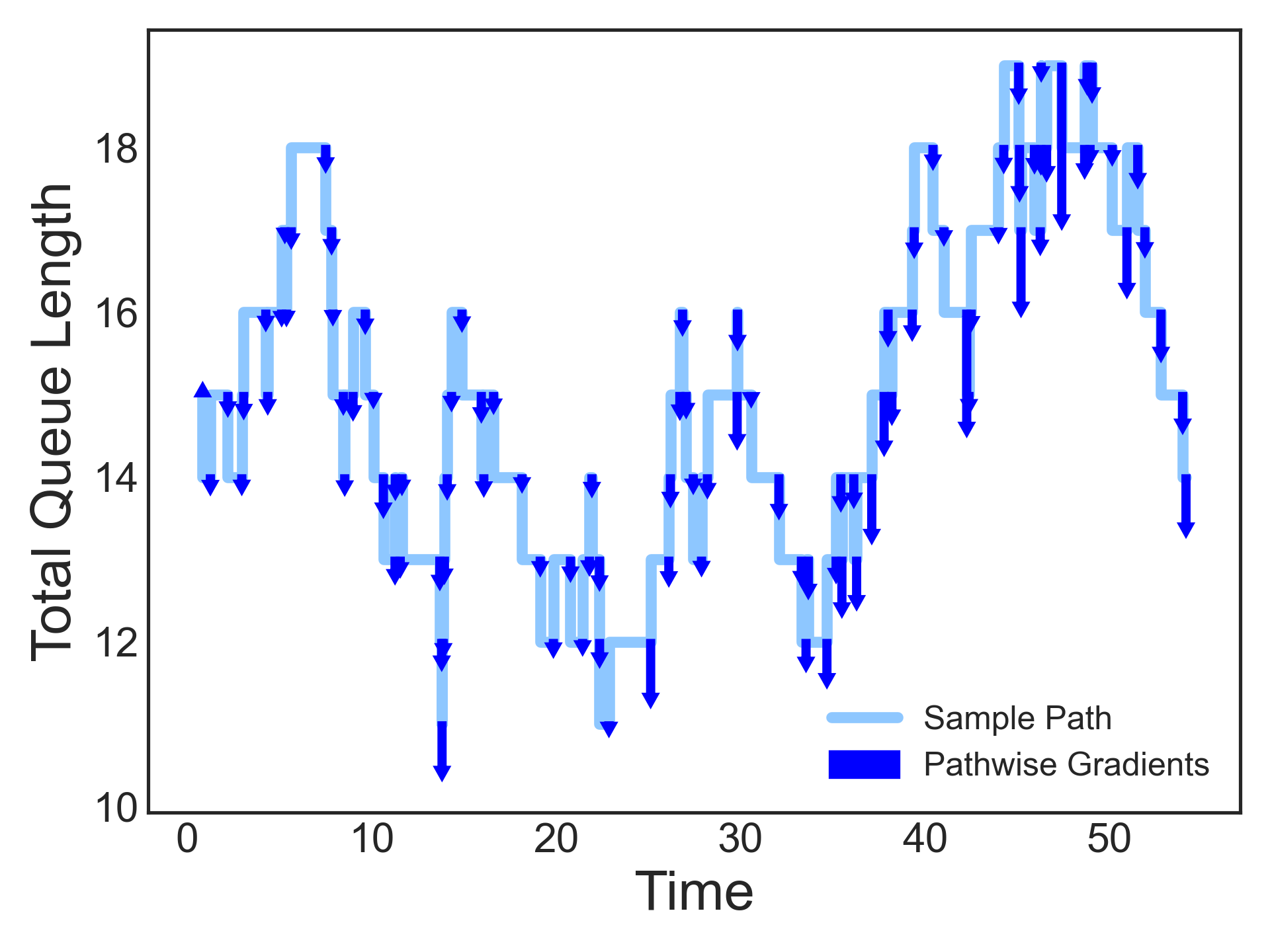

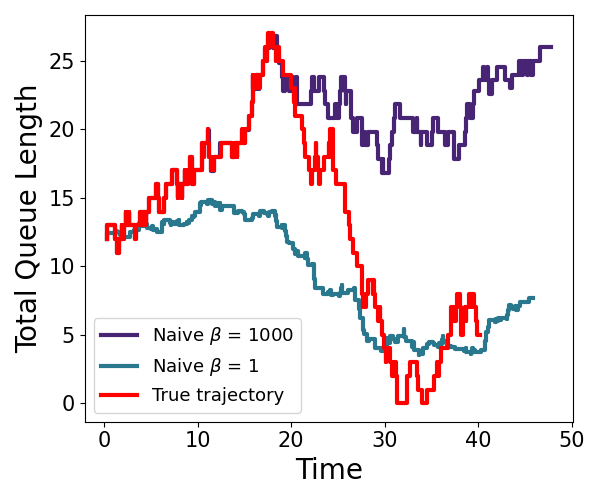

However, queuing networks involve a unique challenge for this approach: one typically considers very long trajectories when evaluating performance in queuing networks, as one is often interested in long-run average or steady-state behavior. Thus, even if one sets to be very large to closely approximate , the smoothing nonetheless results in ‘unphysical’, real-valued queue lengths instead of integral ones, and small discrepancies can accumulate over these long horizons and lead to entirely different sample paths. This can be observed concretely in the left panel of Figure 6, which displays the sample paths of the total queueing length processes for a criss-cross queueing network (in Example 3.2) under the original dynamic and under direct smoothing, using the same inter-arrival and service times. We observe that when setting the inverse temperature , the sample path under direct smoothing is completely different from the original one, even though all of the stochastic inputs are the same. Even when setting a very high inverse temperature, i.e., , for which is almost identical to , the trajectory veers off after only a hundred steps.

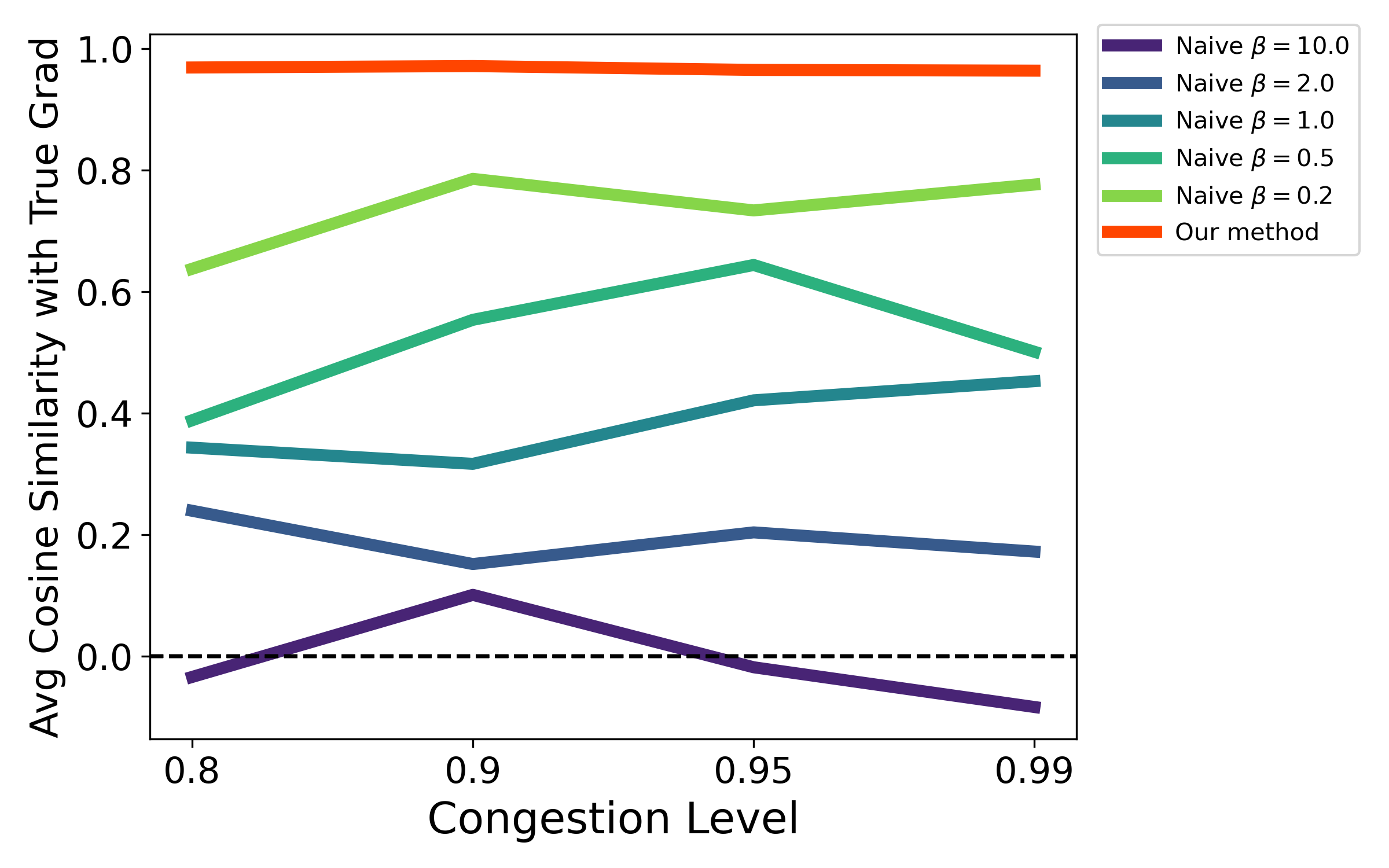

This can greatly affect the quality of the gradient estimation. We observe in the right panel of Figure 6 that across a range of inverse temperatures, the average cosine similarity between the surrogate gradient and the true gradient (defined in (18)) are all somewhat low. In the same plot, we also show the average cosine similarity between our proposed gradient estimator, which we will discuss shortly, and the true gradient. Our proposed approach substantially improves the gradient estimation accuracy, i.e., the average cosine similarity is close to , and as we will show later, it does so across a wide range of inverse temperatures.

Our approach: ‘straight-through’ estimation

The failure of the direct smoothing approach highlights the importance of preserving the original dynamics, as errors can quickly build up even if the differentiable surrogate is only slightly off. We propose a simple but crucial adjustment to the direct smoothing approach, which leads to huge improvements in the quality of gradient estimation.

Instead of replacing the operation with when generating the sample path, we preserve the original dynamics as is, and only replace the Jacobian of with the Jacobian of when we query gradients. In short, we introduce a gradient operator such that

| (16) |

where is respect to the input . This is known as the ‘straight-through’ trick in the machine learning literature and is a standard approach for computing approximate gradients in discrete environments [11, 97]. To the best of our knowledge, this is the first application of this gradient estimation strategy for discrete-event dynamical systems. Using this strategy, we can use the chain rule to compute gradients of performance metrics that depend on the event selection. Consider any differentiable function of ,

In contrast, direct smoothing involves the derivative where . Evaluating the gradient of at is a cause of additional bias.

With these relaxations, the transition function of the system is differentiable. We can now compute a gradient of the sample path cost , using the chain rule on the transition functions. Given a sample path of states , actions , and , the pathwise gradient of the sample path cost is with respect to an action is,

The gradient consists of the sensitivity of the current cost with respect to the action as well the sensitivity of future costs via the current action’s impact on future states. The policy gradient with respect to can then be computed as

| () |

As a result of the straight-through trick, we do not alter the event selection operation ’s and thus the state trajectory is unchanged.

We refer to the gradient estimator () as the policy gradient estimator. Although this formula involves iterated products of several gradient expressions, these can be computed efficiently through reverse-mode auto-differentiation using libraries such as PyTorch [77] or Jax [13] with time complexity in the time horizon . This time complexity is of the same order as the forward pass, i.e., generating the sample path itself, and is equivalent to the time complexity of . The policy gradient algorithm with gradient is summarized in Algorithm 1. In Section 5, we perform a careful empirical comparison of and , and find that can lead to orders of magnitude improvements in sample efficiency.

It is important to re-emphasize that when computing the gradient, we evaluate the policy differently than we would for . Instead of drawing a random discrete action , we use the probabilities output by the policy directly as a fractional routing matrix in ,

However, this is only for gradient computation. When we evaluate the policy, we draw .

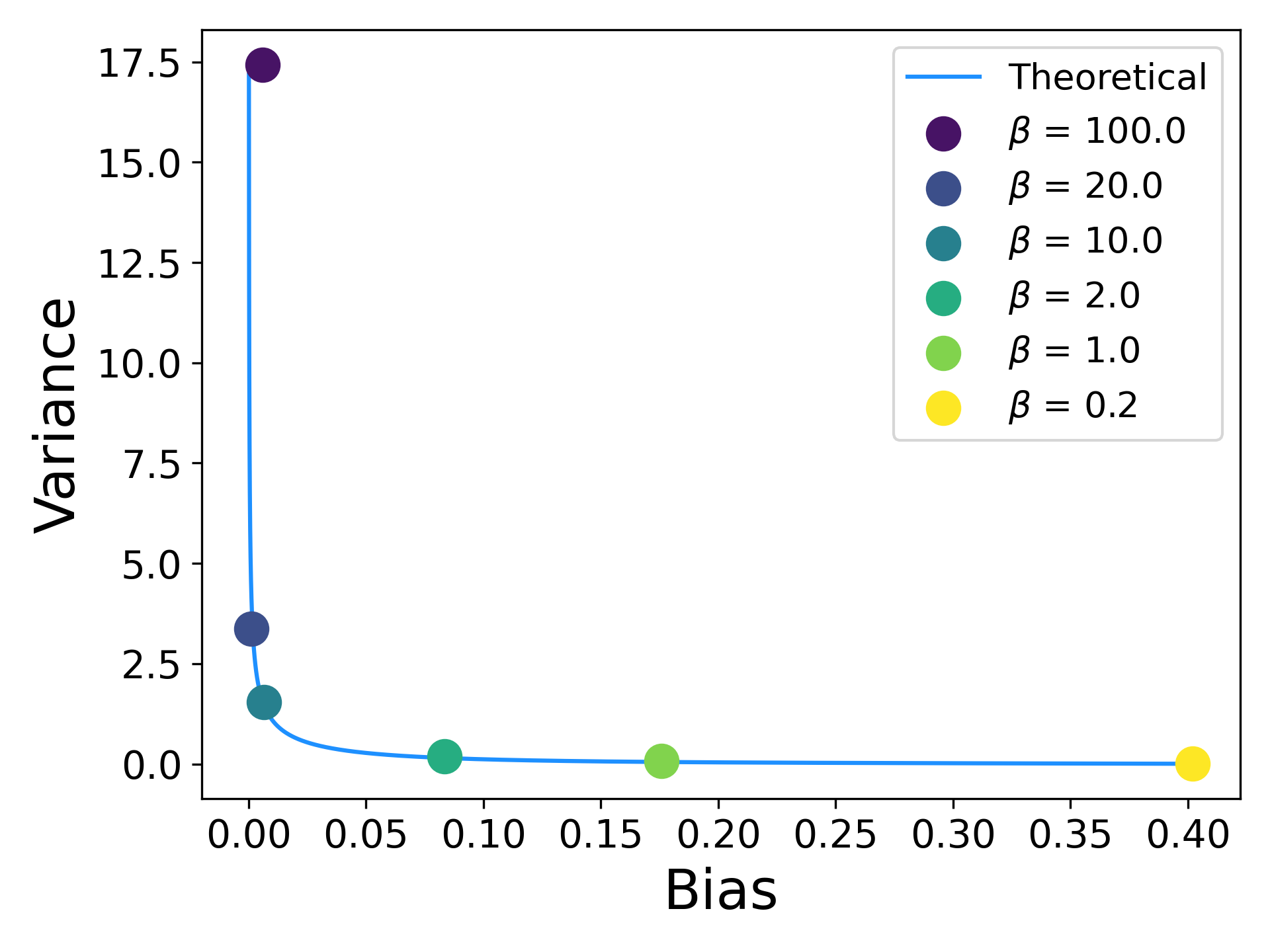

Bias-variance trade-off for inverse temperature: One-step analysis

The inverse temperature is a key hyperparameter that determines the fidelity of the approximation to . The choice of poses a bias-variance trade-off, with a higher leading to a smaller bias but a higher variance and a smaller incurring a higher bias but a lower variance.

In general, it is difficult to assess the bias since we often do not know the true gradient. However, for some simple examples, we can evaluate the true gradient explicitly. We next analyze the gradient of the one-step transition of the queue with respect to the service rate ,

This permits an exact calculation of the mean and variance of our proposed pathwise gradient estimator. Although we can derive analytical expressions for these quantities, we present the leading order asymptotics as for conciseness of presentation. While it is straightforward to see that almost surely as , it is much less clear whether the gradient converges, i.e., whether . Since has a gradient of zero almost everywhere, the expectation and gradient operators cannot be interchanged. Instead, we analyze the expectations directly using properties of the exponential distribution.

Theorem 1.

Let denote the gradient estimator of the one-step transition of the queue with respect to . For , as ,

See section B.1 for the proof. As , the bias is while the variance is . This means that one can significantly reduce the bias with only a moderate size of . The left panel of Figure 7 shows the bias-variance trade-off of for various inverse temperatures . The blue line is based on the analytical expression for the bias-variance trade-off curve. We observe that with the inverse temperature , both the bias and the variance are reasonably small.

Corollary 1.

Suppose we compute the sample average of iid samples of , which are denoted as , . In particular, the estimator takes the form . The choice of that minimizes the mean-squared error (MSE) of the estimator is and .

The estimator provides a more statistically efficient trade-off than other alternatives. As an example, a standard gradient estimator is the finite-difference estimator in which one evaluates the one-step transition at and for some small , and the estimator is constructed as

where ’s are iid samples of . If we set , it is well-known that the bias scales as while the variance scales as . The choice of that minimizes the MSE is and .

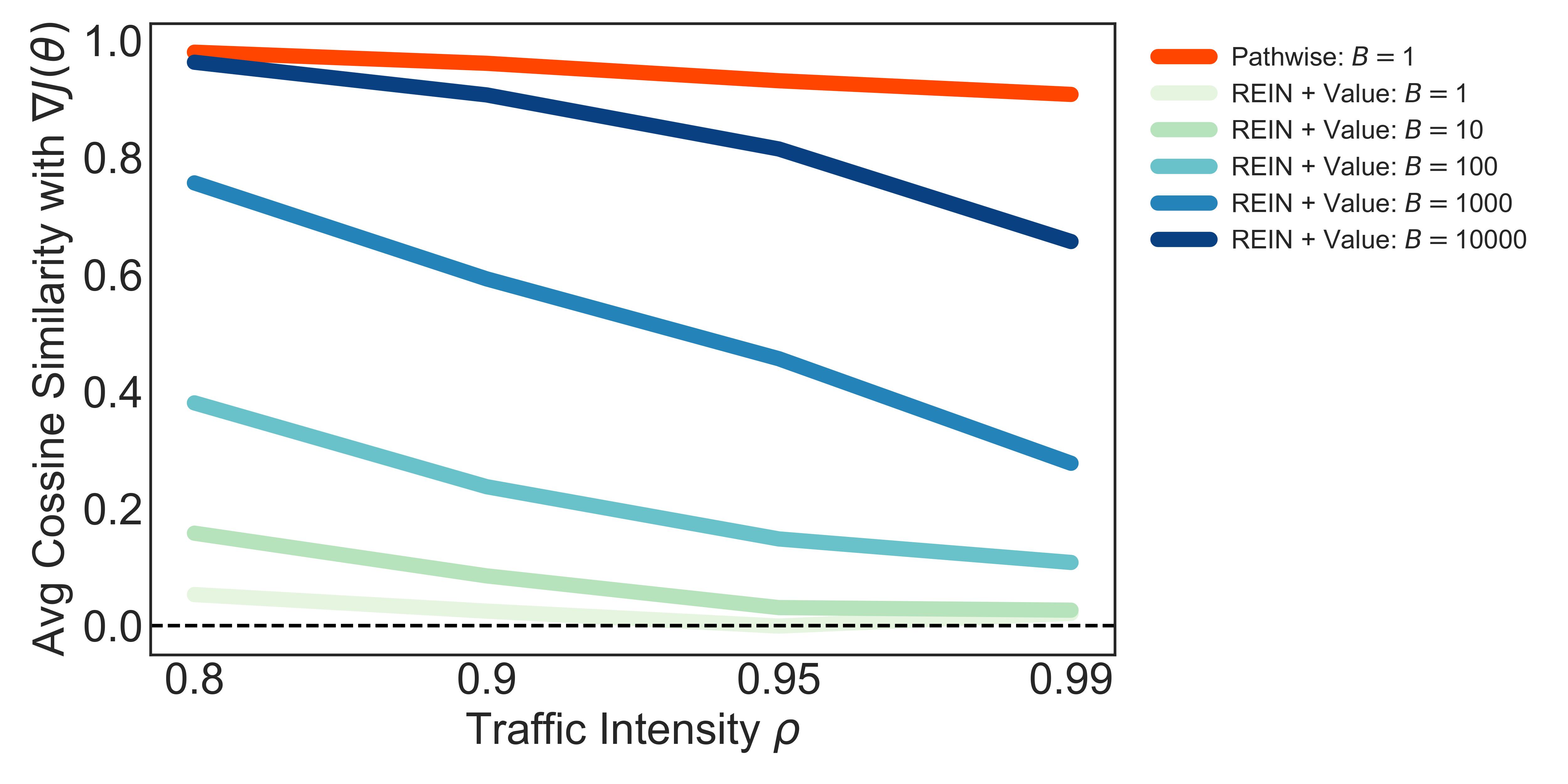

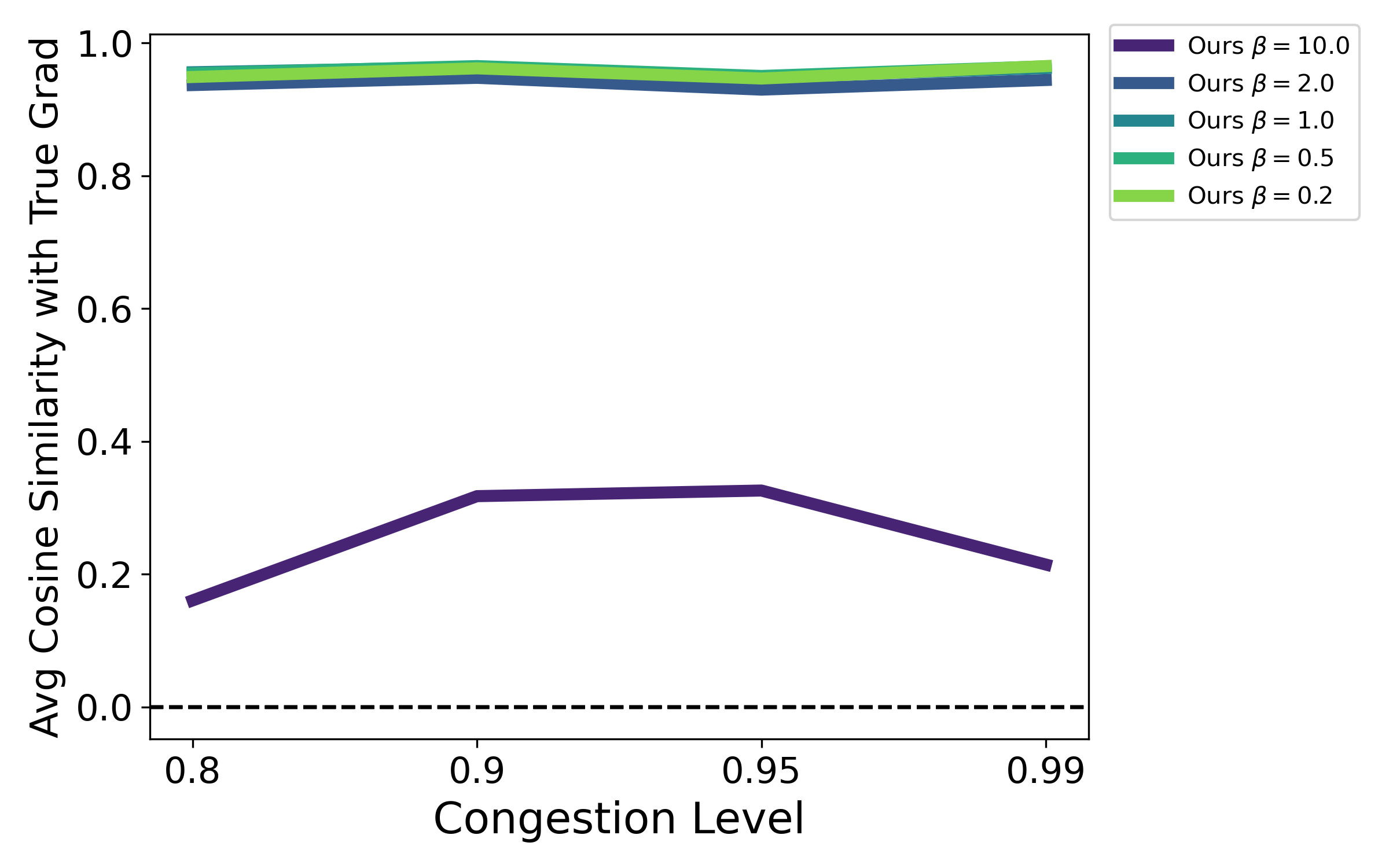

While this analysis is restricted to the one-step transition of the queue, these insights hold for more general systems and control problems. The right panel of Figure 7 displays the average cosine similarity (defined in (18)) between the gradient estimator and the true gradient for a policy gradient task in a 6-class reentrant network across different congestion levels and for different inverse temperatures. We observe that for a wide range of inverse temperatures, , the estimator has near-perfect similarity with the true gradient, while a very large inverse temperature suffers due to high variance. This indicates that while there is a bias-variance trade-off, the performance of the gradient estimator is not sensitive to the choice of the inverse temperature within a reasonable range. In our numerical experiments, we find that one can get good performance using the same inverse temperature across different settings without the need to tune it for each setting.

5 Empirical Evaluation of the Gradients

In the previous section, we introduced the gradient estimator for computing gradients of queuing performance metrics with respect to routing actions or routing policy parameters. In this section, we study the statistical properties of these gradient estimators and their efficacy in downstream policy optimization tasks. We use as the baseline gradient estimator. First, in section 5.1 we empirically study the estimation quality across a range of queuing networks, traffic intensities, and policies. After that, in section 5.2, we investigate their performance in a scheduling task: learning the rule in a multi-class queuing network. Finally, we demonstrate the applicability of our framework beyond scheduling: we investigate the performance of the gradient estimator for admission control tasks in section 5.3.

5.1 Gradient Estimation Efficiency

In general, it is challenging to theoretically compare the statistical properties of different gradient estimators, and very few results exist for systems beyond the queue (see section 8 for a theoretical comparison between and for the queue). For this reason, we focus on numerical experiments across a range of environments and queuing policies typically considered in the queuing literature. Specifically, we will be comparing the statistical properties of estimator with the baseline estimator . While introduces bias into the estimation, we find in our experiments that this bias is small in practice and remains small even over long time horizons. At the same time, the estimator delivers dramatic reductions in variance, achieving greater accuracy with a single trajectory than with trajectories.

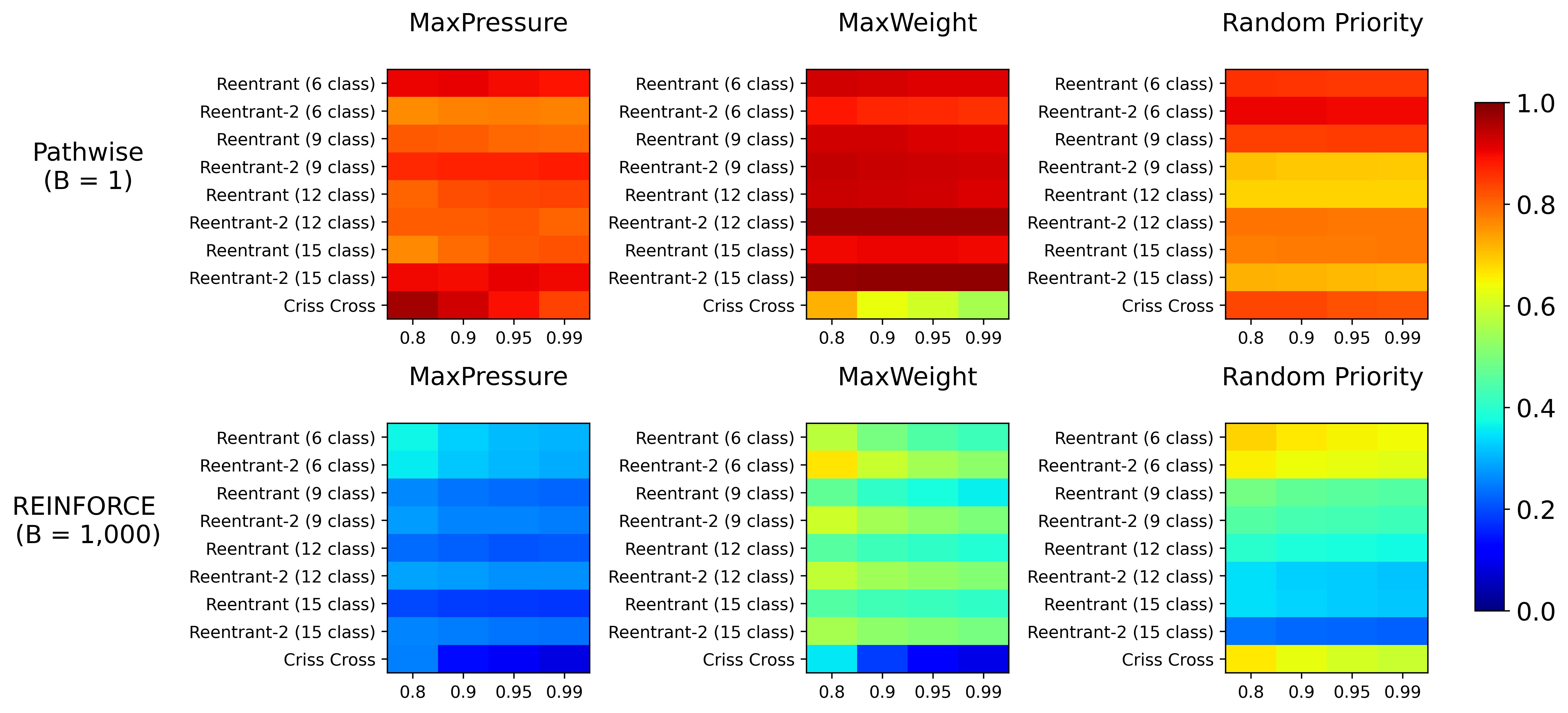

First, recall that a policy maps queue-lengths to assignment between servers and queues, represented by an matrix in (allowing for fractional routing matrices). We visit three classical queuing policies: priority policies [25], MaxWeight [93], and MaxPressure [27]. Each of these methods selects the routing that solves an optimization problem. This means that the routing generated by the policy is deterministic given the state and is not differentiable in the policy parameters. In order to apply either or the gradient estimator to compute a policy gradient, we require differentiable surrogates of these policies. To this end, we define softened and parameterized variants of these policies, denoted as soft priority (), soft MaxWeight (), and soft MaxPressure (),

| (17) |

where are a vector of costs/weights for each queue, denotes the matrix of service rates with denoting the service rates associated with server . The operation refers to element-wise multiplication and the operation maps a vector into a set of probabilities .

We are interested in identifying the parameter that minimizes long-run average holding cost where . We use the objective where is a large enough number to approximate the long-run performance, and the goal of the gradient estimation is to estimate .

We consider the following environments, which appear throughout our computational experiments and serve as standard benchmarks for control policies in multi-class queuing networks. We describe the network structure in detail in Figure 13.

- •

-

•

Re-entrant 1 ( classes): We consider a family of multi-class re-entrant networks with a varying number of classes, which was studied in [12, 26]. The network is composed of several layers and each layer has 3 queues. Jobs processed in one layer are sent to the next layer. Arrivals to the system come to queues 1 and 3 in the first layer while queue 2 receives re-entered jobs from the last layer (see Figure 13 (a) for a two-layer example).

-

•

Re-entrant 2 ( classes): We consider another family of re-entrant network architecture that was studied in [12]. It also consists of multiple layers with 3 queues in each layer. It differs from the Re-entrant 1 environment in that only queue 1 receive external arrivals while queues 2 and 3 receive re-entered jobs from the last layer (see Figure 13 (b) for a two-layer example).

For a gradient estimator , the main performance metric we evaluate is , which is the expected cosine similarity with the ground-truth gradient,

| (18) |

where the expectation is over randomness in . The higher the similarity is, the more aligned is to the direction of . This metric incorporates both bias and variance of the gradient estimator. If the gradient estimator is unbiased but has a high variance, then each individual realization of is likely to have low correlation with the true gradient, so the average cosine similarity will be small even if . At the same time, if the gradient estimator has a low variance but a high bias, then the could still be small if is small. We focus on this metric, because it directly determines how informative the gradient estimates are when applying various gradient descent algorithms. For our experiments, we evaluate (a close approximation of) the ground-truth gradient by using the unbiased gradient estimator over exceedingly many trajectories (in our case, trajectories).

We compare the similarity of with that of . We denote as the number of trajectories we use to calculate each or gradient estimator.

| (19) |

We compute the gradient with only trajectory, while gradient is calculated using trajectories. For each policy and setting, we compute these gradients for different randomly generated values of , which are drawn from a distribution (as the parameters must be positive in these policies). In total, we compare the gradients in unique parameter settings, and each gradient estimator is computed times to evaluate the average cosine similarity. When computing the policy gradient, we consider a time horizon of steps.

Figure 8 compares the estimator with trajectory with the estimator averaged over trajectories. For the estimator, costs are computed with a discount factor , as using a lower discount rate introduced significant bias in the estimation. For , we use an inverse temperature for the relaxation across all settings. Each cell in Figure 8 corresponds to a (policy, network, traffic-intensity) and the cell value is the average expected cosine similarity of the estimator averaged across the randomly drawn values. We observe that across these diverse settings, the estimator consistently has a much higher average cosine similarity with the true gradient despite using only a single trajectory. In fact, for 94.5% of the 10,800 parameter settings, has a higher average cosine similarity with 99% confidence than with trajectories. In most cases, the cosine similarity of is close to 1, indicating almost perfect alignment with the true gradient even under high congestion. on the other hand suffers greatly from high variance. Overall, this demonstrates that is able to deliver greater estimation accuracy with an order of magnitude fewer samples.

5.2 Learning the rule

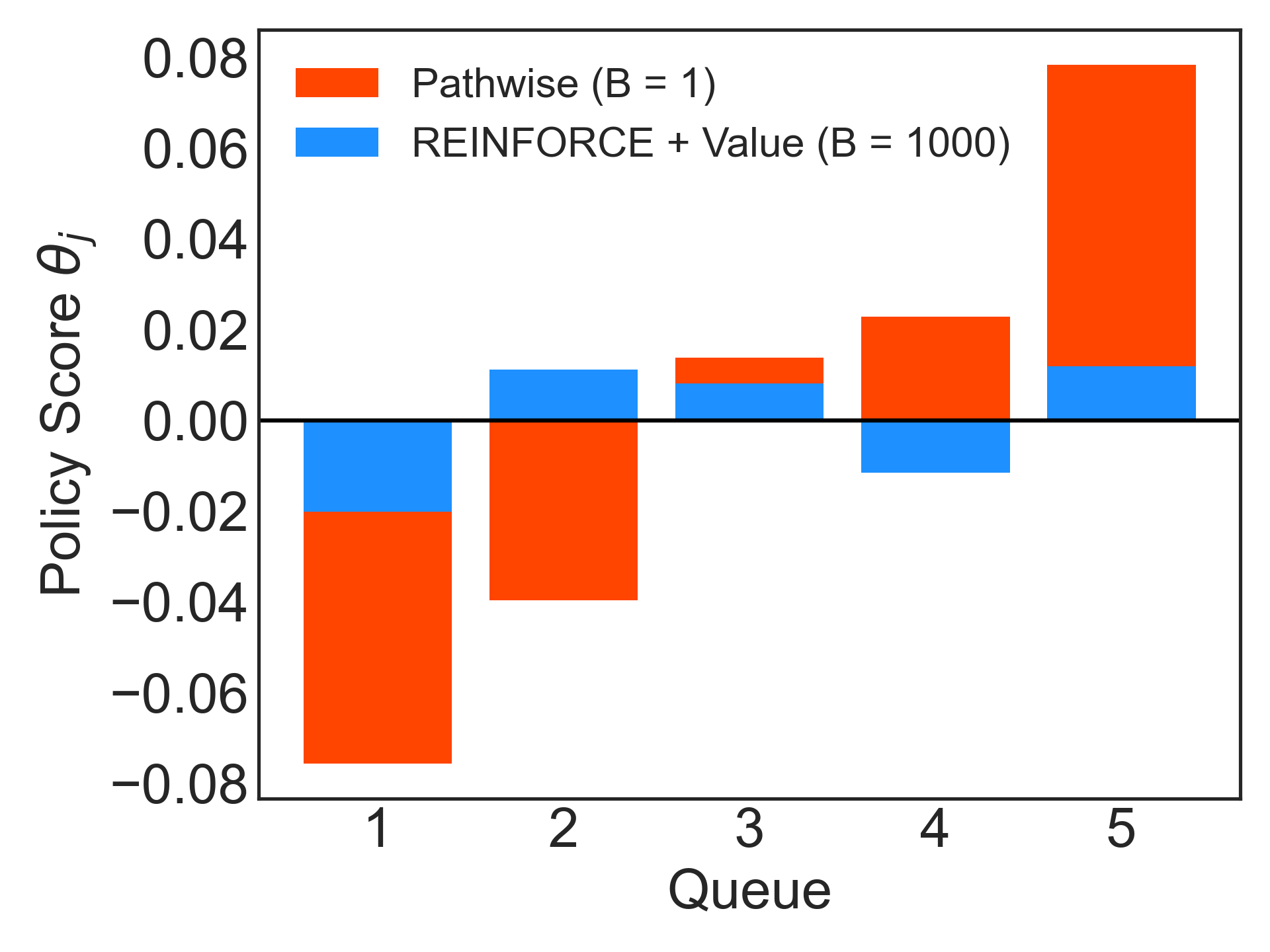

Given the strong improvements in estimation efficiency, we turn to evaluate how these translate to a downstream optimization task. In single-server multi-class queues, it is well-known that the -rule minimizes the long-run average holding cost [25]. We assess whether gradient descent with the or gradients is capable of converging to the -rule, without knowing the holding costs or and only using feedback from the environment. Despite its simplicity, it has been observed in prior work that this is a difficult learning task, particularly under heavy traffic [95].

We revisit the soft priority policy mentioned before, but with only the parameters , i.e.,

| (20) |

We also modify the policy to ensure that it is work-conserving, i.e., not assigning the server to an empty queue (see section 6 for further discussion).

We consider a family of multi-class single-server queues with queues. Holding costs are identically . Inter-arrival and service times are exponentially distributed, the service rates are , for some , and the arrival rates are identical and are set such that the traffic intensity for some . Note that in this case, the -rule prioritizes queues with higher indices . We consider a grid of gap sizes to adjust the difficulty of the problem; the smaller is, the harder it is to learn.

We compare with trajectory and with trajectories for trajectories of steps. In order to isolate the effect of the gradient estimator from the optimization scheme, for both estimators we use an identical stochastic gradient descent scheme with normalized gradients (as these two estimators may differ by a scale factor). That is, for gradient estimator , the update under step-size is

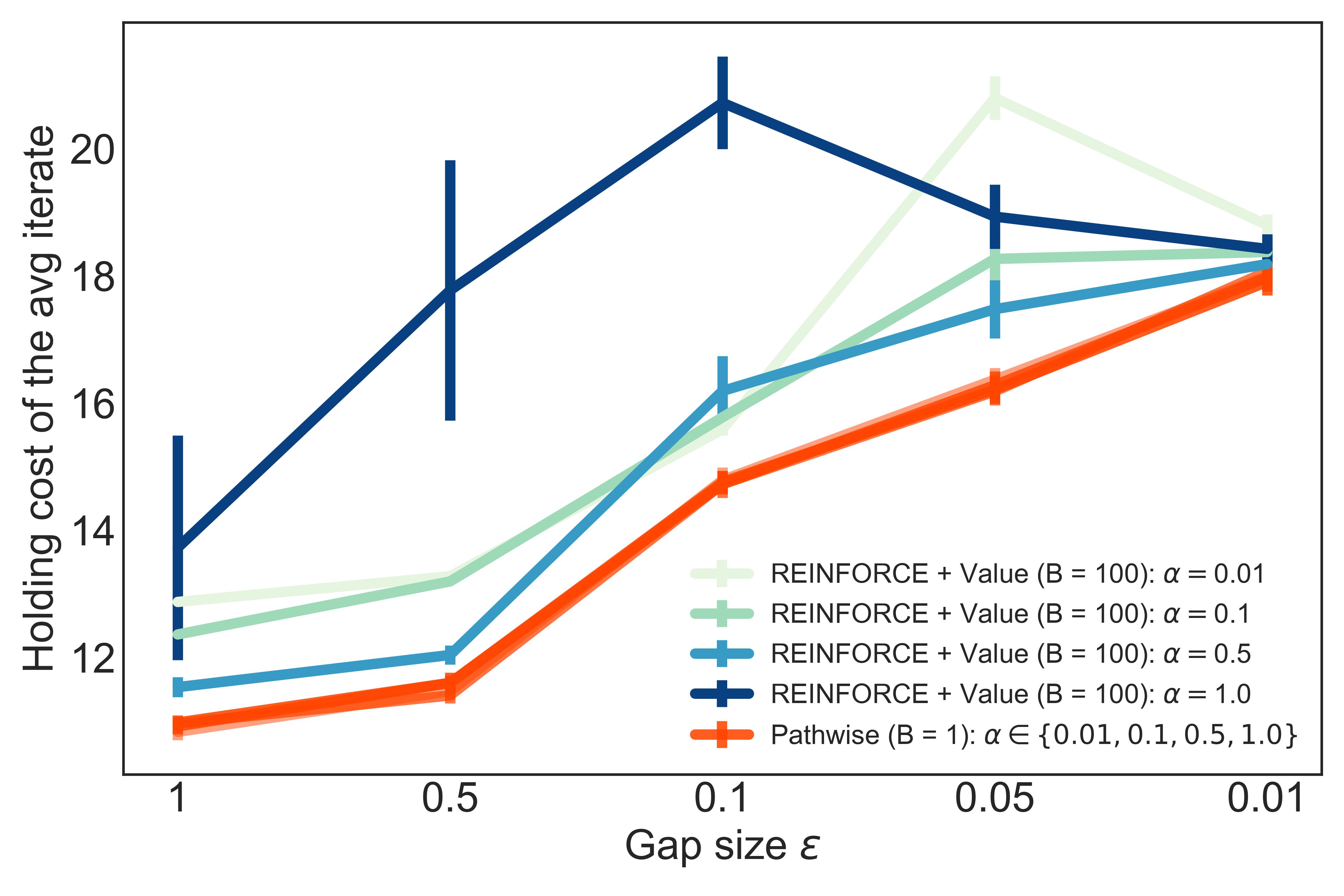

We run gradient descent steps for each gradient estimator. To allow for the fact that different estimators may have different performances across different step sizes, we consider a grid of step sizes . Gradient normalization may prevent convergence, so we use the averaged iterate for . We then evaluate the long-run average holding cost under a strict priority policy determined by , i.e., .

The left panel of Figure 9 displays the values of after gradient iterates for and with , , and . We observe that while sorts the queues in the correct order (it should be increasing with the queue index), even with trajectories fails to prioritize queues with a higher index. Remarkably, we observe in the right panel of the same figure that with just a single trajectory achieves a lower average holding cost than uniformly across various step sizes and difficulty levels, whereas the performance of varies greatly depending on the step size. This indicates that the improvements in gradient efficiency/accuracy of make it more robust to the step-size hyper-parameter. It is also worth mentioning that when gap size becomes smaller, it is more difficult to learn. At the same time, since ’s are more similar to each other, the cost difference between different priority rules also diminishes.

5.3 Admission Control

While we focus mainly on scheduling tasks in this work, our gradient estimation framework can also be applied to admission control, which is another fundamental queuing control task [75, 21, 22, 34, 62]. To manage congestion, the queuing network may reject new arrivals to the network if the queue lengths are above certain thresholds. The admission or buffer control problem is to select these thresholds to balance the trade-off between managing congestion and ensuring sufficient resource utilization.

Under fixed buffer sizes , new arrivals to queue are blocked if . As a result, the state update is modified as follows,

| (21) |

While a small can greatly reduce congestion, it can impede the system throughput. To account for this, we introduce a cost for rejecting an arrival to the network. Let denote whether an arrival is overflowed, i.e., an arrival is blocked because the buffer is full,

| (22) |

Given a fixed routing policy, the control task is to choose the buffer sizes to minimize the holding and overflow costs:

| (23) |

Similar to the routing control problem, despite the fact that overflow is discrete, our gradient estimation framework is capable of computing a gradient of the cost with respect to the buffer sizes, which we denote as , i.e., we can evaluate gradients at integral values of the buffer size and use this to perform updates. Since the buffer sizes must be integral, we update the buffer sizes via sign gradient descent to preserve integrality:

| (24) |

Learning for admission control has been studied in the queuing and simulation literature [16, 17, 51, 23]. While exact gradient methods are possible in fluid models [16, 17], the standard approach for discrete queuing models is finite perturbation analysis [51], given the discrete nature of the buffer sizes. Randomized finite-differences, which is also known as Simultaneous Perturbation Stochastic Approximation (SPSA) [88, 31], is a popular optimization method for discrete search problems. This method forms a finite-differences gradient through a random perturbation. Let be a random -dimensional vector where each component is an independent random variable, taking values in with equal probability. For each perturbation , we evaluate the objective at , i.e., and , using the same sample path for both evaluations to reduce variance. For improved performance, we average the gradient across a batch of perturbations, i.e., for , drawing a new sample path for each perturbation. The batch SPSA gradient is

| (25) |

We update the buffer sizes according to the same sign gradient descent algorithm as in (24).

In comparison with existing works in the queuing literature (e.g. [75, 22, 34]), which derive analytical results for simple single-class or multi-class queues, we consider admission control tasks for large, re-entrant networks with multiple job classes. Each job class has its own buffer, resulting in a high-dimensional optimization problem in large networks. Moreover, the buffer size for one job class affects downstream congestion due to the re-entrant nature of the networks. For our experiments, we fix the scheduling policy to be the soft priority policy in (20) due to its simplicity and strong performance in our environments. We emphasize however that our framework can be applied to buffer control tasks under any differentiable routing policy, including neural network policies. For each gradient estimator, we perform iterations of sign gradient descent, and each gradient estimator is computed from trajectories of length . For SPSA, we consider batch sizes of whereas we compute with only trajectory. When evaluating the performance, we calculate the long-run average cost with the buffer size determined by the last iterate with a longer horizon and over 100 trajectories. We also average the results across runs of sign gradient descent.

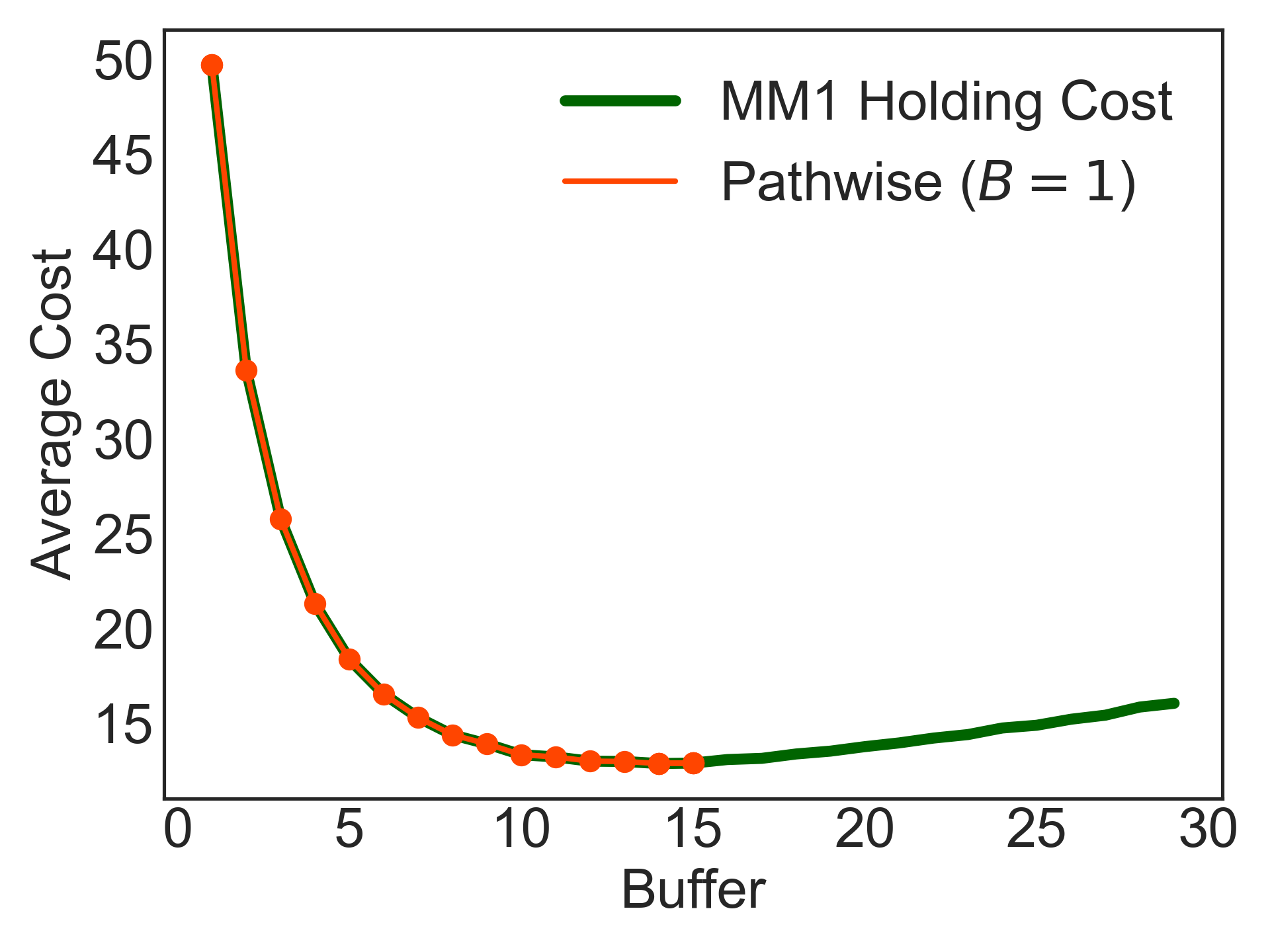

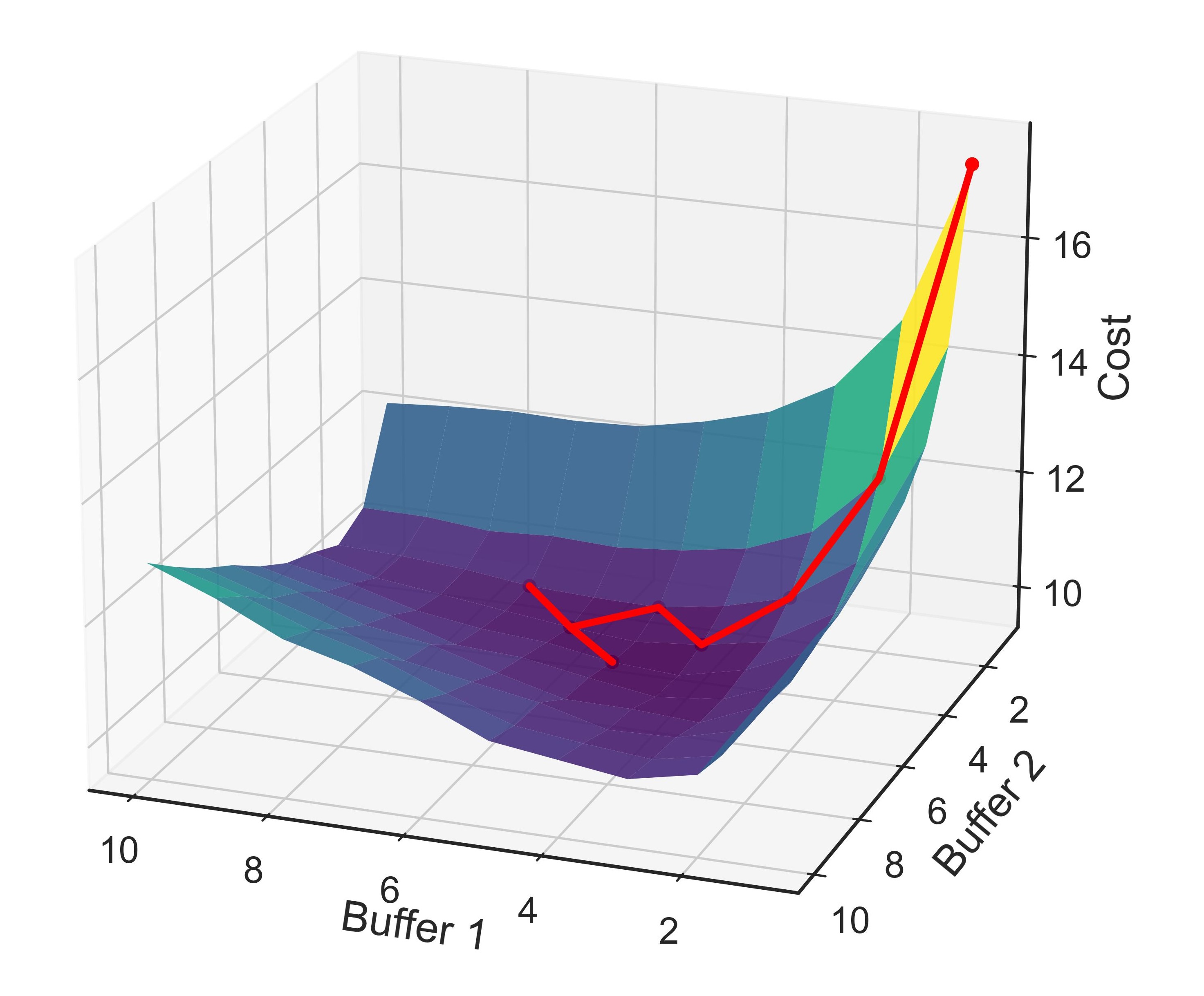

The left panel of Figure 10 displays iterates of the sign gradient descent algorithm with for the queue with holding cost and overflow cost . We observe that sign gradient descent with (computed over a horizon of steps) quickly reaches the optimal buffer size of and remains there, oscillating between and . The right panel shows the iterates for a simple 2-class queue with 1 server, , and under a soft priority policy. We again observe that sign gradient descent with quickly converges to a near-optimal set of buffer sizes.

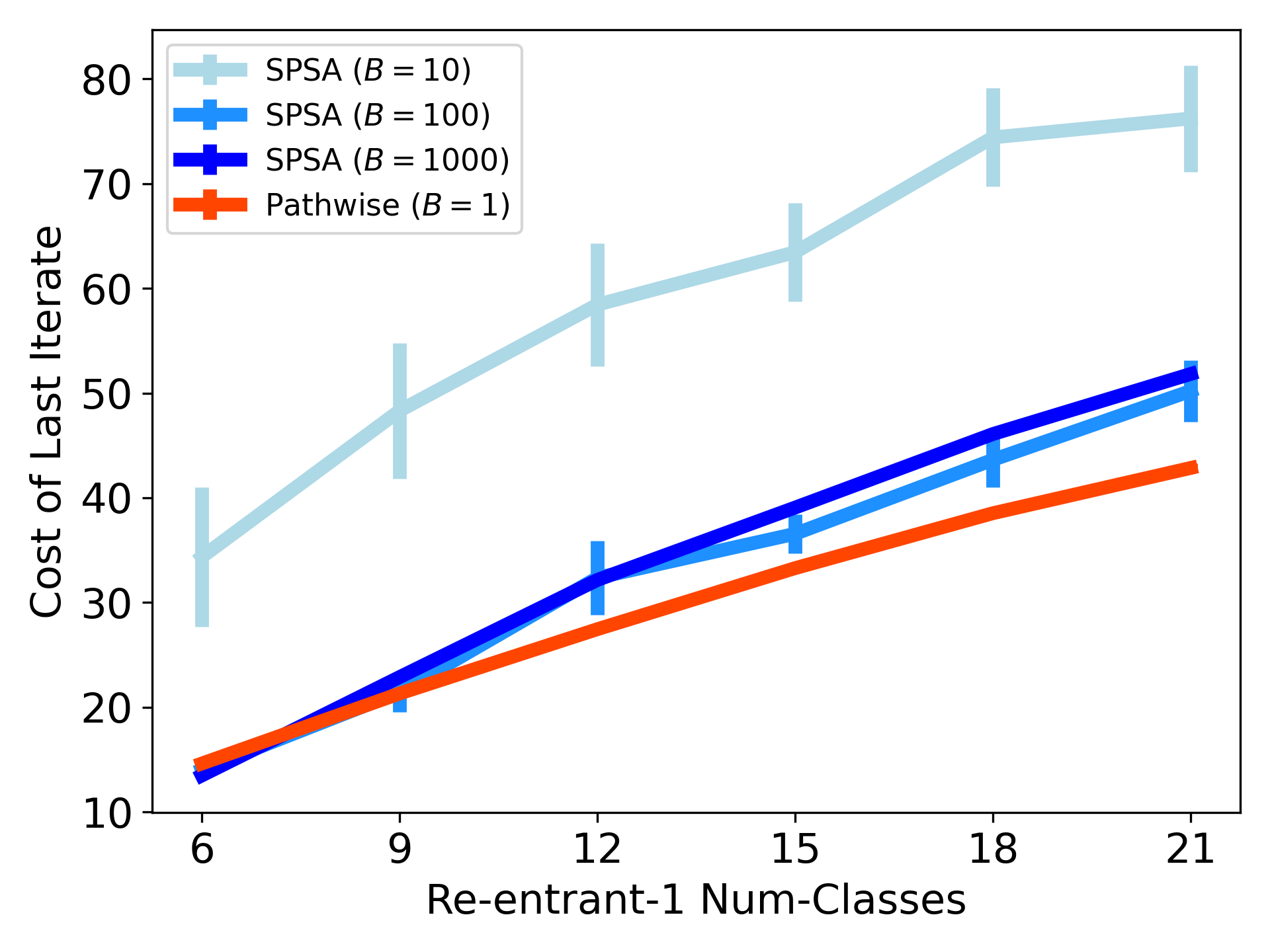

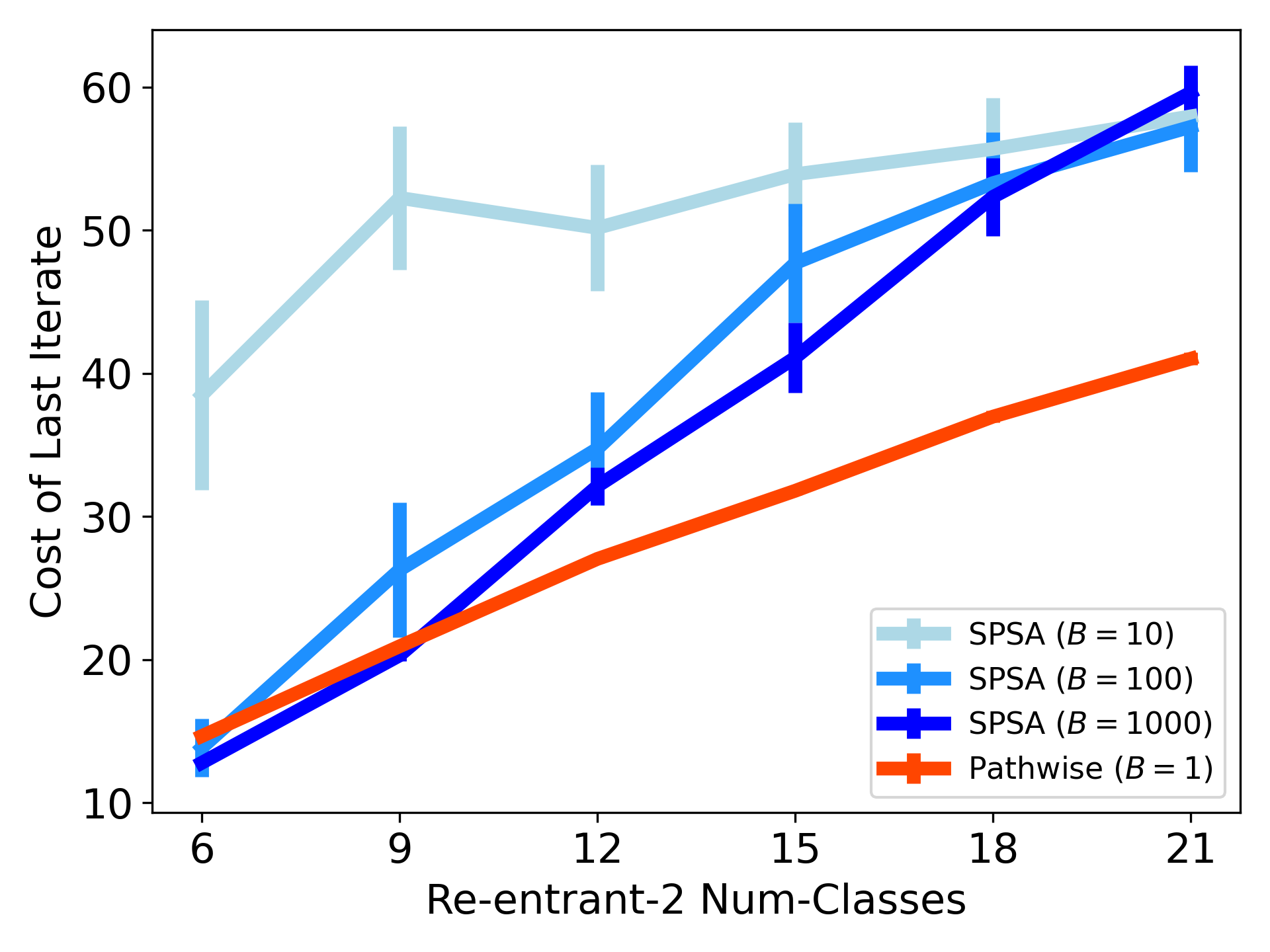

To see how the estimator performs in larger-scale problems, we consider the Re-entrant 1 and Re-entrant 2 networks introduced in Section 5.1 with varying number of job classes (i.e., varying number of layers). Figure 11 compares the last iterate performance of SPSA and for these two families of queuing networks with instances ranging from -classes to -classes. Holding costs are and overflow costs are for all queues. We observe that with only a single trajectory is able to outperform SPSA with trajectories for larger networks. Sign gradient descent using SPSA with only trajectories is much less stable, with several of the iterations reaching a sub-optimal set of buffer sizes that assign to several queues. This illustrates the well-known fact that for high-dimensional control problems, zeroth-order methods like SPSA must sample many more trajectories to cover the policy space and their performance can scale sub-optimally in the dimension. Yet , which is an approximate first-order gradient estimator, exhibits much better scalability with dimension and is able to optimize the buffer sizes with much less data.

6 Policy Parameterization

While our gradient estimation framework offers a sample-efficient alternative for learning from the environment, there is another practical issue that degrades the performance of learning algorithms for queuing network control: instability. Standard model-free RL algorithms are based on the ‘tabula rasa’ principle, which aims to search over a general and unstructured policy class in order to find an optimal policy. However, it has been observed that this approach may be unsuitable for queuing network control. Due to the lack of structure, the policies visited by the algorithm often fail to stabilize the network, which prevents the algorithm from learning and improving. As a result, researchers have proposed structural modifications to ensure stability, including behavior cloning of a stabilizing policy to find a good initialization [26], switching to a stabilizing policy if the queue lengths exceed some finite thresholds [64], or modifying the costs to be stability-aware [78].

We investigate the source of instability in various queuing scheduling problems and find a possible explanation. We note that many policies obtained by model-free RL algorithms are not work-conserving and often allocate servers to empty queues. A scheduling policy is work-conserving if it always keeps the server(s) busy when there are compatible jobs waiting to be served. Standard policies such as the -rule, MaxPressure, and MaxWeight are all work-conserving, which partly explains their success in stabilizing complex networks. We treat work conservation as an ‘inductive bias’ and consider a simple modification to the policy architecture that guarantees this property without sacrificing the flexibility of the policy class.

The de-facto approach for parameterizing policies in deep reinforcement learning is to consider a function , which belongs to a general function family, such as neural networks, and outputs real-valued scores. These scores are then fed into a layer, which converts the scores to probabilities over actions. Naively, the number of possible routing actions can grow exponentially in the number of queues and servers. Nonetheless, one can efficiently sample from the action space by having the output of be a matrix where row , denote as , contains the scores for matching server to different queues. Then by applying the for row , i.e., , we obtain the probability that server is assigned to each queue. We then sample the assignment independently for each server to obtain an action in . For the purpose of computing the estimator, also gives a valid fractional routing in . We let denote the matrix formed by applying the softmax to each row in .

Under this ‘vanilla’ softmax policy, the probability that server is routed to queue (or alternatively, the fractional capacity server allocated to ) is given by

| (Vanilla Softmax) |

Many of the policies mentioned earlier can be defined in this way, such as the soft MaxWeight policy, . This parameterization is highly flexible and can be the output of a neural network. However, for a general , there is no guarantee that if . This means that such policies may waste service capacity by allocating capacity to empty queues even when there are non-empty queues that server could work on.

We propose a simple fix, which reshapes the actions produced by the policy. We refer to this as the work-conserving ,

| (WC-Softmax) |

where is the minimum and is a small number to prevent division by zero when the queue lengths are all zero.

This parameterization is fully compatible with deep reinforcement learning approaches. can be a neural network and critically, the work-conserving preserves the differentiability of with respect to . As a result, and estimators can both be computed under this parameterization, since and both exist.

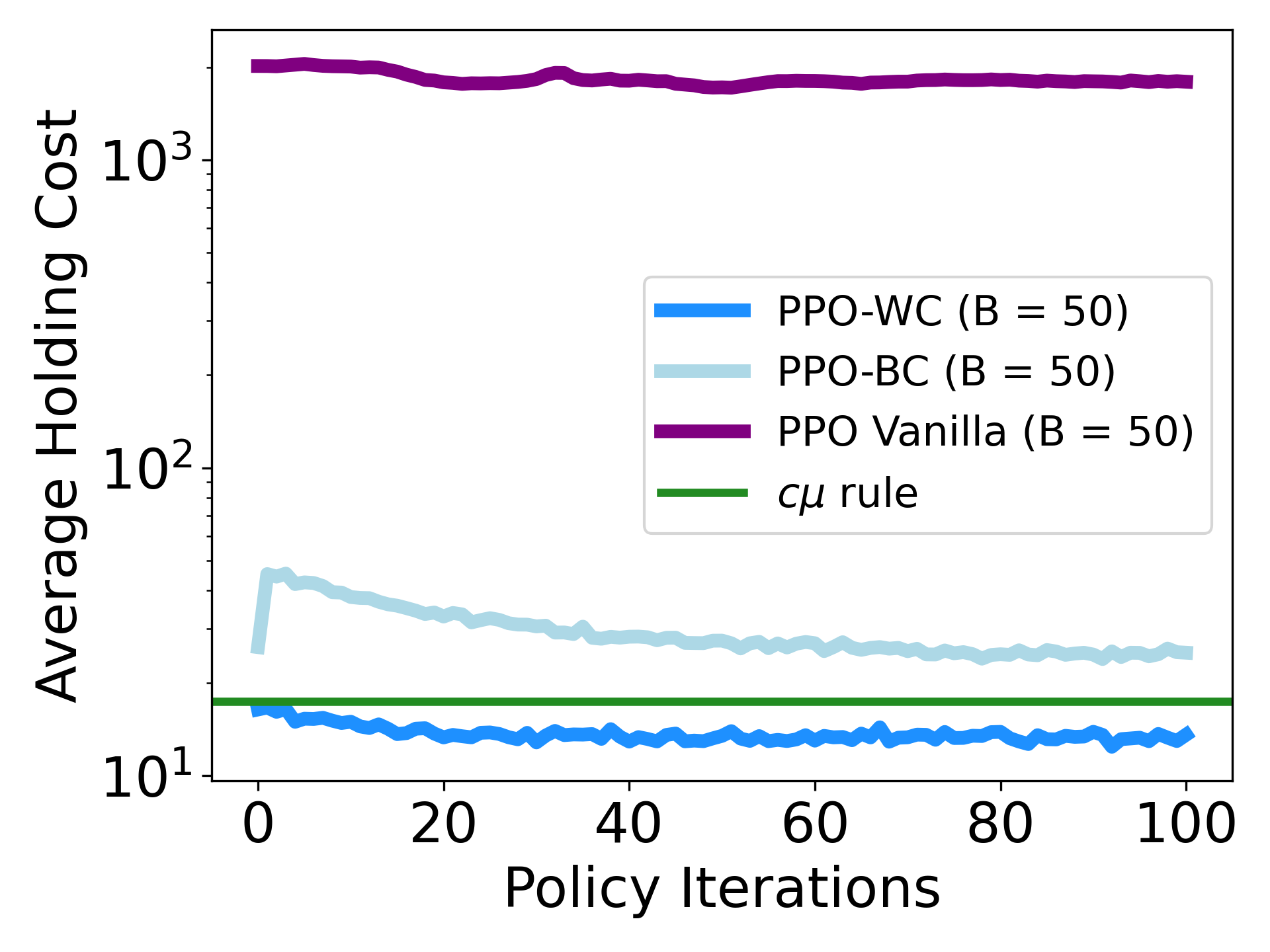

This simple modification delivers substantial improvements in performance. Figure 12 compares the average holding cost across policy iterations for PPO without any modifications, PPO initialized with a policy trained to imitate MaxWeight, and PPO with the work-conserving . Despite its empirical success in many other reinforcement learning problems, PPO without any modifications fails to stabilize the network and incurs an exceedingly high cost. It performs much better under an initial behavioral cloning step, which achieves stability but still underperforms the -rule. On the other hand, with the work-conserving , even the randomly initialized policy stabilizes the network and outperforms the -rule over the course of training. This illustrates that an appropriate choice of policy architecture, motivated by queuing theory, is decisive in enabling learning-based approaches to succeed. As a result, for all of the policy optimization experiments in sections 5.2, 5.3, and 7, we equip the policy parameterization with the work-conserving .

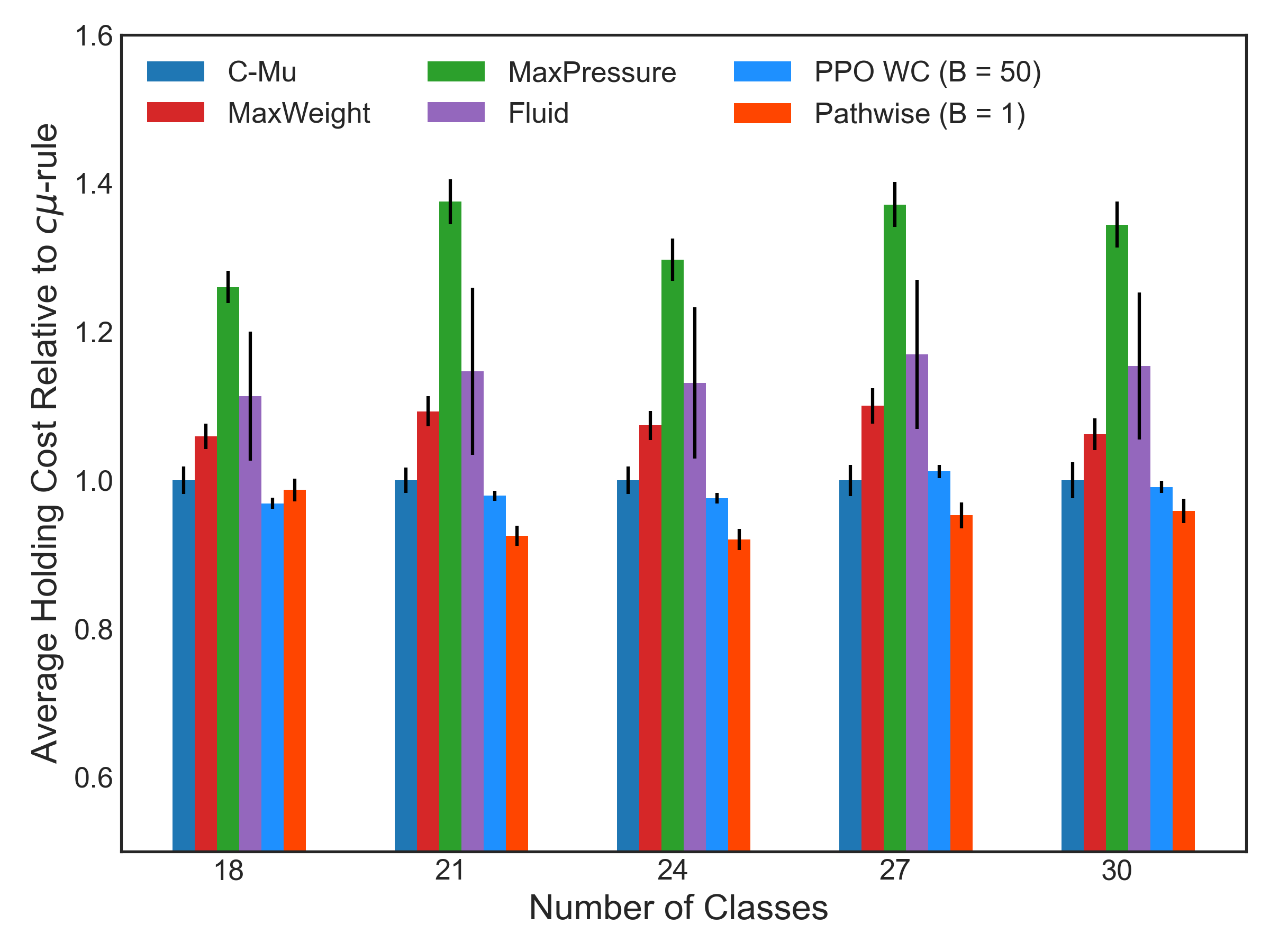

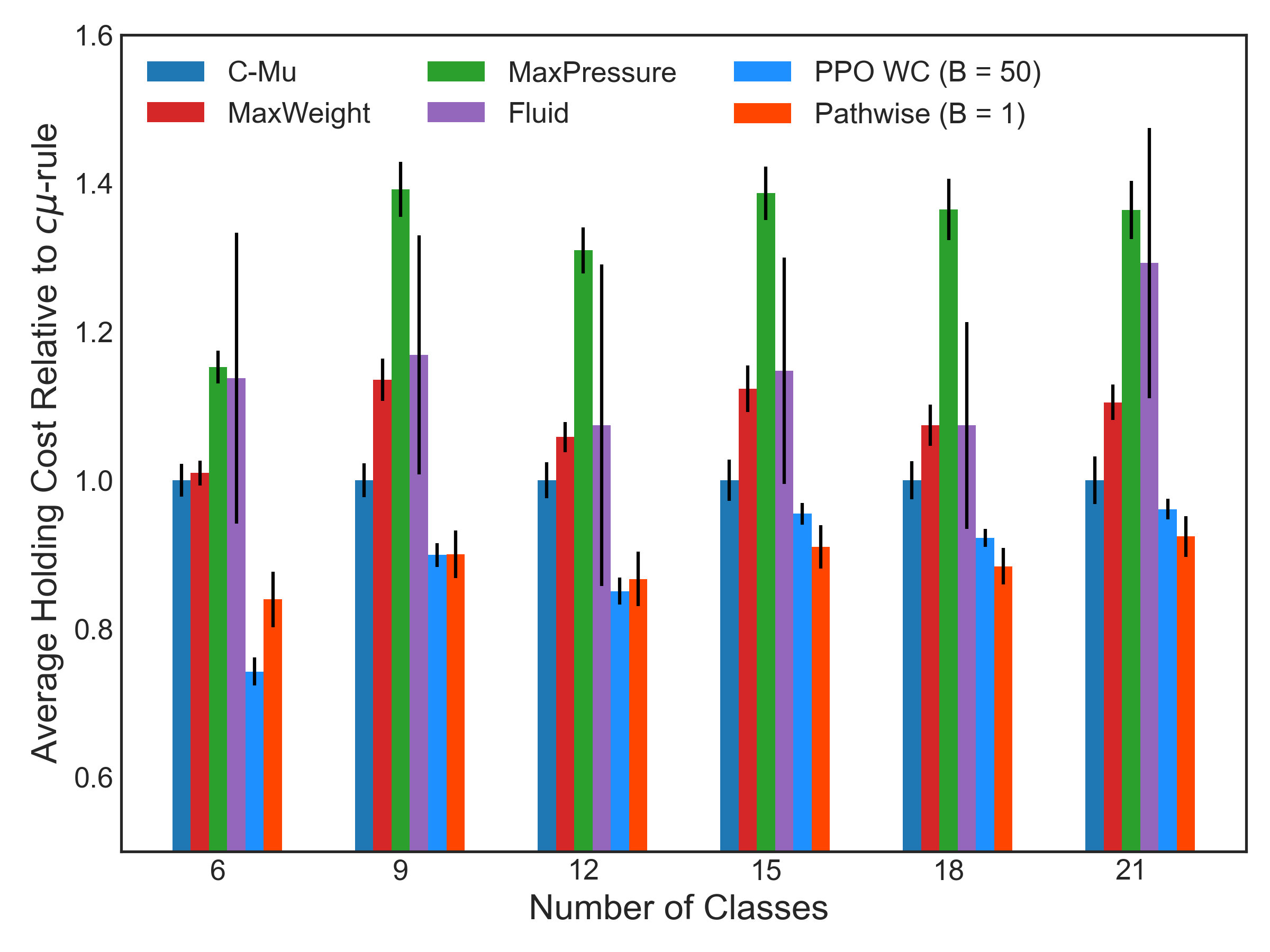

7 Scheduling for Multi-Class Queuing Networks: Benchmarks

We now benchmark the performance of the policies obtained by policy gradient (Algorithm 1) with standard queuing policies and policies obtained using state-of-the-art model-free reinforcement learning algorithms. We consider networks displayed in Figure 13, which were briefly described in section 5.1 and appeared in previous works [26, 12]. Dai and Gluzman [26] used Criss-cross and Re-entrant-1 networks to show that can outperform standard queuing policies. Bertsimas et al. [12] consider the Re-entrant-2 network, but did not include any RL baselines. We consider networks with exponential inter-arrival times and workloads in order to compare with previous results. We also consider hyper-exponential distributions to model settings with higher coefficients of variation, as has been observed in real applications [43]. The hyper-exponential distribution is a mixture of exponential distributions:

for , , , and all are drawn independently of each other. We calibrate the parameters of the hyper-exponential distribution to have the same mean as the corresponding exponential distribution, but with a 1.5x higher variance.

Our empirical validation goes beyond the typical settings studied in the reinforcement learning for queuing literature, and is enabled by our discrete-event simulation framework.

| Noise | MaxWeight | MaxPressure | Fluid | - [26] | - | % improve | ||

| N/A |

We now describe the standard queuing policies considered in this section, which can all be expressed in the form

for some index that differs per method.

-

•

-rule [25]: . Servers prioritize queues with a higher holding cost and a larger service rate.

- •

- •

-

•

Fluid [10]: The scheduling policy is based on the optimal sequence of actions in the fluid relaxation, which approximates the average evolution of stochastic queue lengths by deterministic ordinary differential equations. We aim to solve the continuous-time problem

s.t. For tractability, we discretize the problem with time increment and horizon , and solve as a linear program. We then set . The linear program is re-solved periodically to improve fidelity with the original stochastic dynamics.