Logarithmic regret in the ergodic Avellaneda–Stoikov market making model

Abstract.

We analyse the regret arising from learning the price sensitivity parameter of liquidity takers in the ergodic version of the Avellaneda–Stoikov market making model. We show that a learning algorithm based on a regularised maximum-likelihood estimator for the parameter achieves the regret upper bound of order in expectation. To obtain the result we need two key ingredients. The first are tight upper bounds on the derivative of the ergodic constant in the Hamilton–Jacobi–Bellman (HJB) equation with respect to . The second is the learning rate of the maximum-likelihood estimator which is obtained from concentration inequalities for Bernoulli signals. Numerical experiment confirms the convergence and the robustness of the proposed algorithm.

Key words and phrases:

Regret, Online learning, Adaptive control, Ergodic control, Market making, Maximum likelihood estimation2020 Mathematics Subject Classification:

Primary 93E35; Secondary 93C40, 93C41, 93E20, 91G801. Introduction

Market makers are market participants who are willing to both buy and sell an asset at any time thus providing liquidity. They aim to make a profit from the spread, i.e. buying at a lower price (bid) and selling at a higher price (ask) at the cost of carrying inventory risk. While the principle is simple, executing this consistently profitably is not straightforward due to price volatility, various market micro-structure considerations, information asymmetry and other factors.

Avellaneda and Stoikov [9] have proposed a formulation of the market making task as a stochastic control problem within a parsimonious model. Since then, the framework has been extensively studied and extended to incorporate various additional features, see [26, 34, 15, 14, 12, 13] and the references therein.

In this paper we introduce the ergodic formulation of the model. We will establish an upper bound on regret of order arising from having to learn the key unknown parameter online (while executing a strategy) in the ergodic market making model. In the remainder of the introduction we will briefly introduce the ergodic market making model, the concept of regret, provide a literature review and highlight the main contributions of this paper. In Section 2 we will state all the assumptions and results in detail.

Ergodic formulation of the Avellaneda–Stoikov model

The market maker places one buy / sell order at distances , from the mid price denoted and updates these continuously as new information arrives. These are the controls. On average per unit of time buy / sell market orders (orders from liquidity takers) arrive. These hit the limit order posted by the market maker with probability of . The system thus has the controlled dynamics given by

where is the exogenous mid-price process, is the market maker’s inventory and is the market maker’s cash balance. The inventory and cash processes are driven by , two independent Poisson jump processes with intensities . The market maker wishes to maximize the long-run average reward which sums the earnings and changes to mark-to-market value of their holdings of the risky asset but is subject to a quadratic inventory penalty expressing their risk aversion:

If the values of all the parameters are known then the market maker can solve the ergodic Hamilton–Jacobi–Bellman (HJB) equation associated to the problem and obtain the optimal strategy in closed form as we show in Section 2.1. Under the optimal strategy, the market maker’s reward, per of unit time, will be given by the ergodic constant

Online learning and regret

The model parameters are: liquidity takers orders’ arrival rates , the price sensitivity of the liquidity takers , the mid price volatility (which actually plays no role as the mid price process is a martingale) and the risk aversion . The market maker chooses their risk aversion and thus it’s not a parameter that they would need to learn. The liquidity takers orders’ arrival rates can be observed and learned offline (without participating in the market) since, in the framework of the model where our market maker is assumed to provide a relatively small fraction of the overall liquidity, it is unlikely that the presence of their volume in the market would impact the rate of liquidity taking. This leaves and this is the key parameter. It is not reasonable to assume that this could be learned offline. Exchanges provide visibility of the order book and some information on executed trades but often not enough to allow good offline estimate for . Furthermore other market makers will react to the presence of the additional volume placed by our market maker at the distance thus potentially rendering any offline estimate of invalid. Indeed, some may choose to place their volume at better price (they want to trade) than the spread given by our market maker while others may wish to place the volume at worse price (they may think our market maker knows something about the price they don’t).

The key parameter to learn online (i.e. while participating in the market) is thus . At each time the market maker will have their estimate of the parameter denoted while the true, unknown, value is . They can solve the ergodic control problem and obtain the strategy which would be optimal if would be the true parameter. Let us denote this by strategy by .

Our aim is to gain asymptotic understanding of the regret given by

| (1) |

This is the difference between the optimal, inaccessible, reward up to time and the reward the agent gains by following their chosen method of learning.

If the market maker would use a fixed then their expected regret would be roughly i.e. linear. Any algorithm which achieves sub-linear regret is learning. We construct a regularised maximum-likelihood estimator, see (25), and employ it in Algorithm 1, to achieve the expected regret upper bound of order . See Theorem 19.

Existing literature

Before we proceed to discussing online learning let us mention the “offline” learning approach in Cartea [12]. There, parameter uncertainty for the finite-time-horizon market making model is accepted and robust controls which take model ambiguity into account are derived.

Online learning and regret analysis in stochastic control has been studied in the context of adaptive control and reinforcement learning. Broadly, there are three relatively distinct areas.

The first area is discrete and finite space and time Markov decision problems (either discounted or ergodic). Here regret of order is expected in the general setting and with additional structural assumptions regret of order is achievable, see Auer and Ortner [8], Auer et al. [7] and references therein.

The second area is still discrete time with linear dynamics and convex cost / concave rewards. This makes the setting tractable even in the case of more general state spaces and action spaces. This is the setting most explored in the literature over the years: Kumar [33], Campi and Kumar [11], Abbasi-Yadkori [1], Abeille and Lazaric [2], Agarwal et al. [4] Dean et al. [19], Cohen et al. [18], Cassel et al. [17], Faradonbeh et al. [22], Lale et al. [35], Simchowitz and Foster [37], Hambly et al. [29] and undoubtedly some others. The theme is again that order is achievable and if more can be assumed (e.g. “identifiability conditions” which imply “self-exploration”) then regret upper bound of order holds.

Finally, the third which is the continuous-time, in linear-convex framework setting is the least explored. Guo et al. [28] considers finite-time-horizon linear-convex episodic learning and propose algorithm which achieves order regret (with being the episode number) under an identifiability assumption. In Basei et al. [10] where, the episodic learning LQR is studied, regret bound of order is obtained, again under an identifiability assumption. Szpruch et al. [39] show that without the identifiability assumption it is possible to balance exploration and exploitation (by adding an entropic regularizer) to achieve order regret. In Szpruch et al. [38] this is improved to by means of establishing stronger (2nd order) regularity result for the dependence of the problem value function on the unknown system parameters.

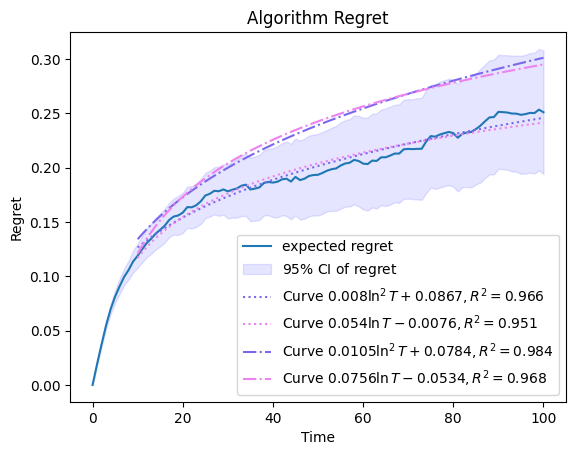

Having reviewed existing results, we note that the study of regret in continuous-time ergodic control has been limited. Fruit and Lazaric [23] derive regret bounds in semi-Markov decision processes (SMDP) within the ergodic setting and show that the regret of order is achievable under certain assumptions (e.g. lump sum reward). In Gao and Zhou [24], the order of regret is improved to by focusing on continuous-time Markov decision processes, a more specific case than SMDP. This represents a significant step forward, showing that logarithmic regret is achievable in continuous-time ergodic frameworks. Nevertheless jump diffusion dynamics and non-linear running rewards required in the Avellaneda–Stoikov model do not fit into the framework of any of the existing papers. From other results in the literature we see that our result showing regret is nearly as good as it gets but a question remains whether this is optimal i.e. what is the regret lower bound in this setting. The numerical experiment shows regret of order is a good fit for what we observe, see Figure 3.

Our contributions

To the best of authors’ knowledge this is the first paper on regret analysis for ergodic control of jump diffusions. The control problem we focus on is the ergodic version of the Avellaneda–Stoikov market making model and we show that the expected regret has an upper bound of order of .

There are three main ingredients which allow us to obtain this result. First, we prove existence of and convergence to an invariant measure in the ergodic Avellaneda–Stoikov market making model. While the well-posedness of the ergodic problem follows mostly from the analysis carried out in Guéant and Manziuk [27] the result on existence of and convergence to the invariant measure is new and relies on newly established explicit solution the the ergodic HJB corresponding to our problem.

Second, we obtain bounds on the second derivative of the average earnings per unit time (the ergodic constant) with respect to the parameter which has to be learned.

Finally, using concentration inequalities for Bernoulli random variables we show that a regularised maximum likelihood estimator yields a high probability bound of order on the distance between the true value and the estimate obtained after market orders have arrived.

2. Main results

In this section, we will introduce the ergodic Avellaneda–Stoikov market making model and state the main results of the paper.

The market maker (agent) proposes bid and ask depths (control) pegged to the mid-price of an asset and wish to make profit from the spread. The space supports a Brownian motion that describes the asset mid-price process , following the dynamics

| (2) |

Apart from the market maker, there are liquidity takers sending market orders (MOs) at random times. The model assumes that the arrivals of buy and sell MOs, , follow two independent Poisson processes with intensities and defined on . Given two independent IID sequences defined on an incoming market buy/sell order trades with the sell/buy volume posted by the market maker when . The probability space for the model is thus

| (3) |

The filtration is , where . Let and denote the market maker’s inventory limits. The market maker will stop posting buy/sell orders when their inventory is at and at respectively. At other times their strategy is to post at a distance from the mid-price . Clearly, the strategy must be adapted to the filtration . Let be the controlled counting processes for the agent’s filled buy/sell orders, i.e.

Hence the inventory process of the market maker is

| (4) |

Let us write , so that takes values in for . Let denote the market maker’s cash balance, satisfying

| (5) |

Let us define the class of admissible policies as

| (6) |

2.1. The ergodic market making model

In this section we will formulate the ergodic control problem, state key results connecting the control formulation with the ergodic HJB equation, provide explicit solution for the ergodic HJB and formulae for the Markovian ergodic optimal controls, state equilibrium properties of the system and state a result on convergence to equilibrium.

Control problem formulation

The market maker aims to maximise a long-run average reward of the accumulated PnL with a running inventory penalty. Let be the ergodic reward functional given by

| (7) |

where the notation represents expectation conditional on and is the running inventory penalty parameter. For the optimal ergodic control problem, the purpose is to give a characterisation of the optimal long-run average reward, also known as the ergodic constant

and to construct an optimal feedback (Markov) control . We will later see that is indeed independent of and thus calling it the ergodic constant is justified. Of course it still depends on all the model parameters, in particular on .

Let us define a running reward function as

| (8) |

where are independent compensated Poisson processes. As the intensities of and would be whenever and and otherwise is clearly square integrable, therefore and . Moreover, is adapted and bounded and so . Hence the ergodic market making control problem can be reduced from dimension of 3 to 1 by Fubini’s theorem

| (9) |

To analyse the ergodic control problem (9), some preliminaries are required. We start with the existence and uniqueness analysis for the classical market making problem in the discounted finite and infinite-time-horizon settings.

Key results for the discounted finite time and infinite-time problems

We first define the unoptimised Hamiltonian function and the optimised Hamiltonian function for the market making model as

| (10) |

Now we consider the optimal market making problem in the discounted finite-time-horizon setting. We assume that the market maker has a penalty for any inventory held at the terminal time

| (11) |

with the terminal inventory penalty parameter. Let be the value function given by

| (12) |

where is the discounted factor, the running reward function is given by (8) and denotes the class of admissible policies defined by (6). The associated Hamilton–Jacobi–Bellman (HJB) equation to the value function (12) is

| (13) |

subject to the terminal condition (11).

Theorem 1 provides the existence and uniqueness for the optimal market making problem in the discounted finite-time-horizon setting. The proof is provided in Appendix A.1. We also recommend Guéant et al. [27] for the proof of a more general stochastic control problem with a discrete state space.

Theorem 1 (Existence and uniqueness for discounted finite-time HJB).

It is well known [15, 25] that there is an explicit solution to satisfying (12) in the case of , denoted by , given by the following theorem.

Theorem 2 (Explicit Solution of Finite-time-horizon Model).

Let us move to discussing the infinite-time-horizon problem. The value function, in the discounted infinite-time-horizon setting, is

| (14) |

where, in this case, the discount factor is strictly positive . The associated HJB equation for the control problem (14) is

| (15) |

The ergodic HJB and its connection the ergodic control problem

In this section, we analyse the ergodic control problem (9) by considering the asymptotic behavior of in the finite-time-horizon model (12) with and in the discounted infinite-time-horizon model (14). We prove that is equal to the ergodic constant in (9). Then explicit solutions to the ergodic control problem are derived.

We start with Theorem 4 that analyses the asymptotic behaviour of in the discounted infinite-time-horizon model (14), the proof of which is provided in Appendix A.3.

Theorem 4.

The next theorem, Theorem 5, states that the constant from Theorem 4 is equivalent to the optimal long-run average reward in the ergodic control problem (9), which associates the equation (16) with the ergodic control problem. Hence we call (16) the ergodic HJB equation, which contains an unknown pair of the ergodic constant and ergodic value function . Theorem 5, which will be proved in Appendix A.4, is a first step towards obtaining an explicit solution to the equation (16).

Theorem 5.

So far we’ve established the connection between the ergodic constant and the solution of the ergodic HJB equation (16). Next, we are interested in how this constant depends on the model parameter . This is best seen from an explicit formulation for given in the following theorem.

Theorem 6.

The proof is given in Appendix A.5 and is based on establishing the asymptotic behaviour as in .

The ergodic HJB equation (16) can be solved once we obtain . Proposition 7, which will be proved in Appendix A.7, analyses the uniqueness (defined up to a constant) for the solution to the ergodic HJB equation (16). Then we can obtain the existence and uniqueness for the optimal control by Proposition 8.

Proposition 7.

Proposition 8 (Existence and Uniqueness for Ergodic Optimal Control).

The optimal feedback (Markov) control for the ergodic control problem is uniquely given by

| (18) |

where is the solution to the ergodic HJB equation (16).

Obviously, given by (18) depends on the model parameters, in particular on . We will denote the optimal feedback control for the ergodic problem with the parameter as .

Finally, we come to Theorem 9 proved in Appendix A.9 that provides an explicit solution to the ergodic HJB equation (16) .

Theorem 9.

Convergence to equilibrium

We’ve derived the explicit solutions to the ergodic control problem (9). Now we proceed to analyse the ergodicity of the state , i.e. how fast the state converges to the equilibrium distribution. This will be essential in the regret analysis. Clearly, the state space is discrete, hence we can utilise the classical discrete state-space Markov chain theory. Let us first define the equilibrium under the Markov control for the market making system as follows.

Definition 10 (Equilibrium).

The distribution is said to be an equilibrium distribution for the Markov control if, for any , it holds that where denotes the law and is given by (4) under control with .

The following lemma is proved in Appendix A.10.

Lemma 11.

There exists an equilibrium distribution under the ergodic optimal control given by (18).

As we show in Appendix A.10, the dynamics of the inventory (4) can be considered as a discrete Markov chain with the transition probability matrix defined in (41). For any , we have . Hence, by definition, is aperiodic. Moreover, as is a tridiagonal matrix, for any , has all positive entries, i.e. , . Hence is irreducible. Therefore, the convergence rate for any distribution under to the equilibrium distribution satisfies the so-called Convergence Theorem [21].

2.2. Learning and regret

In this section, we consider the parameter learning problem of the market making model in the ergodic setting, where the price sensitivity of market participants parameter is unknown to the market maker. We assume that the parameter is equal on the bid/ask side and for some with . The market maker does not observe , but has a prior knowledge that . At each time , the market maker generates the estimate of the parameter denoted in the compact set from the learning algorithm, see Algorithm 1 for more details. By assuming this is the true parameter they can solve the ergodic control problem and obtain the policy given by (18) which would be optimal if indeed was the true parameter.

Remark 13.

In a general RL problem the agent aims to learn from data, e.g. states, actions and rewards, a policy that optimises the reward, see [10, 38, 24]. In this learning problem, we have derived the global optimal policy (see Section 2.1). The global optimal policy is attainable if the true is known. Therefore, it is sufficient to define a learning algorithm to generate the parameter .

In view of this it is natural to define the learning algorithm as the function that generates from all available information up to time .

Definition 14.

Let be defined as

see details in (3), be the algebra generated by null sets, and the continuous-time learning algorithm be some function . We say that is an admissible learning algorithm if is measurable, with the algebra defined as .

Remark 15.

To measure the performance of a learning algorithm in the ergodic setting, we utilise the notion of regret proposed by [7].

Definition 16.

Given a learning algorithm that generates in , its expected regret up to time is defined as

| (20) |

where is the optimal long-run average reward under the parameter , is the running reward function given by

| (21) |

and is the inventory process governed by but with the control , i.e.

| (22) |

with the controlled counting processes for the market maker’s filled buy/sell orders and the corresponding compensated Poisson processes.

An alternative definition of the expected regret which is commonly seen in the finite-time-horizon RL problems,e.g. [10, 38], is

| (23) |

The following Lemma will be proved Appendix A.11.

Lemma 17.

There exists a constant independent of such that

| (24) |

Therefore and shares the same asymptotic growth rate, which means that the definitions of regret (20) and (23) are asymptotically equivalent.

The learning algorithm

When a buy or sell MO comes, let denote the number of the market maker’s filled order and be the offset (depth) posted by the market maker. We know that , i.e. the probability of an incoming MO hitting the LO follows the Bernoulli distribution with .

To learn from the Bernoulli signals, we can simply consider a maximum likelihood estimator [16, Example 7.2.7]. The log-likelihood of given and is

then

Observe that the value of the solution to may tend to infinity when the number of Bernoulli signals is limited. Therefore, one of the main issues of the likelihood function is that each term in the summation of the Fisher information can be arbitrarily small since as for any fixed . To overcome this issue, we consider a regularised and biased estimator for . Let us define as a regularised log-likelihood function for estimating such that

| (25) |

with a regularisation parameter. In this case, we have

The learning algorithm is summarised as follows.

Remark 18.

We can observe that, compared with a general RL algorithm, there is no trade-off between the exploration and exploitation in Algorithm 1. The agent can always learn from the Bernoulli signals about since they quote on at least one of the buy side or the sell side.

Regret upper bound

We now state the main result of this section, which shows the logarithmic regret upper bound of Algorithm 1.

Theorem 19.

For the regret upper bound of Algorithm 1 , there exist constants such that ,

| (26) |

It requires some effort to prove Theorem 19, therefore we collect some key results needed for the proof.

Step 1: Analysis of Performance Gap

In this section, we analyse the performance gap of the expected regret defined in (16).

We start with the ergodic analysis for the market making model with misspecified due to the existence of the term, , in regret.

Let us define, for , , and , the Hamiltonian function

| (27) |

and the expected reward in the discounted finite-time-horizon setting under model misspecification, , as

| (28) |

where is given by (21) and is the terminal condition (11). Then satisfies the following linear ODE. See proof in Appendix A.12.

Lemma 20.

Next we focus on the long-run average reward for given by (28) with . Proposition 21 provides the existence of , i.e. the long-run average reward for the model with misspecified . Moreover, with the ergodic value function under the model misspecification, , solves the linear system (31) below. Rigorous definition of and proof of Proposition 21 are provided in Appendix A.13.

Proposition 21.

There exists such that

| (30) |

where is given by (28) with . Moreover, there exist and that solve the linear system

| (31) |

The fact that satisfies the linear ODE (29) with allows us to solve it in a matrix form. Moreover, by analysing the case of in (30), we can obtain a closed-form expression for as shown in Proposition 22. See proof in Appendix A.14.

Proposition 22.

Let be a square tridiagonal matrix whose rows are labelled from to and entries are given by

Let be the matrix whose columns are the eigenvectors of . Let be a dim vector with each component given by

for . Let is the square matrix with the first diagonal element equal to and all other elements equal to . Then given by (30) satisfies

| (32) |

where is a dim vector with entries .

Although Proposition 22 gives an expression for , it is not trivial to prove the regularity of as is not a self-adjoint or normal operator. We first start with the following lemma that establishes the regularity of given in Theorem 6. The proof is provided in Appendix A.6.

Lemma 23.

The ergodic constant given by (4) is in .

Next we analyse the regularity of .

Lemma 24.

is in .

The key approach in the proof of Lemma 24 (see Appendix A.15) is to construct a self-adjoint operator similar to and express in terms of the eigenvector of this self-adjoint operator, which is differentiable.

By Lemma 24, it is trivial to obtain the following lemma by the fact that attains the maximum at , because is the optimal control for (30).

Lemma 25.

There exist a constant such that

So far we have performed the ergodic analysis for the market making model with parameter misspecified. Another key step towards quantifying the performance gap, see Theorem 27, is to analyse the ergodicity under the model misspecification. By simply substituting for and for in the state transition matrix defined in Appendix A.10, we can conclude that there still exists a unique equilibrium, denoted by , for following (22). Proposition 26, whose proof is provided in Appendix A.16, gives a nice property of the equilibrium .

Proposition 26.

Theorem 27.

Given a continuous-time learning algorithm that generates up to time , let be the regret given by (20), then it holds that

with constants independent of .

The proof is provided in Appendix A.17.

Step 2: Concentration Inequality

The next step towards Theorem 19 is to quantify the precise tail behaviour, also known as concentration inequality, of the regularised maximum likelihood estimator in Algorithm 1. Recall that is given in Definition 14.

We start with several significant propositions to the regularised maximum likelihood estimator. The proofs of the following propositions are provided in Appendix A.18.

Proposition 28.

Let be a collection of non-negative random variables taking values in . Then for any and bounded function , it holds that,

Remark 29.

Proposition 30.

There exist constants depending on and such that for any policy taking values in , it holds that for any ,

Proposition 31.

There exists a unique such that , where is given by (25).

Proposition 32.

There exists constants depending on , , and such that for any policy taking values in , it holds that for any ,

With the above propositions, we obtain Theorem 33 with the proof provided in Appendix A.18, which quantifies the concentration inequality of the regularised maximum likelihood estimator in Algorithm 1.

Theorem 33.

Let be the unique solution to . There exists constants such that for any , if , then

2.2.1. Step 3: Proof of Theorem 19

Let be the time when the th market order arrives. By the fact that the summation of two independent Poisson processes is a Poisson process, we have with the convention that . Besides, let us define , where is the number of signals up to time . By using the notation above, we have

Clearly is a non-negative random variable.

The following proposition, Proposition 34, which is proved in Appendix A.20, states that, given any , i.e. the number of signals up to time , the random variable is bounded by with high probability.

Proposition 34.

There exist constants such that for any ,

Let . Then, by using Proposition 34, we have

Let us set and we can take out of the expectation. Besides, we know that is concave and, for large , i.e. , is concave, hence by Jensen’s inequality, we have

where we use the fact that for large and we ignore the term of order . By using Theorem 27, we then have

where and are constants independent of in Theorem 27 and are constants independent of and in Proposition 34, hence the result of Theorem 19.

3. Numerical experiments

In this section, we numerically simulate the ergodic market making model (7) and the achieved regret of Algorithm 1.

Let us consider the following parameters in the simulation: , , , , , and . In the learning part, we set , and .

By Theorem 2, we can determine the square matrix and the largest eigenvalue of is . Then we have by using Theorem 6. Figure 1 (left panel) plots the asymptotic behaviors of as increases, which is the value function in the discounted finite-time-horizon setting with the discount factor given by (12). We can see that, for any initial , the value as as stated in Theorem 5.

We then solve the ergodic HJB equation (16) and find the optimal feedback control . By Theorem 9, there exists the null space of the square matrix with non-trivial solutions satisfying with . We consider the positive solutions in the null space, hence the solutions to the ergodic HJB equation can be well-defined. Figure 1 (middle panel) represents several solutions to the ergodic HJB equation (16). It can be seen that the solution is unique up to a constant. For all possible solutions , the optimal control for the ergodic control problem is unique, as shown in Figure 1 (right panel).

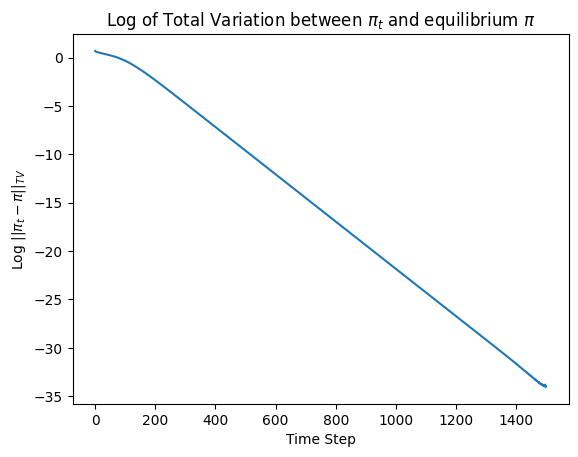

We continue to analyse the ergodicity of the market making system. Figure 2 (left panel) plots the inventory distribution at time , , , and under the ergodic optimal control . We can see that the distribution tends to converge to the dotted blue line over time, which is the theoretical equilibrium distribution of the inventory as derived in Appendix A.10. The right panel in Figure 2 plots the log of the total variation between the distribution and the equilibrium . We terminates the simulation at as it reaches the machine precision. It shows that the convergence rate to the equilibrium is exponential.

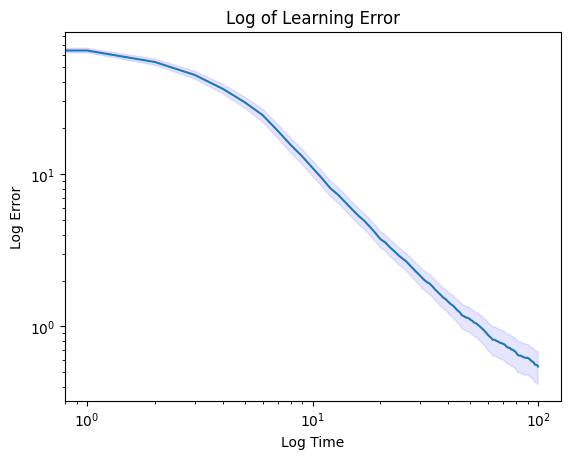

Now we proceed to simulate the proposed learning algorithm for the price sensitivity of market participants parameter and its achieved regret. Figure 3 (left panel) plots the learning error of Algorithm 1 in the log-log scale. Initially, the learning rate is slow due to the limited number of Bernoulli signals. As time increases, the estimated quickly converges to the true parameter . Moreover, the right panel of Figure 3, which is the Monte-Carlo simulation of the achieved (expected) regret of Algorithm 1, demonstrates that the algorithm regret grows sublinearly and is bounded by order . The complete code can be found at https://github.com/Galen-Cao/MM_parmater_learning.

4. Conclusion

In this paper, we introduced and analysed the ergodic formulation of the Avellaneda–Stoikov market making model. We established explicit solutions to the ergodic Hamilton–Jacobi–Bellman (HJB) equation and thus derived the optimal ergodic Markov controls. We’ve further shown that under the ergodic optimal control there is a unique invariant distribution for the market maker’s inventory and that any initial distribution converges exponentially fast to the equilibrium one. This allowed us to establish the regret upper bound of for learning the unknown price sensitivity of liquidity takers . Our work extends the known results on the market making model by providing a rigorous analysis of the ergodic setting and offering a robust solution for parameter learning. The numerical experiments further validate the theoretical results, confirming the robustness of the proposed algorithm.

A number of interesting questions have not been addressed in this paper and are left for future work. In particular, a key extension of the market making framework presented here accounts for adverse selection. Learning the parameters modelling adverse selection and establishing a regret bound would be interesting. Further, it would be interesting to compare this approach to a more classical RL algorithms where the optimal policy is learned directly. One would conjecture that as long as the market is behaving as the model postulates (up to the unknown parameter) using the optimal control derived from the maximum likelihood performs better. However, should the environment deviate from the model it’s possible that the pure RL approach will outperform the method proposed here.

Appendix A Proofs

A.1. Proof of Theorem 1

We first prove the properties of the Hamiltonian function given by (10).

Lemma 35 (Hamiltonian function).

For the Hamiltonian function , we have

-

(i)

, is finite.

-

(ii)

, such that

-

(iii)

is strictly increasing for any and ; and is strictly increasing for any and .

-

(iv)

is locally Lipschitz for any .

Proof.

Consider the function as , where and are given. By letting the first derivative of be and checking that the second derivative is less than , we know that attains its supremum at . Therefore, with the fact that ,

Moreover, the supremum in the right hand side can be attained at given by the above expression, hence the results.

(iii) Given and , consider and such that . Since , we have

By taking the supremum on both sides, we have . Similarly, we have if given and .

A.2. Proof of Theorem 3

Proof.

We first prove that for any taking values in and is bounded. We know that, by using Lemma 35 (1), there exists a constant such that,

| (33) |

and by the boundedness from below of the admissible control set , there exists such that

| (34) |

A.3. Proof of Theorem 4

To prove Theorem 4, we first prove the following lemma.

Lemma 36.

Let be given by (14), we have

-

(i)

such that for any and .

-

(ii)

such that for any and .

Proof.

By using the fact that the running reward function is bounded (33) and (34), we can apply [27, Lemma 4.3(1)] to get statement (i) of the lemma.

To prove statement (ii), we first define the stopping time under a control as

With the fact that, for , the transition probability for from , , we have . See more detailed discussion in Appendix A.10 for the transition probability matrix.

Let us consider with such that

Now we are ready to prove Theorem 4.

Proof.

In the proof we follow the ideas from [27, Proposition 4.6, 4.7]. As and by Lemma 36, we can consider a sequence converging towards such that the sequences and are convergent for . Let denote the limit of the sequence , we have

Let be a constant, then for any .

Next, we prove that is independent of the sequence . From the HJB equation (15), we have, for the sequence ,

Let . As the sequence is convergent, we know that is well defined. Take on both sides, we have

| (35) |

We then consider another sequence converging towards that leads to another limit for the sequence , i.e. . Let , then we have

Let . Since the domain for is bounded, we know that the supremum and infimum exist. Let us denote , and .

Let us first assume and prove that by contradiction. By the definition of , we have, for ,

Therefore,

By using the comparison principle, see [27, Lemma 4.4], we know that , for , which indicates a contradiction with the definition of . Hence, we have . By simply changing the order of and , we can obtain that . Therefore, we conclude that , i.e. is independent of the sequence . ∎

A.4. Proof of Theorem 5

Proof.

Let us define , then satisfies the following equation

| (36) |

subject to the initial condition with given by (11). We consider for with given in Theorem 4. We proceed to prove that is bounded.

Let us consider with the constant and given in Theorem 4 and , where is a sequence converging towards such that is convergent. From the ergodic HJB equation (16), we have,

Let us denote , where is the initial condition for the equation (36). Then we have, ,

By using the comparison principle (see [27, Proposition 3.2]), we know that for . We then consider , and clearly . By using the comparison principle again, we have . Therefore,

By the expression of and , we have

As is well defined that has been proved in Appendix A.3 and is bounded by definition, we can conclude that is bounded on .

Now let us consider with . Take the limit , we have

Since is bounded, therefore

where satisfies the HJB equation (13) with

A.5. Proof of Theorem 6

Proof.

By Theorem 2, the solution to can be given by . As the subdiagonal and the superdiagonal elements of are , , we can find a real and symmetric tridiagonal matrix whose entries are given by

| (37) |

which is similar to . Hence, by [36], (and ) can be diagonalised with distinct eigenvalues. Let , be real eigenvalues of with and be the diagonal matrix of such that , where ’s columns are the corresponding eigenvectors.

By Theorem 5, we have

Therefore, by considering the vector form of and using Theorem 2, we obtain

Let us denote and , then

hence the result.

∎

A.6. Proof of Lemma 23

Proof.

As discussed in Appendix A.5, we can find a real and symmetric tridiagonal matrix that is similar to , whose eigenvalues are simple, i.e. the algebraic multiplicity is . Moreover, it is obvious that given by (37) is . By [30, 32, 41], can be parameterised smoothly on , i.e. is . By Theorem 6, we know that . Therefore, we can conclude that is and is bounded on the compact set . ∎

A.7. Proof of Proposition 7

A.8. Proof of Proposition 8

Proof.

Notice that the right hand side of

| (38) |

is invariant under constant shifts in the solution and hence the optimal control for the ergodic control problem is uniquely given by expression (18) by simply solving the right hand side of (38) with the convention that for , respectively. Moreover from (10) it is easy to see that is single-valued and given by the result. ∎

A.9. Proof of Theorem 9

Proof.

By using Theorem 6, we get an explicit solution for . Therefore, to solve the ergodic HJB equation, the next step is to solve . Let , then

| (39) |

Let , be an -dim vector and be an - square matrix given by

Therefore, the equation (39) can be written in a matrix form as

| (40) |

By the fact of , we observe that , where the matrix is given in Theorem 2, is the largest eigenvalue of and is the identity matrix. As has distinct eigenvalues as proved in Appendix A.5, hence . Therefore, is the set of non-trivial solutions to the homogeneous equation (40) with the coefficient matrix . ∎

A.10. Proof of Lemma 11

Proof.

Given the ergodic optimal control , we consider the dynamic of inventory process (4) as a discrete Markov chain. Let be an square matrix labelled from to denoting the state transition matrix. The entries of are

| (41) |

From the discussion for the tridiagonal matrix in Appendix A.5, clearly is diagonalisable. Let be real eigenvalues of . Let be the diagonal matrix of with , where ’s columns are the eigenvectors of . As is a stochastic matrix, hence by Perron–Frobenius theorem,

Therefore, given an initial distribution , the equilibrium under as goes to infinity is

with an square matrix with only on the first diagonal element and otherwise

∎

A.11. Proof of Lemma 17

Proof.

The equation (24) is a step in the proof of Theorem 27 in a simpler case. We know that is the optimal control for the ergodic market making model under satisfying (18). Hence, from the ergodic HJB equation (16), we have

Therefore,

where we ignore the indicator functions in the first line and use for respectively. Moreover, we notice that the first line satisfies (21), therefore

Let denote the equilibrium of the optimal ergodic market making model under parameter and function be

By Lemma 36 (2), is bounded by . From a simpler version of Proposition 26 by substituting to , Lemma 12 and Lemma 36 (2), we have

with constants and independent of , hence the result. ∎

A.12. Proof of Lemma 20

Proof.

Let satisfy the linear ODE (29) subject to the terminal condition (11), i.e.

and . Clearly, the equation (29) is a linear ODE, hence there exists , which is a solution to (29).

Let us consider the following stochastic process, and we omit the superscript for for notational simplicity.

We know that follows the SDE (4) with market parameter and control , i.e.

where are compensated Poisson processes.

A.13. Proof of Proposition 21

Proof.

First, let be the expected reward in the discounted infinite-time-horizon setting, where the true price sensitivity parameter is but the market maker uses the strategy given by (18) with parameter , i.e.

| (42) |

where is given by (21). Then we claim that satisfies the following linear system

| (43) |

We would like to provide a sketch of proof for the claim. First, the existence of defined by (42) can follow the proof in Section A.2 for Theorem 3 but substituting the Hamiltonian function (10) for (27). Let be a solution for the linear system (43). Consider

By Itô’s formula

where the last equality comes from the definition of (27) and (21). Take the integral and expectation for , we have

As satisfies (43), therefore,

Take limit on both sides, with the fact that the limit exists, i.e.

Hence defined by (42).

Now, we would like to to show that given defined by (30), it holds that

| (44) |

where is defined by (42).

Let us start with the following lemma.

Lemma 37.

-

(1)

such that for and .

-

(2)

such that for and .

As , i.e. the collection of all Markov controls optimal for the ergodic control problem is a subset of the admissible control, the running reward function is bounded. By (21), we have

| (45) |

and by the boundedness from below of ,

| (46) |

To prove Lemma 37 (1), we first consider that

On the other hand,

Hence

with .

To prove Lemma 37 (2), we define the stopping time for with as

With the fact that, , the transition probability for from , i.e. , see the more detailed discussion in Section A.10, it implies that .

By (45) and (46), there exists such that for any . Therefore,

Therefore,

Since , we conclude that is bounded from above. By simply changing the order of and , we conclude the lower boundedness. Hence, we can find such that

.

With the fact that and are bounded, we can follow the discussion in Appendix A.3, i.e. consider a sequence converging towards such that the sequences and are convergent for , then show that there exists such that . Again by substituting (10) for in the proof of Theorem 5 in Appendix A.4, we can easily conclude that given by (44) also satisfies

Let us define for . By the convergent of under the sequence converging towards , we know that is well defined.

A.14. Proof of Proposition 22

Proof.

By (29), the linear ODE for can be written in a matrix form. Let be an vector, where . Now, let denote an -square matrix whose rows are labelled from to and entries are given by

| (47) |

Let be an vector where each component is

| (48) |

for . Then satisfies

| (49) |

with the terminal condition , with given by (11). Let denote the vector . We know that there exists a solution to the linear ODE (49) with the terminal condition on .

Now, let us consider the case of . We use to denote the th column of the coefficient matrix with . With the entries given by (47) under , we can observe that

which means is singular. Hence the solution to (49) under can be given by

| (50) |

By (47), is a real tridiagonal matrix with all positive off-diagonal entries. Clearly the eigenvalues of are simple, i.e. the algebraic multiplicity is 1. Furthermore, is diagonally dominant matrix with all negative diagonal entries, i.e.

then is negative semi-definite. Let be the eigenvalues of with , be the matrix whose columns are the corresponding eigenvectors and be the diagonal matrix. Then

where is the square matrix with only on the first diagonal element and otherwise. By (30), we know with the dim vector with all entries . ∎

A.15. Proof of Lemma 24

Proof.

First, we would like to prove that with given by 18 is . By Proposition 8 and Theorem 9, it is equivalent to show that by (19) is . Let us consider a matrix as

| (51) |

with for and . Then given in Theorem 9 can be transformed into a real and symmetric tridiagonal matrix by with entries

| (52) |

As there exists an solves (19), there must be an eigenvalue of , or as they are similar, with the corresponding eigenvector of and of . Therefore,

| (53) |

As is non-singular, we have . As shown in Appendix A.6, is , therefore given by (52) is . Hence, by [5, Result 7.2; Theorem 7.6], the eigenvector can be parameterised smoothly on . Obviously, is independent of . Therefore, we can conclude that is .

Proposition 22 gives an analytical solution to but it is not enough to show is twice differentiable, as ’s columns are the eigenvectors of whereas is not a self-adjoint or normal operator. Let us consider the matrix as

| (54) |

with for and . Then is a real and symmetric tridiagonal matrix with the entries as

| (55) |

There exists an orthogonal matrix whose columns are the eigenvectors of such that , where is the diagonal matrix with eigenvalues of since is similar to . Moreover, we have

hence . Therefore,

Let where is the corresponding eigenvector of with the eigenvalue . Then

where is the square matrix with all entries and is the eigenvector of with .

| (56) |

Clearly, is a smooth function and is . Therefore, (54), , (48) and are . Moreover, is a real and symmetric tridiagonal matrix with the simple eigenvalue . By [5, Result 7.2; Theorem 7.6], we know that can be chosen to be parameterised smoothly in . Hence, by (56), is at least and is bounded on the compact set . ∎

A.16. Proof of Proposition 26

Proof.

By Proposition 21 and by (27), the equation (31) can be expressed as

Take integral from to and then take the expectation with respect to the probability measure under the controlled SDE (22) with , we have

where we omit the indicator function in the first line since when , respectively. As is independent of and by Proposition 21, dividing by we get

Moreover, for the initial distribution , we have

Hence

which concludes the proof. ∎

A.17. Proof of Theorem 27

Proof.

By (31) in Proposition 21 and (27), we have,

where we ignore the indicator functions in the first line since for , respectively. Also, by definition, we know that

Therefore, by Definition 16 of regret,

| (57) |

Let us define

| (58) |

Then

where the last inequality comes from Corollary 25. Moreover, is the probability measure evolves under control and parameter with . By Lemma 37 (2), there exists a constant such that for . Therefore,

where is the probability measure of equilibrium distribution under control and parameter , and the last step uses Proposition 26. Then,

where denotes the total variation. By Lemma 12, we have

where and for . The existence of and can be concluded by the following discussion. Since the convergence rate is actually the second largest eigenvalue of the transition probability matrix [20, 21], which is a continuous function of on by the fact that all eigenvalues for the tridiagonal transition matrix are simple, i.e. the multiplicity is 1. Therefore, there exists . Moreover, can be given by the norm of the eigenvectors for . By [3], if all the eigenvalues of the are simple, the corresponding eigenvectors can be chosen absolutely continuous on , hence the existence of .

Let and , we conclude the result. ∎

A.18. Proof of Concentration Inequality

A.18.1. Proof of Proposition 28

Proof.

Let . Since and since , we get that

Therefore, by the Markov inequality, for any ,

In particular,

By applying the same argument to , we obtain the reverse inequality and prove the required result conditional on . Taking the tower property, we achieve the required claim. ∎

A.18.2. Proof of Proposition 30

A.18.3. Proof of Proposition 31

Proof.

Observe that as , and as , . Hence, the solution exists by continuity. The uniqueness follows from the fact that for all . ∎

A.18.4. Proof of Proposition 32

Proof.

Since ,

Let , we know that is bounded given and . Therefore, by Proposition 28, with -probability at least ,

where

∎

A.18.5. Proof of Theorem 33

A.19. Proof of Corollary 33.1

A.20. Proof of Proposition 34

On the event that Corollary 33.1 holds, we can see that

By choosing to be sufficiently large, i.e. , we have

| (59) |

where the last inequality comes from for any .

Next we need the following lemma which is proved in [39, Lemma 3.1].

Lemma 38.

Let be an IID sub-exponential random variable with mean and . Then there exists a constant such that for any and

By using the above result applying to and taking the countable union of the above events, we have

Now, we note that is sub-exponential with mean . Hence, on the event that Corollary 33.1 and Lemma 38 hold with , we know that with probability at least , it holds that

| (60) |

where the last inequality uses the fact that for large and for small . Note that the constant comes from Lemma 38 which is independent of , hence the result.

References

- [1] Yasin Abbasi-Yadkori and Csaba Szepesvári. Regret bounds for the adaptive control of linear quadratic systems. In Proceedings of the 24th Annual Conference on Learning Theory, pages 1–26. JMLR Workshop and Conference Proceedings, 2011.

- [2] Marc Abeille and Alessandro Lazaric. Improved regret bounds for thompson sampling in linear quadratic control problems. In International Conference on Machine Learning, pages 1–9. PMLR, 2018.

- [3] Andrew F Acker. Absolute continuity of eigenvectors of time-varying operators. Proceedings of the American Mathematical Society, 42(1):198–201, 1974.

- [4] Naman Agarwal, Elad Hazan, and Karan Singh. Logarithmic regret for online control. Advances in Neural Information Processing Systems, 32, 2019.

- [5] Dmitri Alekseevsky, Andreas Kriegl, Mark Losik, and Peter W Michor. Choosing roots of polynomials smoothly. arXiv preprint math/9801026, 1998.

- [6] Mariko Arisawa and P-L Lions. On ergodic stochastic control. Communications in partial differential equations, 23(11-12):2187–2217, 1998.

- [7] Peter Auer, Thomas Jaksch, and Ronald Ortner. Near-optimal regret bounds for reinforcement learning. Advances in neural information processing systems, 21, 2008.

- [8] Peter Auer and Ronald Ortner. Logarithmic online regret bounds for undiscounted reinforcement learning. Advances in neural information processing systems, 19, 2006.

- [9] Marco Avellaneda and Sasha Stoikov. High-frequency trading in a limit order book. Quantitative Finance, 8(3):217–224, 2008.

- [10] Matteo Basei, Xin Guo, Anran Hu, and Yufei Zhang. Logarithmic regret for episodic continuous-time linear-quadratic reinforcement learning over a finite-time horizon. Journal of Machine Learning Research, 23(178):1–34, 2022.

- [11] Marco C Campi and PR Kumar. Adaptive linear quadratic gaussian control: the cost-biased approach revisited. SIAM Journal on Control and Optimization, 36(6):1890–1907, 1998.

- [12] Álvaro Cartea, Ryan Donnelly, and Sebastian Jaimungal. Algorithmic trading with model uncertainty. SIAM Journal on Financial Mathematics, 8(1):635–671, 2017.

- [13] Álvaro Cartea, Fayçal Drissi, Leandro Sánchez-Betancourt, David Siska, and Lukasz Szpruch. Automated market makers designs beyond constant functions. Available at SSRN 4459177, 2023.

- [14] Álvaro Cartea and Sebastian Jaimungal. Risk metrics and fine tuning of high-frequency trading strategies. Mathematical Finance, 25(3):576–611, 2015.

- [15] Álvaro Cartea, Sebastian Jaimungal, and José Penalva. Algorithmic and high-frequency trading. Cambridge University Press, 2015.

- [16] George Casella and Roger Berger. Statistical inference. CRC Press, 2024.

- [17] Asaf Cassel, Alon Cohen, and Tomer Koren. Logarithmic regret for learning linear quadratic regulators efficiently. In International Conference on Machine Learning, pages 1328–1337. PMLR, 2020.

- [18] Alon Cohen, Tomer Koren, and Yishay Mansour. Learning linear-quadratic regulators efficiently with only regret. In International Conference on Machine Learning, pages 1300–1309. PMLR, 2019.

- [19] Sarah Dean, Horia Mania, Nikolai Matni, Benjamin Recht, and Stephen Tu. Regret bounds for robust adaptive control of the linear quadratic regulator. Advances in Neural Information Processing Systems, 31, 2018.

- [20] Persi Diaconis and Daniel Stroock. Geometric bounds for eigenvalues of markov chains. The annals of applied probability, pages 36–61, 1991.

- [21] Rick Durrett. Probability: theory and examples, volume 49. Cambridge university press, 2019.

- [22] Mohamad Kazem Shirani Faradonbeh, Ambuj Tewari, and George Michailidis. On adaptive linear–quadratic regulators. Automatica, 117:108982, 2020.

- [23] Ronan Fruit and Alessandro Lazaric. Exploration-exploitation in mdps with options. In Artificial intelligence and statistics, pages 576–584. PMLR, 2017.

- [24] Xuefeng Gao and Xun Yu Zhou. Logarithmic regret bounds for continuous-time average-reward markov decision processes. arXiv preprint arXiv:2205.11168, 2022.

- [25] Olivier Guéant. The Financial Mathematics of Market Liquidity: From optimal execution to market making, volume 33. CRC Press, 2016.

- [26] Olivier Guéant, Charles-Albert Lehalle, and Joaquin Fernandez-Tapia. Dealing with the inventory risk: a solution to the market making problem. Mathematics and financial economics, 7:477–507, 2013.

- [27] Olivier Guéant and Iuliia Manziuk. Optimal control on graphs: existence, uniqueness, and long-term behavior. ESAIM: Control, Optimisation and Calculus of Variations, 26:22, 2020.

- [28] Xin Guo, Anran Hu, and Yufei Zhang. Reinforcement learning for linear-convex models with jumps via stability analysis of feedback controls. SIAM Journal on Control and Optimization, 61(2):755–787, 2023.

- [29] Ben Hambly, Renyuan Xu, and Huining Yang. Policy gradient methods for the noisy linear quadratic regulator over a finite horizon. SIAM Journal on Control and Optimization, 59(5):3359–3391, 2021.

- [30] Roger A Horn and Charles R Johnson. Matrix analysis. Cambridge university press, 2012.

- [31] Robert I Jennrich. Asymptotic properties of non-linear least squares estimators. The Annals of Mathematical Statistics, 40(2):633–643, 1969.

- [32] Andreas Kriegl and Peter W Michor. Differentiable perturbation of unbounded operators. Mathematische Annalen, 327:191–201, 2003.

- [33] PR Kumar. Optimal adaptive control of linear-quadratic-gaussian systems. SIAM Journal on Control and Optimization, 21(2):163–178, 1983.

- [34] Mauricio Labadie and Pietro Fodra. High-frequency market-making with inventory constraints and directional bets. Quantitative Finance, 2013.

- [35] Sahin Lale, Kamyar Azizzadenesheli, Babak Hassibi, and Anima Anandkumar. Explore more and improve regret in linear quadratic regulators. arXiv preprint arXiv:2007.12291, 31:32, 2020.

- [36] Beresford N Parlett. The symmetric eigenvalue problem. SIAM, 1998.

- [37] Max Simchowitz and Dylan Foster. Naive exploration is optimal for online lqr. In International Conference on Machine Learning, pages 8937–8948. PMLR, 2020.

- [38] Lukasz Szpruch, Tanut Treetanthiploet, and Yufei Zhang. Exploration-exploitation trade-off for continuous-time episodic reinforcement learning with linear-convex models. arXiv preprint arXiv:2112.10264, 2021.

- [39] Lukasz Szpruch, Tanut Treetanthiploet, and Yufei Zhang. Optimal scheduling of entropy regularizer for continuous-time linear-quadratic reinforcement learning. SIAM Journal on Control and Optimization, 62(1):135–166, 2024.

- [40] Daniel H Wagner. Survey of measurable selection theorems: an update. In Measure Theory Oberwolfach 1979: Proceedings of the Conference Held at Oberwolfach, Germany, July 1–7, 1979, pages 176–219. Springer, 2006.

- [41] Yongjia Xu and Yongzeng Lai. Derivatives of functions of eigenvalues and eigenvectors for symmetric matrices. Journal of Mathematical Analysis and Applications, 444(1):251–274, 2016.