Factor Analysis: A P-Stationary Point Theory

Abstract

Factor Analysis is a widely used modeling technique for stationary time series which achieves dimensionality reduction by revealing a hidden low-rank plus sparse structure of the covariance matrix. Such an idea of parsimonious modeling has also been important in the field of systems and control. In this article, a nonconvex nonsmooth optimization problem involving the norm is constructed in order to achieve the low-rank and sparse additive decomposition of the sample covariance matrix. We establish the existence of an optimal solution and characterize these solutions via the concept of proximal stationary points. Furthermore, an ADMM algorithm is designed to solve the optimization problem, and a subsequence convergence result is proved under reasonable assumptions. Finally, numerical experiments demonstrate the effectiveness of our method in comparison with some alternatives in the literature.

Index Terms:

Factor Analysis, low-rank plus sparse matrix decomposition, norm, nonconvex nonsmooth optimization, ADMM.I Introduction

Factor Analysis (FA) is a classic topic which originates in psychology [1, 2, 3] and is studied in econometrics [4, 5, 6, 7] with modern developments in diverse fields such as system identification, signal processing, statistics, and machine learning, cf. [8, 9, 10, 11, 12, 13, 14, 15, 16] and the references therein. A standard model for FA can be found e.g., in [17, Sec. 7.7] and reads as

| (1) |

where

-

•

is an observed vector,

-

•

is a mean vector,

-

•

is a deterministic “factor loading” matrix with linearly independently columns,

-

•

the random vector stands for the hidden factors,

-

•

and is the additive noise with an unknown covariance matrix independent of .

The model is widely used for linear dimensionality reduction due to the typical situation that . Suppose that we have obtained i.i.d. samples from the model. The problem is about estimating the loading matrix , or equivalently, the rank symmetric matrix , and the noise covariance matrix . From the viewpoint of system identification, this is a static identification problem in which the output depends solely on the current input .

Assume for simplicity that the mean vector . According to the independence assumption, the covariance matrix of admits an additive decomposition as

| (2) |

In the special case where , the problem reduces to the standard Principal Component Analysis (PCA). A slightly relaxed assumption requires to be diagonal, as is typically done in FA. Then (2) can be interpreted as a kind of “low-rank plus sparse” matrix decomposition. In practice, the true covariance matrix is very often not available and instead must be estimated from the observed samples. For example, a usual averaging scheme gives

| (3) |

where is a residual matrix. The FA problem now becomes estimating the low-rank and the sparse from the noisy estimate of the covariance matrix.

Following this type of thinking, there has been extensive research on the so-called robust PCA, see e.g., [18, 19, 20, 21, 22, 23], where convex optimization methods are employed to separate the low-rank matrix from the sparse one, and techniques from compressed sensing are used to establish strong recovery guarantees. Applications include foreground/background extraction in video surveillance, and face recognition, etc. However, we must point out that these works mostly utilize the norm on the component in order to enforce sparsity, while the most natural choice is the norm111Notice that the norm is not a bona fide norm as it obviously violates the absolute homogeneity. It is still termed “norm” in this paper for simplicity. which counts the number of nonzero entries in a matrix. Moreover, they use the squared Frobenius norm to quantify the mismatch between candidate and the estimate . In this way, no special attention is paid to covariance matrices, and even rectangular matrices are allowed.

In the recent paper [15], the FA problem is formulated via constrained convex optimization involving the Kullback–Leibler (KL) divergence between two positive definite matrices. The KL divergence here is in fact a special case of the object with the same name, and can be interpreted as a pseudodistance between two zero-mean multivariate normal distributions where the two positive definite matrices are the covariance matrices, see e.g., [24]. It has been extensively used in information theory, statistics [25], and system identification, notably in spectral estimation [26, 27, 28, 29] and graphical model learning [30, 31, 32, 14, 33, 34, 35, 36, 37]. Motivated by the work in [15], in the current paper we shall remove the usual constraint for to be diagonal, and instead require to be sparse as measured by the norm. The resulting optimization problem is, however, nonconvex and nonsmooth due to the discrete nature of the norm. Drawing inspirations from recent developments in the sparse optimization, cf. e.g., [38, 39, 40, 13, 41, 42, 43, 44, 45, 46, 47], we approach the problem via the theory of proximal stationary points which can be viewed as a nonsmooth version of the first-order Karush-Kuhn-Tucker (KKT) conditions. Then the optimality conditions are integrated into an Alternating Direction Method of Multipliers (ADMM) for the numerical solution of the optimization problem, and a subsequence convergence result is provided under certain assumptions. Simulations on synthetic and real data show that our method is able to find the number of hidden factors, i.e., the rank of , in a robust way.

I-A Organization

The remainder of our paper is organized as follows. Using the norm in conjunction with the KL divergence, Section II constructs the nonconvex optimization model for low-rank plus sparse matrix decomposition and establishes the existence of a solution. Section III provides the optimality theory that connects an optimal solution to a P-stationary point. Section IV presents an ADMM algorithm to find a solution and its local convergence analysis. Section V conducts numerical experiments to assess the effectiveness of the proposed algorithm through its application to both synthetic and real datasets. Finally, we conclude this work in Section VI.

I-B Notation

Throughout this article, we use bold uppercase letters and bold lowercase letters to represent matrices and vectors, respectively. For two square matrices and of the same size, we write the inner product as . The symbols and denote transpose and the Frobenius norm, respectively. The norm counts the number of nonzero entries in a matrix or a vector. If is positive semidefinite, we write , and means that is positive definite.

II Problem Formulation and Existence of a Solution

In this paper, we mainly consider the following optimization problem:

| (4a) | ||||

| s.t. | (4b) | |||

| (4c) | ||||

| (4d) | ||||

where , , and the sample covariance matrix are all square of size ,

is the KL divergence between two positive definite matrices, and and are tuning parameters. The first term in the objective function is equal to the nuclear norm which is a convex surrogate of the rank function [48]. Throughout this article, we assume that so that we can take its inverse in the definition of the KL divergence. To get a more concise optimization model, we substitute the variable in (4) with . Then we get the following equivalent form

| (5a) | ||||

| s.t. | (5b) | |||

where the feasible set

| (6) |

and

| (7a) | ||||

| (7b) | ||||

Remark 1.

The paper [15] considered the following optimization problem for FA:

| (8) | ||||||

| s.t. | ||||||

The idea is to utilize the KL divergence to constrain the candidate covariance matrix in a “neighborhood” of controlled by the tuning parameter . The interest in this constrained version instead of the regularized version similar to (4) lies in the fact that a probabilistic strategy can be adopted to select the parameter via analysis with the Gaussian Orthogonal Ensemble, so that ad-hoc procedures for parameter selection such as the cross validation is not needed. We assume that the computational power does not pose serious limitations for us, and hence do not insist on this constrained version in the current work.

It is worth noting that the nonconvexity of the objective function is solely attributed to the term .

More precisely, we have the next result.

Proposition 1.

The function in (7) is smooth and jointly strictly convex in .

Proof.

The additive structure of in (7) can be simplified as , where is linear and is smooth and strictly convex [24]. The claim of the proposition follows directly from the fact that the term is smooth and strictly convex. The smoothness is trivial as long as . The strict convexity reduces simply to definition checking. ∎

Remark 2.

The next result concerns the existence of a solution to (5) whose proof needs some additional lemmas.

Theorem 1.

The optimization problem (5) admits a solution in and the set of all minimizers is bounded.

Lemma 1.

The objective function in (5) is lower semicontinuous.

Proof.

In view of Proposition 1, we only need to show that the norm is lower semicontinuous. Let be arbitrary. By the definition of lower semicontinuity, we have to establish the fact that for any , there exists such that

| (9) |

Indeed, when is small enough, all the nonzero entries of must remain nonzero in , and we have

| (10) |

A fortiori, (9) must hold and the proof is complete. ∎

Lemma 2.

Suppose that there is a sequence such that or tends to infinity as . Then the sequence of function values also goes unbounded.

Proof.

Since the term always remains bounded, we only need to show the divergence of the sequence . Suppose first that as . Then the largest eigenvalue of must also tends to infinity due to norm equivalence. Consequently, we have . For other terms in (7a), we know (bounded from below), see e.g., [24], and the rest are constants. Hence necessarily diverges.

Next suppose that as . Let us write for simplicity. Obviously, in this case the largest eigenvalue of must tend to infinity. According to (7b), we only need to compare the two terms in the brace, namely . We shall use the spectral decomposition where is orthogonal and is the diagonal matrix of eigenvalues. Likewise, we have . Then it is not difficult to derive that

| (11a) | ||||

| (11b) | ||||

where , and is the norm squared of the -th column of . Clearly, each is bounded away from zero because of the structure of . Consider the function defined for with a parameter . It is strictly convex on the positive semiaxis and has a minimum value of at . Consequently, each summand in (11b) is bounded from below and because as argued above. Therefore, must also diverge in this case. ∎

Lemma 3.

Suppose that we have a convergent sequence which tends to some as such that but is singular. Then the sequence of function values tends to infinity.

Proof.

It is clear that formula (11) is still valid for . Now due to convergence, each eigenvalue must remain bounded. It is easy to observe that when . This implies that when is singular, the sum in also diverges following the argument in the proof of Lemma 2. As a result, , and hence , must go to infinity as . ∎

We are now ready to prove Theorem 1.

Proof of Theorem 1.

Take an arbitrary feasible point of (5), and let . Consider the sublevel set

| (12) |

which is obviously nonempty because it contains . Suppose that we have a convergent sequence which tends to some . We first exclude the possibility that but is singular. Indeed, if that were true, then by Lemma 3, would eventually surpass which means that would step out of the sublevel set, a contradiction. Therefore, the limit point must be such that and still feasible, that is, . Furthermore, Lemma 1 implies that the sublevel set is closed.

In addition, one can argue that the sublevel set is also bounded. To see this, suppose the contrary, i.e., the sublevel set were unbounded. Then according to Lemma 2, there would exist a sequence such that the function value diverges, leading to a contradiction similar to the previous one.

Due to finite dimensionality, the sublevel set (12) is seen to be compact. Finally, appealing to the extreme value theorem of Weierstrass, we conclude that a minimizer of exists in , and the boundedness claim comes from the compactness of the sublevel set. ∎

III Optimality Theory

In this section, we shall characterize the optimal solutions to (5). To begin with, we shall review some well known results concerning the proximal operator, see e.g., [49], [50] where it is called hard thresholding operator.

III-A proximal operator

We first discuss the scalar case. Given a parameter , the proximal operator of is defined as

| (13) |

The proof of the next lemma is a simple exercise and is therefore omitted.

Proposition 2.

The solution to the proximal operator in (13) is expressed as

| (14) |

In order to avoid ambiguity, we choose to absorb the middle case of (14) into the first case. In terms of the formula, we use

| (15) |

in the remaining part of this paper. The graph of such a function is drawn in Fig. 1.

The matricial version of (13) is then not difficult to derive. Indeed, for we have

| (16) | ||||

Since the objective function above can be decoupled for each element , the solution to the matricial proximal operator can be written as

| (17) |

In plain words, the outcome of the proximal operator is obtained by elementwise applications of the scalar solution (15).

III-B General optimization model

In this subsection and the next one, we work on the abstract optimization model (5) and temporarily forget about the specific functional form of in (7). More precisely, we make the following assumptions.

Assumption 1.

The function in (5) is jointly strictly convex in .

Assumption 2.

The gradient of is Lipschitz continuous with a Lipschitz constant on the sublevel set (12), that is, for any and in , it holds that

| (18) |

where the gradient operators and are identified with suitable symmetric matrices. Here the superscripts are simply labels for the variables instead of usual exponents.

The next result is straightforward, and it also shows that the specific problem (5) with in (7) is just a special case for the optimality theory provided in this section.

Proof.

The strict convexity of has been shown in Proposition 1. To show that in (7) has a Lipschitz continuous gradient, we use a previous result claiming that has a compact sublevel set, see the proof of Theorem 1. More precisely, it is well known that a smooth function ( here in view of Proposition 1 again) is Lipschitz continuous on any compact convex set, which yields the assertion. ∎

III-C P-stationarity conditions

The Lagrangian of the optimization problem (5) can be expressed as

| (19) |

where and are the Lagrange multipliers for the constraints and . For the moment, we ignore the strict inequality constraint . Now we introduce a generalized definition of a KKT point in nonlinear programming.

Definition 1 (P-stationary point of (5)).

The pair is called a proximal stationary (abbreviated as P-stationary) point of (5) if there exist by symmetric matrices , and a real number such that the following set of conditions hold:

| (20a) | ||||

| (20b) | ||||

| (20c) | ||||

| (20d) | ||||

| (20e) | ||||

| (20f) | ||||

Formulas in (20) describe the usual first-order KKT conditions [51] except for (20f). Indeed (20a) and (20b) are the primal constraints, (20c) is the dual constraint, (20d) is the complementary slackness condition, and (20e) and (20f) are the stationarity condition of the Lagrangian with respect to the primal variables. The unique distinction is that the nondifferentiable term results in the proximal operator (16).

Theorem 2.

Proof.

To show Point 1), we first fix , and (20b) is just a feasibility condition. Obviously, we have

| (21) |

where the right hand side is a smooth convex optimization problem. Hence the usual KKT conditions read as (20a), in (20c), in (20d), and (20e), where is the Lagrange multiplier.

Then we fix and derive the remaining conditions, namely in (20c), in (20d), and (20f). Similarly, we have

| (22) |

The usual KKT analysis brings about the conditions and . In fact, we must have due to the additional assumption and holds trivially. Hence (20f) reduces to

| (23) |

which is to be shown next. By global optimality, we have

| (24) |

where is an arbitrary positive semidefinite matrix that satisfies . Then using the mean value theorem, Cauchy–Schwarz inequality, and Assumption 2, it is not difficult to show that

| (25) | ||||

where for some , and we have set for short.

Now, let us take a particular which is the left side of (23) with . According to the definition of the proximal operator (16), we have

| (26) |

Combining the previous inequalities, we obtain the following:

| (27a) | ||||

| (27b) | ||||

| (27c) | ||||

where (27a) is the same as (24), (27b) is implied by (25), (27c) is a consequence of (26), and the last inequality comes from the fact due to our choice of . Therefore, we have and thus which is precisely (23), a simplified version of (20f).

Now let us treat Point 2). Suppose that we are given a P-stationary point in the sense of Definition 1. For simplicity, we write and still . The aim is to show that there exists a sufficiently small neighborhood

| (28) |

with such that is locally optimal in where is the feasible set given in (6). That is to say, for all , it holds that

| (29) |

First, we know that there exists such that

| (30) |

holds for all , and the reason has been explained in the proof of Lemma 1. Then by the continuity of , there exists such that implies

| (31) |

We take in (28). In order to show the inequality (29), we need to introduce some index sets. Let and be the Cartesian product providing indices for the entries of matrices. Define and the complement. According to the evaluation formula (15) for the proximal operator, we have the following observations.

Next we work on two cases corresponding to a partition of the feasible set . Define

| (34) |

where the latter set in the intersection is a linear subspace.

Case 1: . We can employ Assumption 1 and write down the following chain of inequalities:

| (35a) | ||||

| (35b) | ||||

| (35c) | ||||

| (35d) | ||||

| (35e) | ||||

| (35f) | ||||

where,

-

•

(35a) is the first-order characterization of convexity,

- •

- •

- •

In short, the reasoning above gives which plus (30) yields the desired inequality (29).

Case 2: . In this case, there exists some such that while . It follows that . Combining this point with (31) leads to

| (36) | ||||

Therefore, in both cases (29) holds and this completes the proof of local optimality of a P-stationary point. ∎

IV Numerical Algorithm

In this section, we propose an ADMM algorithm to solve the optimization problem (5) and perform convergence analysis of this algorithm.

IV-A ADMM for (5)

The presence of the log-determinant term in (5) implicitly enforces that . To simplify the algorithm design, we temporarily disregard this constraint. In addition, we introduce two auxiliary variables and with equality constraints and , and the indicator function to handle the remaining inequality constraints, see [52, Sec. 5]. The problem (5) can be reformulated as

| (37) | ||||||

| s.t. | ||||||

where the indicator function

| (38) |

Let and denote the Lagrange multipliers associated with the equality constraints in (37). Then we construct the augmented Lagrangian [52]

| (39) | ||||

where is a penalty parameter. Given the current iterate , the ADMM updates each variable via a Gauss–Seidel scheme:

| (40a) | ||||

| (40b) | ||||

| (40c) | ||||

| (40d) | ||||

| (40e) | ||||

| (40f) | ||||

- •

-

•

The -subproblem (40b) can be expressed as

(43) Due to the presence of , it is difficult to find a closed-form solution. In this case, we employ a proximal gradient descent step

(44) where is a step size.

-

•

The -subproblem (40c) can be reduced to

(45) In order to deal with the constraint , we introduce the projection operator onto , the cone of positive semidefinite matrices. Let be the spectral decomposition of a symmetric matrix , where and represent the -th eigenvalue and the corresponding eigenvector. Then the projection operator can be expressed as

(46) With the help of the projection operator, we take

(47) as a solution to (45).

-

•

The -subproblem (40d) is similar to , and a minimizer can be calculated by

(48)

IV-A1 Initialization of Algorithm 1

We first compute the spectral decomposition of where is the eigenvalue matrix such that . Let with . Then we initialize the ADMM as follows:

| (49) |

and the initial Lagrange multiplier matrices and are set to zero matrices.

IV-A2 Stopping condition of Algorithm 1

We terminate Algorithm 1 when two successive iterates are sufficiently close. Such a condition can be described as

| (50) |

where represents the tolerance level, and

| (51) | ||||

IV-B Convergence analysis

In this subsection, we present convergence analysis of the proposed ADMM algorithm. For convenience, let us set . Suppose that is a sequence generated by Algorithm 1. The next lemma shows that the sequence of function values satisfies a kind of sufficient descent condition at each iteration.

Lemma 4.

For a sufficiently large penalty parameter , we choose any . Then the ADMM iterates satisfy the inequality

| (52) | ||||

for some sufficiently small and all .

Proof.

See the appendix. ∎

Based on the above intermediate result, next we demonstrate the boundedness property of the whole sequence of the ADMM iterates.

Proposition 4.

Under the conditions of Lemma 4, suppose further that the sequence of dual variables is bounded. Then is bounded.

Proof.

Using the argument in the proof of Lemma 1, we can show that the augmented Lagrangian is lower semicontinuous. Let be the initialization of Algorithm 1. According to Lemma 4, for we have

| (53) | ||||

Exploiting the boundedness assumption on , we can show without difficulty that the quadratic function is bounded from below, and that the function value diverges to infinity if or tends to infinity separately. The same argument applies to the quadratic function .

Now we are ready to prove the boundedness of . Suppose first that is unbounded, which means that there exists a subsequence, still written as , such that . Then we have

It follows from Lemma 2 that approaches infinity, which is a contradiction to (53). Therefore, remains bounded. In the same manner, we can derive the boundedness of . In addition, boundedness of and can be shown via properties of the quadratic functions which are observed right after (53). Consequently, the boundedness of is established. ∎

By the Bolzano–Weierstrass theorem, Proposition 4 implies that there exists a subsequence that converges to a cluster point . The next result shows that two successive iterates are eventually close to each other.

Proposition 5.

Under the conditions of Lemma 4, we have .

Proof.

According to the proof of Lemma 2, the objective function in (5) is bounded from below. It is then straightforward to show that the same holds for the augmented Lagrangian (39), i.e., for some constant . By Lemma 4, the sequence of function values is monotonically decreasing, and hence must converge by the monotone convergence theorem. More precisely, we have

| (54) | ||||

Letting , we have

| (55) | |||

which clearly implies . ∎

Remark 3.

Global convergence of the ADMM is hard to establish without the Kurdyka–Łojasiewicz (KŁ) property in the presence of a nonconvex or nonsmooth term in the objective function [54, 55, 56]. It is known that semialgebraic functions and continuous subanalytic functions over closed domains satisfy the KŁ property. While our objective function can be written as a sum of functions of these two types, it is in general not true that the KŁ functions have the additive property. For this reason, we are unable to prove that our augmented Lagrangian (39) satisfies the KŁ property. Therefore, the issue of global convergence appears very challenging and will be left for future research.

In the final part of this subsection, we show that if the whole sequence of the ADMM iterates converges, the cluster point is indeed a locally optimal solution to (5).

Proposition 6.

Proof.

Taking the limit of (40e), we have and thus

| (56) |

Since the subproblem (40c) for is smooth, we can write down its KKT conditions as

| (57a) | ||||

| (57b) | ||||

| (57c) | ||||

| (57d) | ||||

where is the Lagrange multiplier for . It follows from (57d) that must also converge to some . In view of (56), we immediately have . Now we let , and the relations in (57) can be rewritten as

| (58a) | ||||

| (58b) | ||||

| (58c) | ||||

Similarly, a limit argument on (40f) yields , and a KKT analysis on (40d) gives the conditions

| (59a) | ||||

| (59b) | ||||

| (59c) | ||||

The first-order optimality condition of the subproblem (40a) is . Taking the limit as , we arrive at (20e). In a similar fashion, if we take limits on both sides of (44), we obtain (20f). The remaining condition (20b) holds by the premise of theorem. Thus we have shown that the cluster point is a P-stationary point, and its local optimality is a consequence of Theorem 2. ∎

V Numerical Experiments

In this section, we evaluate the performance of Algorithm 1 via numerical experiments on synthetic and real economic datasets. All these simulations are implemented in MATLAB (R2022a) on a MacBook Pro with 64 GB RAM and an Apple M1 Max processor.

V-A Synthetic data examples

In this subsection, we conduct Monte Carlo simulations, each having 100 repeated trials, following the steps outlined below.

-

i)

Randomly generate a matrix with rank and a diagonal of size , where the cross-sectional dimension .

-

ii)

Generate a sample sequence of length according to the FA model (1) with .

-

iii)

Compute the sample covariance matrix

-

iv)

Select parameters through the Cross Validation (CV) and then run Algorithm 1 to compute the estimate .

-

v)

Compute the numerical rank of the optimal via

(60) where represent the eigenvalues of , and denotes the minimum index satisfying in accordance with [15].

V-A1 Evaluation metrics

Estimation of the number of factors is an important task in FA. Two performance indices are proposed in [15] which are also used here:

-

•

the root mean squared error (RMSE) between the true rank and the numerical rank , namely

(61) where is a label for trials in a Monte Carlo simulation,

-

•

and the subspace recovery accuracy

(62) where and are the true and estimated factor loading matrices, respectively, and denotes the projection matrix onto the column space (range) of . Evidently, the above ratio is between and , and a larger value indicates better alignment of the column spaces of and .

V-A2 Parameters setting

We set the tolerance parameter in (50) to be and the maximum number of iterations . The tuning parameters and represent the trade-off between the low-rankness of , the model misfit as measured by the KL divergence, and the sparsity of , while is the penalty parameter in the augmented Lagrangian (39). We use a CV procedure to select them. The candidate set for and is and is selected from . We randomly partition the samples generated in Step ii) above into training and validation sets of equal size. Using the optimal solution computed on the training set under a specific parameter configuration and the sample covariance matrix computed on the validation set, we define the following score function

| (63) |

The parameter triple corresponding to the minimum score function value is selected.

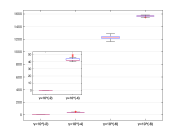

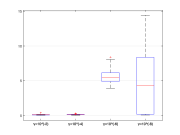

Next, we consider the selection of the parameter in the update of in (44) which comes from the proximal operator (15) and can be interpreted as a step size. We must emphasize that in our implementation, once is selected, it does not change in each simulation, including the CV and the final solution with the chosen parameters . If is large, it will immediately set into a zero matrix due to the thresholding operation, thus leading to convergence of the update. On the other hand, when is extremely small, the proximal operator (15) essentially reduces to an identical mapping, and Algorithm 1 is simply the ADMM for (5) without the sparsity enforcing term . As a consequence, such a solution does not induce sparsity on . This point can also be observed from our simulations. Indeed, we take , respectively, and perform Monte Carlo simulations on the same dataset with and the true rank . To speed up the convergence of Algorithm 1, a projection step onto the cone of semidefinite matrices was incorporated into the updates of . Fig. 2 shows the results in terms of three metrics: the KL divergence between the computed and the true covariance matrix , , and the running time. The subfigure 2(ii) indicates that when , the returned is a zero matrix. In contrast, when or , has poor sparsity. The choice appears to produce the best estimate . In addition, Table I presents the RMSE (61) of the numerical rank estimate (60) for two Monte Carlo simulations in which and the true rank is and , respectively. In view of the results in Fig. 2 and Table I, we set which seems rather reasonable for synthetic datasets.

| 0 | 0 | 0 | 1.5556 | |

| 0 | 0 | 0 | 2.2782 |

(I) )

(ii)

(iii) Runtime

V-A3 Comparison with [15]

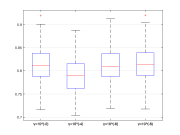

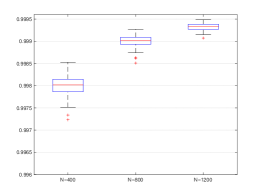

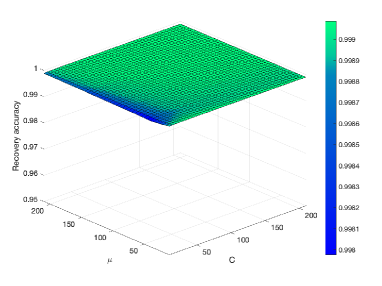

Similar to the simulation setup in [15], we consider two scenarios in which the true rank of is and , respectively, and perform Monte Carlo simulations with different data lengths . The subspace recovery index (62) for each trial is shown via the boxplot in Fig. 3. One can observe that the subspace recovery accuracy increases with the number of available samples. Moreover, despite the presence of a few outliers, the values of consistently surpass the threshold. Compared to the prior work [15], more precisely, Fig. 2 in that paper, we remark that Algorithm 1 has made visible improvements in the subspace recovery of .

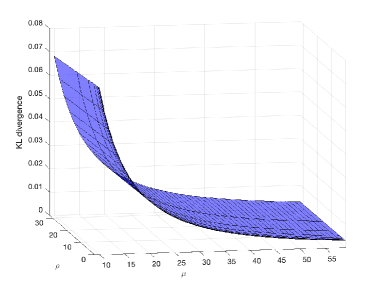

In addition, we have also generated a set of samples of size and to see the effect of parameters , , and on the subspace recovery index. More specifically, Fig. 4 illustrates the quantity as a function of for a fixed . The surface plot is quite flat which means that Algorithm 1 achieves robust recovery of the column space of under different parameter configurations which are used in the CV. We add that the figure basically does not change for different values of (with the same range for ) and hence they are not reported here.

V-A4 Comparison with the ADMM

In order to examine the sparsification effect of the norm on via a comparison, we consider the convex relaxation model of (5), where the sparsity enforcing term is replaced by . The resulting problem can also be solved via the ADMM, called ADMM, once we replace the proximal operator in Algorithm 1 with the corresponding version whose scalar form reads as

| (64) |

and the matrix form is also an elementwise application of the scalar form above. The proximal operator is also called soft thresholding operator in the literature.

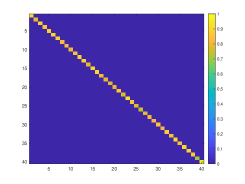

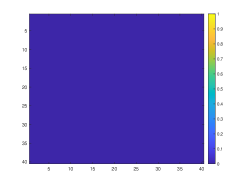

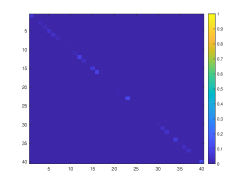

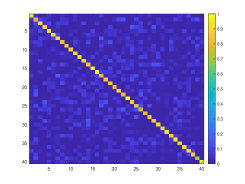

When the true is set as the identity matrix, panels (a) and (b) of Fig. 5 show graphically the estimates computed from the and the versions of the ADMM with fixed. We note that the ADMM correctly recognizes the underlying diagonal structure of , while the version returns a zero matrix which is similar to the outcome of the ADMM for . See the comment in Subsubsec. V-A2. Panels (c) and (d) of Fig. 5 show the results of the ADMM corresponding to and , respectively. When , the ADMM returns only a few nonzero entries along the diagonal of with small numerical values and fails to reveal the diagonal structure of . For the case of , the ADMM treats the optimization problem that essentially neglects the sparsity enforcing term , much similar to the case. Indeed, both the and the proximal operators reduce to the identity mapping when . The simulation results are also not far from each other: the estimate of has many spurious off-diagonal nonzeros (see panel (d) of Fig. 5) and the situation of the estimate can be seen from panel (ii) of Fig. 2. In summary, the ADMM with a suitable choice of appears to be able to identify the sparse structure of in a more reliable fashion.

(a)

(b)

.

(a)

(b)

(c)

(d)

V-B A real data example

In this subsection, Algorithm 1 is applied to an economic dataset222The dataset was sourced from http://www.stern.nyu.edu/~adamodar/pc/datasets/betas.xls (downloaded in May 2023)., which collects the data corresponding to nine financial indicators () across 92 different sectors () of the U.S. economy. These indicators include the Hi-Lo risk, the standard deviation of operating income, the debt/equity ratio, the beta, the unlevered beta, the unlevered beta adjusted for cash, the effective tax rate, the cash/firm value ratio, and the standard deviation of equity. For detailed definitions and calculation of these indicators, we refer the readers to the website written in the footnote.

On this real dataset, since the true factor loading matrix and the true noise covariance matrix are unknown, we are mostly interested in estimating the number of latent factors, i.e., the rank of . Similar to simulations on synthetic datasets, we set , and use the CV to select parameters , , and from the candidate sets , , and , respectively. The other parameters are identical to those in the synthetic data examples. As a result, Algorithm 1 returns a rank estimate . Moreover, it is important to point out that Algorithm 1 can robustly estimate the number of latent factors as under any parameter configuration selected from the candidate sets above for the CV333In this case, we do not carry out the CV procedure for the selection of parameters, but simply take parameters from the candidate sets and run Algorithm 1., and [15] also discussed the rationality of . In addition, Fig. 6 displays the changes in the value of with respect to the parameters and , with fixed. Under the same simulation setup, the Alternating Minimization method described in [57], which updates the sparse component using coordinate descent and the low-rank component using the CVX [58, 59], can stably return a rank estimate of only when is taken from the subset . Meanwhile, comparing Fig. 6 in the present paper with Fig. 4 of [57] which depicts as a function of under a fixed , we see that the refined estimate of the covariance matrix returned by Algorithm 1 appears to stay closer to the sample covariance matrix as measured by the KL divergence.

VI Conclusion

We have formulated an optimization model for Factor Analysis which can be described in terms of low rank plus sparse matrix decomposition. Although the objective function includes the norm of a nonconvex nonsmooth nature, we have established an optimality theory using a generalized notion of the KKT point called P-stationary point. Furthermore, we have developed an ADMM solver for the optimization problem and have provided convergence analysis of the algorithm. At last, results of numerical simulations have demonstrated not only the superiority of our algorithm in subspace recovery of the low-rank component, but also its ability to explore the unknown structure of the sparse component. In particular, the number of hidden factors can be estimated in a robust manner as shown in the real data example.

We first recall the definition of a strongly convex function which can be found e.g., in [51].

Definition 2 (Strongly convex function).

A differentiable function is strongly convex, if for any there exists a constant such that

| (65) |

Following Definition 2, suppose that is a minimizer of the strongly convex function with a constant . Then the inequality

| (66) |

holds because is not a descent direction for any feasible and hence .

Proof of Lemma 4. The Hessian of with respect to is

where denotes the Kronecker product. Given and properties of the Kronecker product [60], we have

which means that the function is -strongly convex with respect to . Therefore, for any , the minimizer of satisfies

| (67) | ||||

in view of (66).

Next we consider the subproblem (40b) which can be expressed as

| (68) |

where

Using the fact that is a smooth function and following Proposition 3, we can deduce that the gradient of is Lipschitz continuous with a Lipschitz constant . In addition by Lemma 1, is a lower semicontinuous function with an obvious lower bound zero. Since we have chosen , for any , it follows from [55, Lemma 2] that

| (69) | ||||

namely

| (70) | ||||

Notice also that is -strongly convex with respect to . Hence for any , we have

| (71) | ||||

and similarly,

| (72) | ||||

Combining the formulas (67), (70), (71), (72), and (73), for any , we obtain

| (74) | ||||

where . It remains to show that the terms in the last line of (74) are nonnegative for some suitable choice of and . To this end, we impose that

| (75) |

Due to the strict inequality, there must exist a sufficiently small such that the left hand side of (75) can be replaced by . These two strict inequalities imply that

holds for all . Thus we complete the proof.

References

- [1] C. Spearman, ““General Intelligence” objectively determined and measured.,” American Journal of Psychology, vol. 15, no. 2, pp. 201–293, 1904.

- [2] W. Ledermann, “On the rank of the reduced correlational matrix in multiple-factor analysis,” Psychometrika, vol. 2, no. 2, pp. 85–93, 1937.

- [3] A. Shapiro, “Rank-reducibility of a symmetric matrix and sampling theory of minimum trace factor analysis,” Psychometrika, vol. 47, pp. 187–199, 1982.

- [4] M. W. Watson and R. F. Engle, “Alternative algorithms for the estimation of dynamic factor, mimic and varying coefficient regression models,” Journal of Econometrics, vol. 23, no. 3, pp. 385–400, 1983.

- [5] G. Picci, “Parametrization of factor analysis models,” Journal of Econometrics, vol. 41, no. 1, pp. 17–38, 1989.

- [6] M. Forni and M. Lippi, “The generalized dynamic factor model: representation theory,” Econometric Theory, vol. 17, no. 6, pp. 1113–1141, 2001.

- [7] J. Bai and S. Ng, “Determining the number of factors in approximate factor models,” Econometrica, vol. 70, no. 1, pp. 191–221, 2002.

- [8] B. D. Erson and M. Deistler, “Identification of dynamic systems from noisy data: Single factor case,” Mathematics of Control, Signals and Systems, vol. 6, no. 1, pp. 10–29, 1993.

- [9] C. Heij and W. Scherrer, “System identification by dynamic factor models,” SIAM Journal on Control and Optimization, vol. 35, no. 6, pp. 1924–1951, 1997.

- [10] M. Deistler and C. Zinner, “Modelling high-dimensional time series by generalized linear dynamic factor models: An introductory survey,” Communications in Information and Systems, vol. 7, no. 2, pp. 153–166, 2007.

- [11] C. Lam and Q. Yao, “Factor modeling for high-dimensional time series: inference for the number of factors,” Annals of Statistics, vol. 40, no. 2, pp. 694–726, 2012.

- [12] G. Bottegal and G. Picci, “Modeling complex systems by generalized factor analysis,” IEEE Transactions on Automatic Control, vol. 60, no. 3, pp. 759–774, 2014.

- [13] D. Bertsimas, M. S. Copenhaver, and R. Mazumder, “Certifiably optimal low rank factor analysis,” Journal of Machine Learning Research, vol. 18, no. 1, pp. 907–959, 2017.

- [14] M. Zorzi and A. Chiuso, “Sparse plus low rank network identification: A nonparametric approach,” Automatica, vol. 76, pp. 355–366, 2017.

- [15] V. Ciccone, A. Ferrante, and M. Zorzi, “Factor models with real data: A robust estimation of the number of factors,” IEEE Transactions on Automatic Control, vol. 64, no. 6, pp. 2412–2425, 2018.

- [16] L. Falconi, A. Ferrante, and M. Zorzi, “A robust approach to ARMA factor modeling,” IEEE Transactions on Automatic Control, vol. 69, no. 2, pp. 828–841, 2024.

- [17] T. Hastie, R. Tibshirani, and M. Wainwright, Statistical Learning with Sparsity: The Lasso and Generalizations. CRC press, 2015.

- [18] E. J. Candès, X. Li, Y. Ma, and J. Wright, “Robust principal component analysis?,” Journal of the ACM, vol. 58, no. 3, pp. 1–37, 2011.

- [19] V. Chandrasekaran, S. Sanghavi, P. A. Parrilo, and A. S. Willsky, “Rank-sparsity incoherence for matrix decomposition,” SIAM Journal on Optimization, vol. 21, no. 2, pp. 572–596, 2011.

- [20] D. Hsu, S. M. Kakade, and T. Zhang, “Robust matrix decomposition with sparse corruptions,” IEEE Transactions on Information Theory, vol. 57, no. 11, pp. 7221–7234, 2011.

- [21] A. Agarwal, S. Negahban, and M. J. Wainwright, “Noisy matrix decomposition via convex relaxation: Optimal rates in high dimensions,” Annals of Statistics, pp. 1171–1197, 2012.

- [22] F. Wen, R. Ying, P. Liu, and R. C. Qiu, “Robust PCA using generalized nonconvex regularization,” IEEE Transactions on Circuits and Systems for Video Technology, vol. 30, no. 6, pp. 1497–1510, 2019.

- [23] Y. Chen, J. Fan, C. Ma, and Y. Yan, “Bridging convex and nonconvex optimization in robust PCA: Noise, outliers and missing data,” Annals of Statistics, vol. 49, no. 5, pp. 2948–2971, 2021.

- [24] A. Lindquist and G. Picci, Linear Stochastic Systems: A Geometric Approach to Modeling, Estimation and Identification, vol. 1 of Series in Contemporary Mathematics. Springer-Verlag Berlin Heidelberg, 2015.

- [25] T. M. Cover and J. A. Thomas, Elements of Information Theory. John Wiley & Sons, Inc., 2005.

- [26] T. T. Georgiou and A. Lindquist, “Kullback–Leibler approximation of spectral density functions,” IEEE Transactions on Information Theory, vol. 49, no. 11, pp. 2910–2917, 2003.

- [27] M. Pavon and A. Ferrante, “On the Georgiou–Lindquist approach to constrained Kullback–Leibler approximation of spectral densities,” IEEE Transactions on Automatic Control, vol. 51, no. 4, pp. 639–644, 2006.

- [28] A. Ferrante, M. Pavon, and F. Ramponi, “Hellinger versus Kullback–Leibler multivariable spectrum approximation,” IEEE Transactions on Automatic Control, vol. 53, no. 4, pp. 954–967, 2008.

- [29] A. Ferrante, F. Ramponi, and F. Ticozzi, “On the convergence of an efficient algorithm for Kullback–Leibler approximation of spectral densities,” IEEE Transactions on Automatic Control, vol. 56, no. 3, pp. 506–515, 2011.

- [30] J. Songsiri and L. Vandenberghe, “Topology selection in graphical models of autoregressive processes,” Journal of Machine Learning Research, vol. 11, pp. 2671–2705, 2010.

- [31] E. Avventi, A. G. Lindquist, and B. Wahlberg, “ARMA identification of graphical models,” IEEE Transactions on Automatic Control, vol. 58, no. 5, pp. 1167–1178, 2013.

- [32] M. Zorzi and R. Sepulchre, “AR identification of latent-variable graphical models,” IEEE Transactions on Automatic Control, vol. 61, no. 9, pp. 2327–2340, 2015.

- [33] V. Ciccone, A. Ferrante, and M. Zorzi, “Learning latent variable dynamic graphical models by confidence sets selection,” IEEE Transactions on Automatic Control, vol. 65, no. 12, pp. 5130–5143, 2020.

- [34] D. Alpago, M. Zorzi, and A. Ferrante, “A scalable strategy for the identification of latent-variable graphical models,” IEEE Transactions on Automatic Control, vol. 67, no. 7, pp. 3349–3362, 2022.

- [35] J. You, C. Yu, J. Sun, and J. Chen, “Generalized maximum entropy based identification of graphical ARMA models,” Automatica, vol. 141, 2022.

- [36] D. Alpago, M. Zorzi, and A. Ferrante, “Data-driven link prediction over graphical models,” IEEE Transactions on Automatic Control, vol. 68, no. 4, pp. 2215–2228, 2023.

- [37] J. You and C. Yu, “Sparse plus low-rank identification for dynamical latent-variable graphical AR models,” Automatica, vol. 159, 2024.

- [38] M. Nikolova, “Description of the minimizers of least squares regularized with -norm. uniqueness of the global minimizer,” SIAM Journal on Imaging Sciences, vol. 6, no. 2, pp. 904–937, 2013.

- [39] G. Marjanovic and A. O. Hero, “ sparse inverse covariance estimation,” IEEE Transactions on Signal Processing, vol. 63, no. 12, pp. 3218–3231, 2015.

- [40] L.-L. Pan, N.-H. Xiu, and S.-L. Zhou, “On solutions of sparsity constrained optimization,” Journal of the Operations Research Society of China, vol. 3, pp. 421–439, 2015.

- [41] H. Zhang, L. Pan, and N. Xiu, “Optimality conditions for locally Lipschitz optimization with -regularization,” Optimization Letters, vol. 15, no. 1, pp. 189–203, 2021.

- [42] S. Zhou, L. Pan, and N. Xiu, “Newton method for -regularized optimization,” Numerical Algorithms, pp. 1–30, 2021.

- [43] S. Zhou, N. Xiu, and H.-D. Qi, “Global and quadratic convergence of Newton hard-thresholding pursuit,” Journal of Machine Learning Research, vol. 22, no. 12, pp. 1–45, 2021.

- [44] S. Zhou, L. Pan, N. Xiu, and H.-D. Qi, “Quadratic convergence of smoothing Newton’s method for 0/1 loss optimization,” SIAM Journal on Optimization, vol. 31, no. 4, pp. 3184–3211, 2021.

- [45] H. Wang, Y. Shao, S. Zhou, C. Zhang, and N. Xiu, “Support vector machine classifier via soft-margin loss,” IEEE Transactions on Pattern Analysis and Machine Intelligence, vol. 44, no. 10, pp. 7253–7265, 2022.

- [46] Y. Shi and B. Zhu, “An ADMM solver for the MKL--SVM,” in Proc. of the 62nd IEEE Conference on Decision and Control (CDC 2023), pp. 3339–3346, IEEE, 2023.

- [47] D. Bertsimas, R. Cory-Wright, and N. A. G. Johnson, “Sparse plus low rank matrix decomposition: A discrete optimization approach,” Journal of Machine Learning Research, vol. 24, pp. 1–51, 2023.

- [48] M. Fazel, Matrix rank minimization with applications. PhD thesis, Department of Electrical Engineering, Stanford University, Stanford, CA, USA, 2002.

- [49] T. Blumensath and M. E. Davies, “Iterative thresholding for sparse approximations,” Journal of Fourier analysis and Applications, vol. 14, pp. 629–654, 2008.

- [50] T. Blumensath and M. E. Davies, “Iterative hard thresholding for compressed sensing,” Applied and computational harmonic analysis, vol. 27, no. 3, pp. 265–274, 2009.

- [51] S. P. Boyd and L. Vandenberghe, Convex Optimization. Cambridge University Press, 2004.

- [52] S. Boyd, N. Parikh, E. Chu, B. Peleato, and J. Eckstein, “Distributed optimization and statistical learning via the alternating direction method of multipliers,” Foundations and Trends in Machine Learning, vol. 3, no. 1, pp. 1–122, 2011.

- [53] J. V. de Miranda Cardoso, J. Ying, and D. Palomar, “Graphical models in heavy-tailed markets,” Advances in Neural Information Processing Systems, vol. 34, pp. 19989–20001, 2021.

- [54] H. Attouch, J. Bolte, and B. F. Svaiter, “Convergence of descent methods for semi-algebraic and tame problems: proximal algorithms, forward–backward splitting, and regularized Gauss–Seidel methods,” Mathematical Programming, vol. 137, no. 1-2, pp. 91–129, 2013.

- [55] J. Bolte, S. Sabach, and M. Teboulle, “Proximal alternating linearized minimization for nonconvex and nonsmooth problems,” Mathematical Programming, vol. 146, no. 1, pp. 459–494, 2014.

- [56] L. Yang, T. K. Pong, and X. Chen, “Alternating direction method of multipliers for a class of nonconvex and nonsmooth problems with applications to background/foreground extraction,” SIAM Journal on Imaging Sciences, vol. 10, no. 1, pp. 74–110, 2017.

- [57] L. Wang, W. Liu, and B. Zhu, “ factor analysis.” Submitted to IEEE Conference on Decision and Control (CDC 2024), 2024.

- [58] M. Grant and S. Boyd, “CVX: Matlab software for disciplined convex programming, version 2.1.” http://cvxr.com/cvx, Mar. 2014.

- [59] M. Grant and S. Boyd, “Graph implementations for nonsmooth convex programs,” in Recent Advances in Learning and Control (V. Blondel, S. Boyd, and H. Kimura, eds.), Lecture Notes in Control and Information Sciences, pp. 95–110, Springer-Verlag Limited, 2008. http://stanford.edu/~boyd/graph_dcp.html.

- [60] P. Lancaster and M. Tismenetsky, The Theory of Matrices: With Applications. Elsevier, 1985.

![[Uncaptioned image]](/html/2409.01888/assets/Linyang.jpg) |

Linyang Wang received the B.S. degree in Applied Mathematics from Qufu Normal University, China, in 2018, the M.S. degree in Operation Research and Control Theory from the Beijing University of Technology, in 2022. She is currently pursuing the Ph.D. degree from the School of Intelligent Systems Engineering, Sun Yat-sen University. Her current research interests include systems identification, signal processing, and sparse optimization. |

![[Uncaptioned image]](/html/2409.01888/assets/BinZhu.jpg) |

Bin Zhu received a B.Eng. degree from Xi’an Jiaotong University, Xi’an, China in 2012 and a M.Eng. degree from Shanghai Jiao Tong University, Shanghai, China in 2015, both in control science and engineering. In 2019, he obtained a Ph.D. degree in information engineering from University of Padova, Padova, Italy, and he had a one-year postdoc position in the same university. Since December 2019, he has been working at the School of Intelligent Systems Engineering, Sun Yat-sen University, Shenzhen, China, where he is now an associate professor. His current research interest includes spectral analysis, frequency estimation, and sparsity-promoting techniques for system identification, signal processing, and machine learning. Dr. Zhu has been appointed as an Associate Editor of the Editorial Board of the International Conference on System Theory, Control and Computing (ICSTCC) since December 2023. |

![[Uncaptioned image]](/html/2409.01888/assets/Wanquan_Liu.png) |

Wanquan Liu (Senior Member, IEEE) received the B.S. degree in applied mathematics from Qufu Normal University, China, in 1985, the M.S. degree in control theory and operation research from the Chinese Academy of Sciences in 1988, and the Ph.D. degree in electrical engineering from Shanghai Jiao Tong University in 1993. He is currently a Full Professor with the School of Intelligent Systems Engineering, Sun Yat-sen University, Shenzhen, China. He once held the ARC Fellowship, the U2000 Fellowship, and the JSPS Fellowship, and attracted research funds from different resources over 2.4 million dollars. His current research interests include large-scale pattern recognition, signal processing, machine learning, and control systems. |