secReferences in the Online Appendix \noptcrule \doparttoc\faketableofcontents

Prices and Concentration: A U-shape?

Theory and Evidence from Renewables††thanks: An older version of this paper circulated under the title “Saving for a Dry Day: Coal, Dams, and the Energy Transition.” We would like to thank Jaap Abbring, Ricardo Alonso, Johannes Boehm, Robin Burgess, El Hadi Caoui, Estelle Cantillon, Thomas Chaney, Zoe Cullen, Áureo de Paula, Francesco Decarolis, Natalia Fabra, Alessandro Gavazza, Daniel Gottlieb, Gautam Gowrisankaran, Joao Granja, Sergei Guriev, Joseph Hotz, Alessandro Iaria, Rocco Macchiavello, Alex Mackay, Thierry Mayer, Bob Miller, Nathan Miller, Francesco Nava, Marco Ottaviani, Fausto Panunzi, Martin Pesendorfer, Roger Moon, Lars Nesheim, Veronica Rappoport, Mar Reguant, Geert Ridder, Jean-Marc Robin, Alejandro Robinson-Cortez, Pasquale Schiraldi, Nicolas Schutz, Jesse Shapiro, Catherine Thomas, Otto Toivanen, Iivo Vehviläinen, and numerous seminar and conference participants for helpful comments and discussions. We are extremely indebted to Jaime Castillo and Luis Guillermo Vélez for introducing us to the Colombian electricity market and patiently addressing all our questions. Excellent research assistance was provided by Santiago Velásquez Bonilla, Cristian Chica, Mathias Dachert, Brayan Perez, and Nicolás Torres. Michele Fioretti thanks the Sciences Po Advisory Board for financial support. All errors and omissions are ours.

Abstract

We study firms’ strategic interactions when each firm may own multiple production technologies, each with its own marginal cost and capacity. Increasing industry concentration by reallocating non-efficient capacity to the largest and most efficient firm can decrease market prices as it incentivizes the firm to outcompete its rivals. However, with large reallocations, the standard monotonic relationship between concentration and prices re-emerges as competition weakens due to the rival’s lower capacity. Thus, we demonstrate a U-shaped relationship between market prices and industry concentration when firms are diversified. This result does not rely on economies of scale or scope. We find consistent evidence from the Colombian wholesale energy market, where strategic firms are diversified with fossil-fuel and renewable technologies, exploiting exogenous variation in renewable capacities. Our findings not only apply to the green transition but also to other industries and suggest new insights for antitrust policies.

JEL classifications: L25, D24, Q21

Keywords: diversified production technologies, energy transition, renewable energy, hydropower, storage, supply function equilibrium, oligopoly

1 Introduction

Economic models typically assume firms use a single technology or production function, resulting in a single marginal cost for any level of production (e.g., Olley and Pakes, 1996). However, firms can often produce the same good using multiple technologies, each with different capacities and marginal costs. These technologies can act as substitutes, replacing each other in production or as complements, providing a firm with the opportunity to influence market prices by simultaneously producing with different technologies. Nonetheless, there is a lack of understanding about how firms make production and pricing decisions with multiple technologies. This gap is crucial for energy firms, where environmental challenges require them to diversify their technology portfolio by including renewables (e.g., Elliott, 2024, Gonzales et al., 2023).111Other industries where firms have typically diversified technology portfolio are mining, telecommunication, and aluminium.

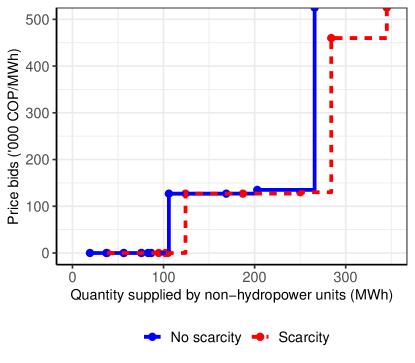

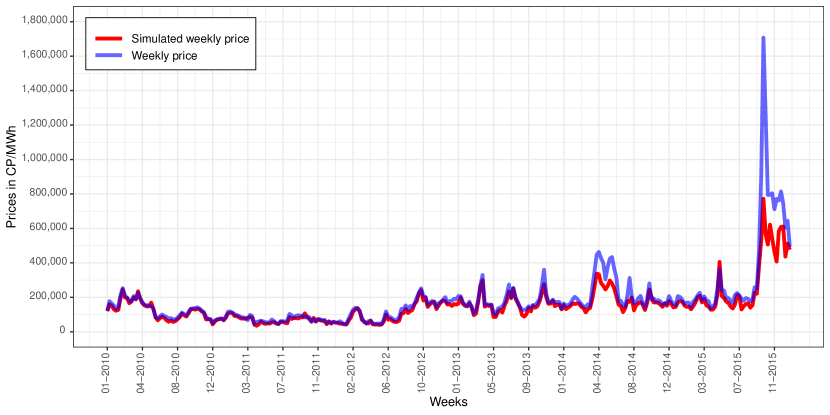

How do firms with multiple production techonologies compete? In this paper, we define a firm as diversified if it can produce the same good using technologies with different marginal costs and capacities. We introduce new theoretical and empirical evidence to study the strategic decisions of such firms. Our analysis is based on the Colombian wholesale energy market, where major suppliers own both renewable (dams) and conventional thermal generators (fossil fuels). Droughts provide exogenous variations in a firm’s renewable capacities without affecting those of conventional generators. Typically, a firm responds to a drought by reducing its hydropower supply, which increases the market price but lowers the firm’s market share. A diversified firm, however, can maintain its market share by increasing production with its conventional generators, as illustrated in Figure 1. This additional supply (gap between red and blue curves) lowers the market price and helps the firm conserve water, as production shifts from hydro to conventional sources. The steeper the firm’s demand curve, the greater its market power, but the more prices will drop as the firm increases its conventional supply. This demonstrates how considerations of market power become non-trivial with diversified firms. Similar incentives may arise in other industries due to mergers (e.g., Morck et al., 1990, Atalay et al., 2019) or trade disruptions altering firms’ boundaries (e.g., Acemoglu and Tahbaz-Salehi, 2024).

The figure plots the supply schedule of the non-hydropower generators owned by a Colombian diversified energy firm when it either faces scarcity (red dashed line) or not at its dams. Scarcity is defined as observing a water inflow in the first two deciles of its distribution. The red supply schedule was submitted by ENDG on December 12, 2010 at noon, whereas the blue schedule was submitted two weeks before. Total demand differ by less than 1% in the two markets.

Our main finding is a novel U-shaped relationship between market prices and industry concentration when firms are diversified and face uncertain demand. This U-shaped pattern arises because a firm with a highly efficient technology can disrupt its competitors by producing at their marginal cost, potentially driving them out of the market. When the market leader has limited efficient capacity, we show that reallocating a small amount of inefficient capacity from its competitors to the market leader incentivizes the leader to crowd them out further in low-demand scenarios while relying on the newly added inefficient capacity in high-demand situations. This increase in market concentration can lower market prices as competitors expand their supply to maintain market shares. Conversely, complete crowding out may not always be the optimal strategy, as a firm might prefer raising prices when competition decreases. We demonstrate that large capacity reallocations increase prices as competition weakens due to rivals’ low capacity, resulting in a U-shaped relationship between prices and industry concentration. Quantitatively, our structural model finds that prices drop by up to 10% for small capacity reallocations to the market leader but increase substantially for larger transfers.

Thus, the impact of concentration on prices hinges on two factors: the efficiency of each technology a firm possesses and its overall capacity, which generate Bertrand and Cournot forces, respectively. Market prices generally decrease with small capacity reallocations as firms employ their most efficient technology more but increase with larger reallocations, forming a U-shaped pattern. In contrast, prices will always rise with concentration if the market leader has abundant low-cost capacity, because, in essence, the leader is not diversified, eliminating any crowding-out incentives. The latter result echoes standard trade and industrial organization models (e.g., Atkeson and Burstein, 2008, Nocke and Whinston, 2022), where markups increase with a firm’s market share, justifying the usage of Herfindahl Indices (HHI) as a measure of industry market power. A consequence of our results is that such measures lose meaning when firms are diversified.

More broadly, in oligopolistic industries where the efficient technology is scarce, a larger diversified market leader might result in smaller market prices than if its inefficient technology were allocated to a smaller rival. Our results also extend to studying the price effect of mergers rather than capacity transfers while relaxing the common assumption that the new firm’s marginal cost equals the minimum of the merging parties. Our insights find applications across diverse sectors. For example, in the industrial sectors, firms commonly produce aluminum with various technologies (Collard-Wexler and De Loecker, 2015). In oil and gas, a firm owns reservoirs with different costs and capacities (Asker et al., 2019, Fioretti et al., 2022). In healthcare, hospitals can complement doctors’ advice with cheaper artificial intelligence algorithms (Agarwal et al., 2023).

We theoretically examine the behavior of diversified firms through a static homogeneous-good oligopoly game where firms confront demand uncertainty and own both low- and high-cost technologies, representing hydropower and thermal generation, respectively.222We focus on a stylized static setting that relies only on strategic interactions between firms owning multiple technologies with different marginal costs and capacities to highlight the generality of our findings. When taking the model to the data, we allow for dynamic considerations as Colombian energy generators respond to expected hydropower capacity changes. Each technology features its own cost curve, which becomes vertical at capacity. A firm’s total cost is the horizontal sum of its technologies’ cost curves, and, hence, it is increasing in the quantity produced. The equilibrium price is determined by firms submitting supply schedules detailing the quantity they are willing to produce at various market prices, following the supply function equilibrium concept proposed by Klemperer and Meyer (1989). This concept, unlike traditional models such as Cournot and Bertrand, is ex-post optimal and encompasses them as extreme cases by permitting any non-negative slope at different market prices.333This theoretical framework (see also Wilson, 1979, Grossman, 1981) has found several applications not only in energy markets (Green and Newbery, 1992), but also in financial markets (Hortaçsu et al., 2018), government procurement contracts (Delgado and Moreno, 2004), management consulting, airline pricing reservations (Vives, 2011), firm taxation (Ruddell et al., 2017), transportation networks (Holmberg and Philpott, 2015), and also relates to nonlinear pricing (e.g., Bornstein and Peter, 2022).

Initially, in this market, no firm is diversified and the largest firm also has the most efficient technology. We then study what happens when we diversify it by reallocating high-cost capacity to this market-leading firm in different scenarios. If the leader’s low-cost capacity was substantially larger than that of its rivals before the transfer, as under the abundance of hydropower, we find that the transfer reduces its rivals’ ability to compete, leading to higher prices. Therefore, when the leader’s market power comes from its total size, reallocating capacity to the leader effectively “removes resources from the market,” as the leader prioritizes its low-cost technology in production over the high-cost one to minimize costs, following the so-called merit order.

Conversely, the same reallocation of high-cost capacity “brings capacity back into the market” when the leader’s relative capacity advantage is not as large even though being the largest firm. Because of the merit order, the new capacity will be produced only after the exhaustion of its low-cost one, hence only in high-demand situations. However, the firm cannot expand its supply only from a high price onward because this strategy encourages undercutting by its rivals. Hence, both the market leader and its competitors expand their supply schedules, resulting in lower prices than before the reallocation despite more capacity concentration. Importantly, standard synergies like economies of scale play no role in this economy because average costs stay unchanged at the realized market price. Therefore, our results illustrate two sources of market power when firms are diversified: total capacity, driving prices up, and relative efficiency, driving them down.

Alternatively, if a significantly large portion of the high-cost capacity is transferred to the market leader – imagine the extreme scenario where it becomes a monopolist – we demonstrate that market prices invariably increase. This is because the firm can now reduce its production to raise prices without losing inframarginal units, explaining the U-shaped relationship between prices and concentration.

Our empirical investigation centers on the Colombian energy market for several reasons. Firstly, all major players in this market operate diversified production, utilizing a mix of hydropower and thermal energy. Secondly, regulatory requirements ensure the availability of data on firms’ desired production for each technology they employ, a rarity in many other industries. Thirdly, natural fluctuations in weather patterns provide an exogenous factor affecting hydropower capacity, allowing us to study market power and concentration without relying on potentially endogenous events like mergers.

To quantify the impact of diversification on market prices, we extend the theoretical model to account for the main features of the Colombian energy market. In particular, thermal capacity is consistently available, while dry and abundant spells directly influence a firm’s hydropower capacity by altering the opportunity cost of its supply. Empirically, we exploit variation in this opportunity cost as a shifter to a firm’s hydropower capacity, as it does not affect its operating cost and the costs and capacities of other technologies.

To causally identify this U-shape in the data, we simulate market prices in different scenarios where we exogenously endow the market-leading firm with increasing fractions of its competitors’ thermal capacity. The model primitives – the marginal cost of thermal and hydropower generators and the intertemporal opportunity cost of holding water – are identified from the first-order conditions.444We build on the multi-unit (e.g., Wolak, 2007, Reguant, 2014) and dynamic auctions literature (e.g., Jofre-Bonet and Pesendorfer, 2003), and examine externalities across generators (e.g., Fioretti, 2022). We estimate the model on hourly markets between 2010 and 2015 and show that the model fits the data well.

Our findings reveal that during droughts, average market prices decline by up to 10% if we double the size of the market leader’s thermal capacity. However, for larger reallocations, prices increase substantially, aligning with the conclusions from models featuring non-diversified firms. During abundant periods, reallocations diminish rivals’ competitiveness, resulting in higher market prices. Notably, the disparity in prices between dry and abundant spells can be significant, with prices during droughts reaching up to ten times higher. This underscores the welfare benefit of diversification, particularly evident in situations where the low-cost technology is scarce.

Earlier investigations have warned against joining renewable and thermal generators because when firms compete à la Cournot, they benefit by reducing their thermal supplies when they also have renewables, as renewables induce a more inelastic demand (Bushnell, 2003, Acemoglu et al., 2017). In contrast, concurrent work by Fabra and Llobet (2023) shows that diversifying suppliers competing à la Bertrand can lead to lower prices if a firm has private information about its realized renewable capacity, as is common for solar and wind farms.555In their setting, higher renewable capacity leads thermal generators of a diversified firm to bid more aggressively for extra market shares because its renewable capacity makes the firm’s supply inframarginal. However, in our case, we observe different behavior: firms increase rather than decrease thermal generation when facing scarcity.666Also Garcia et al. (2001) and Crawford et al. (2007) studied competition across energy firms with multiple generators but do not examine the downward price pressure created by capacity reallocations.

We provide a unifying account featuring results from both types of conduct that allows us to discuss when diversifying production increases or decreases market prices. Instead of asymmetric information, as Colombian suppliers are aware of each others’ water stocks, we explain the thermal generators’ strategies through their market power, which pushes them to steal market shares when they internalize higher prices due to scarcity. As the storability of solar and wind resources continues to improve (Schmalensee, 2019, Koohi-Fayegh and Rosen, 2020, Andrés-Cerezo and Fabra, 2023), we expect our results to apply also to other renewables, in which case firms could substitute across renewables technologies, without the need for polluting thermal generators, thereby speeding the transition by solving renewables’ intermittency problems (Gowrisankaran et al., 2016, Vehviläinen, 2021) and making it more affordable (Butters et al., 2021).

How might our findings guide policy decisions? Antitrust regulation emerges as an innovative tool for driving down the costs of the green transition, complementing standard approaches like subsidies (Acemoglu et al., 2012, Abrell et al., 2019, Ambec and Crampes, 2019). While existing literature examines subsidy regulations for renewable capacities and grid integration to foster competition and maintain low energy prices (e.g., De Frutos and Fabra, 2011, Ryan, 2021, Elliott, 2024, Gowrisankaran et al., 2022, Gonzales et al., 2023), it often overlooks how ownership of new and old technologies affects pricing. Our findings open new questions regarding firms’ efficient ownership structures. For example, Colombia limits firms to holding no more than 25% of the total installed capacity to prevent market power abuses. However, this threshold also hampers the advantages of diversified production. Although determining the ideal threshold exceeds the scope of this paper, we contend that it should vary according to a firm’s technological capabilities.

Despite an extensive literature questioning the treatment of capital as a homogeneous input (e.g., Robinson, 1953, Solow, 1955, Sraffa, 1960), previous studies have primarily focused on competition among multiproduct firms (e.g., Nocke and Schutz, 2018b) or capacity constraints in firms operating with a single production technology (Kreps and Scheinkman, 1983, Bresnahan and Suslow, 1989, Staiger and Wolak, 1992, Froeb et al., 2003).777In such models, concentration typically leads to higher markups (De Loecker et al., 2020, Benkard et al., 2021, Grieco et al., 2023), with adverse effects on productivity (Gutiérrez and Philippon, 2017, Berger et al., 2022) and the labor share (Autor et al., 2020). The endogeneous growth literature offers a notable exception (e.g., Aghion et al., 2024), where firms may exhibit multiple production technologies through green and brown patents, albeit without explicit consideration of capacity constraints. This paper explores how diversification generates strategic complementarities within firms and across competitors. Our findings highlight two key implications. First, conventional production function estimation methods may fail to capture productivity gains from factor-augmenting technologies (e.g., Demirer, 2022) without specific technology-level data. Second, our results inform antitrust policies regarding divestitures required of merging entities (Compte et al., 2002, Friberg and Romahn, 2015), suggesting that divestitures could inadvertently raise prices by reducing technology diversification.888Relatedly, Nocke and Whinston (2022) propose that antitrust authorities adjust HHI thresholds based on merger-induced synergies. These synergies, such as economy of scale or scope, differ from the synergies we focus in our paper (e.g., Paul, 2001, Verde, 2008, Jeziorski, 2014, Miller et al., 2021, Demirer and Karaduman, 2022, Elliott et al., 2023). The literature also highlights buyer concentration as a factor decreasing consumer prices (Morlacco, 2019, Alviarez et al., 2023).

The paper is structured as follows: Sections 2 and 3 introduce the Colombian wholesale market, describe the data, and present empirical patterns of supply decisions during scarcity and abundance periods. Section 4 explains these patterns through a simple theoretical framework, which forms the basis of our empirical analysis developed in Sections 5 and 6. Finally, Section 7 concludes by discussing our contributions to antitrust policies and the green transition.

2 The Colombian Wholesale Energy Market

This section provides an overview of the Colombian energy market, focusing on the available technologies and its institutions.

2.1 Generation

Colombia boasts a daily energy production of approximately 170 GWh.999For regional context, neighboring countries’ energy production in 2022 included 227 GWh in Venezuela, 1,863 GWh in Brazil, 165 GWh in Peru, 91 GWh in Ecuador, and 33 GWh in Panama. Globally, figures were 11,870 GWh in the US, 1,287 GWh in France, and 2,646 GWh in Japan. Between 2011 and 2015, the market featured around 190 generators owned by 50 firms. However, it exhibits significant concentration, with six major firms possessing over 50% of all generators and approximately 75% of total generation capacities. The majority of firms operate a single generator with limited production capacity.

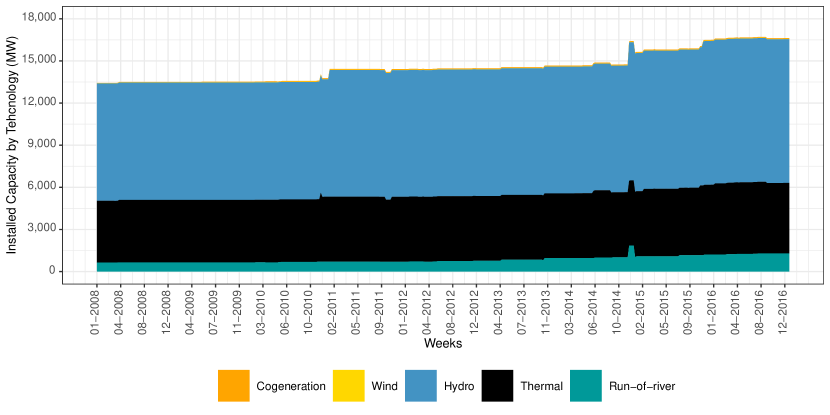

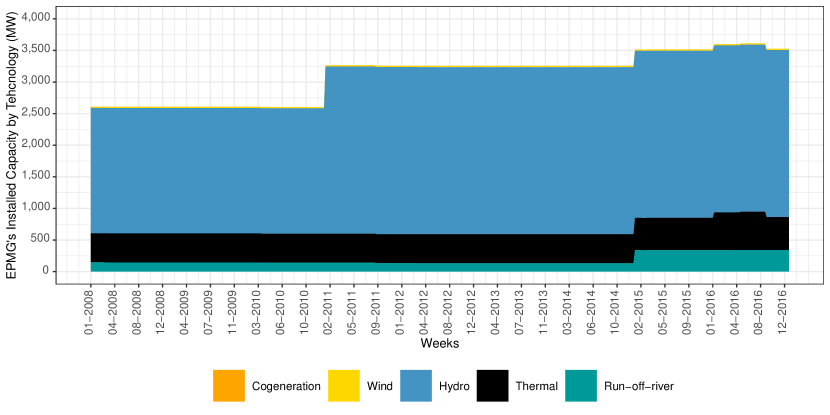

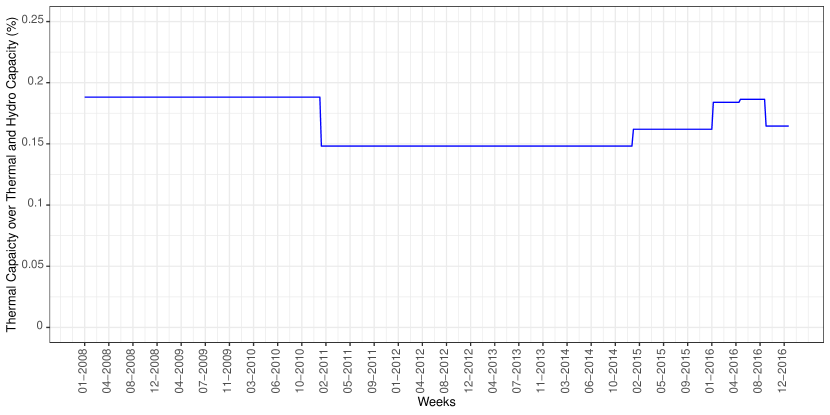

These major players diversify their portfolios, engaging in dam and other generation types, including thermal sources such as fossil fuel-based generators (coal and gas). Additional sources comprise renewables like wind farms and run-of-river, which utilizes turbines on rivers without water storage capabilities. Figure 2a illustrates the hourly production capacities (MW) for each technology from 2008 to 2016, revealing that hydropower (blue) and thermal capacity (black) constitute 60% and 30% of the industry’s capacity, respectively. Run-of-river (green) accounts for less than 6%. Solar, wind, and cogeneration technologies producing energy from other industrial processes are marginal.

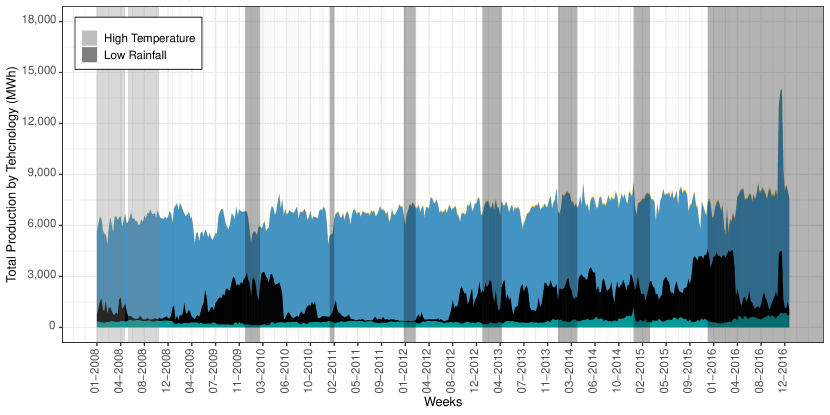

Despite the presence of various sources, hydropower dominates production, averaging around 75% of total dispatched units. The remaining energy needs are met by thermal generation (approximately 20% of total production) and run-of-river (5%). However, production varies over time, as shown in Panel (b) of the same figure, which contrasts production across technologies with dry seasons represented by periods of high temperature or low rainfall at dams (gray bars). During dry spells, hydropower production decreases, and thermal generation compensates for water scarcity.101010Data reveals a correlation between thermal production and minimum rainfall at Colombian dams of -0.32 (p-value 0.01) and 0.27 (p-value 0.01) for hydropower generation. Firms strategically stockpile fossil fuels like coal and gas ahead of anticipated dry spells (Joskow, 2011), with their prices closely tied to global commodity markets. In contrast, run-of-river energy lacks storage capabilities, limiting its ability to offset hydropower shortages.

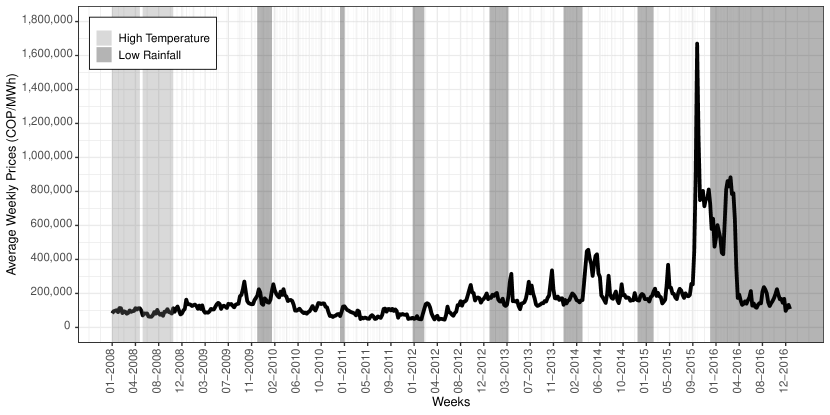

Thermal generation typically incurs higher marginal costs than hydropower. Figure 3 highlights that wholesale energy prices more than double during scarcity periods.111111The correlation of the average hourly price and rainfall is -0.28 (p-value 0.01). Prices are in Colombian pesos (COP) per MWh and should be divided by 2,900 to get their euro per MWh equivalent. Prices experienced a further increase during the sustained dry spell caused by El Niño in 2016 and the annual dry seasons (December to March).

Note: The figure illustrates the total installed capacity (top panel) and production volumes (bottom) by technology. The vertical bars in Panel (b) refer to periods where a hydropower generator experiences a temperature (rainfall) that is at least one standard deviation above (below) its long-run average.

Note: Average market prices across weeks. The vertical gray columns refer to periods where a hydropower generator experiences a temperature (rainfall) that is at least one standard deviation above (below) its long-run average. 2,900 COP 1 US$.

2.2 Institutional Background

The Colombian wholesale energy market is an oligopolistic market with high barriers to entry, as suggested by the fact that the total hourly capacity in Panel (a) of Figure 2 is almost constant over time, and especially so in the period 2010-2015, on which we focus in the following analysis. In this period, only nine generators entered the market (out of 190), all belonging to different fringe firms, leading to a mild increase in market capacity (+4%). The market is highly regulated and consists of a spot and a forward market.

The spot market. The spot market, also known as day-ahead market, sets the output of each generator. It takes the form of a multi-unit uniform-price auction in which Colombian energy producers compete by submitting bids to produce energy the following day. Through this bidding process, each generator submits one quantity bid per hour and one price bid per day.121212Participation in the spot market is mandatory for large generators with capacity over 20MW. Quantity bids state the maximum amount (MWh) a generator is willing to produce in a given hour, while price bids indicate the lowest price (COP/MW) acceptable for production. Each generator bids its own supply schedule, potentially considering the payoffs to the other generators owned by the same firm, which we call siblings of the focal generator.

Spot market-clearing. Before bidding, the market operator (XM) provides all generators with estimated market demand for each hour of the following day. After bidding, XM ranks bid schedules from least to most expensive to identify the lowest price satisfying demand for each hour. XM communicates the auction outcomes or despacho economico to all generators. During the production day, actual generation may differ due to production constraints or transmission failures. The spot hourly price is set at the value of the price bid of the marginal generator, with all dispatched units paid the same price.131313The price paid to thermal generators can vary due to startup costs, which are reimbursed (Balat et al., 2022). Despite high barriers to entry, a central factor sustaining firms’ coordination efforts (Levenstein and Suslow, 2006), there is no evidence of a cartel in the period we study (Bernasconi et al., 2023).

Forward market. The forward market comprises bilateral contracts between pairs of agents. These contracts allow agents to decide the financial position of each generator weeks in advance, serving to hedge against uncertainty in spot market prices. In our dataset, we observe each generator’s overall contract position for each hourly market.

2.3 Data

The data come from XM for the period 2006–2017. We observe all quantity and price bids and forward contract positions. The data also includes the ownership, geolocalization, and capacity for each generator, and daily water inflows and stocks for dams. We complement this dataset with weather information drawn from the Colombian Institute of Hydrology, Meteorology, and Environmental Studies (IDEAM). This information contains daily measures of rainfall and temperature from 303 measurement stations.141414For each generator, we compute a weighted average of the temperatures and rainfalls by all measurement stations within 120 km, weighting each value by the inverse distance between generators and stations. We account for the orography of the country when computing the distance between generators and weather measurement stations, using information from the Agustin Codazzi Geographic Institute.

Rainfall forecasts are constructed using monthly summaries of el Niño, la Niña, and the Southern Oscillation (ENSO), based on the NINO3.4 index from the International Research Institute (IRI) of Columbia University.151515ENSO is one of the most studied climate phenomena. It can lead to large-scale changes in pressures, temperatures, precipitation, and wind, not only at the tropics. El Niño occurs when the central and eastern equatorial Pacific sea surface temperatures are substantially warmer than usual; la Niña occurs when they are cooler. These events typically persist for 9-12 months, though occasionally lasting a few years, as indicated by the large gray bar toward the end of the sample in Panel (b) of Figure 2. ENSO forecasts, published on the 19th of each month, provide probability forecasts for the following nine months, aiding dams in predicting inflows. We have monthly information from 2004 to 2017.

This dataset is complemented with daily prices of oil, gas, coal, liquid fuels, and ethanol – commodities integral to energy production through thermal or cogeneration (e.g., sugar manufacturing) generators.

3 Diversified Production: Empirical Evidence

This section leverages exogenous variations in water inflow forecasts, impacting the capacities of dams, to offer novel perspectives on the production decisions made by diversified firms. Sections 3.1 and 3.2 delineate the empirical methodology and present the primary findings. Finally, Section 3.3 examines the ramifications for market clearing prices.

3.1 Empirical Strategy

This section outlines the empirical strategy used to assess the responses of a firm’s hydro and thermal supplies to variations in its hydropower capacity, utilizing data from periods of drought and abundance within firms.

We construct inflow forecasts for each hydropower generator employing a flexible autoregressive distributed-lag (ARDL) model (Pesaran and Shin, 1995). In essence, these forecasts are derived through OLS regressions of a generator’s weekly average net water inflow, encompassing evaporation, on the water inflows in past weeks and past temperatures, rainfalls, and el Niño probability forecasts. A two-year moving window is used to generate monthly forecasts up to 5 months ahead for the period between 2010 and 2015, where we observe little entry of new plans and no new dams. The forecasting technique is discussed in detail in Appendix B, which also presents goodness of fit statistics.

We investigate generators’ reactions to forthcoming inflows by analyzing the equation:

| (1) | ||||

This equation explores how generator of firm updates its current supply schedule based on anticipations of favorable () or adverse () forecasts months ahead relative to its average forecast. To minimize autocorrelation, we aggregate bids over weeks () per hour (). Instances where a generator’s quantity bid falls below the 5th percentile of the distribution of quantity bids placed by generators of the same technology are excluded to mitigate contamination from unobserved maintenance periods within a week. Importantly, this truncation does not qualitatively impact the results.

The definition of the variables and varies across analysis. Specifically, when focusing on the supply of hydropower, these variables take the value one if dam of firm anticipates its -month ahead forecast to deviate by either a standard deviation higher or lower than its long-run average (for the period 2008-2016), and zero otherwise, respectively. Conversely, when transitioning the analysis to sibling thermal generators – those owned by a firm with dams – these indicators are based on the cumulative -month ahead inflow forecasts associated with the dams owned by .

We control for changes in market conditions in utilizing average market demand, water stocks, and forward contract positions (in log) for week and hour . To account for seasonal variations that may impact generators differently, fixed effects are included at the generator-by-month and firm-by-year levels (). Macro unobservables, such as variations in demand, are captured through fixed effects at the week-by-year () and hour levels (). The standard errors are clustered by generator, month, and year.161616Spatial clustering the standard errors is an alternative approach. However, hydrology literature suggests that a riverbed acts as a ”fixed point” for all neighboring water flows, making shocks at neighboring dams independent (Lloyd, 1963). Moreover, spatial distance has no meaning for thermal generators. Hence, we do not pursue spatial clustering in this analysis.

Exclusion restriction. Identification in (1) relies on the credible assumption that a firm’s current bidding does not directly depend on past temperatures and rains at the dams but only indirectly through water inflows. This restriction is credible because a generator should only care for its water availability rather than the weather per se – due to their rural locations, the local weather at the dam is unlikely to influence other variables of interest to a generator, like energy demand in Colombia, which is controlled for in the estimation. Appendix C is dedicated to robustness checks and also proposes an alternative estimation strategy where generators respond symmetrically to favorable and adverse forecasts. The Appendix also discusses the information content of our inflow forecasts by showing that generators’ responses to forecast errors – the observed inflow minus the forecasted inflow – are insignificant.

3.2 Results

3.2.1 Hydropower Generators

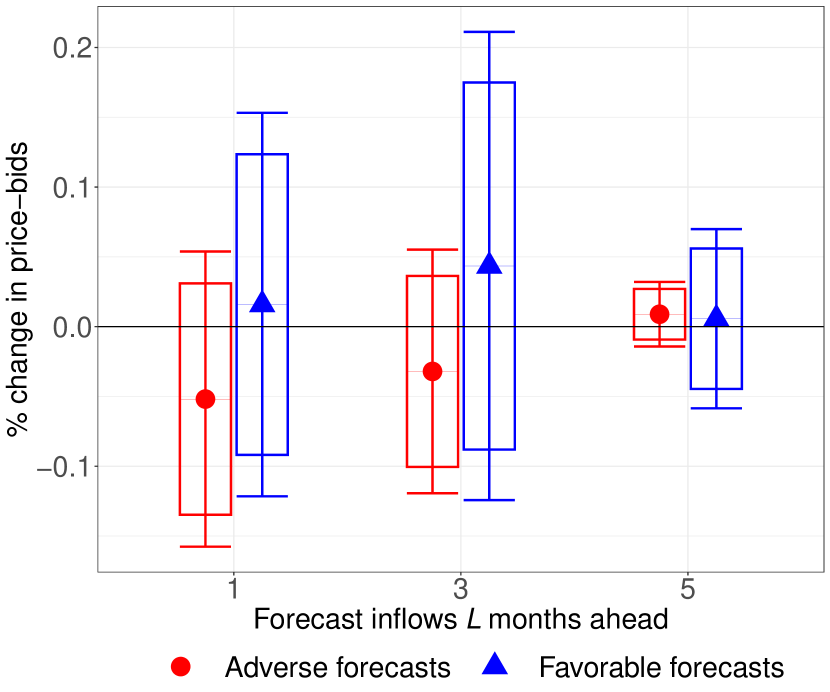

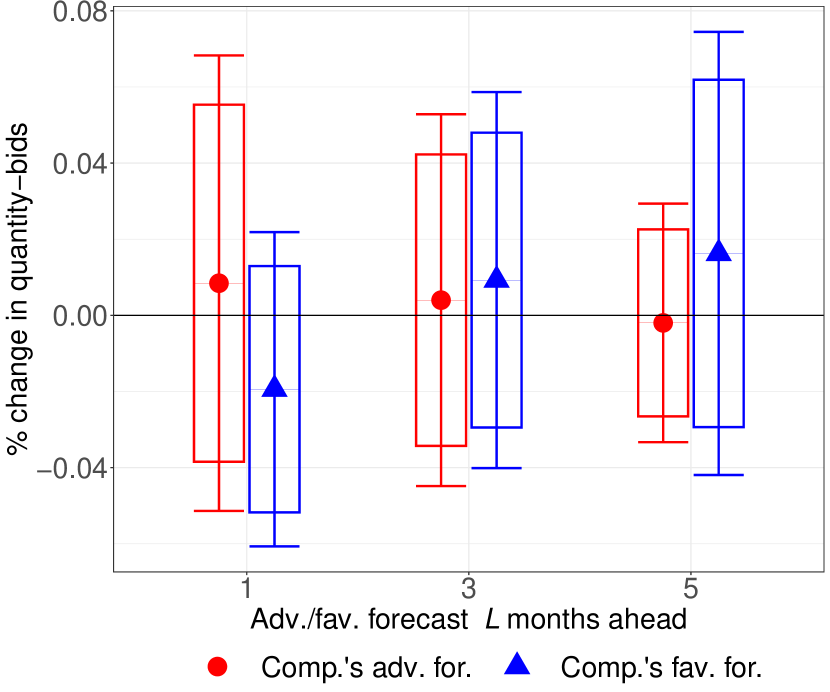

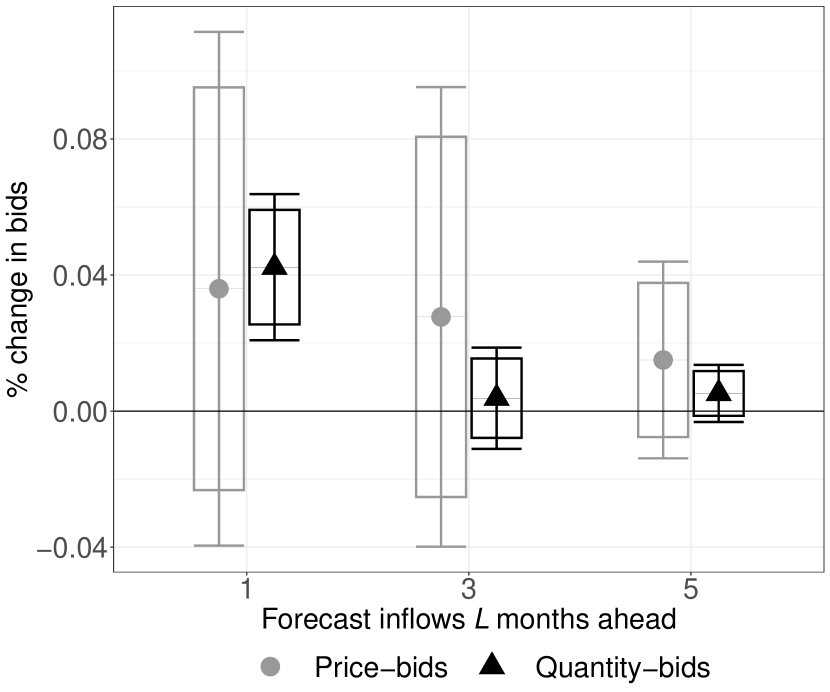

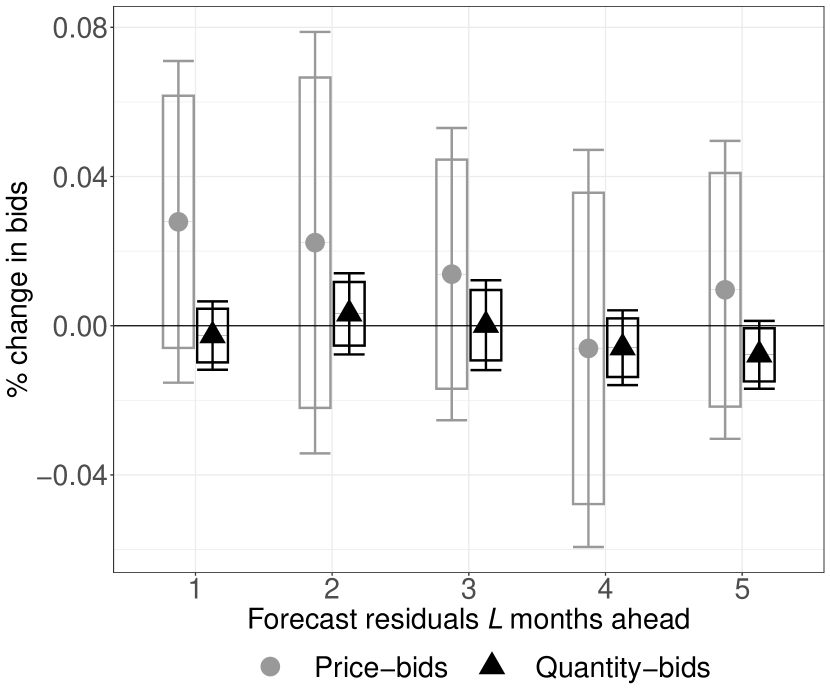

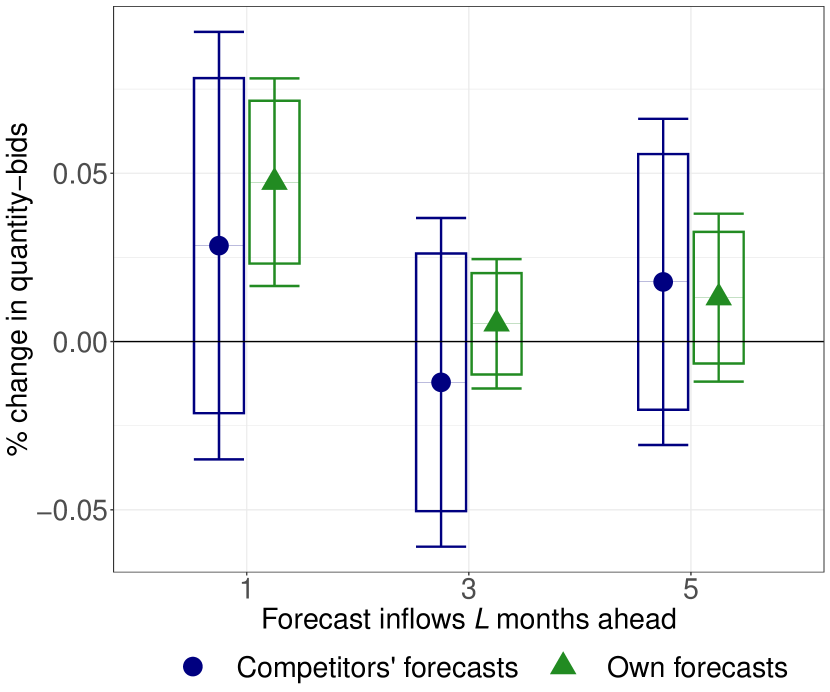

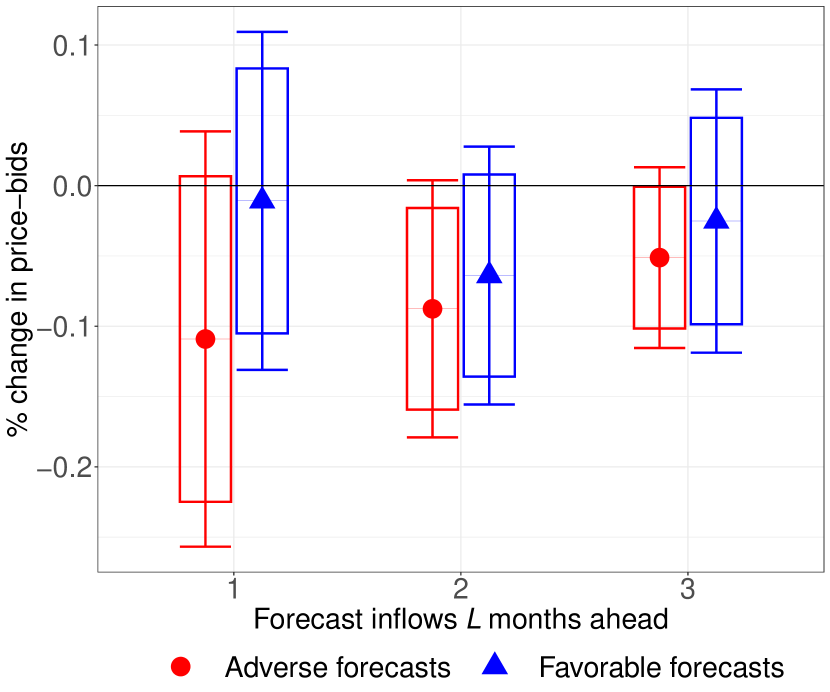

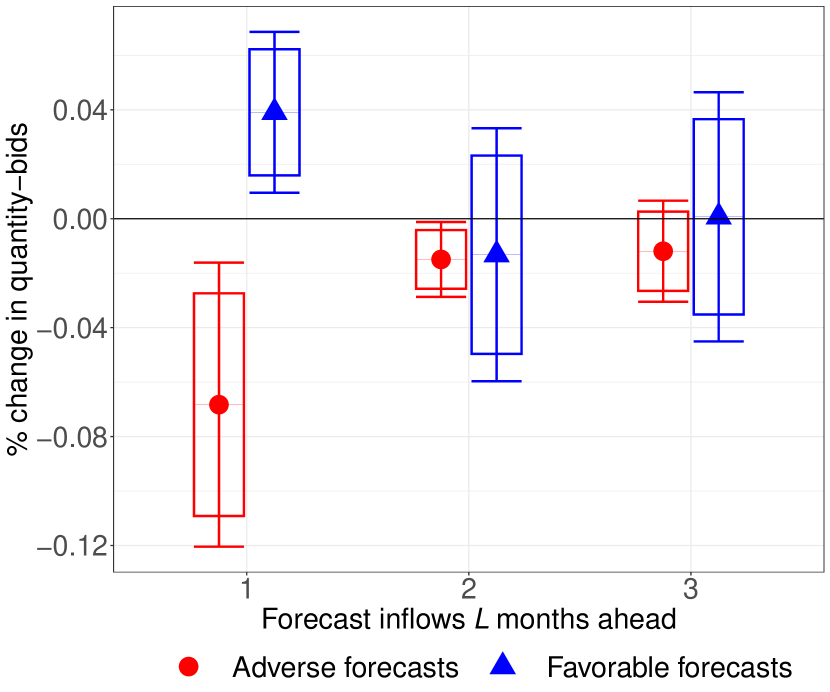

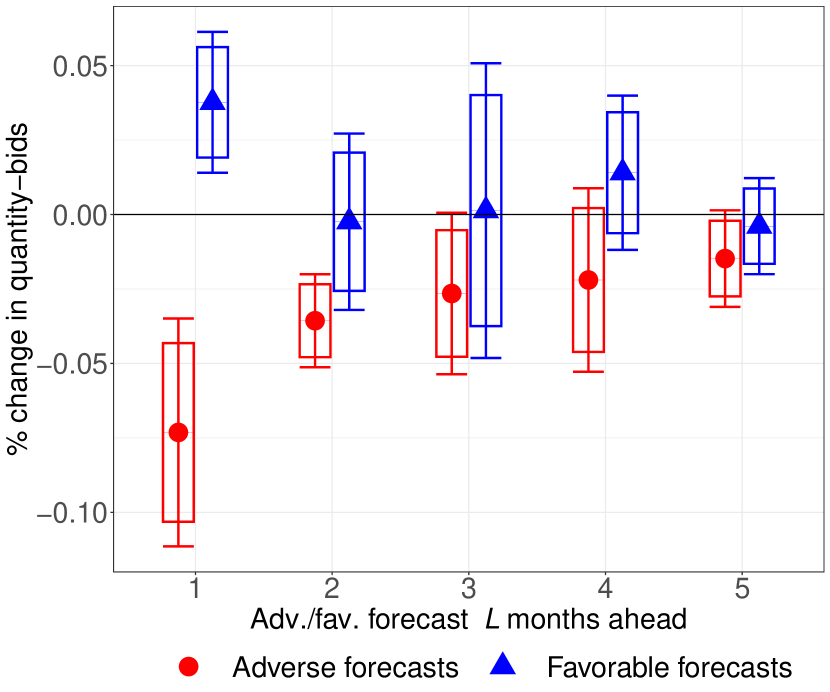

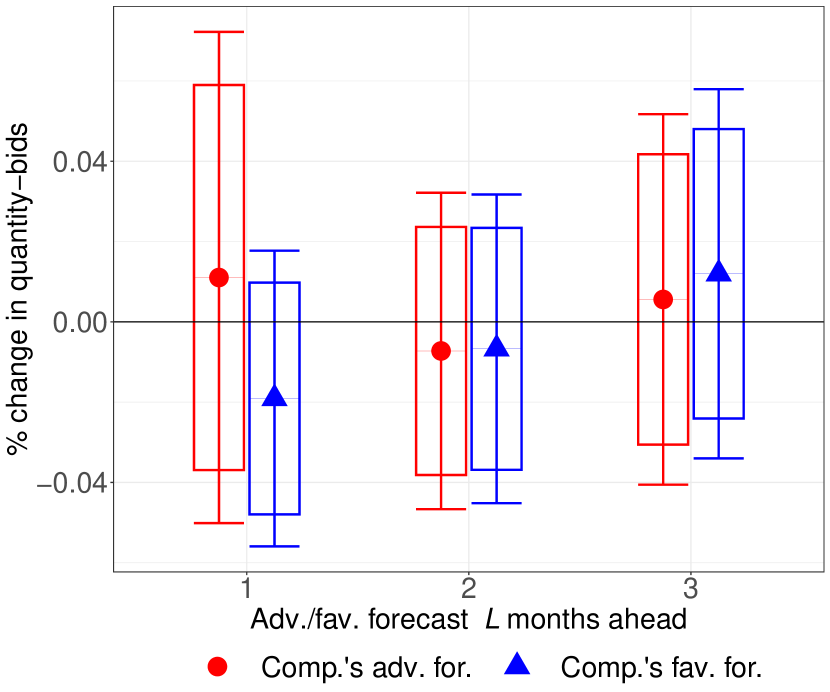

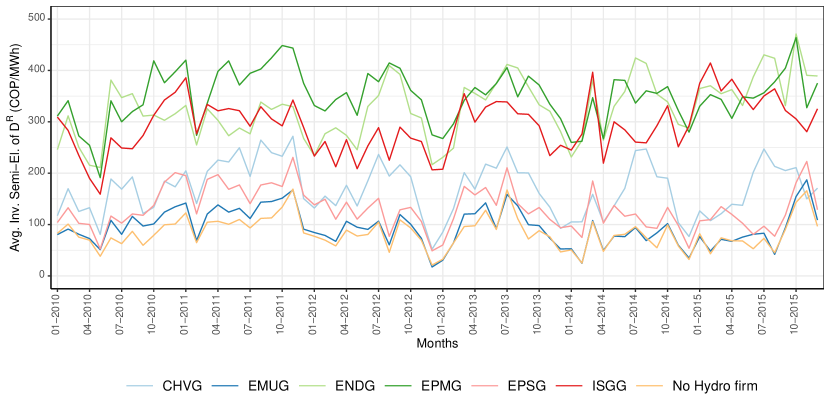

Figure 4 displays the coefficients, ,, from (1). The dependent variable is the logarithm of hydropower generator ’s price bid in Panel (a) and quantity bid in Panel (b). Coefficient magnitudes represent percentage changes when facing an adverse forecast (red circles) or a favorable forecast (blue triangles) one, three, or five months ahead.171717The chosen timing accounts for the limited correlation across monthly inflow forecasts, with a correlation of 0.2 between forecasts two months apart and 0 for forecasts further apart.

Dams strategically adjust their supply schedules in anticipation of extreme events. They adapt their supplies mainly by changing their quantity bids rather than their price bids because, having low marginal costs, they always produce and the market asks for hourly quantity bids but only daily price bids. We find that dams decrease their supply schedules ahead of adverse events, recognizing the negative impact of capacity constraints (e.g., Balat et al., 2015), and increase them ahead of favorable forecasts. Notably, generators are more responsive to adverse events: generation decreases by 7.1% for one-month adverse forecasts and 1.3% for two-month adverse forecasts, whereas it only increases by approximately 3.7% one month ahead of a favorable forecast.181818The results are consistent to to different forecast horizons (Appendix Figure C4) and to running (1) separately for each monthly forecast so to break any possible correlation across months (Figure C5).

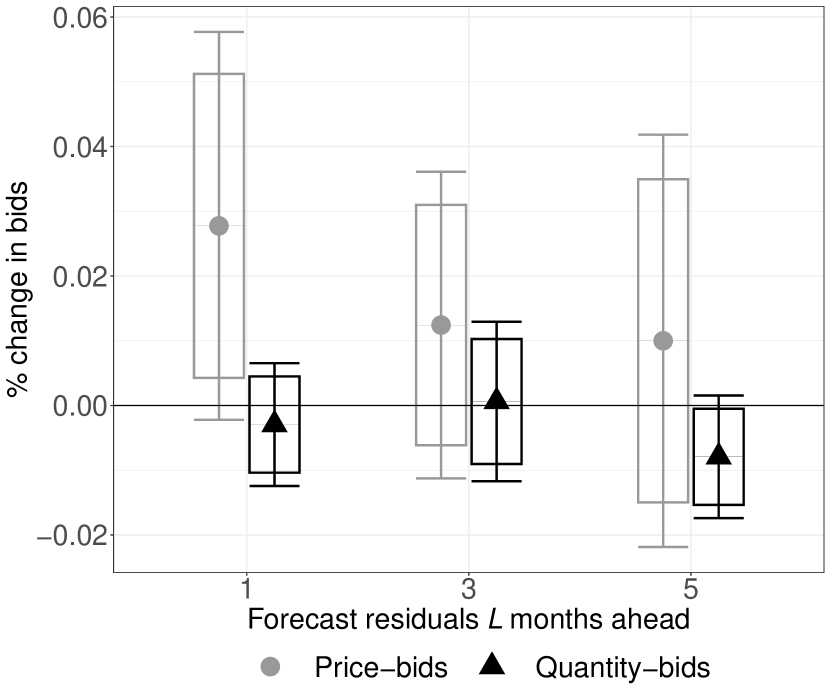

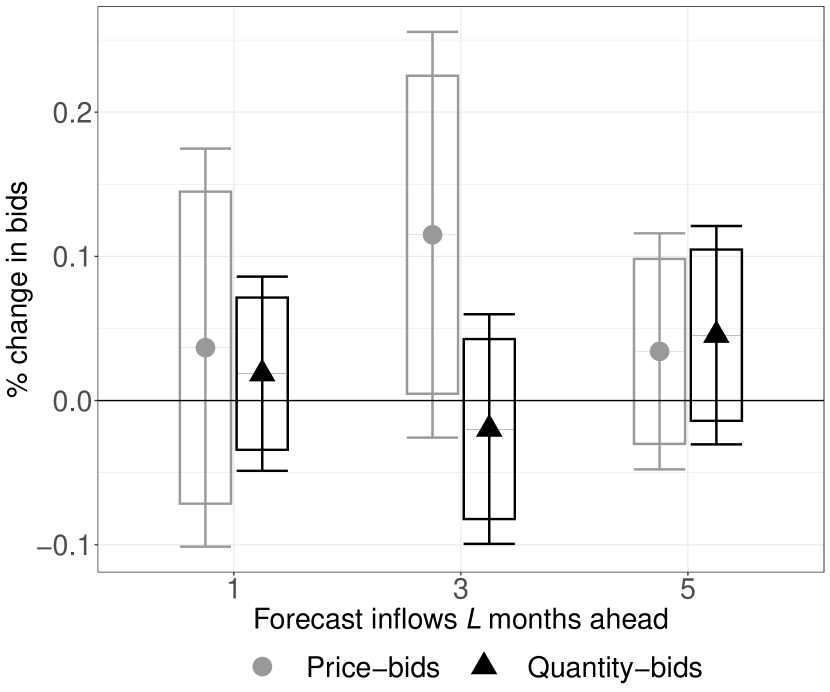

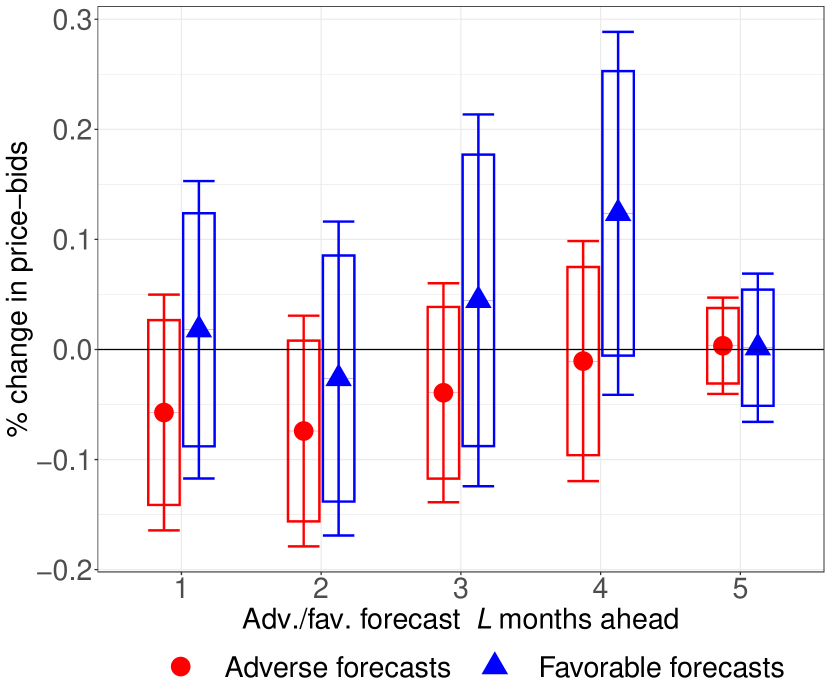

3.2.2 “Sibling” Thermal Generators

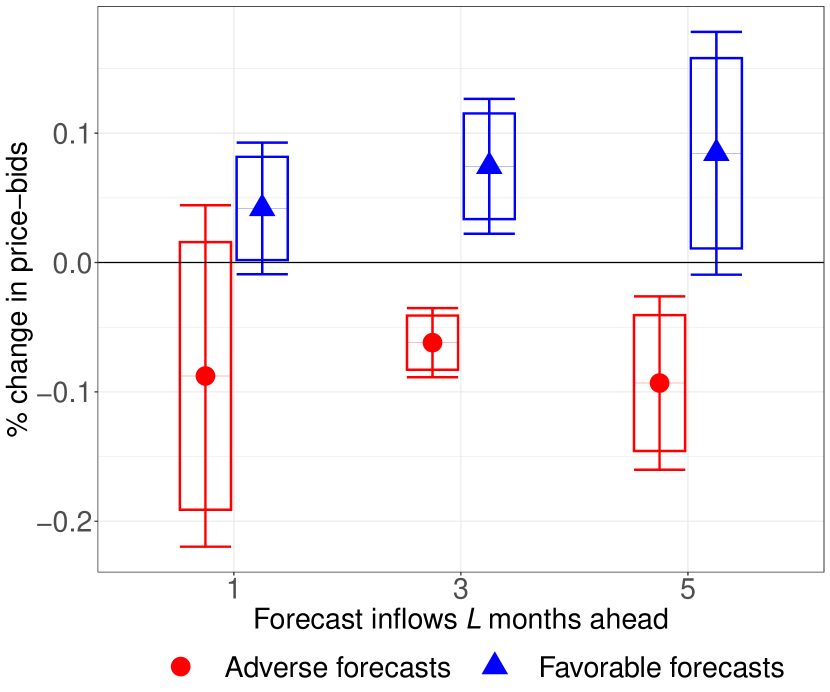

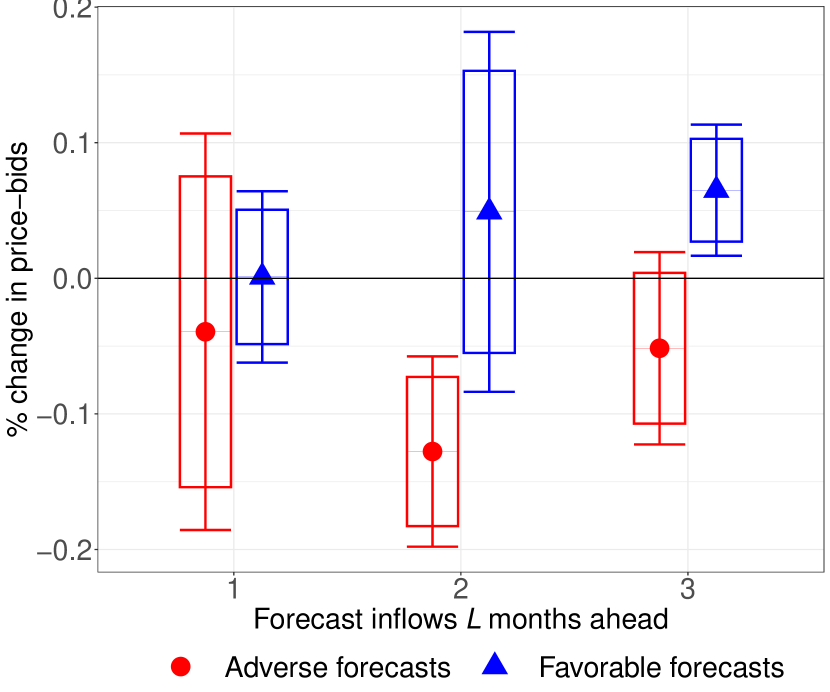

Figure 5 presents the estimation results of (1) on thermal generators that are sibling to dams. Due to the absence of water stocks for thermal generators, we include a control for a firm’s lagged total water stock in . The results unveil distinct responses of sibling thermal generators to forecast inflows compared to hydropower generators. Sibling thermal generators increase their supply schedule before favorable events (blue triangles) and decrease it before adverse ones (red circles). They primarily adjust through their price bids because, given their high marginal costs, they are not operational at all times and lack the flexibly to vary production across hourly markets. Finally, although the analysis indicates that they respond to extreme events well before hydropower generators, it is worth noting that this analysis focuses on extreme firm-level forecasts rather than generator-level forecasts as in the previous section, which might be less severe.191919Appendix Figure C6 shows that generators respond already two months ahead of adverse forecasts.

Notes: The figure studies how hydropower generators respond to favorable or adverse future water forecasts according to (1). Each plot reports estimates of in red and in blue for one, three, and five months ahead. Error bars (boxes) report the 95% (90%) CI.

Notes: The figure studies how sibling thermal generators respond to favorable or adverse future water forecasts according to (1). Each plot reports estimates of in red and in blue for one, three, and five months ahead. Error bars (boxes) report the 95% (90%) CI.

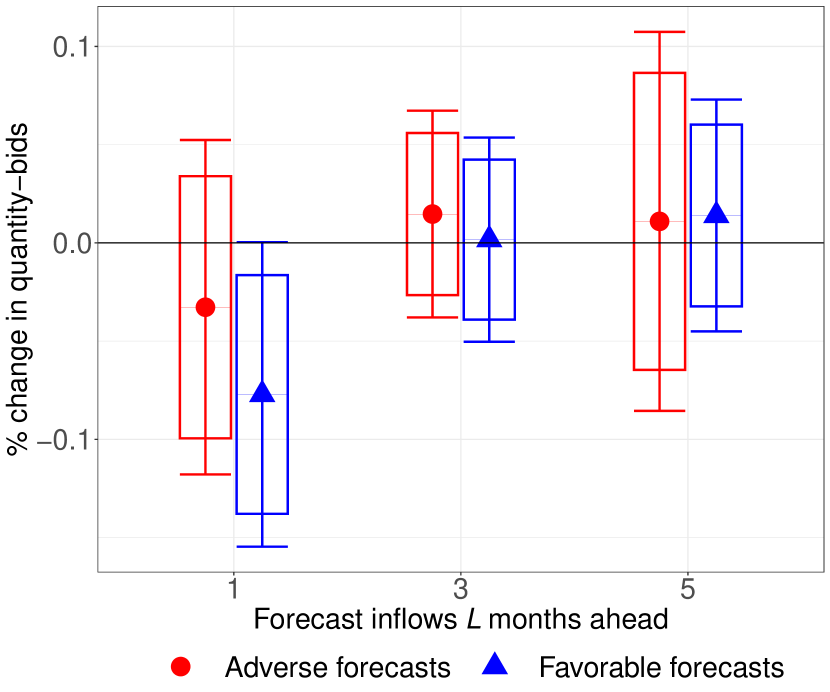

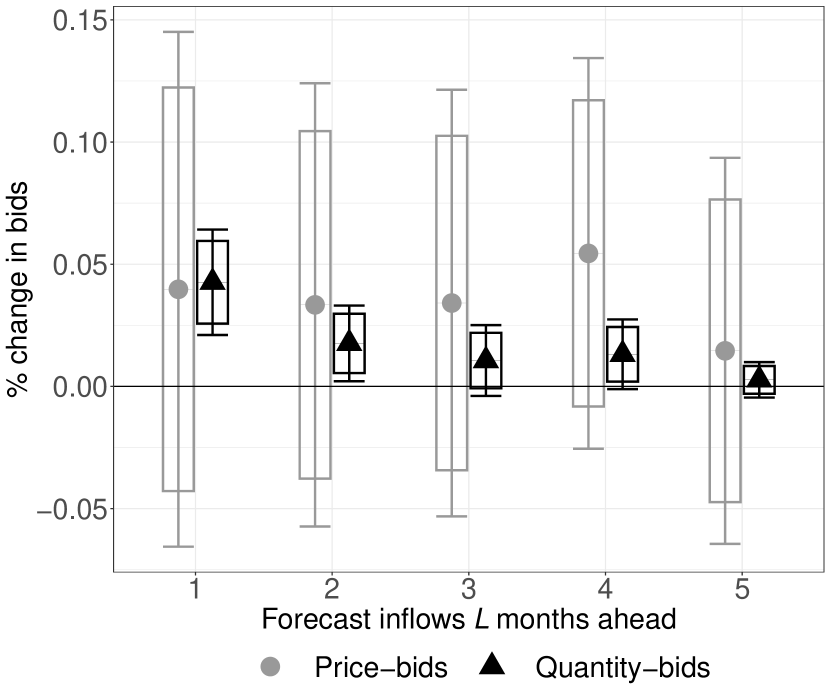

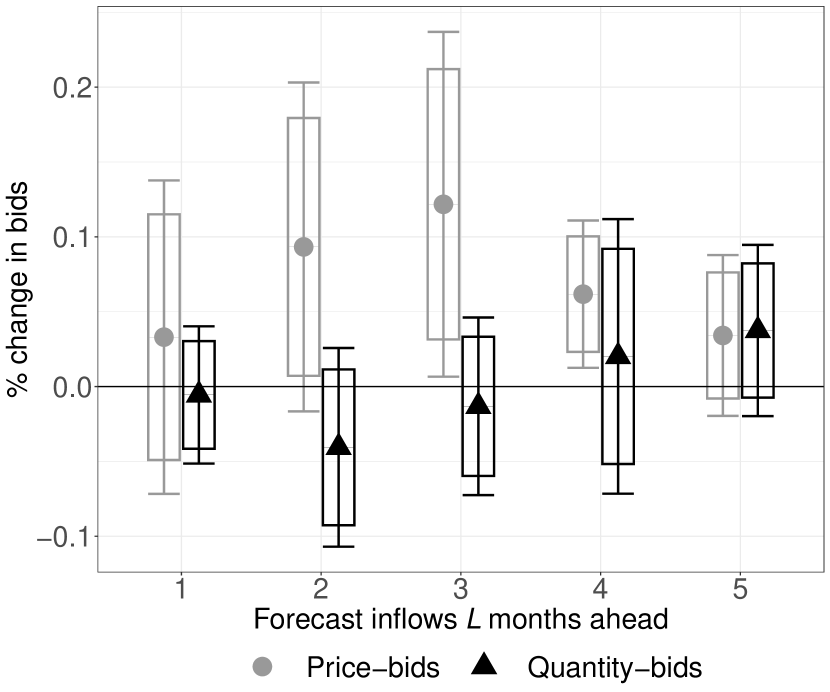

3.2.3 Competitors’ Inflow Forecasts

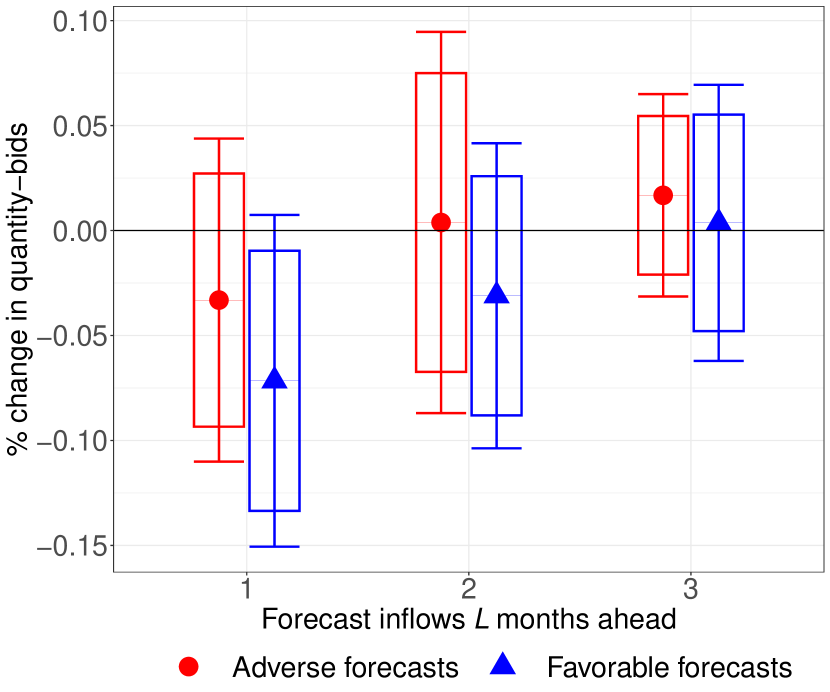

To comprehensively understand firms’ responses to future shocks, we explore whether hydropower generators incorporate reactions to competitors’ forecasts. We model adverse and favorable inflows in (1) based on the sum of inflows at a firm’s competitors. We allow for distinct slopes for each generator’s water stock to control adequately for current water availability at various dams in . Figure 6 reveals minimal movement in a firm’s bid concerning its competitors’ forecasts, with magnitude changes generally within and lacking statistical significance. Separate joint significance tests for adverse and favorable forecasts do not reject the null hypothesis that they are zero at standard levels.202020Appendix Figure C7 confirms similar results on a shorter forecast horizon (one to three months).

Notes: The figure studies how generators respond to favorable or adverse future water forecasts accruing to competitors according to (1). Each plot reports estimates of in red and in blue for one, three, and five months ahead. Error bars (boxes) report the 95% (90%) CI.

Appendix C.1.3 further extends this analysis in two dimensions. First, it demonstrates that generators respond to their own inflow forecasts but not to the inflow forecasts of competitors. Second, despite the potential informativeness of competitors’ water stocks, it offers suggestive evidence against this hypothesis. Consequently, generators do not appear to react substantially to the crucial potential state variables of their competitors. This observation, while potentially counterintuitive in a competitive context, finds parallels in industrial organization literature. For instance, Hortaçsu et al. (2021) show that airline carriers employ simple heuristics in pricing, disregarding the pricing of other airline companies. Similar to hydropower generators, airline firms grapple with forecasting seat demand (inflows) across various routes (dams). In both scenarios, focusing on their own state variable while overlooking those of competitors may simplify a complex problem.

3.3 Implications for Market Prices

Firms strategically deploy their thermal technology differently during periods of abundance (high inflows) and scarcity (low inflow). To assess whether a greater unshocked capacity (i.e., thermal) can alleviate the price hike resulting from dry spells, we capitalize on the exogenous occurrence of such periods across firms with different thermal capacity.

We base our analysis on the following regression model,

| (2) | ||||

where the logarithm of the hourly average weekly price is on the left-hand side. On the right-hand side, the first line of (2) features the interaction between whether a firm expects adverse or favorable inflow forecasts -months ahead with its total sibling thermal capacity in GWh, . We expect that the greater thermal capacity available to generators with adverse forecasts, the lower the price (), and vice-versa for favorable inflows () if thermal generators do not operate in similar periods (cf. Figure 5). The remaining two lines of (2) control for the direct effect of adverse and favorable forecasts and total thermal capacity on spot prices. Finally, includes lagged market outcomes, such as hourly average weekly demand and forward contracts, in logs. As error terms are likely correlated across seasons and hourly markets, we cluster the standard errors at the month and year level.

(1) (2) (3) (4) Average weekly price in hour () Adverse inflows (3 months), 0.166 0.210∗∗ 0.334∗∗ (0.284) (0.058) (0.077) Adverse inflows (5 months), 0.413∗∗ -0.127 -0.241 (0.126) (0.094) (0.117) Thermal cap. available to adv. inflows (3 months), -1.303 -1.746∗∗ -2.769∗∗ (2.539) (0.540) (0.747) Thermal cap. available to adv. inflows (5 months), -3.508∗∗∗ 0.875 1.979 (0.492) (0.721) (0.944) Favorable inflows (3 months), 0.032 0.021 -0.162∗∗ (0.203) (0.037) (0.044) Favorable inflows (5 months), 0.374 0.001 -0.368∗ (0.195) (0.083) (0.154) Thermal cap. available to fav. inflows (3 months), -0.038 -0.045 1.380∗∗ (1.654) (0.249) (0.348) Thermal cap. available to fav. inflows (5 months), -2.939 0.064 3.133∗ (1.722) (0.741) (1.322) Total sibling thermal capacity (GW), -0.012∗∗ -0.007∗∗∗ -0.005∗∗∗ -0.020∗∗∗ (0.003) (0.001) (0.001) (0.003) Lag demand (ln) Lag contract position (ln) Lag water stock (ln) Lag spot price (ln) FE: Hour FE: Year-by-season FE: Year-by-month Subset All All Dry season Wet season 7,464 7,464 2,424 5,040 R2 Adj. 0.639 0.934 0.920 0.915 * – ; ** – ; ∗∗∗ –

-

•

Notes: This table shows the estimated coefficients from (2). The main regressors are the number of adverse (rows 1 and 2) and favorable inflows (rows 5 and 6) and their interactions with the thermal capacity available to the firms that expect an adverse (rows 3 and 4) and a favorable inflow (rows 7 and 8). All variables are standardized. Column 1 includes fixed effects by year-by-season, while the remaining columns have fixed effects by year-by-month. Column 3 examines adverse inflow in dry seasons (from December to March) and Column 4 examines favorable inflows in wet seasons (from April to November). Standard errors clustered by year and month.

Table 1 presents the results, where we focus on forecasts three and five months ahead to avoid the correlation between the current total water stocks and the one- and two-month ahead forecasts. Column (1) controls for current market conditions using lag demand and forward contract position, as well as hydropower availability using total water stock. Fixed effects are at the hour and at the year-by-season (dry or rainy) level. Column (2) utilizes lag spot prices to control for market conditions and month-by-year fixed effects to account for hydropower availability. All regressors, including those that are a function of multiple variables, are standardized.

The estimates in Column (1) indicate that a one standard deviation increase in the number of adverse inflows expected three to five months ahead increases current prices. However, a concurrent one-standard-deviation increase in the sibling thermal capacity available partially compensates for these higher prices. Column (2) produces qualitatively similar findings, with the primary difference being that the largest effect appears three months ahead instead of five. This result can be attributed to the different controls, as including the lagged water stock in Column (1) captures some variation pertaining to three-month forecasts, as it correlates more strongly with the three-month forecasts than the five-month ones.

The results are less clear for favorable inflows, likely stemming from a correlation across forecasts. To gain deeper insights into the impact of favorable inflows on market prices, we refine our analysis by subsetting the sample in Columns (3) and (4). Specifically, we focus on adverse forecasts during dry seasons and favorable forecasts during wet seasons to further highlight the capacity constraint mechanism. The analysis confirms the previous results during droughts (Column 3). However, the opposite holds during wet seasons (Column 4). Here, prices are, on average, lower ahead of favorable inflows as dams expand their supplies. At the same time, thermal generators decrease their own supplies according to the mechanism outlined in Section 3.2.2. Therefore, more thermal capacity at firms expecting abundance increases market prices as these firms “take capacity out of the market” by decreasing their thermal supplies.

These findings hold significant implications for policy. The concentration of thermal capacity around firms expecting droughts may potentially decrease market prices, while conversely, it could raise prices during periods of expected abundance of renewables. To fully understand this result, the following sections introduce an oligopoly model to examine how diversified firms wield their market power under diverse capacity configurations. Then, we extend and estimate the model using data from the Colombian wholesale energy market, conducting counterfactual exercises to quantify the price benefits resulting from moving thermal capacity to renewable suppliers.

4 A Competition Model With Diversified Firms

This section introduces an oligopoly model that reproduces the key empirical findings from the preceding section. Firms exhibit diversified production, enabling each to produce the same homogeneous good by means of technologies with differing marginal costs and capacities. In this context, market dominance hinges on either a firm’s larger overall capacity or the superior efficiency of one of its technologies. When a firm dominates in capacities, it acts as a monopolist on the market unsatisfied by its competitors. Conversely, having the most efficient technology helps a firm “crowd out” its competitors by selling below their marginal cost. We find that the opposing impacts of these two sources of market power on market outcomes produce the empirical patterns in Section 3.2.

The firm’s problem. Consider an oligopolistic market where firms sell a homogeneous good, such as electricity, and face an inelastic market demand, , subject to an exogenous shock shifting demand horizontally, with a strictly positive density in . Before is realized, firm commits to a supply schedule, , which maximizes

| (3) |

where is firm ’s cost of producing at the market price, . The market clearing constraint forces firm ’s supply to equate its residual demand, , which is the demand not satisfied by ’s competitors at .

We adopt the supply function equilibrium (SFE) concept proposed in the seminal work of Klemperer and Meyer (1989), in which firm selects by best-responding to the supply of its competitors, , to maximize (3). SFEs come with two key advantages. First, we need no assumption on firm’s beliefs about the random demand shock : Klemperer and Meyer (1989) demonstrate that maximizing (3) with respect to a function, , is equivalent to choosing the optimal price for every possible demand realizations , or . By varying , we obtain all possible realizations of in which firm best responds to all its competitors: these quantity-price combinations, , depict the that solves (3).

Second, this ex-post optimality property does not apply to other standard models of competition like Bertrand and Cournot under demand uncertainty and increasing marginal costs. This property makes SFEs a natural equilibrium concept to examine the behavior of a firm whose technologies have different marginal costs and capacities. In addition, by allowing any non-negative supply slope, SFEs include these competition models as limiting cases: a horizontal schedule (a price for all quantities) aligns with Bertrand, while a vertical schedule (a quantity for all prices) aligns with Cournot.

Baseline (non-diversified firms). There are three production technologies: a low-, a high-, and a fringe-cost technology, with constant unit costs , , and , respectively, with , non-negative, and finite. Firm ’s technology portfolio is a vector detailing its capacity of low-, high- and fringe-cost technologies, namely, . Hence, depends on its technology-specific supply, , at price .

There are firms, with none of the firms being diversified in this baseline scenario. The technology portfolios of the strategic firms are for Firm 1 and for Firm 2. Firm 1 can be viewed as a supplier of cheap renewable energy, such as a dam, and Firm 2 as a fossil-based generator. Given the size of dams in the empirical application, we assume that , making Firm 1 the market leader. The technology portfolio of fringe firm is and includes only the fringe technology: since is small, these firms are price takers.212121Fringe firms ensure that the two strategic firms face decreasing residual demands. A price ceiling can replace this assumption as in Fabra and Llobet (2023), or we could assume that the market demand decreases in as in the original work of Klemperer and Meyer (1989).

The equilibrium supply for strategic firm depends on the market price. either firm produces for , as Firm 2, whose marginal cost is , would make a loss in this price range, while Firm 1 can unilaterally inflate to (an below) by not producing for any as in Bertran competition. For , firm ’s first-order condition (FOC) is:

| (4) |

Hence, in this price range, depends on the slope of its competitors’ supply, , and the unit cost of the marginal technology that firm uses in production , resulting in different slopes given a different market price and marginal technology. At , firm exhausts all its capacity to prevent being crowded out by the fringe firms (i.e., ). are continuous for any as a discontinuous supply provides opponents with a profitable deviation by increasing production at a slightly lower price.

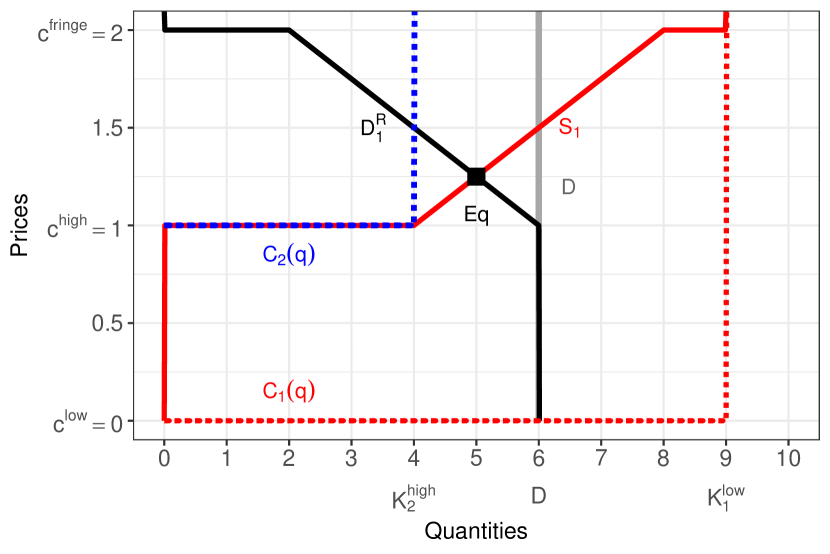

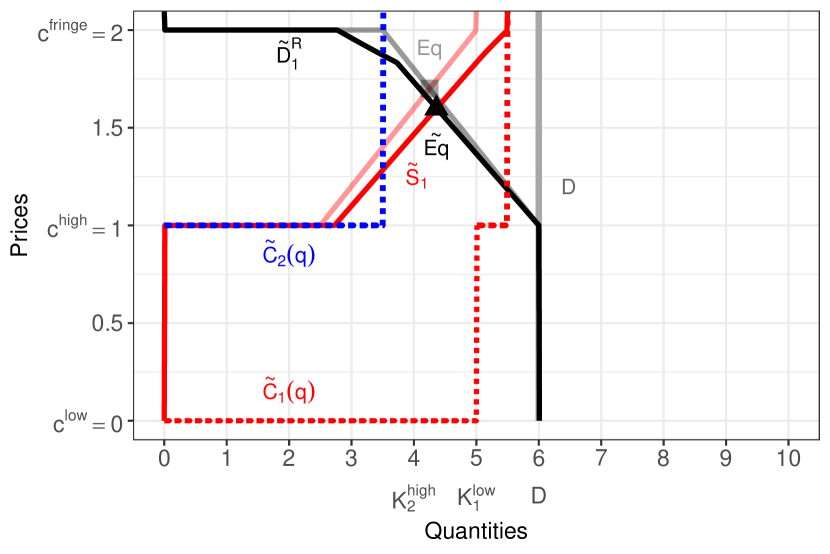

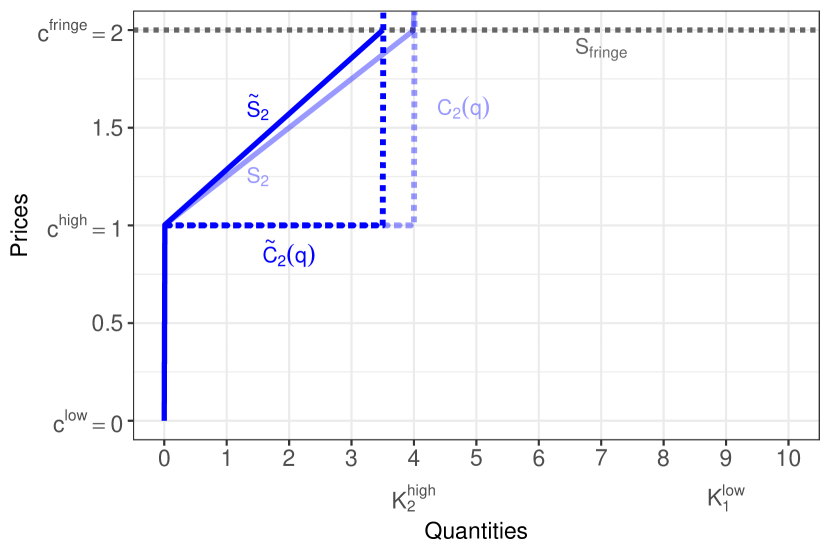

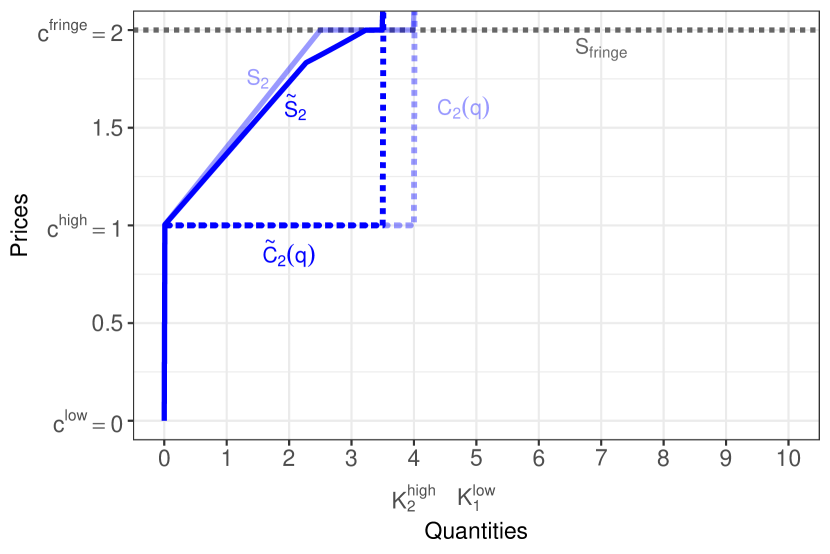

Before presenting a formal proposition, we numerically illustrate the equilibrium outcomes in this market in the left panels of Figure 4 and use them to visually compare the impact of diversification, which we illustrate in the right panels. The red (blue) dotted lines report the assumed cost structures of Firm 1 (Firm 2). Under abundance (Panel a), Firm 1’s low-cost capacity is but only under scarcity (Panel c). The other primitives are constant across scenarios at , , , and . Solid lines report equilibrium outcomes from the point of view of Firm 1. The solid red line is Firm 1’s supply, , and its residual demand, , is in black. Without loss of generality, we fix the realized market demand at 6 (vertical gray line).

The shape of follows (4) and, hence, is quite similar across panels. As mentioned above, for . At the price level , Firm 1 undercuts its opponent thanks to the greater efficiency of its low-cost technology, similar to the equilibrium that we would observe under Bertrand competition with asymmetric firms. Unlike Bertrand, Firm 1 does not employ all its capacity at this price because firms have incentives to reduce their production, similar to a Cournot game. For every , the FOC in (4) entails comparing the profits from pricing the marginal unit at against the alternative case of selling at , thereby losing the marginal unit to competitors while raising higher revenues from the inframarginal ones. Hence, the slope of becomes positive at large enough quantities and similarly for Firm 2. This tradeoff disappears at , the price at which fringe firms flood the market, so that becomes vertical at capacity.

has a similar shape to . can be found as the horizontal difference between the gray () and the black () lines, with part of ’s horizontal segment at shared with the fringe firms, as Firm 2 can price its last units slightly below to avoid being crowded out. To avoid cluttering Figure 4, we plot in Appendix Figure A1.

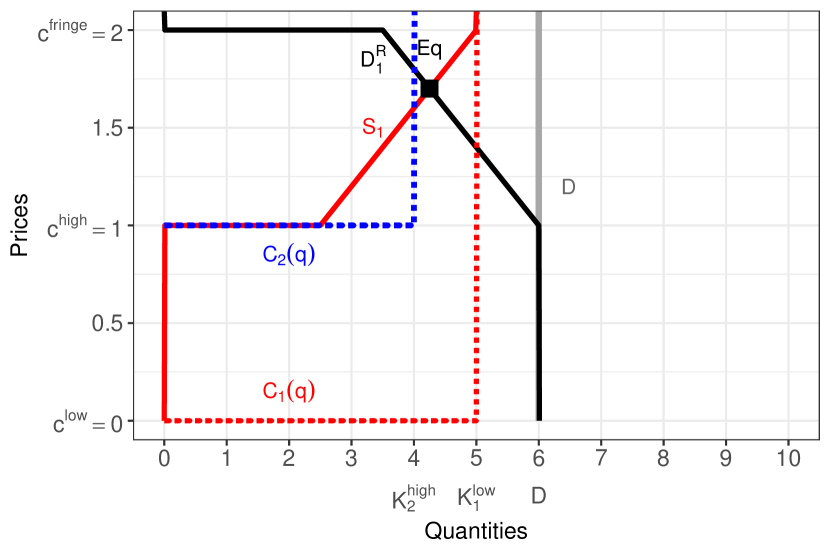

Since, in equilibrium, at least one of the two firms must exhaust all its capacity,222222If not, undercutting one’s rival by producing more at lower prices is the optimal strategy. a key difference arises across the two panels. In Panel (a), Firm 2 exhausts all its capacity as , while is horizontal meaning that Firm 1 is willing to sell multiple units at . This outcome is reversed under scarcity in Panel (c). Here, Firm 2 has a greater ability to unilaterally raise prices for greater demand realizations since Firm 1’s capacity is smaller. As both firms supply less compared to Panel (a), Firm 1 exactly exhausts its capacity as , while Firm 2 has idle capacity at this price. Scarcity does not prevent Firm 1 from crowding out Firm 2 for low-demand realizations; however, the horizontal segment of is now shorter compared to that in Panel (a) as Firm 1 rumps up production earlier to exhaust capacity at . Equilibrium prices are higher in Panel (c) than in Panel (a), echoing the results in Table 1, which shows that adverse inflows and lower capacities are associated with higher prices.

&

&

&

&

Notes: Each panel illustrates equilibrium outcomes from the perspective of Firm 1. Solid lines represent equilibrium outcomes, while dotted lines depict marginal cost curves for Firm 1 (red) and Firm 2 (blue). In each panel, the left plot shows outcomes before a capacity transfer, and the right plot shows outcomes after transferring 0.5 units of high-cost capacity from Firm 2 to Firm 1. The shaded square () and curves in the right plot represent the pre-transfer equilibrium, and symbols with a denote post-transfer equilibrium variables. Each subcaption details the technology profile of each firm as . Market demand is constant at 6 (gray solid line), and the cost parameters are , , and .

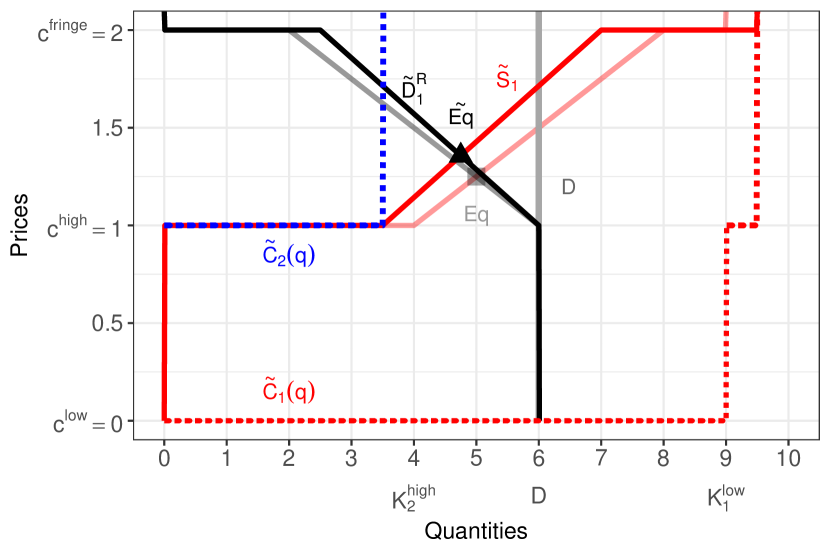

Equilibrium with diversified firms. To replicate the analysis in Table 1, where we studied market price changes when the firm experiencing a drought (low ) or abundance (high ) had more or less thermal capacity ( or ), we diversify Firm 1 by considering a reallocation of units of high-cost technology from Firm 2 to Firm 1. As a result, the technology portfolios in Panels (b) and (d) of Figure 4 change to and , where we overlaid and shaded the original and to compare the market outcome with the relevant baseline scenario.

We find that diversifying Firm 1 has opposite effects on market prices in the two scenarios. First, notice that the new marginal cost curves, and , denote a greater capacity concentration around Firm 1 in Panels (b) and (d) compared to Panels (a) and (c), respectively. Panel (b) presents the standard effects of concentration in oligopolistic markets: as Firm 1 prioritizes its low-cost capacity to its new high-cost one – the so-called, merit order – it employs its high-cost capacity only at . Before the transfer, this capacity was sold by Firm 2 for . Both firms react by decreasing their supply schedules, leading to higher prices, consistent with the role of greater thermal concentration during wet periods, as in Column 4 of Table 1.

In contrast, a similar technology transfer decreases prices under scarcity. In Panel (d), Firm 1 has more capacity than in Panel (c), but it still exhausts its overall capacity () at in equilibrium because is small relative to the size of Firm 2 – note that its supply was flat for 1.5 units at in Panel (c), which effectively are not produced in that equilibrium (Appendix Figure A1). In Panel (d), the transfer enables the firm to employ more of its low-cost technology to outcompete its rivals more than in Panel (c), even though its low-cost capacity stays unchanged, because it alters Firm 1’s trade-off between marginal and inframarginal units at all , with the new high-cost units utilized for approaching . Therefore, after the transfer, Firm 1’s hydropower supply is still steeper under scarcity than under abundance (Panel b), but it expands in Panel (d) compared to Panel (c). On the other hand, comparing Panels (b) and (d), Firm 1’s high-cost capacity is priced at a higher price under abundance than scarcity, which matches the empirical evidence from Panel (a) of Figure 5.

Turning to Firm 2’s best response, the gap between and the shaded pre-transfer whitness Firm 2’s new agressive pricing strategy, as its supply expands for all to limit its revenue loss due to Firm 1’s more aggressive pricing.232323 At this level, Firm 1’s supply flattens slightly according to (4) because the following marginal units cost the firm instead of . This response is easily detected for prices above the price at which Firm 1 exhausts its units (). As Firm 2 priced the transferred units exactly at before the transfer, but Firm 1 sells them for after it, equilibrium prices decrease compared to Panel (c). This result mirrors the finding in Table 1 that increased thermal capacity among firms anticipating droughts helps temper price surges. It is worth noting that across all panels, Firm 1 exclusively utilizes its low-cost technology at the equilibrium , highlighting the absence of economies of scale because the average cost stays unchanged.

The following proposition generalizes these numerical examples.

Proposition 1

A marginal capacity transfer from Firm 2 to Firm 1 increases the equilibrium price if (abundance scenario) and decreases it if (scarcity scenario).

The proposition demonstrates that the lower (higher) prices observed when the firm experiencing relative scarcity (abundance) has more high-cost thermal capacity, as depicted in Table 1, are attributable to strategic competition. In addition, the proposition clarifies the exact meaning of scarcity and abundance, as Firm 1’s relative capacity compared to Firm 2, taking into account its cost advantage through the ratio . In Appendix A.1.1, we show that this equilibrium exists and is unique.

Therefore, diversification can incentivize a more efficient usage of the low-cost technology. If firms had the same technologies, moving capacity from a small to a large firm would always result in higher prices, as it severs Bertrand forces, making one’s capacity the sole source of market power. Similarly, if both Firms 1 and 2 were diversified with the same capacity profile with and , moving high-cost capacity from Firm 2 to 1 raises market prices as Firm 2 becomes less competitive at high prices due to Firm 1’s larger high-cost capacity (the proof is in Appendix A.1.3).

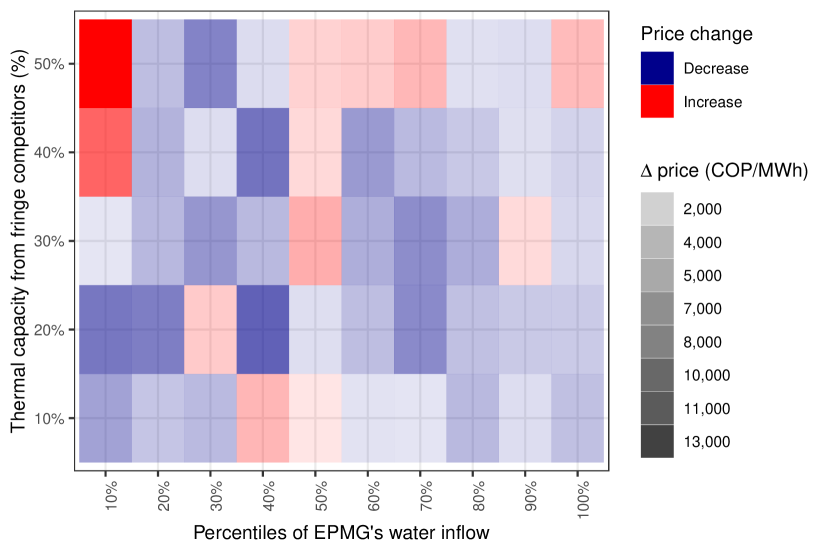

Concentration & market power. Our analysis underscores a novel U-shaped relationship between concentration and market prices when efficiency dominates. To see it, focus on the scarcity scenario and imagine that all the capacity of Firm 2 is transferred to Firm 1 instead of just units, making . Due to such a dominant capacity position, Firm 1 will best respond by selling all its capacity at , meaning a higher equilibrium price than in Panel (d).

Therefore, if firms are diversified, a small -reallocation to the most efficient firm pushes the price down as the receiving firm expands its supply to crowd out its competitors – i.e., Bertrand forces. Further increases in lead to smaller marginal drops in prices, as the greater capacity provides the firm with the standard monopolistic incentives to exclude consumers by raising prices – i.e., Cournot forces. Prices will first drop, reach a plateau, and then increase as shares of capacities are transferred. When capacity dominates instead, any capacity transfers of less efficient technologies to the dominant firm can only raise prices due to the merit order.

General framework. Extending the game presented in the previous section to strategic players and a downward-sloping market demand, Appendix A.1 finds that when the market clears and uncertainty resolves,

| (5) |

As in Cournot, the left-hand side portrays firm ’s markup. Unlike Cournot, the right-hand side features not only the price elasticity of demand faced by firm but also the ratio of the slopes of firm ’s supply and residual demand at price , which we term “crowd out.” The ratio in parenthesis is non-negative: if greater than one, gains market shares from its rivals and loses to them when smaller than one, as changes marginally. The equilibrium supply balances a firm’s efficiency, as measured by the merit order of ’s production technologies, , with a firm’s capacity dominance, which relates the firm’s technology portfolio to that of its competitors through and .

To gain intuition, imagine either plot in Figure 4 as a grid where prices and quantities are discretized: if at a given price increase competitors increase their supply more than , then loses quotes of the market as . In standard oligopoly games, firms only internalize that increasing production decreases prices through the price elasticity, (),242424Since demand is vertical, the demand elasticity to prices, , is not defined in our model. Hence, in an abuse of notation, in (5) is firm ’s share of the demand elasticity of market prices, with market demand , which is analogous to the demand elasticity of prices faced by a firm in the Cournot and in the homogeneous-good Bertrand models. but do not internalize the strategic response of their competitors through the slope of their supplies (). As a result, firms’ equilibrium schedules in (5) are strategic complements, as we prove in Proposition 3 in Appendix A.1 and as illustrated from the best-responses in Figure 4.

In the remainder of the paper, we use the insights developed in this section to quantify the benefits of diversification in the Colombian wholesale energy market.

5 Quantitative Model

This section extends our framework to account for the main institutional and competitive aspects of the Colombian energy market, namely, the structure of the spot market and responses to the expectation of future water availability. The latter will provide exogenous variation in a firm’s low-cost capacity, which we use to quantify the efficiency and capacity forces introduced in Section 4.

Generation. Each firm is equipped with generators indexed by . For simplicity, as illustrated in Figure 2, we focus on two technologies: hydro, characterized by a marginal cost , and thermal, with a marginal cost . Let () represent the set of hydropower (thermal) generators owned by firm . If both sets and are not empty, then firm is diversified with technology portfolio . This analytical framework can be extended seamlessly to incorporate additional technologies.

Institutions. In the spot market at time , each generator from firm submits a price bid, , along with hourly quantity bids, . As in the previous section, the hourly demand, denoted as , is vertical and is only known to firms up to a noise parameter, with zero-mean and full support. The system operator crosses the supply schedules submitted by each firm, , against the realized demand to ascertain the lowest price, , such that demand equals supply:

| (6) |

Thus, firm ’s profits in hour of day hinge on and and can be expressed as:

| (7) |

Here, the first term is ’s spot market profits similar to that in (3). Additionally, firm ’s profits are influenced by its forward contract position, resulting in an economic loss (profits) if it sells MWh at below (above) . The reliability charge mechanism, known as cargo por confiabilidad, mandates generators to produce whenever the spot price exceeds a scarcity price, , also contributes to firm ’s overall profits.252525Scarcity prices are updated monthly and computed as a heat rate times a gas/fuel index plus other variable costs (Cramton and Stoft, 2007), with scarcity quantities, , determined through yearly auctions (Cramton et al., 2013).

Law of motion of water. Hydropower capacity depends on water inflows, and firms take it into account in their pricing decisions, as shown in Section 3.2. Drawing from the hydrology literature (e.g., Lloyd, 1963, Garcia et al., 2001), a generator’s water stock depends on the past water stock, the water inflow net of evaporation and other outflows, and the water used in production. At the firm level, the law of motion of a firm’s overall water stock can be summarised through the following “water balance equation” as,

| (8) |

where denotes the observed water stock of firm in period in MWh, is hydropower supplied by firm ’s generators at the market price in each market hour, and is the water inflow of generator in day .

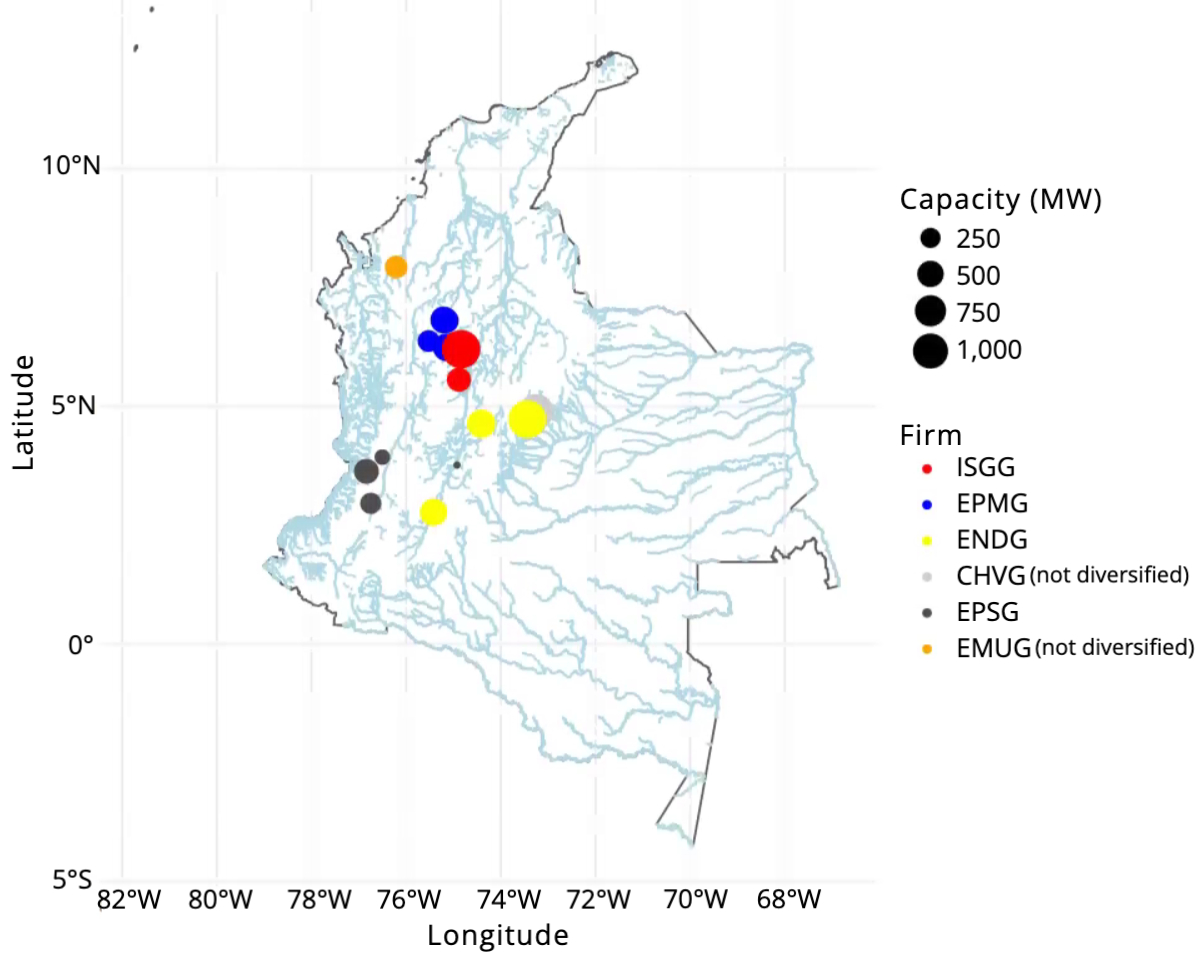

The law of motion in (8) is at the firm level for various reasons. First, our findings indicate that the generators of the same technology that a firm owns respond to forecasts accruing to the whole firm, suggesting that the locus of control is the firm itself. Second, dams belonging to the same firm tend to be on nearby rivers (Figure 8), meaning dependence on the water inflow of dams owned by the same firm. In contrast, the inflow correlation across firms’ water stocks – after accounting for seasons and lagged inflows – is less than . Such a low correlation depends on riverbeds acting as “fixed points” for the perturbation in an area: given the spatial distribution of dam ownership in Colombia, local rainfalls accrue to just one firm, reducing the correlation across firms.

Notes: The location of Colombia dams by firm (color) and capacity (size). Colombia’s West border is with the Pacific Ocean while rivers streaming East continue through Brazil and Venezuela. To give a sense of the extension of Colombia, its size is approximately that of Texas and New Mexico combined.

Strategic firms. We consider all firms with at least a dam as strategic. For these firms, the actual value of holding water results in a trade-off between current and future production. To the extent that firms take into account future inflows, a firm will choose a supply schedule to maximize the sum of its current and future profits according to

where the expectation is taken over the market demand uncertainty, , and is the discount factor. Using a recursive formulation, a firm’s objective function becomes

| (9) |

where vectors are in bold font. The state variable is the vector of water stocks, with domain , and transition matrix following (8). The inputs in are the water stocks, the realized hydropower productions, and the water inflows on day .

Competitive fringe. As in Section 4, the supply schedules of fringe firms is zero for prices below their marginal cost. They supply all their capacity for higher prices.

5.1 Market Power and Market Prices with Diversified Firms

In this section, we derive the optimal quantity bid submitted by generator of firm . Our focus on quantity bids is grounded on the fact that generators submit hourly quantity bids but only daily price bids, providing greater flexibility in selecting quantities than price bids. We then study how market power affects pricing with differentiated firms.

Generators’ supply schedules are characterized by step functions, which makes them not differentiable (Kastl, 2011). To study the FOCs from (9), we smooth supply schedules for each firm following Wolak (2007) and Reguant (2014) (see Appendix E for the smoothing procedure). We analyze the change in discounted profits for firm resulting from a marginal change in generator ’s quantity bid, , where is either a hydro () or thermal () generator. Omitting the expectation with respect to and the firm and generator indices () of technology for clarity, the FOCs are:

| (10) | ||||

The derivative of firm ’s current revenues from (7) with respect to is in the first line of (5.1). The first term in parenthesis is the marginal revenue in the spot market. Market power lowers marginal revenues below market prices, , if . Conversely, if the firm is a price taker (), it is paid precisely on its marginal unit. This capacity channel prompts firm to reduce for all its technologies when market power increases, akin to the capacity effect witnessed in Panel (b) of Figure 4, in which market power resulted from an exogenous capacity transfer. The second term in the same line addresses how the forward contract position and the reliability payment system influence bidding in the spot market.

Market power affects equilibrium outcomes also through an efficiency channel. The actual marginal cost is the sum of its operating marginal costs, , in line two, and its intertemporal opportunity cost, in the remaining lines of (5.1), which endogeneizes the firm’s capacity constraint through a tradeoff between current and future production. By allocating more capacity to the current hydro supply, this tradeoff intensifies as it decreases the firm’s future water stock and profits. Hence, the integral in line three of (5.1) is non-positive. Since is constant over time, this intertemporal opportunity cost contracts or expands ’s cost curve for different realizations of setting the firm under scarcity when , or abundance when .

Generator adjusts its response to scarcity based on its market power. In the absence of market power, when , the firm experiences a decrease in its future profits that its equal to the change in the water stock, , times the expected change in future profits as in the integral in line three. The introduction of market power, denoted as , counteracts this loss. With market power, the firm recognizes that increasing marginally decreases , resulting in a smaller portion of its hydropower supply being satisfied in equilibrium as . Consequently, the two terms in parentheses in the third line of (11) exert opposing influences on marginal costs during scarcity events, leading to a net positive effect for hydropower generators, which is consistent with the drop in supply ahead of droughts in Figure 4. In contrast, thermal generators cannot directly impact the firm’s hydropower supply (). In this case, the net effect is negative, prompting a firm to raise its thermal supply ahead of a drought to preserve its hydropower capacity. This observation is in line with results in Figure 5.

We join these observations regarding the supplies of hydro and thermal generators in the following proposition,

Proposition 2

If a firm’s revenue function is strictly concave and twice differentiable, the marginal benefit of holding water decreases in its thermal capacity , i.e., .

Proof. See Appendix A.3.

This proposition reveals that a firm’s hydropower production increases in its thermal capacity, which squares with the theoretical analysis in the bottom panels of Figure 4. The availability of high-cost supply eases Firm 1’s resource constraint, leading to increased hydro production. Intuitively, thermal capacity reduces future water requirements, diminishing the value of holding water now. Thus, examining the efficiency channel in isolation shows that a diversified firm’s output surpasses that of two specialized firms, each with either thermal or hydro generators.

Finally, notice that the state space includes all firms’ current water stocks, : the last line of (5.1) considers how a change in a competitor’s hydropower generator impacts and, thus, ’s expected profits through the market clearing (). Because this channel does not affect firm ’s thermal and hydro generators differently, it does not shed light on the implications of diversified technologies, on which this paper focuses.

5.1.1 Capacity vs. Efficiency in the Data

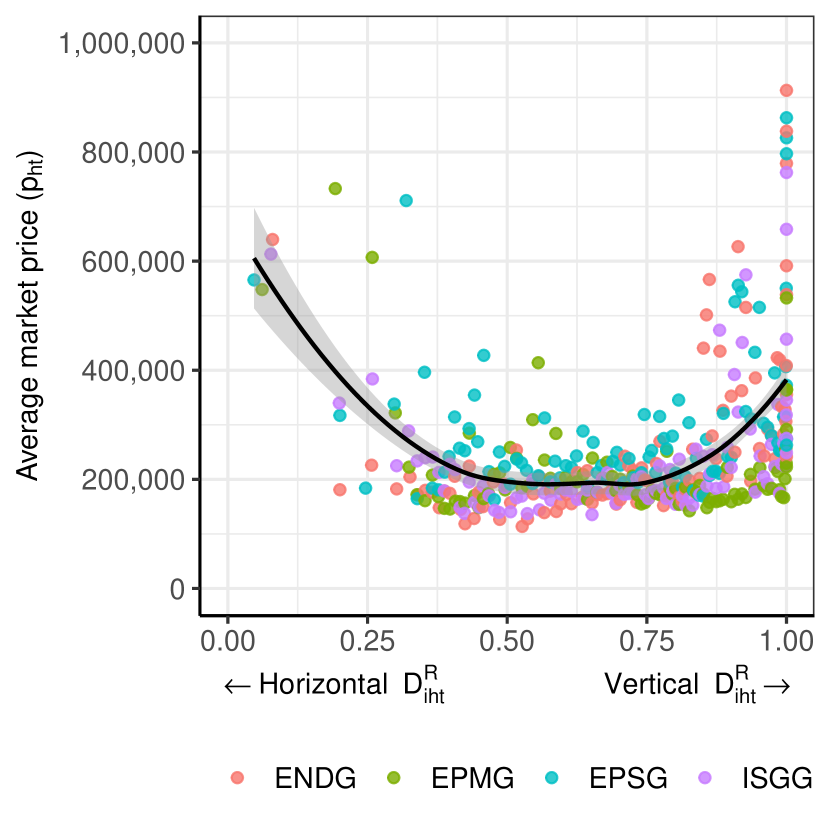

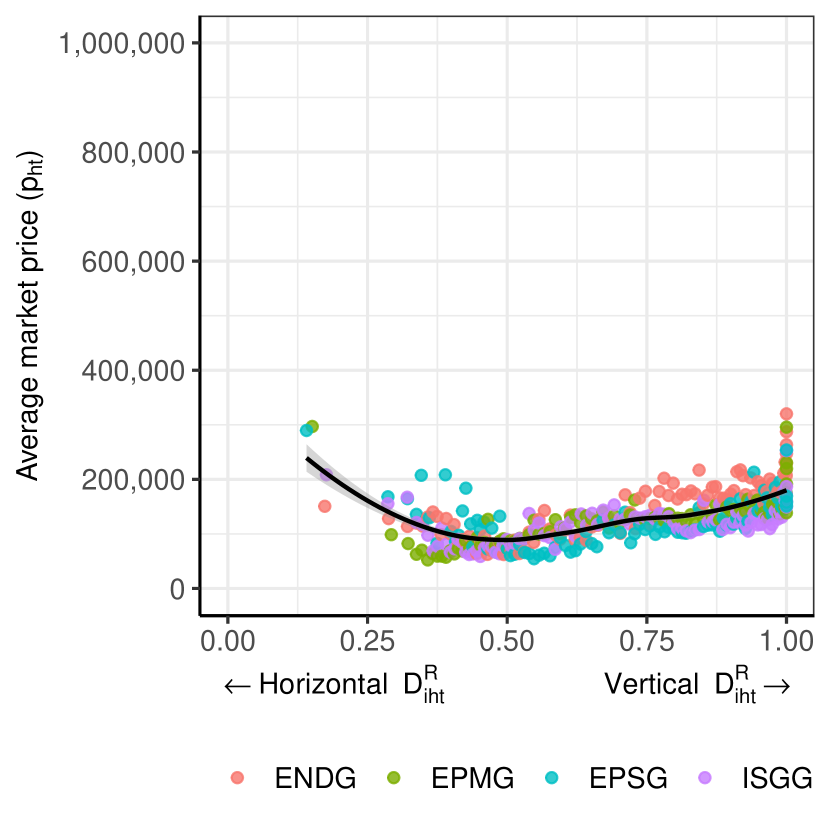

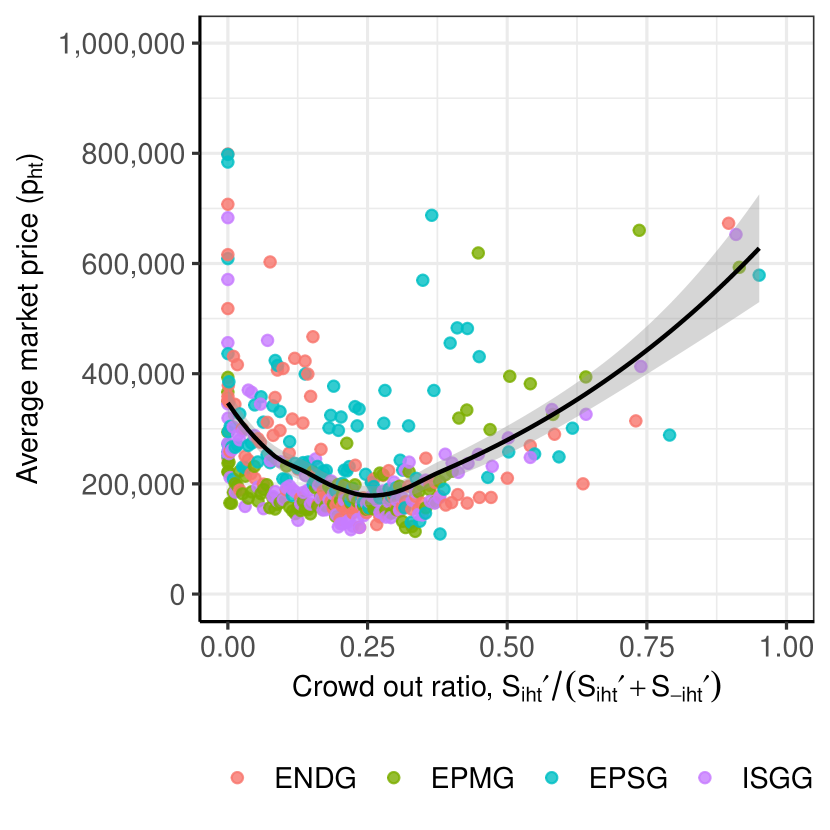

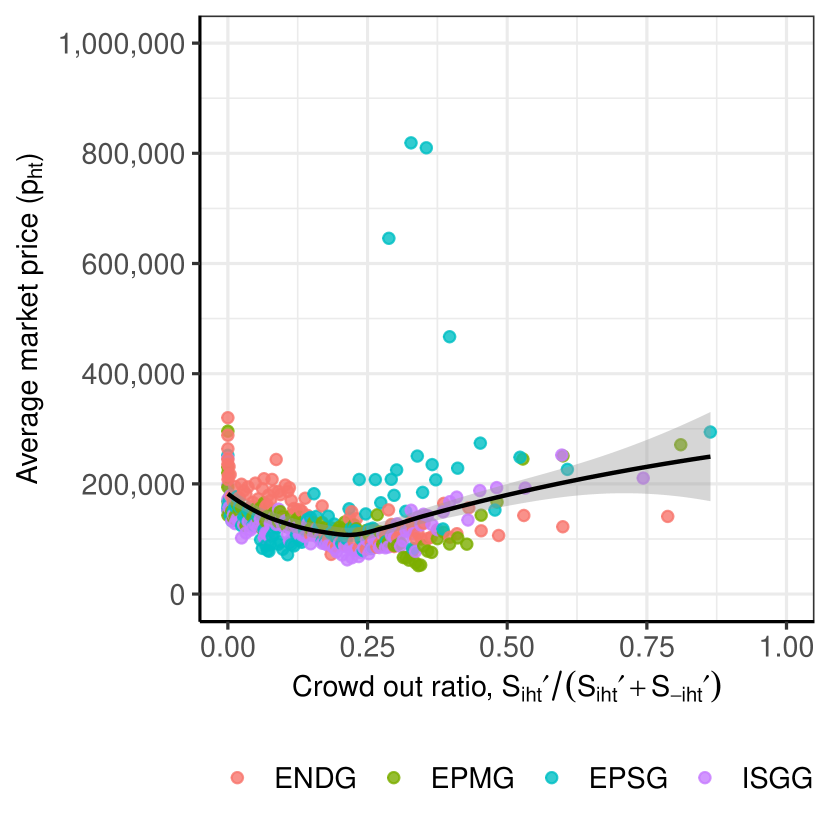

Combining the capacity and efficiency channels described above, Figure 9 illustrates the relationship between market prices (y-axis) and the slope of a firm’s residual demand (x-axis), which is flat at 0 (indicating the firm is a price taker) and vertical at 1. In Panel (a), the focus is on scarcity periods where firm has water stocks below its 30th percentile, whereas Panel (b) considers water-abundant periods with firm ’s water stock above its 70th percentile. Each scatter plot represents the average of hour-by-day markets with similar coordinates over 100 points per firm.

Viewing variation in market power as induced by variation in the technology portfolio of the firms facing scarcity, Panel (a) reveals a U-shaped relationship between prices and market power similar to that discussed in Section 4. Efficiency dominates when market power is low, causing an initial drop in market prices as demand becomes more inelastic. As market power increases, firms opt to reduce production across all technologies, leading to higher prices due to the marginal revenue effect. In contrast, the U-shape is less pronounced in Panel (b) of Figure 9, where , reducing the dependence of future profits on current production. Interestingly, this U-shape relationship is entirely driven by the crowd out ratio, which we introduced in (5) (Appendix Figure D1).262626This result is not surprising given that an application of the envelope theorem to (6) finds that .

Notes: The figure presents binned scatter plots of the market prices (y-axis) for different slopes of a firm’s residual demand (x-axis), computed as , with 100 bins per firm. Only diversified firms with dams whose bids are dispatched are considered. The black line fits the data through a spline (the 95% CI is in gray). Panel (a) focuses on markets where firm has less than the 30th percentile of its long-run water stock. Panel (b) focuses on periods where ’s water stock is greater than its 70th percentile.

5.2 Identification and Estimation

The extensive state space outlined in (5.1) presents a dimensionality challenge in estimating the relevant primitives. Existing literature offers two primary strategies to address this issue. The first method involves leveraging terminal actions (Arcidiacono and Miller, 2011, 2019), which eliminates the need to compute the value function during estimation. This approach is not applicable to our study since no exit occurred in our sample.

Our proposed solution approximates the value function with a low-dimensional function of the state space, denoted as , where are appropriately chosen basis functions.272727Basic polynomials or, as suggested by Bodéré (2023), neural networks can serve as basis function. This approach echoes the work of Sweeting (2013), who introduced a nested iterative procedure. In his procedure, given an initial policy function detailing the optimal course of action for each generator in a market, the algorithm (i) simulates forward the static profits in (9) for days for each potential initial value of firm ’s water stock given a discount factor , (ii) regresses the discounted sum of the daily profits on to estimate the parameters of , and (iii) finally estimates the cost parameters in (9) given the approximated . The iterative process halts when the implied policy from maximizing , , is sufficiently close to the previous one. Alas, we cannot simulate forward the contribution of forward markets to current profits in step (i), as we do not observe the price of forward contracts in (7), . Therefore, disregarding in the regression of discounted profits in step (ii), , on water stocks, , will not identify the coefficients, as the left-hand side is a poor proxy of discounted cumulative profits, .

To overcome these problems, we follow Wolak (2007) and Reguant (2014) and base our analysis on the FOCs with respect to a firm’s quantity bids (5.1), which do not require knowledge of . We rewrite (5.1) as follows:

| (11) |

where we grouped known terms into the following variables. The left-hand side, , is the marginal revenue or the first line of (5.1). On the right-hand side, we denote the sum of the direct and indirect effects, , by ; the superscript indicates the technology of generator , whether hidro or thermal . In the last term, denotes the sum of the indirect effects at ’s competitors in the last line of (5.1). These terms and are directly identified from the data. The only unknowns are and . Given the linearity of the FOCs, variation in and identifies and the coefficient vectors approximating . We postpone the analysis of the policy function to the next section where we run counterfactual analyses.

5.2.1 Estimation

Estimation requires fixing the number of coefficients, , and the bases , for approximating . Typically, a standard spline approximation of a univariate function necessitates five bases, or knots (e.g., Stone and Koo, 1985, Durrleman and Simon, 1989). Hence, five parameters must be estimated to approximate a function in one dimension. With four firms, allowing for interactions between all the bases would require estimating parameters, which is not feasible, given that we need to instrument them. Our working assumption, echoed by the empirical results in Section 3.2.3, is that a firm only considers its future water stock when bidding. With this assumption, the transition matrix simplifies to , and a firm’s future profits, , depend on its future water stock and its law of motion (8) through but on only through .

We allow the transition matrix to vary across firms, . We model firm-level water inflows using an ARDL model mirroring the estimation of inflow forecasts in Section 3 (Pesaran and Shin, 1995). The unexplained portion, or model residual, informs the probability that firm will have a certain water stock tomorrow, given the current water stock and net inflows. For each firm, we fit this data with a Type IV Pearson distribution, a commonly used distribution in hydrology. This distribution’s asymmetric tails assist in exploring firms’ behaviors during water-scarce and abundant periods. Appendix B outlines the estimation of the transition matrix and discusses its goodness of fit.

Under these assumptions, the moment condition is expressed as:

| (12) |

where we modeled so that no assumption about the discount factor is needed. We assume that both the marginal costs and the value functions have a non-deterministic i.i.d. component, which gives rise to the error term in (12).

The estimation of and requires instruments as unobserved variation in supply and demand (e.g., an especially hot day) might be correlated with . We employ variables shifting a generator’s cost to control for endogeneity.282828The set of instruments includes temperature at the dams (in logs) for hydropower generators and lagged gas prices (in logs) for thermal generators, which we interact with monthly dummies to capture unforeseen shocks (i.e., higher-than-expected evaporation or input costs), switch costs, which we proxy by the ratio between lagged thermal capacity employed by firm ’s competitors and lagged demand, and its interaction with lagged gas prices (in logs) for thermal generators. Importantly, gas is a global commodity, and we expect that Colombian wholesale energy firms cannot manipulate its market price. We also include various fixed effects in to account for constant differences across firms and generators – in the real world, generators’ operating costs may differ within the hydro and thermal cathegories – and time-varying factors that affect equally all generators of a certain technology like changes in gas prices.

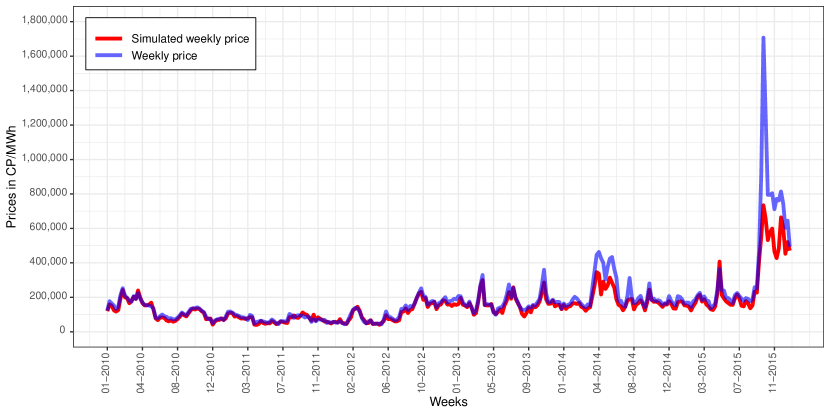

5.2.2 Estimation Results

We estimate (12) on daily data from January 1, 2010, to December 31, 2015. We use two-stage least squares and show the results in Table 2. We change the fixed effects used in each column. Columns (1) and (2) have fixed effects by week, while Columns (3) and (4) use daily fixed effects. Columns (2) and (4) also include month-by-technology fixed effects, in addition to fixed effects by firm, generator, and time. These adjustments help us control for seasonal factors differently affecting technologies over time.

The table has four panels. The first two panels show estimates for thermal () and hydro () marginal costs and for the five value function parameters (). The third panel indicates the fixed effects, whereas the last panel displays test statistics for the IVs.