Nash equilibrium in a singular stochastic game between two renewable power producers with price impact

Abstract

In this paper we solve the general problem, already formulated in [2], of finding a Nash equilibrium between two agents who can install irreversibly photovoltaic panels in order to maximize their profits of selling the produced electricity net of installation costs, in the case that their cumulative installations have an impact on power prices. Starting from a static version of the game, we find out that there exists a region in the state space where Nash equilibrium dictates that both players install, and in some cases this optimal installation strategy is non-unique. We then come back to the original continuous time problem, which needs a generalization of the Verification Theorem present in [2], taking into account a lack of smoothness of the value functions and the possible non-uniqueness of optimal strategies seen above. Finally, we explicitly construct the equilibrium strategies and the value functions, which depend on the two free boundaries which separate the region where each player installs or waits.

Keywords: singular stochastic control, irreversible investment, variational

inequality, singular stochastic games, Nash equilibria, market impact

MSC: 35C99; 35D99; 35K10; 49L12; 60G99; 60H30; 91B70; 93E20.

1 Introduction

The paper [9] formulates the problem of optimal irreversible installation of photovoltaic panels for a single power-producing company, willing to maximize the profits from selling electricity in the market on an infinite time horizon and under the constraint that the cumulative installation cannot exceed a given maximum capacity , and assumed to be large enough that its installation has an impact on power price. More in detail, the power price is assumed to follow an Ornstein-Uhlenbeck (OU) process (which reflects the stylyzed fact, empirically observed in several markets, that power price could possibly be negative), where the long-term mean decreases linearly with respect to the cumulative installation. The resulting optimal control problem is of singular type, and the optimal strategy is to install the minimal capacity so that the power price is always lower than a given nonlinear function of the installed capacity, which is characterized by solving an ordinary differential equation deriving from a free-boundary problem.

The paper [2] is a first step in extending this problem to the case when companies are present in the market, and the price impact is due to the cumulative installations of all of them, now with the constraint that the sum of their total installations cannot exceed a given . This problem can be formulated in several mathematical ways, among which the two most well-studied are that of Pareto optimum and Nash equilibrium. The problem of finding a Pareto optimum has been fully solved in [2]. However, the problem of finding a Nash equilibrium is much more technically demanding: [2] presents a verification theorem for the case , which involves a system of variational inequalities, and fully solves only the case when no price impact is present. The aim of this paper is to solve the general case when price impact is present and a Nash equilibrium is reached by two players.

This problem is formulated as a nonzero-sum game of singular control, where the two players control one state variable each (their own cumulative installation) and these two state variables have a cumulative impact on a third one (the electricity price). The typical situation in these games, see e.g. [4, 5, 6, 7], is that the state space, where state variables can take values, is divided in a continuation region common to both players where they do not exercise control and let the system evolve, and two intervention regions, one for each player, where one player intervenes and the other one does not. However, this problem is more general, as the possibility that both players install simultaneously is explicitly present and must be taken into account: for this reason, we should introduce another region, where both players can install simultaneously.

In order to have an intuition of how this generalization should be implemented, we first present a static version of this game where the two players have both only one possibility of installing at the beginning of the game, when they can choose the amount of additional installed capacity, with the constraint that the sum of the resulting total capacities of both players cannot exceed . This characterizes a 3-dimensional state space, which is the Cartesian product of the whole real line (where the power price lies) times the 2-dimensional simplex of size (where installed capacities lie). For a given initial level of power price , the resulting Nash equilibrium can be explicitly characterized, and it requires to divide the 2-dimensional simplex in four regions, one being the no-installation region common to both players, two being the regions where only one of the players installs and the other one stays idle, and a fourth one being the region of joint installation. Depending on the price level , some of these regions could be absent from the corresponding section of the state space, but in general one should take into account the presence of all four of them. While the players’ strategy in the first three regions is analogous to other examples in literature (i.e., each player either does not install, or installs enough power to arrive to the boundary of the common no-installation region), the novelty of this problem is the fourth region where both players install, which in this case is the intersection of a suitable square, depending on the price level , with the simplex. In this region, both players install enough capacity to move their installation from their current state to the upper right corner of the square, net of the constraint on the capacity of the plant. Thus, if this vertex is inside the simplex, then they reach the same level of installed power; however if the vertex is outside of the simplex, then we have a non-uniqueness of Nash equilibria, as any admissible strategy which makes the two installations reach the simplex’s boundary is a Nash equilibrium.

Inspired by this, we pass to the continuous time formulation of our singular game. The first step is to review the verification theorem present in [2] by taking into account a possible non-uniqueness of strategies in the region of joint installation. In particular we select a preferred strategy at saturation by assuming that the players never install when their current level of installed power is greater or equal than . As in [2], this results in two systems of variational inequalities, each one satisfied by the value function of player . The first equation in the system is a variational inequality involving a second order operator in the space variable and a first order operator in : it characterizes a continuation region and an installation region , and has as domain the continuation region of player . The verification theorem in [2] also specifies a variational inequality on the domain , however we find out that it can be replaced by a much simpler first order equation on the variable , thus simplifying the the task of constructing a solution. Moreover, we find out that there is also a loss of smoothness of the value functions from the case of optimal control to the case of games: in fact, we show that there may not exist a solution to the variational problem that is and on , as that would be not compatible, roughly speaking, with the optimality condition on . Therefore we generalize the verification theorem of [2] also in this direction, making use of a weak Itô formula, and allowing the solution to be not smooth on his own free boundary. This loss of smoothness is analogous to what happens e.g. when going from impulsive control to games, see [1] for this result and the relative discussion, or in optimal stopping problems, see [3] and the references therein.

Having established a verification theorem general enough, we are then able to build the solution of the problem, both in terms of solutions , of the system of variational inequalities, as well as in terms of the corresponding free boundaries: since in this case the state space is three-dimensional, the resulting free boundaries are surfaces, in particular parameterized by , . This allows to build the Nash equilibrium strategies in terms of reflected diffusions: these strategies are analogous to the one-player case of [9], i.e. they can possibly jump at the initial time and then they are continuous. More in detail, if the initial state , then only Player makes an instantaneous installation to hit the boundary of . Instead, if , then both players make an instantaneous installation to hit the separation boundary of the 4 regions: after this lump installation, the equilibrium strategy is to have always for all . After this possible initial installation, the equilibrium strategy will always keep the process inside the closure of . In particular, when hits the boundary of , then Player will install; this also includes the case when hits both the boundaries of and simultaneously: this will happen when , in which case both players will install the same amount of capacity in order to keep this equality always satisfied.

The paper is organized as follows. In Section 2 we introduce the general problem of finding a Nash equilibrium between the two players, with all the relative definitions. In Section 3 we restrict the set of admissible strategies to those such that the two players can only perform one initial installation and then they cannot control the system anymore, and derive the relative Nash equilibria, with a possible non-uniqueness on the common installation region . In Section 4 we come back to the general continuous-time game, presenting the relative Verification Theorem and the weak Ito formula used to prove it, and then constructing explicitly the equilibrium strategies.

2 A market with 2 players

Let be a standard one-dimensional Brownian motion on a complete filtered space and denote with a point in and a point in . We assume that, in absence of any companies’ economic activities, the electricity price evolves according to a mean reverting Orstein-Uhlenbeck dynamics

for some constants and .

We consider a market in which two producers, indexed by , operate. The level of installed power of producer is described by the process

| (2.1) |

where is the initial level of installed power, is the total power installed by the two producers within the interval , and each component identifies the company’s control variable. We also assume that the total level of installed power cannot exceed a certain threshold , since, for instance, only a finite real estate is available for the installation of solar panels or wind power plants. Accordingly, the set of admissible controls is given by

| (2.2) |

Notice that each player is constrained, in its strategy, by the installation strategy of the other. Following [9] we assume that the current total level of electricity production, which is proportional to , has a negative effect on the electricity price: its mean level at time is instantaneously reduced by a factor of , for some . Therefore, the spot price evolves according to

| (2.3) |

In this setting, each company aims at maximizing the profit, derived from selling electricity in the market, which for an admissible control is described by the following utility functional

| (2.4) |

where is the discount factor and is the constant representing the cost of installing one unit of power.

2.1 Problem formulation

In [2], the authors considered the cooperative situation of a social planner, where the problem consists of finding an efficient installation control which maximizes the aggregate expected profit, net of investment cost. This is known as a Pareto optimum and is expressed as

Set and , it is straightforward to check that

| (2.5) |

Then the aggregate optimal strategy for the social planner is equivalent to the optimal control for a single player, as investigated in [9]. Such strategy does not characterize the single installations , and it is indeed not unique. Notice as well that the problem can be formulated for players without any modification.

In this paper we look for an equilibrium solution to the competitive game between the two companies, also known as Nash equilibrium. Generally speaking, a Nash equilibrium is an optimal control for both players, in the sense that neither one can improve their profit by changing their control while the other keeps theirs unchanged. To precisely define the Nash equilibrium we will employ in our analysis, we first need to introduce some additional notations as well as the notion of admissible strategy.

Notation 2.1.

We denote by the two-dimensional simplex of size , defined as

| (2.6) |

which corresponds to the set of all possible installed power states. Moreover, for a given , we denote by and the sets of real-valued continuous functions and non-decreasing cadlag functions, respectively, defined on .

Definition 2.2 (Admissible strategy).

A family of Borel-measurable functions such that, for any , there exists a unique such that

| (2.7) |

is called an admissible strategy. The set of all admissible strategies is denoted by .

Definition 2.3 (Nash equilibrium).

A function is called a Nash equilibrium if, for any permutation of and we have:

| (2.8) |

with as in (2.7), for any such that

| (2.9) |

3 One step game

To develop an intuition on how a Nash equilibrium strategy should work and to introduce some key concepts for the subsequent analysis, we first look at the simpler case when both players can install only at time . In this situation an admissible control (equivalently a strategy) for the player is completely determined by the deterministic value

The expected profit can be computed exactly as

| (3.1) |

which is a quadratic function of . Then the equilibrium condition (2.8) of Definition 2.3 can be expressed as follows: the function is a Nash equilibrium if, for any permutation of and , denoted , , , we have

| (3.2) |

where is a linear function of the price at time , precisely

| (3.3) |

3.1 Equilibrium strategies

For the rest of the Section we will denote , . Assume that the player chooses the optimal strategy . Then we look for a strategy given by

| (3.4) |

Then, by a simple derivation of (3.1) it is easy to check that

| (3.5) |

This means that we can characterize by the geometric properties of the locus of points (3.5), depending on , i.e. a linear function of the price. Let us first consider the intersection of the lines

| (3.6) |

which corresponds to the solution to the optimization problem in the absence of constrains. By (3.5) we can make the following preliminary observations:

-

i)

If , then , .

-

ii)

If and , then by (3.5), . This means that, if , the player installs when and saturates the capacity of the system if .

-

iii)

If , then both players do install if .

Let us now visualize both players strategies, depending on the electricity price at time . We may distinguish four cases:

-

i)

: in this situation , , therefore . Roughly speaking, the electricity price is too low to justify any installation.

-

ii)

: in this price interval one or both players may install, depending on the initial condition . However the system will never reach saturation, since

If , , i.e. the intersection point (3.6) corresponds to an admissible strategy, then

Notice that, regardless on the initial level of installed power, both players reach the same level after installation. We will comment again on this later.

If and , by (3.5) we have , and

(3.7) Lastly, if , , then .

-

iii)

: this case is analogous to ii) until , . On this subset we have indeed

and therefore the player must install up to saturating the capacity . Precisely we have

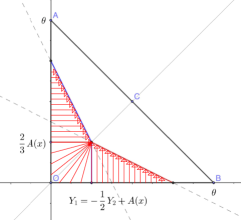

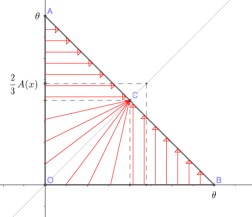

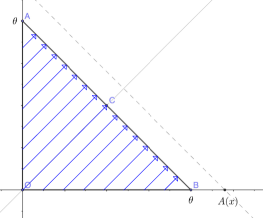

See Figure 1 for a visual representation of cases ii) and iii).

Figure 1: Cases ii) and iii) -

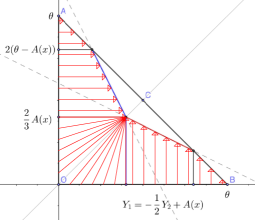

iv)

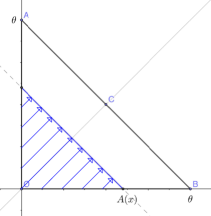

: in this price level, the system always reach a saturation state. Indeed, if , then , otherwise , .

As before, if , then . Otherwise it is straightforward to check that the setcorresponds to

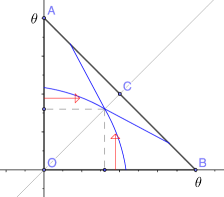

See for instance Figure 2.

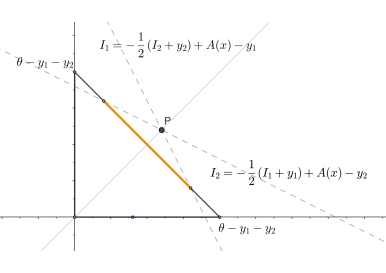

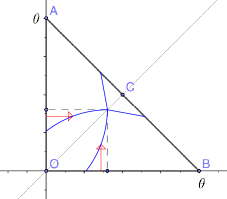

Figure 2: Case iv), saturation at This means that any admissible strategy which saturates the capacity of the system is an equilibrium strategy. In Figure 3 we show two possible strategies at saturation. The strategy a appears to be more regular with respect to , while on the other hand, strategy b is easier to implement. Hereafter will set our analysis to match the latter idea.

Figure 3: Case iv), strategies a and b

The reader can easily check (3.2) through cases i) to iv).

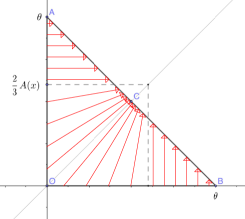

3.2 The free boundary function

Let us examine figure 1 which corresponds to the cases (ii) and (iii) for reference. The set of points highlighted in blue can be interpreted as the level set of a boundary function , separating what we might call the installation and waiting regions for the player 1. Similarly the points in red, with respect to a boundary function . Clearly by the symmetry of the game.

In order to extend the computation above to the dynamic case, it is crucial to understand the structure of these regions and the free boundaries. For any and we put

| (3.8) |

Then we can characterize the waiting region for the player as follows:

| (3.9) |

with

The component matches the choice of strategy b in case iv): indeed player never installs if his current level of installed power is higher than . On the other hand we put

| (3.10) |

In figure 4 we may observe the typical boundary structure on the three dimensional plane.

Finally, let us characterize the strategy and value function with respect to the free boundary and the regions (3.9), (3.10). First, let

| (3.11) |

be the expected profit associated to a non-installation strategy. Then it is clear that

| (3.12) |

Next, we set as

| (3.13) |

We also set as

| (3.14) |

and accordingly, .

With these notations at hand we can characterize the equilibrium strategy as follows: if a player is in its installation region, and is not, then makes an installation , pushing the initial state of the system to the boundary of (therefore ) in the direction constants. If and are both in their installation region, they both make an installation , pushing the state on the boundary of . Therefore, recalling (3.12) we have

| (3.15) |

3.3 Comparison with Pareto optima

The Pareto optimum is an installation strategy which maximizes the aggregate expected profit

Again, this quantity can be computed exactly: denoting and we have

Optimizing w.r.t the cumulative installation we get

| (3.16) |

where is as in (3.3). Clearly, depending on the proportion in which the two players install, there are infinite Pareto optima. However, even in the case and assuming , the Pareto optimum is fundamentally different from the Nash equilibrium: for instance it is easy to see that for the former, the system reaches saturation for , while for the latter the system reach saturation earlier, when .

3.4 Final remarks and ansatz for the general game

Similarly to the one step case, a Nash equilibrium for the general game will keep the state process in the closure of by a possible lump installation at time , and successive infinitesimal installations for . With this in mind, the previous computations provide a good intuition on the structure of the regions and , . On one hand, the cross structure of the boundaries, as well as their monotonicity can be heuristically explained by the principle that the firm which has the least installed power should install before the other. Then, it would be also true that the joint installation region should be a square for every fixed , as seen in Figures 1. Indeed, if that was not the case, then there would be states of the system which are transported to an installation region by any admissible control, see Figures 6 for reference.

4 Continuous game

4.1 HJB free-boundary system and verification theorem

Let us now go back to the original problem. In this section we prove a verification theorem, which characterizes the equilibrium solution of the game.

First, let denote the infinitesimal generator of the diffusion , which is given by the second order operator

| (4.1) |

for , to be specified, and let be the function defined in (3.11), which corresponds to the expected profit of firm when both firms follow a non-installation strategy. Finally, let be a permutation of and consider the variational PDE on the domain :

| (4.2) |

for an open set , together with the boundary condition

| (4.3) |

Definition 4.1 (Admissible boundary).

Let be a permutation of . A real-valued function defined on is called a -admissible boundary if it is continuous and strictly increasing in both single variables.

Remark 4.2.

The restriction of an admissible boundary to the segment is monotonic increasing, i.e.

| (4.4) |

Motivated by the analysis on the one-step problem, we define the waiting and installation regions of the players as follow:

Notation 4.3.

Let be a permutation of . For any -admissible boundary , we set

| (4.5) | ||||

| which corresponds to the graph of the function F. Moreover we set | ||||

| (4.6) | ||||

| (4.7) | ||||

| (4.8) | ||||

| (4.9) | ||||

| (4.10) | ||||

and as

| (4.11) |

where .

We now introduce two reflection operators. Let given by

| (4.12) |

and its extension given by

| (4.13) |

Let also the and be acting, respectively, as

| (4.14) |

Remark 4.4.

Let be a permutation of . If is a -admissible boundary, then is an -admissible boundary and

| (4.15) |

We now introduce a notion of solution that is useful to the resolution of the stochastic game. The idea is that the area is divided into a waiting region and an installation region, determined by a free-boundary function .

Definition 4.5 (General solution to the variational PDE).

Let be a permutation of and be a -admissible boundary. We say that a continuous function is a (general) solution to the variational problem if

-

(i)

and there exists a constant such that

(4.16) -

(ii)

the partial derivative exists and is continuous on and a neighbourhood of . More precisely, there exists such that , with , where denotes the Euclidean ball centred at the origin, with radius ;

-

(iii)

there exists such that

(4.17)

We now introduce the notion of regular solution, which is useful to the resolution of the stochastic game. The idea is that the area is divided into a waiting region and an installation region, determined by a free-boundary function .

Definition 4.6 (Regular solution to the variational PDE).

Let be a permutation of and be a -admissible boundary. We say that a pair is a regular solution to the variational problem if

-

(i)

is a general solution to the variational problem

-

(ii)

is an -admissible boundary

-

(iii)

, and it holds that

(4.18) (4.19) where

(4.20)

Such is called a free-boundary function for .

Remark 4.7.

At this stage, the regularity requirements on may seem convoluted at first sight. For instance, on the waiting region (of player ), one would expect to find second order regularity on the spatial variable, in order for the variational equation to be well defined everywhere as in the single player control setting [9]. However, it is common to observe a loss in regularity when passing from a control setting to the associated games, see discussion in [1], in the context of impulsive games. Similarly, in optimal stopping times it is generally difficult to prove that the value is regular up to the free boundary, see the discussion and examples in [3].

Our requirement are chosen to be somehow the minimal natural ones on in order to prove a verification theorem. In Section 4.3.2 we will further discuss these regularity aspects in the context of the construction of the free boundaries, and importantly, we will show that requiring the second order regularity on would actually prevent us from finding an equilibrium solution. On the other hand we still expect to obtain at least the Lipschitz continuity of the gradient in , which, together with the monotonicity of the boundary , allow us to employ an Itô formula which does not involve local times. As for the regularity in , we require that the second equation in (4.2) is well defined slightly beyond his natural domain .

We are now in the position to state the HJB-system associated to the Nash equilibria of our stochastic game.

Definition 4.8 (Equilibrium solution to the variational PDE).

We say that a pair is an equilibrium solution to VP if is a -admissible boundary and is a regular solution to the variational problem .

Remark 4.9 (Symmetry).

It is straightforward to see that is an equilibrium solution to VP if and only if is a -admissible boundary and is a regular solution to the variational problem .

Notation 4.10.

If is a fixed equilibrium solution to VP, we set

| (4.21) | ||||

| (4.22) |

Definition 4.11 (-optimal strategy).

Let , a -admissible boundary and . A control is called -optimal with respect to and if both the following conditions hold -almost surely:

| (4.23) | ||||

| (4.24) |

and if is continuous with

| (4.25) |

Theorem 4.12 (Verification theorem).

Let be an equilibrium solution to VP. Let also such that, for any and , every control process such that

| (4.26) |

is -optimal w.r.t. and .

Then is a Nash equilibrium and

| (4.27) |

where is the unique admissible control such that

| (4.28) |

in accordance with Definition 2.2.

To prove Theorem 4.12 we need some preliminary results. Lemma 4.13 below guarantees that the value function is smooth outside a set of probability zero. This would be clear if the law of were absolutely continuous with respect to the Lebesgue measure, however the marginal law of is not, a priori, absolutely continuous, and no information is available for the joint law of the process. We we do exploit is the monotonicity of and the fact that is optimal with respect of F. This allows us to prove an ad hoc Itô formula, accounting for the lack of regularity in the proof of the verification theorem.

Lemma 4.13.

Let be a permutation of , let , be an -admissible boundary and a -admissible boundary respectively, and . If is -optimal with respect to and , we have

| (4.29) |

Proof.

We first prove the statement in the control setting of [9]. Assume for the moment that there is one player involved in the game with an initial installed capacity . Assume is a continuous and strictly increasing function and

Assume that the installed capacity evolves according to

| (4.30) |

where

| (4.31) |

In particular, the strategy is optimal with respect to , in the sense that for all and if by construction. When is the free boundary, it corresponds to the optimal control in [9]. Observe now that is bounded. Thus, by Girsanov’s theorem (see [10], Theorem 10.5), there exists an equivalent measure and a Brownian motion , such that the dynamics of is

| (4.32) |

Consider the event

| (4.33) |

Then by (4.31) and monotonicity we have

where the last equality stems from the fact that the random time has an absolutely continuous distribution on . This is a well known fact when is a Brownian motion (see, for instance [8], Chapter 2.8), then it holds for the O-U process (4.32) by a second change of measure. In particular, this show that in the control setting of [9], if is the free boundary and the player acts optimally, then (4.29) holds true. Also note that is the optimal strategy w.r.t which keeps the state closer to the boundary.

Let’s now go back to the two players setting and fix w.l.o.g. Consider

Clearly . Since is 2-optimal we have , then by monotonicity . Thus we have

Finally, we infer

| (4.34) |

again by monotonicity. The RHS of (4.34) can be treated as in the one player case by means of a Girsanov change of probability, yielding . Finally, the case can be treated by comparison principle, using again the monotonicity of . ∎

Lemma 4.14 (Itô formula).

Let be a permutation of , and let , be an -admissible boundary and a -admissible boundary respectively. Let such that conditions (i)-(ii) of Definition 4.5 hold true, and such that . Then, for any , and any -optimal with respect to and , we have

| (4.35) | ||||

| (4.36) |

Remark 4.15.

Note that the regularity conditions (i)-(iii) in Definition 4.6 are sufficient to write (4.35). The j-optimality of guarantees that the process for any so that the partial derivative appearing in (4.35) is well defined. Moreover, when , then by (4.24), so that only need to be well defined in a neighbourhood of . In particular, by the monotonicity of , once the process enters the set it will never leave. Finally, the second order derivative is intended as a weak derivative.

Proof.

Let us fix , and -optimal with respect to and . To ease notation, we will drop the superscripts in the processes and , and fix throughout the proof. Note that, it is not restrictive to assume . Indeed, if , we have

| (4.37) |

where by Definition 4.11. For simplicity, we also assume . The proof of the case is a simpler modification as for any (see Remark 4.15).

Note that (4.24) implies

| (4.38) |

In particular, we have

| (4.39) |

where is the stopping time

| (4.40) |

We also have

| (4.41) |

where is the stopping time

| (4.42) |

Note that .

We first set a regularizing in sequence , obtained by convolution with the standard mollifiers: more precisely

| (4.43) |

where is such that and has unity integral. Next we regularize w.r.t : for we take

| (4.44) |

Then , and are continuous and the derivatives read

| (4.45) | ||||

| (4.46) | ||||

| (4.47) |

By (4.45) we directly infer that, for any compact set

| (4.48) |

Moreover, for any

The crucial point here is the fact that and for any since is increasing in both variables. This observation then allows us to exploit conditions (i)-(iii) of Definition 4.5 for small enough. Therefore it also holds that

| (4.49) |

Analogously, by the monotonicity of we can show that

| (4.50) |

Next we apply the standard Itô formula to . For any set

| (4.51) |

Then we have

| (4.52) | ||||

| (4.53) | ||||

| (4.54) | ||||

| (4.55) |

We now let . Since is continuous we have for all and . Furthermore, in light of (4.48), (4.49) and (4.50) we have, as that

| (4.56) |

as well as

| (4.57) | |||

| (4.58) |

Here again we exploit the fact that the couple for any , as well as outside (cfr. Remark 4.15).Therefore, (4.55) converges in probability to the analogous expression for .

It only remains to let and to infinity: we only check the term in (4.55) which involves the second order derivative , the other ones being simpler. Since , and given that for a.e. by Lemma 4.13, it suffices to show that

| (4.59) |

and exploit the dominated convergence to pass the limit under the integral sign. The uniform bounds (4.59) is easily deduced by the Lipschitz property (4.16). Indeed, by (4.43) we can write

| (by a change of variable) | ||||

Then we have (4.59) with by (4.16). Finally, upon letting in the other terms of (4.55), and we infer that, for any ,

which corresponds to (4.35) P-a.s. by the -optimality of I (cfr. (4.23)-(4.24)). The proof is complete. ∎

Lemma 4.16.

Let be an equilibrium solution to VP and . If is -optimal w.r.t. and for both and , then the following conditions hold -almost surely:

| (4.60) | ||||

| (4.61) | ||||

| (4.62) |

and is continuous with

| (4.63) |

Proof.

Proof of Theorem 4.12.

Step I. For fixed permutation of and , we first prove that

| (4.68) |

for any such that (4.26) holds true. By symmetry, it is enough to consider . For any set

| (4.69) |

and

| (4.70) |

By Lemma 4.14, together with stochastic integration-by-parts formula, we obtain

| (4.71) |

where

| (4.72) | ||||

| (4.73) | ||||

| (4.74) | ||||

| (4.75) | ||||

| (4.76) |

Here, denotes the continuous parts of . By assumption, the control is -optimal in the sense of Definition 4.11. Therefore, by (4.23) and the fact that is a regular solution to , we have

| (4.77) |

As for , employing in particular that is a general solution to , we have

| (4.78) |

where the last equality stems from (4.24). We now study : as is continuous we have

| (4.79) |

where

| (4.80) | ||||

| (4.81) | ||||

| (4.82) |

We have

| (4.83) |

where the last inequality stems from the fact that is a regular solution to and for any . The latter is true since (by (4.25)) and since is increasing in . An analogous argument yields

| (4.84) |

On the other hand, (4.25) yields for any if , and thus

| (4.85) |

Finally, as satisfies the growth condition (iv) in Definition 4.5 and the process , we obtain . Summing up, we proved

| (4.86) |

As is a general solution to to , owing to condition (iv) of Definition 4.5 we obtain

| (4.87) |

Taking the limit as and applying Lebesgue dominated convergence theorem proves (4.68).

Step 2. We prove (4.27), which, together with (4.68), proves that is a Nash equilibrium. By symmetry, it is enough to prove it for .

First note that, by assumption, the control as in (4.28) is -optimal with respect to and for any and . Therefore, by Lemma 4.16 and the fact that is a regular solution to , we obtain

| (4.88) | |||||

| (4.89) |

-almost surely, and

| (4.90) |

Therefore, proceeding as in Step 1 with , the inequalities (4.77) and (4.83) become equalities. Furthermore, the sum in (4.84) is null as is continuous. Then we obtain

| (4.91) |

Passing to the limit as yields (4.27) for and concludes the proof. ∎

4.2 Construction of equilibrium strategies

Let be a fixed equilibrium solution to VP. We construct an associated Nash equilibrium , namely an admissible strategy such that (4.27)-(4.28) holds true. Recalling Notation 4.3 and Notation 4.10, we set

| (4.92) |

For any permutation of , define

| (4.93) |

Theorem 4.17.

Proof.

Remark 4.18.

We complete the section with the Lemmas that appear in the proof of Theorem 4.17.

Lemma 4.19.

For any permutation of and , every control process such that

| (4.98) |

is -optimal w.r.t. and in the sense of Definition 4.11.

Proof.

By symmetry, it is enough to consider the case . Furthermore, to ease the notation, we suppress the explicit dependence on in and .

We first check the continuity of . Note that the process is left-countinuous because by assumption. Therefore, by Lemma 4.20 and by the continuity of , we have that is also left-continuous. Furthermore, we have

| (4.99) | ||||

| (4.100) |

where the last inequality stems from the fact that and that the function is non-increasing (this stems from the fact that is increasing in both variables). On the other hand, by (4.98) one simply has , and thus .

We now prove (4.23) by contradiction. Assume there exists such that, with positive probability,

| (4.101) |

Therefore, we have

| (4.102) |

As is increasing in both variables, we also have

| (4.103) |

By (4.98) and by , we obtain

| (4.104) |

which is a contradiction. To show (4.24), we need to prove that, if , then there exits a (random) such that

| (4.105) |

If the claim is obvious by definition of . Assume then . First note that implies that for sufficiently close to , and thus

| (4.106) |

Furthermore, as is increasing in both variables, we also have

| (4.107) |

Therefore, for sufficiently close to we have , which (by (4.98)) implies .

The reader may check the following property.

Lemma 4.20.

The function defined in (4.92) is globally Lipschitz-continuous.

Proof.

Let be fixed throughout the proof. We have to show that there exists a unique pair , with continuous and càdlàg, satisfying (4.95) and

| (4.109) |

By symmetry, it is enough to consider .

Step 1: pathwise uniqueness. Let be a solution to the system (4.95)-(4.109). By Lemma 4.19, we have that is -optimal w.r.t. and , for both , in the sense of Definition 4.11. This, recalling that we are assuming , implies that

| (4.110) | ||||

| (4.111) |

where is the stopping time defined as

| (4.112) |

Denoting now by a second solution to the system (4.95)-(4.109), by (4.110) we obtain

| (4.113) |

which yields

| (4.114) | ||||

| (4.115) | ||||

| (by Lemma 4.20) | ||||

| (4.116) | ||||

| (4.117) | ||||

Gronwall’s inequlity then yields

| (4.118) |

On the event , we also have

| (4.119) | ||||

| (by (4.111)) | ||||

| (4.120) | ||||

which, by Lemma 4.20, yields

| (4.121) | ||||

| (by (4.118)) | ||||

| (4.122) | ||||

By same argument, estimate (4.122) can be obtained for . Therefore, Gronwall’s inequality yields

| (4.123) |

which concludes the proof of pathwise uniqueness.

Step 2: weak existence. Recalling that is a fixed Brownian motion on a given filtered probability space , we show that there exist a Brownian motion on the same probability space, and a pair satisfying (4.95)-(4.109) with replaced by .

Let be defined as

| (4.124) |

As we are considering , we have

| (4.125) |

To ease notation, we will neglect the explicit dependence on and in all the stochastic processes. Let be the unique solution to the SDE

| (4.126) |

and set

| (4.127) |

Note that is continuous (by Lemma 4.20), non-decreasing and . Set now the stopping time

| (4.128) |

Note that

| (4.129) |

and

| (4.130) |

Define now

| (4.131) |

Owing again to Lemma 4.20, we have that is continuous, non-decreasing and, by (4.129) together with the continuity of , we also have . Finally, for any we can set

| (4.132) |

Note that implies that the process defined above is continuous. Also, (4.130) yields

| (4.133) |

Therefore, a direct inspection shows that the pair satisfies (4.95)-(4.109) with .

Observe now that, by construction, the process is bounded. Thus, by Girsanov’s theorem (see [10], Theorem 10.5), there exists a probability measure under which the process

| (4.134) |

is a Brownian motion. Therefore, the pair satisfies (4.95)-(4.109) with replaced by . This concludes the proof of weak existence for the system (4.95)-(4.109). ∎

4.3 Construction of an equilibrium solution to the HJB system

Assume that is an equilibrium solution to VP; in particular, recalling notations 4.10, is a regular solution to VP and according to Definition 4.6 (4.7) we have

| (4.135) |

Equation (4.135) can be interpreted as a second order ODE parametrized by the vector , for which in (3.11) is a particular solution. Reasoning as in [9], one finds that should correspond to a function

| (4.136) |

where

is a positive and strictly increasing fundamental solution for the homogeneous ODE

and has to be determined, by imposing the minimal regularity required for the value at the boundaries , . Similarly to the one-step case, represents the value of selling permanently units of energy, which is the initial level of installed power, but here we also add the product of and , which may be interpreted as the value of the option to increase the production of energy.

For the rest of the section we consider w.l.o.g. the case . Let us now examine the equilibrium strategy (4.95)-(4.93): practically speaking, when enters the region , the agent pushes the process to the boundary in direction , as to increase his level of installed power by . The associated payoff to this action is the difference between the continuation value starting from the new state and the associated costs of installation . The agent on the other hand would enjoy a payoff given by his continuation value computed at the new state. In particular, if the agent has to restrict his action due to the capacity limit , accordingly the associated payoffs for and would be respectively and . On the other hand, if the process enters , both agents push it to , as to increase their level of installed power by and , up to saturation.

In light of the previous discussion, our candidate value function is defined as follows:

| (4.137) |

4.3.1 Smooth fitting

Next we impose the fitting conditions on and to characterize the function .

Case : On , the graph separates the regions , where we have

| (4.138) |

according to Definition 4.6, and inside . Enforcing the continuity of inside (cfr. point (i) of Definition 4.5) we get

| (4.139) |

with as in (4.136). By (4.136) we get

| (4.140) |

for any . Now let

so that . Then (4.140) provides a differential condition on which reads

| (4.141) |

Case : The graph , separates the regions , where

since solves the (4.2), and inside . Condition (ii) in Definition 4.5 prescribes that the partial derivative should be continuous in a neighbourhood of : we recall that this allows us to apply our version of the Itô formula in the verification Theorem, under the hypothesis that player 2 acts optimally whereas player 1 may not. Thus we should have

| (4.142) |

With similar computations as above, this provides a differential condition on which reads

| (4.143) |

where .

Boundary conditions: Hereafter we set , , the vertexes of the set , and denote with the line segment connecting two points and on , excluding of the endpoints.

Equation (4.141) can be seen as an ODE parametrized by , on for and for . Therefore it is enough to determine an appropriate initial datum on . Conversely equation (4.143) is parametrized by , on for and for . Therefore it is enough to determine an appropriately initial datum on .

By (4.3) we simply have

| (4.144) |

Next we impose that is continuous on . We have

by (4.141). On the other hand, the left derivative is provided by (4.143). Equating the right and left derivatives we infer

| (4.145) |

Equation (4.145), together with the boundary condition characterize the function on and this is enough to characterize on , depending on . Notice that and may still be discontinuous on the lines and respectively, which is to say that the boundary conditions may not attach at the point with regularity. To ensure continuity we provide an additional condition on the value of .

Let the unique solution solution of the ODE

| (4.146) |

that is (4.143), prolonged on . We impose that the directional derivative is continuous on the boundary . Write now:

| (4.147) |

On , we must have

| (4.148) |

by (4.144). Exploiting (4.145) and recalling that we infer

| (4.149) |

and therefore

| (4.150) |

Lastly, we should check that the above condition also guarantees the continuity of on the line : indeed letting be the prolongation of (4.141) on we may write

| (4.151) |

and imposing continuity on we get

| (4.152) |

The above construction, together with the Cauchy-Peano Theorem and the continuity of , on justifies the following statement.

4.3.2 Consistency of the fit conditions

Proposition 4.23.

Proof.

Recalling that , and the function is continuous on , the regularity properties of only depend on the those of and the smooth fitting conditions on and .

Regularity in : On we have that is continuous, therefore by the smooth fitting (4.139) we claim that exists and is continuous on . In particular we have for any . On we formally have

where exists and is continuous on . Therefore we infer that the partial derivative exists and extends with continuity on .

Regularity in : First note that on by construction (cfr. (4.137)). Moreover, by the smooth fitting (4.142), the partial derivative is continuous on . Let now and check the continuity on . By (4.92) we need to distinguish the cases and . If we have two possible regimes:

-

i)

;

-

ii)

.

In the regime (i), the partial derivative is well defined and we have

by (4.139). Since exists and is continuous on , we infer that exists and is continuous on . On , the partial derivative may not be well defined (cfr. (4.92)). However, by (4.144) we have, for every with ,

so that

On the other hand, we have

Recalling (4.141) and (4.144), we can write:

Therefore, recalling the identity , we infer

| (4.153) |

which shows that is continuous on . In the case , we only distinguish the regime:

-

i)

;

Indeed, we have , and therein by construction. Continuity in up to the boundary can be checked as before, exploiting (4.139). Putting everything together we infer that can only be discontinuous at .

Regularity in x: For any , a direct computation shows that

| (4.154) | ||||

| (4.155) |

Let now . We should again take into account the different regimes for if the system is close or far from saturation, arising from the definition (4.92). To motivate the statement, we only show the case with , the other ones being similar. The continuity on the critical points stems from the boundary condition (4.144) and the continuity of (4.92), an be checked as in the computations above. We have:

| (4.156) | ||||

| (4.157) |

where we used again (4.139) in the last equality. This gives the continuity of on . With similar computations we also have

| (4.158) | ||||

| (4.159) | ||||

| (4.160) |

which shows that is not necessarily continuous on . In the same manner, the fitting condition (4.142) guarantees the continuity of on , but not necessarily the continuity of . Let’s take, for instance, , with and . Then we have

| (4.161) | ||||

| (4.162) | ||||

| and similarly | ||||

| (4.163) | ||||

This show that and .

Linear growth and conclusions: The proof is analogous to the one of Proposition 3.2 in [9], we repeat it here for completeness. First, notice that, for any , we have

for some constant independent of . On the other hand, for any , we have

for some other constant independent of . To conclude the proof, it is straightforward to check that the value (4.137) satisfies the equalities in (4.18) with and , as well as for by construction. ∎

Remark 4.24 (Consistency of the fit conditions).

A first reading of the proof (cfr. (4.158) and (4.163))suggests that we could recover the continuity of on the boundary points , by imposing the fitting condition

| (4.164) |

that is to say that the mixed derivative is continuous on . By (4.136) this condition yields

| (4.165) |

which, together with (4.140), allows to derive an explicit expression of on the upper half of the simplex , as function of . Let us denote this function by . We have

| (4.166) | ||||

| (4.168) |

where . Proceeding as in [9], by deriving (4.166) and equating with (LABEL:eq:ste3) it is also possible to infer a differential equation for an appropriate function , characterizing the boundary function in the upper side of the simplex , once an initial condition on and (cfr. notations in the proof of Proposition 4.23) is provided. The initial condition on is directly derived by solving (4.144), while a suitable condition on is not obvious a priori and will be shown below. However, equation (4.144), together with (4.165) and the positivity of the function , yields that is positive at least on . Moreover, by the properties of the fundamental solution it admits the equivalent representation

| (4.169) |

By (4.169), the positivity of and , we infer that the quantity inside the square parentheses should negative. Therefore, taking in particular we find

which turns out to be incompatible with (4.150). Similar inconsistencies arise by reasoning on the lower half of , or when trying to prove the inequalities in (4.18).

More importantly, even if we were to drop condition (4.150), we would still run into issues when trying to prove the inequality on . This can be even checked by simulations, since the relevant quantities and are completely determined on and respectively. Below we explain our reasoning.

First we show how to specify on . Recall that by imposing the continuity of on the bisector we have (4.145). On the other hand, by (4.169) we have

| (4.170) |

where

with

Comparing (4.169) and (4.170) we find, after further lengthy computations

| (4.171) |

where is as before and

Together with the initial condition on given by equation (4.144), (4.171) provides a characterization of , hence on OC. Therefore we can also fully characterize on as solution to (4.143) with initial data on and on . In particular, on we have

| (4.172) |

where by symmetry. Deriving with respect to and letting we get

Therefore we have

and we may check, with the help of a machine, that the RHS is not for , equivalently . Indeed, let us take for simplicity the set of parameters: and and let also take . The value of in , is given by equation (4.144), thus it is the unique root of

which is approximated as for the chosen set of parameters (see Figure 7). Then

We infer that condition (4.164) actually prevents us from finding an equilibrium solution to the variational problem, and that is the main motivation to prove a verification theorem which avoids the use of the regularity of on all the continuation region of the other player. This observations clearly show how much the fitting conditions on and are interconnected and, in general, one must be careful to assume additional regularity on the value function on one side of , so as not to run into inconsistencies with the conditions on the other half.

References

- [1] Aïd, R., Basei, M., Callegaro, G., Campi, L., and Vargiolu, T. Nonzero-sum stochastic differential games with impulse controls: a verification theorem with applications. Math. Oper. Res. 45, 1 (2020), 205–232.

- [2] Awerkin, A., and Vargiolu, T. Optimal installation of renewable electricity sources: the case of Italy. Decis. Econ. Finance 44, 2 (2021), 1179–1209.

- [3] Cai, C., and De Angelis, T. A change of variable formula with applications to multi-dimensional optimal stopping problems. Stochastic Process. Appl. 164 (2023), 33–61.

- [4] Cont, R., Guo, X., and Xu, R. Interbank lending with benchmark rates: Pareto optima for a class of singular control games. Math. Finance 31, 4 (2021), 1357–1393.

- [5] De Angelis, T., and Ferrari, G. Stochastic nonzero-sum games: a new connection between singular control and optimal stopping. Adv. in Appl. Probab. 50, 2 (2018), 347–372.

- [6] Guo, X., Tang, W., and Xu, R. A class of stochastic games and moving free boundary problems. SIAM J. Control Optim. 60, 2 (2022), 758–785.

- [7] Guo, X., and Xu, R. Stochastic games for fuel follower problem: versus mean field game. SIAM J. Control Optim. 57, 1 (2019), 659–692.

- [8] Karatzas, I., and Shreve, S. E. Brownian motion and stochastic calculus, second ed., vol. 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, 1991.

- [9] Koch, T., and Vargiolu, T. Optimal installation of solar panels with price impact: a solvable singular stochastic control problem. SIAM J. Control Optim. 59, 4 (2021), 3068–3095.

- [10] Pascucci, A. PDE and martingale methods in option pricing, vol. 2 of Bocconi & Springer Series. Springer, Milan; Bocconi University Press, Milan, 2011.