Efficient and Accurate Explanation Estimation with Distribution Compression

Abstract

Exact computation of various machine learning explanations requires numerous model evaluations and in extreme cases becomes impractical. The computational cost of approximation increases with an ever-increasing size of data and model parameters. Many heuristics have been proposed to approximate post-hoc explanations efficiently. This paper shows that the standard i.i.d. sampling used in a broad spectrum of algorithms for explanation estimation leads to an approximation error worthy of improvement. To this end, we introduce compress then explain (cte), a new paradigm for more efficient and accurate explanation estimation. cte uses distribution compression through kernel thinning to obtain a data sample that best approximates the marginal distribution. We show that cte improves the estimation of removal-based local and global explanations with negligible computational overhead. It often achieves an on-par explanation approximation error using 2–3 less samples, i.e. requiring 2–3 less model evaluations. cte is a simple, yet powerful, plug-in for any explanation method that now relies on i.i.d. sampling.

1 Introduction

Computationally efficient estimation of post-hoc explanations is at the forefront of current research on explainable machine learning (strumbelj2010efficient; covert2021improving; slack2021reliable; jethani2022fastshap; chen2023algorithms; donnelly2023rashomon; muschalik2024beyond). The majority of the work focuses on improving efficiency with respect to the dimension of features (covert2020understanding; jethani2022fastshap; chen2023algorithms; fumagalli2023shapiq), specific model classes like neural networks (erion2021improving) and decision trees (muschalik2024beyond), or approximating the conditional feature distribution (chen2018learning; aas2021explaining; olsen2022using; olsen2024comparative).

However, in many practical settings, a marginal feature distribution is used instead to estimate explanations, and i.i.d. samples from the data typically form the so-called background data samples, also known as reference points or baselines, which plays a crucial role in the estimation process (lundberg2017unified; covert2020understanding; scholbeck2020sampling; erion2021improving; ghalebikesabi2021locality; lundstrom2022rigorous). For example, covert2020understanding mention “[O]ur sampling approximation for SAGE was run using draws from the marginal distribution. We used a fixed set of 512 background samples […]” and we provide more such quotes in Appendix LABEL:app:motivation-quotes to motivate our research question: Can we reliably improve on standard i.i.d. sampling in explanation estimation?

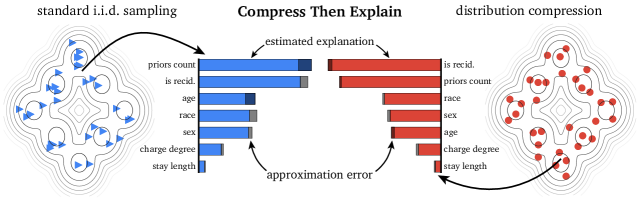

We make a connection to research on statistical theory, where kernel thinning (kt, dwivedi2021kernel; dwivedi2022generalized) was introduced to compress a distribution more effectively than with i.i.d. sampling. kt has an efficient implementation in the compress++ algorithm (shetty2022distribution) and was applied to improve statistical kernel testing (domingo2023compress). Building on this line of work, this paper aims to thoroughly quantify the error introduced by the current sample then explain paradigm in feature marginalization, which is involved in the estimation of both local and global removal-based explanations (covert2021explaining). We propose an efficient way to reduce this approximation error based on distribution compression (Figure 1). We refer the reader to the arguments provided in (herrmann2024position) concerning the added value of conducting such empirical research in machine learning. Namely, the research question is rather open and we aim to gain insight into a previously unexplored area.

Contribution.

In summary, our work advances current literature in multiple ways: (1) Quantifying the error of standard i.i.d. sampling: We bring to attention and measure the approximation error introduced by using i.i.d. sampling of background and foreground data in various explanation methods. (2) Compress then explain: We introduce a new paradigm for estimating post-hoc explanations based on a marginal distribution compressed more effectively than with i.i.d. sampling. (3) Kernel thinning for (explainable) machine learning: We show experimentally that kt outperforms i.i.d. sampling in compressing the distribution of popular datasets used in research on explainable machine learning. In fact, this is the first work to evaluate distribution compression via kt on datasets for supervised learning. (4) Decreasing the computational cost of explanation estimation: We benchmark compress then explain (cte) with popular explanation methods and show it results in more accurate explanations of smaller variance. cte often achieves on-par error using 2–3 less samples, i.e. requiring 2–3 less model evaluations. cte is a simple, yet powerful, plug-in for a broad class of methods that sample from a dataset, e.g. removal-based and global explanations.

Related work.

Our work is the first to empirically evaluate kt on datasets for supervised learning, and one of the first to reliably improve on i.i.d. sampling for multiple post-hoc explanation methods at once. laberge2023fooling propose a biased sampling algorithm to attack the estimation of feature attributions, which further motivates finding robust improvements for i.i.d. sampling. Our research question is orthogonal to that of how to sample perturbations around an input (petsiuk2018rise; slack2021reliable; li2021learning; ghalebikesabi2021locality; li2023glime), or how to efficiently sample feature coalitions (chen2018learning; covert2021improving; fumagalli2023shapiq). Instead of generating samples from the conditional distribution itself, which is challenging (olsen2022using), we explore how to efficiently select an appropriate subset of background data for explanations (hase2021outofdistribution; lundstrom2022rigorous). Specifically for Shapley-based explanations, jethani2022fastshap propose to predict them with a learned surrogate model, while kolpaczki2024approximating propose their representation detached from the notion of marginal contribution. We aim to propose a general paradigm shift that would benefit a broader class of explanation methods including feature effects (apley2020visualizing; moosbauer2021explaining) and expected gradients (erion2021improving).

Concerning distribution compression, the method most related to kt (dwivedi2021kernel) is the inferior standard thinning approach (owen2017statistically). cooper2023cdgrab use insights from kt to accelerate distributed training, while zimmerman2024resourceaware apply kt in robotics. In the context of data-centric machine learning, we broadly relate to finding coresets to improve the efficiency of clustering (agarwal2004approximating; harpeled2004coresets) and active learning (sener2018active), as well as dataset distillation (wang2018dataset) and dataset condensation (zhao2021dataset; kim2022dataset) that create synthetic samples to improve the efficiency of model training.

2 Preliminaries

We aim to explain a prediction model trained on labeled data and denoted by where is the feature space; it predicts an output using an input feature vector . Usually, we assume . Without loss of generality, in the case of classification, we explain the output of a single class as a posterior probability from . We usually also assume a given dataset , where every element comes from , the underlying feature and label space, on which the explanation are computed. Depending on the explanation method, this can be a training or test dataset, and it could also be provided without labels. We denote the dimensional data matrix by where appears in the -th row of , which is assumed to be sampled in an i.i.d. fashion from an underlying distribution defined on . We denote a random vector as . Further, let be a feature index set of interest with its complement . We index feature vectors and random variables by index sets to restrict them to these index sets. We write and for marginal distributions on and , respectively, and for conditional distribution on . We use to denote an empirical distribution approximating based on a data matrix .

Sampling from the data matrix is prevalent in explanation estimation.

Various estimators of post-hoc explanations sample from the data matrix to efficiently approximate the explanation estimate (Appendix LABEL:app:motivation-quotes). For example, many removal-based explanations (covert2021explaining) like shap (lundberg2017unified) and sage (covert2020understanding) rely on marginalizing features out of the model function using their joint conditional distribution

Note that the practical approximation of the conditional distribution itself is challenging (chen2018learning; aas2021explaining; olsen2022using) and there is no ideal solution to this problem (see a recent benchmark by olsen2024comparative). In fact, in (covert2020understanding, Appendix D), it is mentioned that the default for sage is to assume feature independence and use the marginal distribution ; so does the kernel-shap estimator (a practical implementation of shap, lundberg2017unified). This trend continues in more recent work (fumagalli2023shapiq; krzyzinski2023survshap).

Definition 2.1 (Feature marginalization).

Given a set of observed values , we define a model function with marginalized features from the set as .

In practice, the expectation is estimated by i.i.d. sampling from the dataset that approximates the distribution . This sampled set of points forms the so-called background data, aka reference points, or baselines as specifically in case of the expected-gradients (erion2021improving) explanation method defined as

Furthermore, i.i.d. sampling is used in global explanation methods, which typically are an aggregation of local explanations. To improve the computational efficiency of these approximations, often only a subset of is considered; called foreground data. Examples include: feature-effects explanations (apley2020visualizing), an aggregation of lime (ribeiro2016should) into g-lime (li2023glime), and again sage (covert2021improving), for which points from require to have their corresponding labels .

Background on distribution compression.

Standard sampling strategies can be inefficient. For example, the Monte Carlo estimate of an unknown expectation based on i.i.d. points has integration error requiring points for 10 relative error and points for 1 error (shetty2022distribution). To improve on i.i.d. sampling, given a sequence of input points summarizing a target distribution , the goal of distribution compression is to identify a high quality coreset of size . This quality is measured with the coreset’s integration error for functions in the reproducing kernel Hilbert space induced by a given kernel function (muandet2017kernel). The recently introduced kt algorithm (dwivedi2021kernel; dwivedi2022generalized) returns such a coreset that minimizes the kernel maximum mean discrepancy (, gretton2012kernel).

Definition 2.2 (Kernel maximum mean discrepancy (gretton2012kernel; dwivedi2021kernel)).

Let be a bounded kernel function with measurable for all , e.g. a Gaussian kernel. Kernel maximum mean discrepancy between probability distributions on is defined as where is a reproducing kernel Hilbert induced by .

An unbiased empirical estimate of can be relatively easily computed given a kernel function (gretton2012kernel). compress++ (shetty2022distribution) is an efficient algorithm for kt that returns a coreset of size in time and space, making kt viable for large datasets. It was adapted to improve the kernel two-sample test (domingo2023compress).

3 Compress Then Explain (cte)

We propose using distribution compression instead of i.i.d. sampling for feature marginalization in removal-based explanations and for aggregating global explanations. We now formalize the problem and provide theoretical intuition as to why methods for distribution compression can lead to more accurate explanation estimates.

Definition 3.1 (Local explanation based on feature marginalization).

A local explanation function of model that relies on a distribution for feature marginalization. For estimation, it uses an empirical distribution in place of . Examples include shap (lundberg2017unified) and expected-gradients (erion2021improving).

Local explanations are often aggregated into global explanations based on a representative sample from data resulting in estimates of feature importance and effects.

[ht]