Extensions of Panjer’s recursion for mixed compound distributions

Spyridon M. Tzaninis

Department of Statistics and Insurance Science

University of Piraeus

80 Karaoli and Dimitriou str.

185 34 Piraeus

Greece

stzaninis@unipi.gr; bozikas@unipi.gr and Apostolos Bozikas

Abstract.

In actuarial practice, the usual independence assumptions for the collective risk model are often violated, implying a growing need for considering more general models that incorporate dependence. To this purpose, the present paper studies the mixed counterpart of the classical Panjer family of claim number distributions and their compound version, by allowing the parameters of the distributions to be viewed as random variables. Under the assumptions that the claim size process is conditionally i.i.d. and (conditionally) mutually independent of the claim counts, we provide a recursive algorithm for the computation of the probability mass function of the aggregate claim sizes. The case of a compound Panjer distribution with exchangeable claim sizes is also studied. For the sake of completeness, our results are illustrated by various numerical examples.

Compound distributions are widely used in actuarial science for modelling the aggregate claims amount (denoted as ) paid by an insurance company over a fixed period of time. The computation of the probability distribution of is one of the main topics in the field. More formally, the random variable is defined as the random sum , where represents the individual claim sizes and is the random number of claims. Usually, the sequence is assumed to be independent and identically distributed and independent of . Even under these independence assumptions, the determination of can be a difficult task, since one usually has to compute higher order convolutions. Consequently, recursive algorithms are often used for the computation of .

One of the most prominent algorithms in actuarial literature is Panjer’s recursion (see Panjer (1981), Theorem, p. 24), which in the case of discrete claims size distribution simplifies the computation of the probability mass function (abbreviated as pmf) of . Recall that the Panjer class of order , denoted by , is a collection of claim number distributions , satisfying for any and

(1)

(see Hess et al. (2002), p. 283). The members of the aforementioned class have been characterized by Sundt & Jewell (1981) for , Willmot (1988) for and Hess et al. (2002) for a general . Recently, Fackler (2023) proposed a reparametrization for the members of the class for resulting in a more practical and unified representation of the corresponding probability distributions. More general recursive expressions than (1) have also been studied by Hesselager (1994), Schröter (1990), Sundt (1992) and Wang & Sobrero (1994). For an extensive review on recursive formulas for actuarial applications, we refer to Sundt & Vernic (2009) and the references therein.

In the case of inhomogeneous insurance portfolios, mixtures of claim number distributions are considered for modelling the claim counts. Gençtürk & Yiğiter (2016), Gómez-Déniz et al. (2004), Mansoor et al. (2020), Tzougas et al. (2019) and Wang (2011) proposed some (compound) mixed negative binomial distributions with different parametrizations using various mixing distributions. On the other hand, the literature for mixed Poisson and compound mixed Poisson distributions is much more enriched, encompassing, among others, the works of Antzoulakos & Chadjiconstantinidis (2004), Karlis & Xekalaki (2005), Nadarajah & Kotz (2006a, b), Sundt & Vernic (2004), Tzougas et al. (2021) and Willmot (1986, 1987). In particular, recursive formulas have been obtained by Willmot (1993) under the additional assumption that the logarithm of the induced (by the mixing distribution) probability density function can be written as the ratio of two polynomials. Moreover, by adopting the usual independence assumptions, Hesselager (1996) obtained a recursive formula for the computation of .

In actuarial practice, the assumptions of independence among the random variables of and the mutual independence between and are often violated (see among others Albrecher & Boxma (2004), Albrecher & Teugels (2006) and Kolev & Paiva (2008)). In particular, the mutual independence assumption seems to be unrealistic, especially when considering inhomogeneous portfolios. This motivates us to consider a dependence structure among the random variables of and between and . In contrast to the existing notion of compound (mixed) counting distributions, where the sequence is considered to be i.i.d. and mutually independent of (see Grandell (1997), Chapter 8, and Lyberopoulos & Macheras (2019), p. 4), in our case is only conditionally i.i.d. and conditionally mutually independent of . This leads to the concept of mixed compound distributions (see Section 3), which constitute a strong generalization of compound (mixed) distributions.

Under the above framework, this work studies the mixed counterpart of the original class and the corresponding compound distributions, by allowing the parameters of the claim number distribution to be measurable functions of a random vector, the claim size process to be conditionally i.i.d. and conditionally mutually independent of . The above assumptions allow for a (possible) correlation (positive or negative) between and , as well as correlation among the random variables of . In addition, we consider the case of compound Panjer distributions with exchangeable claims. Henceforth, we denote by the mixed Panjer class, where is a -dimensional () random vector (also referred as structural parameter).

The rest of this paper is organized as follows. Section 2 provides a characterization for the members of class in terms of regular conditional probabilities, and a recursive algorithm for the computation of their pmfSection 3 studies the probabilistic aspects of mixed compound distributions. Section 4 presents a recursive algorithm for the computation of in the case that and the claim size distribution is concentrated on . Numerical applications are also given in Section 4, whereas Section 5 concludes the paper.

2. The class of mixed Panjer claim number distributions

and stand for the natural and the real numbers, respectively, while and . If , then denotes the Euclidean space of dimension . Given a topology on a set , write for its Borel -algebra on , i.e., the -algebra generated by . Also and , where with , are the Borel -algebras of subsets of and , respectively. For a non-empty set , denote by and by its indicator function and its power set, respectively. Also, for a map and a non-empty set , write to denote the restriction of to . Given two measurable spaces and , as well as a --measurable map , denote by the -algebra generated by .

Throughout what follows is an arbitrary probability space and is a random variable on taking values in a subset of containing .

Sundt & Jewell (1981) proved that the only non-degenerate members of the original Panjer class of claim number distributions are the Poisson, the binomial and the negative binomial distributions (see Sundt & Jewell (1981), Theorem 1). These distributions will be referred as basic claim number distributions. Since the members of satisfy the recursive condition (1), an interesting question is whether their mixtures also satisfy a recursive relation. The previous question traces back to Sundt (1992), but for a more general family of claim number distributions, where it seems not to have a definite answer.

A way to model the mixtures of claim number distributions is to assume the existence of a random variable (or more generally of a random vector) on with values in , such that the conditional distribution of given satisfies condition -almost surely (written a.s. for short), where is a conditional distribution (cf., e.g., Lyberopoulos et al. (2019), p. 455, for the definition of a conditional distribution). A claim number distribution that satisfies the previous condition is said to be a mixed claim number distribution. This motivates us to provide the following definitions within the class of mixed claim number distributions.

Definitions 2.1.

Let be a -dimensional random vector with values in . A random variable is distributed according to:

(a) the mixed Poisson distribution with structural parameter (written MP for short), where is a --measurable function, if

for any ;

(b) the mixed binomial distribution with structural parameters and (denoted by MB for short), where and are -- and --measurable functions, respectively, if

for any -a.s.. In particular, if or is degenerate, simply write MB () or MB (), respectively;

(c) the mixed negative binomial distribution with structural parameters and (written MNB for short), where and are -- and --measurable functions, respectively, if

for any . In particular, if or is degenerate, simply write MNB () or MNB (), respectively.

In what follows, unless stated otherwise, is a -dimensional random vector with values in and and are as in Definitions 2.1.

Definition 2.2.

A claim number distribution belongs to the class if, the conditional distribution of given satisfies for every the condition

(2)

where and are real-valued -measurable functions.

Remarks 2.3.

(a) In the special case , where denotes the Dirac measure concentrated on , the class coincides with the original Panjer class of claim number distributions.

(b) Recursive formulas for mixed claim number distributions can be found also in Gerhold et al. (2010), Lemma 5.7, but in a different context from condition (2). More precisely, these recursive formulas arise from a change of distributions technique for the mixing distribution.

Since the definition of involves conditioning, it is natural to expect that the notion of regular conditional probabilities (also known as disintegrations) will play a crucial role in order to avoid trivialities and to treat conditioning in a rigorous way. The following definition is a special instance of Fremlin (2013), Definition 452E, appropriately adapted for our purposes (see also Lyberopoulos & Macheras (2021), Definition 3.1).

Definition 2.4.

Let be a probability space. A family of probability measures on is called a regular conditional probability (written rcp for short) of over if

(d1)

for each the map is -measurable;

(d2)

for each .

If is an inverse-measure-preserving function (i.e., for each ), an rcp of over is called consistent with if, for each , the equality holds for -almost all (written a.a. for short) .

The following result is taken from Lyberopoulos & Macheras (2012), and serves as a basic tool for the proofs of the upcoming results. In order to present it, denote by the function composition operator.

Lemma 2.5.

(Lyberopoulos & Macheras (2012), Lemma 3.5) Let be a probability space and be an inverse-measure-preserving function. Put and suppose that an rcp of over consistent with exists. Then, for each and the following hold true:

(i)

-a.s., where is a --measurable function such that is defined on ;

(ii)

.

Henceforth, is an rcp of over consistent with . For any and , set .

Remarks 2.6.

(a) The use of rcp’s in applied probability has been criticized mainly due to the fact that their existence is not always guaranteed (cf., e.g., Stoyanov (2013), Subsection 2.4). However, if is countably generated and is perfect (see Fremlin (2013), 451A(d), for the definition of a perfect measure), then there always exists an rcp of over consistent with every inverse-measure-preserving function from into , provided that is also countably generated (see Faden (1985), Theorems 6 and 3). Note that the most important applications in actuarial science are still rooted in the case that is a Polish space (cf., e.g., Cohn (2013), p. 239, for its definition), where such rcp’s always exist. In particular, and are typical examples of Polish spaces appearing in applications (see also Lyberopoulos & Macheras (2021), Remark 3.2). For an excellent review on rcp’s and their applications, we refer the interested reader to Chang & Pollard (1997).

(b) Each of the probability measures of the corresponding rcp can be interpreted as a version of the conditional probability , which is well-defined, up to an a.s. equivalence, as a function of , while the consistency of with can be interpreted as the concentrating property for any of conditional probabilities.

(c) Assume that is a positive random variable and let be a mixed claim number distribution. If the map is increasing (resp. decreasing) for -a.a. , then the random variables and are -positively (resp. negatively) correlated.

In fact, assume first that the map is increasing for -a.a. . By applying Lemma 2.5, we get that , implying together with Schmidt (2014), Theorem 2.2, and Lemma 2.5, that ; hence and are positively correlated. The proof for a decreasing map is similar.

It is natural to ask which are the members of Panjer, and if they can be characterized in terms of the basic claim number distributions. By applying Lemma 2.5, the next result yields a characterization for the members of the class via rcp’s, connecting in this way the defining property of the original Panjer class and of its mixed counterpart. This characterization also serves as a useful tool for proving the results presented throughout the paper.

Proposition 2.7.

The following statements are equivalent:

(i)

;

(ii)

for -a.a. .

Proof.

Fix on arbitrary and . Statement (i) is equivalent to

which is equivalent to statement (ii). This completes the proof.

∎

Remark 2.8.

In other words, Proposition 2.7 demonstrates that a claim number distribution is an element of if and only if it is a mixture of a -basic claim number distribution. The next table summarizes the members of the mixed Panjer family.

Table 1. The members of and their corresponding functions and .

0

Recall that the so-called Neyman Type A distribution arises as a mixed Poisson distribution with Poisson distributed structure parameter (cf., e.g., Johnson et al. (2005), Section 9.6 for more details). The next example presents a recursive formula for such a mixture of distributions (see also Beal (1940), condition (4)) by applying the characterization appearing in Proposition 2.7.

Example 2.9.

Let and take with (). Fix an arbitrary . Applying Proposition 2.7, along with Lemma 2.5, yields

which implies

The initial value for the recursion is given by the formula

Remark 2.10.

In the case that is mixed Poisson distributed with structure distribution , i.e.,

(cf., e.g., Lyberopoulos et al. (2019), Definitions 3.1(b)), Willmot (1993) and Hesselager (1996) have provided some important results concerning recursive formulas, under the additional assumption that the logarithm of the mixing density can be written as the ratio of two polynomials. However, these results cannot, in general, be transferred to the class of MP, as it is not always possible given an arbitrary probability space and a probability distribution to construct a random variable on , such that (see Lyberopoulos & Macheras (2021), Remark 4.5). Even if one assumes the existence of , it is not, in general, possible to construct an rcp of over consistent with (see Lyberopoulos et al. (2019), Examples 4 and 5). Nevertheless, for the most interesting cases appearing in applications, there exist a random variable such that and an rcp of over consistent with (see Lyberopoulos & Macheras (2013), Theorem 3.1, and Lyberopoulos et al. (2019), Examples 1, 2 and 3).

It is evident that if , then by applying Proposition 2.7 we get

For various choices of the functions and (see Table 1), we can obtain recursive formulas for the computation of the probabilities , see e.g., Gómez-Déniz et al. (2004), Willmot (1993) and Wang (2011). However a unified formula for these recursions does not exist in the literature; hence a question that naturally arises is whether we can obtain a recursion of the form

where , for the members of . The next theorem introduces an appropriate rcp of over consistent with in order to obtain such a recursive formula.

Theorem 2.11.

Let . There exists a family of probability measures on defined by means of

being an rcp of over consistent with , such that for any and , the condition

holds true, where

Proof.

Fix on an arbitrary and define the set-function by

A standard computation justifies that is a probability measure on . Let be fixed, but arbitrary. First note that condition (d1) holds since the map is clearly -measurable while condition (d2) follows from

hence the family of probability measures is an rcp of over . The consistency of follows immediately by the definition of .

As and is an rcp of over consistent with , we can apply Proposition 2.7, together with Lemma 2.5, to get that

(3)

But since

where the second equality follows by Lemma 2.5, we obtain

The latter together with condition (3) completes the proof.

∎

In the next set of examples, we apply Theorem 2.11 in order to obtain recursive formulas for the pmf of a mixed counting distribution that belongs to . In our first example, we revisit the case of the mixed Poisson distribution.

Example 2.12.

Fix an arbitrary and let . Since is an element of with and (see Table 1), we apply Theorem 2.11 to get

Setting (), the latter equality becomes

(4)

where notation stands for the -th order derivative of a real-valued function . Note that the initial value for the recursion is

In particular, let , , where by is denoted the identity map on , and consider the gamma distribution with parameters (written Ga for short) defined as

where denotes the restriction to of the Lebesgue measure on . Take (), where with . Since

it follows easily that

where , and denotes the ascending factorial (cf., e.g., Johnson et al. (2005), p. 2); hence condition (4) yields the recursive formula

(5)

with initial value

(6)

In the special case and , conditions (5) and (6) yield

which is the usual negative binomial recursion (see Panjer (1981), p. 23).

Now take , and . For this particular case we get

implying that the structural parameter is distributed according to the Lindley distribution (cf., e.g., Ghitany et al. (2008) for the definition and its basic properties). Conditions (5) and (6) give

The next example presents a general recursive formula for the () distribution. As a special case, we obtain a well-known recursive formula for the negative hypergeometric distribution (cf., e.g., Johnson et al. (2005), Section 6.2.2, for the definition and its properties) appearing in Hesselager (1994), Example 3.

Example 2.13.

Letting (), we fix on an arbitrary . Since with and (see Table 1), we can apply Theorem 2.11 to get

(7)

In this case, the initial value is given by

In particular, let , let and take for (cf., e.g., Schmidt (2012), p. 179, for the definition of the beta distribution). An easy computation yields

Similarly to the previous example, in the next one we treat the case (). As a special instance, a well-known recursion for the generalized Waring distribution (cf., e.g., Johnson et al. (2005), Section 6.2.3, for the definition and its properties) is rediscovered (see Hesselager (1994), Example 4).

Example 2.14.

Let , where , and fix on arbitrary . As with and (see Table 1), apply Theorem 2.11 to get

Let be a sequence of random variables on with values in , and consider the random variable on taking values in , defined by

The sequence and the random variable are known as the claim size process and the aggregate claims size, respectively. Recall that a sequence of random variables on is:

(i)

-conditionally (stochastically) independent given , if for each with

whenever are distinct members of and ;

(ii)

-conditionally identically distributed given , if

whenever , and .

For the rest of the paper, we simply write “conditionally” in the place of “conditionally given ” whenever conditioning refers to , and, unless otherwise stated, is a sequence of -conditionally i.i.d random variables, and -conditionally mutually independent of .

Denote by either the Lebesgue measure on or the counting measure on , and for any let

where is the probability (density) function of with respect to . Since is an rcp of over consistent with , it follows by Lyberopoulos & Macheras (2022), Lemma 3.2, that the latter is equivalent to

Remark 3.1.

If is non-degenerate and if , then the random variables , with are -positively correlated.

In fact, for any such that , we get

where the first equality follows by Tzaninis & Macheras (2023), Remark 2.1, while the second one follows since is -conditionally i.i.d.; hence .

The next proposition provides an expression for the probability distribution of a sum of -conditionally i.i.d. random variables.

Proposition 3.2.

If for any , then

where denotes the -th convolution of with itself.

Proof.

Fix on arbitrary . For any and , the consistency of with , along with Lemma 2.5, yields

But since is -conditionally i.i.d., it follows by Lyberopoulos & Macheras (2022), Lemma 3.4(ii), that is -i.i.d. for -a.a. , implying that

(9)

hence for , we get

which completes the proof.

∎

The next example shows how Proposition 3.2 can be utilized in order to compute convolutions in the case of -conditionally i.i.d. random variables.

Example 3.3.

Let and fix on arbitrary . Assume that -a.s. and with . Since by Lyberopoulos & Macheras (2022), Lemma 3.4(ii), the claim size process is -independent and for -a.a. , we deduce that for -a.a. . Now, by applying Proposition 3.2, we get

for any , implying

i.e., is distributed according to the generalized Pareto distribution (cf., e.g., Willmot (1993), p. 118). Note that since each is -conditionally exponentially distributed and is gamma distributed, it follows easily that each is Pareto distributed with parameters and (cf., e.g., Schmidt (2012), p. 180 for the definition of the Pareto distribution).

The following definition is in accordance with the definition of mixed compound Poisson processes in Lyberopoulos & Macheras (2021), p. 780 and Lemma 3.3.

Definition 3.4.

The aggregate claims distribution is a mixed compound distribution, written for brevity, if is a mixed claim number distribution and the sequence is -conditionally i.i.d. and -conditionally mutually independent of .

In particular, if for some , then reduces to a compound distribution, written for short (cf., e.g., Schmidt (2012), p. 109).

Remark 3.5.

Assume that is a positive random variable and let . If the maps and have the same (resp. different) monotonicity for -a.a. , then the random variables and are -positively (resp. negatively) correlated.

In fact, assume first that the maps and have the same monotonicity for -a.a. . By applying Lemma 2.5 we get that , implying together with Schmidt (2014), Theorem 2.2, and Lemma 2.5, that ; hence and are positively correlated. The proof when the maps and have different monotonicity, for -a.a. , is similar.

The following characterization of mixed compound distributions in terms of consistent rcp’s allows us to eliminate conditioning via a suitable change of measures, and to convert a mixed compound distribution into a compound one with respect to the probability measures of the corresponding rcp.

Proposition 3.6.

The following statements are equivalent:

(i)

;

(ii)

for -a.a. .

Proof.

Statement (i) is equivalent to the facts -a.s., is -conditionally i.i.d. and -conditionally mutually independent of . Due to Lyberopoulos & Macheras (2022), Lemmas 3.2, 3.3 and 3.4(ii), we equivalently get that , that and are -mutually independent and that is -i.i.d., respectively, for -a.a. , which is equivalent to (ii).

∎

The characterization appearing in Proposition 3.6 allows the extension of well-known results for compound distributions to their mixed counterpart. In the next result, we present a formula for the probability distribution of in the case .

Corollary 3.7.

If , then

Proof.

Since , apply Proposition 3.6 to get for -a.a. ; hence by Schmidt (2012), Lemma 5.1.1, we obtain

The latter, together with Lemma 2.5, completes the proof.

∎

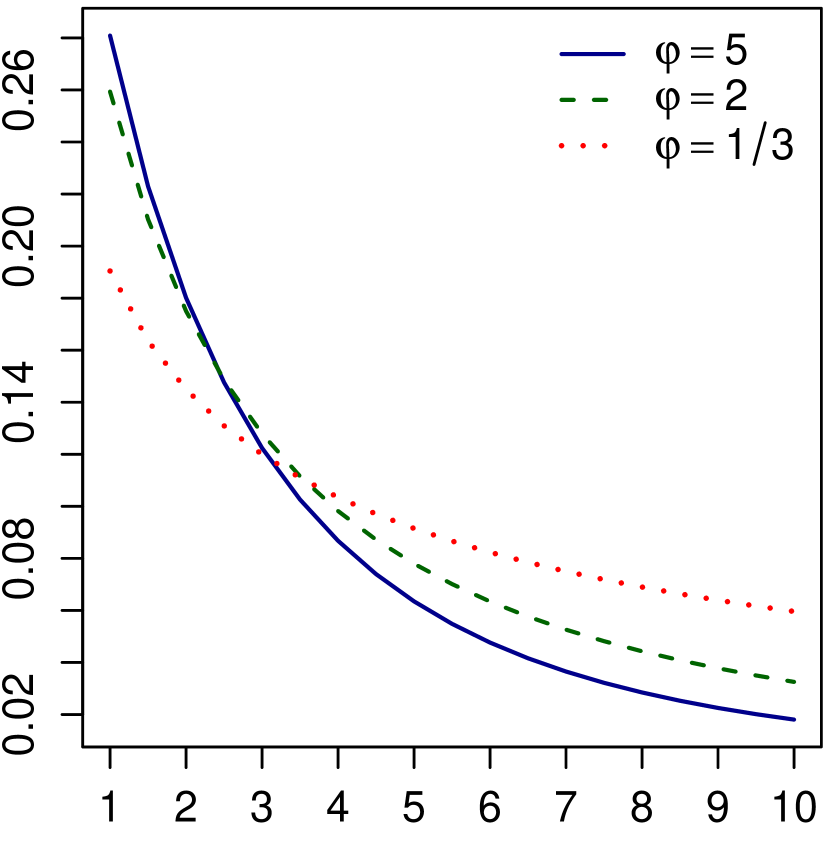

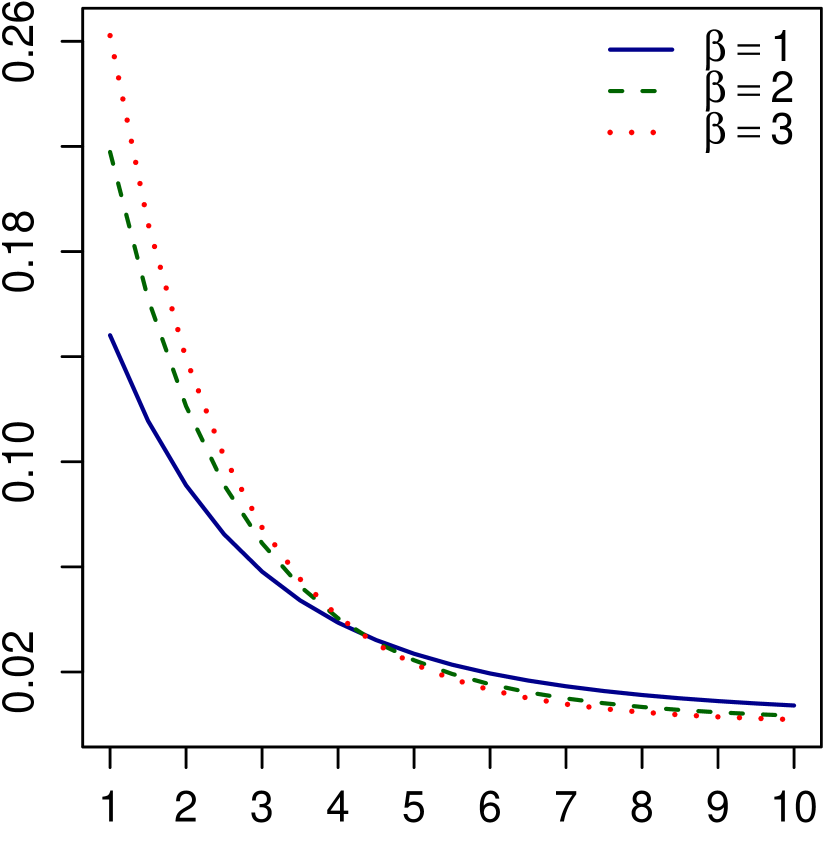

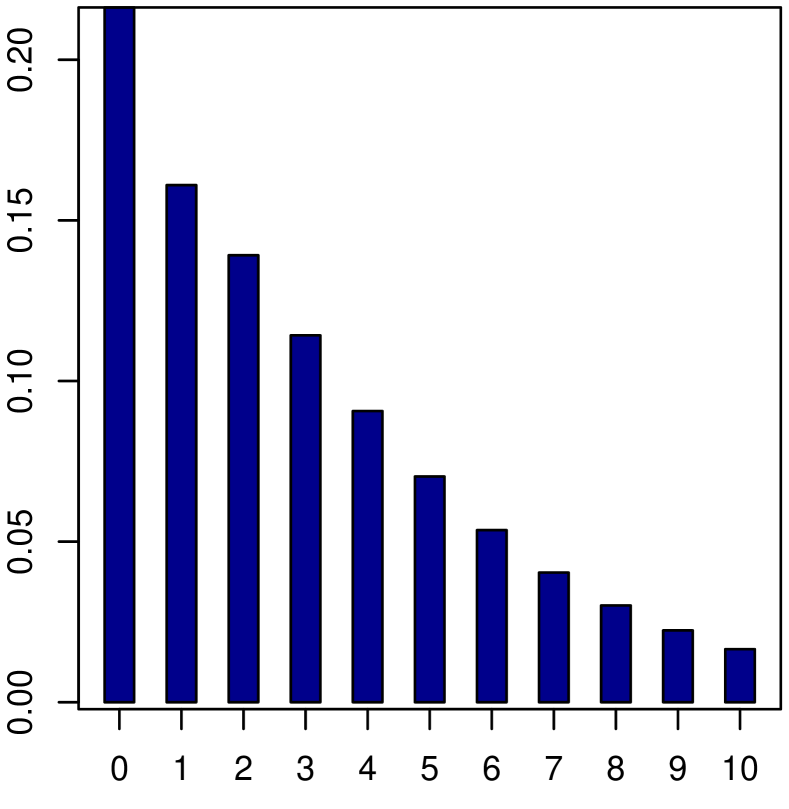

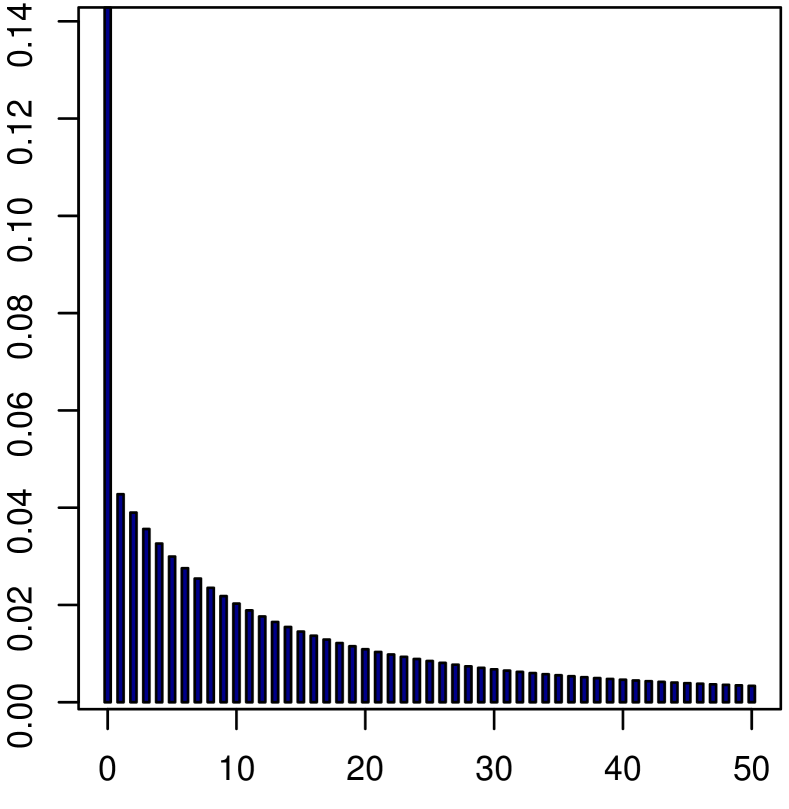

Denote by the probability (density) function of the random variable with respect to . The next example presents an explicit formula for the tail probability in the case of a mixed compound geometric distribution with conditionally exponentially distributed claim sizes.

Example 3.8.

Let with and -a.s., where is a --measurable function. By Proposition 3.6, we get that with and for -a.a. . An easy computation yields

hence

(10)

In particular,

(a) if , and , then condition (10) can be rewritten as

Figure 1 displays the tail probability in the case that the random variable is distributed according to the Inverse Gaussian distribution with parameters (written IG for short), i.e.,

iIG

iiIG

Figure 1. The tail probability for different values of and .

Note that this particular selection for and has also been adopted in a regression context by Tzougas et al. (2019);

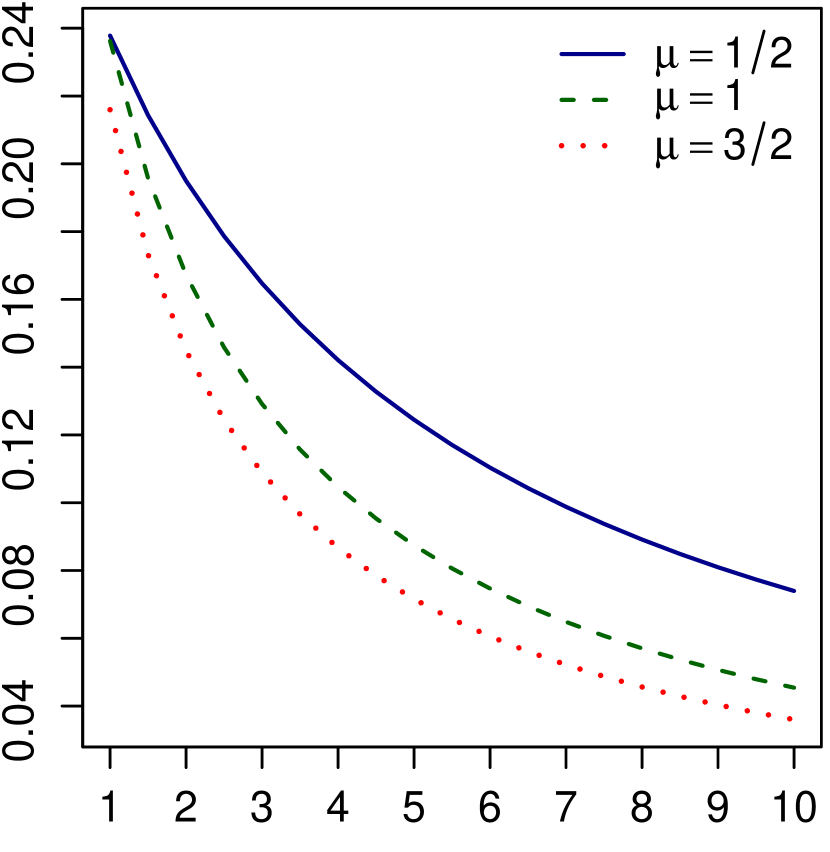

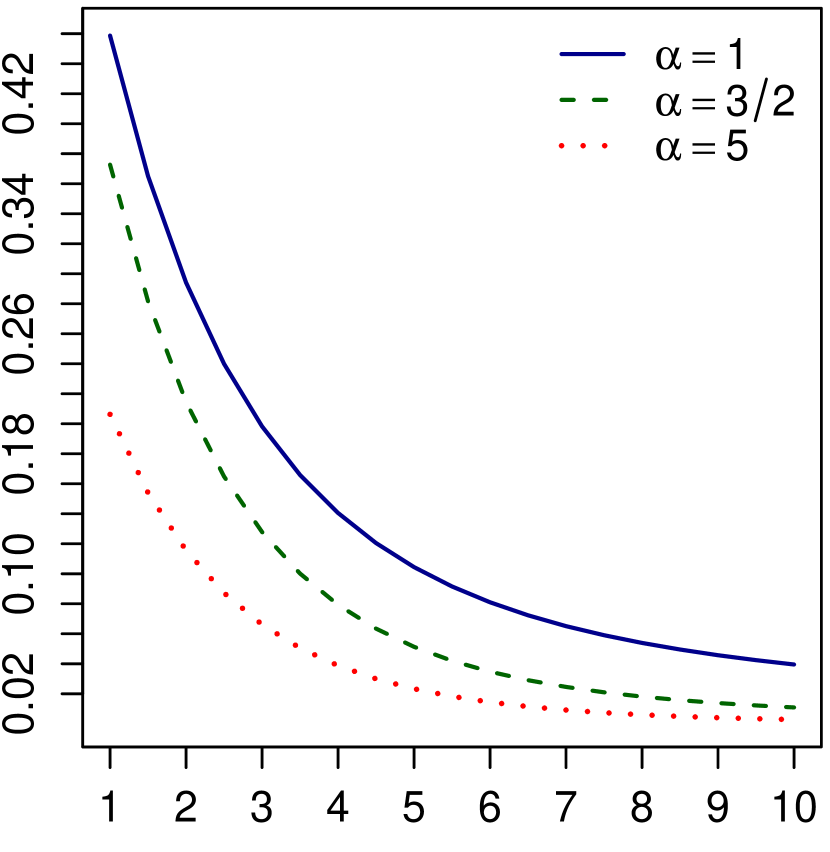

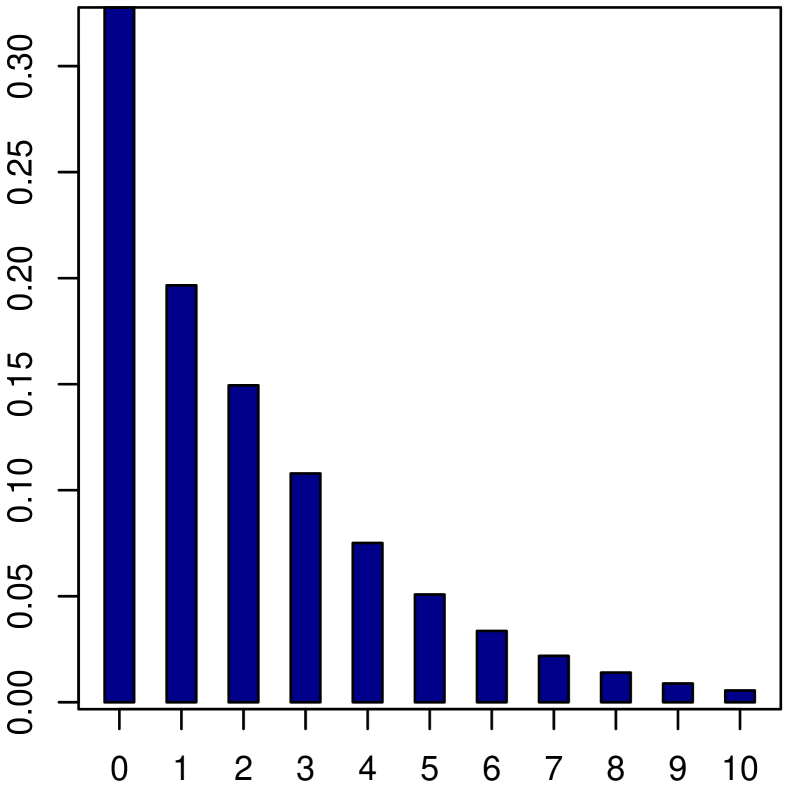

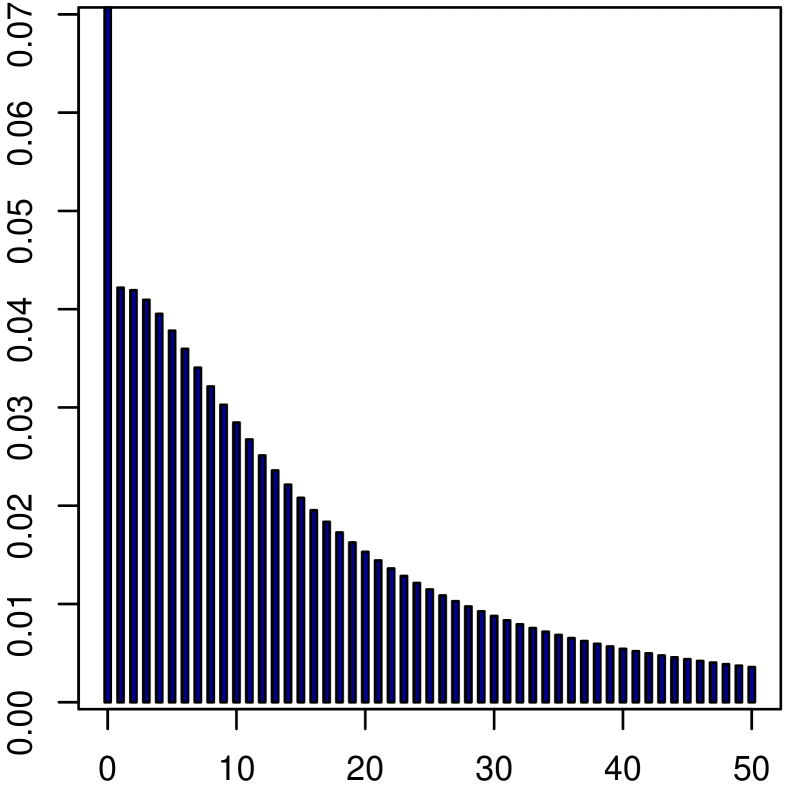

(b) Analogously, if , , then condition (10) becomes

Figure 2 depicts the tail probability in the case , where .

iGa

iiGa

Figure 2. The tail probability for different values of and .

Note that a similar mixture for has been studied by Gençtürk & Yiğiter (2016);

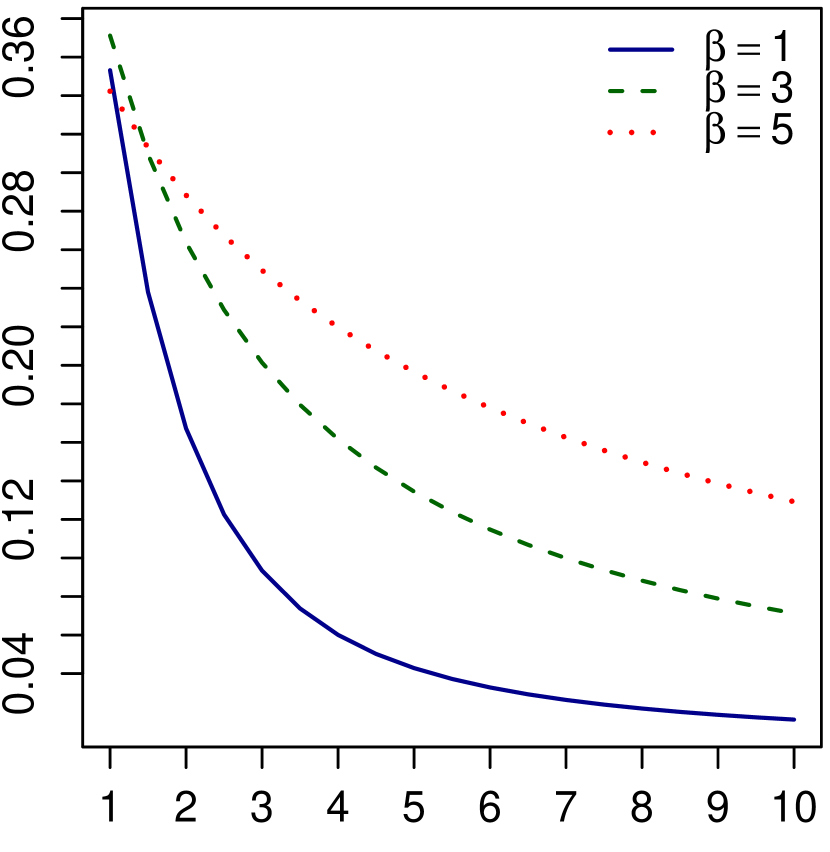

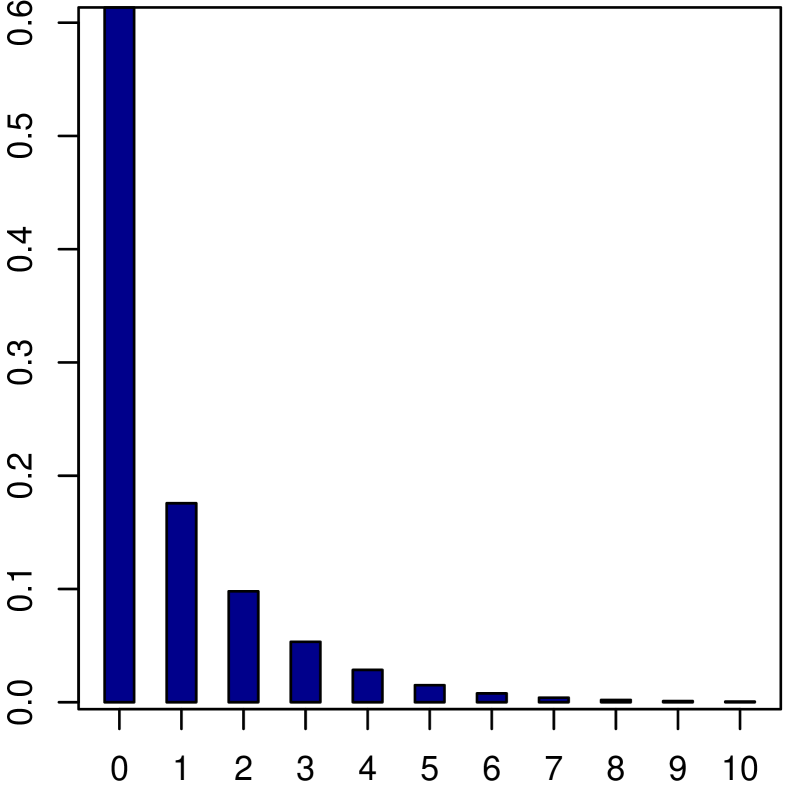

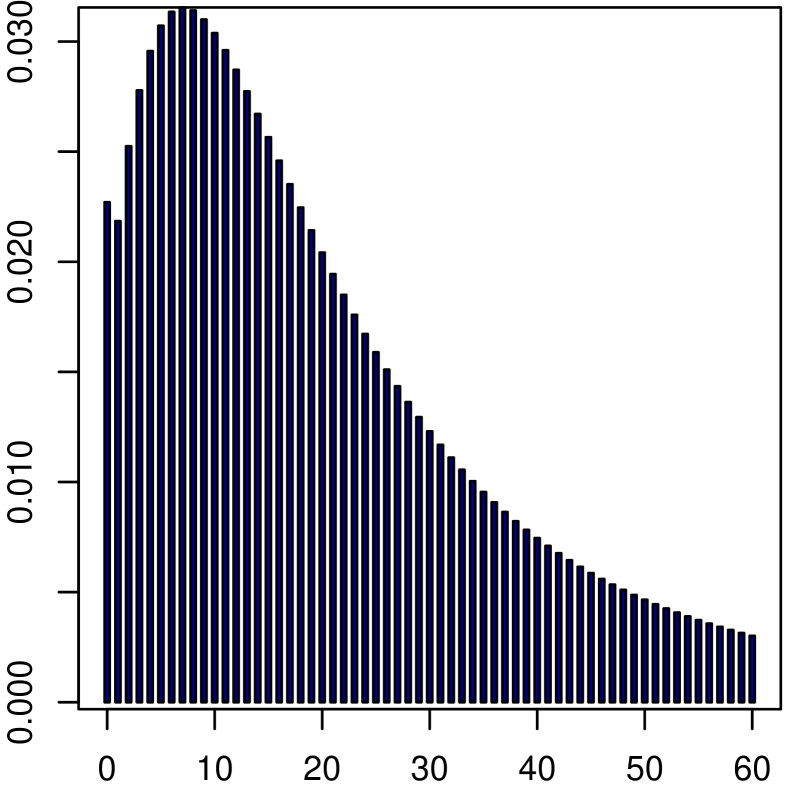

(c) Now, let , and . In this case, condition (10) can be rewritten as

Figure 3 illustrates the tail probability in the case , where . Note that such a mixture for has been considered by Wang (2011).

iBe

iiBe

Figure 3. The tail probability for different values of and .

4. Recursive formulas for mixed compound distributions

Throughout what follows in this section, unless stated otherwise, with and .

Since in the collective risk model the random variable represents the total claim amount paid out from an insurance company over a fixed period of time, the determination of its pmf is of great importance. However, even in the classical case where is -i.i.d. and are -mutually independent, it is difficult to obtain a closed form for the pmf of , which usually involves the computation of higher-order convolutions, a task that may be proven difficult, or at least time consuming. As a consequence, actuaries usually resort to recursive expressions, which seem to be more convenient and computationally efficient.

In the next result, we obtain a recursive formula for the pmf of by extending the famous Panjer recursion (cf., e.g., Schmidt (2012), Theorem 5.4.2) to the class . In order to present it, we denote by the conditional probability generating functions of , i.e., for any with .

Theorem 4.1.

There exists a family of probability measures on defined by

being an rcp of over consistent with , such that

where

for any and .

In particular, if -a.s. then

where

for any and .

Proof.

Fix on arbitrary and define the set-function by

By applying similar arguments to those appearing in the proof of Theorem 2.11, it follows easily that the family is an rcp of over consistent with . Furthermore, first note that condition is an immediate consequence of Corollary 3.7 for . By Lyberopoulos & Macheras (2022), Lemmas 3.4(ii) and 3.3, the sequence is -i.i.d. and are -mutually independent for -a.a. , respectively. Since , Proposition 2.7 implies that for -a.a. ; hence we may apply Schmidt (2012), Theorem 5.4.2, to get

where denotes the pmf of with respect to . The latter, together with Corollary 3.7 and Lemma 2.5, yields

(11)

But since

where the second equality follows by Lemma 2.5, we easily get that

(12)

for any . Conditions (11) and (12) complete the first part of the proof.

In particular, first note that if -a.s., then -a.s.. The latter, along with conditions (11) and (12), completes the proof.

∎

Remark 4.2.

Assume that is absolutely continuous with respect to the Lebesgue measure on . By applying the characterization appearing on Proposition 3.6 in conjunction with Panjer (1981), Theorem on p. 24, we can easily prove the equality

(13)

for any . The integral equation (13) has to be solved numerically, however its implementation presents some serious difficulties (see Gómez-Déniz et al. (2004), p. 42). The proof of a recursion for in the spirit of Theorem 4.1 and its implementation is the subject of a forthcoming paper.

Remark 4.3.

If and are -independent, it follows by Lemma 2.5 that -a.s.. Hence Theorem 4.1 gives

where for any and .

Recall that a sequence of random variables on is called exchangeable, if the joint distribution of the sequence is invariant under the permutation of the indices (cf., e.g., Fremlin (2013), 459C). In non-classical Risk Theory, the concept of exchangeability seems to be an appealing way to introduce a dependence structure between the claim sizes. Actually, exchangeability can be a natural assumption in the risk model context (see Albrecher et al. (2011), Remark 2.7). Note that by Lyberopoulos & Macheras (2022), Proposition 4.1, we get that a sequence is exchangeable under if and only if there exists a random vector such that is -conditionally i.i.d. over .

Corollary 4.4.

Let be the family of probability measures constructed in Theorem 4.1. If and , are -independent then

where for any and .

The proof follows immediately by Theorem 4.1 and therefore it is omitted.

The following example shows that if , then the claim number distribution, for example in the case of an Excess of Loss reinsurance, remains in the same class, but with different parameters (cf., e.g., Schmidt (2012), p. 108).

Example 4.5.

Let be a --measurable function and set for any . Fix an arbitrary and define the function by for any . For an arbitrary, but fixed , set . Define the real-valued function on by and the sequence . Clearly is -conditionally i.i.d. and -conditionally independent of with . Consider the random sum . It then follows by Theorem 4.1 that

where

The latter, along with the fact that is a claim number distribution (cf., e.g., Schmidt (2012), Theorem 5.1.4), implies that , where and .

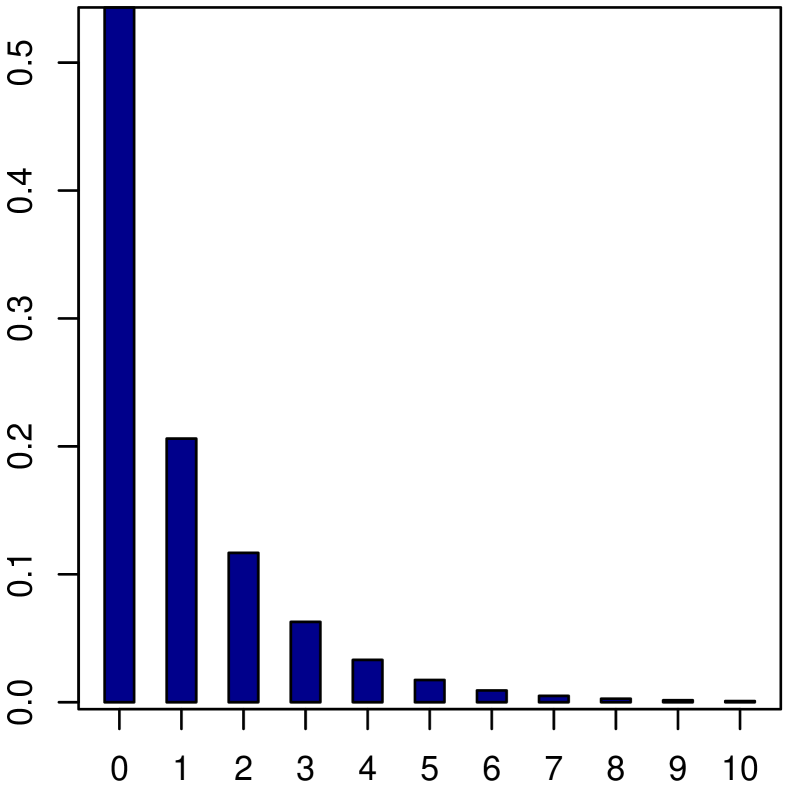

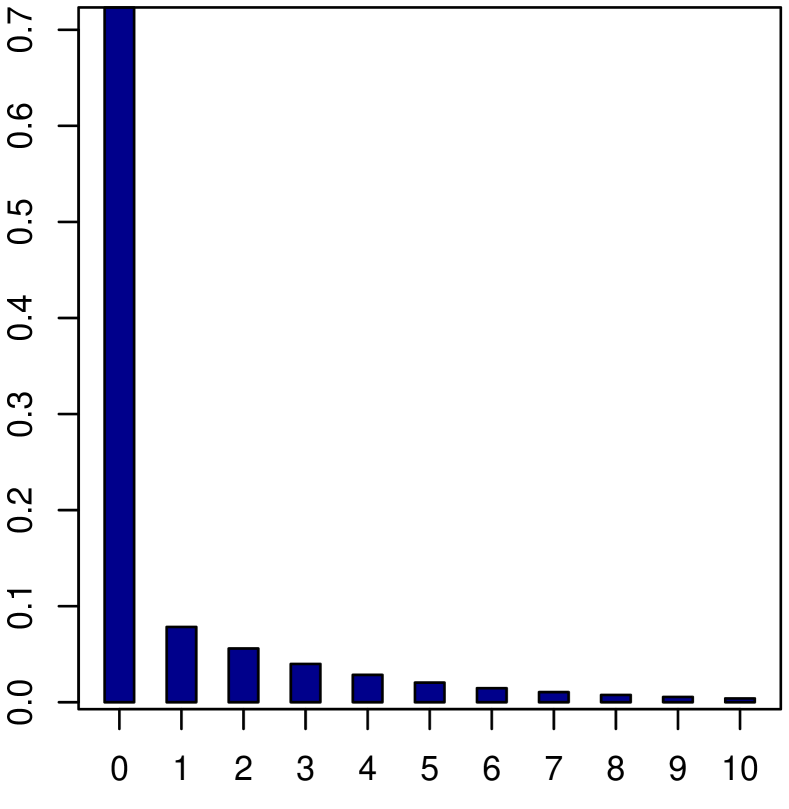

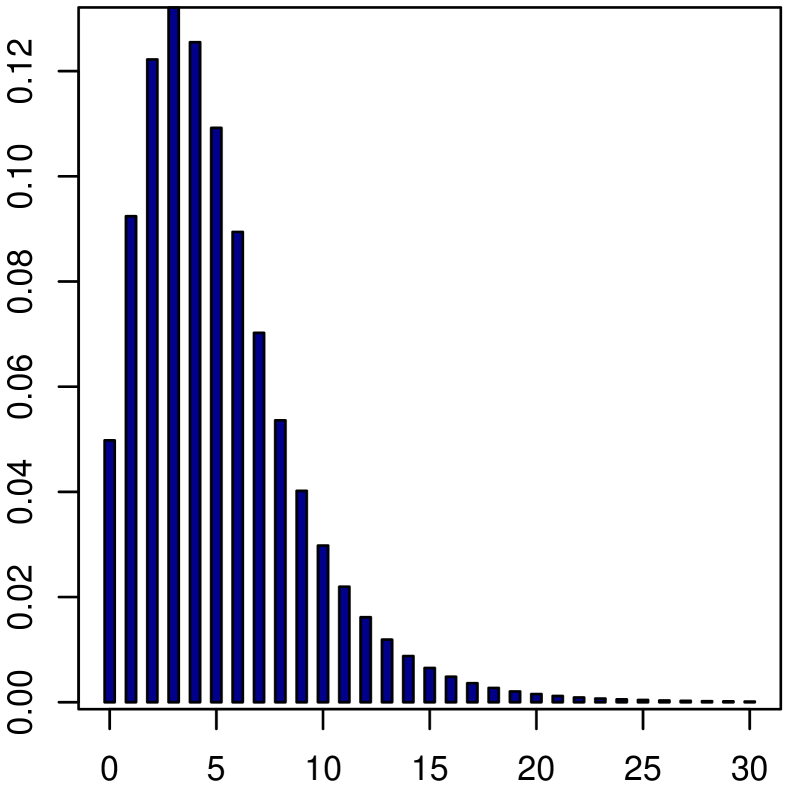

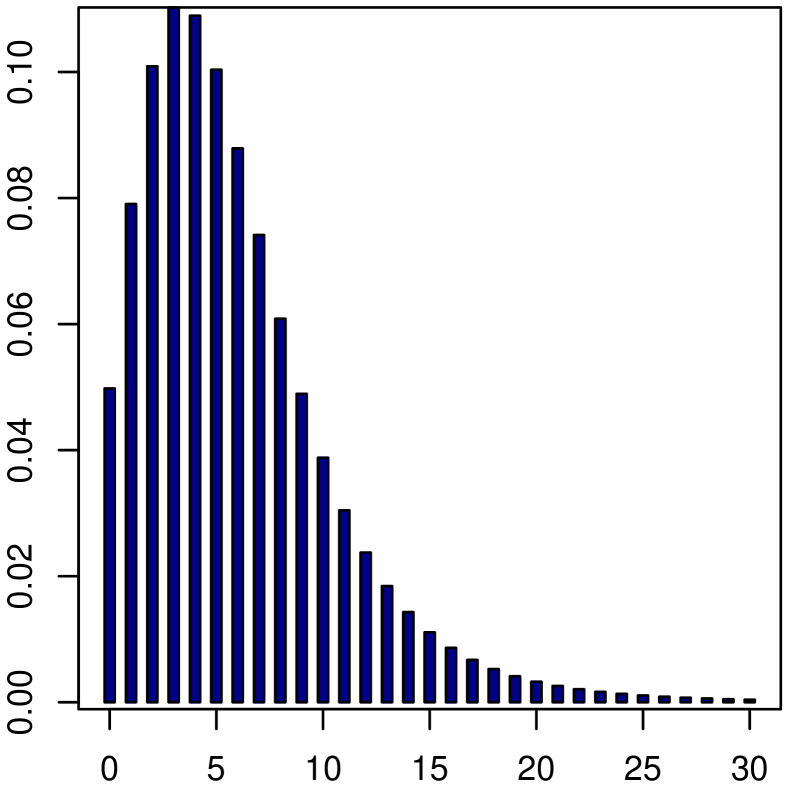

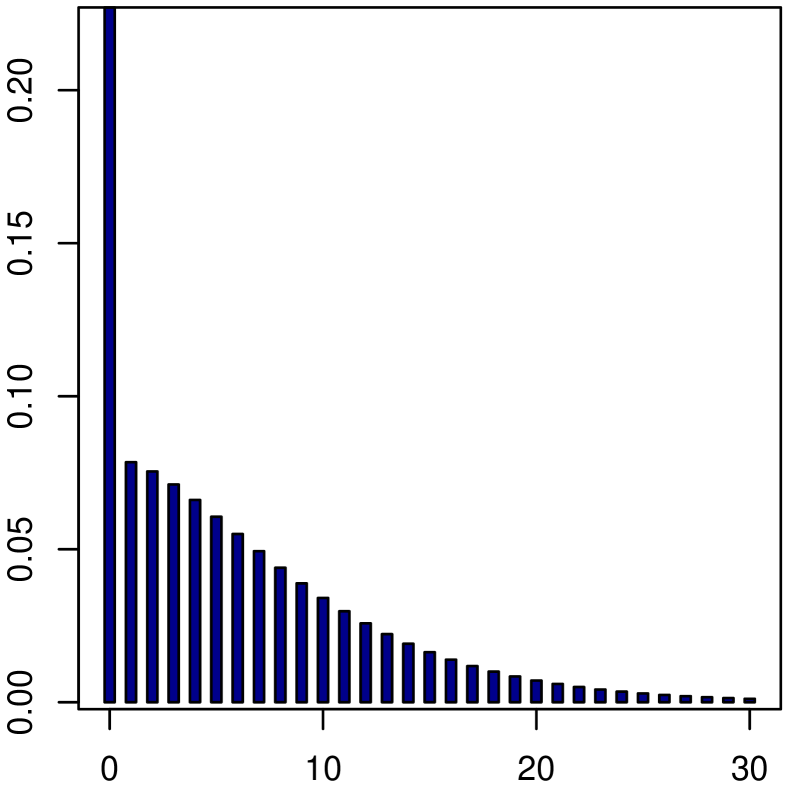

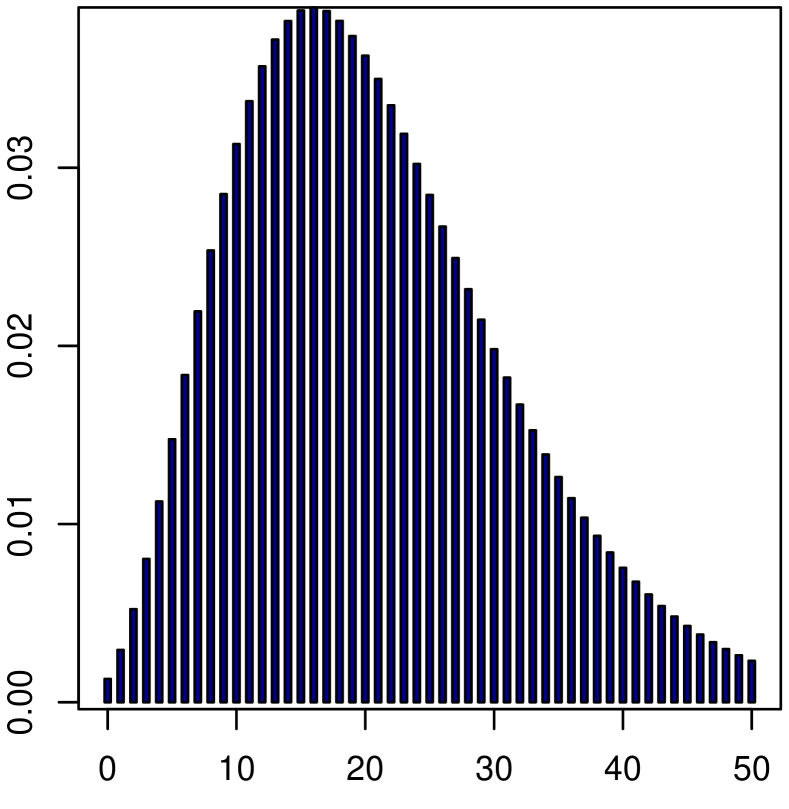

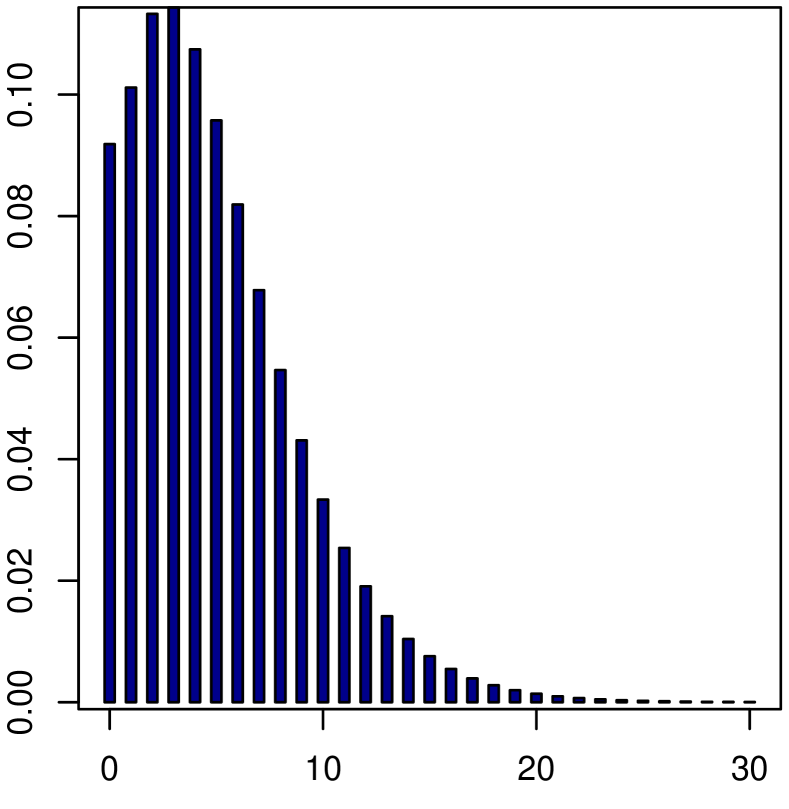

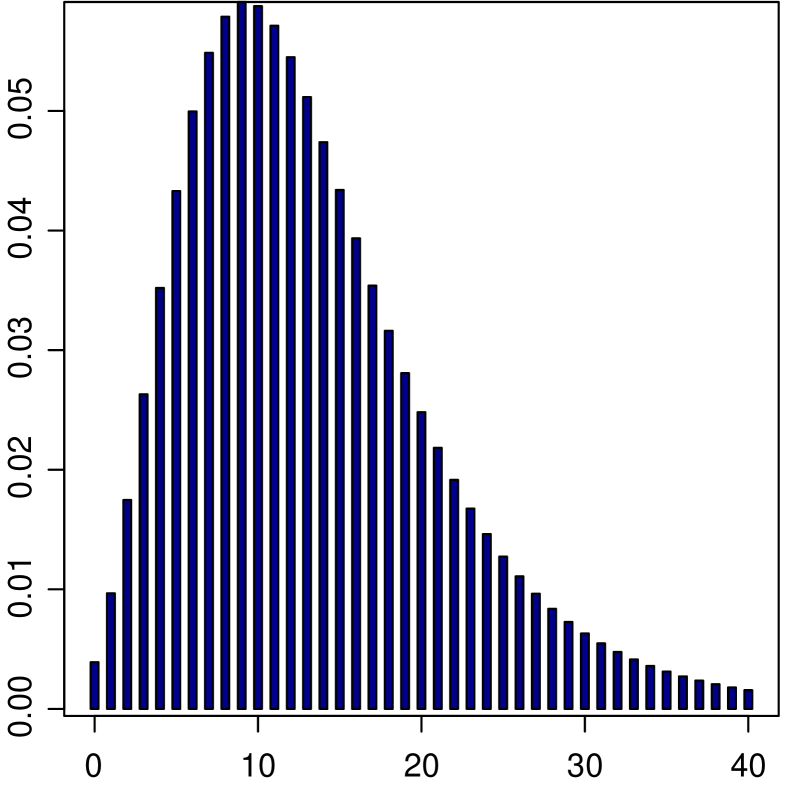

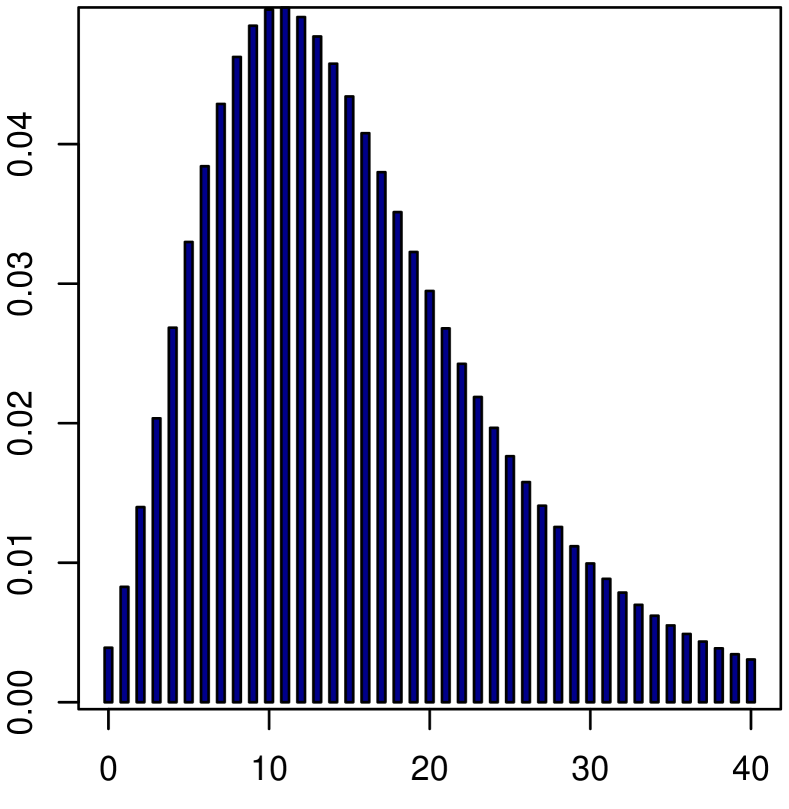

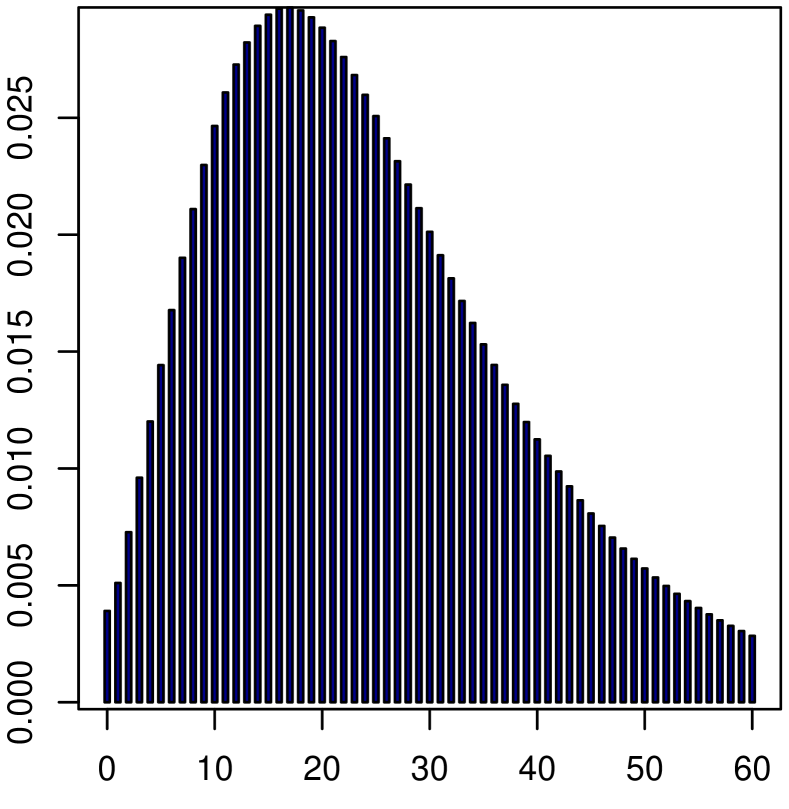

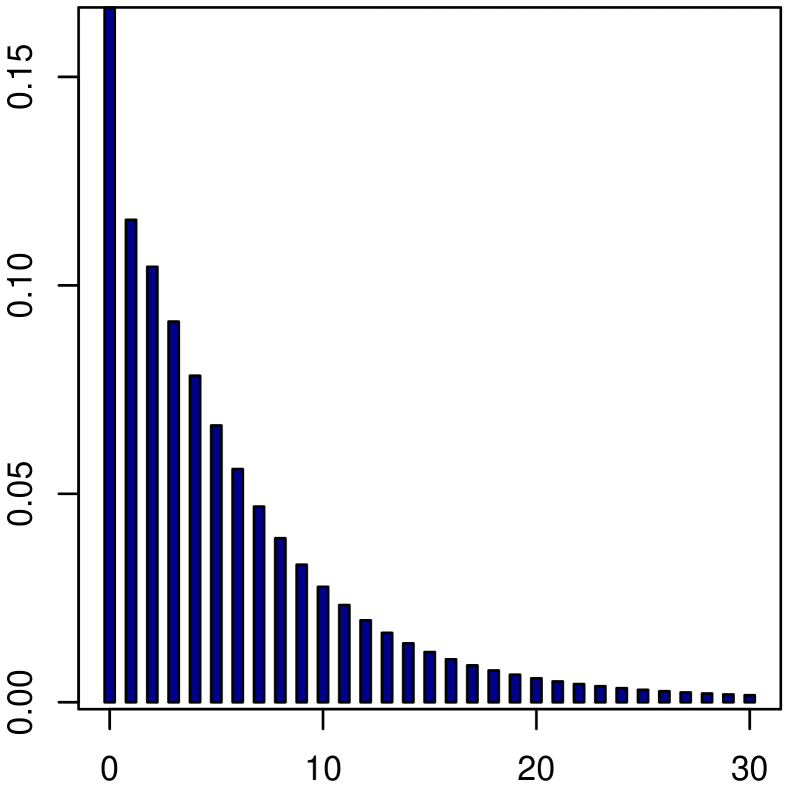

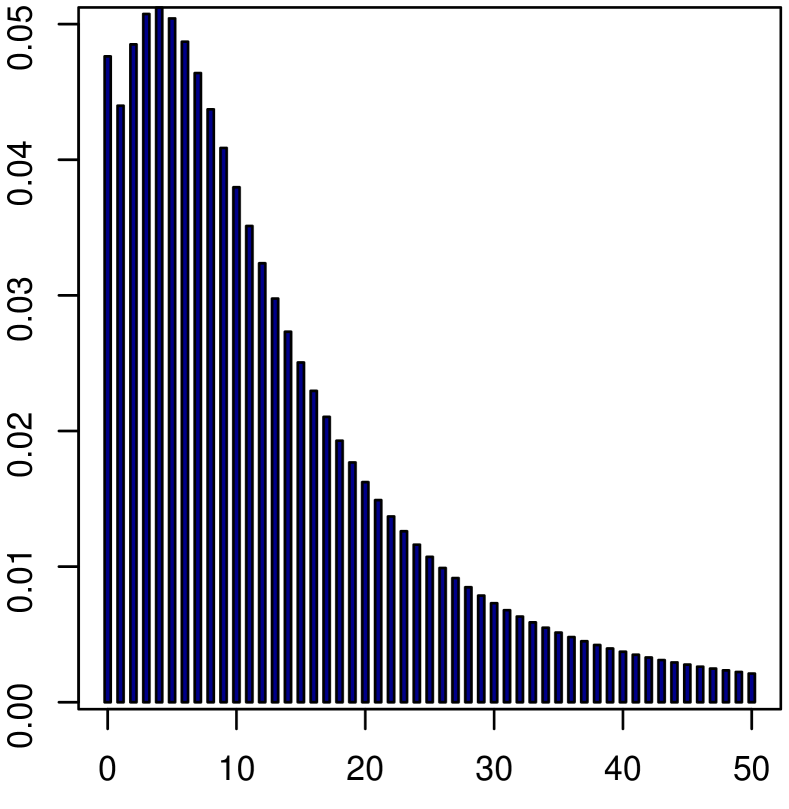

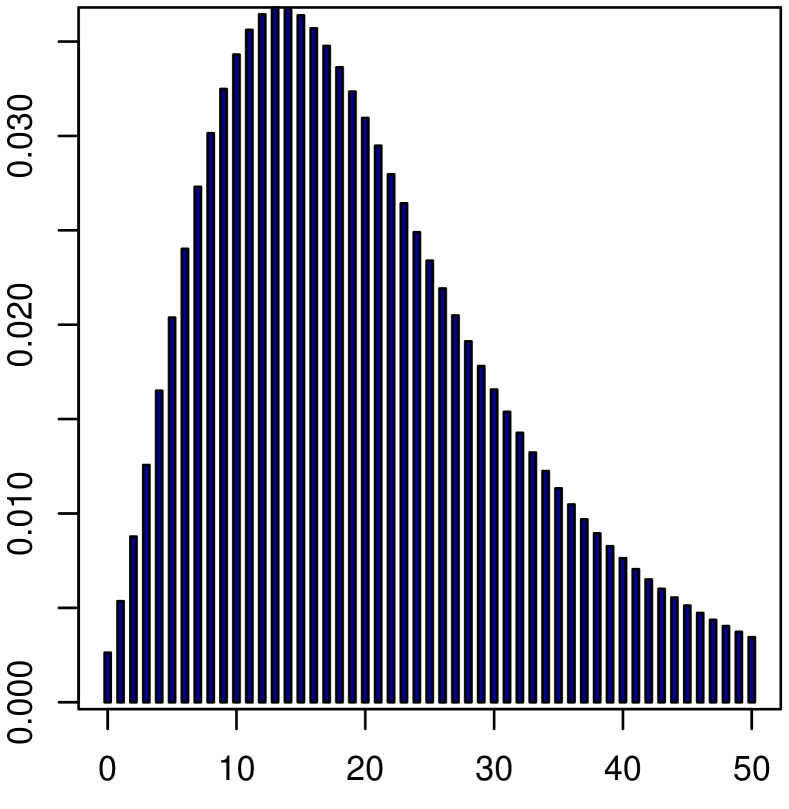

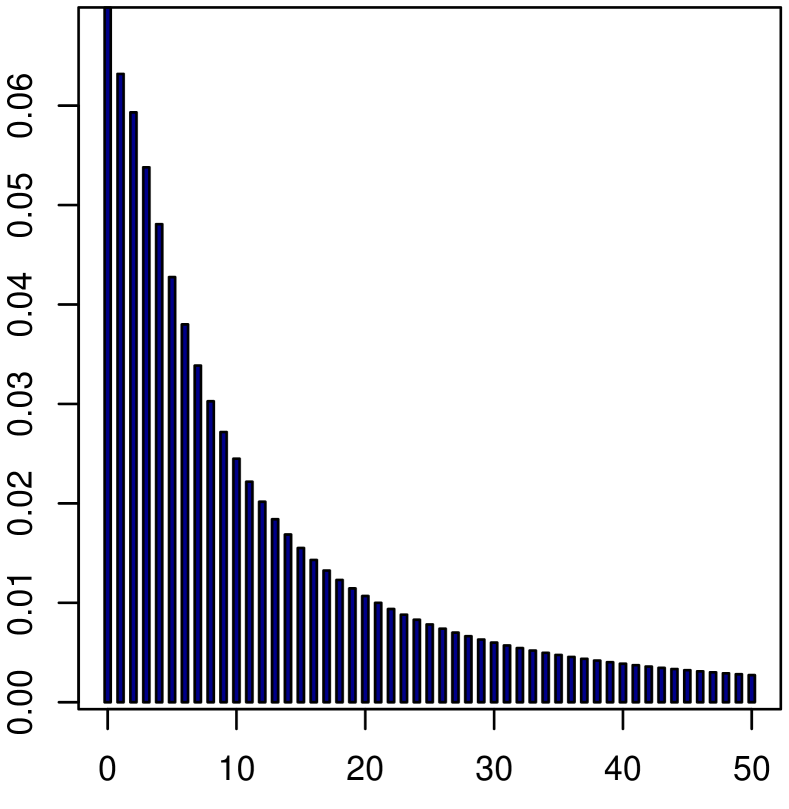

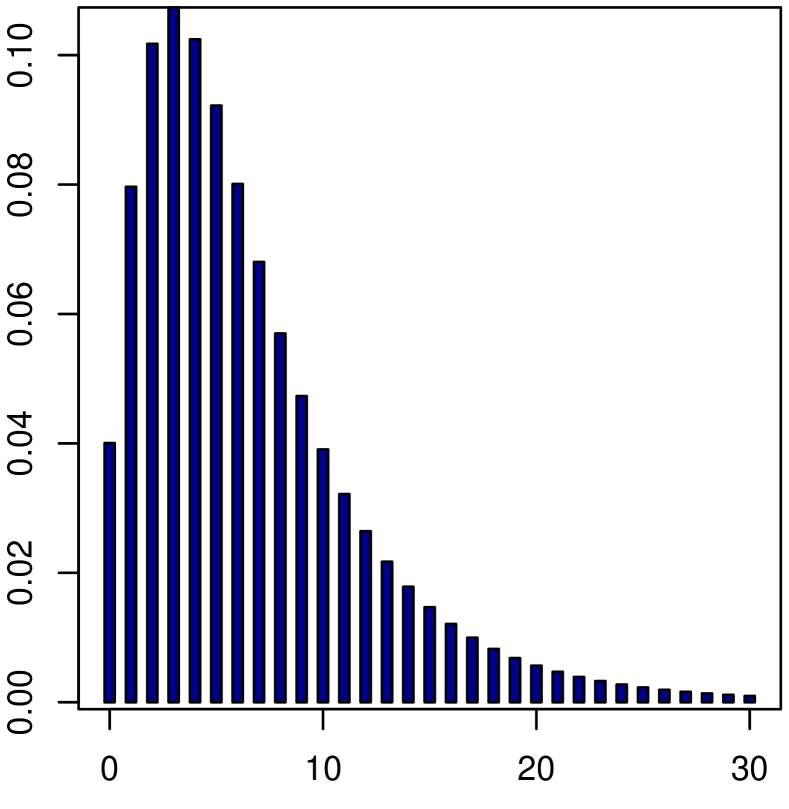

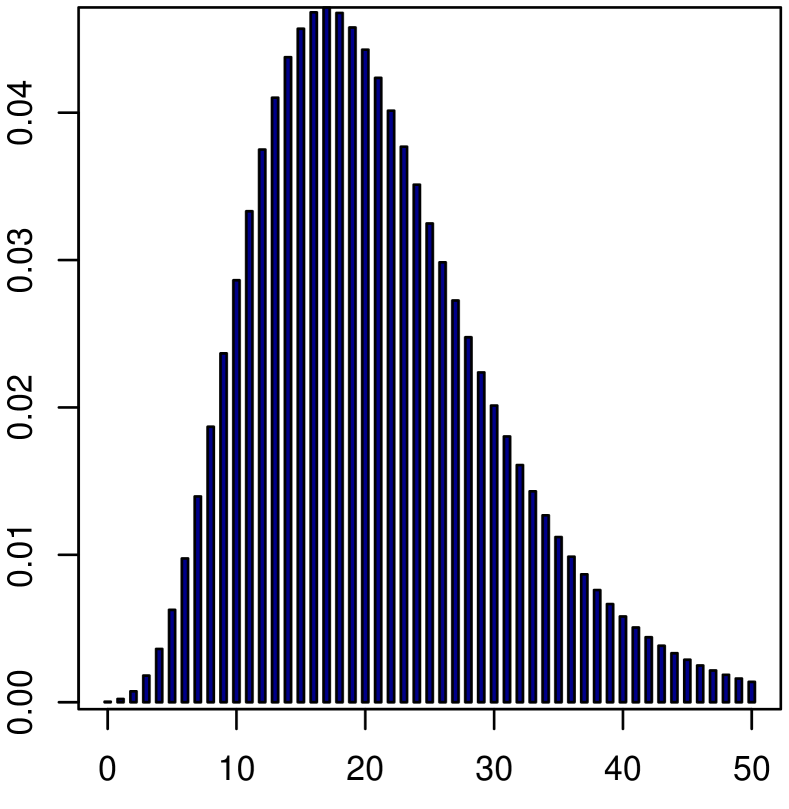

The following numerical examples demonstrate the behaviour of the pmf of the aggregate claims . For illustrative purposes, we focus on three widely used mixing distributions in actuarial literature, namely the Inverse Gaussian (IG), the the Gamma (Ga) and the Beta (Be) distribution.

Example 4.6.

Let and , where is a --measurable function. Since , we get and (see Table 1). Let be a --measurable function.

(a) Take . Since , we may apply Theorem 4.1 to get

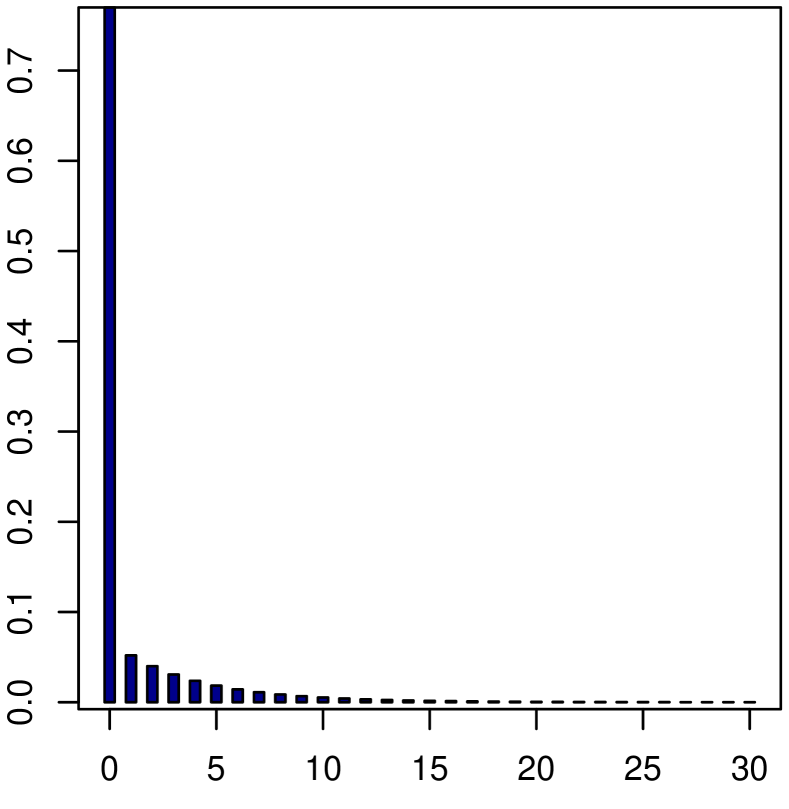

where for any and . Figure 4 depicts the behaviour of for and .

iIG

iiGa

iiiBe

Figure 4. The pmf of for and .

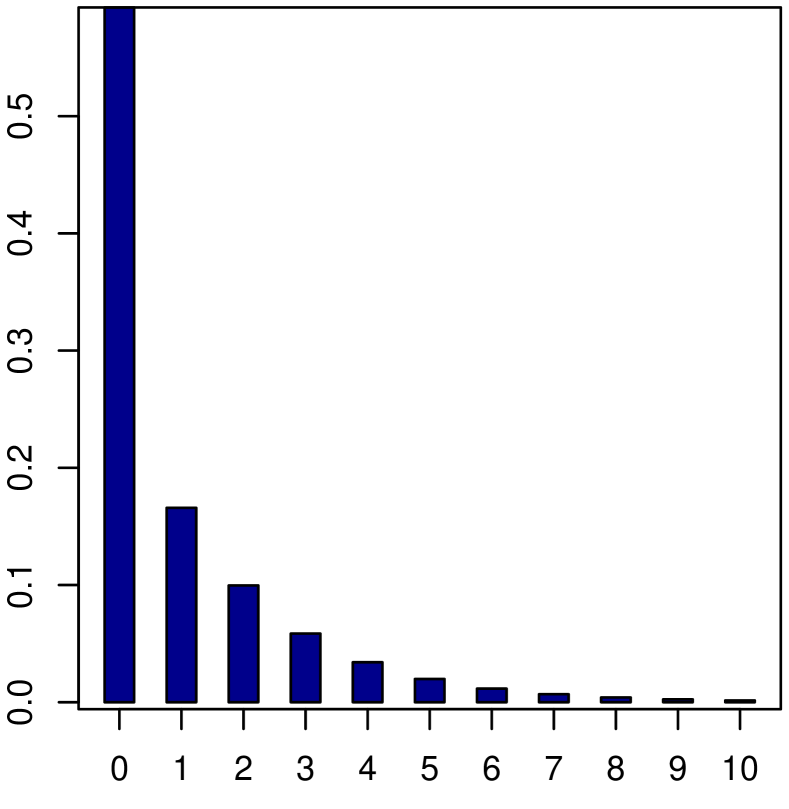

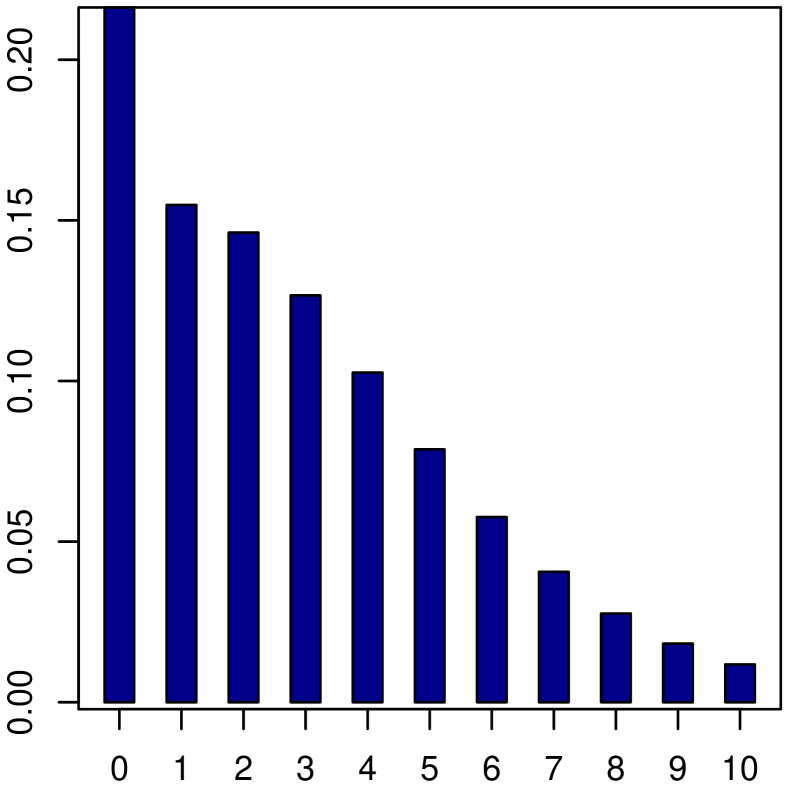

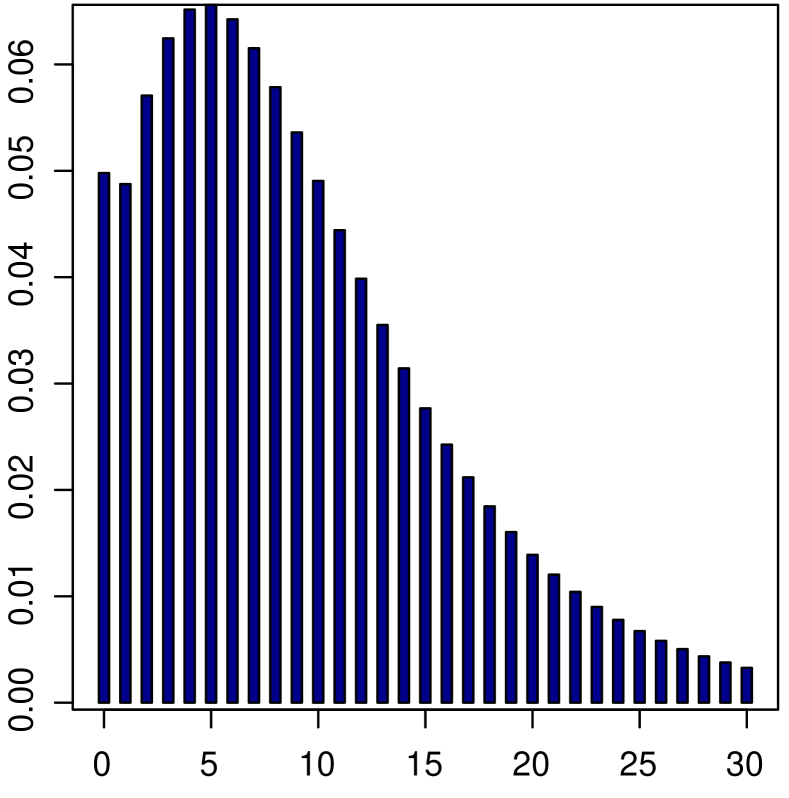

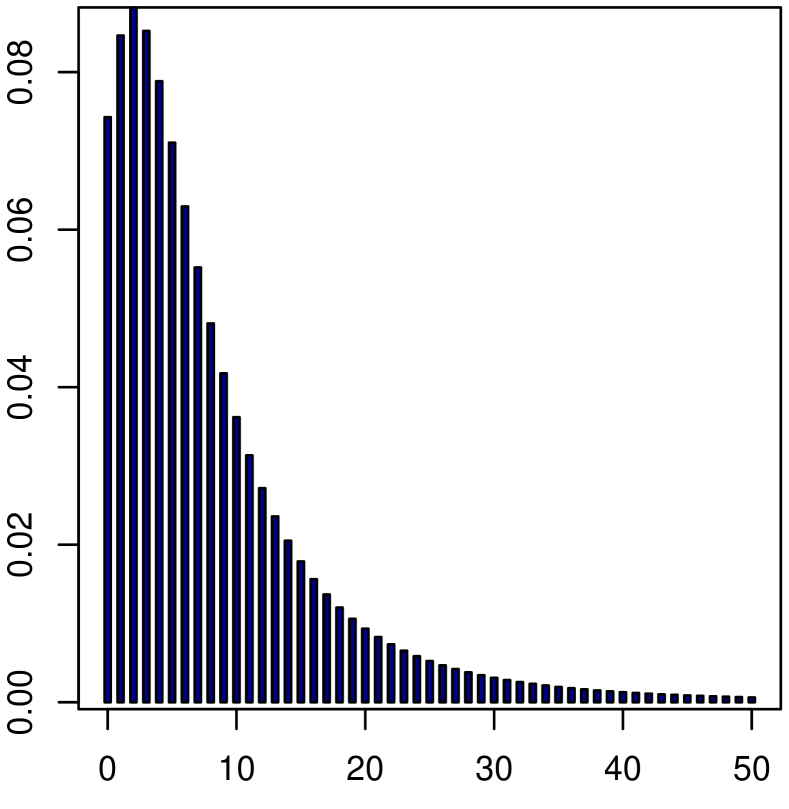

(b) Assume now that the claim sizes are distributed according to a mixed zero truncated geometric distribution with parameter (written for short), i.e.,

for any . Since with -a.s., we may apply Theorem 4.1 to get

where for any and . Figure 5 illustrates the behaviour of for the same choices of and as in (a).

iIG

iiGa

iiiBe

Figure 5. The pmf of for and .

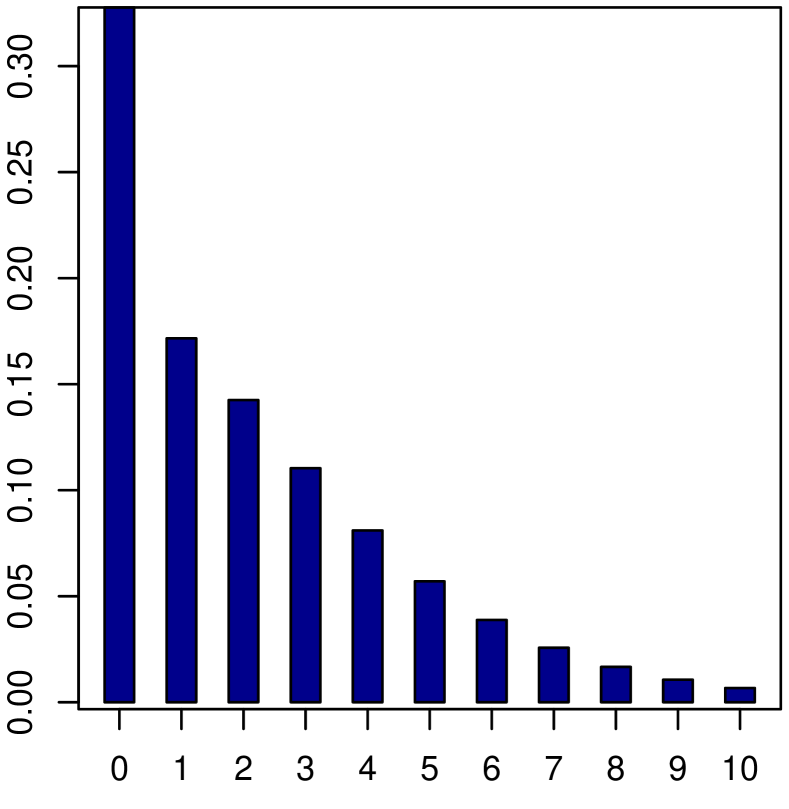

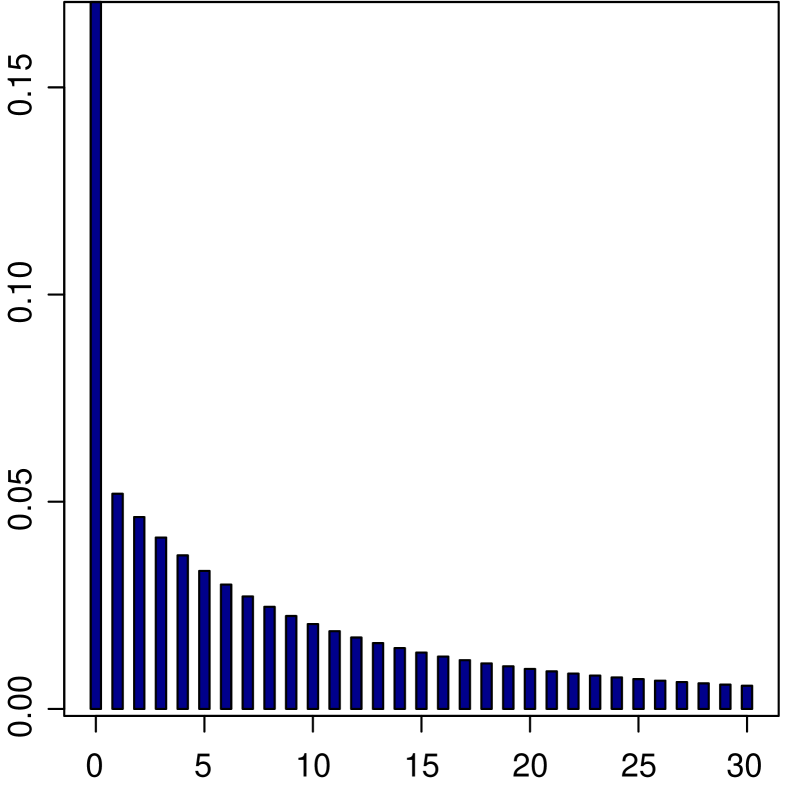

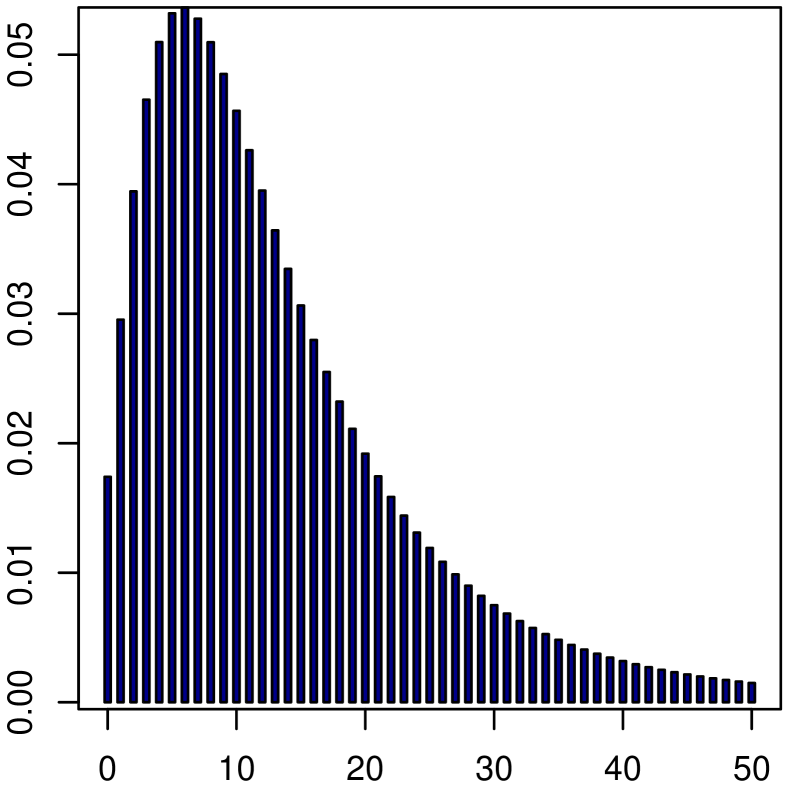

(c) Assume that and are -independent and that is degenerate at some point . If , then we can apply Theorem 4.1, along with Remark 4.3(a), to get

where for any and . Figure 6 depicts for and as in (a).

iIG

iiGa

iiiBe

Figure 6. The pmf of for and .

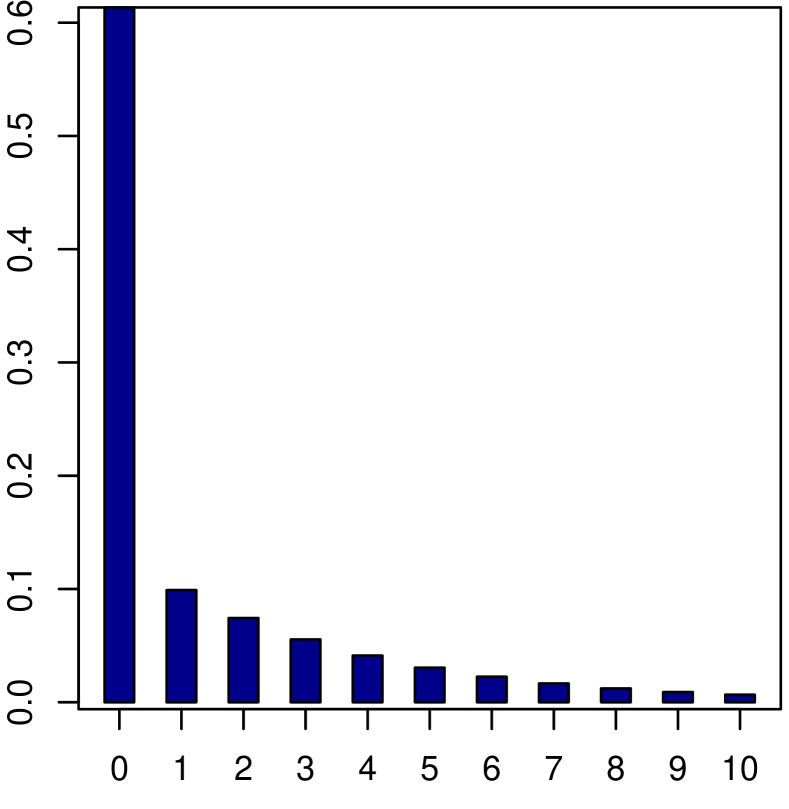

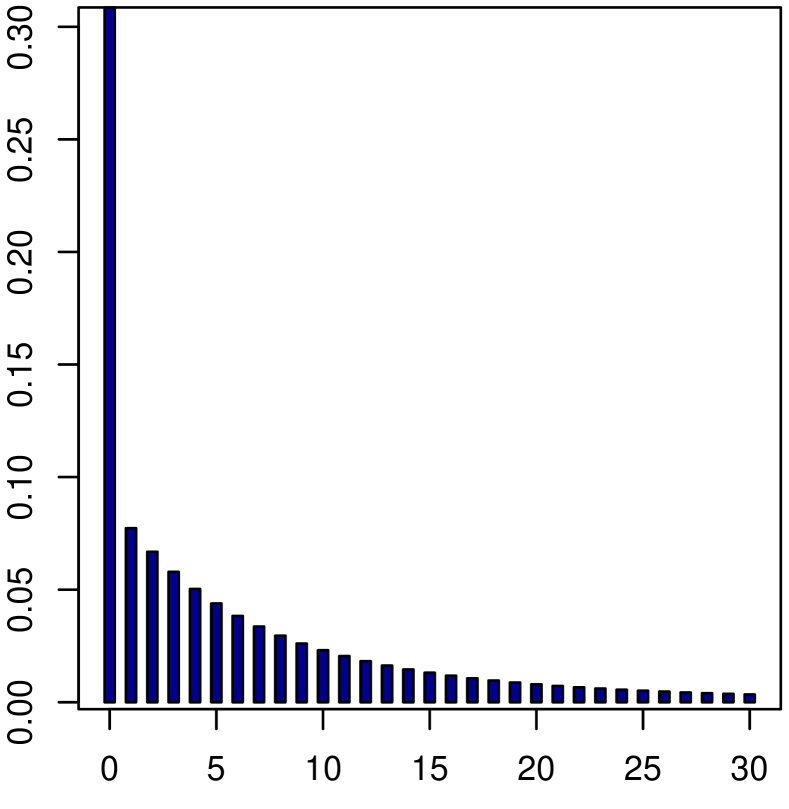

(d) Assume that and are -independent and that is degenerate at some point . If , we may apply Corollary 4.4 to get

where for any and . Figure 7 exhibits for and as in (a).

iIG

iiGa

iiiBe

Figure 7. The pmf of for and .

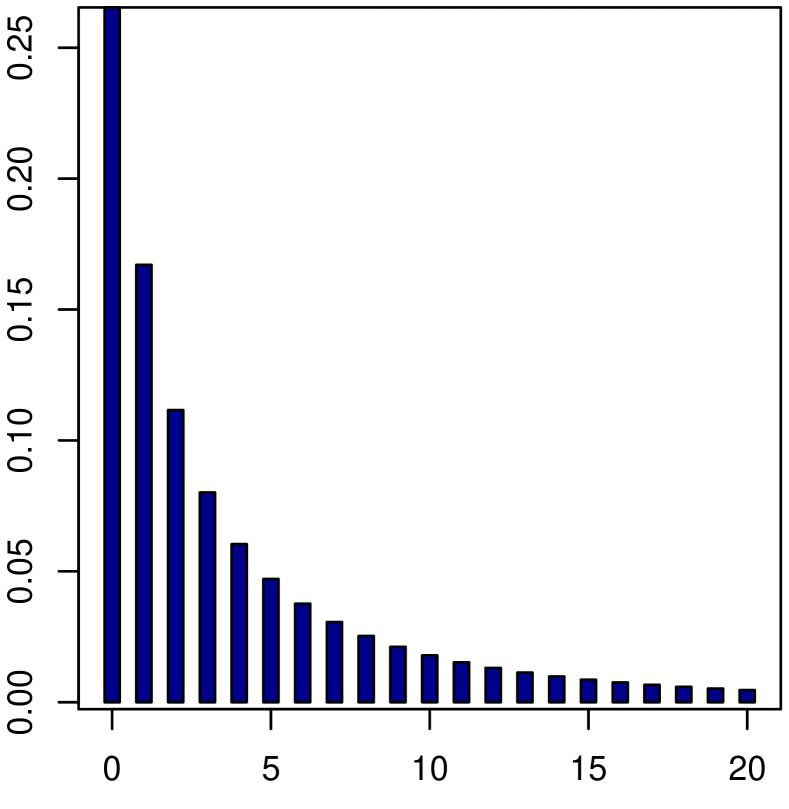

Example 4.7.

Let , , where are -- and --measurable functions, respectively. Since , we get and (see Table 1). Take .

(a) Let for any . Since and , we may apply Theorem 4.1 to get

Let , , where and is a --measurable function. As , we get and (see Table 1). Take .

(a) Let and take for any . Since and , we may apply Theorem 4.1 to get

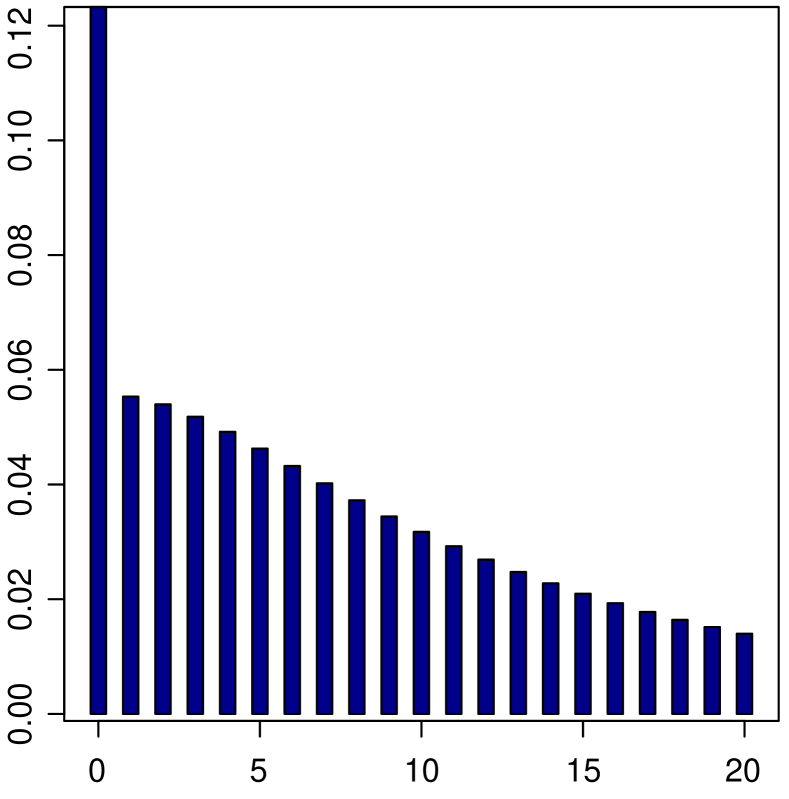

where for any and . Figure 13 depicts for , where , and different values of .

i; ;

ii; ;

iii; ;

Figure 13. The pmf of for different values of , and .

(b) Let and take for any . As and , we may apply Theorem 4.1, together with Remark 4.3(a), to get

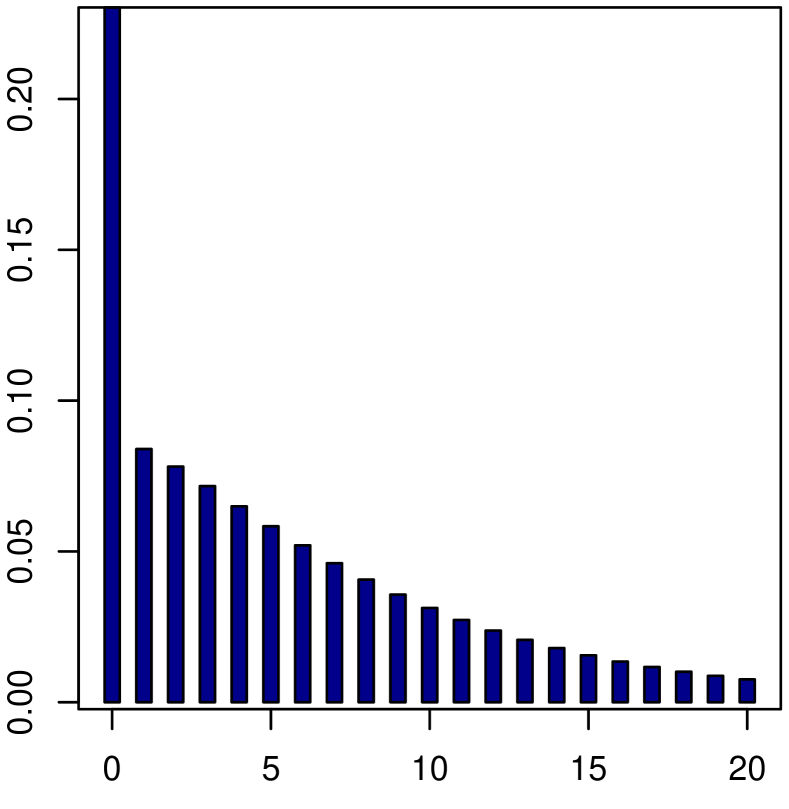

where for any and . Figure 14 illustrates for , where , and various values of .

i; ;

ii; ;

iii; ;

Figure 14. The pmf of for different values of , and .

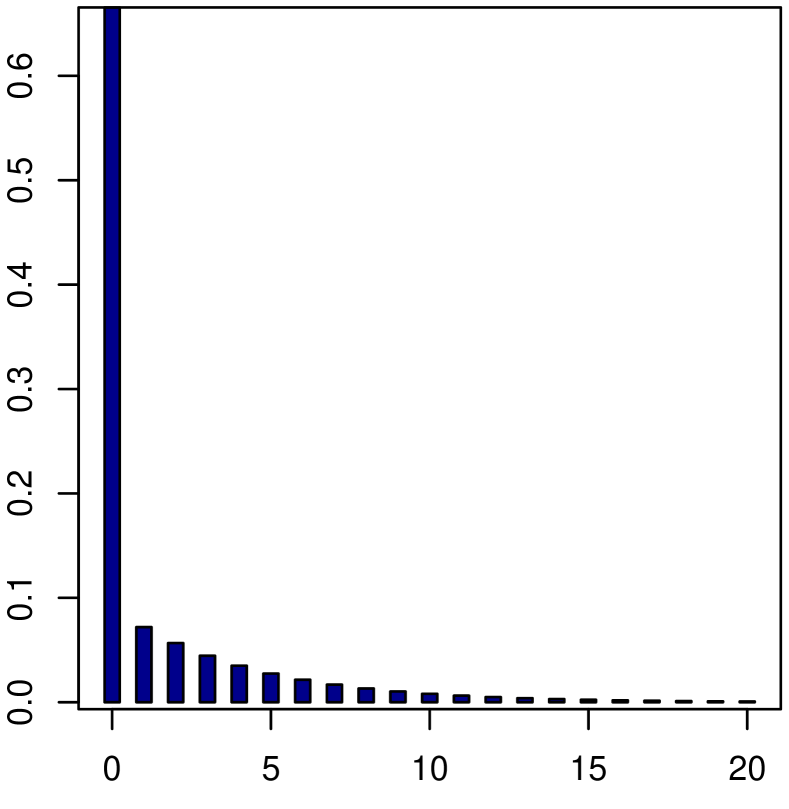

(c) Let and take for any . Since and , we may apply Theorem 4.1 to get

where for any and . Figure 15 depicts for , where , and different values of .

i; ;

ii; ;

iii; ;

Figure 15. The pmf of for different values of , and .

5. Concluding Remarks

When dealing with inhomogeneous insurance portfolios, mixtures of claim number distributions are frequently used to model the claim counts. In actuarial practice, the usual independence assumptions seem to be unrealistic. In particular, the mutual independence between claims sizes and counts appears to be implausible, especially when considering inhomogeneous portfolios. The above led us to the development of this work.

This paper aims to investigate the mixed counterpart of the original class and the corresponding compound distributions by relaxing the usual independence assumptions in two ways. More specifically, we allow the parameters of the claim number and the claim size distributions to be random, and we assume that the claim size process is conditionally i.i.d. and conditionally mutually independent of the claim counts.

Based on the above assumptions and the fundamental concept of regular conditional probabilities, this work provides a characterization for the members of class, as well as two recursive algorithms for and , respectively, where the recursion for also covers the case of a compound Panjer distribution with exchangeable claims. Our results are accompanied by various numerical examples to highlight the practical relevance of this work.

It is worth mentioning that the members of the class may be of particular interest in non-life insurance problems, for example, when insurance data exhibit overdispersion. Finally, this research allows us to consider some possible extensions of actuarial interest beyond the scopes of this paper, such as the study of the mixed counterpart of for and the derivation of De Pril’s recursion for the moments of (see De Pril (1986), Theorem, p. 118).

References

Albrecher & Boxma (2004)Albrecher, H. & Boxma, O. J. (2004). A ruin model with dependence between claim sizes and claim intervals. Insurance: Mathematics and Economics, 35(2), 245–254.

Albrecher & Teugels (2006)Albrecher, H. & Teugels, J. L. (2006). Exponential behavior in the presence of dependence in risk theory. Journal of Applied Probability, 43(1), 257–273.

Albrecher et al. (2011)Albrecher, H., Constantinescu, C. & Loisel, S. (2011). Explicit ruin formulas for models with dependence among risks. Insurance: Mathematics and Economics, 48(2), 265–270.

Antzoulakos & Chadjiconstantinidis (2004)Antzoulakos, D. L. & Chadjiconstantinidis, S. (2004). On mixed and compound mixed Poisson distributions. Scandinavian Actuarial Journal, 2004(3), 161–188.

Beal (1940)Beal, G. (1940). The fit and significance of contagious distributions when applied to observations on larval insects. Ecology, 21(4), 460–474.

Chang & Pollard (1997)Chang, J. T. & Pollard, D. (1997). Conditioning as disintegration. Statistica Neerlandica, 51(3), 287–317.

Cohn (2013)Cohn, D. L. (2013). Measure Theory, 2nd ed. Birkhäuser Advanced Texts.

De Pril (1986)De Pril, N. (1986). Moments of a class of compound distributions . Scandinavian Actuarial Journal, 1986(2), 117–120.

Fackler (2023)Fackler M. (2023). Panjer class revisited: one formula for the distributions of the Panjer class. Annals of Actuarial Science, 17(1), 145–169.

Faden (1985)Faden, A. M. (1985). The existence of regular conditional probabilities: Necessary and sufficient conditions. Annals of Probability, 13(1), 288–298.

Fremlin (2013)Fremlin, D. H. (2013). Measure theory (Vol. 4). Torres Fremlin (Ed.).

Gençtürk & Yiğiter (2016)Gençtürk, Y. & Yiğiter, A. (2016). Modelling claim number using a new mixture model: negative binomial gamma distribution. Journal of Statistical Computation and Simulation, 86(10), 1829–1839.

Gerhold et al. (2010)Gerhold, S., Schmock, U. & Warnung, R. (2010). A generalization of Panjer’s recursion and numerically stable risk aggregation. Finance and Stochastics, 14(1), 81–128.

Ghitany et al. (2008)Ghitany, M. E., Atieh, B. & Nadarajah, S. (2008). Lindley distribution and its application. Mathematics and computers in simulation, 78(4), 493–506.

Gómez-Déniz et al. (2004)Gómez-Déniz, E., Sarabia, J. M. & Calderín-Ojeda, E. (2008). Univariate and multivariate versions of the negative binomial-inverse Gaussian distributions with applications. Insurance: Mathematics and Economics, 42(1), 39–49.

Grandell (1997)Grandell, J. (1997). Mixed Poisson Processes, Chapman & Hall.

Johnson et al. (2005)Johnson, N. L., Kotz, S. & Kemp, A. W. (2005). Univariate Discrete Distributions, 3rd ed. John Wiley and Sons, New York.

Hess et al. (2002)Hess, K. T., Liewald, A. & Schmidt, K. D. (2002) An extension of Panjer’s recursion. ASTIN Bulletin: The Journal of the IAA, 32(2), 61–80.

Hesselager (1994)Hesselager, O. (1994). A recursive procedure for calculation of some compound distributions. ASTIN Bulletin: The Journal of the IAA, 24(1), 19–32.

Hesselager (1996)Hesselager, O. (1996). A recursive procedure for calculation of some mixed compound Poisson distributions. Scandinavian Actuarial Journal1996(1), 54–63.

Karlis & Xekalaki (2005)Karlis, D. & Xekalaki, E. (2005). Mixed poisson distributions. International Statistical Review/Revue Internationale de Statistique, 73(1), 35–58.

Kolev & Paiva (2008)Kolev, N. & Paiva, D. (2008). Random sums of exchangeable variables and actuarial applications. Insurance: Mathematics and Economics, 42(1), 147–153.

Lyberopoulos & Macheras (2012)Lyberopoulos, D. P. & Macheras, N. D. (2012). Some characterizations of mixed Poisson processes. Sankhyā A, 74(1), 57–79.

Lyberopoulos & Macheras (2013)Lyberopoulos, D. P. & Macheras, N. D. (2013). A construction of mixed Poisson processes via disintegrations. Mathematica Slovaca, 63(1), 167–182.

Lyberopoulos & Macheras (2019)Lyberopoulos, D. P. & Macheras, N. D. (2019). A characterization of martingale-equivalent compound mixed Poisson process. arXiv preprint arXiv:1905.07629.

Lyberopoulos & Macheras (2021)Lyberopoulos, D. P. & Macheras, N. D. (2021). A characterization of martingale-equivalent mixed compound Poisson processes. Annals of Applied Probabability, 31(2), 778–805.

Lyberopoulos & Macheras (2022)Lyberopoulos, D. P. & Macheras, N. D. (2022). Some characterizations of mixed renewal processes. Mathematica Slovaca72(1), 197–216.

Lyberopoulos et al. (2019)Lyberopoulos, D. P., Macheras, N. D. & Tzaninis S. M. (2019). On the equivalence of various definitions of mixed Poisson processes. Mathematica Slovaca, 69(2), 453–468.

Mansoor et al. (2020)Mansoor, M., Tahir, M. H., Cordeiro, G. M., Ali, S. & Alzaatreh, A. (2020). The Lindley negative-binomial distribution: Properties, estimation and applications to lifetime data. Mathematica Slovaca, 70(4), 917–934.

Nadarajah & Kotz (2006a)Nadarajah, S. & Kotz, S. (2006a). Compound mixed Poisson distributions I. Scandinavian Actuarial Journal, 2006(3), 141–162.

Nadarajah & Kotz (2006b)Nadarajah, S. & Kotz, S. (2006b) Compound mixed Poisson distributions II. Scandinavian Actuarial Journal, 2006(3), 163–181.

Panjer (1981)Panjer, H. H. (1981). Recursive evaluation of a family of compound distributions. ASTIN Bulletin: The Journal of the IAA, 12(1), 22–26.

Schmidt (2012)Schmidt, K. D. (2012). Lectures on Risk Theory. Springer Science & Business Media.

Schmidt (2014)Schmidt, K. D. (2014). On inequalities for moments and the covariance of monotone functions. Insurance: Mathematics and Economics, 55, 91–95.

Schröter (1990)Schröter, K. (1990). On a class of counting distributions and recursions for related compound distributions. Scandinavian Actuarial Journal, 1990(2-3), 161–175.

Stoyanov (2013)Stoyanov, J. M. (2013). Counterexamples in Probability, 3rd ed.. Dover Publications.

Sundt (1992)Sundt, B. (1992). On some extensions of Panjer’s class of counting distributions. ASTIN Bulletin: The Journal of the IAA, 22(1), 61–80.

Sundt & Jewell (1981)Sundt, B. & Jewell, W. S. (1981). Further results on recursive evaluation of compound distributions. ASTIN Bulletin: The Journal of the IAA, 12(1), 27–39.

Sundt & Vernic (2004)Sundt, B. & Vernic, R. (2004). Recursions for compound mixed multivariate Poisson distributions. Blätter der DGVFM, 26(4), 665–691.

Sundt & Vernic (2009)Sundt, B. & Vernic, R. (2009). Recursions for convolutions and compound distributions with insurance applications. Springer Science & Business Media.

Tzaninis & Macheras (2023)Tzaninis, S. M. & Macheras, N. D. (2023). A characterization of progressively equivalent probability measures preserving the structure of a compound mixed renewal process. ALEA, Latin American Journal of Probability and Mathematical Statistics, 20, 225–247.

Tzougas et al. (2019)Tzougas, G., Hoon, W. L.& Lim, J. M. (2019). The negative binomial-inverse Gaussian regression model with an application to insurance ratemaking. European Actuarial Journal, 9, 323–344.

Tzougas et al. (2021)Tzougas, G., Hong, N. & Ho, R. (2021). Mixed poisson regression models with varying dispersion arising from non-conjugate mixing distributions. Algorithms, 15(1), 16.

Wang (2011)Wang, Z. (2011). One mixed negative binomial distribution with application. Journal of Statistical Planning and Inference, 141(3), 1153–1160.

Wang & Sobrero (1994)Wang, S. & Sobrero, M. (1994). Further results on Hesselager’s recursive procedure for calculation of some compound distributions. ASTIN Bulletin: The Journal of the IAA, 16(2), 161–166.

Willmot (1986)Willmot, G. E. (1986). Mixed compound Poisson distributions. ASTIN Bulletin: The Journal of the IAA, 16(1), 59–79.

Willmot (1987)Willmot, G. E. (1987). The Poisson-Inverse Gaussian distribution as an alternative to the negative binomial. Scandinavian Actuarial Journal, 1987(3-4), 113–127.

Willmot (1988)Willmot, G. E. (1988). Sundt and Jewell’s family of discrete distributions. ASTIN Bulletin: The Journal of the IAA, 18(1), 17–29.

Willmot (1993)Willmot, G. E. (1993). On recursive evaluation of mixed Poisson probabilities and related quantities. Scandinavian Actuarial Journal, 1993(2), 114–133.