Model Uncertainty in Latent Gaussian Models with Univariate Link Function

Abstract

We consider a class of latent Gaussian models with a univariate link function (ULLGMs). These are based on standard likelihood specifications (such as Poisson, Binomial, Bernoulli, Erlang, etc.) but incorporate a latent normal linear regression framework on a transformation of a key scalar parameter. We allow for model uncertainty regarding the covariates included in the regression. The ULLGM class typically accommodates extra dispersion in the data and has clear advantages for deriving theoretical properties and designing computational procedures. We formally characterize posterior existence under a convenient and popular improper prior and propose an efficient Markov chain Monte Carlo algorithm for Bayesian model averaging in ULLGMs. Simulation results suggest that the framework provides accurate results that are robust to some degree of misspecification. The methodology is successfully applied to measles vaccination coverage data from Ethiopia and to data on bilateral migration flows between OECD countries.

Keywords: Bayesian Model Averaging, Count Data Regression, Overdispersion, Variable Selection, Markov chain Monte Carlo

1 Introduction

Non-Gaussian regression models are extensively applied across numerous disciplines. The emergence of large datasets, coupled with significant uncertainty regarding the relevant variables for explaining an outcome of interest, has highlighted the importance of variable selection and model averaging techniques in non-Gaussian settings. The Bayesian approach to addressing model uncertainty involves placing a prior probability on each model, typically defined by a subset of predictors, as well as a prior on the corresponding parameters. This approach yields a joint posterior distribution of models and parameters, offering insights into the importance of specific variables within the regression model and making it particularly well-suited for predictive inference.

Bayesian model averaging (BMA) for non-Gaussian data encounters two primary challenges. First, in the presence of covariates, the model space is of size , making it infeasible to enumerate in many cases. Second, the weights used to construct model-averaged estimates are typically based on marginal likelihoods, which are often unavailable analytically in non-Gaussian frameworks. To address these challenges, several procedures for variable selection and model averaging under non-Gaussian likelihoods have been proposed. Well-known approaches rely on approximate marginal likelihoods (Volinsky et al., 1997; Rossell et al., 2021) or reversible jump Markov chain Monte Carlo (MCMC) algorithms (Dellaportas et al., 2002; Lamnisos et al., 2009) to calculate posterior model probabilities. More recently, the increasing availability of data augmentation schemes for non-Gaussian regression models (Frühwirth-Schnatter and Wagner, 2006; Polson et al., 2013) has led to the development of specialized augmented MCMC algorithms to address model uncertainty in Poisson (Dvorzak and Wagner, 2016), negative binomial (Jankowiak, 2023), and logistic (Wan and Griffin, 2021) models.

We extend this literature by proposing a general and exact framework for formal BMA in a wide class of non-Gaussian regression models. Specifically, we focus on models that combine a standard likelihood specification (such as Poisson or Binomial) with a latent Gaussian linear regression framework applied to a transformation of a key scalar parameter. This approach offers clear advantages for deriving theoretical properties and designing computational procedures. Importantly, we demonstrate the existence of the posterior distribution under a convenient and popular uninformative prior setting. This is crucial as BMA is typically sensitive to prior choices, making the theoretical justification of available uninformative benchmark priors highly relevant in practice. For posterior simulation, we introduce a simple, general and efficient MCMC algorithm for parameter estimation under model uncertainty.

We study two members of the model class in more detail, both used for overdispersed count data regression. These models are applied to simulated data and further illustrated using real-world datasets on early childhood measles vaccination coverage rates in Ethiopia and bilateral migration flows between OECD countries. In addition, we conduct an extensive out-of-sample cross-validation exercise with the real-world datasets to examine the comparative predictive performance of the models. Our results demonstrate the accuracy and predictive quality of the proposed framework, as well as its robustness under misspecification. A software implementation of the algorithms used is provided in the R package LatentBMA, available from CRAN.

The remainder of this article is organized as follows. Sec. 2 introduces the model class we consider and discusses two members of the model class in detail. Sec. 3 discusses prior specifications. Sec. 4 summarizes our formal results on posterior existence and provides details on key posterior distributions. Sec. 5 develops the computational framework for posterior simulation. Sec. 6 reports the results from a simulation study, while Sec. 7 examines real-world applications. Sec. 8 concludes the paper and suggests directions for future research. Additional details and results are provided in the supplementary material.

2 Univariate Link Latent Gaussian Models

Consider the following general class of models for observations

| (1) | ||||

| (2) |

where, given and , the are independently drawn from some (continuous or discrete) distribution with support and which is indexed by a scalar parameter and possibly another (low-dimensional) parameter vector . The index is constructed on the basis of a latent variable using an invertible and continuously differentiable link function which takes values in some univariate space. The latent is modelled through the normal linear regression model in (2), where is an intercept term, is a regression coefficient vector, is (usually) an overdispersion parameter and groups observable covariates for observation . Assuming a Gaussian distribution in (2) to model unobserved heterogeneity can be motivated as capturing a large number of independent heterogeneity terms, using a central limit theorem. The class of models formed by (1) and (2) are covered by the definition of “Latent Gaussian Models with a Univariate Link Function” in Hrafnkelsson and Bakka (2023). We shall call our models in (1) and (2) ULLGMs (Univariate Link Latent Gaussian Models). Approximate Bayesian inference for latent Gaussian Models (LGMs) was discussed in Rue et al. (2009). In contrast to most of the existing literature, for our ULLGMs does not need to belong to the exponential family111For example, the Negative Binomial distribution with a free parameter is not in the exponential family. and is not necessarily equal to the mean of (the latter need not even exist). In addition and more importantly, we will formally deal with model uncertainty regarding the choice of regressors in (2); see Subsection 2.3.

| Model | Proper | |||

|---|---|---|---|---|

| Poisson Log-Normal (PLN) | Poisson() | yes | ||

| Binomial Logistic (BiL) | Bin(), | yes | ||

| Negative Binomial Logistic (NBL) | Neg Bin(), | yes | ||

| Erlang Log-Normal (ErLN) | Erlang(), | yes | ||

| Log-Normal Normal (LNN) | log-Normal() | yes | ||

| Log-Normal Log-Normal (LNLN) | log-Normal(), | yes, for fixed | ||

| Bernoulli Cdf (BeC) | Bernoulli() | no |

The members of the ULLGM class are mapped out by choosing different and . Table 1 lists some examples. In the table indicates a parameter in , takes values in , is a parameter on the unit interval and denotes a known continuous cumulative distribution function (cdf) defined on . The last column indicates posterior propriety (discussed in Section 4.1) under a convenient improper prior that will be introduced in Section 3. Some models in the table have an additional parameter , which allows for more flexibility and is considered fixed for now (until Subsection 2.4).

Certain can generate more than one member of the ULLGM class, depending on which of the parameters we model through the latent Gaussian variable , one example being the case where is log-normal. The LNN model can be shown to be equivalent to the usual log-Normal regression model (where log-Normal with ), and it tends to this standard model with as . Advantages of expressing this model as a member of the ULLGM class include the ease of deriving theoretical results on posterior existence and the simple treatment of model uncertainty (see Sec. 2.2). The LNLN model introduces the Gaussian regression for the scale parameter of the log-Normal and treats the location parameter as an additional parameter .

PLN, NBL and ErLN models converge to the usual Poisson, negative Binomial and Erlang regression models as tends to zero. The Erlang distribution is a Gamma distribution with integer shape parameter and reduces to the Exponential distribution for . The negative Binomial distribution with is also called the geometric distribution. These standard single-parameter models are often found to be unable to account for overdispersion in the observed data. For nonzero , the random nature of the latent Gaussian component in ULLGM models will allow for such extra variation or dispersion.

The subclass of models based on Bernoulli sampling is a special case of Binomial sampling models when and is defined by the choice of the link cdf . For example, if the cdf of a standard normal distribution is chosen for , the BeC model becomes equivalent to a probit model with an additional unidentified parameter . For other choices of , the BeC model can be shown to interpolate between the corresponding binary regression model (where ) and the probit model, with the value of indicating its proximity to these extremes. Further theoretical details and empirical examples are provided in Appendix A2. Nevertheless, since is typically unidentified in BeC models, this subclass is expected to be mainly of theoretical interest and is unlikely to have major empirical utility.

2.1 Selected ULLGMs for Count Data Regression

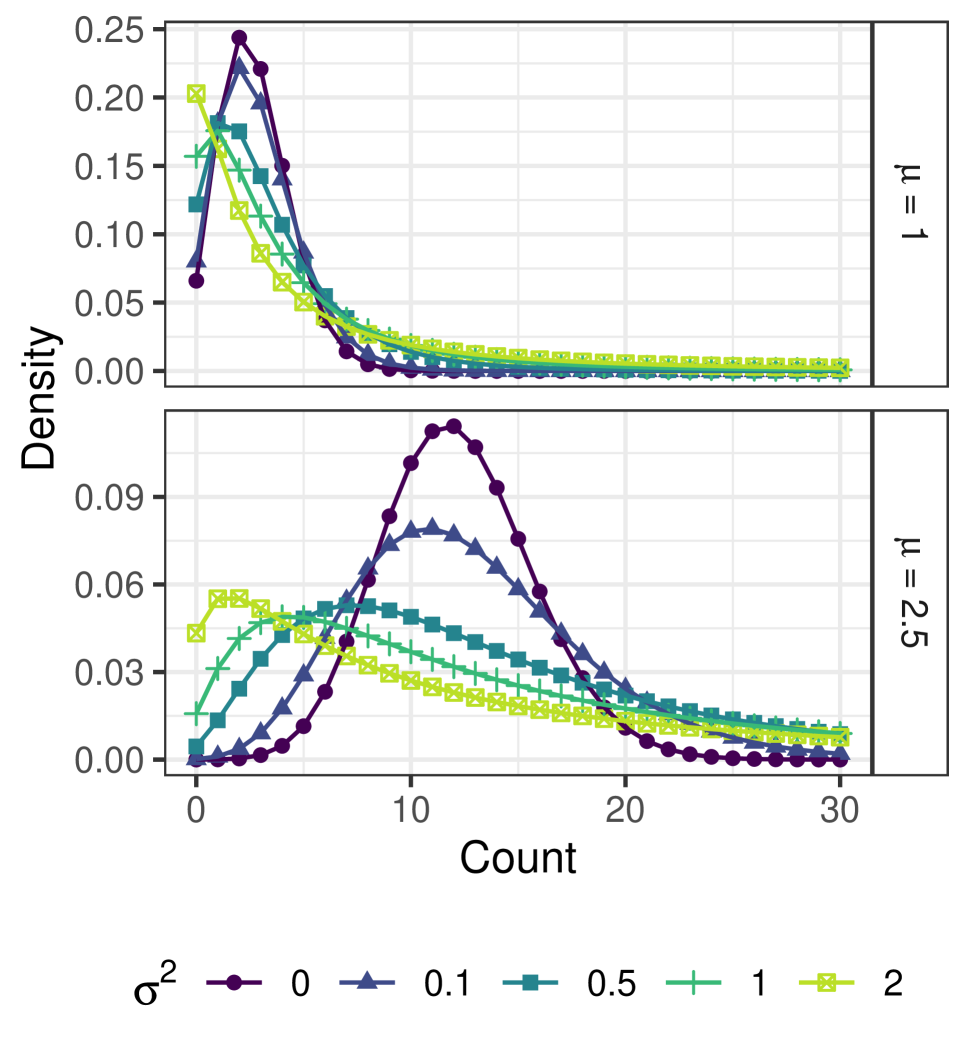

Consider the PLN model, which applies to count-valued data and is based on a Poisson likelihood. The observed counts () are assumed to be Poisson distributed with an intensity parameter . In the standard, equi-dispersed, Poisson regression framework is a deterministic function of observed covariates. In the presence of unobserved heterogeneity and overdispersion, it makes sense to assume that is random, arising from an appropriate mixing distribution. Commonly considered mixing distributions include the Gamma distribution, which results in a negative binomial model (Greenwood and Yule, 1920), or an inverse Gaussian distribution which was used in Dean et al. (1989). A Log-normal mixing distribution model has appeared as such in the literature: Bulmer (1974) uses this mixture model in a location-scale context, which was extended to a multivariate setting in Aitchison and Ho (1989). The regression structure as used here was mentioned in Hinde (1982) and used in Tsionas (2010) in a Bayesian setting.

For the PLN model as in Table 1, we can show that

| (3) |

allowing for overdispersion since . The expression for the expected value further shows that the PLN model maintains a simple and intuitive interpretation of the regression parameters , similar to a Poisson regression model. Note that the usual dispersion index

| (4) |

is a monotonous function of taking values on all of . With the exception of the BeC class, similar results hold for the other models in Table 1, which gives the interpretation of a dispersion parameter, controlling excess dispersion beyond the one implied by . 1(a) shows example probability mass functions (pmfs) for the PLN model.

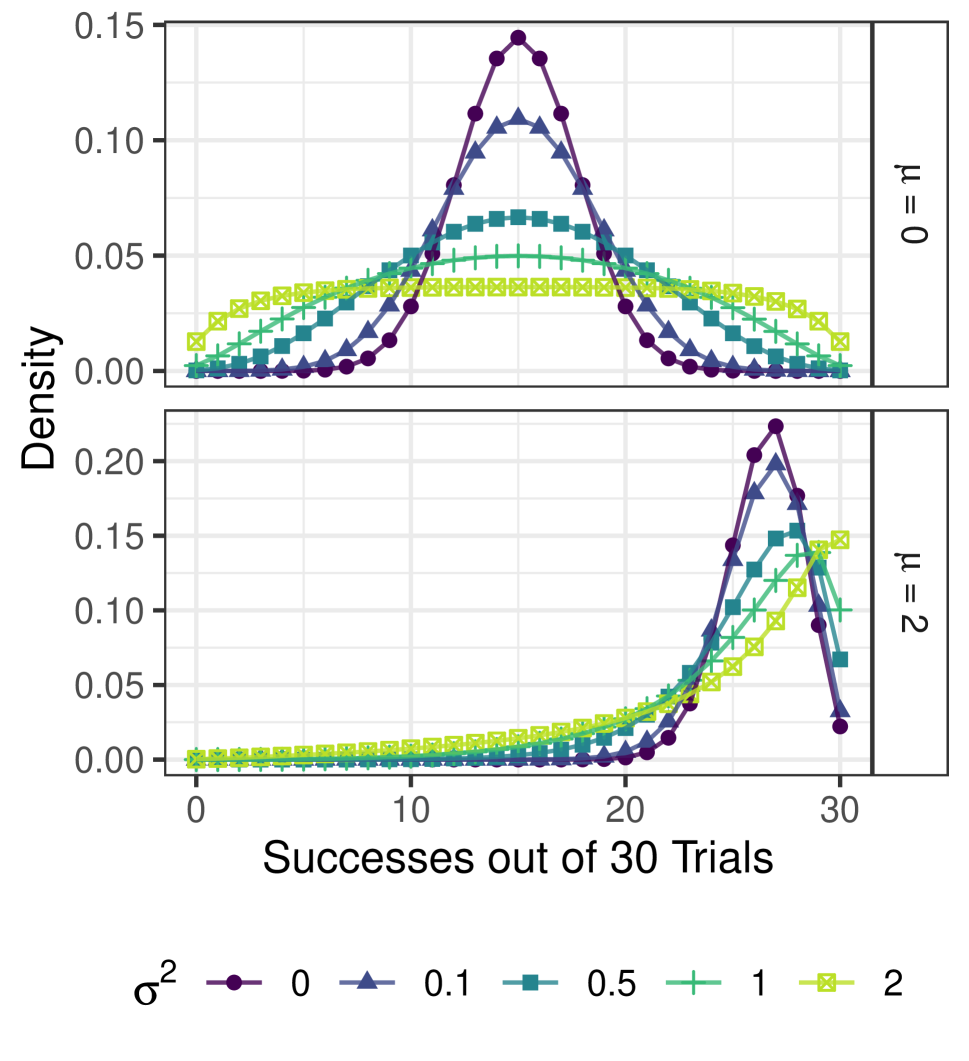

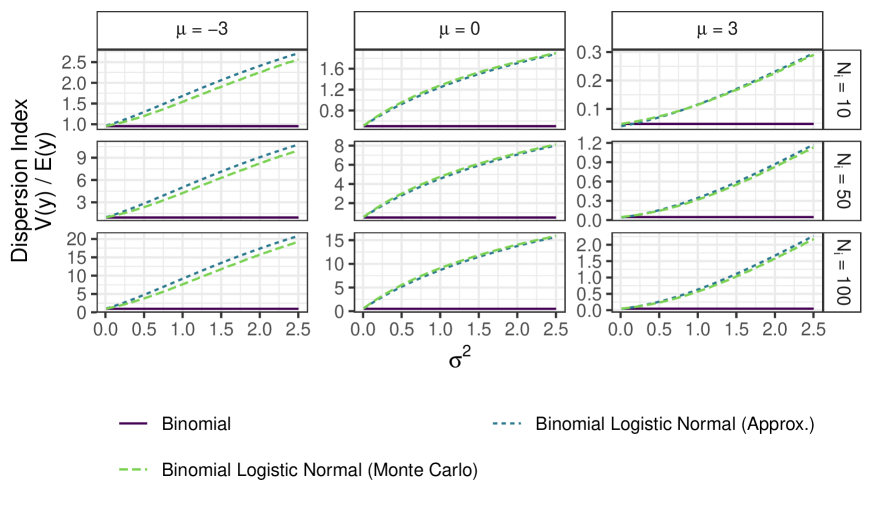

The BiL model represents another important member of the ULLGM family, generalising a Binomial model. To address overdispersion, it employs a logistic-normal distribution for the success probabilities of individual observations (Aitchison and Shen, 1980). Illustrations of pmfs of Binomial logistic normal distributions are provided in 1(b), underscoring the role of as overdispersion parameter. BiL regression constitutes a highly flexible alternative to Beta-Binomial regression models for the analysis of overdispersed binomial outcomes. Although analytical expressions for the moments and are not known for a logistic link function, approximate results can be derived, such as

| (5) |

for a suitable value of , where is the cdf of a standard Gaussian random variable. Full details and an approximation of the variance are provided in Appendix A1. From (5), the interpretation of the coefficients and error variance is intuitive in the BiL model. As the value of increases, the impact of the coefficients is more muted. Also, can be shown to approach the usual binomial variance for . Similarly, the dispersion index tends to the binomial dispersion index for , but is larger than the binomial dispersion index when , as also shown in Fig. A1; see Sec. A1 for more details.

2.2 Advantages of the ULLGM class

As previously discussed, for most underlying distributions , the ULLGM specification intuitively allows for overdispersion, which is regulated by the extra parameter in (2). In regression analysis, failing to account for overdispersion can lead to an underestimation of the standard errors. In the context of model selection and model averaging, ignoring overdispersion can lead to a preference for overly complex models, which compensate for the inability to account for the extra variation in the outcome. This undesirable phenomenon is illustrated for Poisson and Binomial regression models in Supplementary Sec. A3.

In addition, the structure of the models in the ULLGM class in (1) and (2) has a number of theoretical and practical benefits. Firstly, in the context of model uncertainty, the tractability of the Gaussian distribution lends itself to convenient applications of standard BMA methods. In particular, the parameters and can be integrated out analytically with a popular and convenient prior, conditionally on . This greatly simplifies the computational implementation (see Section 5) as well as the characterisation of posterior existence under this improper prior (see Section 4.1). The computational implementation is simple, allows for exact inference, and is significantly more flexible (e.g., accommodating situations where ) and often more efficient than related approximate and exact model averaging tools for generalized linear models (GLMs). In addition, the computational strategy can easily be modified to accommodate other members of the ULLGM class.

For specific ULLGM models, anecdotal empirical evidence suggests that relying on Gaussian error terms in the latent linear specification often provides superior model fits compared to allowing for overdispersion using non-Gaussian terms, such as log-Gamma errors in negative binomial regression models (Winkelmann, 2008; Tsionas, 2010). The Gaussian latent specification also holds theoretical merit, as normal error terms can be justified by a central limit theorem, if they capture a sum of latent shocks to the linear predictor. Finally, ULLGMs possess great potential for relatively straightforward generalization to multivariate settings with correlated observations (Aitchison and Ho, 1989; Chib and Winkelmann, 2001).

Certain limiting cases of ULLGM models are closely related to Gaussian regression models. For example, as , the PLN model converges to a Gaussian regression model with outcome . Similarly, as , the BiL model converges to a Gaussian regression model with the outcome , see Sec. A4 for further discussion. However, the ULLGM class has a number of key benefits compared to such Gaussian approximations. For example, ULLGMs do not rely on (potentially crude) approximations, provide valid uncertainty quantification and can naturally handle zero outcomes.

2.3 Model uncertainty

Given the model class defined in (1) and (2), the goal is to design a theoretical framework and a computational strategy for posterior and predictive inference, in the face of model uncertainty. Specifically, we are interested in model uncertainty with respect to inclusion and exclusion patterns of the components of the regression coefficient vector . Models will thus be characterized by the inclusion or exclusion of any of the columns of , which is the matrix with as its th row. We denote the total number of potential covariates in by while indicates the number of covariates from that are included in model . An intercept term is included in all models. This gives us a model space with elements and for model the distribution of now becomes

| (6) |

where is a column vector of ones, is the -dimensional identity matrix, consists of the columns of that correspond to the regressors that are included in and groups the corresponding regression coefficients. The regressors in are standardized by subtracting their means, which makes them orthogonal to the intercept and renders the interpretation of the intercept common to all models.

2.4 ULLGMs with random

Sofar, we have focused on inference on the scalar observation-specific parameter, represented by for observation . We now consider situations where we also want to conduct inference on other parameters added to the model, grouped in and common to all observations. We will assume that is a priori independent of given a model within the set of models described in subsection 2.3:

| (7) |

Examples are the NBL and ErLN models, where we now allow to be an unknown parameter on which we conduct inference, rather than simply fixing it. In these models, is an integer scalar and it would be natural to assume (7) holds.

3 Prior Specification

We will focus on the prior setup that is most often encountered in the context of BMA. For the linear regression model in (6) taken in isolation, this prior satisfies many of the desiderata of Bayarri et al. (2012) for objective priors, such as measurement and group invariance and exact predictive matching. Specifically, we assume an improper, ’non-informative’ prior on the parameters common to all models

| (8) |

which is a convenient prior that has the advantage of being invariant with respect to rescaling and translating the s. For the regression coefficients , we adopt a so-called -prior which is invariant under affine linear transformations of the covariates

| (9) |

where . Throughout, we will assume that the matrix formed by adding a column of ones to is of full column rank. If the model space contains models for which this is not the case (for example because ), we will assign prior probability zero to those models.222This can be easily implemented while running the MCMC sampler, without needing to restrict the total number of possible covariates . Alternative approaches to use -priors in situations where can be found in Maruyama and George (2011) and Berger et al. (2016), based on different ways of generalizing the notion of inverse matrices. The scalar can either be fixed or assigned a hyperprior as described in, e.g., Liang et al. (2008) or Ley and Steel (2012). We will consider both fixed and random when illustrating the framework in later sections. For BMA or model selection we require well-defined pair-wise Bayes factors between all models in the model space. In case a hyperprior is specified on , it is necessary to take into account that does not appear in the null model (with ). Hence, a proper is necessary in order to ensure meaningful model comparisons. For the null model with no regressors and only an intercept, the prior will simply be (8). Components of that correspond to excluded regressors under are assigned a prior point mass at zero for that model.

As a prior on the model space, we employ the beta-binomial structure of Brown et al. (1998a), Ley and Steel (2009) and Scott and Berger (2010), which amounts to using a Beta prior on the common prior inclusion probability for each covariate and results in

| (10) |

This type of prior is less informative in terms of model size than fixing the prior inclusion probability of the covariates. Following the suggestions of Ley and Steel (2009), we choose and , where is the prior expected model size. This means that the user only needs to specify a value for . If there are any additional parameters as in Subsection 2.4, we specify a proper prior on , satisfying (7).

4 Posterior Results

If we combine the -prior setup proposed in Section 3 with the sampling model in (1) and (6), the conditional posterior distributions and the marginal likelihoods of the latent data can be easily derived. We summarize the posterior on the model parameters as follows:

| (11) |

where ,

| (12) |

with and

| (13) |

where for any matrix of full column rank. Finally, the marginal likelihood under fixed is

| (14) |

where is the coefficient of determination of regressed on (and an intercept) and the proportionality constant is the same for all models, including the null model for which . Under random with hyperprior , the marginal likelihood is

| (15) |

4.1 Posterior existence

The prior for each given model is improper, as can be seen from the prior specification on the common parameters shared by all models in (8). Thus, we need to make sure that the posterior distribution of the parameters in each model is well-defined in the sense that the marginal likelihood is a finite quantity for each possible value of the observations . We can state the following for cases where the possible additional parameter is fixed:

Theorem 1: If we combine the sampling model in (1) and (6) (ULLGMs defined in Table 1) with the improper prior structure in (8) and (9), then the posterior is well-defined for any model in the model space, if and only if the matrix composed of a column of ones and has full column rank and, in addition, the following condition holds:

-

•

for the PLN and NBL models: at least two of the observations are nonzero;

-

•

for the BiL model: at least two observations are nonzero and smaller than , where is the number of trials for observation ;

-

•

for the ErLN, LNN and LNLN models: we have at least two observations.

The ULLGM models based on Bernoulli sampling (the BeC models) do not allow for a posterior under the prior in (8) and (9).

Proof: See Appendix A5.

Theorem 1 provides necessary and sufficient conditions for all the models in Table 1 that are not based on Bernoulli sampling, and thus fully characterizes posterior propriety for these ULLG models.

For models where the additional parameter is treated as random as in Subsection 2.4, we can derive the following:

Theorem 2: If we combine the sampling model in (1) and (6) with the improper prior structure in (8) and (9), along with a proper prior on , satisfying (7), then the posterior is well-defined for any model in the model space, if the corresponding model with fixed leads to a proper posterior and if, in addition

| (16) |

where we have defined

| (17) |

Proof: See Appendix A6.

An immediate consequence of Theorem 2 is that the NBL model and the ErLN model with random have proper posteriors under any proper prior on respecting (7), since is constant in for these models (see sections A5.2 and A5.4). The situation is quite different for the LNLN model where Appendix A6 shows that we can not conclude that posterior inference on can be conducted with the overall prior structure assumed here.

5 Computational Considerations and Implementation

For PLN models, traditional maximum likelihood methods can yield unreliable parameter estimates even in simple scenarios, as highlighted in Tsionas (2010). As an alternative, Tsionas (2010) focuses on a Bayesian treatment of the univariate PLN regression setting, using an expectation-maximization algorithm for model estimation. MCMC estimation for the PLN model and extensions to -distributed noise distributions are discussed in Chib and Winkelmann (2001). However, these contributions do not account for model uncertainty. Likewise, although estimation of BiL frameworks has been examined previously (Coull and Agresti, 2000), model uncertainty is typically not addressed.

The computational strategy we propose is based on the observation that, conditional on , the posterior distributions of the latent Gaussian regression parameters, along with the marginal likelihoods and Bayes factors, assume a simple and convenient form. Hence, data augmentation, where the observed data is augmented with a posterior sample of , is a natural choice for a posterior simulation strategy (Tanner and Wong, 1987). Given , the parameters , , and can then be updated using a simple Bayesian regression update.

To conduct inference under model uncertainty, we construct a partially collapsed Gibbs sampler over latent outcomes, regression parameters, and models. In particular, defining , we iterate between drawing from and from where the second step is composed of drawing from and , which are both simple to simulate from. A similar blocking strategy for MCMC in latent Gaussian models is suggested in Geirsson et al. (2020). Details of the MCMC algorithm are summarized in Algorithm 1.

To obtain a sample of , note that its conditional posterior distribution can be written as the product of a likelihood term defined via (1) and a Gaussian ’prior’ term (6). This factorization implies that the s are all conditionally independent, given the remaining parameters and the data. Consequently, independent univariate updates can be performed, one for each , in each iteration of the Gibbs sampler. To simulate from , a simple strategy is to employ independent random-walk Metropolis-Hastings updates for all . However, the simple structure of renders gradient-based methods a convenient and more efficient alternative. In the ULLGM framework, gradients of the likelihood and priors are typically available analytically and inexpensive to compute. We found that updating using an adaptive version of the Barker proposal from Livingstone and Zanella (2022) offers a good balance between mixing speed and robustness of the algorithm. Robustness is particularly important in certain ULLGMs, such as those involving the Poisson distribution, where gradient-based methods may exhibit numerical instabilities. The adaptive MCMC scheme we implement is based on diminishing adaptation rates, aiming for an acceptance probability of 0.57 for each (Roberts and Rosenthal, 2009). We provide the log posterior gradients of for selected models in Supplementary Sec. A7.

When is weakly identified by the likelihood, the proposed data augmentation scheme can induce some autocorrelation in the posterior draws.333For the PLN and BiL models, likelihood identification of a given becomes weaker when either the count is close to zero (PLN) or the number of trials is close to one (BiL); see Supplementary Sec. A4 for details. Nonetheless, the proposed algorithm is straightforward to implement and strikes a favorable balance between computation time and sampling efficiency. Moreover, it integrates effortlessly into the standard BMA framework. In contrast, conventional posterior simulation algorithms for high-dimensional non-Gaussian regression models often encounter significant difficulties, such as low sampling efficiency, expensive repeated likelihood evaluations, or the necessity for complex algorithmic techniques like Hamiltonian Monte Carlo. Extending conventional non-Gaussian regression model algorithms to handle model uncertainty efficiently is also challenging, as gradient-based methods can struggle with discrete sampling spaces, motivating approximate methods or intricate and computationally intensive reversible jump MCMC algorithms. In comparison, the ULLGM framework only requires very basic algorithmic techniques and knowledge of model averaging in linear Gaussian models, making it a simpler and more accessible approach while not relying on approximations. In addition, it allows for an easy adaptation of the general sampler in Algorithm 1 to accommodate specific members of the ULLGM class, simply by modifying the update of the latent variables .

For model proposals, we utilize an add-delete-swap (ADS) algorithm where each iteration involves adding, deleting, or swapping variables to create a new model proposal. This method has proven effective for the scenarios we examined. For very high-dimensional applications, future research might extend adaptive model proposals as suggested in Zanella (2020), Griffin et al. (2021), and Liang et al. (2023) to the ULLGM context. Details on the ADS proposal can be found in Sec. A8.

Assuming is random requires only minor modifications to the MCMC scheme outlined above. Given a prior density , we follow Ley and Steel (2012) and construct a Gibbs sampler that jointly explores latent outcomes, regression parameters, models, and values of . This entails, in addition to the ’within-model’ update steps for , , and , simulating a new value of . We use a univariate Metropolis-Hastings step with proposal mechanism . The corresponding acceptance probability involves the prior , the marginal likelihood in (14), and the appropriate Jacobian, accounting for the proposal on the log-scale, and is given by . Similar to the adaptive approach for , the update utilizes adaptive MCMC techniques, aiming for an acceptance rate of . Consequently, the Gibbs sampler is fully automatic, requiring no manual input beyond the initial prior specification. Finally, if additional auxiliary parameters are involved, the MCMC scheme can be expanded to a Gibbs sampler that jointly explores latent variables, regression parameters, models, , and auxiliary parameters. These auxiliary parameters will typically be univariate or low-dimensional, rendering further (adaptive) Metropolis steps a viable sampling strategy.

6 Applications to Simulated Data

To assess the effectiveness of the PLN and BiL model averaging algorithms, we used simulated data, varying both the number of observations ( and ) and the number of regressors ( and ), while using for the BiL model. In all scenarios, the linear predictor was defined as , where the first ten regression coefficients were non-zero. The coefficients were specified as:

The regressors were drawn from a normal distribution with mean 0 and covariance matrix , where , determined by a correlation coefficient . We used in our examples, representing a challenging setting with relatively high correlation among the regressors.

To test the resilience against misspecification, we utilized three different DGPs to generate the latent outcomes . First, we added noise terms from with to the linear predictor (the ULLGM case). In the second setting, we used a noise-free linear predictor (), corresponding to a GLM setting. Finally, we added logarithmic samples from (a gamma distribution with mean one and variance ) as noise to the linear predictor. The implied error distribution has a variance of approximately 0.2, but is skewed and has a non-zero mean.

Regarding the prior setup, we choose to favor sparse models. We compared two settings for . Firstly, a ’unit information prior’ that fixes , a popular and empirically successful default in many BMA applications (Kass and Wasserman, 1995). The second setting accounts for theoretical shortcomings of fixed (Liang et al., 2008) by letting be random using a hyper- prior, as favored in Ley and Steel (2012). For each of the 24 settings per model, we simulated 100 replicate data sets, collected several measures of accuracy – such as the Brier score, false positive and negative rates and expected model size – and averaged the results. In each model run, we collected 300,000 posterior samples after an initial burn-in of 250,000 iterations.

Detailed results of the simulation study are summarized in Table A1 in Appendix A9. They suggest a reasonably high level of accuracy across all settings. In general, the simulation results are in line with what one would expect, for instance increasing accuracy with increasing . The simulation runs indicate that the ULLGM framework performs well, even in situations with challenging signal-to-noise ratios and in scenarios with misspecification of the sampling model, implying a certain level of robustness of the ULLGM framework for variable selection and model averaging. In terms of prior choices, we find the unit information prior to be slightly more robust in the settings we investigate, with the hyper- prior showing a tendency to favor slightly larger models. In general, a certain sensitivity of model averaging outcomes to prior settings is well documented in the literature and warrants a careful comparison of results based on a range of priors in applied contexts.

7 Real Data Applications

7.1 Measles Vaccination Coverage in Ethiopia

Vaccination coverage rates are a key metric for assessing the performance of national health and immunization systems. Such performance indicators are, however, generally measured using national statistics or at the scale of large regions. This is often due to the design of surveys, administrative convenience, or operational constraints. This approach can obscure subnational variations and ’coldspots’ of low coverage, potentially allowing diseases to persist even when overall coverage rates are high. Hence, to reduce health inequalities and make steps towards disease elimination targets, it is crucial to more accurately characterize fine-scale variations in coverage. Growing demand for subnational health metrics has led to significant interest in empirical models that provide regional vaccination coverage estimates, along with the uncertainties associated with these estimates (Utazi et al., 2018). These efforts often rely on Binomial models, which forms the basis of the BiL model in Table 1. These models typically incorporate a regression function and spatial smoothing mechanisms, but usually do not address model uncertainty.

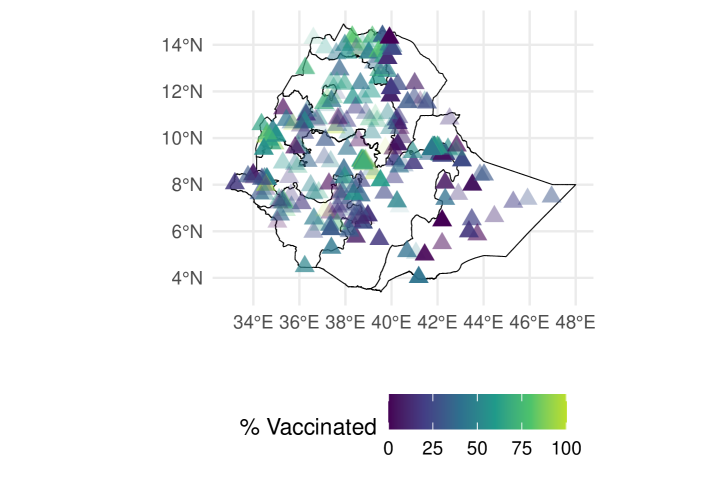

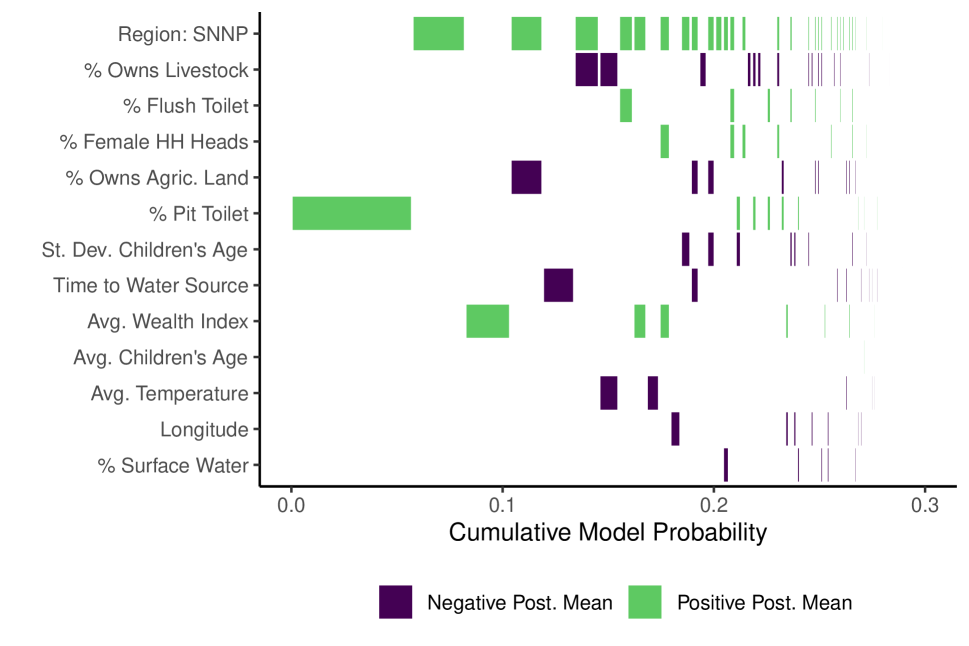

Given the potential effectiveness of BMA as a predictive tool, we employ the BiL model to analyze data on vaccination coverage in Ethiopia. Specifically, we utilize data from the 2019 Demographic and Health Survey (DHS) in Ethiopia.444The DHS Program provides comprehensive, nationally representative survey data on population, health, and nutrition in over 90 countries worldwide. The data is collected in survey clusters, with a cluster typically consisting of 25-30 households, representing for example a rural settlement or an urban neighborhood. The dataset includes a total of clusters. For each cluster, we record , the number of children born in the three years before the survey who have received the first dose of a measles (or measles-containing) vaccine, out of , the total number of children born within the same period whose vaccination status is known. The observed vaccination rates within these clusters vary from 0% to 100%, with an average rate of 44.8% across all clusters. A map illustrating the distribution of survey clusters across Ethiopia and their respective sample estimates of vaccination coverage rates is presented in Supplementary Fig. A6. On this map, clusters with lighter coloring indicate a smaller local sample size , implying a smaller influence of cluster on the BiL parameter estimates.

We gather a set of potentially relevant predictors of vaccination rates and apply BMA to identify a robust subset of determinants. The covariates include a variety of factors that are related to health outcomes, such as regional sociodemographic characteristics, household living standards, and proxies for local economic development like a satellite-based nightlight intensity measure. Additionally, the covariates cover climatic conditions, measures of accessibility of different regions, and several nutritional scores based on anthropometric measurements of children in the survey clusters. To account for latent spatial variation in vaccination rates, we also incorporate indicators for Ethiopia’s 11 regions and GPS-based data on the clusters’ latitude, longitude, and altitude. This set of covariates encompasses a range of variables that can be found in most DHS surveys or can be collected from publicly accessible sources. Therefore, this analysis might hold broader interest beyond the Ethiopian case study presented here. Detailed information on the full set of covariates, along with summary statistics, is provided in Supplementary Table A2.

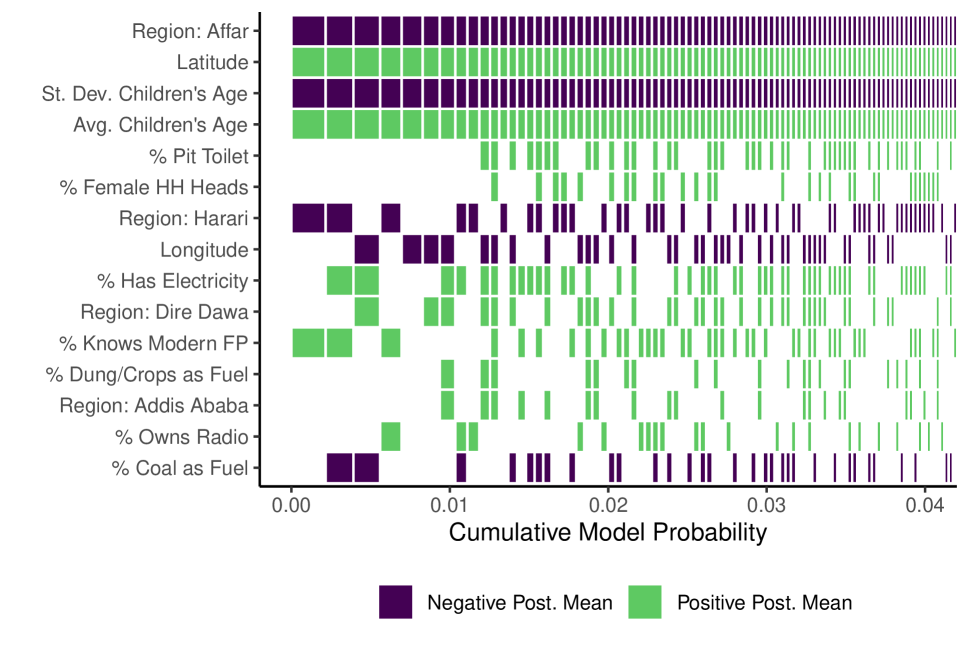

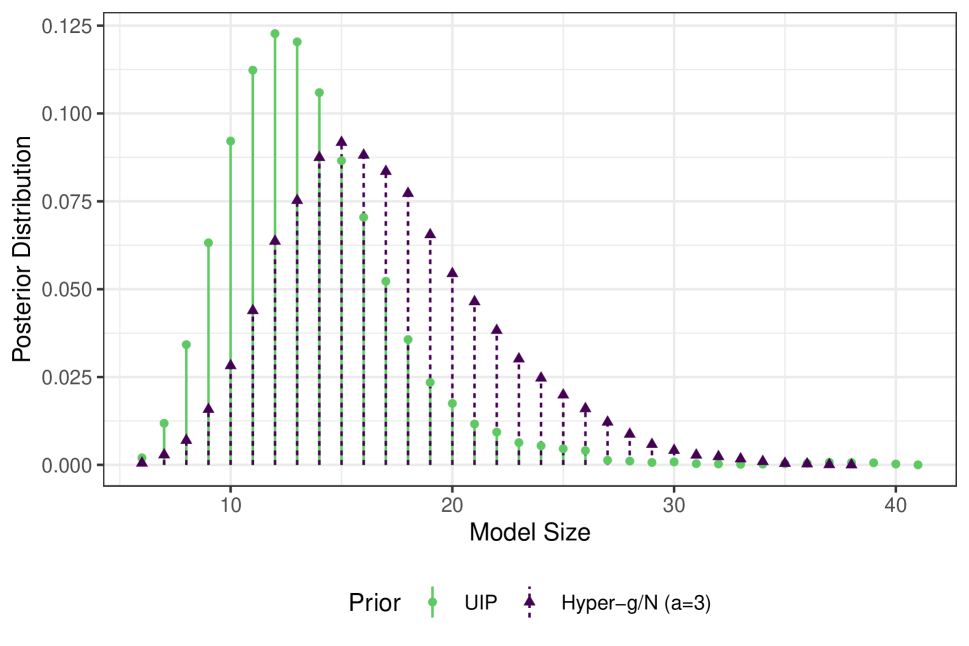

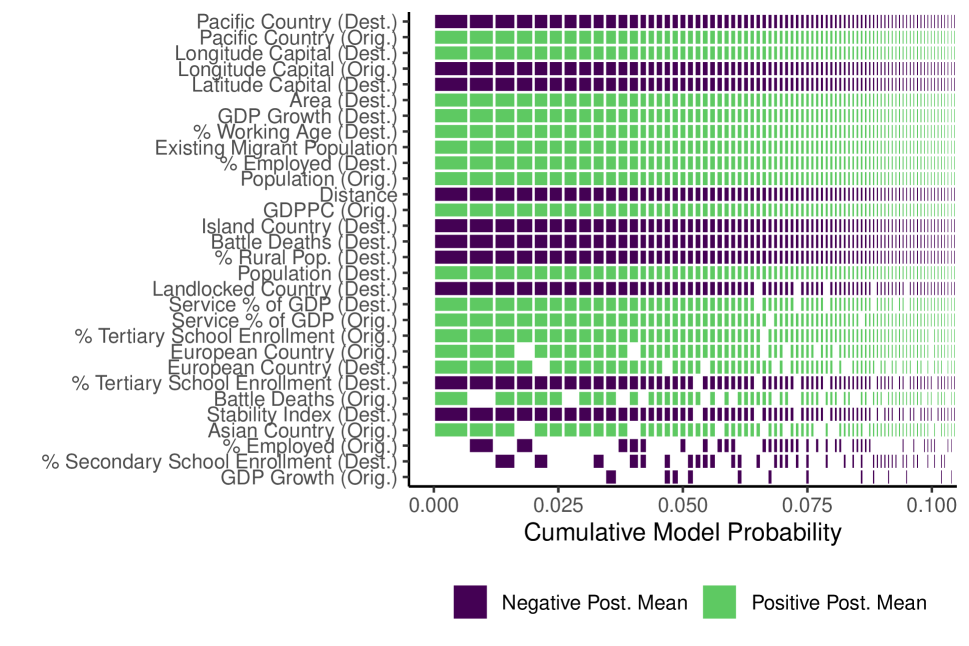

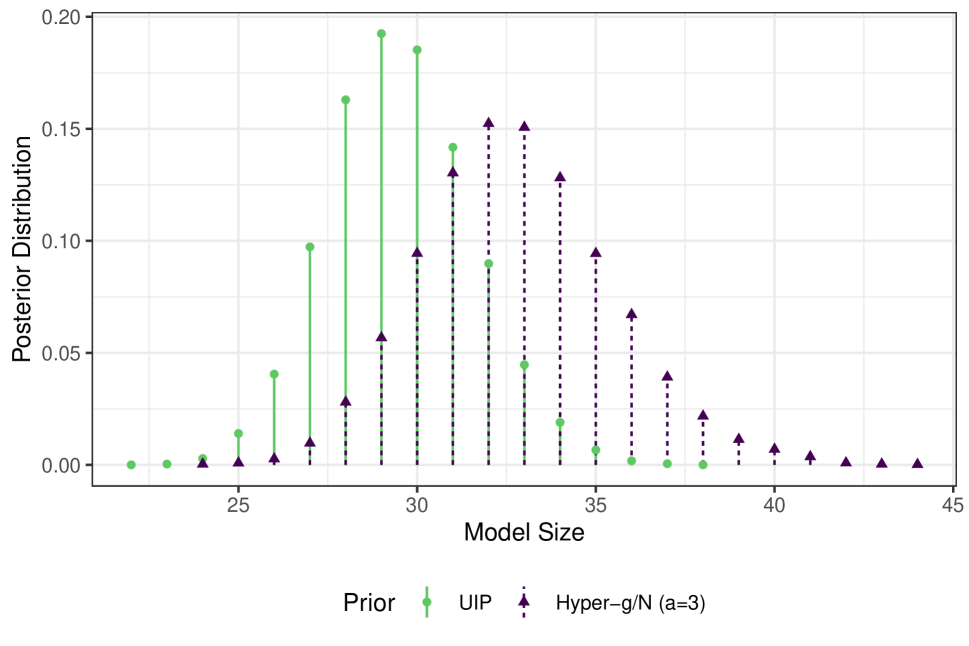

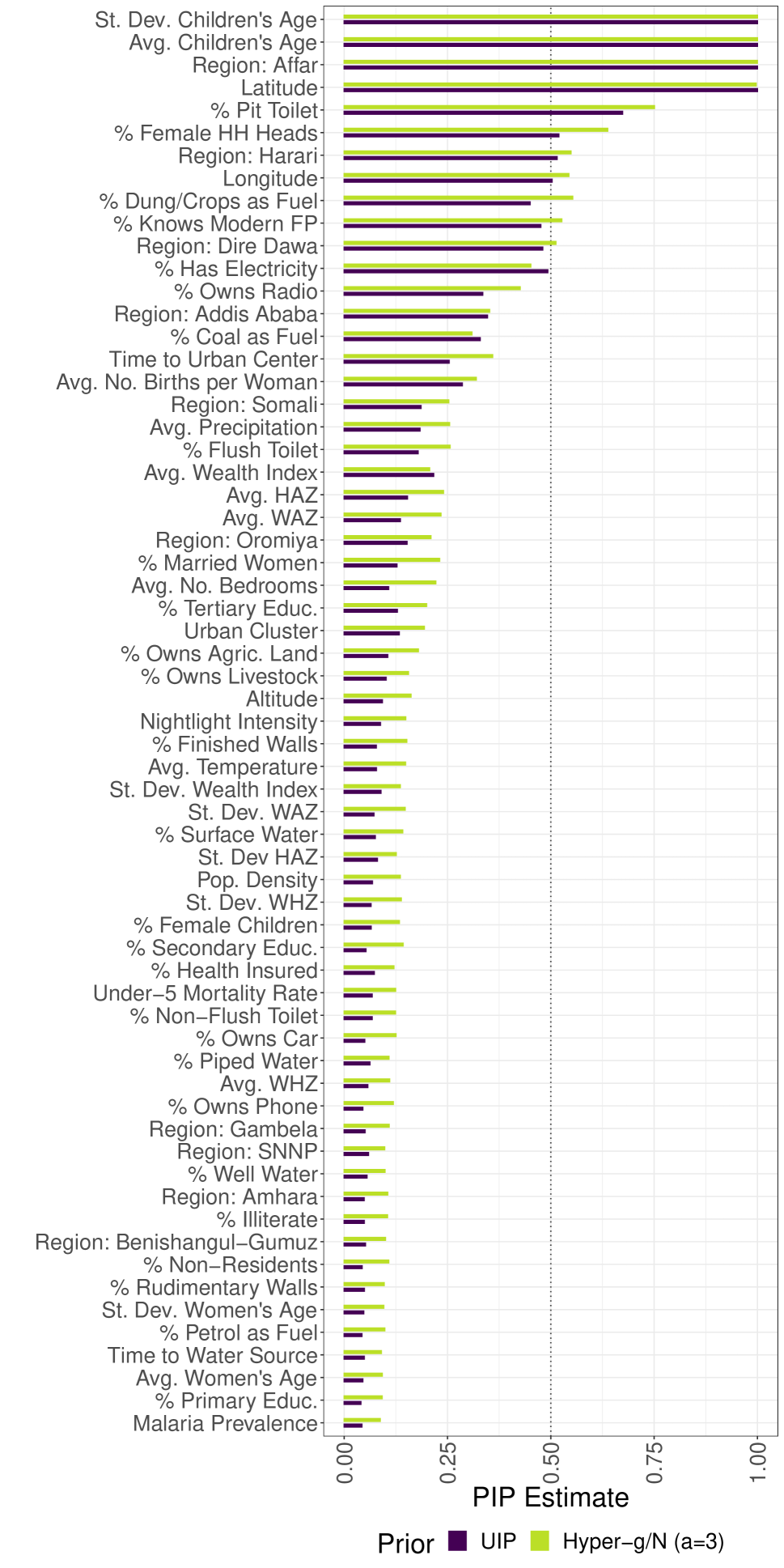

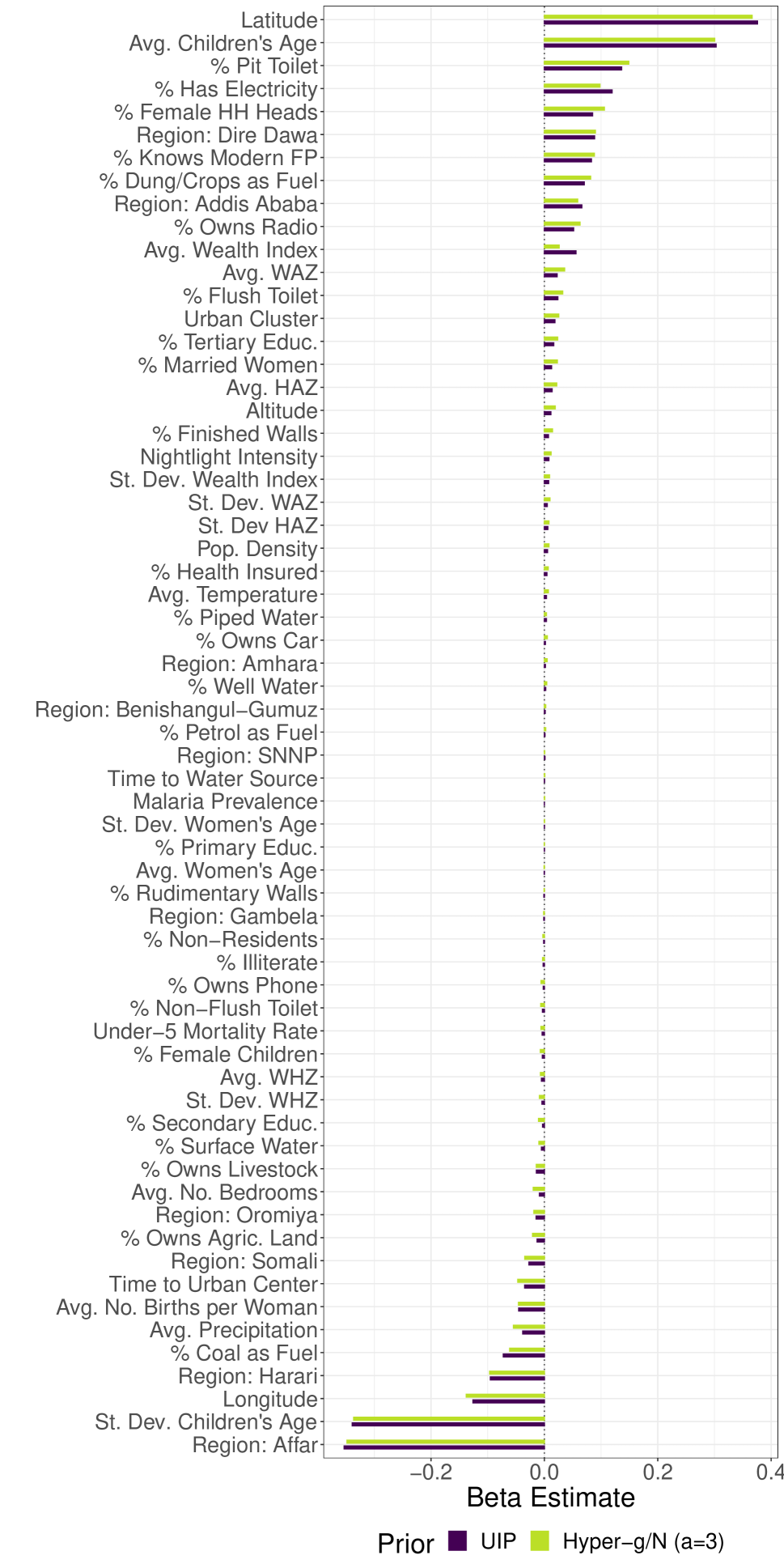

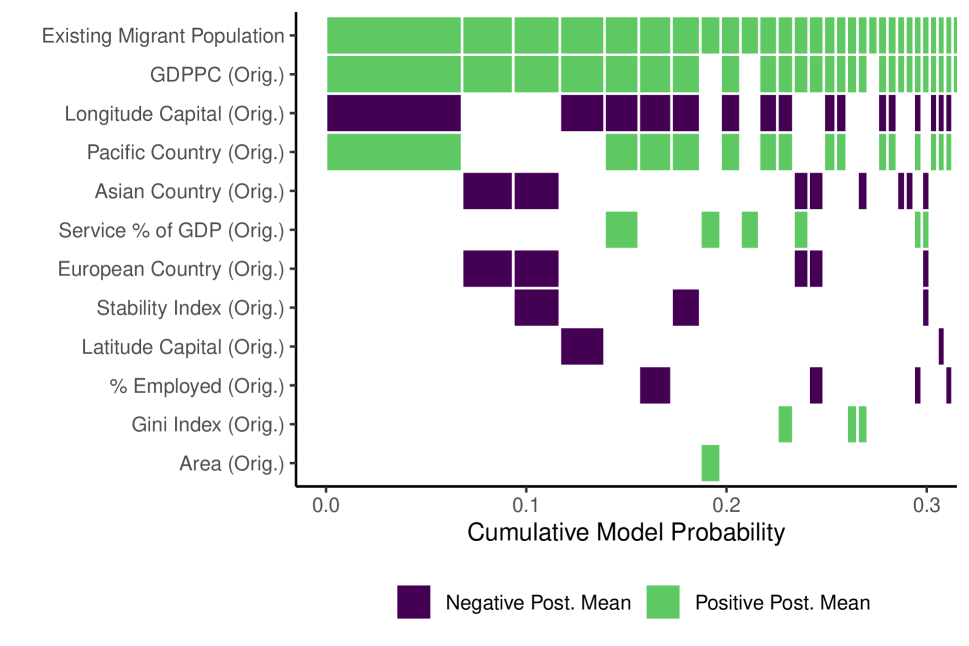

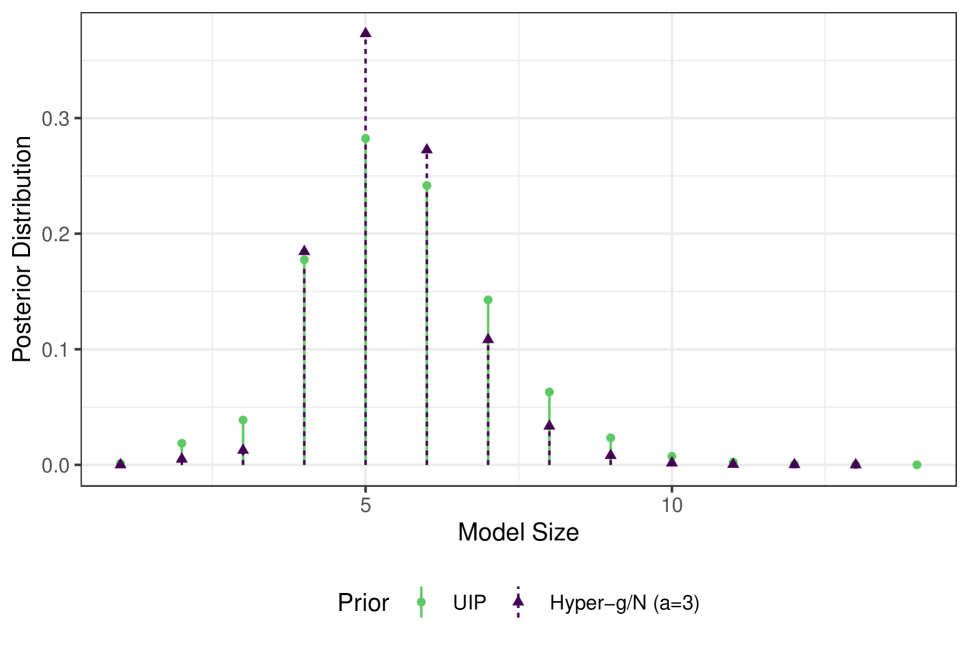

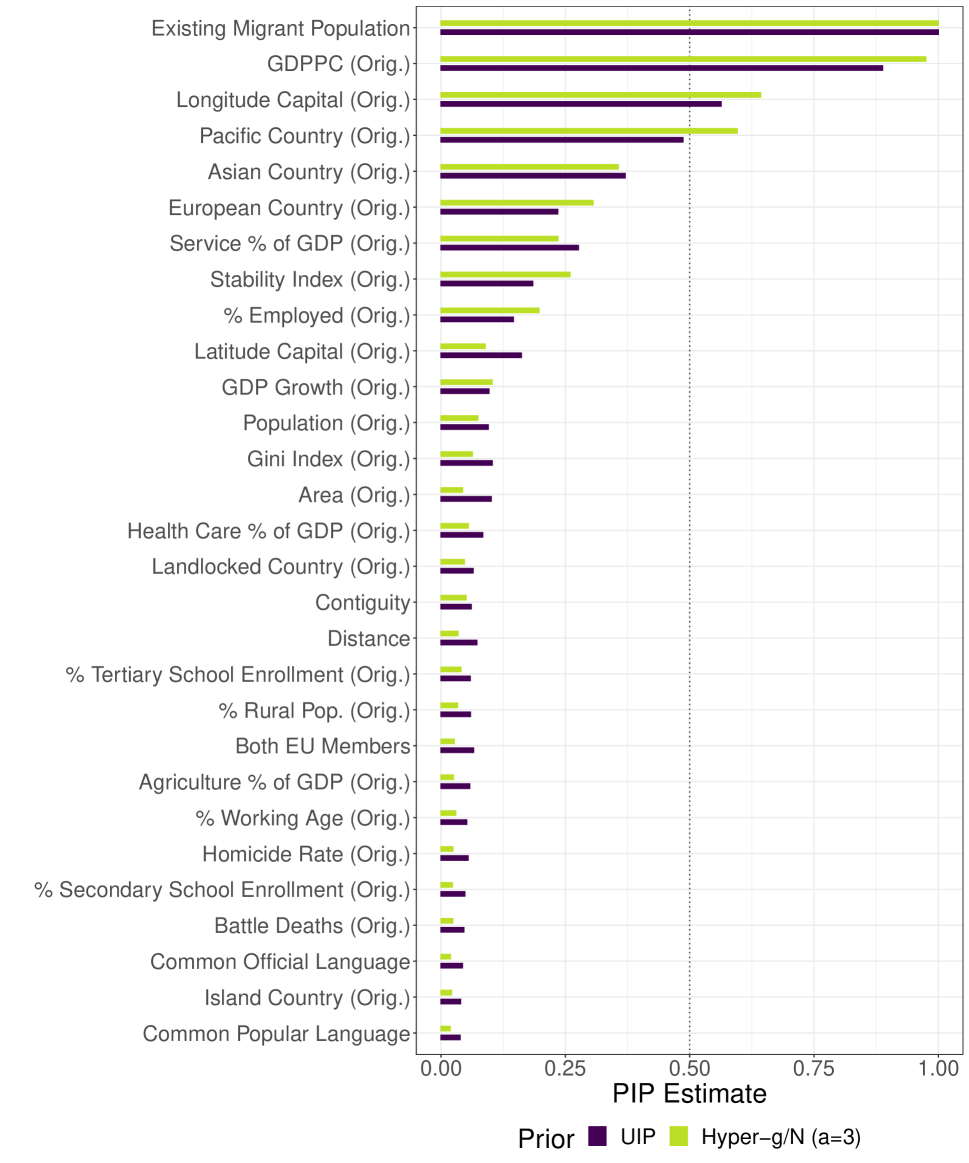

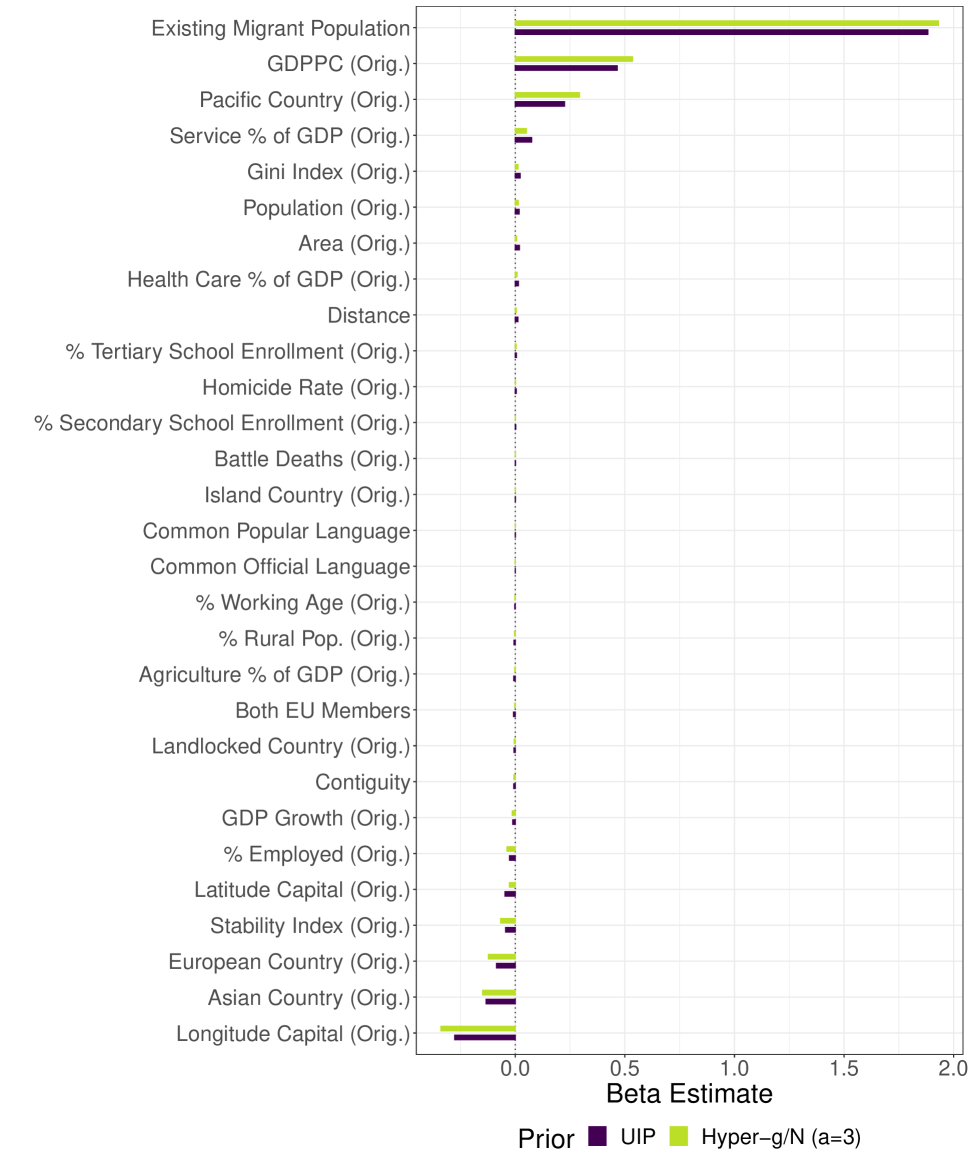

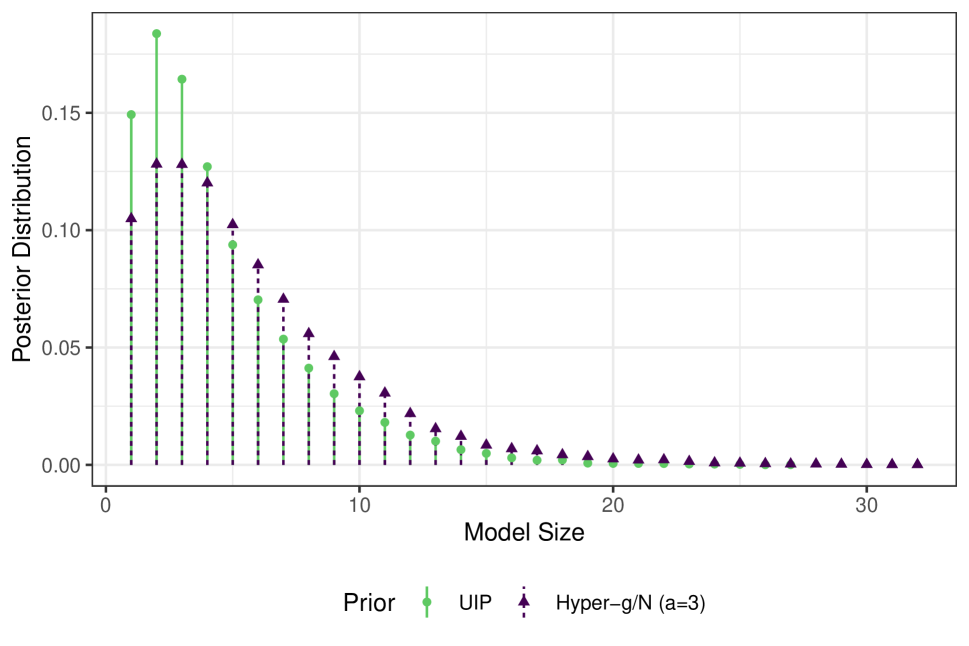

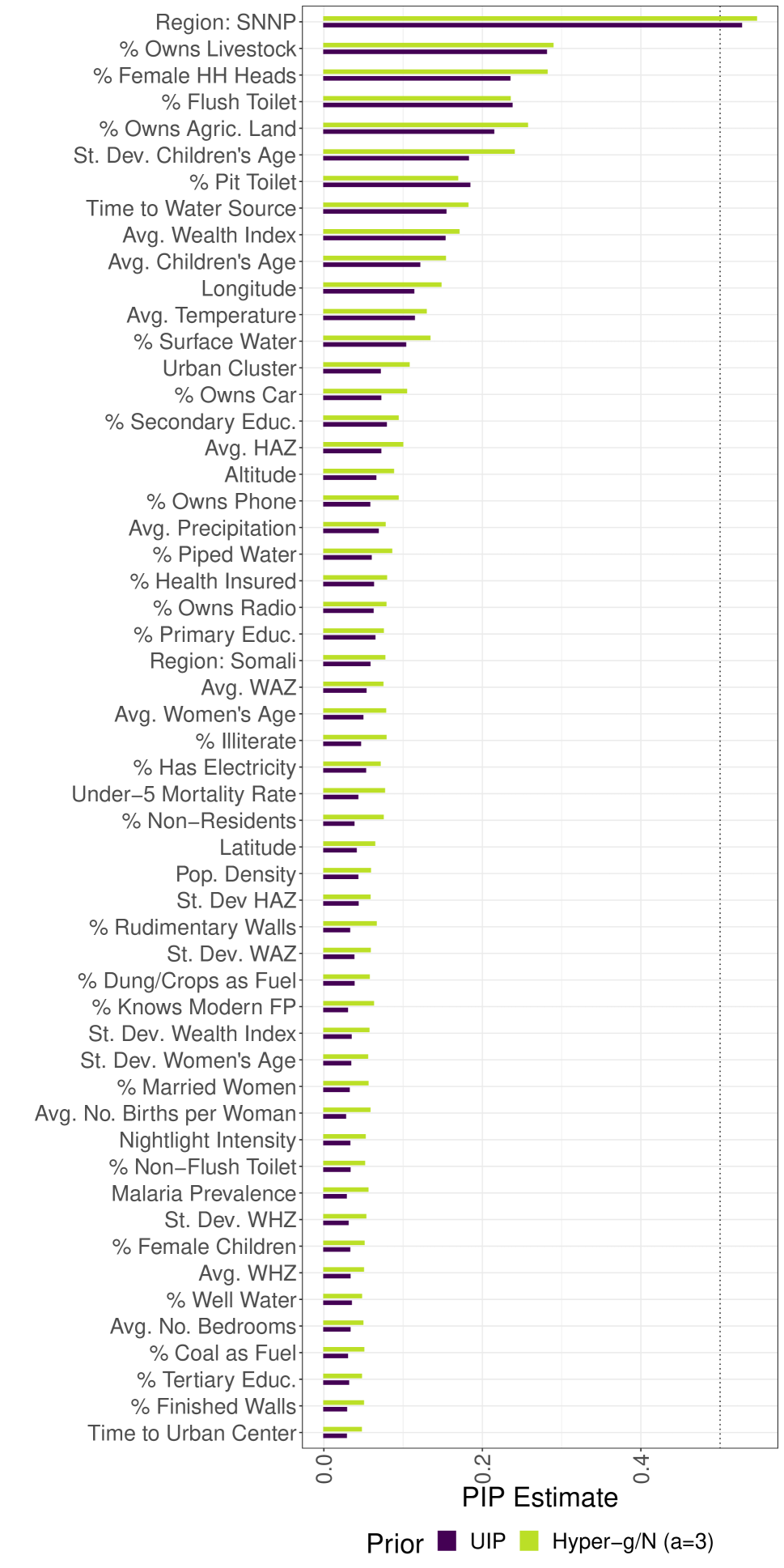

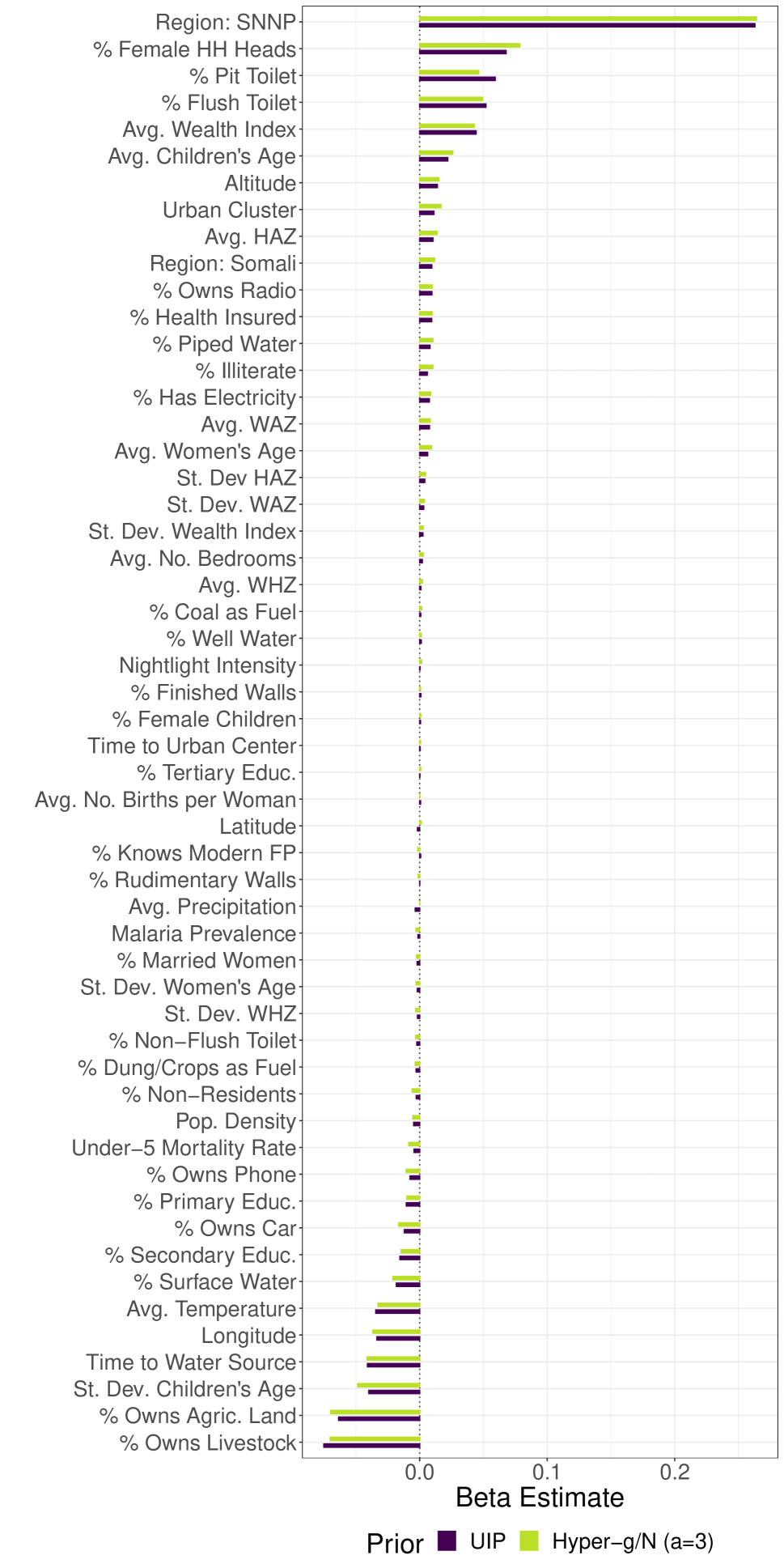

We implement the BiL model using the algorithm described in Section 5, under a UIP prior () and a hyper- () prior, alongside an agnostic uniform prior on model size (). The analysis is based on posterior draws, collected following a burn-in phase of iterations. We provide the estimated posterior inclusion probabilities and posterior means of in Supplementary Fig. A7. Under both priors, the posterior means of the intercept are while under the unit information prior and under the hyper- prior. 2(a) shows the highest probability models under the unit information prior, while 2(b) illustrates the posterior distributions of model size, indicating a slight preference for larger models under the hyper- prior (which tends to lead to somewhat smaller values for ). The median probability models, which include those covariates with a posterior inclusion probability (PIP) greater than , agree on eight influential variables. The average age of children in a cluster is strongly positively associated with vaccination rates, likely due to increased interactions with healthcare systems over time and the fact that vaccines are typically not scheduled for administration directly after birth, decreasing the likelihood of very young children being vaccinated. Conversely, a larger standard deviation in children’s ages within a cluster, indicating a more dispersed age distribution, is significantly associated with lower vaccination rates, suggesting that age homogeneity can enhance the effectiveness of health interventions and vaccination campaigns. Such uniformity may support more targeted health education and vaccination efforts, encourage communal sharing of health information, and enable healthcare providers to better plan and deliver vaccination services to the predominant age group, thereby boosting overall coverage. The significant positive relationship between latitude and vaccination rates suggests higher coverage in northern clusters, while the pronounced negative impact of being in the Affar region—characterized by remoteness, pastoralist communities and regional political tensions — indicates unobserved factors affecting spatial variations in vaccination rates. Model probabilities are in general relatively spread out, reflecting a rather high amount of collinearity among the covariates. The highest probability models are detailed in Supplementary Table A4 and Table A5. Numerical results on estimated posterior means, standard deviations, and inclusion probabilities are available in Supplementary Table A3.

7.2 Bilateral Migration Flows Between OECD Countries

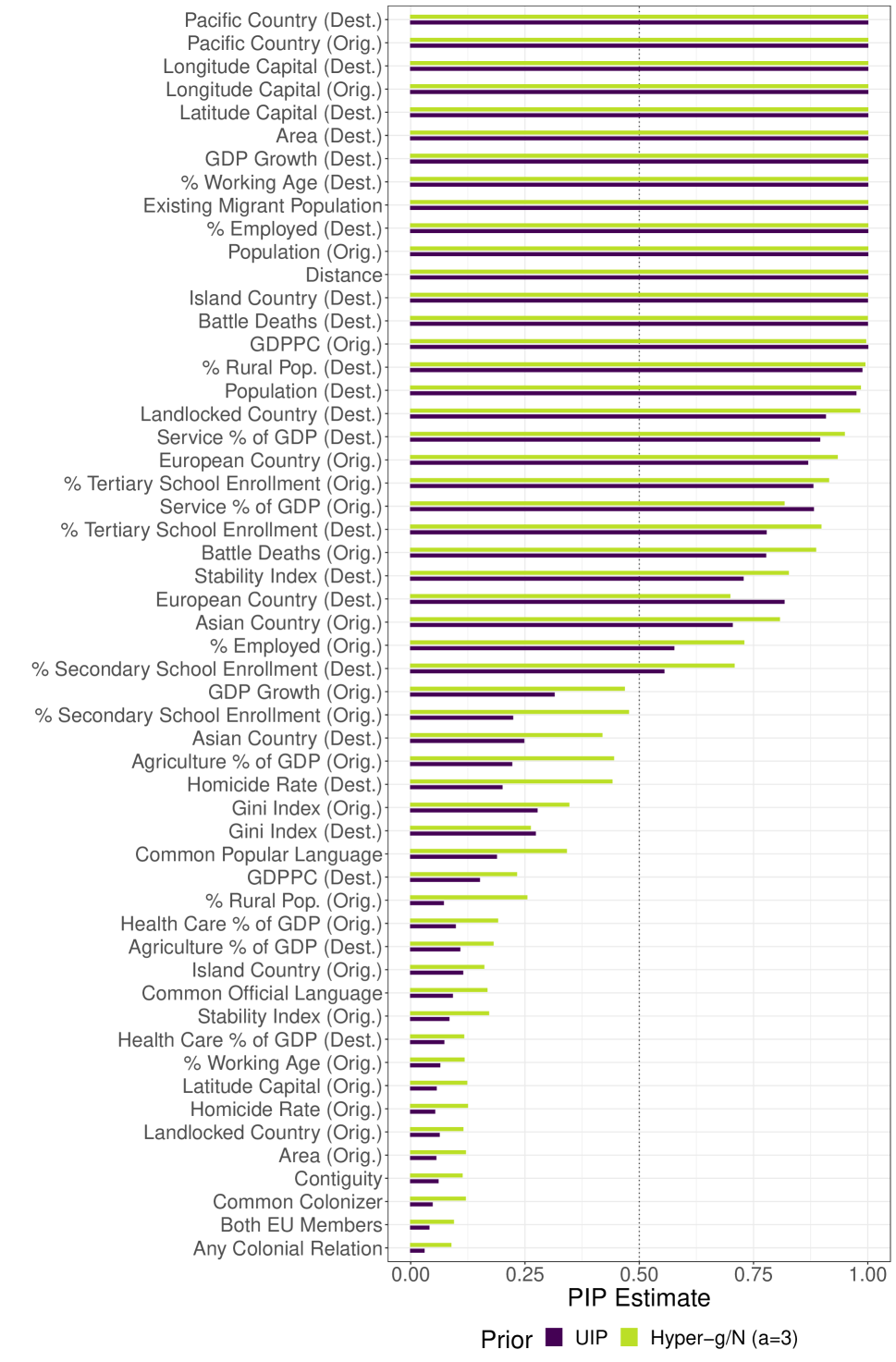

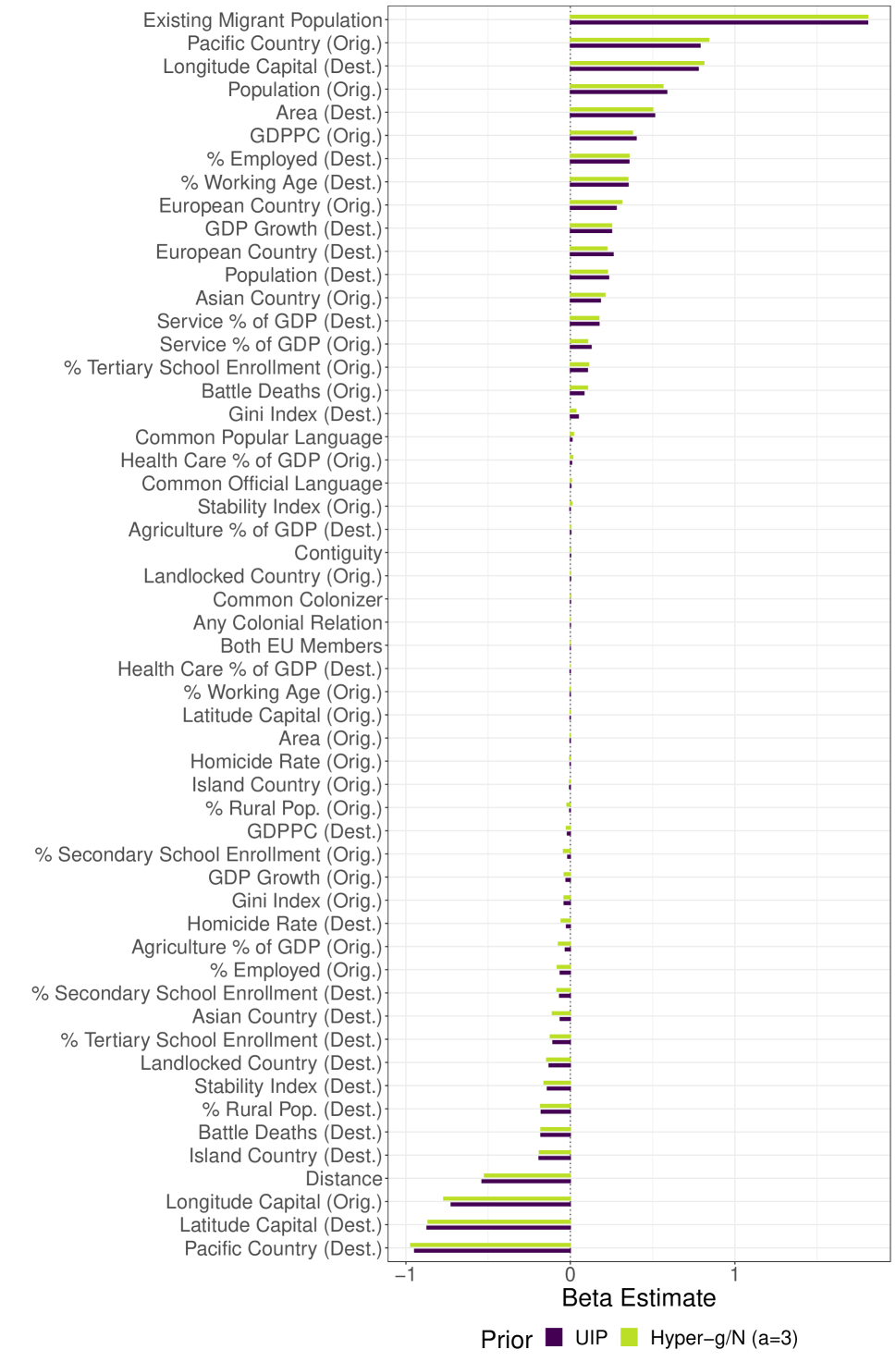

We use the PLN model to examine migration flows between the 38 OECD countries from 2015 to 2020. This challenging dataset comprises bilateral migration flows, ranging from zero to 1.6 million migrants, leading to a dispersion index of 345,000. BMA is conducted with a set of potentially important covariates and results are presented in Appendix A10.

7.3 Comparative Predictive Performance

To understand the predictive capabilities of ULLGMs, we carried out a predictive exercise based on the measles vaccination data and the migration data. Each data set was randomly split into test (prediction) and training sets 100 times, with 15% allocated to the test set and the remaining 85% to the training set. Then, we estimated models using the training data and evaluated their prediction accuracy on the test data. For the ULLGMs, a unit information prior and a hyper- prior were used. Non-BMA versions of ULLGMs were estimated as well, including the full, null, median probability, and highest probability models, based on the unit information prior BMA results. For the bilateral migration data, we also performed a Poisson regression BMA analysis using adaptations of the AutoRJMCMC algorithm of Lamnisos et al. (2009). In addition, the full, null, median probability, and highest probability models, based on the AutoRJMCMC results were included in the analysis. For the vaccination data, we added Binomial logistic regression models without overdispersion using BMA and also considering the full, null, median, and highest posterior models. For BMA methods, we set to stay agnostic about model size a priori. In the case of the GLM models, we used and as priors on the regression parameters. For each model, we collected 300,000 posterior samples after an initial burn-in period of 250,000 iterations. For posterior simulation under Binomial and Poisson GLMs, we employed a multivariate Gaussian posterior approximation, derived from a Bayesian IWLS algorithm (Gamerman, 1997).

In addition to analyzing the full samples, we performed leave-one-out cross-validation555For the smaller samples, we employ leave-one-out cross-validation as the 85/15 test-training splits used for the larger samples lead to near rank deficiency in the design matrix in some cases, causing instability in the corresponding estimation runs. on subsamples of the data sets to gain insights into predictive performance in smaller samples. For the migration data, we examined the migration flows from OECD countries to Austria, excluding all destination-specific and three multicollinear covariates (resulting in ). For the vaccination data, we considered the data for the three regions with the lowest vaccination rates (, ). Given the small sample size, we expect sparser models to be relevant a priori, and set to slightly favor smaller models. Graphical summaries of the BMA results for these subsamples, comparable to those presented in Sec. 7.1 and Sec. A10, are provided in Supplementary Figures A10 to A13.

For predictive evaluation, we employ the logarithmic score or log predictive score (LPS, see e.g. Fernández et al., 2001), which is a proper scoring rule for counts (see Czado et al., 2009). Denoting the training data as and the holdout data to be predicted as with elements and associated covariate values , LPS is defined as

| (18) |

The required posterior predictive probabilities evaluated at the holdout counts are approximated as detailed in Supplementary Sec. A11.

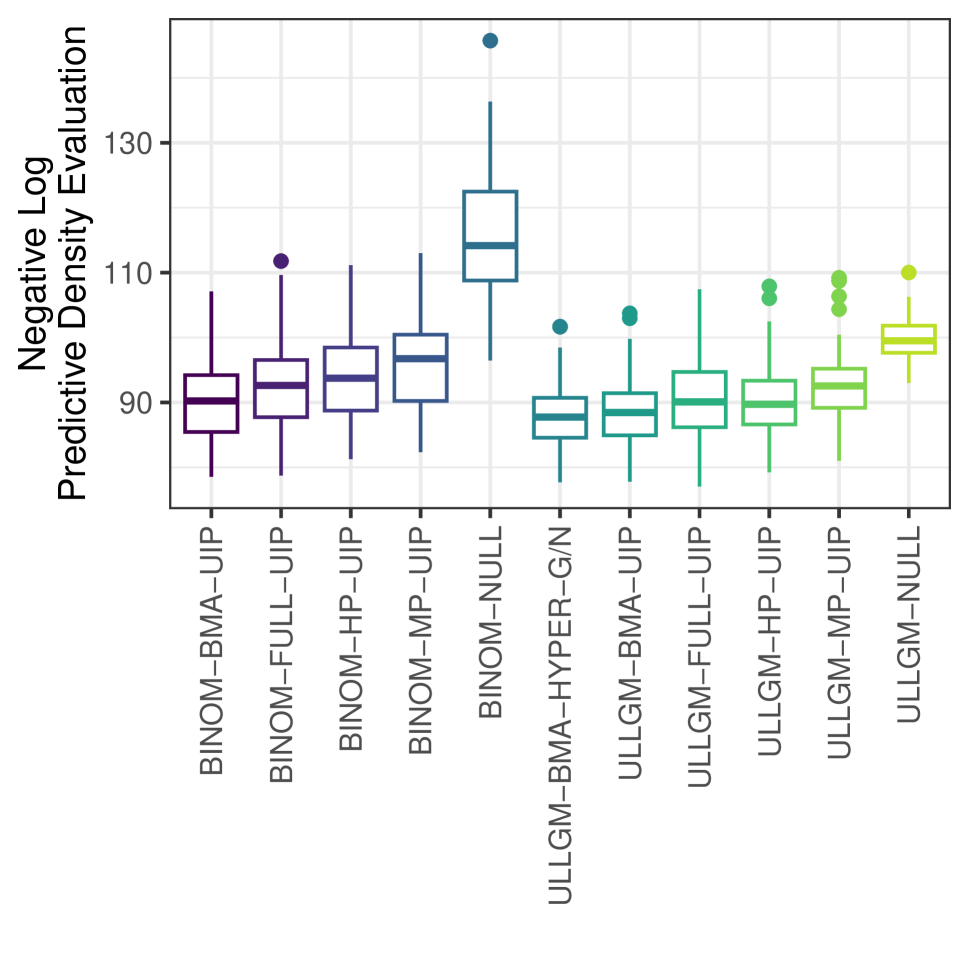

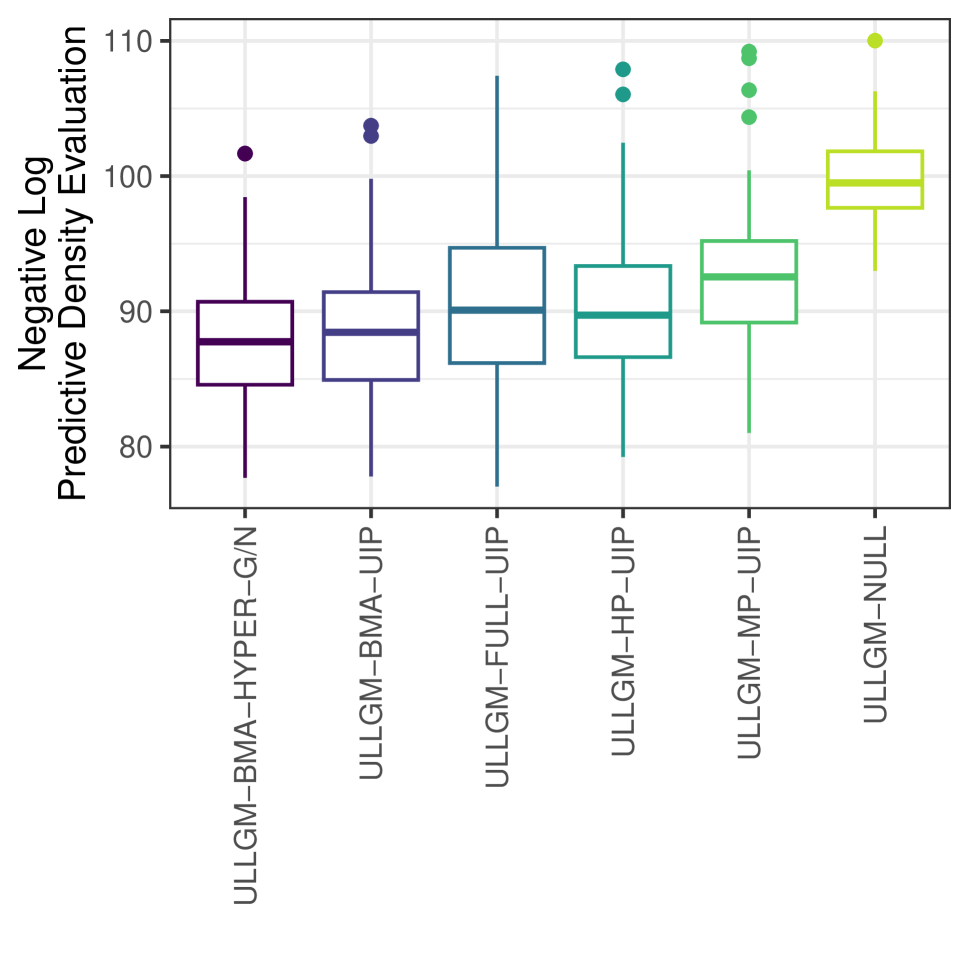

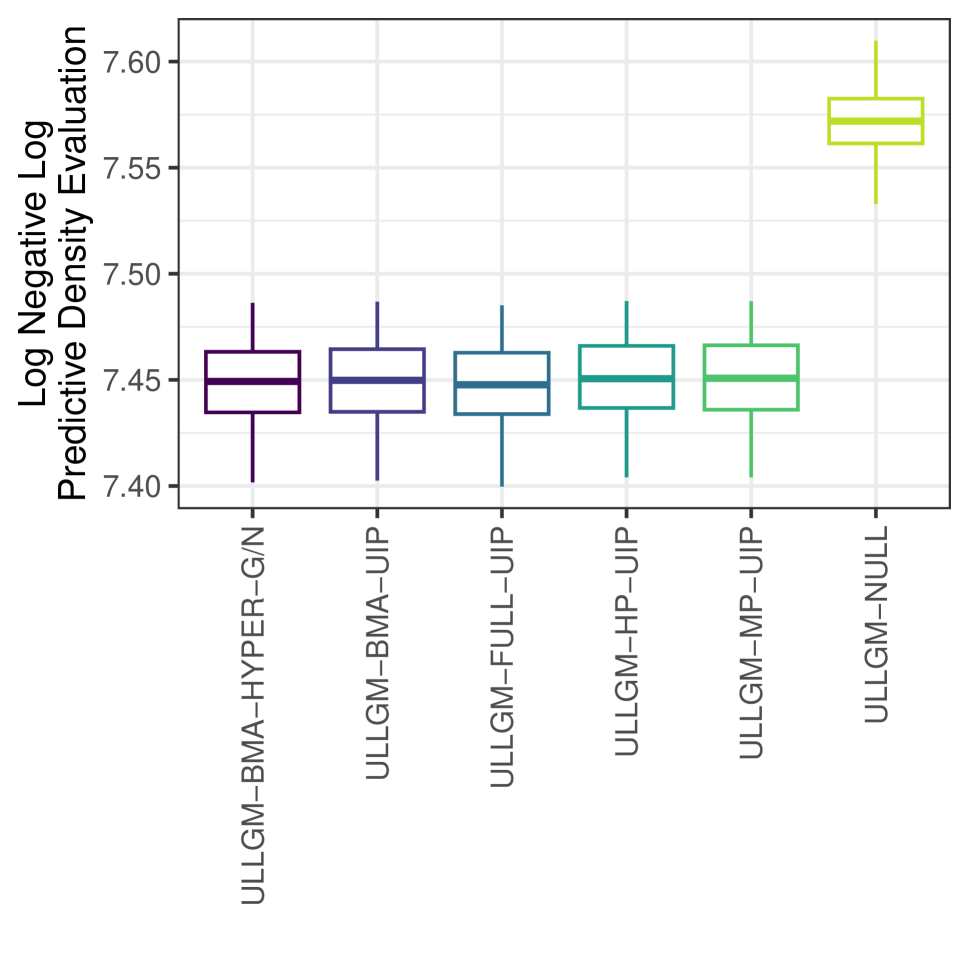

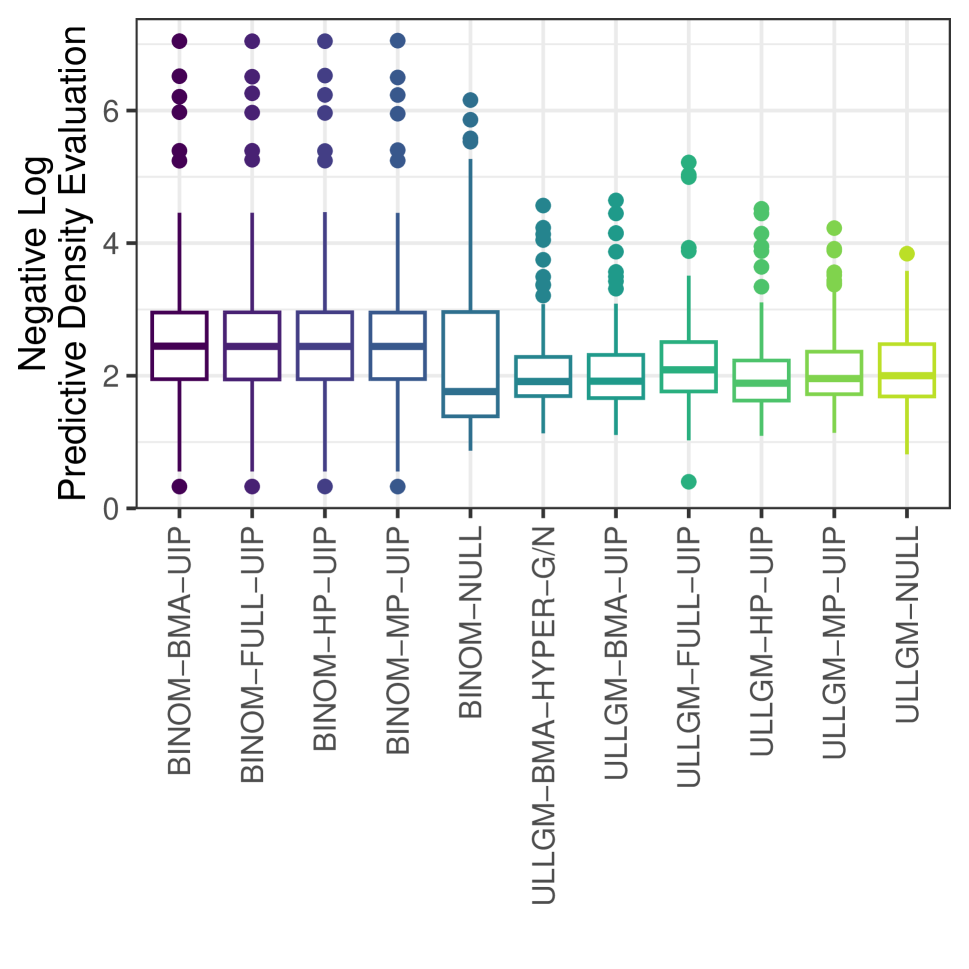

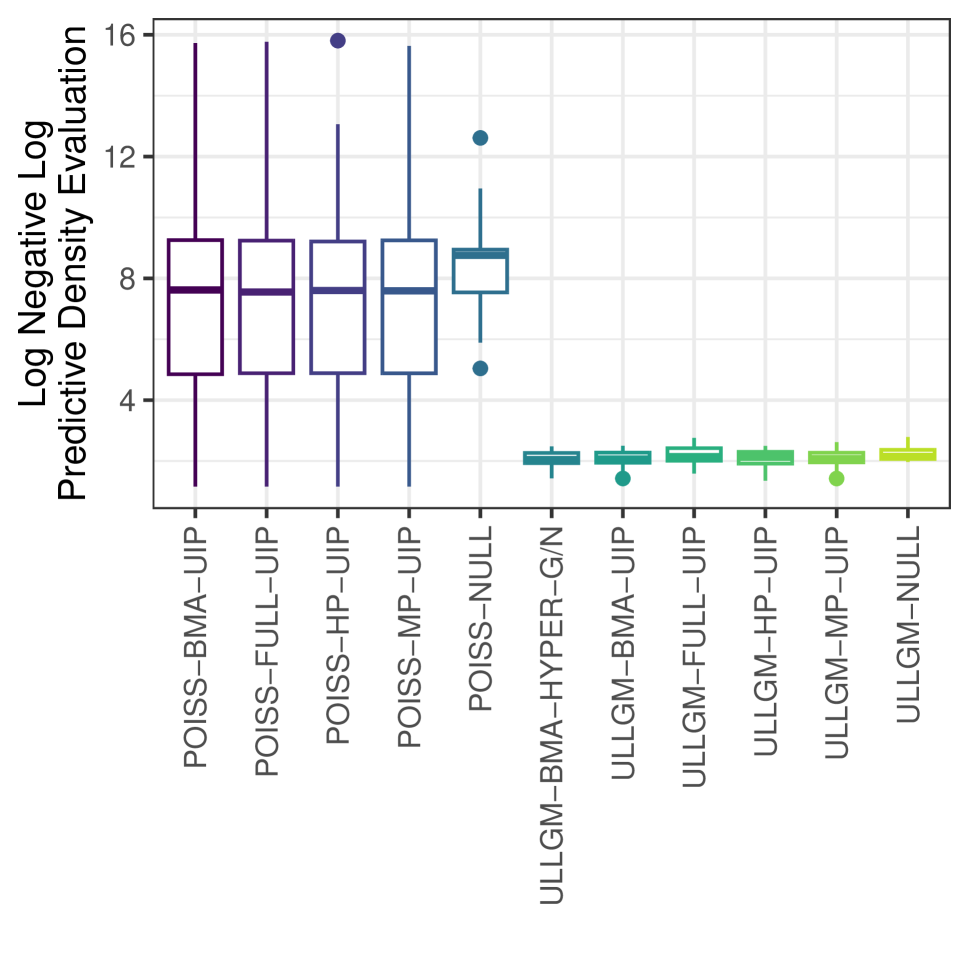

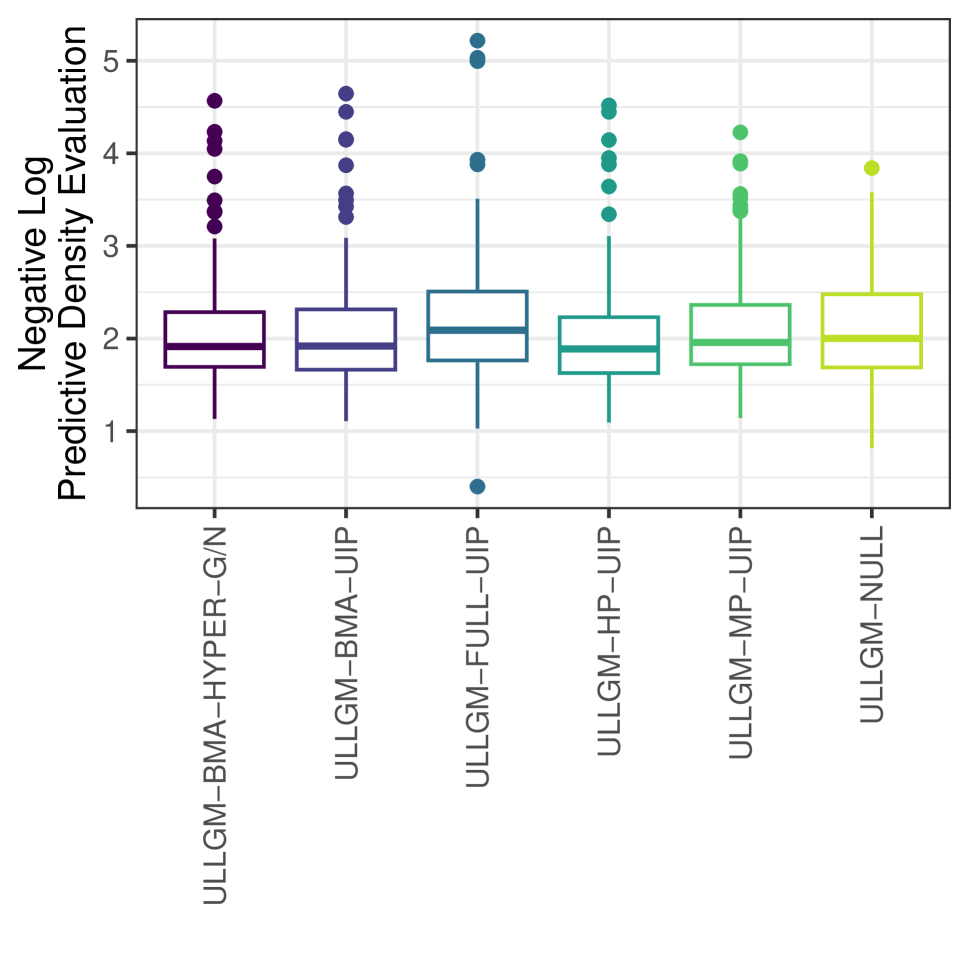

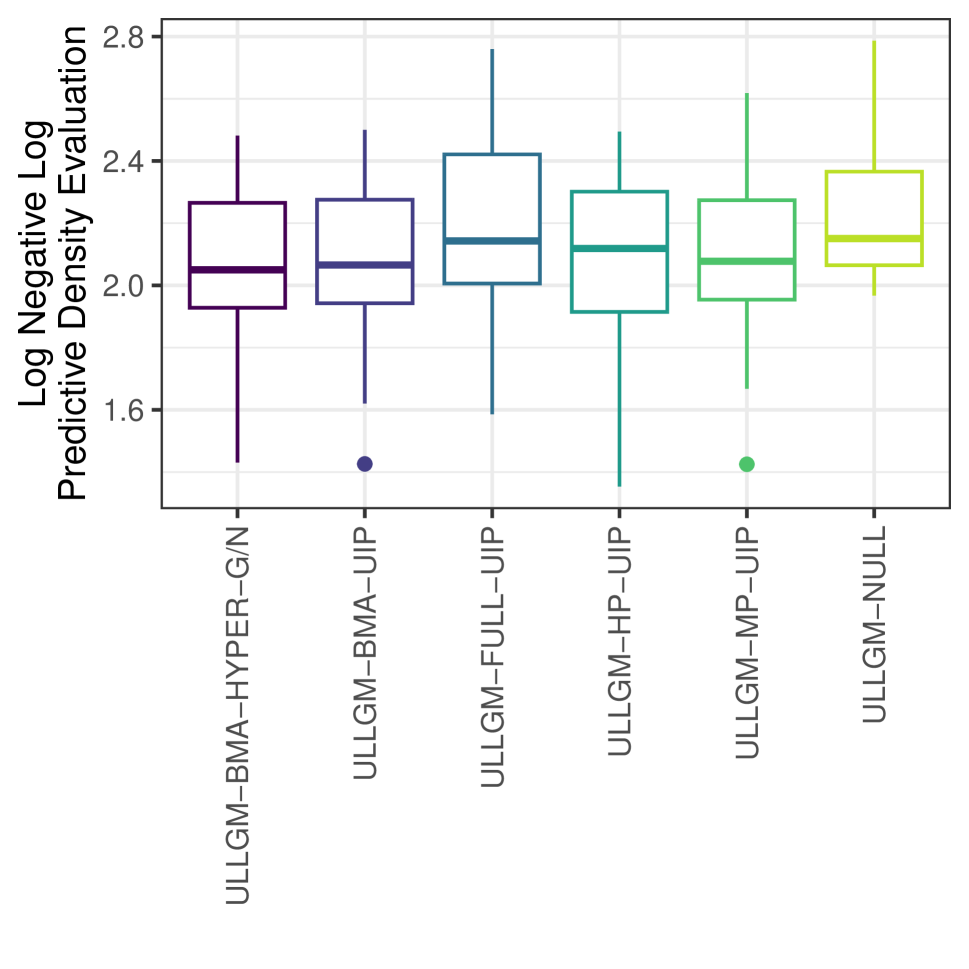

The results are presented in Table 2. Smaller values of LPS indicate better predictive performance. The mean, median, minimum, and maximum scores for each model across 100 partitions, as well as the share of replications where a model ranked as the best or worst, along with its average ranking are provided. Additionally, for the ULLGMs, average posterior means for are reported. The model size, indicating the posterior mean number of included regressors, is also documented, averaged over all partitions. Boxplots of the LPS across the 100 replications are provided in Supplementary Fig. A14 and Fig. A15.

| Avg. LPS | Med. LPS | Min. LPS | Max. LPS | % Best | % Worst | Avg. Rank | Avg. Model Size | ||

| Full Vaccination Data (n=305) | |||||||||

| ULLGM-BMA-HYPER-g/n | 1.95 | 1.95 | 1.73 | 2.26 | 0.61 | 0.00 | 1.67 | 0.22 | 16.53 |

| ULLGM-BMA-UIP | 1.96 | 1.97 | 1.73 | 2.31 | 0.10 | 0.00 | 2.35 | 0.16 | 13.85 |

| ULLGM-FULL-UIP | 2.01 | 2.00 | 1.71 | 2.39 | 0.09 | 0.00 | 4.44 | 0.01 | 63 |

| ULLGM-HP-UIP | 2.01 | 1.99 | 1.76 | 2.40 | 0.05 | 0.00 | 4.59 | 0.25 | 7.44 |

| ULLGM-MP-UIP | 2.06 | 2.06 | 1.80 | 2.43 | 0.01 | 0.00 | 6.36 | 0.28 | 7.94 |

| ULLGM-NULL | 2.22 | 2.21 | 2.07 | 2.44 | 0.00 | 0.00 | 9.17 | 0.98 | 0 |

| BINOM-BMA-UIP | 2.01 | 2.01 | 1.75 | 2.38 | 0.09 | 0.00 | 4.30 | 0 | 14.32 |

| BINOM-FULL-UIP | 2.06 | 2.06 | 1.75 | 2.48 | 0.03 | 0.00 | 6.55 | 0 | 63 |

| BINOM-HP-UIP | 2.08 | 2.08 | 1.81 | 2.47 | 0.01 | 0.00 | 7.23 | 0 | 12.12 |

| BINOM-MP-UIP | 2.13 | 2.15 | 1.83 | 2.51 | 0.01 | 0.01 | 8.35 | 0 | 11.40 |

| BINOM-NULL | 2.56 | 2.54 | 2.14 | 3.24 | 0.00 | 0.99 | 10.99 | 0 | 0 |

| Subset Vaccination Data (n=85) | |||||||||

| ULLGM-BMA-HYPER-g/n | 2.11 | 1.91 | 1.13 | 4.57 | 0.02 | 0.00 | 4.64 | 0.29 | 5.76 |

| ULLGM-BMA-UIP | 2.12 | 1.92 | 1.11 | 4.64 | 0.04 | 0.04 | 4.45 | 0.25 | 4.78 |

| ULLGM-FULL-UIP | 2.27 | 2.09 | 0.40 | 5.22 | 0.13 | 0.00 | 5.18 | 0.01 | 54 |

| ULLGM-HP-UIP | 2.08 | 1.89 | 1.09 | 4.52 | 0.15 | 0.02 | 4.39 | 0.39 | 1.00 |

| ULLGM-MP-UIP | 2.15 | 1.96 | 1.14 | 4.23 | 0.04 | 0.02 | 5.51 | 0.45 | 1.04 |

| ULLGM-NULL | 2.13 | 2.00 | 0.82 | 3.84 | 0.09 | 0.08 | 5.99 | 0.63 | 0 |

| BINOM-BMA-UIP | 2.69 | 2.45 | 0.33 | 7.05 | 0.04 | 0.14 | 7.76 | 0 | 53.99 |

| BINOM-FULL-UIP | 2.69 | 2.44 | 0.33 | 7.05 | 0.02 | 0.16 | 7.78 | 0 | 54 |

| BINOM-HP-UIP | 2.69 | 2.44 | 0.33 | 7.05 | 0.07 | 0.16 | 7.96 | 0 | 54.00 |

| BINOM-MP-UIP | 2.69 | 2.44 | 0.33 | 7.05 | 0.01 | 0.13 | 7.72 | 0 | 54.00 |

| BINOM-NULL | 2.29 | 1.76 | 0.87 | 6.16 | 0.41 | 0.24 | 4.64 | 0 | 0 |

| Full Migration Data (n=1,406) | |||||||||

| ULLGM-BMA-HYPER-g/n | 8.18 | 8.18 | 7.80 | 8.49 | 0.19 | 0.00 | 1.93 | 0.73 | 31.30 |

| ULLGM-BMA-UIP | 8.19 | 8.19 | 7.81 | 8.50 | 0.03 | 0.00 | 2.86 | 0.72 | 28.13 |

| ULLGM-FULL-UIP | 8.18 | 8.17 | 7.79 | 8.48 | 0.71 | 0.00 | 1.65 | 0.69 | 54 |

| ULLGM-HP-UIP | 8.20 | 8.19 | 7.82 | 8.50 | 0.00 | 0.00 | 4.53 | 0.72 | 26.04 |

| ULLGM-MP-UIP | 8.20 | 8.20 | 7.82 | 8.50 | 0.07 | 0.00 | 4.03 | 0.72 | 26.84 |

| ULLGM-NULL | 9.25 | 9.25 | 8.90 | 9.61 | 0.00 | 0.00 | 6.00 | 6.82 | 0 |

| POISS-BMA-UIP | 0.00 | 0.00 | 8.35 | 0 | 54.00 | ||||

| POISS-FULL-UIP | 0.00 | 0.00 | 8.56 | 0 | 54 | ||||

| POISS-HP-UIP | 0.00 | 0.00 | 8.47 | 0 | 54.00 | ||||

| POISS-MP-UIP | 0.00 | 0.00 | 8.62 | 0 | 54.00 | ||||

| POISS-NULL | 0.00 | 1.00 | 11.00 | 0 | 0 | ||||

| Subset Migration Data (n=38) | |||||||||

| ULLGM-BMA-HYPER-g/n | 8.10 | 7.77 | 4.18 | 11.96 | 0.51 | 0.00 | 2.24 | 0.16 | 5.37 |

| ULLGM-BMA-UIP | 8.14 | 7.89 | 4.16 | 12.18 | 0.05 | 0.00 | 3.22 | 0.27 | 5.51 |

| ULLGM-FULL-UIP | 9.19 | 8.53 | 4.88 | 15.80 | 0.05 | 0.00 | 4.84 | 0.16 | 28 |

| ULLGM-HP-UIP | 8.33 | 8.32 | 3.87 | 12.11 | 0.22 | 0.00 | 3.03 | 0.26 | 3.95 |

| ULLGM-MP-UIP | 8.39 | 7.99 | 4.16 | 13.71 | 0.08 | 0.00 | 3.54 | 0.33 | 3.51 |

| ULLGM-NULL | 9.48 | 8.59 | 7.15 | 16.23 | 0.03 | 0.00 | 5.54 | 4.06 | 0 |

| POISS-BMA-UIP | 3.19 | 0.03 | 0.14 | 8.46 | 0 | 28.00 | |||

| POISS-FULL-UIP | 3.19 | 0.00 | 0.03 | 8.73 | 0 | 28 | |||

| POISS-HP-UIP | 3.19 | 0.03 | 0.19 | 8.54 | 0 | 28.00 | |||

| POISS-MP-UIP | 3.19 | 0.00 | 0.03 | 8.38 | 0 | 28.00 | |||

| POISS-NULL | 0.00 | 0.62 | 9.49 | 0 | 0 |

In the real data applications examined, ULLG models outperform their counterparts that do not account for overdispersion. For the vaccination data, overdispersion is moderate, resulting in relatively comparable outcomes for ULLGMs and non-ULLGMs. On average, the ULLGMs perform better. At the same time, they tend to select smaller models. We attribute this to the inability to accommodate the variability in the data without the overdispersion parameter: the standard models have to compensate by including more covariates. This effect is particularly pronounced in the migration data analysis, where substantial overdispersion in the data causes all coefficients in a standard Poisson regression model to appear as important predictors. Consequently, the RJMCMC-BMA algorithm for Poisson regression predominantly visits the full model. This still does not adequately capture the data dispersion, which results in overly concentrated predictive distributions and very suboptimal predictive performance. In contrast, ULLGMs can accommodate overdispersion through and produce dramatically better predictive scores. Note that estimates for are substantially higher for the null models (where all overdispersion has to be accommodated through ) and lower for the full models. Among the ULLGMs, the hyper- prior tends to favor larger models, but provides similar or slightly better predictive performance compared to the unit information prior framework in both data sets. Irrespective of whether we use an LGM structure or not, the null models tend to predict badly, for all data sets. Thus, covariate information substantially improves prediction, empirically justifying the regression framework. The best overall performance is shown by the ULLGM-BMA model with a hyper prior which never predicts worst and predicts best in over 50% of the holdout samples for two of the four datasets considered.

8 Concluding Remarks

In this article, we present a formal and general framework for BMA in non-Gaussian regression models, based on the class of ULLGMs. We provide full characterisations of posterior existence for key models within this class and develop a simple, efficient and adaptable MCMC algorithm to handle posterior simulation under model uncertainty. Our empirical investigations focus on PLN and BiL regression models for overdispersed count data. A simulation study suggests high accuracy and robustness to likelihood misspecification, making the framework potentially useful in a wide range of settings. Finally, we apply the models to two real data applications and conduct a comparative predictive exercise, further illustrating the advantages of the proposed framework.

For the measles vaccination rate application, we deal with data that are often modeled using spatial methods. The migration data are essentially network data, models for which often include latent variables to capture similarities between the nodes. Here, we used simple regression models for both applications. The ability to use BMA allows us to include many potential predictors, which helps to explicitly capture structures that are usually treated as latent. This approach not only aids in interpretation and simplifies modeling but also enables us to predict observables using only the covariates. For some applications, combining BMA with latent variable modeling could provide an even more powerful framework. Adapting existing MCMC algorithms for latent variable models to incorporate model uncertainty is a natural extension of the algorithms developed here.

Several additional research directions are attractive avenues for future exploration. In terms of substantive applications, the proposed framework is broadly applicable and could be particularly valuable for analyzing model uncertainty in multi-way contingency tables (Ntzoufras et al., 2000) and related problems, such as multiple systems analysis (Silverman, 2020). Furthermore, many practically relevant applications of regression models involve multivariate outcomes. Combining multivariate latent Gaussian models with multivariate Bayesian variable selection techniques (Brown et al., 1998b) could yield very interesting modeling environments.

References

- The multivariate Poisson-log normal distribution. Biometrika 76 (4), pp. 643–653. Cited by: §2.1, §2.2.

- Logistic-normal distributions: some properties and uses. Biometrika 67 (2), pp. 261–272. Cited by: §2.1.

- Criteria for Bayesian model choice with application to variable selection. Annals of Statistics 40 (481), pp. 1550–77. Cited by: §3.

- Bayesian variable selection in high dimensional problems without assumptions on prior model probabilities. technical report Technical Report arXiv:1607.02993v1. Cited by: footnote 2.

- Bayesian Wavelength Selection in Multicomponent Analysis. Journal of Chemometrics 12, pp. 173–82. Cited by: §3.

- Multivariate Bayesian variable selection and prediction. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 60 (3), pp. 627–641. Cited by: §8.

- On fitting the Poisson lognormal distribution to species-abundance data. Biometrics, pp. 101–110. Cited by: §2.1.

- Markov chain Monte Carlo analysis of correlated count data. Journal of Business & Economic Statistics 19 (4), pp. 428–435. Cited by: §2.2, §5.

- Random effects modeling of multiple binomial responses using the multivariate binomial logit-normal distribution. Biometrics 56 (1), pp. 73–80. Cited by: §5.

- Predictive Model Assessment for Count Data. Biometrics 65 (4), pp. 1254–1261. Cited by: §7.3.

- A mixed Poisson–inverse-Gaussian regression model. Canadian Journal of Statistics 17 (2), pp. 171–181. Cited by: §2.1.

- On Bayesian model and variable selection using MCMC. Statistics and Computing 12 (1), pp. 27–36. Cited by: §1.

- Sparse Bayesian modelling of underreported count data. Statistical Modelling 16 (1), pp. 24–46. Cited by: §1.

- Benchmark priors for Bayesian model averaging. Journal of Econometrics 100, pp. 381–427. Cited by: §7.3.

- Auxiliary mixture sampling for parameter-driven models of time series of counts with applications to state space modelling. Biometrika 93 (4), pp. 827–841. Cited by: §1.

- Sampling from the posterior distribution in generalized linear mixed models. Statistics and Computing 7 (1), pp. 57–68. Cited by: §7.3.

- LGM split sampler: an efficient MCMC sampling scheme for latent Gaussian models. Statistical Science 35 (2), pp. 218–233. External Links: Document, Link Cited by: §5.

- An inquiry into the nature of frequency distributions representative of multiple happenings with particular reference to the occurrence of multiple attacks of disease or of repeated accidents. Journal of the Royal statistical society 83 (2), pp. 255–279. Cited by: §2.1.

- In search of lost mixing time: adaptive Markov chain Monte Carlo schemes for Bayesian variable selection with very large p. Biometrika 108 (1), pp. 53–69. Cited by: §5.

- Compound Poisson regression models. In GLIM 82: Proc. Internat. Conf. Generalized Linear Models, pp. 109–121. Cited by: §2.1.

- Bayesian latent gaussian models. In Statistical Modeling Using Bayesian Latent Gaussian Models : With Applications in Geophysics and Environmental Sciences, B. Hrafnkelsson (Ed.), pp. 1–80. External Links: ISBN 978-3-031-39791-2, Document, Link Cited by: §2.

- Bayesian variable selection in a million dimensions. In Proceedings of The 26th International Conference on Artificial Intelligence and Statistics, F. Ruiz, J. Dy, and J. van de Meent (Eds.), Proceedings of Machine Learning Research, Vol. 206, pp. 253–282. External Links: Link Cited by: §1.

- A reference Bayesian test for nested hypotheses and its relationship to the Schwarz criterion. Journal of the American Statistical Association 90 (431), pp. 928–934. Cited by: §6.

- Transdimensional sampling algorithms for Bayesian variable selection in classification problems with many more variables than observations. Journal of Computational and Graphical Statistics 18 (3), pp. 592–612. Cited by: §1, §7.3.

- Mixtures of -priors for Bayesian model averaging with economic applications. Journal of Econometrics 171 (2), pp. 251–66. Cited by: §3, §5, §6.

- On the effect of prior assumptions in Bayesian model averaging with applications to growth regression. Journal of Applied Econometrics 24 (4), pp. 651–674. Cited by: §3, §3.

- Mixtures of priors for Bayesian variable selection. Journal of the American Statistical Association 103 (481), pp. 410–23. Cited by: §3, §6.

- Adaptive MCMC for Bayesian Variable Selection in Generalised Linear Models and Survival Models. Entropy 25 (9). External Links: Link, ISSN 1099-4300, Document Cited by: §5.

- The Barker proposal: Combining robustness and efficiency in gradient-based MCMC. Journal of the Royal Statistical Society, B 84 (2), pp. 496. Cited by: §5.

- Fully Bayes factors with a generalized -prior. Annals of Statistics 39, pp. 2740–2765. Cited by: footnote 2.

- Stochastic search variable selection for log-linear models. Journal of Statistical Computation and Simulation 68 (1), pp. 23–37. Cited by: §8.

- Bayesian inference for logistic models using Pólya–Gamma latent variables. Journal of the American statistical Association 108 (504), pp. 1339–1349. Cited by: §1.

- Examples of adaptive MCMC. Journal of computational and graphical statistics 18 (2), pp. 349–367. Cited by: §5.

- Approximate Laplace approximations for scalable model selection. Journal of the Royal Statistical Society Series B: Statistical Methodology 83 (4), pp. 853–879. Cited by: §1.

- Approximate Bayesian Inference for Latent Gaussian models by using Integrated Nested Laplace Approximations. Journal of the Royal Statistical Society, Ser. B 71, pp. 319–392. Cited by: §2.

- Bayes and empirical Bayes multiplicity adjustment in the variable-selection problem. Annals of Statistics 38, pp. 2587–619. Cited by: §3.

- Multiple-systems analysis for the quantification of modern slavery: classical and Bayesian approaches. Journal of the Royal Statistical Society, A 183 (3), pp. 691–736. Cited by: §8.

- The calculation of posterior distributions by data augmentation. Journal of the American statistical Association 82 (398), pp. 528–540. Cited by: §5.

- Bayesian analysis of Poisson regression with lognormal unobserved heterogeneity: With an application to the patent-R&D relationship. Communications in Statistics—Theory and Methods 39 (10), pp. 1689–1706. Cited by: §2.1, §2.2, §5.

- High resolution age-structured mapping of childhood vaccination coverage in low and middle income countries. Vaccine 36 (12), pp. 1583–1591. Cited by: §7.1.

- Bayesian model averaging in proportional hazard models: assessing the risk of a stroke. Journal of the Royal Statistical Society Series C: Applied Statistics 46 (4), pp. 433–448. Cited by: §1.

- An adaptive MCMC method for Bayesian variable selection in logistic and accelerated failure time regression models. Statistics and Computing 31 (1), pp. 1–11. Cited by: §1.

- Econometric analysis of count data. Springer Science & Business Media. Cited by: §2.2.

- Informed proposals for local MCMC in discrete spaces. Journal of the American Statistical Association 115 (530), pp. 852–865. Cited by: §5.

SUPPLEMENTARY MATERIAL

A1 Moments and Dispersion of under the BiL model

In order to approximate the first two moments of under the BiL model, we approximate the logistic cdf with a scaled Gaussian cdf, such that

| (A1) |

for a suitable value of , where is the cdf of a standard Gaussian random variable. To show that the penultimate equality holds we need to verify

| (A2) |

For this, consider two random variables and . Note that

| (A3) |

and, by the law of total probability,

| (A4) |

which is equivalent to the left-hand side of (A2). Now note that and due to Gaussianity, . This implies that , verifying (A2).

Approximate variance terms and can be derived based on similar considerations. Consider first the variance of the success probability for . Again approximating the logistic cdf with a scaled probit cdf and following Owen (1980), it can be shown that

| (A5) |

for a suitable value of and where is Owen’s function. By the properties of this function, it follows that as and as . For or , . By the law of total variance, we have

| (A6) |

which approaches the usual binomial variance for , as implies . The dispersion index is equivalent to

| (A7) |

which tends to the binomial dispersion index for and can be written as

| (A8) |

where stems from the usual binomial specification. The term accounts for extra-binomial dispersion, and increases in as well as in , while it decreases with increasing and vanishes as . Fig. A1 shows that the BiL dispersion index is larger than the binomial dispersion index whenever . As the overdispersion term will tend to , for any finite value of . Note, finally, that if we assume a probit link instead of a logistic link, resulting in an overdispersed binomial probit model, then the approximate equalities in (A1) and (A5) hold exactly with .

A2 Interpretation of for BeC models

The use of the latent variable representation of the BeC models is helpful in getting a better understanding of what this model class represents. Below we focus on link functions that are cdf’s of scale mixtures of normals (which is the case for the most popular choices).

If we take for the cdf of a standard Normal, the BeC model is equivalent to the Probit model with an extra unidentified parameter .

Choosing alternative specifications maps out a class of models with a link function that sits in between that of the corresponding standard binary regression model and that of the Probit BeC model. For example, taking to be a student- cdf with leads to the ”-link” model of Albert and Chib (1993). Let us consider the latent variable representation of this model as follows: for some latent variable and for with , where . Extending this to the ULLGM setting gives us , and integrating out with (2) leads to . Thus, the probability that becomes

| (A9) |

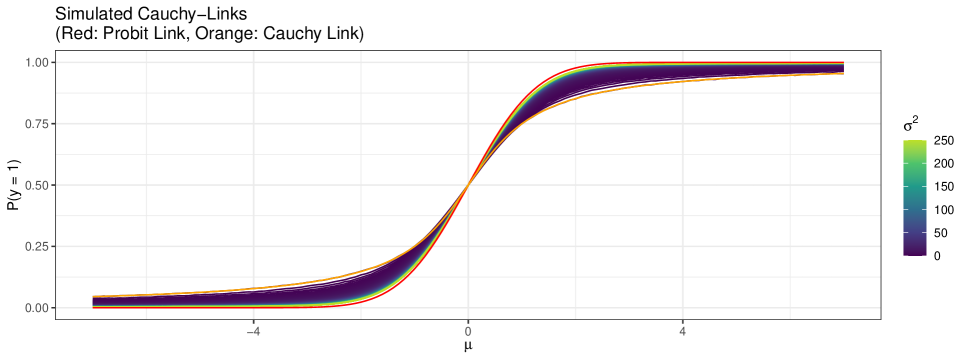

where denotes the cdf of the standard Normal distribution. Clearly, if this simply describes the -link model and as we will tend to the overparameterised Probit model with . For nonzero finite values of , the probability in (A9) together with describes a hybrid model. That is, in BeC models, the interpretation of is the relative weight of the Probit link version. If we take to be the logistic cdf instead, the same kind of argument holds, only changing the distribution for . In particular, (A9) applies where now and has a Kolmogorov-Smirnov distribution (Holmes and Held, 2006). An example for a Cauchy link is shown in Fig. A2. To scale things comparably for different values of , the figure plots simulated values of

for and values of ranging from 0 (Cauchy link) to 250 (close to Probit link).

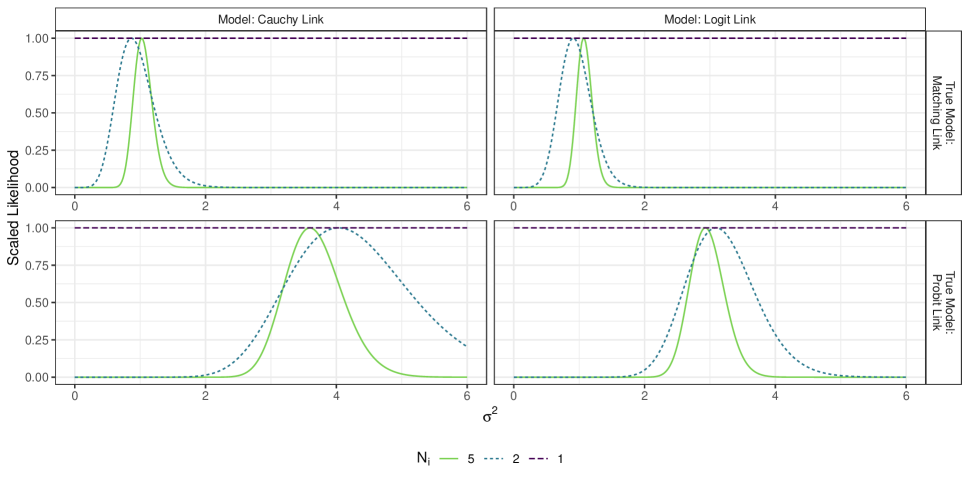

Fig. A3 illustrates the likelihood behavior of Binomial ULLGM models for various values of and number of trials and for different specifications of , using logistic and Cauchy link functions. The data are generated from Binomial ULLGMs with and three possible link functions: the Cauchy or logistic link functions lead to correct model specifications and the probit link function leads to misspecification. The figure highlights that while provides likelihood information about , the likelihood for the Bernoulli case, where , is completely flat with respect to . This implies that cannot be identified from the likelihood for BeC models. Consequently, the posterior distribution becomes improper under the prior in (8)-(9), as discussed in Sec. A5. Inference on will be fully determined by the prior on , which needs to be proper.

A3 Effect of Neglecting Overdispersion in Poisson and Binomial Regression

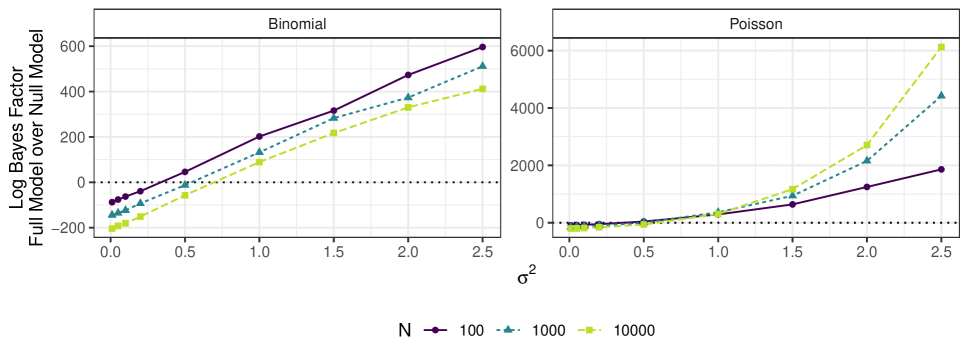

To illustrate the shortcomings of neglecting overdispersion in model averaging for non-Gaussian models, we conduct a small simulation exercise. Data were simulated from both a BiL model (with 100 trials per observation) and a PLN model, with overdispersion parameter ranging from 0.01 (approximating the GLM case) to 2.5 (indicating clear overdispersion). We vary the sample sizes () while keeping the number of iid standard Gaussian regressors constant at . The linear predictor is simulated from , implying no relationship with the regressors. We analysed these data with Poisson and Binomial models and approximated the log Bayes factors of the full model over the null model using the BIC approximation . Each setting was replicated 100 times, and the median Bayes factors across these replications are displayed in Figure A4.

The results demonstrate that with increasing overdispersion, models without additional variation mechanisms attempt to account for the data variation by adding extra covariates and increasingly favoring larger models. This effect is more pronounced in the Poisson case, which has a more rigid variance structure compared to the binomial case, where variance is influenced by both the number of trials, and the imbalance of the dataset (as reflected in the success probabilities). Nonetheless, in both cases, even moderate amounts of overdispersion strongly favor the full model over the correct null model, even with sample size growing large. Interestingly, for the Poisson model this effect gets stronger with , while for the Binomial it goes the other way.

A4 Uncertainty in , MCMC efficiency and limiting cases of PLN and BiL models

To develop an understanding of the spread or concentration of the posterior distribution of in the PLN and BiL models, it is helpful to examine the posterior approximations derived in Sec. A11. For the PLN model, the posterior distribution is approximated as follows:

| (A10) |

From this, it becomes evident that larger imply a smaller posterior variance. As , the posterior distribution of converges to a point mass at . Conversely, smaller values of result in greater uncertainty in the likelihood contributions of observation . For observations where , the Poisson likelihood contribution provides minimal information beyond , and in fact the likelihood function degenerates. Consequently, a certain number of non-zero outcomes is necessary for a proper posterior under improper priors (compare the corresponding proof conditions in Sec. A5). This indicates that likelihood identification of , and therefore MCMC efficiency, strongly depends on the number of zero outcomes and the size of the remaining counts. For very large counts, the PLN model behaves approximately like a Gaussian regression model with outcome . For small counts, is more strongly informed by prior information, resulting in decreased MCMC efficiency due to increased dependency between and , , and .

Similar considerations apply to the BiL framework, where the posterior approximation of from Sec. A11 is given by:

| (A11) |

From this approximation, it can be seen that likelihood identification is strongest when and . For such observations, the BiL model behaves approximately like a Gaussian regression model with outcome as when , with the approximation becoming accurate faster when . Conversely, as approaches a single trial (Bernoulli case) and/or outcomes become more imbalanced ( close to 0 or ), likelihood identification weakens and MCMC efficiency decreases. When or , the likelihood contributions become degenerate, even for large , which is reflected in the conditions for the proofs in Sec. A5.

A5 Proof of Theorem 1

In this Appendix, we will derive the conditions under which the posterior resulting from the sampling model in (1) and (6) is well-defined under the improper prior structure in (8) and (9) for any model in the model space. Theorem 1 considers the case where any additional parameter is fixed. Thus, in the proof we will not explicitly condition on .

Denote by the vector of all observations and partition as where groups all observations that allow for the integral to be finite. Now consider the marginal likelihood for model

| (A12) |

and we need to show that this marginal likelihood is finite for all values of and for any model . First, let us focus on the vector :

| (A13) |

where denotes those that correspond to and we can write

| (A14) |

where is the set of observation indices of . Let us now consider . If the matrix is of full column rank (Condition 1) and if (Condition 2), we can derive that

| (A15) |

where

| (A16) |

and . Under Condition 1, is invertible and for fixed choices of , the expression in (A15) is almost surely bounded from above by a finite number, say . For hyperpriors on that are proper distributions with pdf , the relevant marginal likelihood for is the expression in (A15) integrated with respect to . As tends to zero, (A15) tends to a finite constant in and as tends to the expression in (A15) behaves like . Thus any proper will lead to a finite value of the marginal likelihood . For the null model with only the intercept, the prior is simply (8) and the marginal likelihood is

| (A17) |

(with the same proportionality constant as in (A15)), which is also bounded. In the latter expression we have defined

| (A18) |

Therefore, (A13) becomes

| (A19) |

and it is sufficient to show that each of the integrals in the above expression is finite. In the sequel, we will consider the models presented in Table 1 and drop subscripts for convenience.

A5.1 PLN model

Here, we consider

| (A20) |

and use the variable transformation to obtain

| (A21) |

which means that consists of all nonzero observations. This leads directly to

| (A22) |

Thus, we have a well-defined posterior distribution after taking into account at least 2 nonzero observations. These observations in will then update the improper prior into a proper posterior which can then be used as the (proper) prior for the analysis of the zero observations in . Of course, the latter will lead to a proper posterior with a finite integrating constant. Thus, and using (A12) and (A22) we obtain that which proves the result. Conditions 1 and 2 jointly are thus sufficient for propriety. Condition 1 is also necessary, since we need to be of full column rank for the prior specification in (9) and given that the regressors are demeaned this also implies that Condition 1 holds. In order to prove that Condition 2 is also necessary for propriety, we consider the same line of proof as in Subsection A5.7. If condition 2 does not hold, we need to rely on observations for which to obtain a proper posterior ( with does not lead to a proper posterior). As explained in Subsection A5.7, the integral in (A38) then needs to integrate in each which requires that tends to zero in the tails for . For we have

| (A23) |

which tends to 1 as . Thus, (A38) will not integrate and condition 2 is necessary for posterior propriety in the PLN model.

If we change the distribution for the observables or the link function , then all that changes in the proof is the definition of and the expression for (A19).

A5.2 NBL model

If Negative Binomial then the integrals in (A19) are

| (A24) |

defining . Thus, we obtain

| (A25) |

The integral above is finite for all observations where . Thus, if we denote by those observations for which , we have

| (A26) |

which means that we have a well-defined posterior distribution after taking into account at least 2 observations in . The rest of the proof mirrors that for the PLN model. If we do not have two observations for which , we can use the same arguments as in Subsection A5.7 to show that the posterior does not exist, so that conditions 1 and 2 are both necessary and sufficient for posterior propriety in the NBL case.

A5.3 BiL model

If we use Binomial then we obtain

| (A27) |

defining . Thus, we obtain

| (A28) |

The integrand above is the kernel of a Beta distribution. Provided we have , this leads to

| (A29) |

The latter expression is finite for all observations where . Thus, if we denote by those observations for which , we have

| (A30) |

which means that we have a well-defined posterior distribution after taking into account at least 2 observations in . The rest of the proof mirrors that for the PLN model. If we do not have two observations for which , we can use the same arguments as in Subsection A5.7 to show that the posterior does not exist, so that conditions 1 and 2 are both necessary and sufficient for posterior propriety in the case of the BiL model.

A5.4 ErLN models

The Erlang case where Erlang (i.e. a Gamma distribution with integer shape parameter ) covers the Exponential model if we take . We assume that , so that the integrals in (A19) are given by

| (A31) |

Using the transformation , we obtain

| (A32) |

This integral is finite for all observations where is different from 0. This is an event of measure zero in the sampling distribution, so the posterior distribution is almost surely well-defined for any value of , taking .

A5.5 LNN model

If we use log Normal sampling log-Normal with , the integrals in (A19) are given by

| (A33) |

This immediately leads to

| (A34) |

which is finite for all observations where . The event has zero probability in the sampling distribution, so the posterior distribution is almost surely well-defined, taking .

A5.6 LNLN model

If we use log Normal sampling log-Normal with , the integrals in (A19) are given by

| (A35) |

Using the transformation , we obtain

| (A36) |

which can be solved using the inverse gamma distribution to leave us with

| (A37) |

This integral is finite for all observations where is different from 0 or . These are events of measure zero in the sampling distribution, so the posterior distribution is almost surely well-defined, taking .

A5.7 Bernoulli-based models BeC

Consider the marginal likelihood for model based on the entire sample:

| (A38) |

As explained in Appendix A5.8, the marginal density of given is a quadratic form which does not have sufficiently thin tails to integrate in . Thus, for the integral in (A38) to be finite the tails need to be squeezed by . In other words, when integrating with respect to , the corresponding needs to go to zero fast enough as tends to and . Since

| (A39) |

and we have a link function in BeC models that associates with it is clear that an observed will not change the right-hand tail of along dimension ( , which will be bounded from below for large ). Similarly, the value will leave the left-hand tail untouched. Thus, for any possible observation the marginal likelihood in (A38) will not be finite and the posterior will not exist.

A5.8 Marginal prior distribution of

As stated in (14), the marginal likelihood under fixed is

| (A40) |

where is the coefficient of determination of regressed on (and an intercept). Thus, the pdf of can be written as

| (A41) | ||||

| (A42) | ||||

| (A43) |

where we have defined and

| (A44) |

The matrix is positive definite as it is the sum of two positive definite matrices. The distribution of for each model is reminiscent of a multivariate Student- but is not a proper distribution as it would correspond to negative degrees of freedom and an unbounded density at zero. As expected, the expression for in (A15) simplifies to (A43) if we take , barring a proportionality constant , which appears in (A40) but is immaterial to the considerations in this section.

A6 Proof of Theorem 2

This theorem applies to models with additional parameters and its proof has a similar structure as that for Theorem 1.

Again, we focus on the marginal likelihood for a subsample which groups the observations corresponding to a finite . We can write for the marginal likelihood of in model :

| (A45) |

Using the fact that is bounded by some finite constant under conditions 1 and 2 (see the proof of Theorem 1), and applying (7) along with (A14), we obtain

Substituting the definition of in (17), we obtain directly

| (A46) |

so that the condition in (16) is sufficient for posterior existence. The rest of the proof follows a similar reasoning to the proof of Theorem 1.

For the LNLN model we have

from (A37), which means that the condition in (16) would require the prior on to compensate for behaving like in neighbourhoods around . This would need the prior on to have vanishing mass in these neighbourhoods, but of course their location depends on the observations. Thus, there is no (non-data based) prior that can satisfy (16) for the LNLN model, so we can not conclude that posterior inference on can be conducted with the overall prior structure assumed here for the LNLN model.

A7 Log Posterior Gradients for PLN and BiL models

Note that in any ULLGM model, the gradient of the conditional log posterior of additively decomposes into two parts. The first part is the gradient of the log of the Gaussian prior . Regardless of which likelihood is chosen as the basis for a ULLGM, this gradient is given by

The second part is the gradient of the log of the likelihood term , which depends on the type of model. For the PLN model, we have that

and hence

For the BiL model, we have that

and hence

A8 Details on Add-Delete-Swap Proposal

In the context of proposing a new candidate model , our approach involves deciding between three potential moves—addition, swap, and deletion—to transition between models. Let denote the total number of predictors, and let denote the number of predictors currently included in the model. The move is selected based on the current composition of the model:

-

•

If , the only possible move is addition.

-

•

If , the only possible move is deletion.

-

•

Otherwise, any of the three moves may be chosen, with the choice made uniformly at random.

This setup requires accounting for appropriate correction terms in the Metropolis-Hastings acceptance probability to ensure detailed balance. We denote the probability of proposing a move from the current model to a proposed model as , and the reverse move probability as .

-

•

Addition:

Here, is the number of predictors after the addition. This reflects the uniform probability of selecting any of the predictors in for deletion to reverse to .

-

•

Swap: In this case, the proposal is symmetric and therefore

-

•

Deletion:

Here, is the number of predictors after the deletion. This reflects the uniform probability of selecting any of the predictors not in for addition to reverse to .

A9 Results for Simulated Data

| Prior | DGP | Size | Frac. True | Brier | FNR | FPR | ln(g) | |||

|---|---|---|---|---|---|---|---|---|---|---|

| Poisson Log-Normal | ||||||||||

| Hyper-g/n (a=3) | ULLGM | 150 | 50 | 14.848 | 0.006 | 0.026 | 0.034 | 0.137 | 3.971 | 0.180 |

| Hyper-g/n (a=3) | ULLGM | 150 | 100 | 15.248 | 0.005 | 0.010 | 0.049 | 0.064 | 4.134 | 0.186 |

| Hyper-g/n (a=3) | ULLGM | 1000 | 50 | 14.894 | 0.010 | 0.021 | 0.012 | 0.128 | 3.940 | 0.197 |

| Hyper-g/n (a=3) | ULLGM | 1000 | 100 | 15.072 | 0.010 | 0.007 | 0.012 | 0.060 | 4.069 | 0.198 |

| Hyper-g/n (a=3) | GLM | 150 | 50 | 13.529 | 0.046 | 0.009 | 0.001 | 0.090 | 6.297 | 0.014 |

| Hyper-g/n (a=3) | GLM | 150 | 100 | 13.451 | 0.046 | 0.003 | 0.001 | 0.041 | 6.312 | 0.010 |