Optimal Bailouts in Diversified Financial Networks

Abstract

Widespread default involves substantial deadweight costs which could be countered by injecting capital into failing firms. Injections have positive spillovers that can trigger a repayment cascade. But which firms should a regulator bailout so as to minimize the total injection of capital while ensuring solvency of all firms? While the problem is, in general, NP-hard, for a wide range of networks that arise from a stochastic block model, we show that the optimal bailout can be implemented by a simple policy that targets firms based on their characteristics and position in the network. Specific examples of the setting include core-periphery networks.

JEL Code: C62, D85, F65, G32, G33, G38

1 Introduction

The ties of debt and equity between firms enable efficient risk sharing and capital allocation. They are also a conduit by which a negative shock to a small set of firms can be amplified to generate widespread default. Defaults involve substantial deadweight costs, including fire sales, early termination of contracts, administrative costs of government bailouts, and legal costs.

To mitigate these costs a regulator can inject capital into failing firms so as to prevent defaults. Injecting capital into a firm has positive spillovers if, by paying back its obligations to others, that firm allows its counterparties to meet their own obligations, triggering a repayment cascade. Given these spillovers, which firms should the regulator bailout so as to minimize the total injection of capital while ensuring solvency of all firms? Even in this simple form, absent moral hazard and asymmetric information, the problem is hard. The first difficulty arises from the presence of multiple equilibria. Who to target and how much to inject will depend upon the equilibrium outcome that prevails post-injection. Second, even if one fixes the choice of equilibrium (which we will), the incremental benefit of spillovers triggered by injecting capital into a firm depend on which other firms have received infusions. Indeed, most variations of the problem of determining who to bailout and by how much so as to achieve the desired equilibrium at minimum cost is NP-hard. For examples, see Jackson and Pernoud (2020), Klages-Mundt and Minca (2022), Dong et al. (2021) and Papachristou and Kleinberg (2022). This eliminates the possibility of an optimal policy that can be described by a ‘simple’ index rule. Such a rule would assign an index to a firm that depends only on its characteristics and easily computed ‘global’ information such as how central they are in the network. The index would determine whether it should be bailed out. Demange (2018), for instance, offers an index in this spirit to prioritize firms linked by debt. However, this index relies on the uniqueness of the underlying equilibrium and it is not invariant to injections of cash.

NP-hardness excludes a simple index policy for all networks but does not eliminate this possibility for special cases. We consider one such case where the underlying financial linkages are via equity cross holdings as in Elliott, Golub, and Jackson (2014). Here, a firm’s value depends on its cash endowment (in the form of held primitive assets) and the shares it owns in other firms.111Such equity holding networks, are pervasive Shi et al. (2019). When a firm’s value drops below a solvency threshold, it discontinuously imposes losses on its counter-parties, e.g., as distress costs. The counter-parties in turn may drag other firms below the solvency threshold.

The network of cross holdings is modeled as random with arbitrary block structure called the stochastic block model (SBM). SBMs are a popular model in the statistical analysis of networks, see Lee and Wilkinson (2019). Firms are partitioned into finitely many blocks, and the probability that one firm holds shares in another depends only on the blocks containing each firm. Two important examples of the SBM are core-periphery networks and cross-border relations in a global financial system, with financial systems in different countries represented as different blocks in the network.222The following document such structures in a variety of financial networks: Bech and Atalay (2010), Afonso et al. (2013), Boss et al. (2004), Daan and Lelyveld (2014), Blasques et al. (2018), Peltonen et al. (2014), Chinazzi et al. (2013) and Minoiu and Reyes (2013). We allow any sufficiently dense network structure between the blocks. The precise distributional assumptions of the SBM are discussed in Section 2 and can be interpreted as providing a model of diversified financial networks.

Given an amount of cash available to inject into the network, we wish to maximize the number of firms that achieve a value that exceeds the given solvency threshold. When the underlying network is a draw from an SBM, and the number of vertices is sufficiently large, we argue for a solution in terms of an index policy. Whether a firm is bailed out or not depends upon its cash endowment and how central the block to which it belongs is. The precise number of firms directly bailed out in each block is proportional to the block’s Katz-Bonacich centrality, adjusted to account for the cost of rescuing firms in that block. Using this relationship we show that the number of firms that receive an injection increases with the cash available. However, the set of firms that receive an injection is not monotone in the sense of subset inclusion. Furthermore, the relative dispersion in endowments, also affects the proportion of firms within a block that receive an injection relative to other blocks.

We justify this policy by passage to a continuum version of the underlying network to bypass the difficulties associated with discrete network models such as ties and inessential corner cases.333This is not unusual in other contexts, see Schmeidler (1969) and Azevedo and Leshno (2016). Continuum analogs of networks are called graphons, (see Lovász (2012) and Borg, Chayes, Cohn, and Holden (2017)) introduced in the previous decade as interest in large dense networks surged in a variety of different areas. They have been deployed to study targeting in networks, equilibria of network games, and the study of contagion (Erol et al. (2020), and Parise and Ozdaglar (2023)).

As our technique may be useful in other contexts, we outline the key steps involved.

-

1.

The first is to establish a concentration result. We show that with high probability, equilibrium firm valuations in any realization of an SBM are concentrated around the equilibrium valuations of a particular deterministic network. Thus, the impact of bailouts on any random instance of an SBM, must mirror that in this particular deterministic network.

-

2.

To determine the bailout policy in the deterministic network we pass to its graphon analog. The graphon analog admits a characterization of the extremal equilibrium firm valuations in terms of cutoffs in firms initial endowments. Within each block, there is a cutoff and firms in the block are solvent if and only if their endowments exceed that cutoff. This allows us to characterize the optimal bailout policy (assuming an extremal equilibrium) in terms of cutoffs for each block and relate each block specific cutoff to the centrality of the block.

-

3.

The concluding step is to show that there is a bailout policy in the finite network that approaches the optimal policy in the graphon as the size of the network increases.

Section 2 describes the SBM of equity networks and the deterministic network that determines the equilibrium profile of valuations around which the equilibrium of each instance of an SBM concentrates. It is this deterministic network that determines the graphon model analyzed in Section 3. The characterization of extremal equilibrium valuations in terms of cutoffs will be found there. Section 4 characterizes the optimal cash injection policy in the graphon. We also show how this policy translates into a policy for a large finite network with approximately the same performance.

2 The Stochastic Block Model

In the equity cross-holding network of Elliott et al. (2014) there are firms; each firm has a cash endowment and a (book) value . A share of firm is held by firm . Firms pay a bankruptcy cost if their values drop below a threshold . The equilibrium values of firms satisfy the system of equations

| (1) |

where is the indicator function which takes value when and value when . The system of equations is more compactly represented in vector notation: write for the (column) vector of valuations; for the vector of endowments; for the vector indicator which picks out indices for which ; and for the cross-holdings matrix interpreted as the adjacency matrix of an edge-weighted directed graph with self links permitted. The matrix of cross-holdings is not in general symmetric—there is no reason to believe that equals in general—and abeyant a cross-holding, we set if the corresponding edge is absent in the graph. In vector form the equilibrium firm valuations may be identified with the solutions of the non-linear fixed-point equation

| (1’) |

There can be multiple equilibria and they form a lattice. We focus on the extremal (maximal or minimal) equilibria.

A stochastic block equity network

We will generate a random network via a stochastic block model and then construct equity cross-holdings based on this random network. The firms are partitioned into blocks representing distinct firm types; the blocks can differ in size. A random digraph (directed graph) is generated by inserting a directed edge between firms with a probability depending only on the blocks in which the firms reside: insert an edge directed from a firm in block to a firm in block with probability , the directed edges being independent of each other. Denote the realization of the multi-type random digraph by and its adjacency matrix by where if is in the th block and is in the th block. The directed edges of represent directional equity sharing links.

We proceed to graft a regular equity-sharing model atop the engendered random graph . Suppose is a fixed parameter of the system and, for each , write for the in-degree of vertex .444The possibility that has vanishing probability asymptotically as long as any of the edge probabilities is non-zero and the blocks have sizes growing with . We could finesse this nuisance possibility by conditioning on the high probability set or, simply, by just setting in the diagonal terms of the adjacency matrix . Either approach will introduce a small amount of notational clutter that will have to be carried through the analysis without ultimately changing any of our reported results. We will accordingly unclutter presentation by ignoring this notational nuisance: suppose resolutely from now on that for each . We form a regular equity cross-holdings matrix by setting

| (2) |

The interpretation of the model is that equity shares flow only across the directed edges in the graph with a fixed fraction of the equity of each firm shared evenly between the firms that are connected by an edge to . The quantity is called exposure and represents that portion of each firm’s valuation that is held by investors external to the network. This is also how random networks are modeled in Elliott, Golub, and Jackson (2014).

It is as well to clear up a terminological point here. The vector of valuations , called “book” values, inflates actual firm valuations because of double counting. Elliott, Golub, and Jackson (2014) sidestep this by focusing instead on the “market” values

which are the values held by outside investors. A firm’s health is now assessed by its market value and in the Elliott, Golub, and Jackson (2014) formulation all that is requisite is that the indicator in the fixed-point equation (1’) be replaced by where is a fixed market insolvency threshold. Specialized to our setting, market values are related to book values via the simple scaling relation and, as pointed out in Amelkin, Venkatesh, and Vohra (2021), the two formulations for the fixed-point equation are equivalent once is scaled appropriately: our book value insolvency threshold is related to the market value insolvency threshold via the simple scaling relation . If a firm defaults at some profile of book values in our setting, it will also do so with respect to its market value, and vice versa. Hence, for analytical purposes we may safely ignore the distinction between book and market values and focus on the book value equilibria of the fixed-point equation (1’).

A block-regular clique

The random equity cross-holdings matrix thus constructed is generically, by design, asymmetric. While individual instantiations can vary wildly, the analysis of equilibria is simplified enormously by virtue of a concentration phenomenon in the theory of random matrices: the equilibrium valuations associated with almost all instances of concentrate at the equilibrium valuations associated with a fixed matrix of cross-holdings, , that we identify with a block-regular clique.

Some notation: write for the expected in-degree of vertex . Suppose block is comprised of vertices, . If is in block , we may then identify

and the expected in-degree of a given vertex is completely determined by the block in which it resides. Form the block-regular cross-holdings matrix whose entries are given by

| (3) |

whenever is in block and is in block . We call the corresponding equity sharing network a block-regular clique; it is the extension of the regular clique described in Amelkin, Venkatesh, and Vohra (2021) to the stochastic block setting.

With the parametric setting unchanged—endowment vector , failure cost , and threshold —write for the equilibrium firm valuations associated with the block-regular clique. In analogy with (1’), satisfies the fixed-point equation

| (4) |

As before, there can be multiple solutions.

Putative equilibria and concentration

The fixed-point equations (1’) and (4) induce a family of putative equilibria that we now describe. For each fixed binary vector consider the fixed-point equations

| (5) |

We call each such a putative solvency vector and think of it as identifying a putative list of solvent firms: firm is putatively solvent if and putatively insolvent if . The solutions of the fixed-point equations (5) can be inconsistent in that the picture of solvency that emerges need not agree with , hence the hedge “putative”. A putative solvency vector is feasible for the random cross-holdings matrix if, and only if, the corresponding fixed-point satisfies

Likewise, is feasible for the block-regular cross-holdings matrix if, and only if, the corresponding fixed-point satisfies

The equilibria associated with the fixed-point equations (1’) and (4) may hence be associated with the feasible solutions of (5).

A geometric viewpoint adds color to the picture. Each putative solvency vector induces a feasibility orthant of points in satisfying

The feasibility orthants partition into regions as varies over . A putative solvency vector is feasible for a given cross-holdings matrix if, and only if, the corresponding orthant contains its putative solution: is feasible for (respectively, ) if, and only if, (respectively, ).

The value of the putative fixed-point formulation (5) is that it replaces the non-linear fixed-point formulation (1’) which, in general, has a multiplicity of somewhat opaque solutions, by a system of linear fixed-point equations each of which has a unique, completely characterized solution. The price to be paid for the analytical felicity conferred by this finesse is that not all the putative solutions are feasible: one has to winnow through the list to extract the equilibria.

We now consider large random networks and show a concentration result for putative equilibria: the values are close to the values . Reintroduce the explicit dependence on in the notation to keep the role of dimensionality firmly in view. Suppose is any component-wise uniformly bounded sequence of endowment vectors and is any sequence of putative solvency vectors. The insolvency cost and the number of blocks are held fixed, as are the inter-block edge probabilities , and we assume each block contains a non-vanishing fraction of firms. Consider now a sequence of multi-type random directed digraphs , the induced random cross-holdings matrices , and the corresponding block-regular cross-holdings matrices . Let and be the corresponding sequences of putative solutions of the fixed-point equations (5).

Now introduce asymptotics. Our first result says that, for large , the putative solution in the stochastic block model is close to the putative solution in the block-regular clique. The following theorem says this somewhat more succinctly and accurately—and a lot more besides. The proof may be found in the appendix.

Theorem 1.

almost surely as .

With high probability we may conclude that, for any chosen sufficiently small, , eventually, for all sufficiently large . The result characterizes putative equilibria, but will be applied in the next section to characterize actual equilibria.

The proof shows, by applying Bernstein’s inequality, that with high probability the spectrum of the matrix of cross-holdings is close to the spectrum of the deterministic matrix . The remainder of the analysis establishes that potential small perturbations to the matrix of cross-holdings do not have large impacts on the values of firms at the putative equilibrium . A challenge relative to prior concentration results is that the network of connections is directed, so results on Hermitian matrices cannot be applied.

In the next step we finesse the usual computational complications associated with edge effects in discrete networks by passing to a continuum analogue of .

3 The Graphon Model

This section describes the graphon model as well as characterizes extremal equilibrium firm valuations in terms of cutoffs.

A kernel is a bounded, symmetric, measurable function .555It is more usual to define graphons on the Cartesian product of the closed unit interval with itself. Our decision to work with the half-closed unit interval instead is for notational convenience only. None of the results is altered by the addition or deletion of points at the boundary (or indeed, the addition or deletion of sets of Lebesgue measure zero) but the felicitous choice of the half-closed interval as generator avoids the nuisance of having to introduce additional notation merely to handle an inconsequential measure zero case at the boundary. Kernels generalize weighted graphs in the sense that to each weighted graph we may associate a distinct kernel : if the graph has vertex set , vertex weights , and edge weights , partition the unit interval into intervals where has length , and set if .

A kernel taking values in the unit interval, , is called a graphon, the name being a contraction of graph function. In the construction above, if the edge weights take values in the unit interval, then is a graphon. In the case of a simple, unweighted graph, the associated graphon takes values in . Viewed more broadly, graphons provide a natural generalization of Erdös–Rényi random graphs and, more generally, multi-type random graphs, via the intuitive interpretation of the values as probabilities of links.

Conversely, a graphon can be interpreted as a limit of a sequence of graphs with an increasing number of vertices (see Lovász (2012)).

A graphon equity network

If we relax the symmetry requirement on we obtain continuous analogs of directed graphs. This is the segue to the continuum germane for our purposes. Suppose, henceforth, that is a directed graphon, that is to say, is bounded and integrable, not necessarily symmetric. To obviate trivialities, we suppose that, for each , is non-zero in some -interval of positive measure.

Passing to a continuous limit of equity networks we may interpret the unit interval as a continuum of firms, each associated with a label , with the natural interpretation now that the (directed) graphon denotes the share that firm holds in firm . Then represents that fraction of the value of firm that is held by other firms in the network including firm . Reusing notation from the discrete setting, we suppose . This is the continuous analog of the sub-stochasticity condition on the cross-holdings. We may interpret as the (maximal) fraction of value held in-network with at least of the value held by investors external to the network. Call such a an equity graphon.

In the continuous limit, firm valuations are replaced naturally by valuation densities (with units of value/length): the total valuation of firms in an interval is given by . Reusing notation, we are now led to write a formal continuous analogue of the fixed-point equilibrium equation (1) in the form

| (6) |

In this equation represents the valuation density at the point (with the lower case symbol serving to distinguish the continuous from the discrete), is bounded with representing the endowment density at , and is the bankruptcy cost density.

An equilibrium in the equity graphon is associated with a solution of the fixed-point equation (6). While individual equilibria can have a rather wild and chaotic character, a standard application of the Knaster–Tarski theorem provides an elegant superstructure to the family of equilibria. Imbue any space of functions on the unit interval with the natural, pointwise partial order : if for each .

Proposition 1.

The set of equilibria of the fixed-point equation (6) forms a non-empty, complete lattice with respect to the pointwise partial order .

We conclude a fortiori that the fixed-point equation (6) has at least one solution, and indeed that there is a unique maximal equilibrium and a unique minimal equlibrium . The maximal equilibrium pointwise dominates all other equilibria, while the minimial equilibrium is pointwise dominated by all other equilibria. The maximal and minimal equilibrium may coincide in which case (6) has a single solution. Say that an equilibrium of the block equity graphon is extremal if it is maximal, , or minimal, .

A block equity graphon

Partition the unit interval into sub-intervals, each sub-interval representing a contiguous block of firms of a given type. Denote by the length of the th sub-interval or block: this represents the fraction of all firms that are of type . With , write for the partial sums and identify the sub-interval corresponding to firms of type by . A generic firm is indexed by ; it is of type if .

We suppose that endowments are type-dependent and piecewise smooth. Without loss we may take it that firms of each type are ordered by increasing endowment. Accordingly we begin with a family of type-specific endowment functions where, for each , is continuously differentiable and increasing in the sub-interval , and stitch these functions together to create an endowment density

| (7) |

which is piecewise continuously differentiable and increasing in every sub-interval. Intuitively, our formulation corresponds to firm values drawn randomly from distributions that can depend on the types . The function is then the CDF of this density. A leading case is linear, which corresponds to values drawn uniformly from intervals .

In analogy with the construction of the regular-block clique in the discrete setting, equity sharing links between firms are described via a function whose value at any given point depends only on the types of and : if is of type and is of type . With representing, as before, the in-network shared fraction of equity, we identify the block equity graphon

Some notation clarifies matters: if then, reusing notation from the discrete equity setting, the integral

is determined solely by the type of firm . If firm is of type and is of type , then

| (8) |

and a comparison with (3) shows that we have constructed the block equity graphon analogue of the block-regular clique.

The justification of the block equity graphon formulation (8) rests in the fact that it can be viewed as the natural continuum limit of the stochastic block model equity network (2) of the previous section; the utility of the formulation rests in the computational simplicities that a passage to the continuum brings.

For the graphon to give a reasonable approximation, we require that firms are small and the cross-holdings are sufficiently diversified. In practice, an important concern is that individual firms can generate systemic risk. Our model could be extended to allow a finite number of such large firms as well as a continuum of infinitesimal firms represented via a graphon. We can then study equilibria by jointly analyzing a discrete problem and a continuous problem, and the latter will be amenable to the techniques we develop in the remainder of the paper.

Cutoffs and cutoff equilibria

In view of (7) and (8), the generic fixed-point equation (6) for equilibrium valuations reduces in the case of the block equity graphon to the family of equations

| (9) |

as the firm of type traverses through . The block structure of the graphon is manifested in the middle term on the right which is piecewise constant in each interval .

The example below will illustrate that a simple characterization of all equilibria of the block equity graphon will be elusive. Within any block, the intervals of solvency and insolvency can fluctuate wildly. We conjecture our concentration results have analogues for larger classes of equilibria (e.g., when all firms above a cutoff are solvent and all firms below the cutoff are insolvent), but our subsequent focus will be on the extremal equilibria.

Example 1.

The swap. For any (Lebesgue-) measurable set on the line, write for its translation consisting of the points as varies over . We take to be larger than the diameter of so that . Continuum exemplars for are choices of tiny intervals while discrete exemplars are singleton sets, though the structure does not preclude wilder sets. With this for preparation, suppose now that both and are subsets of some interval . Introduce the nonce notation

The right-hand side is positive in view of the monotonicity of .

Swapping solvency and insolvency: I. Suppose is an equilibrium of the block equity graphon which satisfies

| (10) |

In words, firms in are solvent with a margin while firms in are insolvent with the same margin. Construct a new function by setting

| (11) |

In rough terms, is constructed by swapping endowment-adjusted values of and as varies over while keeping all other values fixed. The symmetry of the swap keeps the cross-share holding contribution due to the second term on the right in (9) unchanged: as for each , by grouping terms inside the integral, we have

Moreover, as for each , in view of (10), we see that

An easy algebraic verification now shows that is another equilibrium of the block equity graphon. Indeed, leveraging the swap (11), if , then firm is solvent (with margin ), and so

Similarly, if , then firm is insolvent (with margin ), and so

The remaining cases are trite as if is not in or in . Thus, the endowment-adjusted swap (11) creates another equilibrium of the block equity graphon, this time with the roles of insolvency and solvency interchanged for and .

Swapping solvency and insolvency: II. Reusing notation, suppose is an equilibrium of the block equity graphon where firms in are solvent and firms in are insolvent:

We don’t need a margin anymore as with the roles of and reversed the endowments are working in our favor. Following the same argument as before, it is easy to verify that the swap (11) yields a new equilibrium which is insolvent over and solvent over . Or simply reverse the previous construction. ∎

While an arbitrary equilibrium can have complicated structures, the extremal points of the lattice of equilibria inherit a more regular character from the block structure of the graphon. These extremal equilibria are the most important members of the lattice of equilibria: they delineate bookend bounds on the overarching valuation picture and stability, and can also be selected via dynamic processes in which firms fail sequentially. We focus on extremal equilibria from this point onwards.

Proposition 2.

If is an extremal equilibrium of the block equity graphon, then, for each , the restriction of to is (i) increasing and (ii) continuous from the right with at most a single point of jump. Moreover, (iii) if has a jump at the point in , then and, furthermore, if is maximal, and if is minimal.

We proffer two observations and two definitions motivated by them and defer the elementary proof to the appendix.

-

1.

If both and have jumps at points, say, and , respectively, in an interval , then . It follows that if either extremal equilibrium has a point of jump in any interval then the extremal equilibria are distinct. As a corollary, if the maximal and minimal equilibira coincide then the firms of each given type are either all solvent or all insolvent.

-

2.

Part (iii) of the theorem is where the graphon model proves useful. While the extremal equilibria are monotone in each block in the discrete setting as well, it is not generically true in the discrete setting that the size of the jump achieves exactly the distress cost . Nor is it true in the discrete setting that at the point of jump the maximal equilibrium achieves a valuation exactly equal to the insolvency threshold or that the minimal equilibrium achieves a valuation exactly equal to . The elimination of such nuisance edge effects in the continuum simplifies analysis and clarifies conclusions.

-

3.

In view of (iii), if has a jump point at , then and we identify with the smallest index at which a firm is solvent. A jump point , if one exists in the interval , of an extremal equilibrium represents a cutoff where the character of the extremal equilibrium valuation changes abruptly. View these cutoffs more expansively to include intervals in which does not have a jump by setting if all firms in are solvent and if all firms in are insolvent. We call the set of cutoffs (associated with the extremal equilibrium ).

-

4.

If a cutoff is at the boundary then the firms in are either all solvent or all insolvent.666If one were to be punctilious, in the latter case one must account for the possibility of a jump exactly at , which occurs if and , by modifying the language to exclude the measure zero point but this seems obsessively pedantic. It does not change the general tenor of the observation. The case where is interior in is more interesting. Informally speaking, in this case there is a cutoff below which all firms of type are insolvent and above which all firms of type are solvent:

In a more graphic language, we say that an extremal equilibrium is a cutoff equilibrium if all its cutoff are interior.

For a cutoff equilibrium to be computationally useful, the cutoffs should have a convenient characterization. As an illustrative example, we consider the simplest case when the endowment density linear within each block.

Example 2.

Suppose the endowment density is piecewise linear with each increasing linearly from to in the interval :

If has a jump in the interior of the interval (a fortiori, if it is a cutoff equilibrium) then the endowment of the cutoff firm is linear in the cutoff type . In view of Proposition (2), , and so the fixed-point equation (9) yields

| (12) |

Suppose there is a jump discontinuity in each block; the subsequent equations are easily adapted to relax this assumption. Iteratively substituting for using equation (9) (details can be found in the proof of Theorem 3), and using to denote the matrix , we obtain the linear equations

Here is the diagonal matrix whose entry is The upshot is that the linearity of implies the cutoffs are characterized by a system of linear equations. ∎

Connection to the SBM

The justification for the introduction of the block equity graphon is that it is, in a certain formal sense, the natural continuous limit of the SBM and replicates its equilibrium structure. The construction is standard though the concentration argument demonstrating asymptotic equivalence requires technical finesse.

As a gedanken experiment, consider a sequence of SBM networks engendered by a sequence of multi-type random digraphs . We suppose that the number of types is fixed, as are the inter-block link probabilities , and that the number of firms of each type grows linearly with . In the notation of the previous section, let be the number of firms of type in the graph . Then there exist positive real values , …, with such that , …, as .

The block equity graphon (8), parametrized by , …, , and the link probabilities , is the natural limit object. Starting with the block equity graphon we can reverse the procedure and construct a sequence of random equity networks by sampling from the continuum model. For given , begin by identifying vertices of a random graph on vertices with equispaced points in the unit interval: . For each ordered pair of vertices insert a directed edge from to with probability , where as before, the link probability function takes value when and . Directed edges are drawn independently. The resulting multi-type random graph has approximately vertices of type and engenders a stochastic block equity network of firms via the regular equity-sharing formulation (2).

The number of vertices of type in the sampled multi-type directed random graph differs from only in the addition or deletion of a bounded number of points near the boundary of the interval . Hence, the graphs and are stochastically asymptotically equivalent. In this sense the block equity graphon (8) is the continuous limit of the stochastic block equity sequence. But more can be said: the graphon mimics the asymptotic equilibrium structure as well.

At an extremal equilibrium in the stochastic block equity sequence engendered by the sampled sequence of multi-type random digraphs , let be the maximal index of a firm of type that fails and let be the minimal index of a firm of type that does not fail.

We will need a notion of stability to ensure that perturbation arguments from a Picard-style iteration converge. In the interests of providing an early preview of the type of result that is achievable we state it sans specifics: we reserve the definition of stability to the next section where it arises more naturally in the consideration of a fictitious dynamic in the context of the impact of cash infusions, and defer the bulk of the proof to the appendix.

Theorem 2.

Suppose an extremal equilibrium of (9) is stable. Then along the sampled stochastic block equity sequence, and converge almost surely to the cutoffs for all .

The theorem says that in large finite random networks, the set of solvent and insolvent firms at an extremal equilibrium are approximately determined by the cutoff types at the maximal equilibrium in the graphon from which they have been sampled.

We briefly describe the idea of the proof. The maximal equilibrium on the graphon is defined by a cutoff in each block, and we can define a putative equilibrium in a finite network by declaring firms solvent above and insolvent below these cutoffs. A key ingredient in the proof is Theorem 1, which we use to show this putative equilibrium is likely to be “close” to being a feasible equilibrium on large finite networks. There are, however, small differences in values between this putative equilibrium and the graphon maximal equilibrium. The stability condition implies these differences do not lead to large spillovers, and we show there is indeed a feasible equilibrium near the putative one. This establishes a lower bound on the set of solvent firms at the maximal equilibrium on a large finite network. Similar arguments show that given a sequence of equilibria on growing finite networks, we can construct a nearby equilibrium on the graphon. This gives an upper bound on the set of solvent firms at the maximal equilibrium on a large finite network, and these lower and upper bounds together imply Theorem 2.

4 Cash Infusions

We use the graphon model to determine the optimal way to inject units of cash so as to maximize the fraction of firms that are solvent in a maximal equilibrium. A cash infusion with budget is an integrable function with . Think of as representing the amount of cash provided to firms in an infinitesimal interval at the point .

The spillover matrix

The challenge is to quantify the spillovers generated by injecting capital into a particular firm. This is where the graphon model comes into its own. We use it to compute for each block , the share of firms in block whose values drop below the solvency threshold if an infinitesimal share of firms in block fail. The ability to conduct marginal analyses of this kind are impossible in a discrete set up.

Mirroring our consideration of putative equilibria of stochastic block networks in (5), for any given Boolean function , consider the graphon fixed-point equation

which, in the setting of the block equity graphon (8), simplifies to

| (13) |

for . Borrowing from our language in the stochastic block setting, we call each such a putative solvency function and think of it as identifying a putative set of solvent firms in the continuum: firm is putatively solvent if and putatively insolvent if . We naturally call any solution of (13) a putative equilibrium. Following in the same vein as before, a putative solvency function is feasible if

in which case is an equilibrium solution of (9).

For obvious reasons we focus on putative solvency functions that correspond to cutoff equilibria. In a mild abuse of notation, for each vector , write for the indicator function parametrized by which satisfies

as varies from through . The associated putative equilibrium solves the system of equations (13) with . If is a cutoff equilibrium valuation density with cutoffs , then is called a feasible solvency function and the associated putative equilibrium is feasible and equal to .

Suppose now that are the cutoffs in the maximal equilibrium of (9).777Our definition of the spillover matrix below can be modified for the minimal equilibrium case. We instead decrease the cutoff by and define to be the derivative at of the measure of firms below the cutoff with putative equilibrium value . Theorem 3 will continue to hold. Perturb one component, say the th, very slightly, to form the vector where is tiny. Imagine for a moment that the vector corresponds to the cutoffs of a different equilibrium in which a slightly larger set of firms of type are insolvent. This has a spillover effect on firms of type through the cross-holdings that firms of type have with firms of type . It is this spillover we need to quantify. The difficulty is that need not describe an equilibrium. Instead, we will focus on the associated putative equilibrium

Some firms of type that are putatively solvent before the perturbation may become insolvent after the perturbation. We introduce notation to track them. Write for the set of in the interval for which but the corresponding value of the putative equilibrium satisfies .

With this for preparation, for each and , set

| (14) |

where stands for Lebesgue measure. Call the matrix with entries the spillover matrix.

The entries of the spillover matrix measure the rate of change of (putative) solvency of firms of any given type occasioned by the failure of an infinitesimally small set of firms of any other given type. As foreshadowed in the preamble to Theorem 2, we need a stability condition to ensure that the positive spillovers from an injection of capital are limited.

Stability assumption: The spectral radius of the spillover matrix is strictly less than one.

Recall from the construction of the block equity graphon (8) that

represents the share of a firm of type that is held by a firm of type . As in Example 2, let denote the matrix of cross-shares and be the diagonal matrix whose entry on the leading diagonal is .

The following result gives an explicit expression for the spillover matrix, which is obtained by analyzing how firm failures cascade in the graphon. We include the proof here as it demonstrates the types of calculations driving several of our examples and results, but the reader can also safely skip to the characterizations of optimal cash infusions below.

Theorem 3.

If represents the cutoffs of a cutoff equilibrium, the corresponding entries, , of the associated spillover matrix are given by

Proof.

Let be the cutoffs in a cutoff equilibrium of (9). Perturb one component, say the th, very slightly by , to form the vector

We focus on the associated putative equilibrium Following the proof of Proposition 2 let , then, for in the sub-interval . Also, let be the average endowment of firms in block . Recall, is the partial sums of the block lengths with per standard convention. Then

For and we have

For and when and when Working as in Example 2, a recursive application of these identities shows that

Let denote the column vector whose row is Then,

| (15) |

We use equation (15) to determine . To this end, denote the entry in the row and column of by Then,

If we perturb by this reduces the value of all firms in block by . The additional firms that fail as a consequence are those whose values were between and before the perturbation. Since and the relevant firms’ endowments and values differ only by a constant, these are exactly the firms with endowments between and . The measure of this set of firms is

The entry is defined to be the derivative of this measure in evaluated at . Applying the inverse function rule we determine this derivative to be

as desired. ∎

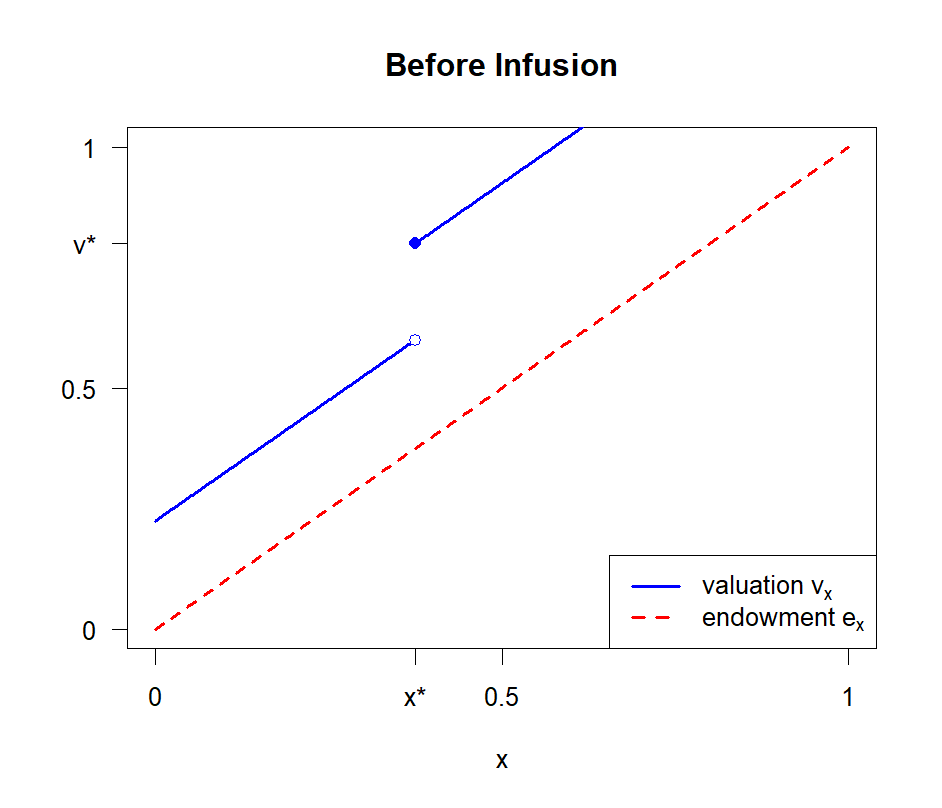

Example 3.

Consider a single block with linear firm endowments given by . Suppose the maximal equilibrium before the cash infusion is characterized by an interior cutoff but the budget, is insufficient to make all firms solvent under an optimal infusion.

To determine the spillover matrix, observe that the matrix in this case will be scalar with value and will just be the number 1. Hence, . It is also easy to see that . Thus, the matrix is the scalar Stability requires that .

Optimal infusions

Given a cash infusion , let be the firm valuations at the maximal equilibrium with cash endowments and be the firm valuations at the maximal equilibrium with endowments . Our goal is to find a cash infusion with budget that maximizes the sum of firm valuations, .888Since the objective only depends on integrals of , we will characterize optimal interventions up to changes in values on measure zero sets. This is equivalent to maximizing the fraction, , of solvent firms. While we focus on the maximal equilibrium our analysis extends to the minimal equilibrium as well. In this way one can bracket the magnitude of the impact of a cash infusion.

Given a cutoff equilibrium on the graphon, recall matrix where

The entries of matrix are the instantaneous rates at which firms in block fail when an infinitesimal fraction of firms in block fail. Finally, let be the vector of ones and be the standard unit basis vector.

Proposition 3.

Suppose the support of an optimal intervention is interior in each block. In each block there exists such that increases the endowments of all firms in an interval with measure upto a constant , but leaves the endowments of other firms in the block unchanged.

The optimal policy uses global information about the network encoded in the matrix as well as local information, the endowments of each firm. The measure of firms directly rescued in each block is proportional to the Katz-Bonacich centrality of the block in the weighted network defined by the matrix , adjusted to account for the cost of rescuing firms in that block.

Within each block, the optimal infusion increases the cash endowments of an interval of firms with endowments in to . At the post-infusion maximal equilibrium, these firms all have value . There is an additional interval of firms with endowments that would be insolvent without the infusion, but are solvent after the infusion. Intuitively, these correspond to firms that would have not failed directly but are exposed to contagion if other firms are allowed to fail. A graphical depiction appears in Figure 1 of Example 4.

The next proposition explicitly characterizes the optimal intervention when the are linear. It will specify for each block, which firms should be bailed out and by how much. It will also tell us the measure of firms within a block that are indirectly bailed out because of positive spillovers.

Theorem 4.

Suppose the support of an optimal intervention is interior in each block and each is linear with slope . Then, for each block there exists and such that the optimal intervention increases the endowments of firms in the intervals to , where the are characterized by

| (16) |

for all and and the budget constraint

and the are given by

The assumption that is linear can be interpreted as the endowments in each block being uniformly distributed. Nevertheless, Theorem 4 can be extended to accommodate that are non-linear but approximable by a piecewise linear function with a bounded number of segments. Within each block split the interval of endowments into several pieces consisting of firms with endowments in the same linear segment and treat each of these pieces as a block.

Theorem 4 characterizes the implicitly. The next two examples provide an illustration of how the optimal intervention can be computed from this characterization.

Example 4.

We continue Example 3 by computing the optimal cash infusion. Recall that the matrix is the scalar

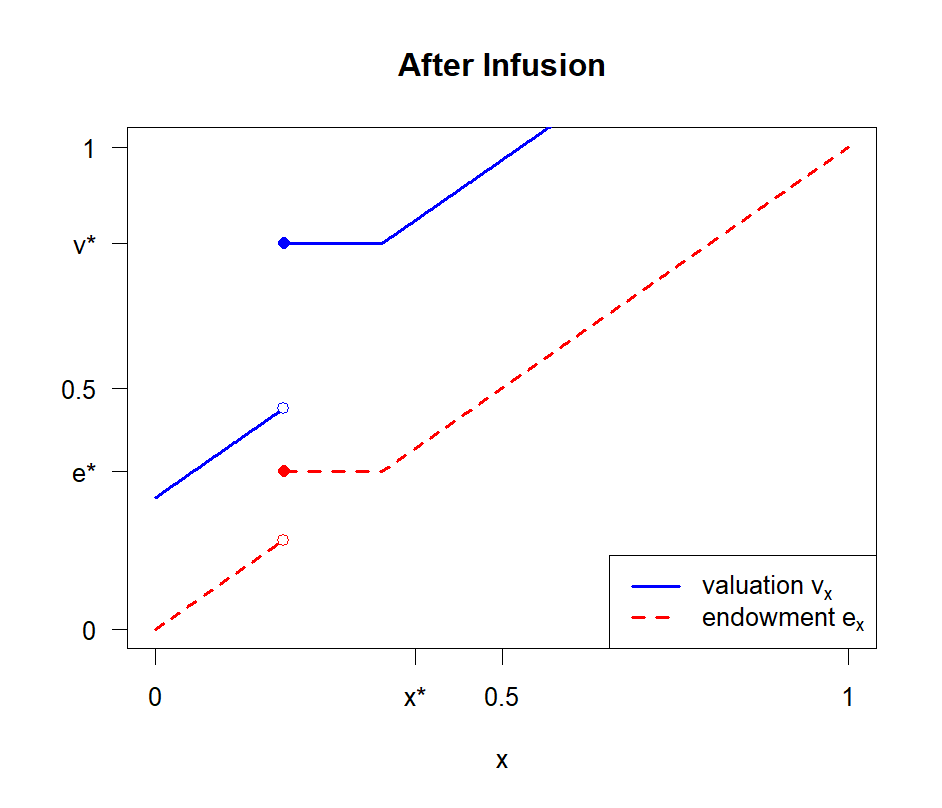

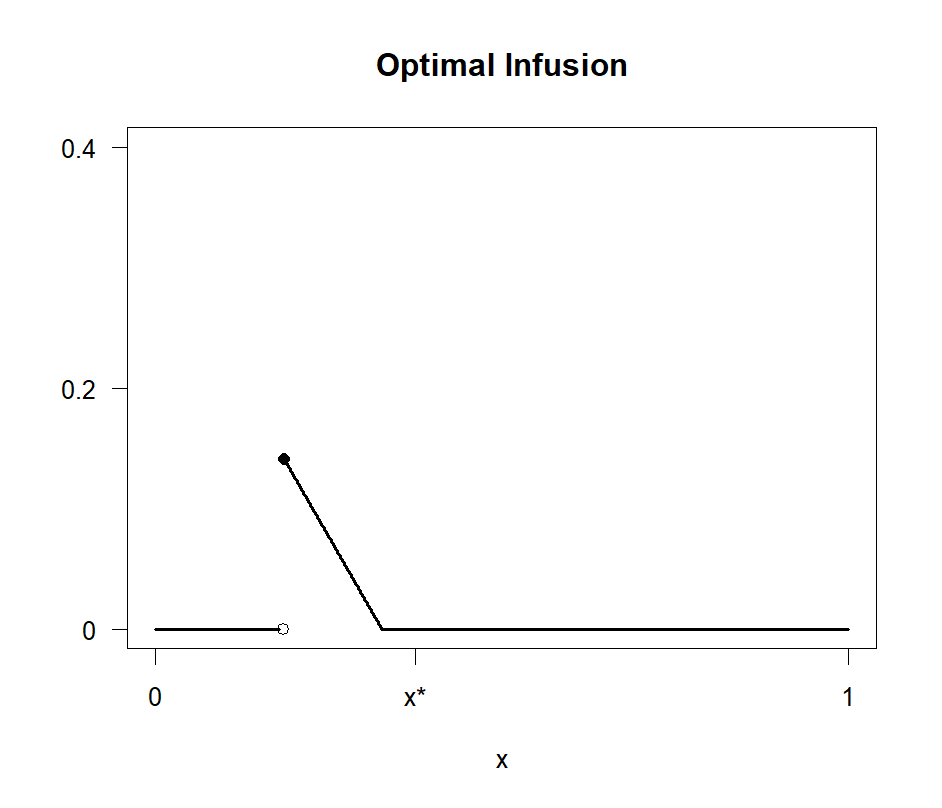

If is the measure of firms in the block that receive an injection, then, Proposition 3 tells us that for some the optimal intervention increases the endowments of firms in an interval to . Therefore, each firm receives an infusion of which means the total infusion is If is the total budget, and , then, , otherwise Notice, the measure of firms that receive an injection is independent of either the exposure, , or the distress cost . In the remainder of this example we suppose .

Consider Figure 1. The top two panels (Figures 1(a) and 1(b)) show firm valuations (blue solid lines) and endowments (red dashed line) before and after the infusion, respectively. The support of the infusion is an interval of firms strictly to the left of the cutoff . The bottom panel (Figure 1(c)) depicts which firms receive an infusion. Each of them receives sufficient cash to achieve value after the intervention.

An additional interval of firms is not directly bailed out by the cash infusion, but are nevertheless rescued due to spillovers. One interpretation is that this interval contains firms that would fail due to a domino effect in the absence of an intervention. We can, in this example, compute the measure of such firms.

Directly moving firms from insolvency to solvency can lead to at most insolvent firms becoming solvent. Therefore, , the measure of firms indirectly rescued by the optimal cash infusion is

As one might expect, as , the exposure of each firm, increases, the measure of firms that are indirectly rescued increases. This is because and increase with .

As , the slope of the endowment function, increases, the measure of firms that receive an injection declines. Furthermore, because both and decline with , the measure of firms that are indirectly rescued, also shrinks. In both cases it is because each firm needs less cash to get over the solvency threshold.

The number of indirectly rescued firms increases with . This is because increases with . Increasing , the amount of cash available to inject into firms has three effects. First, the measure of firms that receive an injection increases. Second, the interval of firms that receive an injection shifts to the left, because the cutoff type becomes smaller. Thus, an insolvent firm that was close to the solvency threshold that received an injection when was small, will not necessarily receive it when increases. Third, the measure of firms indirectly rescued increases with , but this indirect effect suffers diminishing returns.

Example 5.

We consider a simple core-periphery model where the core will be block 1 and the periphery will be block 2 but the cross-holdings satisfy . Thus, firms in the periphery only own shares in core firms. Firm endowments in the core are described by and by in the periphery. For economy of exposition only, assume that the core and periphery each contain half of the firms.

Before the infusion, the maximal equilibrium is characterized by two interior cutoffs, for block 1 and for block 2. Proposition 3 tells us that for some , the optimal intervention increases the endowments of firms in intervals to for We describe the intervention when is small enough, so that is interior in each block. The budget constraint is

The matrix of equity cross-holdings is given by

while . By Theorem 3, the spillover matrix is

| (17) |

Applying equation (16),

| (18) |

When , for example, because endowments are drawn from the same distribution in the core and periphery, the optimal bailout injects cash to the same measure of firms in each of the blocks. In general, the optimal bailout injects cash to more firms in a block where the endowments are less dispersed because there are more firms close to the failure threshold. But that difference diminishes when is larger and is smaller, i.e., when the peripheral firms are more exposed to the core firms.

The budget constraint describes an ellipse in the space. Equation (18) describes a hyperbola and it is straightforward to show that there is a single intersection in the non-negative orthant.

The measure of firms indirectly rescued in each block is

In the special case , so that as well, we have

Therefore, while the number of firms directly bailed out is the same in each block in this case, more firms are indirectly snatched from insolvency in the core than in the periphery. This is because firms in the core have equity holdings in both groups rather than only the core, so they benefit more from spillovers from the bailout. The gap is larger when is larger relative to as then the periphery’s holdings are smaller.

Optimal Cash Infusions in Random Networks

In this section we discuss how to extend the optimal cash infusion in the graphon setting to a finite instance sampled from the graphon. We show that given a cash infusion in the graphon setting, there exists a cash infusion in the corresponding finite instance keeping at least the same proportion of firms solvent for a slightly higher budget.

As before, we consider a stochastic block equity graphon and a sequence of sampled from . A cash infusion for a finite random network specifies the amount of cash given to each firm Given a cash infusion , we write for the values of firms at the maximal equilibrium after the cash infusion.

To maintain consistency with the continuum model, suppose the budget for the finite random network cash infusion is for some small . Thus, the average budget per firm is . In other words, we increase the budget per firm by an arbitrarily small amount when we switch from the graphon to the sampled finite network. We now show that given the optimal intervention on the continuum, we can find an intervention keeping at least the same fraction of firms solvent on large random networks using a slightly higher budget. To formalize this on the graphon, recall we use for the Lebesgue measure.

Proposition 4.

Let and consider the optimal cash infusion with budget for the block equity graphon. There exists a sequence of cash infusions with budgets such that

The construction gives a bit of additional cash to firms near the solvency threshold to insure against adverse network draws. As the network grows large, our concentration results imply the amount of additional cash needed vanishes.

5 Conclusion

Even if one ignores the problems of moral hazard, private information and equilibrium multiplicity, the problem of finding which firms in a financial network to bailout, is a difficult one. This paper uses a continuum analog of the underlying financial network to identify which firms should be prioritized for a bailout. Whether a firm is bailed out or not depends upon its cash endowment and how ‘central’ is the block it belongs to. The number of firms directly bailed out in each block is proportional to the block’s Katz-Bonacich centrality, adjusted to account for the cost of rescuing firms in that block.

Acknowledgements

We thank Mengjia Xia for useful comments and Chengyang Zhu for useful comments and implementing numerical examples.

References

- Afonso et al. (2013) Afonso, G., A. Kovner, and A. Schoar (2013): “Trading Partners in the Interbank Lending Market,” Staff Reports 620, Federal Reserve Bank of New York.

- Amelkin et al. (2021) Amelkin, V., S. Venkatesh, and R. Vohra (2021): “Structure and Dynamics of Contagion in Financial Networks,” Working paper.

- Azevedo and Leshno (2016) Azevedo, E. M. and J. D. Leshno (2016): “A supply and demand framework for two-sided matching markets,” Journal of Political Economy, 124, 1235–1268.

- Bech and Atalay (2010) Bech, M. and E. Atalay (2010): “The topology of the federal funds market,” Physica A: Statistical Mechanics and its Applications, 389, 5223–5246.

- Blasques et al. (2018) Blasques, F., F. Bräuning, and I. v. Lelyveld (2018): “A dynamic network model of the unsecured interbank lending market,” Journal of Economic Dynamics and Control, 90, 310–342.

- Borg et al. (2017) Borg, C., J. T. Chayes, H. Cohn, and N. Holden (2017): “Sparse exchangeable graphs and their limits via graphon processes,” Journal of Machine Learning Research, 7740–7810.

- Boss et al. (2004) Boss, M., H. Elsinger, M. Summer, and S. Thurner (2004): “Network topology of the interbank market,” Quantitative Finance, 4, 677–684.

- Chinazzi et al. (2013) Chinazzi, M., G. Fagiolo, J. A. Reyes, and S. Schiavo (2013): “Post-mortem examination of the international financial network,” Journal of Economic Dynamics and Control, 37, 1692–1713.

- Daan and Lelyveld (2014) Daan, i. V. and I. Lelyveld (2014): “Finding the core: Network structure in interbank markets,” Journal of Banking & Finance, 49, 27–40.

- Demange (2018) Demange, G. (2018): “Contagion in Financial Networks: A Threat Index,” Management Science, 64, 955–970.

- Dong et al. (2021) Dong, Z.-L., J. Peng, F. Xu, and Y.-H. Dai (2021): “On some extended mixed integer optimization models of the Eisenberg–Noe model in systemic risk management,” International Transactions in Operational Research, 28, 3014–3037.

- Elliott et al. (2014) Elliott, M., B. Golub, and M. O. Jackson (2014): “Financial networks and contagion,” American Economic Review, 104, 3115–53.

- Erol et al. (2020) Erol, S., F. Parise, and A. Teytelboym (2020): “Contagion in Graphons,” in Proceedings of the 21st ACM Conference on Economics and Computation, New York, NY, USA: Association for Computing Machinery, EC ’20, 469.

- Jackson and Pernoud (2020) Jackson, M. O. and A. Pernoud (2020): “Credit Freezes, Equilibrium Multiplicity, and Optimal Bailouts in Financial Networks,” CoRR.

- Klages-Mundt and Minca (2022) Klages-Mundt, A. and A. Minca (2022): “Optimal intervention in economic networks using influence maximization methods,” European Journal of Operational Research, 300, 1136–1148.

- Lee and Wilkinson (2019) Lee, C. and D. J. Wilkinson (2019): “A review of stochastic block models and extensions for graph clustering,” Applied Network Science.

- Lovász (2012) Lovász, L. (2012): Large networks and graph limits, vol. 60, American Mathematical Soc.

- Minoiu and Reyes (2013) Minoiu, C. and J. Reyes (2013): “A network analysis of global banking: 1978–2010,” Journal of Financial Stability, 9, 168–184.

- Papachristou and Kleinberg (2022) Papachristou, M. and J. Kleinberg (2022): “Allocating Stimulus Checks in Times of Crisis,” in Proceedings of the ACM Web Conference 2022, New York, NY, USA: Association for Computing Machinery, WWW ’22, 16–26.

- Parise and Ozdaglar (2023) Parise, F. and A. Ozdaglar (2023): “Graphon games: A statistical framework for network games and interventions,” Econometrica, 91, 191–225.

- Peltonen et al. (2014) Peltonen, T., M. Scheicher, and G. Vuillemey (2014): “The network structure of the CDS market and its determinants,” Journal of Financial Stability, 13, 118–133.

- Schmeidler (1969) Schmeidler, D. (1969): “Competitive equilibria in markets with a continuum of traders and incomplete preferences,” Econometrica, 37.

- Shi et al. (2019) Shi, M. Y., R. M. Townsend, and W. Zhu (2019): Internal capital markets in business groups and the propagation of credit supply shocks, International Monetary Fund.

- Tarski (1955) Tarski, A. (1955): “A lattice-theoretical fixpoint theorem and its applications,” Pacific journal of Mathematics, 5, 285–309.

Appendix A Omitted Proofs

Proof of Theorem 1.

We will prove a more general result allowing link probabilities to vanish at a polynomial rate.

Given a matrix , we let be the matrix 2-norm. We omit the indices of matrices in the proof.

Define to be the difference between the matrix of cross-holdings and its expectation. We begin with a lemma bounding this difference.

Lemma 1.

Let . Given and , there exists such that for sufficiently large

with probability at least .

Proof.

We first observe that:

We will bound the norm using Bernstein’s inequality:

Lemma 2.

[Bernstein’s Inequality for Matrices] Suppose is a sequence of independent Hermitian matrices satisfying

Write and let denote the matrix variance statistic of the sum:

Then, for all ,

Fix . To apply Lemma 2, condition on the event that for all nodes and all blocks , the number of links are in the interval

(where is the block containing node ). The event holds when all are sufficiently close to their expected values. By the Chernoff bounds, the probability of the complement of this event vanishes at an exponential rate in .

We define the matrix by and let . We will:

-

(1)

Bound the spectral norm of the entry-wise mean .

-

(2)

Bound the spectral norm of the variance .

-

(3)

Bound the spectral norm uniformly on the event .

We now show three claims. We will use the following growth rates repeatedly: is grows at the same rate as for all because each block size is non-vanishing, when the event holds is for all blocks and and nodes in block , and when the event holds and are for all .

Claim (1): is

The entries for in block and in block are equal to if and otherwise. So if is in block and is in block , we compute that

The right-hand side is

Now consider nodes in block , in block , and in block with . We compute that for ,

Since we have conditioned on the event , the quantity

is because and are . So is

Similarly, for we compute that

The right-hand side is again when the event holds.

From the bounds on the entries of , we can express as the sum of a diagonal matrix with entries and an arbitrary matrix with entries . Both of these summands have 2-norm at most . Applying the triangle inequality to this sum, we can conclude that is

Claim (2): is .

By the triangle inequality, it is sufficient to show that is for all . We have

We showed in the previous claim that is so is by the submultiplicativity of the spectral norm. Relaxing the upper bound, this term is since .

To complete the proof of the claim, we must bound . Say is in block . The inner product is

| (19) |

So we have

We computed in the previous claim that conditioning on the event , the expectations of the diagonal entries of are and the expectations of the off-diagonal entries are . From equation (19), the inner product is when holds. So conditional on the event , the diagonal entries of

are and the off-diagonal entries are . Therefore is .

Now recall that

We have shown both terms on the right-hand side are , which proves the claim.

Claim (3): There exists such that when holds.

The summation is . Claim (1) showed that is . So is when holds.

This completes the proofs of the claims. We now apply Bernstein’s inequality with . For all ,

We let and will compute the minimum on the right-hand side. By Claim (2), there exists such that

Therefore,

By Claim (3), there exists such that

Therefore,

Since we can choose , these bounds imply there exists such that

for sufficiently large.

We now compute that for large

where the inequality follows from Claim (1) and the triangle inequality, continuing to take . We conclude that

for large. We have shown the probability of the complement of the event vanishes at an exponential rate in , and increasing if necessary we can take . Since by assumption, this proves the lemma. ∎

By the preceding lemma, the Neumann series

converges with probability at least for sufficiently large. Since and therefore is bounded, the Neumann series

also converges with probability at least

for sufficiently large.

As in the proof of Lemma 19 of Amelkin, Venkatesh, and Vohra (2021), we have

So

by the triangle inequality. We conclude that

| (20) |

by the comparison of the and norms.

Lemma 3.

almost surely.

Proof.

We first compute . By symmetry, has two entries for each block corresponding to firms in that block with and . We call these and , respectively. Then given in block ,

By the Lyapunov central limit theorem for triangular arrays, we can choose such that the probability that the right-hand side has absolute value at least for some node vanishes at an exponential rate in .

Next, observe that the entries depend only on the blocks of and . For each node and each block , we have

for some constant .

The entry of is equal to

By the bound on above, the probability that each summand on the right-hand side has absolute value at least vanishes at an exponential rate in . Since there are summands, this implies almost sure convergence. ∎

Lemma 4.

almost surely.

Proof.

By the submultiplicativity of the norm,

By Lemma 1, given and we have with probability at least . Because , the norm is bounded by some constant . Finally, the norm is at most for some constant because the endowments are bounded. Combining these observations, we find that

with probability at least . Whenever grows at rate at least for some , we can choose such that the right-hand side converges to zero as . Taking any positive , this shows almost sure convergence. ∎

Applying the two previous lemmas to inequality (20) completes the proof. ∎

Proof of Proposition 1.

The equilibria of the equity graphon are the fixed points (if any exist) of the map where

Begin with the easy observation that is order-preserving. Suppose indeed that . Then and, as is non-negative, . We conclude that

for each , whence .

Moreover, if lies in a sufficiently large bounded box, then so does , or, in notation, if, for some sufficiently large , , then . Indeed, there exists such that as the endowment function is bounded and, bearing in mind the sub-stochasticity condition on the equity graphon , we see that

The right-hand side is for any selection .

With so chosen, consider the space of measurable, bounded functions with . Restricting to , we conclude that is order-preserving and maps each element of back into . The stage is set for the Knaster–Tarski theorem (Tarski, 1955, Theorem 1, (i-iii)): as is a non-empty, complete lattice with respect to the pointwise partial order , the set of fixed points of forms a non-empty, complete lattice. ∎

Proof of Proposition 2.

The proof is by contradiction and follows by a small (and simpler) variant of the swap construction of Example 1. Begin with an extremal equilibrium .

(i) Suppose that for some , there exist and points , with . By (9),

As and the term is the same in both expressions, it must be the case that (whence ) while (whence ).

If is maximal, consider the effect of changing to and keeping all other values the same, if . Then

so that . The cross-share holdings term is unaffected if we replace by as the integral is invariant with respect to changes in function value at isolated points,

and we conclude that

whence is a new equilibrium. But then , leading to a contradiction of maximality.

Likewise, if is minimal, consider the effect of changing to and keeping all other values the same, if . Arguing exactly as before,

so that . We are thus led to the conclusion

whence we have yet another equilibrium. But now , leading to a contradiction of minimality.

Thus, in either case, is increasing.

(ii) Introduce the nonce notation for the set consisting of the points in for which and let consist of the remaining points in at which . As is monotone per part (i), and are disjoint intervals (with one of the two possibly empty or consisting of a singleton point). Writing to compact notation, the fixed-point equation (9) satisfies for in the sub-interval , while it satisfies for in the sub-interval . The continuity of the endowment function on now carries the day and is continuous in each of the sub-intervals and .

If either or is empty then is continuous everywhere on . If both intervals are non-empty, by the monotonicity of , there exists a unique point such that for and for . It follows that there is a jump discontinuity at with continuous on either side of it. To show that is continuous from the right it will suffice to show that . We will show a little bit more besides following the same pattern of construction as in part (i).

Suppose has a jump at the point in . Then

Approaching from the right and the left in turn, by the continuity of , we see that

| (21) |

The first of the identities is vacuous if when the jump is on the boundary of .

Suppose, to establish a contradiction, that . Then . But then cannot be on the boundary as else there is no jump. So must be an interior point of jump. Writing for the deficit, by the continuity of , we may select so that . (Any factor could be chosen on the right; the choice of just keeps the algebra neat.) By construction, , whence .

If is maximal, mirror the construction in part (i) by forming a new function by setting and keeping all the other values of unchanged. Then

and we have constructed an equilibrium larger than the maximal equilibrium.

If is minimal, form a new function by setting and keeping all other values of unchanged. Then

and we have constructed an equilibrium smaller than the minimal equilibrium.

Having established a contradiction in all cases, we conclude that and, a fortiori, is continuous from the right.

(iii) It only remains to consider the behavior of the valuation at a point of jump. Suppose that has a jump at the point in . We’ve established that , whence . By (21), it follows that the size of the jump, , is exactly equal to the distress cost .

Now, on the one hand, from the conclusion of the proof of part (ii), while on the other, as a consequence of the just-established size of the jump. Indeed, if then and is forced to contain points with valuations in excess of by the continuity of on the sub-interval . But this contradicts the definition of . We conclude that .

Suppose is maximal and, to set up a contradiction, suppose further that . Reusing notation, write for the excess. By the continuity of we may select a point in such that and we so do. Now form a new function by setting and keeping all other values of unchanged. Then

and we have constructed an equilibrium larger than the maximal equilibrium. With our hypothesis leading to a contradiction, it must hence be the case that if is maximal.

The case when is minimal is even simpler. To set up a contradiction again, suppose that . Form a new function by setting and keeping all other values of unchanged. Then and we have constructed an equilibrium smaller than the minimal equilibrium. As this is impossible, we conclude that if is minimal. This concludes the proof. ∎

Proof of Theorem 2.

We assume that is a maximal equilibrium. The minimal equilibrium case proceeds by a straightforward modification of the same arguments.

Let be a putative solvency vector and recall that are the corresponding values, so that solves

Given a vector of firms with one in each block, we define a putative solvency vector for a finite random network by for all in block . That is, a firm in block is solvent if and only if its index is at least the threshold .

Similarly, given a vector of firms , recall we define a putative equilibrium for the graphon by supposing firms are solvent if and only if . Recall we refer to the corresponding values as and that these values solve

Given , let be the values of firms on a finite network with deterministic link weights and firm failures described by the putative solvency vector . We begin with a lemma establishing several properties of , , and

Lemma 5.

(i) , , and are increasing in ,

(ii) is continuous in and in any neighborhood where is constant and is contained in a single block,

(iii) uniformly in .

Proof.

(i) We prove monotonicity by expressing each of the values in terms of firm endowments and failure costs. Given , we have

where . Substituting for , we obtain

Solving and expressing the in vector form,

| (22) |

We conclude that is a linear combination of the and with non-negative coefficients. Since is increasing in , so are the and therefore the values

Similarly, we have

and therefore

We conclude that each entry of is a linear combination of the entries of and with non-negative coefficients. Since is increasing in , so is .

Finally, we have

and therefore

We conclude that each entry of is a linear combination of the entries of and with non-negative coefficients. Since is increasing in , so is .

(ii) This follows from equation (22) since each term is continuous in the thresholds and the endowment is continuous in .

(iii) Let on the graphon and in the finite case. From equation (22), we have

| (23) |

We also have

The entries of converge uniformly to the corresponding entries of , as the differences are due to the addition or deletion of a bounded number of firms near the boundaries of the intervals . Since the Riemann sums

converge to the integral

the desired limit holds. The convergence is uniform in since there are only finitely many blocks and therefore finitely many such sequences of Riemann sums. ∎

The proof of Theorem 1 shows that there exists a sequence such that the probability that

decays at an exponential rate in (with constants independent of the firms ). We also have the deterministic limit

by Lemma 5(iii).

Combining these limits and applying the triangle inequality, we can choose a sequence such that probability that

also decays at an exponential rate in .

Now let be the set of vectors of firms such that each can be expressed as a rational number with denominator at most . The cardinality of is polynomial in , so

almost surely.

For the remainder of the proof, fix a sequence of realized random networks for which this random variable converges to zero. We will show that for all , along this sequence and . This will imply that almost surely and almost surely for all .

Step 1: for all .

Suppose for the sake of contradiction that for some . Passing to a convergent subsequence, we can assume that converges to some .

Let be the spillover matrix. We next prove a matrix algebra lemma about .

Lemma 6.

Suppose is a non-negative matrix with . There exists a vector with all entries positive and real and a constant such that for all .

Proof.

Because is continuous, we can choose such that for all and , for all and , and .

By the Perron-Frobenius theorem, we can choose a vector with all entries real and positive such that . Taking we have

as desired. ∎

Choose and as in the preceding lemma and consider the thresholds for . Define to be the Lebesgue measure of firms in block above the threshold with values under the putative equilibrium below . Because the derivative of at is linear in each , we have

where the last line follows from our choice of and . Because the are continuously differentiable, we can choose with and such that

for all and all . There exists such that

for all and all . By monotonicity (Lemma 5(i)),

for all with and all .

Recall we chose such that . So we can fix such that . By Lemma 5(ii) and the density of the rational numbers, we can choose with all rational and such that

for all with . By our choice of a sequence of realized random networks above, we have

So for sufficiently large,

By the triangle inequality, for sufficiently large whenever with . We will show that this implies that the same holds at the maximal equilibrium.

The profile need not be an equilibrium, but we have shown that whenever . Therefore, we can obtain an equilibrium from as follows. Set . Then, repeatedly define by beginning with and setting entries to if . Because is monotone increasing in (Lemma 5(i)), this process does not decrease any firms’ values at any point. So for all we have whenever .

This process converges in at most steps. By construction the limit must satisfy whenever . Since we noted in the previous paragraph that whenever , the putative solvency vector is feasible and therefore is indeed an equilibrium.

For sufficiently large whenever with . Since , for sufficiently large we must have for all in an open neighborhood of . But any firm that is solvent under the equilibrium is also solvent under the maximal equilibrium. So this contradicts the definition of . We conclude that for all , completing step 1.

Step 2: almost surely for all .

Suppose for the sake of contradiction that for some . Passing to a subsequence, we can assume that converges to some for each and that .

We write for the solvency vector at the maximal equilibrium for the realized random network with agents. By the definition of , each firm has value . The putative solvency vector , so by monotonicity (Lemma 5(i)) we have .

Note that the values are all rational with denominators at most , so . By our choice of a sequence of realized random networks above, we have

and therefore

for all . Since for all , by Lemma 5(ii) we have for all . Applying Lemma 5(i) again, we have whenever satisfies .

We claim that this implies that the maximal equilibrium value for all . Since we assumed at the start of Step 2 that there exists a such that this will give a contradiction.

The claim is a special case of the following lemma:

Lemma 7.

Let be a putative solvency function. If whenever , then each firm that is solvent under is solvent under the maximal equilibrium.

Proof.

To prove the lemma, recall the order-preserving operator from the proof of Proposition 1. Let be the set of measurable, bounded functions with . Because whenever satisfies , for any we have whenever satisfies .

Suppose that . Then for ,

This shows that , so maps the set to itself. Applying Tarksi’s fixed point theorem as in the proof of Proposition 1, we conclude there is an equilibrium in . The equilibrium values satisfy whenever . So the maximal equilibrium also satisfies whenever . ∎

We have established a contradiction, so we can conclude that for all .

Step 3: for all .

Fix . We have shown that and . So we can choose such that all firms in that are insolvent have and all firms that are solvent have . Equivalently, all firms with are solvent and all firms with are insolvent. So for all . Since , this implies that . ∎

Proof of Proposition 3.

We begin with a lemma, which states that any firm receiving cash under an optimal infusion must have value after the infusion.

Lemma 8.

If is an optimal cash infusion, then, .

Proof.

Suppose for a positive measure of firms with . Choose a positive measure subset of these firms contained in some block, , say. Consider any cash infusion obtained by decreasing by for all firms in and increasing for other firms in block by a total of .

Let be the solvency function corresponding to the maximal equilibrium after cash infusion . We write for the values under putative solvency function after cash infusion . Applying equation (23) with endowments , we find that for any

The second equality holds because for all . By the construction of , we have

whenever . So whenever . By Lemma 7, this implies that any firm that is solvent at the maximal equilibrium after cash infusion is solvent at the maximal equilibrium after cash infusion . We have shown that weakly increases the measure of firms solvent at the maximal equilibrium relative to .

It remains to obtain a strict improvement. By assumption, the support of is interior in block . The construction of thus far did not depend on how we reallocated the amount within block . We can do so to obtain a positive measure of firms such that

but . Then, Lemma 7 similarly shows these firms are solvent at the maximal equilibrium under . So, the set of firms solvent after is a strict subset of the set of firms solvent after . This contradicts the optimality of the original cash infusion .

So we cannot have for a positive measure of firms with . Essentially the same argument shows that we cannot have a positive measure of firms with and , as we can reduce the cash infusion for those firms from to and increase the cash infusion to other firms in the same block. So we must have whenever . ∎

Within each block , the value of each firm with after the cash infusion is equal to for some constant depending on the block . Lemma 8 implies that is equal to some value, which we call , for all firms in block with .