Lookback Prophet Inequalities

Abstract

Prophet inequalities are fundamental optimal stopping problems, where a decision-maker observes sequentially items with values sampled independently from known distributions, and must decide at each new observation to either stop and gain the current value or reject it irrevocably and move to the next step. This model is often too pessimistic and does not adequately represent real-world online selection processes. Potentially, rejected items can be revisited and a fraction of their value can be recovered. To analyze this problem, we consider general decay functions , quantifying the value to be recovered from a rejected item, depending on how far it has been observed in the past. We analyze how lookback improves, or not, the competitive ratio in prophet inequalities in different order models. We show that, under mild monotonicity assumptions on the decay functions, the problem can be reduced to the case where all the decay functions are equal to the same function , where . Consequently, we focus on this setting and refine the analyses of the competitive ratios, with upper and lower bounds expressed as increasing functions of .

1 Introduction

Optimal stopping problems constitute a classical paradigm of decision-making under uncertainty (Dynkin, 1963) Typically, in online algorithms, these problems are formalized as variations of the secretary problem (Lindley, 1961) or the prophet inequality (Krengel and Sucheston, 1977). In the context of the prophet inequality, the decision-maker observes a finite sequence of items, each having a value drawn independently from a known probability distribution. Upon encountering a new item, the decision-maker faces the choice of either accepting it and concluding the selection process or irreversibly rejecting it, with the objective of maximizing the value of the selected item. However, while the prophet inequality problem is already used in scenarios such as posted-price mechanism design (Hajiaghayi et al., 2007) or online auctions (Syrgkanis, 2017), it might present a pessimistic model of real-world online selection problems. Indeed, it is in general possible in practice to revisit previously rejected items and potentially recover them or at least recover a fraction of their value.

Consider for instance an individual navigating a city in search of a restaurant. When encountering one, they have the choice to stop and dine at this place, continue their search, or revisit a previously passed option, incurring a utility cost that is proportional to the distance of backtracking. In another example drawn from the real estate market, homeowners receive offers from potential buyers. The decision to accept or reject an offer can be revisited later, although buyer interest may have changed, resulting in a potentially lower offer or even a lack of interest. Lastly, in the financial domain, an agent may choose to sell an asset at its current price or opt for a lookback put option, allowing them to sell at the asset’s highest price over a specified future period. To make a meaningful comparison between the two, one must account for factors such as discounting (time value of money) and the cost of the option.

1.1 Formal problem and notation

To encompass diverse scenarios, we propose a general way to quantify the cost incurred by the decision-maker for retrieving a previously rejected value.

Definition 1.1 (Decay functions).

Let be a sequence of non-negative functions defined on . It is a sequence of decay functions if

-

(i)

for all ,

-

(ii)

the sequence is non-increasing for all ,

-

(iii)

the function is non-decreasing for all .

In the context of decay functions , if a value is rejected, the algorithm can recover after subsequent steps. The three conditions defining decay functions serve as fundamental prerequisites for the problem. The first and second conditions ensure that the recoverable value of a rejected item can only diminish over time, while the final condition implies that an increase in the observed value corresponds to an increase in the potential recovered value. Although the non-negativity of the decay functions is non-essential, we retain it for convenience, as we can easily revert to this assumption by considering that the algorithm has a reward of zero by not selecting any item.

The motivating examples that we introduced can be modeled respectively with decay functions of the form where is a non-decreasing positive sequence, with and a non-increasing sequence of probabilities, and with . In one of these examples (housing market), the natural model is to use random decay functions: the buyer makes the same offer if they are still interested, and offers otherwise. Definition 1.1 can be easily extended to consider this case. However, to enhance the clarity of the presentation, we only discuss the deterministic case in the rest of the paper. In Appendix D, we explain how all the proofs and theorems can be generalized to that case.

The -prophet inequality

For any decay functions , we define the -prophet inequality problem, where the decision maker, knowing , observes sequentially the values , with drawn from a known distribution for all . If they decide to stop at some step , then instead of gaining as in the classical prophet inequality, they can choose to select the current item and have its full value, or select any item with among the rejected ones but only recover a fraction of its value. Therefore, if an algorithm ALG stops at step its reward is

with the convention . If the algorithm does not stop at any step before , then its reward is , which corresponds to .

Remark 1.1.

As in the standard prophet inequality, an algorithm is defined by its stopping time, i.e., the rule set to decide whether to stop or not. Hence, if and are two different sequences of decay functions, any algorithm for the -prophet inequality, although its stopping time might depend on the particular sequence of functions , is also an algorithm for the -prophet inequality. Consider for example an algorithm ALG with stopping time that depends on . Its reward in the -prophet inequality is .

Observation order

Several variants of the prophet inequality problem have been studied, depending on the order of observations. The standard model is the adversarial (or fixed) order: The instance of the distributions is chosen by an adversary, and the algorithm observes the samples in this order (Krengel and Sucheston, 1977, 1978). In the random order model, the adversary can again choose the distributions, but the algorithm observes the samples in a uniformly random order. Another setting in which the observation order is no longer important is the IID model (Hill and Kertz, 1982; Correa et al., 2021b), where all the values are sampled independently from the same distribution . The -prophet inequality is well-defined in each of these different order models: if the items are observed in the order with a permutation of , then the reward of the algorithm is . In this paper, we study the -prophet inequality in the three models we presented, providing lower and upper bounds in each of them.

Competitive ratio

In the -prophet inequality, an input instance is a finite sequence of probability distributions . Thus, for any instance , we denote by the expected reward of ALG given as input, and we denote by the expected maximum of independent random variables , where . With these notations, we define the competitive ratio, which will be used to measure the quality of the algorithms.

Definition 1.2 (Competitive ratio).

Let be a sequence of decay functions and ALG an algorithm. We define the competitive ratio of ALG by

with the infimum taken over the tuples of all sizes of non-negative distributions with finite expectation.

An algorithm is said to be -competitive if its competitive ratio is at least , which means that for any possible instance , the algorithm guarantees a reward of at least . The notion of competitive ratio is used more broadly in competitive analysis as a metric to evaluate online algorithms (Borodin and El-Yaniv, 2005), as it lower bounds their performance even in worst-case scenarios, when the input instance is chosen adversarially.

1.2 Contributions

It is trivial that non-zero decay functions guarantee a better reward compared to the classical prophet inequality. However, in general, this is not sufficient to conclude that the standard upper bounds or the competitive ratio of a given algorithm can be improved. Hence, a first key question is: what condition on is necessary to surpass the conventional upper bounds of the classical prophet inequality? Surprisingly, the answer hinges solely on the constant , defined as follows,

| (1) |

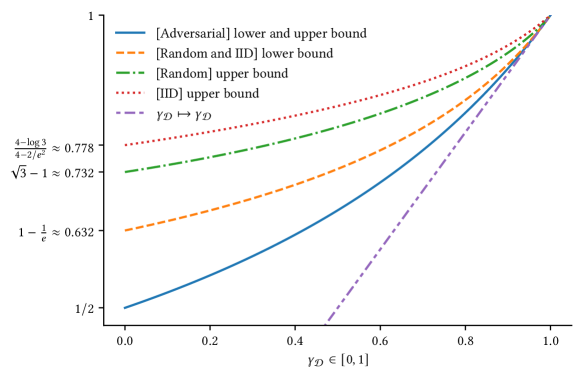

In the adversarial order model, we demonstrate that the optimal competitive ratio achievable in the -prophet inequality is determined by the parameter alone. Additionally, in both the random order and IID models, we demonstrate the essential requirement of for breaking the upper bounds of the classical prophet inequality. In particular, this implies that no improvement can be made with decay functions of the form with , or with . Subsequently, we develop algorithms and provide upper bounds in the -prophet inequality, uniquely dependent on the parameter . We illustrate them in Figure 1, comparing them with the identity function , which is a trivial lower bound.

1.3 Related work

Prophet inequalities

The first prophet inequality was proven by Krengel and Sucheston (Krengel and Sucheston, 1977, 1978) in the setting where the items are observed in a fixed order, demonstrating that the dynamic programming algorithm has a competitive ratio of , which is the best possible. It was shown later that the same guarantee can be obtained with simpler algorithms (Samuel-Cahn, 1984; Kleinberg and Weinberg, 2012), accepting the first value above a carefully chosen threshold. For a more comprehensive and historical overview, we refer the interested reader to surveys on the problem such as (Lucier, 2017; Correa et al., 2019). Prophet inequalities have immediate applications in mechanism design (Hajiaghayi et al., 2007; Deng et al., 2022; Psomas et al., 2022; Makur et al., 2024), auctions (Syrgkanis, 2017; Dütting et al., 2020), resource management (Sinclair et al., 2023), and online matching (Cohen et al., 2019; Ezra et al., 2020; Jiang et al., 2021; Papadimitriou et al., 2021; Brubach et al., 2021). Many variants and related problems have been studied, including, for example, the matroid prophet inequality (Kleinberg and Weinberg, 2012; Feldman et al., 2016), prophet inequality with advice (Diakonikolas et al., 2021), and variants with fairness considerations (Correa et al., 2021a; Arsenis and Kleinberg, 2022).

Random order and IID models

Esfandiari et al. (2017) introduced the prophet secretary problem, where items are observed in a uniformly random order, and they proved a -competitive algorithm. Correa et al. (2021c) showed later a competitive ratio of , which currently stands as the best-known solution for the problem. They also proved an upper bound of , which was improved to in (Bubna and Chiplunkar, 2023). Addressing the gap between the lower and upper bound remains an engaging and actively pursued open question. On the other hand, the study of prophet inequalities with IID random variables dates back to papers such as (Hill and Kertz, 1982; Kertz, 1986), demonstrating guarantees on the dynamic programming algorithm. The problem was completely solved in (Correa et al., 2021b), where the authors show that the competitive ratio of the dynamic programming algorithm is , thus it constitutes an upper bound on the competitive ratio of any algorithm, and they give a simpler adaptive threshold algorithm matching it. Another setting that we do not study in this paper, is the order selection model, where the decision-maker can choose the order in which the items are observed, knowing their distributions (Chawla et al., 2010; Beyhaghi et al., 2021; Peng and Tang, 2022).

Beyond the worst-case

In recent years, there has been increasing interest in exploring ways to exceed the worst-case upper bounds of online algorithms by providing the decision-maker with additional capabilities. A notable research avenue is learning-augmented algorithms (Lykouris and Vassilvtiskii, 2018), which equip the decision-maker with predictions about unknown variables of the problem. Multiple problems have been studied in this framework, such as scheduling (Purohit et al., 2018; Lassota et al., 2023; Merlis et al., 2023; Benomar and Perchet, 2024b), matching (Antoniadis et al., 2020; Dinitz et al., 2021; Chen et al., 2022), caching (Antoniadis et al., 2023; Chlkedowski et al., 2021; Christianson et al., 2023), and in particular, online selection problems (Dütting et al., 2021; Sun et al., 2021; Benomar and Perchet, 2024a; Diakonikolas et al., 2021). More related to our setting, the ability to revisit items in online selection has been studied in problems such as the multiple-choice prophet inequality, where the algorithm can select up to items and its reward is the maximum selected value (Assaf and Samuel-Cahn, 2000). This allows for revisiting up to items, chosen during the execution, for final acceptance or rejection decisions. Similarly, in Pandora’s box problem (Weitzman, 1978; Kleinberg et al., 2016) and its variants (Esfandiari et al., 2019; Gergatsouli and Tzamos, 2022; Atsidakou et al., 2024; Gergatsouli and Tzamos, 2024; Berger et al., 2024), the decision maker decides the observation order of the items, but a cost is paid for observing each value , with the gain being the maximum observed value minus the total opening costs. A very recent work investigates a scenario closely related to the lookback prophet inequality (Ekbatani et al., 2024) where, upon selecting a candidate , the decision-maker has the option to discard it and choose a new value at any later step , at a buyback cost of , where . The authors present an optimal algorithm for the case when , although the problem remains open for .

2 From -prophet to the -prophet inequality

Let us consider a sequence of decay functions. By Definition 1.1, for any the sequence converges, since it is non-increasing and non-negative. Hence, there exists a mapping such that for any , . Furthermore, we can easily verify that is non-decreasing and satisfies for all .

Thanks to these properties, we obtain that also satisfies Definition 1.1, and is hence a valid sequence of decay functions. We thus refer to the corresponding problem as the -prophet inequality. Since for any , it is straightforward that the stopping problem with the decay functions would be less favorable to the decision-maker. More precisely, for any random variables , observation order , and algorithm ALG with stopping time , it holds that

which corresponds to the output of ALG (with the same decision rule) when all the decay functions are equal to . Therefore, any guarantees established for algorithms in the -prophet inequality naturally extend to the -prophet inequality. However, it remains uncertain whether the -prophet inequality can yield improved competitive ratios compared to the -prophet inequality. In the following, we prove that this is not the case, for all the order models presented in Section 1.

Theorem 2.1.

Let be the pointwise limit of the sequence of decay functions . Then for any instance of non-negative distributions, in the adversarial order and the random order models it holds that

| (2) |

where the supremum is taken over all the online algorithms A. In the IID model, the same inequality holds with an additional term, which depends only on the size of the instance.

The main implication of Theorem 2.1 is the following corollary.

Corollary 2.1.1.

In the adversarial order and the random order models, if is an optimal algorithm for the -prophet inequality, i.e. with maximal competitive ratio, then is also optimal for the -prophet inequality. Moreover, it holds that

A direct consequence of this result is that, in the adversarial and the random order models, the asymptotic decay entirely determines the competitive ratio that is achievable and the upper bounds for the -prophet inequality. Therefore, we can restrict our analysis to algorithms designed for the problem with identical decay function. In the IID model, the same conclusion holds if the worst-case instances are arbitrarily large, making the additional term vanish. This is the case in particular in the classical IID prophet inequality (Hill and Kertz, 1982).

2.1 Sketch of the proof of Theorem 2.1

While we use different techniques for each order model considered, all the proofs share the same underlying idea. Given any instance of non-negative distributions, we build an alternative instance such that the reward of any algorithm on with decay functions it at most its reward on with decay functions all equal to . To do this, we essentially introduce an arbitrarily large number of zero values between two successive observations drawn from distributions belonging to . Hence, under the algorithm cannot recover much more than a fraction for any past observation collected from .

In the adversarial case, implementing this idea is straightforward, since nature can build by directly inserting zeros between each pair of consecutive values, and the result is obtained by making arbitrarily large. For the random order model, we use the same instance , but extra steps are needed to prove that the number of steps between two non-zero values is very large with high probability.

Moving to the IID model, an instance is defined by a pair , where is a non-negative distribution, and is the size of the instance. In this scenario, we consider an instance consisting of IID random variables , each sampled from with probability , and equal to zero with the remaining probability. We again achieve the desired result by letting be arbitrarily large compared to . However, the number of variables sampled from is not fixed; it follows a Binomial distribution with parameters . We control this variability by using concentration inequalities, which causes the additional term .

3 From -prophet to the -prophet inequality

As discussed in Section 2, Theorem 2.1 implies that, for either establishing upper bounds or guarantees on the competitive ratios of algorithms, it is sufficient to study the -prophet inequality, where all the decay functions are equal to . The remaining question is then to determine which functions allow to improve upon the upper bounds of the classical prophet inequality. Before tackling this question, let us make some observations regarding algorithms in the -prophet inequality.

In the -prophet inequality, it is always possible to have a reward of by rejecting all the items and then selecting the maximum by the end. Thus, there is no advantage in stopping at step where . An algorithm respecting this decision rule is called rational.

Lemma 3.1.

For any rational algorithm ALG in the -prophet inequality, if we denote its stopping time, then for any instance and for all we have

Moreover, the optimal dynamic programming algorithm in the -prophet inequality is rational.

The best competitive ratio in the -prophet inequality is achieved, possibly among others, by the optimal dynamic programming algorithm, which is a rational algorithm by the previous Lemma. Hence, by the previous Lemma, it suffices to prove it on rational algorithms. We use this observation to prove the next propositions.

Proposition 3.2.

In the -prophet inequality, if , then it holds, in any order model, that

| (3) |

where the supremum is taken over all the online algorithms A.

Proposition 3.2 implies that if , then, in any order model, any upper bound on the competitive ratios of all algorithms in the classical prophet inequality is also an upper bound on the competitive ratios of all algorithm in the -prophet inequality. Consequently, for surpassing the upper bounds of the classical prophet inequality, it is necessary to have, for some , that for all . Furthermore, the next Proposition allows giving upper bounds in the -prophet inequality that depend only on .

Proposition 3.3.

Let , and . Consider an instance of distributions with support in , then in any order model and for any algorithm ALG we have that

where is to the reward of A if all the decay functions were equal to .

The core idea for proving this proposition is that rescaling an instance, i.e. considering instead of , has no impact in the classical prophet inequality. However, in the -prophet inequality, rescaling can be exploited to adjust the ratio . By considering instances with random variables taking values in almost surely, where , a reasonable algorithm facing such an instance would never reject the value . Consequently, the value it recovers from rejected items is either or . Rescaling this instance by a factor and taking the ratio to the expected maximum, the ratio appears, with a free parameter that can be chosen to satisfy .

As a consequence, if , then any upper bound obtained in the -prophet inequality (when the decay functions are all equal to ) using instances of random variables satisfying a.s. for all , is also an upper bound in the -prophet inequality.

Implication

Let us consider any sequence of decay functions, and define

For any and it holds that , therefore, any guarantees on the competitive ratio of an algorithm in the -prophet inequality are valid in the -prophet inequality, under any order model. Furthermore, combining Theorem 2.1 and Proposition 3.3, we obtain that for any instance of random variables taking values in a set it holds that

with an additional term of order in the IID model. In the particular case where , Proposition 3.3 with Theorem 2.1 give a stronger result, showing that no algorithm can surpass the upper bounds of the classical prophet inequality. This is true also for the IID model since the instances used to prove the tight upper bound of are of arbitrarily large size (Hill and Kertz, 1982).

Therefore, by studying the -prophet inequality for , we can prove upper bounds and lower bounds on the -prophet inequality for any sequence of decay functions.

4 The -prophet inequality

We study in this section the -prophet inequality, where all the decay functions are equal to , for some . For any algorithm ALG with stopping time and random variables , if the observation order is , we use the notation

and we denote by the competitive ratio of ALG in this setting. In the following, we provide theoretical guarantees for the -prophet inequality. For each observation order, we first derive upper bounds on the competitive ratio of any algorithm, depending on , using only hard instances satisfying the condition in Proposition 3.3. This would guarantee that the upper bounds extend to the -prophet inequality if . We also design single-threshold algorithms with well-chosen thresholds depending on and the distributions, with competitive ratios improving with . A crucial property of single-threshold algorithms, which we use to estimate their competitive ratios, is that their reward satisfies

| (4) |

The additional term appearing due to depends only on , which is the reward of the prophet against whom we compete. This property is not satisfied by more general class of algorithms such as multiple-threshold algorithms, where each observation is compared with a threshold .

Remark 4.1.

We only consider instances with continuous distributions in the proofs of lower bounds. The thresholds considered are such that , with depending on , the order model and the size of the instance . Such a threshold is always guaranteed to exist when the distributions are continuous. However, as in the prophet inequality, the algorithms can be easily adapted to non-continuous distributions by allowing stochastic tie-breaking. A detailed strategy for doing this can be found for example in (Correa et al., 2021c).

Before delving into the study of the different models, we provide generic lower and upper bounds, which depend solely on the bounds of the classical prophet inequality and .

Proposition 4.2.

In any order model, if is a lower bound in the classical prophet inequality, and an upper bound, then, in the -prophet inequality

-

(i)

there exists a trivial algorithm with a competitive ratio of at least ,

-

(ii)

the competitive ratio of any algorithm is at most .

4.1 Adversarial order

We first consider the adversarial order model, and prove the upper bound of . Then, we provide a single-threshold algorithm with a competitive ratio matching this upper bound, hence fully solving the -prophet inequality in this adversarial order model.

Theorem 4.3.

In the adversarial order model, the competitive ratio of any algorithm for the -prophet inequality is at most . Furthermore, there exists a single threshold algorithm with a competitive ratio of at least : given any instance , this result is achieved with the threshold satisfying .

4.2 Random order

Consider now that the items are observed in a uniformly random order , and . As for the adversarial model, we first prove an upper bound on the competitive ratio as a function of , and then prove a lower bound for a single-threshold algorithm. However, for this model, there is a gap between the two bounds, as illustrated in Figure 1.

We first prove an upper bound that depends on , matching the upper bound of Correa et al. (2021c) when and equal to when . Our single-threshold algorithm has a competitive ratio of at least when , which is the best competitive ratio of a single threshold algorithm in the prophet inequality (Esfandiari et al., 2017; Correa et al., 2021c), and equal to for .

Theorem 4.4.

The competitive ratio of any algorithm ALG in the -prophet inequality with random order satisfies

Furthermore, denoting by is the unique solution to the equation , the single-threshold algorithm with satisfies

While the equation defining cannot be solved analytically, the solution can easily be computed numerically for any . Before moving to the IID case, we propose in the following a more explicit lower bound derived from Theorem 4.4.

Corollary 4.4.1.

In the random order model, the single threshold algorithm with a threshold satisfying has a competitive ratio of at least .

4.3 IID Random Variables

In the classical IID prophet inequality, Hill and Kertz (1982) showed that the competitive ratio of any algorithm is at most . The proof of this upper bound is hard to generalize for the IID -prophet inequality. As an alternative, we prove a weaker upper bound, which equals for and for , and the prove relies on instances of arbitrarily large size satisfying the condition of Proposition 3.3, hence the lower bound can be extended to the -prophet inequality.

Subsequently, we present a single-threshold algorithm with the same competitive ratio as the random order algorithm. However, the proof is different, leveraging the fact that the variables are identically distributed. More precisely, we introduce a single-threshold algorithm with guarantees that depend on the size of the instance, then we show that its competitive ratio is at least that of the algorithm presented in Theorem 4.4, with equality when approaches infinity.

Although it might look surprising that the obtained competitive ratio in the IID model is not better than that of the random-order model, the same behavior occurs in the classical prophet inequality. Indeed, Li et al. (2022) established that no single-threshold algorithm can achieve a competitive ratio better than in the standard prophet inequality with IID random variables, which is also the best possible with a single-threshold algorithm in the random order. However, considering larger classes of algorithms, the competitive ratios achieved in the IID model are better than those of the random order model.

We describe the algorithm and give a first lower bound on its reward depending on the size of the instance in the following lemma.

Lemma 4.5.

Let be the unique solution of the equation , then for any IID instance , the algorithm with threshold satisfying has a reward of at least

We can prove that the reward presented in the Lemma above is strictly better than that of the reward in the case of the random order model. However, both are asymptotically equal as we show in the following theorem, thus yielding the same theorem.

Theorem 4.6.

The competitive ratio of any algorithm in the IID -prophet inequality is at most

In particular, is increasing, and . Furthermore, there exists a single-threshold algorithm satisfying

where is defined in Theorem 4.4.

4.4 Extension to the -prophet inequality

As detailed in the previous sections, all the competitive ratios proved in the case of the -prophet inequality remain true in the - and the -prophet inequality for .

Moreover, Proposition 3.2 shows that upper bounds that are demonstrated through instances of random variables taking values in some set a.s. remain true in the -prophet inequality and consequently also in the -prophet inequality by Theorem 2.1. Since we restricted ourselves to using such instances for proving upper bounds in the -prophet inequality, they all remain also true in the -prophet inequality for .

5 Conclusion

In this paper, we addressed the -prophet inequality problem, which models a very broad spectrum of online selection scenarios, accommodating various observation order models and allowing to revisit rejected candidates at a cost. The problem extends the classic prophet inequality, corresponding to the special case where all decay functions are zero. The main result of the paper is a reduction from the general -prophet inequality to the -prophet inequality, where all the decay functions equal to for some constant . Subsequently, we provide algorithms and upper bounds for the -prophet inequality, which remain valid, by the previous reduction, in the -prophet inequality. Notably, the proved upper and lower bounds match each other for the adversarial order model, hence completely solving the problem. Our analysis paves the way for more practical applications of prophet inequalities, and advances efforts towards closing the gap between theory and practice in online selection problems.

Limitations and future work

Better upper bounds in the -prophet inequality

Proposition 3.3 establishes that upper bounds proved in the -prophet inequality using instances of random variables with support in some set remain true in the -prophet inequality, and hence in the -prophet inequality, by Theorem 2.1, for . This is enough to establish a tight upper bound in the adversarial order model, but not in the random order and IID models. An interesting question to explore is if more general upper bounds can be extended, or not, from the - to the -prophet inequality.

Algorithms for the -prophet inequality

As explained in Section 4, our analysis of the competitive ratio of single-threshold algorithms relies on the identity (4), which is not satisfied for instance by multiple-threshold algorithms. In the adversarial order model, we proved that the optimal competitive ratio can be achieved with a single-threshold algorithm. However, this is not the case in the random order or IID models. An open research avenue is to study other classes of algorithms in the -prophet inequality.

References

- Antoniadis et al. [2020] Antonios Antoniadis, Themis Gouleakis, Pieter Kleer, and Pavel Kolev. Secretary and online matching problems with machine learned advice. Advances in Neural Information Processing Systems, 33:7933–7944, 2020.

- Antoniadis et al. [2023] Antonios Antoniadis, Joan Boyar, Marek Eliás, Lene Monrad Favrholdt, Ruben Hoeksma, Kim S Larsen, Adam Polak, and Bertrand Simon. Paging with succinct predictions. In International Conference on Machine Learning, pages 952–968. PMLR, 2023.

- Arsenis and Kleinberg [2022] Makis Arsenis and Robert Kleinberg. Individual fairness in prophet inequalities. In Proceedings of the 23rd ACM Conference on Economics and Computation, pages 245–245, 2022.

- Assaf and Samuel-Cahn [2000] David Assaf and Ester Samuel-Cahn. Simple ratio prophet inequalities for a mortal with multiple choices. Journal of applied probability, 37(4):1084–1091, 2000.

- Atsidakou et al. [2024] Alexia Atsidakou, Constantine Caramanis, Evangelia Gergatsouli, Orestis Papadigenopoulos, and Christos Tzamos. Contextual pandora’s box. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 38, pages 10944–10952, 2024.

- Benomar and Perchet [2024a] Ziyad Benomar and Vianney Perchet. Advice querying under budget constraint for online algorithms. Advances in Neural Information Processing Systems, 36, 2024a.

- Benomar and Perchet [2024b] Ziyad Benomar and Vianney Perchet. Non-clairvoyant scheduling with partial predictions. arXiv preprint arXiv:2405.01013, 2024b.

- Berger et al. [2024] Ben Berger, Tomer Ezra, Michal Feldman, and Federico Fusco. Pandora’s problem with deadlines. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 38, pages 20337–20343, 2024.

- Beyhaghi et al. [2021] Hedyeh Beyhaghi, Negin Golrezaei, Renato Paes Leme, Martin Pál, and Balasubramanian Sivan. Improved revenue bounds for posted-price and second-price mechanisms. Operations Research, 69(6):1805–1822, 2021.

- Borodin and El-Yaniv [2005] Allan Borodin and Ran El-Yaniv. Online computation and competitive analysis. cambridge university press, 2005.

- Brubach et al. [2021] Brian Brubach, Nathaniel Grammel, Will Ma, and Aravind Srinivasan. Improved guarantees for offline stochastic matching via new ordered contention resolution schemes. Advances in Neural Information Processing Systems, 34:27184–27195, 2021.

- Bubna and Chiplunkar [2023] Archit Bubna and Ashish Chiplunkar. Prophet inequality: Order selection beats random order. In Proceedings of the 24th ACM Conference on Economics and Computation, pages 302–336, 2023.

- Chawla et al. [2010] Shuchi Chawla, Jason D Hartline, David L Malec, and Balasubramanian Sivan. Multi-parameter mechanism design and sequential posted pricing. In Proceedings of the forty-second ACM symposium on Theory of computing, pages 311–320, 2010.

- Chen et al. [2022] Justin Chen, Sandeep Silwal, Ali Vakilian, and Fred Zhang. Faster fundamental graph algorithms via learned predictions. In International Conference on Machine Learning, pages 3583–3602. PMLR, 2022.

- Chlkedowski et al. [2021] Jakub Chlkedowski, Adam Polak, Bartosz Szabucki, and Konrad Tomasz .Zolna. Robust learning-augmented caching: An experimental study. In International Conference on Machine Learning, pages 1920–1930. PMLR, 2021.

- Christianson et al. [2023] Nicolas Christianson, Junxuan Shen, and Adam Wierman. Optimal robustness-consistency tradeoffs for learning-augmented metrical task systems. In International Conference on Artificial Intelligence and Statistics, pages 9377–9399. PMLR, 2023.

- Cohen et al. [2019] Alon Cohen, Avinatan Hassidim, Haim Kaplan, Yishay Mansour, and Shay Moran. Learning to screen. Advances in Neural Information Processing Systems, 32, 2019.

- Correa et al. [2019] Jose Correa, Patricio Foncea, Ruben Hoeksma, Tim Oosterwijk, and Tjark Vredeveld. Recent developments in prophet inequalities. ACM SIGecom Exchanges, 17(1):61–70, 2019.

- Correa et al. [2021a] Jose Correa, Andres Cristi, Paul Duetting, and Ashkan Norouzi-Fard. Fairness and bias in online selection. In International conference on machine learning, pages 2112–2121. PMLR, 2021a.

- Correa et al. [2021b] José Correa, Patricio Foncea, Ruben Hoeksma, Tim Oosterwijk, and Tjark Vredeveld. Posted price mechanisms and optimal threshold strategies for random arrivals. Mathematics of operations research, 46(4):1452–1478, 2021b.

- Correa et al. [2021c] Jose Correa, Raimundo Saona, and Bruno Ziliotto. Prophet secretary through blind strategies. Mathematical Programming, 190(1-2):483–521, 2021c.

- Deng et al. [2022] Yuan Deng, Vahab Mirrokni, and Hanrui Zhang. Posted pricing and dynamic prior-independent mechanisms with value maximizers. Advances in Neural Information Processing Systems, 35:24158–24169, 2022.

- Diakonikolas et al. [2021] Ilias Diakonikolas, Vasilis Kontonis, Christos Tzamos, Ali Vakilian, and Nikos Zarifis. Learning online algorithms with distributional advice. In International Conference on Machine Learning, pages 2687–2696. PMLR, 2021.

- Dinitz et al. [2021] Michael Dinitz, Sungjin Im, Thomas Lavastida, Benjamin Moseley, and Sergei Vassilvitskii. Faster matchings via learned duals. Advances in neural information processing systems, 34:10393–10406, 2021.

- Dütting et al. [2020] Paul Dütting, Thomas Kesselheim, and Brendan Lucier. An o (log log m) prophet inequality for subadditive combinatorial auctions. ACM SIGecom Exchanges, 18(2):32–37, 2020.

- Dütting et al. [2021] Paul Dütting, Silvio Lattanzi, Renato Paes Leme, and Sergei Vassilvitskii. Secretaries with advice. In Proceedings of the 22nd ACM Conference on Economics and Computation, pages 409–429, 2021.

- Dynkin [1963] Evgenii Borisovich Dynkin. The optimum choice of the instant for stopping a markov process. Soviet Mathematics, 4:627–629, 1963.

- Ekbatani et al. [2024] Farbod Ekbatani, Rad Niazadeh, Pranav Nuti, and Jan Vondrák. Prophet inequalities with cancellation costs. arXiv preprint arXiv:2404.00527, 2024.

- Esfandiari et al. [2017] Hossein Esfandiari, MohammadTaghi Hajiaghayi, Vahid Liaghat, and Morteza Monemizadeh. Prophet secretary. SIAM Journal on Discrete Mathematics, 31(3):1685–1701, 2017.

- Esfandiari et al. [2019] Hossein Esfandiari, MohammadTaghi HajiAghayi, Brendan Lucier, and Michael Mitzenmacher. Online pandora’s boxes and bandits. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 1885–1892, 2019.

- Ezra et al. [2020] Tomer Ezra, Michal Feldman, Nick Gravin, and Zhihao Gavin Tang. Online stochastic max-weight matching: prophet inequality for vertex and edge arrival models. In Proceedings of the 21st ACM Conference on Economics and Computation, pages 769–787, 2020.

- Feldman et al. [2016] Moran Feldman, Ola Svensson, and Rico Zenklusen. Online contention resolution schemes. In Proceedings of the twenty-seventh annual ACM-SIAM symposium on Discrete algorithms, pages 1014–1033. SIAM, 2016.

- Gergatsouli and Tzamos [2022] Evangelia Gergatsouli and Christos Tzamos. Online learning for min sum set cover and pandora’s box. In International Conference on Machine Learning, pages 7382–7403. PMLR, 2022.

- Gergatsouli and Tzamos [2024] Evangelia Gergatsouli and Christos Tzamos. Weitzman’s rule for pandora’s box with correlations. Advances in Neural Information Processing Systems, 36, 2024.

- Hajiaghayi et al. [2007] Mohammad Taghi Hajiaghayi, Robert Kleinberg, and Tuomas Sandholm. Automated online mechanism design and prophet inequalities. In AAAI, volume 7, pages 58–65, 2007.

- Hill and Kertz [1982] Theodore P Hill and Robert P Kertz. Comparisons of stop rule and supremum expectations of iid random variables. The Annals of Probability, pages 336–345, 1982.

- Jiang et al. [2021] Zhihao Jiang, Pinyan Lu, Zhihao Gavin Tang, and Yuhao Zhang. Online selection problems against constrained adversary. In International Conference on Machine Learning, pages 5002–5012. PMLR, 2021.

- Kertz [1986] Robert P Kertz. Stop rule and supremum expectations of iid random variables: a complete comparison by conjugate duality. Journal of multivariate analysis, 19(1):88–112, 1986.

- Kleinberg and Weinberg [2012] Robert Kleinberg and Seth Matthew Weinberg. Matroid prophet inequalities. In Proceedings of the forty-fourth annual ACM symposium on Theory of computing, pages 123–136, 2012.

- Kleinberg et al. [2016] Robert Kleinberg, Bo Waggoner, and E Glen Weyl. Descending price optimally coordinates search. arXiv preprint arXiv:1603.07682, 2016.

- Krengel and Sucheston [1977] Ulrich Krengel and Louis Sucheston. Semiamarts and finite values. 1977.

- Krengel and Sucheston [1978] Ulrich Krengel and Louis Sucheston. On semiamarts, amarts, and processes with finite value. Probability on Banach spaces, 4:197–266, 1978.

- Lassota et al. [2023] Alexandra Anna Lassota, Alexander Lindermayr, Nicole Megow, and Jens Schlöter. Minimalistic predictions to schedule jobs with online precedence constraints. In International Conference on Machine Learning, pages 18563–18583. PMLR, 2023.

- Li et al. [2022] Bo Li, Xiaowei Wu, and Yutong Wu. Query efficient prophet inequality with unknown iid distributions. arXiv preprint arXiv:2205.05519, 2022.

- Lindley [1961] Denis V Lindley. Dynamic programming and decision theory. Journal of the Royal Statistical Society: Series C (Applied Statistics), 10(1):39–51, 1961.

- Lucier [2017] Brendan Lucier. An economic view of prophet inequalities. ACM SIGecom Exchanges, 16(1):24–47, 2017.

- Lykouris and Vassilvtiskii [2018] Thodoris Lykouris and Sergei Vassilvtiskii. Competitive caching with machine learned advice. In International Conference on Machine Learning, pages 3296–3305. PMLR, 2018.

- Makur et al. [2024] Anuran Makur, Marios Mertzanidis, Alexandros Psomas, and Athina Terzoglou. On the robustness of mechanism design under total variation distance. Advances in Neural Information Processing Systems, 36, 2024.

- Merlis et al. [2023] Nadav Merlis, Hugo Richard, Flore Sentenac, Corentin Odic, Mathieu Molina, and Vianney Perchet. On preemption and learning in stochastic scheduling. In International Conference on Machine Learning, pages 24478–24516. PMLR, 2023.

- Papadimitriou et al. [2021] Christos Papadimitriou, Tristan Pollner, Amin Saberi, and David Wajc. Online stochastic max-weight bipartite matching: Beyond prophet inequalities. In Proceedings of the 22nd ACM Conference on Economics and Computation, pages 763–764, 2021.

- Peng and Tang [2022] Bo Peng and Zhihao Gavin Tang. Order selection prophet inequality: From threshold optimization to arrival time design. In 2022 IEEE 63rd Annual Symposium on Foundations of Computer Science (FOCS), pages 171–178. IEEE, 2022.

- Psomas et al. [2022] Alexandros Psomas, Ariel Schvartzman Cohenca, and S Weinberg. On infinite separations between simple and optimal mechanisms. Advances in Neural Information Processing Systems, 35:4818–4829, 2022.

- Purohit et al. [2018] Manish Purohit, Zoya Svitkina, and Ravi Kumar. Improving online algorithms via ml predictions. Advances in Neural Information Processing Systems, 31, 2018.

- Samuel-Cahn [1984] Ester Samuel-Cahn. Comparison of threshold stop rules and maximum for independent nonnegative random variables. the Annals of Probability, pages 1213–1216, 1984.

- Sinclair et al. [2023] Sean R Sinclair, Felipe Vieira Frujeri, Ching-An Cheng, Luke Marshall, Hugo De Oliveira Barbalho, Jingling Li, Jennifer Neville, Ishai Menache, and Adith Swaminathan. Hindsight learning for mdps with exogenous inputs. In International Conference on Machine Learning, pages 31877–31914. PMLR, 2023.

- Sun et al. [2021] Bo Sun, Russell Lee, Mohammad Hajiesmaili, Adam Wierman, and Danny Tsang. Pareto-optimal learning-augmented algorithms for online conversion problems. Advances in Neural Information Processing Systems, 34:10339–10350, 2021.

- Syrgkanis [2017] Vasilis Syrgkanis. A sample complexity measure with applications to learning optimal auctions. Advances in Neural Information Processing Systems, 30, 2017.

- Weitzman [1978] Martin Weitzman. Optimal search for the best alternative, volume 78. Department of Energy, 1978.

Appendix A From -prophet to the -prophet inequality

In this section, we prove the reduction from the -prophet to the -prophet inequality problem in the adversarial and random order models, and the reduction up to an additional term in the IID model. First, we prove Corollary 2.1.1, which is the principal implication of Theorem 2.1.

A.1 Proof of Corollary 2.1.1

Proof.

Let us denote the algorithm taking optimal decisions for any instance in the -prophet inequality (obtained via dynamic programming). Then, by Theorem 2.1 we obtain for the adversarial and random order models that

| (5) |

Since for any algorithm, we deduce that (5) is an equality. If we consider now any algorithm that is optimal for the -prophet inequality, not necessarily , then Equation (5) provides

The previous inequality is again an equality, and it implies that is also optimal, in the sense of the competitive ratio, for the -prophet inequality, and

∎

A.2 Auxilary Lemma

The efficiency of the proof scheme introduced in Section 2.1 relies on the following key argument: if converges pointwise to , then for any algorithm A and any instance , the output of A when all the decay functions are equal to converges to its output when all the decay functions are equal to . If are the realizations of observed by A and if is the order in which they are observed, then denoting the stopping time of A we can write that

where is the set of all permutations of . The latter upper bound is independent of and A. We show in the following lemma that it converges to when .

Lemma A.1.

Let be the set of all permutations of . For any fixed instance , considering for all , define for all

If , then .

Proof.

Let us denote the respective probability density functions of . For any and , let us define for all the function by . is positive because . The sequence is non-increasing, converges to pointwise, and is dominated by , which is integrable with respect to the probability measure . Therefore, using the dominated convergence theorem, we deduce that . It follows that

∎

A.3 Proof of Theorem 2.1

Proof of Theorem 2.1.

We provide a separate proof for each of the adversarial order, random order and IID models.

Adversarial order

Let be any instance and for all . Consider the instance , where for any and a.s. for all . It is clear that no reasonable algorithm would stop at a zero value: if the current observation is it is preferable to wait for a non-null value, or it would have been preferable to stop at the previous non-null value. Hence, is a multiple of : for some . Given that for all and the sequence is non-increasing, we have that

where is defined in Lemma A.1. We can then use that the first right-hand term is the output of some other algorithm that would choose a stopping time when facing in the context of the -prophet inequality. More precisely, consider the algorithm which, given any instance , simulates the behavior of ALG facing the sequence , where at each step

-

•

if : ALG observes ,

-

•

otherwise, if for some : observes and ALG observes

-

•

if ALG stops on , then also stops, and its reward is .

stops at the same value as , their reward in the -prophet inequality is the same, and since this yields to

and taking the limit when gives the result, by making the second term vanish.

Random order

Let be an instance of distributions and for . Using the notation for the Dirac distribution in , we consider containing copies of so that the observations from this instance always contain at least null values. Let be a realization of this instance. For simplicity, say that for , and for .

We first show that when , since the observation order is drawn uniformly at random, the algorithm observes a large number of zeros between every two random variables drawn from . Let us denote by the uniformly random order in which the observations are received, i.e. the algorithms observes , and let be some positive integer, and be the increasing indices in which the variables are observed, i.e. and . Therefore, any observation outside is zero. Using the notation , we obtain that

Taking , we find that . Therefore, for any algorithm ALG, observing that the reward of is at most a.s., and by independence of and , we deduce that

| (6) |

Let us denote the stopping time of ALG and the last time when a variable was observed by ALG. The sequence of functions is non-increasing, hence

| (7) | ||||

| (8) | ||||

| (9) |

Equation (7) holds because the only non-zero values up to step are . Inequality (8) uses that the sequence is non-increasing, and (9) uses, in addition to that, the independence of and . We now argue that the term is the expected reward of an algorithm in the -inequality. Given that is a uniform random permutation of and by definition of , the application is a random permutation of . Therefore we consider the algorithm that receives as input the instance , then considers the array composed of values equal to and zero values, and a uniformly random permutation of , then simulates as follows: at each step

-

•

if , then ALG observes the value ,

-

•

if , then observes the next value , and ALG observes ,

-

•

when ALG decides to stop, also stops, and its reward is the current value .

With this construction, is indeed a realization of the instance , and stops on the last value sampled from observed by ALG. Therefore, denoting the stopping time of , and as defined in Lemma A.1, we have

Taking and substituting into Equation (6), then observing that , gives that

Finally, taking and using Lemma A.1, we deduce that

which completes the proof for the random order.

IID random variables

For any probability distribution on and for any we denote the expected maximum of independent random variables drawn from , and for any algorithm ALG we denote its expected output when given IID variable sampled from as input. The proof of Theorem 2.1 for this last model is much more technical than for previous models, so we first prove several auxiliary results that we will later use to provide a concise proof of the last part of the theorem.

Lemma A.2.

For any probability distribution and , we have

Proof.

We first write

and then use that

so we directly obtain

which gives that

As we consider non-negative random variables, it follows directly that

∎

Lemma A.3.

Let and let , then we have

Proof.

Let such that . For any let . is a partition of , thus we have

and observing that

we obtain, given , that

| (10) | ||||

| (11) |

is a Bernoulli random variable with expectation . Therefore, Chernoff’s inequality gives for any that

where the second inequality can be derived by treating separately and . In particular, for any , taking such that yields

Substituting this Inequality into (11) with , we obtain

and taking proves the first inequality of the lemma.

Let us move now to the second inequality. We have

and thus, using Inequality (10), again with and , it follows that

∎

Lemma A.4.

Let , , and , then for any we have

Proof.

The random variables and are not independent, thus we need to adequately compute the distribution of conditional to . For any and we have

therefore

Using this inequality and Lemma A.3, we deduce that

∎

Using the previous lemmas, we can now prove the theorem. Let , , and let be the probability distribution of a random variable that is equal to with probability , and drawn from with probability .

Let us consider i.i.d. variables , and for each we denote by the indicator that is drawn from . Define the number of random variables drawn from the distribution . In the following, we upper bound the competitive ratio of any algorithm by analyzing its ratio on this particular instance. For this, we first provide a lower bound on using Lemma A.2, and obtain

thus we have

| (12) |

where, for the last three inequalities, we used respectively Bernoulli’s inequality, Chernoff bound, then .

Then, we upper bound the reward of any algorithm given the instance as input. Let the smallest gap between two successive variables drawn from , and let the indices for which . We have for any algorithm ALG and positive integer that

| (13) |

Using Lemma A.3 and Lemma A.4, the first term can be bounded as follows

Considering that (i.e. ) and taking , we obtain

| (14) |

Regarding the second term in Equation (13), let be the stopping time of ALG and the last value sampled from and observed by ALG before it stops. We have

We then prove that the last term is the reward of an algorithm in the -prophet inequality. Let us be the algorithm that takes as input an instance of IID random variables, then simulates as follows: let set and for each

-

•

if : ALG observes the value ,

-

•

if : increment , then observes the next value , and ALG observes ,

-

•

if or ALG stops, then also stops.

When ALG decides to stop, the current value observed by is : the last value observed by ALG such that . Observe that stopping when , is equivalent to letting ALG observe zero values until the end, and stopping when ALG stops. Hence, the variables have the same distribution as IID samples from conditional to . Denoting the stopping time of and as defined in Lemma A.1, we deduce that

| (15) |

Substituting (14) and (15) in (13), with , yields

and using Inequality 12, it follows that

taking the limit and using Lemma A.1 gives

where the last inequality holds because for any algorithm A. From here, the statement of the theorem can be deduced by observing that, for , we have , thus , and we obtain

∎

Appendix B From -prophet to the -prophet inequality

B.1 Proof of Lemma 3.1

Proof.

Let ALG be any rational algorithm in the -prophet inequality. If ALG stops at some step , then by definition we have that , and thus . Otherwise, if it stops at , then its reward is , because -is non increasing.

On the other hand, let be the optimal dynamic programming algorithm for the -prophet inequality. At any step , if , then stopping at gives a reward of , while by rejecting , the final reward is guaranteed to be at least . Thus rejecting can only increase the reward, it is therefore the optimal decision. ∎

B.2 Proof of Proposition 3.2

Proof.

Let us place ourselves in any order model, or in the IID model. Assume that , then there exist a sequence such that .

Let an instance of non-negative random variables with finite expectation, and for all . Let ALG be a rational algorithm for the -prophet inequality and let us denote its stopping time. Denoting and using Lemma 3.1, we have for any constant that that

| (16) |

Let a positive integer, a positive constant, and consider the instance of random variables with for all . We have that and for any algorithm A. Therefore, using Inequality (16) with instead of and , then dividing by gives that

and taking the limit , we obtain

and since has finite expectation, taking the limit gives

Finally, taking the infimum over all instances, we obtain that

As in the proof of Corollary 2.1.1, permuting and is possible because there is an algorithm (dynamic programming) achieving the supremum for any instance. By Lemma 3.1, the inequality above holds for in particular for the optimal dynamic programming algorithm, which has a maximal competitive ratio. Therefore, the inequality remains true for any other algorithm A, not necessarily rational. ∎

B.3 Proof of Proposition 3.3

Proof.

Let us place ourselves in any order model or in the IID model. Since , there exists a sequence of positive numbers such that .

For the random variables taking values in a.s., in any order model, it is clear that the optimal decision when observing a zero value is to reject it, and when observing the value is to accept it. Let ALG be an algorithm satisfying this property and let be its stopping time. If then necessarily , and the reward of ALG in that case is if and otherwise. In particular, ALG is rational in the -prophet inequality and we have by Lemma 3.1 that

| (17) |

Consider now the instance of random variables where for all . satisfies the same assumptions as with and , and we have , and . It follows that

Taking the limit gives

ALG is also reasonable in the -prophet inequality. Therefore, using Lemma 3.1, we deduce that

This upper bound is true for the optimal dynamic programming algorithm, since it rejects all zeros and accepts , therefore the upper bound also holds for any other algorithm. ∎

Appendix C The -prophet inequality

C.1 Proof of Proposition 4.2

Proof.

For the lower bound, it suffices to consider the following trivial algorithm: if then run , and if then observe all the items then select the one with maximum value.

For the upper bound, let be an instance of the problem and for all , and let . Let A be any algorithm, its stopping time, and , where is the observation order. With the previous notations, we can write that . For any , the application is convex on , hence it can be upper bounded by . Therefore

Therefore, . Taking the infimum over all the instances gives the result. Indeed, if we denote the optimal dynamic programming algorithm for the standard prophet inequality, then

∎

C.2 Proofs for the adversarial order model

Proof.

We first prove the upper bound, and then analyze the single threshold algorithm proposed in the theorem.

Upper bound

Let , and let (such that ). Let the two random variables defined by almost surely and

Stopping at the first step gives a reward of , while stopping at the second step gives

hence the expected output of any algorithm is exactly equal to . On the other hand

and we deduce that, for any algorithm ALG for the -prophet inequality, we have

and this is true for any , thus taking gives

Lower bound

Consider an algorithm with an acceptance threshold , i.e. that accepts the first value larger than . Let be any instance, such that for all , and let us define and . In the classical prophet inequality, if no value is larger than then the reward of the algorithm is zero, and we have the classical lower bound

For the -prophet, if no value is larger than (i.e ), then the algorithm gains instead of . Therefore, it holds that

and observing that

we deduce the lower bound

The right term is maximized for satisfying , that leads to

Hence, by choosing a threshold satisfying we obtain a competitive ratio of at least . ∎

C.3 Proofs for the random order model

We prove here the upper and lower bounds stated in Theorem 4.4.

C.3.1 Proof of Theorem 4.4

Proof.

We first prove the upper bound, and then derive the analysis for single threshold algorithms.

Upper bound

Let , and let be independent random variables such that a.s. and for

Any reasonable algorithm skips zero values and stops when observing the value . The only strategic decision to make is thus to stop or not when observing . By analyzing the dynamic programming solution we obtain that the optimal decision rule is to skip if it is observed before a certain step , and select it otherwise. The step corresponds to the time when the expectation of the future reward is less than . Let be the random order in which the variables are observed. Then, if , i.e. if the value is observed before time , is not selected. The output of this algorithm is hence if at least one random variable equals , and otherwise. This leads to

where we used the inequality . On the other hand, if , then is selected if the value has not been observed before it, hence for any we have

we deduce that

where the last inequality is obtained by maximizing over . Finally, we directly obtain that

so for any algorithm ALG we obtain that

The function above is minimized for , which translates to

Lower bound

We still denote by the input instance and for all . Let ALG be the algorithm with single threshold , then it is direct that

| (18) |

We start by giving a lower bound on . We use from [Correa et al., 2021c] (Theorem 2.1) that for any it holds that

and for it holds that

from which we deduce that

| (19) |

On the other hand, we obtain that

| (20) |

Using (18), (19) and (20) we deduce that

Finally, choosing gives the result. ∎

C.3.2 Proof of Corollary 4.4.1

Proof.

For , we have immediately that

and for any . Since the function is concave, we can lower bound it on by , which is the line intersecting it in and . Therefore we have

Finally, using the previous theorem, this choice of guarantees a competitive ratio of at least

∎

C.4 Proofs for the IID model

Proof of Lemma 4.5

Proof of Lemma 4.5.

Let be the cumulative distribution function of , and ALG the algorithm with single threshold such that . We denote . As in the previous proofs, we will begin by lower bounding . For any , ALG stops at step if and only if and all the previous items were rejected, i.e. for all . Thus we can write

| (21) |

where the second equality is true by the independence of the random variables . On the other hand, we can upper bound as follows

Using the definition of , the independence of then Bernoulli’s inequality we have that

and observing that , we deduce that

by substituting into (21), we obtain

Finally, the reward in the -prophet inequality is

The equation , is equivalent to

| (22) |

and for any the function is decreasing on and goes from to , thus Equation (22) admits a unique solution , and taking guarantees a reward of . ∎

Proof of Theorem 4.6

Proof.

We first prove the upper bound, and then we give the single-threshold algorithm satisfying the lower bound.

Upper bound

We consider an instance similar to the one used in the proof of Theorem 4.4. Let , and let be IID random variables with the following the distribution defined by

A reasonable algorithm would always reject the value and accept the value . However, if the algorithm faces an item with value , it must decide to either accept it, or reject it with a guarantee of recovering at the end. By analyzing the dynamic programming algorithm , we find that the optimal decision is to reject if observed before a certain step , and accept it otherwise. Let us denote the stopping time of . By convention, we write to say that no value was selected by the algorithm, in which case the reward is .

If then necessarily , because rejects the value if it is met before step , and if then , because otherwise the algorithm would have selected the value and stopped earlier. It follows that the expected output of on this instance is

| (23) |

Let us now compute the terms above one by one.

where we used Bernoulli’s inequality . For , stops at if and if it has not stopped before, i.e. for all and for all , hence

the second equality is true by independence, and the last inequality holds because and . By independence of the variables , we also have that

Finally, the event is equivalent . In fact, the algorithm does not stop before if and only if for all and for all , and under these conditions, it holds that . Therefore

All in all, we obtain by substituting into 23 that

On the other hand, we have that

therefore, the expected maximum value is

We deduce that

Consequently, for any and for any algorithm ALG we have

In particular, for and we find that

This proves the upper bound stated in the theorem, and we can verify that it is increasing, and satisfies

Lower bound on the competitive ratio

We will prove that the algorithm presented in Lemma 4.5 has a competitive ratio of at least , where , first introduced in Theorem 4.4, is the unique solution of the equation , which is equivalent to .

Let . It follows from the definition of that is the unique solution of the equation . For any and we have that , hence, by definition of and

| (24) |

Moreover, the function is decreasing on . In fact its derivative at any point is

It follows from (24) that . Finally, given that is non-increasing on , we deduce that

We deduce that the competitive ratio of the algorithm described in Theorem 4.6 is at least .

∎

Appendix D Random decay functions

While we only studied deterministic decay functions in the paper, it is also possible to have scenarios with random decay functions. Consider for example that rejected items remain available after steps with a probability , this is modeled by with a Bernoulli random variable with parameter . We explain in this section how the definitions and our results extend to this case.

Definition D.1 (Random process).

Let is a non-empty set. A random process o is a collection of random variables . Two random processes and are independent if any finite sub-process of is independent of any sub-process of . For simplicity, let us say that the random processes are mutually independent if, for any , the random variables are mutually independent.

Definition D.2 (Random decay functions).

Let be a sequence of mutually independent random processes. We say that is a sequence of random decay functions if

-

1.

for any and ,

-

2.

is non-increasing for any ,

-

3.

is non-decreasing for any and .

The second condition asserts that the random variable has first-order stochastic dominance over . Along with the first condition, reflect that the distributions of the rejected values become progressively smaller. The last condition indicates that for any integer and non-negative real numbers , has a first-order stochastic dominance over , which means that, as the value of increases, so does the potential recovered value after steps.

The decision-maker

In the -prophet inequality with deterministic decay functions, we assumed that the decision-maker has full knowledge of the functions . In the randomized setting, we assume instead that the decision-maker knows the distributions of the decay functions, i.e. knows the distribution of the random variables for all and . However, they do not observe their values until they decide to stop. The online selection process is therefore as follows: the algorithm knows beforehand the distributions of the decay functions, then at each step, it observes a new item with value , and decides to stop or continue. Once they decide to stop at some time , they observe the values and then they choose the maximal one. As a consequence, the stopping time is independent of the randomness induced by the decay functions. As in the deterministic case, the expected reward of any algorithm ALG can be written as

The limit decay

A key result in our paper is the reduction of the problem to the case where all the decay functions are identical, and we prove this reduction by considering the pointwise limit of the decay functions. In the case of random decay functions, instead of the pointwise convergence, it holds for all that the random variables converge in distribution to some random variable . In fact, for any and , the sequence is non-increasing and non-negative, thus it converges to some constant . Given that is non-decreasing for any , we obtain by taking the limit that is non-increasing, and with similar argument we obtain, for any , that for all and for all . Therefore, defined the cumulative distribution of a random variable such that

-

•

is non-decreasing for all ,

-

•

for al .

Therefore, for all , is the limit in distribution of , hence a sequence of mutually independent random processes such that for any and defines a sequence of decay functions. We say in this case that all the decay functions are identically distributed as . Moreover, it holds for all that

From there, all the proofs of Section 2 can be easily generalized to the case of random decay functions, and it follows that we can restrict ourselves to studying identically distributed decay functions. Moreover, Proposition 3.2 can be generalized to the case of random decay functions, and the necessary condition for surpassing becomes . Similarly, using that the stopping time of the algorithm is independent of randomness induced by , Proposition 3.3 remains true with .

Lower bounds

For establishing lower bounds, observe that, for any random decay functions , if we denote for all , then defines a sequence of deterministic decay functions. Furthermore, for any instance and any algorithm ALG, it holds that

It follows that lower bounds established for deterministic decay functions can be extended to random decay functions by considering their expectations.

Implications

With the previous observations, both the lower and upper bounds, depending on that we proved in the deterministic -prophet inequality can be generalized to the random -prophet inequality, by taking