Robustness to Missing Data:

Breakdown Point Analysis

First draft: 12 January, 2023)

Abstract

Missing data is pervasive in econometric applications, and rarely is it plausible that the data are missing (completely) at random. This paper proposes a methodology for studying the robustness of results drawn from incomplete datasets. Selection is measured as the squared Hellinger divergence between the distributions of complete and incomplete observations, which has a natural interpretation. The breakdown point is defined as the minimal amount of selection needed to overturn a given result. Reporting point estimates and lower confidence intervals of the breakdown point is a simple, concise way to communicate the robustness of a result. An estimator of the breakdown point of a result drawn from a generalized method of moments model is proposed and shown -consistent and asymptotically normal under mild assumptions. Lower confidence intervals of the breakdown point are simple to construct. The paper concludes with a simulation study illustrating the finite sample performance of the estimators in several common models.

JEL classification: C01, C14, C18, C21, C25.

Keywords: Missing data, generalized method of moments, robustness, sensitivity analysis.

1 Introduction

Virtually every economic dataset is plagued by missing and incomplete records. Survey nonresponse is the most visible cause, and appears to be worsening over time. Bollinger et al. (2019) report that the Current Population Survey’s Annual Social and Economics Supplement item and whole nonresponse has been increasing, reaching 43% in 2015. By linking these data with the Social Security Administration Detailed Earnings Record, the authors show that the distribution of nonreponders differs from that of responders even after conditioning on a large set of covariates.

Samples with missing or incomplete observations fail to identify the population distribution (Manski, 2005). To make progress, researchers commonly apply standard procedures to the complete observations. This practice is typically justified by assuming the data are “missing completely at random” (MCAR); that is, incomplete observations follow the same distribution as that of the complete observations. In many settings such an assumption is implausible. Without it, the conclusions drawn are uncomfortably qualified as being about the distribution of the complete observations, rather than the actual distribution of interest.

This paper proposes a method to investigate the robustness of a conclusion when asserted about the whole population. Results are more robust when overturning them would require more selection. To make this intuition precise, selection is measured with the squared Hellinger divergence between the distribution of complete observations and that of the incomplete observations. Although many different statistical divergences could be used to measure selection, squared Hellinger is interpretable as a measure of how well the variables under study would predict an observation being complete. This gives the values of the selection measure context, allowing researchers to guage how much selection can be expected in a given setting.

The breakdown point is the minimum amount of selection needed to overturn a conclusion. Readers who doubt the setting exhibits that much selection will find the conclusion compelling. In models identified with the generalized method of moments (GMM), the breakdown point is the constrained minimum of the value function of a convex optimization problem. Estimators of the breakdown point are constructed from the dual of this convex inner problem, and shown to be -consistent and asymptotically normal. Lower confidence intervals are simple to construct. Reporting the point estimates and lower confidence intervals of the breakdown point is a simple, concise way to communicate a result’s robustness.

This approach has a number of advantages over existing methods for incomplete datasets. Sample selection models consider regressions with samples where the dependent variable is sometimes missing, and obtain point identification by modeling the selection process (Heckman, 1979; Das et al., 2003). These models require the data include a variable changing the probability of observation but not the dependent variable. This “exclusion restriction” is difficult to satisfy in many applications. The breakdown point approach proposed here can be used on most common GMM models (including but not restricted to regressions with missing outcomes), and requires no additional data. The breakdown point can be estimated even if the incomplete observations are in fact completely missing, a distinct possibility when using survey data.

The econometric literature on missing data has also explored bounding the parameter of interest based on the support (Manski, 2005; Horowitz & Manski, 2006). If all parameter values within these “worst-case” bounds satisfy the researcher’s conclusion, the conclusion is undoubtedly robust. Unfortunately, the bounds may be uninformative in practice. Proponents of this approach are well aware these bounds are conservative, and propose this exercise as a place to begin an investigation rather than end one. Additional identifying assumptions should then be considered, in order to make plain to readers what needs to be assumed to reach a given conclusion (Manski, 2013). The breakdown approach proposed here is a simple version of this exercise, as the assumption that selection is less than the breakdown point leads one to conclude the hypothesis under investigation.

A growing literature advocates for breakdown analysis as a general, tractable method to assess the sensitivity of a result to relaxations of identifying assumptions. The term “identification breakdown point” can be found as early as Horowitz & Manski (1995) in the context of corrupted data. Masten & Poirier (2020) advocates for the approach generally, and illustrates it with the potential outcomes framework. Diegert et al. (2022) define and study breakdown points in linear regressions suffering from omitted variable bias.

This paper is not the first to notice the appeal of breakdown point analysis in the context of missing data. Kline & Santos (2013) consider a setting with a missing scalar, propose measuring selection with the maximal Kolmogorov-Smirnov (KS) distance between the conditional distributions of complete and incomplete observations across all values of covariates, and advocate for “reporting the minimal level of selection necessary to undermine a hypothesis,” (p. 233). The methodology proposed here has some notable advantages. First, measuring selection with the maximal KS distance limits researchers to the case where only a scalar is missing, while measuring selection as proposed here allows any number of variables to be missing. Second, in a given setting it is easier to gauge whether the variables under study are likely to be good predictors of missingness than what share of the missing data is missing at random. This makes squared Hellinger a more natural measure of selection than KS distance. Which approach is more tractable will depend on the parameter of interest. Kline & Santos (2013) derives sharp, closed form bounds to the conditional quantiles of the missing variable, and frame the conclusion to be investigated in terms of those quantiles. This paper assumes the parameter of interest is identified with GMM and uses the model directly, giving up closed form solutions. In thoery this could lead to computational difficulties, but the simulations in section 5 present no issue.

The remainder of this paper is structured as follows. Section 2 formalizes the setting, the proposed measure of selection, and the breakdown point. The dual problem is presented and discussed in section 3. Section 4 defines the estimator and states the main results on estimation and inference, which are proven in the appendix. Section 5 presents a simulation study investigating the finite sample performance of the estimators. Section 6 concludes.

2 Measuring selection and breakdown analysis

Suppose the available data is the i.i.d. sample , where contains the variables of interest and indicates whether is observed. Note that may be a vector, and may be empty. Let denote the probability of observing , the distribution of conditional on , and the distribution of conditional on . and are called the complete case and incomplete case distributions respectively. The distribution of interest is the unconditional distribution of , given by . When is nonempty, the marginal distribution of conditional on is denoted . For simplicitly, is assumed to have the same finite support when as when . Remark 2.3 below discusses this assumption further.

To fix ideas, consider data collection via survey. is a vector of data the survey hopes to collect, which is observed only if the recipient responds (). The survey’s response rate, , is essentially always less than one in practice. It is common for administrative data to provide basic information about a survey recipient (such as age, occupation, etc.), which is collected in .

Analyses based on the complete observations may not convince researchers who worry that differs from . Such concerns are common, as few settings plausibly satisfy the missing completely at random assumption. However, it is often similarly implausible that differs greatly from . Researchers who convincingly argue that is not too different from can still convince their audience of conclusions drawn from an analysis of .111In some cases, such as correctly specified regression models, it suffices that the conditional distributions are the same as the identified . This weaker “missing at random” (MAR) assumption is also rarely plausible in practice, and analyses based on this assumption often rely heavily on the model being correctly specified.

A quantitative measure of the difference between and is needed to make this argument formal and convincing. The statistics literature provides a natural solution in the form of divergences: functions mapping two probability distributions to the nonnegative real line that take value zero if and only if the two distributions are the same. There are many such functions. To be useful as a measure of selection, a divergence should have a tractable interpretation, so that researchers can gauge whether a given amount of selection is reasonable for their setting.

2.1 An interpretable measure of selection

Missing data cause greater concern when researchers expect the variables of interest () to be a good predictor of incompleteness (). Consider again the example of data collection via survey. Researchers are rightfully more concerned about survey nonresponse when asking about the respondent’s arrest record than when asking for opinions on recent television programming. People with criminal records may be less willing to answer questions about that record.222For example, Brame et al. (2012) estimate the cumulative prevalence of arrest from ages 8 to 23 from a survey directly asking about prior arrests. The authors report upper and lower bounds derived by assuming the entire set of nonresponders had or had not been arrested, essentially the worst-case bounds advocated for by Manski (2005). This suggests that the distribution of responders may look quite different from the distribution of nonresponders, and that criminal records would be a good predictor of nonresponse.

To illustrate this more formally, let and be densities of and with respect to respectively:

An optimist may assume is independent of , implying that and . In contrast, a pessimist may assume is close to a deterministic function of , allowing to predict well. This would imply is close to or for many values of , and that differs greatly from .

As in the survey example, the setting often makes it clear whether would be a good predictor of . This hueristic is useful to identify and discuss selection concerns. The following lemma shows that measuring selection as the squared Hellinger distance between and captures this intuition, with larger values corresponding to having greater capability of predicting .333The Hellinger distance between probability measures and is where is any measure dominating both and .

Lemma 2.1.

Let be random variables with . Let and . Then

| (1) |

where the expectation is taken with respect to , the marginal distribution of .

All results are proven in the appendix.

Equation (1) states that the squared Hellinger distance between and is the expected percent of the standard deviation of reduced by conditioning on . In the extreme case where , equation (1) implies and the conditional distributions are the same. As the ability of to predict grows, the variance of conditional on decreases and grows toward one.

Remark 2.1.

It’s straightforward to see that implies

where , are the marginal distributions of conditonal on and respectively. This lower bound on selection is identified from the sample, and motivates the common practice of comparing the distribution of conditional on with that of conditional on ; the distributions and can only be “further” apart.

2.2 Divergences

Squared Hellinger provides an intuitive measure of selection, but there are many other options. A function mapping two probability distributions and to is called a divergence if , with equality if and only if . Divergences need not be symmetric nor satisfy the triangle inequality. The set of -divergences are particularly well behaved. Given a convex function satisfying for and taking a unique minimum of , the corresponding -divergence is given by

| (2) |

Many popular divergences are equal to -divergences when dominates .

| Name | Common formula | |

|---|---|---|

| Squared Hellinger | ||

| Kullback-Leibler (KL) | ||

| “Reverse” KL | ||

| Cressie-Read | – | , |

Although squared Hellinger has intuitive appeal outlined in Section 2.1, the breakdown point analysis proposed in this paper remains tractable for any -divergence listed in Table 1.444It is worth noting that the Cressie-Read divergence nests the other three as special cases. Squared Hellinger corresponds to . l’Hôpital’s rule shows that Kullback-Leibler corresponds to and Reverse Kullback-Leibler to . See Broniatowski & Keziou (2012) for additional discussion. Precise assumptions regarding the -divergence are collected in Assumption 1 below.

Remark 2.2.

Measuring selection with an -divergence facilitates estimation and inference, as the space of distributions with corresponds to the set of densities with respect to . In substance, this assumes and rules out selection mechanisms that “truncate” data.

2.3 Breakdown analysis in GMM models

Suppose a preliminary analysis supports an alternative hypothesis over a null hypothesis .555For example, such an analysis may be based on the complete observations assuming MCAR, or using imputation and assuming is MAR conditional on . The breakdown point is the minimum amount of selection needed to overturn such a conclusion. When selection is measured in terms of the squared Hellinger distance, the breakdown point translates the claim that is true into a claim about the ability of to predict . Specifically, if were true then would be weakly larger than the breakdown point. If this is implausible, then is similarly implausible.

This section formalizes this idea for generalized method of moment (GMM) models. Suppose the parameter of interest is characterized as the unique solution to a finite set of moment conditions,

where the expectation is taken with respect to the unconditional distribution, . The conclusion to be investigated is that falls outside a particular set , motivating the null and alternative hypotheses

Recall that the observed data is , where . The sample identifies , , and . A hypothetical distribution of the incomplete observations rationalizes the parameter if it has the identified marginal distribution of , , and the implied unconditional distribution solves the moment conditions for . The set of such distributions implying finite selection is

| (3) |

The breakdown point is the minimum selection needed to rationalize the null hypothesis:

| (4) |

where the infimum over the empty set is understood as . A simple example illustrates the idea.

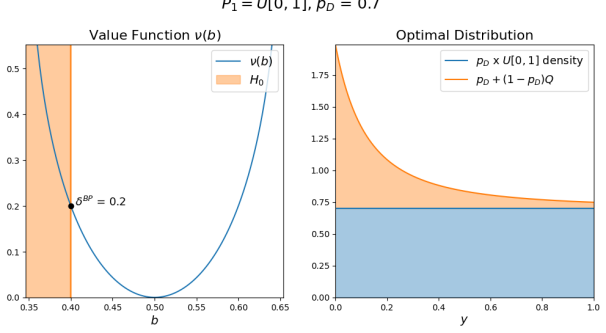

Example 2.1.

Let and . Let and be . The claim to support is , and selection is measured with squared Hellinger. is the set of continuous distributions on with expectation , so that implies

The inner minimization in display (4) chooses the distribution that minimizes selection while rationalizing . The outer minimization chooses the parameter that minimizes selection while rationalizing . Unsurprisingly, the outer minimization is solved by . The breakdown point is slightly above . A researcher convinced should conclude .

Breakdown analysis can also be framed as an exercise in partial identification, as in Kline & Santos (2013), Masten & Poirier (2020), and Diegert et al. (2022). In this framing, the researcher considers assumptions of the form for some , which continuously relax the assumption . The identified set for grows with . As long as the identified set is a subset of , it is clear the researcher’s conclusion holds. The breakdown point can then be defined as either the largest for which the identified set is contained in , or the smallest for which the identified set has nontrivial intersection with (the latter of which corresponds to the definition given in display (4)). For further discussion of this equivalent framing of the breakdown point, see appendix B.2.

The remainder of this paper constructs a -consistent and asymptotically normal estimator of , and constructs a lower confidence interval for . Researchers working with partially complete datasets should discuss the plausible amount of selection in their setting, and report the point estimate and the lower confidence interval for for each asserted conclusion. This will make plain to readers which conclusions are more sensitive to missing data concerns, and whether crucial results are sufficiently robust.

2.4 Preview of results

The estimation proceeds by separating the optimizations in (4). Define the primal problem

| (5) |

and notice that . The first step is to estimate the value function over a set large enough that , while the second step estimates through a simple plug-in estimator.

The primal problem is an infinite dimensional convex optimization problem over the space of probability distributions, but one that is very well studied in convex analysis. In particular, when defined in display (3) is characterized by a finite number of moment conditions, the primal problem has a well behaved, finite-dimensional dual problem with the same value function (Borwein & Lewis, 1991, 1993; Csiszár et al., 1999; Broniatowski & Keziou, 2006). Section 3 discusses this dual problem and the assumptions needed to make use of it. Under regularity conditions discussed in Section 4, sample analogue estimators based on this dual problem are uniformly consistent and asymptotically Gaussian on compact sets. Differentiability of the infimum then implies convergence in distribution of the plug-in estimator.

To conclude this section, Assumption 1 collects conditions on the setting, the GMM model, and the -divergence used to measure selection.

Assumption 1 (Setting).

is an i.i.d. sample from a distribution satisfying

-

(i)

,

-

(ii)

and have the same finite support ,

-

(iii)

, where , and

-

(iv)

is closed, proper, strictly convex, essentially smooth, takes its unique minimum of at , and satisfies for all . The interior of , denoted , satisfies , and is twice continuously differentiable on .

The finite support condition (ii) ensures that is characterized by a finite number of moments (see remark 2.3 below for additional discussion). Condition (iv) ensures the -divergence used to measure selection is well behaved, and is satisfied by every divergence in Table 1. In particular, strict convexity of ensures the primal problem (5) has a unique solution (-almost surely). is required to be essentially smooth to ensure the dual problem has a unique solution. The requirements that take a unique minimum of at and for ensures that is a well defined -divergence.

Remark 2.3.

If is not finitely valued, it is easy to see that requiring match a finite number of moments of will estimate a value no larger than . If this value is large enough to assuage missing data concerns, the breakdown point can only be larger.

3 Duality

As defined in display (5), is the value function of an infinite dimensional convex optimization problem. Fortunately, when selection is measured with an -divergence, this minimization becomes a well-studied problem known by various names: maximal entropy (Csiszár et al. (1999)), partially finite programming (Borwein & Lewis (1991)), or simply -divergence projection (Broniatowski & Keziou (2006)). The convex analysis results in these papers connect the primal problem in display (5) to a finite dimensional dual problem that is much easier to study and estimate. Under mild conditions, the value function of this dual problem coincides with the value function of the primal.

To state the dual problem, first note that the primal can be viewed as a problem over the set of densities with respect to :

where

| (6) |

The dual problem corresponding to (5) is given by

| (7) |

where is the convex conjugate of , given by . For convenience, table 2 summarizes the convex conjugate for several common divergences.

| Name | , | , | ||

|---|---|---|---|---|

| Squared Hellinger | , | , | ||

| Kullback-Leibler | , | , | ||

| “Reverse” KL | , | , |

Remark 3.1.

To ensure corresponds to a probability density, the constraints must enforce . This is implied by the constraints ensuring when is present. If there are no always-observed variables, set and .

3.1 Weak and strong duality

Assumption 1 suffices to show . This fact is known as weak duality, and implies that

| (8) |

for any . This inequality shows that using the dual problem for estimation of the breakdown point is at worst conservative. If is large enough to assuage selection concerns, researchers are assured that the breakdown point can only be larger.

Assuming only slightly more ensures strong duality holds, that is, . Recall from Assumption 1 (iv) that the interior of is denoted .

Assumption 2 (Strong duality).

is convex, compact, and satisfies . Furthermore, for each ,

-

(i)

there exists such that , almost surely , and

-

(ii)

solving (7) is in the interior of .

That strong duality holds under these conditions is a well known result.666To the authors knowledge, the first to show strong duality holds under similar conditions was Borwein & Lewis (1991). The proof of theorem 3.1, found in appendix C, uses a result due to Csiszár et al. (1999).

Theorem 3.1 (Strong duality).

The first order condition of the dual problem (7) provides intuition. Exchanging expectation and differentiation, the first order condition is

where solves the dual problem. Consider as a density with respect to . Notice that the first equations of the first order condition ensure , while the remaining equalities ensure the marginal distribution of matches . In fact, the proof of theorem 3.1 shows that under assumptions 1 and 2, is the -density of the solution to the primal problem.

Assumption 2 ensures the set on which is estimated is large enough to estimate the breakdown point, but not so large as to contain parameter values that cannot be rationalized with a well behaved -density. To illustrate, consider again example 2.1. is a scalar, , and is . For tractability suppose that Kullback-Leibler is used to measure selection. Since takes values on , the Manski bounds for are . Appendix E.1 shows that strong duality is satisfied whenever . Thus for this example, can be any convex, compact set in the interior of the Manski bounds.

Assumption 2 is maintained throughout the remainder of the paper. Accordingly, the notation will be used for the value function of the dual problem as well.

4 Estimation

4.1 The estimator

The sample analogue of the dual problem provides an estimator of the value function, and suggests a simple plug-in estimator of the breakdown point. The asymptotic properties of these estimators are easier to study if the objective of the dual problem is expressed with a single unconditional expectation, which comes at the cost of additional notation.

First define the matrix where and are identity matrices. Notice that and

| (9) |

Define

| (10) |

and observe that the dual problem is . The estimator of the value function is defined pointwise by

| (11) |

where estimates . Finally, estimates the breakdown point.

4.2 Asymptotic normality

The following assumption suffices for to be -consistent and asymptotically normal. First observe that the estimands solve the moment conditions , where

| (12) |

Let denote the graph of . For , the closed -expansion about this graph is .

Assumption 3 (Estimation).

Suppose that

-

(i)

is closed,

-

(ii)

has a unique solution,

-

(iii)

the matrix is nonsingular for each ,

-

(iv)

is continuously differentiable with respect to for each , and

-

(v)

there exists a convex, compact set containing for some satisfying

and

As previewed in section 2.4, is viewed as a two-step estimator where estimates in the first step, and is a plug-in estimator for . Conditions (iii), (iv), and (v) imply converges weakly in the space of bounded functions on , to a limiting process that is almost surely continuous. This is shown by linearizing uniformly over . Conditions (i) and (ii) ensure minimization over is a (Hadamard) differentiable map on the set of continuous functions of . The delta method then implies converges in distribution to a normal distribution.

Assumption 3 (i) and (iv) are easily verified by inspection of and respectively. Conditions (iii) and (v) are similar to conditions required of generalized empirical likelihood estimators (see, e.g., Antoine & Dovonon (2021) assumption 1 (v) and assumption 3 (iv), (vii)). Assumption 3 (ii) deserves additional scrutiny. When is a convex set, condition (ii) holds when is a strictly convex function. The following lemma shows that this is the case when describes a linear model with the outcome being the only missing data value.

Lemma 4.1 (Convex value function, linear models).

Lemma 4.1 covers instrumental variable models directly, and ordinary least squares as a special case (by setting ). It also covers parameters of the form , because the OLS regression of on a constant recovers . Simulation evidence presented in appendix E suggests data generating processes and models not covered by lemma 4.1 also produce convex . Remark 4.1 below discusses an approach to relaxing assumption 3 (ii), at the cost of additional complexity.

Theorem 4.2 below formally states the convergence in distribution result along with consistency of an estimator of the asymptotic variance. The variance depends on the jacobian term , which is estimated with

| (13) |

where and .

4.3 Inference

A large breakdown point implies the incomplete distribution would have to differ greatly from to rationalize the null hypothesis. If is larger than the plausible amount of selection in the setting, the null hypothesis is similarly implausible. Skeptical readers following this argument may worry the point estimate is larger than due to sample noise – but the force of the argument is only strengthened if falls below .

To address these concerns, researchers should report lower confidence intervals along with point estimates of the breakdown point. Theorem 4.2 implies that under assumptions 1, 2, and 3,

| (14) |

satisfies when is the quantile of the standard normal distribution.

Remark 4.1.

Assumption 3 (ii) can be relaxed at the cost of additional complexity. Without assumption 3 (ii), still converges in to , a tight Gaussian process on , and minimization of a function over remains a (Hadamard) directionally differentiable map on the set of continuous functions of . The delta method continues to imply converges in distribution to , where is the set of minimizers of .

Given a bootstrap such that converges weakly in probability conditional on to , confidence intervals can still be constructed by utilizing the tools developed in Fang & Santos (2019). One approach is to estimate the set through “near maximizers” of and using this estimated set to form an estimator of the map . The confidence interval for is formed by replacing in display (14) with the quantile of this estimated function applied to the bootstrap sample; see Fang & Santos (2019) theorem 3.2 and appendix lemma S.4.8.. As most cases of interest appear to satisfy assumption 3 (ii), this extension is left for future research.

5 Simulations

This section presents simulation results on a variety of different data generating processes. This serves both to illustrate the wide scope of models which can make use of breakdown point analysis and to investigate the finite sample properties of the proposed estimators. In each case, selection is measured using squared Hellinger divergence.

5.1 Simple mean

Recall example 2.1. The parameter of interest is the mean of a scalar random variable , , and the sample is . The distribution of is the uniform distribution on . The probability of observing is . To support the claim , let . Recall that the true breakdown point, , of this example is just over .

The following table summarizes 1,000 simulations for several different sample size.777Here .

| n | Bias | St. Dev. | Coverage | Ave. CI Length |

|---|---|---|---|---|

| 1,000 | 0.005 | 0.056 | 98.5 | 0.090 |

| 3,000 | 0.002 | 0.032 | 96.3 | 0.051 |

| 5,000 | 0.001 | 0.025 | 95.8 | 0.039 |

| 10,000 | 0.001 | 0.017 | 95.8 | 0.028 |

The simulations show little bias. Coverage is slightly above the targeted 95% significance level in smaller samples.

5.2 Linear models

Linear models are the among the most common tools used by empirical researchers. This subsection uses simulations to investigate linear regression with exogenous regressors.888Lemma 4.1 shows that when the outcome of a regression is the only missing variable, is convex. Appendix E.2 shows simulation evidence that the of the following DGP is convex.

Consider the model

| (15) |

where are the exogenous regressors: . Here is a continuous outcome variable, is the regressor of interest, is a continuously distributed control, and is a discrete control. The conclusion to be investigated is that the coefficient on is positive:

| (16) |

The researcher observes the sample and uses squared Hellinger to measure selection.

The data generating process specification takes inspiration from mincerian wage equations. For worker , let be ’s log-income, an indicator for being a college graduate, be ’s work experience, and the number of parents with college degrees (, , or ). Specifically, let be multinomial, , and .999, , and . Let (independent of all other variables), and . The coefficients are specified as and . Finally, is generated according to equation (15). Notice the support of is compact, ensuring the moment conditions in assumption 3 (v) are satisfied.

For the missing data process, let , where . The population value of the breakdown point is approximated as the point estimate obtained from a sample with one million observations. This sample reveals is about , and suffers from selection. Specifically, ignoring the incomplete observations is equivalent to solving for , which results in . The estimated squared Hellinger distance between and is . This large sample suggests the breakdown point of the conclusion described in display (16) is about 0.163.

The following table summarizes 1,000 simulations for several different sample sizes.

| n | Bias | St. Dev. | Coverage | Ave. CI Length |

|---|---|---|---|---|

| 1,000 | 0.016 | 0.049 | 98.7 | 0.076 |

| 3,000 | 0.007 | 0.026 | 95.8 | 0.041 |

| 5,000 | 0.004 | 0.019 | 95.5 | 0.031 |

| 10,000 | 0.003 | 0.013 | 94.5 | 0.022 |

Once again the simulations show little bias, with coverage slightly above the targeted 95% significance level in smaller samples.

5.3 Logistic regression

The logistic model is a popular choice for estimating the conditional probability of an event. Let and suppose that , where . The log-likelihood is concave, so estimating this model through maximum likelihood is equivalent to solving the first order condition

The model can be viewed as nonlinear GMM, with moment function .

This simulation considers the model’s prediction for for a known , and investigates the robustness of the conclusion that this conditional probability is at least 0.5. The corresponding null and alternative hypotheses are

| (17) |

Simulation evidence presented in appendix E.3 suggests the data generating process described below produces a convex value function. Since is equivalent to and is therefore convex, this suggests that assumption 3 (ii) holds.

The data generating process is one where the outcome is always observed, and the explanatory variables are sometimes missing. Specifically, is constructed by drawing and setting ; the result is that each has uniform marginal distributions on , and nontrivial covariance matrix. The outcome is always-observed: . The true underlying coefficients are , and the missing data process is conditionally binomial with ; that is, the probability of a complete observation is at least when and grows weakly with .

The resulting samples suffer from selection. A sample with one million observations suggests that is about . Ignoring the incomplete observations is equivalent to solving , which results in . The estimated squared Hellinger distance between and is . The covariate value of interest is . The true value for is , while the estimate assuming using the complete observations of the large sample above is . The point estimate for the breakdown point described by (17) using this large sample is . This is treated as the truth when evaluating the 1,000 simulations per sample size summarized in the following table:

| n | Bias | St. Dev. | Coverage | Ave. CI Length |

|---|---|---|---|---|

| 1,000 | 0.003 | 0.018 | 94.5 | 0.029 |

| 3,000 | -0.000 | 0.010 | 96.1 | 0.017 |

| 5,000 | 0.001 | 0.008 | 94.8 | 0.013 |

| 10,000 | -0.000 | 0.005 | 95.9 | 0.009 |

These simulations shows essentially zero bias and correct coverage at relatively small sample sizes.

6 Conclusion

This paper proposes breakdown point analysis as a tractable approach to assessing the sensitivity of a researcher’s conclusion to the common MCAR assumption. When defined with squared Hellinger, the breakdown point has a natural interpretation: if the result were false, the variables under study () would have to predict an observation being selected into the sample () at least well enough that . Estimators based on the sample analogue of the dual problem are shown -consistent and asymptotically normal, which facilitates the construction of lower confidence intervals. Researchers working with incomplete datasets should report the breakdown point estimate and lower confidence interval along with standard results, making transparent to their audience how robust the conclusion is to relaxing the MCAR assumption.

References

- Aliprantis & Border (2006) Aliprantis, C. D., & Border, K. C. (2006). Infinite Dimensional Analysis: A Hitchhiker’s Guide. Berlin, Heidelberg: Springer Berlin Heidelberg.

- Antoine & Dovonon (2021) Antoine, B., & Dovonon, P. (2021). Robust estimation with exponentially tilted hellinger distance. Journal of Econometrics, 224(2), 330–344.

- Bhatia (1997) Bhatia, R. (1997). Matrix Analysis. New York, NY: Springer New York.

- Bollinger et al. (2019) Bollinger, C. R., Hirsch, B. T., Hokayem, C. M., & Ziliak, J. P. (2019). Trouble in the tails? what we know about earnings nonresponse 30 years after lillard, smith, and welch. Journal of Political Economy, 127(5), 2143–2185.

- Borwein & Lewis (1991) Borwein, J. M., & Lewis, A. S. (1991). Duality relationships for entropy-like minimization problems. SIAM Journal on Control and Optimization, 29(2), 325–338.

- Borwein & Lewis (1993) Borwein, J. M., & Lewis, A. S. (1993). Partially-finite programming in l_1 and the existence of maximum entropy estimates. SIAM Journal on Optimization, 3(2), 248–267.

- Brame et al. (2012) Brame, R., Turner, M. G., Paternoster, R., & Bushway, S. D. (2012). Cumulative prevalence of arrest from ages 8 to 23 in a national sample. Pediatrics, 129(1), 21–27.

- Broniatowski & Keziou (2006) Broniatowski, M., & Keziou, A. (2006). Minimization of -divergences on sets of signed measures. Studia Scientiarum Mathematicarum Hungarica, 43(4), 403–442.

- Broniatowski & Keziou (2012) Broniatowski, M., & Keziou, A. (2012). Divergences and duality for estimation and test under moment condition models. Journal of Statistical Planning and Inference, 142(9), 2554–2573.

- Coleman (2012) Coleman, R. (2012). Calculus on normed vector spaces. Springer Science & Business Media.

- Csiszár et al. (1999) Csiszár, I., Gamgoa, F., & Gassiat, E. (1999). Mem pixel correlated solutions for generalized moment and interpolation problems. IEEE Transactions on Information Theory, 45(7), 2253–2270.

- Das et al. (2003) Das, M., Newey, W. K., & Vella, F. (2003). Nonparametric estimation of sample selection models. The Review of Economic Studies, 70(1), 33–58.

- Diegert et al. (2022) Diegert, P., Masten, M. A., & Poirier, A. (2022). Assessing omitted variable bias when the controls are endogenous. arXiv preprint arXiv:2206.02303.

- Fang & Santos (2019) Fang, Z., & Santos, A. (2019). Inference on directionally differentiable functions. The Review of Economic Studies, 86(1), 377–412.

- Heckman (1979) Heckman, J. J. (1979). Sample selection bias as a specification error. Econometrica: Journal of the econometric society, (pp. 153–161).

- Horowitz & Manski (1995) Horowitz, J. L., & Manski, C. F. (1995). Identification and robustness with contaminated and corrupted data. Econometrica: Journal of the Econometric Society, (pp. 281–302).

- Horowitz & Manski (2006) Horowitz, J. L., & Manski, C. F. (2006). Identification and estimation of statistical functionals using incomplete data. Journal of Econometrics, 132(2), 445–459.

- Kline & Santos (2013) Kline, P., & Santos, A. (2013). Sensitivity to missing data assumptions: Theory and an evaluation of the us wage structure. Quantitative Economics, 4(2), 231–267.

- Manski (2005) Manski, C. F. (2005). Partial identification with missing data: concepts and findings. International Journal of Approximate Reasoning, 39(2-3), 151–165.

- Manski (2013) Manski, C. F. (2013). Response to the review of ‘public policy in an uncertain world’.

- Masten & Poirier (2020) Masten, M. A., & Poirier, A. (2020). Inference on breakdown frontiers. Quantitative Economics, 11(1), 41–111.

- Newey & McFadden (1994) Newey, W. K., & McFadden, D. (1994). Large sample estimation and hypothesis testing. Handbook of econometrics, 4, 2111–2245.

- Rockafellar (1970) Rockafellar, R. T. (1970). Convex analysis, vol. 18. Princeton university press.

- van der Vaart & Wellner (1997) van der Vaart, A., & Wellner, J. A. (1997). Weak convergence and empirical processes with applications to statistics. London: Royal Statistical Society, 1988-.

- van der Vaart (2007) van der Vaart, A. W. (2007). Asymptotic statistics. Cambridge university press.

- Zeidler (1986) Zeidler, E. (1986). Nonlinear functional analysis vol. 1: Fixed-point theorems.

Appendices

Appendix A Appendix: notation

This appendix summarizes notation and facts used throughout the paper and appendices.

A.1 Calculations

A number of expressions are useful for verifying conditions in proofs and programming estimators. These are collected here for convenience.

Recall that , where is the population value of the value function, is the corresponding Lagrange multiplier, and . The notation refers to a vector in Euclidean space.

| (18) | ||||

| (19) | ||||

| (20) |

| (21) |

| (22) | ||||

A.2 Graphs

Let and . For a function , the graph of the function refers to the set . Define the closed -expansion of the graph of :

Note that is closed, and bounded if is bounded.

Given and , one can view as a function from to :

Define the graph of this function, , and the closed -expansion about this graph:

Several easily constructed subsets of imply useful inequalities. For example,

implies . It follows that for a function ,

Similarly,

implies that

It follows that , and hence for a function ,

Finally, note that any constant can be viewed as a trivial function of . The graph of this function is the set and is the set .

A.3 Spaces of bounded functions

For any set , denotes the set of real-valued bounded functions on . is equipped with the sup-norm: for , . The space of bounded functions taking values in for some is the product space , but can also be viewed as a process on . The latter notation makes it clear that standard empirical process results, typically stated for scalar-valued processes, apply.

If is a compact metric space, the extreme value theorem implies that continuous functions on are also bounded and hence form of a subpace of . This subspace is denoted

the notation will be used to mean when the metric is clear from context.

Some results will refer to subsets of bounded functions whose graphs falls into a particular set. Specifically, let for each , , and be the subset of whose graph is a subset of :

For an example of how this will be used, let and note that the function is uniformly continuous on the set . Defining and as above, we have that is uniformly continuous on this set. This implies that given by is continuous (see lemma D.1).

A.4 Matrices

For a matrix , let be the operator norm of , and , where is the entry in the -th row and -th column of . Let be the ordered singular values of . For a square real matrix , let be the ordered eigenvalues of .

Recall that all norms on finite dimensional real vector spaces are strongly equivalent, meaning that if and are any norms on , there exist constants such that for any matrix . If for some set , it follows that for any norm if and only if . Notice that strong equivalence with implies that, for any submatrix of , implies .

Recall that the singular values of a matrix are related to the eigenvalues of the square matrix by . The operator norm of a matrix is equal to its largest singular value, , and for invertible matrix and any , is a singular value of . These imply . Finally, for a vector , .

Appendix B Appendix: measuring selection and breakdown analysis

B.1 Measuring selection

See 2.1

Proof.

The marginal, unconditional distribution of is . This distribution dominates and , which have densities

with respect to . This implies

∎

B.2 Nominal identified sets

The exercise proposed in section 2.3 can also be understood with a framework of nominally identified sets. This approach to exposition is used in Kline & Santos (2013), Masten & Poirier (2020), and Diegert et al. (2022), and described for the current setting in this appendix.

Under the assumption and , the identified set for is a function of :

| (23) |

Notice is always growing with , in the sense that .

The researcher is primarily interested in testing against . Naturally, if has trivial intersection with she is confident in rejecting . This leads to the question “what is the largest value of such that has empty intersection with ?” Formally, define the breakdown point as

| (24) |

if , otherwise define .

B.2.1 Characterization through a value function

Lemma B.1 shows that the definition of the breakdown point given in (24) is equivalent to that given by (4).

Lemma B.1 (Characterization of breakdown point).

Proof.

Define the “robust region” as the set of where the identified set has trivial intersection with the null hypothesis:

and let be its compliment in . Notice that

The proof consists of two steps:

-

1.

Showing that

(25) where the infimum over the empty set is defined to be .

-

2.

Arguing that

and

Step 1. is a consequence of being a growing set (in the sense that ). Define . There are three possibilities:

-

(i)

. Then contains , hence .

-

(ii)

. Notice that implies that , from which it follows that

since , we have contains . Similarly, contains , and since , we have . For , let , and notice that , equivalently, . Therefore

let to see that .

-

(iii)

. Then the argument above implies contains , so and .

Therefore (25) holds.

For step 2., first notice that

| (26) |

Appendix C Appendix: proofs of duality results

Lemma C.1 (Unique primal solution).

Proof.

Let attain the finite infimum in (5), and let and denote their densities with respect to . We have that and . For any , the measure is feasible in (5), and characterized by the -density .

Suppose for contradiction that and differ on a set of positive -measure. Strict convexity implies that for any in that set,

Integrating with respect to reveals , contradicting optimality of . ∎

Lemma C.2 (Weak duality).

Proof.

First note that if the inequality holds trivially.

Suppose . Then , hence there exists at least one density satisfying . Notice that implies . Use this to see that for any with -density ,

integrating over with respect to gives

the left hand side of the last inequality doesn’t depend on , while the right hand side doesn’t depend on . Hence,

∎

See 3.1

Proof.

Let M be the set of measurable functions mapping . Consider the relaxed problem

for any , is a (possibly signed) measure with total measure one. Notice this problem has the same objective as the primal problem (5), but a larger feasible set (the set of finite signed measures with total measure one).

Now apply Theorem II.2 of Csiszár et al. (1999), with trivial . The dual of the relaxed problem is (7). Assumption 2 (i) is the “constraint qualification” of Csiszár et al. (1999) Theorem II.2, implying strong duality holds for the relaxed problem, , and the dual problem’s value is attained at a maximum. Let solve the dual problem. Assumption 2 (ii) allows application of the second part of Theorem II.2, implying the solution to the relaxed problem is given by

By assumption 1 (iv) and Lemma C.1, this solution is unique -almost surely.

Now we show that in fact solves the primal problem, (5). Notice is nonnegative, because is only defined on the non-negative reals. Furthermore,

where the third equality follows from . So the measure given by is a probability distribution dominated by . Therefore is feasible in the primal problem (5). Being feasible in the primal and solving the relaxed problem, must also solve the primal problem. ∎

Appendix D Appendix: proofs of estimation results

D.1 Technical lemmas

These results are self contained, with notation not related to the present paper.

Lemma D.1 (Uniform continuity of maps between bounded functions).

Let be a set, for each , , and be the subset of whose graph is a subset of :

Let be such that for any , and define

If is uniformly equicontinuous, then is uniformly continuous.

Proof.

Let , and use uniform equicontinuity to choose such that

for any . Notice that if with , then

and hence . ∎

Remark D.1.

Lemma D.2 (Restricted infimum is uniformly continuous).

For any and any ,

as a result, given by is uniformly continuous.

Proof.

Notice that

hence , or equivalently

Use this to see the claimed inequality:

Regarding the continuity claim, let and set . Then

hence implies . ∎

Lemma D.3 (Restricted infimum is Hadamard directionally differentiable).

Let be a metric space, a compact subset of , and

Then is Hadamard directionally differentiable at any tangentially to . is nonempty, and the directional derivative is given by

If is the singleton , then is fully Hadamard differentiable at tangentially to and .

Proof.

The result is essentially a corollary of Fang & Santos (2019) Lemma S.4.9, which shows that given by is Hadamard directionally differentiable at any tangentially to , with directional derivative

See Fang & Santos (2019) definition 2.1 for definitions of Hadamard directionally differentiable and fully Hadamard differentiable.

Let and note that is nonempty by the extreme value theorem. Let and be such that and . For , let be the restriction of to , given by . Observe that implies . Now notice that

where the last equality follows from the definitions and the fact that .

implies . Thus Fang & Santos (2019) Lemma S.4.9 and the definition of Hadamard directional differentiability implies

Finally, if then is linear in , and hence is fully Hadamard differentiable at . ∎

Lemma D.4 (Uniform consistency of estimated moments).

Let , , , ,

| and |

Suppose that

-

(i)

is i.i.d.,

-

(ii)

,

-

(iii)

is bounded, and

-

(iv)

there exists a finite such that is continuous on

for all , and

Then

Proof.

The triangle inequality implies

Consider the second term first. The dominated convergence theorem, being continuous, and implies that

is continuous. is a closed and bounded subset of , hence compact by the Heine-Borel theorem. Thus is in fact uniformly continuous by the Heine-Cantor theorem. Lemma D.1 then implies

is continuous. follows from and the continuous mapping theorem.

Now consider the first term. Compactness of , continuity of on , and implies that is Glivenko-Cantelli by van der Vaart (2007) example 19.8. With probability approaching one, and when this holds,

This concludes the proof. ∎

Lemma D.5 (Uniform consistency of matrix inverses).

Let . If

-

(i)

exists for all ,

-

(ii)

and , and

-

(iii)

,

then with probability approaching one, the function mapping to is well defined and

Proof.

It suffices to show that the singular values of converge in probability to the singular values of , uniformly over :

| (27) |

To see why, notice that implies . Condition (27) implies that with probability approaching one,

and on this event the function mapping to is well defined. Then notice that

implying

| (28) |

and are assumed, the latter implying by the continuous mapping theorem. Thus (28) implies .

The argument that (27) holds is broken into three steps:

-

1.

Show that is uniformly consistent for .

Notice that

Recall that for any square matrix ,

Use this to see that

and and therefore

(29) and by assumption, implying by the continuous mapping theorem, and thus by (29).

-

2.

Show the eigenvalues of converge to the eigenvalues of uniformly over .

Apply Weyl’s perturbation theorem, found in Bhatia (1997) as corollary III.2.6: for Hermitian matrices and ,

For real matrices Hermitian is equivalent to symmetric, so Weyl’s perturbation theorem implies

In other words, the eigenvalues of converge to the eigenvalues of uniformly over . These eigenvalues are the squared singular values of .

-

3.

Apply the continuous mapping theorem to conclude (27) holds.

∎

D.2 Consistency

Lemma D.6 (Unique dual solution).

Proof.

Let and . Since is essentially smooth, is strictly convex and as a result,

| (30) |

for any where , equivalently, where . Since , nonsingularity of implies

implies is a -nonnegligible set. It follows that

and hence

Therefore is strictly concave. attains a maximum by Theorem 3.1, and strict concavity implies this maximizer is unique. ∎

Lemma D.7 (Continuous dual solution and value function).

Proof.

Jensen’s inequality and assumption 3 (v) imply that

and, therefore, the following inequalities as well:

where and . It follows from the dominated convergence theorem that is twice continuously differentiable with respect to in a neighborhood of for every , with and .

must therefore solve the first order condition

Apply the implicit function theorem to this equation. The maps and exist and are continuous on an open neighborhood of . Moreover, strict concavity of shown in lemma D.6 implies is negative definite and hence invertible. It follows from the implicit function theorem (found in Zeidler (1986) as theorem 4.B) that is continuous in a neighborhood of . Since this holds for every , the function is continuous.

Lemma D.8 (Uniform consistency of the dual objective).

Proof.

Note that

and so the claim can be shown by applying technical lemma D.4, with indexed by , and the constant map for all . Verify the conditions of lemma D.4:

-

(i)

is i.i.d. by assumption 1.

-

(ii)

by the law of large numbers.

- (iii)

-

(iv)

implies . Let and

Observe that

is continuous on for each . Moreover, implies

and hence . This implies

Thus the result follows from lemma D.4. ∎

Lemma D.9 (Uniform consistency of the first stage).

Proof.

Let and . The proof consists of three steps:

-

1.

Show .

The following argument shows that for any there exists such that implies , and the probability of the former event converges to one. Let , and recall that and are continuous by lemma D.7. This implies is continuous in and

is compact. It follows by the extreme value theorem that is attained, say by . Lemma D.6 shows is the unique maximizer of over , which is a subset of , and therefore . Observe that implies , and thus

(31) Now notice that

(32) Lemma D.8 implies that holds with probability approaching one. When it does, (31) and (32) imply . Therefore .

-

2.

Show .

The claim follows from lemma D.8, because

-

3.

Show that with probability approaching one, .

This follows from an argument similar to the proof of Theorem 2.7 in Newey & McFadden (1994). With probability approaching one, and on this event, for every . Since

is concave in , no outside of could make the objective larger than . Thus when holds, for every or equivalently, .

∎

D.3 Inference

Proof.

Recall that . Jensen’s inequality and convexity of norms implies

and is implied by assumption 3 (v) and Jensen’s inequality. Therefore .

To establish , first use expression (21) to see that

where is the first order condition of the dual problem.

The middle matrix, , is invertible for each . To see this, first recall that lemma D.7, this matrix equals , which is also continuous in . The mapping from matrices to eigenvalues is continuous (see Bhatia (1997) corollary III.2.6 or its application in the proof of lemma D.5), so the extreme value theorem implies is attained by some . Lemma D.6 argues that is strictly concave in , hence is negative definite and thus . To summarize,

which implies is invertible for each . With this invertibility claim, it is straightforward to verify that for each , exists and is given by

To see that is finite, first recall that for conformable matrices,

Apply these inequalities to find that

| (33) |

and are the operator norms of submatrices of . Thus , argued above, implies

| and | (34) |

Finally, since is symmetric and negative definite, and

| (35) |

where the final claim follows from as argued above. Taken together, (33), (34), and (35) show that . ∎

Lemma D.12 (Donsker influence functions).

Proof.

By verifying the conditions of van der Vaart (2007) example 19.7.

Lemma D.13 (Weak convergence of the first stage).

Proof.

For legibility, the proof is presented in six steps:

-

1.

Mean value theorem.

-

2.

Show .

First, notice that

where is the square matrix whose -th entry is one and all other entries are zero.111111 When premultiplying a square matrix , “selects” the -th row. For example,

-

3.

Uniform linearization.

-

4.

Show in .

Define pointwise as

is a subset of the class considered in lemma D.12, and is therefore Donsker (see van der Vaart & Wellner (1997) theorem 2.10.1). Thus, in , where is a tight, mean-zero Gaussian process with covariance function

Now define

and observe that . Note that is a linear operator on . Lemma D.11 shows , which along with

shows that is bounded, hence continuous. The continuous mapping theorem then implies

where is a tight, mean-zero Gaussian process on . Letting be the -th row of the matrix , the covariance function of is

Notice that the marginals of are equal in distribution to those of . By van der Vaart & Wellner (1997) lemma 1.5.3, this implies the two distributions are the same and hence .

-

5.

Uniform linearization remainder control.

-

6.

Conclusion.

∎

Lemma D.14 (Support of ).

Proof.

Lemma D.13 and the continuous mapping thoerem implies . The Portmanteau theorem (van der Vaart & Wellner (1997) theorem 1.3.4) shows that this is equivalent to

for all closed sets . Since is closed and is continuous by lemma D.7, it suffices to show that is continuous with probability approaching one.

The argument is based on the Berge maximum theorem (Aliprantis & Border (2006) theorem 17.31). Recall and . Let . Lemma D.9 implies holds with probability approaching one, and when it does,

It thus suffices to show that is continuous with probability approaching one. This will follow from the Berge maximum theorem, once it is shown that is a continuous correspondence and is continuous on . Since

we can view , and thus

-

1.

Consider continuity of the objective first.

Assumption 3 (iv) implies is continuous in , and assumption 1 (iv) includes that is essentially smooth. It follows that

is continuous at if and only if for every , which holds if and only if . Notice that contains because is an element of . Assumption 3 (v) implies is finite, and lemma D.8 shows that is uniformly consistent for on , thus the continuous mapping theorem implies and therefore is finite with probability approaching one. When it is,

and is continuous on .

-

2.

Now consider continuity of .

Upper hemicontinuity will follow by application of the Closed Graph Theorem, Aliprantis & Border (2006) theorem 17.11. is compact by assumption 2 and D.7 shows that is continuous, therefore is compact, and hence is compact. Suppose converges to . Then because is closed. Since is continuous, , and therefore

shows that , i.e. . Thus , so is closed. Aliprantis & Border (2006) theorem 17.11 then implies is upper hemicontinuous.

Regarding lower semicontinuity, note that and are both metric spaces and hence first countable. Thus Aliprantis & Border (2006) theorem 17.21 implies is lower hemicontinuous at if and only if for any sequence with and any , there exists a subsequence and elements for each such that . For the subsequence we can take the sequence itself. Notice that satisfies

and therefore . Continuity of and implies , and thus is lower semicontinuous.

To summarize,

| and |

hold with probability approaching one. When both hold, is continuous by the berge Maximum theorem, implying . Thus

As argued above, the Portmanteau theorem implies . ∎

Lemma D.15 (-consistency and convergence in distribution).

Proof.

See 4.2

Proof.

Since is a singleton, say , lemmas D.13 and D.15 imply where

and . Now notice that is the sample analogue:

It suffices to show and

| (37) |

With these, the continuous mapping theorem will imply , hence , and another application of the continuous mapping theorem gives the conclusion .

To show and (37), first notice that

are special cases of van der Vaart (2007) example 19.8 and hence Glivenko-Cantelli. Specifically, is closed and bounded and hence compact. and are continuous by inspection of (19), (21), and (22). Finally, and

Next, observe that . First, follows from a standard extremum estimator argument. The function is continuous, uniquely minimized over the compact at , and by lemma D.9. Thus Newey & McFadden (1994) theorem 2.1 implies are consistent for . Use the triangle inequality, , continuity of (lemma D.7), and (lemma D.9) to see that

Appendix E Appendix: examples

E.1 Expectation

This simple example is useful primarily to illustrate the ideas in a concrete setting.

Suppose the parameter of interest is , and the sample is . The conclusion to be supported is that , motivating the null and alternative hypotheses

The model is characterized by . For the dual problem, set . The dual problem is

| (38) |

where .

E.1.1 Dual solution when is Kullback-Leibler and is

Suppose that , the distribution of , is . Let . Note that, since the support of is contained within as well, we have . The endpoints are only attained if concentrates degenerately at or respectively, distributions which violate .

For tractability, let the measure of selection be Kullback-Leibler. For this divergence we let , which has convex conjugate . The dual problem has first order condition

From the second equation we have

| (39) |

Suppose . Then the first equation requires

| (40) |

Now suppose . Consider the dual objective, and notice that

Since , it follows that and so . Thus the integral above can be solved with -substition, setting :

where , , and . Thus (38) becomes

from which we can compute the first order conditions

Once again, the second equation can be solved for . The following form will be more useful:

| (41) |

The first equation is

where the second to last equality uses (41) above. Rearranging gives

Now notice that is well defined and continuous whenever , takes values between and , with limits

Repeated applications of l’Hôpital’s rule shows that

Therefore there exists a solution whenever . Given this solution, (41) can be rearranged to obtain

Now notice that

and recall that implies solves the dual problem. Therefore the dual problem has a solution whenever .

has compact support, and is continuous in for any . Thus the extreme value theorem implies the solution is in the interior of . The implied solution to the primal, satisfies on the support of and solves the moment conditions. Thus assumption 2 is satisfied for any convex, compact .

E.2 Linear models

See 4.1

Proof.

Let , be distinct, , and . The proof of theorem (3.1) shows that the primal problem at and is attained by and with densities , . The moment conditions are , so and implies

| (42) | ||||

| (43) |

implying that

Similarly, for all . It follows that is feasible for . This implies

has -density . Convexity of implies that for any ,

integrating with respect to shows that

Since the left hand side equals , this shows is convex. Notice that no properties of , were specified in the argument above, so the same argument works to show is convex in by replacing , with their empirical counterparts.

Finally, to see that is strictly convex when has full column rank, use equations (42) and (43) to see that

Since has full column rank and ,

and thus differs from , implying differs from on a set of positive measure. For in that set, strict convexity of assumed in (1) (iv) implies

integrating with respect to implies , and thus . ∎

Simulations suggest that OLS more generally produces convex . Consider the data generating process described in section 5.2. Here the data is of the form , and the model is given by

The following figure investigates convexity of the (where ) numerically, by looking for convexity along random line segments. Specifically, let and be points in the sample space and compute for many values of between and . The following figure shows the results of this exercise for 10 randomly selected pairs, and shows that no deviation from convexity was detected.

![[Uncaptioned image]](/html/2406.06804/assets/Figs/convex_OLS_simulation.png)

E.3 Binary choice models

Let , , and suppose interest is in . A common choice of model assumes

for a known CDF . This model can be derived from a latent variable model of the form , where conditional on , the unobserved “latent variable” has distribution .

For example, the logistic regression uses , while the probit model uses .

Given i.i.d. data of the form , the model can be estimated through maximum likelihood. The likelihood of an observation is , implying a population log-likelihood of

Assuming is differentiable with density and that differentiation and expectation can be interchanged, the score is given by

and supposing is differentiable with derivative , the Hessian can be calculated and shown negative definite when is full rank. This implies the log-likelihood is strictly concave, and hence the first order condition suffices for maximization. Therefore the model could also be viewed as a GMM model solving

E.3.1 Logistic model

For the logistic model, , we can compute that

and thus the score simplifies to

This makes it straightforward to compute the Hessian of the log-likelihood as

Let and observe that is negative definite if is full rank. Thus, the logistic model can be viewed as a GMM model, where solves

This model can be put into the form used in assumption 1 with , , and .

Simulations suggest that the logistic model may also produce a convex . Consider the data generating process described in section 5.3. The logistic model can also be investigated for convexity. The same numerical exercise described above results in a figure that again shows no deviation from convexity.

![[Uncaptioned image]](/html/2406.06804/assets/Figs/convex_logistic_simulation.png)