Quantitative convergence guarantees for the mean-field dispersion process

Abstract

We study the dispersion process on the complete graph introduced in the recent work [19] under the mean-field framework. In contrast to the probabilistic approach taken in [19] and many other related works, our focus is on the investigation of the large time behavior of solutions of the associated kinetic mean-field system of nonlinear ordinary differential equations (ODEs). We establish various analytical and quantitative convergence results for the long time behaviour of the mean-field system and related numerical illustrations are also provided.

Key words: Dispersion of particles; Agent-based model; Interacting particle systems; Fokker–Planck equations; Econophysics

1 Introduction

We study the so-called dispersion process on the complete graph with vertices (denoted by ) introduced by Cooper, McDowell, Radzik, Rivera and Shiraga [17] and investigated in many subsequent works [19, 24, 37]. The dispersion process proposed in [17, 19] can be described as follows: Initially, indistinguishable particles are placed on a single vertex of . At the beginning of each time step, for every vertex occupied by at least two particles, each of these particles moves independently to another vertex on chosen uniformly at random. It is easy to convince us that the aforementioned process will freeze at the first time when each vertex hosts at most one particle, if .

In this manuscript, we will investigate a continuous-time version of the aforementioned dispersion model by virtue of the tools from kinetic theory. To fix notations throughout the rest the paper, we will label the vertex set of from to and denote by the number of particles inhabiting vertex at time , and set

to be the state vector of the dynamics. The state space is thus

| (1.1) |

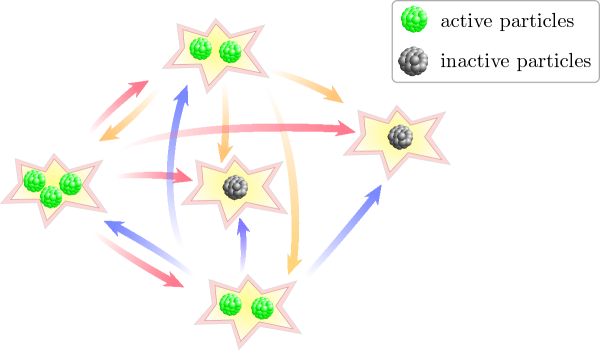

The continuous-time analog of the dispersion model suggested in [17, 19] is dictated by the following dynamics: at random times (generalized by exponential law), each non-empty vertex which is inhabited by at least two particles expels a particle at the rate to another uniformly chosen vertex . We illustrate our model via Figure 1 below.

Employing the terminology introduced in [19], a particle will be called happy if it does not occupy the same site with other particles, otherwise it is unhappy. Consequently, in the dispersion process on the complete graph, only unhappy (or “active”) particles have the motivation to move to a different site.

Remark. It is also possible to interpret the dispersion process using terminologies from econophysics (which is a sub-branch of statistical physics that apply concepts and techniques of traditional physics to economics and finance [20, 15, 21, 28, 35, 36]). Indeed, if we think of particles as dollars, vertices as agents, and as the amount of dollars agent has at time , then the aforementioned dispersion process can be viewed as the following simple dollar exchange mechanism in a closed economical system: at random times (generated by an exponential law), an agent who has at least two dollars in his/her pocket (i.e., ) is picked at a rate proportional to his/her fortune , then he or she will give one dollar to another agent picked uniformly at random. It is clearly from the set-up that we have

| (1.2) |

since the economical system is closed, where denotes the average amount of dollars per agent in this context. Mathematically, the update rule of this multi-agent system can be represented by

| (1.3) |

It is worth noting that the model (1.3) resembles the so-called poor-biased exchange model in econophysics [7, 13] in which one replaces the update rule (1.3) by the following:

| (1.4) |

Therefore, one can view the dispersion process as a modified dynamics of the poor-biased exchange model (1.4) with the inclusion of a wealth-flooring policy, which prevents agents whose wealth are no more than dollar from giving out their dollars to other agents.

We emphasize that earlier works on the dispersion process on complete graphs [19] focuses only on the asymptotic region where the total number of particles scales no faster than the total number of sites (i.e., ). In this regime, the process ends almost surely when no particle is sharing the same site with other particles, and every particle becomes happy at the (random) time termed as the dispersion time. The main quantity under investigation in [17, 19, 24, 37] is the aforementioned dispersion time via advanced probabilistic tools. By resorting to a kinetic/mean-field approach, we aim to treat the case where remains a positive constant of order and we also allow for general initial distributions of particles beyond the common choice of putting all particles on a single site.

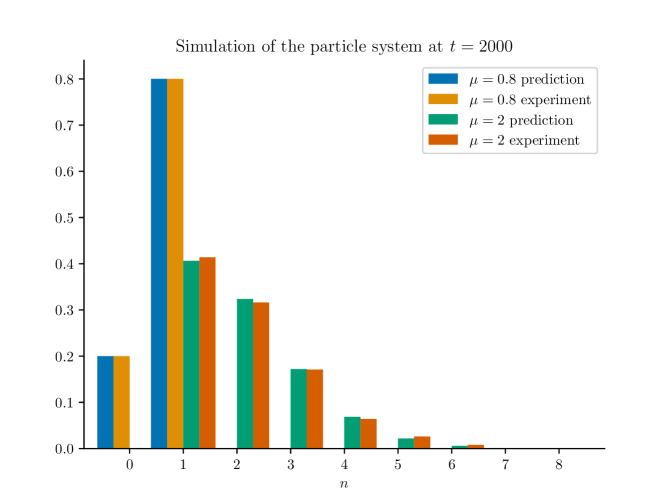

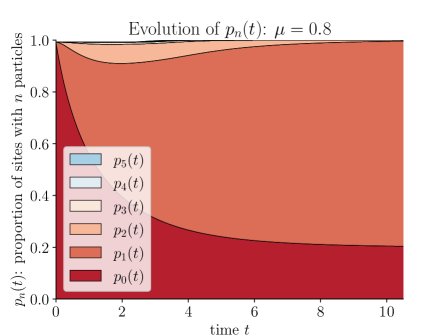

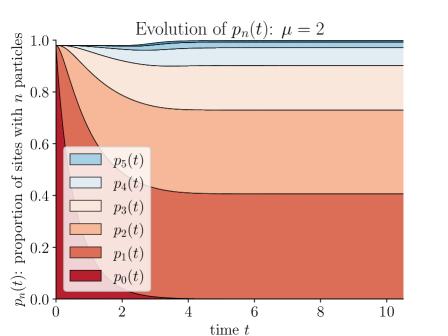

To foresee the behavior of the dynamics under the large time and the large population limits, we perform agent-based simulations using after time units using two different values for (see Figure 2). We observe that the distribution of the number of particles in a site converges to a Bernoulli distribution with mean for (Figure 3-left) and that it stabilizes near a zero-truncated Poisson distribution with mean predicated by (1.10) for (Figure 3-right).

The continuous-time dispersion model we have described is a standard interacting particle system and is amenable to mean-field type analysis under the large population limit , which is detailed in a recent work [11] on a related model. In order to carry out the mean-field analysis as , the concept of propagation of chaos [38] plays a crucial role. Bearing in mind our aim to obtain a simplified (and fully deterministic) dynamics when we send , we consider the probability distribution function of particles:

| (1.5) |

with . It has been indicated in a very recent work [11] that evolution of is governed by the following deterministic system of nonlinear ordinary differential equations:

| (1.6) |

with

| (1.7) |

The rigorous justification of this transition from the stochastic interacting agents systems (1.3) into the associated mean-field ODE system (1.6)-(1.7) requires the proof of the propagation of chaos property [38], which is beyond the scope of the present manuscript. On the other hand, propagation of chaos property has been proved for other econophysics models, see for instance [7, 8, 9, 10, 13, 18] and we also refer interested readers to [4, 5, 6, 12, 14, 16, 26, 30, 31, 32] for many other interesting models in econophysics literature that we omit to describe in details.

Once the mean-field system of ODEs (1.6)-(1.7) associated to the interacting particle system has been identified, one natural follow-up step is to investigate the long time behaviour of the infinite dimensional ODE system (1.6)-(1.7) with the hope of showing convergence of its solution towards an equilibrium distribution, and we take on this task in the following sections. As will be shown in Section 2, the large time asymptotic of the solution to (1.6)-(1.7) depends on the value of the parameter which represents the average amount of particles per site initially. We prove in Section 3 via the construction of a appropriate Lyapunov functional that solutions of (1.6)-(1.7) converges to the following Bernoulli distribution

| (1.8) |

when . Note in particular that the two-point Bernoulli distribution (1.8) boils down to the Dirac delta distribution centered at , defined via

| (1.9) |

when . We demonstrate in Section 4 the convergence of solutions of (1.6)-(1.7) to the following zero-truncated Poisson distribution (in various senses) when :

| (1.10) |

where and denotes the principal branch of the Lambert function [29].

We remark here that the mathematical analysis of the large time behavior of the system (1.6)-(1.7) is much trickier when . Instead of finding a Lyapunov function, we analyze the long time behavior of the probability generating function (PGF), which satisfies a transport equation. We deduce convergence to the zero-truncated Poisson distribution at exponential rate by establishing pointwise convergence of the PGF.

The main result is summarized in the following theorem, which combines Corollary 3.2 and Corollary 4.11.

Theorem 1

There exists a positive constant depending only on and , such that any solution to (1.6)-(1.7) with finite initial variance converges strongly to its equilibrium distribution as . To be precise, denote for and for , we have:

-

1.

If , then

-

2.

If , then

-

3.

If , then

-

4.

If , then there exists depending only on such that

2 Elementary properties of the ODE system

After we achieved the transition from the interacting agents system (1.3) to the deterministic nonlinear ODE system (1.6)-(1.7), our main goal is to show convergence of solution of (1.6)-(1.7) to its (unique) equilibrium solution. We aim to describe some elementary properties of solutions of (1.6)-(1.7) in this section. As we have indicated in the introduction, the large time behavior of solutions to (1.6)-(1.7) depends critically on the range to which the parameter belongs. Before we dive into the detailed analysis of the system of nonlinear ODEs, we first establish some preliminary observations regarding solutions of (1.6)-(1.7).

Lemma 2.1

The proof of Lemma 2.1 is based on straightforward computations and will be skipped. Thanks to these conservation relations, the solution lives in the space of probability distributions on with the prescribed mean value , defined by

| (2.2) |

More importantly, the system (1.6)-(1.7) will be equivalent to the following system of nonlinear ODEs:

| (2.3) |

in which

| (2.4) |

Remark. The Fokker–Planck type equation (2.3)-(2.4) admits a heuristic interpretation as a jump process with loss and gain, and we illustrate this perspective via Figure 4 below. We also recall that represents the proportion of unhappy particles at time .

Remark. The system (2.3)-(2.4) also resembles another system of nonlinear ODEs known as the Becker-Döring cluster equations. For both systems, the generator is a second-order difference operator linear in but is nonlinear in . We refer interested readers to [1, 3, 2, 27, 33, 34] and references therein.

Proposition 2.2

Proof.

From the evolution equation defined by (2.3)-(2.4), it is straightforward to check that

| (2.5) |

must hold at equilibrium. On the one hand, if , then for all , and we deduce that the unique equilibrium solution, denoted by , is

On the other hand, for , we deduce from (2.5) that , and the unique equilibrium distribution, denoted by , is

| (2.6) |

where is chosen such that . Since , we deduce that , whence . We finish the proof by introducing a new constant .

Remark. The zero-truncated Poisson distribution defined in (1.10) admits a simple interpretation in terms of random variables. Indeed, if , then the distribution of conditioned on obeys the zero-truncated Poisson distribution, whose law is given by .

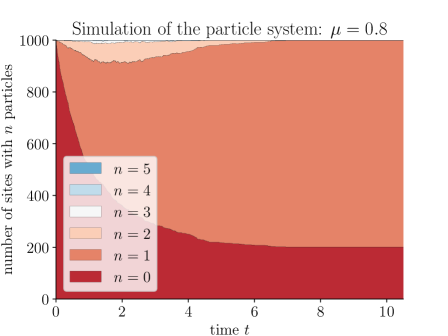

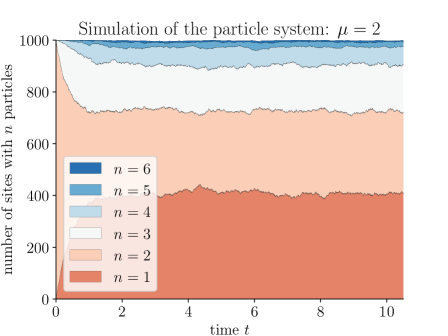

As a warm-up before we dive into the analytical investigation of the nonlinear ODE system (2.3)-(2.4) in the upcoming sections, we investigate numerically the convergence of to its equilibrium distribution. We use and respectively. To discretize the model, we use components to describe the distribution (i.e., ). As initial condition, we use , and for . The standard Runge-Kutta fourth-order scheme is used to discretize the ODE system (2.3)-(2.4) with the time step . We plot in Figure 5 the evolution of the numerical solution at different times corresponding to and , respectively. It can be observed that convergence to equilibrium occur in both cases.

3 Convergence to Bernoulli distribution for

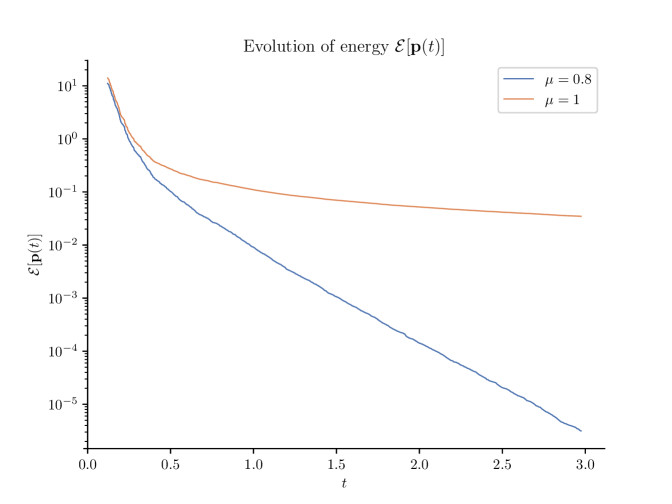

To justify the large time convergence of solutions of the system (2.3)-(2.4) when , we employ a suitable Lyapunov functional associated to the dynamics (2.3)-(2.4). For this purpose, we define the following energy functional:

| (3.1) |

for each , which is just a shifted version of the second (raw) moment of the distribution . We first start with an elementary variational characterization of the Bernoulli distribution .

Lemma 3.1

For each , the Bernoulli distribution with parameter satisfies

| (3.2) |

Consequently, for all and the equality holds if and only if .

Proof.

Since , we have and thus , in which the inequality will become an equality if and only if for all . This finishes the proof of Lemma 3.1.

We now prove the following quantitative convergence result for the dissipation of along solutions to the system of nonlinear ODEs (2.3)-(2.4) when .

Theorem 2

Proof.

A straightforward computation gives us

| (3.5) | ||||

We observe that for all , thus for we deduce from (3.5) that

from which the exponential decay of (3.3) follows immediately. On the other hand, for , we have since . The differential equation satisfied by implies that , whence

for all . Consequently, we derive from (3.5) the following differential inequality:

whence

| (3.6) |

To conclude the proof and reach the advertised upper bound (3.4), it suffices to notice that

for all . Thus the proof of Theorem 2 is completed.

To illustrate the decay of the energy numerically, we use the same set-up as in the previous experiment shown in Figure 6 for two different values of , using the semi-log scale.

As an immediate corollary, we can readily deduce the following strong convergence in .

Corollary 3.2

Under the settings of Theorem 2, if has a finite variance, then there exists some constant depending only on and the initial datum such that for all , it holds that

| (3.7) |

and

| (3.8) |

4 Relaxation to zero-truncated Poisson distribution for

We use a different approach to study the system (2.3)-(2.4) when . Treating as a known function, we first show that the probability generating function solves a first order partial differential equation (PDE), which turns out to be an explicitly solvable transport equation. By writing out the solution, we show that an auxiliary function

| (4.1) |

must satisfy a nonlinear Volterra-type integral equation [25]. We then study this integral equation to extract convergence and convergence rate, which further sheds light on the convergence of the distribution to the zero-truncated Poisson distribution (1.10).

4.1 Probability generating function

Define the probability generating function of the solution to (2.3)-(2.4) by

Since and , we know the above series is absolutely summable. Moreover, because , we know that

is absolutely summable. The ODE system (2.3)-(2.4) can thus be written as the following PDE for :

| (4.2) |

We also recall that the probability generating function can recover the following statistics:

Moreover, since for all , we have monotonicity in all derivatives:

Lemma 4.1

The probability generating function can be expressed using the following explicit formula: for with , , we have

where is defined by (4.1).

Proof.

We only prove for with . This will be sufficient because both sides are analytic in and the equality follows by identity theorem.

Define , then

Now we let , then the evolution of satisfies

with

So satisfies the following first order linear ODE with the above initial condition:

Setting

| (4.3) |

we have and

Integrating from to and using , we deduce that

Finally, notice that and , we conclude the proof of Lemma 4.1.

4.2 Convergence of the auxiliary function

In this subsection, we first show that the auxiliary function satisfies an integral equation, and then prove it converges to a limit which depends on the value of .

Lemma 4.2

For , satisfies

where .

Proof.

We now investigate the limiting behavior of as . First, since for all , we can bound using its definition (4.1):

By direct computations, we obtain the following bound:

| (4.6) |

In particular, .

Next, we control the nonlinear integral term using the following lemma.

Lemma 4.3

Let . If for all , then

where is a strictly increasing continuous function defined by

and the remainder term is .

Proof.

First, we separate our target integral as follows:

The first term has an exponential decay since

The second term is bounded from above by

and from below by

The proof is thus completed because and .

We are now ready to prove the convergence of .

Lemma 4.4

Let , then

Proof.

Denote

| (4.7) |

Since

we deduce that

| (4.8) |

With the above error function, we can write the integral equation in Lemma (4.2) as

| (4.9) |

Since is bounded (uniformly in time), as , the liminf and limsup of exist and are bounded between

We claim that . To prove this, we first fix with , then there exists such that

Invoking Lemma 4.3 together with the monotonicity of the map , we conclude for all that

Therefore, the limsup and liminf of are bounded by

This is true for any sufficiently small so the advertised claim is justified.

Within the interval , we demonstrate that the function is a contraction mapping. Indeed, note that

Moreover, the derivatives of are

So for , we know is bounded by

Since is a contraction mapping and is contained in this interval, we conclude from that where is the unique fixed point of in . It satisfies

We observe that and are two real roots to the equation , hence we can use the Lambert function to select the principal branch and arrive at the relation . This finishes the proof of Lemma 4.4.

Remark. The convergence of implies the pointwise convergence of the probability generating function. Indeed, sending in Lemma 4.1 and applying the result of Lemma 4.3 (with being replaced by ), we obtain

where denotes the PGF of the zero-truncated Poisson distribution (1.10). According to a classical result [22], if the PGF exists and the above convergence holds in a neighborhood of then converges to in distribution. However, in the following we will strengthen the results obtained so far and prove convergence for , which are stronger convergence guarantees.

4.3 Quantitative convergence of the auxiliary function

Next, we study the quantitative rate of convergence of . We do it in two steps. In the first step we prove a decay, and in the second step we refine the previous estimate to reach a decay. First, we show an improved lower bound.

Lemma 4.5

There exists such that for all .

Proof.

Lemma 4.6

There exist constants depending only on , such that

Proof.

For , we set

which is a nonnegative and decreasing function.

Let be a sequence of increasing times to be determined later. Denote and , then for all . Using Lemma 4.5, we deduce that . By Lemma 4.3, we know that at any time , it holds that

In particular,

Since is -Lipschitz in , we have

Now we take the supremum over to obtain the following recursive inequality

in which depends only on and we employed the bound (4.8) for .

Denote . For , we take , then

where is chosen such that for all . The recursive inequality now becomes

Taking the summation from to , we have

We thus conclude by monotonicity that

Finally, the restriction can be easily removed by taking to be sufficiently large.

We can see that both the convergence and the above estimate are based on comparison. To obtain a sharper estimate, we take the difference:

| (4.10) |

Therefore, we can control the difference by

| (4.11) | ||||

| (4.12) |

Here we used the fact that the power function is -Lipschitz on for . Define this integral quantity on the right by

Then , so satisfies the following differential inequality

If , then will decay exponentially. However, this estimate is useless when . We need to estimate the difference in the following integral sense.

Lemma 4.7

Denote . For any , define

If converges, then for , it holds for all that

| (4.13) |

in which is a constant depending only on .

Proof.

Notice that

Combined they satisfy the following differential equality:

| (4.14) |

As , if we drop the last term then we directly get a decay at rate

| (4.15) |

In the following, we would like to improve the decay rate from to .

By (4.11), we can estimate by

where

Note that now we have an improved estimate of . Indeed, using the crude estimate established in Lemma 4.6, we have

Therefore we can improve the estimate (4.8) to

| (4.16) |

As is bounded, we have

We now exchange the order of the double integral:

The absolute value symbol is extracted because the (inner) integrand has a fixed sign for each and . To compute the inner integral, we define

Then the inner integral can be expressed as

We will leave the detailed proof of the Lipschitzness of in Lemma 4.8. Denote , then we show in Lemma 4.8 that is -Lipschitz on , and -Lipschitz on . By Lemma 4.6, for with

we have , so

Thus

| (4.17) |

Rearranging (4.17) leads us to

Combining it with (4.14) we obtain

Recall that . We have

Upon integration this inequality from to , we get for all that

Note that (4.15) yields

The right hand side also dominates for . Indeed, we have from (4.15) that

Next, notice that for , is uniformly bounded by

As for the error term, we have

from which the advertised estimate (4.13) follows.

Lemma 4.8 (Lipschitzness of the function )

Denote , then is -Lipschitz on , and -Lipschitz on .

Proof.

We remark that can be computed and expressed using Euler’s Gamma function, but we will not need the exact form. Its derivative

is positive and decreasing in . Thus for all ,

Moreover, the partial derivative of with respect to reads as

hence for any it holds

In particular,

On the other hand, for we have

Therefore, if , then

If , then . We thus conclude that the function is -Lipschitz on .

Lemma 4.7 provides an iteration scheme to improve the decay rate. In the following proposition, we will use Lemma 4.7 to bootstrap the decay rate from lemma 4.6 to a sharper exponential decay rate.

Proposition 4.9

If , then there exists a constant depending on such that

If , then there exist constants depending on such that

where denotes the usual Japanese bracket shorthand.

Proof.

We first claim that for any with , it holds that

Indeed, given any , we have

which is convergent. We now iterate this using Lemma 4.7. Clearly, in view of Lemma 4.6. After finitely many steps, , and we have

From this claim, we proved for . For the case , we know that for all . To use Lemma 4.7, we need to quantify the size of , which is actually the Laplace transform of evaluated at . Although it can be estimated from the above iteration, we use the following strategy instead. Taking the derivative of with respect to yields

Using Lemma 4.7 and bearing in mind that implies that , we can control it by

whence by taking . Thus we also have

This is true for all , so for we can take and obtain

In summary, we find has the desired decay rate.

As a corollary, we deduce the following convergence rate of as .

Corollary 4.10

For , we have

Proof.

It suffices to notice that can be recovered from via

Since both and occur at this rate, the result follows.

4.4 Strong convergence of the ODE system

In this subsection, we are ready to prove the various strong convergence results regarding the solution of the system (2.3)-(2.4) towards the zero-truncated Poisson distribution (1.10) as . First, we show convergence in . Recall that

Theorem 3

Let . There exists constants , depending on such that for all , it holds that

Proof.

We first recall the classical Parseval’s identity:

By Lemma 4.1, we have

for all with . Notice that

On the other hand, we know for with that

Assembling these estimates, we proved for with that

Since

the above implies uniform convergence of to for all with , which shows that converges to in by Parseval’s identity.

Utilizing the tail estimate for the (zero-truncated) Poisson distribution, we can also establish the following convergence result in .

Corollary 4.11

Let . There exists constants , depending on such that for all , it holds that

Proof.

For to be specified later, we have

The first term is easily controlled by the norm:

The second term is amenable to explicit computations, leading us to

Thanks to the Chernoff bound for the Poisson distribution, for it holds that

We know for our zero-truncated Poisson distribution that

Finally, setting allows us to deduce that , whence

This completes the proof.

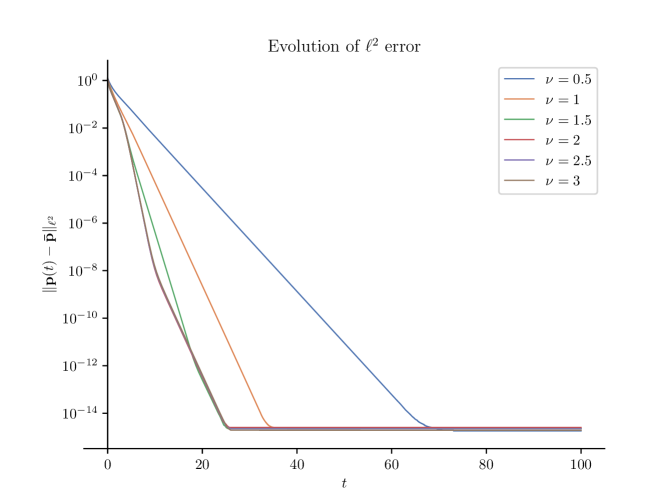

To illustrate the quantitative convergence guarantee reported in Theorem 3 we plot the evolution of the error over time (see Figure 7) with , under the same set-up as used for Figure 5. We observe the exponential decay of as predicted by Theorem 3, although our analytical rate might be sub-optimal for .

5 Conclusion

In this manuscript, we adopted a kinetic perspective and investigated the continuous-time version of the so-called dispersion process (on a complete graph with vertices) introduced and studied in a number of recent works [17, 19, 24, 37]. Instead of the probabilistic approach employed in the aforementioned papers, we make use of the classical kinetic theory [39] and focus on the analysis of the associated mean-field system of nonlinear ODEs. We also emphasize that via the identification of particles as dollars and vertices (or sites) as agents, it is possible to reformulate the model using econophysics terminologies as well [20, 15, 28, 35, 36], and such reinterpretation of the dispersion model enables us to design and create intriguing models for econophysics literature.

This work also leaves some important follow-up problems which deserve their own treatments and attentions. For instance, it is possible to prove a (uniform in time) propagation of chaos result in order to make the derivation of the mean-field ODE system (1.6) rigorous? Can one design a natural Lyapunov functional associated to the solution of the nonlinear ODE system (1.6) when ? Lastly, we are also wondering the possibility of sharpening the quantitative convergence guarantee provided by Theorem 3, as numerical simulations suggest that we might hope for a decay of the form when .

Acknowledgement It is a great pleasure to express our gratitude to Sebastien Motsch for generating Figure 1 that illustrates the dispersion model under investigation. The second author is partially supported by the NSF grant: DMS 2054888.

References

- [1] John M. Ball, Jack Carr, and Oliver Penrose. The Becker-Döring cluster equations: basic properties and asymptotic behaviour of solutions. Communications in Mathematical Physics, 104:657–692, 1986.

- [2] John M. Ball, and Jack Carr. The discrete coagulation-fragmentation equations: existence, uniqueness, and density conservation. Journal of Statistical Physics, 61:203–234, 1990.

- [3] John M. Ball, and Jack Carr. Asymptotic behaviour of solutions to the Becker-Döring equations for arbitrary initial data. Proceedings of the Royal Society of Edinburgh Section A: Mathematics, 108(1-2):109–116, 1988.

- [4] Bruce M.Boghosian, Merek Johnson, and Jeremy A. Marcq. An Theorem for Boltzmann’s Equation for the Yard-Sale Model of Asset Exchange: The Gini Coefficient as an Functional. Journal of Statistical Physics, 161:1339–1350, 2015.

- [5] Fei Cao, and Stephanie Reed. A biased dollar exchange model involving bank and debt with discontinuous equilibrium. arXiv preprint arXiv:2311.07851, 2023.

- [6] Fei Cao, and Nicholas F. Marshall. From the binomial reshuffling model to Poisson distribution of money. Networks and Heterogeneous Media, 19(1):24–43, 2024.

- [7] Fei Cao, and Sebastien Motsch. Derivation of wealth distributions from biased exchange of money. Kinetic & Related Models, 16(5):764–794, 2023.

- [8] Fei Cao, Pierre-Emannuel Jabin, and Sebastien Motsch. Entropy dissipation and propagation of chaos for the uniform reshuffling model. Mathematical Models and Methods in Applied Sciences, 33(4):829–875, 2023.

- [9] Fei Cao. Explicit decay rate for the Gini index in the repeated averaging model. Mathematical Methods in the Applied Sciences, 46(4):3583–3596, 2023.

- [10] Fei Cao, and Pierre-Emannuel Jabin. From interacting agents to Boltzmann-Gibbs distribution of money. arXiv preprint arXiv:2208.05629, 2022.

- [11] Fei Cao, and Sebastien Motsch. Sticky dispersion on the complete graph: a kinetic approach. arXiv preprint arXiv:2404.08868, 2024.

- [12] Fei Cao, and Sebastien Motsch. Uncovering a two-phase dynamics from a dollar exchange model with bank and debt. SIAM Journal on Applied Mathematics, 83(5):1872–1891, 2023.

- [13] Fei Cao, and Roberto Cortez. Uniform propagation of chaos for a dollar exchange econophysics model. European Journal of Applied Mathematics, 1–13, 2024.

- [14] Anirban Chakraborti, and Bikas K. Chakrabarti. Statistical mechanics of money: how saving propensity affects its distribution. The European Physical Journal B-Condensed Matter and Complex Systems, 17(1):167–170, 2000.

- [15] Anirban Chakraborti, Ioane Muni Toke, Marco Patriarca, and Frédéric Abergel. Econophysics review: I. Empirical facts. Quantitative Finance, 11(7):991–1012, 2011.

- [16] Arnab Chatterjee, Bikas K. Chakrabarti, and Subhrangshu Sekhar Manna. Pareto law in a kinetic model of market with random saving propensity. Physica A: Statistical Mechanics and its Applications, 335(1-2):155–163, 2004.

- [17] Colin Coopery, Andrew McDowellz, Tomasz Radzikx, and Nicolás Rivera. Dispersion processes. Random Structures & Algorithms, 53(4):561–585, 2018.

- [18] Roberto Cortez, and Joaquin Fontbona. Quantitative propagation of chaos for generalized Kac particle systems. The Annals of Applied Probability, 26(2):892–916, 2016.

- [19] Umberto De Ambroggio, Tamás Makai, and Konstantinos Panagiotou. Dispersion on the complete graph. arXiv preprint arXiv:2306.02474, 2023.

- [20] Adrian Dragulescu, and Victor M. Yakovenko. Statistical mechanics of money. The European Physical Journal B-Condensed Matter and Complex Systems, 17(4):723–729, 2000.

- [21] Bertram Düring, Daniel Matthes, and Giuseppe Toscani. Kinetic equations modelling wealth redistribution: a comparison of approaches. Physical Review E, 78(5):056103, 2008.

- [22] Manuel L. Esquivel. Probability generating functions for discrete real-valued random variables. Theory of Probability & Its Applications, 52(1):40–57, 2008.

- [23] Lawrence C. Evans. Partial differential equations. American Mathematical Society, Vol. 19, 2022.

- [24] Alan Frieze, and Wesley Pegden. A note on dispersing particles on a line. Random Structures & Algorithms, 53(4):586–591, 2018.

- [25] Gustaf Gripenberg, Stig-Olof Londén, and Olof Staffans. Volterra integral and functional equations. Cambridge University Press, 1990.

- [26] Els Heinsalu, and Patriarca Marco. Kinetic models of immediate exchange. The European Physical Journal B, 87(8):1–10, 2014.

- [27] Pierre-Emmanuel Jabin, and Barbara Niethammer. On the rate of convergence to equilibrium in the Becker–Döring equations. Journal of Differential Equations, 191(2):518–543, 2003.

- [28] Ryszard Kutner, Marcel Ausloos, Dariusz Grech, Tiziana Di Matteo, Christophe Schinckus, and H. Eugene Stanley. Econophysics and sociophysics: Their milestones & challenges. Physica A: Statistical Mechanics and its Applications, 516:240–253, 2019.

- [29] Johann-Heinrich Lambert. Observationes variae in mathesin puram. Acta Helvetica, 3(1):128-168, 1758.

- [30] Nicolas Lanchier. Rigorous proof of the Boltzmann–Gibbs distribution of money on connected graphs. Journal of Statistical Physics, 167(1):160–172, 2017.

- [31] Nicolas Lanchier, and Stephanie Reed. Rigorous results for the distribution of money on connected graphs (models with debts). Journal of Statistical Physics, 176(5):1115–1137, 2019.

- [32] Daniel Matthes, and Giuseppe Toscani. On steady distributions of kinetic models of conservative economies. Journal of Statistical Physics, 130(6):1087–1117, 2008.

- [33] Barbara Niethammer. On the evolution of large clusters in the Becker-Döring model. Journal of Nonlinear Science, 13:115–122, 2003.

- [34] Barbara Niethammer. A scaling limit of the Becker-Döring equations in the regime of small excess density. Journal of Nonlinear Science, 14:453–468, 2004.

- [35] Eder Johnson de Area Leão Pereira, Marcus Fernandes da Silva, and HB de B. Pereira. Econophysics: Past and present. Physica A: Statistical Mechanics and its Applications, 473:251–261, 2017.

- [36] Gheorghe Savoiu. Econophysics: Background and Applications in Economics, Finance, and Sociophysics. Academic Press, 2013.

- [37] Yilun Shang. Longest distance of a non-uniform dispersion process on the infinite line. Information Processing Letters, 164:106008, 2020.

- [38] Alain-Sol Sznitman. Topics in propagation of chaos. In Ecole d’été de probabilités de Saint-Flour XIX—1989, pages 165–251. Springer, 1991.

- [39] Cédric Villani. A review of mathematical topics in collisional kinetic theory. Handbook of mathematical fluid dynamics, 1:71–305, 2002.