1pt \cellspacebottomlimit1pt \newdateformatmonthyeardate\monthname[\THEMONTH] \THEYEAR

Risk-Sensitive Online Algorithms

Abstract

We study the design of risk-sensitive online algorithms, in which risk measures are used in the competitive analysis of randomized online algorithms. We introduce the -competitive ratio () using the conditional value-at-risk of an algorithm’s cost, which measures the expectation of the -fraction of worst outcomes against the offline optimal cost, and use this measure to study three online optimization problems: continuous-time ski rental, discrete-time ski rental, and one-max search. The structure of the optimal and algorithm varies significantly between problems: we prove that the optimal for continuous-time ski rental is , obtained by an algorithm described by a delay differential equation. In contrast, in discrete-time ski rental with buying cost , there is an abrupt phase transition at , after which the classic deterministic strategy is optimal. Similarly, one-max search exhibits a phase transition at , after which the classic deterministic strategy is optimal; we also obtain an algorithm that is asymptotically optimal as that arises as the solution to a delay differential equation.

1 Introduction

Randomness can improve decision-making performance in many online problems; for instance, randomization improves the competitive ratio of online ski rental from to [30], of metrical task systems (MTS) from linear to polylogarithmic in number of states [11, 12], and of online search from polynomial to logarithmic in the fluctuation ratio [22, 38]. However, this improved performance can only be obtained on average over multiple problem instances, as a randomized algorithm may vary wildly in its performance on any particular run. While this may not pose a concern for decision-making agents facing a large number of problem instances, such variability may be undesirable if an agent has only a small number of instances to solve, or if they are sensitive to risks of a particular magnitude or likelihood.

Numerous fields, including economics, finance, and decision science, have fielded research on risk aversion and alternative risk measures that enable modifying decision-making objectives to accommodate these risk preferences (e.g., [42, 46, 29, 4, 56]). One of the most well-studied risk measures in recent years, due to its nice properties (as a coherent risk measure) and computational tractability, is the conditional value-at-risk (), which measures the expectation of a random loss/reward on its -fraction of worst outcomes [48, 49, 1]. and other risk measures have been applied to problems spanning finance and insurance [35, 14], energy systems [45, 40], and robotic control [27, 2], and have been studied as an objective in place of the expectation in MDPs [15, 16, 33], bandits [57, 7], and online learning [24, 58, 53].

Despite the significant extent of literature on risk-sensitive algorithms for online learning with the conditional value-at-risk, there has been no work on the design and analysis of competitive algorithms for online optimization problems like ski rental, online search, knapsack, function chasing, or MTS with risk-sensitive objectives. These types of online optimization problems have deep connections with online learning [9, 13, 19], but also substantial qualitative differences due varied problem structures and the competitive analysis framework. Coupled with their practical applications (e.g., [32, 60, 3, 54]), we are thus motivated to ask: how can we design competitive online algorithms when we care about the of the cost/reward, and what are the optimal competitive ratios for different problems?

In this work, we begin to work toward answering this question, studying risk sensitivity in the design of competitive online algorithms for online optimization. In particular, we focus on two of the prototypical problems in online optimization: ski rental, which, as a special case of MTS, encapsulates the fundamental “rent vs. buy” tradeoff inherent in online optimization with switching costs [6, 3], and one-max search, which exhibits a complementary “accept vs. wait” tradeoff fundamental to constrained online optimization [25, 37]. While both of these problems are simple to pose, they both reflect crucial components of the difficulty of more complicated online optimization problems, and thus serve as ideal analytic testbeds for investigating the design of risk-sensitive algorithms in online optimization.

1.1 Contributions

In this work, we define a novel version of the competitive ratio that penalizes a randomized algorithm’s cost via the conditional value at risk (), which we call the -competitive ratio (). We then study the design of algorithms for several online problems with the objective. We make contributions along three fronts:

(1) Optimal Risk-Sensitive Online Algorithms We find the optimal -competitive algorithm for continuous-time ski rental with any and characterize its as . For discrete-time ski rental, we analytically characterize the optimal -competitive algorithm when , where is the buying cost, and we prove that there is a phase transition at , after which the optimal coincides with the deterministic optimal . Finally, we propose an algorithm for one-max search whose is asymptotically optimal for small , and we prove that one-max search exhibits a phase transition at , after which the optimal coincides with the deterministic optimal , where is the so-called “fluctuation ratio” of the problem.

(2) Techniques For continuous-time ski rental and one-max search, we show that the conditional value-at-risk of an algorithm’s cost can be written as an integral expression of its inverse cumulative distribution function. This parametrization is useful both for proving analytic bounds on algorithms’ , and as a source for optimal algorithms for these problems: it is through this formulation that we obtain the delay differential equation describing the optimal algorithm for continuous-time ski rental, and similarly how we obtain our algorithm for one-max search, which is asymptotically optimal when is small. For both versions of ski rental, our results rely on structural characterizations of the optimal algorithm which, while evocative of similar results from the ski rental literature, require significantly more care due to the complicated behavior of the conditional value-at-risk.

(3) Insights We gain several new insights from our results. The phase transitions in the discrete-time ski rental and one-max search problems, where sufficiently large implies that the optimal is the deterministic optimal competitive ratio, suggests that there is a sharp limit to the benefit that randomization can yield in certain risk-sensitive online problems. Moreover, the qualitative difference between the continuous- and discrete-time ski rental problems – namely, the fact that the latter has a phase transition while the former does not – indicates that continuous and discrete problems may, in general, behave differently when risk sensitivity is introduced.

1.2 Related Work

Risk-aware online algorithms

As mentioned earlier, while numerous problems in MDPs, bandits, and online learning have been studied with the conditional value-at-risk and other risk measures penalizing the objective, we are not aware of existing work in the literature designing competitive online algorithms for online optimization with such objectives. Even-Dar et. al [24] consider the related problem of online learning with expert advice and rewards depending on the Sharpe ratio and mean-variance risk measures; they prove lower bounds precluding the possibility of obtaining sublinear regret in this setting as well as upper bounds for several relaxed objectives. While their work also considers a notion of competitive ratio against the best fixed expert in its lower bounds, their upper bounds focus on regret-style results, and their problem setting is markedly different from those we consider. A related problem is the demonstration of high-probability guarantees on the competitive ratio of randomized online algorithms, which was studied by Komm et al. [34] for a general class of online problems. However, their work is concerned with proving that existing algorithms have performance close to some nominal value with high probability, rather than designing new algorithms that are provably optimal given an agent’s particular risk preferences and the distribution over algorithm performance.

Closest to our current work is the recent paper of Dinitz et al. [20] on risk-constrained algorithms for ski rental, where the objective remains to minimize the competitive ratio defined in terms of expected cost, but algorithms must satisfy additional constraints on the likelihood that their cost will exceed a specified value. This amounts to imposing constraints on the value-at-risk (), or quantiles, of the algorithm’s competitive ratio; in contrast, we focus on algorithms that are optimal for a risk-sensitive objective involving the conditional value at risk, which considers not just the likelihood of exceeding a certain value, but the expectation over the resulting tail of the distribution. and have been exhaustively compared in the financial literature (e.g., [50, 14]), and , which is a so-called coherent risk measure, often exhibits more favorable robustness and handling of tail events than , which is not coherent [4]. Indeed, is very sensitive to problem structure and parameter selection, leading to the interesting non-continuous behavior in solution structure observed in [20]. does not beget such sensitivity, but influences the solution structure in its own unique way: for continuous-time ski rental and one-max search, we obtain algorithms that result from the solution of delay differential equations.

Beyond worst-case analysis of algorithms

The strengthening and weakening of the adversary as is varied in the -competitive ratio is similar in spirit to beyond worst-case analysis, where the adversary is weakened or additional information is provided to enable improved bounds over the pessimistic and unrealistic adversarial setting. There is a significant breadth of work in the literature applying these ideas to online optimization and other online problems. Some notable directions on this subject are smoothed analysis [51, 26], in which an adversary’s decision is tempered with stochastic noise; algorithms with advice [10, 23], in which an algorithm receives a small number of accurate bits of information about the problem instance in advance; and algorithms with predictions [39, 47, 55, 17, 36], in which algorithms are augmented with potentially unreliable predictions about the problem instance, and algorithms seek to exploit these predictions when they are accurate while maintaining worst-case guarantees when they are not.

1.3 Notation

Throughout, capital letters (e.g., ) refer to random variables on , which we interchangeably refer to via their measures (e.g., ) or their cumulative distribution functions (e.g., ). Given a random variable with support bounded in the interval , we define its inverse CDF as ; note that, given the bounded support, this definition agrees with the standard definition (where the infimum is taken over all of ) for all , with the only disagreement being at , where , whereas the standard definition yields ; this variant is well-established in the literature (e.g., [59, Definition 1.16]). We use this definition to ensure finiteness of on , and the bounded support of will be clear by context whenever the inverse CDF is discussed. denotes the nonnegative reals and the strictly positive reals, and denotes the natural numbers. The notation refers to the function, and for any , we write and denote by the -dimensional probability simplex. For a vector , we denote its th entry . The function refers to the th branch of the Lambert function, which is defined as a solution to (see, e.g., [18]).

2 Background & Preliminaries

In this section, we introduce risk measures and the conditional value-at-risk, and give overviews of the three online problems we study in this work.

2.1 Risk Measures and the Conditional Value-at-Risk

A risk measure is a mapping from the set of -valued random variables to that gives a deterministic valuation of the risk associated with a particular random loss. As risk preferences can vary by decision-making agent and application, many different risk measures have been introduced and studied in the literature (see, e.g., [52, Chapter 6] for several examples). A prominent class of measures that has emerged in practice due to its favorable properties is the set of coherent risk measures [4]. Perhaps one of the most well-studied coherent risk measures in recent years is the conditional value-at-risk (): the at probability level of a random variable , written , is the expectation of on the -tail of its distribution, i.e., its -fraction of worst outcomes. It can be defined in several ways:

Definition 1 (Conditional Value-at-Risk).

Let be a real-valued random variable with CDF . If has a density , then for the conditional value-at risk at level of is defined as the expectation of , conditional on its outcome lying in the -tail of its distribution [48]:

For a general random loss with probability measure , can be defined in several equivalent ways [49, 1, 21]:

| (1) |

where in the final expression, is an uncertainty set of probability measures defined as

The first expression in (1) is a variational form of , and is useful for tractable formulations of risk-sensitive optimization problems. The latter two expressions highlight the intuition that computes the expected loss of on the worst -fraction of outcomes in its distribution, or, in the parlance of [21] which we sometimes adopt, on the “worst -sized subpopulation”.

From the above definition it is clear that and , the largest value that can take [41]; we thus define , so that is defined for all .

2.2 Online Algorithms and Competitive Analysis

In the study of online algorithms, algorithm performance is typically measured via the competitive ratio, or the worst case ratio in (expected) cost between an algorithm and the offline optimal strategy that knows all uncertainty in advance.

Definition 2 (Competitive ratio).

Consider an online problem with uncertainty drawn adversarially from a set of instances . Let Alg be a deterministic online algorithm for the problem, and let Opt be the offline optimal algorithm. Alg’s competitive ratio () is the worst-case ratio in cost between Alg and Opt over all problem instances:

If Alg has competitive ratio , it is also called -competitive. If Alg is a randomized algorithm, then the competitive ratio is defined with its expected cost:

where the expectation is taken over Alg’s randomness.

In our work, we introduce a new version of the competitive ratio for randomized algorithms that goes beyond expected performance: instead, we penalize a randomized algorithm via the ratio between the conditional value-at-risk of its cost and the offline optimal’s cost, terming this metric the -competitive ratio (abbreviated ).

Definition 3 (-Competitive Ratio).

Let Alg be a randomized algorithm, and let Opt be the offline optimal algorithm. The -Competitive Ratio () is defined as the worst-case ratio between the of Alg’s cost and the offline optimal cost:

where the is taken over Alg’s randomness.

It is immediately clear that any deterministic algorithm has for all , while for randomized algorithms these metrics will generally differ for . Note that, given the definition of as focusing on the worst -fraction of a distribution, the may also be interpreted as a metric that gives the adversary additional power to shift the distribution of the algorithm’s randomness. Under this interpretation, the may be viewed as an interpolation between the classic randomized case where the adversary has no power over Alg’s randomness (), and the case where the adversary has full control over Alg’s randomness and determinism is optimal (). This model can also be seen as a complement to the oblivious adversary, which knows Alg but cannot see the realization of its randomness, and the adaptive adversary, which sees all random outcomes; in the case, while the adversary does not see Alg’s random outcome directly, it has the ability to control this outcome in a way limited by the .

2.3 Online Problems Studied

We now provide a brief introduction for each of the three problems we study in this work.

Continuous-Time Ski Rental

In the continuous-time ski rental (CSR) problem, a player faces a ski season of unknown and adversarially-chosen duration , and must choose how long to rent skis before purchasing them. In particular, the player pays cost equal to the duration of renting, and cost for purchasing the skis. Deterministic algorithms for ski rental are wholly determined by the day on which the player stops renting and purchases the skis: an algorithm that rents until day and then purchases pays cost . Randomized algorithms can be described by a random variable over purchase days, in which case the algorithm pays (random) cost . Given knowledge of the total number of skiing days , the offline optimal strategy is to rent for the entire season if , incurring cost , and to buy immediately otherwise, yielding cost . Defining as the of a strategy , we have

where denotes the competitive ratio of the strategy when the adversary’s decision is . We denote by the smallest of any strategy. We will omit the “CSR” in the superscript when it is clear through context that we are discussing the continuous-time ski rental problem.

We will assume without loss of generality that . It is well known that , which is achieved by purchasing skis deterministically at time , and , which is achieved by a probability density supported on the interval [31, 30]. In the following lemma, which is proved in Appendix A.1, we show that when considering as a performance metric with general , we may similarly restrict our focus to probability measures with support on .

Lemma 4.

Let be a distribution on . There is a distribution with support in such that, for any , has no worse than : .

An important consequence of the preceding lemma is that we can restrict the adversary’s decisions to , since choosing will not change the for any random strategy supported on . Thus for supported in , we have .

Discrete-Time Ski Rental

In the discrete-time ski rental (DSR) problem, a player faces a ski season of unknown and adversarially-chosen duration and must choose an integer number of days to rent skis before purchasing them; renting for a day costs , and purchasing skis has an integer cost . The cost structure is essentially identical to the continuous-time case, except the algorithm’s and adversary’s decisions are restricted to lie in : if a player buys skis at the start of day and the true season duration is , their cost will be . Thus for a random strategy with support on , the is defined as follows:

As in the continuous-time setting, we denote by the smallest of any strategy, and will omit the “DSR” from the superscript when it is clear from context, instead writing just . It is well known that , achieved by deterministically purchasing skis at the start of day , and , which approaches as . Following identical reasoning as in Lemma 4 for the continuous-time setting, we may without loss of generality restrict our focus to strategies with support on , and likewise to adversary decisions in . Finally, note that the discrete problem is easier than the continuous-time problem, i.e., for all and ; this is because we can embed DSR into the continuous setting by restricting the continuous-time adversary to choose season durations and reducing the player’s buying cost by .

One-Max Search

In the one-max search (OMS) problem, a player faces a sequence of prices arriving online, with known upper and lower bounds on the price sequence; we define the fluctuation ratio as the ratio between these bounds. The player’s goal is to sell an indivisible item for the greatest possible price: after observing a price , the player can choose to either accept the price and earn profit , or to wait and observe the next price. The duration of the sequence is a priori unknown to the player, and if elapses and the player has not yet sold the item, they sell it for the smallest possible price in a compulsory trade. In the deterministic setting, the player aims to minimize their competitive ratio, defined as the worst-case ratio between the price accepted by the player and the optimal price :

with an expectation around Alg in the denominator if the algorithm is randomized. Note that this definition of competitive ratio differs from that in Definition 2 because this is a reward maximization, rather than a loss minimization, problem. Likewise, when discussing the conditional value-at-risk and in this setting, we will use the reward formulation, which is the expected reward on the worst (i.e., smallest) -fraction of outcomes in the reward distribution [1]:

| (2) |

While these definitions of and differ from those employed in discussion of the ski rental problem, we will generally not distinguish which version we are using throughout this paper, as it will be clear from context which problem (and hence which version) we are concerned with.

The one-max search problem was first studied in [22], which found that the optimal deterministic competitive ratio is , achieved by a “reservation price” or “threshold” [55] algorithm that accepts the first price above . Randomization improves the competitive ratio exponentially: the optimal randomized competitive ratio is , where is the principal branch of the Lambert function [22, 38]. In this work, we restrict our focus to the class of random threshold algorithms without loss of generality;111This restriction is made without loss of generality, in the sense that any randomized algorithm for OMS with can be approximated by a random threshold policy with , with arbitrarily small; see Appendix A.2 for a full explanation. such algorithms fix a distribution with support on , draw a threshold at random, and accept the first price above , earning profit .222When the player uses a random threshold algorithm, we may assume that they earn profit exactly whenever , since if the adversary (who is unaware of ) plays a sequence of prices that increases by at every time until reaching , then the player will accept the first price above , which will be at most ; sending , the player’s profit is exactly . Thus the of a threshold algorithm is defined:

| (3) |

where we denote by the of one-max search with fluctuation ratio restricted to price sequences with maximal price , which is wholly determined by the distribution of the random threshold . As in the ski rental problems, we denote by the optimal for the problem, and we omit “OMS” from the superscript when the problem is clear from context.

3 -Competitive Continuous-Time Ski Rental:

Optimal Algorithm and Lower Bound

As noted in the previous section, the optimal deterministic competitive ratio for continuous-time ski rental is , and the optimal randomized competitive ratio is . This immediately motivates the question of what the optimal is, for arbitrary : how does grow as ? And does strictly improve on the deterministic worst case of 2 whenever ?

The classical approach for obtaining the optimal randomized algorithm for continuous-time ski rental is to assume that the optimal purchase distribution has a probability density supported on , use this to express the expected cost of the algorithm given any adversary decision, and write out the inequalities that must be satisfied for the algorithm to be -competitive for some constant [30]:

The optimal is found by setting these inequalities to equalities, differentiating with respect to , solving the resulting differential equations, and choosing to ensure integrates to . If we attempt to apply this methodology to the problem with the objective, we are met with two challenges: first, while the assumption that the optimal strategy has a density and the trick of setting the above inequalities to equalities works in the expected cost setting, there is no guarantee that these assumptions can be imposed without loss of generality when the expectation is replaced with . Second, and more formidably, even if we can restrict to densities, the limits of integration in the case will depend on the particular quantile structure induced by . If and , using the definition of as the expected cost on the worst -sized subpopulation of the loss, one can compute

whose lower limit of integration depends on ’s quantile structure in a nontrivial way (i.e., it is the smallest point with CDF value equal to ), significantly complicating the formulation of any differential equation we could construct using this expression.

Not all is lost, however: if we instead take inspiration from the formulation of in terms of the inverse CDF of the loss distribution, it is possible to formulate the of the loss of an arbitrary strategy (i.e., not necessarily one with a density) in terms of the inverse CDF of . We state this result formally in the following lemma, which is proved in Appendix B.1.

Lemma 5.

Let be a random variable supported in , and fix an adversary decision . Then the of the cost incurred by the algorithm playing is

While the integral representation of the algorithm’s cost given in Lemma 5 depends on both the CDF and the inverse CDF , it is possible to remove the CDF when it is continuous and strictly increasing on ; in this case, for any , we may define a corresponding and replace with and with in Lemma 5’s representation. We will show later that the optimal strategy indeed has such a continuous and strictly increasing (see Lemmas 20 and 21 in Appendix B.3).

As a first application of the representation for the -cost in Lemma 5, we construct in the following theorem a family of densities parametrized by whose we can compute analytically, giving an upper bound on , and in particular showing that for all .

Theorem 6.

Let be a probability density defined on the unit interval as

with constant , where is the branch of the Lambert function. Then the strategy that buys on day achieves competitive ratio

In particular, for all .

We present a proof of this theorem in Appendix B.2. Our approach is to compute the inverse CDF corresponding to the proposed density and reformulate the inequalities defining -competitiveness using Lemma 5; the rest of the work is concerned with computing .

Intuitively, the strategy in Theorem 6 behaves like one might expect a good algorithm for ski rental with the metric should: it assigns less probability mass to earlier times and more to later times, and as increases, it shifts mass from earlier times to later times. However, the algorithm cannot be optimal, since , which is larger – though only slightly – than the randomized optimal . This motivates the question: is it possible to leverage the representation in Lemma 5 to obtain the optimal algorithm for continuous-time ski rental with the objective? In the following theorem, we answer this question in the affirmative: in particular, the optimal algorithm’s inverse CDF is the solution to a delay differential equation defined on the interval .

Theorem 7.

For any , let be the solution to the delay differential equation

with initial condition on . Then when , is the inverse CDF of the unique optimal strategy for continuous-time ski rental with the metric.

We prove this theorem in Appendix B.3. The crux of the proof is a pair of structural lemmas (Lemmas 16 and 19) which establish that, for any , the optimal algorithm is indifferent to the adversary’s decision, i.e., for all . This is analogous to the trick of “setting the inequalities to equalities” in the classical version of ski rental [30], but requires a great deal more care in the continuous-time setting to make rigorous. In addition, this result depends on the fact that , which we showed in Theorem 6. With this property established, we can apply Lemma 5 to pose a family of integral equations constraining the optimal inverse CDF, which can be transformed to obtain the delay differential equation in Theorem 7.

Note, however, that the delay differential equation yielding the optimal inverse CDF depends on the optimal , which we have no analytic form for. Fortunately, the solution to the delay differential equation in Theorem 7 has the property that is strictly decreasing in for each (see Appendix B.4); since the optimal inverse CDF must have (see Lemma 21 in the appendix), is equivalently defined as the unique choice of for which the solution to the above delay differential equation satisfies . We may thus determine via binary search: given some , we solve the delay differential equation numerically and evaluate ; if , then we decrease , and if , we increase . We plot the optimal obtained via this binary search methodology (with delay differential equations solved numerically in Mathematica) alongside the upper bound from Theorem 6 in Figure 1.

While Theorem 7 gives us a method for computing the optimal strategy and for continuous-time ski rental, it does not give an analytic form of this solution or metric. An analytic form of can be obtained when , though its form is complicated and does not facilitate analysis of the optimal in this regime (see Appendix B.5). We thus conclude this section by providing a lower bound on , which we prove in Appendix B.6.

Theorem 8.

For any , the optimal has the lower bound

We plot this lower bound in Figure 1 alongside the upper bound from Theorem 6 and the optimal competitive ratio. While this lower bound is vacuous for , in which case it is exactly the expected cost lower bound of , it has the same asymptotic form as the upper bound in Theorem 6 as approaches . Thus, Theorems 6 and 8 together give us that , as .

4 -Competitive Discrete-Time Ski Rental:

Phase Transition and Analytic Optimal Algorithm

Having characterized the optimal algorithm and for continuous-time ski rental in the previous section, we now turn to the discrete-time version of the problem, and ask: are there any qualitative differences between the optimal algorithm or for the discrete problem and the continuous-time problem? And are there any regimes of for which we can analytically characterize the optimal algorithm? It turns out that the answer to both of these questions is yes; we begin by showing, in the following theorem, that the optimal for the discrete-time ski rental problem exhibits a phase transition at such that, for beyond this transition, the optimal algorithm is exactly the deterministic algorithm that buys at time .

Theorem 9.

Let be the optimal for discrete-time ski rental with buying cost . Then exhibits a phase transition at , whereby before this transition, strictly improves on the deterministic optimal of , whereas after this transition, . Specifically:

-

(i)

For all , the optimal is strictly bounded above by the deterministic optimal : (where as in Theorem 6).

-

(ii)

For all , the optimal is exactly the deterministic optimal : . Thus, the optimal algorithm for this regime purchases deterministically at time .

We prove this result in Appendix C.1; the proof of part (i) of follows essentially immediately from our analytic upper bound for the continuous setting (Theorem 6), and the proof of part (ii) is adapted from that for the continuous-time lower bound (Theorem 8) in order to handle the discrete nature of the problem. Note that this phase transition behavior is in sharp contrast to the behavior of the optimal and algorithm in the continuous time setting: whereas in continuous time, strictly improves on the deterministic optimal for all , in discrete time, is equal to the deterministic optimal for a non-degenerate interval of , implying a limit to the benefit of randomization in the risk-sensitive setting. In addition, this phase transition result gives an analytic solution for the algorithm with optimal when is sufficiently large; a natural, complementary question is whether it is possible to obtain an analytic solution for the optimal algorithm with smaller . We prove in the next theorem that such a solution can be obtained when .

Theorem 10.

Suppose . Then the optimal and strategy for discrete-time ski rental with buying cost are

where is the optimal competitive ratio for the case. In particular, is constant as a function of , and is identical to the optimal algorithm for the expected cost setting.

We prove this result in Appendix C.2; the proof follows a similar strategy to the proof characterizing the optimal strategy in the continuous-time setting, and in particular involves the proof of several technical lemmas that, similar to Lemmas 16 and 19 in the continuous-time setting, characterize the optimal algorithm via the adversary’s indifference to its chosen ski season duration. As a consequence of this theorem, we can analytically obtain the optimal algorithm for discrete-time ski rental with the objective whenever , and the corresponding is a rational function of . We anticipate that extensions of this result may be possible for larger , but in general the optimal will be a piecewise function of whose pieces, including the number of pieces and the intervals they are defined on, will depend on , so we leave the problem of characterizing the for all and general to future work. However, if computational results suffice, an adapted form of the binary search approach employed in [20, Appendix E] can be used in tandem with a linear programming formulation of the in order to approximate the optimal solution for any with .

5 -Competitive One-Max Search:

Asymptotically Optimal Algorithm and Phase Transition

We now turn our focus to the one-max search problem. As noted in Section 2, existing results for this problem in the deterministic and randomized settings have established that the optimal deterministic competitive ratio is and the optimal randomized competitive ratio is , where is the fluctuation ratio. We seek to obtain an upper bound on the for more general ; to this end, we prove a lemma that, in an analogous fashion to Lemma 5 for the continuous-time ski rental problem, leverages the integral form of the conditional value-at risk to let us express the -reward of a particular randomized threshold algorithm in terms of the inverse CDF of .

Lemma 11.

Let be a random variable supported in , and fix an adversary choice of the maximal price . Then the of the profit earned by the algorithm playing the random threshold is

We prove this lemma in Appendix D.1. While the representation of the of profit in this case differs substantially from the cost representation for ski rental in Lemma 5, it nonetheless also has a relatively simple parametrization in terms of the inverse CDF of the decision , which will facilitate algorithm design. This is due, in part, to the piecewise linear structure exhibited by the cost/profit in these problems, and we anticipate that extending our results to online problems with more general classes of piecewise linear costs and rewards may be a fruitful avenue for future work.

While the representation of the -reward in Lemma 11 depends on both the CDF and the inverse CDF of , we can eliminate the CDF so long as the maximal price . Using this fact, we prove the following theorem, proposing an algorithm and establishing an upper bound on the for all . We prove the result in Appendix D.2.

Theorem 12.

Let , and let be the solution to the following delay differential equation:

| (4) |

with initial condition on , where is chosen such that when , and when . Then is the inverse CDF of a random threshold algorithm for one-max search with . Moreover, is bounded above by the unique positive solution to the equation

| (5) |

where , with the case defined by taking . In particular,

| (6) |

with the equality when , where the asymptotic notation omits dependence on .

We make three brief remarks concerning this result. First, note that the proposed algorithm merely gives an upper bound on the of one-max search and might not be optimal, although its matches the optimal randomized and deterministic algorithms in the and cases. Second, when , it is possible to analytically solve the delay differential equation (4) by integrating step-by-step (see Appendix D.2):

| (7) |

When , (7) simplifies to , the optimal randomized algorithm [54]. On the other hand, when , all terms with disappear for , so is a continuous, piecewise polynomial function. In either case, is strictly increasing in , so the can be obtained numerically by solving via standard root-finding methods.

Finally, when , Theorem 12 asserts that , which is identical to the optimal deterministic competitive ratio. This raises the question: can any algorithm improve upon the deterministic bound when , or is this behavior reflective of a phase transition at such that randomness cannot improve performance when is greater than this level? In the following result, which we prove in Appendix D.3 by leveraging connections with the -max search problem [38], we provide a lower bound establishing that the latter case is true, and that moreover, the algorithm in Theorem 12 is asymptotically optimal for small .

Theorem 13.

Fix , let be the optimal for one-max search, and define to be the unique positive solution to the equation

| (8) |

where , with the case defined by taking . Then ; in particular,

| (9) |

where the asymptotic notation omits dependence on .

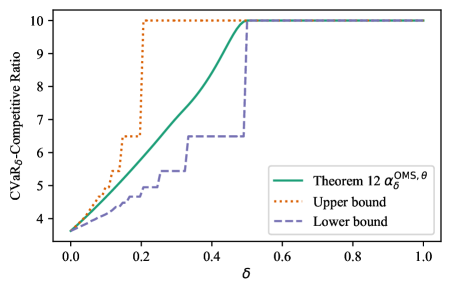

Thus, in contrast to the continuous-time ski rental problem, which exhibited no phase transition in its competitive ratio, and the discrete-time ski rental problem, which had a phase transition that shrank as , Theorem 13 establishes that the one-max search problem has a phase transition at that remains present even as . As such, there is a significant limit to the power of randomization in risk-sensitive one-max search. In addition, note that the form of the implicit lower bound (8) matches that of the upper bound (5), aside from the definitions of the functions and . This suggests that our upper and lower bounds are tight up to the choice of the function . In particular, this tightness is made clear in the analytic bounds (6) and (9) in the limit, which indicate that our algorithm is asymptotically optimal when is small. We plot the numerically obtained together with the upper and lower bounds (5) and (8) in Figure 2 when and , which confirms the near-tightness of the bounds and the phase transition at .

6 Conclusion

In this work, we considered the problem of designing risk-sensitive online algorithms, with performance evaluated via a competitive ratio metric – the – defined using the conditional value-at-risk of an algorithm’s cost. We considered the continuous- and discrete-time ski rental problems as well as the one-max search problem, obtaining optimal (and suboptimal) algorithms, lower bounds, and analytic characterizations of phase transitions in the optimal for discrete-time ski rental and one-max search. Our work motivates many interesting new directions, including (a) obtaining an exact or asymptotic analytic form of the optimal for discrete-time ski rental and one-max search across all , (b) the design and analysis of risk-sensitive algorithms for online problems with more general classes of cost and reward functions, or more complex problems such as metrical task systems, (c) exploring the use of alternative risk measures in place of the conditional value-at-risk, and (d) exploring potential connections between risk-sensitive online algorithms and robustness to distribution shift in learning-augmented online algorithms, drawing motivation from the framing of in terms of distribution shift.

7 Acknowledgments

The authors acknowledge support from an NSF Graduate Research Fellowship (DGE-2139433), NSF Grants CNS-2146814, CPS-2136197, CNS-2106403, and NGSDI-2105648, the Resnick Sustainability Institute, and a Caltech S2I Grant.

References

- Acerbi and Tasche [2002] Carlo Acerbi and Dirk Tasche. On the coherence of expected shortfall. Journal of Banking & Finance, 26(7):1487–1503, July 2002. ISSN 0378-4266. doi: 10.1016/S0378-4266(02)00283-2.

- Ahmadi et al. [2022] Mohamadreza Ahmadi, Xiaobin Xiong, and Aaron D. Ames. Risk-Averse Control via CVaR Barrier Functions: Application to Bipedal Robot Locomotion. IEEE Control Systems Letters, 6:878–883, 2022. ISSN 2475-1456. doi: 10.1109/LCSYS.2021.3086854.

- Antoniadis et al. [2021] Antonios Antoniadis, Christian Coester, Marek Elias, Adam Polak, and Bertrand Simon. Learning-Augmented Dynamic Power Management with Multiple States via New Ski Rental Bounds. In Advances in Neural Information Processing Systems, volume 34, pages 16714–16726. Curran Associates, Inc., 2021.

- Artzner et al. [1999] Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent Measures of Risk. Mathematical Finance, 9(3):203–228, July 1999. ISSN 0960-1627, 1467-9965. doi: 10.1111/1467-9965.00068.

- Aumann [1964] Robert J. Aumann. Mixed and behavior strategies in infinite extensive games. In Melvin Dresher, Lloyd S. Shapley, and Albert William Tucker, editors, Advances in Game Theory (AM-52), pages 627–650. Princeton University Press, Princeton, NJ, 1964.

- Bansal et al. [2015] Nikhil Bansal, Anupam Gupta, Ravishankar Krishnaswamy, Kirk Pruhs, Kevin Schewior, and Cliff Stein. A 2-Competitive Algorithm For Online Convex Optimization With Switching Costs. In Naveen Garg, Klaus Jansen, Anup Rao, and José D. P. Rolim, editors, Approximation, Randomization, and Combinatorial Optimization. Algorithms and Techniques (APPROX/RANDOM 2015), volume 40 of Leibniz International Proceedings in Informatics (LIPIcs), pages 96–109, Dagstuhl, Germany, 2015. Schloss Dagstuhl–Leibniz-Zentrum fuer Informatik. ISBN 978-3-939897-89-7. doi: 10.4230/LIPIcs.APPROX-RANDOM.2015.96.

- Baudry et al. [2021] Dorian Baudry, Romain Gautron, Emilie Kaufmann, and Odalric Maillard. Optimal Thompson Sampling strategies for support-aware CVaR bandits. In Proceedings of the 38th International Conference on Machine Learning, pages 716–726. PMLR, July 2021.

- Bellman and Cooke [1963] Richard Bellman and Kenneth Cooke. Differential-Difference Equations. RAND Corporation, Santa Monica, CA, 1963.

- Blum and Burch [1997] Avrim Blum and Carl Burch. On-line learning and the metrical task system problem. In Proceedings of the Tenth Annual Conference on Computational Learning Theory - COLT ’97, pages 45–53, Nashville, Tennessee, United States, 1997. ACM Press. ISBN 978-0-89791-891-6. doi: 10.1145/267460.267475.

- Böckenhauer et al. [2017] Hans-Joachim Böckenhauer, Dennis Komm, Rastislav Královič, Richard Královič, and Tobias Mömke. Online algorithms with advice: The tape model. Information and Computation, 254:59–83, June 2017. ISSN 0890-5401. doi: 10.1016/j.ic.2017.03.001.

- Borodin et al. [1992] Allan Borodin, Nathan Linial, and Michael E. Saks. An optimal on-line algorithm for metrical task system. Journal of the ACM, 39(4):745–763, October 1992. ISSN 0004-5411, 1557-735X. doi: 10.1145/146585.146588.

- Bubeck et al. [2021] Sébastien Bubeck, Michael B. Cohen, James R. Lee, and Yin Tat Lee. Metrical Task Systems on Trees via Mirror Descent and Unfair Gluing. SIAM Journal on Computing, 50(3):909–923, January 2021. ISSN 0097-5397, 1095-7111. doi: 10.1137/19M1237879.

- Buchbinder et al. [2012] Niv Buchbinder, Shahar Chen, Joshep (Seffi) Naor, and Ohad Shamir. Unified Algorithms for Online Learning and Competitive Analysis. In Proceedings of the 25th Annual Conference on Learning Theory, pages 5.1–5.18. JMLR Workshop and Conference Proceedings, June 2012.

- Chi and Tan [2011] Yichun Chi and Ken Seng Tan. Optimal Reinsurance under VaR and CVaR Risk Measures: A Simplified Approach. ASTIN Bulletin: The Journal of the IAA, 41(2):487–509, November 2011. ISSN 0515-0361, 1783-1350. doi: 10.2143/AST.41.2.2136986.

- Chow and Ghavamzadeh [2014] Yinlam Chow and Mohammad Ghavamzadeh. Algorithms for CVaR Optimization in MDPs. In Advances in Neural Information Processing Systems, volume 27. Curran Associates, Inc., 2014.

- Chow et al. [2015] Yinlam Chow, Aviv Tamar, Shie Mannor, and Marco Pavone. Risk-Sensitive and Robust Decision-Making: A CVaR Optimization Approach. In Advances in Neural Information Processing Systems, volume 28. Curran Associates, Inc., 2015.

- Christianson et al. [2023] Nicolas Christianson, Junxuan Shen, and Adam Wierman. Optimal robustness-consistency tradeoffs for learning-augmented metrical task systems. In Proceedings of The 26th International Conference on Artificial Intelligence and Statistics, pages 9377–9399. PMLR, April 2023.

- Corless et al. [1996] R. M. Corless, G. H. Gonnet, D. E. G. Hare, D. J. Jeffrey, and D. E. Knuth. On the Lambert W function. Advances in Computational Mathematics, 5(1):329–359, December 1996. ISSN 1019-7168, 1572-9044. doi: 10.1007/BF02124750.

- Daniely and Mansour [2019] Amit Daniely and Yishay Mansour. Competitive ratio vs regret minimization: Achieving the best of both worlds. In Proceedings of the 30th International Conference on Algorithmic Learning Theory, pages 333–368. PMLR, March 2019.

- Dinitz et al. [2024] Michael Dinitz, Sungjin Im, Thomas Lavastida, Benjamin Moseley, and Sergei Vassilvitskii. Controlling Tail Risk in Online Ski-Rental. In Proceedings of the 2024 Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), pages 4247–4263, 2024. doi: 10.1137/1.9781611977912.147.

- Duchi and Namkoong [2021] John C. Duchi and Hongseok Namkoong. Learning models with uniform performance via distributionally robust optimization. The Annals of Statistics, 49(3), June 2021. ISSN 0090-5364. doi: 10.1214/20-AOS2004.

- El-Yaniv et al. [2001] R. El-Yaniv, A. Fiat, R. M. Karp, and G. Turpin. Optimal Search and One-Way Trading Online Algorithms. Algorithmica, 30(1):101–139, May 2001. ISSN 1432-0541. doi: 10.1007/s00453-001-0003-0.

- Emek et al. [2011] Yuval Emek, Pierre Fraigniaud, Amos Korman, and Adi Rosén. Online computation with advice. Theoretical Computer Science, 412(24):2642–2656, May 2011. ISSN 0304-3975. doi: 10.1016/j.tcs.2010.08.007.

- Even-Dar et al. [2006] Eyal Even-Dar, Michael Kearns, and Jennifer Wortman. Risk-Sensitive Online Learning. In José L. Balcázar, Philip M. Long, and Frank Stephan, editors, Algorithmic Learning Theory, pages 199–213, Berlin, Heidelberg, 2006. Springer. doi: 10.1007/11894841˙18.

- Geulen et al. [2010] Sascha Geulen, Berthold Vocking, and Melanie Winkler. Regret Minimization for Online Buffering Problems Using the Weighted Majority Algorithm. In 23rd Annual Conference on Learning Theory, 2010.

- Haghtalab et al. [2022] Nika Haghtalab, Tim Roughgarden, and Abhishek Shetty. Smoothed Analysis with Adaptive Adversaries. In 2021 IEEE 62nd Annual Symposium on Foundations of Computer Science (FOCS), pages 942–953, February 2022. doi: 10.1109/FOCS52979.2021.00095.

- Hakobyan et al. [2019] Astghik Hakobyan, Gyeong Chan Kim, and Insoon Yang. Risk-Aware Motion Planning and Control Using CVaR-Constrained Optimization. IEEE Robotics and Automation Letters, 4(4):3924–3931, October 2019. ISSN 2377-3766, 2377-3774. doi: 10.1109/LRA.2019.2929980.

- Hathaway [2011] Dan Hathaway. Using Continuity Induction. The College Mathematics Journal, 42(3):229–231, May 2011. ISSN 0746-8342, 1931-1346. doi: 10.4169/college.math.j.42.3.229.

- Jia and Dyer [1996] Jianmin Jia and James S. Dyer. A Standard Measure of Risk and Risk-Value Models. Management Science, 42(12):1691–1705, 1996. ISSN 0025-1909.

- Karlin et al. [1994] A. R. Karlin, M. S. Manasse, L. A. McGeoch, and S. Owicki. Competitive randomized algorithms for nonuniform problems. Algorithmica, 11(6):542–571, June 1994. ISSN 0178-4617, 1432-0541. doi: 10.1007/BF01189993.

- Karlin et al. [1988] Anna R. Karlin, Mark S. Manasse, Larry Rudolph, and Daniel D. Sleator. Competitive snoopy caching. Algorithmica, 3(1):79–119, November 1988. ISSN 1432-0541. doi: 10.1007/BF01762111.

- Karlin et al. [2001] Anna R. Karlin, Claire Kenyon, and Dana Randall. Dynamic TCP acknowledgement and other stories about e/(e-1). In Proceedings of the Thirty-Third Annual ACM Symposium on Theory of Computing, STOC ’01, pages 502–509, New York, NY, USA, July 2001. Association for Computing Machinery. ISBN 978-1-58113-349-3. doi: 10.1145/380752.380845.

- Keramati et al. [2020] Ramtin Keramati, Christoph Dann, Alex Tamkin, and Emma Brunskill. Being Optimistic to Be Conservative: Quickly Learning a CVaR Policy. Proceedings of the AAAI Conference on Artificial Intelligence, 34(04):4436–4443, April 2020. ISSN 2374-3468, 2159-5399. doi: 10.1609/aaai.v34i04.5870.

- Komm et al. [2022] Dennis Komm, Rastislav Královič, Richard Královič, and Tobias Mömke. Randomized Online Computation with High Probability Guarantees. Algorithmica, 84(5):1357–1384, May 2022. ISSN 1432-0541. doi: 10.1007/s00453-022-00925-z.

- Krokhmal et al. [2001] Pavlo Krokhmal, Tanislav Uryasev, and Jonas Palmquist. Portfolio optimization with conditional value-at-risk objective and constraints. The Journal of Risk, 4(2):43–68, March 2001. ISSN 14651211. doi: 10.21314/JOR.2002.057.

- Lechowicz et al. [2024] Adam Lechowicz, Nicolas Christianson, Bo Sun, Noman Bashir, Mohammad Hajiesmaili, Adam Wierman, and Prashant Shenoy. Online Conversion with Switching Costs: Robust and Learning-Augmented Algorithms, January 2024. arXiv:2310.20598.

- Lin et al. [2019] Qiulin Lin, Hanling Yi, John Pang, Minghua Chen, Adam Wierman, Michael Honig, and Yuanzhang Xiao. Competitive Online Optimization under Inventory Constraints. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 3(1):10:1–10:28, March 2019. doi: 10.1145/3322205.3311081.

- Lorenz et al. [2009] Julian Lorenz, Konstantinos Panagiotou, and Angelika Steger. Optimal Algorithms for k-Search with Application in Option Pricing. Algorithmica, 55(2):311–328, October 2009. ISSN 1432-0541. doi: 10.1007/s00453-008-9217-8.

- Lykouris and Vassilvtiskii [2018] Thodoris Lykouris and Sergei Vassilvtiskii. Competitive Caching with Machine Learned Advice. In Proceedings of the 35th International Conference on Machine Learning, pages 3296–3305. PMLR, July 2018.

- Madavan et al. [2024] Avinash N. Madavan, Nathan Dahlin, Subhonmesh Bose, and Lang Tong. Risk-Based Hosting Capacity Analysis in Distribution Systems. IEEE Transactions on Power Systems, 39(1):355–365, January 2024. ISSN 1558-0679. doi: 10.1109/TPWRS.2023.3238846.

- Mafusalov et al. [2018] Alexander Mafusalov, Alexander Shapiro, and Stan Uryasev. Estimation and asymptotics for buffered probability of exceedance. European Journal of Operational Research, 270(3):826–836, November 2018. ISSN 03772217. doi: 10.1016/j.ejor.2018.01.021.

- Markowitz [1959] Harry M. Markowitz. Portfolio Selection: Efficient Diversification of Investments. Yale University Press, 1959. ISBN 978-0-300-01372-6.

- [43] Claire Mathieu. Online algorithms: Ski rental. https://cs.brown.edu/~claire/Talks/skirental.pdf.

- Mitrinović et al. [1993] D. S. Mitrinović, J. E. Pečarić, and A. M. Fink. Classical and New Inequalities in Analysis. Springer Netherlands, Dordrecht, 1993. ISBN 978-90-481-4225-5 978-94-017-1043-5. doi: 10.1007/978-94-017-1043-5.

- Ndrio et al. [2021] Mariola Ndrio, Avinash N. Madavan, and Subhonmesh Bose. Pricing Conditional Value at Risk-Sensitive Economic Dispatch. In 2021 IEEE Power & Energy Society General Meeting (PESGM), pages 01–05, Washington, DC, USA, July 2021. IEEE. ISBN 978-1-66540-507-2. doi: 10.1109/PESGM46819.2021.9637845.

- Pratt [1964] John W. Pratt. Risk Aversion in the Small and in the Large. Econometrica, 32(1/2):122–136, 1964. ISSN 0012-9682. doi: 10.2307/1913738.

- Purohit et al. [2018] Manish Purohit, Zoya Svitkina, and Ravi Kumar. Improving Online Algorithms via ML Predictions. In Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc., 2018.

- Rockafellar and Uryasev [2000] R. Tyrrell Rockafellar and Stanislav Uryasev. Optimization of conditional value-at-risk. The Journal of Risk, 2(3):21–41, 2000. ISSN 14651211. doi: 10.21314/JOR.2000.038.

- Rockafellar and Uryasev [2002] R. Tyrrell Rockafellar and Stanislav Uryasev. Conditional value-at-risk for general loss distributions. Journal of Banking & Finance, 26(7):1443–1471, July 2002. ISSN 0378-4266. doi: 10.1016/S0378-4266(02)00271-6.

- Sarykalin et al. [2008] Sergey Sarykalin, Gaia Serraino, and Stan Uryasev. Value-at-Risk vs. Conditional Value-at-Risk in Risk Management and Optimization. In Zhi-Long Chen, S. Raghavan, Paul Gray, and Harvey J. Greenberg, editors, State-of-the-Art Decision-Making Tools in the Information-Intensive Age, pages 270–294. INFORMS, September 2008. ISBN 978-1-877640-23-0. doi: 10.1287/educ.1080.0052.

- Schäfer and Sivadasan [2004] Guido Schäfer and Naveen Sivadasan. Topology Matters: Smoothed Competitiveness of Metrical Task Systems. In Volker Diekert and Michel Habib, editors, STACS 2004, Lecture Notes in Computer Science, pages 489–500, Berlin, Heidelberg, 2004. Springer. ISBN 978-3-540-24749-4. doi: 10.1007/978-3-540-24749-4˙43.

- Shapiro et al. [2009] Alexander Shapiro, Darinka Dentcheva, and Andrzej Ruszczyński. Lectures on Stochastic Programming: Modeling and Theory. Society for Industrial and Applied Mathematics, January 2009. ISBN 978-0-89871-687-0 978-0-89871-875-1. doi: 10.1137/1.9780898718751.

- Soma and Yoshida [2023] Tasuku Soma and Yuichi Yoshida. Online risk-averse submodular maximization. Annals of Operations Research, 320(1):393–414, January 2023. ISSN 1572-9338. doi: 10.1007/s10479-022-04835-9.

- Sun et al. [2020] Bo Sun, Ali Zeynali, Tongxin Li, Mohammad Hajiesmaili, Adam Wierman, and Danny H.K. Tsang. Competitive Algorithms for the Online Multiple Knapsack Problem with Application to Electric Vehicle Charging. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 4(3):1–32, November 2020. ISSN 2476-1249. doi: 10.1145/3428336.

- Sun et al. [2021] Bo Sun, Russell Lee, Mohammad Hajiesmaili, Adam Wierman, and Danny Tsang. Pareto-Optimal Learning-Augmented Algorithms for Online Conversion Problems. In Advances in Neural Information Processing Systems, volume 34, pages 10339–10350. Curran Associates, Inc., 2021.

- Szegö [2002] Giorgio Szegö. Measures of risk. Journal of Banking & Finance, 26(7):1253–1272, July 2002. ISSN 0378-4266. doi: 10.1016/S0378-4266(02)00262-5.

- Tamkin et al. [2019] Alex Tamkin, Christoph Dann, Ramtin Keramati, and Emma Brunskill. Distributionally-Aware Exploration for CVaR Bandits. In NeurIPS 2019 Workshop on Safety and Robustness on Decision Making, 2019.

- Uziel and El-Yaniv [2018] Guy Uziel and Ran El-Yaniv. Growth-Optimal Portfolio Selection under CVaR Constraints. In Proceedings of the Twenty-First International Conference on Artificial Intelligence and Statistics, pages 48–57. PMLR, March 2018.

- Witting [1985] Hermann Witting. Mathematische Statistik I. Vieweg+Teubner Verlag, Wiesbaden, 1985. ISBN 978-3-322-90151-4 978-3-322-90150-7. doi: 10.1007/978-3-322-90150-7.

- Zhang and Conitzer [2020] Hanrui Zhang and Vincent Conitzer. Combinatorial Ski Rental and Online Bipartite Matching. In Proceedings of the 21st ACM Conference on Economics and Computation, pages 879–910, Virtual Event Hungary, July 2020. ACM. ISBN 978-1-4503-7975-5. doi: 10.1145/3391403.3399470.

Appendix A Additional Details for Section 2

A.1 Proof of Lemma 4

Let , and define another random variable with support on as

Suppose . Clearly and , and since when , for . Thus

| (10) |

Now, consider the case . By construction, , so and , and thus

| (11) | ||||

| (12) |

where (11) uses translation invariance of . On the other hand, we have

| (13) | ||||

| (14) | ||||

| (15) |

where (13) follows by monotonicity of , (14) follows by translation invariance, and (15) follows by monotonicity when (in which case ). Combining (10), (12), and (15), we obtain , as claimed.

A.2 On the Restriction to Random Threshold Policies

In this section, we briefly justify the claim that the restriction to random threshold policies for one-max search is made without loss of generality. Let Alg be an arbitrary randomized algorithm for one-max search. Following the argument in the proof of [22, Theorem 1], the lack of memory restrictions in this problem implies, by Kuhn’s Theorem, that Alg is, without loss of generality, a mixed strategy, or a probability distribution over deterministic algorithms [5]. For some , let , and define a restricted set of adversary price sequences as

i.e., is the set of all price sequences that begin at and increase by at each time. If the adversary is restricted to choosing price sequences in , then any deterministic algorithm is equivalent in behavior to some deterministic threshold algorithm. To see why, note that comprises price sequences, each of a unique length in ; we will call the sequence of length . Moreover, constitutes the first entries of . As such, the behavior of a deterministic algorithm on will be identical to its behavior on the first prices revealed in ; in particular, if sells at time in , it will do the same in and earn the same profit . As a result, ’s behavior on is wholly determined by the price at which it chooses to sell, which will be consistent across price sequences in this set; in other words, is equivalent to a deterministic threshold algorithm, with threshold chosen amongst the choices .333If never sells on any of the sequences in , we can choose a corresponding deterministic threshold of , which obtains performance at least as good. Thus, on , the mixed strategy Alg is equivalent to a distribution over such threshold algorithms, i.e., a random threshold algorithm with support on . Formally, we have

| (16) |

where denotes the (random) profit of Alg on the price sequence , , and (16) holds by the construction of . Then since is a random threshold algorithm, its (with unrestricted adversary) is defined as in (3):

| (17) | ||||

| (18) | ||||

| (19) |

where the inequality (17) holds due to having support restricted to , which implies that is equal to the case for all , (18) follows by the fact that the algorithm’s profit is lower bounded by , and (19) follows by the inequality in (16). Thus, by selecting arbitrarily large (i.e., arbitrarily small), the random threshold algorithm can be made to have arbitrarily close to the original randomized algorithm Alg.

Appendix B Proofs and Additional Results for Section 3

B.1 Proof of Lemma 5

Before proving the result, we first prove a general lemma that allows for writing an algorithm’s -cost given a particular adversary’s decision in terms of the inverse CDF of the algorithm’s decision.

Lemma 14.

Let be a random variable supported in , and fix an adversary’s decision . Then the inverse CDF of the ski rental cost given by the random variable is

for .

Proof Observe that the cost takes value when , and is equal to otherwise, which is always at least ; as such, we can easily compute its CDF:

Note that is supported in ; thus, we define its inverse CDF as

just as claimed.

Lemma 5 now follows as a near-immediate consequence of the preceding lemma.

Proof of Lemma 5 Define as the algorithm’s cost given a strategy and adversary’s decision , just as in Lemma 14. By the second definition of in (1) expressing it as an integral of the inverse CDF, we may write as:

We break into two cases. If , then by Lemma 14, on the entire domain of integration, so we have

On the other hand, if , then by Lemma 14, on and on . Thus,

B.2 Proof of Theorem 6

First, note that the CDF of the strategy on is

which is strictly increasing (and hence one-to-one) on , with and . The corresponding inverse CDF is

for . This is strictly increasing in , so is one-to-one, and any adversary decision corresponds to some such that .

Now suppose the adversary’s decision is for . Then by Lemma 5, the the of the algorithm’s cost in this case is

| (20) | ||||

| (21) |

where the final inequality (21) follows from the straightforward observation that (20) is increasing in , so is maximized in this case at (recall we have assumed ).

Now, consider the alternative case that . By Lemma 5, the the of the algorithm’s cost in this case is

| (22) | ||||

| (23) |

where the final inequality (23) follows from the fact that (22) is increasing in , and thus is maximized for (recall that in this case). To see that this is the case, observe that

| (24) | ||||

where (24) follows by the assumption in the theorem statement that , since if we substitute this definition of into , we obtain

| (25) |

since the Lambert function is defined to satisfy .

Combining the two cases (21) and (23), we have that the of the algorithm that buys on a random day with density is

| (26) |

We will now show that for our chosen constant , the latter entry in the maximum is larger for all . Define a function as the difference of (23) and (21):

Our goal is to show that for all . First, observe that . Moreover, since , we have

where the final equality follows from rearranging the equality shown in (25), which follows from our choice of . Thus the function is zero at the endpoints of the interval . Since is continuously differentiable, if we can show that and that exactly once on the interval , these together will imply the desired property that for all .444To see that this is the case, suppose instead that for some , and note that strict positivity of the initial derivative , continuity of , and the limit imply that must be zero at least twice on the interval, contradicting the supposition that exactly once.

Computing the derivative of at , we find

| (27) | ||||

| (28) | ||||

where (28) follows from (25). Moreover, inspecting the form of (27), it is clear that and the denominator are both strictly positive (recall, in particular, that ). As such, the sign of is exactly the sign of , so to determine the zeros of , we may instead determine the zeros of the expression

To this end, we compute another derivative:

for all , since . As

and

it follows that , and thus , has exactly one zero on . As argued previously, this implies that for all , and hence the second entry on the right-hand side of (26) is always larger:

Simplifying this formula via (25), we have

from which it is readily observed that for all ; moreover, , so the above expression for is valid, and indeed optimal, in the case of (in this case, we interpret the algorithm as placing full probability mass on purchasing at time 1). On the other hand, , so this algorithm is not optimal for all , though it provides a very close approximation of the optimal competitive ratio in the case of .

B.3 Proof of Theorem 7

It is known that the optimal ski-rental algorithm is indifferent to the adversary’s decision when (in the expected cost case), i.e., for all [30]. A similar tightness property was proved in [20] in the setting of discrete-time ski rental with constraints. In the following, we show that this tightness property also holds for any for continuous-time ski rental: if is optimal for the , then for all . Following the high-level strategy of [20], we prove this result in two steps: first, we prove that . Then, we prove that for any algorithm , if for some , we can construct an algorithm with a competitive ratio that is no worse than , yet which has , thus implying is not optimal. We begin with a lemma establishing that any optimal algorithm cannot have a probability mass more than on any single point.

Lemma 15.

Let , and let be an algorithm with optimal for continuous-time ski rental. Then cannot assign any point a probability mass greater than .

Proof By Lemma 4 we can assume that has support in ; now suppose for the sake of contradiction that for some . We can easily construct a lower bound on the as follows:

where the final inequality follows since is decreasing in and . Since was assumed optimal, this strict inequality clearly yields a contradiction.

We conclude by briefly noting that , since by Theorem 6, for any .

Now, we prove that the competitive ratio must be tight when .

Lemma 16.

Let , and let be an algorithm with optimal for continuous-time ski rental, so . Then .

Proof Suppose otherwise, and let for some . Note that by Lemma 15, cannot place a probability mass greater than on any single point, which is strictly less than by the fact that for (Theorem 6). In particular, this implies that does not assign all its probability to the decision , and decreasing the probability mass assigned to a particular decision and moving it to an earlier decision will strictly decrease the at that decision.

Now, consider another algorithm with measure defined as:

with a small constant and where is a unit point mass at . For any , one of the following two cases must hold:

-

(a)

Suppose . This means that the worst -sized subpopulation of the loss distribution (i.e., the distribution of the random variable ) is contained in the event , so it must be that takes values at most with probability zero, i.e., . Likewise, we must have , so as well.

-

(b)

Alternatively, let . This means that . We break into two subcases:

(i) If , then the worst -sized subpopulation of the loss distribution must yield a loss of with probability ; hence we may write

Let be independent of , and define as a random variable that is equal to when and is 1 otherwise; clearly has distribution . Then since , we similarly obtain

(29) (30) (31) where (29) holds since, by construction, implies ; (30) follows from the fact that the event is exactly the joint event and is independent of ; and (31) is a consequence of and for .

(ii) If , then the worst -sized subpopulation of the loss distribution is wholly induced by outcomes of lying in the interval ; calling this subpopulation distribution of , we have . This subpopulation shrinks to size in the construction of , so in order to construct the worst-case -sized loss subpopulation of , we must augment with an additional loss subpopulation (call it ) with size . It must hold that some nontrivial portion of the losses included in are strictly less than , for if this were not the case, it would imply that contains a probability atom of size , violating optimality. Thus, we may calculate:

(32) where (32) follows from a nontrivial portion of the losses in being strictly less than .

Finally, consider the case of . In this case, the loss is always , since without loss of generality (Lemma 4); since this is strictly increasing in the outcome of , the worst -sized subpopulation of the loss distribution is exactly the tail of , which we call . This tail shrinks to size in the construction of , but an additional probability mass of weight is added to the outcome , and as this outcome maximizes the loss, the worst -sized subpopulation of the loss under is easily seen to be . Thus, if we choose ,

It follows from the above cases that : for satisfying case (a), , and in case (b) and the case of , we have shown . However, this implies that has strictly better than , contradicting the optimality of . As a result, we must have .

We will now begin to prove the second structural result: that if for some , we can construct an algorithm with that is no worse than and for which , which by the previous lemma implies that is not optimal. We will first prove a series of technical lemmas that support this proof: the first tells us that, if there is “slack” in the for a given adversary decision , then this implies that there is slack of a comparable magnitude in a small interval .

Lemma 17.

Let , and let be an algorithm for continuous-time ski rental with support in . Suppose there exists an for which , and define . Then there exists some such that for any , .

Proof When , is exactly the expectation, so we have:

| (33) |

which is easily seen to be right-continuous at , by right-continuity of the CDF. Thus there must exist some ensuring for all , which implies the desired property.

On the other hand, suppose . We can choose sufficiently small such that (this is always possible due to right-continuity of ). Defining the algorithm’s cost given an adversary decision as , we have

| (34) |

Now, applying Lemma 14, we can bound each of the two integrals in (34). For the first integral, there are two cases according to the two cases in Lemma 14: if , then on the domain of integration, so we have

where the final equality follows by Lemma 5. Dividing both sides by , we obtain

| (35) |

since implies . Similarly, if , the value of depends on which part of the domain of integration contains :

Dividing both sides by , we obtain

| (36) |

where the final step is a consequence of Lemma 5; note this exactly matches the bound (35) in the first case. For the second integral in (34), since , we have , so by Lemma 14 we may calculate

| (37) | ||||

| (38) |

where the bound (37) follows by monotonicity of the inverse CDF, and (38) is from the well-known bound (e.g., [59, Lemma 1.17f]).

Inserting (35), (36), and (38) into (34), we obtain the bound

| (39) |

Right-continuity of the CDF ensures that the right-hand side of (39) can be made at most by choosing sufficiently small, thus establishing the result.

The second technical lemma we will need to prove the structural result asserts that if comes from a distribution with a probability atom at , then there is a non-degenerate interval of slack in the . The assumed bound on the size of the probability atom is made without loss of generality due to Lemma 15, since we solely focus on the optimal algorithm.

Lemma 18.

Fix , and let be a random variable supported in with a probability atom of mass at some . Then there is some and such that for all .

Proof Let us assume that there exists an such that ; the alternative case follows from an essentially identical argument. Then by Lemma 5,

| (40) | ||||

where (40) follows by taking the limit and by the assumption . The final inequality follows from on , along with the fact that on , which implies that the integrand of the second integral in (40) is strictly less than the first integrand (which is ), as . This strict inequality holds in the limit, so there exists some for which ; that this holds in the limit implies that there is some such that for all , as desired.

We are now prepared to prove the structural result establishing that the optimal algorithm has that is independent of the adversary’s choice of season duration .

Lemma 19.

Let , and let be an algorithm with optimal for continuous-time ski rental, so . Then for all .

Proof Suppose for the sake of contradiction that for some . We will construct another algorithm with and , which by Lemma 16 immediately implies that , and therefore , is not optimal. In the following proof, we will say that has “slack” at when .

Define . If and , clearly by Lemma 16 we’re done. On the other hand, if , we must have by the supremum definition of and Lemma 17. Thus, we may proceed assuming that and . Note that the interval , if it is nonempty, cannot contain any probability atoms, by Lemma 18 and the definition of .

We will now proceed to prove the result in two parts. First, we will show that we can construct a distribution with no worse than that has slack at , i.e., . Then, we will show that we can construct new distributions iteratively propagating this slack toward , eventually culminating with the desired with and .

Part (1): Obtaining slack at

We break into two cases depending on whether has a probability atom at .

-

(a)

Suppose has a probability atom at of size ; by Lemma 15, must be bounded as

Then by Lemma 18, there is an and such that for all . Define a measure from by moving a small amount of mass from to ; it can easily be seen that this will not change for , it will strictly decrease due to shifting of its mass to an action with a smaller cost, and similarly it will either decrease or not affect for . Note that Lemma 15’s bound on ’s size is crucial to obtain that strictly decreases, since if were larger than , decreasing its mass by a small amount might not change the at .

On the interval , the will increase, but at most by , which by choosing small can be kept sufficiently small that remains true for all . To see this, note that this movement of mass increases by on the interval ; as a result, on the interval , will decrease to . That is, will have inverse CDF of the form

(41) Assuming that (the alternative case proceeds similarly), we may compute, using Lemma 5:

implying that . Similarly, for any with (any others are not impacted by this change), we can obtain an analogous bound:

implying that . Note that these bounds are coarse, and intuitively capture the idea that if we introduce a new point mass of size within the support of the worst-case loss subpopulation distribution realizing the , the worst that this added loss can do is increase the in proportion to the loss value that it adds, weighted by its probability normalized by . Thus, it is clear that by selecting sufficiently small, we can guarantee that for all , while we have still strictly decreased by moving some of its mass to an earlier decision, thus introducing slack at .

-

(b)

Suppose that does not have a point mass at ; thus, is continuous at . We break into two further cases:

-

(i)

Suppose that there is some such that has a point mass at and

By the argument in part (a), we can construct a measure by moving some small amount of mass from to for some , which will not impact for , will increase it in a controlled manner (such that we can maintain slack by choosing sufficiently small) for , and will strictly decrease it for . We can choose sufficiently small that , by the strict inequality in the limit assumed above. Moreover, this modification will also strictly decrease for . In particular, for we have, using the inverse CDF expression (41) and Lemma 5,

where the strict inequality results from being strictly decreased on the domain

and the choice of satisfying . In the above derivation we have assumed that ; the alternative case proceeds similarly.Thus, if the worst fraction of loss outcomes when the adversary chooses contains decisions (of positive probability) from a non-degenerate set , and has a probability atom, we have that introducing slack at in turn introduces slack at .

-

(ii)

Suppose that has no point mass at any satisfying the property that and

. This implies that there must be a small interval to the left of on which is continuous, since must increase from to without any discontinuities. There thus must exist, by the supremum definition of , some at which is continuous, , and . Continuity of the on this subinterval, and the bound (39) in particular, imply that there is some non-degenerate interval and such that for all . By the assumption that while there are no point masses on the interval , the bound (39) in particular tells us that we can choose such that the half-open interval has strictly positive measure. Then suppose we move a small fraction of the probability mass on to . By the same basic argument as employed previously, this will not affect the for , and if we choose small enough, it will increase for in a controlled fashion so that we can keep . Moreover, by the assumption , will strictly decrease, just as it did in the previous subcase. Thus, we can introduce slack at while not increasing the .

-

(i)

Having obtained a measure with a not worse than and with slack at , we now proceed to the second part.

Part (2): Obtaining slack at

If , we are done; otherwise, recall that by definition cannot have any probability atoms, since this would introduce slack in the interval by Lemma 18, so is continuous on (note that at itself, it may only be right-continuous). The argument employed to obtain slack at follows an iterated form of the approach in case (b.ii) from part 1: Because has slack at , the bound (39) implies that it has slack in an interval with the property that . Then we may transfer a fraction of the probability mass on to , and as long as is chosen sufficiently small, this will increase for while maintaining slack, and it will strictly decrease for all such that (note we can choose so that this set of is nonempty). Thus we can “propagate” the slack in the to decisions whose CDF value is up to greater than that of the original slack point, , without increasing the of the algorithm. Iteratively applying this construction at most times, we eventually obtain an algorithm with no worse than , and with slack at : .

Using the structural characterization of the optimal algorithm in terms of its ’s indifference to the adversary’s choice of ski season duration, we may now prove that the optimal algorithm has a CDF that is both strictly increasing and continuous (i.e., one-to-one) on the interval .

Lemma 20.

Fix , and let be a random variable yielding the optimal for continuous-time ski rental, i.e., . Then is strictly increasing on .

Proof When , this is an immediate consequence of the strict inequality (39) in the proof of Lemma 17: if weren’t strictly increasing, there would exist a non-degenerate interval with for all , which by (39) would imply that for some small , contradicting (via Lemma 19) the optimality of . Likewise, in the case, not strictly increasing means for all sufficiently small , so the expression (33) in the proof of Lemma 17 implies that will strictly decrease for some small interval starting at , again contradicting the optimality of by Lemma 19.

Lemma 21.

Fix , and let be a random variable yielding the optimal for continuous-time ski rental, i.e., . Then is continuous on , , and .