Stability via resampling: statistical problems beyond the real line

Abstract

Model averaging techniques based on resampling methods (such as bootstrapping or subsampling) have been utilized across many areas of statistics, often with the explicit goal of promoting stability in the resulting output. We provide a general, finite-sample theoretical result guaranteeing the stability of bagging when applied to algorithms that return outputs in a general space, so that the output is not necessarily a real-valued—for example, an algorithm that estimates a vector of weights or a density function. We empirically assess the stability of bagging on synthetic and real-world data for a range of problem settings, including causal inference, nonparametric regression, and Bayesian model selection.

1 Introduction

Statistical stability holds when our conclusions, estimates, fitted models, predictions, or decisions are insensitive to small perturbations of data. Stability is a pillar of modern data science (Yu and Kumbier, 2020). Nonparametric tools for statistical inference—e.g. the bootstrap, subsampling, the Jackknife—perturb data to assess variability and can thus be viewed as aspects of stability analysis (Yu, 2013). While assessing stability is in general statistically intractable without placing assumptions on the data (Kim and Barber, 2023), these resampling-based approaches can also be used to reduce the issue of instability: for instance, Breiman (1996a, b) originally proposed bagging—which applies bootstrap resampling to construct an ensemble of machine learning models—as an off-the-shelf stabilizer for regression and classification. In this paper, we show how bagging can be used to stabilize statistical methods far beyond its origins in supervised learning problems.

1.1 Problem settings

We begin by highlighting some specific statistical problems where provably stable methods are desirable.

Problem setting 1 (background): the supervised learning setting

In the supervised learning setting, we are given a labeled data set and are tasked with constructing a regression function to predict given for new data points. Many modern methods from the recent machine learning literature offer powerful predictive performance, but suffer from high sensitivity to the training data, where a prediction (at a new test point ) may vary immensely if the training data is perturbed slightly. Interestingly, both high accuracy and poor stability can often be a consequence of working with highly overparameterized models.

Suppose that the response is real-valued, so that our regression functions take values in , i.e., . Recent work by Soloff et al. (2024) establishes that bagging the predictive model—that is, re-fitting on bootstrapped training sets, and then returning the averaged prediction—yields an assumption-free guarantee on the stability of the prediction .

While Soloff et al. (2024)’s work is presented as a result for supervised learning, it can be viewed more generally as a guarantee of stability for any algorithm that is trained on data and returns a real-valued output. But even with this generalization, this result only covers a very specific statistical scenario. For many statistical problems, we might be interested in the stability of a procedure that returns a more complex object, such as a function or a vector of weights, rather than a real-valued output.

Problem setting 2: reproducible Bayesian inference

In Bayesian data analysis, given a data set containing observations drawn from some distribution , we are interested in the posterior distribution of the parameter . For instance, might represent a particular model from a finite set of possibilities, in which case the posterior distribution on is simply a vector of weights on this finite set. Alternatively, might take values in a continuous space such as (e.g., if represents a probability) or (e.g., coefficients for some regression model), in which case the posterior distribution is a distribution over or over —a more complex object.

Bayesian inference may sometimes lead to answers that are highly sensitive with respect to perturbations of the data. In particular, this can occur in settings where the model is misspecified (but nonetheless, is a reasonably good approximation to the observed data, so that computing the posterior is still a reasonable goal). To alleviate this instability, the BayesBag approach (Bühlmann, 2014) averages posterior distributions over different resamplings of the data . Huggins and Miller (2023) analyzes the accuracy and stability properties of the BayesBag approach for the specific problem of Bayesian model selection, where lies in a finite set of models (and so the posterior on is given by a vector of weights of length , i.e., with the th weight indicating the posterior probability ). Their work establishes BayesBag as an empirically effective method with asymptotic guarantees, but has not yielded finite-sample guarantees even in the finite model setting. Of course, we can also ask this question even more generally: will BayesBag lead to greater stability in a general setting, where may lie in an arbitrary space (e.g., if the posterior is a distribution on , or on , etc.)?

Problem setting 3: synthetic controls for causal inference

The synthetic control method (SCM) is a popular approach for estimating causal effects with panel data (Abadie and Gardeazabal, 2003; Abadie et al., 2010, 2015; Abadie, 2021). The method is particularly useful in settings with a single treated unit and a relatively small number of control units. A synthetic control is a weighted combination of control units, where the weights are chosen to match the treated unit’s pre-treatment outcomes and other covariates. SCM estimates the counterfactual—what outcomes would we expect for the treated unit had the policy not been adopted?—using the synthetic control’s post-treatment outcomes. For example, Abadie et al. (2015) applies SCM to the 1990 German reunification and its impact on per capita GDP in West Germany. Per capita GDP was increasing prior to reunification and continued to increase in subsequent years, for this was a period of sustained growth across industrialized countries. To assess the counterfactual, a ‘synthetic West Germany’ is constructed as follows: we find the convex combination of other industrialized countries such that the pre-1990 economic trend most closely resembles that of West Germany. Abadie et al. (2015) finds that West Germany’s economy did not grow as much as it would have without reunification.

Often SCM’s weights are of direct interest, as they say something about which peer countries are most relevant in this counterfactual assessment. However, in order to reliably interpret the weights, we should first ensure they are stable (Murdoch et al., 2019). For instance, if we remove Denmark from the analysis (a country which receives zero weight in the synthetic West Germany) then there is no longer a positive weight on the United States, which previously received of the weight. This sensitivity appears to betray our intuitive interpretation of the meaning of SCM’s weights. Can a resampling-type approach to SCM alleviate these issues?

1.2 Our contributions

Algorithmic stability is desirable for statistical methods far beyond its origins in statistical learning theory (Devroye and Wagner, 1979a, b; Bousquet and Elisseeff, 2002). Broadly, stability is considered a ‘prerequisite for trustworthy interpretations’ (Murdoch et al., 2019). The goal of this paper is to establish quantitative guarantees on the stability of bagging as a general-purpose tool across a wide range of problems where the output—the output being estimated from the data—might not be real-valued and might even be infinite-dimensional. Table 1 lists a range of problem settings where our framework can be directly applied (including the settings discussed above, namely, supervised learning, Bayesian inference, and synthetic controls). Formally, our results will apply to any algorithm, randomized or deterministic, with outputs in bounded subset of a separable Hilbert or Banach space—we give details below. We highlight one particularly important finding: our main results will show that for a Hilbert space, there is no cost to high dimensionality in terms of the stability guarantees that can be obtained (in contrast, for the more general setting of a Banach space, this is no longer the case).

Outline

The remainder of this paper is organized as follows. In Section 2, we define a framework for algorithmic stability in any metric space, and then define bagging for an arbitrary algorithm in Section 3. Our main results on the stability of bagging are presented in Section 4 and Section 5. In Section 6, we take a closer look at the implications of our results on a range of specific settings appearing in Table 1, and discuss some consequences of our stability guarantee. We conclude with a discussion in Section 7. All proofs are deferred to the Appendix.

| Applications | Output Space | Metric on | ||||

|---|---|---|---|---|---|---|

| Supervised learning | Predicted value range | Absolute value | ||||

|

Probability simplex |

|

||||

|

-ball | -norm | ||||

|

-Lipschitz densities on | Total variation dist. | ||||

| Nonparametric regression | Sobolev ball of functions | Sobolev norm |

2 Framework: algorithmic stability in a metric space

We define a randomized algorithm as function that takes in a finite sequence of data , as well as some independent randomness , and returns an output . The term , which we refer to as the random seed, determines all randomness used by the algorithm—for instance, a random initialization or a random split of the data into batches. The algorithm is deterministic if it does not depend on the seed .

This notion of a (deterministic or randomized) algorithm covers many disparate problems in statistical learning, such as the problem settings introduced in Section 1.1.

-

•

Consider a supervised learning setting (Problem Setting 1) with data points . If we are interested in predicting given a new feature , our algorithm can return , the predicted value at , as its output. (Alternatively, if we are interested in building a model for given , our algorithm can return an entire fitted regression function —a more complex output.)

-

•

In Bayesian inference (Problem Setting 2), we observe data points drawn from some distribution , where is the unknown parameter. To perform Bayesian inference on , our algorithm would then return the posterior distribution over .

-

•

For the problem of synthetic controls (Problem Setting 3), our data points are the feature vectors for each control unit , and the algorithm returns a weight vector of dimension , specifying the convex combination of control units that define the synthetic control.

In some settings it may be common to use a randomized, rather than deterministic, algorithm. For example, in Bayesian inference, in a high-dimensional setting we might choose to approximate the posterior through (random) sampling rather than computing the density explicitly.

Formally, we write

where the output takes values in some space equipped with a metric —see Table 1 for examples. From this point on, we write to denote the output, regardless of the nature of the output (e.g., a finite-dimensional vector of weights for the synthetic control problem, or a posterior density function for the Bayesian inference setting, etc.).111We assume throughout that , which is a function from to , is measurable for any fixed . Measurability is defined with respect to the Borel -algebra on .

2.1 Defining stability

There are many related definitions of algorithmic stability in the literature. We focus on stability of the algorithm’s output with respect to dropping a data point: will the output of the algorithm be similar if one data point is removed at random from the training data set?

Definition 1.

An algorithm has mean-square stability with respect to a metric if, for all data sets of size ,

where is the output of the algorithm run on the full data set , is the output of the algorithm run on the leave-one-out data set , and the expectation averages over .

This first definition captures the average perturbation in when one data point is removed at random from some data set —that is, , averaged over which data point gets removed. An alternative way to define stability is to control the tails of these perturbations , ensuring that not too many of them can be large.

Definition 2.

An algorithm has tail stability with respect to a metric if, for all data sets of size ,

where and as in Definition 1.

The terminology ‘ has mean-square stability ’ in Definition 1, and ‘ has tail stability ’ in Definition 2, suppresses the dependence on the sample size . Since we perform a non-asymptotic stability analysis, we treat as a fixed positive integer throughout.

These two notions of stability are clearly very similar in flavor, and the following simple result shows that each implies the other.

Proposition 3.

If has mean-square stability with respect to , then has tail stability with respect to , for any satisfying . Conversely, if has tail stability with respect to , then has mean-square stability with respect to .

Proof.

The first claim follows by Markov’s inequality, since

For the second claim, since , we have

completing the proof. ∎

2.2 Related notions of stability

Our definitions of stability are stronger than many common definitions in the literature. For instance, we require the algorithm to be stable for any fixed data set to certify the stability of the method without looking at the specific data set. Definition 2 implies in particular that the algorithm is stable when the data are i.i.d. from some distribution , but our definition does not require any stochastic model.

In many cases, practitioners care specifically about the stability of the algorithm’s output , e.g., if we want to interpret the values of some learned weights, cluster assignments, etc. However, in other cases, we may be more concerned with the stability of some downstream decisions or outcomes based on an analysis. For instance, in supervised learning (Problem Setting 1), we may desire stability of a loss incurred by the output —e.g., a predictive error . These types of loss-based stability properties can often be inferred from stability of the output (see Soloff et al. (2024) for further discussion). In this paper, we only consider the stability of itself.

3 Constructing a bagged algorithm via resampling

In this section, we formally define the construction of a bagged algorithm.

Stability is about (in)sensitivity to perturbed data sets. Resampling methods deliberately perturb the data, so they are naturally a useful tool for stabilizing algorithms: given a data set containing data points, we might retrain our algorithm repeatedly on resampled data sets, and then average the resulting outputs. There are several common schemes for constructing these resampled data sets. Here, we mention two of the most common methods:

-

•

Bootstrapping constructs each resampled data set by sampling indices uniformly with replacement from (the term “bootstrap” commonly refers to this method with the choice , so that the resampled data sets are of the same size as the original ).

-

•

Alternatively, we may instead sample data points without replacement, so that each contains a uniformly drawn subset containing of the original data points (e.g., with ). This type of approach is known as subbagging.

We now define some notation that unifies these two variants (as well as allowing for other resampling schemes, as we discuss below).

Following the framework and notation of Soloff et al. (2024), we define the set of finite sequences of indices in :

A sequence is commonly referred to as a bag in the context of data set resampling. For any , define , the corresponding data set. Note that if the bag contains repeated indices (i.e., for some ), then the same data point from the original data set will appear multiple times in .

We are now ready to define the bagged version of any base algorithm , using a particular resampling distribution .222While the term “bagging” is sometimes used as a synonym for bootstrap averaging (i.e., averaging outputs after sampling from the data set without replacement) in the literature, in this paper we will use “bagging” more broadly, allowing for any resampling distribution . From this point on, we assume that is a closed and compact subset of a separable Banach space—this technical condition ensures that taking an average or an expected value of outputs in is well-defined.

Definition 4 (Bagging for an algorithm ).

Given a data set and a distribution on , return the output

where .

For example, bootstrapping corresponds to choosing as the uniform distribution over all sequences of length , while subbagging takes as the uniform distribution over sequences of distinct elements.

For our theoretical analysis, it will be useful to consider taking , so as to “derandomize” the procedure.

Definition 5 (Derandomized bagging for an algorithm ).

Given a data set and a distribution on , return the output

where the expected value is computed with respect to .

3.1 A general framework for bagging

The two variants discussed above, bagging and subbagging, are special cases of a broader framework, allowing for more flexibility in the choice of the resampling distribution . (See Soloff et al. (2024) for a more complete discussion of this framework, and for examples of resampling methods beyond bagging and subbagging.) Here we formalize the conditions that needs to satisfy, in order for our main results to be applied.

Assumption 1.

Fix a sample size . The following conditions must be satisfied by the resampling distribution .

-

•

Symmetry: for all , , and permutations ,

-

•

Nontrivial subsampling: it holds that , where we define

the expected fraction of data points appearing in a bag sampled from .

-

•

Nonpositive covariance:

-

•

Compatibility with the leave-one-out distribution: the corresponding distribution on must equal the distribution of conditional on the event .

Before proceeding, we comment on the last part of the assumption: why does appear in our assumptions on ? To study the stability of the bagged algorithm (Definition 4), it is not sufficient to consider only , the distribution on —when we compare to the result of the algorithm on the leave-one-out data set , we now have sample size (instead of ), and consequently we need to specify a distribution on , as well.

The four conditions of 2 are all satisfied by the standard resampling schemes described above, with for bootstrapping (sampling out of points uniformly with replacement), and for subbagging (sampling out of points uniformly without replacement).

4 Main results for a Hilbert space

We are now ready to present our stability guarantees for bagging. Our first main result establishes that derandomized bagging automatically provides mean-square stability for any algorithm with outputs in a bounded subset of a Hilbert space. In this section, we work with stability with respect to the Hilbert norm . For instance,

-

•

If , then the Hilbert norm may be chosen to be the Euclidean norm , or more generally, a Mahalanobis distance for a fixed positive definite matrix .

-

•

If , the space of square-integrable functions , then the Hilbert norm is given by the norm on functions, . Alternatively, we can take a Sobolev space of functions with smoothness parameter with the Hilbert norm being the Sobolev norm (defined formally later on in (3)—see Experiment 3 in Section 6.1 for details).

Theorem 6.

Suppose takes values in a convex and closed subset , where is a separable Hilbert space, and define

as the radius of the set . Fix a resampling distribution on , which satisfies 1. Then derandomized bagging, run with base algorithm and resampling distribution , has mean-square stability with respect to , with

| (1) |

Combining this result with 3 immediately yields a guarantee on -stability.

Corollary 7.

Under the notation and assumptions of Theorem 6, derandomized bagging has tail stability with respect to for any satisfying

| (2) |

Comparing to prior bounds

The main result of (Soloff et al., 2024, Theorem 8), ensuring the stability of algorithms that return a real-valued output, can be recovered as a special case of Corollary 7 above, by taking (note that we then have ). But remarkably, the result of Theorem 6 shows that there is no price to pay for high-dimensionality (or even for infinite dimensionality): the stability guarantee is exactly the same for any Hilbert space, regardless of dimension, as long as the radius of the output space is bounded.

4.1 Results for a finite number of bags

The results above apply to the derandomized bagged version of , as constructed in Definition 5. In practice, of course, it is not feasible to calculate this output since we would need to average over all possible bags , so we would instead use the bagged estimator constructed in Definition 4 for some finite number of bags . Since we are simply taking a Monte Carlo approximation to the derandomized bagged estimator of Definition 5, we would expect to incur error on the order of . To formalize this, we first recall a generalization of the Azuma-Hoeffding inequality:

Theorem 8 ((Hayes, 2005)).

Let be independent random variables in a Hilbert space such that almost surely for . Then for any ,

In particular,

Note that, aside from the additional factor , this result is the same as what we would obtain for the case . Combining this result with Theorem 6 yields the following stability guarantee for bagged algorithms with a finite number of bags .

Corollary 9.

Under the notation and assumptions of Theorem 6, let be fixed. Then bagging, run with base algorithm and resampling distribution and with bags, has mean-square stability with respect to , with

Of course, tail stability follows as an immediate consequence of 3.

5 Extension: results outside the Hilbert space setting

We now turn to the question of stability in a more general setting, where the output space is not necessarily a Hilbert space. We assume that returns outputs lying in , where is a separable Banach space equipped with norm , and we now aim to establish stability with respect to this norm directly.

As a motivating example, consider a setting where returns an output that specifies a distribution—for instance, this may arise in Bayesian inference (Problem Setting 2 from Section 1.1), where returns a posterior distribution over some parameter of interest. In this type of setting, since represents a distribution, it is natural to study its stability with respect to , the total variation distance. While defines a valid norm, this is not a Hilbert norm and so the theoretical guarantees of Section 4 cannot be directly applied.

To allow for meaningful stability guarantees in a broader range of settings, then, we now consider stability in this more general context, where is not necessarily a Hilbert norm.

5.1 Theoretical guarantee

Unlike the special case of a Hilbert space, in this more general setting we need an additional assumption to ensure that stability will hold.

Assumption 2.

There exists a constant such that , and moreover, there exist some fixed elements with unit norm, , and a constant such that for any , the difference can be approximated by a linear combination of the ’s,

for some with .

Here is playing a role analogous to the radius, , in the Hilbert space setting. For instance, returning to our earlier example, if (and the norm is given by ) then we can take to be the th canonical basis vector. Then 2 holds, with this same value of , and with and .

Theorem 10.

Suppose takes values in a convex and closed subset , where is a separable Banach space equipped with norm , and where satisfies 2 for some integer and some . Fix a resampling distribution on , which satisfies 1. Then derandomized bagging, run with base algorithm and resampling distribution , has mean-square stability with respect to , with

where , for denoting the th harmonic number.

As in the Hilbert space setting, we can also extend this theorem to verify tail stability and to prove a stability result for bagging with a finite —see Appendix B for details.

5.2 Examples

Now we return to Problem Setting 2, as discussed in the motivation for the extension to Banach spaces, where returns a distribution (e.g., a posterior), to see what the new theorem implies in this setting. To make this more concrete, we can consider two specific scenarios: a discrete setting and a continuous setting. We will see how, in each scenario, the new result of Theorem 10 gives a much stronger guarantee than what can be derived from the results of Section 4. For intuition, in this discussion, we treat as a constant.

Problem Setting 2(a): the discrete case

First, consider a finite setting, where returns a distribution on many values—for instance, if the output of specifies a Bayesian posterior over many possible models. In this scenario, takes values in the simplex , and so the total variation distance is given by .

Of course, since is itself a Hilbert space (with norm ), we can apply our results from Section 4—but this will not give a very useful bound for the stability of derandomized bagging. Specifically, Theorem 6 tells us that mean-square stability with respect to holds, for . Since (the usual inequality relating norm to the norm in ), this immediately implies that

or in other words, mean-square stability with respect to holds, for . But if the dimension is large relative to , then this is not a very useful guarantee.

In contrast, let us now see what can be guaranteed via Theorem 10. As mentioned above, 2 holds with equal to the dimension, and with and . Then Theorem 10 tells us that mean-square stability with respect to holds for —a far better bound.

Problem Setting 2(b): the continuous case

Next, consider a continuous setting, where returns a density on , given by some function satisfying . In this case we have .

To formalize this setting, consider the Banach space

equipped with the norm (note that this differs from the usual norm by the factor , in order to agree with total variation distance). Suppose that our algorithm returns densities that are further constrained to be -Lipschitz, so that we have

As for Problem Setting 2(a), we again begin by asking whether the Hilbert space result of Theorem 6 might already be sufficient in this setting. Indeed, while is not a Hilbert space, the Lipschitz constraint on means that for all , meaning that can be viewed as a subset of the Hilbert space , equipped with norm . A straightforward calculation verifies that , meaning that by Theorem 6, derandomized bagging satisfies mean-square stability with respect to for . Since for this function space we have , this immediately implies that mean-square stability with respect to also holds with parameter . However, if the Lipschitz constant is large, this may not be a satisfying result.

Now we turn to our new result, Theorem 10, to see if the stability guarantee can be improved. First, observe that 2 holds for any if we take and . This holds because we can take to be the function , for each —then for any -Lipschitz densities , the -Lipschitz difference can be approximated with a piecewise constant function, i.e., a linear combination of these ’s. Choosing , we apply Theorem 10, which then leads to a guarantee on the mean-square stability with respect to , with . Again, as for the discrete case, if is large (i.e., ) then this is a much stronger bound than the one we can obtain via the Hilbert space result.

Summary of examples

The following table summarizes our results for the two settings, in terms of the stability guarantee with respect to . The improved scaling in the right column highlights the utility of Theorem 10 in extending our results to a broader range of settings.

| Output space |

|

|

||||||

|---|---|---|---|---|---|---|---|---|

|

||||||||

|

Remark 11 (On the necessity of 2).

Our stability guarantee for general Banach spaces essentially requires that lies (approximately) in a convex hull of many points—namely, , …, . In particular, this implies that is (approximately) contained in a finite-dimensional subspace of . In contrast, our Hilbert space results apply regardless of dimensionality—while we do require to be bounded via its radius, , there is no implicit cost to the dimension of in the results of Theorem 6. It turns out that some assumption of this form is actually required for the Banach case—see 13 (in Section B.2) for an explicit counterexample verifying stability fails without this type of assumption.

6 Experiments

In this section, we study the stability of subbagging in experiments across several simulation and real data settings. Code to reproduce all experiments is available at

6.1 Data and Methods

We start by presenting an overview of our four experiments. Experiments 1, 2, and 3 each examine stability in a Hilbert space, with respect to the appropriate Hilbert norm (as studied in Section 4). In contrast, the setting of Experiment 4 is a Banach space (as in Section 5).

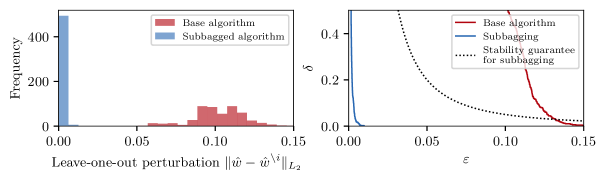

Experiment 1 (Estimating a regression function using bagged decision trees)

We draw data from the following data-generating process:

with and . We then set so that each response is in the unit interval . Note that the algorithm has access to the observed data , i.e., and are latent variables used only to generate the data . We apply sklearn.tree.DecisionTreeRegressor to train the regression trees, setting max_depth=50 and leaving all other parameters at their default values. We evaluate the stability of the learned function in the norm .

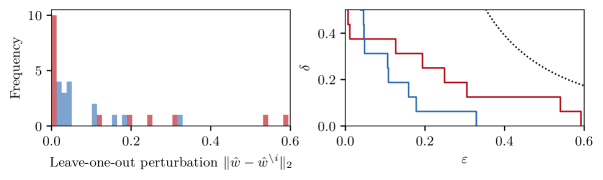

Experiment 2 (Synthetic controls real data example)

For this experiment, we reproduce Abadie et al. (2015)’s SCM analysis on the 1990 reunification of Germany, as discussed above in Section 1.1 (see Problem Setting 3). The data contains countries (aside from Germany), with predictors measured for each country (pre-treatment averages of various macroeconomic factors such as inflation and trade openness—see Table 1 of Abadie et al. (2015) for more details). SCM then estimates a weighted combination of these countries that represents a ‘synthetic West Germany’, meaning that the output of the algorithm is a vector . When we run SCM on a subset of the countries, we assign a weight of to each omitted country. We run SCM using the Python package pysyncon and make extensive use of their reproduction of the original study Abadie et al. (2015). We evaluate the stability of these weights in the Euclidean norm .

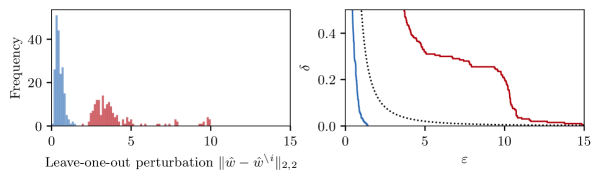

Experiment 3 (Least-squares spectrum analysis)

We study function estimation in a Sobolev space, corresponding to the Hilbert space with smoothness parameter , with the corresponding norm

| (3) |

where denotes the th Fourier coefficient, indexed by . We wish to recover , which is equivalent to estimating the Fourier coefficients. We restrict our estimation problem to even functions, so that we may constrain the Fourier coefficients to be real valued.

Least squares spectral analysis (LSSA) is one method for estimating the Fourier coefficients of a function from irregularly spaced samples Vaníček (1969). Given a data set , we first construct a countable set of features , where , and . The base algorithm returns a function , given by

and where the constraint set is given by

For our simulation, we sample random variables iid from a non-uniform density . Then, the corresponding responses are given by , where and . We run the base algorithm above using the Python package cvxpy, setting . We evaluate the stability of the learned function in the Sobolev norm (see Equation 3 above).

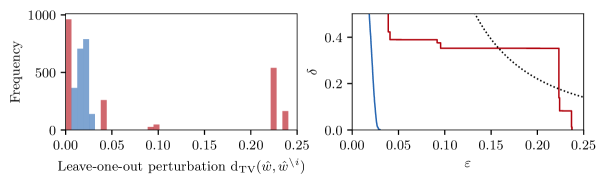

Experiment 4 (Stability of the softmax function)

We simulate a binary data matrix using , where and . The base algorithm takes the softmax of the column sums , i.e.

We evaluate stability with respect to the total variation distance . (As discussed in Section 5, the norm is not a Hilbert norm—that is, unlike the first three experiments, stability guarantees for Experiment 4 hold only due to the extension to the Banach space setting given in Theorem 10.)

Experiment 1: Regression trees

Experiment 2: Synthetic controls, German reunification example (Abadie et al., 2015)

Experiment 2: Synthetic controls, German reunification example (Abadie et al., 2015)

Experiment 3: Least-squares spectral analysis

Experiment 3: Least-squares spectral analysis

Experiment 4: Softmax

Experiment 4: Softmax

6.2 Results

Our experiments compare the stability of the base algorithm to the stability of subbagging with and . Our results are shown in Figure 1 and Table 2. The left panels of Figure 1 show the histogram of leave-one-out perturbations for . In the right panels of Figure 1, for a fixed data set and algorithm, we measure stability by plotting, for each value of , the smallest value of such that the algorithm is -stable:

Furthermore, in Table 2, we record the mean-square stability

For all four experiments, we observe that the subbagged algorithm has better stability than the base algorithm, both in terms of the mean-square stability parameter and in terms of the tail stability parameters (across all, or nearly all, values of ).

| Setting |

|

|

||||

|---|---|---|---|---|---|---|

| Regression trees | ||||||

| Synthetic controls (SCM) | ||||||

| Spectral analysis (LSSA) | ||||||

| Softmax |

7 Conclusion

In supervised learning, algorithmic stability plays a fundamental role in generalization theory (Bousquet and Elisseeff, 2002; Mukherjee et al., 2006; Shalev-Shwartz et al., 2010). More broadly, various forms of stability are fundamental across applied statistics, in part for their role in establishing reproducibility and interpretability (Yu and Kumbier, 2020; Yu and Barter, 2024). This work provides general, finite sample theoretical guarantees supporting the use of bagging and related techniques as general-purpose stabilizers. Our stability guarantees represent a major generalization of Soloff et al. (2024)—which studied algorithms with outputs on the real line—as our results apply to infinite dimensional settings.

An important remaining open question is how to define and guarantee stability for algorithms with discrete outputs. In the synthetic controls setting, for example, our theory shows that bagging can stabilize the SCM weights. However, our results do not imply stability in the resulting support—that is, the set of control units that receive nonzero support. In a sense, the goal of sparsity is incompatible with stability (Xu et al., 2011), so we need a new framework to reconcile these two desiderata. We leave these questions for future work.

Acknowledgements

We gratefully acknowledge the support of the National Science Foundation via grant DMS-2023109 DMS-2023109. R.F.B. and J.A.S. gratefully acknowledge the support of the Office of Naval Research via grant N00014-20-1-2337. R.M.W. gratefully acknowledges the support of NSF DMS-2235451, Simons Foundation MP-TMPS-00005320, and AFOSR FA9550-18-1-0166.

Appendix A Proofs for the Hilbert space setting

Proof of Theorem 6.

For each , define , the expected output of the randomized algorithm for the data set given by . From this point on, we write to denote expectation with respect to . We then have and

by construction, and therefore, a straightforward calculation shows that

| (4) |

Therefore,

The last step holds because we have

where the first equality holds since minimizes mean-square error.

To calculate the last remaining expected value, we first note that since we have assumed symmetry and nonpositive covariance for (see 1), we have for all , for some . Moreover, since the covariance matrix of the random vector must be positive semidefinite, we must have . We then have

Combining everything, then, we have

which yields

after rearranging terms. ∎

Proof of Corollary 9.

Let and be the output of the bagged algorithm (as in Definition 4), and let and be the corresponding derandomized bagged estimators (as in Definition 5). For each , we have

since is nonrandom, while has mean zero. Next,

We next have . Note that the random variables are i.i.d., with mean , and with almost surely. Applying Theorem 8,

By an identical argument, the same holds for the leave-one-out outputs, and . Therefore,

Finally, is bounded by Theorem 6. ∎

Appendix B Proofs and additional results for the Banach space setting

B.1 Proof of main theorem

Proof of Theorem 10.

Let represent the dual norm to . First, for each , as a consequence of the Hahn–Banach theorem (see, e.g., Folland (1999), Theorem 5.8), there is a linear operator on such that , and

We then have

Next, by 2, for each we can find some with and . Then, since is linear and has unit dual norm , for each , and so

where for the last step, we use the fact that for any . Since for each , and , we can rewrite this as

Next, define , so that . Using 1 we can verify that . Then, since for all ,

Combining with the work above, then,

Now we bound the remaining expected value. Let have entries , and observe that and , for each , because . Moreover, for any , , where , and so (by 2), and so for all . Applying Lemma 12 (with vectors ), then,

Finally, since is concave for and for fixed , marginalizing over , and applying Jensen’s inequality, yields

Combining all the above calculations proves that , where

and

Then, solving the quadratic,

This completes the proof of the theorem. ∎

Lemma 12.

Let be a uniformly random permutation of , and let . Let be fixed, with and . Then

where , for denoting the th harmonic number.

Proof.

Applying (Barber, 2024, Theorem 10), for each , for any , it holds that

Therefore, from the definition of and , for any , this implies

for each . We then have

Taking

this yields the desired bound. ∎

B.2 Is 2 needed?

We return to the role of 2, as discussed in Remark 11. In particular, this assumption requires that is approximately contained in a -dimensional subspace of .

We will now see that no uniform stability guarantee can hold without this type of condition. A counterexample can be found with a standard infinite-dimensional Banach space: . We will equip with the norm induced by the metric, given by . This is an infinite-dimensional and separable Banach space.

Next, define , the infinite-dimensional probability simplex. To relate this to our earlier examples, this can be viewed as an infinite-dimensional version of Problem Setting 2(b)— is the space of distributions over , so for instance, we might have an algorithm that returns a posterior distribution over countably infinitely many possible models. Although is bounded in the norm , it cannot be approximated by any finite-dimensional subspace in . The following result shows stability can fail when bagging algorithms with output in .

Proposition 13.

Let , the set of positive integers. Let (equipped with the norm ), and let . Then there exists a (deterministic) algorithm , such that for all , for any distribution satisfying 1, derandomized bagging fails to satisfy mean-square stability with respect to for any .

In other words, stability results of the type shown in Theorem 10 guarantee a bound on (the stability parameter), uniformly over all algorithms , that vanishes as . In contrast, the above example, we show that—for a particular construction of the algorithm —the stability parameter is bounded away from zero even as .

Proof of 13.

Let denote all finite subsets of , and let be a bijective map that assigns each finite subset of to a (unique) positive integer. For any dataset , we define

the set of unique values appearing in the data set. Then define where is the th canonical basis vector, with a in the th location and ’s elsewhere.

Now consider data set . Let and denote the derandomized bagged estimators, as before, for data sets and , respectively. By construction of , we can verify that and similarly . Therefore,

since . Since this holds for every , we have , which completes the proof. ∎

B.2.1 Remark on dimensionality

To relate the construction in this proof back to 2 and Theorem 10, note that in the construction of , at each sample size we are essentially working in a -dimensional space for —that is, even though is the space of all infinite sequences, the algorithm only ever returns sequences with nonzero values in the first entries (and in particular, will always lie in the convex hull of ).

Compare this to the result of Theorem 10, which essentially suggests that mean-square stability vanishes at the rate if can be approximated as a convex hull of many points. Since we have taken to be nonvanishing in this example (due to being the “effective dimension”, as described above), stability is no longer ensured as .

B.3 Additional results

First, we state a result for tail stability in the Banach space setting.

Corollary 14.

Under the notation and assumptions of Theorem 10, derandomized bagging has tail stability with respect to for any satisfying

Proof.

This result follows immediately from Theorem 10 together with 3. ∎

Finally, we state a finite- result for the Banach space setting.

Corollary 15.

Under the notation and assumptions of Theorem 10, let be fixed. Then bagging, run with base algorithm and resampling distribution and with bags, has mean-square stability with respect to , with

Proof.

Let and be the output of the bagged algorithm (as in Definition 4), and let and be the corresponding derandomized bagged estimators (as in Definition 5). We have

since , for any (because satisfies the triangle inequality). The first term in the upper bound is bounded by Theorem 10. Now we bound the remaining terms.

First, let be an i.i.d. copy of . Under the same notation as in the proof of Theorem 10, let denote the dual norm. Then

where the second step holds since and . Now let , for each , so that we have , and similarly write , where the and samples are independently drawn, so that . Then is equal in distribution to where the ’s are i.i.d. random signs.

Now we will bound for any fixed . For each we can write with and , by 2. Then

since for all , and for all . Therefore,

Combining all our work we then have

The same bound holds for . Combining all our calculations establishes the result. ∎

References

- (1)

- Abadie (2021) Abadie, A. (2021). Using synthetic controls: Feasibility, data requirements, and methodological aspects, Journal of Economic Literature 59(2): 391–425.

- Abadie et al. (2010) Abadie, A., Diamond, A. and Hainmueller, J. (2010). Synthetic control methods for comparative case studies: estimating the effect of California’s tobacco control program, J. Amer. Statist. Assoc. 105(490): 493–505.

- Abadie et al. (2015) Abadie, A., Diamond, A. and Hainmueller, J. (2015). Comparative politics and the synthetic control method, American Journal of Political Science 59(2): 495–510.

- Abadie and Gardeazabal (2003) Abadie, A. and Gardeazabal, J. (2003). The economic costs of conflict: A case study of the basque country, American economic review 93(1): 113–132.

- Barber (2024) Barber, R. F. (2024). Hoeffding and Bernstein inequalities for weighted sums of exchangeable random variables, arXiv preprint arXiv:2404.06457 .

- Bousquet and Elisseeff (2002) Bousquet, O. and Elisseeff, A. (2002). Stability and generalization, The Journal of Machine Learning Research 2: 499–526.

- Breiman (1996a) Breiman, L. (1996a). Bagging predictors, Machine learning 24(2): 123–140.

- Breiman (1996b) Breiman, L. (1996b). Heuristics of instability and stabilization in model selection, The Annals of Statistics 24(6): 2350–2383.

- Bühlmann (2014) Bühlmann, P. (2014). Discussion of big Bayes stories and BayesBag, Statistical science 29(1): 91–94.

- Devroye and Wagner (1979a) Devroye, L. and Wagner, T. (1979a). Distribution-free inequalities for the deleted and holdout error estimates, IEEE Transactions on Information Theory 25(2): 202–207.

- Devroye and Wagner (1979b) Devroye, L. and Wagner, T. (1979b). Distribution-free performance bounds for potential function rules, IEEE Transactions on Information Theory 25(5): 601–604.

- Folland (1999) Folland, G. B. (1999). Real analysis, Pure and Applied Mathematics (New York), second edn, John Wiley & Sons, Inc., New York. Modern techniques and their applications, A Wiley-Interscience Publication.

- Hayes (2005) Hayes, T. P. (2005). A large-deviation inequality for vector-valued martingales, Combinatorics, Probability and Computing .

- Huggins and Miller (2023) Huggins, J. H. and Miller, J. W. (2023). Reproducible model selection using bagged posteriors, Bayesian Analysis 18(1): 79–104.

-

Kim and Barber (2023)

Kim, B. and Barber, R. F. (2023).

Black-box tests for algorithmic stability, Inf. Inference 12(4): Paper No. iaad039, 30.

https://doi.org/10.1093/imaiai/iaad039 - Mukherjee et al. (2006) Mukherjee, S., Niyogi, P., Poggio, T. and Rifkin, R. (2006). Learning theory: stability is sufficient for generalization and necessary and sufficient for consistency of empirical risk minimization, Advances in Computational Mathematics 25(1): 161–193.

- Murdoch et al. (2019) Murdoch, W. J., Singh, C., Kumbier, K., Abbasi-Asl, R. and Yu, B. (2019). Definitions, methods, and applications in interpretable machine learning, Proceedings of the National Academy of Sciences 116(44): 22071–22080.

- Shalev-Shwartz et al. (2010) Shalev-Shwartz, S., Shamir, O., Srebro, N. and Sridharan, K. (2010). Learnability, stability and uniform convergence, The Journal of Machine Learning Research 11: 2635–2670.

-

Soloff et al. (2024)

Soloff, J. A., Barber, R. F. and Willett, R. (2024).

Bagging provides assumption-free stability, Journal of Machine

Learning Research 25(131): 1–35.

http://jmlr.org/papers/v25/23-0536.html - Vaníček (1969) Vaníček, P. (1969). Approximate spectral analysis by least-squares fit: Successive spectral analysis, Astrophysics and Space Science 4: 387–391.

- Xu et al. (2011) Xu, H., Caramanis, C. and Mannor, S. (2011). Sparse algorithms are not stable: A no-free-lunch theorem, IEEE transactions on pattern analysis and machine intelligence 34(1): 187–193.

- Yu (2013) Yu, B. (2013). Stability, Bernoulli 19(4): 1484–1500.

- Yu and Barter (2024) Yu, B. and Barter, R. (2024). Veridical Data Science: The Practice of Responsible Data Analysis and Decision Making, MIT Press.

- Yu and Kumbier (2020) Yu, B. and Kumbier, K. (2020). Veridical data science, Proc. Natl. Acad. Sci 117(8): 3920–3929.