Nonparametric Inference on Dose-Response Curves Without the Positivity Condition

Supplement to “Nonparametric Inference on Dose-Response Curves Without the Positivity Condition”

Abstract

Existing statistical methods in causal inference often rely on the assumption that every individual has some chance of receiving any treatment level regardless of its associated covariates, which is known as the positivity condition. This assumption could be violated in observational studies with continuous treatments. In this paper, we present a novel integral estimator of the causal effects with continuous treatments (i.e., dose-response curves) without requiring the positivity condition. Our approach involves estimating the derivative function of the treatment effect on each observed data sample and integrating it to the treatment level of interest so as to address the bias resulting from the lack of positivity condition. The validity of our approach relies on an alternative weaker assumption that can be satisfied by additive confounding models. We provide a fast and reliable numerical recipe for computing our estimator in practice and derive its related asymptotic theory. To conduct valid inference on the dose-response curve and its derivative, we propose using the nonparametric bootstrap and establish its consistency. The practical performances of our proposed estimators are validated through simulation studies and an analysis of the effect of air pollution exposure (PM2.5) on cardiovascular mortality rates.

keywords:

[class=MSC2020]keywords:

, and

1 Introduction

In observational studies, the causal effect of interest does not always result from a standard binary intervention but rather comes as a consequence of a continuous treatment or exposure. Such a causal effect on the outcome variable from a continuous treatment variable is known as the (causal) dose-response curve or relationship due to its major application in studying biological effects (Waud, 1975). More precisely, a dose-response curve characterizes the average outcome if all units would have been assigned to a certain treatment level . In practice, it is fairly common that an additional set of covariates is collected, which, to some extent, contains all the possible confounding variables that influence both the treatment and the outcome . Under regularity conditions (see Section 2.2), the dose-response curve coincides with the so-called covariate-adjusted regression function with and is thus identifiable from the observed data for any (Robins et al., 2000; Neugebauer and van der Laan, 2007; Díaz and van der Laan, 2013; Kennedy et al., 2017). Alternatively, the covariate-adjusted regression function can be viewed as a univariate summary function of the outcome against a continuous covariate when we average the regression function over all other covariates (Takatsu and Westling, 2022).

However, the regularity conditions for identifying and estimating the dose-response curve might not be verifiable or could even be violated in observational studies. In particular, it is commonly assumed that there is a sufficient amount of variability in the treatment assignment within each strata of the covariates, which is captured by the following positivity or overlapping condition.

Assumption A0 (Positivity).

The conditional density is bounded above and away from zero almost surely for all and .

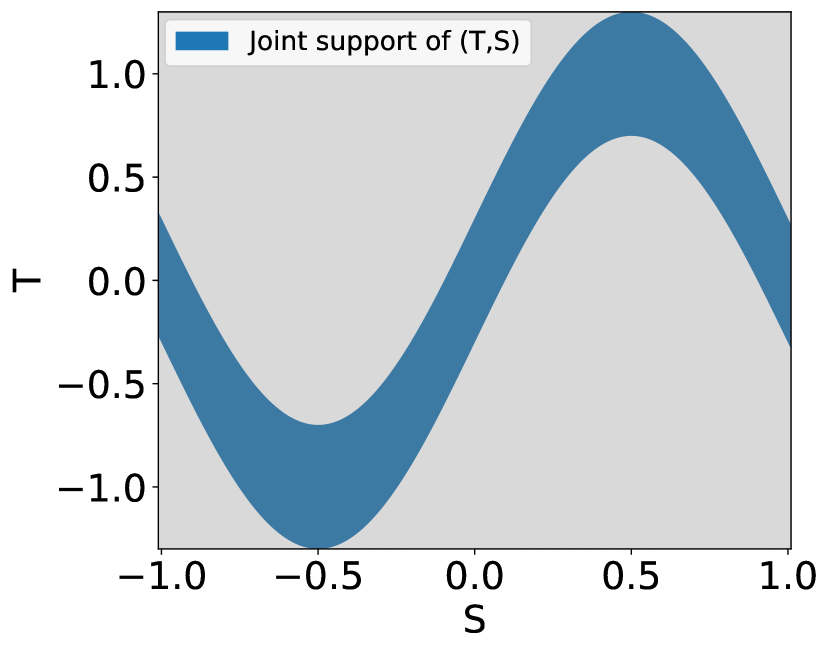

The positivity condition (A0) may be violated in observational studies for either of the following two reasons: (i) theoretically, it is impossible for some individuals with certain covariate values to receive some levels of the treatment, and (ii) practically, individuals at some levels of the treatment may not be collected in the finite data sample; see Cole and Hernán (2008); Westreich and Cole (2010); Petersen et al. (2012) for related discussions. These problems are particularly pervasive under the context of continuous treatments. For instance, air pollution levels can vary greatly across larger regions but remain relatively consistent within smaller and nearby areas. Therefore, individuals at the same location are typically only get exposed to one level of air pollution, i.e., spatial confounding variables may change at a finer scale than the variation of exposure, thereby violating the positivity condition (Paciorek, 2010; Schnell and Papadogeorgou, 2020; Keller and Szpiro, 2020). As a more concrete example, consider a single confounder model

| (1) |

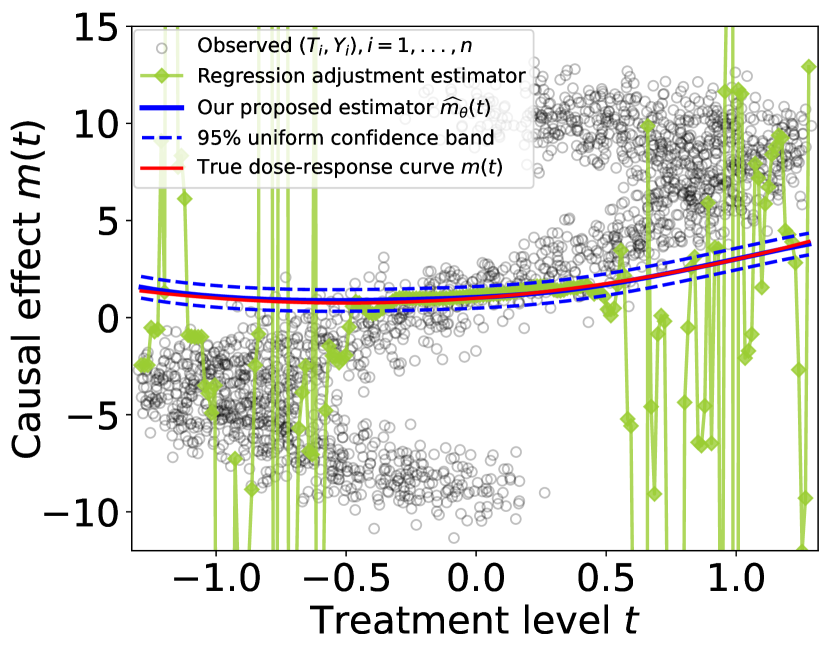

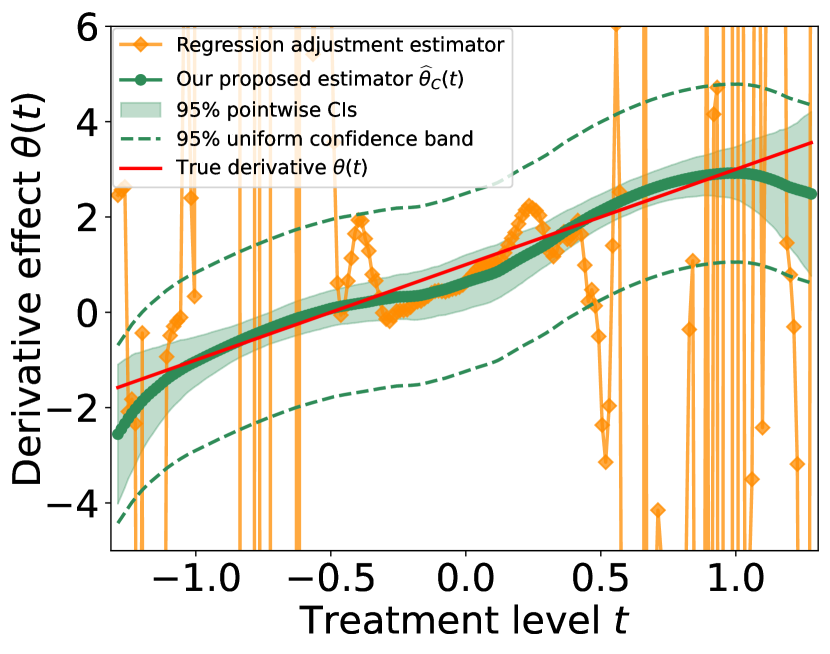

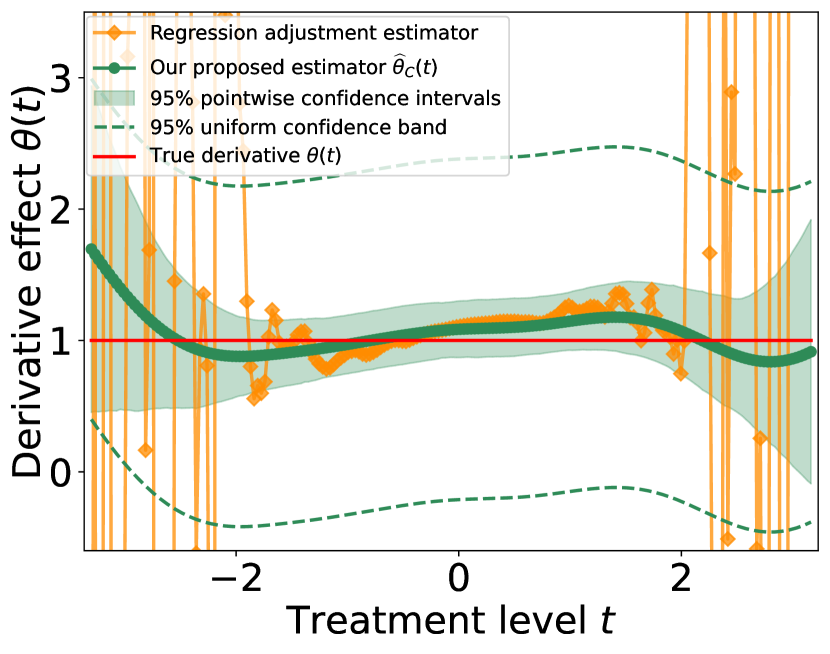

where is an independent treatment variation and is an exogenous normal noise. The marginal supports of and are and respectively, while the joint support of only covers a thin band region of the product space ; see the left panel of Fig 1. The conditional density for any is 0 within the gray regions, and the positivity condition (A0) clearly fails. Without (A0), the existing approaches for estimating the dose-response curve and its derivative can be very unstable at some specific treatment levels; see the usual regression adjustment estimators (defined in (6) and Remark 1 below) in the middle and right panels of Fig 1 for illustrations.

In this paper, we propose a novel integral estimator that can consistently recover the entire dose-response curve and a localized estimator of its derivative even when the positivity condition (A0) fails to hold in some regions of the product space ; see the middle and right panels of Fig 1. Our main contributions are summarized as follows:

1. Methodology: After discussing the identification conditions of as a causal dose-response curve in Section 2, we introduce our integral estimator of in Section 3.1, which is constructed from a localized estimator of around the observed data and extrapolate to any treatment level through the fundamental theorem of calculus. Such an integral estimator can also be efficiently computed in practice via the Riemann sum approximation in Section 3.2 and be reliably inferred through nonparametric bootstrap in Section 3.3.

2. Asymptotic Theory: We establish uniform consistencies of our proposed integral estimator and localized derivative estimator under the context of kernel smoothing methods in Section 4.2. We also prove the validity of nonparametric bootstrap inference in Section 4.3.

3. Experiments: We demonstrate the finite-sample performances of our proposed estimators through simulation studies and a case study of the effect of fine particulate matter (PM2.5) on cardiovascular mortality rates in Section 5. All the code for our experiments is available at https://github.com/zhangyk8/NPDoseResponse/tree/main/Paper_Code.

1.1 Other Related Works

Estimating the dose-response curve is a technically difficult problem in causal inference due to the fact that is not pathwise differentiable and cannot be consistently estimated in a rate (Chamberlain, 1986; van der Vaart, 1991). Parametrically, Robins et al. (2000) pioneered a marginal structural model to estimate , whose dependence on the correct specification of a parametric model was later relaxed by van der Laan and Robins (2003); Neugebauer and van der Laan (2007) through a projection of to the parametric model space. Nonparametrically, a regression adjustment approach to estimating under a two-stage kernel smoothing estimator was first studied by Newey (1994) and later adapted to the estimation of dose-response curves by Flores (2007). However, the consistency and asymptotic normality of their kernel-based estimators rely on an undersmoothing bandwidth, which is asymptotically smaller than the one that attains the optimal asymptotic bias-variance trade-off and is difficult to select in practice; see Section 5.7 in Wasserman (2006). On the contrary, our proposed integral estimator of under the context of kernel smoothing is based on the derivative estimation and require neither explicit undersmoothing nor bias correction (Calonico et al., 2018; Takatsu and Westling, 2022), permitting the use of any bandwidth selection method in nonparametric regression.

There are many existing works about the estimation of average derivative effects in the literature; see Härdle and Stoker (1989); Powell et al. (1989); Newey and Stoker (1993); Cattaneo et al. (2010); Hirshberg and Wager (2020) and references therein. Under some regularity conditions, average derivative effects are identical to the so-called incremental treatment effects, which are closely related to the derivatives of dose-response curves; see Proposition 1 in Rothenhäusler and Yu (2019) and Section 6.1 in Hines et al. (2023).

All the aforementioned methods for estimating and assume the positivity condition (A0). Under the context of binary treatments, there are previous researches studying the dependence of common estimators on (A0) from the perspectives of convergence rates (Khan and Tamer, 2010; D’Amour et al., 2021) and empirical performances (Busso et al., 2014; Léger et al., 2022). To address the violation of positivity, some approaches considered trimming the extreme values of (estimated) propensity scores (i.e., discrete versions of the conditional density ; Dehejia and Wahba 1999; Crump et al. 2009; Yang and Ding 2018), while others proposed robust estimation methods against the violation (Rothe, 2017; Ma and Wang, 2020). In addition, Kennedy (2019) considered switching the causal estimand to the incremental treatment effect for discrete treatments, which can be nonparametrically estimated without positivity. Rothenhäusler and Yu (2019) later studied the same estimand for continuous treatments. To the best of our knowledge, none of existing works address the nonparametric inference on and without assuming (A0).

1.2 Notations

Throughout the paper, we consider a real-valued outcome variable , univariate continuous treatment , and a vector of covariates with a fixed dimension . We write when the random variables are independent. The data sample consists of independent and identically distributed (i.i.d.) observations with the common distribution and Lebesgue density . Here, and are the marginal densities of and , respectively, and is the conditional density of given covariates . We also denote the joint density of by . Let be the empirical distribution of the observed data so that for some measurable function . At the population level, we denote for -integrable function . In addition, we define the empirical process evaluated at a -integrable function as . Finally, we use to denote the indicator function of a set .

We use the big- notation if is upper bounded by a positive constant multiple of when is sufficiently large. In contrast, when . For random variables, the notation is short for a sequence of random variables converging to zero in probability, while the expression denotes the sequence that is bounded in probability. We also use the notation or when there exists an absolute constant such that when is large. If and , then are asymptotically equal and it is denoted by .

2 Model Setups and Identification Conditions

We assume that are i.i.d. observations generated from the following model:

| (2) | ||||

where is the treatment variation with , , and is an exogenous noise variable with and . The function determines how the covariates (or confounding variables) influence the treatment . Under model (2), the covariate-adjusted regression function (or the dose-response curve under identification conditions in Section 2.2) is given by

and its derivative is written as . Notice that the derivative function can be viewed as the continuous version of the average treatment effect in causal inference. In the presence of confounding variables , cannot be identified by regressing only with respect to , because .

2.1 Motivating Example: Additive Confounding Model

One important exemplification of model (2) that we will frequently refer to in this paper is the following additive confounding model:

| (3) | ||||

where is the primary treatment effect of interest and is the random effect with . Such an additive form is a common working model in spatial confounding problems (Paciorek, 2010; Schnell and Papadogeorgou, 2020) and also known as the geoadditive structural equation model (Kammann and Wand, 2003; Thaden and Kneib, 2018; Wiecha and Reich, 2024), where are the spatial locations (usually with ) or other spatially correlated covariates that affect both the treatment and the outcome . We summarize key properties of the additive confounding model (3) in the following proposition.

Proposition 1 (Properties of the additive confounding model (3)).

Let and , where . Under the additive confounding model (3) with , the following results hold for all :

-

(a)

.

-

(b)

when .

-

(c)

.

-

(d)

when .

-

(e)

even when .

The above results hold even if the treatment variation almost surely.

The proof of Proposition 1 is in Section B.1. Note that in Proposition 1(e), the first expectation is taken with respect to the joint distribution of while the second expectation is taken with respect to the marginal distribution of .

2.2 Identification Conditions

While can be defined through model (2), we need some additional assumptions in order to express as a causal effect of on and identify it from the observed data . Following the potential outcome framework (Rubin, 1974), we let denote the potential outcome that would have been observed under treatment level and covariate vector . We summarize the required assumptions as follows.

Assumption A1 (Identification conditions for ).

-

(a)

(Treatment effect and consistency) for any and .

-

(b)

(Ignorability or unconfoundingness) for all .

-

(c)

(Treatment variation) The treatment variation has nonzero variance, i.e., .

Assumption A1(a) is a continuous version of the stable unit treatment value assumption (SUTVA; Page 19 of Cox 1958 and Rubin 1980). The first equality ensures that the potential outcome under treatment level is well-defined whatever value the covariate vector takes, while the second equality guarantees that the treatment level of any subject does not affect the potential outcomes of others (i.e., no interference) and there are no different versions of treatments. Given that both the treatment and the outcome are continuous, the essential consistency condition that we need is the identity of conditional distributions for any and ; see Gill and Robins (2001) for details. The ignorability condition (Assumption A1(b)) was first generalized to continuous treatments by Hirano and Imbens (2004), stating that the potential outcome variable is independent of the treatment level within any specific strata of covariates. In the context of spatial confounding, the ignorability condition holds when the spatial locations are taken into account (Gilbert et al., 2023). It also implies that the mean potential outcome under remains the same across all treatment levels when we condition on . Finally, the treatment variation condition (Assumption A1(c)) is crucial for identifying the conditional mean outcome (or regression) function on a non-degenerate region of . When , can only be identified on the lower dimensional surface , which is also the support of . We derive nonparametric bounds on and its derivative in Section A. We also demonstrate how can lead to ambiguous definitions of the associated dose-response curves in Example 1 below.

Example 1 (Necessity of ).

Suppose that and almost surely, where is the first component of . We further assume that . Now, consider two equivalent conditional mean outcome functions

both of which are equal to and agree on the support . However, these two conditional mean outcome functions lead to two distinct treatment effects:

whose derivatives are different as well.

Under Assumption A1, the dose-response curve is identical to the standard covariate-adjusted regression function and can thus be estimated from the observed data . To estimate the derivative of the dose-response curve from the observed data sample, we impose an additional assumption on the conditional mean outcome function that enables us to bypass the positivity condition (A0).

Assumption A2 (Identification condition for ).

The function is continuously differentiable with respect to for any and the following two equalities hold true:

| (4) |

and

| (5) |

The first equality in (4) is a mild condition and can be satisfied under various settings. In particular, it holds when is bounded by an integrable function with respect to the distribution of ; see Theorem 1.1 and Example 1.8 in Shao (2003). The second equality in (4) as well as the equation (5) of Assumption A2 are stricter but still valid under the additive confounding model in Section 2.1; recall Proposition 1(c,e). Under Assumption A2, we can express in three different but also equivalent ways

Estimating the derivative effect through the form of is our key technique to bypass the particularly strong positivity condition (A0) under the continuous treatment setting. After is consistently recovered, we refer the estimation back to the dose-response curve by (5) and the fundamental theorem of calculus; see Section 3.1 for details.

3 Nonparametric Inference Without the Positivity Condition

Under the positivity condition (A0), together with Assumption A1, the dose-response curve can be identified through the covariate-adjusted regression function from the observed data , suggesting the following regression adjustment (RA) or G-computation (Robins, 1986; Gill and Robins, 2001) estimator as:

| (6) |

where is any consistent estimator of the conditional mean outcome function . However, when the positivity condition (A0) does not hold for some region in , the above estimator (6) will be unstable and even inconsistent. This is because without (A0), the joint density can be close to 0 for some , and cannot be consistently estimated for those query points . Other existing methods for estimating , such as the inverse probability of treatment weighted (IPTW) or its augmented variants, also relies on the validity of (A0) for their consistency and empirical behaviors (Díaz and van der Laan, 2013; Kennedy et al., 2017; Huber et al., 2020; Colangelo and Lee, 2020). The same issue incurred by the failure of (A0) also applies to the estimation of .

In this section, we introduce a novel integral estimator to resolve the inconsistency issues of existing estimators in recovering the dose-response curve and its derivative without the positivity condition (A0). On one hand, the estimation of is based on the conditional expectation in (4), which only relies on the consistent estimation of in the high density region of . On the other hand, our proposed estimator of generalizes the regression adjustment estimator (6) but remains consistent and numerically stable even when the conditional density is zero for some values of thanks to its integral formulation. We also provide a fast algorithm for computing our proposed estimator of in practice and delineate the bootstrap inference procedures for both estimators of and .

3.1 Proposed Integral Estimator of

Given the observed data , our proposal for removing the reliance of the positivity condition (A0) from (6) is based on three critical insights.

-

•

Insight 1: Consistent estimation of and at each . Given that the observed data generally appear in a high density region of , the conditional mean outcome function can be well-estimated at each observation . As a result, one can expect that the partial derivative can be consistently estimated at each observation as well.

-

•

Insight 2: Consistent estimation of from a localized form . The equations (4) in Assumption A2 lead to two possible approaches to estimating the derivative effect . One approach is via , while the alternative is based on . Estimating by is preferable because relies on a consistent estimator of at each pair , which is not possible when the positivity condition (A0) fails to hold at some for . In contrast, the expression only requires the estimator of to be accurate at the covariate vector with a high conditional density value .

-

•

Insight 3: Integral relation between and . For any , the fundamental theorem of calculus reveals that

Under Assumption A2, we take the expectation on both sides of the above equality to obtain that

(7) This expression suggests that as long as we have consistent estimators of at and near , we can then use the integration to extrapolate the estimation to and for any even when .

According to the integral relation (7), we propose an integral estimator of the dose-response curve as:

| (8) |

where is a consistent estimator of . To construct an estimator of , we need to estimate two nuisance functions: (i) the partial derivative of the conditional mean outcome function and (ii) the conditional cumulative distribution function (CDF) . In this paper, we leverage the following two kernel smoothing methods for estimating these two nuisance functions and leave other possibilities as a future direction.

3.1.1 Local Polynomial Regression Estimator of

We consider estimating by the local polynomial regression (Fan and Gijbels, 1996) because of its robustness around the boundary of support (also known as the automatic kernel carpentry in Hastie and Loader 1993).

Let be two symmetric kernel functions and be their corresponding smoothing bandwidth parameters. Some commonly used univariate kernel functions include the Epanechnikov kernel and Gaussian kernel . For the multivariate kernel function, one often resorts to the product kernel technique as for . To estimate from the observed data , we fit a partial local polynomial regression of order () with monomials of as the polynomial basis in treatment variable and the local linear function in covariate vector (Ruppert and Wand, 1994). Specifically, we let for and consider

| (9) | ||||

For simplicity, we use the same bandwidth parameter for each coordinate in here. One can generalize the above method and related theoretical results to a general bandwidth matrix in with little effort. Let be a matrix with the -th row as and . We also define a diagonal weight matrix as:

Then, (9) has a closed-form solution from a weighted least square problem as:

| (10) |

Finally, the second component of the fitted coefficient provides a natural estimator of . In practice, we recommend to choose to be an even number when estimating the first-order (partial) derivative via (9), because there is an increment to the asymptotic variance of when changes from an even number to the consecutive odd number. Additionally, fitting (partial) local polynomial regressions of higher orders often give rise to a possible reduction of bias but also a substantial increase of the variability; see Chapter 3.3 in Fan and Gijbels (1996). Therefore, we mainly focus on the (partial) local quadratic regression when constructing our derivative estimator in the subsequent analysis.

3.1.2 Kernel-Based Conditional CDF Estimator of

We consider estimating through a Nadaraya-Watson conditional CDF estimator (Hall et al., 1999) defined as:

| (11) |

where is again a kernel function and is the smoothing bandwidth parameter that needs not be the same as the bandwidth parameter for estimating by the local polynomial regression. Practically, there are several strategies for choosing the bandwidth in (11) as described by Bashtannyk and

Hyndman (2001); Holmes et al. (2012).

Combining the partial derivative estimator in (10) with the conditional CDF estimator in (11), we deduce the final localized estimator of as:

| (12) |

In essence, is a regression adjustment estimator with two nuisance functions: and . Here, we have showcased how to use the (partial) local polynomial regression (9) to estimate and Nadaraya-Watson conditional CDF estimator (11) to estimate .

Remark 1 (Regression adjustment estimator of ).

Under the additive confounding model (3), one can directly estimate via or the regression adjustment estimator , because by Proposition 1,

The estimator is suboptimal, because it only uses the value from a single location. Furthermore, will not be a stable and consistent estimator of when the positivity condition fails to hold at those ; see Fig 1 for an illustration. In contrast, what we propose in (12) relies on the conditional CDF estimator and remains valid and consistent even without the positivity condition (A0).

Remark 2 (Linear smoother).

It is worth noting that our integral estimator (8) under the kernel-based estimator (12) is that it is a linear smoother. Let . Then, with (10) and , we know that in (12) can also be written as:

It implies that

As a consequence, we can also utilize the theory of linear smoothers to derive its effective degrees of freedom and fine-tune the smoothing bandwidth parameters (Buja et al., 1989; Wasserman, 2006).

3.2 A Fast Computing Algorithm for the Proposed Integral Estimator

Our proposed estimator of the dose-response curve involves an integral that may be analytically difficult to compute in practice. Here, we propose a fast computing algorithm that can numerically approximate with an error of the order at most . The key idea is to approximate the integral via a Riemann sum, evaluate only at the data sample , and then use the linear interpolation to obtain the value at any arbitrary .

Let be the order statistics of and for be their consecutive differences. The integral estimator in (8) can be rewritten as:

To compute evaluated at the -th order statistic, we consider approximating the second integral term as follows.

-

•

When , we have the following Riemann sum approximation as:

-

•

When , we use another Riemann sum approximation as:

Plugging the above results into , we obtain that for ,

where the equality (i) follows from switching the orders of summations. Similarly, when or , we also have that

Therefore, we propose the following approximation for as:

| (13) |

Finally, to evaluate at any arbitrary , we conduct the linear interpolation between and on the interval . One biggest advantage of using the approximation formula (13) is that we only need to compute the derivative estimator at the order statistics . When and its derivative are Lipschitz and the marginal density is uniformly bounded away from 0 on the region of interest, this approximation formula has at most error, which is asymptotically negligible compared to the dominating estimation error of ; see Theorem 4 for details.

3.3 Bootstrap Inference

Since it is complicated to derive consistent estimators of the (asymptotic) variances of our integral estimator (8) and localized derivative estimator (12), we consider conducting inference on and through the empirical bootstrap method (Efron, 1979) as follows. Other bootstrap methods, including residual bootstrap (Freedman, 1981) and wild bootstrap (Wu, 1986), also work under some modified conditions.

-

1.

Compute the integral estimator and localized derivative estimator on the original data .

-

2.

Generate bootstrap samples by sampling with replacement from the original data and compute the integral estimator and localized derivative estimator on each bootstrapped sample for .

-

3.

Let be a pre-specified significance level.

-

•

For a pointwise inference at , we calculate the quantiles and of and respectively, where and for .

-

•

For an uniform inference on the entire dose-response curve and its derivative , we compute the quantiles and of and respectively, where and for .

-

•

-

4.

Define the confidence intervals for and as:

respectively, as well as the simultaneous confidence bands as:

for every .

In Section 4.3, we will establish the consistency of the above bootstrap inference procedures.

4 Asymptotic Theory

In this section, we study the consistency results of our integral estimator (8) and localized derivative estimator (12) proposed in Section 3.1 and the validity of bootstrap inference described in Section 3.3.

4.1 Notations and Assumptions

We introduce the regularity conditions under the general confounding model (2) for our subsequent theoretical analysis. Let be the support of the joint density , be the interior of , and be the boundary of .

Assumption A3 (Differentiability of the conditional mean outcome function).

For any , the conditional mean outcome function is at least times continuously differentiable with respect to and at least four times continuously differentiable with respect to , where is the order of (partial) local polynomial regression in (9). Furthermore, and all of its partial derivatives are uniformly bounded on .

Assumption A4 (Differentiability of the joint density).

The joint density is bounded and at least twice continuously differentiable with bounded partial derivatives up to the second order on . All these partial derivatives of are continuous up to the boundary . Furthermore, is compact and is uniformly bounded away from 0 on . Finally, the marginal density of is non-degenerate, i.e., its support has a nonempty interior.

Assumptions A3 and A4 are commonly assumed differentiability conditions in the literature of local polynomial regression (Ruppert and Wand, 1994; Fan and Gijbels, 1996), which can be slightly relaxed via the Hölder continuity condition. It ensures that the bias term of from the local polynomial regression (10) is at least of the standard order ; see Lemma 2 below. Notice that the projection of the joint density support onto the domain of coincides with the marginal support . Hence, will be compact as well under Assumption A4.

To control the boundary effects of the local polynomial regression, we impose the following conditions on , , and the geometric structure of near the boundary .

Assumption A5 (Boundary conditions).

-

(a)

There exists some constants such that for any and all , there is a point satisfying

where with being the standard Euclidean norm.

-

(b)

For any , the boundary of , it satisfies that and for all .

-

(c)

For any , the Lebesgue measure of the set satisfies for some absolute constant , where .

Assumption A5(a) is adopted from the boundary condition (Assumption X) in Fan and Guerre (2015), whose primitive and stronger version also appeared as Assumption (A4) in Ruppert and Wand (1994). This is a relatively mild condition that holds when the boundary is smooth or only contains non-smooth vertices from some regular structures, such as dimensional cubes and convex cones. Indeed, Assumption A5(a) is valid as long as any ball centered at a point in near a vertex of has its radius shrunk linearly when approaching the vertex. More examples and discussions about Assumption A5(b) can be found in Ruppert and Wand (1994); Fan and Guerre (2015). The main purpose of imposing this support condition is to ensure that there are enough observations near the boundary points so that the rate of convergence for our local polynomial estimator remains the same order at the boundary points as the interior points of . Assumption A5(b) regularizes the slope of and the curvature of at the boundary point . Specifically, at the boundary , the joint density needs to be flat, while should embrace zero curvatures. Similar to Assumption A4, the partial derivatives are defined by computing them at a nearby interior point and taking the limit . This condition is another key requirement for the bias term from in the local polynomial regression (10) to remain the same rate of convergence at the boundary points as the interior points of . Finally, Assumption A5(c) also regularizes the boundary so that it will not have any fractal or other peculiar structures leading to an infinite perimeter of .

To establish the (uniform) consistency of our local polynomial regression estimator (10) and Nadaraya-Watson conditional CDF estimator (11), we rely on the following regularity conditions on the kernel functions.

Assumption A6 (Regular kernel and VC-type conditions).

-

(a)

The functions and are compactly supported and Lispchitz continuous kernels such that , , and is radially symmetric with . In addition, for all and , it holds that

Finally, both and are second-order kernels, i.e., and for all .

-

(b)

Let . It holds that is a bounded VC-type class of measurable functions on .

-

(c)

The function is a second-order, Lipschitz continuous, and symmetric kernel with a compact support, i.e., , , and .

-

(d)

Let . It holds that is a bounded VC-type class of measurable functions on .

Assumption A6(a,c) are indeed not the regularity conditions but rather properties of those commonly used kernel functions. Assumption A6(b,d) are critical conditions for the uniform consistency of kernel-based function estimators (Giné and Guillou, 2002; Einmahl and Mason, 2005) and can be satisfied by a wide range of kernel functions, including Gaussian and Epanechnikov kernels. For example, it is satisfied when the kernel is a composite function between a polynomial in variables and a real-valued function of bounded variation; see Lemma 22 in Nolan and Pollard (1987). Given that the kernel functions are bounded, we can always take constant envelope functions for and in Assumption A6(b,d).

Finally, we introduce some notations that will be used in proofs of the consistency results of from the local polynomial regression (10) (Lemmas 2 and 3) and the asymptotic linearity results of our integral estimator and localized derivative estimator (Lemma 5). Under the notations in Assumption A6(a), we define a matrix

| (14) |

Notice that only depends on the kernel functions in the local polynomial regression. For any , we also define the functions as:

| (15) | ||||

4.2 Consistency of the Integral Estimator

Before establishing the consistency of our proposed integral estimator (8) and localized derivative estimator (12), we first discuss the pointwise and uniform consistency results of from the local polynomial regression (10) as building blocks.

Lemma 2 (Pointwise convergence of ).

The complete statement of the asymptotic expressions for the conditional variances and bias of and the proof of Lemma 2 are given in Section B.2. Notice that our (conditional) rates of convergence of in Lemma 2 align with the standard results in the literature of local polynomial regression (Ruppert and Wand, 1994; Fan and Gijbels, 1996; Lu, 1996). The extra bias rate or comes from a higher order term in the Tyler’s expansion and will be asymptotically negligible when as ; see (26) and (28) in Section B.2 for an example. More importantly, when we utilize the (partial) local quadratic regression (i.e., ) to obtain , the order of that optimally trades off the bias and variance in Lemma 2 will be , which also leads to the optimal rate for derivative estimation established in Stone (1980, 1982). Conventional bandwidth selection methods generally will not yield with this optimal order. However, the validity of bootstrap inference in Section 4.3 requires bandwidths to be of a smaller order so that the asymptotic bias is negligible compared to the stochastic variation (Bjerve et al., 1985; Hall, 1992); see Lemma 5 below. Since is an optimal bandwidth order for estimating the regression function , we can then apply any off-the-shelf bandwidth selection method of multivariate local polynomial regression (Wand and Jones, 1994; Yang and Tschernig, 1999; Li and Racine, 2004) to obtain our bandwidth parameters ; see also Remark 4 below.

We also strengthen the pointwise rate of convergence to the uniform one as follows.

Lemma 3 (Uniform convergence of ).

The proof of Lemma 3 can be found in Section B.3. At a high level, the uniform rate of convergence for the bias term remains the same as in Lemma 2 under our regularity conditions. To handle the stochastic variation term , we approximate it (up to a scaled factor ) by an empirical process so that the upper bound for its uniform rate of convergence follows from the results in Einmahl and Mason (2005). This uniform rate of convergence in Lemma 3 is not only useful for deriving the asymptotic behaviors of our integral estimator (8) and localized derivative estimator (12) in Theorem 4 below but can also facilitate our study of the bootstrap consistency in Section 4.3.

With Lemma 3, we now present the uniform consistency results for our integral estimator (8) and localized derivative estimator (12).

Theorem 4 (Convergence of and ).

The pointwise rates of convergence for and will remain the same as stated in Theorem 4 due to the randomness of observations near the boundary of density support ; see the proof of Theorem 4 in Section B.4 for detailed arguments. We restrict the uniform consistency results in Theorem 4 to a compact set in order to avoid the density decay of near the boundary of its support . If is uniformly bounded away from 0 in its support, we can take . The (uniform) rate of convergence of consists of two parts. The first part comes from the simple sample average of and is asymptotically negligible. The second dominant part is due to the integral component

| (16) |

whose rate of convergence is determined by . Furthermore, the (uniform) rate of convergence of comprises the rate for estimating the partial derivative and the rate for estimating the conditional CDF .

4.3 Validity of the Bootstrap Inference

Before proving the consistency of our bootstrap procedure in Section 3.3, we first derive the asymptotic linearity of our integral estimator (8) and localized derivative estimator (12) as intermediate results.

Lemma 5 (Asymptotic linearity).

Let in the local polynomial regression for estimating and be a compact set so that is uniformly bounded away from 0 within . Suppose that Assumptions A1, A2, A3, A4, A5, and A6 hold. Then, if and for some such that and for some finite number and as , then for any , we have that

where and

| (17) | ||||

Furthermore, we have the following uniform results as:

and

The proof of Lemma 5 is in Section B.5, in which our key argument is to write and in the form of V-statistics (Shieh, 2014). We make two remarks to this crucial lemma.

Remark 3 (Non-degeneracy and validity of pointwise confidence intervals).

We prove in Lemma 13 of Section B.6 that the variances and of the influence functions in (17) are positive for each as long as in model (2). Thus, the asymptotic linearity results in Lemma 5 are non-degenerate. Similarly, one can show that the bootstrap estimates and are also asymptotically linear given the observed data . It indicates that the pointwise bootstrap confidence intervals for and in Section 3.3 are asymptotically valid; see Lemma 23.3 in van der Vaart (1998) and related results in Arcones and Gine (1992); Tang and Westling (2024).

Remark 4 (Bandwidth selection).

In order for those remainder terms of the asymptotically linear forms in Lemma 5 to be of the order , we can choose the bandwidths to be of the order and to be of the order , both of which match the outputs by the usual bandwidth selection methods for nonparametric regression (Wasserman, 2006; Schindler, 2011). In other words, we can tune via the standard bandwidth selectors for estimating the regression function and conditional CDF without any explicit undersmoothing.

Apart from asymptotic linearity, we establish couplings between and (and similarly, for ) in Lemma 5. These coupling results serve as key ingredients for deriving the Gaussian approximations for and in Theorem 6 below and their bootstrap consistencies. Consider two function classes

| (18) |

with defined in (17) respectively. Let be two Gaussian processes indexed by and respectively with zero means and covariance functions

with for any and .

Theorem 6 (Gaussian approximation).

Let in the local polynomial regression for estimating and be a compact set so that is uniformly bounded away from 0 within . Suppose that Assumptions A1, A2, A3, A4, A5, and A6 hold. If and for some such that and for some finite number and as , then there exist Gaussian processes such that

where are defined in (18).

The proof of Theorem 6 is in Section B.6. It demonstrates that the distributions of and can be asymptotically approximated by the suprema of two separate Gaussian processes respectively. To establish the consistency of our bootstrap inference procedure in Section 3.3, it remains to show that the bootstrap versions of the differences and , conditioning on the observed data , can be asymptotically approximated by the suprema of the same Gaussian processes, which are summarized in the following theorem.

Theorem 7 (Bootstrap consistency).

The proof of Theorem 7 is in Section B.7. These results, together with Theorem 6, imply the asymptotic validity of bootstrap uniform confidence bands in Section 3.3; see Corollary 8 below with its proof in Section B.8.

Corollary 8 (Uniform confidence band).

Under the setup of Theorem 7, we have that

5 Experiments

In this section, we evaluate the finite-sample performances of our proposed integral estimator (8) and localized derivative estimator (12) through several simulation studies. We also apply them to analyzing the causal effects of fine particulate matter on the cardiovascular mortality rate as a case study.

5.1 Parameter Setup

Throughout the experiments, we use the Epanechnikov kernel for and (with the product kernel technique) in the (partial) local quadratic regression (10). To choose its default bandwidth parameters , we implement the rule-of-thumb method in Appendix A of Yang and Tschernig (1999) as:

where are defined in Assumption A6(a), with from the local polynomial regression (10) with and (i.e., global (partial) forth-order polynomial fitting), are the differences between coordinatewise maxima and minima that approximate the integration ranges, and are the estimated density-weighted curvatures (or second-order partial derivatives) of . We obtain by fitting coordinatewise global fourth-order polynomials and averaging the estimates over the observed data ; see also Section 4.3 in García Portugués (2023). Here, we set as a bandwidth vector instead of a scalar so that it can be more adaptive to the scale of each covariate. In addition, unless stated otherwise, we set the scaling constants to be for all the experiments. Finally, to maintain fair comparisons between our proposed estimators and the usual regression adjustment estimators in (6) and in Remark 1, we obtain and using the (partial) local quadratic regression (10) with the same choices of bandwidth parameters .

As for the conditional CDF estimator (11), we leverage the Gaussian kernel for and set its default bandwidth parameter to the normal reference rule in Chacón et al. (2011); Chen et al. (2016) as , where is the sample standard deviation of . This rule is obtained by assuming a normal distribution of and optimizing the asymptotic bias-variance trade-off, which could potentially oversmooth the conditional CDF estimator (Sheather, 2004). However, since our proposed estimators of and are not very sensitive to the choice of and the order of aligns with our theoretical requirement (see Remark 4), we would stick to for in the subsequent analysis.

As for the bootstrap inference, we set the resampling time and the significance level , i.e., targeting at 95% confidence intervals and uniform bands for inferring the true dose-response curve and its derivative .

5.2 Simulation Studies

We consider three different model settings under the additive confounding model (3) for our simulation studies. For each model setting, we generate with i.i.d. observations.

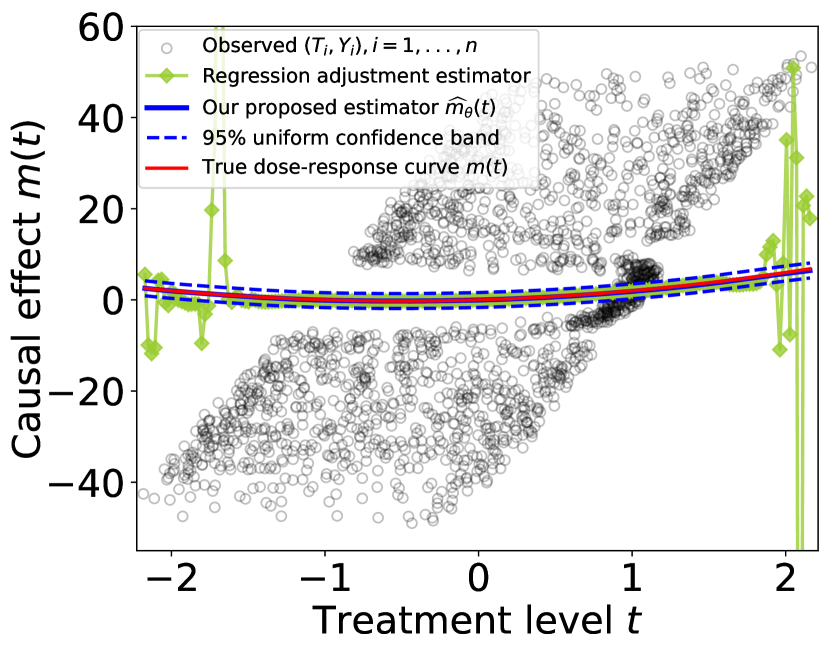

Single Confounder Model: The data-generating model is described in (1).

Linear Confounding Model: We consider the following linear effect model with

| (19) |

where and . The marginal supports of and are and respectively, and the support of conditional density for any is much narrower than .

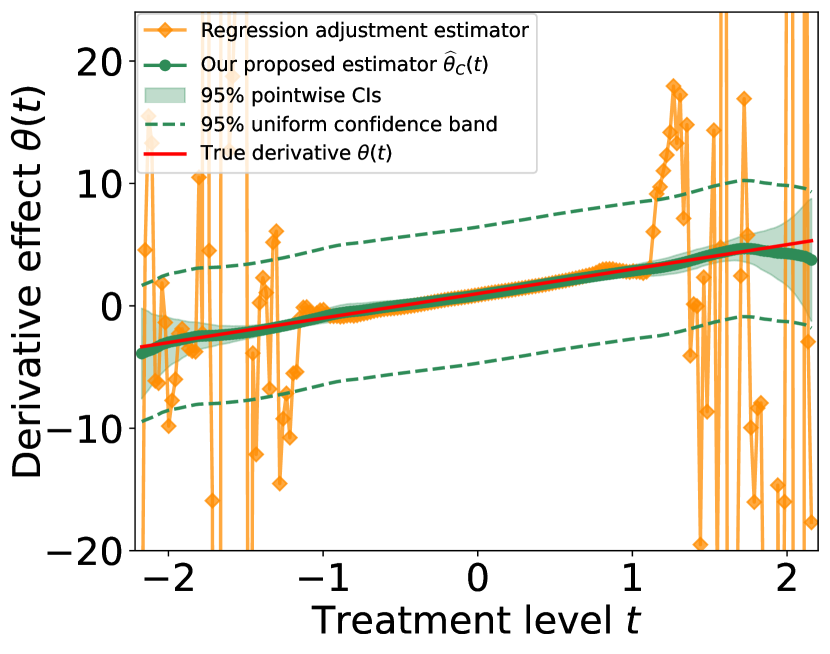

Nonlinear Confounding Model: We consider the following nonlinear effect model with

| (20) | ||||

where and . Again, due to the nonlinear confounding effect and small treatment variation , the positivity condition (A0) fails on the generated data from (20). We also note that the debiased estimator of proposed by Takatsu and Westling (2022) (and similarly, Kennedy et al. 2017) is incapable of recovering under this data model, because some of their pseudo-outcomes have invalid values caused by nearly zero estimated conditional densities of .

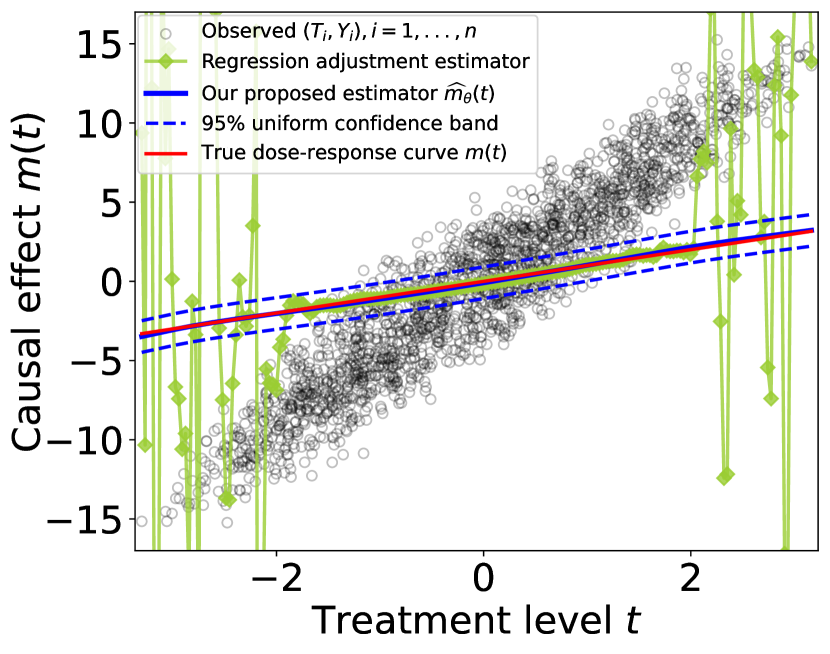

Because of the presence of confounding variables, simply regressing ’s to ’s in the generated data from each of the above models will give rise to biased estimates of . We apply both the proposed integral estimator and localized derivative estimator with bootstrap inferences in Section 3.3 to the generated data respectively. For comparisons, we also implement the usual regression adjustment estimators using the (partial) local quadratic regression (10) under the same choices of bandwidth parameters. The results are shown in Fig 1, Fig 2, and Fig 3. Note that the regression adjustment estimators are extremely unstable, especially around the boundary of the marginal support . Due to the failure of (A0), fine-tuning the bandwidth parameters will not ameliorate the stability and consistency of regression adjustment estimators. On the contrary, our proposed estimators can recover the true dose-response curves and its derivatives with relatively narrow pointwise confidence intervals and uniform bands.

5.3 Case Study: Effect of PM2.5 on Cardiovascular Mortality Rate

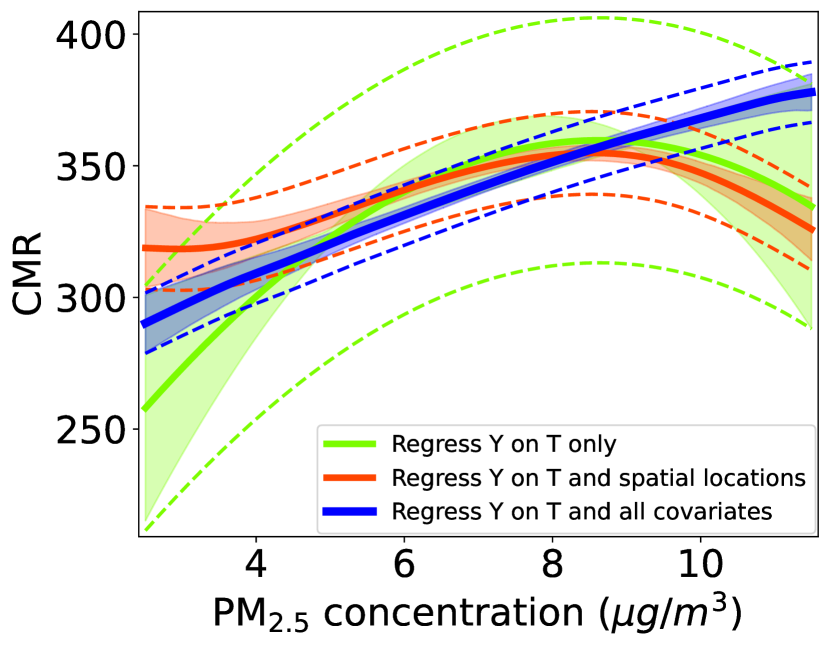

Air pollution, especially fine particulate matter with diameters less than 2.5 (PM2.5), is known to contribute to an increase in cardiovascular diseases (Brook et al., 2010; Krittanawong et al., 2023). Some recent studies also identify a positive association between the PM2.5 level () and the county-level cardiovascular mortality rate (CMR; deaths/100,000 person-years) in the United States after controlling for socioeconomic factors (Wyatt et al., 2020a).

To showcase the applicability of our proposed integral and its derivative estimators, we apply them to analyzing the PM2.5 and CMR data in Wyatt et al. (2020b). The data contain average annual CMR for outcome and PM2.5 concentration for treatment/exposure from 1990 to 2010 within counties, which were obtained from the US National Center for Health Statistics and Community Multiscale Air Quality modeling system, respectively. Our covariate vector comprises two parts of confounding variables. The first part consists of two spatial confounding variables, latitude and longitude of each county, that helps incorporate the spatial dependence. The second part includes eight county-level socioeconomic factors acquired from the US census: population in 2000, civilian unemployment rate, median household income, percentage of female households with no spouse, percentage of vacant housing units, percentage of owner occupied housing units, percentage of high school graduates or above, and percentage of households below poverty. For each county in a given year, we use the closest records from a US census year (1990, 2000, or 2010) as the values of its socioeconomic variables and then average the values of for each county over these 21 years as the final data. Finally, similar to Takatsu and Westling (2022), we focus on the values of PM2.5 between 2.5 and 11.5 to avoid boundary effects.

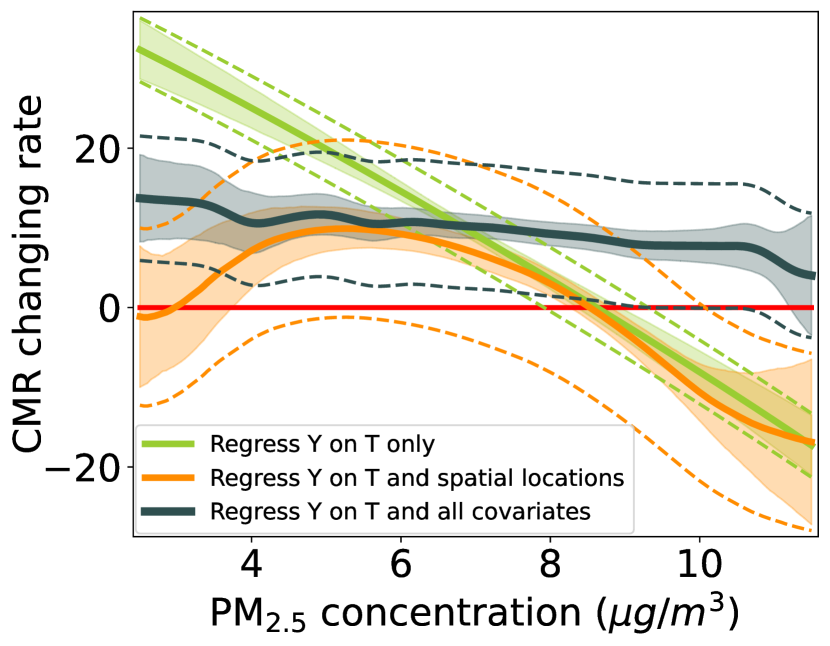

We apply our proposed integral estimator (8) and localized derivative estimator (12) to the final data with the choices of bandwidth parameters in Section 5.1. To take the magnitude differences of treatment and covariates in into consideration, we multiply the (coordinatewise) standard deviations of and on the data to respectively and set to smooth out the estimated derivatives. To study the effects of confounding, we also consider regressing on only via local quadratic regression estimators as well as fitting on and spatial locations only via our proposed estimators. The results in the left panel of Fig 4 demonstrate that the effects of confounding. Before controlling any confounding variables, the fitted curve is not monotonic and peaks at around 8 . After controlling for spatial locations, it becomes flatter but still decreases when PM2.5 level is above 8 . Only when we incorporate both spatial and socioeconomic covariates can the estimated relationship between PM2.5 and CMR becomes monotonically increasing. The estimated changing rate of CMR with respect to PM2.5 in the right panel of Fig 4 reveals the same conclusion from a different angle. More interestingly, after we adjust for all available confounding variables, the changing rate of CMR and its 95% confidence intervals flatten out and are unanimously above 0 when the PM2.5 level is below 9 . This indicates a strong signal of a positive association between the PM2.5 level and CMR. However, when the PM2.5 level is above 10 , it is unclear whether PM2.5 still positively contributes to cardiovascular mortality, possibly due to other competing risks (Leiser et al., 2019). Our findings generally align with the conclusions in Wyatt et al. (2020a); Takatsu and Westling (2022), but the superiority of our proposed estimators comes from two aspects. First, we estimate not only the relationship between PM2.5 and CMR but also its derivative function, providing new insights into their association. Second, our proposed estimators are capable of resolving the potential violation of the positivity condition (A0) and thus lead to convincing conclusions in this observational study.

6 Discussion

In summary, this paper studies nonparametric inference on the dose-response curve and its derivative function via innovative integral and localized derivative estimators. The main advantage of our proposed estimators is that they can consistently recover and infer the dose-response curve and its derivative without assuming the unrealistically strong positivity condition (A0) under the context of continuous treatments. We establish the consistency and bootstrap validity of the proposed estimators when nuisance functions are estimated by kernel smoothing methods but without requiring explicit undersmoothing on bandwidth parameters. Simulation studies and real-world applications demonstrate the effectiveness of our proposed estimators in addressing the failure of (A0). There are several future directions that can further advance the impacts of our proposed estimators.

1. Estimation of nuisance parameters/functions: The proposed integral estimator (8) and localized derivative estimator (12) require us to estimate two nuisance functions, the partial derivative and the conditional CDF . When we focus on the kernel smoothing methods, the finite-sample performances of our integral estimator (8) and localized derivative estimator (12) depend on the choices of three bandwidth parameters . We only consider the rule-of-thumb and normal reference bandwidth selection methods in this paper, but it would be of research interest to study how the bandwidth choices can be improved through the plug-in rule (Ruppert et al., 1995) or cross-validation (Li and Racine, 2004). More broadly, other estimators, such as regression splines for (Friedman, 1991; Zhou and Wolfe, 2000) and nearest neighbor-type or local logistic approaches for (Stute, 1986; Hall et al., 1999), are also be applied to estimating the nuisance functions and may lead to better performances of our proposed estimators and .

2. IPTW and doubly robust estimators: Our proposed estimators (8) and (12) are based on the idea of regression adjustment. Naturally, it would also be interesting to investigate how to leverage our integral and localized techniques to resolve the positivity requirement in the existing generalized propensity score-based approaches (Hirano and Imbens, 2004; Imai and van Dyk, 2004) and doubly robust methods (Kennedy et al., 2017; Westling et al., 2020; Colangelo and Lee, 2020; Semenova and Chernozhukov, 2021; Bonvini and Kennedy, 2022) for estimating the dose-response curve and its derivative function.

3. Additive model diagnostics: Assumption A2 is vital to the consistency of our proposed estimators, and it is unclear if this assumption holds beyond the additive confounding model (3). However, it is possible to utilize our estimators to test the correctness of the additive structure in (3). Under the positivity condition (A0), one can test (3) by estimating the absolute difference of from 0 via the regression adjustment estimator in Remark 1 and our estimator in (12). Other testing procedures, such as the marginal integration regression method (Linton and Nielsen, 1995), are also applicable. When the positivity condition (A0) is violated, the partial derivative is still independent of for any under (3), and our estimator in (10) should not depend on asymptotically. It suggests that statistical quantities, such as and , should converge to 0 as . Thus, one may derive the limiting distribution of or to carry out a procedure for statistically testing the additive confounding model (3) without assuming (A0).

4. Violation of ignorability (Assumption A1(b)): In observational studies, there could be some unmeasured confounding variables that go beyond our covariate vector and bias our inference (VanderWeele, 2008). Hence, it is important to analyze the sensitivities of the dose-response curve and its derivative with respect to the violation of ignorability. In this scenario, the instrumental variable model (Kilbertus et al., 2020) and the Riesz-Frechet representation technique (Chernozhukov et al., 2022) might be useful for the analysis. As an alternative, one can also incorporate an additional high-dimensional covariate vector into our model (2) to avoid unmeasured confounding variables. However, since nonparametric estimations on and have slow rates of convergence when is large, one may consider imposing a linear form on so that

or utilize some orthogonalization techniques in Section 4.3 of Rothenhäusler and Yu (2019) to conduct valid inference. We will leave them as future works.

Acknowledgements

YZ is supported in part by YC’s NSF grant DMS-2141808 and AG’s NSF grant DMS-2310578. YC is supported by NSF grants DMS-1952781, 2112907, 2141808, and NIH U24-AG07212. AG is supported by NSF grant DMS-2310578.

References

- Arcones and Gine (1992) {barticle}[author] \bauthor\bsnmArcones, \bfnmMiguel A.\binitsM. A. and \bauthor\bsnmGine, \bfnmEvarist\binitsE. (\byear1992). \btitleOn the Bootstrap of and Statistics. \bjournalThe Annals of Statistics \bvolume20 \bpages655 – 674. \endbibitem

- Bahadur (1966) {barticle}[author] \bauthor\bsnmBahadur, \bfnmR Raj\binitsR. R. (\byear1966). \btitleA note on quantiles in large samples. \bjournalThe Annals of Mathematical Statistics \bvolume37 \bpages577–580. \endbibitem

- Bashtannyk and Hyndman (2001) {barticle}[author] \bauthor\bsnmBashtannyk, \bfnmDavid M\binitsD. M. and \bauthor\bsnmHyndman, \bfnmRob J\binitsR. J. (\byear2001). \btitleBandwidth selection for kernel conditional density estimation. \bjournalComputational Statistics & Data Analysis \bvolume36 \bpages279–298. \endbibitem

- Bjerve et al. (1985) {barticle}[author] \bauthor\bsnmBjerve, \bfnmSteinar\binitsS., \bauthor\bsnmDoksum, \bfnmKjell A\binitsK. A. and \bauthor\bsnmYandell, \bfnmBrian S\binitsB. S. (\byear1985). \btitleUniform confidence bounds for regression based on a simple moving average. \bjournalScandinavian Journal of Statistics \bpages159–169. \endbibitem

- Bonvini and Kennedy (2022) {barticle}[author] \bauthor\bsnmBonvini, \bfnmMatteo\binitsM. and \bauthor\bsnmKennedy, \bfnmEdward H\binitsE. H. (\byear2022). \btitleFast convergence rates for dose-response estimation. \bjournalarXiv preprint arXiv:2207.11825. \endbibitem

- Brook et al. (2010) {barticle}[author] \bauthor\bsnmBrook, \bfnmRobert D.\binitsR. D., \bauthor\bsnmRajagopalan, \bfnmSanjay\binitsS., \bauthor\bsnmPope, \bfnmC. Arden\binitsC. A., \bauthor\bsnmBrook, \bfnmJeffrey R.\binitsJ. R., \bauthor\bsnmBhatnagar, \bfnmAruni\binitsA., \bauthor\bsnmDiez-Roux, \bfnmAna V.\binitsA. V., \bauthor\bsnmHolguin, \bfnmFernando\binitsF., \bauthor\bsnmHong, \bfnmYuling\binitsY., \bauthor\bsnmLuepker, \bfnmRussell V.\binitsR. V., \bauthor\bsnmMittleman, \bfnmMurray A.\binitsM. A., \bauthor\bsnmPeters, \bfnmAnnette\binitsA., \bauthor\bsnmSiscovick, \bfnmDavid\binitsD., \bauthor\bsnmSmith, \bfnmSidney C.\binitsS. C., \bauthor\bsnmWhitsel, \bfnmLaurie\binitsL. and \bauthor\bsnmKaufman, \bfnmJoel D.\binitsJ. D. (\byear2010). \btitleParticulate matter air pollution and cardiovascular disease: an update to the scientific statement from the American Heart Association. \bjournalCirculation \bvolume121 \bpages2331–2378. \endbibitem

- Buja et al. (1989) {barticle}[author] \bauthor\bsnmBuja, \bfnmAndreas\binitsA., \bauthor\bsnmHastie, \bfnmTrevor\binitsT. and \bauthor\bsnmTibshirani, \bfnmRobert\binitsR. (\byear1989). \btitleLinear Smoothers and Additive Models. \bjournalThe Annals of Statistics \bvolume17 \bpages453 – 510. \endbibitem

- Busso et al. (2014) {barticle}[author] \bauthor\bsnmBusso, \bfnmMatias\binitsM., \bauthor\bsnmDiNardo, \bfnmJohn\binitsJ. and \bauthor\bsnmMcCrary, \bfnmJustin\binitsJ. (\byear2014). \btitleNew evidence on the finite sample properties of propensity score reweighting and matching estimators. \bjournalReview of Economics and Statistics \bvolume96 \bpages885–897. \endbibitem

- Calonico et al. (2018) {barticle}[author] \bauthor\bsnmCalonico, \bfnmSebastian\binitsS., \bauthor\bsnmCattaneo, \bfnmMatias D\binitsM. D. and \bauthor\bsnmFarrell, \bfnmMax H\binitsM. H. (\byear2018). \btitleOn the effect of bias estimation on coverage accuracy in nonparametric inference. \bjournalJournal of the American Statistical Association \bvolume113 \bpages767–779. \endbibitem

- Cattaneo et al. (2010) {barticle}[author] \bauthor\bsnmCattaneo, \bfnmMatias D\binitsM. D., \bauthor\bsnmCrump, \bfnmRichard K\binitsR. K. and \bauthor\bsnmJansson, \bfnmMichael\binitsM. (\byear2010). \btitleRobust data-driven inference for density-weighted average derivatives. \bjournalJournal of the American Statistical Association \bvolume105 \bpages1070–1083. \endbibitem

- Chacón et al. (2011) {barticle}[author] \bauthor\bsnmChacón, \bfnmJosé E\binitsJ. E., \bauthor\bsnmDuong, \bfnmTarn\binitsT. and \bauthor\bsnmWand, \bfnmMP\binitsM. (\byear2011). \btitleAsymptotics for general multivariate kernel density derivative estimators. \bjournalStatistica Sinica \bpages807–840. \endbibitem

- Chamberlain (1986) {barticle}[author] \bauthor\bsnmChamberlain, \bfnmGary\binitsG. (\byear1986). \btitleAsymptotic efficiency in semi-parametric models with censoring. \bjournalJournal of Econometrics \bvolume32 \bpages189–218. \endbibitem

- Chen et al. (2015) {barticle}[author] \bauthor\bsnmChen, \bfnmYen-Chi\binitsY.-C., \bauthor\bsnmGenovese, \bfnmChristopher R.\binitsC. R. and \bauthor\bsnmWasserman, \bfnmLarry\binitsL. (\byear2015). \btitleAsymptotic theory for density ridges. \bjournalThe Annals of Statistics \bvolume43 \bpages1896–1928. \endbibitem

- Chen et al. (2016) {barticle}[author] \bauthor\bsnmChen, \bfnmYen-Chi\binitsY.-C., \bauthor\bsnmGenovese, \bfnmChristopher R.\binitsC. R. and \bauthor\bsnmWasserman, \bfnmLarry\binitsL. (\byear2016). \btitleA comprehensive approach to mode clustering. \bjournalElectronic Journal of Statistics \bvolume10 \bpages210 – 241. \endbibitem

- Chen et al. (2017) {barticle}[author] \bauthor\bsnmChen, \bfnmYen-Chi\binitsY.-C., \bauthor\bsnmGenovese, \bfnmChristopher R\binitsC. R. and \bauthor\bsnmWasserman, \bfnmLarry\binitsL. (\byear2017). \btitleDensity level sets: Asymptotics, inference, and visualization. \bjournalJournal of the American Statistical Association \bvolume112 \bpages1684–1696. \endbibitem

- Cheng and Chen (2019) {barticle}[author] \bauthor\bsnmCheng, \bfnmGang\binitsG. and \bauthor\bsnmChen, \bfnmYen-Chi\binitsY.-C. (\byear2019). \btitleNonparametric inference via bootstrapping the debiased estimator. \bjournalElectronic Journal of Statistics \bvolume13 \bpages2194 – 2256. \endbibitem

- Chernozhukov et al. (2014) {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmChetverikov, \bfnmDenis\binitsD. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2014). \btitleGaussian approximation of suprema of empirical processes. \bjournalThe Annals of Statistics \bvolume42 \bpages1564–1597. \endbibitem

- Chernozhukov et al. (2022) {btechreport}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmCinelli, \bfnmCarlos\binitsC., \bauthor\bsnmNewey, \bfnmWhitney\binitsW., \bauthor\bsnmSharma, \bfnmAmit\binitsA. and \bauthor\bsnmSyrgkanis, \bfnmVasilis\binitsV. (\byear2022). \btitleLong story short: Omitted variable bias in causal machine learning \btypeTechnical Report, \bpublisherNational Bureau of Economic Research. \endbibitem

- Colangelo and Lee (2020) {barticle}[author] \bauthor\bsnmColangelo, \bfnmKyle\binitsK. and \bauthor\bsnmLee, \bfnmYing-Ying\binitsY.-Y. (\byear2020). \btitleDouble debiased machine learning nonparametric inference with continuous treatments. \bjournalarXiv preprint arXiv:2004.03036. \endbibitem

- Cole and Hernán (2008) {barticle}[author] \bauthor\bsnmCole, \bfnmStephen R\binitsS. R. and \bauthor\bsnmHernán, \bfnmMiguel A\binitsM. A. (\byear2008). \btitleConstructing inverse probability weights for marginal structural models. \bjournalAmerican Journal of Epidemiology \bvolume168 \bpages656–664. \endbibitem

- Cox (1958) {bbook}[author] \bauthor\bsnmCox, \bfnmDavid Roxbee\binitsD. R. (\byear1958). \btitlePlanning of Experiments. \bpublisherWiley. \endbibitem

- Crump et al. (2009) {barticle}[author] \bauthor\bsnmCrump, \bfnmRichard K\binitsR. K., \bauthor\bsnmHotz, \bfnmV Joseph\binitsV. J., \bauthor\bsnmImbens, \bfnmGuido W\binitsG. W. and \bauthor\bsnmMitnik, \bfnmOscar A\binitsO. A. (\byear2009). \btitleDealing with limited overlap in estimation of average treatment effects. \bjournalBiometrika \bvolume96 \bpages187–199. \endbibitem

- Dehejia and Wahba (1999) {barticle}[author] \bauthor\bsnmDehejia, \bfnmRajeev H\binitsR. H. and \bauthor\bsnmWahba, \bfnmSadek\binitsS. (\byear1999). \btitleCausal effects in nonexperimental studies: Reevaluating the evaluation of training programs. \bjournalJournal of the American statistical Association \bvolume94 \bpages1053–1062. \endbibitem

- Díaz and van der Laan (2013) {barticle}[author] \bauthor\bsnmDíaz, \bfnmIván\binitsI. and \bauthor\bparticlevan der \bsnmLaan, \bfnmMark J\binitsM. J. (\byear2013). \btitleTargeted data adaptive estimation of the causal dose–response curve. \bjournalJournal of Causal Inference \bvolume1 \bpages171–192. \endbibitem

- Dvoretzky et al. (1956) {barticle}[author] \bauthor\bsnmDvoretzky, \bfnmA.\binitsA., \bauthor\bsnmKiefer, \bfnmJ.\binitsJ. and \bauthor\bsnmWolfowitz, \bfnmJ.\binitsJ. (\byear1956). \btitleAsymptotic Minimax Character of the Sample Distribution Function and of the Classical Multinomial Estimator. \bjournalThe Annals of Mathematical Statistics \bvolume27 \bpages642 – 669. \endbibitem

- D’Amour et al. (2021) {barticle}[author] \bauthor\bsnmD’Amour, \bfnmAlexander\binitsA., \bauthor\bsnmDing, \bfnmPeng\binitsP., \bauthor\bsnmFeller, \bfnmAvi\binitsA., \bauthor\bsnmLei, \bfnmLihua\binitsL. and \bauthor\bsnmSekhon, \bfnmJasjeet\binitsJ. (\byear2021). \btitleOverlap in observational studies with high-dimensional covariates. \bjournalJournal of Econometrics \bvolume221 \bpages644–654. \endbibitem

- Efron (1979) {barticle}[author] \bauthor\bsnmEfron, \bfnmBradley\binitsB. (\byear1979). \btitleBootstrap Methods: Another Look at the Jackknife. \bjournalThe Annals of Statistics \bvolume7 \bpages1 – 26. \endbibitem

- Einmahl and Mason (2005) {barticle}[author] \bauthor\bsnmEinmahl, \bfnmUwe\binitsU. and \bauthor\bsnmMason, \bfnmDavid M.\binitsD. M. (\byear2005). \btitleUniform in bandwidth consistency of kernel-type function estimators. \bjournalThe Annals of Statistics \bvolume33 \bpages1380 – 1403. \endbibitem

- Fan and Gijbels (1996) {bbook}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ. and \bauthor\bsnmGijbels, \bfnmIrene\binitsI. (\byear1996). \btitleLocal polynomial modelling and its applications \bvolume66. \bpublisherChapman & Hall/CRC. \endbibitem

- Fan and Guerre (2015) {barticle}[author] \bauthor\bsnmFan, \bfnmYanqin\binitsY. and \bauthor\bsnmGuerre, \bfnmEmmanuel\binitsE. (\byear2015). \btitleMultivariate Local Polynomial Estimators: Boundary Properties and Uniform Asymptotic Linear Representation. \bjournalAdvances in Econometrics. \endbibitem

- Fan et al. (1996) {barticle}[author] \bauthor\bsnmFan, \bfnmJianqing\binitsJ., \bauthor\bsnmGijbels, \bfnmIrène\binitsI., \bauthor\bsnmHu, \bfnmTien-Chung\binitsT.-C. and \bauthor\bsnmHuang, \bfnmLi-Shan\binitsL.-S. (\byear1996). \btitleA study of variable bandwidth selection for local polynomial regression. \bjournalStatistica Sinica \bvolume6 \bpages113–127. \endbibitem

- Flores (2007) {btechreport}[author] \bauthor\bsnmFlores, \bfnmCarlos\binitsC. (\byear2007). \btitleEstimation of dose-response functions and optimal doses with a continuous treatment \btypeTechnical Report, \bpublisherDepartment of Economics, University of Miami. \endbibitem

- Freedman (1981) {barticle}[author] \bauthor\bsnmFreedman, \bfnmDavid A\binitsD. A. (\byear1981). \btitleBootstrapping regression models. \bjournalThe Annals of Statistics \bvolume9 \bpages1218–1228. \endbibitem

- Friedman (1991) {barticle}[author] \bauthor\bsnmFriedman, \bfnmJerome H\binitsJ. H. (\byear1991). \btitleMultivariate adaptive regression splines. \bjournalThe Annals of Statistics \bvolume19 \bpages1–67. \endbibitem

- García Portugués (2023) {bmisc}[author] \bauthor\bsnmGarcía Portugués, \bfnmEduardo\binitsE. (\byear2023). \btitleNotes for nonparametric statistics. \bnote(Accessed on March 26, 2024). \endbibitem

- Giessing (2023) {barticle}[author] \bauthor\bsnmGiessing, \bfnmAlexander\binitsA. (\byear2023). \btitleGaussian and Bootstrap Approximations for Suprema of Empirical Processes. \bjournalarXiv preprint arXiv:2309.01307. \endbibitem

- Gilbert et al. (2023) {barticle}[author] \bauthor\bsnmGilbert, \bfnmBrian\binitsB., \bauthor\bsnmDatta, \bfnmAbhirup\binitsA., \bauthor\bsnmCasey, \bfnmJoan A.\binitsJ. A. and \bauthor\bsnmOgburn, \bfnmElizabeth L.\binitsE. L. (\byear2023). \btitleA causal inference framework for spatial confounding. \bjournalarXiv preprint arXiv:2112.14946. \endbibitem

- Gill and Robins (2001) {barticle}[author] \bauthor\bsnmGill, \bfnmRichard D\binitsR. D. and \bauthor\bsnmRobins, \bfnmJames M\binitsJ. M. (\byear2001). \btitleCausal inference for complex longitudinal data: the continuous case. \bjournalAnnals of Statistics \bvolume29 \bpages1785–1811. \endbibitem

- Giné and Guillou (2002) {barticle}[author] \bauthor\bsnmGiné, \bfnmEvarist\binitsE. and \bauthor\bsnmGuillou, \bfnmArmelle\binitsA. (\byear2002). \btitleRates of strong uniform consistency for multivariate kernel density estimators. \bjournalAnnales de l’Institut Henri Poincare (B) Probability and Statistics \bvolume38 \bpages907–921. \endbibitem

- Hall (1992) {barticle}[author] \bauthor\bsnmHall, \bfnmPeter\binitsP. (\byear1992). \btitleOn bootstrap confidence intervals in nonparametric regression. \bjournalThe Annals of Statistics \bvolume20 \bpages695–711. \endbibitem

- Hall et al. (1999) {barticle}[author] \bauthor\bsnmHall, \bfnmPeter\binitsP., \bauthor\bsnmWolff, \bfnmRodney CL\binitsR. C. and \bauthor\bsnmYao, \bfnmQiwei\binitsQ. (\byear1999). \btitleMethods for estimating a conditional distribution function. \bjournalJournal of the American Statistical Association \bvolume94 \bpages154–163. \endbibitem

- Härdle and Stoker (1989) {barticle}[author] \bauthor\bsnmHärdle, \bfnmWolfgang\binitsW. and \bauthor\bsnmStoker, \bfnmThomas M\binitsT. M. (\byear1989). \btitleInvestigating smooth multiple regression by the method of average derivatives. \bjournalJournal of the American statistical Association \bvolume84 \bpages986–995. \endbibitem

- Hastie and Loader (1993) {barticle}[author] \bauthor\bsnmHastie, \bfnmTrevor\binitsT. and \bauthor\bsnmLoader, \bfnmClive\binitsC. (\byear1993). \btitleLocal regression: Automatic kernel carpentry. \bjournalStatistical Science \bpages120–129. \endbibitem

- Hines et al. (2023) {barticle}[author] \bauthor\bsnmHines, \bfnmOliver\binitsO., \bauthor\bsnmDiaz-Ordaz, \bfnmKarla\binitsK. and \bauthor\bsnmVansteelandt, \bfnmStijn\binitsS. (\byear2023). \btitleOptimally weighted average derivative effects. \bjournalarXiv preprint arXiv:2308.05456. \endbibitem

- Hirano and Imbens (2004) {barticle}[author] \bauthor\bsnmHirano, \bfnmKeisuke\binitsK. and \bauthor\bsnmImbens, \bfnmGuido W\binitsG. W. (\byear2004). \btitleThe propensity score with continuous treatments. \bjournalApplied Bayesian modeling and causal inference from incomplete-data perspectives \bvolume226164 \bpages73–84. \endbibitem

- Hirshberg and Wager (2020) {barticle}[author] \bauthor\bsnmHirshberg, \bfnmDavid A\binitsD. A. and \bauthor\bsnmWager, \bfnmStefan\binitsS. (\byear2020). \btitleDebiased inference of average partial effects in single-index models: Comment on wooldridge and zhu. \bjournalJournal of Business & Economic Statistics \bvolume38 \bpages19–24. \endbibitem

- Holmes et al. (2012) {barticle}[author] \bauthor\bsnmHolmes, \bfnmMichael P\binitsM. P., \bauthor\bsnmGray, \bfnmAlexander G\binitsA. G. and \bauthor\bsnmIsbell, \bfnmCharles Lee\binitsC. L. (\byear2012). \btitleFast nonparametric conditional density estimation. \bjournalarXiv preprint arXiv:1206.5278. \endbibitem

- Huber et al. (2020) {barticle}[author] \bauthor\bsnmHuber, \bfnmMartin\binitsM., \bauthor\bsnmHsu, \bfnmYu-Chin\binitsY.-C., \bauthor\bsnmLee, \bfnmYing-Ying\binitsY.-Y. and \bauthor\bsnmLettry, \bfnmLayal\binitsL. (\byear2020). \btitleDirect and indirect effects of continuous treatments based on generalized propensity score weighting. \bjournalJournal of Applied Econometrics \bvolume35 \bpages814–840. \endbibitem

- Imai and van Dyk (2004) {barticle}[author] \bauthor\bsnmImai, \bfnmKosuke\binitsK. and \bauthor\bparticlevan \bsnmDyk, \bfnmDavid A\binitsD. A. (\byear2004). \btitleCausal inference with general treatment regimes: Generalizing the propensity score. \bjournalJournal of the American Statistical Association \bvolume99 \bpages854–866. \endbibitem

- Kammann and Wand (2003) {barticle}[author] \bauthor\bsnmKammann, \bfnmEE\binitsE. and \bauthor\bsnmWand, \bfnmMatthew P\binitsM. P. (\byear2003). \btitleGeoadditive models. \bjournalJournal of the Royal Statistical Society Series C: Applied Statistics \bvolume52 \bpages1–18. \endbibitem

- Keller and Szpiro (2020) {barticle}[author] \bauthor\bsnmKeller, \bfnmJoshua P\binitsJ. P. and \bauthor\bsnmSzpiro, \bfnmAdam A\binitsA. A. (\byear2020). \btitleSelecting a scale for spatial confounding adjustment. \bjournalJournal of the Royal Statistical Society Series A: Statistics in Society \bvolume183 \bpages1121–1143. \endbibitem

- Kennedy (2019) {barticle}[author] \bauthor\bsnmKennedy, \bfnmEdward H\binitsE. H. (\byear2019). \btitleNonparametric causal effects based on incremental propensity score interventions. \bjournalJournal of the American Statistical Association \bvolume114 \bpages645–656. \endbibitem

- Kennedy et al. (2017) {barticle}[author] \bauthor\bsnmKennedy, \bfnmEdward H\binitsE. H., \bauthor\bsnmMa, \bfnmZongming\binitsZ., \bauthor\bsnmMcHugh, \bfnmMatthew D\binitsM. D. and \bauthor\bsnmSmall, \bfnmDylan S\binitsD. S. (\byear2017). \btitleNonparametric methods for doubly robust estimation of continuous treatment effects. \bjournalJournal of the Royal Statistical Society Series B: Statistical Methodology \bvolume79 \bpages1229–1245. \endbibitem

- Khan and Tamer (2010) {barticle}[author] \bauthor\bsnmKhan, \bfnmShakeeb\binitsS. and \bauthor\bsnmTamer, \bfnmElie\binitsE. (\byear2010). \btitleIrregular identification, support conditions, and inverse weight estimation. \bjournalEconometrica \bvolume78 \bpages2021–2042. \endbibitem

- Kilbertus et al. (2020) {barticle}[author] \bauthor\bsnmKilbertus, \bfnmNiki\binitsN., \bauthor\bsnmKusner, \bfnmMatt J\binitsM. J. and \bauthor\bsnmSilva, \bfnmRicardo\binitsR. (\byear2020). \btitleA class of algorithms for general instrumental variable models. \bjournalAdvances in Neural Information Processing Systems \bvolume33 \bpages20108–20119. \endbibitem

- Kong et al. (2010) {barticle}[author] \bauthor\bsnmKong, \bfnmEfang\binitsE., \bauthor\bsnmLinton, \bfnmOliver\binitsO. and \bauthor\bsnmXia, \bfnmYingcun\binitsY. (\byear2010). \btitleUniform Bahadur representation for local polynomial estimates of M-regression and its application to the additive model. \bjournalEconometric Theory \bvolume26 \bpages1529–1564. \endbibitem

- Krittanawong et al. (2023) {barticle}[author] \bauthor\bsnmKrittanawong, \bfnmChayakrit\binitsC., \bauthor\bsnmQadeer, \bfnmYusuf Kamran\binitsY. K., \bauthor\bsnmHayes, \bfnmRichard B.\binitsR. B., \bauthor\bsnmWang, \bfnmZhen\binitsZ., \bauthor\bsnmThurston, \bfnmGeorge D.\binitsG. D., \bauthor\bsnmVirani, \bfnmSalim\binitsS. and \bauthor\bsnmLavie, \bfnmCarl J.\binitsC. J. (\byear2023). \btitlePM2.5 and cardiovascular diseases: State-of-the-Art review. \bjournalInternational Journal of Cardiology Cardiovascular Risk and Prevention \bvolume19 \bpages200217. \endbibitem

- Léger et al. (2022) {barticle}[author] \bauthor\bsnmLéger, \bfnmMaxime\binitsM., \bauthor\bsnmChatton, \bfnmArthur\binitsA., \bauthor\bsnmLe Borgne, \bfnmFlorent\binitsF., \bauthor\bsnmPirracchio, \bfnmRomain\binitsR., \bauthor\bsnmLasocki, \bfnmSigismond\binitsS. and \bauthor\bsnmFoucher, \bfnmYohann\binitsY. (\byear2022). \btitleCausal inference in case of near-violation of positivity: comparison of methods. \bjournalBiometrical Journal \bvolume64 \bpages1389–1403. \endbibitem

- Leiser et al. (2019) {barticle}[author] \bauthor\bsnmLeiser, \bfnmClaire L\binitsC. L., \bauthor\bsnmSmith, \bfnmKen R\binitsK. R., \bauthor\bsnmVanDerslice, \bfnmJames A\binitsJ. A., \bauthor\bsnmGlotzbach, \bfnmJason P\binitsJ. P., \bauthor\bsnmFarrell, \bfnmTimothy W\binitsT. W. and \bauthor\bsnmHanson, \bfnmHeidi A\binitsH. A. (\byear2019). \btitleEvaluation of the sex-and-age-specific effects of PM2. 5 on hospital readmission in the presence of the competing risk of mortality in the medicare population of Utah 1999–2009. \bjournalJournal of Clinical Medicine \bvolume8 \bpages2114. \endbibitem

- Li and Racine (2004) {barticle}[author] \bauthor\bsnmLi, \bfnmQi\binitsQ. and \bauthor\bsnmRacine, \bfnmJeff\binitsJ. (\byear2004). \btitleCross-validated local linear nonparametric regression. \bjournalStatistica Sinica \bpages485–512. \endbibitem

- Linton and Nielsen (1995) {barticle}[author] \bauthor\bsnmLinton, \bfnmOliver\binitsO. and \bauthor\bsnmNielsen, \bfnmJens Perch\binitsJ. P. (\byear1995). \btitleA Kernel Method of Estimating Structured Nonparametric Regression Based on Marginal Integration. \bjournalBiometrika \bvolume82 \bpages93–100. \endbibitem

- Lu (1996) {barticle}[author] \bauthor\bsnmLu, \bfnmZhan-Qian\binitsZ.-Q. (\byear1996). \btitleMultivariate locally weighted polynomial fitting and partial derivative estimation. \bjournalJournal of Multivariate Analysis \bvolume59 \bpages187–205. \endbibitem

- Ma and Wang (2020) {barticle}[author] \bauthor\bsnmMa, \bfnmXinwei\binitsX. and \bauthor\bsnmWang, \bfnmJingshen\binitsJ. (\byear2020). \btitleRobust inference using inverse probability weighting. \bjournalJournal of the American Statistical Association \bvolume115 \bpages1851–1860. \endbibitem

- Manski (1990) {barticle}[author] \bauthor\bsnmManski, \bfnmCharles F\binitsC. F. (\byear1990). \btitleNonparametric bounds on treatment effects. \bjournalThe American Economic Review \bvolume80 \bpages319–323. \endbibitem

- Massart (1990) {barticle}[author] \bauthor\bsnmMassart, \bfnmPascal\binitsP. (\byear1990). \btitleThe tight constant in the Dvoretzky-Kiefer-Wolfowitz inequality. \bjournalThe Annals of Probability \bvolume18 \bpages1269–1283. \endbibitem

- Neugebauer and van der Laan (2007) {barticle}[author] \bauthor\bsnmNeugebauer, \bfnmRomain\binitsR. and \bauthor\bparticlevan der \bsnmLaan, \bfnmMark\binitsM. (\byear2007). \btitleNonparametric causal effects based on marginal structural models. \bjournalJournal of Statistical Planning and Inference \bvolume137 \bpages419–434. \endbibitem

- Newey (1994) {barticle}[author] \bauthor\bsnmNewey, \bfnmWhitney K\binitsW. K. (\byear1994). \btitleKernel estimation of partial means and a general variance estimator. \bjournalEconometric Theory \bvolume10 \bpages1–21. \endbibitem

- Newey and Stoker (1993) {barticle}[author] \bauthor\bsnmNewey, \bfnmWhitney K\binitsW. K. and \bauthor\bsnmStoker, \bfnmThomas M\binitsT. M. (\byear1993). \btitleEfficiency of weighted average derivative estimators and index models. \bjournalEconometrica \bvolume61 \bpages1199–1223. \endbibitem

- Nolan and Pollard (1987) {barticle}[author] \bauthor\bsnmNolan, \bfnmDeborah\binitsD. and \bauthor\bsnmPollard, \bfnmDavid\binitsD. (\byear1987). \btitle-Processes: Rates of Convergence. \bjournalThe Annals of Statistics \bvolume15 \bpages780 – 799. \endbibitem

- Paciorek (2010) {barticle}[author] \bauthor\bsnmPaciorek, \bfnmChristopher J\binitsC. J. (\byear2010). \btitleThe importance of scale for spatial-confounding bias and precision of spatial regression estimators. \bjournalStatistical Science \bvolume25 \bpages107-125. \endbibitem

- Petersen et al. (2012) {barticle}[author] \bauthor\bsnmPetersen, \bfnmMaya L\binitsM. L., \bauthor\bsnmPorter, \bfnmKristin E\binitsK. E., \bauthor\bsnmGruber, \bfnmSusan\binitsS., \bauthor\bsnmWang, \bfnmYue\binitsY. and \bauthor\bsnmVan Der Laan, \bfnmMark J\binitsM. J. (\byear2012). \btitleDiagnosing and responding to violations in the positivity assumption. \bjournalStatistical methods in medical research \bvolume21 \bpages31–54. \endbibitem

- Powell et al. (1989) {barticle}[author] \bauthor\bsnmPowell, \bfnmJames L\binitsJ. L., \bauthor\bsnmStock, \bfnmJames H\binitsJ. H. and \bauthor\bsnmStoker, \bfnmThomas M\binitsT. M. (\byear1989). \btitleSemiparametric estimation of index coefficients. \bjournalEconometrica \bpages1403–1430. \endbibitem