Some Statistical and Data Challenges When Building Early-Stage Digital Experimentation and Measurement Capabilities

Abstract

Digital experimentation and measurement (DEM) capabilities – the knowledge and tools necessary to run experiments with digital products, services, or experiences and measure their impact – are fast becoming part of the standard toolkit of digital/data-driven organisations in guiding business decisions. Many large technology companies report having mature DEM capabilities, and several businesses have been established purely to manage experiments for others. Given the growing evidence that data-driven organisations tend to outperform their non-data-driven counterparts, there has never been a greater need for organisations to build/acquire DEM capabilities to thrive in the current digital era.

This thesis presents several novel approaches to statistical and data challenges for organisations building DEM capabilities. We focus on the fundamentals associated with building DEM capabilities, which lead to a richer understanding of the underlying assumptions and thus enable us to develop more appropriate capabilities. We address why one should engage in DEM by quantifying the benefits and risks of acquiring DEM capabilities. This is done using a ranking under lower uncertainty model, enabling one to construct a business case. We also examine what ingredients are necessary to run digital experiments. In addition to clarifying the existing literature around statistical tests, datasets, and methods in experimental design and causal inference, we construct an additional dataset and detailed case studies on applying state-of-the-art methods. Finally, we investigate when a digital experiment design would outperform another, leading to an evaluation framework that compares competing designs’ data efficiency.

These approaches aim to enable one to run experiments that produce less biased estimates more quickly and adapt to various business constraints. As we maintain the theoretical rigour, we also emphasise applied use cases, interpretable processes/results, and practical tradeoffs, all to ensure that the contributions are accessible to researchers and practitioners from diverse scientific backgrounds.

I confirm that the thesis reports original research work done by myself during the programme of study. The thesis has not been submitted elsewhere for examination for a PhD degree. Part of the thesis is adapted from research papers that I first-authored and published during the programme of study. They are listed in Section 1.4 and stated at the beginning of relevant chapters where applicable. In addition, I have appropriately referenced ideas from others in the thesis and sought the necessary permission to use copyrighted materials.

The thesis is written at a time when large language models (LLMs) are sufficiently advanced to produce ”human-like” writing on an arbitrary topic and refine the text based on external prompts. I see much potential with such technology in research and industry practice. That said, the use of LLMs in academic writing remains highly controversial as of 2023, with many unresolved issues on correctness, academic integrity and plagiarism, and publishing ethics [2].

As such, I also confirm that I did not use any LLMs or services derived from them to write this thesis. That said, I used (the non-LLM part of) Grammarly, an online contextual proofreading platform, to help correct the written text’s spelling, punctuation, and grammar. The platform also flags redundant, overused, or informal phrases and sentences based on set rules to help improve the overall delivery of the thesis. However, the decision to incorporate the suggestions solely rests with me.

The copyright of this thesis rests with the author. Unless otherwise indicated, its contents are licensed under a Creative Commons Attribution 4.0 International Licence (CC BY 4.0).

Under this licence, you may copy and redistribute the material in any medium or format for both commercial and non-commercial purposes. You may also create and distribute modified versions of the work. This on the condition that you credit the author.

When reusing or sharing this work, ensure you make the licence terms clear to others by naming the licence and linking to the licence text. Where a work has been adapted, you should indicate that the work has been changed and describe those changes.

Please seek permission from the copyright holder for uses of this work that are not included in this licence or permitted under UK Copyright Law.

Acknowledgements

Academic research is never a solo effort, and I would like to acknowledge the many people who have helped, in various ways, for me to deliver this thesis.

First and foremost, I would like to thank my supervisor, Prof Emma McCoy, for her consistent support and guidance throughout the years. She has suggested many worthy research directions, challenged many potential ideas, and helped clarify my exposition on many topics. I would also like to thank Dr Seth Flaxman and Prof Robin Evans for the initial project idea discussions, as well as Prof Niall Adams, Dr Ciara Pike-Burke, Prof Nick Heard, and the anonymous reviewers for their feedback during the initial stages of the PhD.

I am fortunate to have met many collaborators whom I enjoy the many intellectually stimulating discussions and opportunities to publicise the latest results in high-impact venues with: Dr Elaine Bettaney, Dr Ângelo Cardoso, Dr Benjamin Chamberlain, Paul Couturier, Prof Marc Deisenroth, Georg Grob, Dr Duncan Little, and Dr Roberto Pagliari. I have also met many bright minds at Imperial College London and the University of Oxford, many affiliated with the EPSRC CDT in Modern Statistics and Statistical Machine Learning (StatML CDT), whose conversations provided me with new perspectives on the challenges at hand and enabled me to discover new opportunities.

The thesis is one of the many outputs from a fruitful academic-industry collaboration between the StatML CDT at Imperial and Oxford and the AI and Data Science Platform at ASOS.com, with myself also employed at the latter as a data/machine learning scientist. I am blessed to have also worked with and learnt from many talented colleagues at ASOS, including my managers Dr Benjamin Chamberlain, Papinder Dosanjh, and Dawn Rollocks; my teammates in the Customer Understanding (2016–18), Experimentation (2018–19), Prophecy (2019–20), Cassandra (2020), Kernel (2021–22), Experimentation (2022), and the Alchemists (2022–23) teams; and many more unnamed. Among other things, they have ensured that my research remains relevant to industry applications. The research is also generously funded by the two organisations mentioned above (EPSRC grant no. EP/S023151/1), without which I probably would not have taken on the PhD programme at all.

Finally, I would like to thank my friends and family, especially my mum Yvonne, my dad Haston, my sister Nicole, and my grandmother Cecilia, for their love and warm encouragement while I took on the ambitious task of studying a PhD while holding an industry job. My PhD years were dominated by the COVID-19 pandemic, and travel restrictions have made visiting them virtually impossible for a few years. Fortunately, the availability of economical video calls has made the isolation much more bearable.

“The true method of knowledge is experiment.”

– William Blake

“Negative results are just what I want. They’re just as valuable to me as positive results. I can never find the thing that does the job best until I find the ones that don’t.”

– Thomas A. Edison

“An experiment is a question which science poses to Nature and a measurement is the recording of Nature’s answer.”

– Max Planck

“Measurement is the first step that leads to control and eventually to improvement. If you can’t measure something, you can’t understand it. If you can’t understand it, you can’t control it. If you can’t control it, you can’t improve it.”

– H. James Harrington

Chapter 1 Introduction

1.1 Motivation

The value of making data-driven or data-informed decisions has become increasingly clear in recent years [187, 256]. Key to making data-driven decisions is the ability to accurately measure a given choice’s impact and experiment with possible alternatives. We define digital experimentation and measurement (DEM) capabilities as the knowledge and tools necessary to run experiments (controlled or otherwise) with different digital products, services, or experiences and measure their impact. The capabilities may be an online controlled experiment framework, a team of analysts, or a system capable of performing machine learning-aided causal inference.

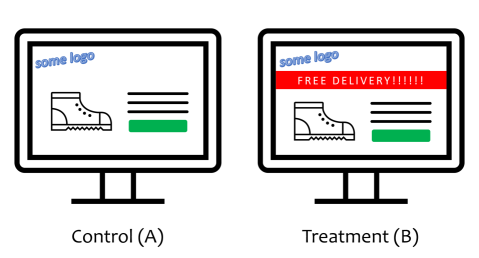

The simplest example of a digital experiment is what is commonly known as an A/B test [155]. Suppose we are interested in whether offering free delivery to users of an e-commerce website will lead to more of them making a purchase (i.e., an increased conversion rate in business speak). We set up an experiment where incoming users are randomly split into two groups, where one group is shown a ”free delivery” banner on the website (the treatment), while the other acts as the control – being shown the original website without any mention of free delivery (see Figure 1.1). We calculate a decision metric (here, the conversion rate) for both groups based on responses from their members and compare the decision metrics using a statistical test to draw causal statements about the treatment. The approach is popular in digital organisations, with the largest technology companies having reported running hundreds or thousands of experiments at any given time [149, 260, 288].

From a statistical point of view, digital experimentation and measurement is essentially the application of experimental design and causal inference methods in a digital setting. Likewise, the free delivery experiment mentioned above is an online randomised controlled trial. Readers will agree that the underlying experimental design and causal inference methods have been established and frequently applied in agriculture, medicine, and economics for decades.

That said, the arrival of the Web and, subsequently, the ability to run an experiment end-to-end online have brought different opportunities and challenges. The differences are well documented in [156], which necessitate the development of a different set of tools and processes exclusively for digital experiments. In some cases, they also require a complete rethink of how we approach experiment design and analysis. Under such premises, we examine the statistical and data challenges one faces when building DEM capabilities.

Guiding Principles

Before we state the research questions in detail (see section below), we outline the three guiding principles that lead us to the questions. Firstly, similar to many contemporaries in digital experimentation, we seek methods that enable one to make better decisions more quickly and thus drive business/organisational growth. The methods may be those that produce less biased estimates, generate measurements more quickly, or give alternatives that can measure the impact of an intervention under various constraints in practice (e.g., inability to perform user-level random assignment in the “free delivery” example above).

Secondly, we seek interpretable processes and results alongside performance to maintain engagement from those beyond our field. We, humans, value the understanding of why a decision is made as such, and the use of black-box models or overly complex procedures in decision-making often faces additional barriers in gaining trust from stakeholders despite its potential to improve performance [237].

Lastly, and perhaps more importantly, we seek to make the knowledge and tools involved in digital experimentation accessible, thus ensuring widened participation.111Clearly, a PhD thesis is a poor medium to engage with a non-technical audience. We thus limit the scope of “widened participation” to include researchers and practitioners with diverse academic backgrounds. Many recent advances in digital experimentation are proposed by researchers and practitioners who operate in an environment with mature capabilities. Focusing on those works may give the impression that mature capabilities are the norm and that we only need a little work to explain the basics on top of what is already available. Both are not true – the DEM capabilities of many individuals and organisations are still in their infancy. These individuals and organisations will benefit from us continuing to consolidate and clarify the building blocks in digital experiments, e.g., statistical tests, datasets, and decision metrics.

1.2 Key Research Questions

The thesis aims to address digital experimenters’ and organisations’ challenges as they build DEM capabilities. As the thesis title suggests, most of the work concerns statistical and data challenges one encounters at the early stage of the process. It also touches upon topics encountered by those with established capabilities, enabling readers to take away something wherever they are on the experimentation maturity spectrum [90]. We ask the following questions:

Why should one engage in digital experimentation and measurement?

While running experiment(s) to evaluate a hypothesis is second nature to scientists, it is unnatural in the business world. Business decision-makers prefer having business cases, ideally complete with a cost-benefit analysis. The ability to quantify the benefits of acquiring DEM capabilities (the knowledge and tools necessary to experiment and measure) will strengthen our business case. It enables us to speak in the language of the business and thus stand a better chance of garnering their support.

What ingredients do we require to run experiments successfully in a digital setting?

Committing to investing in DEM capabilities is the first of many steps to reap the benefits. To run their first experiment successfully, organisations require, at a minimum, a clear hypothesis and evaluation criteria, detailed procedures to deliver different treatments to and collect responses from experiment participants, plus basic knowledge in data processing and statistical testing. They would also require knowledge of advanced mathematical and statistical methods, powerful computer systems with sufficient computing power and data storage capacity, and a growth mindset organisational culture that embraces scientific, data-driven discoveries to scale their experiment operations. Each topic, whilst important, warrants extensive consideration. The thesis will focus on statistical testing, data, and advanced methods. We will provide a brief overview and pointers to relevant work for other topics for those interested.

When would an experiment design outperform another?

In the parable of two woodcutters, the more experienced woodcutter emerged victorious in a woodchopping contest by spending most of their time sharpening their axe. In the same spirit, it is vital to continuously improve our tools, one of which is experiment designs, as we engage in experimentation efforts. While there are many qualities that we can use to compare two experiment designs, in digital experimentation, we usually care about data efficiency. This is represented by the minimum number of experiment participants required to reach a statistically sound conclusion.222This is closely related to optimal design [8] and the asymptotic efficiency of a statistical test [254] in the statistical theory literature. We will approach the challenge from a more applied point of view. Increasing the data efficiency (i.e., requiring fewer experiment participants) enables experimenters to make decisions sooner, leading to better organisational performance as one can deploy improvements and roll back harmful changes more quickly.

1.3 Contributions and Chapter Organisation

The thesis is divided into seven chapters, each detailing contributions to a different statistical and data topic necessitated by developing early-stage DEM capabilities. The broad coverage of topics means the thesis embeds the background knowledge required for each topic within the individual chapters.

The remainder of Chapter 1 covers housekeeping items: a list of publications from the research programme and a list of mathematical symbols and the quantities/concepts they represent.

Chapter 2 introduces the ranking under lower uncertainty problem as a novel model to value DEM capabilities. This arises from the observation that DEM capabilities reduce measurement uncertainty on the value of individual business propositions, improving the inherent value of business propositions chosen during prioritisation. We derive the expected gain and the variance of our gain estimate and provide case studies based on large-scale meta-analyses. This addresses the first research question and enables one to build a quantitative business case to justify investment in the capabilities.

Chapter 3 provides an introduction to statistical testing in digital experimentation that is both mathematically rigorous and accessible to researchers and practitioners with different backgrounds. It starts from the very beginning of a statistical test (i.e., specifying the statistical hypotheses), provides a detailed treatment on the popular null hypothesis significance testing (NHST) framework, and involves other more advanced test paradigms (e.g., sequential and Bayesian testing) and alternatives. It aims to provide a sufficient theoretical grounding to appreciate what is happening behind the scenes while highlighting the pitfalls in test design and interpretation that can trap even the most experienced.

Chapter 4 describes a systemic investigation of datasets in digital experiments. We create the first ever taxonomy for digital experiment datasets and compile the first ever survey for publicly available online controlled experiment datasets. We also map the relationship between the dataset taxonomy and statistical tests discussed in Chapter 3. The taxonomy and survey also identify gaps in dataset availability, leading to the development of the ASOS Digital Experiments Dataset. This first real, multi-experiment time series dataset enables the design and running of experiments with adaptive stopping.

Chapter 5 reviews existing challenges in digital experimentation and the established and emerging methods that address such challenges. We also complement the review by viewing some of the reported methodological advances through a practical lens. This is done by interleaving the review with case studies on randomised controlled trials with dependent responses and quasi-experiments with geographical regions as treatment units. They provide evidence on the extent of reported challenges and practical considerations when implementing relevant methods. Together with Chapters 3 and 4, these chapters address the second research question.

Chapter 6 develops an evaluation framework for personalisation strategy experiment designs. These experiment designs face unique challenges, such as low test power and partial non-compliance from users, issues that we will cover in Chapters 3 and 5. The evaluation framework enables one to compare two experiment setups given the circumstances they face with their target audience, thus addressing the third research question. We also derive interpretable rules of thumb from the framework to enable experimenters to compare typical experiment setups quickly.

We conclude in Chapter 7 with an outline of promising investigation pathways arising from each workstream. In addition, we make all the code used for experiments and simulations described in the thesis, as well as the ASOS Digital Experiment Dataset, publicly available. Readers can find the links to the code repositories and the dataset at the bottom of this page333The link to code repositories and the dataset are as follows: • Code repository associated with the ranking under lower uncertainty framework (as described in Chapter 2): https://github.com/liuchbryan/ranking_under_lower_uncertainty; • ASOS Digital Experiments Dataset and accompanying datasheet (as described in Chapter 4): https://osf.io/64jsb/. The OSF project also embeds a code repository with experiments on the dataset (https://github.com/liuchbryan/oce-dataset/); • Code repository and results on the two publicly available datasets associated with e-commerce experiments with dependent responses (as described in Section 5.5): https://github.com/liuchbryan/oce-ecomm-abv-calculation; and • Code repository associated with the evaluation framework for personalisation strategy experiment designs (as described in Chapter 6): https://github.com/liuchbryan/experiment_design_evaluation. and again in the footnotes of the relevant chapters.

1.4 Publications

This thesis contains research that has been published during PhD study. We list where readers can find them in the thesis, together with details of the associated conference and journal papers, below:

-

•

Chapter 2 and Appendix A.1: C. H. B. Liu and B. P. Chamberlain (2019). What is the Value of Experimentation & Measurement? In: 2019 IEEE International Conference on Data Mining (ICDM ’19), 1222–1227. DOI: 10.1109/ICDM.2019.00151.

-

•

Chapter 2 and Appendix A.1: C. H. B. Liu, B. P. Chamberlain and E. J. McCoy (2020). What is the Value of Experimentation and Measurement? Data Science and Engineering 5, 152–167. DOI: 10.1007/s41019-020-00121-5. Part of Special Issue: Highly-Rated Short Papers of ICDM 2019.

-

•

Chapter 4: C. H. B. Liu, Â. Cardoso, P. Couturier and E. J. McCoy (2021). Datasets for Online Controlled Experiments. In: Proceedings of the Neural Information Processing Systems Track on Datasets and Benchmarks (NeurIPS Datasets and Benchmarks ’21). URL:https://datasets-benchmarks-proceedings.neurips.cc/paper/2021/file/274ad4786c3abca69fa097b85867d9a4-Paper-round2.pdf.

-

•

Chapter 5 (Section 5.5): C. H. B. Liu and E. J. McCoy (2023). Measuring e-Commerce Metric Changes in Online Experiments. In: Companion Proceedings of the ACM Web Conference 2023 (WWW ’23 Companion). DOI: 10.1145/3543873.3584654.

-

•

Chapter 6, Appendix A.2, and Appendix A.3: C. H. B. Liu and E. J. McCoy (2020). An Evaluation Framework for Personalization Strategy Experiment Designs. arXiv: 2007.11638 [stat.ME]. Presented in AdKDD ’20 Workshop (in conjunction with KDD ’20),awarded Best Student Paper.

1.5 List of Acronyms and Mathematical Symbols

Readers may encounter the following acronyms recurring in multiple thesis sections. We will define the acronyms in the main text at least once before referring to the acronyms.

-

•

ATE: Average treatment effect

-

•

CATE: Conditional average treatment effect

-

•

CI: Confidence interval

-

•

CDF: Cumulative density function

-

•

CLT: Central limit Theorem

-

•

CVR: Conversion rate

-

•

DEM: Digital experimentation and measurement (usually followed by the word “capability/capabilities”)

-

•

MDE: Minimum detectable effect

-

•

NHST: Null hypothesis significance test(ing)

-

•

OCE: Online controlled experiment

-

•

PDF: Probability density function

-

•

RCT: Randomised controlled trial

We also list the mathematical symbols and the quantities/concepts they represent below. Each entry is indexed by the leading symbol and follows the following format:

(Applicable chapter(s)) Symbol(s) – (Type) Quantity/concept the symbol represents.

Applicable chapter(s)

Symbol(s)

The thesis covers topics traditionally belonging to multiple statistical disciplines. Thus, it is inevitable to see some notation clash. We follow the order set out below when deciding which set of notations takes precedence:

-

1.

Elementary statistical constructs found in introductory statistical texts (e.g., for a random variable, for the probability density function of , and for the expected value of );

-

2.

Notation specific to statistical testing (e.g., and for null and alternate hypotheses, for the significance level, for the power);

-

3.

Common notation in other sub-fields, including causal inference, order statistics, and econometrics; and

-

4.

Specific notation introduced by individual research articles.

Notations with lower precedence are generally assigned a new symbol to minimise confusion. That said, in a couple of cases, the same symbol may represent two different quantities/concepts in the same chapter – their meaning should be apparent given the context surrounding its use.

Type

We also abbreviate the types of quantities and concepts in the tables as follows:

-

•

calc.: calculated quantity,

-

•

const.: constant,

-

•

dist.: distribution,

-

•

func.: function,

-

•

id.: identifier, and

-

•

r.v.: random variable.

|

Quantity/Concept Represented | |||||||

|---|---|---|---|---|---|---|---|---|

|

||||||||

|

||||||||

|

||||||||

|

||||||||

|

|

Quantity/Concept Represented | |||||

|---|---|---|---|---|---|---|

|

||||||

|

||||||

|

||||||

|

|

Quantity/Concept Represented | ||||

|---|---|---|---|---|---|

|

|||||

|

|||||

|

|||||

|

|||||

|

|||||

|

|

Quantity/Concept Represented | |||||||

|---|---|---|---|---|---|---|---|---|

|

||||||||

|

||||||||

|

||||||||

|

||||||||

|

|

Quantity/Concept Represented | |||||

|---|---|---|---|---|---|---|

|

||||||

|

||||||

|

||||||

|

|

Quantity/Concept Represented | ||||

|---|---|---|---|---|---|

|

|||||

|

|||||

|

|||||

|

|||||

|

|||||

|

|||||

|

|||||

|

|||||

|

|||||

|

|

Quantity/Concept Represented | ||

|---|---|---|---|

|

|||

|

|||

|

|||

|

|||

|

|||

|

Chapter 2 What is the Value of Digital Experimentation and Measurement Capabilities?

From the thesis title, it is reasonable for readers to expect content covering methodological advances in statistical tests, experiment design, and causal inference. While we will address such mainstream topics in later chapters of the thesis, we first present a ranking under lower uncertainty problem as an application of order statistics to motivate our topics. As the chapter title suggests, addressing the problem enables us to value digital experimentation and measurement (DEM) capabilities quantitatively, which, in turn, helps us to answer why we require such capabilities in the first place.

This chapter is adapted from the research paper “What is the Value of Experimentation & Measurement?” It was first presented at the 2019 IEEE International Conference on Data Mining (ICDM) [174] and later extended and published in Data Science and Engineering as part of a special issue on Highly-Rated Short Papers of ICDM 2019 [175]. In Sections 2.1 and 2.2, as well as introducing related work, we will motivate how the requirement to value DEM capabilities arises and leads to our upcoming ranking under lower uncertainty problem. Readers who are more interested in the mathematical formulation of the ranking under lower uncertainty problem can skip straight to Section 2.3, though they may find the chapter organisation at the end of Section 2.1 useful.

2.1 Motivation

The value of DEM capabilities is currently best reflected in the success of organisations that have adopted and advocated for them in the past decade. Many major technology companies report having mature infrastructure for online controlled experiments (OCEs, e.g., Google [260], Linkedin [288], and Microsoft [149]) or are heavily investing in state-of-the-art techniques (e.g., Airbnb [161], Netflix [286], and Yandex [222]), or both. Amazon [123], Facebook [105], and Uber [20] have also reported the use of various causal inference techniques to measure the incrementality of advertising campaigns. Several start-ups (e.g. Optimizely [134] and Qubit [30]) have also recently been established purely to manage OCEs for businesses.

While mature DEM capabilities can quantify the value of a business proposition, it remains a substantial challenge to “measure the measurer” – to quantify the value of the DEM capabilities themselves. To the best of our knowledge, no work addresses the question, “Should we invest in DEM capabilities?” or how to value these capabilities when we first present our ideas. The lack of prior work makes it hard to build a compelling business case to justify investment in the related personnel and infrastructure. We address this problem by calculating both the expected value and the risk, allowing the Sharpe ratio [246] for a DEM capability to be calculated and compared to other potential investments.

The value created by DEM capabilities comes from the following three sources:

-

1.

Recognising value: DEM capabilities enable one to attribute value to a digital product, business proposition or service. They also prevent damage from business propositions that have a negative value. This is important for dynamic organisations with large numbers of business propositions, as the damage caused by individual rollouts can be compartmentalised and contained in a similar fashion, similar to unit and integration testing in software development.

-

2.

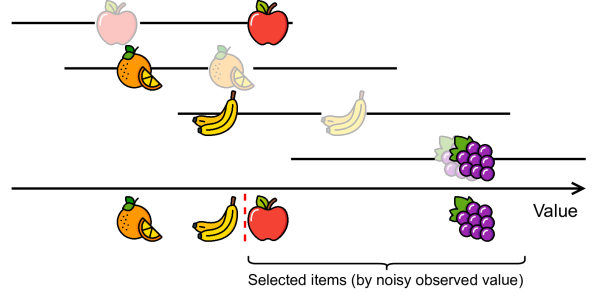

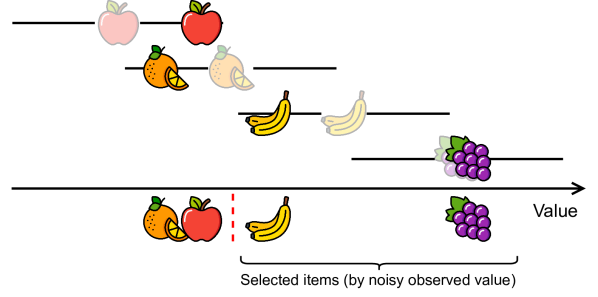

Prioritisation: Without DEM capabilities, one prioritises based on back-of-envelope estimates or gut feel, which has high uncertainty. DEM reduces the magnitude of the noise arising from estimation, enabling prioritisation based on estimates closer to the true values and improving long-term decision-making (see Figure 2.1).

-

3.

Optimisation: DEM capabilities allow one to evaluate large numbers of variants against each other and the best to be selected efficiently. Without such capabilities, we can still experiment with different business propositions sequentially, though it is slow and introduces noise from the changing environment.

Quantifying the value of a DEM capability is relatively straightforward once it is in place. For example, the value of Item 1 comes from rolling back negative business propositions: we can calculate it by summing the negative contributions of unsuccessful business propositions. Likewise, we can calculate the value of Item 3 by summing the difference between the maximum and the mean value for each variant over the business propositions. Indeed, these are the approaches taken by [182] when valuing LinkedIn’s experimentation platform using past experiment data.

The approaches above are not feasible for organisations building DEM capabilities from scratch. One can attempt to estimate the values from Items 1 and 3 using generic value distribution across business propositions, which is given across industries in [136] and [30], though these estimates are generally no better than back-of-envelope calculations. Without an accurate valuation, organisations remain in a chicken and egg situation – no valuation, no investment; no investment, no capability; no capability, no valuation.

Given the above, we see quantifying the value of Item 2 as the less explored yet more compelling approach and the subject of the remainder of this chapter. DEM capabilities improve prioritisation by reducing uncertainty in the value estimates of each business proposition. This is a form of ranking under uncertainty, a well-studied problem in statistics and operations research. However, in all previous work, the variance is assumed to be a fixed constant or changed without measuring the corresponding change in the value of the ranked items. Here, we wish to understand the value of ranking under lower uncertainty through DEM capabilities.

Our contribution is as follows. We

- 1.

-

2.

Derive the variance of our estimator, allowing one to calculate a Sharpe ratio to guide organisations considering an investment in DEM (Section 2.5); and finally

- 3.

2.2 Related work

There is a vast literature on using controlled or natural experiments in a digital technology context. In addition to that mentioned in Section 2.1, there are works dedicated to running trustworthy online controlled experiments [74], choosing good metrics [126] and designing experiments where samples are dependent due to external confounders [18, 19].111We will describe the works in greater detail in Chapter 5. However, these works all assume the existence of DEM capabilities, and to the best of our knowledge, no literature that helps organisations justify the acquisition of DEM capabilities exists. While [182] asked a similar question as this chapter does, they aimed to value an experimentation platform, i.e., an existing DEM capability. We believe that filling this gap is necessary for widespread adoption and that increased participation will accelerate the development of the field.

This chapter is related to existing work in statistics and operations research, particularly on decision-making under uncertainty, which has been extensively studied since the 1980s. Notable work includes proposals for additional components in a decision maker’s utility function [22], alternate risk measures [289], and a general framework for decision-making with incomplete information (i.e., uncertainty) [278]. These works assume the inability to change the noise associated with estimation or measurement (or both).

The sub-problem of ranking under uncertainty has also attracted considerable attention, partially due to the advent of large databases and the requirement to rank results with a certain ambiguity in relevance [255]. While [298] measured the influence of noise levels in their work, they focused on the quality of the ranks themselves but not the value associated with the ranks.

The project selection problem is a related topic in optimisation, where the goal is to find the optimal set of business propositions using mixed integer linear programming, possibly under uncertainty. Work in this domain generally seeks methods that cope with existing risk/noise [186], and to the best of our knowledge, no work considers the value of reducing risk. While [245] have discussed lowering the uncertainty level during the selection process, they refer to the uncertainty of decision parameters instead of the general noise level.

2.3 Mathematical Formulation

We formulate the ranking under lower uncertainty problem, which has a wide variety of important applications in its own right [251, 298], as follows. Consider the scenario where we select business propositions from candidates, where . The Estimated value of each business proposition is given by , where are the true yet unobserved Values estimated with error . The business propositions are labelled in ascending order of estimated value to get the order statistics , and we select the business proposition with the highest estimated values: . We are interested in the true value of the selected business propositions, given by

| (2.1) |

where denotes the index function that maps the ranking to the index of the business proposition. Note one should not confuse the set in Expression (2.1) with the set – the latter denotes the top business propositions ranked by their true value and are likely to be different [298].

We define the mean true value of the selected business propositions as

| (2.2) |

where the best prioritisation maximises .222Readers can internalise the notation by drawing parallels between the name of the letter in French (double vé) and Spanish (doble ve) – both literally meaning “double v” – and the fact that we use to denote an aggregation of two or more .

Part of the value of ranking under lower uncertainty, which DEM capabilities help bring, arises from the observation that increases when the magnitude of the uncertainties arising from estimation () decreases. We are interested in the value gained by reducing estimation uncertainty without changing the set of business propositions (i.e., retaining all ), as the true value of the business propositions does not depend on the measurement method used:

| (2.3) |

Obtaining the value gained () enables us to compare DEM capabilities with other potential investments. The Sharpe ratio is a standard quantity used in finance to compare different investments. This standard score-like ratio represents the risk-adjusted expected excess return on investment compared to a risk-free investment [246]. In our case, represents the expected return on investment of DEM capabilities, represents the risk, and we can specify the return on investment of the risk-free investment as a constant . This enables us to calculate the Sharpe ratio as

| (2.4) |

2.3.1 Modelling values with statistical distributions

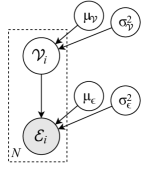

To value a DEM capability using such a generic framework that one can apply in many different ways across diverse organisations, it is first necessary to make some simplifying assumptions about the statistical properties of the business propositions under consideration. We assume the value of the business propositions () and the estimation noises () are randomly distributed:

| (2.5) |

where (see Figure 2.2).

We note two special cases, one when both the value and the noises are assumed to be normally distributed:

| (2.6) |

and the other when both the value and the noises are assumed to follow some Generalized Student’s -distributions:

| (2.7) |

where is a standard Student’s -distribution with degrees of freedom. The location and scaling parameters ensure and have the mean and variance specified in Expression (2.5).

These two cases are particularly relevant as meta-analyses compiled on the results of 6,700 e-commerce [30] and 432 marketing experiments [136], respectively, indicate the uplifts measured by the experiments, and hence the value of the business propositions under some estimation noise, exhibit the following properties:

-

1.

They can be positive or negative,

-

2.

They are usually clustered around an average instead of uniformly spreading across a specific range, and

-

3.

The distributions are heavy-tailed.

The normal assumptions cover the first two properties only, yet enable one to draw on the wealth of results in order statistics and Bayesian inference related to normal distributions to get started. The -distributed assumptions also cover property 3, though valuation under such assumptions is more complicated as -distributions do not have conjugate priors.

We will include the valuation under -distributed assumptions under the general case for brevity. We will, however, present empirical results in Section 2.8.1, showing that the value gained under -distributed assumptions has a higher mean and variance, thus demonstrating that the model can capture the “higher risk, higher reward” concept.

2.3.2 Key results

In the following two sections, we will derive the expected value and variance for , the mean true value of the top business propositions selected after being ranked by their estimated value (as defined in Equation (2.2)), as well as the expected value and the variance of , the value gained when the estimation noise is reduced. This enables us to calculate the Sharpe ratio defined in Expression (2.4).

We will also provide two key insights. Firstly, the expected mean true value of the selected business propositions () increases when the estimation noise () decreases, and the relative increase in value depends on how much noise we can reduce. Secondly, when is small, reducing the estimation noise may not lead to a statistically significant improvement in the true value of the business propositions selected. As a result, improvements in prioritisation driven by DEM may only be justified for larger organisations.

2.4 Calculating the Expectation

We first derive the expected value for . This requires the expected values of, in order:

-

1.

– the estimated value of the ranked business proposition in estimated value;

-

2.

– the true value of the ranked business proposition in estimated value; and

-

3.

– the mean of the true value for the most valuable business propositions ranked by their estimated values.

To obtain the expected value for , we apply a result in Section 4.6 of [56], which approximates the expected value of the order statistics using the quantile function of :

| (2.8) |

where denotes the quantile function for and is a constant correcting the quantile of the ranks.333Many values for were proposed. Early works advocate or depending on how one approaches continuity correction between ranks and quantiles [119]. [27] proposes a compromise value of based on a tabulation of required to yield the correct expected value for different and . [119] expands the tabulation and proposes using a different for each , with the values of hovering around 0.4. For simplicity, we take for all in all our calculations. The formula results from applying the first-order delta method on the underlying compound beta- distribution [223]. Such estimation will inevitably incur a small bias, particularly for extreme order statistics (i.e., close to one or ) and when is small. However, as verified empirically in Section 2.6, we consider such an estimation accurate enough for our application.444[119] also noted for normal order statistics, the maximum error is 0.018 (i.e., less than one percent relative to the value of extreme order statistics) for some choice of . One can also include higher-order terms in the corresponding Taylor expansion to improve estimation accuracy, though we believe the additional complexity and, thus, reduced interpretability in the resultant formula is not worth the marginal gain in accuracy.

We then obtain the expected value of by applying Equation 6.8.3a of [56]:

| (2.9) |

where is the correlation between and .

Equation (2.9) shows that decreasing the estimation noise will increase for any . It follows that the mean true value of the top business propositions, selected according to their estimated value, will generally increase with a lower estimation noise. We show this by applying the expectation function to defined in Equation (2.2) to obtain

| (2.10) |

We finally consider the improvement when we reduce the estimation noise from to . This will be the expected value gained by having better DEM capabilities:

| (2.11) |

2.4.1 Expectation under normal assumptions

In the special case where are normally distributed (with mean and variance ), the expected value for the normal order statistics is approximately

| (2.12) |

where denotes the quantile function of a standard normal distribution [27]. It is worth noting that decreasing the estimation noise will decrease for any , appearing to lower the average value of the top business propositions. This is a common pitfall – we are not optimising the combined estimated value of the selected business propositions. What matters is the true yet unobserved value of that proposition, , as shown below.

For , we can simplify Equation (2.9) by substituting Equation (2.12). We can also evaluate from first principles by noting a standard result in Bayesian inference, which states that the posterior distribution of once is observed is also normally distributed with mean

| (2.13) |

and applying the law of iterated expectations to obtain555, as we rank the business propositions by their estimated values.

| (2.14) |

Here, decreasing the estimation noise will lead to an increase in for any .666While are no longer normally distributed with the ranking information, it remains valid to use the law of iterated expectations to obtain the expected value for all .

The value of business propositions chosen () under normal assumptions then evaluates to

| (2.15) |

This is done by substituting Equation (2.14) into Equation (2.10). Note the absence of in Equation (2.15), which suggests that systematic bias in estimation will not affect the true value of the chosen business propositions in the normal case.

Finally, the expression for the expected value of when we reduce the estimation noise from to is much neater under normal assumptions, as many terms cancel out in Equation (2.11), leading to

| (2.16) |

If we further assume that (i.e., the true value of the business propositions centres around zero), then the relative gain is entirely dependent on , , and :

| (2.17) |

To calculate the relative improvement in prioritisation delivered by DEM under these assumptions, we plug the following into Equation (2.17) to obtain an estimate of how much one will gain from acquiring such capabilities:

-

1.

The estimated spread of the values (),

-

2.

The estimated deviation of the current estimation process (), and

-

3.

The estimated deviation to the actual value upon acquisition of DEM capabilities ().

For example, if Example Company Ltd’s project values are spread with a standard deviation of 1 unit and their current estimation has a standard error of 0.5 units, then by acquiring an A/B test framework that is capable of measuring with an error of 0.4 units, the company gains 3.8% of extra value simply due to the ability to prioritise with more accurate measurements under normal assumptions.

We conclude this section by suggesting how one may estimate , , and , especially when they have yet to build any DEM capabilities. Clearly, it is impossible to recommend specific values for the three parameters as organisations seeking to build DEM capabilities come in all shapes and sizes. That said, one may consider using industry averages published in meta-analyses [30, 136] when estimating . For , they may solicit value estimates for several business propositions from current decision makers and take the variance over such estimates.777It does not matter if the decision makers provide value estimates far from the actual value of the business propositions. In fact, one need not know the business propositions’ actual value. What matters here is the spread of the estimates. Finally, they may leverage the user numbers and the variance of user responses that form the business metric to estimate under an A/B test.888For example, in an A/B test measuring conversion rate (CVR) uplift using a practical -test, the estimation noise ( or ) is the variance of the difference in CVR between two variants under a nil null hypothesis. This equals , where is the base CVR and is the total number of users across both groups. See Chapter 3 for further discussions on statistical tests, particularly Sections 3.5.2 and 3.5.3 on practical -tests and how they are applied to business metrics based on binary responses such as CVR. We also encourage one to explore parameter values around their estimates for robustness, as we will show in Section 2.7 when we provide two case studies.

2.5 Calculating the Variance

It is crucial to understand both the expected gain and the risk or uncertainty of ranking under lower uncertainty to make effective investment decisions. Therefore, having derived the expected value in Equation (2.11), we address the investment risk given by the variance of in this section.

The variance calculation features new challenges in addition to that identified in the section above, the most prominent of which concerns the interactions between quantities generated under different estimation noise levels. While these interactions do not affect the expected value, they influence the variance via the covariance terms. Failure to account for the covariance terms may lead to a large error in the variance estimate.

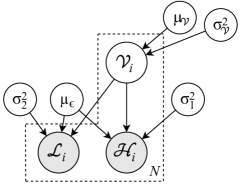

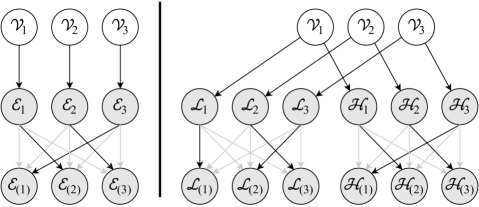

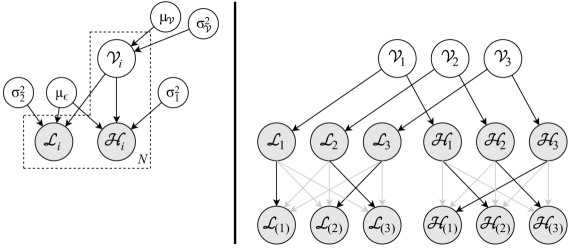

To address the challenges, we first extend the notation to clarify the interactions. Instead of a single set of noise shown in Section 2.3, we define two sets of random noise with different noise levels:

| (2.18) |

Similar to how the problem is modelled in Section 2.3, we assume all true item values () and noises ( and ) are independent, i.e., , , and . The estimated value of each item is then given by

| (2.19) |

The setup is illustrated in Figure 2.3.

Having obtained two sets of estimated values, we rank and trace the corresponding indices for each set separately. For , we denote as the order statistic of , the estimated value of the ranked item under noise level , followed by as the concomitant [56] of , i.e., the true value of the item ranked by its estimated value. We repeat the process for : we denote as the order statistic of and as the concomitant of .999 and are the index functions that map the ranking to the index for and , respectively.

We also define the mean true value of the top items, ranked by their estimated value, under both noise levels as

| (2.20) |

where is the mean true value under , and is the mean true value under . Finally, we denote the difference between the mean true values as .

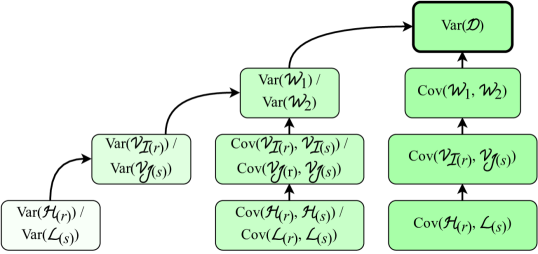

Deriving the variance is similar to deriving the expectation – one has to obtain the variances for (in order) /, /, /, and . The relationship between these quantities is shown in Figure 2.4.

2.5.1 /

We apply a result from [54], which states that the variance of and can be approximated as

| (2.21) | ||||

| (2.22) |

where and denote the probability density function and quantile function of the corresponding r.v., respectively. As is the case with calculating the expected value (see Section 2.4), the formula results from applying the first-order delta method [171], with the same strength and weakness considerations. In the special case where , , and are all normally distributed, the variances are

| (2.23) | ||||

| (2.24) |

where is the probability density function, and is the quantile function of a standard normal distribution.

2.5.2 /

The variance for is obtained using properties of the concomitants of order statistics [55]:101010 and in this thesis correspond to and in [55].

| (2.25) | ||||

| (2.26) |

where denotes the correlation between and , and denotes the correlation between and .

In the multivariate normal case, the same result can also be obtained from first principles. We first recall Equation (2.13), which describes the mean of once we observe (now or ), and note its variance counterpart is

| (2.27) |

Using the results in Equations (2.13) and (2.27), we apply the law of total variance to obtain111111Similar to what has been mentioned in Footnotes 5 and 6, and , since we rank the business propositions by their estimated values. Moreover, while and are no longer normally distributed with the ranking information, using the law of total variance to obtain the variance for all and remains valid.

| (2.28) | ||||

| (2.29) |

2.5.3 /

To derive the variance of , we require the covariance between and , as well as that between and . The same goes for , where we require the covariance between and , as well as that between and . This is necessary as the terms of (see Equation (2.2)), which result from removing noise from successive order statistics, are highly correlated.

Equation 4.6.5 of [56] provided a formula to estimate the covariance between and and between and for any :121212For , simply swap and as covariance functions are symmetrical.

| (2.30) | ||||

| (2.31) |

To obtain the covariance between and for any , we again refer to [55] (Equation 2.3d):

| (2.32) | ||||

| (2.33) |

2.5.4

Finally, we derive the variance of . In addition to the variance of and derived, respectively, in Equations (2.34) and (2.35), we require the covariance between these two terms. This, in turn, requires the covariance between and and that between and .

The covariance between and can be derived using results in [56]:

| (2.36) |

where and are the probability density function and quantile function for , respectively.

Deriving the covariance between and is perhaps the most challenging problem within the work, as they take two forms depending on the indices:

| (2.37) |

where the second case is a standard Bayesian inference result.

The problem arises as the ranked and the ranked can be generated by the same for some . It will not arise if we have only or (see Figure 2.5 for an example). In this case, when we consider the covariance of the concomitants /, we have to take into account both the existing variance of and the ranking information provided by and . If the order statistics are generated by different , we only need to consider the latter as we assumed to be independent and thus uncorrelated.

As we are interested in the overall behaviour, we only need to derive the two cases on the RHS of Equation (2.37) and weigh them using the probability that without worrying about which case applies to each pair. The first case (when ) can be evaluated using the law of total variance with multiple conditioning random variables:

| (2.38) |

The second case can be derived by substituting Equation (2.36) into Equation (2.37).

For the weighting probability , we see its derivation as an interesting and potentially important problem in its own right, yet to the best of our knowledge, no proper treatment was given to the problem. In this work, we approximate the probability using beta-binomial distributions, with parameters derived from quantities calculated above. Without distracting readers from the main question of quantifying the value and risk of DEM capabilities, we relegate the detailed discussion on approximating the quantity to Appendix A.1.

With the three components for the covariance between and in place, we can finally derive and by applying the covariance and variance functions to the definitions of, respectively, / and (see (2.20)) to obtain

| (2.39) | ||||

| (2.40) |

where the first two terms on the RHS of Equation (2.40) are that derived in Equations (2.34) and (2.35).

We conclude this section by observing that and influence considerably. In particular, is generally large when and are small with other parameters fixed. This is crucial as even in cases where is positive, the limited capacity of an organisation to introduce new business propositions may mean that the Sharpe ratio defined in Section 2.3 (see Expression (2.4)) may not be high enough to justify investment in a DEM capability.

The exact threshold where an organisation should consider acquiring such capabilities depends on multiple factors, including their size (which affects ), the size of their backlog (), the nature of their work ( and ), and how good they were at estimation (). Thus, we refrain from providing a one-size-fits-all recommendation but give examples in Section 2.7.

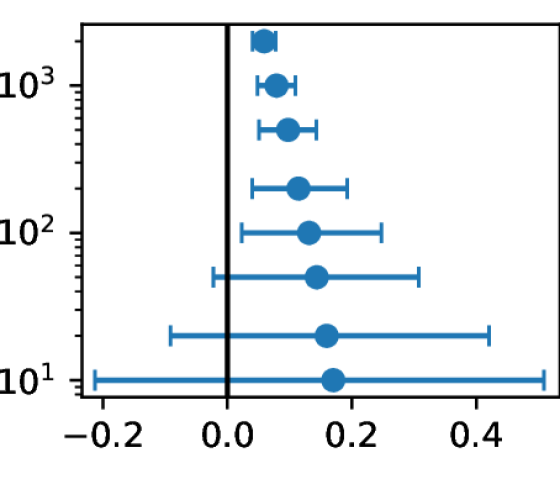

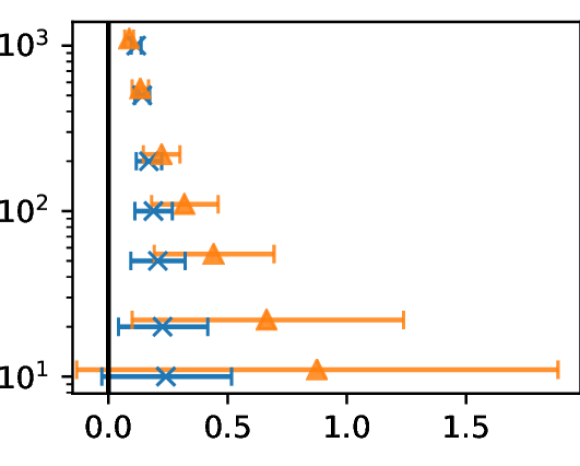

2.6 Empirical Verification

Having performed theoretical calculations for the expectation and variance of the value DEM capabilities deliver through enhanced prioritisation, we verify those calculations using simulation results.131313All code used in the experiments, case studies and extensions are available on GitHub: https://github.com/liuchbryan/ranking_under_lower_uncertainty.

We verify the result derived in Sections 2.4 and 2.5 empirically, in particular under the normal assumptions. We run multiple statistical tests for each quantity of interest – the mean and variance of / and , as well as the covariance between different pairs of order statistics and their concomitants.

In each statistical test, we randomly select and fix the value of the parameters, i.e., , , , , , , , , and (the latter two for the covariance of the order statistics only). We select uniformly on a log scale, with the log scale favoured due to its better resemblance to the organisation size distribution in real life and bounds chosen to represent the usual number of items/propositions an organisation will consider during prioritisation. We also select , , , and randomly from a uniform distribution (on a linear scale), with bounds chosen that are reflective of the usual business metrics an organisation uses to prioritise their items/propositions and their unit of measurement (e.g., percentage points change, revenue impact in hundred thousand pounds).141414Denoting as a uniform distribution with bounds and , we draw , and .

Each parameter is drawn independently from other parameters where possible, with the only exceptions being when the range of a parameter is restricted (i.e., , , and for selected items/propositions). To draw , we draw a uniformly random multiplier between 0.01 and 0.8, then apply the multiplier to .151515In other words, we draw , subjected to rounding with the floor function and a minimum value of one. Multipliers above 0.8 are ignored, as it is unrealistic for organisations to have such a high relative capacity. We apply a similar process to draw , though we use a different multiplier range and apply the multiplier on (the standard deviation) before squaring.161616We draw , subjected to a minimum value of . Multipliers below 0.1 and above 0.99 are ignored, as we consider such an estimation noise reduction unrealistic and of negligible value, respectively. Finally, we draw and independently and uniformly amongst integers between and (both inclusive).

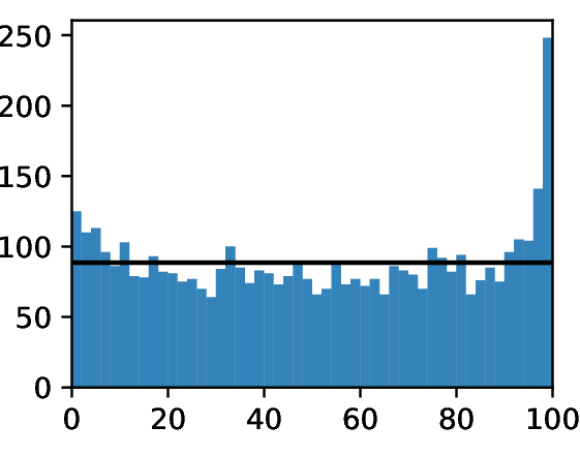

Upon selecting and fixing the value of the parameters, we compare the theoretical value of the quantity of interest to the centred 95% confidence interval (CI) generated from multiple empirical samples. If the derivations above are exact, the 95% CI should contain the theoretical value in around 95% of the statistical tests. The histogram of the percentile rank of the theoretical quantity among the empirical samples should also follow a uniform distribution [259].

| Quantity | # within CI | # statistical tests | % within CI |

|---|---|---|---|

| 3,991 | 4,428 | 90.13% | |

| 4,162 | 4,428 | 93.99% | |

| 3,390 | 4,555 | 74.42% | |

| 4,663 | 4,940 | 94.39% | |

| 4,730 | 4,940 | 95.75% |

Each empirical sample is generated using one of the following two methods depending on the quantity we are evaluating:

a) Bootstrap resampling – We use the method to generate a sample for the mean/variance of / and . We first generate the initial samples for , , and by performing 10,000 simulation runs (see below). We then resample the initial samples and calculate the mean/variance of the resample to obtain an empirical mean/variance sample. Finally, we repeat the resampling 2,000 times to obtain a representative empirical distribution for the mean/variance.

b) Sampling for order statistics – The bootstrapping approach is unlikely to work on the covariance between the order statistics (e.g., and ) and their concomitants (e.g., and ), as the ranking information may not be preserved during resampling. Hence, for these quantities, we opt for a more naïve sampling approach. We generate 200 samples for , , , and via the same number of simulation runs, and calculate the covariance between these quantities to obtain an empirical sample. The process is repeated 1,000 times to yield a representative empirical distribution for the covariance.

Finally, in each simulation run, we obtain one sample for each of /, /, , and w.r.t. the parameters via the following four-step process:171717Identifiers in monospace refer to variables used in software packages, which correspond to the random variables used in Sections 2.3–2.5.

-

1.

Take samples from as Vi;

-

2.

Take samples from , and sum the ith-indexed sample with Vi i to obtain Hi:

-

(a)

Rank all Hi, take the value of the rth-ranked Hi as H(r) and its index as I(r),

-

(b)

Take the value of the I(r)th-indexed sample of Vi as VI(r),

-

(c)

Obtain the indices of the largest samples of the ranked Hi,

-

(d)

Calculate the mean of Vi, where i is in the set of indices in Step 2c, as W1;

-

(a)

-

3.

Take samples from , and sum the ith-indexed sample with Vi i to obtain Li:

-

(a)

Rank all Li, take the value of the sth-ranked Li as L(s) and its index as J(s),

-

(b)

Take the value of the J(s)th-indexed sample of Vi as VJ(s),

-

(c)

Obtain the indices of the largest samples of the ranked Li,

-

(d)

Calculate the mean of Vi, where i is in the set of indices in Step 3c, as W2;

-

(a)

-

4.

Take the difference between W2 obtained in Step 3d and W1 from Step 2d to get D.

We show the results in Table 2.1 and Figure 2.6. We observed that the 95% CI of the quantities , , , , and contain the derived theoretical value for roughly 90%, 94%, 74%, 94%, and 96% of the times respectively. While these numbers are expected for the expectations and covariances, considering they are approximations, they are on the low side for the variances. Upon further investigation, we realised that most out-of-CI cases have a theoretical variance below the CI, suggesting a slight underestimate in our variance derivation. We believe that this is due to the omission of higher-order terms when using the formulas in [54], leading to a small (less than one percent relative) bias, which is more apparent for smaller and . Otherwise, we are satisfied with the soundness of the derived quantities.

2.7 Case Study

“What do e-commerce/marketing companies gain by acquiring digital experimentation and measurement capabilities?”

It is difficult to verify any model that seeks to ascertain the value of DEM capabilities with real-life data. This is because of the inability to observe the true value of a digital product / business proposition / service without any measurement error and the lack of published measurements from organisations. The closest proxies are meta-analyses, including those compiled by Browne and Johnson [30] and Johnson et al. [136], which contain statistics on the measured uplift (in relative %) over a large number of e-commerce and marketing experiments for many organisations.

The information presented by the two groups of researchers, which we describe in more detail below, is sufficient for us to ask the following question: If the same organisation conducted all the experiments presented by Browne and Johnson / Johnson et al., how much value did the DEM capabilities add due to improved prioritisation? We present results under normal assumptions in this section and will revisit the question when we discuss the model under -distributed assumptions in Section 2.8.1.

2.7.1 e-Commerce companies

In [30], Browne and Johnson reported running 6,700 A/B tests in e-commerce companies, with an overall effect in relative conversion rate (CVR) uplift centred at around zero, and the 5% and 95% percentiles at around . We then divide the range by , the 95th percentile of a standard normal, to estimate that the distribution reported has a standard deviation of around 0.75%. Based on this information, we take and , considering that the reported distribution incorporated some estimation noise, and hence, the spread of the true values should be slightly lower.

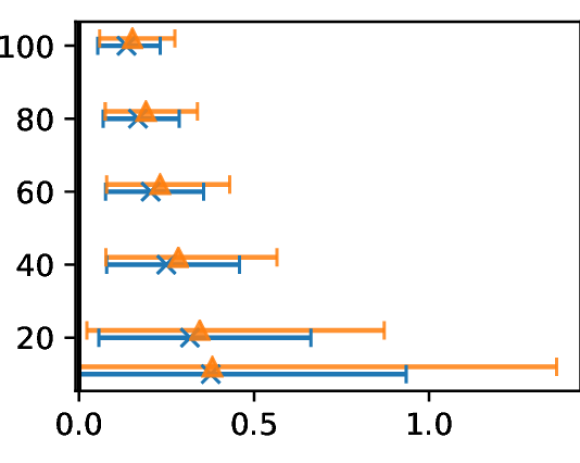

Given an A/B test on CVR uplift run by the most prolific organisations (e.g. one with five million visitors and a 5% CVR) carries an estimation noise of around ,8 we explore the scenarios where we reduce the noise level from to , representing different levels of estimation abilities before and after the acquisition of DEM capabilities for companies of various sizes. We also calculate the value gained under different (from 10 to 2,000) to simulate organisations with different yet realistic capacities while fixing (# experiments). Finally, we set as we do not assume any systematic bias during estimation in this case.

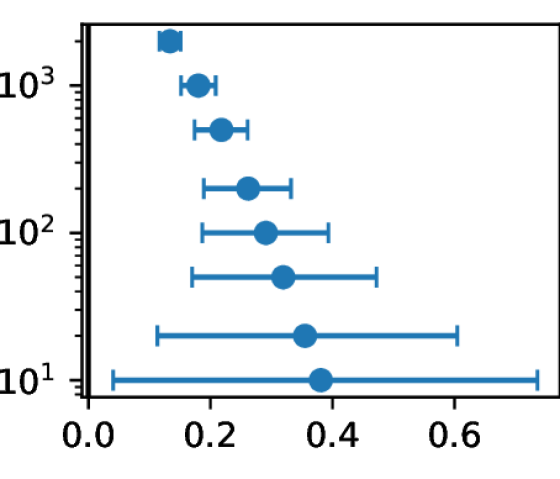

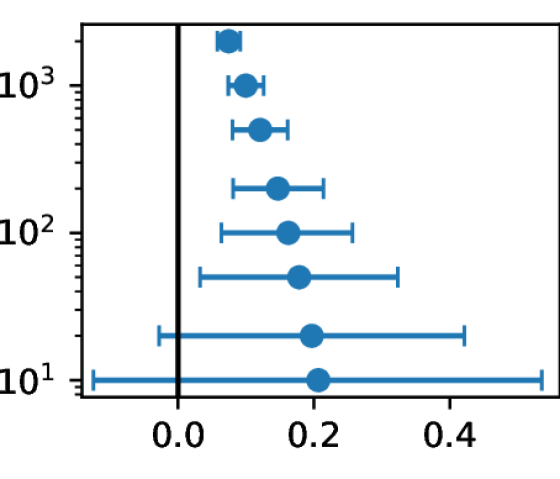

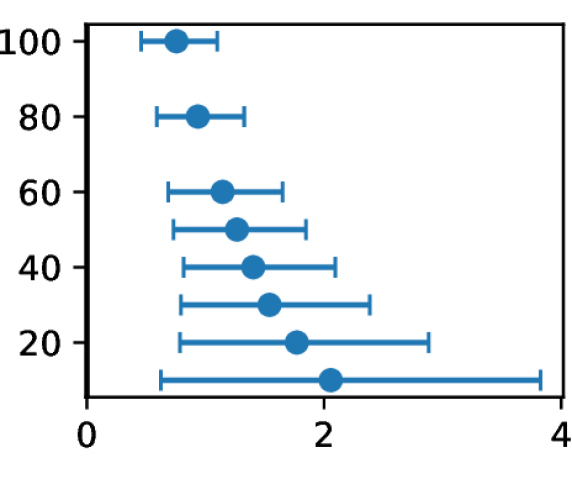

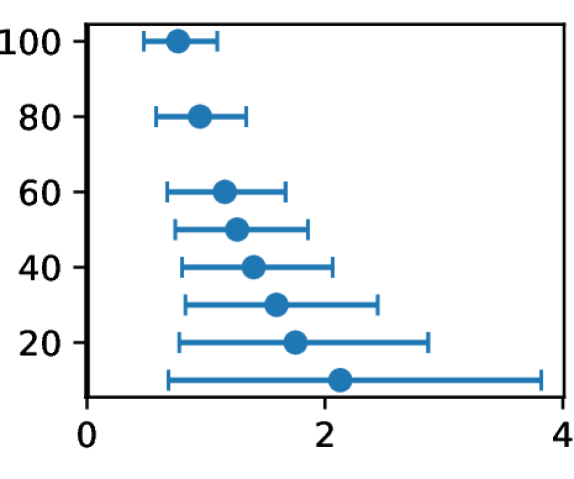

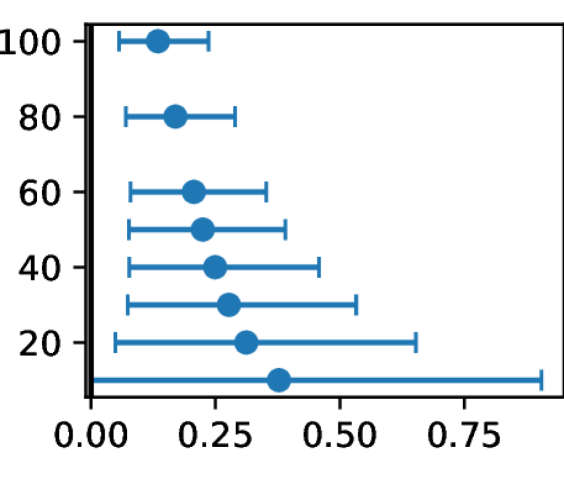

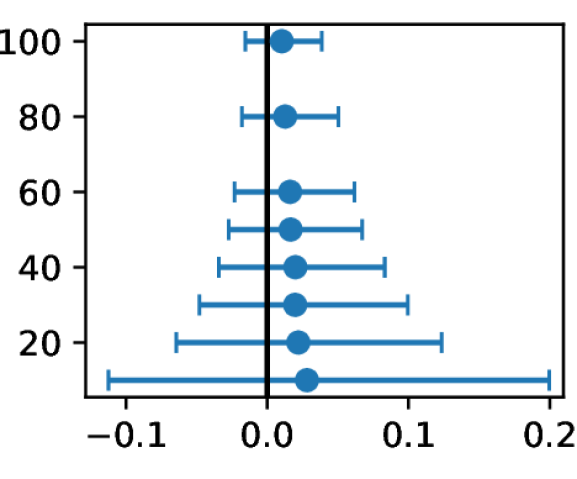

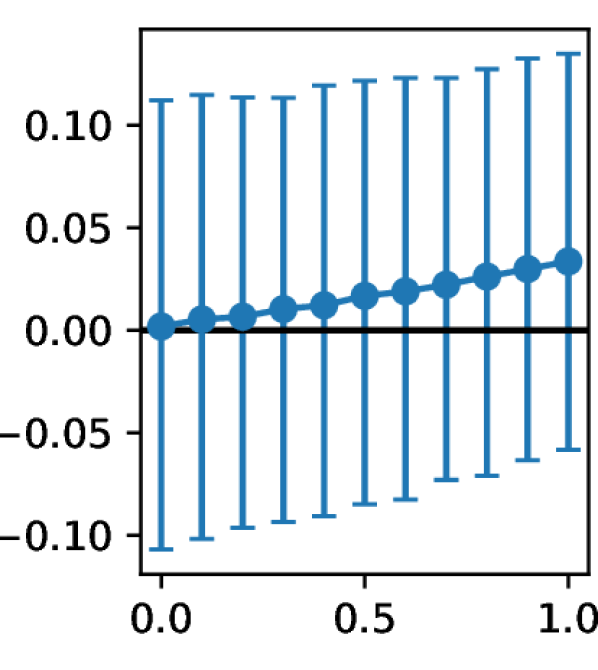

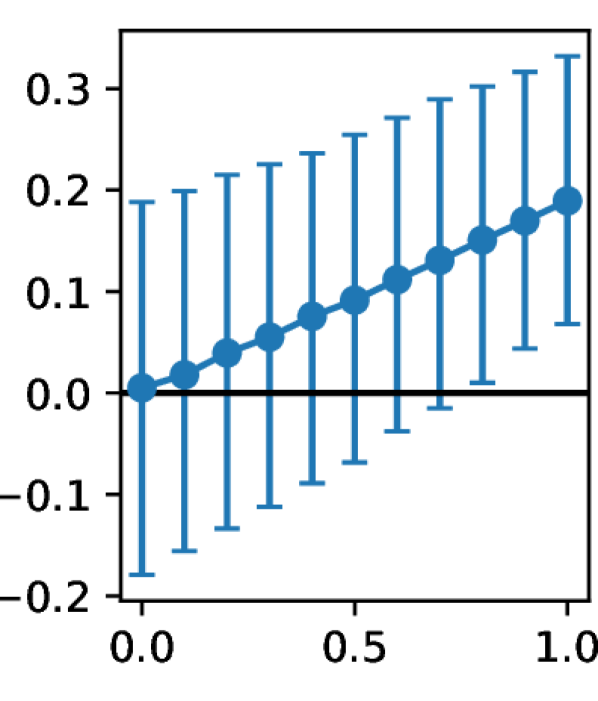

We show the results in Figure 2.7, which shows the relationship between different and the value gained under different magnitudes of estimation noise reduction. One can observe that the expected gain in value decreases when increases. This is expected: as one increases their capacity, they will run out of the most valuable work and have to settle for less valuable work that has many acceptable replacements with similar value, limiting the value DEM capabilities bring.

We can also see an inverse relationship between the size of and the uncertainty of the value gained. As a result, while the expected value gain decreases with increasing , the uncertainty drops quicker, such that at some , we will see a statistically significant increase in value gained or an acceptable Sharpe ratio that justifies investment in DEM capabilities or both. The specific value that tips the balance is heavily dependent on individual circumstances.

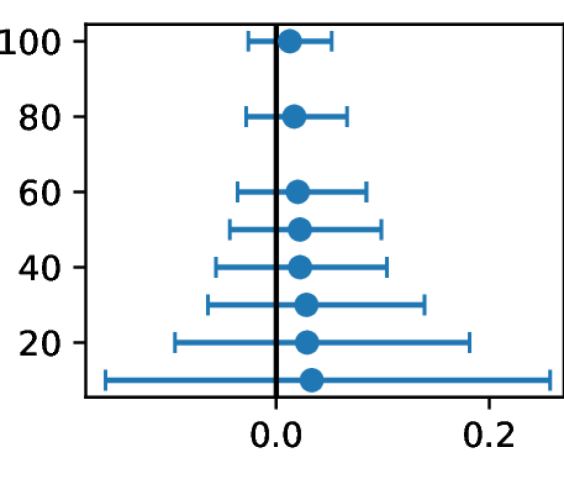

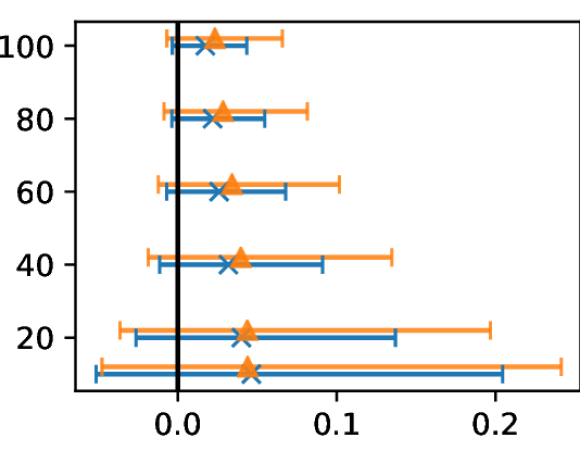

2.7.2 Marketing companies

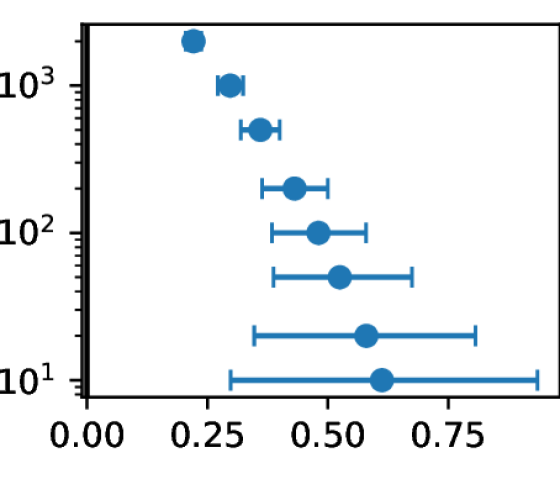

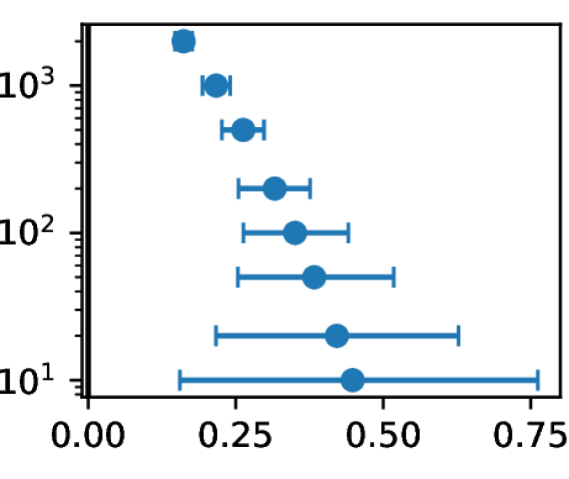

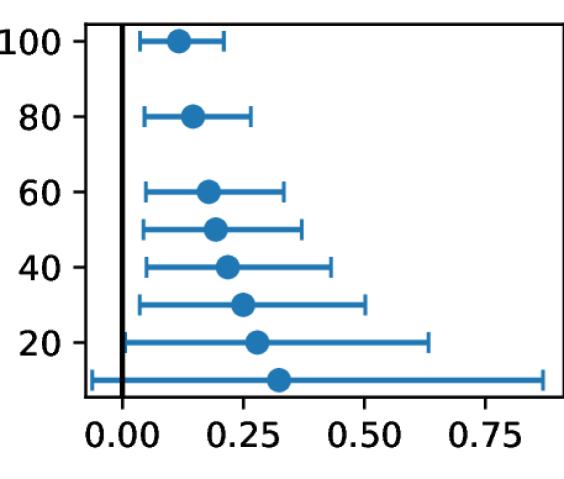

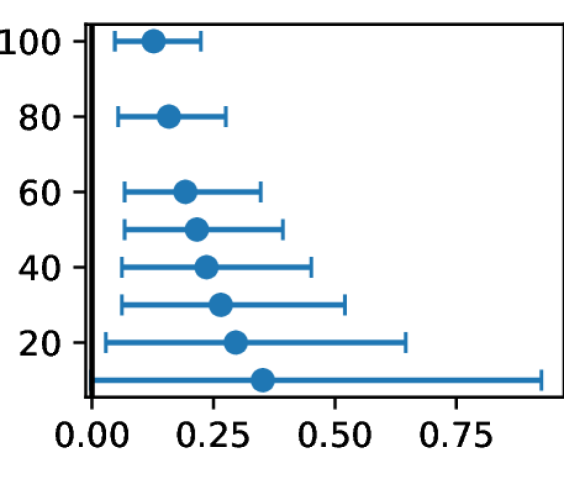

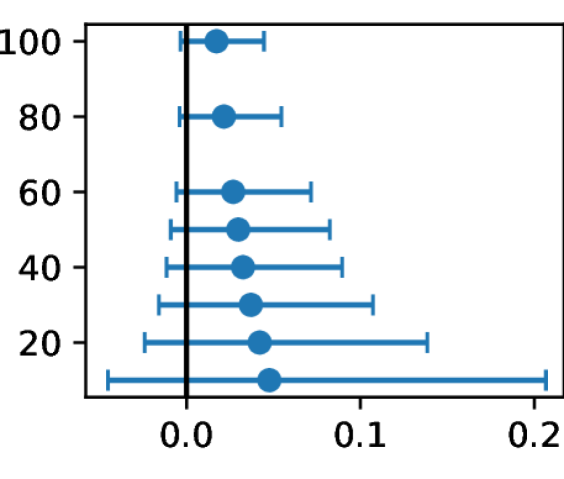

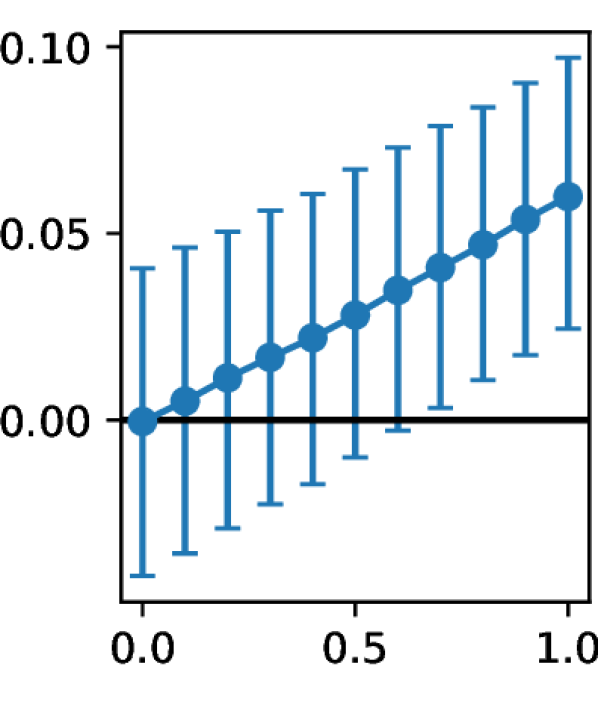

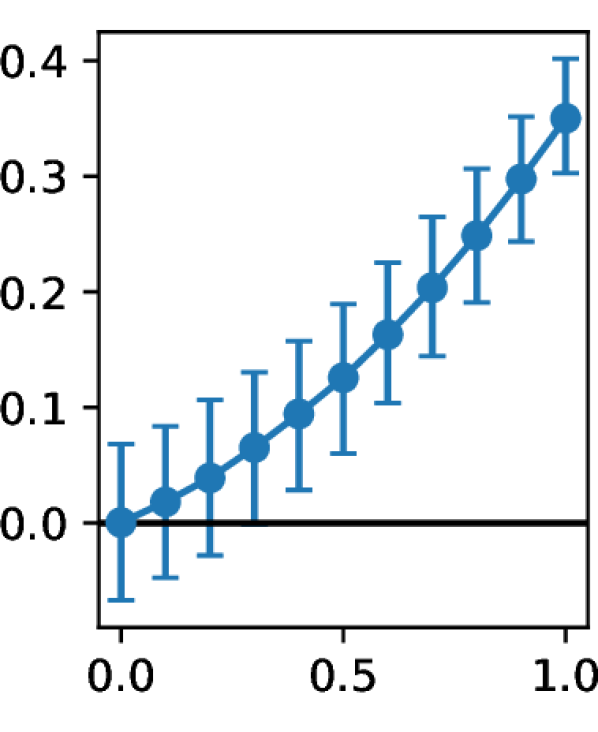

In the second case study, we repeat the process applied to e-commerce in Section 2.7.1 for the marketing experiments described in [136]. In that work, Johnson et al. reported running 184 marketing experiments that measured relative CVR uplift, with a mean relative uplift of 19.9% and standard error of 10.8%. Thus, we take and , which is slightly reduced to account for the estimation noise being included in the reported standard error.

Johnson et al. also noted that the average sample size in these experiments is over five million, which keeps the estimation noise low. However, the design of marketing experiments often comes with additional sources of noise compared to standard A/B tests [105, 172]. Hence, we assume the same estimation noise as in the e-commerce case study above (i.e., ). The larger variance in the uplifts allows us to assume a larger estimation error without DEM capabilities, and we explore the scenarios where . We set (# experiments) and vary between 10 and 100 for each combination of and .

Figure 2.8 shows the results. In the presence of a larger variability in the true uplift of the advertising campaigns () and lower capacity (), the level of estimation noise reduction that gave a statistically significant value gained in the e-commerce example is no longer sufficient. Therefore, one needs a larger noise reduction or to increase their capacity to effectively control the risk in investing in DEM capabilities. They may also be better off increasing their limited number of existing business propositions.

2.8 Empirical Extensions

We also provide two extensions, evaluated empirically, that open the door for future work in this area.

2.8.1 Valuation under independent -distributed assumptions

So far, we have spent much of the work assuming that the business propositions’ true value and the estimation noise are normally distributed. While possessing decent mathematical properties, more is needed to explain the heavy tail in the distribution of uplifts shown in [30] or [136].

In this section, we model the true value of the business propositions and the estimation noise as Generalised Student’s -distributions (see Equation (2.7)). It is difficult to derive the exact theoretical quantities under such model assumptions because Student’s -distributions do not have conjugate priors [230]. We instead simulate the empirical distribution of the value gained under different parameter combinations to understand if this model is a better alternative to that under normal assumptions. The sampling procedure is similar to that described in Section 2.6, with steps modified to generate samples using standard -distributions, which are then scaled and located as specified by Equation (2.7).

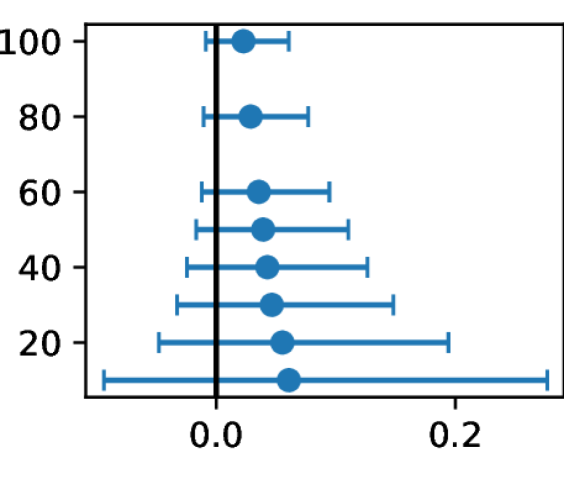

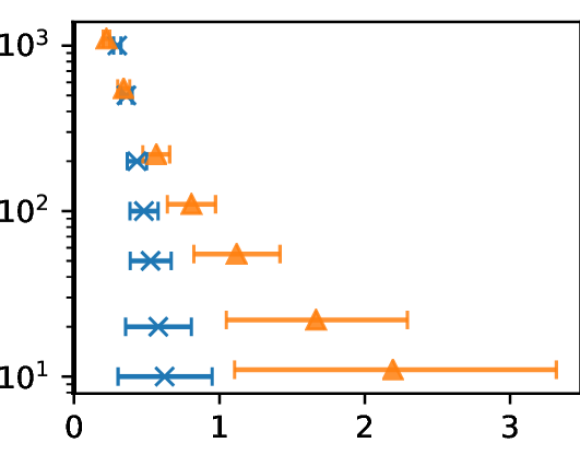

We compare the value gain estimates obtained under t-distributed and normal assumptions. For each comparison, we randomly sample values for , , , , , , , and perform 1,000 simulation runs of the four-step sampling procedure in Section 2.6 to obtain samples of D using both the and normal distributions.181818 (-distribution with three degrees of freedom (d.f.)) is used as it is the distribution with the longest tail under the family with a natural number of d.f. while retaining a finite variance. We then compare the expected values, the 5th and 95th percentile of the value gained under the two distributions.

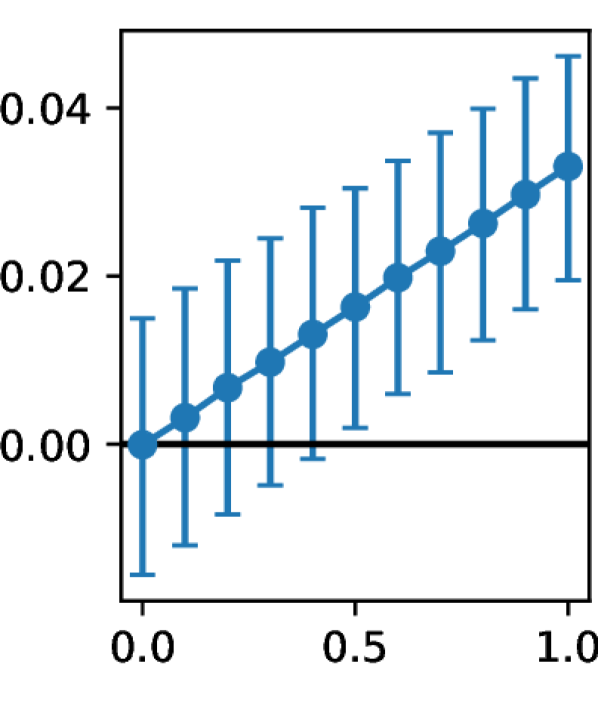

We observed from 840 comparisons that overall, the value gained under the -distributed assumptions has a higher mean (7% higher mean) and variance (7% higher in the 95% percentile on average) than that under normal assumptions. The result arises despite us setting the mean/variance of the true value and estimation noise under the -distributed assumptions to that under the normal assumptions. This suggests that the model under -distributed assumptions can capture the “higher risk, higher reward” concept.

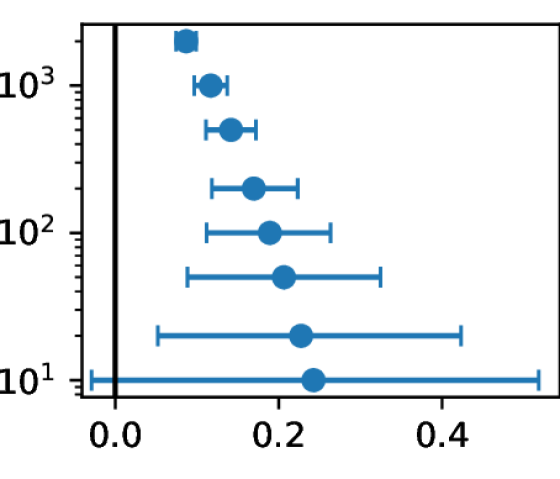

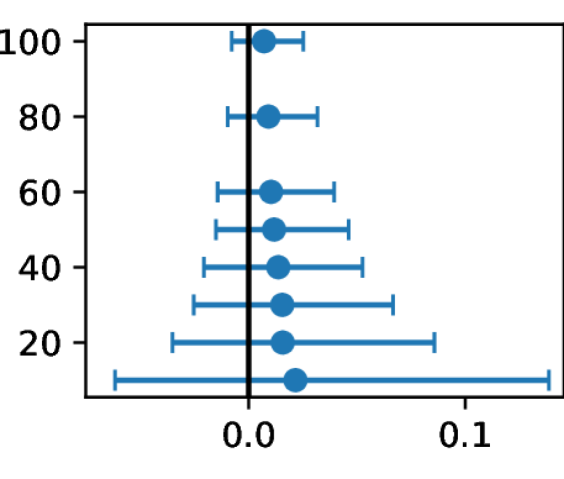

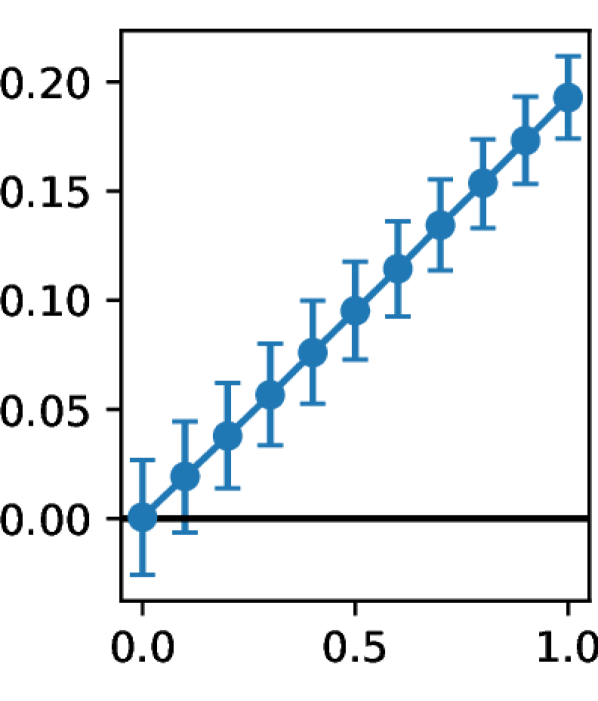

Individual comparisons paint a more nuanced picture, perhaps best illustrated by revisiting the case study in Section 2.7 under -distributed assumptions. We select a few scenarios featured in the previous section and overlay the value gained by having DEM capabilities under -distributed assumptions over that under normal assumptions in Figure 2.9. One can see that while -distributed assumptions generally yield a higher value gained, this is not always the case – for the e-commerce case, as increases, the value gained decreases quicker under -distributed assumptions than under normal assumptions. This shows that the valuation of DEM capabilities is sensitive to model assumptions.

2.8.2 Partial estimation/measurement noise reduction

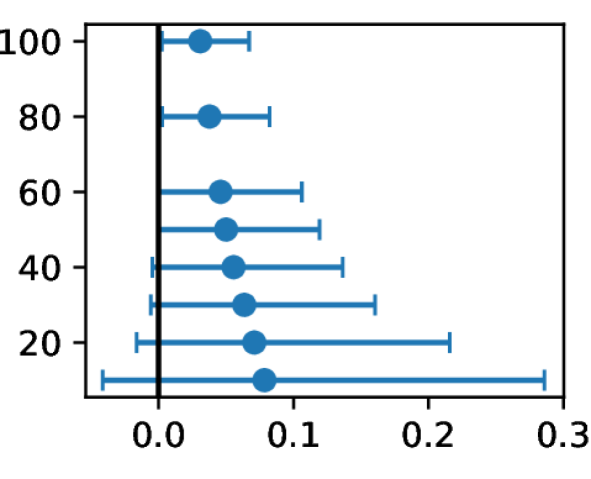

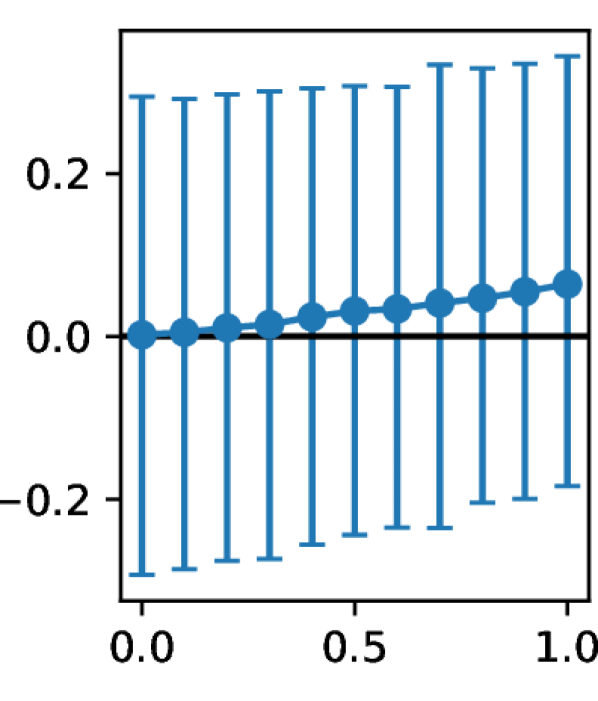

There are many situations when not all business propositions are immediately measurable upon acquiring DEM capabilities. This may be due to the extra work required to integrate additional capabilities in certain legacy systems or the limited ability to run experiments on online but not offline activities. In the case where there is a single backlog, we ask the question, will an organisation still benefit from a partial noise reduction when some business propositions’ values are obtained under reduced uncertainty while others are subject to the original noise level?

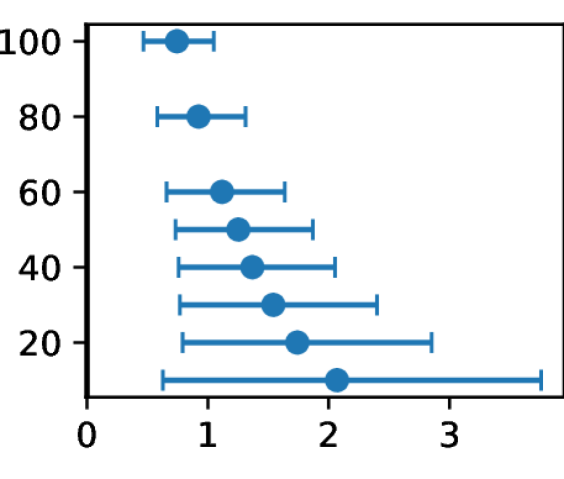

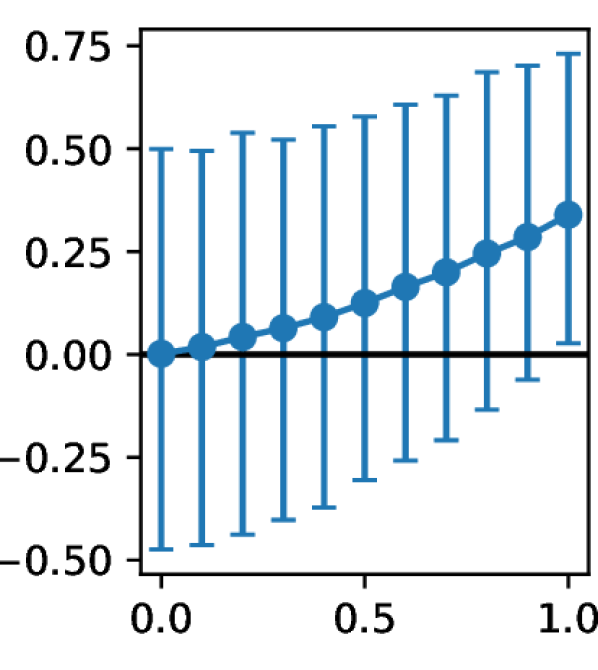

We address this by attempting to establish the relationship between the expected improvement in the mean true value of the selected business propositions and the proportion of business propositions that benefited from a reduced estimation noise (denoted ).191919We can model the estimation noise using a two-component mixture distribution parameterised by . The sampling procedure is similar to that described in Section 2.6, with Step 3 modified: instead of generating all samples from , we generate of the samples from (the lowered estimation noise) and of the samples from (the original estimation noise).

We run the procedure above under various scenarios, including a large/small , a large/small ratio between an organisation’s capacity and backlog (), and a large/small magnitude of noise reduction upon acquisition of DEM capabilities (). Figure 2.10 shows the result. We can see that under most scenarios, the expected value gained increases with linearly, while there are a few scenarios where the expected improvement in mean true value of the selected business propositions curve upward for increasing . This shows that while organisations are incentivised to acquire DEM capabilities that cover the majority of their work, in many scenarios, a partial acquisition yields proportional benefits. Potential experimenters need not consider the acquisition a zero-one decision or worry about any steep initial investment required to unlock returns.

2.9 A Brief Recap

In this chapter, we have addressed the problem of valuing DEM capabilities, which enables one to justify acquiring the said capabilities. Such capabilities deliver three forms of value to organisations. These are

-

1.

Improved recognition of the value of business propositions,

-

2.

Enhanced capability to prioritise, and

-

3.

The ability to optimise individual business propositions.

Of these, improving prioritisation is the most challenging to address while being the most applicable for organisations seeking to build DEM capabilities from scratch.

We have established a methodology to value better prioritisation through reduced estimation error using the framework of ranking under uncertainty. The key insight is that DEM capabilities reduce the estimation error in the value of individual business propositions, allowing prioritisation to follow the optimal order of projects more closely had the true values of business propositions been observable. In addition, we have provided simple formulas that give the value of prioritising under lower estimation error brought by DEM capabilities and the Sharpe ratio governing investment decisions. Finally, alongside two case studies that illustrate how we can apply the methodology in specific situations, we have provided general guidelines for conditions when such investments are inappropriate.

Chapter 3 Statistical Testing

This chapter contains background material that appeared in multiple publications:

-

•

“An Evaluation Framework for Personalization Strategy Experiment Designs”, presented at and awarded Best Student Paper of AdKDD 2020 Workshop (in conjunction with SIGKDD ’20) [176];

-

•

“Datasets for Online Controlled Experiments”, presented at the 35th Conference on Neural Information Processing Systems (NeurIPS 2021) [173]; and

-

•

“Measuring e-Commerce Metric Changes in Online Experiments”, presented at ACM Web Conference 2023 (WWW ’23) [177].

3.1 Motivation

After establishing the business case of engaging in digital experimentation and measurement, we turn our focus to two necessary ingredients for running digital experiments. They are data, which record what happens during an experiment, and statistical tests, which indicate whether groups in the experiment give different responses beyond randomness.

We first discuss statistical testing in this chapter, which will complement our approach to datasets in Chapter 4. We will also build upon the concepts introduced in this chapter in Chapter 5, when we formally describe an experiment and its underlying causal reasoning, and in Chapter 6, when we compare different experimental designs for digital experiments. Generally (and loosely) speaking, a statistical test is a statistical inference procedure that informs us whether the data collected is compatible with our hypothesis(es). In the context of digital experimentation, the data collected is often responses from two or more groups exposed to different treatments, and the hypothesis is usually whether or how much the responses from one group are different from another group.

Statistical testing may appear to be a simple and widely understood topic – at the end of the day, it is taught in many upper secondary education curricula around the globe111A non-exhaustive list of examples includes (in alphabetical order): • China: (National College Entrance Examination) Mathematics - Extended Topic 3: Probability and Statistics (Item 3(3)2), Elective Group A: Probability and Statistics (Topic 4), and Mathematics Elective Group B: Applied Statistics (Topic 4) [197, pp. 48,57,62] • Germany (Berlin & Brandenburg): (Abitur) Mathematics (Semester 4 / Q4, Advanced-level only, Theme 5 / L5) [196, p. 31] • Japan: Mathematics B (Topic (2)A(D)) [198, pp. 104, 108–109] • United Kingdom (AQA): GCE A Level in Mathematics (Subject Content O) [7, p. 23] • United Kingdom (Edexcel): GCE A Level in Statistics (Topics 7–10, 15–17, and 19–20) [219, pp. 11–13, 15–19] • USA: Advanced Placement Statistics (Units 6–9) [48, pp. 125–205] • Worldwide - International Baccalaureate Mathematics: applications and interpretation (Topics SL 4.11 & AHL 4.18) [132, pp. 57–58, 62] and forms part of the standard toolkit in scientific research. It is not. As we will show in this chapter, its development is riddled with assumptions that do not suit practical needs and its application is permeated with careless interpretations. Multiple generations of academics and practitioners have derided its misuse (and sometimes its use) [26, 47, 166, 200, 277, 297], with the latest round of controversy surrounding “-hacking” necessitating an official statement from the American Statistical Association [276].

Despite its many associated problems, statistical testing remains useful for decision-making if applied correctly. This chapter aims to provide a comprehensive introduction to the area, with a good balance between the theoretical foundation and its practical use in digital experiments. We seek to enable practitioners in digital experimentation, having arrived from diverse backgrounds, to quickly acquire the knowledge required to perform a statistical test while being mindful of the nuances and pitfalls.

Target audience

The chapter is written with a mathematically-inclined audience in mind, i.e., those exposed to university-level introductory mathematics. As we place equal importance on the applications, we will not cover formal proofs and skip through many advanced theoretical concepts, relegating them to footnotes with pointers to relevant works. However, the chapter will involve a fair bit of mathematical notations and algebraic manipulations to help us properly navigate the many concepts in statistical testing. For brevity, we also assume readers are already familiar with concepts covered in introductory probability and statistics textbooks, including conditional probability, population vs sample, and probability distributions.222One can refer to, e.g., Chapters 4–7 of [190] (more illustrative), Chapters 1–5 of [36] (more formal), Chapters 1–2 of [275] (more compact), or any relevant massive open online courses (MOOCs) delivered by a reputable higher education institution. Readers may also find expositions aimed at a broader audience in digital experimentation, e.g., early chapters of [101], Chapter 17 of [155], and [194] plus its sibling online articles, as well as works on various aspects of statistical testing written for researchers and practitioners in other fields [36, 76, 87, 96, 166, 178, 275] helpful.

A note of caution