Abstract

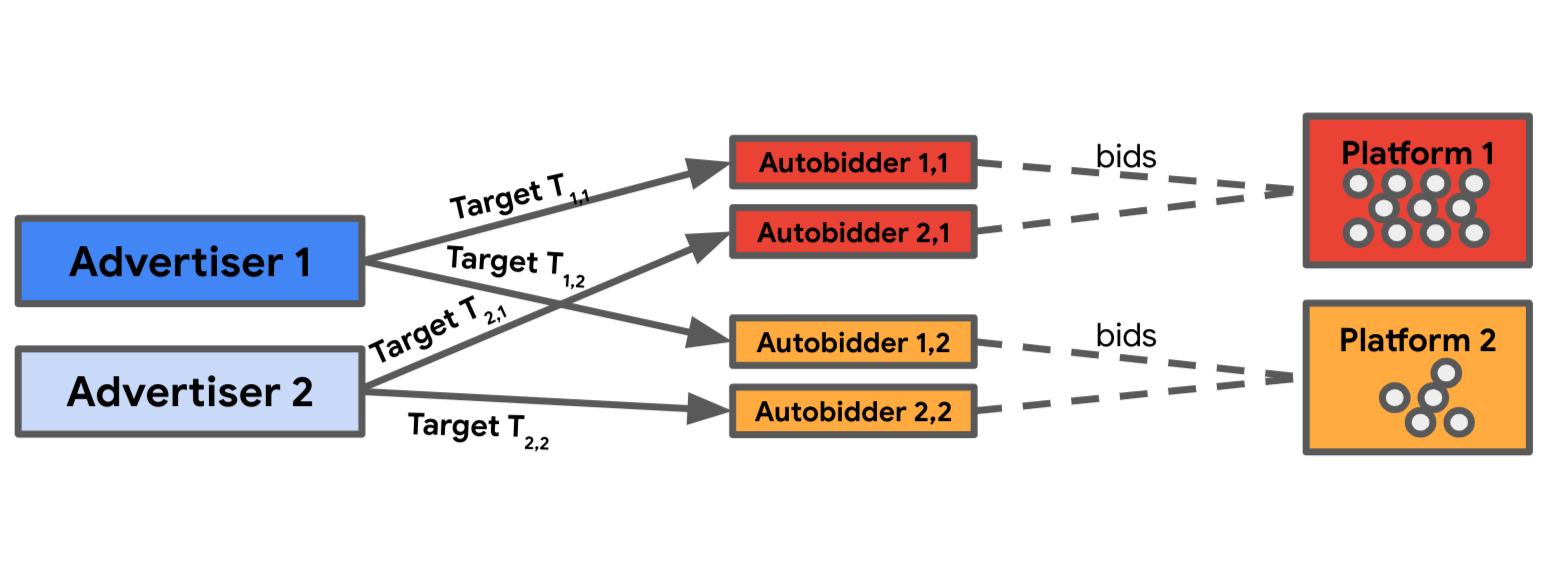

We study the problem of auction design for advertising platforms that face strategic advertisers who are bidding across platforms. Each advertiser’s goal is to maximize their total value or conversions while satisfying some constraint(s) across all the platforms they participates in. In this paper, we focus on advertisers with return-over-investment (henceforth, ROI) constraints, i.e. each advertiser is trying to maximize value while making sure that their ROI across all platforms is no less than some target value. An advertiser interacts with the platforms through autobidders – for each platform, the advertiser strategically chooses a target ROI to report to the platform’s autobidder, which in turn uses a uniform bid multiplier to bid on the advertiser’s behalf on the queries owned by the given platform.

Our main result is that for a platform trying to maximize revenue, competition with other platforms is a key factor to consider when designing their auction. While first-price auctions are optimal (for both revenue and welfare) in the absence of competition, this no longer holds true in multi-platform settings. We show that there exists a large class of advertiser valuations over queries such that, from the platform’s perspective, running a second price auction dominates running a first price auction.

Furthermore, our analysis reveals the key factors influencing platform choice of auction format: (i) intensity of competition among advertisers, (ii) sensitivity of bid landscapes to an auction change (driven by advertiser sensitivity to price changes), and (iii) relative inefficiency of second-price auctions compared to first-price auctions.

1 Introduction

Online advertisers often optimize their advertising campaigns across different advertising platforms like Amazon, Bing, Google, Meta and TikTok to reach their audience effectively. Each platform, driven by its own goals, strategically designs its auction mechanism to sell ad space. While existing research provides valuable insights on auction design within individual platforms, understanding how competition between platforms influences auction design remains largely unexplored.

This question becomes even more important with the increasing popularity of automated bidding where advertisers opt for target-ROI-based bidding algorithms aiming to maximize their value while keeping their return over investment (ROI) above a given target. If advertisers’ true preferences are consistent with such target-based bidding, i.e. advertisers are indeed trying to maximize their value while ensuring that their ROI stays above some target value (such advertisers are sometimes referred to as value-maximizing agents with ROI constraints), then the auction design of one platform creates externalities for the other platforms through the constraints of the advertisers.

In this paper, we study the question of auction design for competing platforms that face strategic advertisers bidding across the platforms. We assume that the advertisers interact with the platforms using autobidders, and that autobidders are using uniform bidding algorithms, i.e. the bid they set on each query (of the relevant platform) is proportional to the advertiser’s value for this query. 555Uniform bidding, also known in the literature as pacing bid, are well-studied algorithms in the literature as their simplicity and good performance make them appealing from a practical standpoint (Deng et al., 2021; Balseiro and Gur, 2019; Bateni et al., 2014) When there are value-maximizing agents with ROI constraints who are bidding uniformly on a single platform, the platform can maximize both welfare and revenue by using a first-price auction (FPA) (Deng et al., 2021). In contrast, we show that in the presence of multiple platforms, competition across platforms is a key factor to consider when choosing an auction format. Indeed, with sufficient competition, a platform often benefits from using a Second Price Auction (SPA) mechanism instead.666Observe that our result does not imply that a platform using FPA is acting as monopolist in the market – there are other reasons why a platform would use FPA that our theory does not cover. For example, in Display Ads, first-price auctions are widely used because they are credible (Akbarpour and Li, 2020) and increase spending confidence of advertisers (Google, 2021; Despotakis et al., 2021) as they are charged by their own bid. The key intuition behind this is as follows: when an advertiser is optimizing across multiple platforms, it tries to equalize its marginal ROI across platforms. The auction format used on a platform has a direct impact on the bid landscape777The bid landscape for an advertiser is a mapping from bid to (cost, value), which indicates the spend and value an advertiser would get if she submits certain bid, when bids for others are fixed. (and hence the marginal ROI) an advertiser faces on that platform. Hence, advertiser’s bids depend on the auction choice of every platform. As such, in choosing its auction format, each platform trades off the efficiency gain it might get from the use of one auction format with the higher bids it might get from the use of another auction format.

We uncover and quantify this trade-off in a stylized model with two platforms and two advertisers. Each revenue-maximizing platform owns a continuum of queries and chooses between SPA and FPA as the per-query auction mechanism to sell all their queries. We assume that platforms are symmetric in the sense that they own the same distribution of inventory, with possibly asymmetric market shares. Each advertiser is a value-maximizing agent with a target ROI constraint that upper-bounds the average cost per unit value (conversion) they can pay across all the platforms they participate in. The platforms and advertisers play a sequential game as follows:

-

1.

First, all platforms independently choose between SPA and FPA to sell their queries.

-

2.

Second, the advertisers strategically choose target ROIs to submit to a platform-specific autobidder who bids on behalf of the advertiser on the respective platform.888Alternatively, we can allow the advertisers to directly submit a uniform bid to each platform., 999Note that there is a separate autobidder corresponding to each advertiser and platform pair.

-

3.

Each autobidder (corresponding to an advertiser and a platform) takes its target ROI input and computes bids using a uniform bidding strategy, i.e. the bid for each query is proportional to advertiser’s value for the query.101010Uniform bidding is the optimal bidding strategy among all bidding strategies when the underlying auction is truthful like SPA (Aggarwal et al., 2019). For other auction formats, an advertiser could potential benefit by splitting their campaigns to induce a non-uniform bidding on the platform. Such strategic behavior is not modeled in this work. It makes sure that the input target ROI is not exceeded.

-

4.

Finally, the queries are allocated and payment accrues according to the chosen auction format.

Advertisers’ targets and per-query valuations are common knowledge to all agents in the game and we consider subgame perfect equilibrium as our solution concept.

We first solve the advertisers’ subgame and characterize the optimal bidding when platforms have already declared the auction formats. Theorem 3.2 shows that an advertiser’s optimal target ROIs for different platforms are such that they obtain the same marginal cost on each of the platforms they participate in. We show that if a platform is using SPA as its auction mechanism, then the marginal cost on that platform is exactly equal to the bid the autobidder sets on the advertiser’s behalf. On the other hand, if the platform is using FPA, then the marginal cost on that platform has an additional term that depends on the bid landscape the advertiser faces on the platform. We further show that since in equilibrium landscapes are endogenously generated by the other advertisers’ bids, the difference between the marginal costs of FPA and SPA depends on the elasticity of advertisers’ valuations. The more elastic the valuations, the more the advertiser’s report changes in reaction to the auction change of the platform. We refer the advertiser’s report change to as bidding reaction throughout the paper.

In Section 4 we show that the bidding reaction is an important factor in allowing (SPA, SPA) to be an equilibrium of the platforms’ game. For this, we first consider a constrained model where advertisers use the same uniform bid across all platforms and, hence, may not be able to equalize marginals. In this case, Theorem 4.1 shows that FPA is a weakly dominant strategy for each platform.111111That is, the platform’s revenue by using FPA is weakly greater than using SPA regardless of what auction format other platforms are using.,121212In the paper, we show that our proof-technique generalises for general N platforms and M advertisers. We next study the case where there is a single large advertiser facing a static bid landscape on each platform.131313For example, this can happen when all the remaining advertisers are small value-maximizing advertisers that are interested in a single query. In this case, the bidding reaction only comes from the large advertiser and hence the bidding reaction is weak. Theorem 4.2 shows that FPA is a weakly dominant strategy for each platform in this case as well.

In Section 5 we study the inefficiency-free setting where, in equilibrium, queries are efficiently allocated regardless of the auction formats chosen by the platforms. We first consider the setting where both platforms have equal market share. Theorem 5.1 shows that a platform’s auction decision depends on (i) the elasticity of advertiser’s valuations (), which measures how strong the bidding reaction is and (ii) the relative difference of advertisers’ valuations across the queries they compete in, captured by a competition metric () which measures how close the valuations are across advertisers. When , then SPA is a dominant strategy and hence (SPA, SPA) is the unique equilibrium of the game. Conversely, if then FPA is a dominant strategy and hence (FPA, FPA) is the unique equilibrium of the game. Thus, given a fixed level of competition, if the bidding reaction is strong enough then SPA is an optimal auction to choose. Likewise, given a fixed level of bidding reaction, as the market becomes sufficiently competitive within advertisers then SPA is an optimal auction to choose. Interestingly, we further show that the same necessary and sufficient condition can be applied to the more general setting with multiple () platforms and asymmetric market share (Theorem 5.3): For every platform, SPA is a dominant strategy if and FPA is a dominant strategy if .141414Observe that even if one of the platforms owns the whole market, because SPA is also efficient, that platform is indifferent between FPA and SPA. In other words, this result shows that from a platform’s perspective, the elasticity and level of competition (both independent of the platform’s market share) outweigh the market share effects in this setting. A consequence of these two theorems is that the intensity of competition across platforms (which depends on the number of platforms and market share) can only impact the platform’s auction decision when there is an efficiency loss when moving from FPA to SPA.

In Section 6, we tackle the case where there is also an efficiency tradeoff between FPA and SPA. Given the technical challenges in characterizing the equilibrium for a general model, we analyze the model for two families of valuations that are tractable. These valuation families depend on a single parameter, , which affects the intensity of competition across advertisers, the elasticity of the advertiser, and the level of efficiency loss of SPA relative to FPA. By solving for the equilibrium, we find that the level of inefficiency of SPA vs. FPA also plays an important role in determining which auction format a platform should choose. In the first example, we observe that, even though elasticity and competition are both increasing in , FPA becomes the dominant strategy for large as the inefficiency loss increases. In the second example, we observe that, for all , the inefficiency loss relative to the competition and elasticity is small and therefore, in equilibrium, it is a dominant strategy for platforms to use SPA. These examples showcase that for a general environment, there are three main factors that a platform should consider when choosing their auction format – level of advertiser competition across queries, elasticity of advertisers, and the level of inefficiency of SPA compared to FPA.

Practical Implications of Our Results

As noted above, when there is only one platform facing value-maximizing advertisers with ROI constraints who are using uniform bidding (either directly or indirectly through autobidders), it is optimal for the platform to use FPA to maximize both welfare and revenue. This might motivate a platform to try using FPA even in the presence of other platforms. Our results show that advertiser response in the form of different target ROIs submitted to autobidders can often be large enough to affect which auction format is better for the platform. Thus, it is very important for a platform to properly account for advertiser response in evaluating different auction formats.

To make this point clear, suppose that a platform is currently using SPA and wants to experiment to see if switching to FPA would increase its revenue. We can then envision the following dynamics. Initially, autobidders (that are typically algorithms that react rapidly to auction changes) would converge to a new bidding equilibrium – for each advertiser, the autobidder will set a uniform bid multiplier equal to the current target (which is the same as the target submitted under SPA, , since the advertiser has not yet responded – see Theorem 6.1 Deng et al. (2021)). After this first stage on the dynamics, the platform obtains a (weakly) higher revenue under FPA than SPA.151515For a fixed set of targets within a platform, Aggarwal et al. (2019) shows that the revenue of SPA can be half of the optimal welfare, while Deng et al. (2021) shows that the revenue of FPA with uniform bidding is exactly the optimal welfare. Thus, if the platform makes a decision at this stage of the dynamics, it would wrongly conclude that FPA is better. In the further stages of the dynamics, advertisers react when they observe that the value obtained from this platform is lower. This might lead them to decrease the target on this platform and increase the targets on other less expensive platforms. These adjustments would trigger iterative responses from auto-bidders across all platforms and further advertiser reactions. Our theory predicts that when this dynamic stabilizes, depending on the competition among advertisers, the elasticity of the advertiser’s valuations and the SPA-to-FPA inefficiency trade-off, the final targets submitted by advertisers could be sufficiently low to make the FPA revenue lower than the SPA revenue. Thus, using measurements from an early stage of the dynamics could lead the platform to mistakenly adopt FPA.

1.1 Related Work

With the growth of autobidding in online ad auctions, there has been substantial research interest in problems related to autobidders. We discuss some of the most relevant work and compare and contrast it with our results.

Multi-Channel Mechanism design

Aggarwal et al. (2023) focuses on a single platform owning multiple channels, each selling their queries using SPA with a reserve price. The authors quantify the cost of having each channel optimizing its own reserve price compared to a global platform policy. In our paper, we study competition across platforms and consider the problem of platforms choosing between different auction mechanisms, not just optimizing their reserve prices. Motivated by the Display Ad market, Paes Leme et al. (2020) studies a model where multiple platforms compete for profit-maximizing bidders that are constrained to use the same bid on all platforms (in our language, they bid using a uniform bid). Their main result shows that FPA is the optimal auction for the platforms, similar to Theorem 4.2 where we show the same conclusion for the value-maximizing case.

Bidding Algorithms for Autobidders, Uniform Bidding

Uniform bidding (aka constant pacing) has been extensively studied in the context of budget constraints and, more generally, for Autobidding on a single platform. Aggarwal et al. (2019) initiated the study of the Autobidding problem and, among other things, showed that uniform bidding is optimal if the platform uses a truthful auction format. Conitzer et al. (2022b, a) studies constant pacing for budget constraints on a platform that uses SPA or FPA. Agarwal et al. (2014); Xu et al. (2015) does an empirical study of the use of uniform bidding on real-world platforms when the bidder has budget constraints. In this work we assume uniform bidding for autobidders and study the platform’s auction choice in a multi-platform environment.

Bidding across Multiple Platforms

Finally, Susan et al. (2023) studies bidding strategies for utility-maximizing advertisers across multiple platforms under budget constraints. Deng et al. (2023) focuses on bidding for value-maximizing advertisers under both budget and ROI constraints and shows that optimizing over per-platform ROIs can be arbitarily bad when the advertiser has both ROI and budget constraints. In contrast, with only ROI constraints, we show that marginal equalization using per-platform ROIs is the optimal bidding strategy.

2 Model

Our environment consists of two groups of strategic agents, platforms and advertisers, as well as autobidders who bid on an advertiser’s behalf on different platforms (see Figure 1).

Platforms: There are platforms on the market and we denote the set of all platforms. Platform owns a continuum of single-slot queries indexed on a set which without of loss of generality we normalize to be .161616We use the standard Lebesgue measure and the Borelian -algebra for Each platform uses a per-query auction mechanism to sell the queries and would like to maximize its own revenue. Throughout this paper, we restrict the space of auction mechanisms to the two canonical auction rules: second-price auction (SPA) and first-price auction (FPA).

Advertisers: There are advertisers interested in the queries and we denote the set of advertisers. Advertiser ’s valuation for query on platform is , where is a continuous differentiable function on .171717We consider the left derivative on and the right derivaitve on The advertiser’s objective is to maximize the total value they get subject to having an average cost per value of at most a given target .181818In this paper we focus on the setting where advertisers are ROI-constrained but not budget-constrained. It’s an interesting open question to study the same problem with budget-constrained advertisers. We notice that it is equivalent to having a target ROI of . Denote the cost of winning query on platform by . Then advertiser ’s objective consists on solving the following problem191919All valuation functions are regular enough so that and are integrable functions.

| s.t. |

Here we denote the set of queries that advertiser wins on platform . Observe that by re-scaling the value functions, we assume without loss of generality that for all . Advertiser ’s action consists of submitting a target to the autobidder for each platform , who bids on behalf of advertiser as described below.

Autobidders: For a given platform , autobidder receives as input target from advertiser and bids on query . The uniform bid multiplier is computed by the autobidder for each advertiser independently with the goal to maximize advertiser ’s value on the platform:

| s.t. |

where is endogenously obtained as function of the auction format chosen by the platform and the bids received for query .202020For any query such that , advertiser wins query . If the auction rule is SPA then . If the auction rule is FPA, the cost is instead .

Timing, Information and Equilibria

The problem we are interested in studying is modeled by the following sequential game where platforms move first and advertisers respond.

-

1.

Platform independently and simultaneously announces if it will use a SPA or FPA to sell their queries.

-

2.

Advertiser independently and simultaneously submits targets to the autobidder managing platform .

-

3.

For each Advertiser , autobidder computes an optimal bid multiplier , and bids for advertiser on query in platform .

-

4.

Allocations and payoffs accrue according to the auction rules.

We assume that the advertisers’ valuations and targets are common knowledge to all players, so that the game is of complete information. 212121This is a reasonable assumption in complex settings, see e.g. Alimohammadi et al. (2023). Our solution concept is subgame perfect Nash equilibrium (SPNE).

Remark 2.1.

Given that the game is of complete information, in any SPNE, advertiser can foretell what bid multiplier autobidder will submit on her behalf. Thus, in the rest of the paper, we omit the autobidders’ role and let the advertiser directly choose without explicitly submitting to autobidders.

Another way to think about this is that the bidding interface provided by a platform allows submission of a by advertiser , with the understanding that ’s bid for query on platform is .

We impose the following equilibrium refinements on the advertisers’ bidding subgame to remove unnatural equilibrium and asymmetric equilibrium in symmetric environments.

Assumption 2.2.

Given SPNE, let be the bidding strategies for a given history of the game. We impose the following refinements:

-

(R1)

The equilibrium bid multiplier is not weakly dominated by a bid multiplier .

-

(R2)

If two advertisers have mirroring valuations on all platforms,222222Two advertisers have mirroring valuations on platform if for all (see Section 5 for more details.) advertisers use the same bid multiplier.

-

(R3)

If each advertiser has the same valuation function on two different platforms, and both platforms use the same auction format (i.e. the two platforms are symmetric both in terms of valuations as well as auction format), then each advertiser uses the same bid multiplier on both platforms.

Refinement (R1) is standard in the literature (e.g., (Aggarwal et al., 2019, 2023)) and removes unnatural equilibria: for example, if there is a single platform running SPA, then the equilibrium where one bidder bids a large number and the second bidder bids does not pass this refinement as the second bidder’s bid is dominated by bidding . Refinements (R2)-(R3) restrict to symmetric bidding equilibrium whenever advertisers’ valuations are symmetric in the mirroring sense (by reordering the queries) or platforms are fully symmetric in terms of their inventory and auction choice.

Benchmarks

Before we finish this section, we define the total liquid welfare of the system as the allocation that maximizes total value across advertisers. This is also an upper-bound on the total revenue that can be generated across platforms.

Definition 2.3 (Liquid Welfare).

The (optimal) liquid welfare of the system is defined as

where is a partition of for all .

Remark 2.4.

Let denote Platform ’s revenue in a given equilibrium. Then, .

We introduce the competition benchmark that captures the level of advertiser competition within a platform.

Definition 2.5 (Competition).

Given advertisers valuations , we define the level of advertisers’ competition on platform by

where are the highest and second-highest valuations for query , respectively.

The competition metric measures, on average across the queries, the difference in valuation between the highest and second highest bidders. The metric is normalized by the liquid welfare so that it lies in and is scale-free. implies that in each query there is only one relevant advertiser that can win the query, whereas if for every query, there are multiple bidders with the same value for it. In particular, if there are just two bidders then their valuations for the queries are identical.

3 The Advertiser Bidding Subgame: Marginal Cost Equalization

In this section, we study the bidding subgame between advertisers under a fixed choice of auction formats for the platforms. All proofs are deferred to Appendix A.

In Section 3.1, we first study a single advertiser’s bidding problem, i.e. how to set bid multipliers on different platforms after observing the auction rules the platforms commit to implement and the others’ bids. The main result in this section is that the advertisers will set their bid multipliers such that the marginal cost per unit value, henceforth marginal cost, is the same across all the platforms they participate in. We find the advertiser’s best strategy by solving for the optimal bidding strategy when facing a general auction environment. We show that when the bid landscapes, i.e. the mapping from multipliers to the total value and cost, satisfy standard convexity conditions (see Theorem 3.4), equalizing marginals across platforms is a necessary and sufficient condition for optimality.

In Section 3.2, we study the bidding equilibrium of the subgame, that is when landscapes are endogenous, and characterize the equilibrium conditions for the case of two symmetric platforms and two advertisers. We define an advertiser’s elasticity, a key component that helps understand the bidding reaction advertiser’s experience when a platform deviates from FPA to SPA.

3.1 Advertiser’s Optimal Bidding

We fix an advertiser and bids of the other advertisers. Denote by the bid functions for all other advertisers. We denote by the aggregate value the advertiser obtains on platform when using a bid multiplier . Formally, , where is the set of queries advertiser wins on platform by using bid multiplier . Throughout this section, we will simplify the notation and use instead when and are fixed and clear from context.

Let be the set of platforms selecting SPA and FPA as their auction rule, respectively. Notice that from Myerson’s characterization of truthful auctions, the total cost on platform is given by . On the other hand, for , the cost on the platform corresponds to the bid of on the queries they win, thus . The advertiser’s problem turns to

| (1) | ||||

| s.t. | (2) |

In what follows we impose the following conditions on the aggregate functions .

Assumption 3.1.

The functions satisfy that

-

1.

is increasing and twice-differentiable for and that equals a constant for , for some .

-

2.

is concave.

Assumption 3.1 (1) implies that a bid level exists (potentially infinity) so that the advertiser gets all the inventory on the platform. Yet the advertiser needs to bid strictly more than their value (i.e. ) to buy all the inventory of platform . Assumption 3.1 (2) means that the marginal gain on value is decreasing as a function of the bid. We show in Lemma 3.3 that the marginal cost function is decreasing if is concave.

The following theorem provides the regularity conditions for existence of a solution to the advertiser problem.

Theorem 3.2.

Marginal Cost Equalization

We now formalize the concept of marginal cost for this environment and show that it is a key element to characterize the advertiser’s bidding problem. The marginal cost intuitively corresponds to the additional cost an advertiser would have to pay to marginally increase their value on a platform. Formally,

The following lemma shows that the marginal cost is directly related to the auction rule chosen by a platform.

Lemma 3.3.

Suppose that Assumption 3.1 holds. Then for ,232323We consider the interior derivative for the extreme points .

Moreover, when is concave, we have that is an increasing function on .

Observe that the marginal cost on an SPA platform () is independent of the bids of other advertisers and only depends on the bid multiplier chosen by the advertiser. On the other hand, on an FPA platform, the marginal cost includes a second positive term which depends on other advertisers’ bids. This makes the marginal cost at a given bid larger on FPA than on SPA.

To see how the marginal cost function is computed in Lemma 3.3, suppose the advertiser increases their bid multiplier from to so they get an increase in value of . Because the auction is SPA, the change in cost by raising the bid multiplier by only affects the new queries the bidder wins at . Thus, the change in cost is . Taking , this leads to a marginal cost of . When the auction is FPA, the cost increase from increasing the bid multiplier to not only comes from the new queries the advertiser obtains, but also from the increased payment for the old queries that it is already winning. This adds an extra cost of , leading to an excess term in the marginal cost of as .

The next theorem shows if the marginal costs are increasing, then an advertiser that equalizes marginal costs while meeting its target constraint bids optimally.

Theorem 3.4.

We conclude this section by providing a sufficient condition on to have a non-trivial solution to (4). Therefore, we show that equalizing marginal costs is a necessary and sufficient condition to solve the advertiser’s bidding problem. In Section 3.2, we translate the condition into conditions on the advertisers’ valuations.

Theorem 3.5.

3.2 Advertiser Bidding Equilibrium

We now apply the previous results that characterize the best response of the advertiser to solve the advertisers’ equilibrium in every platform subgame. We focus on instances where there are two symmetric platforms and two advertisers . Given that platforms are symmetric we drop the index on advertisers’ valuations.

Notice that by re-indexing the queries, without loss of generality we can assume that is non-decreasing on so that queries are ordered non-decreasingly in terms of their value for advertiser 1 relative to advertiser 2. In other words, if advertiser 1 is getting query , then advertiser 1 is also getting query . Moreover, if is an increasing function then for any non-zero bid multipliers used on a platform we have that is the query-threshold for such bid multipliers.242424In case that the minimum does not exist, we take . Thus, advertiser 1 wins all queries in and advertiser 2 gets queries .252525Because queries are a continuous set, it is irrelevant who wins query . In addition, we define to be the threshold query in the efficient allocation.

We are now in position to solve the three possible subgames that can arise in our game: (FPA, FPA), (SPA, SPA) or (SPA, FPA). 262626Due to the symmetry of the platforms, the solutions under (SPA, FPA) and (FPA, SPA) are identical.

Case I: (FPA, FPA) subgame. Since platforms are symmetric and using the same auction format, our equilibrium refinement (see 2.2) imposes that advertisers submit the same bid multipliers in both platforms. Hence, the subgame is equivalent to the case where there is a single platform using FPA. As discussed in Deng et al. (2021), a bid multiplier is a dominant strategy for each of the advertisers, and therefore the equilibrium allocation is . We summarize these findings in the following theorem.

Theorem 3.7 ((FPA, FPA) subgame (Deng et al., 2021)).

For the (FPA, FPA) subgame, the unique equilibrium with undominated strategies is that advertisers bid for both platforms. The equilibrium query threshold and the revenue each platform obtains .

Case II: (SPA, SPA) subgame. As in the previous case, we have that the problem is equivalent to that of a single platform running SPA. The existence and uniqueness of equilibrium has been analyzed in Alimohammadi et al. (2023).

Theorem 3.8 ((SPA,SPA) subgame (Alimohammadi et al., 2023)).

Suppose that is an increasing function. There exists an equilibrium and the equilibrium query-threshold solves the equation

| (5) |

Moreover, if is convex and is decreasing on , the equilibrium is unique.

Case III: (FPA, SPA) subgame. In this case platforms are no longer symmetric in regards to the auction format and, thus, our subgame analysis can no longer be reduced to a single platform problem. For each advertiser , denote and the bid multipliers of advertiser for the platform that uses SPA and FPA respectively.

The following lemma provides the conditions on the bid landscapes so that marginal cost equalization of both advertisers becomes a sufficient condition to pin-down equilibrium.

Lemma 3.9.

Suppose that is an increasing function, a decreasing function and is a convex function. Then for any positive bid multiplier () the landscape advertiser 2 (advertiser 1) faces

satisfies 3.1.

We now use Lemma 3.3 to derive the condition for marginal cost equalization for an advertiser. For this goal, we first define an advertiser’s elasticity – a key metric that dictates how the marginal cost on the FPA platform compares to that on an SPA platform for a given bid. It is a combination of the additional cost paid by winning an additional query and the additional cost paid on existing won queries when the bid is increased to win an additional query. By applying the marginal equalization lemma, we will show that elasticity dictates how different the bid multipliers of an advertiser are on FPA and SPA platforms.

Definition 3.10 (Elasticity).

Let . We define the elasticities for at query

| (6) | |||

| (7) |

Lemma 3.11.

Consider bid multipliers of advertiser . Then, the marginal cost of advertiser on the SPA platform is and on the FPA platform is .

We are now in position to present the main result of the section.

Theorem 3.12 ((FPA, SPA) subgame: Marginal Cost Equalization).

Suppose that is an increasing function, a decreasing function and is a convex function. Suppose is non-zero bid multiplier solution to the system of equations

| (8) | |||

| (9) | |||

| (10) |

where are the equilibrium query thresholds, i.e., and . Then conform an advertiser equilibrium of the subgame.

Furthermore, if the above system of equations has a unique nonzero solution and , the equilibrium is unique.

Observe that the system of equations (8)-(10) correspond to the marginal cost equalization problem of Theorem 3.4 (Equation (4)) which implies that a nontrivial solution is an equilibrium. To guarantee uniqueness of equilibrium we need to rule out the corner-case equilibrium where one of the advertiser is obtaining all the inventory of any platform and might not be equalizing their marginal costs. However, since for any positive bid multiplier, advertiser 1 (or advertiser 2) cannot get a subset of queries close enough to (or ). Thus, with this assumption, there is no corner-case equilibrium.

4 Importance of Bidding Reaction

In this section, we present two examples that showcase the importance of the advertisers’ bidding reaction in allowing for (SPA, SPA) to be a feasible equilibrium of the platform-advertiser game. When a platform changes its auction, the advertisers will solve the problem in Equation (1,2) and may change their bid multipliers in reaction to the auction change. We refer to this effect as the advertiser’s bidding reaction.

In the first example, advertisers are forced to use the same bid multiplier across platforms, and thus cannot equalize marginal costs;272727If all platforms are using SPA, notice from Theorem 3.2 that using the same bid multiplier is optimal, and hence, it equalizes the marginal cost. In the second example, there is a single large advertiser bidding across platforms and competitors are small value-maximizing advertisers bidding in a single query, and thus, they don’t adjust their bids when the auction changes. These two examples disable advertisers’ reaction to the auction change to some degree. The main conclusion of this section is that in these two examples the platforms will always end up at the (FPA, FPA) equilibrium. We attribute this result in large part to the lack of advertisers’ bidding reaction.

4.1 Case I: Suboptimal uniform bidding across platforms

We first study the case where advertisers are forced to use the same bid multiplier across all platforms, i.e. advertiser ’s bid on a query in platform is given by for all .

The main result of this section is that if advertisers are using weakly undominated 282828Weakly undominated strategies are those that are not weakly dominated by any other strategy. bidding strategies then in the unique Nash equilibrium of the game, each platform uses FPA to sell their queries and in return, each advertiser uses a bid multiplier of across all platforms. Removing weakly dominated strategies, those where there are weakly dominant alternatives, precludes spurious equilibria. Furthermore, the revenue across all platforms matches the liquid welfare . In particular, this implies that if a single entity owns all platforms, then the platform is implementing the revenue-maximizing policy. The proof of Theorem 4.1 is deferred to Section B.1.

Theorem 4.1.

The unique equilibrium of the platform-advertiser game under uniform bidding is for the platforms to announce FPA to sell their queries and for advertisers to submit multipliers . Furthermore, the total revenue across all platforms is equal to the liquid welfare .

4.2 Case II: Single Strategic advertiser vs. static advertisers

In this section, we study the setting where a single strategic advertiser bids across all platforms. For each platform and each query , the strategic advertiser competes with a static value-maximizing advertiser that only bids on this query. Since the static advertiser only participates in the auction for a single query, it is optimal for them to bid truthfully.292929If the auction is FPA, their value is the largest bid to without violating the ROI constraint; Suppose the auction is SPA. When the second-highest bid is less than their value, bidding truthfully can win the auction without violating the ROI constraint. On the other hand, when the second-highest bid is larger than their value, they can not win without violating the constraint. In other words, no static advertiser will respond to the auction change.

We show that for this case, the unique Nash equilibrium of the game is for all platforms to announce FPA to sell their queries, and for the strategic advertiser to submit a multiplier of .

Theorem 4.2.

In the case of a single strategic advertiser against static advertisers, the unique Nash equilibrium is for the platforms to use FPA and for the strategic advertiser to use a multiplier of 1 on each platform.

The high-level idea of the proof is as follows. Since static advertisers will always bid their value regardless of the auction choice, the single strategic advertiser is competing with some static value function for each platform . We notice that if a platform uses FPA, the revenue must be at least . If the strategic advertiser wins some query , their bid must be at least which is also the payment; if the static advertiser wins, the payment is . Similarly, the revenue when platform uses SPA is at most . Thus FPA is a weakly dominant strategy for all platforms. Finally, if all platforms use FPA, then it’s clearly optimal for the advertiser to send their target on all platforms, i.e. use a bid multiplier of 1. See Section B.2 for a formal proof of Theorem 4.2.

5 The Inefficiency-free Case

In this section, we study the inefficiency-free setting where queries are efficiently allocated at the bidding equilibrium of any auction outcome. Recall that is the threshold query such that , which allocates efficiently. In this section we study settings where, for any profile of the platforms’ auctions, the allocation is efficient at the (advertisers’) bidding equilibrium, i.e. is the allocation threshold in all platforms.

A simple example of the setting mentioned above is when the valuation functions of both advertisers are mirrored versions of each other, i.e., for all queries , for some monotone increasing . In this case, the advertisers are symmetric, and as noted in Section 2, we will focus on symmetric equilibria where where both advertisers use the same bid multiplier for each platform (the bid multipliers are the same across advertisers, but could vary by platform if they use different auction formats). Hence for all platforms, advertiser 1 wins while advertiser 2 wins , making the allocation efficient regardless of the chosen auction format.

We first solve the case where there are two symmetric platforms with equal market share competing for the advertisers. We provide a full characterization of the platform equilibrium. In particular, we show that for any valuation function, either SPA or FPA is a dominant strategy for each platform. We give necessary and sufficient conditions under which each of FPA and SPA are dominant. Then we extend our result to the case of multiple platforms with different market share. We show that the same conditions apply regardless of the number of platforms nor the market share. All proofs in this section are deferred to Appendix C.

5.1 Two Symmetric Platforms with Equal Market Share

We first consider the case where platforms are symmetric (with equal market share). We show in Theorem 5.1 a full characterization of the platform equilibrium of the game.

We show that in this setting the elasticity of both advertisers are equal at , i.e. and simply denote it as . Recall that is the competition level of the game. Here we drop the subscript since platforms are symmetric. We prove the following theorem that characterizes the platform equilibrium of the game.

Theorem 5.1.

For any inefficiency-free instance of 2 advertisers and 2 symmetric platforms, where the following holds. If , SPA is a dominant strategy and thus (SPA, SPA) is the only NE of the game. If , then FPA is a dominant strategy of the game and (FPA, FPA) is the only NE. If , then the game is degenerate: all four profiles of the game have the same outcome.

Theorem 5.1 implies that in this setting, the equilibrium of the game is only determined by the following two factors: the competition level of the game and the elasticity of the advertisers . An instance with a larger competition level indicates enhanced competition between the advertisers, which makes SPA more favorable. As discussed in Section 3, the elasticity indicates how large the bid change is when a platform changes it auction. Theorem 5.1 provides a direct contrast with Theorems 4.1, 4.2: given the competition level of the game, if the elasticity of the advertisers is sufficiently high, then SPA will be the dominant strategy of the game.

We then examine the classic monomial value function () in the mirrored setting, i.e. . First we notice that is convex when . Using Theorem 5.1, we show that SPA is a dominant strategy for any monomial function. We examine other classic value functions and show that SPA is a dominant strategy in those cases as well. See Section C.2 for details.

Corollary 5.2.

Suppose . Then for any , SPA is a dominant strategy in the game and thus (SPA, SPA) is the only NE.

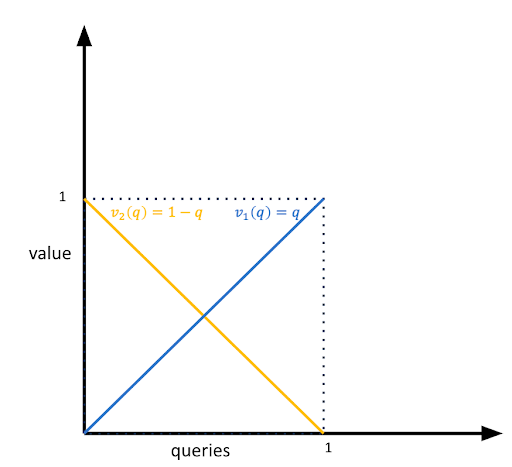

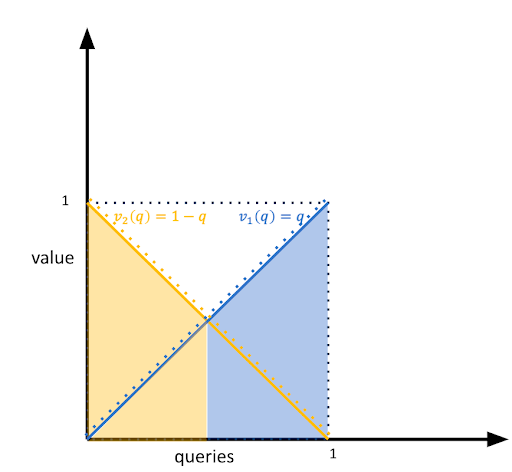

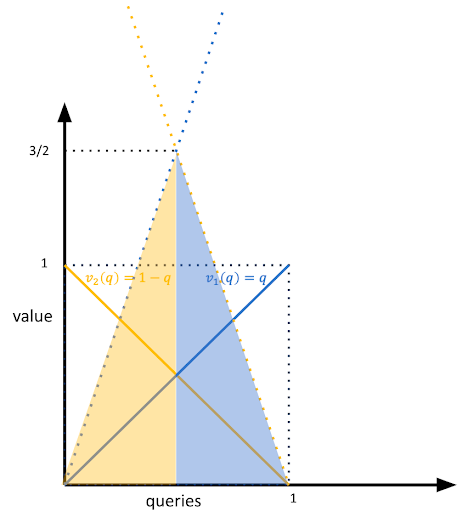

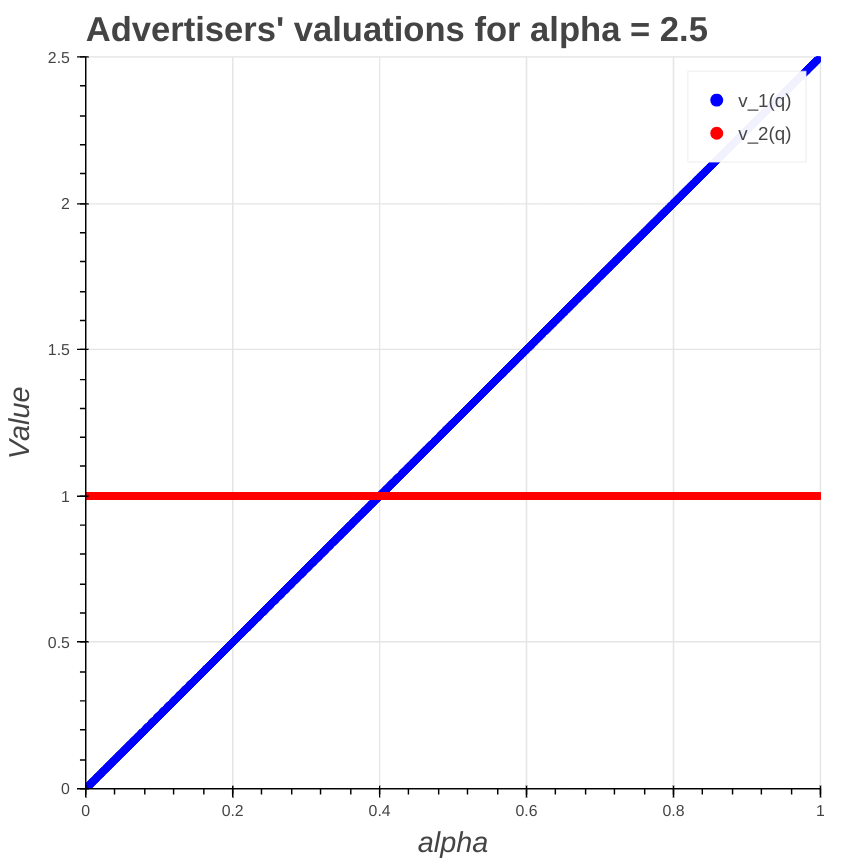

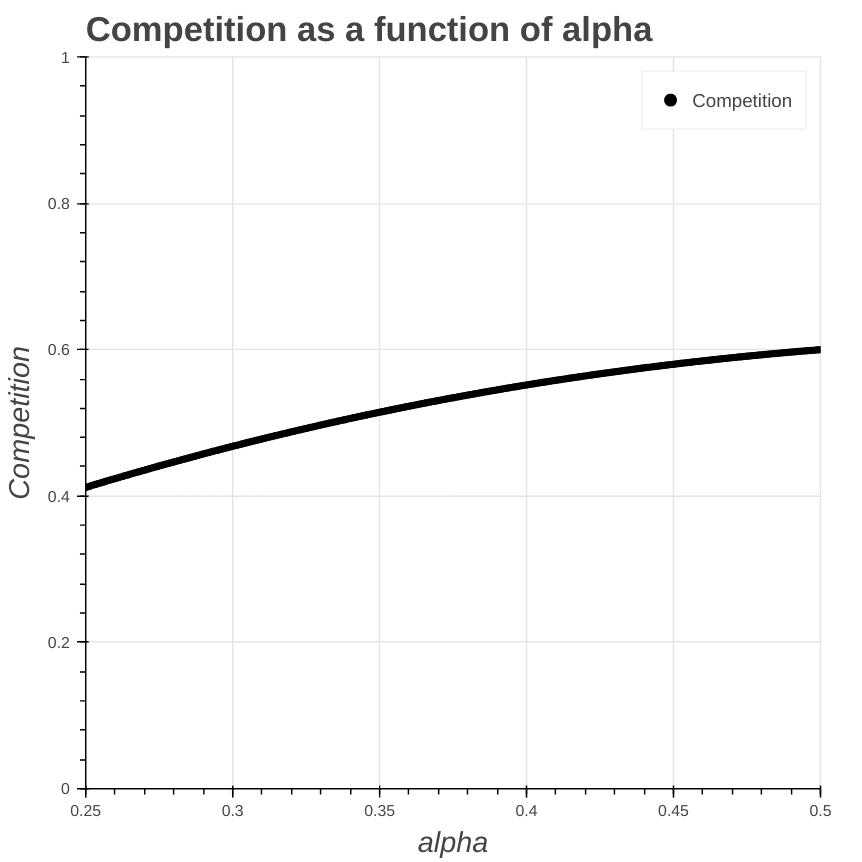

We present an illustrating example in the remainder of this section, to show the advertisers’ equilibrium for each auction outcome and the platform-level game. Suppose (Figure 2(a)). Now . Figures 2(b), 2(c), 2(d) illustrate the outcome of the game under (FPA, FPA), (SPA, SPA) and (FPA, SPA), respectively.

-

1.

(FPA, FPA): both advertisers use a multiplier of 1, platforms collect revenue (Figure 2(b)).

-

2.

(SPA, SPA): advertiser 1 wins queries which induces a total value of . To meet the target, they set the bid multiplier such that the total payment is also (which implies a bid multiplier of ). Similarly for advertiser 2 (Figure 2(c)).

-

3.

(SPA, FPA): we solve the problem of marginal equalization and get that both advertisers use a bid multiplier of in the FPA platform, and for the SPA platform (Figure 2(d)).

The payoff matrix for the platforms, induced by the subgame equilibria of the advertisers, is shown in Table 1. We can see that (SPA, SPA) is the only NE of the game, despite the fact that revenue and allocation are identical for the (FPA, FPA) subgame.

| Platform 2 | |||

|---|---|---|---|

| SPA | FPA | ||

| Platform 1 | SPA | ||

| FPA | |||

5.2 Multiple Platforms with Asymmetric Market Share

In this section we generalize the result in the previous section to the setting of multiple platforms () with identical inventory but asymmetric market share. For each , let be the market share of platform . Here . Advertiser has value for any query in platform , and advertiser has value . Notice that if for some , then a single platform owns all the market and is indifferent between FPA and SPA, while when and the setting is equivalent to the one in Section 5.1.

Interestingly, we show that the same condition in Theorem 5.1 holds in this general case, regardless of the number of the platforms and the market share .

Theorem 5.3.

For any inefficiency-free instance of 2 advertisers and multiple platforms with asymmetric market share the following holds. If , SPA is a dominant strategy and thus (SPA, SPA) is the only NE of the game. If , then FPA is a dominant strategy of the game and (FPA, FPA) is the only NE. If , then the game is degenerate: all profiles of the game have the same outcome. 303030One can easily verify that and are both independent of the market share .

Here we give a proof sketch of Theorem 5.3. Fix any platform and any auction choices of the other platforms. We prove the claim that SPA is the platform’s best response if and only if and this directly implies Theorem 5.3. To prove the claim, we compare the revenue of platform when it chooses SPA () and the revenue when it chooses FPA (). As the setting is inefficiency-free, the advertisers use the same bid multiplier on any given platform. Morever, due to identical inventories across platforms, this bid multiplier is the same for all platforms that use SPA – we denote this bid multipliers by . Here represents the total market share of the platforms choosing SPA. Similarly, the bid multiplier on all FPA platforms is the same, we denote it by . Observe that by merging all SPA platforms and FPA platforms respectively, the advertiser equilibrium in this multi-platform setting is equivalent to the one of the (SPA, FPA) outcome in the two-platform setting. Thus as moves from SPA to FPA, the multiplier that both advertisers use on this platform moves from to .313131If chooses FPA, then the total market share of the SPA platforms become . We then derive the ratio as

and show that regardless of and .

At a high level, the result can be interpreted as follows. When the number of platforms goes to infinity and each platform has negligible market share, the advertisers’ equilibrium will (almost) not be affected by the auction choice of a single platform, or formally tends to . Thus SPA is the platform’s best response if and only if . If the market share of one platform is not negligible, one can think of the platform having the option to change the auction format for part of its market share. Now similar to the above argument, the platform will have the incentive to gradually move its auction from one to another (say from FPA to SPA if ) and will at the end chooses a unified auction format for all its market share.

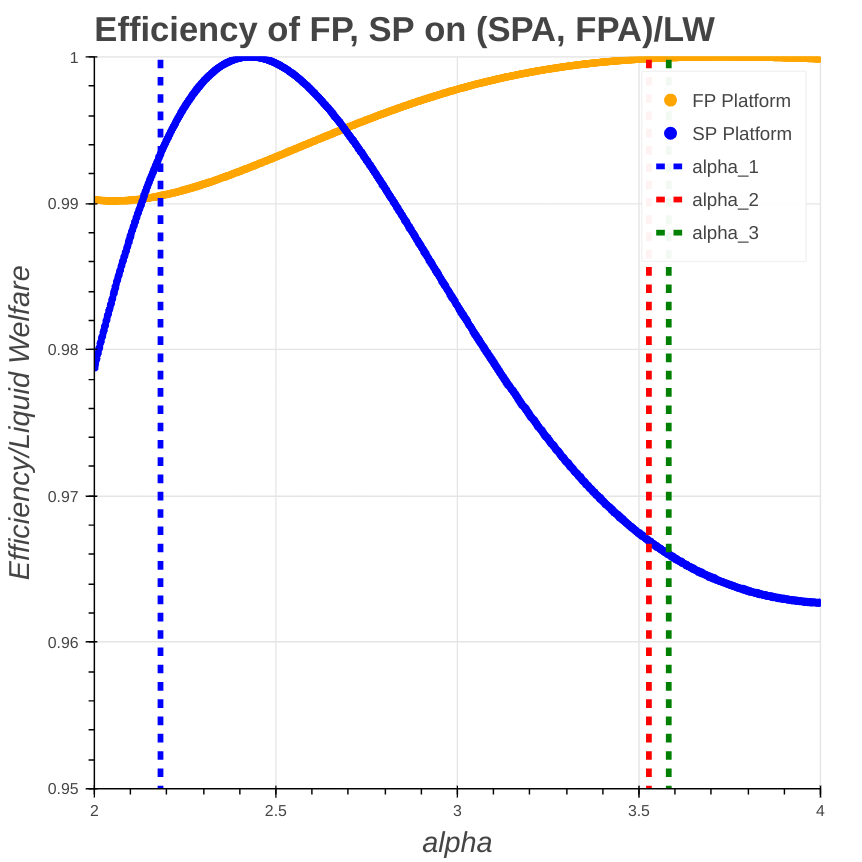

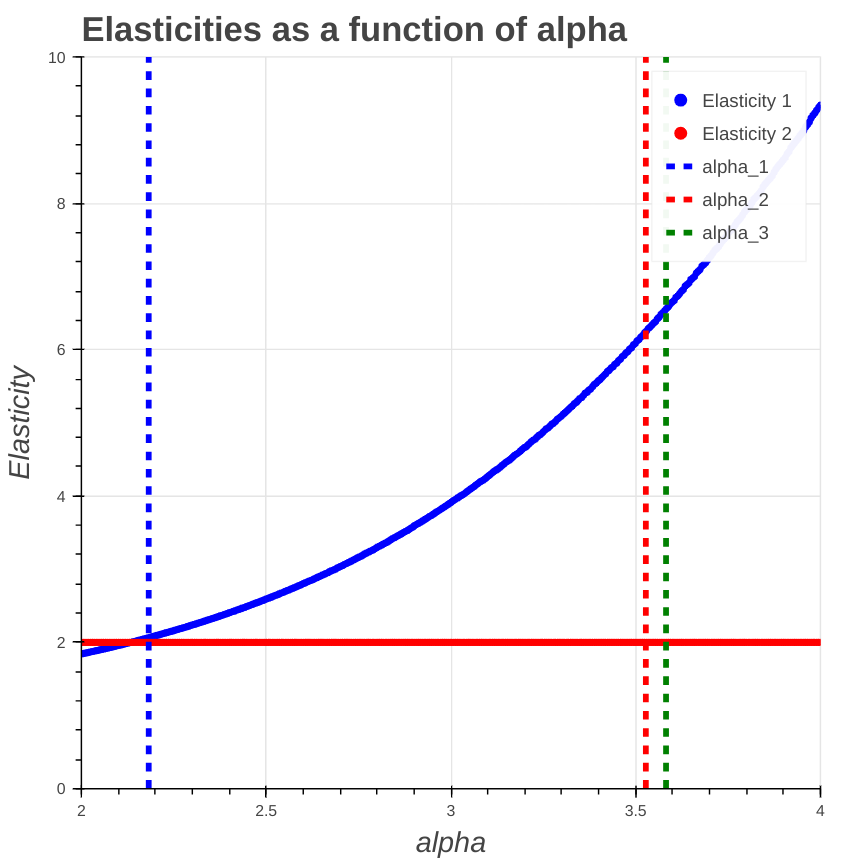

6 Efficiency vs. Bidding Reaction

In Section 5 we solved the inefficiency-free setting where the allocation remains efficient for any auction change. This section tackles the case where FPA allocates more efficiently than SPA, and therefore, there is an aggregate revenue loss when a platform deviates from FPA to SPA. Now a platform faces a trade-off across efficiency loss, competition and bidding reaction in switching from FPA to SPA. While solving the model in its full generality is complex and no simple analytical solution seems to exist, we illustrate the trade-off for two particular classes of valuation functions. In the first case, we observe that when the advertisers’ elasticities are small but advertiser competition is high, even with a small loss in efficiency, the resulting equilibrium will be (SPA, SPA). However, when the elasticities are larger and the advertiser competition is smaller, a small loss in efficiency can cause the equilibrium to be (FPA, FPA). In the second case, we observe that one advertiser’s slowly decreasing elasticity and a slowly increasing advertiser competition , paired with small efficiency losses do not suffice to exhibit multiple equilibria: the equilibrium will always be (SPA, SPA).

6.1 Linear vs Constant-valued Advertisers

We first consider two symmetric platforms and two advertisers, one with valuation (for some ) and (see Figure 3 for an example). We restrict our attention to the case where because for values outside this range, the equilibria of the game result in non-interior solutions.

Claim 6.0.1.

For , in any advertisers’ equilibrium of the (SPA, SPA) auction profile, one advertiser will win all queries in both platforms.

It will follow from our analysis that advertiser 2’s optimal bid multiplier in the second price platform is , which is independent of . This means that, no matter what, advertiser will bid on every query sold in a second price auction. If , advertiser will outright win all queries in this platform since it would be prohibitive for advertiser to bid above . On the other hand, if , then the total value of advertiser 1 for all queries is greater than 2, which is the total value of the bids placed by advertiser 2. Therefore, advertiser 1 would be fine submitting an arbitrarily high bid on the second price platform and winning (virtually) all queries. In fact, for any bid multiplier chosen by advertiser 1, a bid multiplier will be strictly preferable. This implies that for there is no equilibrium. Thus is the sweet-spot for this family of valuations where advertiser 1’s value is high enough to win some queries by shading their bid lightly, but not high enough to be able to outright win all of them.

We now state the main result of this section.

Theorem 6.1.

The platforms’ equilibria of the game in the linear-vs-constant setting depend on the value of as follows. There exist s.t.:

-

•

for there are three Nash equilibria: (SPA, FPA), (FPA, SPA) and a mixture of both,

-

•

for , there is a unique Nash equilibrium: (SPA, SPA),

-

•

for , there are three Nash equilibria: (FPA, FPA), (SPA, SPA) and a mixture of both,

-

•

for , there is a unique Nash equilibrium: (FPA, FPA).

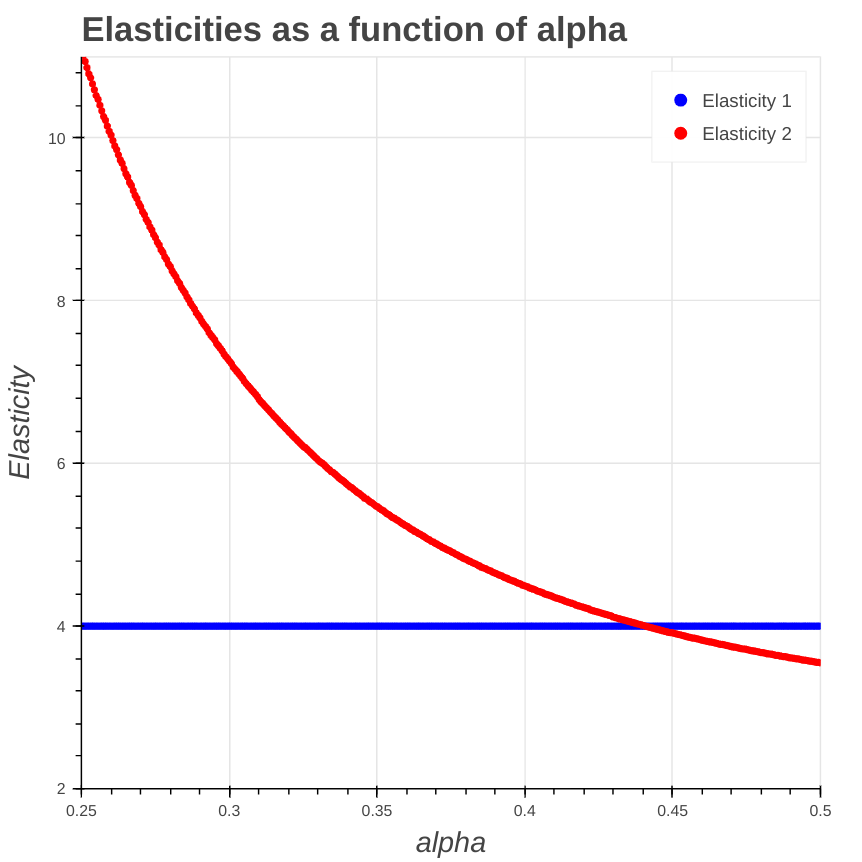

Without getting in to the proof details of Theorem 6.1 (whose proof is deferred to Appendix D), it is worth observing the plots of efficiency, competition and elasticities as a function of the parameter (see Figures 4, 5, 6). As increases, there is a sharp loss of efficiency on the SP platform relative to the FP platform. This, combined with a decrease in advertiser competition , is sufficient to overcome an increase in elasticity and shift the equilibrium from (SPA, SPA) to (FPA, FPA) (for high values of ). This observation contrasts with the results from Section 5 where advertiser competition and elasticity were the only driving factors in determining equilibria. Here we observe that efficiency losses may also play a substantial role in determining equilibria.

[h!]

[h!]

6.2 Exponential Valuations

We next consider the case where both advertisers have exponential valuations , . In this case, we extend the continuum of queries to the entire real line (i.e., ). We also restrict our attention to a particular subset of values for , as values outside of this range would yield non-interior solutions.

Claim 6.1.1.

For this case, when , either a single advertiser wins all queries or there is no equilibrium in the (SPA, SPA) subgame.

The proof of Claim 6.1.1 will be apparent from the analysis of the (SPA, SPA) subgame, so we do not provide a separate proof for it. We now state the main result of this subsection.

Theorem 6.2.

For any , SPA is a dominant strategy. Hence (SPA, SPA) is the only NE of the game.

In contrast to the results from Section 5 and Section 6.1, in this case we observe a small decrease in one of the advertisers’ elasticities and a steeper increase in competition as increases. The loss of efficiency in this case does not suffice to allow for multiple equilibria. The proof of Theorem 6.2 can be found in Appendix E.

References

- Agarwal et al. [2014] Deepak Agarwal, Souvik Ghosh, Kai Wei, and Siyu You. Budget pacing for targeted online advertisements at linkedin. In Proceedings of the 20th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, KDD ’14, page 1613–1619, New York, NY, USA, 2014. Association for Computing Machinery. ISBN 9781450329569. doi: 10.1145/2623330.2623366. URL https://doi.org/10.1145/2623330.2623366.

- Aggarwal et al. [2019] Gagan Aggarwal, Ashwinkumar Badanidiyuru, and Aranyak Mehta. Autobidding with constraints. In Web and Internet Economics: 15th International Conference, WINE 2019, New York, NY, USA, December 10–12, 2019, Proceedings 15, pages 17–30. Springer, 2019.

- Aggarwal et al. [2023] Gagan Aggarwal, Andres Perlroth, and Junyao Zhao. Multi-channel auction design in the autobidding world. In Proceedings of the 24th ACM Conference on Economics and Computation, EC ’23, page 21, New York, NY, USA, 2023. Association for Computing Machinery. ISBN 9798400701047. doi: 10.1145/3580507.3597707. URL https://doi.org/10.1145/3580507.3597707.

- Akbarpour and Li [2020] Mohammad Akbarpour and Shengwu Li. Credible auctions: A trilemma. Econometrica, 88(2):425–467, 2020. doi: https://doi.org/10.3982/ECTA15925. URL https://onlinelibrary.wiley.com/doi/abs/10.3982/ECTA15925.

- Alimohammadi et al. [2023] Yeganeh Alimohammadi, Aranyak Mehta, and Andres Perlroth. Incentive compatibility in the auto-bidding world. In Proceedings of the 24th ACM Conference on Economics and Computation, EC ’23, page 63, New York, NY, USA, 2023. Association for Computing Machinery. ISBN 9798400701047. doi: 10.1145/3580507.3597725. URL https://doi.org/10.1145/3580507.3597725.

- Balseiro and Gur [2019] Santiago R. Balseiro and Yonatan Gur. Learning in repeated auctions with budgets: Regret minimization and equilibrium. Management Science, 65(9):3952–3968, 2019. doi: 10.1287/mnsc.2018.3174. URL https://doi.org/10.1287/mnsc.2018.3174.

- Bateni et al. [2014] MohammadHossein Bateni, Jon Feldman, Vahab Mirrokni, and Sam Chiu-wai Wong. Multiplicative bidding in online advertising. In Proceedings of the Fifteenth ACM Conference on Economics and Computation, EC ’14, page 715–732, New York, NY, USA, 2014. Association for Computing Machinery. ISBN 9781450325653. doi: 10.1145/2600057.2602874. URL https://doi.org/10.1145/2600057.2602874.

- Boyd and Vandenberghe [2004] Stephen P Boyd and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Conitzer et al. [2022a] Vincent Conitzer, Christian Kroer, Debmalya Panigrahi, Okke Schrijvers, Nicolas E. Stier-Moses, Eric Sodomka, and Christopher A. Wilkens. Pacing equilibrium in first price auction markets. Management Science, 68(12):8515–8535, 2022a. doi: 10.1287/mnsc.2022.4310. URL https://doi.org/10.1287/mnsc.2022.4310.

- Conitzer et al. [2022b] Vincent Conitzer, Christian Kroer, Eric Sodomka, and Nicolas E. Stier-Moses. Multiplicative pacing equilibria in auction markets. Oper. Res., 70(2):963–989, mar 2022b. ISSN 0030-364X. doi: 10.1287/opre.2021.2167. URL https://doi.org/10.1287/opre.2021.2167.

- Deng et al. [2021] Yuan Deng, Jieming Mao, Vahab Mirrokni, and Song Zuo. Towards efficient auctions in an auto-bidding world. In Proceedings of the Web Conference 2021, WWW ’21, page 3965–3973, New York, NY, USA, 2021. Association for Computing Machinery. ISBN 9781450383127. doi: 10.1145/3442381.3450052. URL https://doi.org/10.1145/3442381.3450052.

- Deng et al. [2023] Yuan Deng, Negin Golrezaei, Patrick Jaillet, Jason Cheuk Nam Liang, and Vahab Mirrokni. Multi-channel autobidding with budget and roi constraints. In Proceedings of the 40th International Conference on Machine Learning, ICML’23. JMLR.org, 2023.

- Despotakis et al. [2021] Stylianos Despotakis, R. Ravi, and Amin Sayedi. First-price auctions in online display advertising. Journal of Marketing Research, 58(5):888–907, 2021. doi: 10.1177/00222437211030201. URL https://doi.org/10.1177/00222437211030201.

- Google [2021] Google. Moving adsense to a first-price auction, 2021. URL https://blog.google/products/adsense/our-move-to-a-first-price-auction/.

- Paes Leme et al. [2020] Renato Paes Leme, Balasubramanian Sivan, and Yifeng Teng. Why do competitive markets converge to first-price auctions? In Proceedings of The Web Conference 2020, WWW ’20, page 596–605, New York, NY, USA, 2020. Association for Computing Machinery. ISBN 9781450370233. doi: 10.1145/3366423.3380142. URL https://doi.org/10.1145/3366423.3380142.

- Susan et al. [2023] Fransisca Susan, Negin Golrezaei, and Okke Schrijvers. Multi-platform budget management in ad markets with non-ic auctions. arXiv preprint arXiv:2306.07352, 2023.

- Xu et al. [2015] Jian Xu, Kuang-chih Lee, Wentong Li, Hang Qi, and Quan Lu. Smart pacing for effective online ad campaign optimization. In Proceedings of the 21th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, KDD ’15, page 2217–2226, New York, NY, USA, 2015. Association for Computing Machinery. ISBN 9781450336642. doi: 10.1145/2783258.2788615. URL https://doi.org/10.1145/2783258.2788615.

Appendix

Appendix A Missing Proofs from Section 3

Proof of Theorem 3.2.

To show the existence of a solution, observe that bidding for all is a feasible solution and therefore the optimization set is not empty. Moreover, because we have that writing Problem (1) as supremum is well-defined.

Observe that if for all we have that then we can restrict to a compact set and because are continuous a solution exists.

On the other hand, if for some , , then let be a sequence of feasible bid multipliers approaching the supremum of Problem (1). We assert that . Suppose for the sake of a contradiction that this is not the case and .

-

•

If , then because are increasing and bounded, we get that

The right hand side of the inequality goes to infinity as , which implies that does not satisfy the target constraint (Equation (2)) for large . This is a contradiction.

-

•

If , from Condition (3) we must have that in one of the platforms the advertiser is bidding less than to make the target constraint feasible. Hence, for all we have that for some constant . Using Lemma 3.3 we obtain that for some constant . Because is bounded, we can assume that it converges and, therefore, we can take such that for large enough if we replace the bids by and by , the new vector of bids is feasible and increases the total value for the advertiser by . Because is independent of this contradicts the assumption that the original sequence is approaching the supremum.

We therefore conclude that if for some , then any sequence approximating the supremum lies on a bounded set. Because are continuous functions we have that a solution exists. ∎

Proof of Lemma 3.3.

Because is twice differentiable on , we have from L’Hopital’s rule that

Then, the characterization of immediately follows by noticing that if then , and if then .

As for the monotonicity of , if , is increasing. For , since is twice differentiable, it suffices to show that for all . Indeed, observe that

We conclude that since is concave, and therefore, . ∎

Proof of Theorem 3.4.

We split the proof in two steps: Step 1 shows the uniqueness of the solution to (4). Step 2 shows the existence of a solution. Step 3 shows the uniqueness of the solution to Problem (1).

Step 1. First, notice that if is a nonzero solution to (4) we must have that at least for one of the platforms, say , the advertiser uses a bid multiplier . Otherwise, if all bid multipliers are less than , in each of the platforms the average cost would be less than which contradicts that the target constraint (Equation (2)) holds with equality. Hence, from Lemma 3.3 and the fact the marginal cost are the same in each of the platforms, we conclude that for all , .

To show the uniqueness of the solution to (4), consider for the sake of contradiction, two different nonzero solutions and with for some platform . Therefore, for we obtain that

where the first and third equality hold because both bid multipliers are solving Equation (4), the second strict inequality holds because marginal cost is a strictly increasing function. Using that the marginal cost functions are strict we conclude that for all .

To conclude the proof of uniqueness, observe that

where the strict inequality comes from monotonicity of the marginal cost functions and the result of the first paragraph so that . Therefore,

where the first and last equality hold because both bid multipliers solve (4). This is a contradiction. Therefore there is a unique solution to the system.

Step 2. To show the existence of a solution we assert that if for some platform we have that , then condition (3) holds. Indeed consider the non trivial solution to Equation (4). Then and for all . Therefore, from the logic of the Step 1 replacing by the solution and by we conclude that the target-constraint (Equation (2) at is not feasible. Thus, from Theorem 3.2 we conclude that a solution to Problem (1) exists.

Step 3. Consider a solution of Problem (1), which exists due to Theorem 3.2. Using the Karush-Kuhn-Tucker Theorem (see Boyd and Vandenberghe [2004] for a textbook treatment) consider the Lagrangian of Problem (1) as

where is the vector of bid multipliers and is the Lagrangian dual variable. Then at we have that for the dual solution ,

We assert that . Indeed if , then and because is an increasing function this would imply that for all , . From Step 2 we know that this is not feasible. Thus, .

Because , the KKT conditions can be rewritten as

Notice that since there is a non-zero solution to Problem (1) (take the feasible solution of (4)), we have that . This implies that for all .

To conclude we separate the analysis into two scenarios. In the first scenario, if an optimal bidding solution is such that , then we have the solution solves (4). Hence, from Step 1, the solution has to be . For the second scenario, if the optimal solution is such that for some platform . Using that , we derive that

where the first equality holds because solves the system (4), the strict inequality comes because is increasing, the last equality comes from the KKT conditions. From the last chain of inequalities, we can replicate the same argument as in Step 1 by interchanging by and by and we get a contradiction. Therefore, there is a unique solution to Problem (1). ∎

Proof of Theorem 3.5.

First, notice that using a bid multiplier for all is a feasible solution. This implies that cannot be the zero for all .

Proof of Corollary 3.6.

From Lemma 3.3 we have that the marginal costs functions are increasing on . Because there is a platform with , then for any sequence of bid multipliers with , we have that

the right hand side goes to infinity as . Therefore, condition (3) holds and from Theorem 3.2 we have that a solution to Problem (1), exists. Therefore, . All the conditions for Theorem 3.5 hold which allow us to conclude. ∎

Proof of Theorem 3.7.

From the symmetry refinement (R3) (see 2.2), we have that both bidders have to bid the same in each platform. Therefore, the problem is equivalent to solving the FPA game in a single platform. Theorem 6.5 in Deng et al. [2021] shows that the unique equilibrium with undominated strategies is to bid using a bid multiplier equal to the advertiser’s target CPA. In our case, this means . The authors further show that the equilibrium is efficient so that and the platform gets revenue equal to the optimal liquid welfare. In our two platform case this means that the equilibrium query-threshold is and each platform obtains . ∎

Proof of Theorem 3.8.

From the symmetry refinement (R3) (see 2.2), we have that both bidders have to bid the same in each platforms. Therefore, the problem is equivalent to solving the SPA game in a single platform. The proof of existence and uniqueness for a single platform can be found in Theorem 5.7 of Alimohammadi et al. [2023], where given those conditions the equilibrium of SPA is unique which also implies that it is incentive compatible for autobidders. ∎

Proof of Lemma 3.9.

Fix a bid multiplier . First, observe that for any bid multiplier that advertiser 2 use the query-threshold is for . To show that is increasing observe that

which is positive since is non-negative and increasing and therefore is also increasing. Thus, is increasing.

Similarly, for concavity notice that

The first term is negative since is a decreasing function, and the second term is also negative since is the inverse of a positive convex function.

The proof for is analogous and is therefore omitted. ∎

Proof of Lemma 3.11.

The result is a direct application of Lemma 3.3. Consider the problem of advertiser given bids . For the SPA platform the marginal cost is always the bid multiplier so .

For the FPA platform we have that . For advertiser 2 we have that where so that is the threshold query . Then, and

The first equality comes by taking the derivative over the integral. The second equality comes by using the derivative of the inverse function . The third equality is from the definition of . The fourth equality is a simple algebraic manipulation. The last equality comes from the definition of as the threshold query when advertisers bid using and . Hence, we conclude that .

The proof for advertiser 1 is identical and is therefore omitted. ∎

Proof of Theorem 3.12.

From Lemma 3.11 we have that the system of equations (8)-(10) corresponds to the system of equations (4) given bids for advertiser . Since solves the system with a non-zero solution and from Lemma 3.9 the endogenous bid landscape satisfies Assumption 3.1. Therefore, from Theorem 3.4 we have that are the optimal bids for advertiser given bids . The same reasoning applies to advertiser which implies that is an equilibrium for the subgame.

For uniqueness, consider an equilibrium of the subgame. We assert that bidders cannot be bidding zero on a platform. If bidding only on the FPA platform, then bidding a bid multiplier of on the SPA platform dominates bidding . Under our equilibrium refinement, this cannot happen in equilibrium. If bidding only on the SPA platform, bidding a bid multiplier of on the FPA platform is feasible and dominates bidding . This again contradicts our equilibrium refinement. Thus, bid multipliers are positive. Second, because we have that for the bid landscape of advertiser is such that . Analogously, for the landscape of advertiser we have that . From Corollary 3.6 we conclude that in any equilibrium both advertisers need to simultaneously solve their system of marginal cost equations, which corresponds to the system of equations (8)-(10). The uniqueness of solution to this system of equations implies that the equilibrium is unique. ∎

Appendix B Missing Proofs from Section 4

B.1 Uniform Bid Multipliers Across Platforms

Claim B.0.1.

Any strategy where advertiser uses a multiplier is weakly dominated by a strategy where they use a multiplier of .

Proof.

If an advertiser bids using , the total payment is at most which is strictly less than their value . By using the advertiser could purchase weakly more queries than with without violating their ROI constraint. ∎

Theorem B.1.

If advertisers are using undominated strategies, then the unique equilibrium of the platform-advertiser game under uniform bidding is for the platforms to announce FPA to sell their queries and for advertisers to submit multipliers . Furthermore, the total revenue across all platforms satisfy that .

Proof.

Let , which is the fraction of liquid welfare that platform contributes to the liquid welfare . Recall that .

We claim that in any equilibrium, the revenue platform gets, , satisfies that . Indeed because advertisers are using undominated bidding stategies, if platform uses an FPA then the revenue it would get for each query , which is , is no less than since for all . Thus, . Combining this with Remark 2.4 we get that .

To conclude observe that if valuations are in generalized position (i.e., valuations functions are not fully correlated within advertisers), then there is no such that

Hence, FPA is the unique equilibrium of the game. ∎

B.2 Single-Bidder, Multi-Platform Problem

In this section we study the case of a single bidder and multiple platforms each with possibly different markets made up of static bidders, with non-uniform bids allowed. By static bidders we mean that they are single-query bidders who will bid truthfully and will not respond to changes in the auction format. The main takeaway from this section is that the unique Nash equilibrium of the game is for the platforms to announce FPA to sell their queries, and for the single strategic bidder to submit a multiplier of .

Theorem B.2.

In the single-bidder, non-uniform bidding multi-platform game, the unique Nash equilibrium is for the platforms to announce FPA to sell their queries and for the bidder to use a multiplier of 1 on each channel.

We first prove the following Claim.

Claim B.2.1.

For any platform , announcing FPA to sell their queries weakly dominates SPA.

Proof.

Let be the impressions the bidder gets if they bid , and be its inverse, the price the bidder must bid in order to win all impressions up to (assume is weakly monotone increasing).

Suppose a platform has announced SPA to sell their queries. Let be the multiplier the single strategic bidder uses in order to bid on this platform. The strategic bidder wins the first queries and pays a total of . The static bidders will win the queries and pay for each.

Suppose the platform announced FPA to sell their queries, and let be the multiplier the single strategic bidder uses in order to bid on this platform.

By switching from SPA to FPA, the price weakly increases on all queries. For queries between and queries between , the winner of the query is the same between both auction formats but the price increases. For the remaining queries, the winner of the query changes. If , the price weakly increases. If the price remains the same. In all cases, the revenue of the platform is weakly greater announcing FPA to sell their queries compared to SPA. ∎

We can now easily prove the main result of this section.

Proof of Theorem 4.2.

Since FPA weakly dominates SPA for all platforms, the platforms will all announce FPA to sell their queries, regardless of what other platforms are doing. This in turn makes the bidder’s problem simple. Submitting a multiplier for platform is weakly dominated by submitting . Submitting a multiplier will result in overpaying for all the queries the strategic bidder wins. Submitting a multiplier of is weakly dominated by submitting a multiplier of since this wins weakly more queries while satisfying the tCPA constraint. ∎

Appendix C Missing Proofs from Section 5

We begin with the setting of two platforms with asymmetric market share. We denote the market share of platform (so the market share of platform is ).

C.1 Two Platforms with Asymmetric Market Share

We will compute the advertisers’ equilibrium and the platforms’ revenue for each profile of the 2-player game between platforms. For ease of notation let , , . Recall that is the unique (as is strictly increasing while is strictly decreasing) number such that . We notice that and .

The following claim directly follows from the fact that for any auction format outcome, the allocation at advertisers’ equilibrium is efficient.

Claim C.0.1.

For any auction format outcome, the advertisers’ equilibrium satisfies that for all platform .

Proof.

For any auction format outcome, satisfies that for each platform since is the threshold where the allocation switches from advertiser 1 to advertiser 2. By definition also satisfies . Thus for all . ∎

Now we compute the advertisers’ equilibrium for each auction outcome.

Case 1: (SPA, FPA)

By C.0.1, denote the multipliers for both advertisers on the FPA, SPA platforms respectively. Then by Theorem 3.12 the following equations are satisfied:

| (11) | |||

| (12) | |||

| (13) | |||

| (14) |

Claim C.0.2.

. Moreover, , , i.e. and .

Proof.

and directly follows from Equation 13 and Equation 14, since . For the remaining equality , we notice that

Subtracting the second equality from the first equality implies since . ∎

By C.0.2, we denote , and .

Lemma C.1.

There exists a unique advertisers’ equilibrium with multipliers in the (SPA, FPA) profile such that

-

•

-

•

Proof.

Both conditions in the statement directly follow from Equations (1) - (4) and C.0.2. It remains to verify that there exists that satisfy both conditions. In fact, we have

and . The lemma then follows from Theorem 3.12. ∎

The revenue of platform 1 (SPA) is . The revenue of platform 2 (FPA) is . By Lemma C.1 the total revenue of both platforms is .

Case 2: (FPA, SPA)

This case is analogous to the previous case by swapping the market share parameter. We have the following lemma analogous to Lemma C.1. The proof is omitted.

Lemma C.2.

There exists a unique advertisers’ equilibrium with multipliers in the (FPA, SPA) profile such that

-

•

-

•

Case 2: (FPA, FPA)

We know that advertisers will set multipliers . In both platforms, advertiser 1 wins the query when . Now the revenue of platform 1 is . Similarly the revenue of platform 2 is .

Case 2: (SPA, SPA)

Now both advertisers will set the multipliers such that the payment meets their target, i.e. . The revenue is for platform 1. Similarly the revenue of platform 2 is .

Finally, we can write the payoffs for each platform under all possible action profiles. In particular, note that the welfare of every action profile is . So long as the payoff matrix is not degenerate, the Nash equilibria of this game will be exactly one of (SPA, SPA) or (FPA, FPA). Surprisingly, which of these two profiles is the Nash equilibrium will depend only on the shape of the valuation and not on the market share .

| Ch 2 | |||

|---|---|---|---|

| SPA | FPA | ||

| Ch 1 | SPA | ||

| FPA | |||

Theorem C.3.

Let be the parameter that only depends on and (independent of the market share ). If , then (SPA, SPA) is the only NE of the game. If , then (FPA, FPA) is the only NE. If , then all four profiles of the game have the same outcome.

Before going to the proof, we notice that

So Theorem C.3 is a restatement of Theorem 5.1 and Theorem 5.3 when there are 2 platforms.

Proof of Theorem C.3.

Let , the game can be rewritten as the following table:

| Ch 2 | |||

|---|---|---|---|

| SPA | FPA | ||

| Ch 1 | SPA | ||

| FPA | |||

Observe that in order for (SPA, SPA) to be a Nash equilibrium we need that , (or ). Analogously, in order for (FPA, FPA) to be a Nash equilibrium we need that and (or ). We will now show that .

Claim C.3.1.

.

Proof.

| (15) |

By definition,

Moreover,

Thus if we have that and if we have that . ∎

Therefore, if , the only equilibrium is (SPA, SPA). If , the only equilibrium is (FPA, FPA). If , then the game is degenerate and all action profiles have the same payoffs. ∎

C.2 Equilibrium for Standard Valuations in the Mirrored Setting

We apply the result of Theorem C.3 to show that (SPA, SPA) is the only Nash equilibrium for many standard valuations. Throughout this section we focus on the mirrored setting, i.e. for all for some . In this setting we have and

C.2.1 Polynomial valuations

Corollary C.4.

For polynomial valuations with positive coefficients and no constant term such that is convex, (SPA, SPA) is always the only Nash equilibrium.

Proof.

Let .

First note that if , then all must be , in which case is also and the game is degenerate, hence any action profile would be a Nash equilibrium. Assume for the rest of this proof. We will prove that directly by showing that . By Cauchy-Schwarz we know that

Multiplying both sides by 2 and observing that (for all ) gives the inequality. Since , then . Finally, note that we need convexity of for our results to hold. ∎

We can specialize the results to the case of monomial valuations for some . Corollary C.5 directly follows from Corollary C.4 with the fact that is convex when .

Corollary C.5.

For monomial valuations, (SPA, SPA) is always the only Nash equilibrium.

C.2.2 Fixed crossing point

Given Theorem C.3, we can think of how the equilibrium changes for families of valuations with, say, fixed crossing points. For this section, assume . Moreover, we assume .

Corollary C.6.

For linear valuations with and , (SPA, SPA) is the unique Nash equilibrium.

Proof.

We will again show directly that . We consider two sub-cases. Let be the valuation, and since we know that . Also, note that .

Since , . Therefore we can compute directly.

Thus, . It is easy to verify that for , with equality only when . ∎

C.2.3 Fixed slope

Similar to the previous case, we can consider what happens with linear functions such that for some fixed . Without loss of generality, assume . Let . We further assume that , thus .

Corollary C.7.

For linear functions with , the unique equilibrium will be (SPA, SPA).

Proof.

Then , . Therefore, . It is easy to verify that for , .

∎

C.2.4 Exponential valuations

Corollary C.8.