Sequential monitoring for explosive volatility regimes

Abstract.

In this paper, we develop two families of sequential monitoring procedure to (timely) detect changes in a GARCH(1,1) model. Whilst our methodologies can be applied for the general analysis of changepoints in GARCH(1,1) sequences, they are in particular designed to detect changes from stationarity to explosivity or vice versa, thus allowing to check for “volatility bubbles”. Our statistics can be applied irrespective of whether the historical sample is stationary or not, and indeed without prior knowledge of the regime of the observations before and after the break. In particular, we construct our detectors as the CUSUM process of the quasi-Fisher scores of the log likelihood function. In order to ensure timely detection, we then construct our boundary function (exceeding which would indicate a break) by including a weighting sequence which is designed to shorten the detection delay in the presence of a changepoint. We consider two types of weights: a lighter set of weights, which ensures timely detection in the presence of changes occurring “early, but not too early” after the end of the historical sample; and a heavier set of weights, called “Rényi weights” which is designed to ensure timely detection in the presence of changepoints occurring very early in the monitoring horizon. In both cases, we derive the limiting distribution of the detection delays, indicating the expected delay for each set of weights. Our theoretical results are validated via a comprehensive set of simulations, and an empirical application to daily returns of individual stocks.

Key words and phrases:

Sequential monitoring, GARCH(1,1) processes, explosive volatility, detection delay.1991 Mathematics Subject Classification:

Primary 62M10, 91B84; secondary 60G10, 62F121. Introduction

In recent years, developing tools for the (ex-ante or ex-post) detection of the onset or the collapse of a bubble in financial markets has been one of the most active research areas in financial econometrics; we refer the reader, in particular, to the seminal articles on ex-post detection by Phillips et al. (2011), and Phillips et al. (2015a), and also to Skrobotov (2023) for a review. As far as ex-ante detection - that is, finding the onset or collapse of a bubble in real time, as new data come in - is concerned, this important issue has also been studied in numerous recent contributions; although a comprehensive literature review goes beyond the scope of this paper, we refer to the articles by Homm and Breitung (2012), Phillips et al. (2015b), and Whitehouse et al. (2023), inter alia; in particular, the paper by Whitehouse et al. (2023) also contains a comprehensive literature review of in-sample and online bubble detection methods. A common trait to the vast majority of the existing literature is its reliance on a linear specification, usually an AutoRegressive (AR) model, to capture regime changes in the dynamics of log prices. Whilst such a modelling choice can be justified from the theoretical point of view (see e.g. Phillips and Yu, 2011), and whilst its analytical tractability offers obvious advantages from a mathematical standpoint (see e.g. Phillips and Magdalinos, 2007, and Aue and Horváth, 2007), a major issue is that using an AR model is fraught with difficulties when monitoring for changes from an explosive towards a stationary regime. Several promising solutions have been proposed such as the reverse regression approach by Phillips and Shi (2018). Horváth and Trapani (2023) propose a different model, based on a Random Coefficient Autoregressive (RCA) specification, where inference is always standard normal irrespective of stationarity or the lack thereof (Aue and Horváth, 2011), and develop a family of sequential monitoring procedures based on the weighted CUSUM process, to check whether the deterministic part of the autoregressive root changes over time. Such a testing set-up also encompasses both the case of a switch from a stationary to an explosive regime (thus indicating the start of a bubble phenomenon), and a change from an explosive to a stationary regime (thus signalling the collapse of a bubble).

The theory developed in Horváth and Trapani (2023) paves the way to a more general research question, namely developing sequential monitoring techniques which are robust to both the initial regime (i.e., which can be employed irrespective of whether the observations in the training/historical sample are stationary or explosive), and to the type of change which occurs after a changepoint (i.e., which can detect changes from stationarity to another stationary regime, or to a explosive regime; or from an explosive regime to another explosive regime or a stationary one). From a technical viewpoint, this question is nontrivial for at least three reasons. First, proposing a changepoint detection methodology whose asymptotics is the same irrespective of stationarity or explosivity is not easy per se, because the partial sum processes which constitute the building blocks of e.g. CUSUM-based statistics require completely different approximations depending on whether the observations are stationary or not. Second, in order to ensure timely changepoint detection, weighted versions of the CUSUM process need to be considered, with different sets of weights ensuring optimal detection delays for different changepoint locations within the monitoring horizon. Third, on account of the previous point, it is important to offer, to the applied user, a battery of results on the limiting distribution of the detection delays, so as to gauge the expected detection delay depending on the location of the changepoint and the weighing scheme employed.

Motivated by the questions above, in this paper we investigate, with an emphasis on completeness, the issue of sequential detection for regime changes in a GARCH(1,1) sequence

| (1.1) |

In particular, we develop two families of detectors based on the weighted CUSUM process of the quasi-Fisher scores associated with (1.1): one with “mild” weights, designed to detect changes that may occur “not too early” after the start of the monitoring period; and one with heavy weights, designed instead to detect changes occurring “very early” after the start of the monitoring period. The latter is based on applying to the CUSUM process a set of (heavy) weights, resulting in a family of test statistics known as Rényi statistics (see Horváth et al., 2021 and Horváth et al., 2020, for in-sample tests, and Ghezzi et al., 2024, for sequential monitoring). Our methodologies can, in principle, be applied to detect any type of change in the vector . However, seeing as: (1) our main interest is in detecting changes between regimes (e.g., from stationarity to nonstationarity, or vice versa); the stationarity or lack thereof of (1.1) is determined solely by and ; and (3) in the presence of nonstationarity, is not identified (Jensen and Rahbek, 2004), we focus on monitoring for changes only in the sub-vector . Detecting shifts in the behaviour of the (conditional) volatility process is important in general; as Hillebrand (2005) notes, when neglecting a break inference is biased in finite samples, and the sum of the estimated autoregressive parameters and converges to one. Furthermore, changes (and, occasionally, explosions) in the volatility of time series are often observed in practice (see e.g. Bloom, 2007, and Jurado et al., 2015). Hence, finding the start or the end of an explosive regime in is of practical relevance because, as Richter et al. (2023) put it, one “often sees sudden, integrated, or mildly explosive behaviour in the second moment of the process which bounces back after a while” (p. 468). Changes between stationarity and explosivity in (1.1) can be interpreted as volatility bubbles, i.e. events in which the second moment of the data (rather than the data, e.g. prices, themselves) experiences periods of exhuberance. The link between a volatility phenomenon and a “proper” bubble has not been fully explored yet (see Jurado et al., 2015), and, empirically, explosive regimes in volatility can be ascribed to various sources in addition to bubbles (see Sornette et al., 2018, and Richter et al., 2023). Nevertheless, as Jarrow and Kwok (2023) put it, “price bubbles result from excess speculative trading decoupled from the asset’s fundamentals (dividends and liquidation value), which increases the asset’s price volatility to extreme levels” (p. 478). Hence, an analysis of the regimes of the volatility of financial variables is bound to contribute to a better understanding of bubble phenomena.

Based on the discussion above, in this paper we propose a battery of tests

for the sequential monitoring of the volatility of financial variables,

which complements the existing tests for bubbles based on the conditional

mean. Specifically, we make at least three contributions. First, we study

online detection of changes between stationarity and explosivity and vice

versa, which - to the best of our knowledge - is a novel result in the

literature, and which complements the ex-post detection statistics studied

in Richter

et al. (2023). Second, we develop the full-blown theory for Rényi statistics in the context of sequential monitoring of a GARCH(1,1)

model. Third, we derive the limiting distribution of detection delays for

all our monitoring schemes, including those based on Rényi statistics;

this is an entirely novel result, which complements the results in Horváth

et al. (2020).

The remainder of the paper is organised as follows. We discuss our workhorse model and the main assumptions, as well as the test statistics, in Section 2. The theory is reported in Section 3: in particular, the asymptotics under the null is in Section 3.1, and the full-blown asymptotics of the detection delay in the presence of a changepoint is in Section 3.2. We validate our theory through a comprehensive set of simulations (Section 4), and an empirical application to daily returns of individual stocks (Section 5). Section 6 concludes.

NOTATION. We define the Euclidean norm of a vector as . We denote the integer part of a number as . We use: “a.s” for “almost sure(ly)”; “” for the ordinary limit; “” for convergence in distribution; “” for convergence in probability; “” for equality in distribution. Positive, finite constants are denoted as , , … and their value may change from line to line. Other, relevant notation is introduced later on in the paper.

2. Model, assumptions, and hypothesis testing

2.1. Model, assumptions and hypotheses of interest

The time dependent GARCH (1,1) sequence is defined by the recursion

| (2.1) |

where , are initial values, and , and are positive parameters.

Whilst the hypothesis testing framework is spelt out below, our monitoring schemes are all based on the maintained assumption that we have observations which form a stable period (this is also known as the non-contamination assumption in Chu et al., 1996), viz.

| (2.2) |

We denote the value of the common parameter in (2.2) as . Prior to spelling out the main assumptions, we review the conditions for the stationarity of . As Nelson (1991) shows (see also Bougerol and Picard, 1992, and Francq and Zakoïan, 2012)

-

(1)

if , then converges exponentially fast to a unique, strictly stationary and ergodic solution for all initial values and ;

-

(2)

if , then is nonstationary with exponentially fast (Nelson, 1991);

-

(3)

if , then is nonstationary, but this is a much more delicate case; indeed, Klüppelberg et al. (2004) show that , but a.s. divergence to infinity cannot be established.

We will develop several monitoring schemes for the null hypothesis that the parameter undergoes no changes after the historical training period , i.e.

| (2.3) |

Under the alternative, we assume that there is a change at time ; whilst this would correspond to having for all , it is well know that the ’s cannot be identified in explosive, nonstationary regimes (Francq and Zakoïan, 2012). Hence, we will test for

| (2.4) | ||||

i.e., for the possible presence of changes in and only. Note that these are anyway the parameters of interest, since the stationarity (or lack thereof) of is not affected by .

We require the following assumptions on , and on the innovations .

Assumption 2.1.

It holds that: , and .

Assumption 2.2.

It holds that: (i) are independent and identically distributed random variables; (ii) is nondegenerate; (iii) , , , and with some .

2.2. Estimation and monitoring schemes

As stated in the Introduction, the main purpose of our analysis is to offer a detection scheme which finds changes in the parameters of a GARCH(1,1) model as soon as possible after the training period. In this section, we propose several detectors, all based on the CUSUM process of the quasi-Fisher scores.

As is typical, we estimate the parameter , using the training sample, by Quasi Maximum Likelihood (QML). The likelihood function is given by

where , and , and the random functions given by the recursion

the recursion starts from the initial values and . The QML estimator computed from the historical sample is denoted as , with

where the (compact) space is defined as

.

Starting with the initial values and , we define the random functions based on the observations after the historical sample by the recursion

with the log likelihood function given by

Hence, we define the CUSUM process of the quasi-Fisher scores as

| (2.5) |

Heuristically, under the null of no change, the scores have zero mean; hence, the partial sum process calculated at should also fluctuate around zero with increasing variance. Conversely, in the presence of a break (at, say, ), is a biased estimator for the “new” parameter ; thus, , calculated at , should have a drift term. In the light of these heuristic considerations, we propose the following detector

| (2.6) |

where

Based on (2.6), a break is flagged as soon as the detector exceeds a threshold. We call such a threshold the boundary function. Similarly to Chu et al. (1996), Horváth et al. (2004), Horváth et al. (2020), Homm and Breitung (2012), we use the boundary function, designed for a closed-ended procedure - i.e., for a procedure which terminates at a certain time, say , if there is no change

| (2.7) |

On account of (2.6) and (2.7), a changepoint is found at a stopping time defined as

| (2.8) |

The (user-chosen) parameter in (2.7) determines the timeliness of changepoint detection of our sequential monitoring procedure. Aue and Horváth (2004) and Aue et al. (2008) show that, as approaches , changepoints are detected with a smaller and smaller delay depending on their location; on the other hand, different values of work better for different changepoint locations, as also pointed out in a recent contribution by Kirch and Stoehr (2022b). In particular, values of are able to offer short detection delays for breaks that do not occur “too early” after .

In order to detect earlier changes, Ghezzi et al. (2024) (building on previous contributions by Horváth et al., 2021, and Horváth et al., 2020, developed for in-sample changepoint detection) suggest using Rényi type statistics, with stopping rule

| (2.9) |

where is a trimming sequence specified in Assumption 2.4, and

| (2.10) |

We note that (2.8) and (2.9) exclude the case . Indeed, Aue and Horváth (2004) show that, as far as stopping times under the alternative are concerned, using would produce the shortest detection time. The case requires to be studied separately. Following Horváth et al. (2007), we modify the boundary function. Let

We use the boundary functions

| (2.11) |

and

| (2.12) |

The corresponding stopping times - denoted as and - are defined exactly in the same way as and in (2.8) and (2.9), respectively, using

now the boundaries and .

As mentioned above, we consider a closed-ended scheme, which terminates periods after . The following assumptions characterise the length of the monitoring horizon and of the trimming sequence defined in (2.9); in particular, Assumption 2.3 is designed in order to consider only early changepoint detection.

Assumption 2.3.

It holds that , and .

Assumption 2.4.

It holds that, in equation (2.9), and .

3. Asymptotics

In this section, we investigate the asymptotic behaviour of our monitoring schemes under the null and under the alternative hypotheses.

3.1. Asymptotics under the null

Let be a two dimensional standard Wiener process - i.e., and are two independent Gaussian processes with , and covariance kernel .

Theorem 3.1.

Theorem 3.1 offers a rule to calculate the asymptotic critical values; for a given nominal level , the critical value is defined as

for all , and

for . Using the scale transformation of the Wiener process, it immediately follows that ; hence, for all

Theorem 3.1 rules out the boundary case ; this is because we would need an exact (and large

enough) rate of divergence for as , but this result is not available in the case (see Francq and

Zakoïan, 2012, p. 823; and also Theorem 4 in Horváth and

Trapani, 2019, where a similar problem is

encountered, and the discussion thereafter).

Theorem 3.1 does not consider the case , which corresponds to the stopping times and based on the boundaries defined in (2.11) and (2.12) respectively. The case is studied separately in the following theorem.

Theorem 3.2.

We assume that of (2.3) and Assumptions 2.1–2.3 hold, and that . Then, for all ,

it holds that

(i) .

(ii) If in addition Assumption 2.4 also holds, then we have

Theorem 3.2 stipulates that the asymptotic critical values, for a given nominal level , can be calculated as

| (3.1) |

using or according as (2.11) or (2.12) is employed. Although the theorem offers an explicit formula to compute asymptotic critical values, these are bound to be inaccurate due to the slow convergence to the Extreme Value distribution. In particular, simulations show that, in finite samples, asymptotic critical values overstate the true values thus leading to low power.

3.2. Asymptotics under the alternative

We now study the behaviour of our monitoring schemes under the alternative, focussing, in particular, on the limiting distribution of the detection delay. We report the limiting distribution of the detection delay when using in Section 3.2.1; in Section 3.2.2, we report the limiting distribution of the detection delay when using .

In both cases, under the alternative , of (2.4), the parameter changes to satisfying

Assumption 3.1.

, , and .

3.2.1. Detection delays with

We begin by investigating the asymptotic behaviour of the stopping time defined in (2.8). Whilst the result in Theorem 3.3

below is valid for all cases, we need to introduce some preliminary

notation, separately, for the two cases: (1) when the sequence is stationary after the change and (2) when the sequence is explosive

after the change.

Preliminary notation

We begin by introducing some preliminary notation for the former case, i.e.

| (3.2) |

Under (3.2), after the change the observations are exponentially close to , a stationary GARCH (1,1) sequence given by

| (3.3) |

We also define the log likelihood function

where . Let

and define the size of the change as

| (3.4) |

We define the covariance matrix

| (3.5) |

and

| (3.6) |

where . Finally (as far as preliminary notation is concerned), we define as the unique solution of the equation

| (3.7) |

and as the solution of

| (3.8) |

It is easy to see that , and that , if . We are now ready to introduce the main

notation to spell out the properties of the stopping time when

the observations change into a stationary sequence.

We now introduce the preliminary notation for the case when the observations turn into an explosive sequence after the time of change, i.e.

| (3.9) |

Jensen and Rahbek (2004) proved that

exists. Similarly to in equation (3.4), we define the size of the change under as . Similarly to (3.6), we define

where . Finally, similarly to and we define and as the solutions of the equations

After the change in the parameters, the gradient of the likelihood function is approximated with the sequences

and

Analogously to in (3.5), we finally introduce

| (3.10) |

Main notation

After spelling out the preliminary notation for the two cases of the observations begin stationary and nonstationary, we now introduce the main notation. As we will see in Theorem 3.3 below, in several cases the delay converges to a standard normal random variable after being centered and rescaled; the centering and rescaling for depend on whether or ( or , equivalently). In particular

-

(1)

when (, respectively), will be centered around

and rescaled by

-

(2)

when (, respectively), will be centered around

and rescaled by

In order to present the limiting distribution for both cases, we define: the Gaussian process , with and ; the random variables

| (3.11) |

| (3.12) |

and, finally, the asymptotic variances

| (3.13) |

| (3.14) |

Let denote a standard normal random variable, and let

Theorem 3.3.

In order to understand the practical implications of Theorem 3.3, note that (up to some positive and finite constant)

The case (3.15) corresponds to a “very early” break; in this case, Theorem 3.3 states that the expected delay is approximately , i.e. that it is approximately equal to . Clearly, as increases, decreases; the dispersion around the expected delay, measured by , also decreases, indicating that the choice of plays a role in determining the delay in detecting (very early) changepoints, and that larger values of reduce such a delay. In the presence of an “early, but not so early” break - corresponding to case (ii) of the theorem, where recall that , the expected delay still decreases as increases, as long as , for , but the dispersion around the expected delay - given by the standardization - does not depend on . Finally, the case of a late(r) change is studied in part (iii) of the theorem: in such a case, - and therefore the weight function in the definition of the detector - does not play any role.

3.2.2. Detection delays when

We now investigate the asymptotic behaviour of the stopping time defined in (2.9) - that is, when the detector is a Rényi type statistic with . In such a case, the asymptotic behaviour of the detection delay uses the same notation irrrespective of whether or .

Let

We define two independent normal random vectors and such that and

Similarly to and in (3.11) and (3.12), we define

| (3.17) |

| (3.18) |

and the centering sequence

and the rescaling sequence .

Theorem 3.4.

Similarly to Theorem 3.3, Theorem 3.4 describes the detection delay when using Rényi type statistics depending on the location of the break; to the best of our knowledge, this is the first time such a result has ever been derived. Part (i) of the theorem is also derived in Ghezzi et al. (2024), and, in essence, it states that if the break occurs prior to the trimming sequence in the Rényi type statistics, then it is identified straight at - that is, as soon as the Rényi type statistics starts the monitoring. Parts (ii) and (iii) of the theorem refine and extend the results in Ghezzi et al. (2024). Finally, part (iv) states that, in the case of a break occurring late - or, better, much later than - a large value of could even be detrimental because the centering sequence diverges with , at a faster rate as increases. This confirms the common wisdom (see Kirch and Stoehr, 2022a and Kirch and Stoehr, 2022b), and the findings in Ghezzi et al. (2024), that Rényi type statistics are designed for the fast detection of very early occurring breaks, whereas they may yield suboptimal results for later breaks.

4. Simulations

In this section, we assess the finite sample performance of our monitoring procedures via Monte Carlo simulations. According to the theory in Section 3, we can have two classes of monitoring schemes, based on (covered by Theorem 3.1) and (covered by Theorem 3.2). For the sake of brevity, here we only focus on the case . We consider several data generating processes (DGP). We use three lengths of the historical training sample and two lengths of the monitoring . The sequential procedure is performed times with independently generated samples, and the percentage of simulations for which the detector crosses the boundary functions is reported for several values of . For the Rényi type statistic based on Theorem 3.1(ii), we follow Horváth et al. (2021) and set . Guidelines on implementation are provided in Section A.1 of the Supplement. To obtain critical values, we simulate two independent standard Wiener processes and on a grid of equally spaced points in the unit interval and compute and . We repeat this by times and obtain the empirical , , and percentiles of the above two quantities, corresponding to the critical values at , , and levels based on Theorem 3.1(i) and (ii). Critical values are in Table 4.1.

| Based on Theorem 3.1 (i) | Based on Theorem 3.1 (ii) | |||||||||

| 10% | 5% | 1% | 10% | 5% | 1% | |||||

| 5.838 | 7.215 | 10.474 | 5.609 | 7.024 | 10.235 | |||||

| 6.173 | 7.556 | 10.819 | 5.516 | 6.909 | 10.090 | |||||

| 6.537 | 7.934 | 11.188 | 5.436 | 6.822 | 10.014 | |||||

| 7.191 | 8.622 | 11.861 | 5.340 | 6.715 | 9.913 | |||||

The boundary functions in Section 2 are designed for the case . However, preliminary simulations show that the empirical sizes based on those boundary functions tend to be larger than the nominal levels in finite samples, in particular for DGPs with the Student’s errors. To make our monitoring schemes more practical under small finite samples, we suggest to “tune” the boundary functions as

| (4.1) | ||||||

| (4.2) |

for (2.7) and (2.10) respectively. The intuition underpinning the term is to boost the boundary function in small samples. The term as is typically employed when the monitoring horizon is “long” (see Horváth et al., 2020, Horváth et al., 2021, and Horváth et al., 2022). Although this term is inconsequential for the asymptotic theory in our set-up, we find that it can further improve the empirical size. Both tuning terms are asymptotically negligible. and only play a role in finite samples to achieve better size control at no expense for power. The proposed tuning is tailored to DGPs with Student’s errors, rather than Gaussian errors; indeed, heavy tails are a well-known stylised fact of financial returns.

4.1. Empirical size under the null

Under the null hypothesis, the realisation of GARCH(1,1) in the historical training period () and in the monitoring period () is

where follows a standard normal distribution or the

Student’s distribution with degrees of freedom. Since our monitoring

procedure does not require the historical sample to be stationary or not, we

choose the following two set of GARCH(1,1) parameters, taken from Francq and

Zakoïan (2012): (i) , which represents the stationary case; (ii)

, corresponding to

the nonstationary case since

under errors following either the standard normal or the Student’s

distributions.

Table 4.2 reports the empirical sizes at

significance level for the monitoring scheme based on Theorem 3.1(i) for different values of . A noticeable feature is that a

larger results in a higher rejection rates, and a smaller is

more conservative in rejection. Under the Student’s errors,

is a good choice because the monitoring procedure has reasonably good

empirical sizes when , and the empirical sizes for are

closer to the theoretical level of . Under Gaussian errors, the

monitoring procedure is slightly under-sized, which is mainly due to the

additionally tuning we imposed in (4.1). For practical use, the

tendency to under-reject with Gaussian errors may not necessarily be a

concern, because the empirical power does not seem to be affected, as shown

in Section 4.2. Lastly, the simulation results show that our

monitoring schemed works reasonably well for both stationary and

nonstationary GARCH(1,1) models.

| Student’s | ||||||||

| Stationary GARCH(1,1) | ||||||||

| 6.5% | 4.8% | 3.5% | 8.3% | 8.0% | 6.2% | |||

| 7.1% | 5.5% | 3.8% | 10.1% | 8.9% | 7.5% | |||

| 8.5% | 6.2% | 4.5% | 11.3% | 10.8% | 9.1% | |||

| 10.1% | 8.8% | 6.6% | 14.5% | 13.2% | 10.9% | |||

| 5.2% | 4.3% | 2.7% | 8.3% | 5.4% | 4.6% | |||

| 5.8% | 4.8% | 2.9% | 9.3% | 6.1% | 5.2% | |||

| 6.6% | 5.4% | 3.7% | 11.4% | 8.2% | 6.9% | |||

| 8.7% | 7.4% | 5.6% | 14.3% | 10.5% | 8.8% | |||

| Nonstationary GARCH(1,1) | ||||||||

| 5.4% | 4.3% | 3.7% | 8.8% | 5.2% | 5.0% | |||

| 6.2% | 5.2% | 4.2% | 10.7% | 6.5% | 5.5% | |||

| 7.5% | 6.7% | 5.1% | 12.3% | 8.5% | 6.8% | |||

| 9.9% | 9.4% | 5.9% | 14.7% | 12.2% | 9.1% | |||

| 2.6% | 2.9% | 2.9% | 5.7% | 4.4% | 4.0% | |||

| 3.8% | 3.2% | 3.0% | 7.2% | 5.3% | 4.1% | |||

| 4.5% | 3.9% | 3.6% | 8.7% | 7.7% | 5.3% | |||

| 7.4% | 6.0% | 5.1% | 13.0% | 9.6% | 8.1% | |||

Table A.1 in the Supplement contains the empirical sizes for Rényi type statistics. The rejection rates are slightly higher than the nominal level. We note that, in principle, it would be possible to design a different tuning for Rényi type statistics.

4.2. Empirical power under

We now turn to the analysis of the empirical power. Under the alternative, the data is generated by

and

where the parameter changes to at time . We consider two scenarios

for the time of change: (a) corresponds to a change occurring “early, but not

too early” after the historical sample; (b) indicates a change happening much later than .

There are many possible ways of changes under the alternative. To keep our results clean, we set and , and concentrate on a change in under the following four representative alternatives:

-

:

, i.e. a change from a stationary to another stationary regime,

-

:

, i.e. a change from a stationary to an explosive regime,

-

:

, i.e. a change from an explosive to a stationary regime,

-

:

, i.e. a change from an explosive to another explosive regime.

Tables 4.3 and 4.4

show the empirical power of the monitoring scheme based on Theorem 3.1(i) at significance level when for a change

at and , respectively.111The empirical power of (not reported) is marginally lower

than the empirical power of . There are five major

observations. First, our monitoring scheme is highly effective in detecting

changes under and for both early and late changes. These

alternatives result in a change between a stationary regime and an explosive

regime, which is relatively easy to detect. Second, the monitoring scheme

exhibits high power in detecting early changes under and . These alternatives represent a change within either a stationary or an

explosive regime. Third, there is a deterioration in power when detecting

late changes under and , although satisfactory levels can

be achieved by using a large(r) training sample size of . Fourth,

the power is relatively lower when using the Student’s distribution

errors compared to normal errors. Lastly, there is only a marginal decline

observed in the power with a larger value of .

| before | ||||||||

| after | ||||||||

| 96.76% | 99.94% | 100.00% | 99.76% | 100.00% | 100.00% | |||

| 96.38% | 99.94% | 100.00% | 99.76% | 100.00% | 100.00% | |||

| 96.06% | 99.94% | 100.00% | 99.74% | 100.00% | 100.00% | |||

| 95.44% | 99.84% | 100.00% | 99.72% | 100.00% | 100.00% | |||

| Student’s | ||||||||

| 80.26% | 96.22% | 99.92% | 96.28% | 99.44% | 100.00% | |||

| 79.16% | 95.80% | 99.92% | 96.04% | 99.36% | 100.00% | |||

| 78.20% | 95.40% | 99.92% | 95.94% | 99.34% | 100.00% | |||

| 76.88% | 94.48% | 99.92% | 95.76% | 99.18% | 99.98% | |||

| before | ||||||||

| after | ||||||||

| 100.00% | 100.00% | 100.00% | 99.82% | 100.00% | 100.00% | |||

| 100.00% | 100.00% | 100.00% | 99.74% | 100.00% | 100.00% | |||

| 100.00% | 100.00% | 100.00% | 99.70% | 100.00% | 100.00% | |||

| 100.00% | 100.00% | 100.00% | 99.60% | 100.00% | 100.00% | |||

| Student’s | ||||||||

| 99.96% | 100.00% | 100.00% | 94.00% | 98.90% | 100.00% | |||

| 99.94% | 100.00% | 100.00% | 93.76% | 98.84% | 100.00% | |||

| 99.94% | 100.00% | 100.00% | 93.40% | 98.70% | 100.00% | |||

| 99.94% | 100.00% | 100.00% | 92.98% | 98.42% | 99.98% | |||

| before | ||||||||

| after | ||||||||

| 50.26% | 77.88% | 98.46% | 99.76% | 100.00% | 100.00% | |||

| 47.84% | 76.16% | 98.12% | 99.76% | 100.00% | 100.00% | |||

| 46.38% | 74.32% | 97.56% | 99.74% | 100.00% | 100.00% | |||

| 43.26% | 70.56% | 96.60% | 99.72% | 100.00% | 100.00% | |||

| Student’s | ||||||||

| 25.68% | 43.10% | 72.88% | 96.28% | 99.44% | 100.00% | |||

| 25.02% | 41.18% | 70.48% | 96.04% | 99.36% | 100.00% | |||

| 24.80% | 39.46% | 68.18% | 95.94% | 99.34% | 100.00% | |||

| 25.18% | 37.68% | 64.14% | 95.76% | 99.18% | 99.98% | |||

| before | ||||||||

| after | ||||||||

| 100.00% | 100.00% | 100.00% | 76.78% | 93.14% | 99.90% | |||

| 100.00% | 100.00% | 100.00% | 75.64% | 92.36% | 99.88% | |||

| 100.00% | 100.00% | 100.00% | 74.40% | 91.58% | 99.86% | |||

| 100.00% | 100.00% | 100.00% | 71.98% | 89.88% | 99.66% | |||

| Student’s | ||||||||

| 99.96% | 100.00% | 100.00% | 64.16% | 78.82% | 94.30% | |||

| 99.94% | 100.00% | 100.00% | 63.22% | 78.14% | 93.76% | |||

| 99.94% | 100.00% | 100.00% | 62.38% | 77.00% | 93.26% | |||

| 99.94% | 100.00% | 100.00% | 61.28% | 75.30% | 92.16% | |||

Tables A.2 and A.3 in the

Supplement provide the empirical power for the Rényi type statistics

based on Theorem 3.1(ii) under the same setting. When

detecting early changes at ,

similar observations as above apply; the monitoring schemes with

and proves to be effective. However, one noticeable difference is that

a larger value of is detrimental in the power. In particular, and suffer a remarkable loss of power under . As far as

late changes () are concerned, the

Rényi type statistics become much less effective, as predicted by the

theory. This is because Rényi type statistics are devised for the fast

detection of very early changes, whilst being suboptimal for late changes.

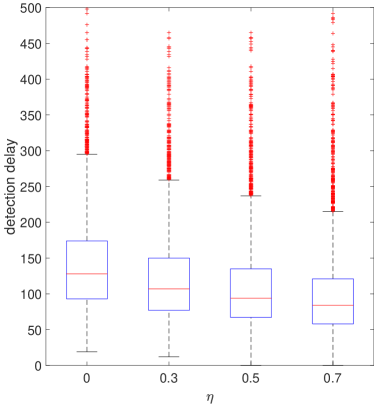

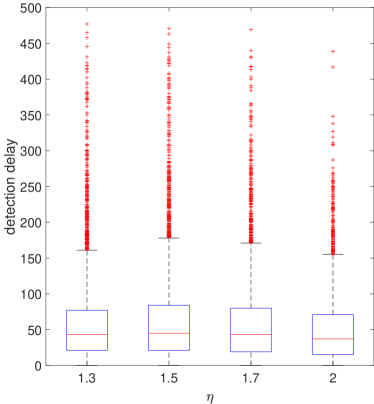

It is also worthwhile to examine the stopping time and in order to investigate the detection delays of our monitoring procedures. Figure 4.1 shows the boxplot of the detection delays of and for a change at under when , . For the monitoring procedure based on Theorem 3.1(i), it is consistent with our theory that larger values of reduce the detection delay. Considering the Rényi type statistics based on Theorem 3.1(ii), there is only a marginal difference in using various values of . Comparing the detection delay between the monitoring procedures based on Theorem 3.1(i) and (ii), we can clearly see the merit of the Rényi type statistics for the fast detection of early changes, as evidenced by shorter detection delays.

5. Empirical illustration

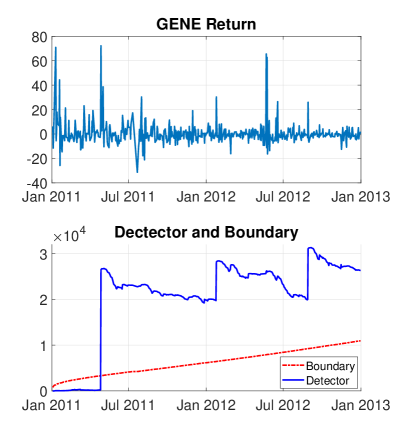

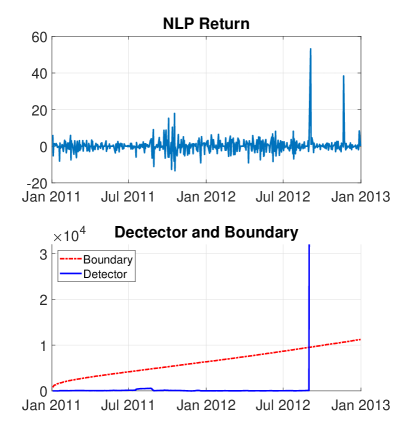

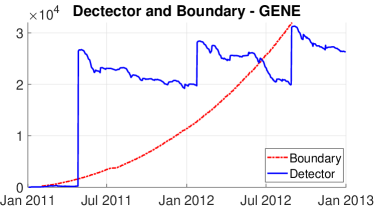

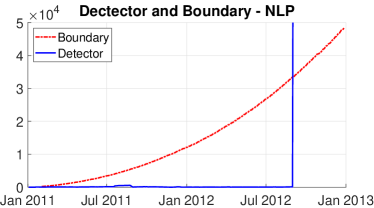

We illustrate our monitoring procedures using daily returns of individual stocks. We focus on four stocks: Apple Inc. (ticker: AAPL, Permno: 14593), Middlefield Banc Corp. (ticker: MBCN, Permno: 14932), Genetic Technologies Ltd (ticker: GENE, Permno: 90899), and NTS Realty Holdings LP (ticker: NLP, Permno: 90508). We download daily returns (without dividend) from the CRSP database.222We choose to use the daily returns without dividend, rather than log difference of prices, to avoid the complication due to stock splits. We consider two periods in order to showcase the detection for four types of changes (in the sense of the four different alternatives in our simulation). Depending on the specific purpose of the researcher, one can choose between the monitoring procedures based on Theorem 3.1(i) and (ii). Based on our simulations,if the aim is to quickly detect very early changes, we suggest using the Rényi type statistics based on Theorem 3.1(ii), with some tolerance for the compromise in size and power; conversely, if the purpose is to have good size control and high power, it is recommended to use the monitoring procedure based on Theorem 3.1(i). In this application, our preference is to have a good balance of size and power, and the procedure based on Theorem 3.1(i) (with the choice of ) delivers a good performance with sample sizes similar to the dataset used in this section.333We relegate the results using Rényi weights in Section A.3 of the Supplement. Before applying our monitoring procedure, it is necessary to ensure there is no change during the historical training sample. To this end, we use the test developed by Horváth and Wang (2024, labeled as HW(2024) hereinafter). Their test is to detect changes in GARCH(1,1) processes without assuming stationarity, which can accommodate either stationary or nonstationary historical sample. A rejection of their test indicates there is no change of in the GARCH(1,1) during the historical sample. At the same time, we are keen to understand which the type of four changes may occur. Thus, we firstly examine whether our historical sample is stationary or not by employing the nonstationarity test developed by Francq and Zakoïan (2012, labeled as FZ(2012) hereinafter). At the end of our monitoring horizon, we use the FZ(2012) test again to check the stationarity of the samples after the change (if there is one).

5.1. Change from a stationary regime

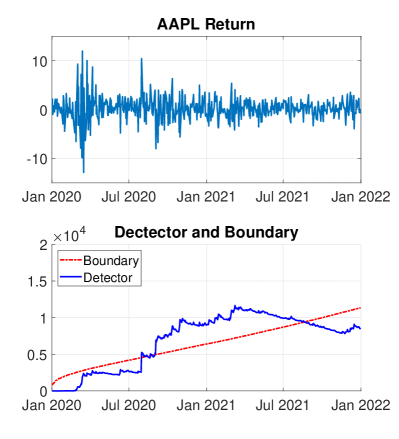

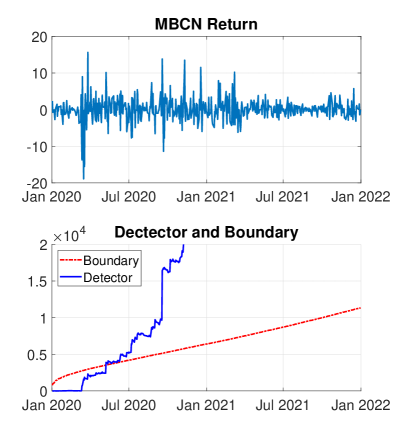

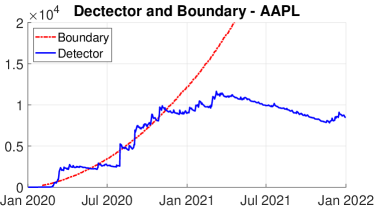

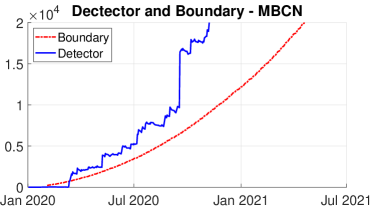

To illustrate changepoint detection from a stationary regime, we choose the training period of 2016–2019 (1007 trading days) and the monitoring period of 2020–2021 (507 trading days). The training period is before the outbreak of COVID-19, while the monitoring period is in the pandemic. We apply our monitoring procedure for the stocks of AAPL and MBCN during this period. Table 5.1 (Columns 1 and 2) reports the results of the sequential monitoring procedure, as well as other information, including HW(2024) test, FZ(2012) test, and parameter estimates. HW(2024) test indicates that there is no parameter change during the training sample for AAPL and MBCN. The nonstationarity test of FZ(2012) indicates that they are both stationary during the training sample. Our sequential monitoring detects a change of AAPL on July 31st, 2020 and a change of MBCN on May 8th, 2020. Based on the FZ(2012) test for the sample after the change, we can conclude that AAPL experienced a change from a stationary to another stationary regime, while MBCN shifted from a stationary regime to a nonstationary one. Figure 5.1 contains returns series (upper panel) during the monitoring period and the detector versus the boundary function (lower panel).

| AAPL | MBCN | GENE | NLP | |

| Training Sample | ||||

| Start Date | 2016-01-04 | 2016-01-04 | 2007-01-03 | 2007-01-03 |

| End Date | 2019-12-31 | 2019-12-31 | 2010-12-31 | 2010-12-31 |

| Sample Size | 1007 | 1007 | 1011 | 1011 |

| HW(2024) Test | ||||

| Test stat | 1.469 | 1.351 | 1.179 | 1.088 |

| Rejection | Not Rej. | Not Rej. | Not Rej. | Not Rej. |

| FZ(2012) NS Test | ||||

| -value | 0.00% | 0.00% | 35.29% | 33.81% |

| Stationary or not | Stationary | Stationary | Nonstationary | Nonstationary |

| Parameter estimates | ||||

| 0.135 | 0.183 | 0.287 | 0.099 | |

| 0.745 | 0.579 | 0.816 | 0.916 | |

| Monitoring Sample | ||||

| Start Date | 2020-01-02 | 2020-01-02 | 2011-01-03 | 2011-01-03 |

| End Date | 2021-12-31 | 2021-12-31 | 2012-12-31 | 2012-12-31 |

| Sample Size | 507 | 507 | 505 | 505 |

| Our Sequential Monitoring | ||||

| Rejection | Rej. | Rej. | Rej. | Rej. |

| Time of Change | 2020-07-31 | 2020-05-08 | 2011-04-27 | 2012-09-04 |

| After the change | ||||

| FZ(2012) NS Test | ||||

| -value | 0.00% | 10.38% | 0.00% | 100.00% |

| Stationary or not | Stationary | Nonstationary | Stationary | Nonstationary |

| Parameter estimates | ||||

| 0.052 | 0.091 | 0.488 | 0.001 | |

| 0.935 | 0.913 | 0.528 | 1.053 | |

5.2. Change from a nonstationary regime

We now consider detection from a nonstationary regime, and use 2007–2010 (1011 trading days) as the training period and 2011-2022 (505 trading days) as the monitoring period. The training period covers the global financial crisis (GFC), while the monitoring period follows the GFC but includes the European debt crisis. In this period, we monitor GENE and NLP. The results of the sequential monitoring procedure, alongside other supporting information, are displayed in Columns 3 and 4 of Table 5.1. Based on the HW(2024) test, we cannot reject that the return series of GENE and NLP have change in the training period. As evidenced by the nonstationarity test of FZ(2012), both stocks are in the nonstationary regime during the training period. Our sequential monitoring procedure reveals a change of GENE on April 27th, 2011 and a change of NLP on September 4th, 2012. After applying FZ(2012) nonstationarity test on the sample after the change, it is found that the change of GENE is from a nonstationary regime to a stationary regime, whilst the change of NLP is from a nonstationary to another nonstationary regime. It is also interesting to note that GENE after the change is in a strict stationary regime, but not in a second-order stationary regime. Figure 5.2 shows their returns series (upper panel) during the monitoring period and the detector versus the boundary function (lower panel).

6. Conclusions and discussions

In this paper, we complement the existing literature on (ex-ante) testing for bubble phenomena by proposing a family of weighted, CUSUM-based statistics to detect changes in the parameters of a GARCH(1,1) process. Our monitoring procedure can be applied irrespective of whether, in the training sample, the observations are stationary or explosive, and it is able to detect all types of changes: (a) from a stationary to another stationary regime (which is helpful in order to avoid the issues concerning the consistent estimation of a GARCH(1,1) process spelt out in Hillebrand, 2005); (b) from a stationary to an explosive regime (which contains information on the possible inception of a bubble); (c) from an explosive to a stationary regime (which, in the light of the previous point, could shed light on the cooling off the turbulence associated with a bubble on a financial market); and (d) from an explosive to another explosive regime (which, depending on the direction of the change - towards a more or a less explosive regime - could indicate whether exuberant volatility is heating up or cooling down). Technically, we propose two families of statistics, both based on weighted versions of the CUSUM process of the quasi-Fisher scores: one family uses lighter weights, and it is designed to detect, optimally, changes occurring not immediately after the start of the monitoring horizon; the other family uses heavier, Rényi-type weights, which make it more sensitive to changepoints occurring immediately after the end of the training period. For both cases, we study the limiting distribution of the detection delays; to the best of our knowledge, no such results exist for the case of a GARCH(1,1) models, and no results in general exist for the case of Rényi statistics. Given the interest in the detection of bubble phenomena, and the scant amount of contributions in the context of detection of changes in the volatility, we believe that our paper should be a useful addition to the toolbox of the financial econometrician.

References

- Aue et al. (2014) Aue, A., S. Hörmann, L. Horváth, and M. Hušková (2014). Dependent functional linear models with applications to monitoring structural change. Statistica Sinica, 1043–1073.

- Aue and Horváth (2004) Aue, A. and L. Horváth (2004). Delay time in sequential detection of change. Statistics & Probability Letters 67(3), 221–231.

- Aue and Horváth (2007) Aue, A. and L. Horváth (2007). A limit theorem for mildly explosive autoregression with stable errors. Econometric Theory 23(2), 201–220.

- Aue and Horváth (2011) Aue, A. and L. Horváth (2011). Quasi-likelihood estimation in stationary and nonstationary autoregressive models with random coefficients. Statistica Sinica 21(3), 973–999.

- Aue et al. (2008) Aue, A., L. Horváth, P. Kokoszka, and J. Steinebach (2008). Monitoring shifts in mean: asymptotic normality of stopping times. Test 17, 515–530.

- Berkes et al. (2003) Berkes, I., L. Horváth, and P. Kokoszka (2003). GARCH processes: structure and estimation. Bernoulli, 201–227.

- Bloom (2007) Bloom, N. (2007). Uncertainty and the dynamics of R&D. American Economic Review 97(2), 250–255.

- Bougerol and Picard (1992) Bougerol, P. and N. Picard (1992). Strict stationarity of generalized autoregressive processes. The Annals of Probability 20(4), 1714–1730.

- Breiman (1968) Breiman, L. (1968). Probability. Classics in Applied Mathematics. Society for Industrial and Applied Mathematics.

- Chu et al. (1996) Chu, C., M. Stinchcombe, and H. White (1996). Monitoring structural change. Econometrica 64(5), 1045–1066.

- Csörgő and Horváth (1997) Csörgő, M. and L. Horváth (1997). Limit Theorems in Change-Point Analysis, Volume 18. John Wiley & Sons.

- Fiorentini et al. (1996) Fiorentini, G., G. Calzolari, and L. Panattoni (1996). Analytic derivatives and the computation of garch estimates. Journal of applied econometrics 11(4), 399–417.

- Francq and Zakoian (2004) Francq, C. and J.-M. Zakoian (2004). Maximum likelihood estimation of pure GARCH and ARMA-GARCH processes. Bernoulli 10(4), 605–637.

- Francq and Zakoïan (2012) Francq, C. and J.-M. Zakoïan (2012). Strict stationarity testing and estimation of explosive and stationary generalized autoregressive conditional heteroscedasticity models. Econometrica 80(2), 821–861.

- Francq and Zakoian (2019) Francq, C. and J.-M. Zakoian (2019). GARCH models: structure, statistical inference and financial applications. John Wiley & Sons.

- Ghezzi et al. (2024) Ghezzi, F., E. Rossi, and L. Trapani (2024). Fast online changepoint detection. arXiv preprint arXiv:2402.04433.

- Hillebrand (2005) Hillebrand, E. (2005). Neglecting parameter changes in GARCH models. Journal of Econometrics 129(1-2), 121–138.

- Homm and Breitung (2012) Homm, U. and J. Breitung (2012). Testing for speculative bubbles in stock markets: a comparison of alternative methods. Journal of Financial Econometrics 10(1), 198–231.

- Horváth et al. (2004) Horváth, L., M. Hušková, P. Kokoszka, and J. Steinebach (2004). Monitoring changes in linear models. Journal of Statistical Planning and Inference 126(1), 225–251.

- Horváth et al. (2007) Horváth, L., P. Kokoszka, and J. Steinebach (2007). On sequential detection of parameter changes in linear regression. Statistics and Probability Letters 80, 1806–1813.

- Horváth et al. (2021) Horváth, L., P. Kokoszka, and S. Wang (2021). Monitoring for a change point in a sequence of distributions. The Annals of Statistics 49(4), 2271–2291.

- Horváth et al. (2022) Horváth, L., Z. Liu, and S. Lu (2022). Sequential monitoring of changes in dynamic linear models, applied to the US housing market. Econometric Theory 38(2), 209–272.

- Horváth et al. (2020) Horváth, L., Z. Liu, G. Rice, and S. Wang (2020). Sequential monitoring for changes from stationarity to mild non-stationarity. Journal of Econometrics 215(1), 209–238.

- Horváth et al. (2020) Horváth, L., C. Miller, and G. Rice (2020). A new class of change point test statistics of rényi type. Journal of Business & Economic Statistics 38(3), 570–579.

- Horváth et al. (2021) Horváth, L., C. Miller, and G. Rice (2021). Detecting early or late changes in linear models with heteroscedastic errors. Scandinavian Journal of Statistics 48(2), 577–609.

- Horváth and Trapani (2019) Horváth, L. and L. Trapani (2019). Testing for randomness in a random coefficient autoregression model. Journal of Econometrics 209(2), 338–352.

- Horváth and Trapani (2023) Horváth, L. and L. Trapani (2023). Real-time monitoring with RCA models. arXiv preprint arXiv:2312.11710.

- Horváth and Wang (2024) Horváth, L. and S. Wang (2024). Detecting changes in GARCH(1, 1) processes without assuming stationarity. Available at SSRN 4712255.

- Jarrow and Kwok (2023) Jarrow, R. A. and S. S. Kwok (2023). An explosion time characterization of asset price bubbles. International Review of Finance 23(2), 469–479.

- Jensen and Rahbek (2004) Jensen, S. T. and A. Rahbek (2004). Asymptotic inference for nonstationary GARCH. Econometric Theory 20(6), 1203–1226.

- Jurado et al. (2015) Jurado, K., S. C. Ludvigson, and S. Ng (2015). Measuring uncertainty. American Economic Review 105(3), 1177–1216.

- Kirch and Stoehr (2022a) Kirch, C. and C. Stoehr (2022a). Asymptotic delay times of sequential tests based on U-statistics for early and late change points. Journal of Statistical Planning and Inference 221, 114–135.

- Kirch and Stoehr (2022b) Kirch, C. and C. Stoehr (2022b). Sequential change point tests based on U-statistics. Scandinavian Journal of Statistics 49(3), 1184–1214.

- Klüppelberg et al. (2004) Klüppelberg, C., A. Lindner, and R. Maller (2004). A continuous-time GARCH process driven by a lévy process: stationarity and second-order behaviour. Journal of Applied Probability 41(3), 601–622.

- Nelson (1991) Nelson, D. B. (1991). Conditional heteroskedasticity in asset returns: a new approach. Econometrica, 347–370.

- Pelagatti and Lisi (2009) Pelagatti, M. and F. Lisi (2009). Variance initialisation in garch estimation. In S. Co. 2009. Sixth Conference. Complex Data Modeling and Computationally Intensive Statistical Methods for Estimation and Prediction, pp. 323. Maggioli Editore.

- Phillips and Magdalinos (2007) Phillips, P. C. and T. Magdalinos (2007). Limit theory for moderate deviations from a unit root. Journal of Econometrics 136(1), 115–130.

- Phillips et al. (2015a) Phillips, P. C., S. Shi, and J. Yu (2015a). Testing for multiple bubbles: historical episodes of exuberance and collapse in the S&P 500. International Economic Review 56(4), 1043–1078.

- Phillips et al. (2015b) Phillips, P. C., S. Shi, and J. Yu (2015b). Testing for multiple bubbles: limit theory of real-time detectors. International Economic Review 56(4), 1079–1134.

- Phillips and Shi (2018) Phillips, P. C. and S.-P. Shi (2018). Financial bubble implosion and reverse regression. Econometric Theory 34(4), 705–753.

- Phillips et al. (2011) Phillips, P. C., Y. Wu, and J. Yu (2011). Explosive behavior in the 1990s Nasdaq: when did exuberance escalate asset values? International Economic Review 52(1), 201–226.

- Phillips and Yu (2011) Phillips, P. C. and J. Yu (2011). Dating the timeline of financial bubbles during the subprime crisis. Quantitative Economics 2(3), 455–491.

- Richter et al. (2023) Richter, S., W. Wang, and W. B. Wu (2023). Testing for parameter change epochs in GARCH time series. The Econometrics Journal 26(3), 467–491.

- Skrobotov (2023) Skrobotov, A. (2023). Testing for explosive bubbles: a review. Dependence Modeling 11(1), 20220152.

- Sornette et al. (2018) Sornette, D., P. Cauwels, and G. Smilyanov (2018). Can we use volatility to diagnose financial bubbles? Lessons from 40 historical bubbles. Quantitative Finance and Economics 2(1), 486–594.

- Whitehouse et al. (2023) Whitehouse, E. J., D. I. Harvey, and S. J. Leybourne (2023). Real-time monitoring of bubbles and crashes. Oxford Bulletin of Economics and Statistics 85(3), 482–513.

A. Implementation guidelines, further Monte Carlo evidence, and further empirical results

A.1. Practical guidance on the implementation

In this section, we provide a detailed step-by-step guidance on implementing our sequential monitoring procedures (based on Theorem 3.1), which could be useful for researchers who want to apply it without studying the underlying theory. The steps are as follows:

-

(1)

Use QMLE to estimate the parameters using the training sample

where

and

-

(2)

Calculate the quasi-Fisher scores of the log likelihood function

-

(3)

Estimate the covariance matrix of the derivatives in the training sample

-

(4)

Obtain the detector

where

- (5)

A.2. Additional simulation results

| Student’s | ||||||||

| Stationary GARCH(1,1) | ||||||||

| 14.2% | 11.9% | 9.4% | 18.5% | 13.8% | 11.1% | |||

| 12.4% | 10.0% | 7.7% | 15.6% | 11.4% | 9.1% | |||

| 11.0% | 8.7% | 6.9% | 14.0% | 10.0% | 7.8% | |||

| 9.4% | 7.7% | 5.8% | 11.9% | 8.7% | 6.9% | |||

| 14.8% | 10.9% | 8.8% | 18.9% | 15.2% | 12.0% | |||

| 12.8% | 9.4% | 7.1% | 15.7% | 12.9% | 9.8% | |||

| 11.2% | 8.3% | 6.3% | 13.9% | 11.6% | 8.6% | |||

| 10.0% | 7.2% | 5.4% | 11.9% | 10.0% | 7.7% | |||

| NonStationary GARCH(1,1) | ||||||||

| 13.8% | 11.6% | 10.1% | 19.1% | 14.5% | 11.2% | |||

| 11.4% | 9.5% | 8.5% | 15.9% | 12.1% | 9.7% | |||

| 10.4% | 8.3% | 7.6% | 14.0% | 10.9% | 8.3% | |||

| 8.7% | 7.3% | 6.6% | 12.0% | 9.5% | 7.1% | |||

| 13.3% | 10.8% | 9.7% | 18.3% | 14.2% | 11.0% | |||

| 11.8% | 9.0% | 8.3% | 15.6% | 12.4% | 9.1% | |||

| 10.5% | 7.9% | 7.3% | 14.0% | 10.7% | 8.0% | |||

| 9.1% | 7.2% | 6.6% | 12.4% | 9.5% | 7.1% | |||

| before | ||||||||

| after | ||||||||

| 83.18% | 96.92% | 100.00% | 97.38% | 100.00% | 100.00% | |||

| 61.78% | 81.22% | 99.62% | 90.36% | 98.68% | 100.00% | |||

| 41.70% | 50.02% | 83.42% | 78.28% | 92.08% | 99.94% | |||

| 23.40% | 21.54% | 21.56% | 57.94% | 65.18% | 86.94% | |||

| Student’s | ||||||||

| 52.46% | 71.82% | 96.60% | 90.46% | 97.16% | 99.88% | |||

| 29.94% | 37.48% | 64.74% | 82.34% | 91.20% | 99.06% | |||

| 19.36% | 16.00% | 16.12% | 72.08% | 79.40% | 93.50% | |||

| 12.90% | 8.98% | 6.62% | 55.80% | 57.54% | 62.86% | |||

| before | ||||||||

| after | ||||||||

| 100.00% | 100.00% | 100.00% | 96.02% | 99.78% | 100.00% | |||

| 99.88% | 100.00% | 100.00% | 87.06% | 97.58% | 100.00% | |||

| 99.48% | 99.98% | 100.00% | 73.94% | 86.94% | 99.68% | |||

| 97.04% | 99.70% | 100.00% | 53.06% | 57.54% | 77.02% | |||

| Student’s | ||||||||

| 99.64% | 99.98% | 100.00% | 86.36% | 94.92% | 99.70% | |||

| 99.26% | 99.86% | 100.00% | 75.78% | 86.50% | 97.92% | |||

| 98.02% | 99.76% | 100.00% | 64.62% | 72.14% | 87.64% | |||

| 94.98% | 98.28% | 99.98% | 48.70% | 47.94% | 50.70% | |||

| before | ||||||||

| after | ||||||||

| 21.96% | 31.82% | 68.10% | 55.94% | 74.74% | 97.18% | |||

| 13.38% | 11.70% | 20.02% | 36.16% | 48.14% | 80.00% | |||

| 11.08% | 7.88% | 7.00% | 22.76% | 24.90% | 38.76% | |||

| 9.34% | 6.60% | 5.90% | 12.82% | 9.52% | 7.22% | |||

| Student’s | ||||||||

| 19.90% | 17.22% | 22.84% | 54.20% | 62.88% | 79.52% | |||

| 15.70% | 11.72% | 9.72% | 39.02% | 41.70% | 52.72% | |||

| 13.78% | 9.82% | 8.06% | 27.32% | 25.60% | 24.78% | |||

| 12.16% | 8.30% | 6.84% | 16.74% | 12.46% | 8.14% | |||

| before | ||||||||

| after | ||||||||

| 96.20% | 99.36% | 99.98% | 49.88% | 66.64% | 94.26% | |||

| 91.46% | 97.62% | 99.78% | 31.74% | 38.80% | 68.92% | |||

| 82.48% | 92.58% | 98.96% | 19.56% | 18.66% | 26.42% | |||

| 64.50% | 75.26% | 91.88% | 12.50% | 9.26% | 7.16% | |||

| Student’s | ||||||||

| 92.50% | 97.56% | 99.84% | 44.16% | 51.12% | 71.38% | |||

| 85.94% | 93.78% | 98.94% | 30.78% | 31.32% | 39.32% | |||

| 77.12% | 86.66% | 96.38% | 21.04% | 17.84% | 15.50% | |||

| 61.24% | 68.16% | 83.06% | 14.72% | 10.76% | 7.32% | |||

A.3. Further results - empirical application using Rényi weights

Figure A.1 presents the detector (with the choice of ) versus the boundary function based on Theorem 3.1 (ii) for the four stocks during the same periods analysed in Section 5. The monitoring procedure based on the Rényi type statistics detects a change of AAPL on March 2nd, 2020, a change of MBCN on March 13th, 2020, a change of GENE on April 27th, 2011, and a change of NLP on September 4th, 2012. Such results illustrate the merit of Rényi type statistics for the fast detection of very early changes, in particular for AAPL (nearly 5 months earlier) and MBCN (about 2 months earlier), compared to the procedure based on Theorem 3.1(i).

B. Technical lemmas

Henceforth, we use and for the gradient vector and

the Hessian matrix. We begin with some facts and notation which we will use

throughout the proofs.

If (3.2) holds, then there is a unique, stationary, non anticipative sequence satisfying

(cf. Berkes et al., 2003, and Francq and Zakoian, 2019). Next we define

. The stationary version of the likelihood function is

and we define

Similarly, the stationary version of is

| (B.1) |

Berkes et al. (2003) and Francq and Zakoian (2019) showed that the matrix

exists and it is non singular.

After the change the observations are given by

| (B.2) |

Lemma B.1.

Lemma B.2.

Lemma B.3.

Proof.

Lemma B.2 yields

It is proven in Berkes et al. (2003) that there is a neighbourhood of , say , such that

Using a two term Taylor expansion coordinate-wise, we conclude that

| (B.5) |

and

The central limit for decomposable Bernoulli shifts (cf. Horváth and Wang, 2024) yields that

| (B.6) |

and therefore Lemma B.1 and Assumption 2.3 give

| (B.7) |

According to the ergodic theorem (cf. Breiman, 1968)

| (B.8) |

and therefore Lemma B.1 implies

Given that is made of the first two coordinates of , the proof is complete. ∎

Lemma B.4.

Lemma B.6.

Lemma B.7.

We assume that Assumptions 2.1–2.3 hold.

(i) If , then we have

(ii) If in addition, Assumption 2.4 also holds, and , then we have

Proof.

Let . Jensen and Rahbek (2004) showed there is a neighbourhood of , say , such that

| (B.14) |

Let denote the vector of the first two coordinates of . Jensen and Rahbek (2004) proved that

| (B.15) |

(note that the estimator might depend on . Using the mean value theorem coordinate–wise, we get from Lemma B.6 that

with probability tending to 1. Thus we get from (B.14) and (B.15) that

Similarly,

∎

Lemma B.8.

If Assumptions 2.1–2.3 hold, then for any we can define a Gaussian process , with

| (B.16) |

such that

(i) if , then

| (B.17) |

(ii) if in addition, Assumption 2.4 also holds and , then

| (B.18) |

Proof.

Horváth and Wang (2024) showed that is a decomposable Bernoulli shift and therefore Lemma S2.1 of Aue et al. (2014) implies that for any there are Gaussian processes such that

| (B.19) |

with some , and and is defined in (B.16). The approximation in (B.19) implies both (B.17) and (B.18) in the same way as (B.10) implies Lemma B.4 and (B.13). ∎

Lemma B.9.

Proof.

The lemma follows from the proof of Theorem 3.1. ∎

Next we assume that (3.9) holds. The observations are generated by (B.2) but in contrast to the previous case, the sequence is explosive and cannot be approximated with a stationary sequence. However, we can approximate the gradient of the log likelihood function with a stationary sequence, we need only minor modifications of the arguments used before. We use the following sequences to approximate the gradient vector of the log likelihood function when (B.2) holds for an explosive sequence:

and

Let

Lemma B.10.

C. Proofs

Proof of Theorem 3.1.

We begin by showing the theorem under stationarity. It follows from Lemmas B.2–B.4 that

The covariance structure of implies that

where has independent coordinates, identically distributed Wiener processes. Using the the scale transformation and continuity of the Wiener process we conclude

The proof of part (i) of the theorem is complete when (3.2) holds since

| (C.1) |

with defined in (B.9). We now turn to proving the second part of the Theorem. We note

due to the almost sure continuity of the Wiener process, and the Law of the Iterated Logarithm for Wiener processes. The result in part (ii) of the theorem now follows from Lemma B.5 and (C.1). Under nonstationarity, the proof is exactly the same as above, only Lemmas B.2–B.5 are replaced with Lemmas B.6–B.8. We also note that according to Jensen and Rahbek (2004) (cf. also Francq and Zakoian, 2019), it holds that , where is defined in (B.16), thus completing the proof. ∎

Proof of Theorem 3.2.

We note that under our conditions, it holds that , for some . Hence in the

proofs we can replace with in

the definition of the detector, without loss of generality. We wish to point

out that the definition of depends on the sign of .

First we assume that

holds. To prove part (i) of the theorem, we note that according to

Lemma B.2

| (C.2) |

and

| (C.3) |

where and with . Following the proof of Lemma B.3 we get

and by (B.7)

Using the approximation in (B.10) we conclude

| (C.4) |

and

| (C.5) |

The Darling–Erdős (cf. Csörgő and Horváth, 1997, pp. 363–365) yields

and

Thus we obtain that

Putting together our estimates on the set , we get

with some . Since

where is defined in Theorem 3.1. Using Appendix 3 in Csörgő and Horváth (1997), we obtain that

for all . Hence the proof Theorem 3.2(i) is complete when .

Lemma B.6, (B.14) and (B.15) imply that (C.2) and (C.3) can be replaced with

and

with some , when . The approximation in (B.19) yields

| (C.6) |

and

| (C.7) |

The approximations in (C.6) and (C.7) imply part (i) of the theorem, in the same way as (C.4) and (C.5) yielded (C.7) under condition .

To prove part (ii) of the theorem, we use again the approximations

in (C.4) and (C.5). By the scale transformation of Wiener

processes we have

| (C.8) |

and therefore the Darling–Erdős limit result (cf. Csörgő and Horváth, 1997, pp. 363–368) with (C.4) and (C.5) yields

and

with

Now we get

Using the approximation of with Gaussian processes we get

with some . Now using the results on pp. 363–365 in Csörgő and Horváth (1997) with (C.8) yields

completing the proof of part (ii) of the theorem when . The same arguments can be used when . ∎

Proof of Theorem 3.3.

First we assume that (3.2) holds. After , the sequence can turn into (asymptotically) stationary sequence. Since (3.2) holds, we have

where

Under we have that Next we write for

| (C.9) |

with

| (C.10) |

We use the decomposition

| (C.11) |

where is defined in (3.4). We note that, for any

First we consider the case when (3.2) holds. The observations can be approximated with a stationary sequence defined in (3.3). Recalling the definitions of and in (3.6)–(3.8), we define

with

Now according to Theorem 3.1

It follows from the proof of Theorem 3.1

and for any

Let and write

where does not depend on . Thus we conclude

Our calculations show that we need to consider the asymptotic properties of

Since the model is the same until , the th observation following the training sample, we have that

| (C.12) | ||||

(Note that the formula for depends on whether the training sample is stationary or non stationary, cf. Berkes et al., 2003 and Jensen and Rahbek, 2004). Along the lines of the proof of Theorem 3.1 one can show that

| (C.13) |

where is a Gaussian process with and

where is defined in (3.5). Hence

Also, for any

Since is increasing on we get that

Next we write

Using (C.13) we get

where denotes a standard normal random variable, is defined in (3.13) and is the covariance matrix in (C.12). Also,

and thus we conclude

We assume now that and also holds. We modify the definition of as

Proceeding as in the previous case we get that for any

| (C.14) | ||||

Using the definitions of and we have

As in the proof of (C.13) we have

where is a standard normal random variable and is defined in (3.14). Now we conclude

where is the standard normal distribution function.

In the final case we write

In this case, we define

We write

and

We use the decomposition in (C.10) and we note

It follows from the proof of Theorem 3.1 that

where is a Gaussian process with and We write

Thus we get

Next we assume that (3.9) holds. We replace (C.10) and (C.11) with

Following the same arguments as in the case of (3.2), we get that if , then

and the definition of depends on if is finite or not. If we use

with

Using the definition of we get

| (C.15) |

Applying (B.19) and Lemma B.10 with the independence of the approximating Gaussian processes we conclude

| (C.16) |

where is a standard normal random variable and is defined in (3.13). The covariance matrix is defined in (C.12). If and , then we use

We still have (C.15) but (C.16) is replaced with

where is given in (3.14). As in the previous case, if , then we use again . Since the sum of gradients (after removing the mean) of the log likelihood function of the observations after the change is negligible, we get that

where recall that is a Gaussian process and .

Next we consider the Rényi type detector. First we investigate the case when after the change we have an (asymptotically) stationary sequence. Assume that , i.e. the change occurred before the monitoring started. By definition,

The proof is based again on (C.9) and (C.10). It follows from Lemma B.9 that

and if and , then

where are independent standard normal random variables with covariance matrices and defined in (3.5) and (3.10), respectively. Thus we get

If , then we use

It follows from the proof of Theorem 3.1 that for all

where is Gaussian process with , with defined in (3.5). Thus we conclude

For the final case we use

We observe that

| (C.17) |

and

| (C.18) |

As in the previous cases,

We obtain from (C.17) and (C.18) that

We get from (C.13) that

where is a standard normal random variable and is defined in (3.14). We now conclude

The proof when (3.9) holds is essentially the same so the details are omitted. ∎