Robust Advertisement Pricing††thanks: The authors are grateful to (alphabetically) Dirk Bergemann, Marina Halac, Elliot Lipnowski, Xiao Lin, Qingmin Liu, Ernesto R. Mora, Ferdinand Pieroth, and the participants of SEA 2023 Annual Meeting and Yale University microeconomic theory lunch for their helpful discussions and comments.

Click here for the latest version

Abstract

We consider the robust pricing problem of an advertising platform that charges a producer for disclosing hard evidence of product quality to a consumer before trading. Multiple equilibria arise since consumer beliefs and producer’s contingent advertisement purchases are interdependent. To tackle strategic uncertainty, the platform offers each producer’s quality type a menu of disclosure-probability-and-price plans to maximize its revenue guaranteed across all equilibria. The optimal menus offer a continuum of plans with strictly increasing marginal prices for higher disclosure probabilities. Full disclosure is implemented in the unique equilibrium. All partial-disclosure plans, though off-path, preclude bad equilibrium play. This solution admits a tractable price function that suggests volume-based pricing can outperform click-based pricing when strategic uncertainty is accounted for. Moreover, the platform prioritizes attracting higher types into service and offers them higher rents despite symmetric information between the platform and the producer.

JEL codes: D47, D82, D86, L86, M37

Keywords: verifiable disclosure, advertisement pricing, contracting with externalities, adversarial equilibrium selection, divide and conquer

1 Introduction

Search engines, social media, and e-commerce platforms offer ad plans that enable producers to disclose product information to consumers to affect product prices. A crucial issue is that consumers often cannot observe the producers’ ad plan choices; they only see the ads if the platforms distribute them. This leads to consumer skepticism111We follow the terminology of Milgrom (1981) in the context of verifiable disclosure.: When consumers find themselves unexposed to any ad, they cannot distinguish between a producer investing little on ads and one investing heavily yet unable to reach out to them.

A key problem of strategic uncertainty thus arises: Consumer skepticism depends on how much consumers expect the producers to spend on ads contingent on product quality; In turn, such skepticism also endogenously determines the producers’ outside value of not purchasing ads, consequently influencing their contingent purchase decisions. Different consumer skepticism can be self-fulfilling and there may be multiple equilibria, some of which lead to extremely low revenue for the platform.

In the presence of such strategic uncertainty, this paper studies a platform’s optimal design of advertisement pricing that maximizes the revenue guarantee across all equilibria. We ask: What is the robustly optimal pricing scheme? How much surplus is left for producers? Should the platform hide information intentionally? Does our solution speak to the prolonged discussion on the modeling of ad prices/costs?

In our model, a producer acquires hard evidence that reveals the quality of her product. For example, the producer can obtain hard evidence through awards, test certificates, product reviews/ratings222Our main model assumes the signal structure that generates the hard evidence is exogenous and full-revealing. Later in Section 5.2, we fully characterize the cases where the signal structure is imperfect and can be designed by the platform. However, the producer cannot disclose the hard evidence to a (representative) consumer by herself. This may be because the producer cannot attract consumer attention, or because it is too costly for each individual consumer to verify the hard evidence. The only way the producer can disclose product information to the consumer is to purchase the ad services offered by a platform. To profit from advertising, the platform designs a profile of menus that contain ad plans. Each plan consists of a (potentially interior) disclosure probability and a price. Since the evidence is usually needed for producing ads, we assume the platform can directly observe the producer’s type and offer type-dependent menus of ad plans.333We further motivate type-dependent menus in Section 2.3. In practice, committed exclusive contracts are widely observed on platforms as a tool to customize. For example, Google Advertising and Microsoft Advertising crawl advertisers’ websites to assess their relevance and quality, which they use to exclusively allocate ad locations, exposure time, and prices. In this way, we eliminate adverse selection as a confounding driving force in the model.

Given any profile of type-dependent menus, a game between the producer and the consumer unfolds as follows. First, the hard evidence is realized and observed by both the producer and the platform. The producer can either choose no disclosure or pick one plan from the menu exclusive to her type. Crucially, the producer’s choice is not observed by the consumer. If a plan is chosen, the platform charges the price and stochastically discloses the evidence with the probability specified in the chosen plan. Upon seeing the evidence, the consumer learns the type. If disclosure does not happen, the consumer updates belief according to his conjecture of the producer’s contingent purchase decisions. Finally, the producer sells the product to the consumer via a take-it-or-leave-it offer at a price equal to his posterior mean.

There may be multiple equilibria between the producer and the consumer. To illustrate how severe the issue of strategic uncertainty can be in our environment and motivate our robust objective, let us start with the benchmark where the platform can select its favorite equilibrium as in standard principal-agent frameworks. In this case, the optimal pricing policy for the platform is to sell full disclosure to producers of any type except the lowest type at the price . In the induced platform’s favorite equilibrium, producers of all types except the lowest type pay for full disclosure. The consumer skepticism in this equilibrium is rather extreme: When the consumer sees no ads, he believes the product has the lowest quality. This extreme skepticism serves as the most powerful punishment against producers who turn down the platform’s offer by giving them an outside value of . The platform can thus achieve maximum possible surplus extraction. However, under the same pricing design, there is an extremely undesirable equilibrium for the platform where it earns zero revenue. In this equilibrium, no producers of any type purchase the ad, and the consumer skepticism belief remains the prior. This mild skepticism means the producer can sell the product at a price equal to the prior mean without advertising, so she has no incentives to purchase the expensive full disclosure.

The stark difference in the revenue among multiple equilibria suggests that the platform faces large strategic uncertainty. In fact, we can show a stronger result: For any pricing policy that achieves close to full-surplus extraction in the platform’s favorite equilibrium, the pricing policy also induces a bad equilibrium where the platform’s revenue is close to 0. To the extent that the platform in our model does not create social surplus, it may especially worry that the producer and the consumer coordinate on its least favorite equilibrium to resist surplus extraction. Moreover, the platform may also worry that market participants cannot play Nash equilibrium and instead resort to weaker notions such as rationalizability.

With these motivations, we solve for the robustly optimal menu profile that guarantees the maximum expected revenue to the platform in the worst-case equilibrium of the induced producer-consumer game. The optimal solution also induces a unique rationalizable outcome, so it remains optimal if the objective is to maximize revenue guarantee among all rationalizable outcomes.

Our main result, Theorem 1, delivers two central characteristics of the robustly optimal menu profile: (i) The menu for each type contains a continuum of plans equivalent to a strictly convex price function, but most of plans are never chosen on the equilibrium path; (ii) The platform adopts a complete divide-and-conquer strategy by offering plans as if it always prioritizes guaranteeing disclosure probabilities from high types over low types.

One can visualize the robustly optimal menu profile through the following procedure: First, the platform uses a plan with a small disclosure probability with a sufficiently low price to bait the highest type producer to deviate from the hypothetical equilibrium where no type discloses. Then, it introduces a continuous sequence of similar bait plans. Each such bait plan lures the highest type out of the hypothetical equilibrium where she chooses the plan right before the bait plan in the sequence. Full disclosure hereby becomes the unique credible choice of the highest type. Next, this continuous baiting process repeats for the second highest type, but the hypothetical equilibria to be broken now take the highest type’s full disclosure as granted. After this, the process continues sequentially for the other lower types, assuming all higher types’ full disclosure as guaranteed.

Our first solution characteristic points out the optimality of using continuous off-path plans. Off-path plans are never chosen by the producer in the induced equilibrium, but they serve as baits to break undesirable equilibria. To provide intuitions for the result, we examine the following binary-type example. Consider a producer whose product is of value either 0 (low) or (high), and each value occurs with equal probabilities. Since it is never profitable to induce the low type to disclose, we assume for now the platform offers a single menu exclusive to the high type.

To see why it is beneficial to offer more than one plan in the menu, let us start by solving the optimal single-plan menu. In this case, it is optimal to offer a full disclosure plan, and the high type must choose between purchasing the plan and ignoring the ads. To robustly induce full disclosure from the high type, the price of the full disclosure plan must be so low that the high type ignoring the ads cannot form an equilibrium. Suppose such under-advertising indeed forms an equilibrium, the consumer skepticism equals the prior, and the producer can sell the product with price without purchasing ads. Thus, to break the hypothetical equilibrium, the full disclosure price cannot exceed , where 1 is the disclosure probability, and are the respective gains from reaching and not reaching the consumer via ads. In conclusion, the robust guarantee cannot exceed with single-plan menus.

However, the platform can do better by offering a second plan in the menu as follows. The menu offers a full disclosure plan with price and a half disclosure plan (probability ) with price . This menu induces full disclosure in the unique equilibrium and guarantees a revenue of , higher than the revenue of in the previous case. To see this, let us first consider the hypothetical equilibrium where the high type ignores the ads completely. Because observing no ads does not alter the consumer’s belief, the producer’s outside value is . The price for half disclosure is strictly smaller than so the high type finds it optimal to deviate to purchase the half disclosure plan. Next, consider the second hypothetical equilibrium where the high type chooses half disclosure. Importantly, since the high type producer does disclose in this hypothetical equilibrium, observing no ads becomes a bad signal: The consumer in skepticism believes that the high type only has probability . This implies the producer’s outside value drops to . Thus, the high type finds it profitable to deviate to full disclosure because the price increment from half to full disclosure is strictly smaller than .

As illustrated in the binary example, an interesting feature of the optimal solution is that the high-type producer is lured to “defeat herself”. In a hypothetical equilibrium where the high type has more disclosure, the consumer thinks worse of the producer in skepticism, creating a lower outside value for her. From above, one can see the outside value of in the half disclosure equilibrium is lower than that of in the ignore-the-ads equilibrium. However, the high type is always lured to deviate to a higher disclosure probability, failing to internalize the indirect externalities this has on herself. The example only shows how to move from a 1-plan menu to a 2-plan menu. One can imagine how to further improve the revenue guarantee by filling in more intermediate plans. As the number of plans grows to infinity, the menu converges to our optimal solution with a continuum of plans.

The intuition for the other solution characteristic, complete divide-and-conquer, is harder to deliver in short sentences. Roughly speaking, one can sense from the previous example that to robustly induce an additional unit of disclosure probability, the platform needs to compensate the producer for giving up her outside value, which equals the consumer’s value expectation in skepticism. Therefore, to reduce the total rent left to the producer while robustly inducing full disclosure, the platform wants to strike down consumer skepticism as “fast” as possible. The disclosure of higher types should be prioritized because the Bayes rule indicates that one unit of ex-ante disclosure probability from a higher type strikes down skepticism more effectively than that from a lower type. Thus, the complete divide-and-conquer strategy is optimal.

It is challenging to prove the optimality of our solution because worst-case implementation requires breaking all the undesirable equilibria and it is unclear what is the optimal way to break them. In other words, the platform has to answer two questions: In each undesirable equilibrium, which type of the producer deviates, and which plan does the type deviate to? We provide clear answers to these questions. Lemma 2 answers the second question by showing that it suffices to look at cases where each equilibrium is broken by some local upward deviation. Lemma 3 answers the first question and says that the deviating type should always be the highest type that has not yet fully disclosed herself.

Our main result gives rise to a couple of interesting implications. First, optimally countering strategic uncertainty does not lead to distortion in “allocations” as full disclosure is induced in the unique equilibrium. For comparison, other frictions such as adverse selection would rather induce inefficient communication.444An imaginable counterpart framework that focuses on adverse selection would be a platform that commits to a single non-type-dependent menu and can choose its most preferred equilibrium. A typical revelation principle will say that it is without loss to focus on menus and equilibria where types report truthfully and disclosure levels are monotonic in types. To reduce information rents to higher types, full disclosure is not likely given the optimal menu. Second, under the optimal solution, producers of higher types enjoy higher rents. Such a monotonic rent structure comes from the optimality condition: Many suboptimal menu profiles induce non-monotonic rents. This contrasts with a setting where adverse selection is the main driving force and monotonic rents result from incentive compatibility. Third, the strictly convex price functions contrast with the well-known click-based pricing yet take a logarithm form that supports the classic volume-based pricing first developed by, for example, Butters (1977) and Grossman and Shapiro (1984).

To explore the allocative role of platform advertising, we first consider two benchmarks where the platform is absent and the producer either can or cannot control disclosure. If the producer cannot self-advertise, then no communication happens and every type earns the prior mean. If the producer does have the option to disclose freely, we have the setting of Grossman (1981) and Milgrom (1981) who show that, in equilibrium, the producer’s unraveling impetus results in every type fully disclosing and earning exactly the type. In both cases, the producer extracts full surplus, albeit distributed differently among types. In comparison, the platform in our model is able to extract high surplus despite adversarial equilibrium selection, and every producer type is strictly worse off than in both benchmarks.

Finally, we consider several robustness checks and extensions. First, we show that under the optimal menu profile, all types expect the lowest type choosing full disclosure is the unique rationalizable outcome so our solution remains robustly optimal even if the platform worries that market participants may fail to play Nash equilibrium.

Second, in the main model, the type-dependent menus are deterministic. We show this is without loss of generality and point out another way of implementing our optimal solution: Instead of offering a deterministic menu with continuous options, the platform can achieve the same by offering only the option of full disclosure at a random price. This implementation may work better in applications where the platform cannot completely control or fine-tune the disclosure probability.

Third, we allow the platform to jointly design the menu profile and the information structure. This extension speaks to applications where evidence about product value is generated and controlled by the platform. For example, Amazon extracts keywords from reviews and YouTube gives out creator awards. We show that the platform’s desire to strike down consumer skepticism as “fast” as possible makes it want to segregate the information. Consequently, perfect revealing is the optimal information structure. Fourth, we show that the producer types still face strictly convex price functions even if the platform needs to pay potentially non-convex advertising costs.

Outline. Section 2 lays out the model, entailing a benchmark case without strategic uncertainty and a discussion of assumptions. With a binary-type example, Section 3 illustrates the optimality of using continuous menus. Section 4.1 discusses our main result. Section 4.2 and Section 4.3 show three lemmas toward the proof and insights. Section 5 analyzes the extensions. All proofs are in the Appendix.

Literature Review

This paper relates to the literature on contracting with externalities in multi-agent settings, pioneered by Segal (1999, 2003). Our solution concept of robust optimum achieves unique implementation, as in most papers in this literature.

The most related paper is Segal (2003) who also studies settings where a principal offers bilateral agent-by-agent (in our case, type-by-type) menus of plans to implement the desired outcome in the unique equilibrium. Our major departure from him and all the others in this literature mentioned below is that the multiple producer types in our model have indirect externalities. In other words, one type’s disclosure will not directly affect other types’ payoffs but it can indirectly influence payoffs through shifting consumer beliefs. Put differently, the consumer’s skepticism belief is an equilibrium element that the platform can neither contract on nor provide incentives to. This key difference separates our solution that offers continuous menus from Segal’s solution where it suffices to use finite ones, even though both settings allow for continuous action spaces. Moreover, one result of Segal (2003), his Lemma 3, is related to our Lemma 2 in showing that every menu profile can be mapped into an alternating divide-and-conquer strategy. However, since we deal with plan continuums and do not have increasing externalities for all types, his Round-Robin optimization argument is not directly applicable.

Another branch of this literature led by Winter (2004) also seeks to weaken contractibility by limiting the principal’s ability to monitor agent actions and offer incentives to them. Many, such as Winter (2004), Bernstein and Winter (2012), and Halac et al. (2020), consider binary actions and simple monitoring systems, which results in the principal offering a single plan to each agent. Halac et al. (2021), Halac et al. (2022), and Halac et al. (2023) allow the principal to jointly design communication or monitoring schemes, which enriches the solution structure. In particular, Halac et al. (2021) study a principal who can offer stochastic contracts and privately inform each agent of his contract realization before choice-making. Their optimal contracts alternatingly divide-and-conquer the probabilities of agents taking actions. However, their solution shares a finite structure with Segal (2003). Our random menus extension (Section 5.3) interprets our optimal solution as random menus with continuous supports.

On the pricing of communication under adversarial equilibrium selection, Ali et al. (2022) study a rating agency that designs a signal about a product, and sets a single price for disclosing the hard evidence to the market after the potential buyer of the rating service observes the signal realization. Our joint-design extension (Section 5.2) shares a similar setup except that our platform has greater pricing power. The platform in our model can offer type-dependent menus; later (Section 5.3), we even allow the price to be random. With this pricing power, our platform prefers the perfect revealing signal structure and shifts all the complexity onto the design of prices. In contrast, in Ali et al. (2022), the optimal information design is noisy because their principal is restricted to a simpler pricing structure - it can only charge a deterministic price that is uniform across all signal realizations.

Our insights build on the literature of verifiable disclosure, starting with Grossman (1981) and Milgrom (1981). The key concept incorporated by many models is skepticism, namely the receiver’s belief when no disclosure happens both depends on and shifts the sender’s contingent behavior. For example, Dye (1985), Ben-Porath et al. (2018), Migrow and Severinov (2022), and Whitmeyer and Zhang (2022) consider a receiver who cannot tell if a sender has acquired evidence. Verrecchia (1983) considers costly disclosure. More broadly, Okuno-Fujiwara et al. (1990) and Hagenbach et al. (2014) discuss the verifiable information sharing among multiple players, and Shin (1994), Hart et al. (2017), and Ben-Porath et al. (2019) develop evidence games.

This paper also interacts with the prolonged discussion on advertisement pricing and costs. Our solution highlights a class of convex price functions in the logarithm form, which looks similar to the classic volume-based pricing first micro-founded by, for example, Butters (1977) and Grossman and Shapiro (1984). It thus contrasts the more recent click-based pricing which tends to admit a linear price. One can see, for example, Bagwell (2007) for a survey on nonlinear advertisement pricing and Kapoor et al. (2016) for a survey on click-based pricing.

2 Model

A risk-neutral producer (she) wants to sell a product to a risk-neutral consumer (he) through a take-it-or-leave-it price offer. The producer observes the product value, , whereas the consumer only knows that the value is drawn from a type space according to a distribution . We focus on finite-type cases, that is with and is represented by prior probabilities , , …, and , which we assume are strictly positive. Reorder the types such that , so refers to the highest type while is the lowest.

Despite the producer’s knowledge of the type, we assume there is no way for her to transmit any information credibly to the consumer. So, absent a third party, the producer will charge a price (slightly lower than) the consumer’s willingness to pay which equals the prior mean and the consumer will buy the product given this price.

Menu profiles of advertisement plans. Before making the price offer, the producer can purchase an advertisement plan from a platform. The key feature is that the platform can obtain (and thus observe) a hard evidence that reveals the type and commit to menus of plans that offer to potentially partially disclose the evidence. Specifically, each plan consists of a disclosure probability and a price , written as . Prior to type realization, the platform chooses a profile of menus where each menu is a set of plans, namely for each type :

| (1) |

As a convention, we use superscript to denote objects that are specific for type and superscript to denote a vector of such type-dependent objects. Each menu can be arbitrarily large and even contain a continuum of plans. To address the issue of equilibrium existence, we make a technical assumption that each menu must induce a compact graph in the joint space of probabilities and prices. Moreover, since the producer can always ignore the platform, we require each menu to contain . The set of all such menu profiles is denoted by .

Timing and payoffs. Before type realization, the platform offers a menu profile . A type, say , is realized and observed by both the producer and the platform. Having observed the menu profile, the producer picks a plan from the menu designated to her type, denoted by . The platform then discloses the hard evidence that reveals to the consumer with the chosen probability . Importantly, the consumer cannot observe the producer’s choice of plan but does observe the menu profile. He observes the hard evidence if and only if disclosure happens. Given these, he updates his belief according to the Bayes rule. Finally, the producer makes a take-it-or-leave-it price offer and the consumer decides whether to accept it or not.

The payoffs are described for the “ex-post” stage right before the producer makes the price offer. The platform earns the chosen price (so advertising per se is costless), the producer earns the consumer’s willingness to pay which now equals the posterior expected type net the price , and the consumer expects zero surplus from the trading.

Disclosure equilibria. We consider the pure-strategy sequential equilibria (Kreps and Wilson (1982)) of the disclosure subgame induced by a menu profile . The timing of this subgame is the same as above except that the menu profile is already chosen and held fixed. Each such equilibrium specifies the producer’s contingent choices, , and the consumer’s posterior beliefs . Here, refers to the probability the consumer’s posterior assigns to following the game path on which the true type is , the producer chooses , and the disclosure action is being if disclosure happens, or if not. The vector without superscript denotes the posterior.

For more notational conventions, we let be some profile of contingent choices of plans, and and be contingent choices of probabilities and prices, respectively. We let denote the types other than , and , , and be the profiles without the th component, and something like be a full profile with the th number being replaced with and the non part unchanged. Moreover, we introduce an incomplete order that compares probability profiles: , if for all .

An equilibrium being sequential is equivalent to the following555In comparison with perfect Bayesian equilibrium, the restriction that sequential rationality puts on beliefs is (ii), which says that irrespective of histories, the hard evidence always reveals the type. See, for example, Hagenbach et al. (2014) who consider a similar equilibrium concept for their disclosure environment.:

(i) Given consumer beliefs, each type chooses a plan to maximize the producer’s interim expected payoff ; (ii) For every and , any observation of hard evidence reveals the type, that is ; (iii) Given producer strategy profile , for every , , and , the belief at nondisclosure, or also called at skepticism (in the terminology of Milgrom (1981)), is given by the Bayes rule:

| (2) |

Let be the set of all such disclosure equilibria when menu profile is fixed. In addition, let denote one such disclosure equilibrium.

Robustness. We investigate the robustly optimal menu profile that maximizes the platform’s expected profit guaranteed across all disclosure equilibria given each menu profile.

Definition 1.

The platform’s maximal revenue guarantee is:

| (3) |

In fact, the infimum above can be replaced with minimum as is compact666This results from the following facts: (i) induces a compact graph; (ii) All inequality conditions for disclosure equilibrium are weak and involve continuous functions; (iii) The Bayes rule (2) is continuous.. Thus, given each menu profile , there exists a worst-case disclosure equilibrium denoted by where we further write , or sometimes without confusion, simply with . We say that robustly induces the probability profile and guarantees revenue .

The supremum in (3), however, may not be attainable and we seek to characterize a robustly optimal menu profile. This solution concept is defined by the following:

Definition 2.

A menu profile is a robustly optimal menu profile if there exists a sequence of menu profiles such that:

-

1.

For all , the menu sequence converges to with respect to the Hausdorff metric;

-

2.

The revenue guarantee sequence converges to .

To simplify the terminology for stating our results, we say that robustly induces a certain probability profile if there is a sequence that approximates in the sense above and some such that for all , robustly induces .

2.1 Simplifying Disclosure Equilibria

We first process a preliminary step that simplifies the notations we use to denote each disclosure equilibrium. To do this, we fix a menu profile. As one can see from (2), if the Bayes rule can be applied, the beliefs in skepticism, namely , do not vary with type realization or producer choice . In cases where the Bayes rule cannot be applied, all types fully disclose, which can only be supported in equilibrium by the skepticism belief that assigns probability one to the lowest type because, otherwise, the lowest type will enjoy the skepticism in her favor and never disclose. Moreover, the beliefs at observation, namely , are pinned down by the type realization . So, it suffices to denote an equilibrium by where is the single skepticism belief determined by as in (2).

The next thing is to define the skepticism value associated with a probability profile as the consumer’s expected type in skepticism, which marks the outside value of each producer type in the equilibrium with contingent disclosure and plays a crucial role in later analysis. According to (2), the skepticism value is given by:

| (4) |

For convenience, we complete this definition by setting . In fact, this is the unique skepticism value that can support probability profile in equilibrium. One crucial feature of this function is that for all disclosure outcomes , if some type satisfies , then increasing the th component of will increase (not change; decrease) . In other words, additional disclosure probability from a type always “pushes away” consumer skepticism from the type.

With this function, we can rewrite the optimal choice of each type as . Moreover, if we fix the consumer’s skepticism value , type ’s indifference curve becomes a straight line, namely for some , she is indifferent between all plans that satisfy:

| (5) |

The line has slope being the marginal benefit of disclosing with higher probability. All plans that lie beneath this line become profitable deviations for (given the fixed ).

2.2 Benchmark without Strategic Uncertainty

We first consider what would happen if the platform does not take into account strategic uncertainty. In this benchmark, the platform chooses the menu profile to maximize the expected revenue in the best-case equilibrium, namely it solves: .

Proposition 1.

Under best-case implementation, an optimal menu profile is given by for all , . All types choose full disclosure in the best-case equilibrium where the platform earns . However, there is another equilibrium where all types choose the outside option.

To see why the two equilibria can coexist given the optimal menu profile in Proposition 1, first notice that with full disclosure of all types, no disclosure is off-path, so the skepticism belief can be arbitrary. Here, we let it assign all probability to the lowest type. Then, given this punishing belief, all types are indifferent between the outside option and the full disclosure plan. Second, with all types choosing the outside option, the skepticism belief is simply the prior, and this less punishing belief makes the full disclosure prices seem too expensive, so all types indeed find the outside option satisfying.

Proposition 1 highlights two observations. First, in the best-case equilibrium, the platform extracts the maximum possible surplus, , because is the total surplus and consumer beliefs cannot be worse than the lowest type . From a technical perspective, this simple feature marks our model as a frictionless benchmark once we rule out strategic uncertainty. This helps us to clearly isolate the driving force of our results. In terms of modeling choices, this benchmark makes it questionable to grant extreme market power to the platform, a point we will elaborate on later.

Second, there is another extremely bad equilibrium where the platform gains no surplus, so the optimal menu profile in the standard framework is extremely fragile to strategic uncertainty. To highlight such fragility, we establish a stronger result. In particular, Proposition 2 shows that every menu profile that induces an equilibrium where the platform’s revenue is close to the maximum possible surplus extraction also induces an equilibrium where the revenue is close to 0.

Proposition 2.

There is such that for any small , any menu profile that induces an equilibrium where the revenue is no less than also has an equilibrium where the revenue is no greater than .

Hence, the extreme strategic uncertainty is not just the feature of one particular optimal mechanism, and it can not be resolved by using approximately optimal mechanisms.

2.3 Discussions of Model Assumptions

Pure-strategy equilibrium. Our equilibrium concept only considers pure strategies to be played by different types, which, nevertheless, is without loss in the following sense. On the one hand, by extending to mixed-strategy equilibrium, the set of equilibria given each menu profile becomes larger making the maximal revenue guarantee lower than in the pure-strategy case. On the other, our main result (Theorem 1) proposes a solution that, even allowing for mixed strategies, implements the desired outcome in the unique equilibrium. Thus, the maximal revenue guarantees in both cases are equal to each other and can be implemented with the same menu profile.

Efficient trading. We make a stylized assumption that the producer always sells the product to the consumer. This setup assumes away the matching value of advertising. Thus, we can focus on the platform’s allocative role and influence on communication quality, even without serving a productive role. What is more subtle is that the platform’s ability to induce disclosure and payment depends on the externalities from actions across different producer types, so without a productive aspect of the game, the externalities are restricted to informational interactions.

Type-dependent menus. Our platform can offer type-dependent menus instead of, for example, a single menu. Apart from the fact that the platform must observe the content of ads before distributing them, this setup is also a stylized assumption that serves the following goal: We must shut down other contractual frictions such as adverse selection, and leave strategic uncertainty to be the sole driving force. On the one hand, Proposition 1 shows that with type-dependent menus and best-case implementation, the platform extracts the maximum possible surplus, so considering worst-case implementation provides a stylized demonstration of the effect of strategic uncertainty. On the other, by instead considering a single menu but maintaining best-case implementation, we obtain a framework where adverse selection is the driving force. In this case, the revelation principle says that every mechanism induces disclosure probabilities that are monotonic in type, and partial disclosure appears in the optimal solution. We can thus compare adverse selection and strategic uncertainty as two common frictions.

3 A Binary-Type Example

We now consider the case . For clarity, we redenote the two types by high type and low type . For this example alone, we use a single scalar to represent consumer belief which refers to the probability of the high type. The prior is also redenoted by . We further set and , which brings the convenience that consumer belief coincides with his value expectation. Moreover, since it is never profitable to induce disclosure out of the low type as the consumer never thinks of the producer worse than the low type, it is without loss to always offer the low type nothing, and the essential choice is a single menu exclusive to the high type. Also, a probability profile now degenerates to the high type’s probability and thus, for this example alone, we rewrite the skepticism value given the profile as a function of :

| (6) |

This example aims to illustrate two things: (i) The platform can do strictly better by enriching a simple menu with partial-disclosure plans; (ii) A continuous menu represented by a tractable price function that is strictly convex in disclosure probability emerges as the optimal menu.

Why large menu and partial disclosure? These two elements are the novel pricing power we give to the platform. They expand the platform’s choice space beyond the bang-bang disclosure options (plans with 0/1 probabilities) studied by, for example, Ali et al. (2022). To see why this is important, consider the following bang-bang menu offered to the high type (with small ):

| (7) |

This menu robustly induces full disclosure out of the high type because the new price breaks the hypothetical equilibrium where both types choose . Namely, suppose both types choose , the consumer’s skepticism belief is the prior which, however, makes the high type want to deviate to and earn . Actually, if we restrict the platform to offer only bang-bang options, delivers the highest revenue guarantee777This can be seen immediately once we introduce Lemma 1 in Section 4.2, which implies that with only bang-bang plans, it suffices to consider the menus in the form for some price . as goes to 0.

However, this binary menu can be improved by a three-plan menu given by (with small ):

| (8) |

Recall that is the skepticism belief when the high type discloses with probability while the low type has no disclosure. The new menu looks similar to in that its second plan is the “half” of the full disclosure plan in . The previous argument again shows that this plan breaks the hypothetical equilibrium where the high type chooses . The difference between and is that the latter includes a third plan constructed to break the hypothetical equilibrium where the high type chooses the second plan of half disclosure. That is, suppose the low type chooses (as she always will) and the high type chooses the half disclosure plan, the consumer’s skepticism belief is exactly . But, the high type now would rather deviate to the third plan of full disclosure to earn .

As a result, robustly induces full disclosure out of the high type while approximating an expected profit, , higher than that with , , because .

The insight behind such improvement is akin to the adverse selection argument of unraveling (e.g., Grossman (1981); Milgrom (1981)) which says that more disclosure out of high types worsens the receiver’s skepticism, which pushes up the opportunity cost of nondisclosure making further disclosure even easier to induce. In , the platform takes advantage of a related implication that a hypothetical equilibrium with more high-type disclosure requires less reduction of price to break. This improvement depends on two elements: large menu and partial disclosure.

For other settings that also allow for these two elements, Segal (2003) studies a model where a principal offers agent-dependent menus of plans to multiple agents to implement certain outcomes in the unique equilibrium. However, his principal will not find the improvement process above helpful, so the optimal menus there tend to be “coarse”. In particular, when there is one menu to be offered, as in our binary-type example, Segal’s optimal menu will be simply binary. In our case, one will see below that by continuing such improvement, we eventually obtain a continuous menu. The cause of such difference is that our model incorporates indirect externalities but Segal (2003) does not. In other words, the disclosure of each type of our producer will not directly affect other types’ payoffs but it can indirectly influence payoffs by shifting consumer beliefs. Segal’s setup only admits direct externalities. Thus, our platform finds it profitable to introduce intermediate plans to shift the beliefs in its favor.

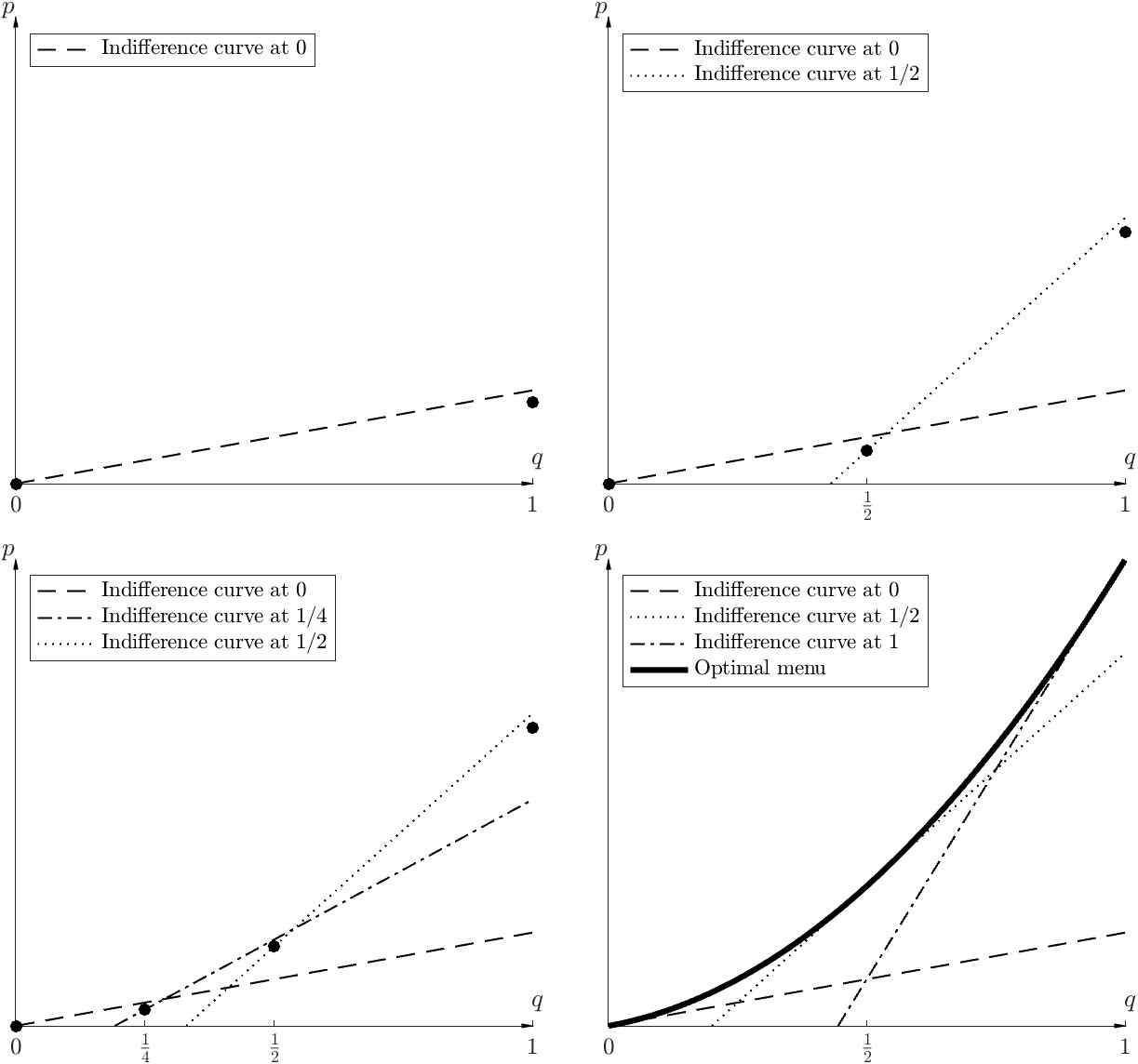

Optimal menu. We demonstrate by construction why the robustly optimal menu can be continuous and represented by a strictly convex price function. The basic idea is to iterate an improvement process like the one from to . Figure 1 illustrates a further improvement upon where a new probability is introduced for a new menu . In each subfigure, the set of black dots composes a menu and each dashed line is the high type’s indifference curve in a hypothetical equilibrium, and in that equilibrium, she wants to deviate to every dot beneath this curve. For example, in the subfigure of , the “Indifference curve at ” in the legend refers to the high type’s indifference curve when the consumer expects the high type chooses half disclosure and the low type has no disclosure, and the full disclosure plan is a profitable deviation in this case because it lies beneath this indifference curve.

(Lower Left), And (Lower Right).

Two features are remarkable: (i) The new menu robustly induces full disclosure via local upward deviation, that is, every partial disclosure plan (including ) is broken by the next plan with a higher probability; (ii) The marginal price increment is upward bounded by the indifference curve of the high type at each plan to be broken. In particular, if and are adjacent plans with , we must have bounded marginal price where is the skepticism belief when the high type chooses . These indifference curve slopes are interpreted as the high type’s marginal benefit of disclosure in different hypothetical equilibria as by disclosing marginally, the high type earns the type and gives up the outside value . As one can imagine, if we continue this improvement process, a continuous menu will emerge as a price function of disclosure probability, denoted by , such that for all . The key to construction is to equate the marginal prices with their upper bounds, namely the slopes of indifference curves. In Figure 1, the lower right subfigure depicts three indifference curves that are tangent to the optimal price function. Formally, the optimal menu is approximated by (with small ):

| (9) | ||||

Notice that in (9), the solution is written without replacing or with their values, and in interpreting our main result later in Section 4.1, we will invoke the form .

The price is strictly convex and induces full disclosure in the unique equilibrium. Plugging in and , we obtain . The platform’s maximal revenue guarantee is thus , strictly lower than full surplus .

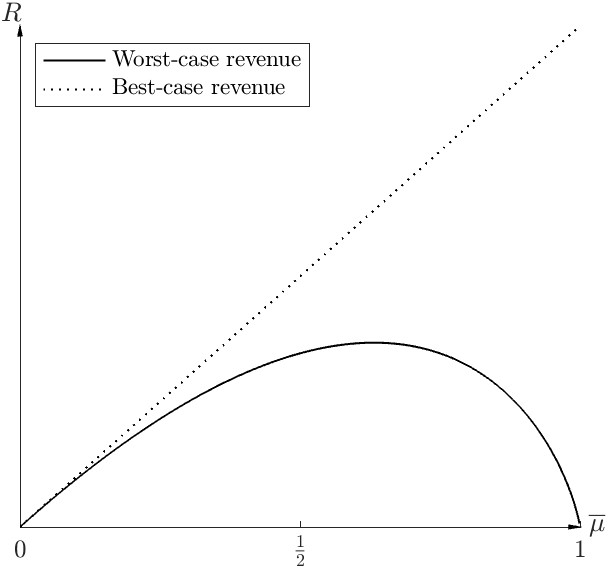

Figure 2 depicts the maximal revenues under our worst-case implementation and the benchmark in Section 2.2 where best-case implementation was considered, and how they vary with the prior. The worst-case revenue curve is intuitive: the platform receives no revenue from quality disclosure when consumers are almost certain about the producer’s quality, whether good or bad. The platform’s profits are highest in the presence of significant uncertainty ( in the middle range).

And Best-Case Implementation

In contrast, the revenue curve for the best-case implementation seems problematic, as there is a sharp discontinuity at . In the corner case where the consumer is certain that the product has high quality, the platform will receive no revenue from the disclosure service, as there is nothing to disclose. However, as long as there is any small doubt so , the platform can extract all the surplus away.

Discussion on bargaining power. The classical approach of assuming the principal can pick the favorite equilibrium is often justified by technique reasons, and in many classical settings, it is innocuous.888For example, in monopoly pricing and Bayesian persuasion. However, when this assumption leads to significant differences, it becomes a questionable modeling choice, especially since it further strengthens the principal’s bargaining power in a context where the platform already has considerable bargaining leverage due to its ability to commit to a take-it-or-leave-it contract. To the extent that the bargaining position between the platform and the producer is perhaps not totally one-sided in reality and the classical principal-agent approach is sometimes a compromise to the lack of an ideal model of bargaining, we think that the worst-case equilibrium selection is an interesting reduce-form approach to give back some bargaining power to the producer.

4 Optimal Menu Profile

In this section, we establish our main result that provides the explicit forms of a robustly optimal menu profile and the maximal revenue guarantee. Section 4.1 states the main result, Theorem 1, followed by a discussion of its interpretation, implications, and proof sketch. Section 4.2 and Section 4.3 elaborate on each proof step and present three useful lemmas, through which we offer insights.

4.1 Main Result

Our main result finds that, to guarantee maximum revenue, the platform wants to robustly induce full disclosure by (i) offering a profile of continuous menus with strictly increasing marginal prices to break any under-advertising equilibrium with a local upward deviation of some type, and (ii) rationalizing the full disclosure choices of different types in a complete divide-and-conquer manner.

Specifically, the following menu profile robustly attains the maximal revenue guarantee:

Theorem 1.

There is a robustly optimal menu profile given by and for all :

| (10) | ||||

Moreover, this profile induces a unique equilibrium where all types except choose the full disclosure plans while chooses zero disclosure. The maximal revenue guarantee is therefore .

To understand (10), recall that the optimal menu for the binary-type example offers the high type a strictly convex price function that breaks every hypothetical equilibrium where the high type discloses only partially by tempting her to deviate locally upward. The multiple-type solution (10) resembles the binary-type solution (9), which gives:

In this case, the high type is , the low type is , and has prior probability .

By comparing (9) and (10), we find that the multiple-type optimal price, for , looks identical to the solution for a binary-type problem where the high type is with prior , and the low type is . This is equivalent to excluding all types higher than from the problem and combining all types lower than to be the low type. Recall that in the binary-type case, the low type stays at zero disclosure, and the optimal menu equalizes the marginal prices to the high type’s marginal benefit of disclosure in different undesirable hypothetical equilibria. This, in (9), refers to for all , where is the skepticism value when the high type discloses with probability (and low type with zero probability). This indicates that the optimal menu profile in Theorem 1 prices each type by also equalizing the marginal prices to the marginal benefit of disclosure in each hypothetical equilibrium where all types higher than fully disclose while all types lower than never disclose. Formally, the skepticism value defined by (4) helps us to write the optimal marginal prices in Theorem 1 as the following, for all and :

| (11) |

Where we use a shorthand notation with ones.

Complete divide-and-conquer. To interpret the price functions in Theorem 1 and their marginal prices given by (11), one can regard them as being constructed along a complete divide-and-conquer path. That is, the platform starts with the worst case where no type ever discloses. First, it increases the highest type ’s disclosure level to 1 while setting the marginal prices of to equal the marginal benefit of disclosure at each level. This delivers (11) for . Next, the platform turns to increasing the second highest type ’s disclosure level and pinning down in a similar way, given that is already fully disclosing, which yields (11) for . By iterating this procedure till the disclosure probability of the second lowest type is depleted, one obtains (11) and thus (10).

In other words, the platform adopts a complete divide-and-conquer strategy which sequentially and robustly induces full disclosure from to . In particular, the platform offers a menu that breaks every hypothetical equilibrium where, regardless of all lower types’ behavior, discloses only partially. Given that full disclosure is the unique credible choice of that can appear in equilibrium, the platform offers a menu that breaks every hypothetical equilibrium where, regardless of all lower types’ behavior, discloses fully while discloses only partially. This procedure continues until full disclosure becomes the unique credible choice of . It stops here because inducing disclosure out of the lowest type is never profitable as she would rather enjoy skepticism than paying anything for exposure.

We keep calling this divide-and-conquer strategy complete since the rationalization procedure above does not proceed in a partial and alternating manner. For example, the platform could have first robustly induced some disclosure level from , then turned to for some level , and come back to again for the remaining probability . In fact, an important lemma discussed later, Lemma 2, implies that every menu profile corresponds to such a partial and alternating divide-and-conquer path such that the points on the path provide upper bounds for all marginal prices induced by the menus. For a loose formalization (which will be clear when we discuss Lemma 2), for all and , there is a probability profile on the path such that its th component and:

| (12) |

Notice that (11) satisfies the complete divide-and-conquer version of (12). We say that a path that satisfies (12) has the property of pointwise upper-boundedness.

The assertion by Theorem 1 that complete divide-and-conquer outperforms all the alternating paths strikingly simplifies the solution form. To compare with literature, Segal (2003) (particularly his Lemma 3) suggests that with increasing externalities among players (or types in our case), alternating divide-and-conquer is usually optimal. In our setting, different types also have increasing externalities in the sense that by first inducing disclosure from high types, the consumer skepticism is worsened so that the other types’ disclosure becomes easier to induce. Moreover, the types are heterogeneous as the disclosure from a high type strikes down consumer skepticism more effectively than the “same” disclosure999By “same”, we mean the ex-ante probabilities of these two types’ disclosure are the same. See Section 4.3 for details. from a low type. Both observations above are consistent with the unraveling insight we gave when we discussed the binary-type example. We will see later how such monotonic-in-type increasing externalities form a crucial force that drives the complete divide-and-conquer solution.

Implications and simple implementation via volume-based pricing. Now, we discuss the implications we can make with Theorem 1 about advertisement pricing. First, despite the platform’s anticipation that the worst-case equilibrium will emerge, it manages to induce full disclosure. Full disclosure also happens in the classic disclosure setting studied by Grossman (1981) and Milgrom (1981) where the producer has free access to disclose its type. Nonetheless, the two settings clearly have different surplus allocations. The full disclosure feature of our solution depends on two things: (i) Advertising is costless, and (ii) the menu profile is type-dependent, so the platform can exploit the type information.

Second, each menu (except for the lowest type) contains a continuum of plans, while only the full disclosure plan is chosen on the equilibrium path whereas most plans serve as baits, or carrots (in the terminology of Ali et al. (2022)) that induce local upward deviations for breaking all the under-advertising hypothetical equilibria. Such “dense” menus are useful in making the consumer believe that an equilibrium with any type partially disclosing cannot exist.

Third, denote the producer surplus conditional on each type by . Proposition 3 displays the main features of the producer’s surplus distribution across types. Since the platform needs to keep compensating the producer for giving up outside values, the surplus can be written as an interal . Moreover, the strategy of complete divide-and-conquer prioritizes attracting higher types into business by offering them better rents. This rent structure emerges even without an adverse selection issue, so it is not a result of incentive compatibility but instead stems from the platform’s optimal order of “conquering”. Namely, to induce disclosure from the highest type first, the platform keeps compensating her for giving up quite high outside values; however, once the highest type’s disclosure is guaranteed, the outside values are struck down, so the compensation to lower types will also be lower.

Proposition 3.

For all , and . Thus, is strictly increasing in types.

However, being offered a higher rent does not mean the type would favor the presence of the platform since Proposition 3 also says that each type is strictly worse off than without the platform. To see this, notice that the upper bound is strictly lower than both the type and the prior mean . These three numbers correspond to the respective surplus levels in three benchmarks: (i) If the platform is restricted to offering only bang-bang disclosure options, ; (ii) If the platform is absent and the producer can self-advertise, ; (iii) If the platform is absent and the producer cannot self-advertise, . Hence, Proposition 3 shows that our platform extracts type-wise strictly higher surplus than in these benchmark setups.

To see Proposition 3, notice that according to (11), the price paid by type can be written as . The type’s rent is therefore net this price, which becomes simply , the skepticism values accumulated along the path on which ’s disclosure is “conquered”. The rents are monotonic in types because the outside value is strictly decreasing along the complete divide-and-conquer path. Furthermore, the outside value starts at the prior mean and eventually decreases to the lowest type. The rent is thus strictly lower than both the prior mean and the type.

One thing the reader might expect is that the price charged from a higher type should also be higher. Nonetheless, this is not true. For a counterexample, imagine three types with the two higher types being very close to each other and the middle type assigned with a very high prior. In this case, the price paid by the middle type will be higher than that of the highest type. The reason is that the type’s rent depends on the ability of her disclosure to strike down consumer skepticism, so a type with higher prior tends to face a lower rent and thus a higher price.

The last implication we make is that the optimal price functions in (10) take a logarithm form, indicating that once strategic uncertainty is accounted for, the platform has less tendency to adopt a linear pricing strategy such as per-click price. Instead, the classic rationale of Butters (1977) and Grossman and Shapiro (1984) for modeling volume-based pricing provides a class of convex price functions, remarkably similar to (10). We hence develop a simple implementation of our solution that (i) avoids the need for the platform to write contracts based on disclosure probability, which is hardly verifiable in practice, and (ii) makes concrete how the continuous menus can be implemented.

Specifically, the platform and the producer contract on the number of ad trials, , and the associated prices . This trial number indicates the volume of ads and is thus the volume-based prices. Given each trial, we assume the consumer sees the information with probability , so with trials, the consumer is informed with probability . In other words, to implement probability , the platform needs to distribute trials. If the platform charges a constant per-trial price, namely is linear in , the relation between price and probability becomes for some . This function resembles our solution (10) except that in the log-function of (10), we have an extra term . Such difference implies that we need nonlinear volume-based prices. For each , the offer exclusive to type is:

| (13) |

This pricing strategy almost produces a constant per-trial price but with a distortion , and becomes linear in as . Moreover, is strictly increasing and strictly concave in volume , and it is bounded by , so the per-trial price is decreasing and it eventually approximates zero. Thus, with such type-dependent volume-based prices, the platform induces a unique equilibrium where all types except for the lowest keep requesting more trials while the lowest never requests anything. Hence, the continuous menus in Theorem 1 are equivalent to diminishing per-trial prices in this sense. Besides, for another simple implementation, see Section 5.3 where we make equivalence between our solution and random pricing.

A sketch of proof. It is convoluted to show Theorem 1 because of the following challenge: In order to robustly induce a probability profile and maximize the revenue guarantee, the platform must “optimally” break every under-advertising hypothetical equilibrium with a deviation of some type; However, it faces two problems: (i) Which type of the producer deviates? and (ii) Which plan does the type deviate to? For binary-type cases, the answer to (i) is clearly the high type since it is never beneficial to offer the low type anything beyond the outside option. With additional arguments, the answer to (ii) is to always use local upward deviations. It is with these prerequisites that we can show (9) is optimal. In contrast, for multiple types, the answers to both (i) and (ii) are ambiguous because the equilibrium-breaking types and directions are now both within the platform’s discretion of choice.

Note that the pointwise upper-boundedness property (12) (see Lemma 2 for formal statement) provides a unifying answer to (ii) that we can always use local upward deviations to break equilibria. Building on this, the strategy of complete divide-and-conquer (see Lemma 3 for formal statement) answers (i) by suggesting the platform always uses the highest type that is not yet fully disclosing to break equilibria. Nonetheless, both claims are difficult to show.

We decompose the proof into four steps where the first three steps are supported by three lemmas, respectively, that will be discussed in Section 4.2 and Section 4.3. The four steps are:

Step 1 - We show that if a menu profile robustly induces a certain probability profile, it also does so if we lower-convexify each menu and delete all the plans that offer probabilities strictly higher than the robustly induced probability. We hence focus on such truncated convexifications.

Step 2 - We develop an algorithm that explicitly finds, for every menu profile, an alternating divide-and-conquer path that has the pointwise upper-boundedness property. To show the existence of such a path, we utilize the fact that every under-advertising probability profile cannot form an equilibrium. Further integration regarding both sides of the inequalities (12) yields an upper bound for the revenue guaranteed by the menu profile which we find the path for.

Step 3 - We show that the complete divide-and-conquer path gives such a revenue upper bound that is no less than any alternating divide-and-conquer path can provide. To show this, we explicitly construct an improvement for every alternating path by exchanging the order of “conquering” to let a high type’s disclosure probability be induced before that of a low type, and by continuing such improvement, we eventually obtain the complete divide-and-conquer path. Thus, the complete divide-and-conquer path determines an upper bound for the maximal revenue guarantee .

Step 4 - We take a sequence of menu profiles , where for all and , where is small. This sequence converges to (10). We verify that every induces full disclosure in the unique equilibrium and gives a revenue that approximates the upper bound for found in Step 3. So, equals this upper bound, and (10) gives a robustly optimal menu profile.

Once three more intermediate results are introduced in the following subsections, we will elaborate on insights for why it is optimal to adopt the complete divide-and-conquer strategy.

4.2 Pointwise Bounded Paths

The first step is to show it is without loss to focus on a subset of menu profiles, in which each profile (i) consists of lower-convexified menus, and (ii) robustly induces the plans with maximal probabilities.

To state the result, we define the price envelope of a menu which is denoted by where is the maximal probability offered in , The price envelope is defined as the highest convex function lying below the menu, given by where is the convex hull of . We further call the graph of price envelope the (lower-)convexification of , denoted as . This implies has nondecreasing left- and right-derivatives at all interior points, denoted by and , respectively. For simplicity, we sometimes denote by the price envelope of menu when a menu profile is specified in the context.

Lemma 1 says that if a menu profile robustly induces some choice profile, it remains a worst-case equilibrium play even if, for every menu, we delete (i) all plans that lie above the convexification, and (ii) all plans that have higher probabilities than the robustly induced one. We call the resulting menu profile defined in Lemma 1 the truncated convexification of , or sometimes convexified menus in short.

Lemma 1.

If a menu profile robustly induces some contingent choices , the menu profile given by for all , also robustly induces .

We prove Lemma 1 by first showing that we can focus on plans lying on the convexifications. To see this, note that for every contingent choice profile , ’s indifference curve is and any plan that lies beneath this curve is a profitable deviation for her. This implies that: (i) reaches optimum if and only if the indifference curve is a subdifferential of the price envelope; (ii) If a profitable deviation exists, we can always find one on the price envelope. Therefore, it suffices to focus on convexifications for both verifying and breaking equilibria.

We then show that deleting high-probability plans is also harmless. This is less obvious since it could be that given , an under-advertising choice profile with is broken by some type wanting to deviate upward to some with , so deleting could cause problems. Let’s suppose this issue indeed creates an under-advertising equilibrium when the menu profile is . Fortunately, this cannot happen. The fact that indifference curves are subdifferentials of price envelopes in equilibrium implies that the indifference curve slopes in the under-advertising equilibrium are lower than in the equilibrium robustly induced by . This implies that if there is a deviation regarding the under-advertising profile given , it must be downward, instead of upward as supposed.

The second step for proving Theorem 1 is to show our central lemma that maps every menu profile to an alternating divide-and-conquer path that offers an upper bound for the revenue guaranteed by the menu profile. We define (and rename) an alternating divide-and-conquer path as follows:

Definition 3.

A nondecreasing alternating path from probability profile to profile with is a sequence of tuples with being either finite or infinite. The path satisfies:

-

1.

and ;

-

2.

For all , and .

In other words, a nondecreasing alternating path specifies the step number and the moving direction for each step , and the probability profile increases only its th component in every step. We also call the direction type and the interval the path stride of step .

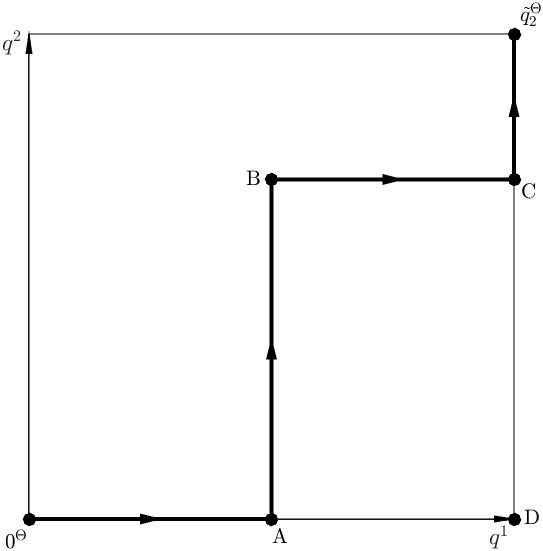

To illustrate what such a path looks like, we consider a three-type example. Let and as the lowest type will never disclose in equilibrium, so it suffices to consider moving in two directions. Figure 3 depicts a possible nondecreasing alternating path from to . In this case, the step number is , and direction types are and . The path is always nondecreasing as it moves by only increasing either or while holding the other directions unchanged.

We now state the following important lemma:

Lemma 2.

If a menu profile robustly induces some probability profile , there exists a nondecreasing alternating path from to some such that is upward bounded by:

| (14) |

In the proof of Lemma 2, we actually show a stronger version of the result which says that there is a pointwise upper bound for every marginal price, in the form of (12). In particular, each step has:

| (15) |

In each step, the path increases the direction type who wants to deviate locally upward at each probability profile in the path stride where the other types’ probabilities stay still. Put differently, the left-hand side and the right-hand side of (15) represent the marginal cost and benefit of disclosure, respectively, for type in the hypothetical equilibrium where the probability profile is . By integrating the left-hand side of (15) along the path weighted by prior probabilities, we can obtain the revenue in the worst-case equilibrium , so the integral with respect to the right-hand side of (15) produces an upper bound for the revenue guaranteed by the given menu profile.

The intuition Lemma 2 conveys is that every menu profile robustly induces a certain disclosure outcome as if it breaks all the under-advertising equilibria in an alternating manner with local upward deviations. Such alternating divide-and-conquer somewhat generalizes the complete divide-and-conquer feature of the robustly optimal menu profile.

Lemma 2, in a way, extends the necessary part of Lemma 3 by Segal (2003) to our setting who borrows the Round-Robin optimization procedure from Topkis (1998), Subsection 4.3.1. The difference, however, is significant. First, as mentioned when we discuss the binary-type example, producer types have indirect externalities, so the optimal menus tend to be continuous and the upper bounds (15) are rather pointwise than piecewise as in Segal’s Lemma 3(c). To see this, notice that an optimal deviation given one belief does not remain optimal with other beliefs, so we differ from Segal by using more than one plan in each path step. Second, Segal (2003) assumed increasing externalities, which our case does not have since if one induces probability out of a type lower than the skepticism value, it makes the other types harder to lure. This fact complicates the proof and invalidates a sufficient counterpart of Segal’s lemma101010For example, one might think that given a nondecreasing alternating path, one can construct a menu profile by setting (15) to equalities and the profile robustly induces the endpoint of the path. This is not true because if a path starts by moving a type that is lower than the prior mean, (15) does not even have meaning..

The proof of Lemma 2 relies on an algorithm that explicitly finds a nondecreasing alternating path recursively. Our algorithm111111See Algorithm 1 in the proof for a formal description. considers the following process: In every step , as long as the path’s current location has not reached the destination , we find a type that wants to deviate upward, namely ; We let be the new direction type and push the path toward this direction until it meets the first point where the upward-deviation inequality above fails; then, the next step begins. In this way, we guarantee (15) holds along the whole path. Notice that the criterion for upward deviation is expressed as a local condition, which is sufficient because the producer’s indifference curve is a straight line and the price envelop is convex.

An illustration is given by Figure 3. The path start at , where there must be some type that wants to deviate upward because, otherwise, forms an under-advertising equilibrium. In Figure 3, the upward-deviating type is . The path moves from to point A by increasing the disclosure probability of , and point A, associated with probability profile , is such that (i) upward deviation vanishes , and (ii) for all lying between and A, upward deviation exists . With a continuity argument, (ii) implies . This along with (i) implies that if is contained in , then by choosing this plan, reaches its optimum given the skepticism belief at point A. indeed must have offered this plan because (ii) implies that has been greater than the skepticism value on the path stride from to A, so further increasing her disclosure level can only worsen skepticism. We then show that if there is no plan offered at A, then the marginal price envelope is locally constant, and (i) and (ii) cannot coexist. Thus, to prevent from forming an under-advertising equilibrium, must want to deviate upward at A.

So, the path moves from A to point B by increasing the disclosure level of , and point B is the first point for ’s upward-deviation inequality to fail. Repeating previous arguments, we show that reaches its optimum there. Since B cannot form an equilibrium, must want to deviate at this point. Suppose wants to deviate downward. We adopt an argument that is somewhat related to Round-Robin (see Segal (2003), Lemma 3) to obtain a contradiction. Notice that ’s willingness to deviate upward at A requires her type to be greater than the skepticism value there, so increasing her disclosure level can only worsen the skepticism further. Hence, if is not afraid of consumer’s skepticism at B and thus wants to deviate downward, then she also cannot be afraid of the skepticism at A, contradicting her optimality at A. This means she must want to deviate upward at B.

So, the path moves from B to point C where depletes its probability. With similar logic, we show must want to deviate upward at C, and thus the path moves up again and ends at its destination .

Two things worth mentioning about the general proof of Lemma 2 are: (i) When the path arrives at a point like C in Figure 3, Lemma 1 which allows us to ignore all plans with excessive probabilities is significant in eliminating the possibility that the hypothetical equilibrium here is broken by the upward deviation of , who has reached her induced probability; (ii) The algorithm must end within countable steps since, otherwise, we can show that the path converges to a point that forms an under-advertising equilibrium using arguments related to those in the above illustration.

4.3 An Upper Bound for Maximal Revenue Guarantee

We have shown that the revenue guarantee of every menu profile is controlled by an upper bound determined by a nondecreasing alternating path. Each such path has a fixed starting point and a flexible endpoint . To further bound the maximal revenue guarantee , we search among all such paths to maximize the path-specific bound (14).

The following result states that the complete divide-and-conquer path is optimal:

Lemma 3.

For the example in Figure 3, the complete divide-and-conquer path corresponds to moving the path first along the bottom edge and then up along the right edge, namely from to point D to .

The insight for the optimality of the complete divide-and-conquer path is related to the intuition we gave in the binary-type example: More disclosure out of high types worsens consumer skepticism, which is also the opportunity cost of nondisclosure, “faster” than inducing disclosure from low types.

To see this formally, consider finding the optimal path while fixing the endpoint to be the full disclosure121212In the proof of Lemma 3, we show that the optimal endpoint can be anything of form with , so it is without loss to set a different full disclosure profile here than in the lemma. profile . We use a quantile to parameterize each path . That is, for every , find the step such that:

| (17) |

Let vary with as above, and redenote the path by:

| (18) |

In other words, denotes the total ex-ante probability that has already been robustly induced along the path. represents the path step in which is reached, and marks the position by which the path has induced total probability . The bound (14) can be rewritten as:

| (19) | ||||

We thus decompose it into two simple parts, and . Only the latter is path-specific and determined by how consumer skepticism changes along the path. This new form expresses the previous insight formally: No matter whether a type is high or low, its disclosure will be induced sooner or later, which results in the non-path-specific constant ; An optimal path constructs a mapping that drives the skepticism value down as “fast” as possible to minimize the total compensation to the producer for giving up outside values along the path, which equals ; The most effective strategy is to prioritize the highest type whose probability has not yet been depleted.

The proof of Lemma 3 follows the same logic. In particular, for every path that is not complete divide-and-conquer, we can always find two consecutive steps where the direction type of the first step is lower than that of the second step. We show that by exchanging the order of these steps, the path ends up with a higher value of (14). All paths can be improved with a sequence of such exchanges until they become (or approximate) complete divide-and-conquer.

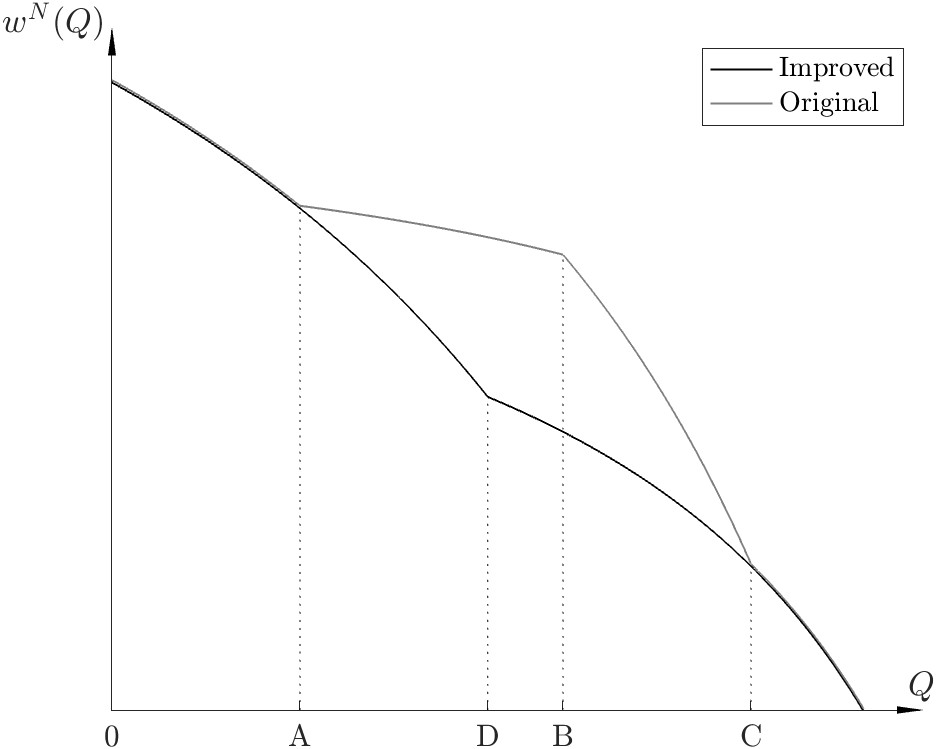

Again, we use Figure 3 as an illustration. The plotted path can be improved by exchanging the moving directions of its second and third steps, which leads to the complete divide-and-conquer path. To exhibit the improvement graphically, for every path , define its quantile-skepticism value . Then, (19) says that a better path must yield a smaller integral , namely a smaller area below its quantile-skepticism value. Figure 4 depicts the quantile-skepticism values associated with the original path and the improved path in Figure 3 that we described. We mark in Figure 4 the correspondences of points A, B, C, and D. The original path moves along A-B-C whereas the improved path passes A-D-C.

As one can see in Figure 4, the quantile-skepticism value of the improved path is uniformly no greater than that of the original path with the middle part from A to C being strictly lower. We have segments satisfying AD=BC and AB=DC, meaning the exchange of two steps does not affect the total probabilities induced out of each type. Nonetheless, the skepticism value drops faster on AD than on AB because the improved path induces the highest type’s disclosure first. Also, the skepticism value drops faster on DC than on AB, both of which correspond to the revelation of the lower type. This feature results from the fact that the types have increasing externalities, that is to say, more disclosure from a higher type makes it easier to induce disclosure from a lower type.

With this optimal path, we obtain an upper bound (16) for . By comparing (16) and (10), one can see that this bound is exactly the full disclosure revenue given by the solution claimed in Theorem 1. Consequently, the only thing left is to show that this claimed menu profile indeed guarantees full disclosure in the worst-case equilibrium, which we relegate to the Appendix.

5 Extensions

We now discuss four extensions. Section 5.1 shows that the unique equilibrium induced by the robustly optimal menu profile can also be solved with iterated deletion of strictly dominated strategies. Thus, our solution is robust under weaker assumptions on player behavior. Section 5.2 analyzes the platform that can jointly design the information structure and the menu profile. We show that the platform wants to perfectly reveal the types, based on which we compare our model with that of Ali et al. (2022). Section 5.3 allows the platform to offer random menus (in the sense of Halac et al. (2021)). We show that it suffices to consider nonrandom menus for achieving maximal revenue guarantee, whereas a class of random menus is equivalent to the robustly optimal menu profile and takes the form of bang-bang menus with price dispersion. Section 5.4 shows that the two main features of our solution are preserved even with costly advertising.

5.1 Rationalizable Outcomes

Traditionally, the term strategic uncertainty may refer to multiple equilibria as well as multiple rationalizable outcomes. This subsection shows that choosing different concepts does not matter: The menu profile in Theorem 1 remains robustly optimal even if the platform seeks to maximize revenue guarantee among all rationalizable outcomes.

In Section 2.1, we show that the disclosure game induced by a menu profile simply consists of the producer’s contingent choices of ad plans and the consumer’s skepticism belief . The implicit modelling of the consumer’s strategy is that the consumer decides whether to purchase the product or not, when facing the take-or-leave-it offer from the producer. Thus, the consumer’s formal strategy is a mapping , where means the consumer purchases the product. In any equilibrium of the producer-consumer game, the consumer’s strategy takes the following form:

Here, is the consumer’s skepticism value defined by (4).131313Here we assume the consumer breaks ties in favor of the producer to simplify the exposition. This does not matter as the producer can break the tie with perturbation. Note that this class of strategy is parameterized by a single variable , so we denote this strategy as .