Bounding Causal Effects with Leaky Instruments

Abstract

Instrumental variables (IVs) are a popular and powerful tool for estimating causal effects in the presence of unobserved confounding. However, classical approaches rely on strong assumptions such as the exclusion criterion, which states that instrumental effects must be entirely mediated by treatments. This assumption often fails in practice. When IV methods are improperly applied to data that do not meet the exclusion criterion, estimated causal effects may be badly biased. In this work, we propose a novel solution that provides partial identification in linear models given a set of leaky instruments, which are allowed to violate the exclusion criterion to some limited degree. We derive a convex optimization objective that provides provably sharp bounds on the average treatment effect under some common forms of information leakage, and implement inference procedures to quantify the uncertainty of resulting estimates. We demonstrate our method in a set of experiments with simulated data, where it performs favorably against the state of the art.

1 Introduction

Estimating causal effects from observational data can be challenging when treatments are not randomly assigned. While the task is doable under some structural assumptions (Shpitser and Pearl 2008), most methods require access to data on potential confounders. This access cannot be generally guaranteed, since confounding variables may be unknown or difficult to measure. One common strategy for identifying causal effects under unobserved confounding relies on instrumental variables (IVs), which have a direct effect on the treatment but only an indirect effect on outcomes. For instance, single nucleotide polymorphisms (SNPs) often serve as IVs in genetic epidemiology, where they may be used to investigate the impact of phenotypes (e.g., cholesterol levels) on health outcomes (e.g., cancer) in Mendelian randomization studies (Didelez and Sheehan 2007).

The IV model relies on three core conditions, formally defined in Sect. 2. Informally, we may describe IVs as variables that are (A1) relevant, i.e. associated with the treatment; (A2) unconfounded, i.e. independent of common causes between treatment and outcome; and (A3) exclusive, i.e. only affect outcomes through the treatment. Under some restrictions on structural equations, IVs can be used to recover causal effects despite the presence of unobserved confounding. Popular IV methods include two-stage least squares (Angrist and Imbens 1995), as well as more recent nonlinear extensions based on deep learning (Hartford et al. 2017, Xu et al. 2021), kernel regression (Singh et al. 2019, Muandet et al. 2020, Saengkyongam et al. 2022), and generalized method of moments (Bennett et al. 2019).

Of the three core conditions that characterize the IV setup, only (A1) can be immediately evaluated via observables. (A2) fails if the latent confounder between treatment and outcome is also a parent of some proposed IV(s). To continue with the Mendelian randomization example, this issue can arise when nearby variants are correlated, a phenomenon known as linkage disequilibrium (Reich et al. 2001). (A3) fails if the proposed IV is a direct cause of the outcome (see Fig. 1). This can happen with complex traits in genetics, where one gene affects multiple seemingly unrelated systems through a process called horizontal pleiotropy (Solovieff et al. 2013). If IV methods are naïvely applied in either case, resulting inferences can be severely biased (VanderWeele et al. 2014).

Since valid IVs may be impossible to identify a priori, several authors in recent years have proposed methods to estimate causal effects given just a set of candidate IVs (see Sect. 5). Details vary, but the goal is almost always to recover point estimates for the average treatment effect (ATE), possibly with associated confidence or credible intervals. We set a strictly more general target, relaxing (A3) to recover nontrivial bounds on this parameter, i.e. to partially identify the ATE. There is a long tradition of analytic and Bayesian methods for partial identification in IV models (Manski 1990, Chickering and Pearl 1996, Balke and Pearl 1997), as well as more recent works that exploit the flexibility of stochastic gradient descent (Kallus and Zhou 2020, Kilbertus et al. 2020, Hu et al. 2021). Generally, a set of valid IVs is presumed—but some authors have considered the case where a single instrument is allowed to have a bounded effect on the outcome (Ramsahai 2012, Conley et al. 2012, Silva and Evans 2016).

We propose a novel procedure for bounding causal effects in settings where the exclusion criterion (A3) may not hold. Our method takes a set of leaky instruments, which are permitted to violate (A3) to some limited degree, and uses them to minimize confounding effects on the causal pathway of interest. Focusing on linear structural equation models (SEMs), we derive partial identifiability conditions for the ATE with access to leaky instruments, and use them to formulate a convex optimization objective. Resulting bounds are provably sharp—that is, they cannot be improved without further assumptions—and practically useful, providing causal information in many settings where classical methods fail. Finally, we propose a statistical test for exclusion and implement a generic bootstrapping procedure with coverage guarantees for estimated bounds.

The rest of this paper is structured as follows. We introduce the leaky IV model in Sect. 2. We present formal results in Sect. 3 and experimental results in Sect. 4. Following a review of related work in Sect. 5, we discuss limitations and generalizations of our method in Sect. 6. We conclude in Sect. 7 with a summary and future directions.

2 Problem Setup

Notation.

We denote individual variables with capital italic letters (e.g., ) and bundled sets of variables in boldface capital italics (e.g., ). We use square brackets to indicate set enumeration, e.g. . Parameters are symbolized as Greek letters, with boldface for vectors (e.g., ) and boldface capitals for matrices (e.g., ).

Standard notation for (co)variances can sometimes be confusing. Here we use the capital for any such quadratic expectation, regardless of whether it is a scalar, vector, or matrix—the subscripts will contain all the necessary information as to its dimensions. For instance, we write for (as opposed to ) and for (as opposed to ). As a convenient byproduct, the notation generalizes more naturally to vector-valued variables.

The Leaky IV Setting.

Consider a linear SEM with treatment , outcome , and a set of candidate IVs . Assume that all variables have mean 0 and finite variance. Data are generated according to the following process (see Fig. 2):

| (1) | ||||

| (2) | ||||

| (3) |

where and are linear weights; and are residuals with mean , standard deviation , and correlation . This latter parameter quantifies the magnitude and direction of unobserved confounding. To better interpret results, we assume all ’s are on roughly the same scale (e.g., standardized to unit variance). We make no further assumptions about the distribution of . Our goal is to bound , which denotes the average treatment effect (ATE) of on .

In the classical nonparametric IV setting, we have a set of unobserved confounders with direct effects on both and . Then is a set of valid instruments if and only if the following conditions are satisfied:111The “exogeneity” assumption in econometrics is sometimes equated with (A2), and sometimes with the conjunction of (A2) and (A3) (see, e.g., (Wooldridge 2019, Ch. 15)). We avoid all talk of exogeneity to avoid confusion.

-

(A1)

Relevance:

-

(A2)

No confounding:

-

(A3)

Exclusion criterion: .

Adapting these assumptions to a linear SEM, we posit that is a parent of both noise variables satisfying and equate (conditional) independence with (conditional) covariance of zero. Under these conditions, we may compute treatment effects via two-stage least squares (2SLS) (Bowden and Turkington 1984). For this procedure, we solve Eq. 1 with ordinary least squares (OLS) and substitute fitted values from this model for in Eq. 2, which is in turn solved via OLS. The resulting is our ATE estimate. Note that (A3) implies that , since in this case each receives zero weight in Eq. 2.

We relax the exclusion criterion and consider two modified variants using scalar or vector-valued thresholds.

-

(A)

Scalar -exclusion:

-

(A)

Vector -exclusion: .

That is, we allow to have some direct effect on but restrict this influence either by placing an upper bound on the -norm of the coefficients (scalar-valued ) or by placing separate thresholds on the magnitude of each individual coefficient (vector-valued ). We derive sharp ATE bounds for both cases, as well as a closed form solution under (A) when .

We call variables that satisfy (A1), (A2), and either form of -exclusion leaky instruments. These features are technically observed confounders (at least those with nonzero coefficients). Were it not for the unobserved confounding induced by , causal effects could be calculated by integrating over , as in the backdoor adjustment (Pearl 2009, Ch. 3.3). Unfortunately, this option is unavailable when . By exploiting known leakage threshold(s), however, we show how to recover sharp bounds on the ATE.

Unlike other methods designed to accommodate potential violations of the exclusion criterion (see Sect. 5), we do not assume that some proportion of candidate IVs are valid, or that biases introduced by direct links from to cancel out. On the contrary, we explicitly allow for a dense set of nonzero weights, provided they satisfy some form of -exclusion. As our experiments below demonstrate, this method naturally accommodates sparse vectors without presuming them upfront.

3 Theory

In this section, we show how to partially identify the ATE under bounded violations of the exclusion criterion and propose methods for statistical inference.

3.1 Scalar -exclusion

We begin with a scalar threshold on information leakage from to . As a first pass, we may formalize our objective as follows:

| s.t. | |||

where is the observational covariance matrix of and is the model covariance matrix implied by Eqs. 1, 2 and 3.

Though technically correct, this formulation is unnecessarily complex. It suggests a potentially high-dimensional constrained optimization problem that is not obviously amenable to polynomial programming techniques. To simplify it, we provisionally assume access to the population covariance matrix . (We discuss methods for estimating these parameters in Sect. 3.3.) This allows us to solve directly for and :

With these parameters fixed, the remaining coefficients are rendered deterministic functions of , with some special care for the non-negativity constraint on . To see this, it helps to define the scalars:

These terms correspond, respectively, to the conditional variance of given (), the conditional covariance of and given (), and the conditional variance of given (). Thus, by the Cauchy-Schwarz inequality, . With these definitions in hand, we are now ready to characterize the relationship between and . (See Appx. A for all proofs.)

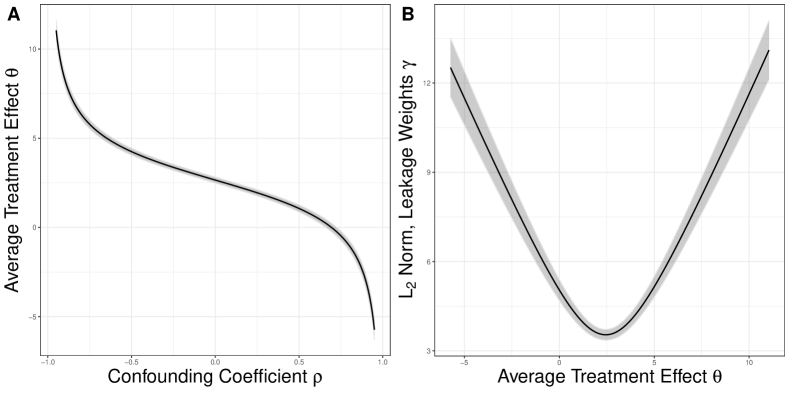

Lemma 1 (ATE as a function of confounding).

There is a bijective, strictly decreasing function that maps values of the confounding coefficient to the ATE :

This function takes the shape of a rotated sigmoid (see Fig. 3A). Note that when , there is no unobserved confounding and can simply be estimated by OLS (if ) or backdoor adjustment on (if ).

Because strong confounding induces extreme values of , more informative bounds on the ATE can be derived if subject matter knowledge allows us to truncate the range of . This is precisely what (A) achieves, although the exact form of this truncation depends on our choice of norm. To see how -exclusion restricts ’s range, we must spell out the relationship between the ATE and leaky weights .

Lemma 2 (Leakage as a function of ATE).

There exists a surjective function that maps values of the ATE to the norm of the leakage weights :

where represents the expected weights of an OLS regression of on .

For the special case of , this function is quadratic (see Fig. 3B). Recall that the norm is convex for all and strictly convex for . Though everywhere differentiable for , the norm may be non-differentiable at countably many points for .

The leakage threshold defines a feasible region of possible models. While we presume that this parameter is provided upfront (more on this in Sect. 6), it cannot be made arbitrarily small in the leaky IV setting. Specifically, the lower bound corresponds to particular values of and .

Lemma 3 (Minimum leakage as a function of ATE).

The minimum degree of leakage consistent with the data can be obtained by solving the following linear regression task in space:

In the special case of , the optimum is given by the standard OLS estimator . Though closed form solutions are not available for arbitrary —even in the well-studied case of (Pollard 1991, Portnoy and Koenker 1997, Chen et al. 2008)—the value is easily computed via numerical methods. Note that is unique for any strictly convex norm, but may form a compact interval for .

Next, we find the corresponding value(s) of .

Lemma 4 (Minimum leakage as a function of confounding).

Define , such that maps vales of to . For any (either a unique solution or any point on the compact interval of solutions), achieves its minimum at:

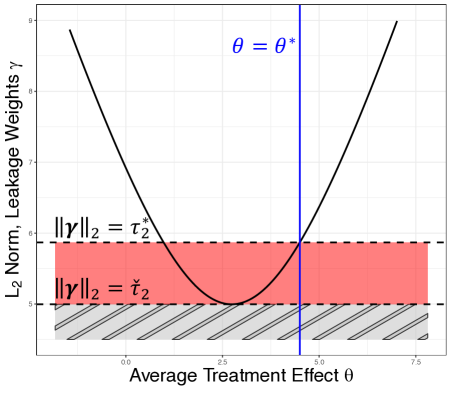

Lemmas 3 and 4 provide an essential criterion for partial identification in the leaky IV model. Define . (Observe that this value is unique even when and are not.) Let denote the true ATE, with corresponding leakage weights and oracle threshold , so named because it quantifies the precise (and unidentifiable) amount of information leakage from to in the true data generating process. These minimum and oracle thresholds fully characterize identifiability conditions in the leaky IV model.

Theorem 1 (Identifiability).

The three-partition of threshold space implied by Thm. 1 is visualized in Fig. 4 for , where we see how bounds go from nonexistent (grey striped region) to small but erroneous (red shaded region), only becoming valid above the oracle threshold . Note that the perpendicular lines and intersect at a point on the leakage curve. This illustrates that valid bounds in the leaky IV model are not generally symmetric about . In fact, for and , the true ATE will coincide with one extremum of the partial identification interval at .

The identifiability conditions of Thm. 1 have an immediate consequence for the classic linear IV model, which is a special case of our leaky IV model with .

Corollary 1.1.

Under the assumptions of Thm. 1, the exclusion criterion (A3) holds iff , in which case .

As we will see in the sequel, this constraint has falsifiable consequences that can motivate the use of the leaky IV approach in practice.

We now reformulate our optimization task:

This is a straightforward one-dimensional objective where all structural constraints have been absorbed into a single function . We now have all the ingredients in place to state our main result.

Theorem 2 (ATE bounds).

Assume the conditions of Thm. 1 hold for some . Then for any (either a unique solution or any point on the compact interval of solutions), there exist unique min/max values of the confounding coefficient consistent with the posited information leakage:

Plugging these values into produces valid and sharp ATE bounds:

Analytic solutions are generally intractable for . However, Thm. 2 guarantees the existence and uniqueness of valid, sharp ATE bounds in the leaky IV model for any . These values can be readily computed with numerical methods, e.g. linear programming techniques (Bertsimas and Tsitsiklis 1997). For the case, we derive the following solution in closed form.

Corollary 2.1.

Under the assumptions of Thm. 2 with , min/max ATE values are given by:

3.2 Vector -exclusion

Our scalar -exclusion criterion is somewhat crude, as it applies a single threshold on a summary statistic of all weights. In many cases, however, background knowledge may license a more fine-grained approach that applies separate thresholds either to individual candidate instruments or groups thereof. For instance, in a Mendelian randomization study, we may partition SNPs by chromosome, exploiting biological knowledge to permit more or less leakage as we move across the genome. Alternatively, we may impose the restriction that our variables should be more “relevant” than “leaky”, with each coefficient exceeding the corresponding in absolute value.

These considerations inspire a more heterogeneous relaxation of the exclusion criterion characterized by (A), which we refer to as vector -exclusion. Fortunately, the solution in this case follows naturally from our previous analysis. Suppose that all thresholds are strictly positive, i.e. that . Then we simply perform a linear transformation of all candidate instruments, scaling them by their respective leakage thresholds to create modified variables . Let denote an augmented threshold vector of length , with dummy entries for and . Then, we define a square transformation matrix with entries and update our covariance parameters:

where denotes the Hadamard product (i.e., entrywise multiplication). Plugging this matrix into the equations of Sect. 3.1 produces transformed linear weights . Vector -exclusion can now be rewritten as:

-

(A)

Vector -exclusion: .

All previous results go through just the same, including identifiability conditions (Thm. 1) and optimal ATE bounds (Thm. 2).

This strategy will need to be modified if we wish to impose for some —i.e., to treat some variable(s) as valid IVs that satisfy the classical exclusion criterion. Let pick out all and only those features such that , with complementary subset . Then for each , we set the corresponding entry in to 1 in our construction of the transition matrix to avoid division by zero, and update the formula for to reflect the reduced degrees of freedom:

for all . We modify the definitions of , and to restrict their range to just those . Now (A) applies and produces sharp bounds, as desired.

3.3 Inference

Thm. 2 provides an exact solution with the population covariance matrix . In practice, of course, all parameters must be estimated from finite data. We generally take the sample covariance matrix as our plug-in estimator, but many alternatives are possible. Numerous Bayesian (Leonard and Hsu 1992, Daniels and Kass 1999, Gelman et al. 2014, Ch. 3.6) and penalized likelihood (Schäfer and Strimmer 2005, Warton 2008, Won et al. 2012) methods have been proposed for this task, or the closely related task of estimating a regularized precision matrix (Friedman et al. 2007, Cai et al. 2011, Mazumder and Hastie 2012). Several of these options are implemented in our accompanying software package. These alternatives may be especially attractive in high-dimensional settings with a large number of leaky IVs to ensure a positive definite .

We use a variety of estimators in our experiments below and augment the procedure with inference techniques. First, we describe a parametric test of the exclusion criterion, as foreshadowed by Corollary 1.1. In the linear IV model with , it is well known (Kuroki and Cai 2005, Chen et al. 2014, Silva and Shimizu 2017) that exclusion imposes a set of so-called tetrad constraints on covariance parameters of the form:

If this holds for all nonidentical pairs of candidate instruments , then vectors are parallel and information leakage goes to zero. Define the matrix . Then our test statistic is and our null hypothesis is , which is necessary and sufficient for .

We propose to test via Monte Carlo, estimating on the original data and creating a null covariance matrix by replacing with . We assume that samples are distributed according to some , where denotes a family of distributions parameterized by a covariance matrix —obvious examples include multivariate Gaussian and -distributions, although alternatives such as multivariate binomial or Poisson distributions are also viable (Krummenauer 1998, Jiang et al. 2021). So long as we can sample data under fixed values of , we can perform the following test.

Theorem 3 (Exclusion test).

Let be a dataset generated according to the conditions of Thm. 1, with , , and sample estimate . Construct a null covariance matrix as detailed above. Draw synthetic datasets of size , , and record the test statistic for all . Then as , the following is an asymptotically valid -value against :

Thm. 3 describes a frequentist method for testing the exclusion criterion in linear IV models. Sufficiently small values of can motivate a leaky approach, as 2SLS results in biased ATE estimates when (A3) fails. Note that is a necessary but insufficient condition for exclusion, which additionally requires that . A minimum possible leakage of zero provides no evidence that the true leakage is in fact zero.

Next, we introduce a nonparametric bootstrapping procedure (Efron 1979) to quantify the uncertainty of ATE bounds. Specifically, we draw many datasets of size by sampling with replacement from the input data and estimate the covariance matrix for each . Our target parameters are , i.e. the bounds we would expect from a partial identification oracle (henceforth a -oracle) with knowledge of the population covariance matrix for observed variables . Note that even with access to the true , and remain unidentifiable, and so we distinguish between -oracles and oracles tout court, who are additionally omniscient with respect to latent parameters and therefore able to point identify the ATE. By contrast, with , a -oracle will produce invalid bounds that lie in the error region of Fig. 4 (see Thm. 1).

Since depends on the data, it is possible that some bootstraps may violate the partial identifiability criterion , especially if the sample size is small and/or the selected threshold is close to the true leakage minimum as determined by a -oracle. Our estimator is undefined when the feasible region is empty, so we discard any offending bootstraps. As can be estimated on the full dataset upfront, this issue may be mitigated by selecting a threshold sufficiently high above this value. The procedure comes with the following coverage guarantee.

Theorem 4 (Coverage).

Let be a dataset generated according to the conditions of Thm. 1. Draw samples with replacement from , subject to for all . For a given and level , we construct the confidence interval as follows. Let be the th smallest value of the bootstrap distribution for , with . Let be the th smallest value of the same set, with . Then as , we have:

We can smooth the bootstraps with kernel density estimation (see Sect. 4) or use a Bayesian bootstrap to get an approximate posterior distribution (Rubin 1981). Either way, Thm. 4 provides a template for testing claims about whether, for instance, zero lies above or below the partial identification interval with high probability.

4 Experiments

For full details of all simulation experiments, see Appx. B. Code for reproducing all results and figures can be found on our dedicated GitHub repository.222https://github.com/dswatson/leakyIV. In this section, we use throughout and estimate all covariance parameters via maximum likelihood.

For our benchmark experiments, we generate data according to Eqs. 1-3 with the following process:

and fixed . The scaling factor and residual variance parameters are chosen to ensure that the signal-to-noise ratio (SNR) of Eqs. 1 and 2 are fixed at the desired level (for details, see Appx. B.2). We simulate data from the leaky IV model under a range of hyperparameters:

-

•

Dimensionality is selected from .

-

•

The covariance matrix is either diagonal or Toeplitz with autocorrelation . In either case, we set marginal variance to for each .

-

•

The confounding coefficient is selected from .

-

•

The SNR for is selected from .

-

•

The SNR for is selected from .

Taking the Cartesian product of all these hyperparameters generates a grid of 684 unique simulation configurations. We hold the sparsity of fixed at and set the true ATE to 1 across all experiments.

Point Estimators.

We present the mean and standard deviation of ATE estimates for a range of methods, computed across 50 runs of . For our own own approach, LeakyIV, we set and shade the interval between our mean estimates for . We benchmark against two classic methods—the backdoor adjustment and 2SLS—as an illustrative baseline. We also compare our results to two methods designed for causal inference with some invalid instruments: sisVIVE, which performs implicit feature selection via an penalty on the candidate IVs (Kang et al. 2016); and mode-based estimation (MBE), which treats invalid instruments as outliers that can be ignored using robust inference techniques (Hartwig et al. 2017). We refer readers to the original papers for details on each.

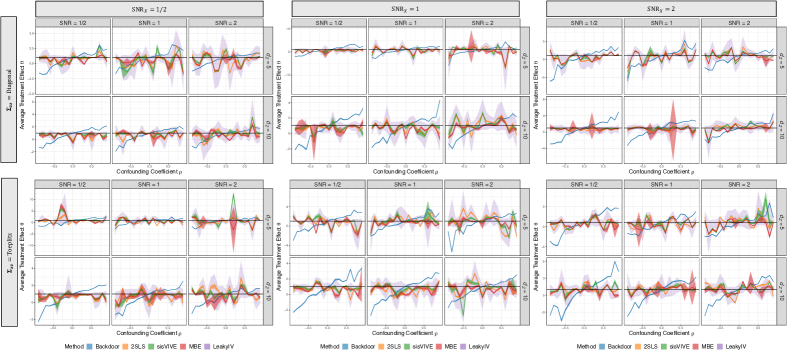

Results for = Toeplitz, are presented in Fig. 5. (Results are broadly similar for alternative simulations; see Appx. B.1.) We find that the backdoor adjustment is systematically biased downward for and upward for , exactly as theory predicts. In most cases, confounding effects on either end of the -axis are sufficiently strong to send the curve beyond the limits of our estimated partial identification interval. Alternative methods designed for the IV setting fare better, but still behave somewhat erratically. MBE in particular appears prone to occasional bursts of uncertainty, especially under extreme confounding.

By contrast, our bounds contain the true ATE in 683 out of 684 settings, or 99.85% of the time. Moreover, they are generally informative, capturing the true direction of causal effects in over half of all trials despite a relatively weak signal from the exposure . Our bounds are clearly correlated with results from IV point estimators, but whereas competitors tend to overstate their confidence—bouncing between positive and negative causal effects multiple times in each panel—our bounds almost never stray so far as to miss the true ATE.

Bayesian Methods.

An alternative family of methods for modeling latent parameters in the IV setting is based on Bayesian inference (Shapland et al. 2019, Bucur et al. 2020, Gkatzionis et al. 2021). The goal in this approach is to estimate a posterior distribution for , with partial identification bounds given by the upper and lower -quantiles of the credible interval. Rather than compare against some off the shelf method that does not explicitly encode our -exclusion criterion, we design a Markov chain Monte Carlo (MCMC) sampler to model causal effects in the leaky IV setting (for details, see Appx. B.3). Due to the computational demands of MCMC sampling, we focus on the case where is diagonal, and the SNR for both and is 2, varying only across a range of six possible values.

Results are presented in Fig. 6, featuring 2000 draws from the estimated posterior distribution for . The blue line denotes the true ATE , while red dashed lines indicate bounds estimated by LeakyIV. We observe that even with uninformative priors on all linear parameters and just observations, the posterior tends to concentrate around a biased estimate, occasionally even placing some of the density outside our partial identification interval. Bayesian methods struggle in this setting because every solution in the feasible region has the same likelihood, which makes posteriors especially sensitive to the choice of prior distribution. Moreover, these methods do not decouple bounds on the causal parameter from the causal parameter itself. Any claims that posterior quantiles can be interpreted as “bounds” are either (i) a direct consequence of the prior; or (ii) heuristics that may be impossible to interpret outside the infinite data limit with an uninformative prior. Of course, this defeats the purpose of having priors on parameters in the first place.

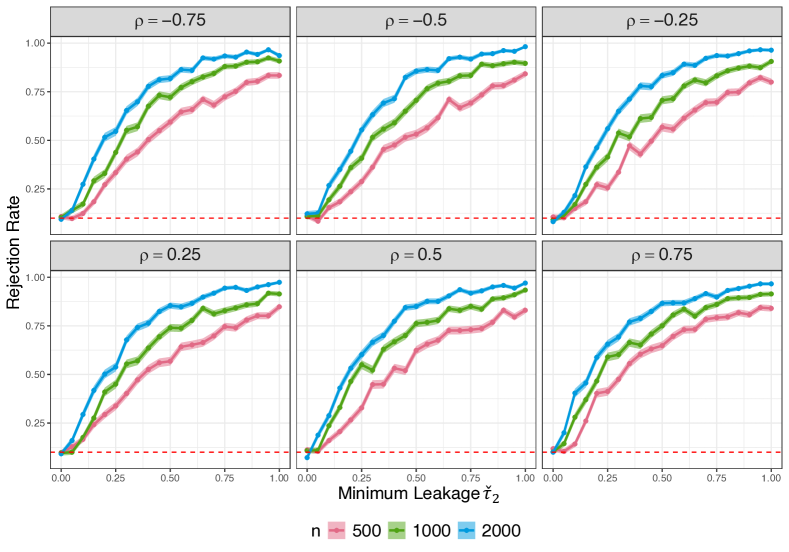

Power.

We run a series of power simulations to evaluate the sensitivity of our Monte Carlo exclusion test. With , diagonal , and fixed for both and , we vary the sample size and effect size under six values of confounding . We compute -values using replicates and reject at level . Empirical rejection rates are recorded over 500 runs (see Fig. 7). We find that type I error is controlled at the target level across all simulations, while power steadily increases with greater effect size, as expected. At , we attain 95% power in all settings.

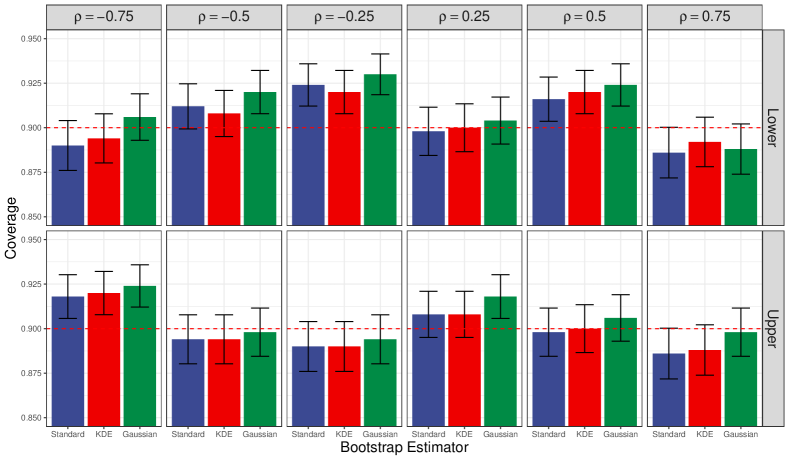

Coverage.

Under the simulation settings of the Bayesian benchmark experiment, we evaluate nominal coverage using three bootstrap variants: the standard empirical distribution, a smoothed kernel estimate, and a Gaussian approximation. We generate 500 unique datasets for each setting and run 2000 bootstraps with fixed level . Results are presented in Fig. 8. Empirical coverage is very close to the nominal 90% target in all settings, with a minimum of 0.886. The target level is always within a standard error of the mean across all trials. Though performance is similar for all three estimators, the Gaussian approximation appears slightly more conservative on average.

5 Related Work

Violations of the exclusion restriction are well-documented in genetics (Hemani et al. 2018) and econometrics (Berkowitz et al. 2008). One strategy for estimating causal effects in such settings is to permit a large number of potentially invalid instruments under the assumption that their average bias will tend to zero in the limit (Bowden et al. 2015, Kolesár et al. 2015). With weak monotonicity constraints, these approaches can also provide nonparametric bounds on local average treatment effects (Flores and Flores-Lagunes 2013).

Another family of methods starts from the assumption that some proportion of candidate instruments are valid and uses statistical procedures to focus on just those variables that satisfy (A1)-(A3). This can be achieved, for instance, via goodness of fit tests (Chu et al. 2001); -penalized regression for feature selection (Kang et al. 2016, Guo et al. 2018, Windmeijer et al. 2019); independence tests for collider bias (Kang et al. 2020); or modal validity assumptions in linear (Hartwig et al. 2017) and nonlinear (Hartford et al. 2021) IV models. Alternatively, data from multiple instruments can be pooled into a single variable using dimensionality reduction techniques (Kuang et al. 2020).

There is a substantial literature on Bayesian approaches to causal inference in IV settings. Lenkoski et al. (2014) use Bayesian model averaging to select IVs based on the strength of their association with the treatment, as codified by the relevance criterion (A1). Shapland et al. (2019) extend this method to account for linkage disequilibrium in Mendelian randomization experiments, which violate the no confounding condition (A2). More recently, several authors have proposed spike-and-slab priors to select genetic variants in the face of horizontal pleiotropy (Bucur et al. 2020, Gkatzionis et al. 2021), thereby addressing (A3).

Conley et al. (2012) propose ATE bounding methods given various kinds of prior information on leaky coefficients , including a range restriction and a (non-uniform) prior distribution. For the former, they return a union of confidence intervals resulting from a grid of possible values for . This method scales exponentially with and is potentially conservative as grid resolution grows finer. By contrast, our convex optimization approach is an efficient one-shot procedure that provides provably sharp bounds—in closed form, for the case. Their Bayesian proposal is similar to the method we compare against in Fig. 6.

The literature on tetrad constraints in linear SEMs goes back over a century (Spearman 1904), although the method was revived and refined following the publication of Spirtes et al. (2000)’s tetrad representation theorem. Our exclusion test builds on generalized results developed by numerous authors (Shafer et al. 1995, Sullivant et al. 2010, Spirtes 2013), although we are to our knowledge the first to propose a Monte Carlo inference procedure for testing such claims.

Partial identification intervals for counterfactual quantities can be computed exactly for discrete variables by formulating the problem as a polynomial program (Zhang et al. 2022, Duarte et al. 2023). Though continuous data can always in principle be discretized with arbitrary precision, this quickly becomes intractable in the response function framework, as it leads to an exponential explosion of parameters. Some continuous alternatives have been proposed with applications to IV models (Kilbertus et al. 2020, Hu et al. 2021, Padh et al. 2023). However, the neural architectures underlying these models can be notoriously unstable, and are ill-suited to the linear SEM setting, which is standard in much biological and econometric research.

6 Discussion

We have limited our analysis in this paper to linear SEMs. Though such linear models remain popular in many applications, it is well known that real-world systems often involve nonlinear dependencies between variables. To generalize the concept of leaky instruments, we could reformulate -exclusion to place an upper bound on the conditional mutual information:

-

(A)

Generalized -Exclusion: .

Alternatively, (A) could place a bound on the gap between and using some appropriate measure such as the Wasserstein distance or the KL-divergence. For binary , Ramsahai (2012) and Silva and Evans (2016) represented this as a difference in expectations . Extensions to vector-valued variants are conceptually straightforward. Estimating these quantities is more difficult than computing linear coefficients, but could help extend our approach to a wider class of data generating processes.

We have assumed in this paper that treatment effects are homogeneous throughout the population. However, a great deal of recent literature in causal machine learning has focused on heterogeneous treatment effects, where potential outcomes are presumed to vary as a function of pre-treatment covariates (Chernozhukov et al. 2018, Künzel et al. 2019, Nie and Wager 2021). Some authors have brought this framework into IV models, showing that tighter ATE bounds are possible with the help of observed confounders (Cai et al. 2007, Hartford et al. 2021, Levis et al. 2023). Future work will consider conditional bounding methods, where extrema for may depend on instruments and/or other features causally antecedent to .

A final note is that our method relies on user specification of the hyperparameter . Ill-chosen thresholds may lead to issues, either in the form of overly conservative bounds (if is too high) or no bounds at all (if is below the minimum consistent with the data). In the worst case, invalid bounds will result from selecting a threshold that is high enough to satisfy the partial identification criterion but underestimates the true value of . However, we emphasize that -exclusion is a strictly weaker assumption than the classical exclusion criterion (A3), which is widely applied—rightly or wrongly—in IV analyses.

In many cases, setting —i.e., assuming perfectly exclusive instrumental variables—is an essentially arbitrary choice, and a tempting one given the veneer of certainty provided by obtaining a point estimate for the ATE. If nothing else, we hope to make practitioners think twice before falling back on this familiar default. Background knowledge is regularly used to guide hyperparameter selection, and it is reasonable to assume that in many applications practitioners will have an a priori sense of how much information leakage is likely between and . In particular, we can interpret this as a type of sensitivity analysis that asks how large can be such that the bounds exclude zero or effects of particular magnitude, and inquire with a practitioner whether larger values of are scientifically plausible.

7 Conclusion

We have presented a novel procedure for bounding causal effects in linear SEMs with unobserved confounding. By relaxing the exclusion criterion associated with the classical IV design, which often fails in many practical settings, our approach extends to a wide range of problems in genetic epidemiology, econometrics, and beyond. We introduce the notion of leaky instruments, which exert a limited direct effect on outcomes, and derive partial identifiability conditions for the ATE under minimal assumptions. Resulting bounds are sharp and practical, providing causal information in many cases where classical methods fail. We propose a Monte Carlo test that can falsify the exclusion criterion and a bootstrapping subroutine that guarantees asymptotic coverage at the target level. Future work will extend our results to multidimensional treatments, conditional bounding problems, and nonlinear systems, where alternative optimization strategies based on stochastic gradient descent may be required.

Acknowledgements – RS has been funded by the EPSRC Fellowship EP/W024330/1 and the EPSRC AI Hub EP/Y00759X/1.

References

- Andrews (2000) Donald W. K. Andrews. Inconsistency of the bootstrap when a parameter is on the boundary of the parameter space. Econometrica, 68(2):399–405, 2000.

- Angrist and Imbens (1995) Joshua D. Angrist and Guido W. Imbens. Two-stage least squares estimation of average causal effects in models with variable treatment intensity. J. Am. Stat. Assoc., 90(430):431–442, 1995.

- Balke and Pearl (1997) Alexander Balke and Judea Pearl. Bounds on treatment effects from studies with imperfect compliance. J. Am. Stat. Assoc., 92(439):1171–1176, 1997.

- Bennett et al. (2019) Andrew Bennett, Nathan Kallus, and Tobias Schnabel. Deep generalized method of moments for instrumental variable analysis. In Advances in Neural Information Processing Systems, pages 3564––3574, 2019.

- Berkowitz et al. (2008) Daniel Berkowitz, Mehmet Caner, and Ying Fang. Are “nearly exogenous instruments” reliable? Econ. Lett., 101(1):20–23, 2008.

- Bertsimas and Tsitsiklis (1997) Dimitris Bertsimas and John N. Tsitsiklis. Introduction to linear optimization. Athena Scientific, Belmont, MA, 1997.

- Bowden et al. (2015) Jack Bowden, George Davey Smith, and Stephen Burgess. Mendelian randomization with invalid instruments: effect estimation and bias detection through Egger regression. Int. J. Epidemiol., 44(2):512–525, 2015.

- Bowden and Turkington (1984) Roger J. Bowden and Darrell A. Turkington. Instrumental variables. Cambridge University Press, Cambridge, 1984.

- Bucur et al. (2020) Ioan Gabriel Bucur, Tom Claassen, and Tom Heskes. MASSIVE: Tractable and robust Bayesian learning of many-dimensional instrumental variable models. In Proceedings of the 36th Conference on Uncertainty in Artificial Intelligence, pages 1049–1058, 2020.

- Cai et al. (2011) Tony Cai, Weidong Liu, and Xi Luo. A constrained minimization approach to sparse precision matrix estimation. J. Am. Stat. Assoc., 106(494):594–607, 2011.

- Cai et al. (2007) Zhihong Cai, Manabu Kuroki, and Tosiya Sato. Non-parametric bounds on treatment effects with non-compliance by covariate adjustment. Stat. Med., 26(16):3188–3204, 2007.

- Chen et al. (2014) Bryant Chen, Jin Tian, and Judea Pearl. Testable implications of linear structural equation models. Proceedings of the AAAI Conference on Artificial Intelligence, 28(1), 2014.

- Chen et al. (2008) Kani Chen, Zhiliang Ying, Hong Zhang, and Lincheng Zhao. Analysis of least absolute deviation. Biometrika, 95(1):107–122, 2008.

- Chernozhukov et al. (2018) Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters. Econom. J., 21(1):C1–C68, 2018.

- Chickering and Pearl (1996) David Maxwell Chickering and Judea Pearl. A clinician’s tool for analyzing non-compliance. In Proceedings of the 13th AAAI Conference on Artificial Intelligence, pages 1269–1276, 1996.

- Chu et al. (2001) Tianjiao Chu, Richard Scheines, and Peter L. Spirtes. Semi-instrumental variables: A test for instrument admissibility. In Proceedings of the 17th Conference on Uncertainty in Artificial Intelligence, pages 83–90, 2001.

- Conley et al. (2012) Timothy G Conley, Christian B Hansen, and Peter E Rossi. Plausibly exogenous. Rev. Econ. Stat., 94(1):260–272, 2012.

- Daniels and Kass (1999) Michael J. Daniels and Robert E. Kass. Nonconjugate bayesian estimation of covariance matrices and its use in hierarchical models. J. Am. Stat. Assoc., 94(448):1254–1263, 1999.

- Davison and Hinkley (1997) A.C. Davison and D.V. Hinkley. Bootstrap methods and their application. Cambridge University Press, New York, 1997.

- Didelez and Sheehan (2007) Vanessa Didelez and Nuala Sheehan. Mendelian randomization as an instrumental variable approach to causal inference. Stat. Methods Med. Res., 16(4):309–330, 2007.

- Duarte et al. (2023) Guilherme Duarte, Noam Finkelstein, Dean Knox, Jonathan Mummolo, and Ilya Shpitser. An automated approach to causal inference in discrete settings. J. Am. Stat. Assoc., pages 1–16, 2023.

- Efron (1979) Bradley Efron. Bootstrap Methods: Another Look at the Jackknife. Ann. Stat., 7(1):1 – 26, 1979.

- Flores and Flores-Lagunes (2013) Carlos A Flores and Alfonso Flores-Lagunes. Partial identification of local average treatment effects with an invalid instrument. J. Bus. Econ. Stat., 31(4):534–545, 2013.

- Friedman et al. (2007) Jerome Friedman, Trevor Hastie, and Robert Tibshirani. Sparse inverse covariance estimation with the graphical lasso. Biostatistics, 9(3):432–441, 2007.

- Gelman et al. (2014) Andrew Gelman, John B. Carlin, Hal S. Stern, David B. Dunson, Aki Vehtari, and Donald B. Rubin. Bayesian data analysis. CRC Press, Boca Raton, FL, third edition, 2014.

- Gkatzionis et al. (2021) Apostolos Gkatzionis, Stephen Burgess, David V Conti, and Paul J Newcombe. Bayesian variable selection with a pleiotropic loss function in Mendelian randomization. Stat. Med., 2021.

- Guo et al. (2018) Zijian Guo, Hyunseung Kang, T Tony Cai, and Dylan S Small. Confidence intervals for causal effects with invalid instruments by using two-stage hard thresholding with voting. J. R. Stat. Soc. Series B Stat. Methodol., 80(4):793–815, 2018.

- Hall (1992) Peter Hall. The bootstrap and Edgeworth expansion. Springer, New York, 1992.

- Hartford et al. (2017) Jason Hartford, Greg Lewis, Kevin Leyton-Brown, and Matt Taddy. Deep IV: A flexible approach for counterfactual prediction. In Proceedings of the 34th International Conference on Machine Learning, 2017.

- Hartford et al. (2021) Jason S Hartford, Victor Veitch, Dhanya Sridhar, and Kevin Leyton-Brown. Valid causal inference with (some) invalid instruments. In Proceedings of the 38th International Conference on Machine Learning, pages 4096–4106, 2021.

- Hartwig et al. (2017) Fernando Pires Hartwig, George Davey Smith, and Jack Bowden. Robust inference in summary data Mendelian randomization via the zero modal pleiotropy assumption. Int. J. Epidemiol., 46(6):1985–1998, 2017.

- Hemani et al. (2018) Gibran Hemani, Jack Bowden, and George Davey Smith. Evaluating the potential role of pleiotropy in Mendelian randomization studies. Hum. Mol. Genet., 27(R2):R195–R208, 2018.

- Hu et al. (2021) Yaowei Hu, Yongkai Wu, Lu Zhang, and Xintao Wu. A generative adversarial framework for bounding confounded causal effects. In Proceedings of the 35th AAAI Conference on Artificial Intelligence, 2021.

- Jiang et al. (2021) Wei Jiang, Shuang Song, Lin Hou, and Hongyu Zhao. A set of efficient methods to generate high-dimensional binary data with specified correlation structures. Am. Stat., 75(3):310–322, 2021.

- Kallus and Zhou (2020) Nathan Kallus and Angela Zhou. Confounding-robust policy evaluation in infinite-horizon reinforcement learning. In Advances in Neural Information Processing Systems, 2020.

- Kang et al. (2016) Hyunseung Kang, Anru Zhang, T. Tony Cai, and Dylan S. Small. Instrumental variables estimation with some invalid instruments and its application to mendelian randomization. J. Am. Stat. Assoc., 111(513):132–144, 2016.

- Kang et al. (2020) Hyunseung Kang, Youjin Lee, T. Tony Cai, and Dylan S. Small. Two robust tools for inference about causal effects with invalid instruments. Biometrics, 2020.

- Kilbertus et al. (2020) Niki Kilbertus, Matt J Kusner, and Ricardo Silva. A class of algorithms for general instrumental variable models. In Advances in Neural Information Processing Systems, 2020.

- Kolesár et al. (2015) Michal Kolesár, Raj Chetty, John Friedman, Edward Glaeser, and Guido W Imbens. Identification and inference with many invalid instruments. J. Bus. Econ. Stat., 33(4):474–484, 2015. ISSN 0735-0015.

- Krummenauer (1998) Frank Krummenauer. Efficient simulation of multivariate binomial and poisson distributions. Biom. J., 40(7):823–832, 1998.

- Kuang et al. (2020) Zhaobin Kuang, Frederic Sala, Nimit Sohoni, Sen Wu, Aldo Córdova-Palomera, Jared Dunnmon, James Priest, and Christopher Re. Ivy: Instrumental variable synthesis for causal inference. In Proceedings of the 23rd International Conference on Artificial Intelligence and Statistics, page 398–410, 2020.

- Kuroki and Cai (2005) Manabu Kuroki and Zhihong Cai. Instrumental variable tests for directed acyclic graph models. In Proceedings of the 10th International Workshop on Artificial Intelligence and Statistics, pages 190–197, 2005.

- Künzel et al. (2019) Sören R Künzel, Jasjeet S Sekhon, Peter J Bickel, and Bin Yu. Metalearners for estimating heterogeneous treatment effects using machine learning. Proc. Natl. Acad. Sci., 116(10):4156 LP – 4165, 2019.

- Lehmann and Romano (2005) E.L. Lehmann and Joseph P. Romano. Testing Statistical Hypotheses. Springer, New York, Third edition, 2005.

- Lenkoski et al. (2014) Alex Lenkoski, Theo S Eicher, and Adrian E Raftery. Two-stage Bayesian model averaging in endogenous variable models. Econ. Rev., 33(1-4), 2014.

- Leonard and Hsu (1992) Tom Leonard and John S. J. Hsu. Bayesian Inference for a Covariance Matrix. Ann. Stat., 20(4):1669 – 1696, 1992.

- Levis et al. (2023) Alexander W. Levis, Matteo Bonvini, Zhenghao Zeng, Luke Keele, and Edward H. Kennedy. Covariate-assisted bounds on causal effects with instrumental variables. arXiv preprint, 2301.12106, 2023.

- Manski (1990) Charles F Manski. Nonparametric bounds on treatment effects. Am. Econ. Rev., 80(2):319–323, 1990.

- Mazumder and Hastie (2012) Rahul Mazumder and Trevor Hastie. The graphical lasso: New insights and alternatives. Electron. J. Statist., 6:2125–2149, 2012.

- Muandet et al. (2020) Krikamol Muandet, Arash Mehrjou, Si Kai Lee, and Anant Raj. Dual instrumental variable regression. In H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 2710–2721, 2020.

- Nie and Wager (2021) X Nie and S Wager. Quasi-oracle estimation of heterogeneous treatment effects. Biometrika, 108(2):299–319, 2021.

- Okamoto (1973) Masashi Okamoto. Distinctness of the eigenvalues of a quadratic form in a multivariate sample. Ann. Stat., 1(4):763 – 765, 1973.

- Padh et al. (2023) Kirtan Padh, Jakob Zeitler, David Watson, Matt Kusner, Ricardo Silva, and Niki Kilbertus. Stochastic causal programming for bounding treatment effects. In Proceedings of the 2nd Conference on Causal Learning and Reasoning, pages 142–176, 2023.

- Pearl (2009) Judea Pearl. Causality. Cambridge University Press, New York, 2009.

- Pollard (1991) David Pollard. Asymptotics for least absolute deviation regression estimators. Econom.Theory, 7(2):186–199, 1991.

- Portnoy and Koenker (1997) Stephen Portnoy and Roger Koenker. The Gaussian hare and the Laplacian tortoise: computability of squared-error versus absolute-error estimators. Stat. Sci., 12(4):279 – 300, 1997.

- Ramsahai (2012) Roland R. Ramsahai. Causal bounds and observable constraints for non-deterministic models. J. Mach. Learn. Res., 13(29):829–848, 2012.

- Ramsahai and Lauritzen (2011) Roland R. Ramsahai and Steffen L. Lauritzen. Likelihood analysis of the binary instrumental variable model. Biometrika, 98(4):987–994, 2011.

- Reich et al. (2001) David E Reich, Michele Cargill, Stacey Bolk, James Ireland, Pardis C Sabeti, Daniel J Richter, Thomas Lavery, Rose Kouyoumjian, Shelli F Farhadian, Ryk Ward, and Eric S Lander. Linkage disequilibrium in the human genome. Nature, 411(6834):199–204, 2001.

- Rubin (1981) Donald B Rubin. The Bayesian bootstrap. Ann. Statist., 9(1):130–134, 1981.

- Saengkyongam et al. (2022) Sorawit Saengkyongam, Leonard Henckel, Niklas Pfister, and Jonas Peters. Exploiting independent instruments: Identification and distribution generalization. In Proceedings of the 39th International Conference on Machine Learning, pages 18935–18958, 2022.

- Schäfer and Strimmer (2005) Juliane Schäfer and Korbinian Strimmer. A shrinkage approach to large-scale covariance matrix estimation and implications for functional genomics. Stat. Appl. Genet. Mol. Biol., 4(1), 2005.

- Shafer et al. (1995) Glenn Shafer, Alexander Kogan, and Peter Spirtes. A generalization of the tetrad representation theorem. In Pre-proceedings of the 5th International Workshop on Artificial Intelligence and Statistics, pages 476–487, 1995.

- Shapland et al. (2019) Chin Yang Shapland, John R Thompson, and Nuala A Sheehan. A Bayesian approach to Mendelian randomisation with dependent instruments. Stat. Med., 38(6):985–1001, 2019.

- Shpitser and Pearl (2008) Ilya Shpitser and Judea Pearl. Complete identification methods for the causal hierarchy. J. Mach. Learn. Res., 9:1941–1979, jun 2008.

- Silva and Evans (2016) Ricardo Silva and Robin Evans. Causal inference through a witness protection program. J. Mach. Learn. Res., 17:1–53, 2016.

- Silva and Shimizu (2017) Ricardo Silva and Shohei Shimizu. Learning instrumental variables with structural and non-gaussianity assumptions. J. Mach. Learn. Res., 18(120), 2017.

- Singh et al. (2019) Rahul Singh, Maneesh Sahani, and Arthur Gretton. Kernel instrumental variable regression. In Advances in Neural Information Processing Systems, pages 4595–4607, 2019.

- Solovieff et al. (2013) Nadia Solovieff, Chris Cotsapas, Phil H Lee, Shaun M Purcell, and Jordan W Smoller. Pleiotropy in complex traits: challenges and strategies. Nat. Rev. Genet., 14(7):483–495, 2013.

- Spearman (1904) Charles Spearman. General intelligence, objectively determined and measured. Am. J. Psychol., 15(2):201–292, 1904.

- Spirtes (2013) Peter Spirtes. Calculation of entailed rank constraints in partially non-linear and cyclic models. In Proceedings of the 29th Conference on Uncertainty in Artificial Intelligence, pages 606–615, 2013.

- Spirtes et al. (2000) Peter Spirtes, Clark N. Glymour, and Richard Scheines. Causation, Prediction, and Search. The MIT Press, Cambridge, MA, 2nd edition, 2000.

- Sullivant et al. (2010) Seth Sullivant, Kelli Talaska, and Jan Draisma. Trek separation for Gaussian graphical models. Ann. Stat., 38(3):1665 – 1685, 2010.

- VanderWeele et al. (2014) Tyler J VanderWeele, Eric J Tchetgen Tchetgen, Marilyn Cornelis, and Peter Kraft. Methodological challenges in Mendelian randomization. Epidemiol., 25(3):427–435, 2014. ISSN 1531-5487.

- Warton (2008) David I Warton. Penalized normal likelihood and ridge regularization of correlation and covariance matrices. J. Am. Stat. Assoc., 103(481):340–349, 2008.

- Windmeijer et al. (2019) Frank Windmeijer, Helmut Farbmacher, Neil Davies, and George Davey Smith. On the use of the lasso for instrumental variables estimation with some invalid instruments. J. Am. Stat. Assoc., 114(527):1339–1350, 2019.

- Won et al. (2012) Joong-Ho Won, Johan Lim, Seung-Jean Kim, and Bala Rajaratnam. Condition-number-regularized covariance estimation. J. R. Stat. Soc. Series B Stat. Methodol., 75(3):427–450, 2012.

- Wooldridge (2019) Jeffrey Marc Wooldridge. Introductory Econometrics: A Modern Approach. South-Western, Mason, OH, seventh edition, 2019.

- Xu et al. (2021) Liyuan Xu, Yutian Chen, Siddarth Srinivasan, Nando de Freitas, Arnaud Doucet, and Arthur Gretton. Learning deep features in instrumental variable regression. In International Conference on Learning Representations, 2021.

- Zhang et al. (2022) Junzhe Zhang, Jin Tian, and Elias Bareinboim. Partial counterfactual identification from observational and experimental data. In Proceedings of the 39th International Conference on Machine Learning, volume 162, pages 26548–26558, 2022.

Appendix A Proofs

A.1 Proof of Lemmas 1 and 2

Consider Eqs. 1, 2, and 3, which define our model. Evaluating the product of and gives a relationship between covariances:

| Solving for gives | ||||

| (4) | ||||

| Likewise, the product of with itself gives | ||||

| Using (4) and solving for gives | ||||

| The product of and gives | ||||

| Solving for gives | |||

| Taking the norm and using the definitions of , we recover Lemma 2: | |||

| (7) | |||

| The product of and gives | ||||

| Using (7) and solving for gives | ||||

| (9) | ||||

| Rearranging for gives | ||||

| (10) | ||||

| The product of with itself gives | ||||

| Using (7), (9), and (10) gives | ||||

Combining the s into s,

collecting powers of ,

and massaging the s and s around, we have

Solving this quadratic for gives the solutions

As corresponds to the lower solution for (and vice versa), we have

Exploiting the identity for , we derive the result stated in Lemma 1:

A.2 Proof of Lemma 3

We can think of the data covariance as constraining to lie in a -dimensional linear subspace . (Recall that are deterministic functions of .) As may not equal zero in general, the resulting norm cannot be made arbitrarily small. Of course, computing the norm-minimizing coefficient is the definition of a linear regression task. Call the solution to this problem (where the index indicates optimization with respect to the norm). Since partial identification is only possible if information leakage exceeds the theoretical minimum consistent with the data covariance, we may define this lower bound as .

A.3 Proof of Lemma 4

Recall that gives as a function of , while gives as a function of . We define as a map from the confounding coefficient to the information leakage . As is a continuous function with a compact domain, the extreme value theorem guarantees that a minimum exists. Moreover, since is bijective, we know by Lemma 3 that our target value must represent the inverse of evaluated at . Setting to and solving for , we derive the expression. We can now equivalently characterize the minimum leakage parameter as .

A.4 Proof of Thm. 1

Thm. 1 provides identifiability criteria for the leaky IV model. In the first part of the theorem, we describe a three-partition of the threshold space in terms of the theoretical leakage minimum and the oracle value . We claim that the identifiability and validity of ATE bounds are fully characterized by where falls in relation to these parameters. Next, we show that point identification is possible if and only if latent parameters align in a specific way.

Take partial identifiability criteria first. The task of bounding the ATE in the leaky IV model amounts to finding the min/max values of that satisfy:

| (12) |

In other words, we fit a horizontal line across the function and report min/max points of intersection. Recall that is defined as the minimum of this function. Thus when falls below , it is clear that there is no intersection between these two curves, and Eq. 12 has no solution. This is our sole partial identifiability criterion: provided all our structural assumptions hold, ATE bounds are well-defined if and only if . Below this minimum leakage point lies the infeasible region.

But just because bounds are identifiable does not mean that they are valid. Suppose (for now) that the oracle threshold strictly exceeds the theoretical minimum, and recall the definition:

where denote the true unobservable parameters. By the convexity of the norm, the solutions to Eq. 12 for any will fail to capture the true ATE, as the resulting horizontal line lies below the point . Even a -oracle—who, recall, has access to the population covariance matrix but not the latent parameters —will return invalid bounds if queried with a threshold in this half-closed interval. For this reason, we call this band the error region.

With a threshold at or above the oracle value , solutions to Eq. 12 are finally guaranteed to contain the true ATE . This once again follows by convexity of . Resulting bounds grow increasingly conservative with . This valid region for all completes our three-partition of the threshold space.

We have thus far assumed that the oracle threshold strictly exceeds the theoretical minimum, but these parameters may coincide. If , then the error region is empty and all identifiable bounds are valid. Moreover, if attains a unique minimum—as it must for all strictly convex norms, i.e. —then there exists just a single solution to Eq. 12 for . In this case, lower and upper bounds for the ATE coincide and the causal parameter is point identified as . Note that this fortuitous circumstance occurs with Lebesgue measure zero, as it imposes a nontrivial polynomial constraint on covariance parameters (Okamoto 1973).

A.5 Proof of Corollary 1.1

Under Eq. 2 and the exclusion criterion (A3), we must have that . Since , it follows that . This is a special case of the point identifiability result of Thm. 1. Define

which represents the expected result of the first OLS regression. Then the 2SLS solution can be written as the ratio:

Exploiting the definitions and , we have:

A.6 Proof of Thm. 2

We assume that partial identifiability criteria are met (see Thm. 1). Recall that is a bijective function of (see Lemma 1). To compute valid, sharp ATE bounds, it is therefore sufficient to show that there exist unique minimum and maximum values of such that . Call these and , respectively. (Since the function is strictly decreasing, it maps the former to and the latter to .) The advantage of working in -space rather than -space is that the confounding coefficient is guaranteed to lie on a compact interval that is independent of the data, namely .

Recall that the norm is convex for all and strictly convex for . Also, by definition, we have that . Thus we have four possibilities to consider, with strict and non-strict variants of both convexity and the leakage inequality (see Table 1). Non-strict convexity raises complications due to the potential for plateaus in the norm; non-strict inequality raises complications if true and minimum leakage parameters coincide. We will show that and are uniquely identified in all four settings.

| Convexity of norm | ||

|---|---|---|

| Inequality | Strict | Non-strict |

| Strict | Unique | Interval |

| Non-strict | Unique | Interval |

Start with the simplest case, in which both the convexity and inequality are strict. In this setting, we have exactly two solutions to the equation , one on either side of , which is the unique minimizer of . Thus one solution lies on the interval , and another on .333In fact, when , we know that is not a viable solution, and so we can replace the closed intervals with half-open intervals and . Since this is not the case when , we stick with closed intervals throughout for greater generality. This establishes the existence and uniqueness of and .

Now consider the case where is strictly convex but the true leakage coincides with the theoretical minimum (lower left quadrant of Table 1). In this case, we have just a single solution to the equation , namely . This implies that .

Greater care is required when is not strictly convex, as we can no longer assume the uniqueness of or that has at most two solutions. However, when no unique minimum exists for a convex function with a compact domain, the set of minimizing solutions forms a compact interval. (This follows from the extreme value theorem.) Consider the setting where the leakage inequality is strict but no single value of minimizes (upper right quadrant of Table 1). We can select any value from the compact interval and use this to partition , since strict inequality guarantees that any solution must intersect with above its minimum. Still, we may have have uncountably many solutions to the equation if aligns with a plateau in the norm on one or both sides of . Convexity guarantees that we will have at most two sets of solutions, one on either side of the minimum. Call these intervals and . Since both are closed, each contains a unique min/max. Our target parameters are therefore identified by taking the extreme values of each, i.e. setting and .

Finally, consider the case where neither the convexity of the norm nor the leakage inequality is strict (lower right quadrant of Table 1). This is arguably simpler than the setting with strict inequality and non-strict convexity, since we have just a single compact interval of solutions at . Our target parameters in this case are identified via and .

A.7 Proof of Corollary 2.1

To find ATE bounds with an threshold on information leakage, we invoke Lemma 2 and find that leakage is quadratic in :

We set and solve for using the quadratic formula:

Observe that the first summand reduces to the norm-minimizing ATE value identified in Lemma 3:

Some light simplifications and rearrangements renders the final expression:

A.8 Proof of Thm. 3

Let be the space of all models satisfying our structural constraints—Eqs. 1, 2, 3 and assumptions (A1), (A2), and (A)—for some fixed distribution family and . (Recall that (A) is consistent with the classic exclusion criterion (A3) under .) We partition into null and alternative classes depending on whether the models in each satisfy . We reiterate that this condition is necessary but not sufficient to guarantee (A3). Each dataset is sampled from some fixed but unknown that belongs to either or .

For every , there exists some nearest null neighbor (not necessarily unique) satisfying

Of course, when , we have and the KL-divergence goes to zero. Let be a function from input data to corresponding test statistics . (The bounded range follows from the fact that all entries in the matrix are non-negative.) Let be a dataset sampled from , and let be the sampling distribution of at sample size , i.e. for any . We denote the corresponding null distribution as , which represents the sampling distribution of under at sample size , i.e. , for null datasets .

To establish that is an asymptotically valid -value against , it suffices to show that the Monte Carlo null distribution converges to . This follows from the validity of our procedure for constructing the null covariance matrix , which involves the minimum perturbation required to guarantee . Specifically, we impose a linear dependence between covariance vectors and using the scaling factor . Thus satisfies by construction. Moreover, since this is achieved by changing as few parameters as possible by as little as possible, there exists no nearer neighbor to within than the resulting distribution, which therefore satisfies our definition of .

We assume access to some method for sampling from , e.g. via if is the family of mean-zero multivariate Gaussians. We draw many datasets of size from and record resulting test statistics to generate the synthetic null distribution . Convergence is assured when is uniformly distributed under . Let denote the critical value at type I error rate for dataset , such that, under , the rejection region of statistics

integrates to . Rejection regions are nested for our one-sided test, i.e. if . Thus represents the quantile of the null distribution . We reject if , resulting in the identity:

Then for all , we have

which implies that:

for all (Lehmann and Romano 2005). In other words, is uniformly distributed under , as desired, and the Monte Carlo null distribution has converged on the target . We add one to the numerator and denominator as a necessary finite sample adjustment.

A.9 Proof of Thm. 4

It may not be immediately clear that bootstrapping is appropriate for ATE bounds. After all, it is well known that the bootstrap cannot provide a valid sampling distribution for fixed order statistics such as ranks, or a target parameter that lies on the boundary of the parameter space (Andrews 2000). But though we refer to our bounds as “min” and “max” solutions, that does not mean they are calculated via fixed order statistics. On the contrary, each represents a continuous solution to a differentiable optimization task, not the smallest or largest element in a discrete set. The only boundary condition for our target parameters is , which automatically holds under the partial identifiability criterion . As our estimator is undefined for samples that violate the criterion, our sampling distribution is always conditioned on this event.

In general, any statistic that is a differentiable function of sample moments admits an Edgeworth expansion and can therefore have its distribution consistently estimated via bootstrap resampling (Hall 1992, Davison and Hinkley 1997). Recall that our ATE bounds represent the intersection of (a) a -feasible region that is fixed a priori; and (b) the norm of , where the latter two vectors are defined as dot products of covariance parameters. Resulting bounds vary smoothly under resampling, since and are differentiable with respect to . Though more generalized relaxations of the exclusion criterion may introduce discontinuities or other issues, our formulation of -exclusion poses no such difficulties. The resulting bootstrap distributions are asymptotically valid and practically useful, providing statistical inference without any parametric assumptions.

Of course, it is perfectly possible that some bootstrap samples may have to be discarded if the intersection of regions (a) and (b) is empty. In such cases, we simply restrict attention to those bootstraps that satisfy the partial identifiability criterion , which should represent a non-negligible proportion of all bootstraps if the inequality is satisfied in the original dataset. This procedure is akin to sampling under a feasibility condition, and requires no extra steps to maintain bootstrap consistency, as in Andrews (2000) and Ramsahai and Lauritzen (2011).

Appendix B Experiments

B.1 Benchmarks

We implement the backdoor adjustment via simple linear regression. Similarly, the 2SLS estimator is computed using OLS. We use the CRAN implementation of sisVIVE. R code for MBE was provided by the authors. Results of benchmark experiments for all simulation configurations are presented in Fig. 9.

B.2 Interpreting the scales of structural parameters

In our experiments, we fix the true causal effect and tune the signal-to-noise ratios (SNRs) for and , denoted here as and respectively. We show that these quantities, coupled with the variance , the magnitude of and the instruments covariance matrix , uniquely define the magnitude of the remaining structural parameters at a given level of confounding , when the directions are randomized. The choice to tune the dimensionless parameters and provides a more interpretable grid search than we would have if we were to vary the structural parameters directly. This is especially true given that the directions of the vector-valued structural parameters—randomized in our experiments and exponentially hard to search through in a high- setting—play a crucial role in the effect in the proportions of each observable’s variance explained by each causal effect.

In our setting, and are randomized through and , where the components and , are drawn identically and independently () from the the standard normal distribution. We show that are uniquely determined through the equations for the variances,

and the signal-to-noise ratios,

Note that “noise” is any contribution involving the unobserved confounding . In a certain sense, the definition of is ambiguous in our setting because can be determined from generated data. We stress our choice of the definition here: if we took to be “signal” then would be infinite.

We solve these four coupled quadratic equations for the remaining parameters . They have unique solutions if we demand each of these scaling factor and the standard deviations to be positive. We choose to write the solutions to these equations in the following form:

| (13) | |||

| (14) | |||

| (15) | |||

| (16) |

where

Notice that the term in the brackets in the equation for is the signal due to -exclusion, i.e., the residual signal not solely due to . This term is, therefore, always greater than , so is always greater than . Notice also that these equations are more general than in our particular experimental setting since we have left , and to be decided.

Inputting the above solutions, in order, to a data generating process allows us to tune these terms by specifying the signal-to-noise ratios. As a final note, one may be interested in studying asymptotic regimes in which the variance of or is dominated either by signal or noise. These equations, or equations very similar to these, allow for the rigorous study of linear models in such regimes through asymptotic expansions with respect to the SNRs.

B.3 Bayesian baseline

One of our choices of a method to compare against ours is a full-likelihood Gaussian model with Bayesian posteriors with a bounded L2 norm on .

Assume all variables follow a joint multivariate zero-mean Gaussian distribution. Recall that that are candidate instruments, is the treatment, is the outcome.

Let be the coefficients of in the equation for , and is such that . We will encode as

where is another (redundant) parameter, and is the free parameter vector of the same dimensionality as . The interpretation is that is the norm of , and is a direction vector. This provides a direct comparison against our constrained optimization method, as both methods are capable of directly using information about the norm of and we will below put an uniform prior on .

Assuming below is a row vector, the model is:

where and are generic positive definite matrices, and means multivariate Gaussian distribution. The parameter set is .

In what follows, we will consider only the independent candidate instruments case

and parameterize as

for . The independence assumption on is merely to simplify our sampler code.

Priors are defined as follows:

where is the identity matrix of corresponding dimensionality, is the uniform distribution on the unit interval, and denotes the log-normal distribution. Remaining symbols and are hyperparameters.

Given a dataset with each of its rows denoting a data point, the sufficient statistic for this model is

The model covariance matrix is given by

Given that, the log-likelihood function is

where the columns/rows of are sorted in the same way as the columns/rows of . We use a plain random walk Metropolis-Hastings method to sample from the posterior of this distribution. We implement the uniform priors by the encoding , where is the standard Gaussian cdf and is a standard Gaussian random variable to be sampled. Likewise, .

B.3.1 Usage

Like MASSIVE (Bucur et al. 2020), this is a full Bayesian approach that returns a full posterior on . Unlike MASSIVE, which is designed for soft sparsity constraints, our prior on is on a Gaussian distributed disc with the radius being given a uniform prior on so that it is the closer match to the principle behind our hard constrained optimization method.

For a comparison to take place, we translate the posterior distribution over as “bounds”. More precisely, let be the -th quantile of the posterior distribution of . A “lower bound” here is taken to mean the interval, although it is not explicitly made to “capture” the population lower bound with probability . That can only happen in a heuristic sense, as the full Bayesian approach is oblivious to non-identifiability issues and has no sense what a “population lower bound” should be. For joint “capturing” of lower and upper bounds, we suggest along with .

Like MASSIVE, the posterior on never converges to a single point in the limit of the infinite data, and any entropy left in that case is a consequence of the prior. If the prior is informative, it is entirely possible for the posterior to exclude the true even if it perfectly fits the population distribution. If the prior is uninformative, the limiting posterior support should coincide with the feasible region obtained by plugging in the population covariance matrix, although any curvature of this posterior within its support is an artefact of the prior. However, with finite data, there is no clear way of separating entropy due to probabilistic uncertainty from entropy due to unidentifiability. Any claims that tails of this distribution have a correspondence to partial identifiability results is an ill-posed heuristic at best.