A Unified Algorithmic Framework for Dynamic Assortment Optimization under MNL Choice

Shuo Sun, Rajan Udwani \AFFDepartment of Industrial Engineering and Operations Research, UC Berkeley, Berkeley, CA 94720, \EMAILshuo_sun@berkeley.edu, \EMAILudwani@berkeley.edu \AUTHORZuo-Jun (Max) Shen \AFFFaculty of Engineering & Faculty of Business and Economics, University of Hong Kong, Hong Kong, \EMAILmaxshen@hku.hk

We consider assortment and inventory planning problems with dynamic stockout-based substitution effects and no replenishment. We consider two settings: 1. Customers can see all available products when they arrive, which is commonly seen in physical stores. 2. The seller can choose to offer a subset of available products to each customer, which is typical on online platforms. Both settings are known to be computationally challenging, and the current approximation algorithms for the two settings are quite different. We develop a unified algorithm framework under the MNL choice model for both settings. Our algorithms improve on the state-of-the-art algorithms in terms of approximation guarantee, runtime, and the ability to manage uncertainty in the total number of customers and handle more complex constraints. In the process, we establish various novel properties of dynamic assortment planning (under the MNL choice) that may be useful more broadly.

1 Introduction

Choosing the optimal assortment of products to offer and determining the inventory levels for each product are fundamental problems in various industries, including retail and airlines. There has been extensive research on static assortment optimization where an optimal assortment is selected for a single customer. This setting assumes that we can stock a sufficiently large inventory for each product so that all customers see the same assortment, which is suitable for scenarios where inventory is not a primary concern, such as for digital goods or services. However, in many real-world scenarios, inventory is finite, and the sequential arrival of customers creates dynamics where products often stock out, leading to notable sales losses in both retail and the sharing economy. Therefore, in addition to deciding which products to stock, it is necessary to consider the dynamic assortment planning problem where we decide how much each product to stock and what assortment to offer to each arriving customer. The dynamic assortment planning problem is notoriously challenging due to the dynamic stockout-based substitution behavior, where customers make purchases based on the available products. (Mahajan and Van Ryzin 2001, Aouad et al. 2018). The demand for each product can be modeled through a stochastic consumption process, which is a sequence of customer choices - upon arrival, a customer randomly selects from available products offered, and the choice probability is determined by the choice model. Thus, the demand for each product is influenced by both customer preferences and the occurrence of stockouts, with these two factors being deeply interconnected. Customer preferences can lead to earlier stockouts for more preferred products, and stockouts affect purchase probabilities since the choice probabilities depend on which products are available. In fact, even efficiently evaluating the expected revenue given a starting inventory (and assortment policy) remains challenging for many choice models, including the Multinomial Logit (MNL) model.

In this work, we consider constrained single-period dynamic assortment planning problems, focusing on developing provable approximate algorithms. Dynamic assortment optimization problems vary across operating environments. In brick-and-mortar retail, once the initial inventory decisions are made, every customer entering the store sees all the available products, and assortment changes sporadically (Aouad et al. 2018, 2019). Conversely, online platforms make it easy to provide real-time personalized assortments from available products (Bai et al. 2022). We distinguish these two settings as the dynamic assortment optimization problem (da) and dynamic assortment optimization with personalization problem (dap), respectively. The existing algorithmic approaches for da and dap are quite different. For dap, when the number of customers is known, there is a natural LP relaxation that serves as a good (fluid) approximation for the expected revenue in the stochastic consumption process. In particular, one can optimize the LP objective, leading to a considerably simpler problem while losing a constant factor in the approximation guarantee (Bai et al. 2022). However, for da, where we are not allowed to change the assortments manually, no strong fluid relaxation was known (to the best of our knowledge). Existing algorithms directly optimize the expected revenue that appears hard to evaluate exactly, which use Monte Carlo sampling to estimate objective value and use computationally intensive enumerative procedures to identify the approximate inventory solutions (Aouad et al. 2018, Aouad and Segev 2022). These challenges highlight the complexities of the da problem and the pressing need for more scalable and efficient algorithmic solutions. Additionally, this raises the intriguing question of whether a unified approximation framework could effectively solve both problems.

In many applications, the number of customers (denoted as ) within a given planning horizon is unknown a priori. The stochasticity in adds additional complexity. In fact, in modern e-commerce and other online platforms, is often highly uncertain and may follow a high-variance distribution (Szpektor et al. 2011, El Housni et al. 2021, Aouad and Ma 2022). While for the da problem, previous work has considered different customer distributions (Aouad et al. 2018, Aouad and Segev 2022), the existing work on dap only considers deterministic (Bai et al. 2022). Consequently, developing algorithms for dap under stochastic remains a challenging open problem.

1.1 Our Contribution

Our main contribution is to develop a unified algorithm framework that addresses both da and dap problems under the MNL choice model. Our framework offers several key advantages, including computational efficiency, improved approximation ratios, the ability to manage uncertainty in the total number of customers, and the ability to handle more complex constraints. We use a two-step approximation framework. In the first step, we develop threshold-based augmentation algorithms to approximately maximize fluid relaxations. In the second step, we make inventory and assortment decisions based on the approximate inventory solution from the first step. We develop several technical ideas to establish the new results, and some of them may be of broader interest, which will be discussed later in Section 1.2.

Table 2 compares our results with the best-known approximation ratios for dynamic assortment optimization under the MNL choice model and cardinality constraints. For da, we improve the best approximation ratio for the distributions with Increasing Failure Rate (IFR) property in Aouad et al. (2018), from to 11endnote: 1Assuming the existence of an efficient oracle, the algorithm in Aouad et al. (2018) provides a approximate solution with a probability of at least for any and . Here is a parameter of the accuracy level we can set. To the best of our knowledge, the existence of the oracle remains an open problem. Moreover, our algorithm offers a better approximation guarantee than this result.. Furthermore, our approach is not randomized and is significantly faster since we avoid partial enumerations that can be time intensive (polynomial in , where is the number of products) and Monte Carlo sampling (polynomial in , where is the probability of failure). Specifically, our algorithm has runtime , where is the cardinality constraint. Aouad and Segev (2022) give a near-optimal algorithm for DA, which is not polynomial time (see Section 1.3 for more details). In addition, for the da problem, our algorithm addresses the previously open problem of accommodating a budget constraint (Aouad et al. 2018), achieving an approximation ratio of , the same as that for a cardinality constraint.

For dap, we achieve an approximation ratio of for deterministic , surpassing the current best guarantee of (Bai et al. 2022). Perhaps more importantly, our approach extends to the setting where is uncertain and follows an arbitrary (known) distribution, including high variance distributions, where no approximation results were known previously. In such scenarios, our algorithm achieves a approximation.

| da | dap | |

| Deterministic | ||

| IFR | ||

| General Distribution |

1.2 Technical Ideas

We use a two-step approximation algorithmic framework. We first find approximate inventory solutions to maximize the fluid approximation of the total expected revenue given constraints. Our fluid approximations are based on the choice-based linear program (CDLP), which is a standard relaxation used in the revenue management literature. We use and to denote the optimal CDLP objective function value considering a single customer type or multiple types, named differently due to their distinct structural properties, as we will discuss later.

Approximating the optimal inventory to the fluid relaxation. While for dap, it is known that is an effective fluid approximation for the stochastic expected revenue, for da, it is highly non-trivial to determine whether serves as an effective relaxation. By effective relaxation, we mean that one can obtain the inventory (and assortment) solutions such that the original expected revenue is at least a constant factor of . In fact, when inventory is fixed, can be arbitrarily larger than the expected revenue even for the MNL choice model. We show that is an effective relaxation for da under the MNL choice model for both deterministic and stochastic , which will be discussed later. So now, let us focus on approximating the optimal inventory for . It is well known that does not exhibit submodularity even when . Bai et al. (2022) propose a modified LP (surrogate) that gives a approximate to (multiple types) that is submodular. As a straightforward extension of their result, we show that for a single customer type, their result can be strengthened, and we obtain a submodular surrogate that is a (1-)-approximation for maximizing . Our main new contribution is an improved approximation algorithm for maximizing , even when comes from an arbitrary stochastic distribution. To show this, we first prove that the decreasing order of prices is a submodular order (SO) for (single type). This gives a approximation for using the threshold algorithm for maximizing SO functions. Perhaps surprisingly, this order is not SO for because allocations the inventory of each item between different customer types. We propose a novel threshold-based algorithm that gives a - approximate solution for maximizing given a cardinality constraint and for a budget constraint. Proving that is SO is quite challenging as the LP optimal solution may change in non-trivial ways due to small changes in inventory. We prove new structural properties of : We show is equal to the total revenue in a fluid process that starts with an inventory vector with generalized revenue-ordered property. Moreover, we establish new structural properties to analyze the influence of changing the starting inventory on the revenue in the fluid process. The revenue-ordered structure and structural properties also inspire us to develop a near-linear time algorithm to solve . Given the widespread application of CDLP in revenue management, this fast algorithm may be of independent interest (see Appendix LABEL:app:fast_cdlp for details).

Transformation to inventory and assortment decisions. For da, when inventory is fixed, can be arbitrarily larger than the original expected revenue, and it is unclear if we can obtain a good solution for the original problem from the approximately optimal inventory for from the first step. This might not be surprising since allows offering a subset of available products to each customer, while in the stochastic consumption process without personalization, low-price products may deplete late on some sample paths. This affects the purchase probability of high-price products due to the substitution effect, thus cannibalizing their demand. In dap, we can manually offer the assortment to exclude low-price products to mitigate the cannibalization effect. However, for da, this cannibalization effect generally poses a significant challenge. Perhaps surprisingly, we show that a small change to the approximate inventory for yields a good inventory solution for da. In essence, we inductively reduce the cannibalization effect to a single ‘bad’ product and show that simple rounding of the inventory of this product can mitigate this product’s effect on overall revenue. Consequently, we obtain an inventory solution with a stochastic expected revenue of at least for deterministic and for stochastic following an IFR distribution. Showing the for stochastic poses additional challenges, as we further use as a fluid approximation of . We establish new stochastic inequalities to show for IFR distributions, which might be of broader interest.

In dap, once the initial inventory is decided, we use standard algorithmic ideas from online assortment to decide the real-time assortments. For deterministic , we show a sampling-based approach yields , which improves over the state-of-the-art ratio of (Bai et al. 2022). When is stochastic and even follows a high-variance distribution, the online greedy algorithm achieves a performance guarantee of (Golrezaei et al. 2014). These performance guarantees hold for general choice models with weak substitutability, not just MNL.

1.3 Related Work

A significant amount of research has focused on the static assortment optimization problem. Under the MNL choice model, previous research has proposed various tractable static assortment optimization algorithms across different settings. Talluri and Van Ryzin (2004) show the optimal unconstrained assortment includes a select number of products with the highest prices, known as the revenue-order structure. Rusmevichientong et al. (2010) consider the assortment optimization problem that the number of products offered is upper bounded, proposing a polynomial algorithm for the cardinality-constrained assortment optimization problem. Other variants of this problem are also considered; for further details, see Rusmevichientong and Topaloglu (2012), Désir et al. (2014), Davis et al. (2013). For a comprehensive review of static assortment optimization under other choice models, we refer the readers to Kök et al. (2015) and Strauss et al. (2018).

The dynamic setting poses a greater challenge due to the stochastic nature of customer behavior, as customer choices depend on sample-path realizations. Several works explore the theoretical difficulty of this problem and develop heuristics based on continuous relaxation. Mahajan and Van Ryzin (2001) show the profit function for the continuous relaxation problem is not quasi-concave and propose a gradient-based heuristic to solve the continuous relaxation problem. Honhon et al. (2010) assume customers always purchase the highest-ranked available product. They use a dynamic programming formulation to model the problem and establish some structural properties to help find local maxima. Recent research has started to develop provably good approximation algorithms. Our work is most closely related to this line of work. We first review the work in da setting, i.e., we only set up a starting inventory and are not allowed to change the assortment during the selling horizon. Aouad et al. (2018) propose the first constant-factor approximation algorithm for the dynamic assortment planning problem under the MNL choice model. Then, assume that the distribution of customers satisfies the IFR property. Aouad and Segev (2022) further explore the structural properties of the stochastic consumption process under the MNL choice model and develop a Monte-Carlo algorithm to compute the starting inventory within an arbitrary degree of accuracy. The runtime is , which is exponential in , where is the maximum weight and is the minimum weight, is the number of products, and is the capacity limit on the total number of units to be stocked. Observe that this algorithm is not a polynomial-time algorithm. As such, it does not directly compare with our polynomial-time result. In addition to the work discussed previously, Goyal et al. (2016), Segev (2015), and Aouad et al. (2019) also propose approximation algorithms for dynamic assortment planning, but consider more restrictive models, such as products being consumed in a specific order. This special structure enables the use of low-dimensional dynamic programs to optimize total revenue, as noted in Aouad et al. (2018). However, the MNL model leads to an exponential number of sample paths, making dynamic programming intractable. Another line of work in dynamic assortment focuses on the setting in which the assortment offered to each customer is decided in an online manner, depending on the remaining inventory and the type of customer. The inventory may have been determined beforehand or is jointly decided with the assortment. Closely related to our work is Bai et al. (2022), which also approaches the dap problem through the lens of CDLP. However, they focus on deterministic and use an approximate LP surrogate for . By showing the submodularity of the LP surrogate under the MNL choice model, they achieve a approximation for maximizing , while we consider directly and develop a guarantee by generalizing algorithmic ideas for submodular order functions. They provide an overall approximate solution for the MNL choice model with deterministic and a approximate solution for a general choice model. We improve the approximation guarantee for MNL to for deterministic and also consider stochastic , which may follow an arbitrary distribution. For further discussion of online assortment optimization problems, the reader may refer to recent work and literature reviews in Ma and Simchi-Levi (2020), Rusmevichientong et al. (2020), Ma et al. (2021), and Chen et al. (2022).

There is some other work considering joint assortment and inventory problems but focusing on developing sublinear regret guarantees. Liang et al. (2021) consider the single-period joint assortment and inventory problem under MNL choice with a non-zero existing initial inventory. They show that fluid LP relaxation can be solved by sequentially solving a series of simpler linear programs, and the optimal solutions of these LPs have the ‘quasi gain-ordered’ property. We establish a different generalized revenue-ordered property for the starting inventory of a fluid process that results in the same revenue as . This coincidence suggests that the optimal inventory for different variants of dynamic assortment problems might have different revenue-ordered-like properties. Mouchtaki et al. (2021) propose a sample average approximation based algorithm for the unconstrained problem, which achieves sublinear regret under a Markov chain choice model. Guo et al. (2023) consider an unconstrained problem under general choice models and arbitrary distribution of customers and reformulate the fluid LP as a bilevel optimization problem. Additionally, some work combines learning and dynamic assortment optimization. Liang et al. (2023) study the dynamic assortment planning problem under the MNL choice with unknown preference weights, which focus on learning the weights and use an existing solution algorithm for the dynamic assortment optimization problem as an oracle.

1.4 Outline

The remainder of this paper is organized as follows. Section 2 provides the problem formulation and introduces preliminary results essential for subsequent discussions. Section 3 details the approximation algorithms for the fluid relaxations. Section 4 introduces the algorithms that transform approximate solutions into inventory and assortment decisions. Finally, section 5 analyzes the overall performance guarantees and runtime, including further algorithm acceleration techniques.

2 Preliminaries

In this section, we formulate the dap and da problems and their fluid relaxations. We also introduce some technical results that are important in our algorithmic approach and analysis.

2.1 Problem Formulations

We start with the common setup for both the dap and da problems. Let denote the ground set of products sorted in the descending order of the (fixed) per-unit prices . We need to decide the stocking level for each product, and we use to denote the number of units (stocking level) of product . These stocking levels are collectively represented by a vector . Let denote the unit vector that only the th component is and other components are all . Let denote the number of customers in the selling horizon. Alternatively, this can be viewed as a selling horizon of periods, with one customer arriving in each period. We use to denote customer arriving in period . may be known (deterministic) or unknown (stochastic) when the inventory decisions are made. For stochastic , we denote its distribution by , which is assumed to be known.

2.1.1 DA Problem

In the da problem, the selling horizon starts with an inventory . Upon arrival, customer sees all products with non-zero inventory (available products), and makes at most one purchase independently based on the MNL choice model . For the MNL model, let denote the attraction parameter for product . Recall that the probability in MNL choice model is given by . Here denotes the outside option and is its attraction parameter. Without loss of generality, we let .

Our objective is to identify a feasible starting inventory that maximizes the expected total revenue. Here is the feasible region given by a cardinality constraint or a budget constraint for certain values of , and . Let denote the expected number of units of product consumed in the selling horizon with customers and starting inventory . Then, the total expected revenue is given by

When is stochastic, we only know the distribution of , not its actual value. Thus, the objective function is

Similar to previous work, we assume that the distribution of satisfies the IFR property for the da setting, meaning that is non-decreasing for any . This property holds for various distributions used in the literature, such as exponential, Poisson, and geometric distributions (Goyal et al. 2016, Aouad et al. 2018).

2.1.2 DAP Problem

In the dap problem, there are different types of customers, denoted by . A customer of type chooses (independently) according to the MNL choice model , with attraction parameters . The probability that customer belongs to type , given by , is known in advance. Every customer’s type is independent and realized on arrival. Unlike the da problem where customers see all available products, in dap, when a customer of type arrives at time , we select a subset of available products (assortment) to offer. We decide the assortment based on the purchase history of the first customers, the current customer’s type, and the distribution of future customer types. We continue using and to denote the expected consumption of product and expected total revenue in the selling horizon with customers. Note that both and depend on the chosen assortment policy and we will specify the policy in the contexts when we discuss them in subsequent sections.

When is deterministic, this setting aligns with Bai et al. (2022). When is stochastic, we decide the initial inventory based on the distribution and the assortment policy. Then the total expected revenue is . Unlike the da case, here we will consider arbitrary distributions of .

2.2 Fluid Relaxation (FR)

We define fluid relaxations (FR) as the optimization problems that maximize fluid approximations of the original expected revenue objective under some constraints. We start by defining these approximations, followed by some preliminary results instrumental to our algorithm and analysis.

We start with da under deterministic . Given the starting inventory , we use the objective value of the CDLP, , as a fluid approximation to the original expected revenue.

| (1) |

relaxes in da problem in two ways: (i) Customers arrive continuously from time to . The customer arriving at time consumes a deterministic infinitesimal amount of product where is the assortment offered at . (ii) We can decide the mix of assortment offered to each customer. Gallego et al. (2015) introduce the following equivalent sales-based formulation (SBLP) under the MNL choice model. In this formulation, each represents the sales of product , and denotes the number of customers making no purchases.

| (2) |

is known to provide an upper bound for , as shown in Gallego and Phillips (2004), Liu and Van Ryzin (2008). Furthermore, is monotone in , since appears on the right-hand side of the inequality constraints in .

Equivalence between and the fluid process without personalization. In the fluid process without personalization (fp), customers arrive continuously and make deterministic purchases but each arriving customer sees all available products. Consider a simple example with a ground set , where both products have inventories , and , with . Thus, the purchase probabilities for both product and are . Initially, the assortment is . The two products are both consumed at the rate of . At time , product runs out, changing the assortment to , with product remaining in stock until . We use fp to denote both the fluid process starting from inventory with customers and the total revenue in the process, and use to denote the consumption of product in fp.

For the MNL model, it is known that equals the revenue in the fp that starts with a subset of the inventory . Moreover, it is straightforward to show this subset of inventory is the optimal starting inventory for the fluid process where the inventory of each product is capped by , i.e., . Moreover, we show that one can construct this optimal inventory by simply setting the inventory of product as the optimal solution to the SBLP. The proof is based on Lemma 8 and Lemma 10 in Goyal et al. (2022), with details in Appendix 7.1.

Lemma 2.1

For any inventory vector and customers, . Moreover, given the optimal solution to the SBLP (2), let for all . Then .

Next, we show there exists an optimal inventory for that has a structure that we define as the generalized revenue-ordered property.

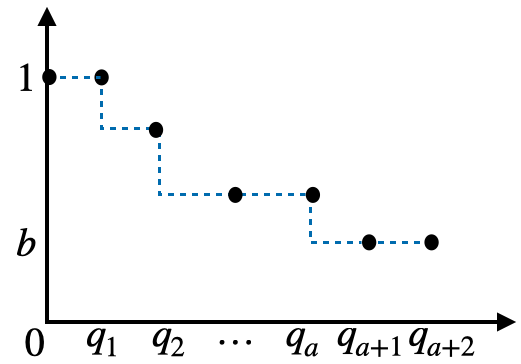

Generalized revenue-ordered property of the optimal starting inventory for the fluid continuous process. When , reduces to the unconstrained static assortment problem with a ground set , where denotes the set of products with positive inventory in . For the MNL model, it is known that there exists a threshold such that products priced above this threshold are included in the optimal assortment, while those below are excluded (Talluri and Van Ryzin 2004). When , we show the optimal starting inventory for the fluid process has a generalized revenue-ordered property: the inventory of products priced above the threshold are fully stocked, whereas those priced below are not stocked. The key distinction is that the product at the threshold price may be partially stocked.

Lemma 2.2 (Generalized revenue-ordered optimal inventory)

Let denote the optimal solution to sales-based CDLP. Define as the highest index for which . We construct an inventory vector as follows:

-

•

For , set ;

-

•

For , set ;

-

•

.

Then .

To show the lemma, we use Lemma 2.1 and observe that sales-based CDLP (2) reduces to a fractional knapsack problem when the decision variable is fixed. The proof is included in Appendix 7.3. From here on, we use to represent the inventory vector with the generalized revenue-ordered property described as in the lemma. Note that technically also depends on but we omit the dependence on for the simplicity of notation. The generalized revenue-ordered structure is crucial for establishing the SO property for (see Section 3) and for the transformation step for da (see Section 4).

Fluid relaxations in other settings. Next, we discuss the fluid relaxations in other settings. For the da problem with stochastic following an IFR distribution, we use as a fluid approximation for the expected revenue. This LP also considers the fluid relaxation of randomness in . One can show that serves as an upper bound on ; see Proposition 7.4 in Appendix 7.4 for details.

For dap, when is deterministic, we use the objective function value of multi-type CDLP as the fluid approximation, denoted as . The multi-type CDLP is a natural generalization of the single-type CDLP considering multiple customer types. A detailed formulation can be found in Appendix 7.5. Notably, serves as an upper bound for the expected revenue in dap for any online assortment policy (Lemma 1 in Golrezaei et al. (2014)). When is stochastic and follows arbitrary distributions, is a weak fluid relaxation, as the ratio between the original expected revenue and the may approach when follows a high-variance distribution (Bai et al. 2023). Instead, we use as the fluid approximation which takes the expectation of over . In , we are not relaxing the stochasticity in , but only in the choices of the customers. Since for any assortment policy, provides an upper bound for under any assortment policy. Perhaps even more important is that upper bounds the revenue under the optimal offline policy that knows the full sequence of arrivals consider optimal inventory whereas Aouad and Ma (2022) and Bai et al. (2023) upper bounds the revenue under the optimal online policy.

For clarity, we summarize the objective functions of the fluid relaxations in the following table.

| da | dap | |

| Deterministic | ||

| Stochastic |

2.3 Submodular Order Property

Given a ground set of elements and a set function , an order is a (strong) submodular order if

Here means . is to the right of in order . Note SO is defined for a set function, and can also be viewed as a set function. Consider an expanded ground set with many copies of each product . Each specifies a subset of the expanded ground set, where is the number of copies of product in . The order is defined for all the items in the expanded ground set. Threshold-based augmentation algorithms can give a -approximate solution to maximize monotone functions with SO property under a cardinality constraint and under a budget constraint. Udwani (2021) shows that the descending order of price is a strong submodular order for the revenue function of static assortment optimization (equivalent to the when ). We extend their result to show that with general has the SO property, as given in Theorem 3.2.

3 Fluid Relaxation Approximation

This section outlines the approximation algorithms for the fluid relaxations (fr). For da, we extend the result in Bai et al. (2022) to get a approximate solution for deterministic in Section 3.1. For dap, our approximation algorithm leverages the SO property of . We first establish the SO property for in Section 3.2 and then introduce the approximate algorithm for maximizing with deterministic in Section 3.3. In Section 3.4, we extend our results to the more general setting where is stochastic.

3.1 Approximation for DA

We start with deterministic . Recall the formulation of the fluid relaxation is as follows:

| (3) |

Recall that is monotone but not submodular, even for . Bai et al. (2022) propose a modified LP formulation wherein the value of is fixed. Let denote the optimal objective value of the sales-based CDLP with fixed at . Bai et al. (2022) show that is submodular in . They fix to and show the function gives a approximation of , thus achieving an overall guarantee of using standard submodular maximization algorithms. However, if we know the optimal value of , we can use the submodular maximization algorithm to achieve a -approximate solution under a cardinality constraint or a budget constraint (Nemhauser et al. 1978, Sviridenko 2004, Badanidiyuru and Vondrák 2014). We show that one can find the near-optimal value of by trying a geometric series of values, thereby achieving performance guarantee. The algorithm details are provided in Appendix 8.1.

Theorem 3.1

Given any accuracy level , can be approximated within a factor of in polynomial time.

Recall that for dap with deterministic , we maximize , where the decision variables in the LP are . It is unclear how to accurately guess the near-optimal values for to improve the approximation guarantee beyond in Bai et al. (2022). Furthermore, this idea cannot be generalized to optimize for dap with stochastic , where we need to guess for different customer types and different . So we take a different algorithmic approach that develops threshold-based augmentation algorithms. First, we establish the SO property for . Leveraging the SO property, we generalize the threshold-based augmentation algorithm for SO functions to maximize for deterministic and for stochastic . It is important to note that we consider the original CDLP, , rather than the modified LP , and we establish the SO property instead of submodularity.

3.2 Submodular Order Property of Single-type CDLP

In this section, we return to consider . Recall that for , it is known that the descending order of price is a submodular order. However, for , proving the SO property becomes more challenging since it requires the structural results of the optimal solutions to LPs. We show that the descending order of price is still a submodular order for , which is formally stated in the following theorem.

Theorem 3.2

For any given , sorting products in descending order of price, breaking ties arbitrarily, is a strong submodular order for . In other words, suppose the products have been sorted in the non-increasing order of prices:, then for any , such that , , we have .

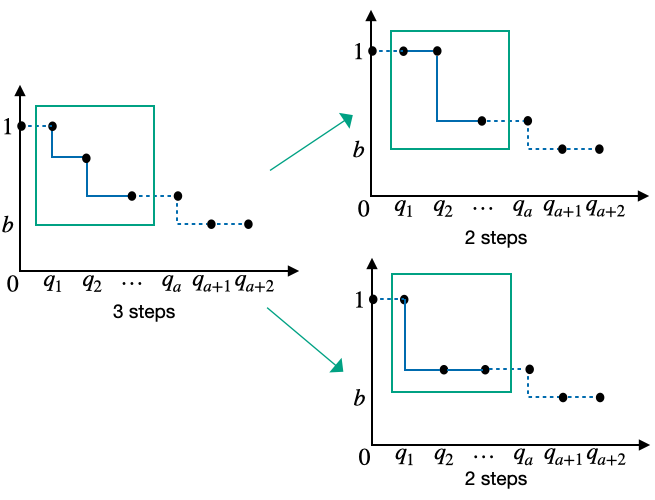

To prove the theorem, we first transform to the revenue in a fluid process starting from inventory , recall that in Lemma 2.2. Then we analyze the structural properties of when changes. We show that only the inventory of product (the lowest-price product) may change. Moreover, we establish a critical lemma, called the Separability Lemma, to analyze the influence of changing the inventory of product on the total revenue in fp. The lemma plays an important role in establishing SO as well as the transformation in Section 4. By separability, we mean that the total revenue from a fluid continuous process that starts with some extra units of product can be divided into two parts:the sales from the additional units of product and the total revenue from a truncated version of the original process. Recall that denotes the consumption of product in fp.

Lemma 3.3 (Separability)

For any inventory vector and customers, consider two fluid processes and . Let denote the extra consumption of product in , given by . Then the following holds:

-

(i)

For product , . For every other product , . In other words, the process can be decomposed into two parts:the process and the consumption of product with probability during the interval .

-

(ii)

.

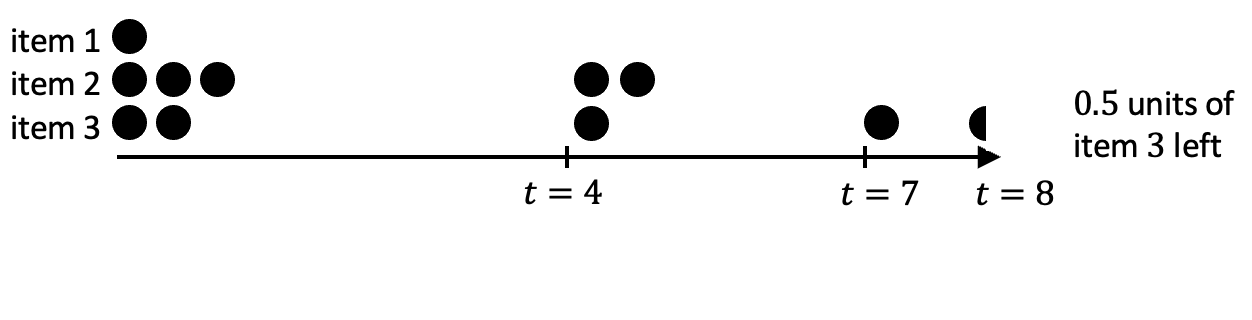

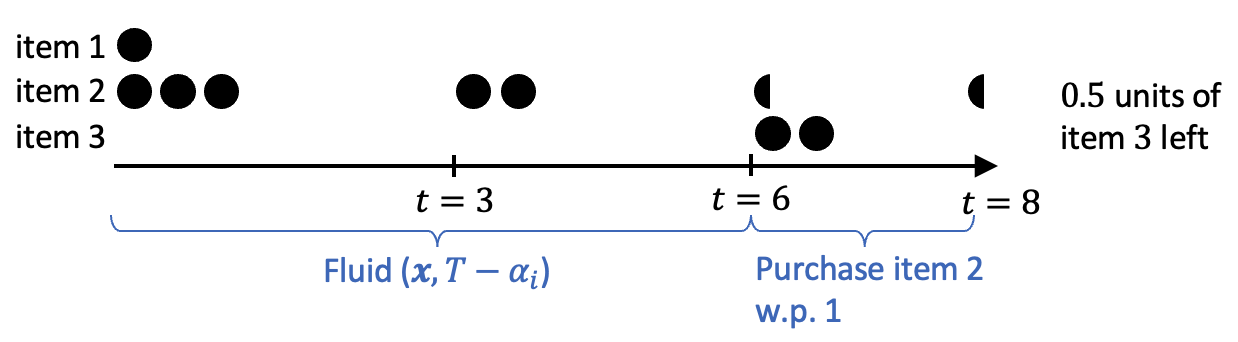

We provide an example to illustrate this lemma. Consider a universe of three products with starting inventory , , . Let and . Then, in , the initial assortment is . By time , product is out of stock, and the assortment changes to . By , product is also out of stock, so customers thereafter can see nothing. Now, suppose that we start with 2 additional units of product 2. The sequence of assortments is visualized in Figure 1(a). Figure 1(b) visualizes the process that consists of two parts:the original process truncated at time , followed by that product is consumed with probability during time . Observe that in both Figure 1 (a) and (b), units of product remain at the end of the selling horizon, and the consumption of all products is identical in the two processes.

The proof of this lemma relies on the Independence of Irrelevant Alternatives (IIA) property of the MNL model. A key observation is that, considering the outside option as a product that never stocks out, the purchase probability of any product before it runs out of stock is times the purchase probability of product . Moreover, the total sales of all products, including , is constantly . The detailed proof is deferred to Appendix 8.2. Next, we proceed to prove Theorem 3.2.

Proof 3.4

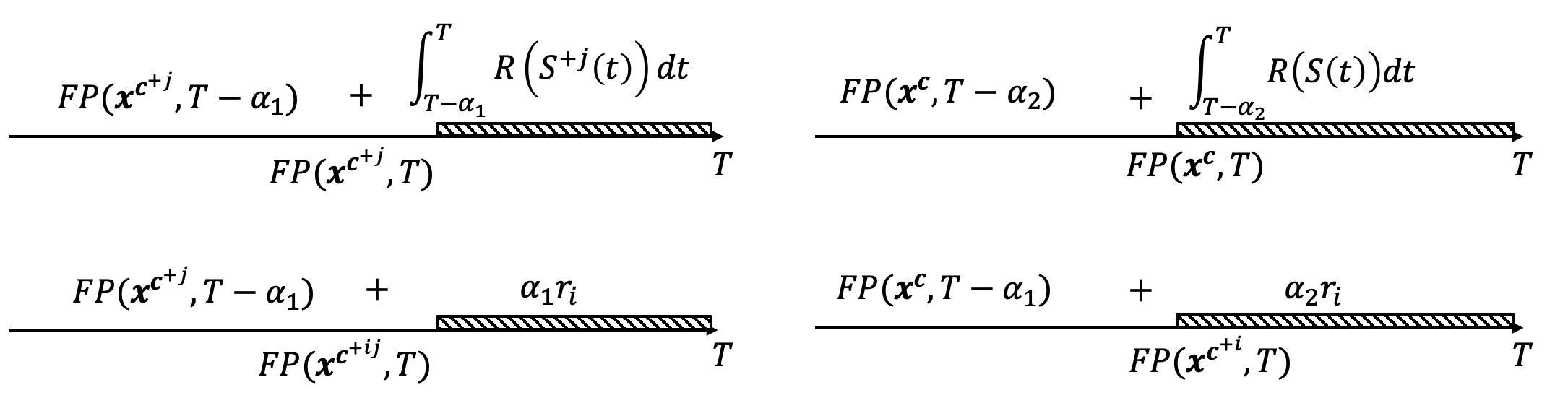

Proof of Theorem 3.2. For clarity and brevity, we introduce the following simplified notation:Let , , denote , , , respectively. Let , , , denote the assortment at time in fp starting from , , , . Recall that (Lemma 2.2), so it suffices to show that

| (4) |

Recall that have established the generalized revenue order property for , which means all the inventory of products before a threshold will be included in . The case is trivial since the right-hand side is nonnegative due to the monotonicity of LP. We further show that when , all the available inventory of products with an index less than is included in , , and , i.e., for all . So we just need to consider the influence of the different number of units of product .

Since both and include inventory of products with an index less than , from Separability Lemma, let , we have:

| (5) |

Intuitively, the marginal benefit comes from replacing the assortment in with selling product with probability . We refer to as the replacement period for and is the length of the replacement period. We visualize the marginal benefit in Figure 2.

Similarly, let , we have:

| (6) |

So we just need to prove , which means the total benefit from replacing the assortment by in the replacement period for is lower than or equal to that in . It suffices to show the following properties: (i) , which means the length of replacement period for is at least as long as that of . (ii) for and for . This means at any time within the replacement periods for both and , the benefit of the replacement is non-negative. (iii) For , . At any time of the replacement period for for , the benefit from replacing the assortment by in is no less than that in . Here (i) and (ii) are shown based on the optimality of for fp and the Separability Lemma. The key to showing (iii) is to observe that due to weak substitutability, and note that has the lowest price among . The complete proof is provided in Appendix 8.3.

3.3 Approximation for DAP

For dap with deterministic , recall we approximately solve the following fluid relaxation in the first step:

| (7) |

When , simplifies to the joint assortment optimization and customization problem under a mixture of MNL, which is proposed by El Housni and Topaloglu (2023). It is known that the descending order of price is a submodular order for the revenue function of this problem (Lemma 10 in Udwani (2021)). For general , does not only decide the quantity of each product to use as , but also how to allocate the inventory across different customer types. Specifically, let denote the optimal solution to , then allocates units of product to customer type . Then the problem structure changes, and perhaps surprisingly, the descending order of prices is not an SO for . We provide a counterexample in Appendix LABEL:app:ce-SO-multitype. This contrasts with the single-type setting, where we establish the SO property for general (Theorem 3.2). Finding other submodular orders appears to be quite challenging.

Let denote the objective function of single-type CDLP under the choice model . Inspired by the fact that and SO property remains closed under additivity, we consider maximizing a new function . We write as for deterministic for simplicity. Here is the inventory allocated to customer type and is the overall inventory allocation vector. So in , the inventory allocation is not fixed by the LP but can be changed arbitrarily. The inventory allocation is called integer allocation if includes only integer components and fractional allocation otherwise. Here is the total stocking level of each product, which must satisfy the constraint . Thus, we now consider the following optimization problem:

| (8) |

In the optimization problem, we decide both the quantity of each product and the amount of inventory assigned to each customer type. It is straightforward to show that (7) and (8) have the same optimal and objective value. Let and denote the optimal solutions to (8).

When is constrained to have integer components, every customer is assigned integer units of every product. We define as product exclusively offered to customer type . Then the optimization problem (8) can be viewed as a subset selection problem on a larger ground set where we create copies of item . As SO remains closed under additivity, the descending order of prices, breaking ties arbitrarily, is a submodular order for on this large ground set. Recall that the threshold-based algorithm gives constant factor guarantees for maximizing monotone SO functions, where we add an item to the set if the marginal benefit exceeds a threshold and the value of depends on , and the items already in the set. We will discuss how to set in Appendix LABEL:app:cdlp-m-T-alg. However, may include fractional componnets. Thus, the approximate solution we obtain by forcing to be integer allocation not be a good approximation to (7). Consider a simple example where there is one single product and two customer types. Suppose the optimal solution to (8) is , , , which means LP assigns units to type and units to type . However, If we restrict attention to integer allocationting, the marginal benefit of adding unit to either type or type may fall below , resulting in no items being added to the inventory. We solve this difficulty by proposing a new threshold-based algorithm that may do the fractional allocation between different customer types. Given , our new threshold based augmentation algorithm is described below. The algorithm for the budget-constrained problem, being similar, is given in Appendix LABEL:app:multi-budget.

Like the standard threshold-based augmentation algorithm for SO functions, now we still iterate over items in the descending order of prices. However, we now calculate the maximum marginal benefit each item can give considering fractional allocation to different customer types. In line 1 of the algorithm above, we calculate the optimal allocation of product that gives the maximum marginal benefit. Here represents the number of units of product allocated to customer type and denotes the optimal allocation. If the maximum benefit exceeds , we include one more unit product in the inventory vector and also update based on the optimal allocation of this item. Consider the previous example that , , . In this new algorithm, we first calculate this item’s optimal allocation, which is . If , we set and . When we select the right value of , . So the new algorithm will output the optimal solution. A straightforward linear program can be used to obtain , and we further show this can be done in time in Appendix LABEL:app:acc. Note in this algorithm, we iterate over all items in the expanded ground set, which may be time-consuming when the size of the expanded ground set is large since we create copies of each product. We show that we just need to iterate over different products; see Section 5 for details.

The complete algorithm is given in Algorithm LABEL:alg:tau-m in Appendix LABEL:app:cdlp-m-T-alg. We show the output of this algorithm provides a approximation guarantee to (7) under a cardinality constraint. The proof leverages the SO property of that allows fractional inventory of products. The SO property still holds for a fractional inventory of products since it is equivalent to the SO property on a larger expanded ground set of items. The proof can be seen in Appendix LABEL:app:prf-3-ap-m-ra-T.

Theorem 3.5

Algorithm LABEL:alg:tau-m outputs a approximate solution to problem 7 under a cardinality constraint.

For the budget constraint, the main difference is that we include one unit of product in the inventory when the maximum marginal benefit over all the customer types exceeds . The algorithm yields a approximate solution; see Appendix LABEL:app:cdlp-m-T-alg for details.

Theorem 3.6

Algorithm LABEL:alg:cdlp-multi-type-budget outputs a approximate solution to problem 7 under a budget constraint.

3.4 Stochastic

So far, we focused on deterministic . We now extend this to stochastic for both da and dap. For da, recall we aim to maximize in the first step. Thus, simply replacing by in the algorithm introduced in 3.1 gives a approximate solution under a cardinality constraint or budget constraint.

For dap with stochastic , recall that we consider the following fluid relaxation in the first step:

| (9) |

In the expectation, each LP, , knows the value of and allocates inventory to different customer types accordingly. Note the allocation can vary for different . The variation adds complexity to analyzing changes in the objective function when changes, making it more challenging to approximate (9). However, still has SO property since the SO property remains closed under additivity. Thus, similar to deterministic , we manually allocate fractional inventory for different customer types and different in the algorithm but keep the inventory vector integer-valued. More specifically, we define and maintain an inventory matrix for each possible value of , denoted by . Here is the maximum in the support of the distribution of . In the algorithm, when examining each product , the difference compared with deterministic is that we first calculate the optimal allocation for each through . Then we calculate the expectation of the maximum marginal benefit over , given by . If the expected benefit exceeds the threshold , we add product to the inventory and update for all . We provide the complete Threshold Add algorithm in Appendix LABEL:app:m-car-stoch-T.

Remark 3.7

To choose the right value of , we still try a geometric series of values. We show this algorithm provides a approximate guarantee under a cardinality constraint. The complete algorithm (Algorithm LABEL:alg:tau-m-DT) and the proof are deferred to Appendix LABEL:app:multi-budget.

Theorem 3.8

Algorithm LABEL:alg:tau-m-DT outputs a approximate solution to problem 9 under a cardinality constraint.

For the budget constraint, we add an item to the inventory if the expected maximum marginal benefit of adding item exceeds . The complete algorithm, referred to as Algorithm LABEL:alg:tau-m-DT-budget, is presented in Appendix LABEL:app:multi-stochT. The output of this algorithm provides a approximate solution.

Theorem 3.9

Algorithm LABEL:alg:tau-m-DT-budget outputs a approximate solution to problem 9 under a budget constraint.

4 Transformation

So far, we have identified a feasible inventory solution that is a constant factor approximation to the fluid optimization problem. We now transform it into a constant factor approximation for the original da and dap problem.

Preliminary Case of a Single Item. To understand the gap between da/dap and fr, we start by considering a simple setting with only one product of inventory , and a single customer type. In da, product is displayed to each customer until the stock is depleted or time runs out, with each customer having a uniform probability of purchasing a unit. Obviously, the optimal online assortment policy in dap will also display it to each customer. Thus, the consumption of product in da and dap are the same. In fr, each customer purchases units in a deterministic fashion until stocks out. When is deterministic, the difference arises only due to the stochasticity of customer choices. Let denote the expected consumption of product in a stochastic consumption process with uniform purchase probability , customers, and inventory . In fr, the consumption is . One can show that , using standard results in the literature on online resource allocation.

Lemma 4.1 (Lemma 5.3 in Alaei et al. (2012))

Given any inventory vector , a product with a uniform purchase probability , and number of customers , it holds that .

When is stochastic, the expected consumption in fr for dap is . Taking expectation over on both sides of the inequality in the above lemma, we have . For da, the consumption in fr is because we consider a fluid relaxation of the uncertainty in T as well as customer choice. It is straightforward to show , using results in Aouad et al. (2018) when follows an IFR distribution. We show this bound is tight when follows a geometric distribution, as seen in Appendix LABEL:app:geo-12. For non-IFR distributions, we show the gap can be arbitrarily large and provide an example in Appendix LABEL:app:exm-nonIFR.

Lemma 4.2 (Lemma 11 in Aouad et al. (2018))

Given any inventory vector , a product with a uniform purchase probability , and assuming follows an IFR distribution with mean , then it holds that .

Challenges with multiple items. When the inventory includes multiple items, bounding the gap between the total expected revenue in da/dap and fr seems to be more challenging. This is mainly due to the dynamic cannibalization effect, which means on some sample paths over customer choice, the low-priced products may not stock out in da/dap after they have sold out in fr. This leads to a lower purchase probability for higher-priced products than fr. In dap, we can easily mitigate this cannibalization effect by not showing the low-price products. However, in da, we are not allowed to change the assortments manually. Thus, the gap between the revenue in da and fr can be arbitrarily large, even for the MNL model. Consider a simple example where there is a single customer and two products, , , , , . The LP will only include product in stock, so . However, the expected revenue in that starts from is since both products are included in . Thus, , which approaches zero as tends to infinity. Therefore, even if we obtain the approximately optimal inventory for , it may not be a good inventory vector for the original problem. We show that the cannibalization effect can be reduced to a single item for a single item, and simply rounding the inventory of this item gives a good inventory solution for da for MNL choice model. For general choice models, however, the inventory vector constructed in this is arbitrarily bad for da, as we will discuss later.

4.1 Assortment policy in DAP problem

In this section, we present the online assortment personalization policy for dap. As previously discussed, in dap, we are allowed to select a subset of available products for each arriving customer, which mitigates the cannibalization effect. Note that the algorithms and performance guarantees discussed herein are not confined to MNL models but work for any choice model with weak substitutability.

4.1.1 Deterministic .

For deterministic , we use independent sampling and rounding algorithm and show that the expected revenue under this policy is at least . Although this algorithm is the same as the algorithm in Bai et al. (2022), we improve the guarantee from to .

Theorem 4.3

Given any , number of customers and any choice model with weak substitutability, let denote the total expected revenue obtained by the assortment policy above, then .

The idea of our proof is to show that when each customer arrives, the expected purchase probability of any product in is no less than that in . Then we can use the single-product result (Lemma 4.1) to obtain . The proof only uses the weak substitutability property and is included in Appendix LABEL:app:thm-tran-d.

4.1.2 Stochastic .

For stochastic , we use the online greedy policy, i.e., provide the subset of the available products with the highest revenue to each arriving customer. It is known that the online greedy algorithm yields a guarantee of without any prior knowledge of (Golrezaei et al. 2014). Consequently, the online greedy algorithm gives a performance guarantee against , even for arbitrary distributions of .

Theorem 4.4 (Corollary 1 in Golrezaei et al. (2014))

Given any and distribution of , let denote the expected revenue obtained by the online greedy algorithm given inventory , then we have .

4.2 Transformation for the DA Problem

In this section, we show how to construct an inventory vector given an approximate solution to fr from the first step, such that the expected revenue in da can be lower bounded by a constant factor of fr.

4.2.1 Deterministic - No ‘bad’ products.

We have shown that under the MNL choice model, the exepcted revenue from the LP () is equivalent to the revenue in the fluid process starting with an inventory with generalized revenue-ordered property (). We start by considering the case that is an integer-valued vector and and show that setting the staring inventory to gives an expected revenue of at least . However, when includes the fractional inventory of some product, these fractional parts can significantly impact the revenue in the fluid process. So we refer to the products with fractional inventory ‘bad’ products. Fortunately, due to our construction of , there can be at most one product with fractional inventory and we show the influence of the fractional item can be bounded for MNL model. We will discuss how to handle this ‘bad’ product later.

To show , it suffices to show the following lemma. Note the results hold for all integer inventory vectors.

Lemma 4.5

Given any inventory vector and product , .

We provide a proof sketch for a simple setting with two products, with inventory and . The complete proof for the general setting is given in Appendix LABEL:app:prf-thm-pro. There are two possible cases in fp: (1) Both products are available until . In this scenario, for each product, the purchase probability in the stochastic process at every moment can only be higher than that in fp, so we can apply the single-item result (4.1) to obtain a . (2) One product stocks out earlier. Without loss of generality, we consider the case that product 2 stocks out earlier than 1, at time . For product 2, we have the same situation as case 1. For product , however, the purchase probability at time in the stochastic consumption process may be lower than that in fp because product may not be depleted at in the stochastic process. If product has a high price and product has a low price, this brings the possibility of low revenue in the stochastic process. In fact, the revenue in the stochastic process is generally much lower than that in fp for the non-MNL choice model; see an example in Appendix LABEL:app:4-1. However, we show the result still holds for the MNL choice model by transforming and into the consumption in two processes with uniform purchase probabilities: For the stochastic consumption process, if at some time , product is not chosen, then conditioned on this, the probability that is chosen is , which is the probability that is chosen when only is available. Since there are at most customers who could have chosen product before , we can lower bound by the expected consumption in a stochastic process with units of product and customers. We have . Next, we consider the consumption in fp. Using Separability Lemma, the consumption of is equal to a process that starts with units of with length . Now we can apply the single-product result to obtain .

4.2.2 Stochastic - No ‘bad’ item.

Then we consider a more general setting where follows an IFR distribution. Recall that in this setting, we consider a fluid relaxation of and use as fr. We still focus on the scenario that is an integer-valued factor. Establishing the performance guarantee for the original expected revenue is more challenging since further considers fluid relaxation of while considers different . We establish novel stochastic inequalities to show a approximation factor. The ratio frequently appears in the pricing literature considering IFR distributions (Dhangwatnotai et al. 2010, Chen et al. 2021). To the best of our knowledge, this is a mere coincidence, as the ratio we analyze involves substantially different quantities.

Lemma 4.6

Consider any inventory vector , for any product , then .

We continue providing a proof sketch with a simple setting with two products, with the complete proof in Appendix LABEL:app:prf-lem-IFRe. Considering the fluid process , there are two possibilities: (1) Both products are available until . In this case, we can use the single-product result (Lemma 4.2) to obtain the bound. (2) Some product stocks out before . Without loss of generality, we consider the case that product depletes before , at time . Recall that when is deterministic, we lower bound the consumption in da by that in a stochastic process of length . However, now is stochastic and could be lower than . To address this, we only consider greater than . Formally, we have . For the consumption in , we again use Separability Lemma to obtain that it is equal to the consumption in fp with length and only product . Thus, it suffices to show . However, the previous single-product bound (Lemma 4.2) cannot be directly applied since we only consider on the left-hand side. Our key technical contribution in this part is to establish this performance guarantee. We show it suffices to establish the ratio for the setting with one product and one unit. Recall that denotes the expected consumption of product in a stochastic consumption process with uniform purchase probability of length and units in stock:

Lemma 4.7

Consider any product with a uniform purchase probability . If follows an IFR distribution and for any integer , suppose , then .

Establishing this lemma is technically involved and may provide insight into other revenue management problems considering IFR distributions. Here, we introduce the high-level idea of our proof and include the complete proof in Appendix LABEL:app:IFRe-2. We formulate a factor-revealing program and show is a lower bound for the program. For any , , . Let , for ; then uniquely characterizes . Since is an IFR distribution, it follows that . We can rewrite and . Then Lemma 4.6 is equivalent to show is a lower bound for the following factor-revealing program.

| (10) | ||||

The second line delineates feasible values and . The last constraint derives from the tail-sum formula for expectation. We show is a lower bound for this program through three steps: (1) we simplify the program by showing the optimal solution must have a constant value for for all beyond a certain index , implying that conditioned on follows a geometric distribution. (2) we identify the structure of the optimal distribution , referred to as ‘shited geometric distribution’. (3) we show the optimal objective value of the program is when restricted to shifted geometric distributions. Here we discuss the second step, which is the most challenging part. The details of other steps are technically involved and deferred to LABEL:app:prf-lem-IFRe. We identify the structure of the optimal distribution as follows.

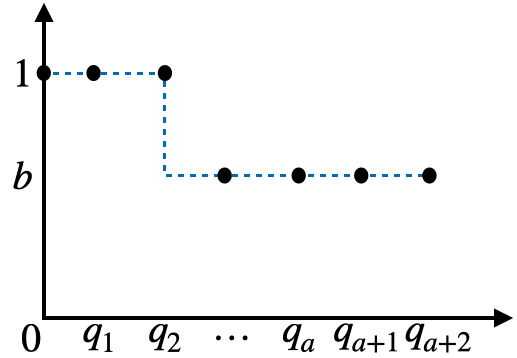

Lemma 4.8

Note that a standard geometric distribution has for all and some constant . If we set , then the distribution of satisfies for all and for . Therefore, we refer to the distributions in the lemma as shifted geometric distributions. To describe the high-level idea of proving this lemma, we define the concept of a step. A step occurs if, for any , (or ). For analytical convenience, we define . Then, a sequence having exactly step characterizes a shifted geometric distribution. In the following, we use figures to illustrate the distributions with varying numbers of steps.

We then prove the optimal must have exactly one step by showing that for any distribution with more than steps, we can always remove one step to obtain a distribution with a lower objective function. So the optimal distribution has at most one step. Figure 4 illustrates the step removal approach. For any such that , we show increasing to or decreasing to yields a lower objective function. In either case, we remove one step.

Remark 4.9

Note that Lemma 4.7 assumes that . If, instead, , we then consider a new distribution with a mean such that . is constructed as follows: for , where . From our derivation,

Here the first inequality holds since has more probability mass only on compared to . The second inequality follows from Lemma 4.7.

4.3 Processing ‘bad’ Products

Let denote the inventory obtained in Section 3, then we have shown that if , then and . However, in general, may not be an integer-valued vector. Since and the constant factor gap between fp and , we essentially want to find an integer-valued vector such that changing the starting inventory from to does not significantly decrease fp. Recall that according to the generalized revenue-ordered structure of (Lemma 2.2), at most one product, specifically the one with the lowest price in , may have fractional inventory. We refer to this item as the ‘bad’ item. Using the Separability Lemma, we show that a simple rounding of the inventory of this ‘bad’ item results in a revenue loss in fp bounded by a factor of at most for any . The rounding procedure is formalized in the following algorithm.

In this algorithm, we keep the inventory of other products except the ‘bad’ item unchanged, and round the inventory of the ‘bad’ item up or down based on which one has a higher revenue in the fluid process. This algorithm is computationally efficient. Calculating can be done in time by using our fast algorithm to solve CDLP (see Appendix LABEL:app:fast_cdlp) and calculating takes time using a straightforward sequencing algorithm (details in Appendix 7.2 for details.

Lemma 4.10

Given any and , let denote the output of Algorithm 4, then .

To prove this lemma, it suffices to show . We use the Separability Lemma to evaluate how keeping or discarding the fractional part of item affects total revenue in fp and formulate a factor-revealing mathematical program to analyze the ratio of to . We show the optimal objective value of the factor-revealing program is . An important observation used in analyzing the factor-revealing program is that the ‘bad’ item has the lowest price. The detailed proof can be found in Appendix LABEL:app:4-prf-T1.

Combining Lemma 4.5 and Lemma 4.10, we have . For stochastic , replacing in Algorithm 4 with yields a . Combining with Lemma 4.6, we have the overall performance guarantee of . Note the factors depend on () and increase as () increase. For small () values, we do not use the output of the algorithms described in this section. Instead, we simply stock one unit of each product in the optimal static assortment. We will discuss the details later in Section 5.1.

5 Approximation Guarantees and Runtime Analysis

In this section, we analyze the overall performance guarantee and runtime of our algorithmic framework. Then we discuss how to accelerate the algorithms further.

5.1 Overall Performance Guarantees

Theorem 5.1

Consider any accuracy level . When is deterministic, da can be approximated within a factor of under a cardinality or budget constraint. When is stochastic and follows a distribution with the IFR property, da can be approximated within a factor of under a cardinality or budget constraint.

We show how to establish the guarantee under a cardinality constraint while the proofs for the budget constraint are similar and deferred to Appendix LABEL:app:5.

When is deterministic, combining Theorem 3.1 and the results in Section 4.3, we obtain an inventory vector such that . Since is an upper bound for (See Section 2), provides a -approximate solution. Note this approximation factor increases as decreases. For small values of , we stock the static assortment as the starting inventory, . Given that the expected revenue obtained from each customer starting from the optimal inventory is less than the expected revenue of the static assortment, we have . Due to the monotonicity of in , it follows that . When , we use as the starting inventory while we use when . Thus, the worst-case performance guarantee is .

When is stochastic, combining Theorem 3.1 and the results in Section 4.3, we obtain an inventory vector such that . Therefore, we have . Here the last inequality is from Proposition 7.4 that is an upper bound for . Similar to deterministic , when , we use as the starting inventory while we use when . Thus, the worst-case performance guarantee is .

Next, we summarize the performance guarantee of dap problem as follows, which is a straightforward combination of Section 3.3 and Section 4.1.

Theorem 5.2

Given any accuracy level , when is deterministic, dap can be approximated within a factor of under a cardinality constraint and under a budget constraint. When is stochastic, for any distribution of , dap can be approximated within a factor of under a cardinality constraint and under a budget constraint.

5.2 Runtime Analysis and Acceleration

Recall that our algorithm framework has two steps. In the second step for both da and dap, we need only to solve the CDLP or a static assortment optimization problem, both of which can be done in polynomial time. Therefore, our primary focus will be on the first step and we will focus on the cardinality constraint.

Recall for da, we try values of . For each value of , we use the standard greedy algorithm to maximize the monotone and submodular functions. In each iteration, we calculate the marginal benefit for all products and add one unit of the product with the maximum marginal benefit. Since is given, calculating the marginal benefit of each product is equivalent to solving a fractional knapsack problem. Since only the inventory of one product changes,it takes time to update the sorting and solve the knapsack problem. Thus, the overall time complexity is .

For dap, recall that in the first step, we iterate over all items in the expanded set and calculate the maximum marginal benefit of each item. The number of queries to calculate the marginal benefit can be very large when the expanded ground set is large. We accelerate the algorithm by iterating only over different products in the ground set (instead of the expanded ground set with many copies) and deciding the inventory of each product. The the query complexity reduces to . Moreover, when examining each product, we use binary search to determine the quantity to add to the inventory. The binary search relies on the fact that the marginal benefit is non-increasing when adding more units of each product. The time complexity of the binary search is for deterministic . The algorithm details and runtime analysis are deferred to Appendix LABEL:app:acc. Thus, the total runtime is . For stochastic , the only difference is just that we need to evaluate the expectation of the marginal benefit over when examining each product. This results in the same overall run time of .

6 Conclusion

In this work, we consider a dynamic assortment optimization problem under the MNL choice model. We develop a unified approximation algorithmic framework for both da and dap. This framework outperforms existing approximation algorithms in terms of speed, approximate guarantees, and also accommodates multiple constraints and a stochastic number of customers. From a technical perspective, we believe that our algorithmic ideas and the novel structural properties of the MNL model can shed light on algorithm design for assortment planning and broader revenue management problems. Further research can consider extending this approximation to other choice models, such as the Nested Logit and Markov Chain choice models. Additionally, we point out that approximating da for general distributions (in polynomial time) remains an interesting open problem.

References

- Alaei et al. (2012) Alaei S, Hajiaghayi M, Liaghat V (2012) Online prophet-inequality matching with applications to ad allocation. Proceedings of the 13th ACM Conference on Electronic Commerce, 18–35.

- Alijani et al. (2020) Alijani R, Banerjee S, Gollapudi S, Munagala K, Wang K (2020) Predict and match: Prophet inequalities with uncertain supply. Proceedings of the ACM on Measurement and Analysis of Computing Systems 4(1):1–23.

- Aouad et al. (2018) Aouad A, Levi R, Segev D (2018) Greedy-like algorithms for dynamic assortment planning under multinomial logit preferences. Operations Research 66(5):1321–1345.

- Aouad et al. (2019) Aouad A, Levi R, Segev D (2019) Approximation algorithms for dynamic assortment optimization models. Mathematics of Operations Research 44(2):487–511.

- Aouad and Ma (2022) Aouad A, Ma W (2022) A nonparametric framework for online stochastic matching with correlated arrivals. arXiv preprint arXiv:2208.02229 .

- Aouad and Segev (2022) Aouad A, Segev D (2022) The stability of mnl-based demand under dynamic customer substitution and its algorithmic implications. Operations Research .

- Badanidiyuru and Vondrák (2014) Badanidiyuru A, Vondrák J (2014) Fast algorithms for maximizing submodular functions. Proceedings of the twenty-fifth annual ACM-SIAM symposium on Discrete algorithms, 1497–1514 (SIAM).

- Bai et al. (2023) Bai Y, El Housni O, Jin B, Rusmevichientong P, Topaloglu H, Williamson DP (2023) Fluid approximations for revenue management under high-variance demand. Management Science .

- Bai et al. (2022) Bai Y, El Housni O, Rusmevichientong P, Topaloglu H (2022) Coordinated inventory stocking and assortment personalization. Available at SSRN 4297618 .

- Chen et al. (2021) Chen N, Li A, Yang S (2021) Revenue maximization and learning in products ranking. Proceedings of the 22nd ACM Conference on Economics and Computation, 316–317.

- Chen et al. (2022) Chen X, Feldman J, Jung SH, Kouvelis P (2022) Approximation schemes for the joint inventory selection and online resource allocation problem. Production and Operations Management 31(8):3143–3159.

- Davis et al. (2013) Davis J, Gallego G, Topaloglu H (2013) Assortment planning under the multinomial logit model with totally unimodular constraint structures. Work in Progress .

- Désir et al. (2014) Désir A, Goyal V, Zhang J (2014) Near-optimal algorithms for capacity constrained assortment optimization. Available at SSRN 2543309.

- Dhangwatnotai et al. (2010) Dhangwatnotai P, Roughgarden T, Yan Q (2010) Revenue maximization with a single sample. Proceedings of the 11th ACM conference on Electronic commerce, 129–138.

- El Housni et al. (2021) El Housni O, Mouchtaki O, Gallego G, Goyal V, Humair S, Kim S, Sadighian A, Wu J (2021) Joint assortment and inventory planning for heavy tailed demand. Columbia Business School Research Paper Forthcoming .

- El Housni and Topaloglu (2023) El Housni O, Topaloglu H (2023) Joint assortment optimization and customization under a mixture of multinomial logit models: On the value of personalized assortments. Operations research 71(4):1197–1215.

- Gallego and Phillips (2004) Gallego G, Phillips R (2004) Revenue management of flexible products. Manufacturing & Service Operations Management 6(4):321–337.

- Gallego et al. (2015) Gallego G, Ratliff R, Shebalov S (2015) A general attraction model and sales-based linear program for network revenue management under customer choice. Operations Research 63(1):212–232.

- Golrezaei et al. (2014) Golrezaei N, Nazerzadeh H, Rusmevichientong P (2014) Real-time optimization of personalized assortments. Management Science 60(6):1532–1551.

- Goyal et al. (2022) Goyal V, Iyengar G, Udwani R (2022) Dynamic pricing for a large inventory of substitutable goods. Available at SSRN .

- Goyal et al. (2016) Goyal V, Levi R, Segev D (2016) Near-optimal algorithms for the assortment planning problem under dynamic substitution and stochastic demand. Operations Research 64(1):219–235.

- Guo et al. (2023) Guo Y, Wang C, Zhang J (2023) A bilevel view for fluid stockout-based substitution. Available at SSRN .

- Honhon et al. (2010) Honhon D, Gaur V, Seshadri S (2010) Assortment planning and inventory decisions under stockout-based substitution. Operations research 58(5):1364–1379.

- Kök et al. (2015) Kök AG, Fisher ML, Vaidyanathan R (2015) Assortment planning: Review of literature and industry practice. Retail supply chain management: Quantitative models and empirical studies 175–236.

- Liang et al. (2021) Liang A, Jasin S, Uichanco J (2021) Assortment and inventory planning under dynamic substitution with mnl model: An lp approach and an asymptotically optimal policy. Technical report, Tech. rep., University of Michigan, Ann Arbor, MI.

- Liang et al. (2023) Liang Y, Mao X, Wang S (2023) Online joint assortment-inventory optimization under mnl choices.

- Liu and Van Ryzin (2008) Liu Q, Van Ryzin G (2008) On the choice-based linear programming model for network revenue management. Manufacturing & Service Operations Management 10(2):288–310.

- Ma and Simchi-Levi (2020) Ma W, Simchi-Levi D (2020) Algorithms for online matching, assortment, and pricing with tight weight-dependent competitive ratios. Operations Research 68(6):1787–1803.

- Ma et al. (2021) Ma W, Simchi-Levi D, Zhao J (2021) Dynamic pricing (and assortment) under a static calendar. Management Science 67(4):2292–2313.

- Mahajan and Van Ryzin (2001) Mahajan S, Van Ryzin G (2001) Stocking retail assortments under dynamic consumer substitution. Operations Research 49(3):334–351.

- Meyer (1977) Meyer J (1977) Second degree stochastic dominance with respect to a function. International Economic Review 477–487.

- Mouchtaki et al. (2021) Mouchtaki O, El Housni O, Gallego G, Goyal V, Humair S, Kim S, Sadighian A, Wu J (2021) Joint assortment and inventory planning under the markov chain choice model. Columbia Business School Research Paper Forthcoming .

- Nemhauser et al. (1978) Nemhauser GL, Wolsey LA, Fisher ML (1978) An analysis of approximations for maximizing submodular set functions—i. Mathematical programming 14(1):265–294.

- Rusmevichientong et al. (2010) Rusmevichientong P, Shen ZJM, Shmoys DB (2010) Dynamic assortment optimization with a multinomial logit choice model and capacity constraint. Operations research 58(6):1666–1680.

- Rusmevichientong et al. (2020) Rusmevichientong P, Sumida M, Topaloglu H (2020) Dynamic assortment optimization for reusable products with random usage durations. Management Science 66(7):2820–2844.

- Rusmevichientong and Topaloglu (2012) Rusmevichientong P, Topaloglu H (2012) Robust assortment optimization in revenue management under the multinomial logit choice model. Operations research 60(4):865–882.

- Segev (2015) Segev D (2015) Assortment planning with nested preferences: Dynamic programming with distributions as states? Available at SSRN 2587440 .

- Strauss et al. (2018) Strauss AK, Klein R, Steinhardt C (2018) A review of choice-based revenue management: Theory and methods. European journal of operational research 271(2):375–387.

- Sviridenko (2004) Sviridenko M (2004) A note on maximizing a submodular set function subject to a knapsack constraint. Oper. Res. Lett. 32(1):41–43, ISSN 0167-6377, URL http://dx.doi.org/10.1016/S0167-6377(03)00062-2.

- Szpektor et al. (2011) Szpektor I, Gionis A, Maarek Y (2011) Improving recommendation for long-tail queries via templates. Proceedings of the 20th international conference on World wide web, 47–56.

- Talluri and Van Ryzin (2004) Talluri K, Van Ryzin G (2004) Revenue management under a general discrete choice model of consumer behavior. Management Science 50(1):15–33.

- Udwani (2021) Udwani R (2021) Submodular order functions and assortment optimization. URL http://dx.doi.org/10.48550/ARXIV.2107.02743.

7 Additional Formulations and Proofs in Section 2

7.1 Proof of lemma 2.1

The proof is based on Lemmas 8 and 10 of Goyal et al. (2022), as detailed below.

Lemma 7.1 (Lemma 8 and 10 in Goyal et al. (2022))

Given any feasible solution to the sales-based formulation of CDLP (2) with inventory and periods , let for all . Then .

This lemma essentially says that if we set the starting inventory of each product as a feasible solution to the sales-based CDLP, then the inventory will be depleted within the selling horizon. Therefore, the revenue in fp is equal to the objective function of the CDLP.

Proof 7.2

Proof of Lemma 2.1. We show that given any feasible solution to , one can construct a feasible solution to with the same objective function value and vise versa.

Let denote a feasible solution to CDLP. Then if we set by , is a feasible solution to since . Moreover, from Lemma 7.1, all inventory in will be depleted, thus .

Let be a feasible solution to , so for all . Then let for all ( is the number of customers who do not make purchases). Obviously, . So, we just need to show that is a feasible solution to CDLP, i.e, , . Since is the consumption of in and , we have . Due to the Independence of Irrelevant Alternatives (IIA) property, we have . So , for all . \Halmos

7.2 Sequencing Algorithm

The Sequencing algorithm is introduced in Goyal et al. (2022), the algorithm outputs a nested sequence of assortments that appear in the fluid process and their time durations.

In the algorithm, is the th assortment appearing in the fluid process. In Line 3, calculates the first product that stocks out after current time .

7.3 Proof of Lemma 2.2

Proof 7.3

Proof of Lemma 2.2. When is fixed, the problem simplifies to a knapsack problem:

This is a knapsack problem, so there exists an optimal solution satisfying the following structure:There is an item , such that for , for , and . Given the starting inventory , where for all , according to Lemma 7.1, all the inventory in will be depleted, . Consequently, . Therefore, to prove this lemma, it suffices to show that .

Note the difference between and arises only for , where . If , then . For , product is available until the end of the fluid process . Thus, adding more units of item does not alter the fluid process. Hence, . \Halmos

7.4 Proposition 7.4

Proposition 7.4

serves as an upper bound to .

Proof 7.5

Proof of Proposition 7.4. The proof is an adaptation from Liu and Van Ryzin (2008) and the key is to show we can construct a feasible solution to that provides an upper bound for .