These authors contributed equally to this work.

[1]\fnmDingwen \surZhang \equalcontThese authors contributed equally to this work.

1]\orgdivSchool of Mathematics, \orgnameJilin University, \orgaddress\streetQianjin Street, \cityChangchun, \postcode130012, \stateJilin, \countryChina

Statistical inference for multi-regime threshold OrnsteinUhlenbeck processes

Abstract

In this paper, we investigate the parameter estimation for threshold OrnsteinUhlenbeck processes. Least squares method is used to obtain continuous-type and discrete-type estimators for the drift parameters based on continuous and discrete observations, respectively. The strong consistency and asymptotic normality of the proposed least squares estimators are studied. We also propose a modified quadratic variation estimator based on the long-time observations for the diffusion parameters and prove its consistency. Our simulation results suggest that the performance of our proposed estimators for the drift parameters may show improvements compared to generalized moment estimators. Additionally, the proposed modified quadratic variation estimator exhibits potential advantages over the usual quadratic variation estimator with relatively small sample sizes. In particular, our method can be applied to the multi-regime cases (), while the generalized moment method only deals with the two regime cases (). The U.S. treasury rate data is used to illustrate the theoretical results.

keywords:

Threshold OrnsteinUhlenbeck process, Least squares estimator, Modified Quadratic variation estimator, Strong consistency, Asymptotic normality1 Introduction

Let be a complete probability space equipped with a right continuous and increasing family of -algebra and be a one-dimensional Brownian motion adapted to . The threshold OrnsteinUhlenbeck (OU) process is defined as the unique solution to the following threshold stochastic differential equation (SDE)

| (1.1) |

where are the drift parameters, satisfy are the so-called thresholds, is the diffusion parameter, is the initial value of the process , and denotes the indicator function. Moreover, we assume that and are larger than zero to ensure the ergodicity of . The existence and uniqueness of the solution to Eq. (1.1) follow, for example, from the results of [1]. Suppose that the discretely observed process is observed at the regularly spaced time points where is the mesh size and is the sample size. In this paper, we aim to propose the least squares estimators (LSEs) for the unknown parameters and based on either the continuously observed process or discretely observed process , respectively. Furthermore, we propose the quadratic variation estimator (QVE) and the modified quadratic variation estimator (MQVE) for the diffusion parameters.

As useful stochastic dynamics models, threshold diffusion processes have been extensively employed in numerous fields. The threshold autoregressive models are introduced to model the nonlinearities in nonlinear time series [see, e.g., 2, 3]. In finance, [19] show that an exponential form of the threshold process generalizes the Black-Scholes model in a way to model leverage effects. [8] model the surplus of a company after the payment of dividends, which are paid only if the profits of the company are higher than a certain threshold. The threshold processes also have numerous applications in physics [see, e.g. 23, 24], meteorology [see, e.g. 11], forecast [see, e.g. 3], and they are in close contact with the skew diffusion processes [see, e.g. 6, 9].

For threshold OU processes, [5] proposes a LSE for a stationary ergodic threshold autoregressive model and proves its consistency and limiting distribution. [26, 27] study the asymptotic behavior of the quasi-likelihood estimator of a diffusion with piecewise regular diffusivity and piecewise affine drift with an unknown threshold. They provide a hypothesis test to decide whether or not the drift is affine or piecewise affine. [20] propose the maximum likehood estimator (MLE) for the drift parameters, with both drift and diffusion coefficients constant on the positive and negative axis, yet discontinuous at zero. [15] studies the asymptotic behavior of the maximum likelihood estimator and Bayesian estimator for the threshold parameter. He also discusses the possibility of the construction of the goodness-of-fit test. [21] discuss the (quasi)-MLE of the drift parameters, both assuming continuous and discrete time observations. [12] propose a generalized moment estimator (GME) to estimate the drift parameter based on the discretely observed process. Their main theoretical basis is the celebrated ergodic theorem. [13] propose the trajectory fitting estimators for the drift parameters and obtain the asymptotic behavior of the estimators. We also draw attention to a related piece of work by [29], in which they propose an estimator for the drift parameter of a skew OU process.

Based on the celebrated Girsanov’s theorem for semimartingales, one could obtain the log-likehood function, and the MLE for the drift parameter is derived by minimizing the log-likehood function [26, 27, 21]. The generalized moment method could deal with low-frequency data such as the gross domestic product. However, it is significantly more complicated to explore the case [see 12]. In this paper, we apply the least squares method to deal with the drift parameter estimation problem based on a continuously observed process and a discretely observed process, respectively.

The remainder of this paper is organized as follows. In Section 2, we introduce some basic facts on the stationary and ergodic properties of threshold OU processes. In Section 3 and 4, we construct the LSEs for the drift parameters based on continuous sampling and discrete sampling. We prove the strong consistency and asymptotic normality of the proposed LSEs. In section 5, we consider a general threshold OU process, and propose the QVEs and the MQVEs for the diffusion parameters . The results of our simulation studies are reported in Section 6, exhibiting improved performance versus the generalized moment method in two-regime cases. In the case of multi-regime, our proposed LSEs and MQVEs have great performance. We also show an application of our method in the U.S. treasury rate. Section 7 concludes with some discussion on the further work.

2 Preliminaries

In this section, we first introduce some basic facts on the stationary and ergodic properties of threshold OU processes. Throughout this paper, we shall use the notation “” to denote “almost sure convergence”, the notation “" to denote “convergence in probability”, and the notation “” or “” to denote “the convergence in distribution of or to where follows a normal distribution with mean and variance ”. For the convenience of the following description, we make a notation , .

The following proposition, adopt from Proposition 3.1 of [2], Section 1 of [4], and Proposition 1 of [12], shows that the process has a unique invariant density.

Proposition 1.

If the drift parameters , , , and satisfy

the unique invariant density of the process is given by

| (2.1) |

where are uniquely determined by the following equations

The following proposition, based on basic stability theories of Markov processes, describes the ergodic properties of threshold OU processes [see Lemma 1 of 12].

Proposition 2.

Remark 1.

When , , the sufficient and necessary condition for the ergodic properties of the threshold OU process is

Let be the covariation process of and , and . The following proposition, consider the representation of martingale, i.e., we treat the continuous local martingale as a time-changed Brownian motion [see Theorem 1.6, Chapter 5, p.188 of 22].

Proposition 3.

If is a -continuous local martingale vanishing at and such that , then we have the following results.

-

(1)

is the so-called Dambis, Dubins-Schwarz Brownian motion and , where

-

(2)

The law of large numbers for continuous local martingale:

-

(3)

The central limit theorem for continuous local martingale:

-

(4)

The law of the iterated logarithm:

Remark 2.

For the proof of (1) of Proposition 3, one can refer to Theorem 1.6, Chapter 5, p.188 of [22]. While (2) of Proposition 3 follows from Corollary 1, Chapter 2, p.144 of [17]. And (3) of Proposition 3 can be obtained by the distribution of Brownian motion, i.e., , for all . Furthermore, (4) of Proposition 3 is obtained by the law of the iterated logarithm [see Theorem 11.1, Section 11.1, p.165 of 25] of Brownian motion, i.e.,

3 The LSE based on continuous sampling

In this section, we construct the continuous-type LSEs for the parameters and , , and prove their consistency and asymptotic normality based on the continuous observations. We separate the discussion into two subsections: the first subsection considers that the drift term is known to be piecewise linear with , while the second subsection considers that the drift term is known to be piecewise linear with unknown and not vanishing piecewise constants .

3.1 Estimate for known and

In this case, the SDE becomes

| (3.1) |

When there is only one regime, i.e., is a standard OU process, the continuous-type LSE for is given by minimizing the following objective function [see for example 14, 10, and the references therein]

The minimum is achieved at

When there are multiple regimes, the continuous-type LSE for is motivated by the following heuristic argument, which aims to minimize

where denotes the formal derivative of with respect to . This is a quadratic function of , , although does not exist. The minimum is achieved at

| (3.2) |

By Eq. (3.1), the facts that and , for , we have

Recall the unique invariant density of , we define

| (3.3) |

The asymptotic behavior of our estimators is given as follows.

Theorem 1.

Proof of Theorem 1. Let

where

To prove the strong consistency, it suffices to show that converges to zero almost surely as . It is obvious that the quadratic variation process of is exactly . By Eq. (2.2), we have

| (3.4) |

Note that is a continuous local martingale. Then by (2) of Proposition 3 and Eq. (3.4), we conclude

which completes the proof of the strong consistency.

3.2 Estimate and for known

In this case, and the SDE becomes

| (3.6) |

The continuous-type LSEs for and aim to minimize the following objective function

which is a quadratic function of and , . By some direct calculations, the minimum is achieved at

| (3.7) | ||||

where . For simplicity, we make some notations as follows

| (3.8) | ||||

The asymptotic behavior of the proposed estimators and is demonstrated in the following theorem.

Theorem 2.

For , the continuous-type LSEs and defined in Eq. (3.7) have the following statistical properties.

-

(1)

The continuous-type LSEs and admit the strong consistency, i.e.,

-

(2)

The continuous-type LSEs and admit the asymptotic normality, i.e.,

as , where , and are defined in Eq. (3.8). Furthermore, the joint distribution of the continuous-type LSEs and is given by

Proof of Theorem 2. By Eq. (3.6), we have

| (3.9) | ||||

Hence, substituting Eq. (3.7)(3.9) into Eq. (3.9) yields

where

To prove the consistency of and , it suffices to prove that and converge to zero almost surely. By Eq. (2.2), we have

| (3.10) | ||||

On the one hand, by Eq. (3.10), we have

| (3.11) |

By It’s isometry, the dominated convergence theorem, and Eq. (3.10), we have

and

Hence, we have

By (2) of Proposition 3, we have

| (3.12) |

Hence, we have

| (3.13) |

This completes the proof of strong consistency.

Furthermore, by (3) of Proposition 3, we have

| (3.14) |

as . Combining Eq. (3.11)-(3.14), and Slutsky’s theorem yields

as , which implies

| (3.15) | ||||

as . Thus, we complete the proof of the asymptotic normality.

Now we consider the joint distribution of and . By Eq. (3.11) and the dominated convergence theorem, the limit of the covariance for and is given by

By Eq. (3.10) and the dominated convergence theorem again, we have

Hence, we have

| (3.16) |

Remark 3.

It is obvious that for and . For all , we have

| (3.17) | ||||

From Eq. (3.17) we have that is independent of , and is independent of as .

Remark 4.

The maximum likehood method and the least squares method yield the same objective function, as well as the formula of the estimators. Hence, the asymptotic behavior of the MLE and the LSE is also the same [26, 21]. The two methods could deal with the cases of multiple thresholds with less calculations, which is a great improvement compared to the generalized moment methods.

4 The LSE based on discrete sampling

Assume that X is observed at regularly spaced time points . In this section, we shall construct the discrete-type LSEs for the parameters and , and prove their consistency and asymptotic normality based on the discretely observed process . It is evident that one often encounters practical difficulties in obtaining a completely continuous observation of the sample path, and only the discretely observed process is possible. In this situation, one can approximate the (stochastic) integral by its “Riemann-It" sum to directly modify the continuous-type estimators to the discrete ones [see, e.g. 20, 16, 21]. However, we obtain the discrete-type estimators by constructing the contrast function. The discussion in this section is separated into two subsections as Section 3.

To study the strong consistency and asymptotic normality of the LSEs for the drift parameters, we impose two hypotheses which propose the joint restrictions on the mesh size and the sample size . Furthermore, depends on n.

Hypothesis 1.

and , as .

Hypothesis 2.

, as .

The Hypothesis 1 guarantees that the strong consistency holds, while the Hypothesis 1-2 guarantee that the asymptotic normality holds.

4.1 Estimate for known and

In this case, the threshold OU process is the solution to Eq. (3.1). To obtain the LSEs for , we introduce the following contrast function

This is a quadratic function of , , and the minimum is achieved at

| (4.1) |

for .

The asymptotic behavior of our estimators is given as follows.

Theorem 3.

Proof of Theorem 3. Note that

| (4.2) |

where . Hence, we have

where

Now, it suffices to show that and converge to zero almost surely. By Eq. (2.2), we have

| (4.3) |

where is defined in Eq. (3.3). Given , is a Gaussian process with finite mean and finite variance. Additionally, the -th moment of is finite for , which implies , a.s. Let . By Eq. (4.2), we have

| (4.4) | ||||

When , we have that . By Gronwall’s inequality and the law of the iterated logarithm, we have

| (4.5) | ||||

which goes to zero as . There exists a constant such that for . Without loss of generality, we could choose . Then we decompose into three terms as follows

| (4.6) |

where

For all , we have

We thus have

Furthermore, by Eq. (2.2), we have

Hence, we have

| (4.7) |

Note that

Let and be the quadratic variation process of . By Eq. (2.2), we have

By (2) of Proposition 3, we have

| (4.8) |

Combining Eq. (4.3), (4.7), and (4.8) completes the proof of the strong consistency.

4.2 Estimate and for known

In this case, the threshold OU process is the solution to Eq. (3.6). To obtain the discrete-type LSEs for and , we introduce the following contrast function

This is a quadratic function of and , , and the minimum is achieved at

where

The asymptotic behavior of the proposed estimators and are given as follows.

Theorem 4.

Proof of Theorem 4. Note that

| (4.11) |

Hence, we have

where

For all , is a Gaussian random variable with finite mean and finite variance, which implies that , a.s. Let and . By some similar arguments as Eq. (4.4) and (4.5), we have

| (4.12) | ||||

It is non-trivial to show that , , , and converge to zero. There exists a constant such that for . By Eq. (4.12), we decompose into three terms as Eq. (4.6). Furthermore, we have

For all , we have

which implies

Furthermore, by Eq. (2.2), we have

From that , we have

which implies

Similarly, we have

Hence, we have

For and , by Eq. (4.12), we deduce

Hence, we have

Then, by Eq. (2.2), we have

and

Using Eq. (2.2) again yields

where , and are defined in Eq. (3.10). Hence, we have

| (4.13) |

Furthermore, we have

| (4.14) | ||||

which tend to as . Let and . Then we have

Let and be the quadratic variation process of and respectively. By Eq. (2.2), we have

By (2) of Proposition 3, we have

Furthermore, we have

| (4.15) | ||||

By Eq. (4.14)-(4.15), we complete the proof of the strong consistency.

Now, we are in a position to prove the asymptotic normality. By Eq. (4.14), we have

| (4.16) | ||||

which tend to zero as . By (3) of Proposition 3, we have

| (4.17) |

as . Combining Eq. (4.13), (4.16)-(4.17), and Slutsky’s theorem yields

| (4.18) | ||||

as .

Now we are in a position to prove the joint distribution of and . Similar arguments as those to derive Eq. (3.16) yield

| (4.19) |

Remark 5.

Remark 6.

When the observations are discrete, [21] propose the discretized likehood function by approximating the (stochastic) integral by its “Riemann-It” sum. The least squares estimator is proprosed by discretizing the SDE and minimizing the sums of squares of error. The two methods yield the same formula for estimators, as well as the asymptotic behavior.

5 Parameter estimation for

In [18], they study the asymptotic behavior of estimators for the oscillating Brownian motion, i.e., a two-valued, discontinuous diffusion coefficient of a SDE as follows

| (5.1) |

where .

Now, we consider a generalized SDE of the form

| (5.2) |

where , are the diffusion parameters and the others keep the same as Eq. (1.1). The LSEs for and proposed in Section 3 and 4 are suitable in this case when long-time observations are available. Hence, in this section, we focus on the problem of proposing estimators for . The SDE (5.1) is a special case of the above SDE (5.2), i.e., the drift term is zero, , and the only threshold is zero. Motivated by [18], we shall propose the QVEs for the diffusion parameters .

Recall that QVE stands for quadratic variation estimator and MQVE stands for modified quadratic variation estimator. Based on the continuously observed process , we define the QVEs for as follows

| (5.3) |

where . We emphasize that the QVEs only need short time observations, i.e., .

Denote by the local time at a point , which represents the time spent by at until , which means

The following theorem shows the strong consistency of the continuous type QVEs .

Theorem 5.

For all , the continuous-type QVEs of defined in Eq. (5.3) admit the strong consistency, i.e., , a.s.

Proof of Theorem 5. Decompose the regimes into three cases where , , and . We give the proof of the third case and the proof of the other two cases is similar.

Consider the following process

Hence, we have

Using Meyer-Tanaka’s formula for yields

By the fact that , we have

where and . Furthermore, we have

Note that is a martingale with quadratic variation

which implies that . Furthermore, the local time , , and are continuous, and is of finite variation. Thus, , , , , and equal to zero almost surely, which implies

Hence, we complete the proof.

For any finite time interval , we consider the discretely observed process in given by and . Let and . Then we define the discrete-type QVE as follows

where .

The following theorem shows the weak consistency of the discrete type QVEs .

Theorem 6.

Assume that and . Then the discrete-type QVEs admit the weak consistency, i.e.,

Proof of Theorem 6. Let . By Eq. (4.11), we have

where

Recall the definition of and , we have

By some trivial calculations, we have

| (5.4) |

Since the quadratic variation of a martingale can be approximated by the sum of squared increments over shrinking partitions, we have

Then we have

| (5.5) |

By the scaling properties of the increments of the Brownian motion, we have

| (5.6) |

Thus, we complete the proof.

Now we consider MQVEs for the diffusion parameters . The main idea is to obtain the consistent estimators for the drift parameters and first. Then we could minimize the error made by the drift term as much as possible. Hence, we need the long-time observations.

When the continuously observed process is obtained, the continuous-type MQVEs for are defined as

where .

The following theorem shows the strong consistency of the continuous-type MQVEs .

Theorem 7.

The continuous-type MQVEs admit the strong consistency, i.e.,

Proof of Theorem 7. According to (1) of Theorem 2, we have

By Eq. (1.1), we have

Hence, we have

Furthermore, the quadratic variation of is given by

which yields

When the long time discretely observed process is obtained, i.e., , , and , the discrete-type MQVEs for are defined as

In the following theorem, we demonstrate the consistency of the MQVE.

Theorem 8.

Under the Hypothesis 1, the discrete-type MQVEs admit the weak convergence, i.e.,

Proof of Theorem 8. Let . By Eq. (4.11), we have

where

On the one hand, similar arguments as Eq. (5.5) and (5.6) yield

On the other hand, we now consider the error term , which is the main improvement of MQVEs compared with QVEs . Decomposing into three terms as Eq. (4.6) yields

When , by Eq. (4.12), and (4.21)-(4.22), we have

We thus have

By Eq. (2.2), we have

Hence, we have

Hence, we complete the proof.

Remark 7.

The main improvement of MQVEs compared with QVEs is to give the consistent estimators for the drift parameters, which ensures us to eliminate the error term .

6 Numerical Results and Applications

6.1 Numerical results

In this section, we will conduct simulation studies to check the performance of the proposed estimators and compare our estimators with the GMEs proposed in [12]. Note that it is significantly more complicated to explore the multiple thresholds case by the generalized moment approach. Hence, we consider the following three scenarios.

-

Scenario 1

(Multi-regime). Set , , , , the two thresholds and . We study the LSEs for and , and compare the QVEs with MQVEs for .

-

Scenario 2

(Two-regime) Set , , , , and . We compare our estimators with the GMEs for .

-

Scenario 3

(Two-regime) Set , , , , and . We compare our estimators with the GMEs for and .

| Sample sizes | ||||||

|---|---|---|---|---|---|---|

| 1000 | 2000 | 3000 | 4000 | 5000 | ||

| bias | 0.082 | 0.020 | 0.021 | 0.004 | 0.007 | |

| Std.dev | 0.412 | 0.291 | 0.247 | 0.198 | 0.183 | |

| bias | 0.054 | -0.026 | 0.030 | 0.032 | 0.018 | |

| Std.dev | 1.270 | 0.878 | 0.693 | 0.626 | 0.549 | |

| bias | 0.150 | 0.079 | 0.039 | 0.020 | 0.023 | |

| Std.dev | 0.917 | 0.625 | 0.507 | 0.439 | 0.377 | |

| bias | -0.064 | -0.011 | -0.013 | -0.001 | -0.004 | |

| Std.dev | 0.432 | 0.308 | 0.262 | 0.215 | 0.194 | |

| bias | -0.001 | -0.001 | 0.008 | -0.008 | -0.008 | |

| Std.dev | 0.372 | 0.250 | 0.215 | 0.177 | 0.169 | |

| bias | 0.109 | 0.088 | 0.024 | 0.007 | 0.019 | |

| Std.dev | 1.344 | 0.954 | 0.785 | 0.671 | 0.576 | |

| Sample sizes | |||||||

|---|---|---|---|---|---|---|---|

| 1000 | 2000 | 3000 | 4000 | 5000 | |||

| bias | -0.016 | -0.006 | -0.005 | -0.003 | -0.001 | ||

| Std.dev | 0.049 | 0.028 | 0.021 | 0.018 | 0.015 | ||

| bias | -0.008 | -0.008 | -0.009 | -0.008 | -0.007 | ||

| Std.dev | 0.036 | 0.026 | 0.020 | 0.018 | 0.015 | ||

| bias | 0.003 | 0.002 | -0.001 | 0.000 | -0.001 | ||

| Std.dev | 0.079 | 0.054 | 0.046 | 0.038 | 0.035 | ||

| bias | -0.001 | -0.001 | -0.003 | -0.002 | -0.004 | ||

| Std.dev | 0.079 | 0.054 | 0.046 | 0.038 | 0.035 | ||

| bias | -0.045 | -0.017 | -0.008 | -0.005 | -0.003 | ||

| Std.dev | 0.207 | 0.111 | 0.091 | 0.075 | 0.065 | ||

| bias | -0.028 | -0.033 | -0.027 | -0.027 | -0.026 | ||

| Std.dev | 0.166 | 0.109 | 0.090 | 0.074 | 0.065 | ||

| bias | 0.006 | 0.003 | 0.002 | 0.001 | 0.001 | ||

| Std.dev | 0.035 | 0.026 | 0.019 | 0.017 | 0.015 | ||

| bias | 0.089 | 0.088 | 0.089 | 0.088 | 0.088 | ||

| Std.dev | 0.035 | 0.026 | 0.020 | 0.018 | 0.016 | ||

| bias | -0.005 | -0.002 | 0.001 | -0.001 | 0.001 | ||

| Std.dev | 0.078 | 0.057 | 0.045 | 0.038 | 0.034 | ||

| bias | 0.016 | 0.017 | 0.021 | 0.018 | 0.021 | ||

| Std.dev | 0.079 | 0.058 | 0.046 | 0.039 | 0.035 | ||

| bias | 0.008 | 0.007 | 0.006 | 0.002 | 0.002 | ||

| Std.dev | 0.141 | 0.098 | 0.081 | 0.072 | 0.063 | ||

| bias | 0.260 | 0.264 | 0.262 | 0.260 | 0.261 | ||

| Std.dev | 0.150 | 0.104 | 0.088 | 0.078 | 0.068 | ||

| Least squares estimator | Generalized moment estimator | ||||

|---|---|---|---|---|---|

| n | bias | Std.dev | bias | Std.dev | |

| 1000 | 0.034 | 0.186 | 0.006 | 0.203 | |

| 0.061 | 0.321 | -0.123 | 0.375 | ||

| 2000 | 0.012 | 0.131 | -0.030 | 0.138 | |

| 0.022 | 0.211 | -0.141 | 0.248 | ||

| 3000 | 0.012 | 0.104 | -0.034 | 0.111 | |

| 0.013 | 0.177 | -0.165 | 0.210 | ||

| 4000 | 0.018 | 0.090 | -0.045 | 0.096 | |

| 0.016 | 0.150 | -0.172 | 0.175 | ||

| 5000 | 0.018 | 0.079 | -0.051 | 0.083 | |

| 0.018 | 0.138 | -0.175 | 0.158 | ||

| Least squares estimator | Generalized moment estimator | ||||

|---|---|---|---|---|---|

| n | bias | Std.dev | bias | Std.dev | |

| 1000 | 0.031 | 0.197 | -0.345 | 0.136 | |

| 0.101 | 0.478 | -0.056 | 0.562 | ||

| -0.006 | 0.075 | 0.337 | 0.084 | ||

| 0.008 | 0.110 | -0.030 | 0.293 | ||

| 2000 | 0.020 | 0.140 | -0.349 | 0.093 | |

| 0.061 | 0.336 | -0.127 | 0.406 | ||

| -0.005 | 0.055 | 0.320 | 0.044 | ||

| 0.005 | 0.079 | 0.030 | 0.255 | ||

| 3000 | 0.018 | 0.116 | -0.349 | 0.073 | |

| 0.028 | 0.260 | -0.178 | 0.342 | ||

| -0.005 | 0.044 | 0.313 | 0.025 | ||

| 0.002 | 0.062 | 0.054 | 0.223 | ||

| 4000 | 0.011 | 0.101 | -0.345 | 0.065 | |

| 0.015 | 0.226 | -0.200 | 0.293 | ||

| -0.003 | 0.039 | 0.310 | 0.013 | ||

| 0.000 | 0.055 | 0.076 | 0.189 | ||

| 5000 | 0.005 | 0.086 | 0.349 | 0.057 | |

| 0.013 | 0.205 | 0.198 | 0.267 | ||

| -0.001 | 0.033 | 0.309 | 0.012 | ||

| 0.001 | 0.050 | 0.076 | 0.171 | ||

We use the Euler scheme to simulate the threshold OU process by discretizing Eq. (1.1) on the interval with different mesh sizes and sample sizes . For each scenario, we generate Monte Carlo simulations of sample paths and each path consists of , and observations. The overall parameter estimates are evaluated by the bias and standard deviation (Std.dev).

Table 1 summarizes the main findings of Scenario 1 over Monte Carlo simulations. We observe that as the sample size increases, the bias decreases and is small. The empirical and model-based standard deviation agree reasonably well. The performance of the LSEs and improves with larger sample sizes in the multi-regime cases.

Table 2 summarizes the results of the QVEs and MQVEs. We can see from the table that the QVEs and MQVEs all have good performance when the mesh size is small(). However, when the mesh size is large(), the QVEs may lead to a rather large bias and such bias does not vanish as the sample size increases. Hence, we conclude that MQVEs have improved performance relative to the QVEs, especially when the sample size and mesh size are large.

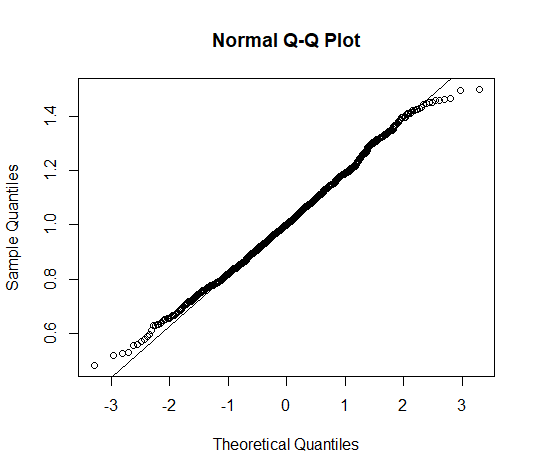

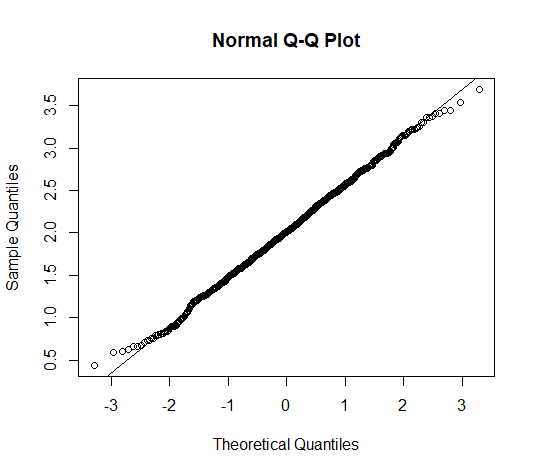

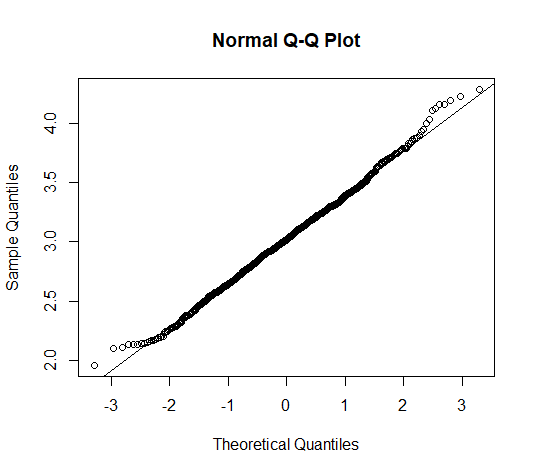

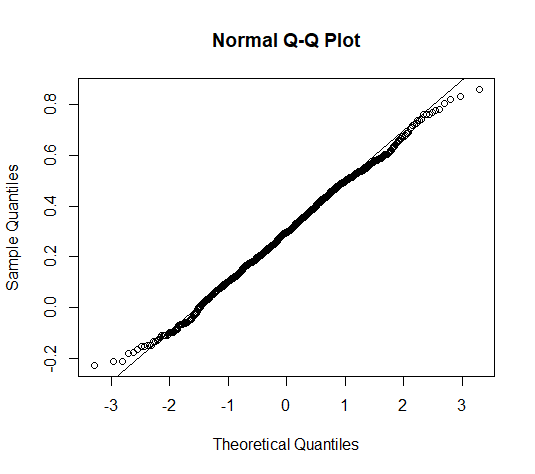

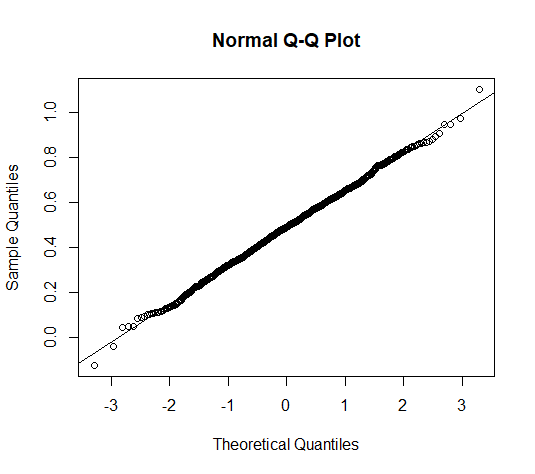

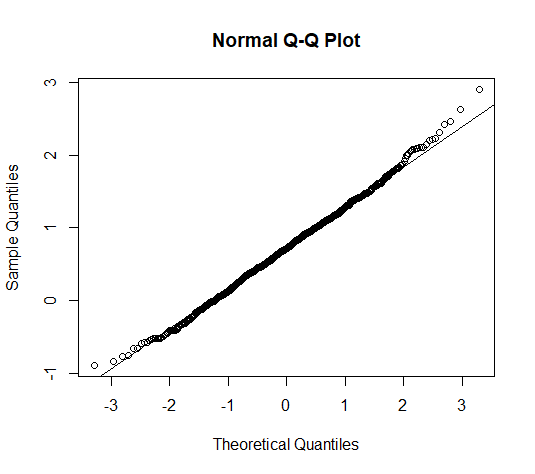

The normal QQ-plots for the estimators of 1000 Monte Carlo simulations with are presented in Figure 1. We can see from the figure that the estimators admit the asymptotic normality, which supports the results in Theorem 1-4.

Shown in Table 3 and 4 are the mean and standard deviation of the LSEs and GMEs in Scenario 2 and Scenario 3. The results exhibit that a rather large bias may be incurred by the generalized moment method. As the sample size increases, such biases may not attenuate. When employing the least squares method, the bias is significantly reduced compared to the generalized moment method. Heuristically, the two estimators perform better as the sample size becomes larger, but for relatively small sample sizes, the LSEs outperform the GMEs.

| 10-year treasury rate | 5-year treasury rate | |||

|---|---|---|---|---|

| value | CI | value | CI | |

| 3.510 | 3.610 | |||

| 0.018 | [0.009, 0.027] | 0.036 | [0.024, 0.048] | |

| 0.058 | [-0.002, 0.119] | 0.075 | [0.018, 0.132] | |

| 0.062 | [0.058, 0.067] | 0.006 | [0.003, 0.009] | |

| 0.215 | [0.180, 0.251] | -0.023 | [-0.055, 0.008] | |

| 0.254 | 0.279 | |||

| 0.280 | 0.250 | |||

| 2-year treasury rate | 1-year treasury rate | |||

| value | CI | value | CI | |

| 4.660 | 4.907 | |||

| 0.006 | [-0.006, 0.019] | -0.005 | [-0.015, 0.006] | |

| 0.016 | [-0.029, 0.061] | 0.004 | [-0.028, 0.036] | |

| 0.299 | [0.298, 0.300] | 0.540 | [0.539, 0.541] | |

| 1.400 | [1.370, 1.420] | 2.678 | [2.661, 2.695] | |

| 0.235 | 0.175 | |||

| 0.195 | 0.134 | |||

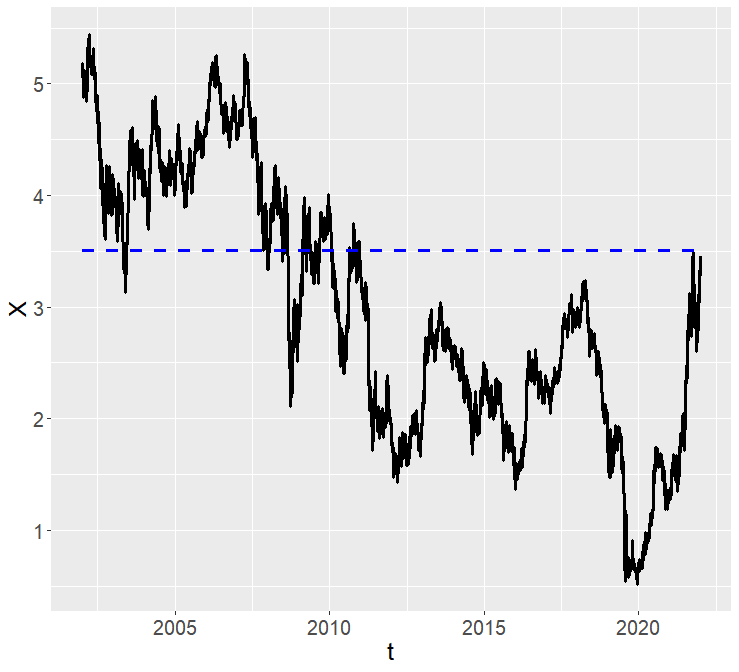

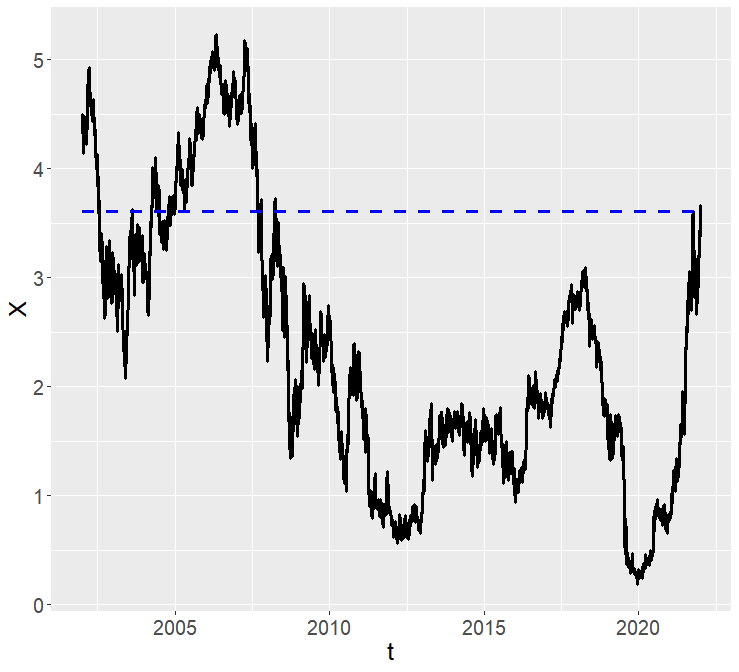

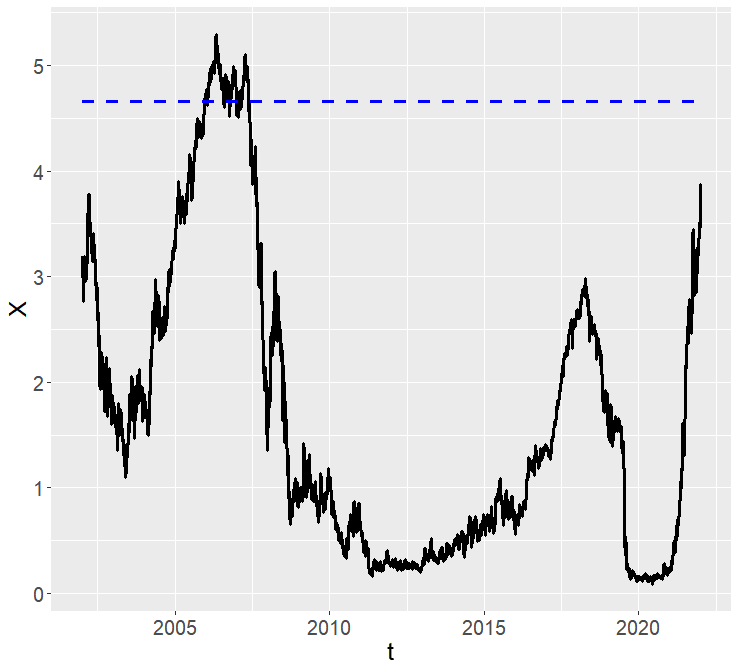

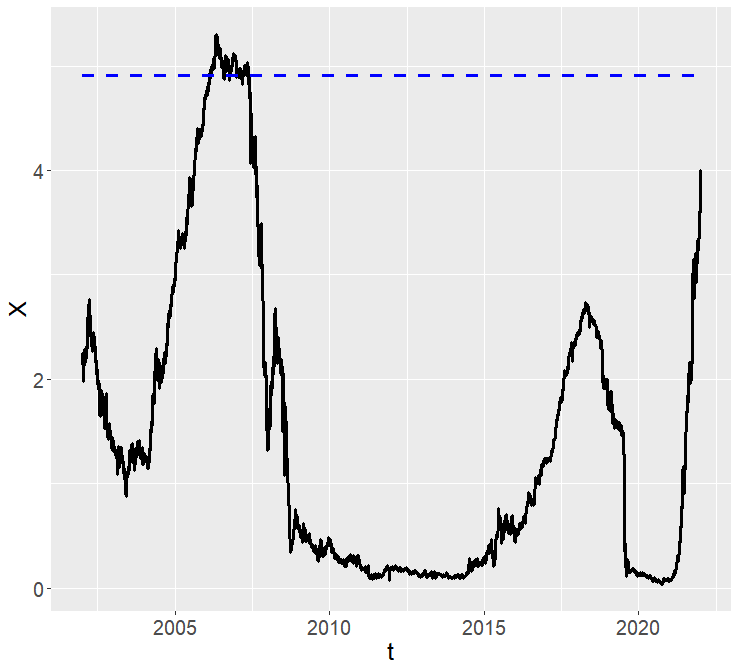

6.2 An application in U.S. treasury rate

In the previous discussion we presented an efficient estimation procedure for the drift parameters of a threshold OU process. [26] apply the threshold OU process to the three-month U.S. treasury rate, which is a high-frequency observed process with data collected on a daily basis. The rates are published on business days and the data shall be treated as equally spaced. However, it is not clear to verify whether the information accumulates twice over two non-business days as fast as over a one-day gap between consecutive daily data.

Here, we consider the U.S. treasury rate based on the data sets from Federal Reserve Bank. We report the treasury rate process for four assets including the ten-year, five-year, two-year, and one-year US treasury rate, all of which are collected from “2002-1-2" to “2022-9-16". We adopt the convention that the equal time interval for the “daily" rates is while one unit in time represents one month.

We model the rate process using the following SDE

Note that determining the number and values of thresholds (i.e., the values of and ) is an essential problem. In real-world applications, we shall transform the model as the following piecewise linear model

where . Then we can use the “segmented” function in “segmented” package of R to obtain the number and values of thresholds. The “segmented” package is a tool designed for segmented regression analysis. This package facilitates the detection and fitting of breakpoints in data, enabling the modeling of distinct linear relationships in different segments. The “segmented” function within the “segmented” package is primarily employed for segmented regression analysis.

Figure 2 displays the U.S. treasury rate process and we set the thresholds as the horizontal dashed blue lines. We shall see from the figure that each of the treasury rate processes has only one threshold (). The value of thresholds of 10-year and 5-year treasury rate processes are similar, as are 2-year and 1-year treasury rate processes. These are the ones that match the reality, since the trends of 10-year and 5-year treasury rate processes are about the same, while 2-year and 1-year treasury rate processes are about the same.

Table 5 summarizes the estimations of the drift and diffusion parameters where “value" is the estimation and “CI" is the confidence interval. Since the long rate is closely related to economic growth and inflation, the drift term does not have a significant slope with respect to its current treasury rate. The drift term in the first regime of the one-year and two-year treasury rate process is close to , which shows that the short rate evolves as a martingale process until it hits the second regime. In the second regime, the drift term has a negative slope which ensures the ergodicity of the process. In general, the short-rate process has the same general trend as the long-rate process.

7 Disscussion

We have considered the parameter estimation problem for the parameters of a threshold OrnsteinUhlenbeck process with multiple thresholds. Under the condition that the thresholds are known, we propose asymptotically consistent estimators for the drift and diffusion parameters. Our simulation results demonstrate that the proposed estimators are superior to the generalized moment estimators proposed by [12] and the usual quadratic variation estimators.

There are several important directions for further research. We would like to study the least squares estimator for all parameters including the thresholds. Consider the following objective function

By the fact that , the above objective function is equivalent to

It is almost impossible to obtain the closed-form formula of the estimator and , . However, various specialized methods have been developed to demonstrate the consistency of the suggested estimators [see, e.g., 7, 28]. Some other further research may include investigating the statistical inference for the generalized threshold diffusions.

Acknowledgments

The authors thank Tiefeng Jiang for the insightful comments. We also thank Yaozhong Hu and Yuejuan Xi for their enthusiastic help including the code of their method. This work is partially supported by the National Natural Science Foundation of China (No. 11871244), and the Fundamental Research Funds for the Central Universities, JLU.

Conflict of interest

All authors disclosed no relevant relationships.

References

- Bass and Pardoux [1987] R.F. Bass, E. Pardoux, Uniqueness for diffusions with piecewise constant coefficients, Probab. Theory Relat. Field 76 (1987) 557-572.

- Brockwell and Hyndman [1991] P.J. Brockwell, R.J. Hyndman, G.K. Grunwald, Continuous time threshold autoregressive models, Statist. Sinica 1 (1991) 401-410.

- Brockwell and Hyndman [1992] P.J. Brockwell, R.J. Hyndman, On continuous-time threshold autoregression, Int. J. Forecast. 8 (1992) 157-173.

- Browne and Whitt [1995] S. Browne, W. Whitt, Piecewise-linear diffusion processes, In Advances in Queueing: Theory, Methods, and Open Problems (1995) 463-480.

- Chan [1993] K.S. Chan, Consistency and limiting distribution of the least squares estimator of a threshold autoregressive model, Ann. Statist. 21 (1993) 520-533.

- Ding et al. [2021] K. Ding, Z. Cui, Y. Wang, A Markov chain approximation scheme for option pricing under skew diffusions, Quant. Finance 21 (2021) 461-480.

- Frydman [1980] R. Frydman, A proof of the consistency of maximum likelihood estimators of nonlinear regression models with autocorrelated errors, Econometrica 48 (1980) 853-860.

- Gerber and Shiu [2006] H. Gerber, E.S. Shiu, On optimal dividends: From reflection to refraction, J. Comput. Appl. Math. 186(2006), 4-22.

- Gairat and Shcherbakov [2017] A. Gairat, V. Shcherbakov, Density of skew Brownian motion and its functionals with application in finance, Math. Finance 27 (2017) 1069-1088.

- Hu and Nualart [2010] Y. Hu, D. Nualart, Parameter estimation for fractional OrnsteinUhlenbeck processes, Stat. Probabil. Lett. 80 (2010) 1030-1038.

- Hottovy and Stechmann [2015] S. Hottovy, S.N. Stechmann, Threshold models for rainfall and convection: Deterministic versus stochastic triggers, SIAM J. Appl. Math. 75 (2015) 861-884.

- Hu and Xi [2022] Y. Hu, Y. Xi, Parameter estimation for threshold OrnsteinUhlenbeck processes from discrete observations, J. Comput. Appl. Math. 41 (2022) 114264.

- Han and Zhang [2023] Y. Han, D. Zhang, Modified trajectory fitting estimators for multi-regime threshold OrnsteinUhlenbeck processes, Stat, 12(1) (2023) e620.

- Kutoyants [2004] Y.A. Kutoyants, Statistical Inference for Ergodic Diffusion Processes, London: Springer-Verlag, 2004.

- Kutoyants [2012] Y.A. Kutoyants, On identification of the threshold diffusion processes, Ann. Inst. Statist. Math. 64 (2012) 383-413.

- Le Breton [1976] A. Le Breton, On continuous and discrete sampling for parameter estimation in diffusion type processes, Mathematical Programming Study 5 (1976) 124-144.

- Liptser and Shiryayev [2011] R. Sh. Liptser, A. N. Shiryayev, Theory of Martingales, Springer-Dordrecht, 2011.

- Lejay and Pigato [2018] A. Lejay, P. Pigato, Statistical estimation of the oscillating Brownian motion, Bernoulli 24 (2018) 3568-3602.

- Lejay and Pigato [2019] A. Lejay, P. Pigato, A threshold model for local volatility: Evidence of leverage and mean reversion effects on historical data, Int. J. Theor. Appl. Financ. 22 (2019) 1950017.

- Lejay and Pigato [2020] A. Lejay, P. Pigato, Maximum likelihood drift estimation for a threshold diffusion, Scand. J. Stat. 47 (2020) 609-637.

- Mazzonetto and Pigato [2020] S. Mazzonetto, P. Pigato, Drift estimation of the threshold OrnsteinUhlenbeck process from continuous and discrete observations, (2020) arXiv:2008.12653.

- Revuz and Yor [1998] D. Revuz, M. Yor, Continuous Martingales and Brownian Motion, New York: Springer-Verlag, 1998

- Ramirez et al. [2013] J.M. Ramirez, E.A. Thomann, E.C. Waymire, Advection-dispersion across interfaces, Stat. Sci. 28 (2013) 487-509.

- Sattin [2008] F. Sattin, Fick’s law and Fokker-Planck equation in inhomogeneous environments, Phys. Lett. A 37 (2008) 3941-3945.

- Schilling et al. [2012] R.L. Schilling, L. Partzsch, B. Bttcher, Brownian Motion: an Introduction to Stochastic Processes, Berlin: De Gruyter, 2012.

- Su and Chan [2015] F. Su, K.S. Chan, Quasi-likelihood estimation of a threshold diffusion process, J. Econom. 189 (2015) 473-484.

- Su and Chan [2017] F. Su, K.S. Chan, Testing for threshold diffusion, J. Bus. Econ. Stat. 35 (2017) 218-227.

- van der Vaart [1998] A.W. van der Vaart, Asymptotic Statistics, Cambridge University Press, 1998.

- Xing et al. [2020] X. Xing, D. Zhao, B. Li, Parameter estimation for the skew OrnsteinUhlenbeck processes based on discrete observations, Comm. Statist. Theory Methods 49 (2020) 2176-2188.