Economic DAO Governance:

A Contestable Control Approach

In this article, we propose a new form of DAO governance that uses a

sequential auction mechanism to overcome entrenched control issues that have

emerged for DAOs by creating a regime of temporary contestable control. The

mechanism avoids potential public choice problems inherent in voting

approaches but at the same time provides a vehicle that can enhance and

secure value than inheres to DAO voting and other DAO non-market governance

procedures. It is robust to empty voting and is code feasible. It facilitates

the ability of DAOs to meet their normative and operational goals in the face

of diverse regulatory approaches. Designed to shift control to the party with

the most promising business plan, at the same time it distributes surplus in

a way that tends to promote investment by

other parties.

February 16, 2024 Version

©Jeff Strnad

1 Introduction

Decentralized Autonomous Organizations (“DAOs”) are a recent innovation, dating from the April 2016 launch of “The DAO.”222Vigna (2016). DAOs operate largely through the execution of code and have no centralized management. When participant decisions are required, DAOs typically utilize voting by token holders, roughly analogous to shareholder voting in a corporate setting. In most cases, the tokens are publicly traded.

Governance issues for DAOs have received considerable attention of late. Lots of experimentation with governance is taking place as well as a large volume of commentary.333The Decentralization Research Center (formerly, the DAO Research Collective) website includes a significant and representative collection of commentary and descriptions of experiments under the headings “Governance” and “Decentralization.” DAO Research Collective (2023). Most of the experimentation has centered around different voting mechanisms, including quorum-based token voting, a “direct democracy” approach in which token holders vote on proposals subject to a quorum requirement, and approaches in which delegation or other forms of representation are possible.444Nigam et al. (2023)(section on “Voting systems”).

Token voting potentially clashes with the goal of decentralization because of the danger of two types of entrenchment that threaten to create the equivalent of centralized management. First, explicit control is attainable by accumulating a sufficiently large token position. Second, it is often the case that a chronic lack of voter participation puts implicit control in the hands of a small set of active token holders who regularly engage in governance voting.555See, e.g., Feichtinger et al. (2023), Sun et al. (2022), and Liu (2023). Chronic lack of participation is consistent with rationality in many instances. The passive token holders may be portfolio investors or may have a small enough holding that the costs of being an informed voter greatly exceed the potential benefits in the form of higher token values or otherwise. More generally, the benefits of any effort expended by a token holder to become an informed voter will accrue mostly to other token holders who are in effect free riders.666Khanna (2022, pp. 239-240) describes this collective action problem in the corporate setting with reference to some of the literature. Reyes et al. (2017, p. 26) appear to be the first to note the presence and importance of the same problem in the DAO setting.

In order to address the danger of entrenchment as well as several other major potential problems for DAOs, we propose a different approach to DAO governance centered on a sequential auction mechanism. The fundamental building block of the mechanism is a basic auction that grants the auction winner temporary, contestable control of the DAO. Bids in the basic auction consist of a token target price, a surplus claim, and revelation of any toehold position held by the bidder at the time of the bid. Under the mechanism, the target token price part of the bid is effectively a value claim, , by the bidder that with control the bidder can implement a business plan that increases the token value from the prevailing market price, , at the time of the bid to . The surplus claim part of the bid is a claim by the bidder of a portion of the total surplus, , generated if the token target price is attained, where is the total number of tokens outstanding. The winning bid is the one that leaves the most surplus to the other token holders, that is, the bid that maximizes total surplus minus the bidder’s surplus claim.

In section 4 and Appendix A.1, we show that the dominant strategy in the basic auction is for the bidder to choose a business plan that produces the largest possible surplus net of the bidder’s cost, , and to truthfully reveal the token value, , that the bidder envisions as attainable under that business plan. As a result, with some minor exceptions, the mechanism will choose the socially best project, the one that maximizes . In addition, because the winning bid is the one that produces the largest amount of surplus for the existing token holders, the mechanism will tend to maximize the amount of surplus realized by token holders from future innovations, which in turn will tend to maximize the market value of the DAO both at start up and on an on-going basis.

The basic auction moves the DAO from a default governance state that typically is a voting regime into a control period in which the winning bidder controls the DAO independent of holding the majority or supermajority of tokens require to secure control under the voting regime. This feature allows the other token holders to enjoy a majority or even an overwhelming majority of the economic surplus generated by the winning bidder’s project through their token ownership. Token ownership and control are separated during the control period.

The sequential aspect of the mechanism ensures that control arising from a basic auction is temporary. There are several terminating events. If the control party succeeds in reaching the token target price, control ends and the DAO reverts to its default governance state. The control period ends if there is a supervening auction and the control party fails to win that auction. Control is contestable because the mechanism allows a supervening auction to take place at any time, triggered by any party willing to make an initial bid. Finally, the control period is limited in time and ends when the limit is reached even if the token target price was not realized and there was no supervening auction.

Section 4 details a set of features that create appropriate bidding and project execution incentives for control parties. Control parties that fail to achieve the token target price forfeit a portion or all of a substantial value deposit to the other token holders, guaranteeing that those token holders receive the full benefit of the winning bidder’s claimed future performance whether or not execution is successful. Value destruction by control parties is deterred by potential loss of both the value deposit and an additional surety deposit. Value destruction is a serious concern because control may be separated from ownership to an extreme degree. A party with control but very few tokens can take a large financial short position and then tank the DAO. The threat of losing the value deposit also creates appropriate post-auction execution incentives.

The mechanism just described defeats potential entrenchment in the form of explicit or implicit control. Holding a majority or supermajority of tokens no longer secures control of the DAO. The majority holder may lose control to a party with little or no token stake by being outbid in a basic auction, and a basic auction may be initiated at any time by a party willing to submit an initial bid. Similarly, implicit control is insecure. A single challenging party can initiate an auction contest for control even in the presence of the massive indifference of the vast majority of token holders, the indifference that enabled a small group to control the DAO implicitly.

The social value properties of the mechanism emerge definitively only if the token value of the DAO represents the intrinsic value of the DAO itself. As a result, the proposed approach is limited to economic DAOs, defined as DAOs with publicly traded governance tokens for which the token value reflects the inherent value of the enterprise.

DAOs vary greatly in purpose and approach. Some DAOs are very similar to commercial businesses providing services such as a trading exchange. These commercial DAOs are the most obvious example of economic DAOs. They provide goods and services with the profits accruing to token holders. The market capitalization of a commercial DAO represents its value in terms of the risk-adjusted present value of future returns. But economic DAOs are a much broader category. All that is necessary is that the market capitalization represents the value of the enterprise to the token holders. A charitable or investment DAO, for example, might gather funds to donate or invest. Such DAOs might have particular objectives, such as promoting environmental or climate change goals. Greater effectiveness at what they do in the view of all potential participants, including the specification of the objectives themselves, translates into a higher demand for the tokens along with a higher market capitalization.777Exit and entry through the token trading market is easy and nearly costless for publicly-traded DAOs. The associated community is open, not limited to current token holders. As a result, designing a governance system for a publicly traded DAO is very different from designing such a system for communities such as nation states or social clubs that are relatively closed because moving in and out of the community voluntarily is much more costly or even impossible. A range of non-commercial DAOs can be analogized to cities and towns offering different mixtures of local public goods in exchange for a different packages of taxes to residents and potential residents in a hypothetical world characterized by negligible moving costs.

An important ideal for a DAO governance mechanism is for most, and ideally all, aspects to be code feasible. Code feasible means implementable using available blockchain technology without recourse to external institutions. Code feasibility is a key aspect of decentralization, close to a necessary condition. By decentralization we mean the ability for the token project to operate in the absence of trusted parties.

The desideratum of code feasibility distinguishes the case of DAOs from conventional corporate or public governance structures. Those structures depend primarily on human management rather than code implementations that are automatic and, at present, are also more constrained by various legal requirements and regulations. The mechanism developed here is potentially applicable to the governance of some conventional institutions, in particular, public corporations. We leave full consideration of such applications to future work because they involve their own considerable and distinct complexities as well as a different, more stringent set of legal constraints. On the other hand, theoretical work and experience with governance of conventional institutions is pertinent, and we draw on both in what follows.

The sequential auction mechanism proposed here eliminates the danger of entrenchment inherent in token-voting schemes. It also has some very positive social value aspects: It tends to promote choice and implementation of the best set of business plans while at the same time securing the highest possible initial and on-going investment value for the DAO by allocating as much surplus as possible to existing token holders. Going further, it is important to consider how the mechanism relates to voting approaches, decentralization, and the associated web3 ideals that emphasize the role that DAOs can play in creating new kinds of democratic communities. Section 2 addresses the interaction of the mechanism with voting approaches, which is possible without first going through a more technical description of the mechanism. That section has an introductory aspect because the interaction with voting is the motivation for the sequential aspects of the mechanism. Section 3 provides a conceptual overview of the mechanism with reference to the pre-existing corporate governance literature. Section 4 together with two Appendices present the full, technical version of the mechanism, including some evaluative aspects that arise naturally as part of the presentation. Section 5 contains further evaluation, including a final subsection discussing decentralization and closely related regulatory considerations. Section 6 concludes with an assessment of the mechanism in light of web3 ideals.

2 Interaction of the Mechanism with Voting

The mechanism enables not only a sequence of auctions for control but also possible intervening periods in which governance reverts to a default governance state, typically a voting method of some kind. This approach allows the mechanism to achieve both operational goals and procedural goals in any combination or sequence. As discussed previously, at the operational level, the basic auctions comprising the sequence allow identification of the best business plans for the DAO combined with a tendency to implement them in a way that shifts as much surplus as possible to existing token holders from the control parties who undertake the implementation. When no party is willing to bid for control, intervening periods set in place a default governance state.

Aside from operational efficiency, DAO participants may value particular procedural approaches that embody process values in the form of certain community, “democratic,” or participatory norms. Potential control periods allow for a reset of the default governance state when it departs from the desired process values or, more ambitiously, revision of the default governance state itself. In terms of voting methods, the mechanism is available to preserve process values both by providing a guardrail that corrects voting method failures in an interim fashion before reinstating the method and by facilitating comprehensive reform of the voting method itself if desired by current and potential DAO participants.

Three subsections follow. The first two describe how the mechanism can correct possible voting method failures that may have negative operational or procedural consequences. The third addresses how the mechanism can promote process values.

2.1 Addressing Social Choice Problems

At present DAOs typically operate through a series of votes on proposals. If vote buying or other forms of bargaining with side payments are not possible, then each voting approach, whether directly or through electing representatives, can be conceptualized as a mechanism with nontransferable utility.888Nontransferable utility implies that players cannot bargain with each other using money or some similar indicator of value to reach a mutually agreeable result. Pareto improving moves, where for instance party A buys off party B to achieve a particular outcome that results in gains for A that outweigh the losses for B are not possible. As such, a large series of well-known potential “social choice” pathologies arise. A striking and relevant instance is the “McKelvey-Schofield Chaos Theorem” derived by McKelvey (1976) and Schofield (1978). This Theorem states that if the choice space is more than one-dimensional and preferences are Euclidean (decline with distance from an ideal point) or meet some more general conditions defined in Schofield (1978), then: (i) majority voting is unstable in the sense that every alternative is dominated by at least one other alternative; and, most strikingly, (ii) a series of majority votes can lead to any alternative in the choice space, even ones that are Pareto dominated. Most DAOs operate through a sequence of majority votes, and it is unlikely that the choice set of possible directions of change reduces to one dimension that fully captures preferences.

Most generally, there is the Gibbard-Satterthwaite Theorem derived by Gibbard (1973) and Satterthwaite (1975) which states that if individual preference orderings are complete and transitive but otherwise unrestricted and there are at least three alternatives, then a direct mechanism is dominant strategy incentive-compatible if and only if it is dictatorial.999 Borgers (2015) provides a concise discussion and proof of this Theorem and its significance. In a rough sense what the Theorem means is that with unrestricted preferences, a mechanism in which each individual votes sincerely, recording their actual preferences, will only work if there is a single individual who decides everything or if there are no more than two alternatives. Once strategic voting enters the picture, results can become unpredictable, difficult to estimate, and possibly very unrepresentative compared to voters’ actual preferences.101010The discussion by Tabarrok and Spector (1999) about how strategic voting might have affected the U.S. Presidential election of 1860 under various voting regimes is a good example.

The mechanism allows a way around these social choice problems. The basic auction creates a determinate outcome, one that awards control to the party that claims it can perform in a way that has the most benefit for the other token holders, a claim that is backed up by a value deposit. Initiating an auction not only creates determinacy, but also is a way to address any inferior operational or procedural outcomes that emerge from the social choice process.

2.2 Addressing Empty Voting

In addition to the social choice difficulties with voting approaches, there is another entirely separate set of potential problems associated with what has been termed “empty voting.” Following the seminal work of Hu and Black (2006), we use the following terminology. Empty voting occurs when a party is able to exercise the voting rights of a token without holding the associated economic rights to token value appreciation and any distributions. Hidden ownership is the opposite: the party holds the economic rights without the right to vote the token, and, typically, without appearing to be an owner in any corporate or blockchain register.

Empty votes can easily be created at little or no cost by a variety of means. A party can borrow tokens and then vote them, leaving the economic ownership to the lender. A party can engage in an equity swap, offloading the economic rights and retaining the votes.111111For example, the party starts with some tokens then swaps the economic return from the tokens for the economic returns of, say, a Treasury bond of equal value. The party still holds the tokens and can vote them, but the economic interest is in the hands of the swap counterparty. There are many methods that employ derivatives.121212For example, the party holding a token can write a call, buy a put, and borrow from a counterparty. The short call removes the token upside, the long put eliminates the downside, and the party can lend out the cash to pay the interest on the amount borrowed. The party is left with no economic position at all, but the party still formally owns the token and can vote it. The cost of entering this position will be nominal except possibly for some fees, which will be low if there are active markets or if potentially competing over-the-counter counterparties are readily available.

Empty voting exists in conventional markets and has been documented by Hu and Black (2006) as well as in a substantial literature following them. There also are identifiable instances of empty voting in cryptocurrency markets along with an awareness of the possible use of empty voting among participants in those markets.131313Buterin (2021) discusses “vote buying” and presents a theoretical example of empty voting that consists of the equivalent of an equity swap. Copeland (2020) describes an actual example from the takeover of Steem in 2020 by Justin Sun. Commentators, including Hu and Black (2006), consistently point out that empty voting can have positive as well as negative effects. Brav and Mathews (2011), for instance, model whether empty voting is likely to have a net positive or negative effect on corporate governance.

Whatever the balance between the positive and negative effects, empty voting creates an element of arbitrariness because prevailing may be a matter of more effectively accumulating empty votes rather than the result of a being able to create more value or virtue.141414As Hu and Black (2006, p. 907) state in the corporate context, potential use of empty voting lead to a situation in which: Voting outcomes might be decided by hidden warfare among company insiders and major investors, each employing financial technology to acquire votes. Adroitness in such financial technology may increasingly supplant the role of merit in determining the control of corporations.

In the context of a battle for control, the mechanism developed here makes empty voting irrelevant, avoiding any possible accompanying arbitrariness. Any party can initiate an auction, and to win control, a party must submit the best bid, one that promises an outcome that delivers the largest possible surplus to the other token holders, with a guarantee in the form a value deposit. It does not matter how many conventional token votes the party or its competitors have, empty or otherwise.

Empty voting can facilitate value destruction. A party can take a large empty voting position, combine that position with a net negative economic interest in the token such as a collection of put options, and then vote for proposals that reduce token value.151515There may be other motives to destroy the token such as being a marketplace competitor. Hu and Hamermesh (2023) discuss a general class of “related non-host assets” situations where an investor might use empty votes to damage the value of one entity in order to enhance the value of another entity in which the investor holds a substantial equity stake. In the most extreme case, the party could promote governance decisions that totally destroy the value of the token and the DAO project. The mechanism proposed here creates potential protection against such value destruction strategies since it offers a profitable auction route that renders empty voting ineffective.

The mechanism itself implicitly relies on empty voting because it permits a party winning control to prevail in all votes during the ensuing control period despite falling short of holding the required majority of tokens. As a consequence, potential value destruction by the control party is a concern. As discussed in the Introduction and described in detail in section 4, the mechanism contains measures to deter value destruction by a control party regardless of how it arises. Value destruction triggers a potential loss of deposits that outweighs any potential benefits and that compensates existing token holders for any resulting drop in token value.

Designing the mechanism involves considering possible deleterious use of hidden ownership as well as empty voting. In particular, section 4.1.4 describes the need for accurate toehold reporting accompanying auction bids. Hidden ownership is one way to conceal part or all of the bidder’s token position, and the mechanism must defeat use of such a device even if it is hard or impossible to detect as such.

It is important for any DAO governance approach or mechanism to be EV-robust in the sense of being effectively resistant both to deleterious uses of empty voting or hidden ownership and to any tendency for the decision mechanism to be compromised or blurred as a result of either manipulation.161616The term “EV-robust” uses the initials “EV” to stand in for “empty voting.” Whenever hidden ownership is created, it is necessarily the case that there will be an offsetting empty voting position. Thus, “EV-robust” can refer to the entire set of strategies hidden ownership as well as empty voting itself. This task is complicated by the fact that empty voting and hidden ownership are easy to conceal, particularly because the elements that result in the empty voting or hidden ownership positions may have a legitimate hedging or other purpose. The mechanism will not be EV-robust unless it is impervious to concealed empty voting or hidden ownership.

2.3 Promoting Process Values

Although voting approaches have serious potential flaws, voting mechanisms and other governance elements may have a process value to participants independent of operational efficiency. One would expect that process value would be captured in token value because token holders will be willing to pay more to participate in a DAO with governance features they value. Three implications follow with respect to the auction mechanism.

First there is rescue. If the indeterminacies and potential pathologies of voting threaten the coherence or direction of the DAO during an open period, causing the value of the DAO to drop, an auction that initiates a control period is a remedy. The control party can set the DAO back on course during the control period and then reinstate the voting mechanism after addressing the threats. This feature may create a safe zone of operation for voting mechanisms that serve important participation or other normative goals despite their potential flaws.171717Hall (2022) describes elegantly how the history of democracy can inform the design of DAOs. Among other elements, he considers the various forms that delegation can take, including delegates of the token holders appointing “managers … who could take certain operational decisions more expertly than tokenholder voting could,” but who remain “accountable to tokenholders because they can be fired by the elected delegates at any time.” He notes that this approach bears “similarities to corporate governance.” The mechanism here can be seen as an extension that adds a way to right the ship through temporary, contestable delegation of control to a competent party if the usual voting and delegation mechanisms break down. It is analogous to external corporate governance through the market for corporate control. The voting mechanism may not be viable otherwise as a long-term way to operate the DAO.

Second, the auction mechanism is a means to promote process values, including various desired voting approaches by facilitating innovations in the default governance state. If an increase in token value is attainable by shifting the governance mechanism in a way that increases its process value without a fully offsetting loss in operational efficiency, then there is the potential for an auction to create the shift. The sequential aspect of the auction mechanism is designed to achieve this result. Successful implementation of a shift in the default governance mechanism after winning an auction will raise token value, ending the control period with a reversion to the new superior default governance mechanism.181818The ideal situation is one in which the winning bidder sets the token target price just high enough to fully reflect the increase in token value from the shift in default governance mechanism. Execution results in an rapid if not instantaneous increase in token value to the target level, which ends the control period. If the winning bidder set the token target price too low, then the same result occurs. If the winning bidder sets the token target price too high, then, as discussed in section 4, the existing token holders will enjoy any overage at the expense of the winning bidder. It may be difficult or impossible to achieve a possibly complex innovation in the default governance state through voting or other procedures that comprise the current state.

Third, the fact that process value is reflected in token value means that a DAO that has sacrificed operational efficiency to add an even larger amount of process value will be immune from a takeover through the auction mechanism that eliminates the process value to increase operational efficiency. A party intending to implement this move through an auction would be unable to initiate the auction if the DAO is currently fully valued and would lose in the auction if the DAO is currently undervalued.191919Initiating an auction requires a bid with a token target price in excess of the current token value. If the DAO is undervalued but the current operational efficiency plus governance mechanism maximize the total value of the DAO, then a bidder maintaining the status quo will win the auction. See section 4 for details.

3 Conceptual Overview

We assume the subject DAO is an economic DAO. We consider a setting similar to Burkart and Lee (2021) in which various parties can use costly effort to increase the value of the DAO. In particular, suppose each party can engage in various projects that consist of expending effort, labor and resources equivalent to monetary units, in order to increase the value of the DAO by monetary units. Suppose that the DAO has tokens outstanding and that the current market price per token is . Define to be the token value emerging from a particular business plan. This business plan will create social surplus . Consider that expectations about the nature of future value-additive projects and about the distribution of surplus from those projects will affect the initial funding value of the DAO, possibly being critical to having enough funding to start up at all. In other words, the expected later treatment and facilitation of value-added projects will have an investment impact on initial funding for DAOs, and also, in an obvious way, on the on-going investment value of the DAO, which continues to depend on possible future projects.

The target is the following first-best outcome:

-

A)

At any point after initiation of the DAO, the mechanism will facilitate implementation of the value-additive project that results in the highest social surplus .

-

B)

When such project is created and implemented, the mechanism will allow the creating party to cover its cost but will allocate the social surplus entirely to the other token holders.

If both targets are met, the result will be the highest positive investment impact as initial and on-going investors will receive the maximum possible benefit from future innovations. In addition, at each point in time the DAO will implement the on-going business plan that adds the highest possible amount of social surplus.

To aim at the target, we create a sequential auction mechanism that produces periods of temporary contestable control interspersed with periods in which the DAO reverts back to a vote-driven default governance state. The mechanism has the property that the highest social surplus project is chosen subject to some constraints that guarantee the continuation of market trading. Some social surplus necessarily leaks to the project creators, resulting in an outcome that falls short of first best.

To describe the setting further, we use some terminology from Burkart and Lee (2021): Jensen-Meckling free riders and Grossman-Hart free riders.202020The names derive from phenomena described in Jensen and Meckling (1976) and Grossman and Hart (1980). Jensen and Meckling (1976) point out that when the party who manages a corporation, expending all the effort, owns less than all of the common stock, the costly effort is matched with only part of the gains. The other shareholders are Jensen-Meckling free riders, reaping gains without bearing any of the costs. These free riders, however, are the successors of the original investors or of parties who contributed effort previously. A policy of rewarding them encourages initial or subsequent investments in the corporate project, having the investment impact described above.

The conventional picture of Grossman-Hart free riders is a corporate enterprise for which the equity holders consist of a large group of parties all of whom own a very small stake. The chance that any one such party will be decisive in a vote is minuscule, which, combined with the large number of holders, creates a collective action problem. Consider a project creator who can profit by building up a share ownership position and then announcing or implementing a project that increases the value of the equity. If the equity holders get wind of the project, they will free ride by refusing to sell at less than the post-project target value of the equity. Open market purchases by the creator will push the price up, and in the U.S., the creator will have to reveal its holdings and intentions once the holdings exceed 5% of the total equity. The free-riding by the equity holders will limit the surplus that the project creator can extract, potentially killing the project if the extractable surplus is lower than the creator’s costs. Alternatively, creators will pick projects that do not maximize social surplus but are viable based on the limited surplus available from a modest toehold.212121Quadratic voting is one possibility for DAOs. As discussed in Lalley and Weyl (2018), when it operates well, quadratic voting aggregates preferences and information accurately with respect to decisions. In the face of the asymmetric information problem discussed here along with the possibility of free-riding, it is doubtful that quadratic voting could play a strong role. Parties without adequate information will not be able to represent their own interests well by voting, and revelation of information will trigger free-riding. If the project creator expends a large amount in the quadratic vote, the project creator will not be able to cover it from token value surplus due to that free-riding. If the DAO returns amounts the creator paid for the votes required to prevail to the creator, voting incentives are distorted.

Burkart and Lee (2021) create a model based on the value impact of effort that captures the current situation for project initiation through activism and tender offers in the United States. The tender offer route is restricted by Grossman-Hart free riding after an offer is made, limiting the offeror to surplus from a toehold. Activists proceed through a costly campaign aimed at managers and other shareholders to initiate a new project, avoiding Grossman-Hart free riding, but still being subject to Jensen-Meckling free riders. Revenues from activism are again limited to a toehold, but the other shareholders potentially benefit from the activism without bearing any costs. Burkart and Lee (2021) also analyze a third route: activism directed at initiating a merger, which they term “takeover activism.” In a merger, the price that shareholders receive is set by the managers of the two firms, allowing surplus to made available by forcing the dispersed shareholders to accept a price below the target price.222222Most states require shareholders to approve a merger by a vote. It will be in the interest of shareholders to do so despite not receiving the target price if a lower price is necessary to make the merger work by providing enough surplus for the acquiring party, here the project creator. Grossman and Hart free riding otherwise creates a collective action problem that potentially precludes shareholder gains entirely. Burkart and Lee (2021) survey the empirical evidence and note that among activist projects, the high-return ones for shareholders are concentrated among instances of takeover activism.

The mechanism created here addresses the potential value-reducing free-riding of both types through two devices. First, by creating a freeze-out feature as part of an auction, the mechanism allows the project creator to buy a proportion of the other token holders’ positions for no premium. Those token holders will earn the full amount of surplus on the retained proportion that is not purchased by the creator. This feature makes the auction equivalent to a merger in which token holders receive only a portion of the surplus on their token position shares because they are forced to sell part of it at less than the target price.232323Although the mechanism creates an outcome somewhat analogous to a merger, no actual merger is involved. Trading in the DAO remains continuous, and the life of the DAO goes forward. A merger in which the acquiring party buys all of the DAO shares would mean the end of the DAO in its current form. It might be that the acquiring party, which may be a shell, is itself set up to be a DAO, perhaps one with a new set of smart contracts meant to upgrade the acquired DAO. We leave exploration of this possibility to future work, including the case in which the selling token holders receive tokens in the new DAO instead of a cash-equivalent in exchange for the tokens in the old DAO. The bidding mechanism creates an incentive for bidders to limit the amount of surplus they attempt to claim via the freeze-out feature to the lowest possible value, the amount required to cover their costs. There is some leakage because the winning bidder has some scope to go beyond that.

Second, there is the problem of post-auction incentives in the face of Jensen-Meckling free riding. At the end of auction, the winning bidder has control but owns less than all of the tokens. The auction mechanism is designed to allocate surplus to the other token holders by limiting the stake held by the winning bidder, and that stake may be much less than half of the outstanding tokens. The mechanism restores full incentives to execute through the value deposit described in the Introduction and discussed more fully below. To the extent that the control party falls short of the target price, the control party has to pay 100% of the shortfall for the entire DAO. Thus, the control party has an incentive to execute that is at least as large as a party that has 100% ownership, eliminating any impact from Jensen-Meckling free riding on post-auction execution incentives.

As discussed in subsection 4.1.1, the value deposit and also the surety deposit employed by the mechanism are equivalent to forcing the control party to take on option positions. Other researchers, most prominently, Burkart and Lee (2015), have described the strong potential role of requiring such positions in implementing a cogent market for corporate control.242424Burkart and Lee (2015) show that a signaling equilibrium in a setting in which there are private benefits to control can attain the full information outcome by combining a cash offer with an offer to sell a call option with an exercise price equal to the bid price. Here the required option positions implicit in the deposits serve different roles. We use deposits rather than requiring option positions because deposits are code feasible, while derivatives require counterparties which raise issues of trust.

The goal throughout is to create an example of a mechanism that has some plausibility and likely effectiveness in order to introduce the idea of auction-based temporary contested control for governing DAOs. No claim is made that the mechanism is optimal among the set of all such mechanisms. We discuss possible alternative features at many points, not attempting to come to a conclusion concerning whether they are superior or inferior to the main variant that we describe.

With this overview in hand, we present the mechanism formally and evaluate it in the next two sections along with two appendices. Section 4 contains three subsections, describing respectively, a single auction, post-auction operation, and subsequent auctions, along with some evaluation of the mechanism. Section 5 completes the task of evaluation, organized topically in separate subsections. One appendix consists of proofs. The other appendix explores the consequences of adding certain stochastic elements to the model developed in the text.

4 A Sequential Auction Mechanism

We construct a sequential auction consisting of a series of basic auctions, implemented via one or more smart contracts, collectively “the DAO Code.” The DAO Code creates periodic basic auctions, with a fixed control period between auctions, subject to early termination under some circumstances. The DAO Code also permits a basic auction to be initiated by any party at any time, independent of the periodic auctions. These features make the control created by the auction both temporary and continuously contestable.

We develop the sequential auction mechanism in a deterministic setting in which the token price moves only because of the adoption of new business plans through the auction mechanism. In Appendix A.2 we examine what might happen in a stochastic setting, in particular possible adjustments to the mechanism and possible hedging by winning auction bidders.

4.1 The Basic Auction

4.1.1 The Basic Auction Mechanism

A basic auction is initiated at a time by a first bidder making a bid. The basic auction is open for the competitive bidding process up until a winner is determined at some later time , with the fixed total time length of the bidding period specified in advance by the DAO Code. Suppose that at the price of the DAO governance token is and tokens are outstanding. A bid, , consists of three parameters: a value claim, , per token; , the proportion of the q tokens held by the bidder at , hereinafter termed the bidder’s toehold; and a surplus claim, where is a parameter set by the DAO Code. The bidder’s toehold, , is deposited into the applicable smart contract simultaneously with the bid, becoming part of the bidder’s required token deposit under the mechanism. The basic auction is an English auction, ascending in the auction parameter . All prices and quantities such as are denominated in the units of a particular reference fiat currency designated by the DAO Code.

From this point on, we assume for convenience that the total number of tokens remains at . Then token price differences translate linearly into total value differences through the multiplicative factor even if the prices are realized at different times. This assumption avoids having to continually correct for possible changes in the number of tokens outstanding, which is trivial but cumbersome.

The rough intuition for the auction parameters, which will emerge with a more rigorous meaning in the Propositions below, is the following. represents a claim by the bidder that the project will reach value after the bidder gains control. A central feature of the basic auction is a freeze-out element which allows the winning bidder to force the other holders as of time to sell of their tokens to the bidder at price . The main function of the surplus claim is to determine , in particular, . If the value claim ends up being correct, then the forced sale results in a transfer of surplus equal to from the other holders to the bidder, the basis for the terminology “surplus claim.” is the freeze-out proportion. is possible, in which case , and the bidder will offer tokens at to the other holders subject to the total holdings of the bidder, i.e., . At the end of the forced sale or purchase of tokens, the bidder holds the proportion of the total tokens, and all of these tokens must be deposited in the applicable smart contract, resulting in the token deposit at the end of the auction totaling .252525The bidder is not barred from buying tokens during the auction, that is between time and time . Any such token purchases do not need to be reported or added to the token deposit. It is likely that the announcement of the bid will drive the token price considerably higher than as Grossman-Hart free riding emerges during the auction period. The toehold position is discussed further in subsections 4.1.4 and 4.1.5 infra.

The DAO Code imposes a market size condition, . This condition guarantees that a minimum proportion of the total tokens remain in the market during and at the end of the auction, which may be necessary to ensure a functioning market after the auction is over.262626The freeze-out step is proportional, leaving each holder immediately after the auction ends with the proportion of their time holdings. I.e., the same time market participants have holdings, albeit proportionately reduced. This feature should allow the market to continue to function smoothly across the transition point. Choosing any limits the maximum size of the surplus shift to the winning bidder to an amount less than the total surplus available. If the bidder has high enough costs, this limitation may cause a surplus-producing business plan not to be viable under the mechanism.

In addition to the token deposit of the tokens, the bidder is required to make three additional deposits in the form of stablecoins of types permissible under the DAO Code representing units of the reference fiat currency:

-

1)

A value deposit: .

-

2)

A purchase deposit: .

-

3)

A surety deposit: , where is defined and discussed below.

The bidder is making a value claim, , that the bidder’s business plan for the DAO will suffice to increase its value to at least . The value deposit transforms this value claim into a commitment. The fact that this deposit is held by the applicable smart contract makes this commitment credible and immediately enforceable in a code feasible manner. The DAO Code refunds part or all of the value claim when a value deposit refund condition is met: If the token price, at some time reaches a sustained price , where , then the DAO Code will refund of the value deposit to the bidder. “Sustained price” must be defined in a manner that is code feasible. For example the criterion might require that the token price as determined by some group of price oracles maintained by the DAO averages at least for 30 days and sustains a value at or above consecutively for at least 10 of those days. After this partial refund, the base level for application of the value deposit refund condition moves up from to , the new value deposit floor at time , and the condition is met again when a sustained price greater than occurs. Applying the condition repeatedly results in a cumulative refund as of some time of where is the largest value of the DAO token price that met the value claim refund condition up until that time.272727The value deposit and associated refund rules can be conceptualized as the bidder writing an in-the-money bear spread consisting of being long a put with strike price and short a put at strike price accompanied by a series of potential knock-in and knock-out put options triggered by the value deposit refund condition that causes the strike price of the short put to move up to the highest value that meets the condition.

The purchase deposit ensures performance when a bid with commits the bidder to buy tokens at price .

The surety deposit addresses the danger that the bidder will engage in value destruction after gaining control of the DAO. Note that the surety deposit is reduced to the extent of the value deposit. As will become apparent, these two deposits working in conjunction perform three functions: creating optimal bidding incentives, incentivizing performance of the business plan by the winning bidder after the auction ends, and deterring value destruction. The choice of the levels of the deposits and the applicable refund conditions for each deposit reflect the confluence of these three goals. We discuss the overall role of the surety deposit including the choice and significance of the parameter in subsection 5.2 after describing the auction mechanism further.

Consistent with the lack of centralized management in a DAO, the auction is designed to be self-executing through the Auction Contracts. To reach that goal, the auction mechanism must be code feasible. All four deposits are useful in that respect. Because of the purchase deposit requirement, non-payment cannot derail the auction. There is no need to have recourse outside of the Code to legal process for purposes of collection. As noted in the margin,282828See note 27 supra. the value deposit serves a function that also could be accomplished through derivatives. Use of a deposit eliminates the need for counterparties and the possible need to enforce counterparty compliance with the option contracts, elements that may not be code feasible without a great deal of added complexity or at all. Similarly, the token and surety deposits substitute for mechanisms that would rely on conventional derivative contracts and escrow arrangements enforced through the legal system.

All four deposits as well as a valid bid are required for the bidder to participate. If the bidder wins the auction, then the DAO Code uses the purchase deposit to purchase the freeze-out proportion of tokens for transfer to the winning bidder and retains the other three deposits, returning them if and only if certain conditions are met. If the bidder loses the auction, all four deposits are returned.

The auction is closed at time , a date which is analogous to a record date in corporate stock transactions, and the following Auction Closing Steps are implemented instantaneously:292929Blockchain technology allows for continuous identification of token holdings, and the steps outlined below can be implemented through smart contracts instantly with respect to the token holdings as of time when the auction closes.

-

1)

The DAO Code identifies token holders of the total tokens other than the bidder’s token deposit as of time , collectively, the token holders who hold the token holdings.

-

2)

If , the DAO Code transfers a total of tokens from the token holdings on a pro rata basis to escrow in the appropriate smart contract as part of the bidder’s token deposit, using the purchase deposit to pay each token holder per token transferred.

-

3)

If , the bidder has chosen to reduce its holdings from the baseline token deposit, , by selling tokens at price , where . The DAO Code initiates a sales process at when the auction ends, making the offering at price first to the token holders and then to market maker external agents (human or automated smart contracts), if any, operating under the DAO protocol. Any proceeds are remitted to the bidder. If tokens remain unsold, they remain under the bidder’s ownership as part of the token deposit. At the end of this process, the total token deposit is where , assuming all the tokens are sold.

-

4)

The DAO Code creates a dynamic vote pool consisting of additional voting rights assigned to the bidder, an amount that is adjusted continuously based on , the number of tokens outstanding and eligible to vote at each future time , to ensure that the bidder retains majority control of the DAO. where is the number of tokens outstanding and eligible to vote as of time when the auction ends. The votes in the pool are empty votes since they are not matched with the corresponding economic interest inherent in the tokens.303030The choice of giving the winning bidder majority control ( of the votes) implicit in this arrangement leaves open the possibility that the winning bidder will not be able to prevail on DAO issues that require a threshold greater than 50% to pass the applicable proposal. The exact percentage established by the DAO Code for the vote pool needs to be sensitive to the hierarchy of voting thresholds and the associated issues set for the DAO more generally. If a less conventional choice method such as quadratic voting is employed by the DAO, the dynamic voting pool must grant whatever number of additional voting rights is required to establish control.

4.1.2 The Optimal Business Plan and Bidding Strategy

Suppose a potential bidder can implement a business plan that involves expending effort, consisting of labor and resources equivalent to monetary units, that will result in a token value . This business plan creates social surplus . Suppose that among all the potential bidder’s possible business plans, the business plan creates the largest amount of social surplus, .313131 We assume that the auction takes place in a “private values” setting with asymmetric information. Each bidder’s potential set of business plans and their value-enhancing potential are known only to the bidder. All bidders agree on the value of the current operation. If there is a common values element in which bidders have different signals concerning the value of the current operation and bid based on perceived undervaluation at price , then the efficiency and surplus-distribution characteristics of the auction mechanism may be affected. However, choosing the English auction as a mechanism tends to make any such impacts benign or even beneficial. See note 52 infra.

The potential bidder must choose both a business plan (V,C) and a bid . It will turn out that the parameter is redundant with

respect to winning the auction. Only and matter. The following

Proposition characterizes the optimal business plan and bidding strategy:

Proposition 1. The following is the optimal project choice and

bidding strategy for a potential bidder:

(i) Regardless of the bidding strategy chosen, the potential

bidder chooses the business plan that results in ,

the largest possible social surplus that the potential bidder can generate

subject to the market liquidity constraint, . If

, the

potential bidder does not make a bid.

(ii) The bid parameters that result in the strongest possible

bid are:

; and

which result in an auction parameter equal to , the

largest possible surplus that the potential bidder can generate subject to

the market

liquidity constraint:

.

This bid results in zero profit for the potential bidder, with all the

surplus shifted to the other token holders.

(iii) If a profit level is feasible given the market

liquidity constraint, then the strongest possible bid parameters are:

; and

which result in the following auction parameter:

This bid results in profit equal to for the potential bidder,

with the remaining surplus, , shifted to the other token

holders.

(iv) The largest obtainable profit level is given . The minimum surplus that

must be transferred to the other token holders is .

Leaving a formal proof to an Appendix, we outline the proof here with an emphasis on intuition and then discuss the significance of the results.

The potential bidder’s highest surplus business plan produces added value of at cost . The potential bidder will realize the proportion of the added value through a toehold of tokens acquired before the auction plus tokens acquired at from the token holders using the freeze-out feature of the auction mechanism. The parameter guarantees that the token holders will gain at least the proportion of the added value as free riders. Under the auction mechanism, . For any fixed level of , choosing is equivalent to choosing , a residual that completely determines the division of added value between the control party and the free riders. For this reason, the fixed toehold proportion is irrelevant to division of the added value, which depends on , where is freely chosen subject only to .

Consider the auction parameter:

It is clear that is increasing in holding , and thus the potential bidder’s share of the added value, fixed. Now consider the potential bidder’s profit function expressed in terms of when the potential bidder implements a business plan :

The first term is the added value realized by the potential bidder, the second term is the potential bidder’s project cost, and the third term is the expected loss from the value deposit given that the potential bidder expects the business plan will result in a token value . Overbidding with results in a loss . As result, the optimal value claim is .323232The result does not follow simply from the loss. Choosing also affects the bid. In the formal proof set forth in Appendix A.1, we show that with , earning the same amount of surplus requires a weaker overall bid versus choosing .

The strongest possible bid will minimize in addition to setting .

must be large enough to cover the cost less the gains on the toehold

, i.e., . Then ,

which is equal to the total social surplus. Clearly the best possible bid

will require choosing , the business plan that maximizes total

social surplus subject to being feasible in the face of the market liquidity

constraint. That constraint allocates at least the proportion of

total added value to the token holders, who are free riders since they

bear none of the cost of adding value. The constraint may bind in the

optimization that determines . Choice of therefore may

preclude execution of the optimal business plan from a social perspective.

Corollary 1. If the market liquidity constraint, , is binding with , then the bidder will choose a business

plan that falls short of creating the greatest possible social surplus.

Suppose there are bidders and that bidder ’s best bid is . In an English auction, the highest bidder will prevail at the second highest bidder’s submitted auction parameter. The highest bidder can prevail with a bid of at most , and typically, , the highest bidder’s highest possible bid. Then, subject to the market liquidity constraint, the highest bidder can increase from its level , where is the bidder’s toehold profit, to }. The term is the maximum possible value of that is feasible under the market constraint, given , the minimum surplus that must be delivered to the free riders.

This algebraic exposition can be visualized through a series of figures.

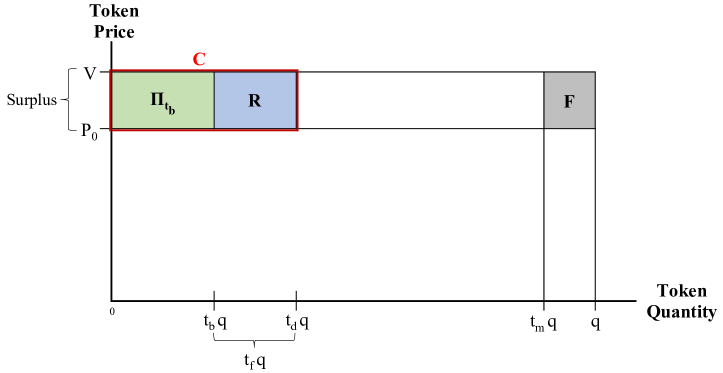

In Figure 1, the business plan induces a value claim and a surplus claim value of just big enough to cover the cost , which results in the winning bidder purchasing tokens at from the token holders through the freeze-out mechanism. This purchase results in the bidder realizing surplus equal to the blue rectangle in the figure. The green rectangle is the surplus that the bidder realizes from the toehold position . The bidder’s total surplus is the sum of the green and blue rectangles, which is equal in this instance to the red rectangle representing the cost . The area in the figure represents the minimum surplus that must be granted to the other post- token holders, the proportion of the total, and these free-riding shareholders also gain surplus equal to the unlabeled white rectangle between the rectangle and the rectangle.

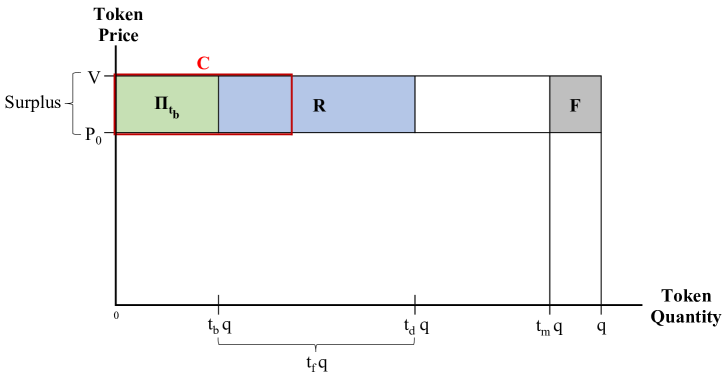

If , the winning bidder will be able to appropriate part or all of the surplus represented by the white rectangle. Figure 2 illustrates the case where the winning bidder is able to appropriate part but not all of it.

These figures illustrate a key feature that enables the mechanism to work. Burkart and Lee (2015) show that in deterministic tender offer games the ability to relinquish private benefits may be necessary for the existence of a separating equilibrium. The auction mechanism here allows bidders to relinquish benefits by choosing , the surplus claim. A lower value of results in a stronger bid but lower surplus. Because of the freeze-out feature of the mechanism, the possibility that free-riding will undermine signaling is eliminated. The bidder can specify an exact claim to surplus, , that otherwise might be inaccessible due to free riding. Combined with the basic auction features that make revealing truthfully a dominant strategy, the flexibility with respect to sets up an effective signaling environment that leads to a separating equilibrium.

proxies for bidder types, and a bidder with a lower cannot profitably mimic one with a higher . For bidder , the strongest possible bid, , is associated with zero profits. A higher bid results in net losses. As the English auction unfolds, if each bidder moves up until the level and then drops out, and will be evident since the bid also reveals . For the winning bidder, only and an upper bound on will be evident since it is possible that the winning bid, so that . In that case, the winning bidder is receiving more surplus than is necessary to induce that bidder to implement the best possible business plan. This situation appears to fall short of the first best which requires that all excess surplus remains with the free riding token holders in order to optimize initial and on-going investment in the DAO. But, as discussed in subsection 5.1, the full picture is more complex.

4.1.3 Bidding Intensity, Group Bidding, and Collusion

Two elements that are relevant to the investment impact of the mechanism are bidding intensity and the possibility of collusion among bidders. Krishna (2010, Chapter 11) lays out basic points about collusion in second price auctions. If there are bidders, then conditional on winning the auction, bidder 1 expects to capture surplus in the amount . The expectation in this expression is the expected value of the highest order statistic of the other values of . If a group of bidders collude, only the bidder with the highest value among them will bid. That strategy eliminates all the other bidders in the group from potentially lowering the highest bidder’s surplus from winning by submitting the second highest bid. If the collusion group is a subset of size , then the expected surplus capture is with respect to a highest order statistic of a smaller number of other bidders, instead of , and therefore is higher. In the extreme situation in which all bidders collude effectively, the highest bidder can prevail with a bid just above , thereby extracting the proportion of the added value, the maximum possible subject to the market liquidity constraint. The winning bidder then splits the added surplus from collusion with the other colluding bidders, a division that motivates them to be part of the collusion group.

Collusion, especially involving more than a few potential bidders, requires costly coordination, but if it occurs, it will impact investment negatively. Collusion results in winning bidders extracting more surplus, reducing the attractiveness ex ante for initial and on-going investment. There are some situations in which collusion is a very plausible threat. For example, if there is a strong outside candidate to add value through an innovative business plan, the most likely competing bidders may be a handful of identifiable “insiders” who previously had been the most active in directing the DAO. Small numbers make collusion easier to coordinate, and if the small group includes the likely highest set of bidders, collusion is likely to be very effective. The fact that DAOs have been characterized by low participation rates and a few key players running the show suggests that this situation may be common. Outside candidate collusion with the insiders creates a substantial opportunity for reducing the surplus that otherwise would accrue to the other token holders.

A key parameter is the expected bidding intensity. If there is a continuum of potential bidders who have values of that are dense in the interval , then it will be impossible to collude and the winning bidder will only be able to cover cost. Investment incentives will be maximized. If there are only a handful of potential bidders, then collusion will be a bigger danger, and, even in the absence of collusion, the winning bidder will be likely to walk away with considerable extra surplus to the detriment of investment.

Bidding intensity and the viability of the mechanism itself depends on capital market adequacy, the depth and development of capital markets. Making a bid through the mechanism requires deposits of the same order of magnitude as the total pre-bid value of the DAO. For established DAOs such as Uniswap, Maker, or Compound, deposit amounts of a billion dollars or more may be required.333333As of January 18, 2024, these three DAO governance tokens had market capitalizations of approximately $3.8 billion, $1.8 billion, and $440 million respectively. Coinmarketcap (2024). A deep bench of institutional investors such as venture capital firms, private equity firms, and hedge funds is required to make the auction mechanism robust and create bidding intensity. At least on the venture capital front, a large number of such firms already exist and are very active with respect to cryptocurrency projects including many DAOs.343434Crowdcreate (2021). These firms would be a ready source of funding for auction bidders. The temporary contestable control created by the auction mechanism, if implemented, might itself spawn specialist institutions similar to hedge funds in the current corporate landscape that combine portfolio investment with selective activism in governance.353535Yin and Zhu (2023) provide an empirical analysis. Such hedge funds typically engage in activism with respect to only a small portion of their portfolios. Burkart and Lee (2021) summarize the evidence that takeover activism aimed at or resulting in changes in corporate control generate higher target and activist returns.

One aspect of the auction mechanism is highly relevant to the possibility of collusion. There is nothing that prevents group bidding. A pool of outsiders, of insiders, or a mixture of both might combine into a bidding entity. It is possible to implement this combination via a smart contract, with the parties contributing the required stablecoins to fund bidding and then jointly holding the control position if their bid prevails. Group bidding may facilitate collusion, but it also may add valuable bidders who otherwise would not participate. For example, an entrepreneur with promising innovative ideas for running the DAO but with limited resources could form a bidding entity with private equity or venture investors who could fund the project.

As described in Krishna (2010), collusion in English auctions typically is illegal or subject to civil penalties in the non-digital world, but is it hard to see how collusion might be detected and policed in a code feasible manner. Group bidding via smart contracts may be detectible but whether it is merely collusive or has bid-formation advantages or is a mixture of the two would be a complex inquiry, requiring something akin to legal processes. Although there are mediation and adjudication tools available apart from the legal system, using these tools adds an additional element of complexity and requires trust in the tools.363636 A prominent example of a mediation and adjudication tool is Kleros. Kleros (2023a). Greig (2022) describes how Kleros operates by rewarding jurors for their performance based on a Schelling point criterion. Kleros is active, with multiple open cases. Kleros (2023b). Guillaume and Riva (2022a) discuss use of dispute resolution vehicles, including Kleros, for DAOs generally, noting that they are most effective when remedies can be executed on-chain because the parties have assets at risk there. In the case of collusion, some relevant parties may not.

4.1.4 Toehold Reporting and Post-auction Market Dangers

The basic auction mechanism requires that the bidder report any toehold position as part of the bid. As discussed above, the toehold proportion has no effect on the bid level. The bidder takes the toehold position into account when choosing a post-auction ownership position that dictates the proportion of added value captured by the bidder. That proportion, is the key choice that the bidder makes. Given the optimal value claim , choosing in light of determines and thus . is a residual that adjusts to whatever is to yield the desired value of .

What then is the purpose of having the bidder report and deposit tokens as part of the bid? There are two purposes. First, although the size of the bid, , is not affected by the toehold, an accurate report of the toehold is necessary for the bidding system to work. Recall that . We have seen that the portion of the first term is canceled out because is a component of R in the optimal bid. Nonetheless, the first term depends on and must be reported accurately for the cancelation to work. Second, the true value of is necessary to enforce the market liquidity condition , which guarantees that at least tokens are held by others, creating a pool of market liquidity. Relevant to both purposes, nothing in the bidding mechanism itself creates an incentive for a true report, and, in fact, the incentive is to cheat by hiding some of the toehold to artificially inflate the bid, .

Effectively addressing potential toehold concealment depends both on the identifiability of the control party’s token holdings, defined as the ability to associate positions to the control party, and on the costs of doing so. Complicating matters, any identification method must be EV-robust. The potential threat is from hidden ownership, which is, as discussed in the introduction, the obverse of empty voting. Instead of voting with no economic ownership, hidden ownership involves economic ownership without voting. It can easily be implemented via an equity swap between the control party and a token holder. In exchange for the economic interest in the DAO, including token appreciation, the control party offers another economic position such as treasury bond returns to the token holder. The token holder continues to own the token and will be identified as the owner on chain, but, secretly, the control party is able to capture surplus without reporting the economic position as part of the control party’s toehold. This maneuver may be very hard to detect. In effect, a much deeper level of identification is required, one that reaches beneath formal ownership.

Potential concealment of part or all of a toehold position is not the only threat that creates a need for identification. There are possible dangers arising from post-auction market manipulation by control parties. If the market is thin enough, the control party can engage in focused buying to drive the market up to sustained levels that substantially reduce the value deposit obligation, and then engage in selling to reverse the temporary position, similar to a pump and dump. Whether the market is robust or not depends both on the market capitalization of the DAO token and on the proportion of tokens not held by the control party.373737Hamrick et al. (2018) provide substantial evidence that pump and dump manipulations are much harder, as measured by the induced percentage price increase, for heavily traded, high market capitalization cryptocurrencies. If the market liquidity constraint is binding, the control party will exit the auction with the maximum proportion of of the total tokens outstanding, a situation that increases the danger of manipulation because of reduced market liquidity stemming from a lower traded-token supply. If the manipulation danger is salient enough, then for the auction mechanism to work it may be necessary to bar the control party from the post-auction market. Enforcing this bar would rely on an identification procedure that could operate effectively during the control period in the face of control by the control party.

For an identification method to work in a decentralized framework it must be code feasible as well as effective. We consider some possible methods in what follows, concluding with what appears to be the most promising one. We focus on the problem of concealment of a toehold position. The discussion applies in an obvious way to attempting to enforce a bar on market participation.

One method of identification is a bounty system. Any party that discovers and proves that the winning bidder concealed part of the toehold rather than reporting it would be awarded a number of tokens with current value equal to the value of the concealed part of the toehold at , the time of concealment, while simultaneously burning the corresponding quantity of concealed tokens held by the control party. If the value of the concealed tokens at the time the bounty is granted is less than their value, the shortfall can be made up by burning part of the control party’s token deposit or by creating debits against the control party’s stablecoin deposits.

Could a bounty system be effective and code feasible? DAO positions appear as a set of public addresses and token quantities. Commercially available technologies to trace and attribute token ownership exist and have a significant degree of effectiveness at what may be feasible cost.383838See Yaffe-Bellany (2023) (discussing Chainalysis). But reliance on outside commercial parties inhibits code feasibility. The DAO may have to implement the bounty system via contracts with outside teams. Doing so effectively while the control party has control of the DAO may not be possible. The task is complicated by the possible need to resolve disputes about the veracity of identifications claimed by the bounty hunters.393939Dispute resolution is more difficult when the parties do not have accessible on-chain assets at risk. See note 36 supra. An approach such as requiring good faith deposits from bounty hunters might be required to implement a dispute resolution mechanism that is code feasible. And possible hidden ownership presents a major challenge to the effectiveness of a bounty systems.404040Bounty hunters do have some possible strategies in the face of hidden ownership. Counterparties to the hidden ownership position used for concealment have a big incentive to collect the bounty by disclosing the failure to report, presumably earning an additional token at the expense of the control party without violating the underlying contract. Bounty hunters may angle for a cut by advertising this opportunity broadly and offering assistance. Although a bounty system may be too difficult to implement, it is potentially a very powerful deterrent. Successful bounty recovery is a disaster for the winning bidder, involving loss not only of potential surplus, the motivation for concealment, but also of the base value, .

One set of approaches to address control party position reporting issues centers around using know your customer registration systems that make token holders identifiable. Requiring registration of all token positions at all times would be very costly both initially and the face of continual revisions as tokens are traded between parties. Registration might also raise privacy considerations requiring costly zero-knowledge proof or other technologies to make identities private yet verifiable. Nonetheless, use of registration limited to subsets of token holders and to particular points in time might be useful and cost-effective as we describe in what follows.

One particularly promising way to address the toehold reporting problem is to use a flush sale variant of the mechanism. This variant is characterized by the following differences from the mechanism described so far:

-

1)

Revised purchase deposit. The purchase deposit is , covering all the tokens other than the toehold rather than the smaller proportion .

-

2)

Flush sale. The DAO Code uses this deposit to purchase all of the tokens other than the toehold at price . This purchase implements the flush sale.

-

3)

Adjust the token deposit. The DAO Code adds or subtracts tokens from the token deposit to adjust that deposit by the quantity .

-

4)

Token auction. At the end of the basic auction, the DAO Code initiates a token auction, selling tokens using a hard-coded auction technology that aims at revenue maximization. Purchases by the control party are barred, enforced to the extent feasible by a registration system.

-

5)

Registration. Parties can register through a know your customer process to demonstrate that they are not the control party or related to the control party.414141Registration can be made consistent with privacy through approaches such as requiring a zero-knowledge proof confirmation that they are not a restricted party linked to the winning bidder. For example, Rosenberg et al. (2022) describe a zero-knowledge proof credentialing system that they call “zk-creds.” In one instantiation, parties embed their passport in a zero-knowledge privacy layer that allows proof of identity. All registered parties are eligible to participate in the token auction. The set of token holders who register will be eligible to receive surplus from the auction.

-

6)

Treatment of token auction surplus or deficit. A token auction deficit caused by an average token auction price below remains a liability of the DAO. Any token auction surplus is distributed pro rata at a specified flush sale surplus distribution date to the set of registered token holders based on their relative holdings. This date is set by the DAO Code to give sufficient time for token holders to register before the flush sale surplus distribution date if they did not do so prior to the token auction.

The flush sale variant attempts to address the problem of non-reporting of the full extent of the winning bidder’s token position. Some or all of it is hidden among the proportion remaining after the proportion is declared and deposited. The flush sale is just that: It flushes out any hidden control party positions among that remaining proportion by forcing sale of the entire remaining proportion at .

It is likely that the auction purchases will be at prices significantly higher than . For that reason, even without the success of a bounty system, registration, or similar measures, the winning bidder is faced with a potential reduction in surplus on any positions that were concealed even if accompanied by corresponding repurchases after completion of the token auction. In contrast, declaring and depositing the pre-auction positions puts them in a safe harbor that allows the winning bidder to collect 100% of any surplus that arises. The registration system is crucial for establishing these incentives because the system ensures that any surplus from the auction flows to token holders other than the control party. Registration for participation in the token auction also plays a role because market trading after the auction is likely to be accompanied by substantial additional demand for tokens and a corresponding sharp price increase similar to what happens in a successful initial public offering in equity markets. Registration requirements block control parties from enjoying these gains. Use of a registration system aimed at blocking control parties from making auction purchases is likely to be particularly effective compared to alternatives such as relying on bounty hunters, and, because it can be limited, relatively low cost.