equation(#1)

Causal Discovery from Poisson Branching Structural Causal Model Using High-Order Cumulant with Path Analysis

Abstract

Count data naturally arise in many fields, such as finance, neuroscience, and epidemiology, and discovering causal structure among count data is a crucial task in various scientific and industrial scenarios. One of the most common characteristics of count data is the inherent branching structure described by a binomial thinning operator and an independent Poisson distribution that captures both branching and noise. For instance, in a population count scenario, mortality and immigration contribute to the count, where survival follows a Bernoulli distribution, and immigration follows a Poisson distribution. However, causal discovery from such data is challenging due to the non-identifiability issue: a single causal pair is Markov equivalent, i.e., and are distributed equivalent. Fortunately, in this work, we found that the causal order from to its child is identifiable if is a root vertex and has at least two directed paths to , or the ancestor of with the most directed path to has a directed path to without passing . Specifically, we propose a Poisson Branching Structure Causal Model (PB-SCM) and perform a path analysis on PB-SCM using high-order cumulants. Theoretical results establish the connection between the path and cumulant and demonstrate that the path information can be obtained from the cumulant. With the path information, causal order is identifiable under some graphical conditions. A practical algorithm for learning causal structure under PB-SCM is proposed and the experiments demonstrate and verify the effectiveness of the proposed method.

Introduction

Causal discovery from observational data especially for count data is a crucial task that arises in numerous applications in biology (Wiuf and Stumpf 2006), economic (Weiß and Kim 2014), network operation maintenance (Qiao et al. 2023; Cai et al. 2022), etc. In online services, for instance, the reason for the number of product purchases is of particular interest, while finding the underlying causal structure among user behavior from purely observational data is appealing and pivotal for online operation.

Much effort has been made to address the identification of causal structure from observational data (Spirtes, Glymour, and Scheines 2000; Zhang et al. 2018; Glymour, Zhang, and Spirtes 2019; Cai et al. 2018). In particular, constraint-based methods (Pearl 2009; Spirtes, Meek, and Richardson 1995), score-based methods (Chickering 2002; Tsamardinos, Brown, and Aliferis 2006) identify the causal structure by exploring the conditional independence relation among variables, but these methods only focus on the category domain and can only identify up to the Markov equivalent class (Pearl 2009). Thus, proper count data modeling is required to further identify the causal structure beyond the equivalence class. Recent work by (Park and Raskutti 2015) introduces a Poisson Bayesian network to model the count data and shows that it is identifiable using the overdispersion properties of Poisson BNs. Subsequently, it has been extended by accommodating a broader spectrum of distributions (Park and Raskutti 2017). In addition, the modeling of the zero-inflated Poisson data (Choi, Chapkin, and Ni 2020) and the ordinal relation data (Ni and Mallick 2022) and its identifiability of causal structure are investigated. However, the majority of these methods model the count data using Bayesian network ignoring the inherent branching structure among the counting relationship which is frequently encountered (Weiß 2018).

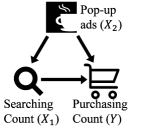

Take Figure 1 as an example, the cause of the purchasing event can be inherited from some of the searching events, the pop-up ads event, or exogenously occurs. As a result, the causal relationship among counts constitutes a branching structure that can be modeled by a binomial thinning operator ‘’ (Steutel and van Harn 1979) with an additive independent Poisson distribution for innovation. That is, the purchasing count () is affected by the pop-up ads count () and the searching count () which can be modeled by where , and . Generally speaking, the thinning operator models the branching structure that not every click will lead to purchasing while the additional noise models the general count of exogenous events. That is, a count represents the random size of an imaginary population, and the thinning operation randomly deletes some of the members of this population while concurrently introducing new immigration. This modeling approach finds widespread utility across various domains, notably within the context of the integer-value autoregressive model (Weiß 2018), which is first proposed by Al-Osh and Alzaid (1987); McKenzie (1985). Despite its extensive used, how to identify the causal structure in such type of model from purely observational data is still unclear.

To explicitly account for the branching structure, we propose a Poisson Branching Structural Causal Model (PB-SCM). We establish the identifiability theory for the proposed PB-SCM using high-order cumulant with path analysis. Theoretical results suggest that for any adjacent vertex and , the causal order is identifiable if is a root vertex and has at least two directed paths to , or the ancestor of with the most directed path to has a directed path to without passing . Based on the results of the causal order we further propose an efficient causal skeleton learning approach featured with FFT acceleration. We demonstrate the effectiveness of the proposed causal discovery method using synthetic data and real data.

Poisson Branching Structural Causal Model

In this section, we first formalize the Poisson branching structural causal model, and then we introduce the preliminary of cumulant and some necessary properties in this model.

Problem Formulation

Our framework is in the causal graphical models. We use , denote the set of parents, ancestors of vertex in a directed acyclic graph (DAG), respectively, and denote the set of common ancestors of vertex and vertex . Moreover, we define a directed path in is a sequence of vertices of where there is a directed edge from to for any with the coefficient of each edge. The set of vertices can be arranged in causal order, such that no later variable causes any earlier variable.

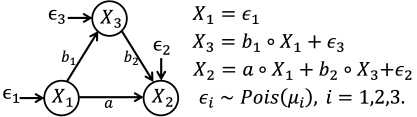

Now, we show the causal relationship in a causal graph can be formalized as the Poisson Branching Structural Causal Model (PB-SCM). Let denotes a set of random Poisson counts, of which the causal relationship consist of a causal DAG with the vertex set and edge set such that each causal relation follows the PB-SCM:

Definition 1 (Poisson Branching Structural Causal Model).

For each random variable , let be the noise component of , then is generated by:

| (1) |

where is the coefficient from vertex to , is the parent set of in , and is a Binomial thinning operation with , is the Bernoulli distribution with parameter .

We further define some graphical concepts. We use denotes the set of all directed paths from vertex to , where , , denote the -th directed path from vertex to . For each directed path , we use denote the corresponding coefficients sequence of path . We let also be a valid directed path for simplicity. Besides, we use denote to perform a consecutive thinning operation on based on the path sequence.

Goal: Given i.i.d. samples from the joint distribution , our goal is to identify the unknown causal structure from , assuming the data generative mechanism follows PB-SCM.

Preliminary

To address the identification of PB-SCM, cumulant are used in our work for building a connection to the path, providing a solution to the identifiability issue. Here, we recall the definition of cumulant and some basis properties.

Definition 2 (k-th order joint cumulant tensor).

The k-th order joint cumulant tensor of a random vector is the -way tensor in whose entry in is the joint cumulant:

| (2) | ||||

where the sum is taken over all partitions of the multiset .

In this work, we use the following specific cumulant form:

Definition 3 (2D slice of joint cumulant tensor).

For a random vector with -th order joint cumulant tensor where , denote its 2D matrix slice of -th order joint cumulant tensor as , where

| (3) |

Cumulant has the property of multilinearity such that . Furthermore, any cumulant involving two (or more) independent random variables equals zero, i.e., if and are independent. More importantly, any two variables in cumulant are exchangeable, e.g., .

Identifiability

In this section, we deal with the identification problem of causal structure under PB-SCM. Due to our identifiability result benefit from the ‘reducibility’ of cumulant in Poisson distribution, we first characterize such property in Theorem 1. After which, an example is provided to reveal the intrinsic relation between the cumulant and the path in a causal graph under PB-SCM. Based on such connection, we complete the identifiability results that are divided into the case when the cause variable is root (Theorem 3) and the case when the cause variable is not root (Theorem 6).

We first introduce a fundamental property of cumulant in PB-SCM that the cumulant is reducible:

Theorem 1 (Reducibility).

Given a Poisson random variable and distinct sequences of coefficients , we have

| (4) | ||||

where each repeats times in the original cumulant and only appears once in the reduced cumulant.

Such a result is a generalization of the property of the Poisson distribution since the cumulant of the Poisson distribution is identical in every order.

Motivating Example

Before describing our theoretical results, we use a motivating example to show the challenges of the non-identifiability issues and then introduce the basic intuition regarding in what case and how can we identify the PB-SCM.

To see the non-identifiability issue, we can show that a reversed model always exists in a two-variable system.

Remark 1.

For any two variables causal graph, the causal direction of PB-SCM is not identifiable and a distributed equivalent reversed model exists.

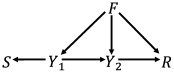

For instance, consider in Fig. 2, the distributed equivalent reverse model satisfies , where and such that this direction is not identifiable.

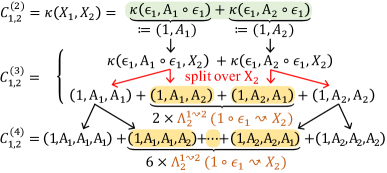

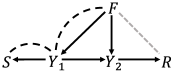

Fortunately, we find that the causal direction is still possible to identify in a more general structure. Considering the causal relationship between and in Fig. 2, here we provide an intuitive example to show how to identify such causal direction by utilizing the relationship between cumulant and path. Considering the cumulant with different orders, we can observe different behaviors of cumulant in the causal direction and the reverse direction. Thanks to the reducibility in Theorem 1, e.g., , the cumulants with different orders for and is shown in Fig. 3(a) and Fig. 4(a). Interestingly, we have in the reverse direction (Fig. 4(a)) but in the causal direction (Fig. 3(a)), i.e., there exists an asymmetry in the inequality relations of cumulants. Such asymmetry intriguing possibility to identify the causal order between two variables using the cumulant.

To understand how this asymmetry occurs and hence use it to identify the causal relations. We first discuss the identification in the simple scenario that the cause variable is a root vertex in , and then we generalize such results into the scenario that the cause variable is not root.

Identification When Cause Variable Is Root

We start with the case that the cause variable is root vertex, in which our goal is to identify causal direction even though we do not know it is a root vertex. Recall the previous example, the key of identification is the inequality rendering an asymmetry for a causal pair. To understand how it occurs, we seek to character and leverage such inequality constraints of cumulants in a causal graph to infer the causal order (Theorem 4).

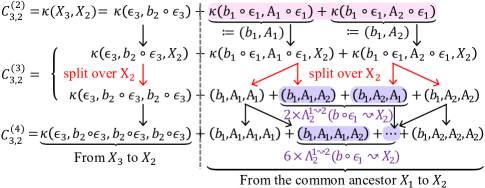

Here, we begin with two basic observations, which illustrate that inequality constraints of cumulants are driven by the number of paths between two variables. As shown in Fig. 3(a), one may see that (i) the decomposition of is composed by a series of cumulants of the common noise ( in this example) between and , which is due to the fact that any cumulant involving two (or more) independent random variables equals zero; (ii) moreover, such decomposition relates to the number of paths between and since and by multilinearity, the cumulant will be split exponentially as the order of cumulant increase. With these observations, the reason why is that there exists more than one path in the causal direction while zero path in the reverse direction, i.e., . As a result, for all order cumulant in the reverse direction.

In the following, we articulate the underlying law of the cumulant in PB-SCM and propose a closed-form solution to it. The first important observation is that due to the reducibility and the exchangeability of cumulant, the for is only composed by three distinct cumulants: , , and with varying number of these cumulants. In particular, if we define the summation of cumulants that only contains one path as and the summation of cumulants that contains two paths as , we will have the following closed-form solution:

| (5) |

where is the multinomial coefficient, indicating the number of ways of placing distinct objects into distinct bins with objects in the first bin, objects in the second bin. As a result, we will eventually have as shown in Fig. 3(a). Generally, we define as the summation of cumulants that contain paths from root vertex to :

Definition 4 (-path cumulants summation for root vertex).

Given two vertices and , for , the -path cumulants summation from vertex to is given by:

| (6) | ||||

where , is an arbitrary sequence of coefficients. For , and for , , and .

Intuitively, Eq. 6 is a summation of all cumulants that contain paths information from vertex to , and denotes the relation from the noise to itself. Based on the -path cumulants summation, can be decomposed as follows:

Theorem 2.

For any two vertices and where is root vertex, i.e., vertex has an empty parent set, the 2D slice of joint cumulant satisfies:

| (7) |

where is the multinomial coefficients.

Theorem 2 plays an important role in the identification of the causal order as it introduces the connection between the joint cumulant and path information. Moreover, since every order of the 2D slice joint cumulant can be obtained by Eq. 3, and thus every order of can also be obtained by solving the equation in Eq. C.1. By using we are able to understand the identifiability in the following theorem:

Theorem 3 (Identifiability for root vertex).

For any vertex and , where is the root vertex in graph , if , then and is the ancestor of .

Intuitively, based on Theorem 2, we have , and thus indicates that there exists more than one path from to than the reverse direction. That is, the causal direction for root vertex is identifiable if there are at least two directed paths:

Theorem 4 (Graphical Implication of Identifiability for Root Vertex).

For a pair of vertices and in graph , if vertex is a root vertex and exists at least two directed paths from to , i.e., , then the causal order between and is identifiable.

Identification When Cause Variable Is Not Root

In this section, we aim to generalize the identification result from the root vertex to the non-root vertex.

When vertex is not root, the main difference is that there might exist more than one common noise between two variables due to the possible common ancestor. Therefore, one may extend the result from the root vertex by considering each noise term as the separated root vertex. We present a general version of -path cumulants summation as follows, which can be expressed as the aggregation of the -path cumulants summations for the root vertices.

Definition 5 (-path cumulants summation).

The -path cumulants summation from vertex to vertex is given by:

| (8) | ||||

where is the -path cumulants summation for root vertex, is the number of directed paths from to .

With the general -path cumulants summation, the general joint cumulant can be decomposed as follows:

Theorem 5.

For any two vertices and , the 2D slice of joint cumulant satisfies:

| (9) |

where is the multinomial coefficients.

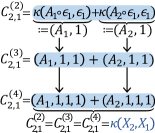

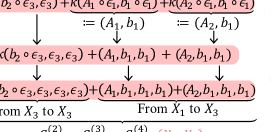

To see the connection with the case of root vertex, we take in Fig. 2 as example. Since can be expressed as , as shown in Fig. 3(b), we can separate the cumulant into two parts , , which can be considered as the cumulant starting from vertex to and to , respectively. As a result, the general -path cumulants summation can be expressed as the aggregate of all different starting with the corresponding noise terms. For instance, for in Fig. 2, we have:

| (10) | ||||

where Eq. 10 contains two different terms starting from and , respectively. In particular, since there only exists one directed path from to , is zero while to has two paths and thus is not zero. Similarly, for the reverse direction, we have

| (11) | ||||

where is zero since there are directed path from to and only directed path from or to . Intuitively, the general -path cumulants summation captures the number of directed paths from the common ancestor to . Moreover, for any two adjacency vertex and their common ancestor , the number of directed paths from to is greater or equal to that from to , and thus, the causal order can be identified using the following strategy:

Theorem 6 (Identification of PB-SCM).

If there exist such that and for any two adjacency vertex and , then is the parent of .

In addition, the -path cumulants summation will be ‘dominated’ by the variables (might be the common ancestor or itself) that has the most paths to since it is the aggregation of all the directed paths from both common ancestor and . Therefore, for a non-root vertex, it is possible to be non-identifiable by Theorem 3 if the dominant variable is the common ancestor. Specifically, we provide the graphical implication of such identifiability given as follows:

Theorem 7 (Graphical Implication of Identifiability).

For a pair of causal relationship . The causal order of is identifiable by Theorem 6, if (i) vertex is a root vertex and ; or (ii) there exists a common ancestor has a directed path from to without passing in .

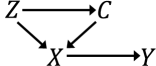

One of the examples is given in Fig. 5, in which Fig. 5(a) is not identifiable but Fig. 5(b) is identifiable. The reason is that is the dominant common ancestor of , and all directed paths from to will pass making it unidentifiable based on Theorem 7. In contrast, Fig. 5(b) includes an additional directed path without passing making identifiable. This intriguingly implies that a denser structure would facilitate the effectiveness of our method.

Generally speaking, once the causal order is identified, one may identify the complete causal structure by orienting edges based on the causal order in the causal skeleton. Such implementation will be provided in the next section. By this, the identifiability of causal structure under PB-SCM is answered.

Learning Casual Structure For PB-SCM

In this section, we propose a causal structure learning algorithm for PB-SCM. Our method involves two steps: learning the skeleton of DAG and inferring the causal direction using the results developed in Theorem 6.

Learning Causal Skeleton

To learn the causal skeleton, instead of using the constraint-based method, we propose a likelihood-based method. This boosts sample efficiency as the likelihood of PB-SCM captures its branching structure but the constraint-based method does not.

Given a set of count data and model parameters , the log-likelihood is Markov respect to , that is . However, calculating the likelihood directly using the probability mass function is costly. Therefore, we propose to calculate the probability mass function by using the probability-generating function (PGF). In detail, for each conditional distribution of , the likelihood can be calculated as follows:

Theorem 8.

Let be the PGF of random variable given its parents variable , we have:

| (12) | ||||

where , is the falling factorial, , and is the noise component of .

The result of Eq. G.1 can be converted to a polynomial coefficient after taking polynomial multiplication, which can be accelerated via Fast Fourier Transform (FFT) (Cormen et al. 2022). A detailed discussion is given in the supplement.

Generally, the likelihood-based method will tend to produce excessive redundant causal edges. Such effect can be alleviated by introducing the Bayesian Information Criterion (BIC) penalty into the , where is the number of edge of and is the size of dataset . The penalized objective function is updated as follows:

| (13) |

We maximum the objective function by using a Hill-Climbing-based algorithm as shown in Lines 2-6 of Algorithm 1. It mainly consists of two phases. First, we perform a structure searching scheme by taking one step adding, deleting, and reversing the graph in the last iteration, i.e., in Line 4, represents a collection of the one-step modified graph of . Second, by fixing the graph , we estimate the parameter of the model via optimizer with initial values from approximated covariance estimates and then calculate the in Lines 5. Iterating the two steps above until the likelihood no longer increases. In the end, we transform into a skeleton (Line 6). The correctness of such a procedure can be guaranteed by the consistent property of BIC which is discussed in (Chickering 2002).

Learning Causal Direction

Given the learned skeleton, we orient each undirected edge using the -path cumulants summation, according to Theorem 6. In detail, for each undirected edge , we calculate and for until one of them being zero or reaches the upper limit . We then orient the direction based on Theorem 6 (Lines 11-14).

To assess whether is equal to 0, a bootstrap hypothesis test is conducted (Efron and Tibshirani 1994) while a threshold can be used for orientation once such testing fails. In detail, we calculate the statistic from resampling dataset . Then, we estimate the distribution by kernel density estimator and centralize it to mean zero. Finally, the p-value of from the original dataset can be obtained.

Complexity Analysis We provide the complexity of calculating likelihood in the worst cases—when graph is complete. Specifically, the complexity of Eq. 13 is , by using FFT acceleration, this complexity can be reduced to , where is the sample size.

Experiment

Synthetic Experiments

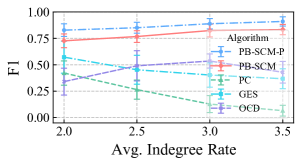

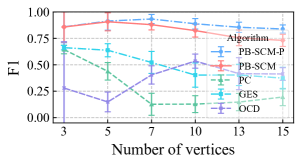

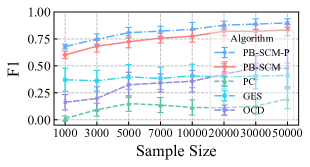

In this section, we test the proposed PB-SCM on synthetic data. We design control experiments using synthetic data to test the sensitivity of sample size, number of vertices, and different indegree rate. The baseline methods include OCD (Ni and Mallick 2022), PC (Spirtes, Glymour, and Scheines 2000), GES (Chickering 2002). We further provide the results using the true skeleton as prior knowledge (PB-SCM-P) to demonstrate the effectiveness of learning causal direction.

In the sensitivity experiment, we synthesize data with fixed parameters while traversing the target parameter as shown in Fig. 6. The default settings are as follows, sample size=30000, number of vertices=10, indegree rate=3.0, range of causal coefficient , range of the mean of Poisson noise , the max order of cumulant . Each simulation is repeated 30 times.

As shown in Fig.6, we conduct three different control experiments for PB-SCM. Overall, our method outperforms all the baseline methods in all three control experiments.

In the control experiments of the indegree rate given in Fig. 6(a), as the indegree rate controls the sparse of causal structure, the higher the indegree rate, the less sparse in causal structure leading to a decrease of performance of the baseline methods. In contrast, PB-SCM keeps giving the best results in all indegree rates. The reason is that our method benefits from the sparsity of the graph and the denser structure would result in more causal order being identified which verified the theoretical result in our work.

In the control experiments of the number of vertices given in Fig.6(b). Our method outperforms all the baseline methods, showing a slight decrease as the number of nodes increases, yet still demonstrating reasonable performance. The reason might be that with an increasing number of vertices, the number of paths for both directions also increases, which requires a higher-order cumulant to obtain the asymmetry. However, estimating high-order cumulant is difficult and has a large variance which leads to a decrease in performance.

In the control experiments of sample size shown in Fig.6(c), as the sample size increases, our method’s performance continues to improve and outperforms all the baseline methods. This suggests a sufficient sample size is beneficial for estimating accurate cumulant.

Real World Experiments

We also test the proposed PB-SCM on a real-world football events dataset111https://www.kaggle.com/datasets/secareanualin/football-events, which contains 941,009 events from 9,074 football games across Europe. For this experiment, we focus on the causal relation in the following count of events: Foul, Yellow card, Second yellow card (abbreviated as 2nd Y. card), Red card, and Substitution. These events possess clear causal relationships according to the rules of the football game. Our goal is to identify the causal relationship from the observed count data while reasoning the possible number of paths between two events as a byproduct of our method.

In detail, we employ the bootstrap hypothesis test with 0.05 significance level to test whether is equal to zero. The result is shown in Table 1. The column of shows the highest order of cumulants summation that is not equal to zero while the column of shows the lowest order of cumulants summation that equals zero.

| Cause | Effect | ||

|---|---|---|---|

| Foul | Yellow card | ||

| 2nd Y. card | |||

| Red card | |||

| Yellow card | 2nd Y. card | ||

| Substitution | |||

| 2nd Y. card | Red card |

The results are given in Fig. 7(b). Generally, PB-SCM successfully identifies five cause-effect pairs, except for . The possible reason might be attributed to the weak causal influence since only a few serious fouls will result in a red card. Interestingly, We find , indicating two paths from or its ancestor to Yellow card. This suggests a hidden confounder between Foul and Yellow card, possibly related to the football team’s style which also coincides with other path findings. Moreover, the causal direction between Yellow card and Substitution is identified suggesting a hidden confounder or indirect relation exists. This result suggests the effectiveness of our method when dealing with complex real-world scenarios.

Conclusion

In this work, we study the identification of the Poisson branching structural causal model using high-order cumulant. We establish a link between cumulants and paths in the causal graph under PB-SCM, showing that cumulants encompass information about the number of paths between two vertices, which is retrievable. By leveraging this link, we propose the identifiability of the causal order of PB-SCM and its graphical implication. With the identifiability result, we propose a causal structure learning algorithm for PB-SCM consisting of learning causal skeleton and learning causal direction. Our theoretical results and the practical algorithm will hopefully further inspire a series of future methods to deal with count data and move the research of causal discovery further toward achieving real-world impacts in different respects.

Acknowledgments

This research was supported in part by National Key R&D Program of China (2021ZD0111501), National Science Fund for Excellent Young Scholars (62122022), Natural Science Foundation of China (61876043, 61976052), the major key project of PCL (PCL2021A12). ZM’s research was supported by the China Scholarship Council (CSC).

References

- Al-Osh and Alzaid (1987) Al-Osh, M. A.; and Alzaid, A. A. 1987. First-order integer-valued autoregressive (INAR (1)) process. Journal of Time Series Analysis, 8(3): 261–275.

- Cai et al. (2018) Cai, R.; Qiao, J.; Zhang, Z.; and Hao, Z. 2018. Self: structural equational likelihood framework for causal discovery. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 32.

- Cai et al. (2022) Cai, R.; Wu, S.; Qiao, J.; Hao, Z.; Zhang, K.; and Zhang, X. 2022. THPs: Topological Hawkes Processes for Learning Causal Structure on Event Sequences. IEEE Transactions on Neural Networks and Learning Systems.

- Chickering (2002) Chickering, D. M. 2002. Optimal Structure Identification with Greedy Search. Journal of machine learning research, 3(Nov): 507–554.

- Choi, Chapkin, and Ni (2020) Choi, J.; Chapkin, R.; and Ni, Y. 2020. Bayesian causal structural learning with zero-inflated poisson bayesian networks. Advances in neural information processing systems, 33: 5887–5897.

- Cormen et al. (2022) Cormen, T. H.; Leiserson, C. E.; Rivest, R. L.; and Stein, C. 2022. Introduction to algorithms. MIT press.

- Efron and Tibshirani (1994) Efron, B.; and Tibshirani, R. J. 1994. An introduction to the bootstrap. CRC press.

- Glymour, Zhang, and Spirtes (2019) Glymour, C.; Zhang, K.; and Spirtes, P. 2019. Review of causal discovery methods based on graphical models. Frontiers in genetics, 10: 524.

- McKenzie (1985) McKenzie, E. 1985. Some simple models for discrete variate time series 1. JAWRA Journal of the American Water Resources Association, 21(4): 645–650.

- Ni and Mallick (2022) Ni, Y.; and Mallick, B. 2022. Ordinal causal discovery. In Uncertainty in Artificial Intelligence, 1530–1540. PMLR.

- Park and Raskutti (2015) Park, G.; and Raskutti, G. 2015. Learning large-scale poisson dag models based on overdispersion scoring. Advances in neural information processing systems, 28.

- Park and Raskutti (2017) Park, G.; and Raskutti, G. 2017. Learning Quadratic Variance Function (QVF) DAG Models via OverDispersion Scoring (ODS). Journal of Machine Learning Research, 18(224): 1–44.

- Pearl (2009) Pearl, J. 2009. Causality. Cambridge university press.

- Qiao et al. (2023) Qiao, J.; Cai, R.; Wu, S.; Xiang, Y.; Zhang, K.; and Hao, Z. 2023. Structural Hawkes Processes for Learning Causal Structure from Discrete-Time Event Sequences. In Proceedings of the Thirty-Second International Joint Conference on Artificial Intelligence, IJCAI-23, 5702–5710.

- Spirtes, Glymour, and Scheines (2000) Spirtes, P.; Glymour, C. N.; and Scheines, R. 2000. Causation, prediction, and search. MIT press.

- Spirtes, Meek, and Richardson (1995) Spirtes, P.; Meek, C.; and Richardson, T. 1995. Causal inference in the presence of latent variables and selection bias. In Proceedings of the Eleventh conference on Uncertainty in artificial intelligence, 499–506.

- Steutel and van Harn (1979) Steutel, F. W.; and van Harn, K. 1979. Discrete analogues of self-decomposability and stability. The Annals of Probability, 893–899.

- Tsamardinos, Brown, and Aliferis (2006) Tsamardinos, I.; Brown, L. E.; and Aliferis, C. F. 2006. The max-min hill-climbing Bayesian network structure learning algorithm. Machine learning, 65: 31–78.

- Weiß (2018) Weiß, C. H. 2018. An introduction to discrete-valued time series. John Wiley & Sons.

- Weiß and Kim (2014) Weiß, C. H.; and Kim, H.-Y. 2014. Diagnosing and modeling extra-binomial variation for time-dependent counts. Applied Stochastic Models in Business and Industry, 30(5): 588–608.

- Wiuf and Stumpf (2006) Wiuf, C.; and Stumpf, M. P. 2006. Binomial subsampling. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences, 462(2068): 1181–1195.

- Zhang et al. (2018) Zhang, K.; Schölkopf, B.; Spirtes, P.; and Glymour, C. 2018. Learning causality and causality-related learning: some recent progress. National science review, 5(1): 26–29.

Supplementary Material of “Causal Discovery from Poisson Branching Structural Causal Model Using High-Order Cumulant with Path Analysis”

Appendix A Proof of Theorem 1

Theorem 1 (Reducibility).

Given a Poisson random variable and distinct sequences of coefficients , we have

| (A.1) |

where each repeats times in the original cumulant and only contains one time in the reduced cumulant.

Outline of Proof

First of all, we introduce the moment-generating function (MGF) and cumulant-generating function (CGF).

Definition 6 (Moment-generating function).

For , an -dimensional random vector, the moment-generating function of is given by:

| (A.2) |

where is a fixed vector.

Definition 7 (Cumulant-generating function).

For , an -dimensional random vector, the cumulant-generating function of is given by:

| (A.3) |

where is the moment-generating function of .

With CGF, we can calculate the joint cumulant of a given random vector by taking deviate of CGF:

| (A.4) |

Furthermore, if each in the random vector repeated times, then we only need to take times of derivatives of the CGF with respect to the corresponding , i.e.,

| (A.5) |

Therefore, Theorem 1 is equivalent to show the following equality hold:

| (A.6) |

To do show, we will prove that the has the form of exponential function, i.e.

| (A.7) |

which is a function that remains unchanged when taking derivatives with respect to any and thus the Eq. A.6 holds.

Following this outline, consider a random vector , , where represents the Poisson noise component of a vertex in graph , and is a sequence of path coefficients corresponding to a direct path from to one of its descendant vertices. Then according to the definition of MGF, we have:

| (A.8) |

where is a fixed vector.

Following the outline, we first provide an intuition of proof through a specific case that each vertex are conditional independce by the root vertex .

Proof of Specific Case

Given a Poisson random variable and distinct sequences of coefficients , in which where is the -th coefficients of .

Assume there exist no between any two and such that , which means that there exist no two paths and sharing the same part from the source point.

We consider the random vector , where each random variable appears uniquely. The moment generating function (MGF) of is:

| (A.9) |

According to the law of total expectation, we have:

| (A.10) |

since for all .

Next, according to the property of thinning operation, we have , where ‘’ means distribution equality and is the binomial distribution, then the is the MGF of a binomial variable , we have:

| (A.11) |

| (A.12) | ||||

According to the power series expansion for the exponential function, i.e. , we have:

| (A.13) |

then the cumulant-generating function (CGF) of is given by:

| (A.14) |

We obtain the cumulant by the partial derivatives of the cumulant generating function:

| (A.15) |

Since has the form of the exponential function, further partial derivatives of it will also retain the same form:

| (A.16) |

Therefore, we have:

| (A.17) | ||||

which finishes the proof:

| (A.18) |

The above proof of specific case highlights that the way to calculate the MGF involves decomposing the expectation using the law of total expectation to establish conditional independence. In the specific case, the conditional independence can be simply established by condition on the since there is no common sub-sequence between any and .

However, given is not enough to build the conditional independence if and share the same sub-sequence, i.e. there exist a such that .

Before going into the formal proof, we provide an example to illustrate why simply conditioning on cannot establish conditional independence. Subsequently, we further show how to establish conditional independence in the presence of a common sub-sequence.

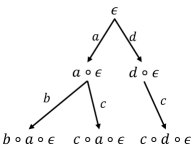

An Example when Common sub-sequence Exists

Consider random variables:

where and and has the common sub-sequence . The generating process can be represented through a tree structure, as shown in Fig. 1.

Now, if we condition on , we obtain conditional independence and , however, . This is because both and are dependent on the binomial random variable generated by the common sub-sequence .

Such dependence occurs due to performing the thinning operation on a random variable, resulting in the creation of a new random variable, distinct from the straightforward linear operations involving mere coefficient multiplication.

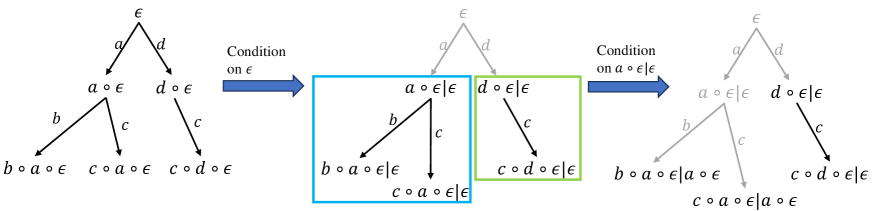

Therefore, to build conditional independence between and , we need to further condition on . Such a process of establishing conditional independence step by step can be represented through the tree structure in Fig.1, as shown in Fig. 2.

Specifically, the MGF of is given by

| (A.19) | ||||

where and correspond to the blue box and the green box in Fig. 2, respectively.

The next step is to establish conditional independence and separate . By applying the law of total expectation to it, we obtain

| (A.20) |

which is calculable since is the MGF of and the same for .

Motivated by the above example, when conditioning on a vertex in a tree, conditional independence is established among the random variables corresponding to each subtree of that vertex (if the subtree exists), enabling the separation of expectations.

Therefore, one can calculate the MGF by conditioning the random variables layer by layer according to the hierarchical structure of the tree in the generating process.

Here, to formalize the computation of the MGF, we introduce the following definition of a tree to model the generating process of the random vector .

Definition 8 (Tree representation of the generating process of random vector in PB-SCM).

For a given random vector , , the generating process of each random variable in can be summarized by a tree . Let denote all the vertices of , where is the root vertex of the tree and . Let with index denote the leaf vertices in the tree, such that

Moreover, let denotes the sub-sequence of that start from . For example, , then and . Let denotes the set of leaf vertex in the tree.

The recursive relation of MGF

Based on this definition, several lemmas are introduced to establish the recursive relation for the MGF of .

Lemma 1 (Start from root vertex ).

For a given random vector and its tree representation , , the MGF of satisfy

| (A.21) |

Proof.

The result is straightforward since the the root of the tree, then given the condition of each child of will be conditional independence:

| (A.22) | ||||

∎

By Lemma 1, MGF can be decomposed into separated conditional expectation in the first level of the tree. Next, we will investigate how such conditional expectation can be further decomposed.

Lemma 2 (From vertex to ).

For a given random vector and its tree representation . Let be a node in a level that decomposed the conditional expectation into the product of its child. Then, one of such decomposed expectation of its child , can be further decomposed if is not leaf,

| (A.23) |

and if is leaf,

| (A.24) |

Proof.

If is not leaf, we can separate the expectation according its child:

| (A.25) |

Then, according to the law of total expectation, we have

| (A.26) | ||||

If is leaf, which means is the exactly index of the leaf vertex and is empty, and then we have:

| (A.27) |

According to the definition of thin operator, we have with , where is Bernoulli distribution with parameter . Thus,

| (A.28) |

Note that is the MGF of . In the end, we obtain:

| (A.29) |

∎

To represent the recursive relation, we now introduce the probability-generating function (PGF):

Definition 9 (Probability-generating function).

For , where each is a discrete random variable, the probability-generating function of is given by: where .

Then, following lemma disclose the recursive relation of MGF.

Lemma 3.

For a given random vector and its tree representation . Let and , where . The joint MGF can be expressed as follows:

| (A.30) |

where

| (A.31) |

Proof.

First, by Lemma 2, we have the following recursive formula

| (A.32) |

and thus

| (A.33) |

Then, since , based on the recursive formula in Eq. A.32, we have

| (A.34) | ||||

Consider the expectation in Eq. A.34 when is not leaf vertex. Since is conditioned such that follows the distribution , then by the probability generating function of Binomial distribution, we have

| (A.35) |

where is the probability generating function of Bernoulli distribution according to the relation between Bernoulli and Binomial distribution. Substituting Eq. A.35 into Eq. A.34 we have

| (A.36) |

As for the joint MGF, similarly, we have

| (A.37) |

which finishes the proof.

∎

After deriving the recursive relation, we now step into the formal proof of Theorem 1 following the proof outline.

Formal Proof of Theorem 1

According to the Lemma 3, for a given random vector and its tree representation , the MGF of it is , where is a Poisson random variable. The cumulant generating function of is given by:

| (A.38) |

Our goal is to show the derivative of is of the exponential form:

| (A.39) |

We start with

| (A.40) |

where is a function involving only , we then have:

| (A.41) |

We then introduce the recursive representation of

Lemma 4.

The higher order partial derivative of can be given by:

| (A.42) |

Proof.

When is not a leaf vertex, according to the Lemma 3, we have:

| (A.43) | ||||

Since is a function involving only , we have:

| (A.44) |

Otherwise, when is a leaf vertex, we have:

| (A.45) |

which finishes the proof. ∎

According to Lemma 4, as the recursion terminates with an exponential function upon reaching the leaf vertex, we can deduce that the expansion of results in the product of for all , along with a series of corresponding path coefficients. Moreover, our focus does not lie in the specific form of these coefficients, and thus we denote the coefficient as . We conclude:

| (A.46) |

Finally, we obtain:

| (A.47) | ||||

which finishes the proof:

| (A.48) |

Appendix B Proof of Remark 1

Remark 1.

For any two variables causal graph, the causal direction of PB-SCM is not identifiable and a distributed equivalent reversed model exists.

Proof.

We prove by the equality of PGFs of both directions. Given a two variables causal graph , where , and we denote the reverse model by , where . We now show the solution of and .

For the causal direction, the PGF is given by:

| (B.1) | ||||

For the reverse direction, the PGF is given by:

| (B.2) | ||||

If these two models are equivalent, we have , i.e.

| (B.3) |

As is a root vertex in the reverse model, we have . Then we have:

| (B.4) |

Expanding the expression and simplifying, we obtain

| (B.5) | ||||

To ensure the equality holds, we equate the coefficients, resulting in following system of equations:

| (B.6) | ||||

where the solution of it is . This completes the proof.

∎

Appendix C Proof of Theorem 2

Theorem 2.

For any two vertex and where is root vertex, i.e., vertex has empty parent set, the 2D slice of joint cumulant satisfies:

| (C.1) |

where is the multinomial coefficients.

Proof

For any two vertex and , where is root vertex, let be the set of paths from vertex to with the corresponding set of sequences of coefficients. According to the definition of , we have:

| (C.2) |

then we expand according to the structural equation of :

| (C.3) |

By applying the multilinearity of cumulant, we obtain the following decomposition:

| (C.4) |

which yields cumulant term where each term correspondent to a different combination of coefficient .

To characterize the combinations of within each cumulant in Eq. C.3, we can conceptualize that choose different into box from number of different coefficient, , i.e., we can select a from for each position in the decomposed cumulant.

To establish the connection between the cumulant and the -path summation, we first recall the definition of :

| (C.5) |

which is the sum of cumulants and each cumulant involve distinct .

Note that due to the reducibility, the can be reduced to several distinct cumulants. In particular, the -path summation contains all the distinct cumulants of which involve distinct . Therefore, the connection between Eq. C.5 and Eq. C.4 can be formulated as how many numbers for each distinct occurs after the reducing.

For each distinct cumulant in , the number of occurrences is the same because each cumulant is constructed by different paths sharing the same property in term of number.

Thus, we only need to count the number of each distinct cumulant for some specific paths. Without loss of generality, consider the cumulant with path information: . Since before the reducing step, there are positions for each , and the count can be formulated by counting the number of ways to place distinguishable into indistinguishable boxes with replacement such that each ball must appear at least once. Such a number can be calculated by , which is the coefficient of . By combining each order of , we can obtain the close-form solution of in Eq. C.3. This completes the proof.

Appendix D Proof of Theorem 3 and Theorem 4

Theorem 3 (Identifiability for root vertex).

For any vertex and , where is the root vertex in graph , if , then and is the ancestor of .

Proof.

For the reverse direction, since is a root vertex, we have:

| (D.1) | ||||

Based on Theorem 1, Eq. D.1 can be reduced as follow:

| (D.2) |

thus .

For the causal direction, based on Theorem 2, we have:

| (D.3) | ||||

Then we have which means that there are more than one path from to , i.e. . Therefore, is the ancestor of . This completes the proof. ∎

Theorem 4 (Graphical Implication of Identifiability for Root Vertex).

For a pair of vertices and in graph , if vertex is a root vertex and exists at least two directed paths from to , i.e., then the causal order between and is identifiable.

Proof.

Suppose the causal order between and can not be identified by Theorem 3. Then there must be in the following cases: (i) ; (ii) .

For (i), since indicating that there exists zero or one path from to which contradict to the fact that .

For (ii), is contradicted to Theorem 3 that when . By combining these two cases, we complete the proof. ∎

Appendix E Proof of Theorem 5

Theorem 5.

For any two vertex and , the 2D slice of joint cumulant satisfies:

| (E.1) |

where is the multinomial coefficients.

Proof.

Since is not a root vertex, the structural equation of is , where is the sequence of coefficients corresponding to the -th path from , one of the ancestor of ,to .

According the structural equation of , we have:

| (E.2) |

then we decompose according to the structural equation of , we have:

| (E.3) | ||||

As those cumulants involve independent noise components equal to zero, is the common ancestor of and in the Eq. E.3.

Now, we consider the decomposition of cumulant: (i) and (ii) . For (i), the term has the similar form as the cumulant we proved in Theorem 2, i.e.,

| (E.4) |

where the only difference is the first noise component, which is instead of . This variation does not impact the result in Theorem 2 leading to

| (E.5) |

For (ii), has the same form as the cumulant we proved in Theorem 2, we have:

| (E.6) |

Substituting Eq. E.5 and Eq. E.6 into Eq. E.3, we have

| (E.7) | ||||

By rewriting Eq. E.7, we have

| (E.8) | ||||

This completes the proof. ∎

Appendix F Proof of Theorem 6 and Theorem 7

Theorem 6 (Identification of PB-SCM).

If there exist such that and for any two adjacency vertex and , then is the ancestor of

Proof.

For the case that is a root vertex. Suppose is not the ancestor of , then and are independent since is the root vertex and is not the ancestor of . In this case, the for each since and are independent.

For the case that is not a root vertex. Suppose is not the ancestor of , then there must exist path from the common ancestor to since . However, this contradicts the condition as it indicates that there not exist paths from the common ancestor to . Hence, we conclude that is the ancestor of . ∎

Theorem 7 (Graphical Implication of Identifiability).

For a pair of vertices and , if is an ancestor of . The causal order of is identifiable by Theorem 6, if (i) vertex is a root vertex and ; or (ii) there exists a common ancestor has a directed path from to without passing in .

Proof.

(i) If vertex is a root vertex and , we have

| (F.1) | ||||

Since there are paths from to and no two paths from to (from noise component of to ), we have and . Based on Theorem 6, is the ancestor of .

(ii) According to the acyclic constraints, the number of paths from their common ancestors to is either equal or more than the number of paths from their common ancestors to , since is an ancestor of and those paths to must reach .

If there exists a common ancestor has a directed path from to without passing in , it implies that the number of paths from to greater than that to , Consequently, there must exist a value such that and , and the causal order of is identifiable based on Theorem 6. ∎

Appendix G Proof of Theorem 8

Theorem 8.

Let be the PGF of random variable given its parents variable , we have:

| (G.1) | ||||

where , is the falling factorial, , and is the noise component of .

Proof.

For probability mass function , which can be decomposed as follow:

| (G.2) |

Let represent the probability generating function (PGF) of , which is the noise component of , and denote the PGF of , we have:

| (G.3) |

where and .

According to the property of PGF, we can calculate the probability mass function by taking derivatives of , and the derivative is expressed as:

| (G.4) |

According to the product rule of higher derivatives, i.e.

| (G.5) | ||||

we have:

| (G.6) |

Furthermore, we have

| (G.7) | ||||

Given , , along with the model parameter , we can compute the probability mass function as follow:

| (G.8) | ||||

where . This completes the proof. ∎

Accelerating Likelihood Computation Using FFT

To compute the likelihood function, we have to calculate the Eq. G.8. However, this task remains computationally intensive due to the numerous parameter combinations satisfying the specific summation condition and .

To address this issue, we show that the likelihood in Eq. G.1 can be formulated as the problem of obtaining the coefficient of a polynomial product.

Specifically, the production of polynomials can be constructed as follows:

| (G.9) | ||||

Then the likelihood in Eq. G.8 is exactly the coefficient of after the production. To obtain the coefficient of such production, we can employ the Fast Fourier Transform (FFT). In detail, we can create a series of vectors of the coefficient of each polynomial in G.9, and pad the list with 0 since the highest power of is :

| (G.10) | ||||

where and . Then the coefficient vector of the expansion of Eq. G.9 is given by:

| (G.11) |

Here, is the element-wise multiplication, and is the implementation of fast Fourier transform and Inverse fast Fourier transform respectively. Consequently, the -th element in the vector is the coefficient of in the expansion of Eq. G.9, which is the likelihood given Eq. G.8.

Appendix H Additional Experiments

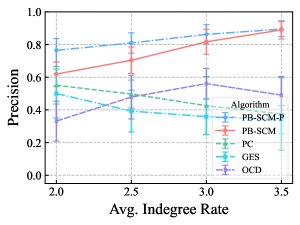

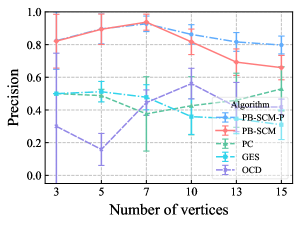

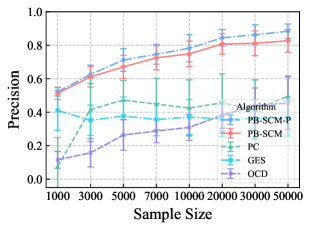

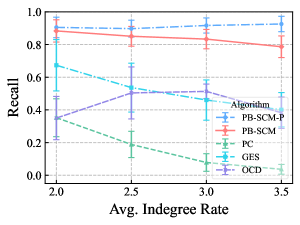

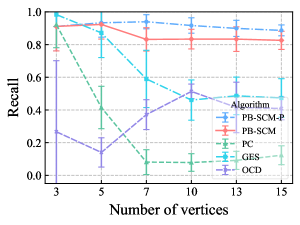

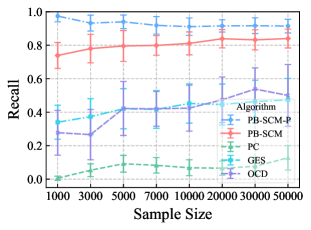

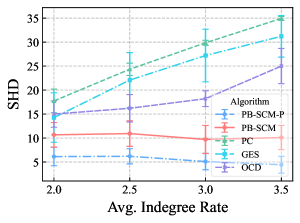

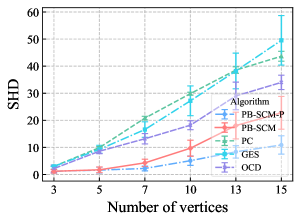

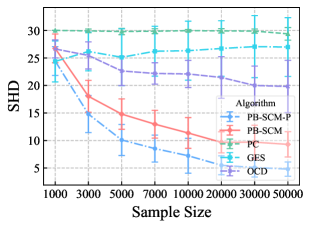

The main paper has shown the F1 scores and other baselines in synthetic data experiments. Here, we further provide the Precision, Recall, and Structural Hamming Distance (SHD) in these experiments, as shown in Fig. 3, Fig. 4 and Fig. 5.

| K | Score type | |||

|---|---|---|---|---|

| F1 | Precision | Recall | SHD | |

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 5 | ||||