Near-Optimal Solutions of Constrained Learning Problems

Abstract

With the widespread adoption of machine learning systems, the need to curtail their behavior has become increasingly apparent. This is evidenced by recent advancements towards developing models that satisfy robustness, safety, and fairness requirements. These requirements can be imposed (with generalization guarantees) by formulating constrained learning problems that can then be tackled by dual ascent algorithms. Yet, though these algorithms converge in objective value, even in non-convex settings, they cannot guarantee that their outcome is feasible. Doing so requires randomizing over all iterates, which is impractical in virtually any modern applications. Still, final iterates have been observed to perform well in practice. In this work, we address this gap between theory and practice by characterizing the constraint violation of Lagrangian minimizers associated with optimal dual variables, despite lack of convexity. To do this, we leverage the fact that non-convex, finite-dimensional constrained learning problems can be seen as parametrizations of convex, functional problems. Our results show that rich parametrizations effectively mitigate the issue of feasibility in dual methods, shedding light on prior empirical successes of dual learning. We illustrate our findings in fair learning tasks.

1 Introduction

Machine learning (ML) has become a core technology of information systems, reaching critical applications from medical diagnostics (Engelhard et al., 2023) to autonomous driving (Kiran et al., 2021). Consequently, it has become paramount to develop ML systems that not only excel at their main task, but also adhere to requirements such as fairness and robustness.

Since virtually all ML models are trained using empirical risk minimization (ERM) (Vapnik, 1999), a natural way to impose requirements is to explicitly add constraints to these optimization problems (Cotter et al., 2018; Chamon & Ribeiro, 2020; Velloso & Van Hentenryck, 2020; Fioretto et al., 2021; Chamon et al., 2023). Recent works (Chamon & Ribeiro, 2020; Chamon et al., 2023) have shown that from a probably approximately correct (PAC) perspective, constrained learning is essentially as hard as classical learning and that, despite non-convexity, it can be tackled using dual algorithms that only involve a sequence of regularized, unconstrained ERM problems. This approach has been used in several domains, such as federated learning (Shen et al., 2022), fairness (Cotter et al., 2019; Tran et al., 2021), active learning (Elenter et al., 2022), adversarial robustness (Robey et al., 2021), and data augmentation (Hounie et al., 2022).

These theoretical works, however, only address (i) the estimation error, arising from the empirical approximation of expectations in ERM and (ii) the approximation error, arising from using finite-dimensional models with limited functional representation capability. These are the leading challenges in unconstrained learning since the convergence properties of unconstrained optimization algorithms are well-understood in convex (e.g., (Bertsekas, 1997; Boyd & Vandenberghe, 2004)) as well as many non-convex settings (e.g., for overparametrized models (Soltanolkotabi et al., 2018; Brutzkus & Globerson, 2017; Ge et al., 2017)). This is not the case in constrained learning, where (iii) the optimization error can play a crucial role.

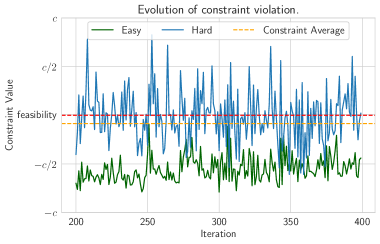

Indeed, dual methods are severely limited when it comes to recovering feasible solutions for constrained problems. In fact, not only might their primal iterates not converge to a feasible point [e.g, Fig. 1 or (Cotter et al., 2019, Section 6.3.1)], but they might not converge at all, displaying a cyclostationary behavior instead. This problem is hard even from an algorithmic complexity point-of-view (Daskalakis et al., 2021). For convex problems, this issue can be overcome by simply averaging the iterates (Nedić & Ozdaglar, 2009). Non-convex problems, however, require randomization (Kearns et al., 2018; Agarwal et al., 2018; Goh et al., 2016; Chamon et al., 2023). This approach is not only impractical, given the need to store a growing sequence of primal iterates, but also raises ethical considerations, since randomization further hinders explainability.

Yet, it has been observed that for typical modern ML tasks, taking the last or best iterate can perform well in practice (Cotter et al., 2018; Chamon & Ribeiro, 2020; Chamon et al., 2023; Robey et al., 2021; Elenter et al., 2022; Hounie et al., 2022; Shen et al., 2022; Gallego-Posada et al., 2022). This work addresses this gap between theory and practice by characterizing the sub-optimality and infeasibility of primal solutions associated with optimal dual variables. To do so, we observe that, though non-convex, constrained learning problems are generally parametrized versions of benign functional optimization problems. We then show that for sufficiently rich parametrizations, solutions obtained by dual algorithms closely approximate these functional solutions, not only in terms of optimal value as per (Cotter et al., 2019; Chamon & Ribeiro, 2020; Chamon et al., 2023), but also in terms of constraint satisfaction. This implies that dual ascent methods yield near-optimal and near-feasible solutions without randomization, despite non-convexity.

2 Constrained Learning

2.1 Statistical Constrained Risk Minimization

As in classical learning, constrained learning tasks can be formulated as a statistical optimization problem, namely,

| () | ||||

| s. to |

where is a function associated with the parameter vector and the hypothesis class induced by this family of functions is assumed to be a subset of some compact functional space . Throughout the paper, we use the subscript (parametrized) to refer to quantities related to (). The functionals , , denote expected risks for loss functions . In this setting, can be interpreted as a top-line metric (e.g., accuracy), while the functionals encode statistical requirements that the solution must satisfy (see example below).

Example 2.1: Learning under counterfactual fairness constraints.

Consider the problem of learning an accurate classifier that is insensitive to changes in a set of protected attributes. Due to the correlation between these attributes and other features, simply hiding them from the model is not enough to guarantee this insensitivity. To do so, this requirement must be enforced explicitly. Indeed, consider the COMPAS study (ProPublica, 2020), with the goal of predicting recidivism based on past offense data while controlling for gender and racial bias. Explicitly, let denote the cross-entropy loss . By collecting the protected features into the separate vector , i.e., , we can formulate the problem of learning a predictor insensitive to transformations that encompass all possible single variable modifications of . Explicitly,

| s. to |

where is the desired sensitivity level. Note that this formulation corresponds to the notion of (average) counterfactual fairness from (Kusner et al., 2018, Definition 5). In this setting, each constraint represents a requirement that the output of the classifier be near-invariant to changes in the protected features (here, gender and race). For instance, the prediction should be (almost) the same whether, all else being equal, the gender of the input is changed from “Male” to “Female” (and vice-versa) or the race is changed from “Caucasian” to “African-American.”

Note that even if the losses are convex in (as is the case of the cross-entropy), the functions need not be convex in . This is the case, for instance, for typical modern ML models (e.g., if is a neural network, NN). Hence, () is usually a non-convex optimization problem for which there is no straightforward way to project onto the feasibility set (e.g., onto the set of fair NNs). In light of these challenges, we turn to Lagrangian duality.

2.2 Learning in the dual domain

Let the Lagrangian be defined as

| (1) |

where is a vector-valued functional collecting the constraints of (). For reasons that will become apparent later, we define over . For a fixed dual variable , the Lagrangian is a regularized version of (), where acts as the regularizing functional. This leads to the dual function

| (2) |

based on which we can in turn define the dual problem of () as

| () |

This saddle-point problem can be viewed as a two-player game or as a regularized learning problem, where the regularization parameter is also an optimization variable. As such, () is a relaxation of (), implying that . This is known as weak duality (Bertsekas, 1997).

The dual function in (2) is concave, irrespective of whether () is convex (it is the pointwise minimum of a family of affine functions on (Boyd & Vandenberghe, 2004)). As such, though may not be differentiable, it can be equipped with supergradients that provide potential ascent directions. Explicitly, a vector is a supergradient of the concave function at a point if for all . The set of all supergradients of at is called the superdifferential and is denoted . When the losses are continuous, the superdifferential of admits a simple description (Nedić & Ozdaglar, 2009), namely,

where denotes the convex hull of the set and denotes the set of Lagrangian minimizers associated to the multiplier , i.e.,

| (3) |

In particular, this leads to an algorithm for solving () known as projected supergradient ascent (Polyak, 1987; Shor, 2013) that we summarize in Algorithm 1.

When executing Algorithm 1, dual iterates move in ascent directions of the concave function (Shor, 2013, Section 2.4). Yet, the sequence of primal iterates obtained as a by-product need not approach the set of solutions of (). The experiment in Figure 1 showcases this behaviour and illustrates that, in general, one can not simply stop the dual ascent algorithm at any iteration and expect the primal iterate to be feasible. Additionally, the Lagrangian minimizers are not unique. In particular, for an optimal dual variable , the set is typically not a singleton and could contain infeasible elements (i.e, for some ). Even more so, as approaches , the constraint satisfaction of primal iterates can exhibit pathological cyclostationary behaviour, where one or more constraints oscillate between feasibility and infeasibility, see e.g., (Cotter et al., 2019, Section 6.3.1). For these reasons, convergence guarantees for non-convex optimization problems typically require randomization over (a subset of) the sequence , which is far from practical [see e.g, (Agarwal et al., 2018, Theorem 2), (Kearns et al., 2018, Theorem 4.1), (Cotter et al., 2019, Theorem 2), (Chamon et al., 2023, Theorem 3)]. In the sequel, we show conditions under which this is not necessary.

3 Near-Optimal Solutions of Constrained Learning Problems

Primal iterates obtained as a by-product of the dual ascent method in Algorithm 1 may fail to be solutions of (). However, it has been observed that taking the last or best iterate can perform well in practice. This can be understood by viewing () as the parametrized version of a benign functional program, ammenable to a Lagrangian formulation. This unparametrized problem does not suffer from the same limitations as () in terms of primal recovery and we can thus use its solution as a reference point to measure the sub-optimality of the primal iterates obtained with Algorithm 1.

The unparametrized constrained learning problem is defined as

| () | ||||

| s.to |

where is a convex, compact subset of an space. For instance, can be a subset of the space of continuous functions or a reproducing kernel Hilbert space (RKHS) and can be induced by a neural network architecture with smooth activations or a finite linear combinations of kernels. In both cases, we know that can uniformly approximate arbitrarily well as the dimension of grows (Hornik, 1991; Berlinet & Thomas-Agnan, 2011). The smallest choice of is in fact (closed convex hull of ).

Analogous to the definitions from Section 2.1,

denotes the unparametrized dual function, is the set of Lagrangian minimizers associated to and

| () |

is the unparametrized dual problem. The subscript is used to denote quantities related to the unparametrized problem (). We now present two assumptions that allow us to characterize the relation between the dual and primal solutions of problem .

Assumption 3.1.

The functionals , , are convex and Lipschitz continuous in . Additionally, is strongly convex.

Note that we require convexity of the losses with respect to their functional arguments and not model parameters , which holds for most typical losses, e.g, mean squared error and cross-entropy loss.

Assumption 3.2.

There exists such that for all , and .

Assumption 3.2 is a stronger version of Slater’s constraint qualification, which requires only . Here, we require the existence of a (suboptimal) candidate that is strictly feasible even for perturbed versions of ().

Under these assumptions, the Lagrangian minimizer is unique. This makes the superdifferential of the dual function a singleton at every : , which means that the dual function is differentiable (Shor, 2013). Let be a solution of problem (). Assumptions 3.1 and 3.2 imply that strong duality (i.e, ) holds in this problem, and that at , there is a unique Lagrangian minimizer which is, by definition, feasible (Bertsekas, 1997).

The only difference between problems () and () is the set over which the optimization is carried out. Thus, if the parametrization is rich enough (e.g, deep neural networks), the set is essentially the same as , and we should expect the properties of the solutions to problems () and () to be similar. This insight leads us to the near universality of the parametrization assumption.

Assumption 3.3.

For all , there exists such that .

The constant in Assumption 3.3 is a measure of how well covers . Consider, for instance, that is the set of continuous functions and the set of functions implementable with a two-layer neural network with sigmoid activations and hidden neurons. If the parametrization has neurons in the hidden layer, it is considerably worse at representing elements in than one with neurons. While determining the exact value of is in general not straightforward, any can be achieved for a large enough number of neurons (Hornik, 1991). The same holds for the number of kernels and an RKHS (Berlinet & Thomas-Agnan, 2011).

Given these facts, it is legitimate to ask: how close are the elements of to in terms of their optimality and constraint satisfaction? Bounding these errors would theoretically justify the use of last primal iterates, doing away with the need for randomization.

3.1 Near-optimality and near-feasibility of dual learning

A key challenge of using duality to undertake () is that the value of the dual problem need not be a good approximation of the value of (i.e, lack of strong duality). This was tackled in (Chamon et al., 2023, Prop. 3.3). Explicitly, under Assumptions 3.1-3.3, the duality gap of problem is bounded as in

| (4) |

where maximizes . This result, however, only shows that the dual problem can be used to approximate the value of the constrained problem (). It says nothing about whether it can provide a (near-)feasible solution, which is the main issue addressed in this paper. We next characterize the sub-optimality and constraint violation of the Lagrangian minimizers by comparing these primal variables with the solution of the unparametrized problem .

The curvature of the unparametrtized dual function around its optimum is central to this analysis. We will first provide a result with the following assumption on this curvature and then describe its connection to the properties of (). Let denote the segment connecting and .

Assumption 3.4.

The dual function is strongly concave and smooth along .

The following proposition characterizes the constraint violation for all with respect to ; the optimal, feasible solution of the unparametrized problem.

Proposition 3.1.

Since () is feasible, is non-positive. Hence, the approximation bound in Proposition 3.1 is stronger than an infeasibility bound on . Indeed, it says not that , but that it approximates the constraint values of the optimal solution . The ratio (i.e, the condition number of ), which determines optimal step sizes in dual ascent methods (Polyak, 1987), also plays a key role here, representing the tension between two fundamental forces driving this bound. On the one hand, the sensitivity of the dual problems, controlled by , which determines how different and are. On the other hand, the sensitivity of the primal problems, linked to the smoothness constant , which determines the effect of this difference on feasibility.

Nevertheless, Proposition 3.1 remains abstract. To connect it to the properties of (), we rely on the following assumptions to obtain bounds on and .

Assumption 3.5.

The functionals , are -smooth on .

Assumption 3.6.

The Jacobian is full-row rank at the optimum, i.e, there exists such that , where denotes the Fréchet derivative of the functional at (see definition in Appendix A.1).

Assumption 3.6 is unlike the previous regularity assumptions over which a practitioner has full control and is not straightforward to satisfy at first sight. It is, however, a typical assumption used to derive duality results in convex optimization known as linear independence constraint qualification or LICQ (Bertsekas, 1997). As such, it could be replaced by a different constraint qualification, such as a stricter version of Assumption 3.2. This is, however, left for future work. Under these assumptions, we can describe the curvature of in terms of the problem parameters as follows.

Lemma 3.1.

Having characterized the curvature of the unparametrized dual function , we can now state the main result of this section, which puts together Proposition 3.1, Lemma 3.1, and the near-optimality result from (Chamon et al., 2023) in (4) to bound the near-optimality and near-feasibility of Lagrangian minimizers associated to optimal dual variables.

Theorem 3.1 shows that the dual problem () not only approximates the value of (), but also provides approximate solutions for it. The quality of these approximations depends on three factors. First, the sensitivity of the learning problem, as captured by the Lipschitz constant and the constants and , that correspond to the condition numbers of the constraint Jacobian and the objective function respectively. Overall, these quantities measure how well-conditioned the problem is. Second, the requirements difficulty. Indeed, the optimal dual variables can be seen as measures of the sensitivity of the objective value with respect to constraint perturbations (see, e.g., (Boyd & Vandenberghe, 2004)). Hence, the more stringent the constraints, the larger and/or .

Finally, the approximation error depends on the factor that denotes the richness of the parametrization, i.e., how good it is at approximating functions in (Assumption 3.3). In fact, Theorem 3.1 shows that as the model capacity increases ( decreases), the approximation bounds (5)–(6) improve. This behavior is not trivial. Indeed, while we expect that richer parametrizations lead to lower approximation errors, Theorem 3.1 states that they also make solving the optimization problem () easier, since dual solutions then provide better approximations of primal solutions. Observe that the effect of these factors on feasibility in (5) are similar to those on optimality in (6) and, e.g., (Chamon et al., 2023). Next, we leverage these results to provide convergence guarantees for Algorithm 1. But first, we outline the main ideas behind the proof of Proposition 3.1.

3.2 Proof Sketch

In this section, we provide a brief outline of the proof of Theorem 3.1. We begin by decomposing the distance between constraint violations as

| (7) | ||||

The first term captures the effect of parametrizing the hypothesis class for a fixed dual variable. In contrast, the second term characterizes the effect of changing the dual variables on the unparametrized Lagrangian minimizer. This is made clear in (7) by using the fact that (see discussion in Section 3). In the sequel, we analyze each of these terms separately. For conciseness, all technical definitions from this section are deferred to Appendix A.1.

3.2.1 Dual variable perturbation

We begin by analyzing the second term in (7). Recall from the beginning of Section 3 that under Assumption 3.1–3.2, it holds that . Hence, . Using the -smoothness of , this gradient difference can be bounded using . The latter can in turn be bounded by combining the -universality of the parametrization (Assumption 3.3) and convex optimization perturbation results to obtain:

3.2.2 Hypothesis class perturbation

Bounding the first term in (7) is less straightforward. To do so, we rely on the perturbation function of the unparametrized problem (), defined as

| () | ||||

| s.to |

for some perturbation . Intuitively, quantifies the impact on the objective value of modifying the constraint specifications by . Note that the unparametrized problem () is recovered for . Motivated by the fact that we can get a strong handle on the sensitivity of the perturbation function (), we seek to bound by instead analyzing for and . Indeed, it holds for every that , where † denotes the Fenchel conjugate (see Appendix A.4). We can therefore relate the curvature of to that (Kakade et al., 2009) to obtain:

Proposition 3.3.

4 Best Iterate Convergence

In this section, we leverage the connection between the parameterized [cf. () and ()] and unparameterized [cf. () and ()] problems to analyze the convergence of Algorithm 1. Seeking a more general result, we relax Steps 4 and 5 to allow for approximate Lagrangian minimization and the use of stochastic supergradients of the dual function respectively.

Explicitly, we assume that for all , the oracle in Step 4 returns a function such that

| (9) |

for an approximation error . In contrast to Step 4, equation 9 accounts for potential numerical and approximation errors in the computation of the Lagrangian minimizer. The existence of such a -approximate oracle is a typical assumption in the analysis of dual algorithms (Cotter et al., 2019; Chamon et al., 2023; Kearns et al., 2018) and is often justified by substantial theoretical and empirical evidence that many ML optimization problems can be efficiently solved despite non-convexity. That is the case, e.g., for deep neural networks (Zhang et al., 2021; Brutzkus & Globerson, 2017; Soltanolkotabi et al., 2018; Ge et al., 2017). Additionally, we consider that the dual variable update in Step 5 is replaced by

| (10) |

where are conditionally unbiased estimates of the statistical risks , i.e., . This stochastic update accounts for, e.g., the use of independent sample batches to estimate the constraint slacks .

The following Lemma establishes the convergence of the best iterate of (9)–(10), i.e., of the dual variables that yield the largest dual function for all .

Lemma 4.1.

Let be the maximum value of the parametrized dual function up to time . Then, for all , it holds that

where .

The existence of a finite is implied by the assumption that . Lemma 4.1 implies that for any , there exists a finite such that achieves the value . We denote this iterate . Note that the step size can be reduced so as to make arbitrarily close to (asymptotically). In view of the bound on the duality gap in (4), Lemma 4.1 implies that is near-optimal. Combine with the near-feasibility results from Section 3, we can also bound the constraint violations of the Lagragian minimizer associated with .

Reasonably, the bound in Proposition 4.1 is governed by the same terms as Theorem 3.1. Here, however, the bound is the loosened by the sub-optimality of with respect to .

5 Experimental Validation

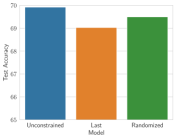

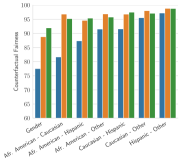

To illustrate the theoretical results from Sections 3 and 4, we return to the counterfactually fair learning problem from Example 2.1. We work with the COMPAS dataset, where the task is to predict recidivism while remaining insensitive to the protected variables gender and race, which can take the values [“Male”, “Female”] and [“African American”, “Hispanic”, “Caucasian”, “Other”] respectively. We take the parametrized model to be a 2-layer NN with sigmoid activations, so that the resulting constrained learning problem is non-convex. Further experimental details are provided in Appendix A.16. We compare the accuracy and constraint satisfaction of three models: an unconstrained predictor, trained without any additional constraints; a last iterate predictor, corresponding to the final iterate of an empirical version of Algorithm 1; and a randomized predictor that samples a model uniformly at random from the sequence of primal iterates for each prediction.

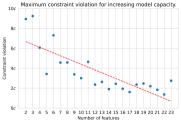

As shown in Fig. 2 (Left), the unconstrained model is slightly better than the two constrained ones in terms of predictive accuracy. This advantage comes at the cost of less counterfactually fair predictions, i.e., a model more sensitive to the protected features (Fig. 2, Middle). The key point of this experiment, however, is that the last iterate and randomized predictors provide similar accuracy and constraint satisfaction, as predicted by Theorem 3.1. Additionally, Fig. 2 (Right) showcases the impact of the parametrization richness on the constraint violation of last primal iterates. We control this richness by means of projecting the data onto a lower dimensional space using a fixed, random linear map. Note that, as Theorem 3.1 indicates, the constraint violation decreases by up to an order of magnitude as we increase the capacity of the model. As we have observed before, this behavior is not straightforward: though richer parametrizations are expected to lead to lower approximation errors, it is not immediate that it should make the optimization problem () easier to solve.

6 Conclusion

We analyzed primal iterates obtained from a dual ascent method when solving the Lagrangian dual of a primal non-convex constrained learning problem. The primal problem in question is the parametrized version of a convex functional program, which is amenable to a Lagrangian formulation. Specifically, we characterized how far these predictors are from the solution of the unparametrized problem in terms of their optimality and constraint violation. This result led to a characterization of the infeasibility of best primal iterates and elucidated the role of the capacity of the model and the curvature of the objective. These guarantees bridge a gap between theory and practice in constrained learning, shedding light on when and why randomization is unnecessary. The findings presented in this work can be extended in several ways. For instance, a study of the estimation error incurred by minimizing the empirical Lagrangian in Algorithm 1 could be added. It might also be possible to characterize the curvature of the dual function by alternative means, which could potentially lift assumptions on the unparametrized problem.

6.1 Acknowledgments

The work of A. Ribeiro and J. Elenter is supported by NSF-Simons MoDL, Award 2031985, NSF AI Institutes program. The work of L.F.O. Chamon is funded by the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) under Germany’s Excellence Strategy (EXC 2075-390740016).

References

- Agarwal et al. (2018) Alekh Agarwal, Alina Beygelzimer, Miroslav Dudík, John Langford, and Hanna Wallach. A reductions approach to fair classification. In International conference on machine learning, pp. 60–69. PMLR, 2018.

- Başar & Bernhard (2008) Tamer Başar and Pierre Bernhard. H-infinity optimal control and related minimax design problems: a dynamic game approach. Springer Science & Business Media, 2008.

- Berlinet & Thomas-Agnan (2011) Alain Berlinet and Christine Thomas-Agnan. Reproducing kernel Hilbert spaces in probability and statistics. Springer Science & Business Media, 2011.

- Bertsekas (1997) Dimitri P Bertsekas. Nonlinear programming. Journal of the Operational Research Society, 48(3):334–334, 1997.

- Bonnans & Shapiro (1998) J. Frédéric Bonnans and Alexander Shapiro. Optimization problems with perturbations: A guided tour. SIAM Review, 40(2):228–264, 1998. ISSN 00361445. URL http://www.jstor.org/stable/2653333.

- Boyd & Vandenberghe (2004) Stephen P Boyd and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Brutzkus & Globerson (2017) Alon Brutzkus and Amir Globerson. Globally optimal gradient descent for a convnet with gaussian inputs. In International conference on machine learning, pp. 605–614. PMLR, 2017.

- Chamon & Ribeiro (2020) Luiz Chamon and Alejandro Ribeiro. Probably approximately correct constrained learning. In H. Larochelle, M. Ranzato, R. Hadsell, M.F. Balcan, and H. Lin (eds.), Advances in Neural Information Processing Systems, volume 33, pp. 16722–16735. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper_files/paper/2020/file/c291b01517f3e6797c774c306591cc32-Paper.pdf.

- Chamon et al. (2023) Luiz F. O. Chamon, Santiago Paternain, Miguel Calvo-Fullana, and Alejandro Ribeiro. Constrained learning with non-convex losses. IEEE Transactions on Information Theory, 69(3):1739–1760, 2023. doi: 10.1109/TIT.2022.3187948.

- Cotter et al. (2018) Andrew Cotter, Maya R. Gupta, Heinrich Jiang, Nathan Srebro, Karthik Sridharan, Serena Lutong Wang, Blake E. Woodworth, and Seungil You. Training well-generalizing classifiers for fairness metrics and other data-dependent constraints. In International Conference on Machine Learning, 2018. URL https://api.semanticscholar.org/CorpusID:49556538.

- Cotter et al. (2019) Andrew Cotter, Heinrich Jiang, Taman Narayan, Seungil You, and Karthik Sridharan. Optimization with non-differentiable constraints with applications to fairness, recall, churn, and other goals. J. Mach. Learn. Res., 20(172):1–59, 2019.

- Daskalakis et al. (2021) Constantinos Daskalakis, Stratis Skoulakis, and Manolis Zampetakis. The complexity of constrained min-max optimization. In Proceedings of the 53rd Annual ACM SIGACT Symposium on Theory of Computing, pp. 1466–1478, 2021.

- Elenter et al. (2022) Juan Elenter, Navid NaderiAlizadeh, and Alejandro Ribeiro. A lagrangian duality approach to active learning. Advances in Neural Information Processing Systems, 35:37575–37589, 2022.

- Engelhard et al. (2023) Matthew M. Engelhard, Ricardo Henao, Samuel I. Berchuck, Junya Chen, Brian Eichner, Darby Herkert, Scott H. Kollins, Andrew Olson, Eliana M. Perrin, Ursula Rogers, Connor Sullivan, YiQin Zhu, Guillermo Sapiro, and Geraldine Dawson. Predictive Value of Early Autism Detection Models Based on Electronic Health Record Data Collected Before Age 1 Year. JAMA Network Open, 6(2):e2254303–e2254303, 02 2023. ISSN 2574-3805. doi: 10.1001/jamanetworkopen.2022.54303. URL https://doi.org/10.1001/jamanetworkopen.2022.54303.

- Fioretto et al. (2021) Ferdinando Fioretto, Pascal Van Hentenryck, Terrence W. K. Mak, Cuong Tran, Federico Baldo, and Michele Lombardi. Lagrangian duality for constrained deep learning. In Yuxiao Dong, Georgiana Ifrim, Dunja Mladenić, Craig Saunders, and Sofie Van Hoecke (eds.), Machine Learning and Knowledge Discovery in Databases. Applied Data Science and Demo Track, pp. 118–135, Cham, 2021. Springer International Publishing. ISBN 978-3-030-67670-4.

- Gallego-Posada et al. (2022) Jose Gallego-Posada, Juan Ramirez, Akram Erraqabi, Yoshua Bengio, and Simon Lacoste-Julien. Controlled sparsity via constrained optimization or: How i learned to stop tuning penalties and love constraints. In S. Koyejo, S. Mohamed, A. Agarwal, D. Belgrave, K. Cho, and A. Oh (eds.), Advances in Neural Information Processing Systems, volume 35, pp. 1253–1266. Curran Associates, Inc., 2022. URL https://proceedings.neurips.cc/paper_files/paper/2022/file/089b592cccfafdca8e0178e85b609f19-Paper-Conference.pdf.

- Ge et al. (2017) Rong Ge, Jason D Lee, and Tengyu Ma. Learning one-hidden-layer neural networks with landscape design. arXiv preprint arXiv:1711.00501, 2017.

- Goebel & Rockafellar (2008) Rafal Goebel and R Tyrrell Rockafellar. Local strong convexity and local lipschitz continuity of the gradient of convex functions. Journal of Convex Analysis, 15(2):263, 2008.

- Goh et al. (2016) Gabriel Goh, Andrew Cotter, Maya Gupta, and Michael P Friedlander. Satisfying real-world goals with dataset constraints. Advances in neural information processing systems, 29, 2016.

- Guigues (2020) Vincent Guigues. Inexact stochastic mirror descent for two-stage nonlinear stochastic programs, 2020.

- Hornik (1991) Kurt Hornik. Approximation capabilities of multilayer feedforward networks. Neural networks, 4(2):251–257, 1991.

- Hounie et al. (2022) Ignacio Hounie, Luiz F. O. Chamon, and Alejandro Ribeiro. Automatic data augmentation via invariance-constrained learning, 2022.

- Kakade et al. (2009) Sham Kakade, Shai Shalev-Shwartz, Ambuj Tewari, et al. On the duality of strong convexity and strong smoothness: Learning applications and matrix regularization. Unpublished Manuscript, http://ttic. uchicago. edu/shai/papers/KakadeShalevTewari09. pdf, 2(1):35, 2009.

- Kearns et al. (2018) Michael Kearns, Seth Neel, Aaron Roth, and Zhiwei Steven Wu. Preventing fairness gerrymandering: Auditing and learning for subgroup fairness. In International conference on machine learning, pp. 2564–2572. PMLR, 2018.

- Kiran et al. (2021) B Ravi Kiran, Ibrahim Sobh, Victor Talpaert, Patrick Mannion, Ahmad A Al Sallab, Senthil Yogamani, and Patrick Pérez. Deep reinforcement learning for autonomous driving: A survey. IEEE Transactions on Intelligent Transportation Systems, 23(6):4909–4926, 2021.

- Kurdila & Zabarankin (2006) Andrew J Kurdila and Michael Zabarankin. Convex functional analysis. Springer Science & Business Media, 2006.

- Kusner et al. (2018) Matt J. Kusner, Joshua R. Loftus, Chris Russell, and Ricardo Silva. Counterfactual fairness, 2018.

- Nedić & Ozdaglar (2009) Angelia Nedić and Asuman Ozdaglar. Approximate primal solutions and rate analysis for dual subgradient methods. SIAM Journal on Optimization, 19(4):1757–1780, 2009. doi: 10.1137/070708111. URL https://doi.org/10.1137/070708111.

- Polyak (1987) Boris T Polyak. Introduction to optimization. 1987.

- ProPublica (2020) ProPublica. Compas recidivism risk score data and analysis., 2020. URL https://www.propublica.org/datastore/dataset/compas-recidivism-risk-score-data-and-analysis.

- Ribeiro (2010) Alejandro Ribeiro. Ergodic stochastic optimization algorithms for wireless communication and networking. IEEE Transactions on Signal Processing, 58(12):6369–6386, 2010. doi: 10.1109/TSP.2010.2057247.

- Robey et al. (2021) Alexander Robey, Luiz Chamon, George J. Pappas, Hamed Hassani, and Alejandro Ribeiro. Adversarial robustness with semi-infinite constrained learning. In M. Ranzato, A. Beygelzimer, Y. Dauphin, P.S. Liang, and J. Wortman Vaughan (eds.), Advances in Neural Information Processing Systems, volume 34, pp. 6198–6215. Curran Associates, Inc., 2021. URL https://proceedings.neurips.cc/paper/2021/file/312ecfdfa8b239e076b114498ce21905-Paper.pdf.

- Rockafellar (1974) R Tyrrell Rockafellar. Conjugate duality and optimization. SIAM, 1974.

- Rockafellar (1997) R Tyrrell Rockafellar. Convex analysis, volume 11. Princeton university press, 1997.

- Shen et al. (2022) Zebang Shen, Juan Cervino, Hamed Hassani, and Alejandro Ribeiro. An agnostic approach to federated learning with class imbalance. In International Conference on Learning Representations, 2022. URL https://openreview.net/forum?id=Xo0lbDt975.

- Shor (2013) N.Z. Shor. Nondifferentiable Optimization and Polynomial Problems. Nonconvex Optimization and Its Applications. Springer US, 2013. ISBN 9781475760156. URL https://books.google.com/books?id=_L_VBwAAQBAJ.

- Solo & Kong (1994) Victor Solo and Xuan Kong. Adaptive signal processing algorithms: Stability and performance. 1994. URL https://api.semanticscholar.org/CorpusID:61115048.

- Soltanolkotabi et al. (2018) Mahdi Soltanolkotabi, Adel Javanmard, and Jason D Lee. Theoretical insights into the optimization landscape of over-parameterized shallow neural networks. IEEE Transactions on Information Theory, 65(2):742–769, 2018.

- Tran et al. (2021) Cuong Tran, Ferdinando Fioretto, and Pascal Van Hentenryck. Differentially private and fair deep learning: A lagrangian dual approach. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 35, pp. 9932–9939, 2021.

- Vapnik (1999) V.N. Vapnik. An overview of statistical learning theory. IEEE Transactions on Neural Networks, 10(5):988–999, 1999. doi: 10.1109/72.788640.

- Velloso & Van Hentenryck (2020) Alexandre Velloso and Pascal Van Hentenryck. Combining deep learning and optimization for security-constrained optimal power flow. arXiv preprint arXiv:2007.07002, 2020.

- Zhang et al. (2021) Chiyuan Zhang, Samy Bengio, Moritz Hardt, Benjamin Recht, and Oriol Vinyals. Understanding deep learning (still) requires rethinking generalization. Commun. ACM, 64(3):107–115, feb 2021. ISSN 0001-0782. doi: 10.1145/3446776. URL https://doi.org/10.1145/3446776.

Appendix A Appendix

A.1 Additional Definitions

Definition A.1.

We say that a functional is Fréchet differentiable at if there exists an operator such that:

where denotes the space of bounded linear operators from to .

The space , algebraic dual of , is equipped with the corresponding dual norm:

which coincides with the norm through Riesz’s Representation Theorem: there exists a unique such that for all and .

Definition A.2.

A function is said to be closed if for each , the sublevel set is a closed set.

Definition A.3.

A convex function is proper if for all and there exists such that .

Definition A.4.

Let be an Euclidean vector space. Given a convex function , its Fenchel conjugate is defined as:

A.2 Proof of Lemma A.1: Distance between dual functions

Lemma A.1.

The point-wise distance between the parametrized and unparametrized dual functions is bounded by:

| (11) |

As defined in section 2.1, denotes the Lagrangian minimizer associated to the multiplier in the unparametrized problem.

By the near-universality assumption, such that . Note that,

where we used the triangle inequality twice. Then, using the Lipschitz continuity of the functionals and the fact that , we obtain:

Since is a Lagrangian minimizer, we know that . Thus,

where the non-negativity comes from the fact that . This implies:

which conludes the proof.

A.3 Proof of Lemma A.2: Differentiability of

Lemma A.2.

Under assumption 3.1, the unparametrized dual function is everywhere differentiable with gradient .

From assumption 3.1, is strongly convex and is a non-negative combination of convex functions. Thus, the Lagrangian is strongly convex on for any fixed dual variable .

The convexity and compactness of imply that, in the unparametrized problem, the Lagrangian functional attains its minimizer for each . (see e.g, (Kurdila & Zabarankin, 2006) Theorem 7.3.1.) Then, by the strong convexity of , this minimizer is unique.

Since is affine on , it is differentiable on . Then, by application of the Generalized Danskin’s Theorem (see e.g: (Başar & Bernhard, 2008) Corollary 10.1) to and using that the set of minimizers of is a singleton, we obtain:

which completes the proof.

A.4 Proof of Lemma A.3: Distance between optimal dual variables

Lemma A.3.

Since is differentiable (see A.2) and strongly concave for :

From Lemma A.2 we have that ), then evaluating at we obtain:

By complementary slackness, . Then, since is feasible and : . Thus,

By Proposition 1: , which implies:

Thus,

| (13) |

Finally, since we have that : . Evaluating at and using that maximizes we obtain:

Using this in equation 13 we obtain,

A.5 Proof of Proposition 3.2: Perturbation of dual variables

Proposition.

The proof follows from straightforward applications of Lemma A.2 and Proposition A.3. Since the dual function is smooth, we have:

Then, the bound between optimal dual variables given in Proposition A.3 yields:

which concludes the proof.

A.6 Proof of Lemma 3.1: Curvature of the dual function

Lemma.

A.6.1 Strong concavity constant

As shown in Lemma A.2, the unparametrized Lagrangian has a unique minimizer for each . Let and .

By convexity of the functions for , we have:

Multiplying the above inequalities by and respectively and adding them, we obtain:

| (16) |

Since , we have that:

| (17) |

Moreover, first order optimality conditions yield:

| (18) | ||||

where denotes the null-opereator from to (see e.g: (Kurdila & Zabarankin, 2006) Theorem 5.3.1).

We will now obtain a lower bound on , starting from the smoothness of :

| (20) | ||||

Then, second term in the previous equality can be characterized using assumption 3.6:

| (21) |

For the second term, using the smoothness of we can derive:

| (22) | ||||

Then, using the reverse triangle inequality:

| (23) | ||||

Combining this with equation 20 we obtain:

| (24) | ||||

This means that we can write equation 19 as:

Letting , we obtain that the strong concavity constant of in is . A similar proof in the finite dimensional case can be found in (Guigues, 2020).

A.6.2 Smoothness constant

Set , , and let and denote the Lagrangian minimizers associated to these multipliers.

Since the unparametrized Lagrangian is differentiable and -strongly convex we have:

Using that is a minimizer, we obtain (see e.g: (Kurdila & Zabarankin, 2006) Theorem 5.3.1) :

Applying this to and we obtain:

Summing the above inequalities and applying Cauchy-Schwarz:

where the last inequality follows from assumption 3.1. Then, applying Lemma A.2 we obtain:

which means that has a smoothness constant .

A.7 Proof Lemma A.4

Lemma A.4.

Let denote the Fenchel conjugate of the perturbation function . For every we have that .

By definition of Fenchel conjugate:

| (25) |

Using the definition of the perturbation function we obtain:

| (26) |

Applying the change of variable , can be written as:

| (27) |

Since , the term is unbounded above for . Thus, we restrict the domain of to . In this region, maximizing over yields . We can thus write as:

| (28) |

Therefore,

A.8 Proof of Corollary A.1: Curvature of the perturbation function

Corollary A.1.

Let denote the segment connecting and . The perturbation function is strongly convex on with constant: .

We begin by stating a well-known Lemma on the duality between smoothness and strong convexity

Lemma A.5.

In order to apply Lemma A.5 we need to show that the perturbation function is convex and closed in the region of interest.

Convexity of for convex functional programs is shown in (Bonnans & Shapiro, 1998) or (Rockafellar, 1997) Theorem 29.1. Now we will show that is proper and lower semi continuous in the region of interest, which implies that it is closed.

The functional , defined on the compact set , is smooth. Thus, it is bounded on . From assumption 3.2 we have that the problem is feasible for . Therefore, . Moreover, by boundedness of , , implying that is proper.

Now, fix . Assumption 3.2 implies that the perturbed problem with constraint: is strictly feasible. Since this perturbed problem is convex and strictly feasible, its perturbation function is lower semi continuous at (see (Bonnans & Shapiro, 1998) Theorem 4.2). Note that . Thus, is lower semi continuous at .

We conclude that is proper and lower semi continuous for all .

A.9 Proof of Proposition A.1: Subgradients of

Proposition A.1.

The conjugate nature of the dual function and the perturbation function also establishes a dependence between their first order variations. This dependence is captured in the following lemma.

Lemma A.6.

If h is a closed convex function, the subdifferential is the inverse of in the sense of multivalued mappings (see (Rockafellar, 1997) Corollary 23.5.1):

Taking the gradient with respect to and evaluating at we obtain: . Then, Lemma A.6, yields the sensitivity result:

A.10 Proof of Proposition A.2: distance between optimal values

Proposition A.2.

Recall that and . We want to show that:

We start by showing that . Note that is feasible in the perturbed problem, since its constraint value is . Then,

Therefore,

| (29) |

Note that the dual function of the problem perturbed by is . Then, weak duality implies that for all . Evaluating at we obtain:

| (30) |

A.11 Proof of Proposition 3.3: Function class Perturbation

Proposition.

Let , using the strong convexity constant obtained in Proposition A.1 we have that:

where is a subgradient of at .

From Proposition A.1 we know that: . Thus,

Using the bound on obtained in proposition A.2 we can write:

This implies:

which concludes the proof.

A.12 Proof of Proposition 3.1: 2-norm near-feasibility

Proposition.

Proposition 3.1 stems from combining the feasibility bounds in Corollary 3.2 and Proposition 3.3:

| (32) | |||

| (33) |

Combining the above equations through a triangle inequality we obtain:

| (34) | ||||

| (35) |

Taking squares on both sides yields the desired result.

A.13 Proof of Theorem 3.1: Near-Feasibility and Near-Optimality

Theorem.

A.13.1 Near-Feasibility

Recall that Lemma 3.1 characterizes the strong concavity and smoothness of the dual function in terms of the properties of the losses and the functional space . The proof of this theorem stems from applying Lemma 3.1 to the 2-norm bound in Theorem 3.1.

We start by observing that:

| (38) | ||||

| (39) |

From proposition 3.1, we have that and . This implies that

where . Plugging this into equation 39, we obtain:

Finally, using the definitions of the condition numbers , we obtain:

| (40) |

which is the desired near-feasibility bound.

A.13.2 Near-Optimality

To derive the near-optimality bound, we combine equation 40 with the duality gap bound from (Chamon et al., 2023, Prop. 3.3):

| (41) |

where maximizes .

Since we have:

Then, using that the solution of the unparametrized problem is feasible (i.e, ) and we obtain

To conclude the derivation, note that the -universality and -Lipschitz continuity (Assumptions 3.3 and 3.1) imply that there exists such that for all . Thus,

| (42) | ||||

Note that the duality gap bound implies the approximate saddle-point relation:

Applying the right-hand side of this inequality to equation 42 we obtain:

which completes the proof.

A.14 Proof of Lemma 4.1: Best Iterate Convergence

Lemma.

4.1 Let be the maximum value of the parametrized dual function up to time . Then,

where is an upper bound on the norm of the second order moment of the stochastic supergradients.

A similar proof in the context of resource allocation for wireless communications can be found in (Ribeiro, 2010), Theorem 2. To ease the notation, we will denote the value of the parametrized dual function at iteration by . Similarly, will denote the largest value of encountered so far.

We start by deriving a recursive inequality between the distances of iterates and an optimal dual variable .

Proposition A.3.

Consider the dual ascent algorithm described in Section 4 using a constant step size . Then,

| (43) |

We delay the proof of Proposition A.3 to section A.14.1. We can observe that as the optimality gap decreases, the fixed term dominates the right hand side of equation (43), suggesting convergence of only to a neighborhood of . In order to show this, the main obstacle is that Proposition A.3 bounds the expected value of and we wish to establish almost sure convergence. This can be addressed by leveraging the Supermartingale Convergence Theorem (see e.g, (Solo & Kong, 1994) Theorem E7.4), which we state here for completeness.

Theorem A.1.

Consider nonnegative stochastic processes and with realizations and having values and and a sequence of nested -algebras measuring at least and . If

| (44) |

the sequence converges almost surely and is almost surely summable, i.e., a.s.

We define and as follows,

Note that tracks until the optimality gap falls bellow the threshold and is then set to 0. Similarly, tracks until the optimality gap falls bellow the same threshold and is then set to 0.

It is clear that , since it is the product of a norm and an indicator function. The same holds for , since the indicator evaluates to whenever . We thus have, for all .

We will leverage Theorem A.1 to show that is almost surely summable. Let be a sequence of -algebras measuring and . We will show that and satisfy the hypothesis of Theorem A.1 with respect to . Note that at each iteration, and are fully determined by . Therefore, conditioning on is equivalent to conditioning on , i.e: . Then we can write,

| (45) | ||||

On one hand, observe that if we have that . This is because in the case where , the indicator function also evaluates to . Therefore, if , it must be that . Then, trivially, .

On the other hand, when :

| (46) | |||

| (47) | |||

| (48) |

where we used the definition of and the fact the the indicator function is not larger than 1. Then, from proposition A.3 we have:

| (49) | ||||

| (50) |

where the last equality comes from the fact that implies .

This means that we can write equation 45 as:

| (51) | ||||

which shows that and satisfy the hypothesis of Theorem A.1. Then, we have that is almost surely summable, which implies,

This is true if either for some , or if , which concludes the proof.

A.14.1 Proof of Proposition A.3

Proposition.

A.3 Consider the stochastic supergradient ascent algorithm from Section 4 using a constant step size . Then,

| (52) |

Let denote the approximate stochastic supergradient . From the definition of :

| (53) |

where we used the fact that setting the negative components of to 0 decreases its distance to the positive vector and then expanded the square.

Note that for a given , the relations in 53 hold for all realizations of . Thus, the expectation of , conditioned on satisifes:

| (54) |

Furthermore, the stochastic supergadient yields, on average, an approximate ascent direction of the dual function :

| (55) |

Evaluating the previous inequality at and combining it with equation 54 we obtain:

| (56) |

which concludes the proof.

A.15 Proof Proposition 4.1

We will bound the distance between and by partioning it into terms that we have previously analyzed in Corollary 3.2 and Proposition 3.3:

The first term is of the same nature as the one analyzed in Corollary 3.2, since it is characterizes a perturbation in dual variables in the unparametrized problem. Thus, using the characterization of the curvature of the dual function from proposition A.3 and the sub-optimality of with respect to , this term can be bounded.

We denote by the segment connecting and and by the strong concavity constant of in . Using Lemma A.1 and the fact that we obtain:

Then, leveraging the almost sure convergence shown in Proposition 4.1 we have:

| (57) |

Note that equation 57 corresponds to the bound in Proposition A.4 but amplified by the sub-optimality of with respect to . Then, since the gradient is -Lipschitz continuous:

| (58) | ||||

| (59) | ||||

| (60) |

which completes the first part of the proof.

The term captures a perturbation in the function class for a fixed dual variable, and can be bounded by leveraging the perturbation analysis of Proposition 3.3. Let and . First note that the duality between smoothness and strong convexity detailed in Corollary A.1 implies that is strongly convex with constant on . Then, as in Proposition A.2, we can bound the distance between the optimal values associated to these perturbations and by:

| (61) |

| (63) |

| (64) | ||||

| (65) | ||||

| (66) | ||||

| (67) |

which concludes the proof.

A.16 Additional Experimental Details

We adopt the same data pre-processing steps as in (Chamon & Ribeiro, 2020) and use a two-layer neural network with 64 nodes and sigmoid activations. The counterfactual fairness constraint upper bound is set to . We train this model over iterations using a ADAM, with a batch size of 256, a primal learning rate equal to 0.1 and weight decay magnitude set to . The dual variable learning rate is set to 2.