Identification of Information Structures in Bayesian Games††thanks: This paper is based on the first chapter of my dissertation submitted to Yale University. I am deeply indebted to my advisors, Mira Frick, Johannes Höner, Ryota Iijima, and Larry Samuelson, for their invaluable advice and encouragement throughout the project. I am grateful to Dirk Bergemann, Krishna Dasaratha, Tetsuya Hoshino, Jonathan Libgober, Hitoshi Matsushima, Kyohei Okumura, Aniko Öry, Philipp Strack, Takashi Ui, Katsutoshi Wakai, and Kai Hao Yang. I also extend my appreciation to the seminar and conference participants from Hitotsubashi, HKU, ITAM, Kyoto, Yale, SWET2023 and the 33rd Stony Brook Conference for their helpful comments and discussion.

Abstract

To what extent can an external observer observing an equilibrium action distribution in an incomplete information game infer the underlying information structure? We investigate this issue in a general linear-quadratic-Gaussian framework. A simple class of canonical information structures is offered and proves rich enough to rationalize any possible equilibrium action distribution that can arise under an arbitrary information structure. We show that the class is parsimonious in the sense that the relevant parameters can be uniquely pinned down by an observed equilibrium outcome, up to some qualifications. Our result implies, for example, that the accuracy of each agent’s signal about the state is identified, as measured by how much observing the signal reduces the state variance. Moreover, we show that a canonical information structure characterizes the lower bound on the amount by which each agent’s signal can reduce the state variance, across all observationally equivalent information structures. The lower bound is tight, for example, when the actual information structure is uni-dimensional, or when there are no strategic interactions among agents, but in general, there is a gap since agents’ strategic motives confound their private information about fundamental and strategic uncertainty.

1 Introduction

1.1 Motivation and Overview

Imagine a situation where a population of agents is engaged in an incomplete information game. Payoffs depend on own and others’ action choices, as well as the realized state of the world. There is an outside observer—called an econometrician—who knows nothing about the structure of the game. This paper asks to what extent the econometrician can recover the informational traits of the agents—such as the informativeness of each agent’s signal about the state, or the correlation between different agents’ signals—by observing the outcome of the game. In other words, our interest lies in the identification of the underlying information structure.

Knowing agents’ informational traits can be of policy relevance because of their decisive roles in shaping the equilibrium of an incomplete information game. For example, in a standard model of market competition, firms may decide their production level based on their private information about an unknown demand function. In addition, the introduction of an exercise tax shrinks each firm’s production level, while private information matters how much it shrinks in equilibrium. Consequently, the government would appreciate learning the underlying information structure to choose the best policy, such as the optimal tax rate, based on reliable predictions about counterfactual economic outcomes. The fundamental difficulty is that the information structure is not directly observable, but it must be inferred from the observable data on firms’ past choices.

The presence of strategic interactions poses a crucial obstacle to identification exercise by confounding agents’ private information about fundamental and strategic uncertainty in their equilibrium action choices, yet, in proportions unknown to the econometrician. To illustrate this, suppose that a fairly high correlation is observed between a state realization and someone’s action. On one hand, the correlation could be attributed to the high predictive accuracy of the agent’s private information about the state. However, another possibility is that the agent has payoff-relevant motives to adjust her action to those of others, who are better informed of the state than her. In general, the observed correlation could be a result of the mixture of the “direct” correlation between the state and one’s signal and the “spurious” correlation confounded by other agents’ strategic behavior.

This paper takes a robust approach to analyze identification in such a situation. That is, we aim to derive identification results that do not require any prior knowledge about the exact parameters of the game.

Our analysis is performed in the general framework of linear-quadratic-Gaussian (LQG) games a là Radner (1962), which maintains the following two structural assumptions. First, each agent’s payoff function is concave and quadratic, so that the induced best-response strategy is linear in one’s best estimates about the fundamental state and other agents’ behavior. Second, the state and signals jointly follow a Gaussian process, known as an infinite-dimensional analog of normal distributions. Except for these requirements, our framework allows for general payoff networks (i.e, actions may be strategic complements or substitutes, with externalities varying flexibly across agents) and general information networks (i.e., correlations of agents’ private signals).

The focus on LQG games allows us to sidestep issues of non-existence or multiplicity of equilibrium. Theorem 1 shows that in almost every LQG game, there exists a unique affine equilibrium—i.e., an equilibrium in which each agent linearly responds to one’s private signal realization—that depends continuously on the parameters of the game. The theorem obtains without any substantial restriction on parameters. To this end, we develop the proof technique that delivers some independent theoretical interests by indicating the usefulness of the Riesz–Fredholm theory of integral equations.

Our identification analysis proceeds in three steps. First, we offer a simple class of canonical information structures, under which every agent receives a uni-dimensional signal that has an additively decomposable structure into the common payoff-relevant state and idiosyncratic noise. Theorem 2 shows that this class is rich enough to rationalize any possible equilibrium outcome that can arise under an arbitrary information structure. From the modeling perspective, therefore, the modeler incurs no loss of generality by proceeding as if signals are drawn from some member of the canonical class. On the other hand, the theorem points out the limit of full identification since it implies that any information structure is observationally equivalent to some canonical information structure. Thus, identification would be a hopeless task without prior restrictions on the class of information structures in consideration.

Second, we show that by restricting attention to the canonical class, the econometrician can identify the relevant parameters of an information structure up to some qualifications. Specifically, any canonical information structure is parameterized by two functions, one representing the exposure of each agent’s signal to the state and the other representing the correlations among idiosyncratic noise terms. Theorem 3 shows that these two functions are uniquely pinned down by an equilibrium outcome distribution up to absolute values. In other words, the econometrician can learn the magnitude of correlations, while the sign might remain ambiguous. Despite this limitation, however, our result implies that the accuracy of each agent’s signal about the state can be uniquely identified, as measured by how much observing the signal reduces the state variance. Moreover, Theorem 4 generalizes this observation and shows that the unique identification is possible for any higher-order uncertainty; for instance, we can identify the amount of second-order uncertainty by measuring it as the residual variance of some agent’s best estimate of the state conditional on other agent’s private signal. Robustness is an important feature of our identification results. Theorems 3 and 4 do not assume any prior knowledge of the econometrician about the underlying payoff structure.

Third, while identification is possible within the class of canonical information structures, a potential issue is that the actual information structure need not belong to this class. However, in this case, our identification result can be still useful, thanks to the systematic relations that hold between observationally equivalent information structures. Specifically, Theorem 5 shows that a canonical information structure characterizes the minimal amount by which each agent’s signal can reduce the state variance, across all observationally equivalent information structures. This result allows the econometrician to identify the lower bound on the accuracy of each agent’s signal. We further derive a necessary and sufficient condition under which the lower bound holds tightly. It turns out that the condition is automatically satisfied when the actual information structure is uni-dimensional, or when there are no strategic interactions among agents. In general, however, there is a gap between the lower bound and the actual variance reduction if there are strategic interactions among agents and the action space is not rich enough compared with the signal space in terms of dimensionality.

The rest of the paper is organized as follows. In Section 1.2 we give a review of the related literature. In Section 2 we set up the model of LQG games and define the relevant equilibrium concept. In Section 3 we investigate the theoretical properties of equilibria. The main analysis of this paper is conducted in Section 4. After we clarify the assumptions used for our identification exercise in Section 4.1, we establish the observational equivalence result in Section 4.2. We investigate the identification of an information structure within the canonical class in Section 4.3, and then, extend the analysis beyond the canonical class in Section 4.4 by focusing on state variance reduction. In Section 4.5 we provide illustrate our results by appealing to geometric arguments. In Section 5 we indicate some possible extensions. Section 6 concludes the paper. The appendixes collect omitted proofs and additional results that do not appear in the main body.

1.2 Related Literature

Bergemann and Morris (2013) study the issue of identification in a symmetric LQG game. They derive the partial identification of payoff structures by assuming that the econometrician is agnostic on the underlying information structure. The identification analysis in this paper is complementary to their analysis, as we are interested in the identification of information structures without assuming prior knowledge about the underlying payoff structure.

Besides the identification analysis, Bergemann and Morris (2013) analyze the issue of robust predictions by characterizing the set of equilibrium outcomes that can arise under any symmetric information structure. In contrast to this line of analysis, our identification analysis recovers the underlying information structure from a given observed equilibrium outcome. In Bergemann et al. (2015, 2021), they incorporate heterogeneous shocks on payoff-relevant states and examine the prediction range of equilibrium variables. These papers treat agents homogeneously, and in this regard, our equilibrium characterization generalizes their insights to accommodate heterogeneity in terms of payoffs and information. In the heterogeneous setting, Lambert et al. (2018b) provide robust predictions of market variables such as prices in the context of an asset market analysis à la Kyle (1985). Within this literature, the closest to this work is Bergemann et al. (2017a), who examine how different combinations of (possibly, heterogeneous) payoff and information structures can lead to an identical equilibrium action distribution. This is, in spirit, similar to our finding in Theorem 2, but we deliver complementary implications to theirs by establishing the outcome equivalence across different information structures while fixing a payoff structure.

There is the econometrics literature addressing identification in linear interaction models (Manski, 1993, 1995, Lee, 2007, Bramoullé et al., 2009). As Bergemann and Morris (2013) clarify, the regression models in these papers constitute the reduced forms of Nash equilibria in network games under complete information. The recent work by Blume et al. (2015) builds a structural model of linear interaction games and extends the identification analysis to incomplete information settings. They allow agents to receive private and public information, where the latter is also observed by the analyst. By contrast, our econometrician is agnostic on agents’ informational traits, and an information structure is arbitrary as long as Gaussian. While this strand of literature focuses on the identification of payoff parameters in a given and fixed network structure, the (informational) connections across agents themselves comprise the parameters of interest for us.

In comparison to the vast literature on belief elicitation in statistics (e.g., Savage, 1971) and economics (e.g., Karni, 2009), this paper aims to identify the ex-ante joint distribution of the state and signals, rather than eliciting the subjective belief about the state that may be formed after the signal realization. Also, we let the payoff structure be exogenously fixed and unknown to the econometrician, while the literature aims to design an incentive-compatible device to induce the agent’s truthful revelation of beliefs. Despite these differences, some papers have a commonality with our analysis. Chambers et al. (2019) take the robust approach of belief elicitation by considering the designer’s ignorance about the agent’s risk or uncertainty attitudes. Lambert et al. (2008) and Arieli and Mueller-Frank (2017) relate the richness of an action space to the possibility of belief elicitation. In a multi-agents setting, Bergemann et al. (2017b) analyze the elicitability of the agents’ higher-order beliefs.

Some recent papers analyze the identification of the information structure faced by a single agent. Lu (2016, 2019) offers revealed preference methods to identify the information structure from random choice. Libgober (2021) considers the identification of the information structure from what he calls contingent hypothetical beliefs. In contrast with these papers, our analysis emphasizes strategic interactions among many agents, which hinder the identification of agents’ informational traits by confounding their private information in the formulation of equilibrium strategies.

Apart from identification issues, the LQG models have been used in economic applications since Radner (1962), e.g., Cournot and Bertrand competitions (Vives, 1984, 1999), speculative trades (Kyle, 1985, Lambert et al., 2018b), beauty contest games (Morris and Shin, 2002), network games (Ballester et al., 2006, Bramoullé et al., 2014, Parise and Ozdaglar, 2018), public information transmissions (Angeletos and Pavan, 2007, Ui and Yoshizawa, 2015), and information design problems (Bergemann and Morris, 2013, Miyashita and Ui, 2023). From a theoretical point of view, this paper offers general results on the well-posedness of affine equilibria, which can also be useful in other contexts. Lambert et al. (2018a) obtain similar generic unique existence results in a finite-population setting. Compared with their results, our unique existence result goes through with a continuum of agents, which involves more technical toil, yet is needed when the modeler wants to eliminate the effect of individual choice on aggregate variables. Also, our proof strategy clarifies the important role of the eigenvalues of the equilibrium operator, which can provide a unified mathematical perspective as to how several existing results can be nested. Lastly, our continuity result is an addition to the literature.

2 Model

Our model is the generalization of the continuum-population models in Angeletos and Pavan (2007) and Bergemann and Morris (2013). We incorporate both payoff-relevant and informational heterogeneity across different agents by dropping their homogeneity assumptions. After we define a payoff structure and an information structure separately, we introduce a relevant equilibrium concept.

2.1 Payoff Structure

There are a continuum of agents who simultaneously choose a uni-dimensional action . Given an action profile , let denote the local aggregate for agent defined by

| (1) |

where is a given weight function such that measures the influence of ’s action over ’s local aggregate. Note that need not be binary-valued or symmetric. Also, the signs of strategic interactions need not be aligned across agents, e.g., when , the local aggregate for agent depends positively on ’s action, while it depends negatively on ’s action.

Let denote agent ’s utility function, where stands for the payoff value resulting from own action choice , the local aggregate , and the realization of an unknown state of the world . We specify each to be quadratic, i.e., for each , let there be a symmetric matrix with such that

We denote by , , and .111Here, denotes the -coordinate of the matrix .

The quadratic payoffs result in linear best-response strategies. Under complete information, given any action profile except , the first-order condition pins down the agent ’s payoff-maximizing action to be

and an analogous affine best-response formula is valid under incomplete information as well. Note that and the first row of —i.e., three functions , , and —suffice to describe the agent’s incentives. Moreover, no modeling flexibility is lost by letting be constant, since otherwise, one can consider an alternative weight function . In this regard, we shall normalize so that holds for all , and we refer to the profile as a payoff structure. Throughout, we assume that , , and are square integrable,222That is, , , and are all finite. but otherwise, they are arbitrary.

Example (Market Competition).

As a running example throughout the paper, we consider the following stylized model of market competition. A similar model has been repeatedly studied in the LQG literature, such as Vives (1984, 1999), Bergemann et al. (2015), and Lambert et al. (2018b).

The agents are interpreted as firms in the market for a single good. Each firm chooses the production level at the expense of the quadratic cost . The gross demand for the good is determined through the aggregate production and the realization of the state . By assuming the linear relations among them, let the firm’s (homogeneous) payoff function be specified as

Here, describes the exercise tax rate that is exogenously set by the tax authority, making the firms face the net price of per unit of the good. Clearly, the above payoff function is quadratic in , , and , with the associated payoff parameters , , and for all .

2.2 Information Structure

Throughout we fix the common prior over the state to be a normal distribution with mean and variance . Before making one’s decision, each agent observes the realization of a random signal , which is possibly multi-dimensional with . We specify the joint distribution of the state and signals to be a Gaussian process, i.e., any finitely many picks from the collection of random variables

follow a multi-variate normal distribution.333Within the economic literature, Gaussian processes are utilized by Bardhi (2020) to formulate a structural model of search and experimentation. Outside of economics, Gaussian processes are actively used in machine learning and spatial statistics; see, e.g., Hofmann et al. (2008) for a survey.

An advantage of Gaussian modeling is that the whole distribution can be summarized solely by the first and second moments of the distribution. Let denote the column random vector of agent ’s signal, and let be its mean vector. We use the following notation to describe the covariance matrices:

Moreover, for finitely many agents , we write

and notice that this matrix is symmetric and positive semidefinite by definition.444While symmetry is often subsumed in positive semidefiniteness, we treat these properties separately. In fact, not only necessary, these two properties are known to be sufficient for the existence of the corresponding Gaussian process.555According to Theorem 12.1.3 of Dudley (1989), given any set and any function , if a function satisfies “symmetry” and “positive semidefiniteness” for a bivariate function, then there exists a probability space on which a Gaussian process over having the mean function and the covariance function takes place. However, the resulting stochastic process may lack the needed integrability property; see Judd (1985) and Uhlig (1996). We shall impose two regularity conditions on strategy profiles in Definition 1 to guarantee their integrability in terms of Pettis (1938). Thus, Gaussian processes allow for flexible correlation of agents’ signals with the state and with other agents’ signals. We assume that is invertible for any finite set .

Since is (strictly) positive definite by assumption, so is . Thus, there exists a unique matrix root of . Then, for any , we define the matrices

In words, and are the standardized covariance matrices defined in a way analogous to correlation coefficients of random variables, i.e., the covariance matrices and are “divided” by the roots of variance matrices. Note that is the identity matrix by construction.

As we will see, an equilibrium depends on an information structure only through the matrix-valued functions and . In light of this, we simply refer to the profile as an information structure.

2.3 Strategy and Equilibrium

An LQG game consists of a payoff structure and an information structure . We assume that the profile is common knowledge among all agents, while an external observer may know it only partially or not at all. Rather, the observer aims at recovering the primitive components of —especially, an information structure—from an observed equilibrium outcome.

In what follows, we present formal definitions of strategies, strategy profiles, and the relevant equilibrium notion to our subsequent analysis.

Definition 1.

Each agent ’s strategy is a measurable mapping such that . Further, a collection of strategies is a strategy profile if it satisfies the following regularity conditions:

-

•

the mapping is (Borel) measurable for every ; and

-

•

the mapping is (Lebesgue) integrable.

Remark 1.

In a continuum-population LQG game, a strategy profile can be regarded as a stochastic process over , where the randomness of actions arises from the randomness of signals. Consequently, we need a formal definition of the integration of a stochastic process to deal with agents’ expected utility maximization, which involves the “stochastic” local aggregates of the form . In this paper, we adopt the notion of Pettis integral as introduced by Pettis (1938). The two regularity conditions in Definition 1 guarantee the integrability of a strategy profile in this context, as demonstrated in Lemma A.1. For further elaboration on the relevant mathematical definitions and lemmas, readers are referred to Miyashita and Ui (2024).

Having clarified the integral notion, we now introduce our equilibrium concept.

Definition 2.

A strategy profile constitutes a Bayesian Nash equilibrium if for any and , we have

| (2) |

where is defined as the Pettis integral. We often write as for the expectation operator conditional on ’s signal.

In this paper, we look at a Bayesian Nash equilibrium in which each agent responds linearly (more precisely, affinely) to one’s standardized Gaussian signal realization.666Other natural ways to define affine strategies would be such that or , but either is equivalent to Definition 3 since different and can be considered if necessary. The standardization turns out to be useful to economize later notation.

Definition 3.

A strategy is called affine if

| (3) |

for some and .

An affine strategy profile consists of functions and that describe the intercept and the slope of agents’ strategies, respectively. We use the notation to express the profile of functions including both. For brevity, the profile itself is often called an affine strategy profile, provided that the regularity conditions in Definition 1 are satisfied. Also, is called an affine equilibrium when it constitutes a Bayesian Nash equilibrium.

Definition 4.

For an affine strategy profile in an LQG game , the collection of random variables is referred to as the induced outcome of .

An induced outcome will be an important building block in our identification exercise, where the econometrician aims to recover the primitives of an LQG game from the distribution of . Note that the linearity of normal distributions implies that any affine strategy profile induces a Gaussian distribution over the state and actions, whose moments are characterized in the next lemma. The lemma also clarifies the necessary and sufficient condition for an affine strategy profile to be “valid” in the sense of Definition 1. The straightforward proof is omitted.

Lemma 1.

An affine strategy profile satisfies the regularity conditions in Definition 1 if and only if for all , where is the space of square integrable functions on . For any such , the induced outcome is a Gaussian process with mean and covariance

Thanks to the standardization of signals in Definition 3, the lemma implies that represents the mean of , and that captures the standard deviation of , as we have .

Example (Continued).

Together with the linear demand and quadratic cost functions, the market competition model becomes an LQG game when the unknown state and each firm’s private information are jointly Gaussian distributed. Each firm’s best-response strategy is linear in one’s best estimates about and the (random) aggregate demand , which is given as follows:

| (4) |

The configuration of equilibrium depends not only on payoff parameters but also on the information structure through the conditional distribution of the relevant variables.

3 Equilibrium Analysis

3.1 Well-posedness of Equilibrium

The first theoretical result posits that “almost every” LQG game is “well-posed,” that is, a unique affine equilibrium generically exists and changes continuously in primitives. In stating the next theorem, we topologize the space of LQG games based on the -norm, and the genericity is defined in terms of openness and denseness with respect to this norm. The formal definitions of relevant mathematical notions are collected in Appendix A.1, where we also provide the formal restatement of Theorem 1.

Theorem 1.

There exists a unique affine equilibrium for almost every LQG game. Moreover, if is a sequence of LQG game that converges to , and if has a unique affine equilibrium , then has a unique affine equilibrium for every large , and converges to .

Remark 2.

In a finite-population setting, Ui (2009, 2016) obtains parametric restrictions on payoff structures, under which an affine equilibrium always exists and is unique in the entire class, including non-affine strategy profiles. In Miyashita and Ui (2024), it is shown that this stronger uniqueness assertion can be extended to an infinite-population setting, up to some qualifications regarding measurability. In contrast, Theorem 1 imposes no restrictions on the parameters of , while the existence obtains “generically” and the uniqueness is restricted to the class of affine strategy profiles.

Remark 3.

In any knife-edge case where unique existence fails, there arise two possibilities, that is, either there exists no affine equilibrium or there exist a continuum of affine equilibria. This is simply because if and are two different solutions to the equation (BNE), then so must be their convex combination by the linear nature of the equation. Therefore, in the case of multiplicity, the cardinality of affine equilibria is necessarily uncountable.777Algebraically speaking, however, the space of multiple equilibria turns out to be small in the sense that it is isomorphic to a finite-dimensional linear space. This claim can be verified by using the first Riesz theorem; see Theorem 3.1 of Kress (2014).

3.2 Characterization via Fredholm Equation

Let us sketch the proof of Theorem 1 to illustrate the construction of an affine equilibrium, while the formal proof appears in Appendix A.2. Let be a candidate strategy profile, which is assumed to be affine and represented by coefficient functions . For this profile to constitute an affine equilibrium, the following first-order condition must be satisfied for all agents:

| (5) |

By substituting the definition of affine strategies (3) into (5), we obtain

where our Lemma A.1 justifies exchanging the order of integration over and ’s conditional expectation. Moreover, by using the Gaussian conditional formula, and are expressed in terms of affine functions of ’s signal , which are plugged into the previous expression of to yield

| (6) |

Matching the coefficients between (3) and (3.2) for each agent, we get the following -dimensional integral equation characterizing an affine equilibrium:

| (BNE) |

Together with Lemma 1, hence, the profile constitutes an affine equilibrium if and only if each component of it belongs to and solves the equation (BNE).

When agents are homogeneous, it is easy to derive a closed-form solution to (BNE) by postulating the symmetric configuration of an equilibrium. Though things are not as tractable in heterogeneous cases, we can still obtain desirable equilibrium properties by exploiting the structure of the equation; from mathematical points of view, it is one instance of Fredholm equation of the second kind, whose solvability is well studied in the Riesz–Fredholm theory of integral equations. The rest of the proof utilizes related tools in functional analysis to investigate when the relevant linear operator on a Hilbert space admits a bounded inverse.

Example (Continued).

Henceforth in the example, we assume that the mean of and are all zero. Also, assume that . Then, the first line of (BNE) implies that holds in equilibrium. Moreover, by substituting the coefficients of (4), the equilibrium slope is characterized as the solution to the equation

| (7) |

Theorem 1 implies that the unique solution to (7) exists for almost every .

3.3 Equilibrium Moment Restrictions

The equation (BNE) puts restrictions on each agent’s affine strategy by forcing it to take the sum of the weighted average of other agents’ affine strategies and the constant term determined through primitives. To gain some interpretations, notice that Lemma 1 allows us to rewrite the first line of (BNE) to

| (8) |

This equation decomposes the mean of each agent’s action into three parts, namely, the average of others’ mean weighted by , the response to the prior state mean, and the payoff-relevant constant term. Note that the characterization of the mean is independent of the signal distribution, but it depends only on and .

In a similar way, the second line of (BNE) imposes restrictions on the second moment of the induced equilibrium outcome. Specifically, by multiplying both sides of the equation by from left, the covariance expressions in Lemma 1 imply that

| (9) |

Thus, we see that individual volatility—i.e., the variance of each agent’s action—is decomposed into two parts, namely, one coming from the correlation with the opponents’ actions and the other coming from the correlation with the state. Notice that any affine strategy profile induces a Gaussian outcome distribution, which is just specified by the first two moments, so the displayed equations (8) and (9) characterize the obedience condition for the corresponding Bayes correlated equilibrium (Bergemann and Morris, 2013, 2016), applied to the present heterogeneous LQG environment.

Example (Continued).

To obtain the closed-form solution in the market competition model, let us assume that the firms face a symmetric and uni-dimensional information structure. Specifically, we consider the following signal-generating process:888As we will see, this corresponds to the special case of canonical information structures, introduced as Definition 5, such that the exposure function is constant and the idiosyncratic kernel is equal to an indicator function.

| (10) |

That is, each firm’s signal is expressed as the distortion of the true state by purely idiosyncratic noise . The constant coefficient measures the informativeness of each firm’s signal about the state. That normalizes the variance of to be one. Under the specification (10), one can explicitly solve (7) to derive the symmetric equilibrium slope

| (11) |

Note that the information structure (10) is parameterized by , while the authority may not know it when setting . Thus, the “optimal” level of is rather ambiguous without the knowledge about the information structure. Intuitively, this is because the increase of shrinks the production level, but how much it is reduced relies on the firm’s private information.

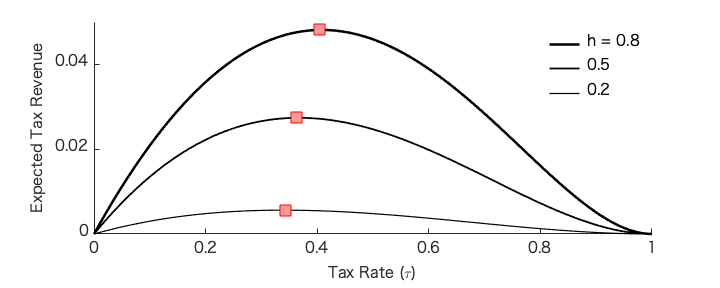

Assume, for concreteness, that the authority maximizes the expected tax revenue, which is equal to a -fraction of the gross price multiplied by the aggregate sales in equilibrium. Taking the expectation about and , we have

| (12) |

where the third line follows from the obedience condition (9), and the last line holds by Lemma 1. Then, plugging (11) into (12), we have

As displayed in Figure 1, the tax revenue as a function of behaves differently across . In particular, the maximizer of the function depends on how much demand uncertainty the firms face, which means that the authority needs to know the underlying information structure to optimally choose .

4 Identification of Information Structures

We now turn to our main focus, investigating the empirical content of Bayesian rational behavior in the LQG framework. This issue will be explored from the perspective of identification in econometrics (Manski, 1995). Suppose that our econometrician has access to the data on equilibrium outcomes, while she does not know precisely the primitives of an LQG game in play. Her objective is to recover the underlying information structure from observables, at least, in a partial sense.

4.1 Data and Hypothesis

Identification hinges crucially on the empirically relevant assumptions about a dataset and a structural model. It becomes more difficult for the econometrician to pin down parameters of interest when available data is weak and only limited hypotheses are made about the structural model. In what follows, we describe layers of such assumptions that we are going to consider.

We begin by describing an assumption about the data that the econometrician observes. Throughout we assume that the econometrician knows, at least, the common state prior, i.e., the fact that is ex-ante normally distributed with mean and variance . Since our interest lies in identifying the agent’s heterogenous informational traits, we consider the possibility of identification with access to rich individual choice data. The strongest form of such is to assume that the entire joint distribution of the state and actions is observable.999In the setting of homogenous agents, the joint observability is essentially equivalent to what is assumed in the identification analysis of Bergemann and Morris (2013). They assume that: “the econometrician observes the realized individual actions and the realized state. In other words, the econometrician learns the first and second moments of the joint equilibrium distribution over actions and state” (see pp. 1290–1291). Note that when private signals (and thus, actions) are conditionally i.i.d., there is no essential difference between assuming that the econometrician observers the realized actions and that she observes the entire distribution of each agent’s action. In contrast, we also consider weaker forms whose requirement levels differ with the chosen number .

-

•

(Joint Observability). The econometrician observes the joint distribution of .

-

•

(-Conditional Observability). The econometrician observes the conditional action distributions for finitely many distinct values of state realizations , which are also observable.

Given that the common state prior is known to the econometrician, the assumption of joint observability essentially postulates that the econometrician can observe the conditional action distribution for every state realization . This would be quite unrealistic if we interpret each realization of as a counterfactual event and the sampling process is limited. By contrast, under the alternative assumption of -condition observability, the econometrician has access to data on conditional action distributions just for finitely many state realizations.

Next, we set out assumptions imposed on a structural model—called hypotheses—that describe the econometrician’s prior knowledge about the underlying data-generating process. Throughout we shall adopt it as the most fundamental hypothesis that observed data is the result of Bayesian rational agents playing an affine equilibrium of some LQG game, while the econometrician does not have precise knowledge as to which LQG game is in play. Put differently, the econometrician faces a “parametric” identification problem, where the relevant parameters are the primitives of an LQG game. In particular, our interest lies in the identifiability of information structures .

| Data |

|

|

|||||

|---|---|---|---|---|---|---|---|

| Section 4.2 (Theorem 2) | Joint Obs. | Known | General | ||||

| Section 4.3 (Theorem 3) | -Cond. Obs. | Unknown | Canonical | ||||

| Section 4.4.1 (Theorem 4) | -Cond. Obs. | Unknown | Canonical | ||||

| Section 4.4.2 (Theorem 5) | -Cond. Obs. | Unknown | General |

Just like the observability assumptions, several hypotheses of varying strength will be considered in this section. A payoff structure is either completely known or unknown to the econometrician, depending on the nature of the results that we are going to derive.101010We employ different assumptions about payoff structures in such a way as to strengthen the conclusion of each theorem. Specifically, the observational equivalence result in Theorem 2 gets stronger by assuming that the econometrician knows the payoff structure. On the other hand, in Theorems 3–5, the possibility of identification becomes more significant without assuming any knowledge about the payoff structure. An information structure is unknown to the econometrician, but the set of information structures deemed possible depends on analysis. Specifically, we assume either the underlying information structure can be arbitrarily general or it belongs to what we call the “canonical” class (Definition 5). Table 1 clarifies the identification assumptions that we are going to consider to derive each result.

Example (Continued).

Hereafter, we discuss the example by viewing the tax authority as the econometrician. As we have seen before, the tax revenue depends both on the chosen and the underlying information structure, which is initially unknown. The tax authority has access to rich data on the firms’ past production choices under the initial tax rate, say , before changing it to another . Our observability assumptions require the observability of the distribution of each individual firm’s choices, by which the availability of a cross-section dataset is presumed.

One way to structure such a dataset is to record the realized values of states and actions for a long period of time. This sort of dataset may be feasible when the identical game is repeated over time but by redrawing shocks on the demand curve and private signals independently across time periods. Another way of interpreting the cross-section dataset is to view each index as the “type” of firms, rather than an individual firm, and construct the type ’s choice distribution in a given period. In this case, -conditional observability requires the repetition of the game just for a short period of time, but instead, there must exist sufficiently many firms belonging to whose choices are perturbed by purely idiosyncratic noise.

Regarding the econometrician’s hypotheses, it would be natural to assume that the payoff structure is known to the tax authority in the current context. More generally, however, our identification results can also speak about the situation where the tax authority does not know precisely how the demand shock and the aggregate production are translated into the market price.

4.2 Canonical Information Structure

In this section, we impose no hypothesis on the class of information structures to be considered. Instead, we assume that the econometrician observes the entire joint distribution of an equilibrium outcome and knows the precise payoff structure .

The next definition offers a class of simple information structures, which is going to be the key throughout all subsequent results.

Definition 5.

An information structure is said to be canonical if every agent receives a uni-dimensional signal, i.e., , which is generated by the following statistical model: For all ,

where is a (deterministic) function and is a centered Gaussian process that has a covariance function .

There are several special aspects of canonical information structures. First, under a canonical information structure, every agent just receives a uni-dimensional signal . Second, the variance is normalized so that . Third, is additively decomposable into two parts, that is, the common part—i.e., —and the idiosyncratic part—i.e., .111111A similar decomposable process is often used in finance under the name of -factor model (see, e.g., Al-Najjar, 1995), but our canonical model is more permissive since different agents’ noise terms can still have correlations. Since these are assumed to be uncorrelated, the exposure function represents the informativeness of each agent’s signal about the state . On the other hand, we still allow for the possibility that different agents’ idiosyncratic parts are correlated with one another, and the correlation is captured by the idiosyncratic kernel . Any canonical information structure is effectively summarized by the two functions and . In light of this, we shall refer to the pair itself as a canonical information structure.

The next theorem states that given any fixed payoff structure , an arbitrary general information structure has an observationally equivalent canonical information structure in the sense of generating the same joint distribution of equilibrium outcomes.121212This result can be related to Bayes correlated equilibrium à la Bergemann and Morris (2013, 2016). Specifically, we can show that given any payoff structure , the image of the mapping from to the distribution of is exactly given by the set of Bayesian correlated equilibria being Gaussian distributed. Analogous results are presented in Bergemann et al. (2017a), Miyashita and Ui (2023), and Miyashita and Ui (2024). As a mnemonic, hereafter, we are going to use superscripts “” with the intention of expressing variables associated with a canonical information structure.

Theorem 2.

Fix any payoff structure . Let be an arbitrary information structure, and let be an affine equilibrium in the LQG game such that for all . Then, there exists a canonical information structure and an affine equilibrium in the LQG game such that the induced outcome of has the same joint distribution as the induced outcome of .

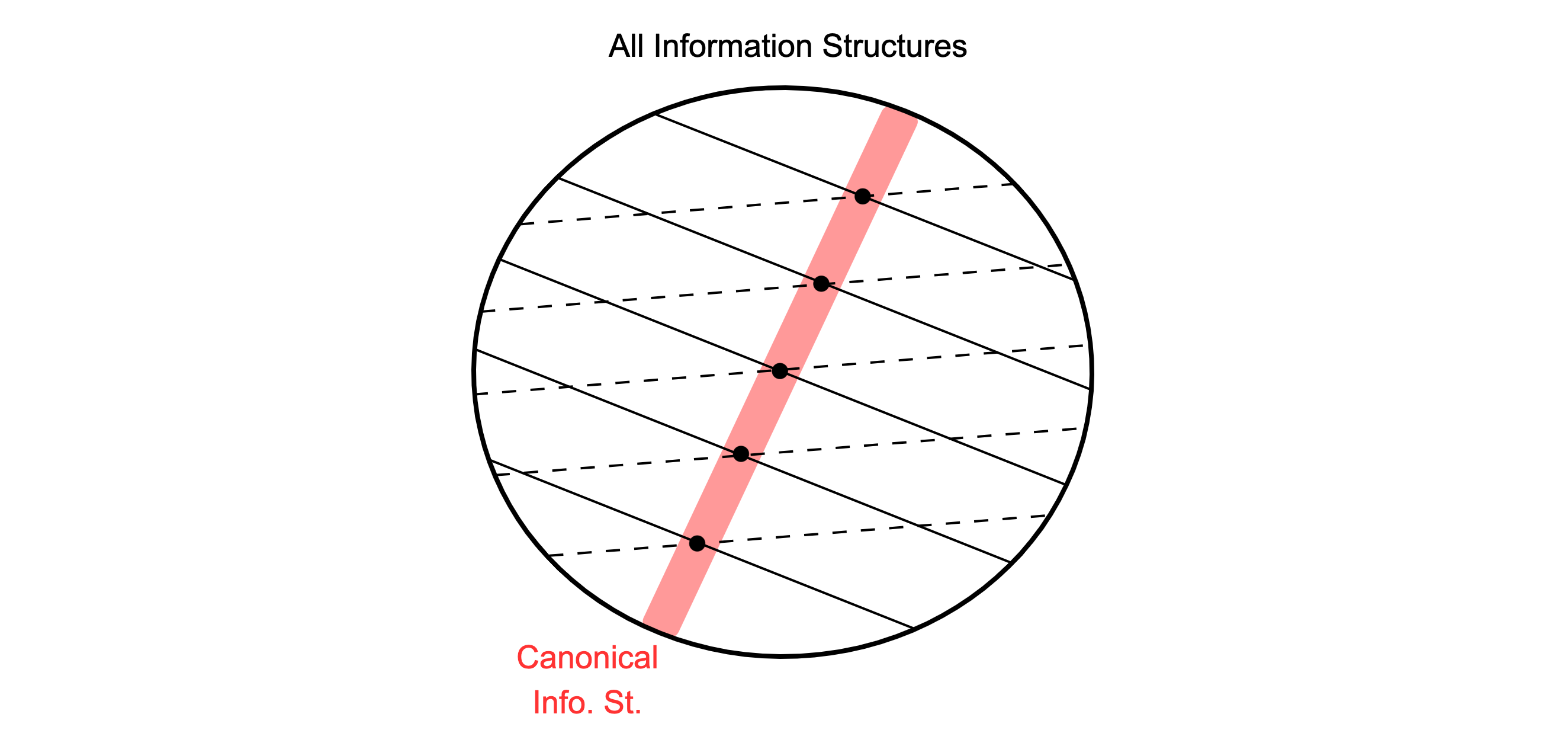

Roughly, Theorem 2 says that, given a fixed payoff structure, the whole set of information structures is divided into observationally equivalent subclasses, each of which has some canonical information structure as the representative element. This is schematically described in Figure 2, where the set of all information structures is divided by observationally equivalent subclasses, which are represented as parallel lines. The way of division depends on the choice of payoff structures, that is, different payoff structures give rise to different collections of parallel lines (solid or dashed). Regardless of the choice of a payoff structure, however, we can always find a canonical information structure as the representative element of each line.

From the modeling perspective, Theorem 2 implies that the modeler incurs no loss of generality to explain any possible equilibrium outcome by assuming as if agents’ signals are generated from some canonical information structure. On the other hand, the theorem points out the limit of the full identification of information structures, even when the strongest data is available to the econometrician if no hypothesis is made as to the class of information structures in consideration. In response to this observation, we thereby seek an affirmative resolution to our identification exercise by hypothesizing that the observed equilibrium outcome is a result of some canonical information structure.

4.3 Identification in the Canonical Class

From now on, we hypothesize that the underlying information structure belongs to the canonical class, and consider the identifiability of the associated exposure function and idiosyncratic kernel . Note that this canonicality hypothesis may not be regarded as an assumption about the econometrician’s prior knowledge. Rather, it can be interpreted as an as-if assumption made by the econometrician to facilitate the identification exercise. A potential issue is that economic variables identified under the as-if assumption need not reflect the actual variables of interest; this issue will be examined in Section 4.4 in relation to the identifiability of variance reduction.

The next theorem states that the parameters of canonical information structures are identified, at least, up to the magnitude. It turns out that the result only requires the weak forms of assumptions on the data and payoff structures, instead of employing the strong form of hypothesis on information structures. Specifically, joint observability is no longer needed, but rather, we just need conditional action distributions for two distinct state realizations. In addition, the identification can be robustly implemented in the sense that it requires no prior knowledge about the underlying payoff structure.

Theorem 3.

Let be an induced outcome of an unknown LQG game , and assume that is canonical and for all . Then, under the -conditional observability, is identified in the canonical class up to the absolute values, i.e., any two conditional action distributions and such that uniquely pin down the values of and for all .

This theorem indicates that identification becomes feasible up to mild qualifications by restricting attention to the canonical class, and in this sense, it proves the canonical class is parsimonious while being able to rationalize all possible equilibrium outcomes. We will illustrate Theorems 2 and 3 in Section 4.5 based on geometric arguments, but the key idea can be roughly explained as follows. The foundation for our identification result lies in the following reduced form expression of equilibrium actions:

| (13) |

implied from the definitions of affine strategies and canonical signals. By viewing the equation as the linear regression model, the orthogonality of the state and noise leads to the identification of coefficients, and , by regressing actions by the state realizations. Moreover, the normalization of canonical signals allows the econometrician to separate the exposure function from the identified cross term , while the value of is determined only in the absolute sense because of the multiplicative nature of coefficients.

As partly illustrated above, in the intermediate step to prove Theorem 3, we obtain the identification of an affine equilibrium that arises under the canonical information structure to rationalize the observed distribution of . The next corollary states that is fully identified, and is identified up to magnitude.

Corollary 1.

Under the same assumptions of Theorem 3, the equilibrium intercept , the magnitude of the equilibrium response , and the cross terms and are identified for all .

Again, the limitation of identification is that only , , and are identified, but not necessarily their signs. In other words, the econometrician can learn the magnitude of correlations, but the sign may remain ambiguous. This limitation comes from the following sort of attribution problem: The actions of two different agents could be negatively correlated for different reasons, that is, either because their signals are positively correlated but their reactions to signal realizations are opposite, or because their signals are negatively correlated but they react in the same direction.

One way to sharpen identification is to further strengthen the hypothesis on information structures. Let us say that a canonical information structure is positive if for all , i.e., every agent’s signal is positively correlated, at least, with the state. Notice that this definition still permits different agents’ signals to be negatively correlated. Clearly, under this additional hypothesis, the exposure function is point-identified from Theorem 3. Moreover, by using the cross terms identified in Corollary 1, the econometrician can also point-identify the equilibrium slope and the idiosyncratic kernel . While positivity may be ad-hoc in some cases, it is satisfied in many informational environments considered in the context of LQG games, e.g., Morris and Shin (2002) and Angeletos and Pavan (2007). In particular, the identification analysis of Bergemann and Morris (2013) also presumes the positivity of state-signal correlations that enables the identification of the sign of payoff-relevant parameters.131313See their Proposition 12. Relatedly, in the econometrics literature on network games, the positivity of social interaction matrices is used to obtain the identification results in De Paula et al. (2020); see their Corollaries 3 and 4.

Example (Continued).

Within the class of information structures (10), Theorem 3 indicates that the econometrician can identify the parameter by observing the choice distribution under initial . This allows the authority to “pin down” the tax revenue function in Figure 1, which in turn makes it possible to choose the optimal in a way to achieve the peak of the function.

The same approach can be used without assuming the symmetry across firms as in (10), but by assuming that an information structure is canonical and positive. Under these hypotheses, as explained above, Theorem 3 and Corollary 1 uniquely pin down the underlying canonical information structure . Then, since the econometrician as the tax authority can choose , she can compute the unique equilibrium slope function as the solution to the equation (7). Moreover, by using the relation (12), the tax revenue after changing the rate to any can be predicted.

4.4 Identification of Variance Reduction

The results in Section 4.3 are subject to two limitations. First, as already mentioned, the econometrician can learn the magnitude of correlations, but the sign may remain ambiguous. Second, identification relies on the as-if assumption that the underlying information structure belongs to the canonical class.

The purpose of this section is to assess the significance of these limitations in the context of identifying the informativeness of individual agents’ signals, as captured by their (state) variance reduction defined by

| (14) |

Here, and , respectively, stand for the conditional expectation and variance operators given the set of signals of agents in . The dependence of on the information structure reflects the fact that agents’ signals are generated from it. A challenge is that is not known a priori. We thereby examine the extent to which this value is revealed through equilibrium behavior in the presence of the two limitations mentioned early.

The above-defined variance reduction is a compelling measurement for the informativeness of signals, especially, in the present Gaussian environment since it does not depend on the realization of conditioning events. Moreover, by viewing each agent’s signal as a statistical experiment for the state, the result of Hansen and Torgersen (1974) implies that the informativeness ranking induced by variance reduction coincides with that of Blackwell (1951). Given the strong theoretical foundations for Blackwell’s ranking, this provides a further rationale for us to focus on variance reduction to measure the informativeness of agents’ signals.

4.4.1 Canonical Identification of (Higher-order) Uncertainty

To begin with, we isolate the first limitation of the previous identification results from the second by hypothesizing that signals are generated from an unknown canonical information structure . Then, by Theorem 3, the parameters of can be identified up to absolute values. Indeed, absolute values will be enough to identify the variance reduction due to the quadratic nature of the index. That is, the indeterminacy of signs is not a serious problem as far as the econometrician’s aim is to identify the amount of private information as measured by variance reduction.

Identification is not only possible for variance reduction, but also for the amount of any higher-order uncertainty faced by agents. To provide systematic analysis, we shall flip the sign of the index, and instead, look at the amount of first-order uncertainty as measured by the residual state variance conditional of team ’s signals. The notion can be extended to higher-order cases; for general , let us define the amount of -th order uncertainty faced by along the path of subsets to be

We interpret this quantity as representing the amount of uncertainty that faces regarding what thinks about thinks about […] thinks about the state (i.e., the estimate made by about ).

Theorem 4.

Under the same assumptions of Theorem 3, is identified for any and any finite sequence of finite sets .

4.4.2 Variance Reduction Gap

While Theorem 4 hypothesizes that signals are generated from a canonical information structure , the potential issues is that the actual information structure could be different yet observationally equivalent to . In other words, the amount of uncertainty, identified under the canonicality hypothesis, may not be invariant with respect to the change of information indistinguishable from the outside point of view.

In what follows, we investigate how well —i.e., the variance reduction identified in Theorem 4 under the canonicality hypothesis—reflects the actual variance reduction when and are “observationally equivalent.” To investigate this question, it will be convenient to introduce the formal notions of observational equivalence.

Definition 6.

Two information structures and are (weakly) observationally equivalent if there exist payoff structures and such that the LQG games and , respectively, have unique affine equilibria and for which the induced outcomes of and have the same joint distribution.

Notice that the above definition is more permissive than the notion of observational equivalence considered in Theorem 2, because and can now be coupled with possibly different payoff structures to induce the same outcome distribution. Adopting this “weak” notion reflects the econometrician’s ignorance not only about an information structure but also a payoff structure. Nevertheless, for two information structures that are just weakly observationally equivalent, we can identify systematic relationships between them as stated in the next theorem.141414Notice that the implication of Theorem 5 gets more substantial by adopting the weak notion of observational equivalence as in Definition 6, while the significance of impossibility in Theorem 2 is strengthened with the strong notion that further requires .

Theorem 5.

Let be an arbitrary information structure, and let be a canonical information structure, and assume that they are observationally equivalent. Then, we have . Moreover, for any finite set , the equality obtains if and only if there exists a vector such that the actual LQG game and its affine equilibrium satisfies

| (15) |

where and are the following block-diagonal matrices:

This theorem delivers two results. The first result is the weak inequality to be generally satisfied between an observationally equivalent pair of information structures. When combined with Theorem 4, this result implies that we can identify the “lower bound” on variance reduction that holds across all information structures that are observationally equivalent to the canonical . This lower bound describes the amount of information about the state that each subset of the population collectively possesses, at least.

In general, however, there is a gap between the lower bound and the variance reduction obtained under the actual information structure . The second result is the necessary and sufficient condition under which the gap disappears. Roughly, the equality condition is satisfied if the team ’s equilibrium strategies in the actual LQG game are “proportional” to the vector in the right-hand side of (15) that is determined by the actual information structure. In particular, in the case of a singleton set , the condition can be simplified to

| (16) |

which says that the equilibrium slope is proportional to the signal-state correlation vector. As such, since and are vectors of dimension , the proportionality condition is trivially satisfied when , provided that . The same observation extends to a general team .

Corollary 2.

Suppose that the actual information structure is uni-dimensional, i.e., . Then, holds for any finite set , provided that for all .

This corollary implies that it is exactly the uni-dimensionality of canonical information structures that enables the canonical class to serve as the characterization of the lower bound on the amount of variance reduction, while other structural assumptions placed in Definition 5, such as normalization or decomposability, is not essential to derive this lower-bound property. Also, it should be remarked that the difference between uni- and multi-dimensional information structures hinges on our modeling assumption that each agent takes a uni-dimensional action, whereas her signal could be multi-dimensional. In Section 5, however, we will generalize Corollary 2 to accommodate multi-dimensional actions and show that the variance reduction gap disappears whenever the dimension of an action space is weakly greater than that of a signal space (Proposition 1). Namely, it is the algebraic richness of actions vis-à-vis signals that is crucial to achieving the full identification of variance reduction.

The algebraic richness demands more than the topological richness, which, roughly speaking, requires any action to be arbitrarily well approximated by another action. The latter has been the key for rational behavior to reveal private information in other contexts such as social learning; Lee (1993) demonstrates that with a continuum of actions, each agent’s rational behavior can fully reveal one’s private signal to successors, and the failure of social learning as in Banerjee (1992) and Bikhchandani et al. (1992) will be stripped away.151515A similar insight extends to a general single agent’s prediction problem about the payoff-relevant state. Specifically, Arieli and Mueller-Frank (2017) show that if (and only if) an action set contains no isolated point, the decision maker’s rational behavior perfectly reveals her subjective belief for generic decision problems. Obviously, the condition is satisfied when the action space is . As such, the crucial ingredient of our model is the presence of payoff externalities among agents, which makes agents care not only about the fundamental state but also others’ strategic behavior. As a result, their equilibrium strategies confound both aspects of each agent’s best estimates about the fundamental and strategic uncertainty, which complicated the econometrician’s identification problem.

The substantial role of strategic interactions can be clearly highlighted through the characterization of the equilibrium slope function, that is, the second-moment restriction. Specifically, in the second line of (BNE), notice that the signal-state covariance vector appears as the second term on the right-hand side, and consequently, the proportionality condition is automatically satisfied for a singleton set if the first integral term vanishes. This happens, for example, when is constantly equal to zero (among other cases). Hence, the absence of strategic interactions makes it possible for equilibrium actions to fully reveal each agent’s best estimate of the fundamental state. This observation leads us to the next corollary, which together collects other possible cases of when the integral term vanishes.

Corollary 3.

Suppose that a unique affine equilibrium exists in the actual LQG game and that . Then, holds if either of functions , , , or is zero for almost every .

To illustrate the confounding issue caused by strategic interactions, suppose that the econometrician observes a fairly high correlation between agent ’s action and the state realization . The correlation could be attributed to the high predictive accuracy of agent ’s signal about , which enables the agent to better adjust her action to the state. Yet, another possibility is that is just highly predictive about another agent ’s signal, as well as ’s action, which is in turn highly correlated with the state. In other words, the observed correlation between and could be just “spurious” as being caused through the combination of ’s strategic motive to coordinate with and ’s fundamental motive to well adapt the state. While these two possibilities are hardly distinguished from the outside viewpoint, the combination of our Theorems 4 and 5 indicates that the econometrician can, at least, tightly identify the minimum amount of private information on the state held by agents.

Example (Continued).

The expected tax revenue could be calculated for a counterfactual tax rate under the hypothesis that an information structure is canonical. This would not be the case in general, however, our identification results can be still useful to derive the lower bound on the expected tax revenue by identifying the lower bound on the accuracy of firms’ private information.

To relate an information structure with the tax authority’s objective, we recall that from (12), the expected tax revenue is represented as a -fraction of the integration of individual action volatility. The next lemma provides a lower bound on the expected tax revenue for a general information structure by deriving the lower bound on individual volatility based on the equilibrium characterization (7).

Lemma 2.

In equilibrium, the following lower bound on the expected tax revenue holds:

| (17) |

Now, we observe that amounts exactly to the variance reduction of firm under an information structure , thus its lower bound can be identified through Theorems 4 and 5 to hold across all observationally equivalent information structures. Combining this with (17), we can then obtain the lower bound on the expected tax revenue for any counterfactual rate .

4.5 Geometric Illustration

In this section, we explain the logic behind our identification results, Theorems 2–5, by appealing to geometric arguments. To this end, suppose for simplicity that the econometrician has access to the data on the joint distribution of an equilibrium outcome . Also, assume that every random variable has zero mean.161616This assumption is without loss of generality since one can consider the de-biased random variable by subtracting the mean if necessary. Then, we consider the Hilbert space consisting of all zero-mean and square-integrable random variables defined on the probability space on which the Gaussian process is taken place. In Figures 3 and 4, we depict by vectors to schematically express any members of . Notice that the inner product between any elements of is given as their covariance. We assume that for all agents to avoid degenerate cases.

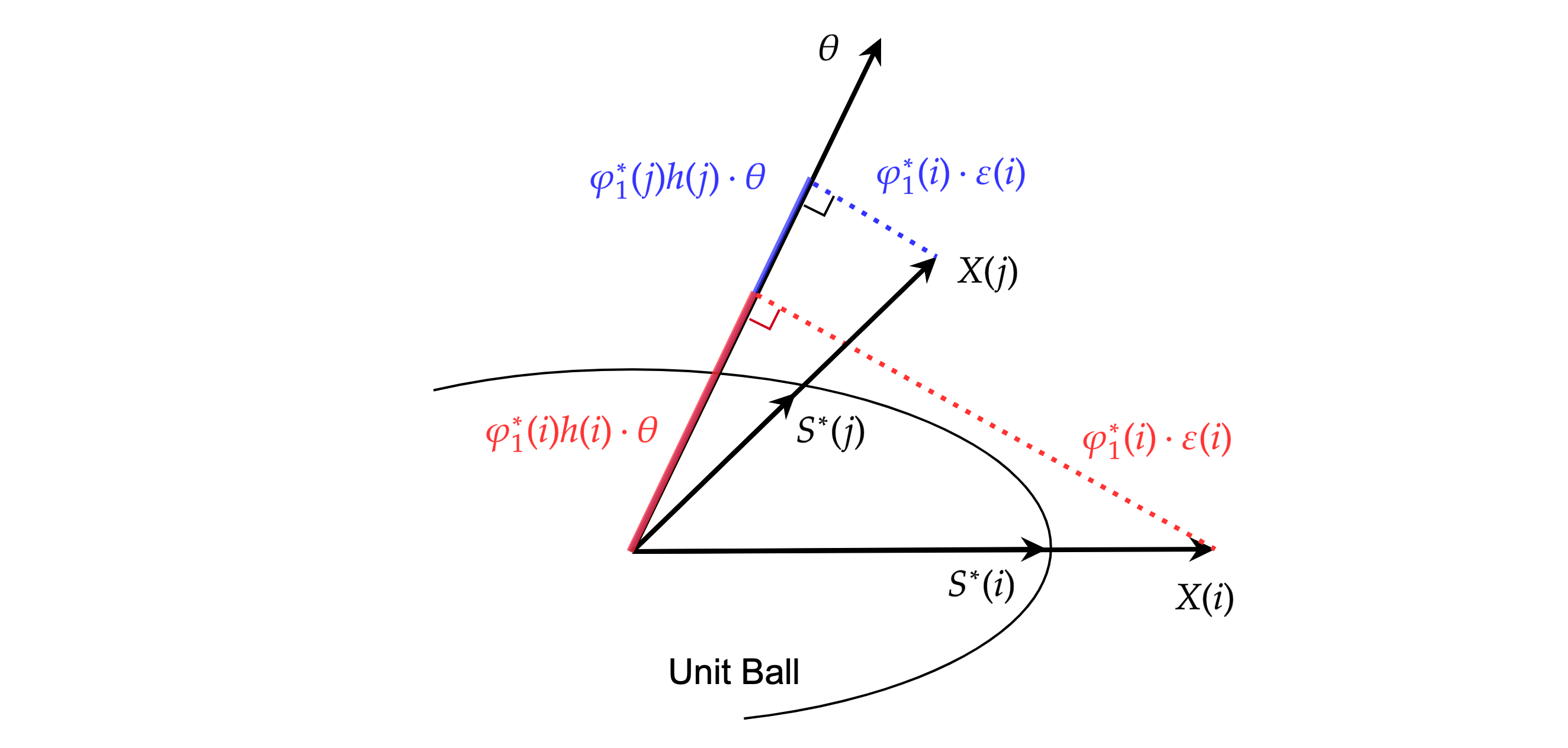

Constructing a canonical information structure. We first discuss Theorems 2 and 3 together to demonstrate how one can construct a “unique” canonical information structure to rationalize the observed equilibrium outcome . Our point of departure is the reduced form equation (4.3) that should be satisfied by , together with the associated affine equilibrium , to be consistent with the distribution of (note that by the zero-mean assumption). To determine the values of these functions, we consider the linear regression of each on . Then, it is a result of the standard projection theorem that there exists a unique function and a unique process living in the orthogonal complement of the span of such that

| (18) |

Then, matching the coefficients between (4.3) and (18), we can uniquely recover the cross term by equalizing it to . Also, we can recover by equalizing it to the inner product between the residual terms and in the regression (18). In particular, the uniqueness of orthogonal decompositions implies that these cross terms are point-identified, as stated in Corollary 1.

The above regression procedure is illustrated in Figure 3. Here, the actions and are orthogonally decomposed into the exposure to the state and the residual, which gives rise to the identification of the cross terms in Corollary 1. In order to determine the canonical information structure from , we still have to extract these functions from the above-identified cross terms. At this point, the normalization of canonical signals—namely, holds—has a role in providing an additional equation that we can use to recover three unknown functions (i.e., , , ). Geometrically, this requirement forces each canonical signal to rest on the boundary of the unit ball. Algebraically, it places the parametric requirement on by forcing them to satisfy . Combining this equation with the preceding cross terms, we can then pin down the three unknown functions, yet, up to absolute values because of the multiplicative nature of the relevant equations.171717An exception is , which must be positive to represent the variance of . In Figure 3, we spot as the positive scalar multiplication of , but it would also be possible to locate it at the exact opposite of the diameter of the unit ball, in which case the signs of and are flipped. This provides the rationale for the uniqueness in Theorem 3. Notice that the underlying payoff structure is relevant to determine , but identification does not require any knowledge about it, as we directly recover the agents’ reactions to their signals by regressing their observed actions on the state realizations.

There are two remaining things to be verified to justify Theorem 2,. First, the recovered function should be positive semidefinite to represent the covariance of the Gaussian process. Second, we have to check that constitutes an affine equilibrium under the canonical information structure . Both can be verified through the distributional properties of , as we will thoroughly discuss in the appendix proof. Especially for the latter, an important observation is going to be that is an equilibrium outcome, and hence, its distribution obeys the moment restrictions of the form (8) and (9).

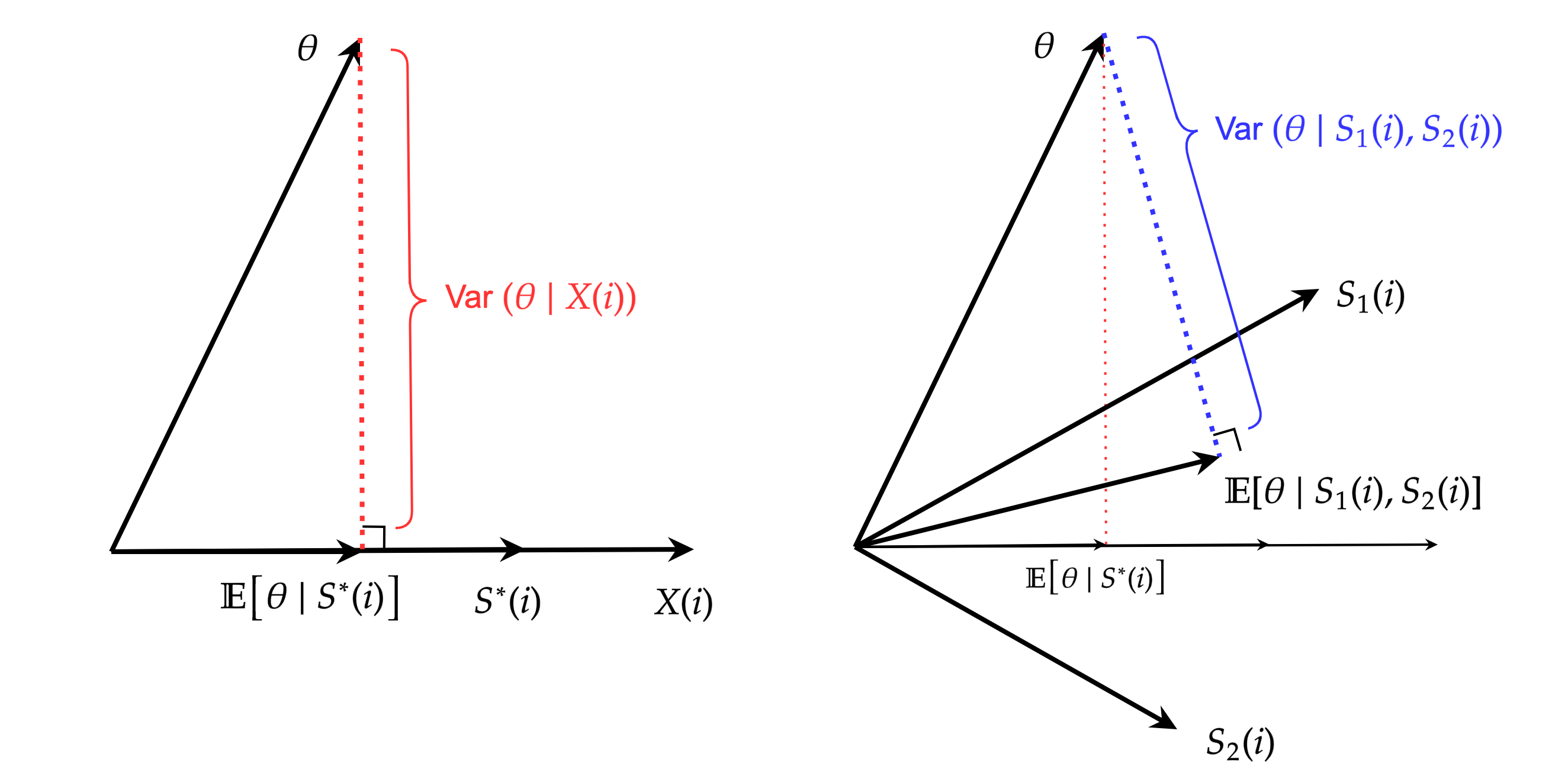

Variance reduction gap. Now, let us provide the intuitions for Theorems 4 and 5 by exploiting similar geometric arguments. Our starting point is the observation that the action is a linear transformation of the canonical signal . Thus, observing either of them reduces the same amount of the state variance, i.e., we have

| (19) |

This is geometrically illustrated in the left panel of Figure 4, where and span the same linear subspace, onto which is orthogonally projected to yield the best estimate about the state conditional on observing , or equivalently, . Then, the residual variance (19) is measured as the distance between and the span of , which corresponds to the residual in the linear regression of on . More generally, the residual variance of any team can be obtained by calculating the residual in the linear regression of on , which provides the rationale for the identifiability of the (first-order) uncertainty in Theorem 4.

Next, to gain the intuition for Theorem 5, let us assume that the actual information structure generates a two-dimensional signal for each agent. In the right panel of Figure 4, the agent ’s best estimate corresponds to the projection of onto the span of and , whose residual gives rise to the agent ’s residual variance . At this point, notice that the action is a linear transformation of the actual signal , and thus, so must be the canonical signal . This implies that we necessarily have a more accurate estimate about the state by estimating it from than from , which indicates that the weak inequality generally holds. We can geometrically interpret this in the figure by observing that the dashed blue line must be always weakly shorter than the dashed red line. On the other hand, equality is achieved if and only if both and lie on the same linear subspace spanned by . This geometric observation can be algebraically translated to the proportionality condition (15). Notice that the condition is automatically satisfied when is uni-dimensional since, in that case, all of , , and must be parallel to each other.

On the other hand, when is multi-dimensional, the condition is generically violated, except on the knife edge, and there generally arises a gap between and . Specifically, the gap can be quantified by the geometric measure of (squared) cosine similarity as follows:

| (20) |

Here, denotes the cosine of the angle between vectors , which is known as a measurement of the proximity between two vectors. The fact that the ratio is expressed as the “squared” cosine similarity means that the variance reduction gap gets small when the agent’s equilibrium response and the signal-state correlations are close to each other in terms of the minor angle spanned by them. In particular, the gap becomes minimal (resp. maximal) when the two vectors are parallel (resp. orthogonal).

5 Extensions

So far, we have imposed several modeling assumptions, either implicitly or explicitly, to facilitate our analysis and notation. Some of them can be relaxed to further generalize our findings. This section discusses some possible extensions.

5.1 Idiosyncratic Payoff Shock

Several preceding papers admit the heterogeneity across agents in terms of payoff-relevant states (Bergemann et al., 2015, 2017a, Lambert et al., 2018a). That is, there are as many states as the number of agents, and each state is relevant just to the corresponding agent’s payoff. For example, Bergemann et al. (2015) model the heterogeneous payoff shocks by letting , where the base state is perturbed by i.i.d. Gaussian noise . In the present framework, we can incorporate general payoff shocks by extending the primitive collection of random variables to

Let us continue to assume that the above-defined is Gaussian, i.e., any finitely many picks from follows a multivariate normal distribution.

We note, however, that this change brings about no essential change in any of our analysis due to the flexibility of our baseline model. Indeed, repeating the same arguments that derive (BNE), one can show that an affine strategy profile constitutes a Bayesian Nash equilibrium under the present setup if and only if solves the following Fredholm equation:

Here, , , , and all other terms are the same as before. Importantly, payoff shocks affect only the constant term in regard with , but they do not affect the integrands. As a result, the above equation has a unique solution if and only if and are such that the original equation (BNE) has a unique solution.181818It is worth mentioning that whether or not a given LQG game has a unique affine equilibrium does depend only on and ; see Lemma A.6 in the proof of Theorem 1. On the other hand, other parameters entering the constant term of the Fredholm equation affect which occurs in a knife-edge irregular case, multiplicity or non-existence. Moreover, when all are i.i.d. perturbations of the common state as in Bergemann et al. (2015), any noise added to is irrelevant for the analyst’s inference problem about . Hence, all the previous results are kept the same verbatim.

5.2 Multi-dimensional Action

As the geometric arguments in Section 4.5 suggests, the key to obtain the variance reduction inequality is to intermediate it by the amount of the state variance reduced by observing the action (whose distribution is the same under and ). That is, we consider the index of variance reduction defined for actions such that

| (21) |

where is an affine strategy defined based on .191919Here, the index is defined as a function of and since it depends on the entire LQG game only through these two components. Note that it is defined for any affine strategy profile , and most results in Section 4.4.2 hold regardless of whether it constitutes an affine equilibrium. The exception is Corollary 3, which exploits the relationship between the affine equilibrium and the primitives of . Then, the proof of Theorem 5 reveals that is, in general, weakly less than , while the equality obtains if is uni-dimensional. At this point, what makes the uni-dimensional information structures special is the uni-dimensionality of actions, which our model has maintained so far. As we show below, however, a similar observation extends to incorporating multi-dimensional actions. This extension highlights the importance of the relative dimension of actions vis-à-vis signals for the point-identification of state variance reduction.

We now consider the situation where each agent takes a multi-dimensional action upon receiving a multi-dimensional signal , where . An affine strategy in this setting is described as

where the intercept is a constant vector, and the slope is a constant matrix such that the -th column describes how the agent ’s -th action is determined responding to her standardized signal. Ignoring the intercept, as it is irrelevant to computing variance reduction, an affine strategy profile would then be identified with a matrix-valued function such that every argument belongs to . Then, for any information structure the index is defined analogously to (21) for each team , as the amount of state variance reduced by observing -dimensional actions of the agents in .

The next proposition reveals that is weakly less than , while the equality obtains if actions are rich enough to span multi-dimensional signals.

Proposition 1.

For any information structure and affine strategy profile , we have . Moreover, for any finite set , the equality obtains if and only if there exists a vector satisfying (15), where the matrix is now defined as

In particular, the equality condition holds if has full row rank.

According to Proposition 1, the observer can reduce the state variance by observing multi-dimensional actions as much as she could do by directly observing multi-dimensional signals if and only if the proportionality condition (15) holds. Importantly, the condition is automatically satisfied when has full row rank, or equivalently, so does for every . As such, when , the full rankedness is just saying that is non-zero, which is generically satisfied. In general, that is necessary for to have row full rank, and conversely, it is “almost” sufficient as well, since generic matrices in have rank . Therefore, our result suggests that the richness of actions, relative to signals, in terms of dimensionality is important to achieve the zero variance reduction gap between those statistical experiments.

6 Conclusion

This paper studies the identification of an information structure from the distribution of equilibrium actions in a game of incomplete information played by a continuum of agents. To this end, we offer a canonical class of information structures and show that the class is sufficient to rationalize any equilibrium outcome, yet, parsimonious to admit sharp identification results. Moreover, it is shown that a canonical information structure characterizes the minimal amount of private information on the fundamental state that each agent possesses, across all observationally equivalent information structures, as measured in terms of state variance reduction. The lower bound is tight when there are no strategic interactions among agents, but in general, there is a strict gap, because agents’ strategic motives confound their private information about fundamental and strategic uncertainty.

Appendix A Omitted Proofs

In this Appendix A, we provide all proofs omitted from the main text. We start by summarizing the notation that we are going to use, especially, in the proof of Theorem 1. All mathematical definitions are standard and can be found in Lax (2002), Brezis (2010), or Kress (2014), which are the main sources of the functional analysis tools that we are going to utilize.

A.1 Mathematical Preliminaries

We denote by the space of -dimensional (column) vectors and by the space of -matrices. We adopt the Euclidean norm on denoted by . The induced operator norm on is denoted by .

For and a compact set , we denote by the Hilbert space of vector-valued functions , equipped with the inner product

and denote the induced norm by . Note that . Extending this definition for a matrix-valued function , we define its norm by . For a linear operator , we denote the induced operator norm by . Let denote the set of real eigenvalues of . An identify operator is usually denoted by .

In accordance with the above notation, the norm for a payoff structure is given by

and all of which are assumed to be finite as mentioned in Section 2.1. Also, the norm for an information structure is given by

Putting these together, we measure the distance between two LQG games having the same dimensionality based on

| (A.1) |