Estimation of parameters and local times in a discretely observed threshold diffusion model

Abstract

We consider a simple mean reverting diffusion process, with piecewise constant drift and diffusion coefficients, discontinuous at a fixed threshold. We discuss estimation of drift and diffusion parameters from discrete observations of the process, with a generalized moment estimator and a maximum likelihood estimator. We develop the asymptotic theory of the estimators when the time horizon of the observations goes to infinity, considering both cases of a fixed time lag (low frequency) and a vanishing time lag (high frequency) between consecutive observations. In the setting of low frequency observations and infinite time horizon we also study the convergence of three local time estimators, that are already known to converge to the local time in the setting of high frequency observations and fixed time horizon. We find that these estimators can behave differently, depending on the assumptions on the time lag between observations.

Keywords: Threshold diffusion, maximum likelihood, generalised moment estimator, local time, discrete observations.

AMS 2020: primary: 62F12; secondary: 62M05; 60F05; 60J55.

1 Introduction

We consider the diffusion process solution to the following stochastic differential equation (SDE)

| (1.1) |

with piecewise constant volatility and drift coefficient, possibly discontinuous at ,

We assume the initial condition to be deterministic. Separately on and , the process follows the drifted Brownian motion dynamics with different parameters. We also assume that and , so that the process is mean reverting and ergodic.

We discuss the estimation of parameters from discrete observations of , when the threshold is known. We consider two types of drift estimator: a generalized moment estimator (GME) and a maximum discretized likelihood estimator (dMLE). We prove that they are equivalent in a suitable sense, so that the asymptotic theory we develop applies to both.

We construct the GME, based on discrete observations, using the theoretical long time behavior of conditional moments and local times of . Maximum likelihood estimation (MLE) of this process has been considered in Lejay and Pigato (2020), assuming that is continuously monitored and the observation span goes to infinity. Since we assume here to observe the process at discrete times, we study the corresponding dMLE, with observation span going to infinity.

We consider two types of asymptotic setting: (a) fixed time lag (low frequency observations) and number of observations going to infinity, and (b) shrinking time lag (high frequency observations) and simultaneously time horizon going to infinity. In all cases we prove consistency and asymptotic normality of GME and dMLE estimators. We also show that the dMLE based on observations converges in high frequency to the MLE based on continuous observations, with speed , and an analogous result for the GME. Moreover, in setting (a), we propose a GME for the diffusion coefficient, for which we prove again consistency and asymptotic normality.

Finally, we consider three different estimators for the local time at the discontinuity level , that are known to converge to the local time with speed in the high frequency limit of the observations. We show that when the observation lag is fixed and the time horizon goes to infinity, the asymptotic behavior is the same as for the local time only for one of the estimators, while the other two have different limit behaviors, that depend on the observation lag.

Related work.

The solution to (1.1) with piecewise affine instead of piecewise constant drift is the so-called threshold Ornstein-Uhlenbeck (OU) process, for which parameters inference (including the threshold ) has been discussed e.g. in Kutoyants (2012); Dieker and Gao (2013); Su and Chan (2015, 2017); Yu et al. (2020); Hu and Xi (2022); Mazzonetto and Pigato (2024). Estimation of a piecewise constant drift as in (1.1), despite the process having several applications (see below), has been considered less, see e.g. Mota and Esquível (2014); Lejay and Pigato (2020).

In the low frequency observations setting, the main tool we use in this paper is the ergodic theorem in the form of (Meyn and Tweedie, 2009, Theorem 17.0.1), in the multidimensional framework as in (Brooks et al., 2011, Section 1.8), in the spirit of Hu and Xi (2022). In the high frequency observations setting, we obtain that the asymptotic behavior is the same as for the continuous observations case, under the condition , analogous to the condition given for diffusions with no threshold in (Kessler, 1997; Ben Alaya and Kebaier, 2013; Amorino and Gloter, 2020) and with threshold in Mazzonetto and Pigato (2024).

As already mentioned, several local time estimators for Brownian motion or skew Brownian motion, with fixed time horizon and observations, have been considered in the literature (see e.g. Portenko (1994); Borodin (1986); Lejay and Pigato (2018, 2020); Lejay et al. (2019)) and they are known to converge to the local time with speed in the high-frequency limit of the observations (Jacod, 1998; Mazzonetto, 2019). Local time approximation is an important topic in statistics of processes, for instance because the amount of time spent at a certain level is related to the accuracy of the estimation of the process at that level (Florens-Zmirou, 1993). Recently in Christensen and Strauch (2023); Christensen et al. (2023) the local time of a scalar diffusion model have been used in the exploration phase of studies of the exploration vs exploitation tradeoff in a reinforcement learning setting. The authors point out the difficulties related to local time estimation and propose strategies to avoid it.

The process in (1.1) and variations of it have been widely used in financial modelling, from the point of view of time series (see e.g. Ang and Timmermann (2012); Mota and Esquível (2014); Lejay and Pigato (2019)), options pricing and implied volatility (see e.g. Lipton and Sepp (2011-10); Gairat and Shcherbakov (2016); Dong and Wong (2017); Lipton (2018); Pigato (2019); Buckner et al. (2024)), interest rates (see e.g. Pai and Pedersen (1999); Decamps et al. (2006); Su and Chan (2015, 2017)) and others. The discrete time analog of threshold diffusions are Threshold autoregressive (TAR) and in particular self-exciting (SETAR) models (Tong, 2011; Chen et al., 2011). They have been widely used in financial modelling, recently also in combination with reinforcement learning in Giorgi et al. (2023). Threshold processes have also a wide range of applications outside of financial modelling; for example, Hottovy and Stechmann (2015) discusses deterministic and stochastic triggers in threshold diffusion models for rainfall and convection. For other applications of the specific threshold diffusion in (1.1) we refer to Lejay and Pigato (2020).

Outline.

2 Estimators and convergence results

Without loss of generality, we assume the threshold is at . Indeed, given solution to (1.1) with known level (threshold) , the process solves (1.1) with threshold at and initial condition . As a consequence, all the results in this document can be easily rewritten in the case .

So, let be the solution to (1.1) with , Brownian motion, and deterministic (see Le Gall (1985) or Bass and Chen (2005) for strong existence results). We assume that and , so that the process is mean reverting and ergodic. In this case, also the discrete time process (the so-called skeleton sampled chain) is ergodic, for any (this can be proved as in (Hu and Xi, 2022, Lemma 1)).

Given , we assume to observe over a time grid with discretization step such that . The (symmetric) local time of at , denoted by , is a continuous process quantifying the amount of time spent by close to level up to time . An estimator of the local time is given by

| (2.1) |

We refer to Section 2.3 for details on the local time, convergence results and alternative local time estimators. Writing , let us introduce quantities

| (2.2) |

and their discrete counterparts

| (2.3) |

Throughout the paper we use the notation for a Gaussian variable with mean vector and covariance matrix . We also write for a standard Gaussian. We use in what follows the notion of stable convergence, that we denote , for which we refer to Rényi (1963); Jacod and Shiryaev (2003); Jacod and Protter (2012). We also write for almost sure convergence, for convergence in probability, for convergence in law.

2.1 Drift parameters inference

We consider estimators for the drift parameters in (1.1), based on the quantities above (see next Section 2.4 for a derivation). The first one is a GME

| (2.4) |

The second one is a dMLE, that can also be interpreted as a least squares estimator (LSE)

| (2.5) |

In what follows, we provide a complete asymptotic theory for these estimators. We consider different settings, depending on the assumptions on and , which can be as follows:

-

1.

is a fixed constant and (long time, since , and low frequency);

-

2.

, with fixed and (high frequency);

-

3.

, with and as (long time and high frequency).

We show that the estimators in (2.4) and (2.5) are asymptotically equivalent as the time horizon goes to infinity (see Lemma 3 in Section 4.2), so that both next Theorems 1 and 2 hold for both estimators, in exactly the same form. For this reason, we state our results in extended form only for .

We first consider the long time, low frequency framework, meaning that we observe the process over a discrete time grid with fixed time lag, with number of observations going to infinity.

Theorem 1.

The result for is proved in Section 4.3 using ergodic theorems. By Lemma 3 in Section 4.2, we deduce the result for from the one for .

We now assume to observe the process over a discrete time grid with vanishing time lag, with the number of observations going to infinity in a way so that the time horizon also goes to infinity (long time and high frequency framework).

Theorem 2.

Let be positive sequences satisfying and

Then

-

i)

the estimator is consistent:

-

ii)

if in addition

(2.6) the estimator is asymptotically normal, i.e.

where

Precisely the same results hold substituting estimator with .

The next result shows that when the time horizon is fixed, both the estimators above, based on discrete observations, converge in high frequency, with speed , to their continuous time analogues.

Theorem 3.

Let be fixed and . Then, both

| (2.7) |

when , converge stably to

| (2.8) |

with a standard Gaussian random variable independent of , and local time of at , up to time .

This theorem is proved in Section 4.2.1.

2.2 Volatility parameters inference

We now introduce an estimator for the volatility parameters based on discrete observations with a fixed discretization step. Let us denote

| (2.9) |

and

| (2.10) |

This is a GME estimator as the one in (2.4). We consider its long time behavior.

Theorem 4.

Let fixed. Then

-

i)

the estimator is consistent:

- ii)

This theorem is proved in Section 4.3.

When high frequency observations are available, the quadratic variation estimators considered in Lejay and Pigato (2018) seem more suitable for estimating . However, in (2.10) could be the better choice for estimating when is observed at a low frequency, since high frequency observations are not required for convergence. Let us also note that a joint version of Theorems 1 and 4 could be written, providing a joint convergence of , with speed and asymptotic covariance again of the form in (4.15), this time a by matrix.

2.3 Local time estimation

Given a semi-martingale and , , the quantity

defines the (symmetric) local time of at , which quantifies the amount of time spent by close to level up to time , properly re-scaled. We focus here on the local time at the discontinuity of , that is . Because of the ergodic property, the rescaled local time converges:

| (2.11) |

(cf. (Borodin and Salminen, 2015, Chapter II 35(c))). There are several ways to approximate the local time from discrete observations of . We have already introduced the estimator in (2.1). A well known estimator is the one from renormalization of number of crossings, which is

We define also the estimator “from sample covariance”

where is the discrete covariation of two one-dimensional processes , over observations with a time lag . The process denotes the positive part of and its negative part (which is positive).

The three statistics above converge to the local time for fixed final horizon when (the number of observations) goes to infinity, with speed (see Mazzonetto (2019)). We now study their behavior for low frequency (fixed time lag) observations, in long time.

Let us denote with any function s.t. as .

Lemma 1.

This lemma is proved in Section 4.3. The behavior of the three estimators is consistent with (2.11) if we only look at the first term in the expansion of the limit. However, the term is non zero for the limit of and . So the only estimator having the same limit behavior as the local time, when observations are in low frequency and the time horizon goes to infinity, is . Furthermore, note that is the only one that does not require previous knowledge of the volatility parameters.

2.4 Derivation of the estimators and comments on the results

Derivation of the estimators.

The dMLE in (2.5) has been proposed in (Lejay and Pigato, 2020) and is the maximum of a discretized classical likelihood for the solution of a SDE, based on the Girsanov transform. It can also be derived as a LSE with contrast function

The GME (2.4) is related to the one proposed for a different threshold SDE in (Hu and Xi, 2022). If the process is ergodic, the GME estimator is derived from the inversion of quantities such as , where and is a r.v. whose distribution is the invariant one (it has density (4.2), see Section 4.1). In particular, one can compute a notion of asymptotic occupations time as

| (2.15) |

These quantities can also be approximated from discrete observations using the ergodic theorem (cf. next equations (4.16) and (4.19)). From the approximations to (cf. next equations (2.11)-(2.12)) and to one can derive the estimators in (2.4). Note that similar estimators could be defined using or , but these would not have the correct limit (they would not be consistent) as , for fixed , because of Lemma 1. However, for small they could give good approximations.

Similarly, the definition of the volatility estimator in (2.10) follows from the same approximations and the asymptotic value of , corresponding to the first conditional moment used in Hu and Xi (2022). Note the dependence on in , not present in and .

The local time estimators are special cases of the class of statistics considered for instance in Jacod (1998) for Brownian diffusions for fixed time horizon. In the context of threshold diffusions for fixed time horizon, was considered in Lejay and Pigato (2020), the estimator related to the number of crossings, , was considerd in Portenko (1994); Lejay et al. (2019), and was considered in Lejay and Pigato (2018).

On the equivalence of drift GME and dMLE, beyond the ergodic regime.

In Lemma 3 we see that, in the ergodic case, GME and dMLE are equivalent in long time. This is because the dMLE is essentially given by the sum of two parts, one corresponding to the GME, the other given by the final and initial value of the process at , normalized with the occupation time:

| (2.16) |

This equation is proved in the proof of Lemma 3 in Section 4.2. In the ergodic case, the fraction in (2.16) vanishes as (see Lemma 2 in Section 4.2).

A complete statistical analysis of the estimators from continuous time observations is proposed in (Lejay and Pigato, 2020, Propositions 3-7, 10-12), more precisely the estimators behavior is studied even if the process is not ergodic. The results of the present document imply the same results for the dMLE in high frequency and infinite horizon. In this paper we deal only with the ergodic case in Theorem 2). The proof, for non ergodic cases, is the same as the one provided in Section 4.4 since Lemmas 9-10 also hold for non-ergodic cases. In the null recurrent case with non-vanishing drift, one needs to impose that .

When the process is not ergodic, GME is not necessarily equivalent to the dMLE. For instance, in long time, in the transient case, the fraction in (2.16) does not vanish on the side where the process stays indefinitely, and it actually is the term providing the convergence of the estimators to the drift parameter. This is reminiscent of the drift MLE in a simple drifted Brownian motion (in finance, the Black-Scholes model), which does not depend on the intermediate observations, but only on the process value at and therefore, does not depend on the frequency of the observations. Note that if the drift is not , the Black-Scholes model is transient, while the model in (1.1) can be transient or recurrent/ergodic depending on the drift parameters. The normalized final value of the process at time is also the leading term for the model (1.1), when at least one of the drift parameters is such that the process is not mean reverting, which includes some null-recurrent cases.

Drift estimation in high frequency and infinite horizon.

Condition (2.6) is in line with what has been obtained in the literature so far for non-threshold diffusions, and it is the best condition obtained so far for threshold ones. Up to the authors knowledge, Theorem 2 is the first result for threshold diffusions allowing for deterministic initial conditions (instead of starting at the stationary distrubutions) when looking at high-frequency observations over an infinite time horizon.

Theorem 2 holds also for non-equally spaced high frequency observations. More precisely, the process is observed at times and represents the maximal observation lag: .

Multi-threshold.

The method we are presenting here should also work in a multi-threshold setting, at least in the high frequency and long time setting, where it works analogously to (Mazzonetto and Pigato, 2024, Supplementary material Section S.3). In the GME case, with more than one threshold, the definition of the estimators would involve more complicated, implicit expressions, that one would need to solve using numerical methods, while, if there is only one threshold, explicit expressions are available. Therefore, for the sake of simplicity of the exposition and ease of implementation, we stick here to the case with only one threshold.

3 Numerical studies

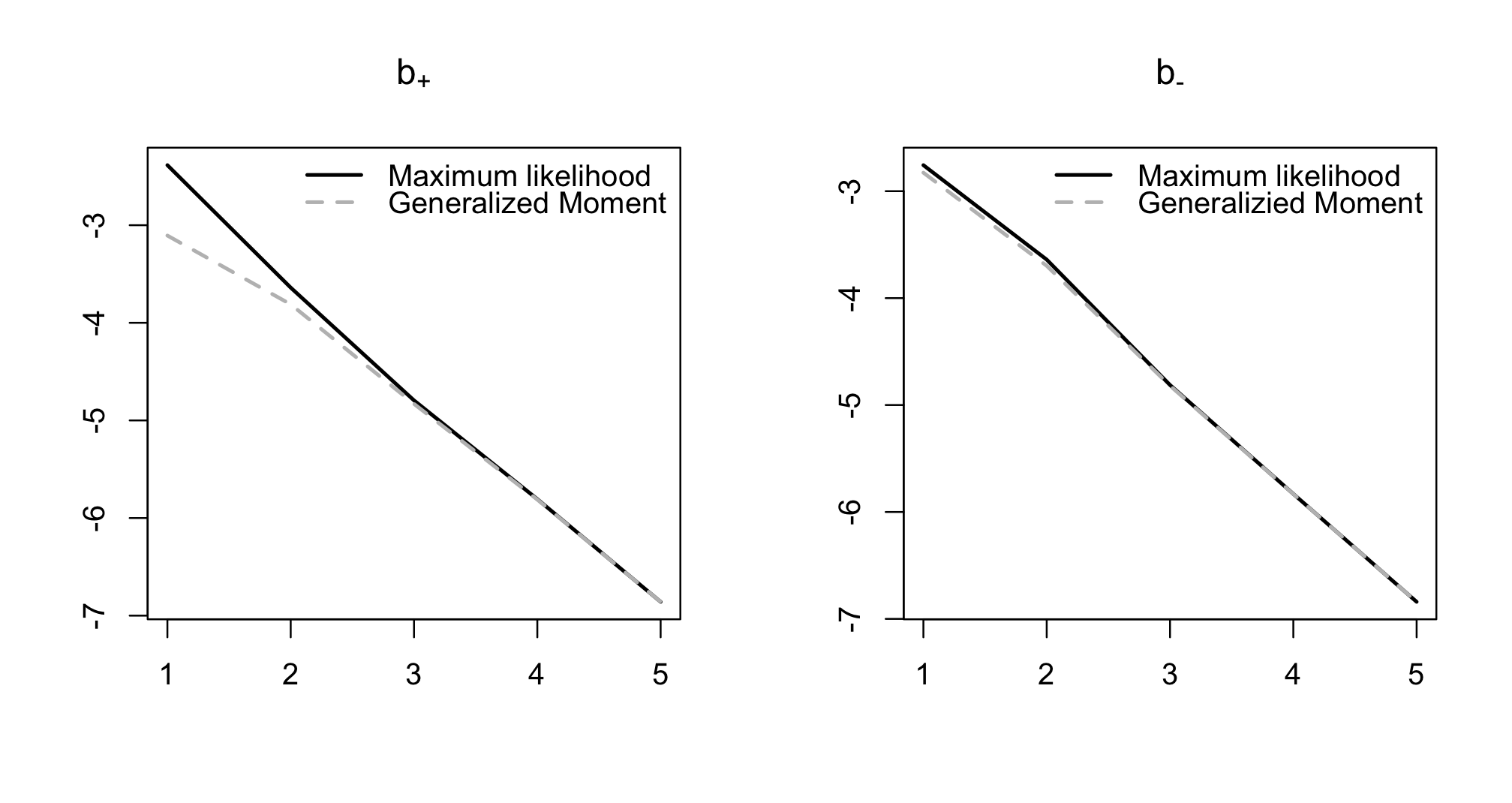

3.1 Comparison of drift estimators

We compare here estimators with , with fixed, as the number of observations goes to infinity, plotting the mean squared error of the estimators (MSE), for a process with parameters as in Table 1, simulated via the Euler-Maruyama scheme.

Clearly, because of Theorems 1 and 2, the asymptotic behavior of the estimators is the same. However, our numerical experiments suggest that the GME slightly outperforms the dMLE, not by a significant margin, but consistently over different sets of parameters and time horizons (see Figure 1). This can be explained by the discussion in Section 2.4, since we are in the ergodic setting.

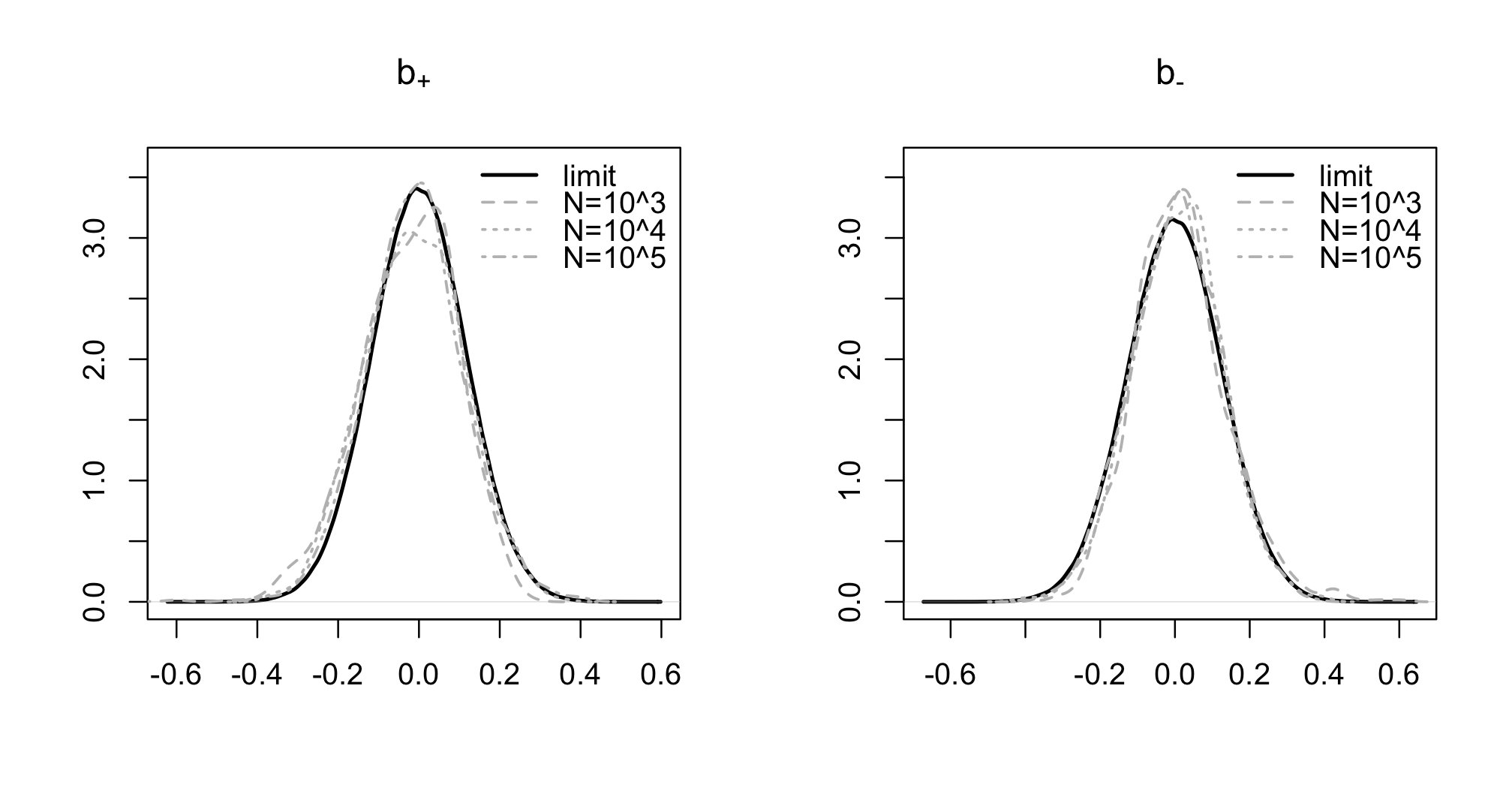

3.2 The asymptotic normality constant in the drift estimator

We look now at the CLT in Theorem 1 - ii). The limit covariance matrix is given in (4.26), for which we do not have an analytical expression. However, it can be evaluated numerically, on synthetic data, simulating several realizations of the process and then computing the empirical covariance. We do so, and plot in Figure 2 the empirical distribution of the error, rescaled with , for various lengths of the observed time series, generated with parameters as in Table 1 via the Euler-Maruyama scheme. A similar numerical representation for Theorem 2 can be found in Lejay and Pigato (2020), where the continuous time equivalent of Theorem 2 is stated and checked numerically.

In view of the independence of the limit Gaussians in Theorem 2, an interesting question is whether the limit cross covariance vanishes or not also in Theorem 1. In our simulations, we can never reject the null hypothesis of limit cross covariance. However, this numerical evidence is not conclusive since the limit cross covariance could be small but non-zero, and still be consistent with our simulations.

These simulations provide a numerical validation of Theorem 1. However, this approach generally cannot be used to estimate the error when dealing with parameters inference from empirical data, since in this case estimation can only be based on one observed time series and several realizations are not available. Estimating the limit covariance can be necessary, for example in order to perform a test on the estimated parameters. In this case, one way to estimate the limit covariance is to split the time series in several batches and use them as separate realizations, as explained in (Brooks et al., 2011, Section 1.10.1). Alternative methods are presented e.g. in (Brooks et al., 2011, Section 1.10.2 and 1.10.3), see also (Brooks et al., 2011, Section 1.12.9) for subsampling techniques.

4 Technical material and proofs

We collect in this section all the mathematical proofs. In Section 4.1 we give some preliminary technical results related to the law of the process via its infinitesimal generator. In Section 4.2 we prove the asymptotic equivalence of the GME and dMLE and Theorem 3. In Section 4.3, we provide the proofs related to the GME, with fixed time lag and long time horizon. Finally, in Section 4.4 the proofs related to the dMLE, in high frequency and with long time horizon.

4.1 Technical tools: scale function, speed measure, fundamental system and resolvent kernel

The infinitesimal generator of the process solution to (1.1) can be written as

cf. e.g. (Itô and McKean, 1996) for a general discussion and (Lejay and Pigato, 2020) for the diffusion in (1.1). The process is a diffusion (roughly-speaking, a strong Markov process with continuous sample paths) which is fully characterized by its speed measure with density and scale function given by

| (4.1) |

When the process is positive or null recurrent, the speed measure is a stationary measure (invariant measure for the transition semigroup). When , we say that the process is ergodic and its invariant distribution is the re-normalized speed measure, denoted by , with density given by

| (4.2) |

Here . (Note that there is a typo in (Lejay and Pigato, 2020).) Throughout the paper, we write for a r.v. independent of following the stationary distribution, i.e., with density (4.2). Let us consider equation

| (4.3) |

For fixed , the set of solutions to (4.3) is a two-dimensional vector space. There exist two continuous, positive functions solution to (4.3), with increasing from to and decreasing from to , such that , called the minimal functions. Such functions can be taken as a basis for the space of solutions to (4.3). With coefficients as in (1), the minimal functions are explicit and given as

| (4.4) | ||||

| (4.5) |

with

Using the minimal functions, one can define the Wronskian of the diffusion as

where is the scale function in (4.1). Note that

| (4.6) |

Let us define the resolvent kernel of (1.1) as the Laplace transform of the transition density

| (4.7) |

It can be computed using the speed measure (4.1), the minimal functions (4.4), (4.5) and the Wronskian, as

| (4.8) |

We can use it as follows to compute Laplace transforms of expectations of functions of starting from a point , if we can exchange the order of time integral and expectation, since

| (4.9) |

4.2 The relation between different estimators

Lemma 2.

Let be solution to (1.1). Then

| (4.10) |

Proof.

Step 1: We first prove that the statement holds with initial condition . We show that

| (4.11) |

which implies the statement. We use that and write

with in (4.7). Using (4.8), we compute

We have

and, usign also (4.6), as ,

So, using the final value theorem (Tauberian theorem), we see that as

which is from (4.2). With a similar computation we prove an analogous result for , and therefore as we obtain and , where the limits can be directly computed and are finite. Markov’s inequality completes the proof of this first step.

Step 2: The statement for implies the statement for any , say . Let us denote the process with such initial condition by . Let be the stopping time identifying the first time for which . Note that is a.s. finite since is recurrent. The process is a weak solution to (1.1) with . Hence, by the strong Markov property, we deduce that converges to a constant as goes to infinity. To prove the statement it suffices to show that is bounded by a constant. From (1.1), follows that . Then, Hölder’s inequality and Itô isometry yield for all

and because the process is positive recurrent. The proof is thus completed. ∎

Lemma 3.

Proof.

Itô-Tanaka formula establishes that the following equalities hold -a.s.:

| (4.12) |

Moreover, it is not difficult to see, similarly to (Mazzonetto and Pigato, 2024, (S2.6) in supplementary material), that for any , we have -a.s.

| (4.13) |

Hence, -a.s.

For fixed, when , we have , because of (4.16). For and such that and (2.6), we have when , because of the ergodic theorem and Lemma 9. Lemma 2 implies that when . The first two statements follow.

Now, when fixed, , we have when and the last statement follows. ∎

4.2.1 Proof of Theorem 3

The result states that, for fixed time horizon, in high frequency, the drift dMLE from discrete observations converges in probability towards the drift MLE from continuous observations (4.29) and provides the convergence rates. It also states that the generalized moment estimator (2.4), converges for fixed time and in high frequency to its continuous-time analog

In Lemma 3 it is shown that, for fixed time and in high frequency,

and, from (4.12)-(4.13) in the proof of Lemma 3, it holds -a.s. that

The speed of convergence of the occupation time is at least (see Lejay and Pigato (2018)) which is larger than . Hence, -a.s.

We are thus reduced to prove the result for . Then, (4.12) and (4.13) ensure that -a.s.:

Recall . The consistency, i.e. when , was already provided in (Lejay and Pigato, 2020, Lemma 1), and the convergence rate is based on the one of the local time approximation (Mazzonetto, 2019, Proposition 2). The proof is thus completed.

4.3 Proofs of asymptotic behaviors in low frequency and long time: GME in Theorem 1 and Theorem 4 and local time in Lemma 1

Let us define the 2-dimensional discrete time process . In the ergodic case, we set , a r.v. that follows its stationary distribution, where is a r.v. following the stationary distribution of (4.2) and is its evolution over a time following equation (1.1).

We also define a solution to (1.1) with and .

Lemma 4.

Let fixed, .

-

I

The discrete time process is ergodic, with invariant measure in (4.2). For any measurable function s.t. ,

-

II

Moreover, if for some we have that

where setting we have

(4.14) -

III

The process is ergodic and, for any measurable function s.t. ,

-

IV

Moreover, if for some , we have that

where setting we have

(4.15)

Remark 1.

Proof.

The proof of I and III is completely analogous to (Hu and Xi, 2022, Theorem 2), the main tool being an application of the ergodic theorem in (Meyn and Tweedie, 2009, Theorem 17.0.1). Let us now discuss IV. Again we start from (Meyn and Tweedie, 2009, Theorem 17.0.1), which only applies to uni-dimensional . The fact that this holds for a multidimensional follows using the Cramer-Wald theorem as described in (Brooks et al., 2011, Section 1.8). Clearly it is enough to prove it for . Let be a Gaussian r.v. in with covariance

For we have, from the univariate version as in (Meyn and Tweedie, 2009, Theorem 17.0.1), after some computations, that in law

because is a centered Gaussian with variance given by

Therefore Cramer Wald theorem implies (4.15) in the multivariate sense. The proof of II is analogous, with the addition of the fact that

The proof is thus completed. ∎

We prove that the convergence results in Theorem 1 hold for . The fact that they hold for as well follows from Lemma 3. Let us recall the expressions of and in (2.15).

Lemma 5.

Proof.

We are going to prove Lemma 1. We first need an auxiliary result. Let us write

| (4.20) |

We have the following lemma.

Lemma 6.

The Laplace transform is

and the Laplace transform is

Proof.

We apply (4.9), with . It is possible to exchange the order of integration because . Using (4.8) we get, for

| (4.21) |

The last integral, using (4.2) and (4.5), can be evaluated as

so that

For the computation is analogous. If we now apply (4.9), with , which again is positive, using (4.8) we get, for

| (4.22) |

The last integral, using (4.2) and (4.5), can be evaluated as

so that

For the computation is analogous. ∎

4.3.1 Proof of Lemma 1

Let us start with . Writing , from (2.1) we have Lemma 4-III implies that

so that, using the tower property of conditional expectation, we get

with in (4.20). The proof strategy consists in computing this quantity via Laplace transform. The Laplace transform is computed in Lemma 6. Using the stationary distribution (4.2), explicit computations give

By Tonelli’s theorem, it holds that

Therefore, inverting the Laplace transform, we obtain

| (4.23) |

which proves (2.12).

Let us now consider . One can rewrite as

so that Lemma 4-III implies that as , converges -a.s. to

Using Lemma 6 and the stationary distribution (4.2), explicit computations give

where with we denote a function s.t. as . Therefore, inverting the Laplace transform, using linearity and a Tauberian theorem for we obtain

| (4.24) |

as , where denotes the -function. This implies (2.14).

4.3.2 Proof of Theorem 1 and Theorem 4

Lemma 7.

It holds

where

| (4.26) |

with

| (4.27) |

Proof.

Proof of Theorem 1.

Proof of Theorem 4.

Consistency follows from (4.16), (4.19) and (2.12). To prove asymptotic normality of the positive side we write

where with we mean a quantity that goes to in probability as , that may vary from line to line. A similar computation also holds for the negative side, so that we can write

with

It can be verified from (4.25) and (2.15) that . Using Lemma 4-IV allows to conclude, analogously to the proof of Lemma 7, this time with asymptotic covariance

| (4.28) |

so that the theorem is proved. ∎

4.4 Proof of Theorem 2: maximum likelihood estimator, high frequency and long time horizon

In Lejay and Pigato (2020) it was proved that the MLE from continuous time observation on the time interval , is given by

| (4.29) |

Note that it coincides with the estimator obtained my maximizing the quasi-likelihood function, which is defined as the likelihood, but with diffusion coefficient set to . The discrete version of the estimator has been provided as well and is (2.5) as the quantity maximizing the discretized likelihood:

We now state the results about the asymptotic behavior in long time of the estimators based on continuous observations.

Lemma 8 (cf. Proposition 3 in Lejay and Pigato (2020)).

Assume the process is ergodic. Let . The MLE (4.29)

-

i)

is consistent: and

-

ii)

satisfies the following CLT: where are two mutually independent, independent of , Gaussian random variables with variance respectively .

The proof of Theorem 2 exploits the latter lemma and the key Lemma 9 which is based on a bound for the transition density proposed in Lemma 10. More precisely for all it holds

We then handle the second term of the sum with Lemma 8. Equations (4.29) and (2.5) imply for that

| (4.30) |

The latter converges in probability to 0 by Lemma 9 and the fact that converges in probability (ergodicity) and converges in law (ergodicity and martingale CLT in Crimaldi and Pratelli (2005)). Lemma 9 is similar to Lemma 4 in Mazzonetto and Pigato (2024). Nevertheless, here we allow a deterministic initial condition using the density bound in Lemma 10.

Lemma 9.

Proof of Lemma 9.

In this proof we use the round ground notation if , where . Moreover, without loss of generality, we assume for all .

Let us first note for every that

Hence

| (4.31) |

Analogously, triangular inequality, Hölder’s inequality, and Itô-isometry imply that

| (4.32) |

Hence, the proof of Lemma 9, which consists in showing that (4.31) and (4.32) are , reduces to prove

| (4.33) |

Step 1: Let be fixed such that . We show that there exist a constant depending only on such that for large enough

| (4.34) |

In order to prove this, let us fix . Note that is bounded by where is the first hitting time of the level 0 of the process solution to the Brownian motion with drift

with a Brownian motion independent of . Then

Let . We apply Lemma 10 and obtain for some non-negative constant :

This completes the proof of the first step.

Step 2: Proof of (4.33).

Let denote the transition density of the drifted oscillating Brownian motion (1.1) with diffusion coefficient in (1). To bound the density, we take inspiration from the article Downes (2009).

Note that the transition density of the oscillating Brownian motion without drift, , is known. It was provided in Keilson and Wellner (1978), and it satisfies for instance that for some constant depending on the parameters.

Lemma 10.

There exist depending on the parameters such that for all , it holds that

Moreover,

Proof of Lemma 10.

Note that, if is a drifted oscillating Brownian motion (1.1) with diffusion coefficient in (1) and drift , then is a skew Brownian motion (SBM) with drift and skewness parameter . This follows from Itô-Tanaka formula, for a proof see e.g. Mazzonetto (2019). Moreover, if denotes the transition density of the -SBM with drift , then

In this proof we only consider a skew-BM with piecewise constant drift (abuse of notation because is actually ) and skewness parameter such that . By Girsanov’s theorem there exists a measure absolutely continuous with respect to such that under is a driftless -SBM with and for all measurable and bounded it holds that

Since , Itô-Tanaka formula applied to the function and the driftless -SBM implies that -a.s.

where . Therefore,

Then

To complete the proof we need to show that

| (4.35) |

Let us first aussume (4.35). Then, for every measurable and bounded

and we complete the proof as in (Downes, 2009, Corollary 5): to consider the transition density we take derivative of the partition function of . More precisely, we consider for , divide for and take the limit on both sides as . Thus,

and the transition density of a -SBM, is known (see Walsh (1978)):

| (4.36) |

which is bounded from above by .

To conclude, we now prove (4.35). In what follows let .

Let be the joint transition density of the skew BM , , and its local time: (see (Étoré and Martinez, 2013, Proposition 1) or Appuhamillage et al. (2011)):

Recall that

where is given by (4.36). It holds for all that

Note that

with and . Therefore

This completes the proof. ∎

Acknowledgements.

We are grateful to A. Lejay and R. Peyre for discussions. PP acknowledges financial support from University of Rome Tor Vergata via Project AIF - E83C22002610005.

References

- Amorino and Gloter [2020] C. Amorino and A. Gloter. Contrast function estimation for the drift parameter of ergodic jump diffusion process. Scandinavian Journal of Statistics, 47(2):279–346, 2020.

- Ang and Timmermann [2012] A. Ang and A. Timmermann. Regime Changes and Financial Markets. Annual Review of Financial Economics, 4:313–337, 2012.

- Appuhamillage et al. [2011] T. Appuhamillage, V. Bokil, E. Thomann, E. Waymire, and B. Wood. Occupation and local times for skew Brownian motion with applications to dispersion across an interface. Ann. Appl. Probab., 21(1):183–214, 2011.

- Bass and Chen [2005] R. F. Bass and Z.-Q. Chen. One-dimensional stochastic differential equations with singular and degenerate coefficients. Sankhyā: The Indian Journal of Statistics, pages 19–45, 2005.

- Ben Alaya and Kebaier [2013] M. Ben Alaya and A. Kebaier. Asymptotic Behavior of the Maximum Likelihood Estimator for Ergodic and Nonergodic Square-Root Diffusions. Stochastic Analysis and Applications, 31(4):552–573, 2013.

- Borodin [1986] A. N. Borodin. On the character of convergence to brownian local time. ii. Probability Theory and Related Fields, 72:251–277, 1986.

- Borodin and Salminen [2015] A. N. Borodin and P. Salminen. Handbook of Brownian motion-facts and formulae. Springer Science & Business Media, 2015.

- Brooks et al. [2011] S. Brooks, A. Gelman, G. Jones, and X.-L. Meng. Handbook of Markov Chain Monte Carlo. CRC press, 2011.

- Buckner et al. [2024] D. Buckner, K. Dowd, and H. Hulley. Arbitrage Problems with Reflected Geometric Brownian Motion. Finance Stoch, 28, Jan. 2024.

- Chen et al. [2011] C. W. S. Chen, M. K. P. So, and F.-C. Liu. A review of threshold time series models in finance. Statistics and its Interface, 4(2):167–181, 2011.

- Christensen and Strauch [2023] S. Christensen and C. Strauch. Nonparametric learning for impulse control problems – Exploration vs. exploitation. The Annals of Applied Probability, 33(2):1569 – 1587, 2023.

- Christensen et al. [2023] S. Christensen, C. Strauch, and L. Trottner. Learning to reflect: A unifying approach for data-driven stochastic control strategies. Bernoulli, 2023.

- Crimaldi and Pratelli [2005] I. Crimaldi and L. Pratelli. Convergence results for multivariate martingales. Stochastic Process. Appl., 115(4):571–577, 2005.

- Decamps et al. [2006] M. Decamps, M. Goovaerts, and W. Schoutens. Self exciting threshold interest rates models. Int. J. Theor. Appl. Finance, 9(7):1093–1122, 2006.

- Dieker and Gao [2013] A. B. Dieker and X. Gao. Positive recurrence of piecewise Ornstein-Uhlenbeck processes and common quadratic Lyapunov functions. Ann. Appl. Probab., 23(4):1291–1317, 08 2013.

- Dong and Wong [2017] F. Dong and H. Y. Wong. Variance Swaps under the Threshold Ornstein-Uhlenbeck Model. Appl. Stoch. Model. Bus. Ind., 33(5):507–521, Sept. 2017.

- Downes [2009] A. N. Downes. Bounds for the transition density of time-homogeneous diffusion processes. Statistics & probability letters, 79(6):835–841, 2009.

- Étoré and Martinez [2013] P. Étoré and M. Martinez. Exact simulation of one-dimensional stochastic differential equations involving the local time at zero of the unknown process. Monte Carlo Methods Appl., 19(1):41–71, 2013.

- Florens-Zmirou [1993] D. Florens-Zmirou. On estimating the diffusion coefficient from discrete observations. J. Appl. Probab., 30(4):790–804, 1993.

- Gairat and Shcherbakov [2016] A. Gairat and V. Shcherbakov. Density of skew Brownian motion and its functionals with application in finance. Mathematical Finance, 26(4):1069–1088, 2016.

- Giorgi et al. [2023] F. Giorgi, S. Herzel, and P. Pigato. A reinforcement learning algorithm for trading commodities. Applied Stochastic Models in Business and Industry, n/a(n/a), 2023.

- Hottovy and Stechmann [2015] S. Hottovy and S. N. Stechmann. Threshold models for rainfall and convection: Deterministic versus stochastic triggers. SIAM Journal on Applied Mathematics, 75(2):861–884, 2015.

- Hu and Xi [2022] Y. Hu and Y. Xi. Parameter estimation for threshold ornstein–uhlenbeck processes from discrete observations. Journal of Computational and Applied Mathematics, 411:114264, 2022.

- Itô and McKean [1996] K. Itô and H. McKean. Diffusion Processes and their Sample Paths: Reprint of the 1974 Edition. Classics in Mathematics. Springer Berlin Heidelberg, 1996.

- Jacod [1998] J. Jacod. Rates of convergence to the local time of a diffusion. Ann. Inst. H. Poincaré Probab. Statist., 34(4):505–544, 1998.

- Jacod and Protter [2012] J. Jacod and P. Protter. Discretization of processes, volume 67 of Stochastic Modelling and Applied Probability. Springer, Heidelberg, 2012.

- Jacod and Shiryaev [2003] J. Jacod and A. N. Shiryaev. Limit theorems for stochastic processes, volume 288 of Grundlehren der Mathematischen Wissenschaften. Springer-Verlag, Berlin, second edition, 2003.

- Keilson and Wellner [1978] J. Keilson and J. A. Wellner. Oscillating Brownian motion. J. Appl. Probability, 15(2):300–310, 1978.

- Kessler [1997] M. Kessler. Estimation of an Ergodic Diffusion from Discrete Observations. Scandinavian Journal of Statistics, 24(2):211–229, 1997.

- Kutoyants [2012] Y. A. Kutoyants. On identification of the threshold diffusion processes. Ann. Inst. Statist. Math., 64(2):383–413, 2012.

- Le Gall [1985] J.-F. Le Gall. One-dimensional stochastic differential equations involving the local times of the unknown process. Stochastic Analysis. Lecture Notes Math., 1095:51–82, 1985.

- Lejay and Pigato [2018] A. Lejay and P. Pigato. Statistical estimation of the Oscillating Brownian Motion. Bernoulli, 24(4B):3568–3602, 2018.

- Lejay and Pigato [2019] A. Lejay and P. Pigato. A threshold model for local volatility: evidence of leverage and mean reversion effects on historical data. International Journal of Theoretical and Applied Finance, 22(4):1950017, 2019.

- Lejay and Pigato [2020] A. Lejay and P. Pigato. Maximum likelihood drift estimation for a threshold diffusion. Scandinavian Journal of Statistics, 47(3):609–637, 2020.

- Lejay et al. [2019] A. Lejay, E. Mordecki, and S. Torres. Two consistent estimators for the skew Brownian motion. ESAIM Probab. Stat., 23:567–583, 2019.

- Lipton [2018] A. Lipton. Oscillating Bachelier and Black-Scholes Formulas. In Financial Engineering. World Scientific, 2018.

- Lipton and Sepp [2011-10] A. Lipton and A. Sepp. Filling the gaps. Risk Magazine, pages 66–71, 2011-10.

- Mazzonetto [2019] S. Mazzonetto. Rates of convergence to the local time of oscillating and skew brownian motions. arXiv preprint arXiv:1912.04858, 2019.

- Mazzonetto and Pigato [2024] S. Mazzonetto and P. Pigato. Drift estimation of the threshold ornstein-uhlenbeck process from continuous and discrete observations. Statistica Sinica, 34:313–336, 2024.

- Meyn and Tweedie [2009] S. Meyn and R. L. Tweedie. Markov Chains and Stochastic Stability. Cambridge University Press, USA, 2nd edition, 2009. ISBN 0521731828.

- Mota and Esquível [2014] P. P. Mota and M. L. Esquível. On a continuous time stock price model with regime switching, delay, and threshold. Quant. Finance, 14(8):1479–1488, 2014.

- Pai and Pedersen [1999] J. Pai and H. Pedersen. Threshold Models of the Term Structure of Interest Rate. In Joint day Proceedings Volume of the XXXth International ASTIN Colloquium/9th International AFIR Colloquium, Tokyo, Japan, pages 387–400. 1999.

- Pigato [2019] P. Pigato. Extreme at-the-money skew in a local volatility model. Finance and Stochastics, 23:827–859, 2019.

- Portenko [1994] N. I. Portenko. The development of I. I. Gikhman’s idea concerning the methods for investigating local behavior of diffusion processes and their weakly convergent sequences. Teor. Ĭmovīr. Mat. Stat., (50):6–21, 1994.

- Rényi [1963] A. Rényi. On stable sequences of events. Sankhyā Ser. A, 25:293–302, 1963.

- Su and Chan [2015] F. Su and K.-S. Chan. Quasi-likelihood estimation of a threshold diffusion process. J. Econometrics, 189(2):473–484, 2015.

- Su and Chan [2017] F. Su and K.-S. Chan. Testing for threshold diffusion. J. Bus. Econom. Statist., 35(2):218–227, 2017.

- Tong [2011] H. Tong. Threshold models in time series analysis — 30 years on. Statistics and its Interface, 4, 2011.

- Walsh [1978] J. B. Walsh. A diffusion with discontinuous local time. In Temps locaux, volume 52-53, pages 37–45. Société Mathématique de France, 1978.

- Yu et al. [2020] T.-H. Yu, H. Tsai, and H. Rachinger. Approximate maximum likelihood estimation of a threshold diffusion process. Computational Statistics & Data Analysis, 142:106823, 2020.