Non-robustness of diffusion estimates on networks with measurement error

Abstract.

Network diffusion models are used to study things like disease transmission, information spread, and technology adoption. However, small amounts of mismeasurement are extremely likely in the networks constructed to operationalize these models. We show that estimates of diffusions are highly non-robust to this measurement error. First, we show that even when measurement error is vanishingly small, such that the share of missed links is close to zero, forecasts about the extent of diffusion will greatly underestimate the truth. Second, a small mismeasurement in the identity of the initial seed generates a large shift in the locations of the expected diffusion path. We show that both of these results still hold when the vanishing measurement error is only local in nature. Such non-robustness in forecasting exists even under conditions where the basic reproductive number is consistently estimable. Possible solutions, such as estimating the measurement error or implementing widespread detection efforts, still face difficulties because the number of missed links is so small. Finally, we conduct Monte Carlo simulations on simulated networks, and real networks from three settings: travel data from the COVID-19 pandemic in the western US, a mobile phone marketing campaign in rural India, and an insurance experiment in China.

Researchers and policymakers studying the spread of ideas, technology, or disease often estimate models of diffusion using network data of how individuals interact. Examples include (i) quantifying the estimated extent of illness or technology take-up; (ii) summarizing diffusion dynamics (e.g., the reproduction number of a disease); (iii) targeting interventions (e.g., where to seed new information to maximize spread, where to lockdown to prevent spread); (iv) and estimating counterfactuals (such as in estimates of peer effects, as we show in an empirical example). See Anderson and May, (1991), Jackson, (2009), Jackson and Yariv, (2011), and Sadler, (2023) and references within for all three classes of topics (as well as an account of how such models are used in the case of strategic behavior).

In this paper, we focus on a setting where the econometrician has imperfect measurement of either the interaction network or initial seeding, and wants to estimate models of diffusion or generate forecasts. Importantly, we let this measurement error be very small. In the case of a mismeasured network, only a vanishing proportion of links are missed asymptotically and nearly all links are observed. This captures the setting where an econometrician is equipped with the richest possible data on individuals and interactions, including geographic information such as residential data, schools and community centers, local markets, and local commuting information, and even mobile cell phone data tracking foot traffic.

We show that this tiny mismeasurement significantly affects the predictions of the econometrician’s estimated diffusion model. We show four key results: (i) predictions of diffusion counts can be arbitrarily incorrect with even vanishingly small measurement error of the network, (ii) predictions of diffusion counts can be arbitrarily sensitive to local uncertainty of the initial seeding; (iii) while aggregated estimated quantities such as the basic reproductive number can be estimated correctly despite measurement error, it provides limited information for more disaggregated targets; (iv) because the measurement error is so small, most data augmentation (either estimating the measurement error or conducting additional data collection) will be ineffectual. In other words, if the measurement error is a needle in a haystack, it will be particularly costly and challenging to find the needle.

The key insight in our theoretical results is that settings with diffusion – where a process spreads as a function of contact with receptive individuals or units – are extremely susceptible to measurement error because missed links create opportunities for the process to propagate out of the econometrician’s view. This missed propagation creates knock-on effects that eventually overwhelm the econometricians’ estimated predictions.

To give intuition, consider a network where connections occur with a higher probability for people with some observable commonality (e.g., geography, school, work) or latent factors (e.g., Hoff et al., (2002)). This is common in many network formation models where dissimilarity between units decreases the probability of linkage. With a perfectly measured graph, when a diffusion process of information or disease is seeded, we can draw a ball around the initial seed that will exhaustively enumerate the number of nodes possibly affected by the process. This ball will expand over time, with the ball’s radius defined by the distance from the initial seed, and heavily influenced by the commonalities that affect peoples’ linking probability.

Now, consider a small set of idiosyncratic links that are missed in this network. If any of these missed links reach further than the ball drawn around the seed, the diffusion process can escape past the econometricians’ determined set of possibly impacted nodes. This set itself is small, but will have significant knock-on effects as the process quickly spreads outside of the ball. Since the link is outside of the ball, it spreads even more quickly because it has the largest possible set of unexposed units to diffuse to. This jump need not be far – it simply needs to be a link that creates diffusion unexpected by the econometrician.111Like all work in this space, we are indebted to Watts and Strogatz, (1998), the seminal paper on small worlds, demonstrating that small probabilities of rewiring links in lattice-like graphs can yield drastic reductions in path length and time to saturation of a simple diffusion process. Our analysis is related but distinct. First and foremost, we do not require that the missed links could go anywhere in the network. Distinctly, our most general results allow for nodes to have mismeasurement to potentially only a vanishing share of nodes in the graph. In our environment, the key condition of polynomial expansion is a joint property of the graph and diffusion process and not a property of the graph alone. This distinct assumption allows for analytic analysis of the diffusion processes, while also allowing for a much wider array of graph structures (including expansive networks). Further, much of the work on small world graphs and diffusion focuses on phase transitions of the diffusion process (e.g., Newman and Watts, (1999)), but we compare shifts within the same (critical) phase. And, of course, our focus is on forecasts of the extent and location of the diffusion, sensitivities to perturbation of the initial seed, and possible solutions to the identified problems. While we begin with the case of missing idiosyncratic links for simplicity, our general results allow each node to have potential mismeasurement to a vanishing share of nodes with an arbitrary distribution, and yet all aforementioned problems persist. This nests cases such as nodes only having missed links to a local neighborhood comprising a vanishing share of nodes; e.g., the measurement error is only allowed to be to a neighboring town and nothing more.

Missing links in the measurement of networks is a common concern (Wang et al.,, 2012; Sojourner,, 2013; Chandrasekhar and Lewis,, 2010; Advani and Malde,, 2018), but our paper highlights the dramatic impact of even the smallest errors when attempting to forecast diffusion. Mismeasurement can happen for several reasons. The first is practical: many analyses using empirical data (including one of our own empirical examples) do some amount of aggregation into groups with measured amounts of interaction. For example, individuals may be binned into groups of location-by-age-by-income, and the interactions between these groups are approximated based on underlying micro data. Using this data on individuals and interactions to construct compartments and forecast diffusion processes implicitly assumes that connections occur with a much higher probability for people with some observable commonality within the bin (Acemoglu et al.,, 2021; Farboodi et al.,, 2021; Fajgelbaum et al.,, 2021). Then, it may mismeasure cross-compartment connections. The choice of compartments may occur in order to smooth information and to have manageable “average” interaction patterns, but the connections across compartments will not capture the full heterogeneity of interactions.

Second, the mismeasurement of the network may occur because the sampling process for the network is imperfect. Studies surveying individuals may focus on local connections (e.g. within a school or village), and ignore other connections. Or, it may be that the network of potential meetings and connections is different from what is observed by many data sources. For example, cell phone data may provide a granular picture and yet omit a number of interactions that will play a crucial role in the diffusion process. Third, there is an intrinsic mismeasurement even with rich, static network data. Because the diffusion process evolves over time, a static snapshot of the network may not capture the relevant links for diffusion by the time the process reaches an individual.

In our theoretical analysis, we consider diffusion at its most disaggregated level, where the researcher estimates the interaction process at the unit level. We show that arbitrarily poor estimates can occur if the underlying interaction data carries even very small imperfections due to issues in the data sampling process. The lack of success in this setting is a conservative result that suggests compartmental models (which we consider in our empirical examples) will do just as badly. Compartmental models introduce a much larger volume of error, by smoothing over individual behavior to form compartments.

Formally, we study an asymptotic model in which parameters depend on the number of agents to tractably approximate finite-sample/time behavior, as is customary in graph theory. We consider a triangular array environment where there is a discrete set of agents who are in an undirected, unweighted network . We take . A SIR (susceptible-infected-recovered) diffusion process proceeds for periods. Each period, a newly infected node passes the disease i.i.d. with probability and is then removed from the process. Since the model applies to diseases, technology adoption, social learning, and other diffusion settings, we use the term activated to nest the application-specific terms such as “infected,” “informed,” or “adopted” (Jackson and Yariv,, 2007).

We consider a time regime where it is neither early nor late. Extremely early on, there is almost no information and nothing has happened. Similarly, if we look far into the future, then the diffusion process saturates the network. Both cases make the problem uninteresting. So we work with the intermediate time regime, which is when estimators are developed, forecasts are made, and policy is designed. Formally, to approximate finite time behavior, we impose that is an increasing function of . In addition to being tractable, it also embeds several intuitive assumptions. First, we impose upper bounds on , in terms of functions of , to ensure that the diffusion does not progress “too far.” This rules out cases where the diffusion covers (approximately) the entire graph, as the process is able to reach the edge of the graph. Second, we impose lower bounds on , again in terms of functions of to rule out the initial periods where all diffusion is extremely local to the initial seed and measurement error will not play a role (unless the measurement error is extreme). The resulting asymptotic framework applies to any that falls within the given bounds, which are determined from the structure of the model.

We define the true network over which the diffusion process spreads as . The subgraph is fully observed by the econometrician and is deterministic, while is an unobserved stochastic error graph222We focus on the case of missing links, as we believe this issue will be the primary one in practice (see Griffith, (2022) for several empirical examples). In the case where the econometrician both misses some links and incorrectly assumes others exist, the problem becomes much more complex. Globally, the net rate of missing or added links seems to be the key factor; locally, it seems that forecasts could either over or underestimate the volume of diffusion.. This setup corresponds to an econometrician taking a sample from and observing (without error) . In practice, this could mean, for example, using a graph constructed from cell phone call logs as the true interaction graph. As discussed below, we assume that is very close to a complete sample from – so close that uncovering the additional missing edges in is impossible with realistic data collection strategies. Motivated by the empirical and statistical literature, we assume that the diffusion process on has a predominantly polynomial expansion structure in our main results, which generalizes a local meeting topology (e.g., geography, social groups). This setup nests any finite-dimensional Euclidean model, including but not limited to geographic networks, Euclidean networks, lattices, latent space models on Riemannian manifolds of weakly positive curvature, and so on, but the term geographic provides a useful intuition. Importantly, our assumption of polynomial expansion of the diffusion does not require polynomial expansion of the underlying graph, nor are our results limited to the polynomial case. We consider polynomial expansion because it reflects the common empirical analogs used in the data. We cover the exponential case for completeness, characterizing when measurement error is problematic despite the more rapid expansion. The exponential case covers the entire graph more rapidly, shrinking the set of sequences in which our analysis applies.

The error graph contains idiosyncratic links that, in our baseline model, are drawn i.i.d. with probability amongst all pairs of nodes.333We relax this considerably in our most general results presented in Section 4. We show mismeasurement of any node’s links can be restricted to a vanishing share of nodes. Crucially, we assume that in the limit essentially all of the links in the true network come from . That is, . We assume an even stronger upper bound on the rate so that no giant component can form in : . Therefore the pathologies we identify due to mismeasurement cannot be a function of a large unobserved component of spread.

We assume that the econometrician collects data and observes the network . Since the econometrician has perfect knowledge of , approximating data collection that is near-perfect for , is the only source of measurement error. In much of our analysis, the initial seed is also known exactly to the econometrician.444We also consider switching the role of mismeasurement, wherein the network is perfectly observed but the initial seed is locally permuted, and find similar difficulties. Collectively, these are strong assumptions that work in favor of the econometrician, reflecting a best-case scenario.

We begin by looking at forecasting difficulties in Section 2. Theorem 1 shows that the econometrician’s estimates of the diffusion count will be of lower order of magnitude than the true counts in the intermediate run (after the very initial periods, and before the disease saturates the entire network). In other words, the prediction will be dominated by the error. Very few idiosyncratic links are necessary for this phenomenon. A key conceptual point is that the idiosyncratic links do not shift the polynomial expansion of the diffusion to an exponential – rather, they increase the polynomial degree.

Second, in Theorem 2, we show that diffusion on – even when the error network is completely known – is not stable. This concretely captures the idea that perturbing the initial seed inside a small town when studying the overall spread at the state level can lead to massive differences in who is activated (i.e., infected, informed, or has adopted, based on application) and where they are in the state. Formally, we define a sequence of neighborhoods about , , to be local relative to the diffusion if the size of the neighborhoods vanishes relative to (the set of all possible nodes activated from by time ). We show that over the time horizons of interest, there is some set that can be constructed which is a non-vanishing share of such that seeding with rather than can lead to numerous disparate regions being diffused to and large disagreement in who is activated. This property holds even when the entire is perfectly known to the policymaker.

In Section 3.1, we turn to the problem of estimating the parameters of the diffusion process. The simple point is that one can consistently estimate both the diffusion parameter and the basic reproduction number in a straightforward manner.555Alimohammadi et al., (2023) makes a similar point. They study a SIR model on a network and design an estimation strategy for the parameters and the trajectory of epidemics. They consider a local estimation algorithm based on sampled network data, and show that asymptotically they identify the correct proportions of nodes that will eventually be in the SIR compartments. These results are analogous to our finding that one can estimate and in a straightforward manner. Common intuition would suggest that equipped with these quantities, one could have a feel for where and how virulently the diffusion spreads to disparate regions. Yet we find that forecasts can become arbitrarily inaccurate, and exhibit sensitive dependence on the initial seeding of the diffusion process. While captures the aggregate behavior of the diffusion, extending it to more disaggregated estimands is a challenging task.

We consider two possible solutions in Section 3.2: (i) estimating the idiosyncratic links through supplementary data collection and (ii) widespread node-level sampling (e.g., testing). In our assumed regime neither solution works. First, consider the case where the econometrician estimates and uses this information. We show that when the econometrician samples the population in a reasonable manner to obtain a large sample to estimate the volume of unobserved, idiosyncratic links, they will be unable to consistently estimate . In fact, with large samples of nodes (on the order of ), the probability of observing no idiosyncratic link in a supplemental survey tends to one (so identically). Even with unrealistically large survey samples, close to order itself, the estimators will likely be inconsistent. Despite not being able to measure the error rate, it is large enough to cause severe forecasting problems.

The second possible solution is to look at when the policymaker uses widespread node-level sampling (e.g., testing) to detect what regions in society have activated agents. Specifically, the policymaker thinks of society as comprised of a number of regions — mutually exclusive connected sets of nodes in — and attempts to estimate which regions of society currently have activated agents. We assume that the policymaker detects every activated agent with i.i.d. probability . In an informational setting, this might reflect the quality of a survey elicitation. In the epidemic setting, this will involve the power of the biological test. In both settings, also involves the yield rate for the sample including non-response and non-consent. The natural intuition is that with many draws, since the policy maker attempts to sample all nodes (so the effective power to detect is ), the share of regions with activated agents that are detected as currently having activated agents should be large and at least . In Theorem 3, we show that the opposite holds. Namely, even with very sparse idiosyncratic links, the misemeasurement makes it such that the share of regions that have activated nodes that are actually marked correctly is at most . The intuition is that even when is very low, newly activated regions have so few activated agents that they may not be detected, and pushing this calculation forward shows that this will be the case for many such regions.666This relates to but is distinct from companion work in Chandrasekhar et al., (2021). There we look at the effects of threshold lockdown strategies that are triggered by the discovery of a certain number of diseases in a region related to the topological structure of the network through a well-balanced condition.

Section 4 contains our strongest result. It generalizes the preceding results and makes clear that they do not rely on the assumption that is comprised of idiosyncratic links between any two nodes with some i.i.d. probability. This is a convenient notational device to write rates in a clear way, depending only on restrictions of , the error rate, without introducing a second concept: the allowable set of mismeasurements. In practice, one can even allow for models where varies at the pair level; we study a structure of measurement error where every only has possible links in to a vanishing share of nodes in : for a vanishing share of s. This nests the case in a “geographic” setting where is only allowed to have these missed links “locally” in a ball around . Despite this very general structure on both the shape of mismeasurement and how limited its domain can be, all of the aforementioned results carry through. We note that in the case where the share of nodes that can be linked to diminishes at a sufficiently fast rate, our results no longer apply.

We formalize this in Theorem 4 and Corollary 1. This generalization is particularly important because it makes clear that the forecasting and robustness failures we identify are not a product of missing “long-range shortcuts” that generate “small worlds.” It can be the case that the only kinds of links that are missed are those which were restricted to a small set of other nodes and which are highly localized in geographic-type models. The force that underlies the robustness failure is not about a few very surprising, long-range links, but instead is about the sheer accumulation of “re-seedings” that are missed, irrespective of the configurations of these misses.

Section 5 contains an extension for completeness. We consider the case wherein the econometricians’ dataset exhibits exponential expansion. Clearly, with exponential expansion, the diffusion saturates the network incredibly quickly, rendering the forecasting problem moot. Nonetheless, exponential expansion in could be because the underlying interaction data contains non-local mavens and non-local heavy tails of interactions and this information is known to the econometrician. For example, if the econometrician could perfectly forecast all future super-spreader events, this would be the case. Surprisingly, even in this case, it is possible to mis-forecast the diffusion, albeit under a stronger bound on idiosyncratic links. Theorem 5 shows that forecasts are not accurate when contains a large component—that is, must contain a component that contains a constant fraction of the nodes.

In simulation, we first examine versions of our main theorems. We directly simulate a diffusion process on both simulated and real-world networks with and without measurement error. In our Monte Carlo exercises, we generate different networks that match features such as degree and clustering in known empirical data. We set the measurement error probability to be quite small () and find that forecasts are problematic even with such small measurement error: underestimates of the diffusion count range from 22% to 83% across the simulations. We also demonstrate extreme sensitivity to initial conditions. Our first example shows that even when we perturb the initial seed in a neighborhood comprising 1% of the graph, 31% of the counterfactual seeds in this neighborhood would generate large failures of predictability of who is activated downstream. We find the expected overlap share of activated nodes over perturbations is only 40% by the time the diffusion could potentially have saturated the network. If we perturb in a 5% neighborhood, then 65% of the neighborhood is counterfactually problematic and then by the time of saturation the overlap percent is only 13%.

As an additional exercise, we fit a simple compartmental SIR model—a continuous time, continuum of agents mean-field approximation—to the generated diffusion data. We explore deviations when the (actual) diffusion process, comprised of discrete agents over discrete time, is approximated through the compartmental SIR model. We find that graphs with higher dimensional diffusion processes can be well approximated “in sample” (data used to estimate the model and build forecasts) by the compartmental SIR model, while lower dimension processes cannot. Further, in both cases, the fitted compartmental model forecasts a much earlier acceleration of diffusion relative to the actual diffusion process. Moreover, the compartmental model predicts at times a dramatically lower overall number of activations.

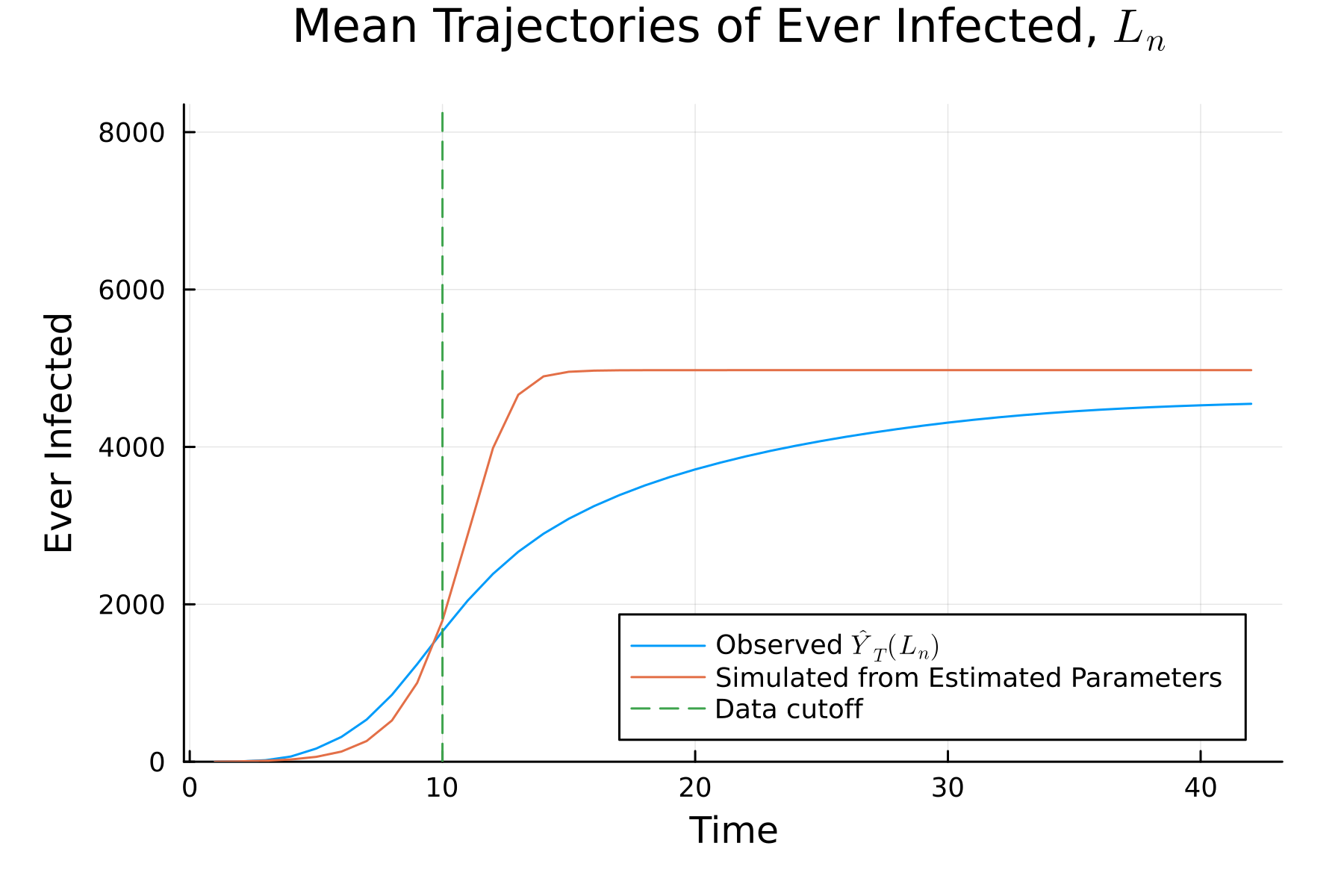

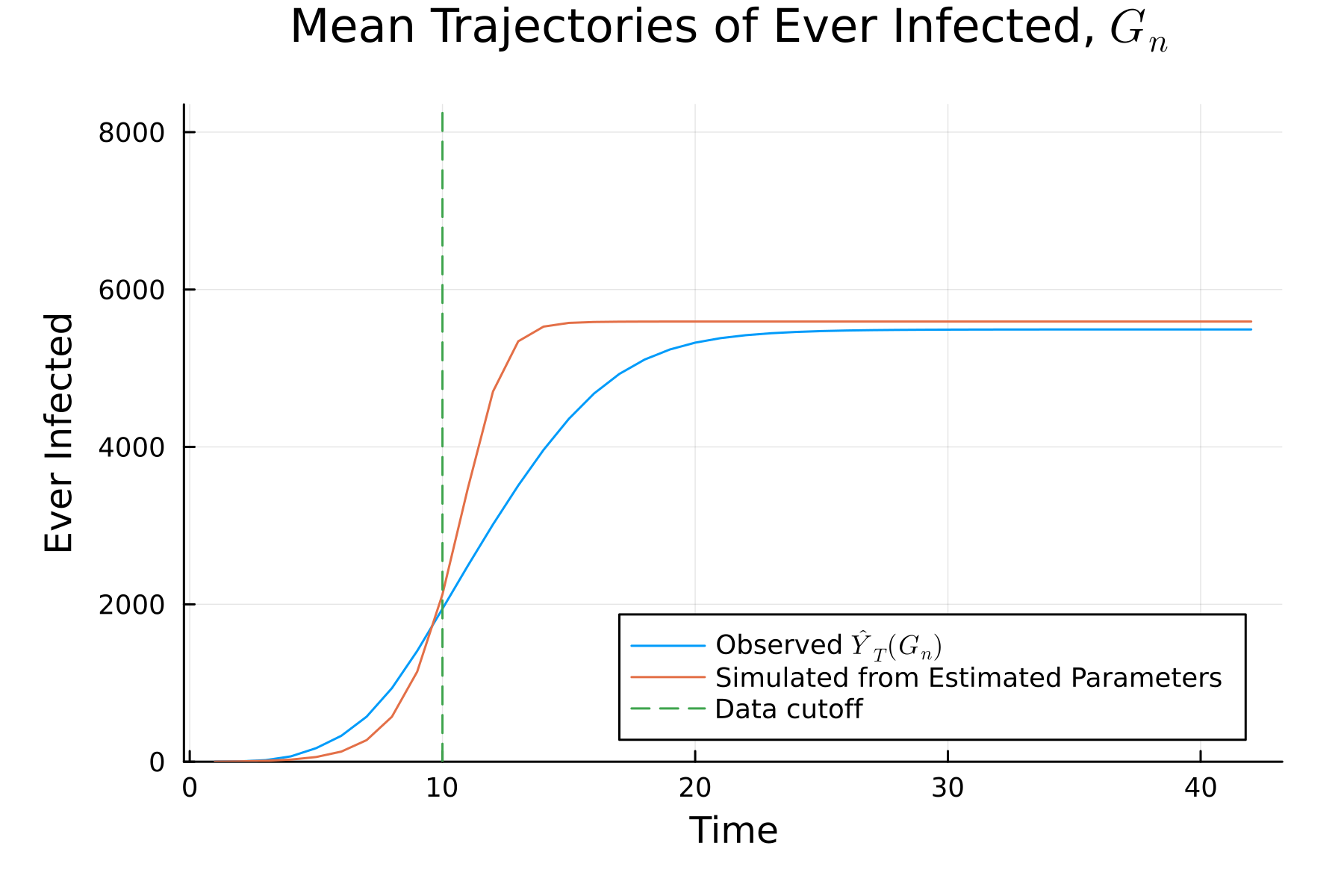

We then turn to exercises using observed data. In our first example, using location data from California and Nevada, we construct a real-world mobility network and examine network mismeasurement due to “pruning” – where links between locations are only included if a sufficient number of people move between them. We find that changing the threshold from five to six people traveling between Census tracts causes the policymaker to underestimate the extent of diffusion by nearly 56 percentage points. If instead of pruning, we induce errors by removing i.i.d. random links (holding fixed the volume of missed links), we find even more extreme underestimation: the policymaker underestimates the extent of diffusion by more than 76 percentage points. In addition, in both cases, there is little spatial overlap between epidemics when we perturb the initial location by only three links in the graph. As a second example, we turn to a viral marketing experiment in rural India (Banerjee et al.,, 2019). We show that similar patterns hold. When we add links with i.i.d. probability in village networks with 200 nodes, the econometrician underestimates diffusion by nearly 15 percentage points. We also document extreme sensitive dependence on the seed set: we move only one single seed (out of up to five seeds in a village) to one of its neighbors, and we find that the resulting diffusion patterns always have distinctions in terms of which nodes are activated. On average across simulations, the intersection of activations starting at the highly similar seeds is only 61 percent of the activations encompassed by both diffusions.

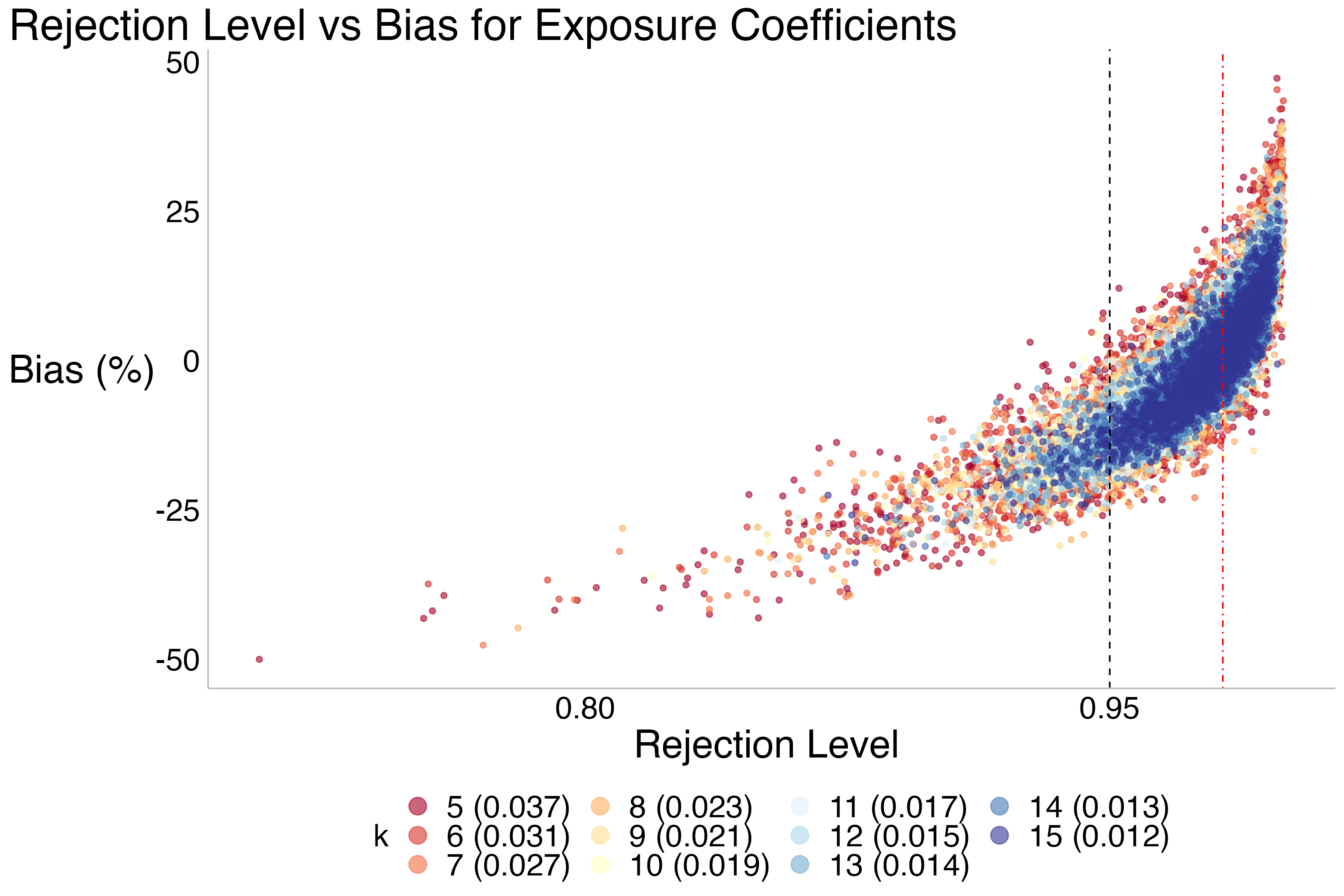

As a final empirical example, we turn to the problem of estimating peer effects. We motivate the connection by considering a peer effects regression based on a diffusion measure. Using data from Cai et al., (2015), we estimate a regression and show that the estimates are sensitive to the network specification. We consider i.i.d. errors that correspond to at most missing one in five links, and show that it leads to dramatic loss of power – we find that the econometrician fails to reject the null under 15% of simulation draws, despite the null being false. While the bias is relatively small on average, any given realization of the network can generate large changes in the coefficient values.

Together, this set of results generates broader implications. For instance, a potential corollary is that compartmental SIR models used to approximate a diffusion process may suffer the aforementioned problems as they generate such mismeasurement from ignoring small leakages across compartments. Our results also have implications for policy design in situations where diffusion plays an important role. Given the forecasting difficulties, we expect that estimated optimal policies may change dramatically depending on the network data collected.

1. Model

1.1. Environment

We model society through a sequence of (random) undirected, unweighted graph , indexed by the number of nodes . is constructed as follows. There is a sequence of “base” graphs, , with minimum degree . We assume that is undirected, unweighted, and connected. Then the full social network is given by , which is the union of the “base” and where is a collection of random links. We assume that the policymaker perfectly observes (samples) only the base graph ; in that sense, can be thought of as an error graph. The links in are formed with i.i.d. probability between each pair of nodes.777We use this as a benchmark case. We generalize the setting to allow for more local dependence in Section 4. There is a diffusion process that spreads over the network following a standard SIR process with i.i.d. passing probability .

It is useful to define as a percolation on the graph . This is a directed, binary graph with each link activated i.i.d. with probability . The SIR process we study is equivalent to a deterministic process emanating from some initial seed through .

We conduct asymptotic analysis, taking limits as both , the number of time periods, and , the number of nodes becomes large. Formally, we will consider a sequence of graphs , where are drawn randomly, that grows with , and consider where is an increasing function in . More precision on exactly how grows is discussed below. We will generally suppress the dependence of on for ease of notation.

As a matter of notation, let denote the ball of radius around vertex in a given graph and let denote the sequence of (possibly random) variables .

We define the expected activation set as

that “activated” could mean “infected,” “informed,” “adopted,” etc., depending on application. To set up our first results, we impose the following condition on the diffusion process.

Assumption 1 (Polynomial Diffusion Process).

For some constant and all discrete time , and .888 is defined as is bounded both above and below by asymptotically in Bachmann-Landau notation. Furthermore, .

We write this assumption over the diffusion process rather than on the graph structure of to allow for more generality. We could have simply assumed that itself has polynomial expansion, and together with the appropriate and i.i.d. draw assumptions, Assumption 1 follows. But, we also allow for more general settings. For example, Assumption 1 covers cases of with non-polynomial expansion and i.i.d. draws of , but with a sub-critical passing probability or short time horizons. The lower bound on is to ensure that the diffusion process spreads with sufficient speed – otherwise, the diffusion may halt before the medium time horizon that we study.

Turning to the substance of the assumption itself, first note that this condition implies that as the diffusion progresses, a growing number of nodes become activated in expectation.999The basic reproductive number on must be greater than one. Second, this condition governs both the structure of the graph and the diffusion process. As an example, consider a latent space network where nodes form links locally in a Euclidean space (Hoff et al.,, 2002). Since volumes in Euclidean space expand at a polynomial rate, this ensures that Assumption 1 will be satisfied.101010As another example, consider the case where the latent space is equipped with hyperbolic, rather than Euclidean, geometry (Lubold et al.,, 2023). While volumes in the space expand at an exponential rate, Assumption 1 may still be satisfied for some and . If the diffusion moves slowly enough, then volumes will still be locally polynomial, satisfying Assumption 1. In the case of sufficiently small , this situation corresponds to the case when the diffusion simply spreads slowly because it has a low passing probability. In the case of sufficiently small , this situation corresponds to the diffusion not having enough time to reach a large portion of the graph. Third, note the geometric relationship between and — governs the total volumetric expansion of the diffusion, while governs the shells of the diffusion (e.g., the boundary at time ). We explore the case where has exponential growth for completeness in Section 5.

We next put specific constraints on the time horizon considered. The first condition restricts the time so that the diffusion has not reached the edge of the graph.111111Formally, this assumption makes sure that the diffusion does not reach the edge of particular subgraphs. Our proof strategy relies on the construction of independent subgraphs to simplify computations, so we adjust the upper bound on to compensate. The second condition contains two substantive points: first, it is a mechanical assumption to ensure that under Assumption 3, there are links in in expectation. The second condition also ensures that we are making a forecast about a time that is appreciably far enough in the future, so idiosyncratic links that are missed have a chance to play a role. Note that our results will hold for any .

Assumption 2 (Forecast Period).

We impose that the sequence has for each , where the following holds:

-

(1)

-

(2)

.

While can go to zero under Assumption 1, the lower bound on rules out the case where as . The intuition for why plays a role in the time bound is that we need enough diffusion for the result to hold.

1.2. Econometrician’s Forecasting Problem

The econometrician’s policy objective is to estimate the expected number of activated (e.g., infected, informed, adopted, etc., based on application) nodes by date . We assume they observe and treat it as their estimate of . They also know the initial seed (an assumption we relax later on). Without loss of generality, we assume the econometrician’s problem begins at period and their objective is to predict the extent of diffusion at some period . Note that perfect knowledge of , knowledge of the initial seed, and knowledge of the start time are all strong assumptions that help the econometrician. Therefore, our first result can be thought of as modeling the policy objective in a best-case scenario. We later relax the assumption of perfect knowledge of the location of and consider the instability of the process to perturbations of the initial seed.

Let be an indicator which denotes if node has ever been activated through time . In principle the target estimand is

where the expectation is taken with respect to the diffusion process on graph and realizations of , with known . However, the econometrician uses only the observed as a stand-in (or mistakenly views this as the actual network driving diffusion),

where the expectation is taken with respect to the diffusion process on (mistakenly assuming ) with known .

1.3. Measurement Error

We impose bounds on , the rate at which idiosyncratic links form.

Assumption 3.

Note that, first, both the upper and lower bounds go to zero as both and grow large. Second, by Assumptions 1 and 2, . Third, it ensures that the missing links that are unobserved by the econometrician are small relative to the observed links, in the following sense: with probability one, is not a connected graph, nor will it contain a giant component as . This means that the large forecast errors we characterize below is not a function of a dense set of missing links, but instead, caused by a small (and disconnected) set of idiosyncratic links. While the forecast errors would also clearly happen if the econometrician missed a dense graph or a giant component, we focus on a regime where the mismeasurement is sparse, making the results more surprising.

2. Forecasting Difficulties

We now show how tiny measurement error leads to large forecasting errors in the diffusion process. First, we show how using the observed network to make forecasts with a known seed can greatly underestimate the average extent of diffusion on the true network . Second, we show how diffusion patterns can be very different even with small perturbations to the location of the initial seed, even when the true graph is known without measurement error.

2.1. Forecasting errors given a known seed

We begin by studying the case where the policymaker has knowledge of both the observed network and the initial seed location of . However, despite these advantages, we show that the econometrician’s forecast error will swamp the forecast as .

All proofs are in Appendix A unless otherwise noted.

We briefly give some intuition of why the forecast error dominates the predicted error in magnitude. Small errors caused by the error network recursively compound on themselves, creating massive forecast error. When considering the diffusion process in period , it is helpful to consider a volume around the initial node (what we call a “shell”) of size . This shell contains all the nodes that could possibly be activated by the process according to our observed network, . As time grows, this shell grows in size, and as one might expect, the likelihood of hitting a low probability mismeasured link in increases. This leads to the creation of a new shell elsewhere on the graph.121212In this setting, with i.i.d. , the shell is almost guaranteed to be far, but as we show later, this is not necessary for our results – we simply need that sufficient number of new shells form that have no overlap with the existing shells. This initial missed jump to other locations in the network does not generate forecasting issues of any consequence. What creates the issue is that these jumps recursively explode. In totality, these new shells caused by the propagating error dwarf the diffusion captured by the observed graph .

The proof strategy formalizes this intuition. We first compute a lower bound on the number of expected new “shells” in each time period. To generate a lower bound on expected activations, we introduce a tiling of the graph and count how many tiles are activated in expectation. We then calculate this number and scale by the number of nodes activated in each tile.

In Appendix F, we prove a similar version of Theorem 1 that allows the diffusion process to slow over time. We consider the case where the diffusion process decays at a polynomial rate: the resulting structure is equivalent to considering a diffusion process with a lower . Doing so requires slightly different assumptions: we require an earlier time window and a higher rate of missing links. The intuition is that we need additional missing links to “compensate” for the slowing diffusion process to get the same result.

In the above analysis, the policymaker is agnostic to the location of diffusion, which may not be realistic in practice. A key consequence of our result, which follows from the proof strategy, is that we assume the policymaker perfectly forecasts the diffusion locally around the initial seed. We decompose the forecast based on into two components: the spread from through , and activation waves “seeded” through links in . Locally, the policymaker has a perfect forecast of exactly . In reality, the policymaker likely has errors locally as well and perhaps more so than globally, a concept we explore in greater depth in Section 4.

2.2. Sensitive Dependence on the Seed Set

We next consider the assumption that the policymaker has perfect knowledge of and show the sensitivity of the process depending on which nodes start the diffusion. This result shows an additional limit of the econometrician’s forecasting ability. Here, we assume that is perfectly observed, removing any sense of measurement error in the network, and consider variation in different seeds (the initially activated nodes). We make this comparison to show a structural lack of robustness of this model, potentially caused by mismeasurement in the initial seed: if seeds differ only slightly, this is enough to generate very different diffusion patterns.

The setup of the result is motivated by a policy-relevant consideration. If the policymaker is slightly incorrect in their assessment of the seed (e.g., patient zero), do we see large differences as to both where the diffusion jumps and who is activated? Here, we give the policymaker the advantage of knowing and facing no measurement error. While there are idiosyncratic links in , the policymaker observes them. Despite these advantages, the policymaker will still encounter problems.

We fix a baseline percolation, , for the diffusion process and vary only the initial seed of the process between and some neighboring . This removes the randomness from the diffusion and holds fixed the set of possible paths that it can take as we vary the initial seed. The percolation is a useful construct because we can study the resulting activated sets, given percolation , when seeding with some versus some . Let and denote the ever-activated sets by period for the two seeds respectively. This holds the counterfactual passing process across each link fixed as we look across different initial seeds.

It is useful to define a catchment region. For some node that is activated at time , if the diffusion process continues for more periods, then the catchment area is the maximal set of nodes that can be indirectly activated beginning with , . In what follows, we will find that, given the extreme sparsity of , for any two nodes and which have edges in (i.e., there exists alters that ), the catchment areas (over periods of transmission) typically will not intersect: with probability tending to one. Intuitively, the catchment areas of these alters in , and , can be thought of as analogous to geographically distinct areas (though the network is not constrained to geographic structure). Each region has potential size in expectation, and is bounded above in size by the total number of nodes in a radius ball around the seed, where is the number of periods post-seeding.

We define a sequence of local neighborhoods relative to a diffusion process. Let be a ball of radius around the reference node, possibly growing, with . Relative to the total expansion of the diffusion process over periods, the local neighborhood about we consider is vanishing.

We make use of the fact that relative to seed , there are two nodes, and , which are the closest and second closest nodes to and also have a link to some respective alters in . In what follows, we condition on the sequence of events : there exists at least one path between and in the percolated graph. The construct helps us rule out pathologies and instead focus on cases where escapes are possible. In general, percolation problems with changes on linkages (e.g., bond percolation) are extremely complicated and not our focus (see, e.g., Smirnov and Werner, (2001); Borgs et al., (2006)). So, we consider sequences under general conditions of interest here.131313To see an example, with infill asymptotics, one can construct sequences where occurs with probability tending to zero just by virtue of adding more independent paths in at a sufficiently high rate relative to .

We will use a version of the Jaccard index (Jaccard,, 1901) to compare the expected set of nodes that are ever activated by both the diffusion processes starting at and starting at relative to the expected number of nodes that are activated by either initial node process. We call this discrepancy measure — the relative expected number of nodes ever activated by only one of the epidemics to the expected number activated by both. It is useful to also condition on the event that and are connected in the percolation, because otherwise the problem is uninteresting since the diffusions never overlap. So, we assert and define our index as

where the expectation is taken over and . If is a non-trivial value for a nearby pair and , then, on average, a large set of nodes are activated through the process by only one diffusion process, and not the other, holding a percolation fixed.

Theorem 2.

Let Assumptions 1, 2, and 3 hold. Let be an arbitrary initial seed and consider the stochastic sequence comprised of a fixed sequence of , random , and condition on . Then with probability approaching one over draws of , the following hold. There exists a sequence of time periods and local neighborhoods vanishing relative to the overall time length, , which may depend on realized , and a sequence of sets such that:

-

(1)

for some positive fraction independent of , and

-

(2)

the number of catchment regions disjoint from activated under seeding with rather than is at least

for growing , and may be order constant or even diverge in .

Further, for any ,

for some fraction constant in .

The key idea is that for a given , the realized may generate “shortcuts” to arbitrary other points in the network, which then may be traversed in a given draw of . When considering a diffusion pattern starting at a nearby , we must consider whether a percolation would activate a different shortcut than that beginning with . We show that there will always exist some and time period for which this is true. The intuition comes from fixing the second closest “shortcut” link in to : before a diffusion pattern from can reach this shortcut, the diffusion from will reach this shortcut. This will induce two effects. First, there will be jumps in the number of distant catchment regions activated in the network. Second, a non-trivial share of activations will be different due to variation in seed. Figure 1 shows a heuristic construction of the set .

Stepping back, we can also note that is close to in the sense that their network distance is small relative to the length of the diffusion, and yet these problems occur. Further, these alternative seeds are not isolated: the first part of the theorem shows that a non-trivial fraction of the location neighborhood about contains such problematic alternative seeds. Our simulations quantify examples to show how extreme the problem can get in even realistic setups.

3. Estimation and Possible Solutions

We now consider several estimation procedures in our setting. First, we consider how the econometrician can estimate the underlying structural parameters like successfully, despite our pathological results above. Second, we show that what seems like a natural solution to our results on forecasting – estimating , our error rate, and adjusting for it – is almost impossible in reasonable samples, because the error rate is so small. Third, we consider a widespread testing regime, and show that the detected number of regions that have activated nodes will dramatically underestimate the true number of regions that have activated nodes.

3.1. Estimating Parameters of the Process

We now show that despite the aforementioned pathologies, some core parameters of the process can be consistently estimated.

The econometrician uses and to estimate , along with knowledge of the initial seed . We assume that the econometrician has perfect detection: they see all true activations. Let be the mean degree in , which is observed by the econometrician. The econometrician estimates in the following manner. Using knowledge of and , the econometrician will be able to derive the exact number of expected activations for a given value of . They can then consistently estimate using the observed .141414We do not solve a general formulation, as solving the generic problem is known to be NP-Hard (Shapiro and Delgado-Eckert,, 2012). Rather, we show an (inefficient) estimator.

Given a consistent estimate of , it then follows that the econometrician will be able to consistently estimate , the basic reproduction number. The estimated basic reproduction number—that is, the number of nodes, in expectation, activated by the first seed in an activation-free equilibrium—can be estimated as where is the (observed) mean degree of , whereas in actuality it is .

Lemma 1.

Proof.

Note that

where the final equality follows by assumption. Then, it is immediate that is a consistent estimator of , as can be computed directly and the econometrician has access to a consistent estimator of . An application of the continuous mapping theorem completes the result. ∎

This means that while the econometrician can consistently estimate they will still be unable to accurately forecast the diffusion as shown in Theorem 1.

We give an example of one way an econometrician might estimate consistently. Let be the set of neighbors of activated at period . Then at time , a consistent (though inefficient) estimator of will be:

Note that by restricting attention to susceptible nodes with exactly one activated neighbor, activations occur independently with probability . Therefore, it is clear that . Note that this estimator makes use of perfect knowledge of via the sets which encode the neighborhoods of each node. Figure 2 depicts how this estimator works in practice, and also highlights how the restriction to nodes that have only exactly one activated neighbor does not utilize all information most efficiently.

This estimator should be used locally, in the sense that the econometrician should choose such that there are unlikely to be any links within a ball of radius to the initial seed. This restriction is to ensure that the econometrician only needs to worry about observed local links, rather than potentially far-reaching global ones.

3.2. Possible Solutions

We explore two possible solutions that a policymaker might pursue. First, they might estimate , the connection rate for the graph, using supplementary measurements. Second, they might use widespread testing.

3.2.1. Estimating

Given the prior results, one approach for the econometrician might be to estimate , and use the estimate in order to inform forecasts. Assume the econometrician already has , but is able to obtain follow-up data. To do so, they sample nodes uniformly at random out of the , and query whether or not each link exists in . In this way, they can potentially find links in to supplement the information of the known . Note that a sample of size will deliver possible links that could be found.

We show that in practical settings, this strategy will not be feasible. Specifically, the above results have shown that even with extremely small levels of measurement error ( very rapidly), we see large forecast errors and sensitive dependence. The challenge is that in order to estimate , since it is very small, a vast amount of data is needed. Unless one is able to collect follow-up data at an enormous scale, estimating will not be possible. In fact, there are two regimes. First, with a large, growing sample (which may describe most realistic survey sizes), the probability that one does not find a single link in the follow up tends to one, even though the rate of is high enough to cause all the problems previously discussed. Second, one may find some missed links with a (potentially unrealistically) larger sample, but one will not be able to develop a consistent estimator.

Lemma 2.

Under Assumption 3, if:

-

(1)

,

-

(2)

, then there exists and such that .

We can use this to give a sense of scale. Say that is equal to one million. Then a survey of one thousand people may deliver essentially no information on . However, we can also consider the case where is known to be much smaller than – in this case, could be much larger than and still deliver essentially no information. Consider a case where (which is valid for and , which are allowable parameters under Assumption 2). Then, with constant , would still deliver nearly no information – in this case, with equal to a million this corresponds to a (perfect) survey of more than 13,800 people. It should become clear that this type of sampling regime quickly becomes infeasible.

In the same example, note that if (which is admissible under Assumption 2), then with constant , under any , an estimator for is not consistent, even if there is information gained in the survey. To see this order statement numerically, keeping the population as one million, let us take , which we show in our simulations below to mimic real data. Then the (perfect) survey of nearly 68,000 people would still generate an inconsistent estimator.

In practice, surveys of 15,000 people, let alone 70,000 people in a city are uncommon. It is unlikely that this is an obstacle that can feasibly be overcome in most policymaking settings.

3.2.2. Widespread Testing

Another solution is the use of widespread testing. Say that a policymaker wishes to estimate where in society activated agents reside at a given time period. This might be because the policymaker wishes to track regions with a disease, or locations that are susceptible to problematic rumors, or where certain technologies have been adopted. Testing could correspond to a biological test (in the disease case), but could also include surveying technological adoption or asking whether certain beliefs hold. We continue with the concept of regions introduced alongside Theorem 2. Recall that catchment regions are areas where the diffusion is re-seeded non-locally via links in . We show that even when the total overall diffusion count is estimated accurately, the number of true regions that are activated at some time period will be grossly underestimated.

Specifically, we assume that the policymaker conducts random tests instantaneously and uniformly throughout the entire society of nodes and detects the activations with i.i.d. probability . Under this widespread testing regime, we can calculate the probability that a region is correctly identified as having been seeded by period with the diffusion process. The basic argument is that there will be a number of regions which have just a few activations, meaning that the probability of not detecting any activations is high.

Theorem 3.

This result is surprising. One imagines that given a detection rate, since there are many opportunities to detect the activation, one should be able to do better than a detection rate of at a regional level. And yet the opposite is true. The result holds because many regions will have few activations, making it harder to accurately detect them. The number of regions with small numbers of activations that are hard to detect will comprise the majority of activated regions.

To further see why this is stark, consider the following numerical example. Imagine that a test for a disease has 99% power. Still, the implicit detection rate need not be 99%, since it is not a guarantee that every approached agent will actually be tested. They may not consent, be hard to reach, or forget, among other things. Let us say the yield rate is 2/3. Then . So our result says that the share of missed regions is at least 34%. The intuition comes from the fact that newly seeded regions are the most unlikely to be detected, since the share of infected individuals is smallest in those regions. Note that increases at a faster rate than . The upshot is that the policymaker will always be chasing the diffusion despite high-quality testing and miniscule measurement problems.

4. With Only Local Mismeasurement

In the above analysis, we took to be constructed with i.i.d. links drawn Bernoulli(). We show that this assumption is not necessary for our results. The choice was a simplification in order to call attention to the fact that very sparse could still generate large problems. We now demonstrate that we can allow every to only have links in to a restricted set of nodes, nesting an intuitive concept of “local mismeasurement.” Despite this, with regularity conditions properly adjusted, the non-robustness results remain.

Now, instead of links in being i.i.d., each node can connect to a fraction of nodes. This is arbitrary, meaning that the share can be collected in any fashion without restriction. In fact, we allow for the possibility that , though there are restrictions on the rate.

Assumption 4.

The probability of connecting to an arbitrary node in is for a fraction of the nodes, and zero otherwise. Furthermore, for some .

Note that this assumption does not necessitate a topological, geometric, or geographic structure on . It simply states that any given node can only have idiosyncratic links with some limited fraction of other nodes. We take the fraction to be homogeneous for the sake of simplifying computations. In fact, this fraction can be vanishing with , meaning that in some sense there is only local mismeasurement but similar results to Theorem 1 apply.151515While we assume that is constant with , we can extend the results to the case where it is growing. In that case, . This allows for to go to zero at a much faster rate, but the corresponding lower time bound will increase exponentially.

Any arbitrary topological sequence of respecting the sparsity () and support fraction () conditions work for our argument. Given the reduced scope for mismeasurement, we need to slightly modify the time interval we study in order to discuss the “medium run” as well as the allowable .

Assumption 5.

We impose that the sequence has for each , where the following holds:

-

(1)

-

(2)

.

Note that the upper bound remains the same. The adjustment for the lower bound is to ensure that our results hold in the case where . In that case, we need a longer minimum time horizon to ensure that there is a chance for measurement error to have an effect.161616In the case where is permitted to grow with , becomes .

Assumption 6.

Then, the following results follow from similar strategies to Theorem 1.

The key change in these results follows from noting that a given node can link to nodes in , rather than the full set of nodes as before. Therefore, the rate of the actual linking in must be higher to compensate in order to still generate the forecasting failure result. Our assumptions ensure that , so the econometrician still only misses a set of disparate links – is comprised of many (small) disparate components asymptotically, as the linking rate will be below the threshold needed for a giant component. This allows for , meaning that even though allowable mismeasurements are restricted to a vanishing share of links themselves, the vanishing share of measurement errors still generate arbitrarily bad forecasts.

If at an arbitrarily fast rate, we can trivially note that the required for inaccurate forecasts will grow greater than 1. For instance, if nodes can only have mismeasured links to two other nodes, no matter , then clearly forecasting will be accurate. Consider the case where the sequence of networks is formed by an increasing number of locations of fixed size. If the econometrician perfectly observes all connections between locations, and measurement error is restricted to occurring only within each location, forecasts will be accurate. More generally, with vanishing at a sufficiently fast rate, the policymaker can still forecast accurately due to the extreme locality of missed links.

An immediate consequence of Theorem 4 is that a similar result about the detection of activations on a region-by-region basis will hold.

Corollary 1.

Despite restrictions on local linking, the overall behavior in terms of regional detection is identical.

5. Extension to the Exponential Case

We now turn to the case of exponential expansion. We include this for completeness. If there was significant exponential expansion globally throughout the network, diffusion would happen so quickly that from a policy perspective, forecasting would become moot and sensitive dependence unnecessary as the process will spread through the graph immediately. Nonetheless, we explore the implications of small mismeasurement even in this case.

Assumption 7.

We impose the following condition for some constant and all , and . In addition, we assume that

5.1. Forecasting

In this section, we study the behavior of forecasts when the diffusion process expands at a much more rapid rate. We then make assumptions that correspond to Assumption 3 and 2, to account for the faster-moving diffusion process.

Assumption 8 ( Bound for the Exponential Case).

Assumption 9 (Forecast Period).

We impose that the sequence has for each , where the following holds:

-

(1)

-

(2)

.

We can then note the differences in the bounds on : we impose a smaller lower bound and a larger upper bound than for a polynomial diffusion process. The smaller lower bound on is intuitive: because the diffusion spreads more quickly, the seeds from idiosyncratic links can cause the diffusion to explode much more quickly.

Then, the following theorem holds.

We can make a few comparisons to our previous result. The first portion of this theorem is an analogue of Theorem 1, though with a different condition on . We impose a stronger lower bound on – in order for similar results to hold, we require a larger probability of idiosyncratic links. This change follows from the structure of the proof – the key comparison is the expansion in all of the areas “seeded" via the idiosyncratic links compared to the expansion of the original diffusion process. When the original diffusion process is faster moving, it means that more idiosyncratic links are needed to overwhelm the original diffusion.

Second, we can note that if , then the condition on implies that as , will contain a giant component almost surely. This condition will hold generically. This is in contrast to the case where the diffusion follows a polynomial process, which generally does not need to contain a giant component asymptotically. While the fraction of links missed by the policymaker still goes to zero, the policymaker still misses a large amount of structure.

In both cases, we give the policymaker access to perfect local forecasting, though it plays distinct roles in each case. We get a similar role as in Theorem 1. The perfect local forecasting cannot save the policymaker from only identifying a vanishing fraction of expected activations.

5.2. Partial Converse

We now introduce additional structure on , first to prove a partial converse to Theorem 5. If we assume that the catchment regions of are disconnected, we can prove a converse to Theorem 5.

Proposition 1.

This result is positive for the econometrician – they correctly identify a fraction of activated nodes that asymptotically goes to 1. Mechanically, this follows from the fact that the initial activation creates too many activations for the additional “seeded” activations through to overwhelm. Note that will not contain a giant component asymptotically. Combined with Theorem 5, this tells us that for a more expansive diffusion, the forecasts made by the policymaker will not be “accurate” if and only if contains a giant component. Because is an Erdos-Renyi random graph, the giant component within will have a tree-like structure meaning that the policymaker is missing a highly expansive structure. Here, perfect local forecasting plays a positive role – it is what allows the policymaker to be arbitrarily accurate. However, given the nature of the network structure itself, a very large share of the population becomes activated very quickly.

5.3. Local Linking

We next show that the above results can be extended to the case where there is only local mismeasurement. This result forms the analogue of Theorem 4. We make the following assumption that is the analogue of Assumption 4.

Assumption 10.

The probability of connecting to an arbitrary node in is for a fraction of nodes, and zero otherwise. Furthermore, .

Proposition 2.

In the case where Assumption 7 holds, we see a similar modification of results. The necessary for the policymaker’s forecast to go to 0 is relatively larger in the local case than in the i.i.d. case, for exactly the same reason. A key difference is that if , the policymaker will be missing a giant component in asymptotically. Given that is likely less than 1, except in the case of mechanical diffusion, it is likely that holds. In the case where the policymaker’s forecast is “accurate,” in that the expected fraction goes to 1, the policymaker still cannot miss a giant component in , as .

6. Simulations

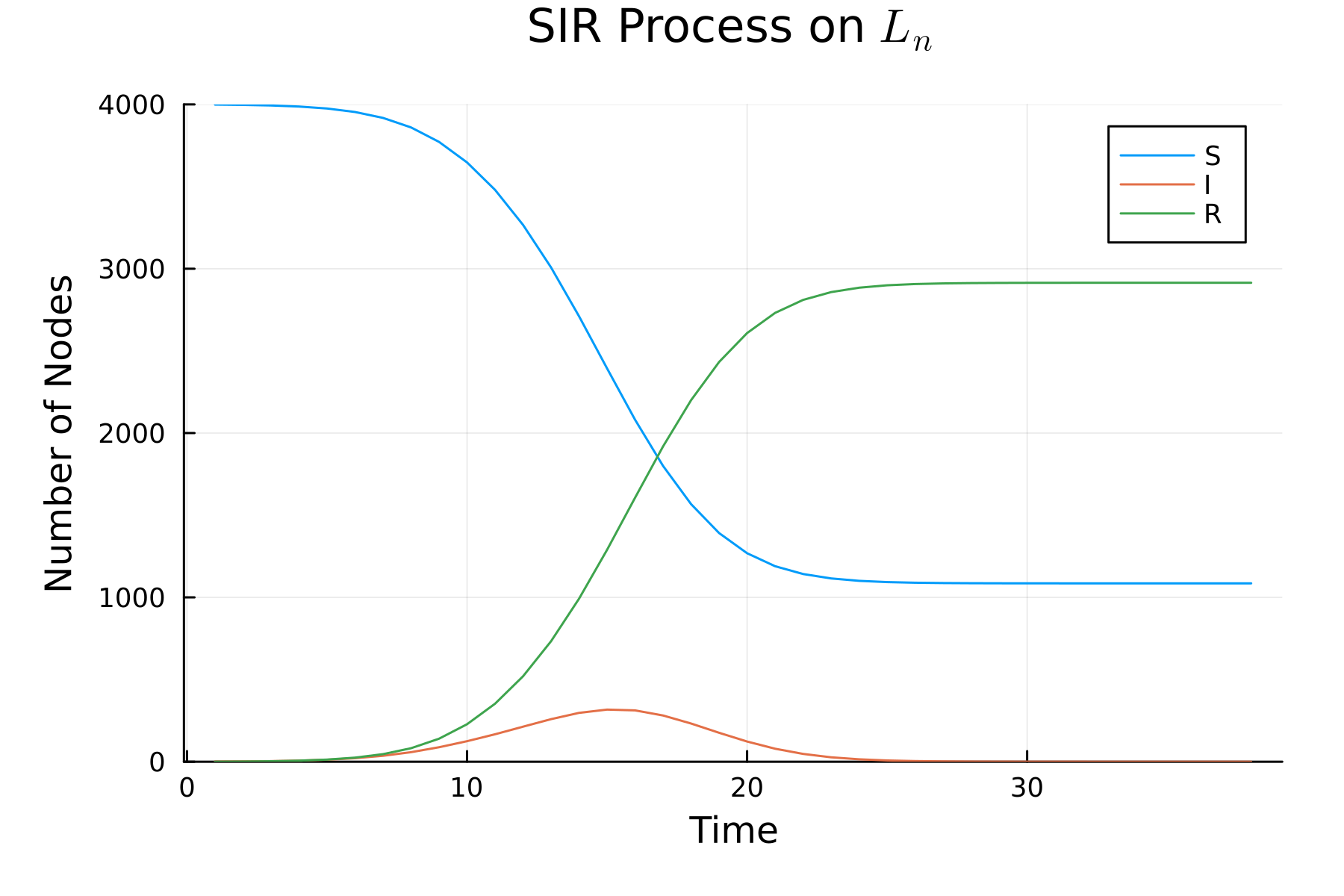

We now present a number of simulations to illustrate our results in finite samples and explore how variation in parameters affects things quantitatively. We simulate a Susceptible-Infected-Removed process on a network with one period of activation before removal, analogous to the processes that we study theoretically. We give an overview of each part of the simulations in the relevant subsections, with full details in Appendix B.

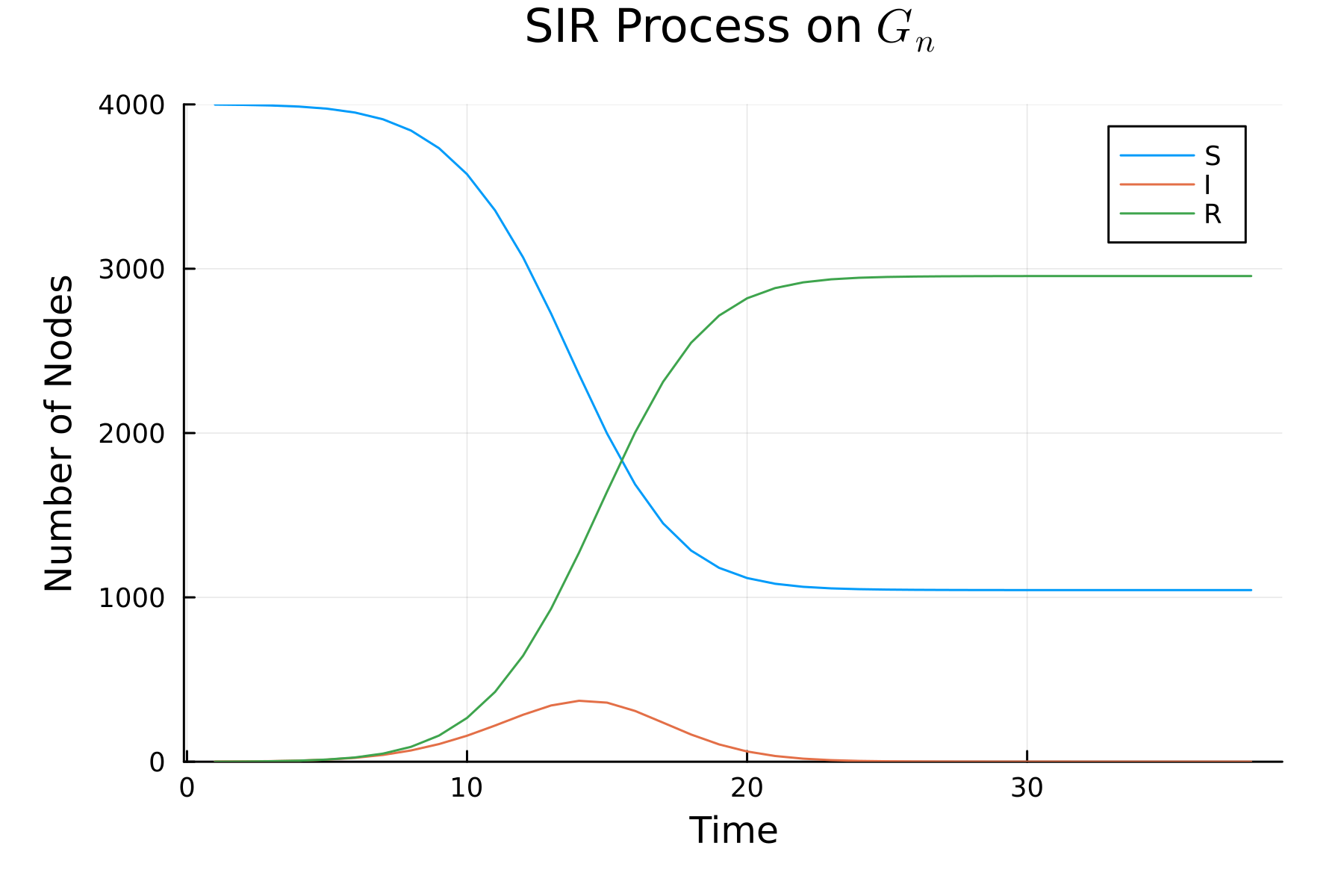

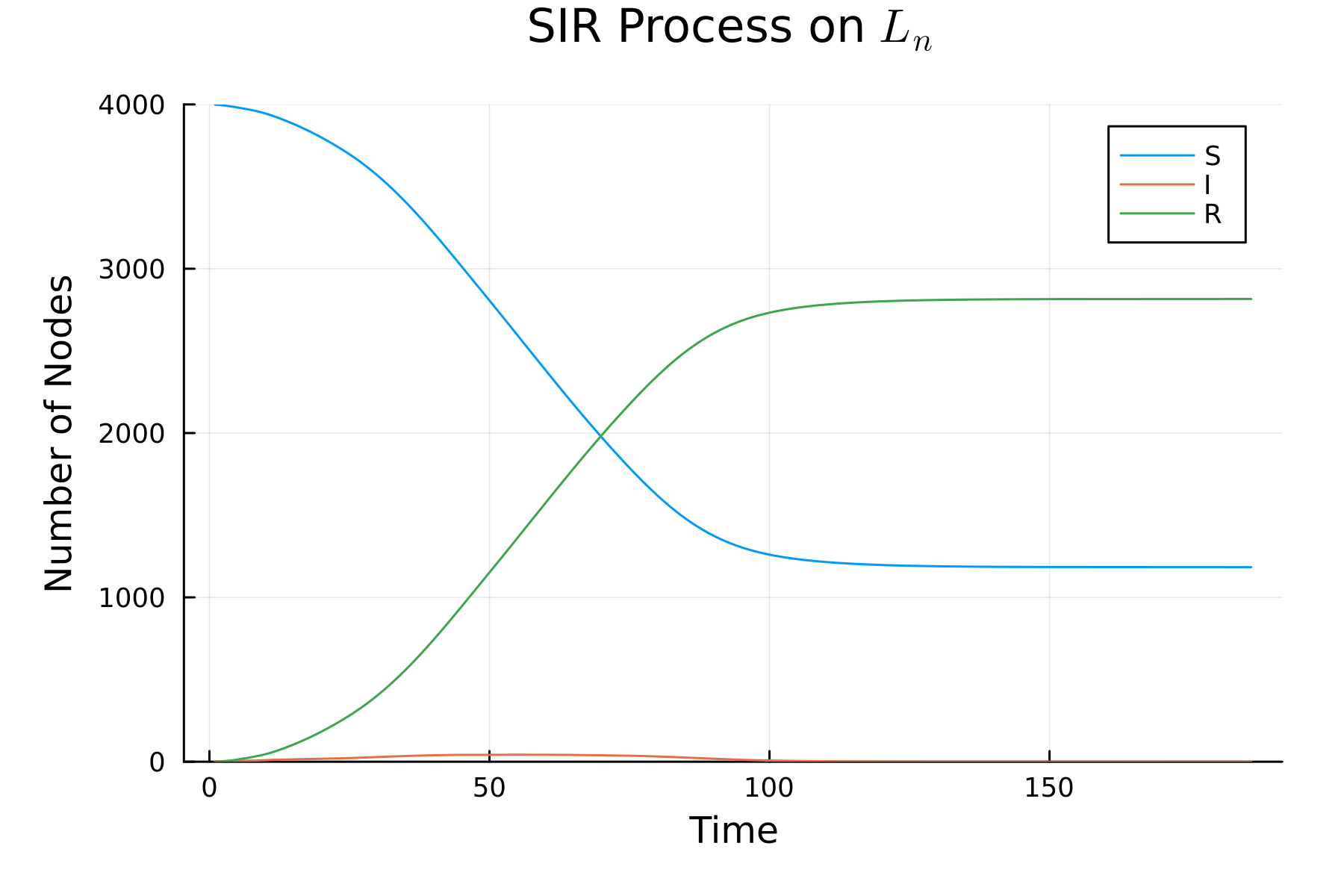

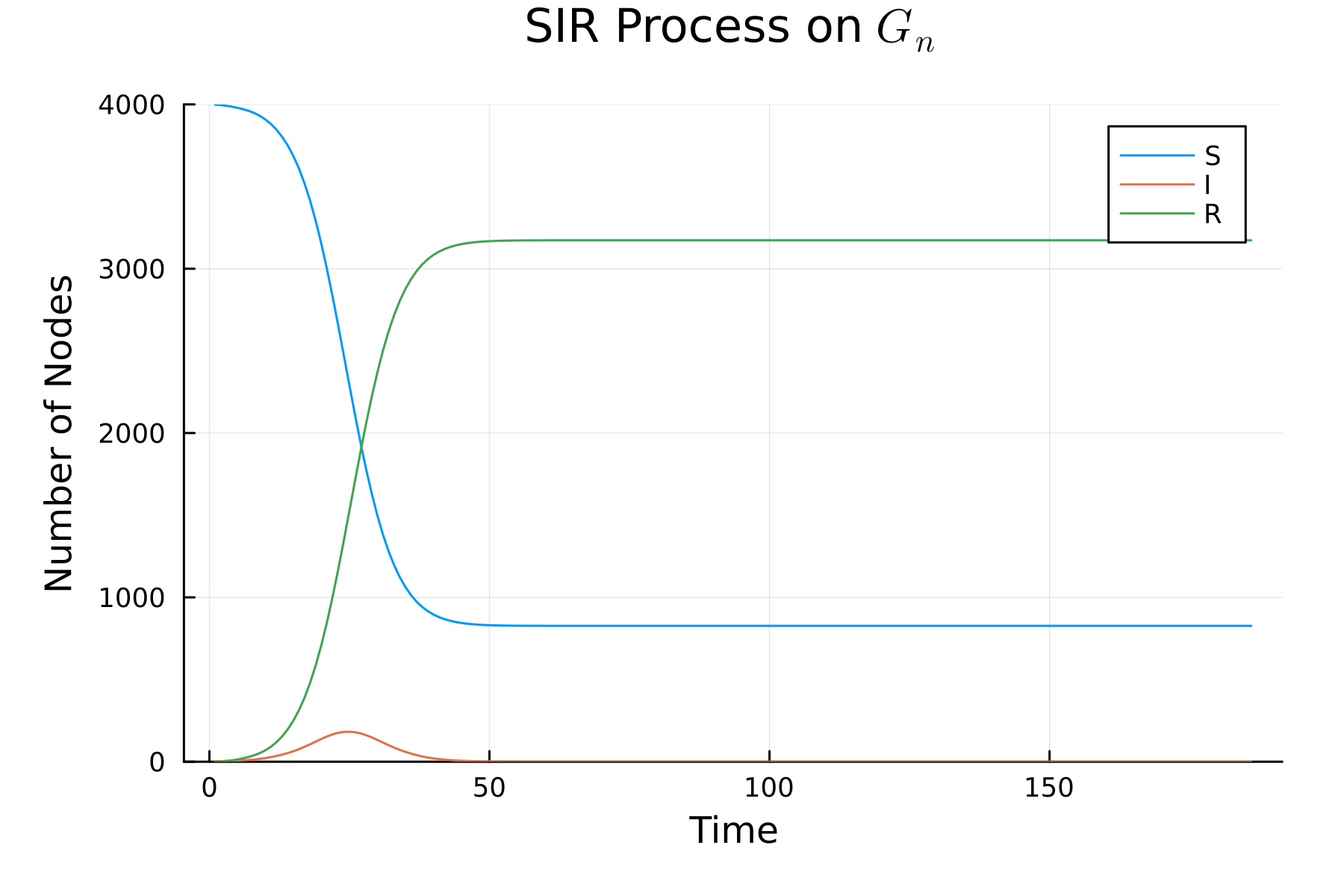

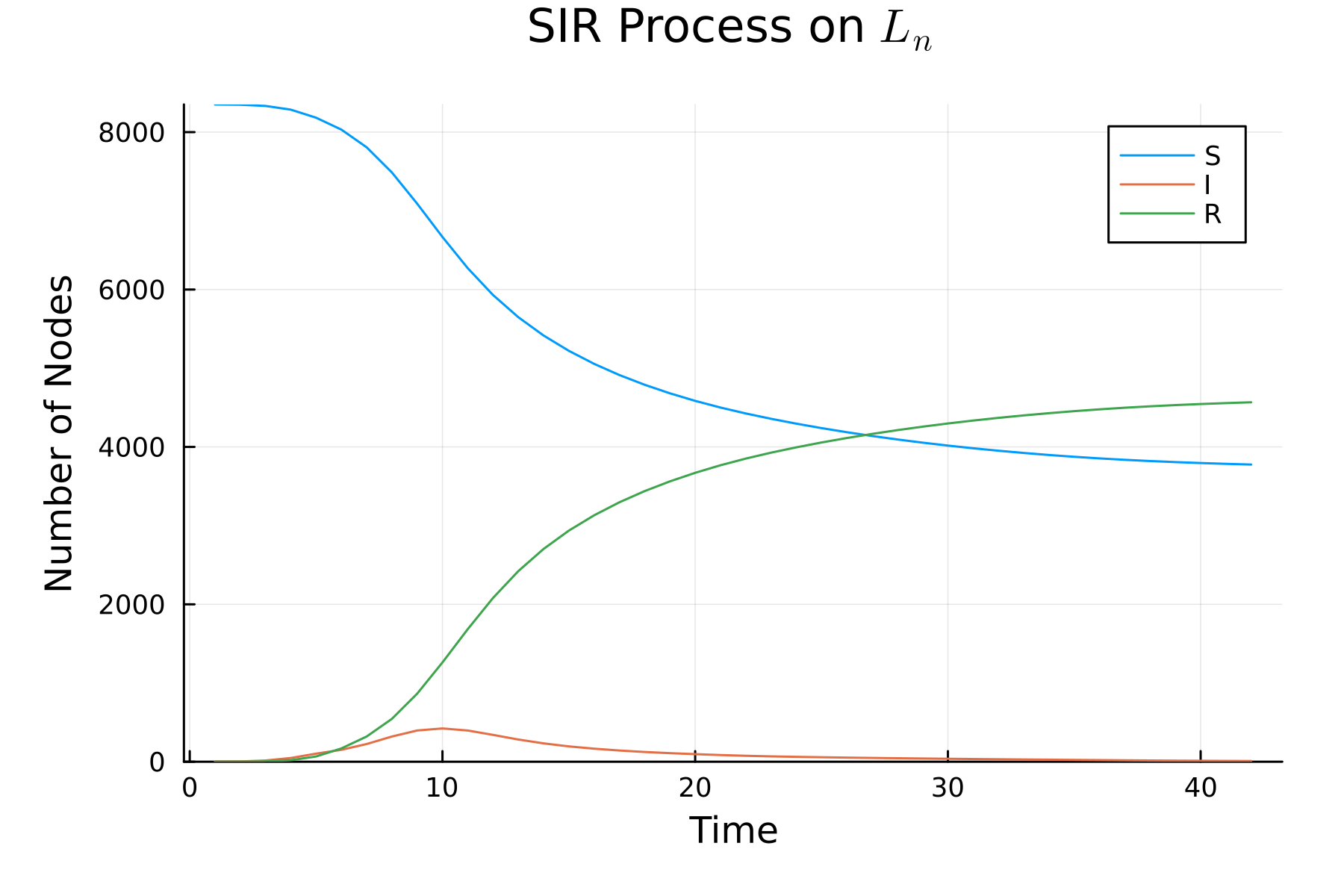

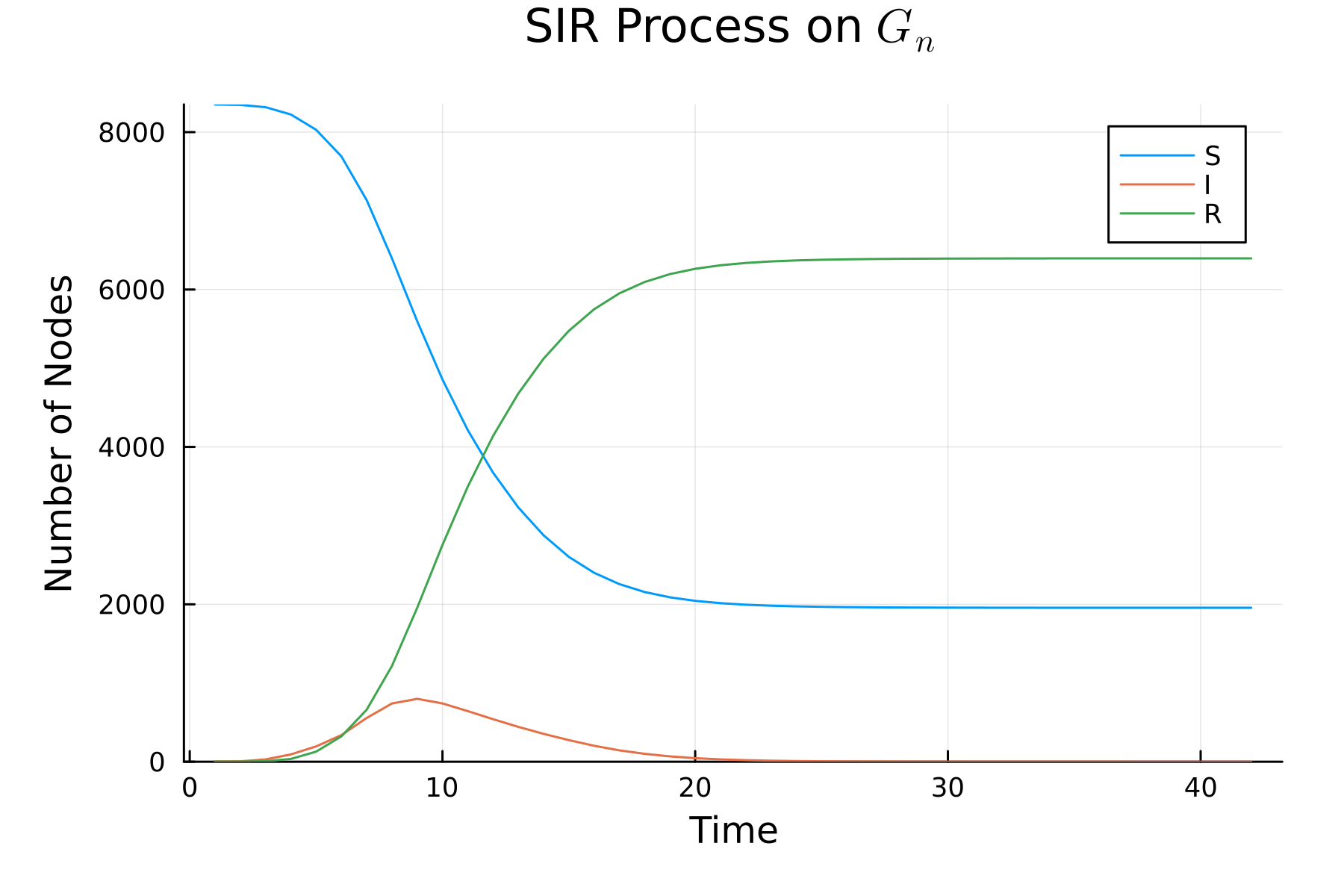

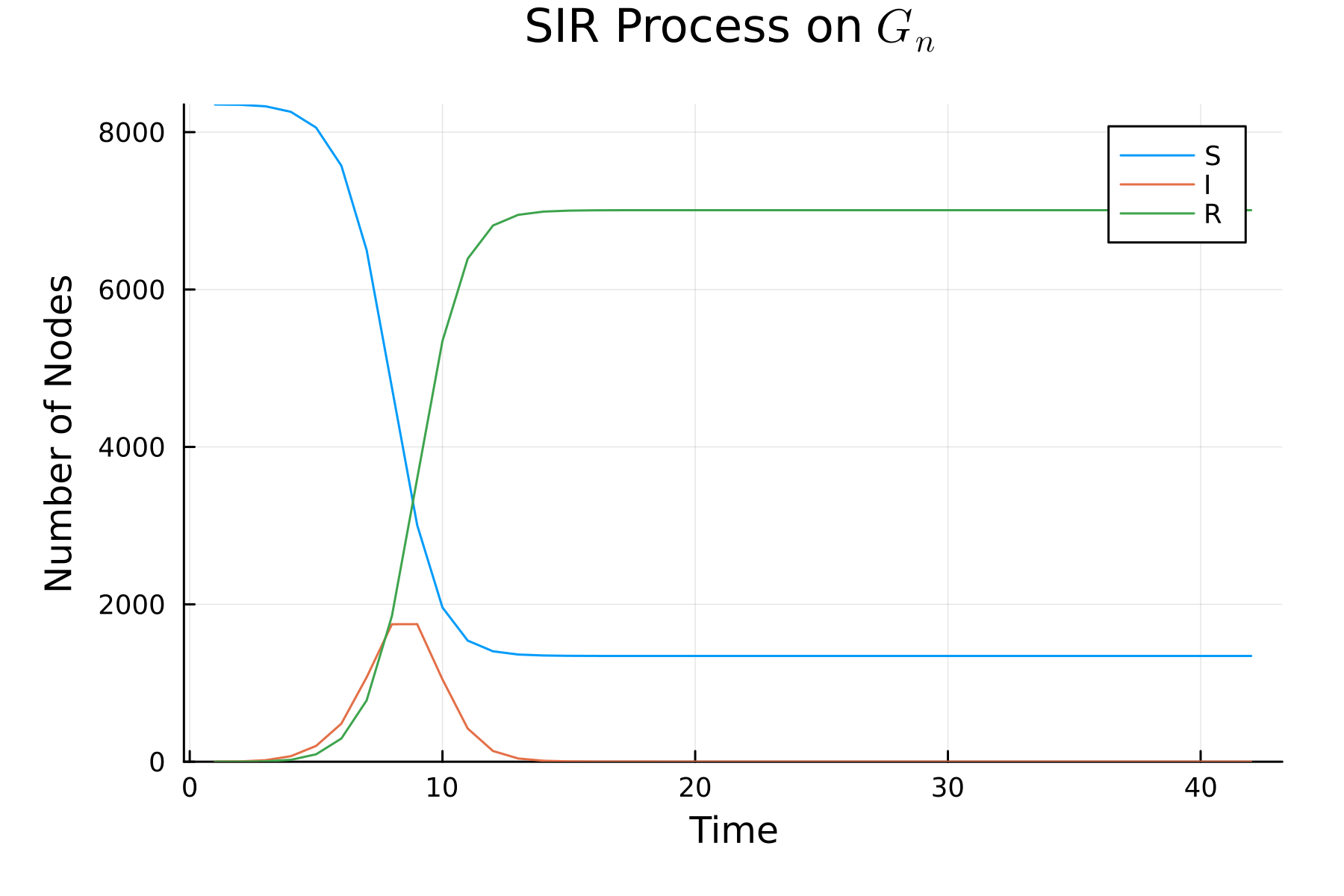

Throughout, we fix , the graph observed by the policymaker and design it to mimic the sparsity and clustering structure in real data. We first generate by placing nodes in a -dimensional lattice on . The remainder of nodes are placed uniformly at random throughout . Nodes then link to nearby nodes, with a radius of connection chosen to ensure both that the lattice is connected and that all randomly placed nodes will be connected to the graph. As an illustrative example, we simulate two different networks with nodes: one with and one with . For the SIR process on the graph, we set , and then compute by dividing by the mean degree in . Summary statistics are shown for both graphs (along with average summary statistics for the corresponding ) in Appendix Table B.1.

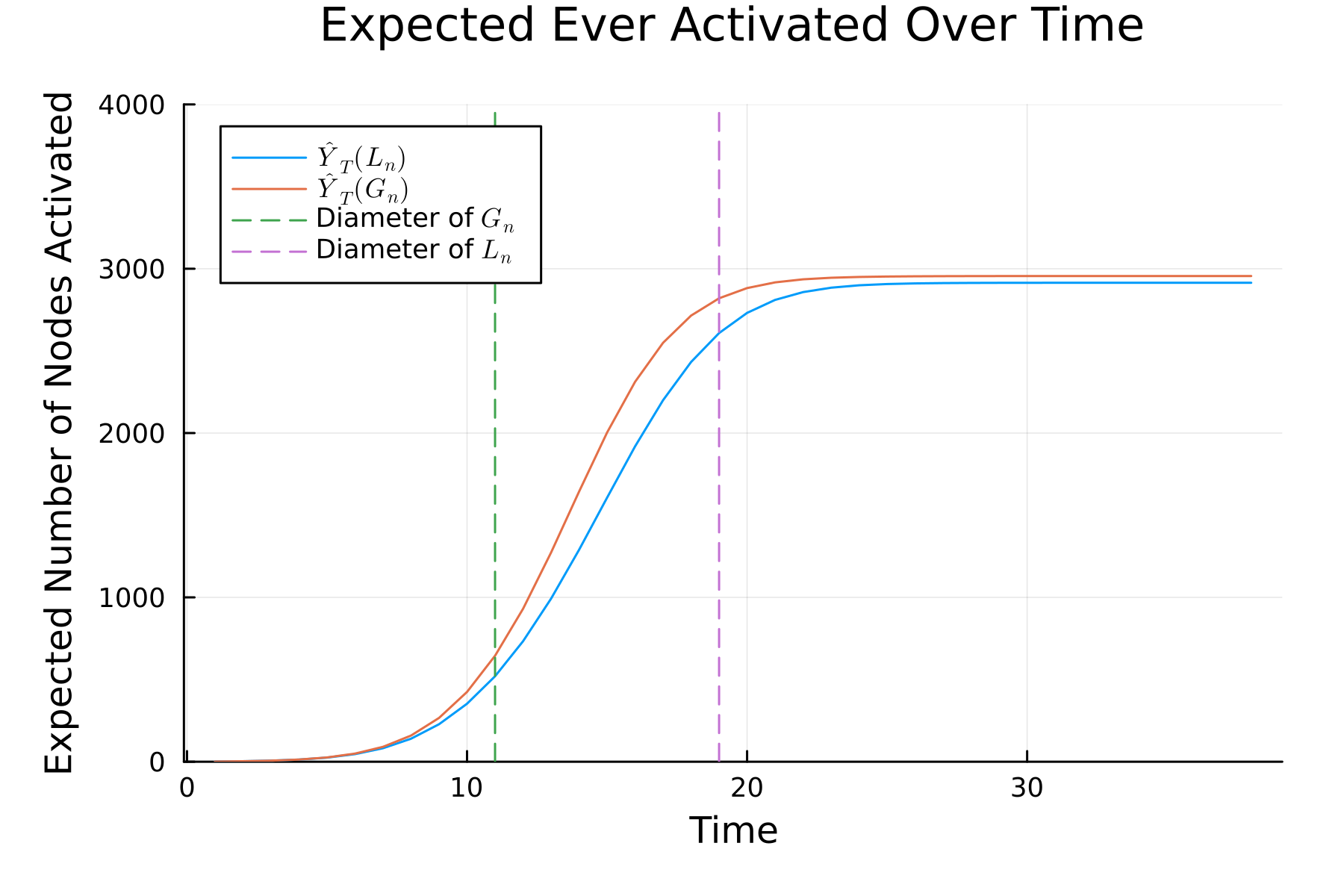

We choose to be twice the diameter of – meaning that for , it is chosen to be 38, while for it is chosen to be 184. This value is chosen to cover both periods early on in the diffusion process, and as well as past the time period covered by our asymptotic theory.171717Recall the time period bounds from Assumption 2 of Theorem 1. Since the asymptotic theory we consider cannot speak to long-run, we simulate to the point when the diffusion extends well past the diameter of the graph, at which point we would expect the diffusion to conclude.

6.1. Forecast Errors and Sensitive Dependence

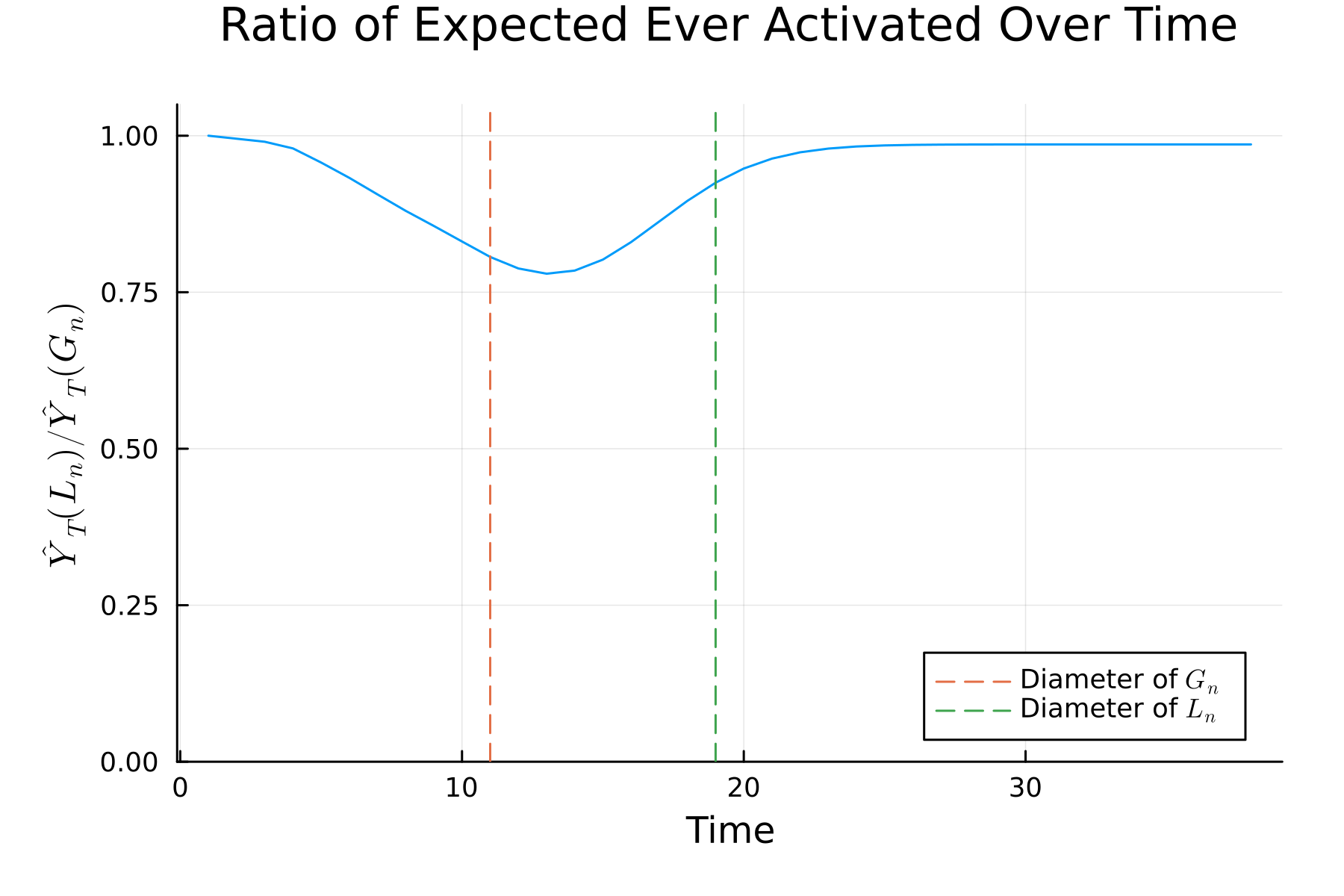

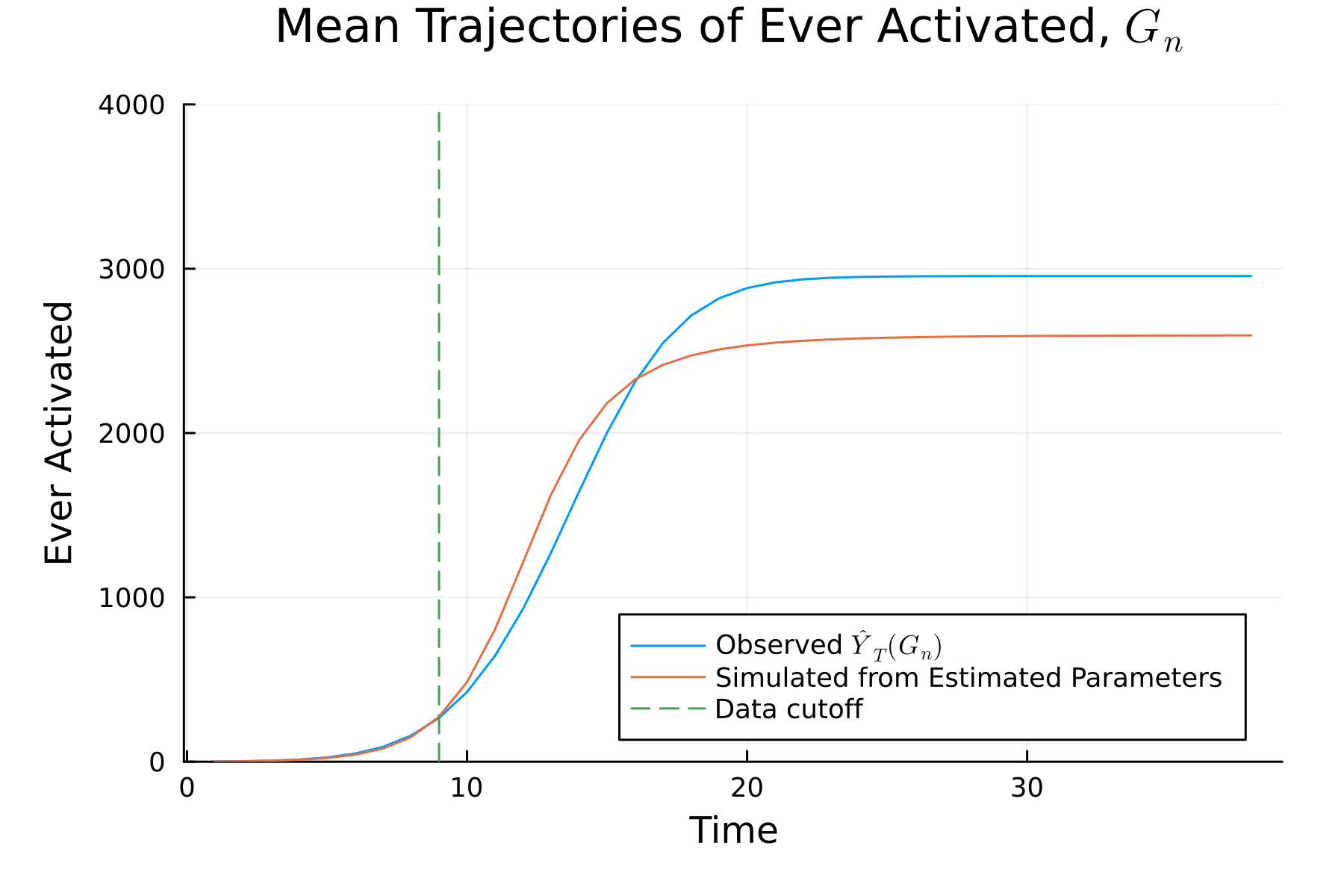

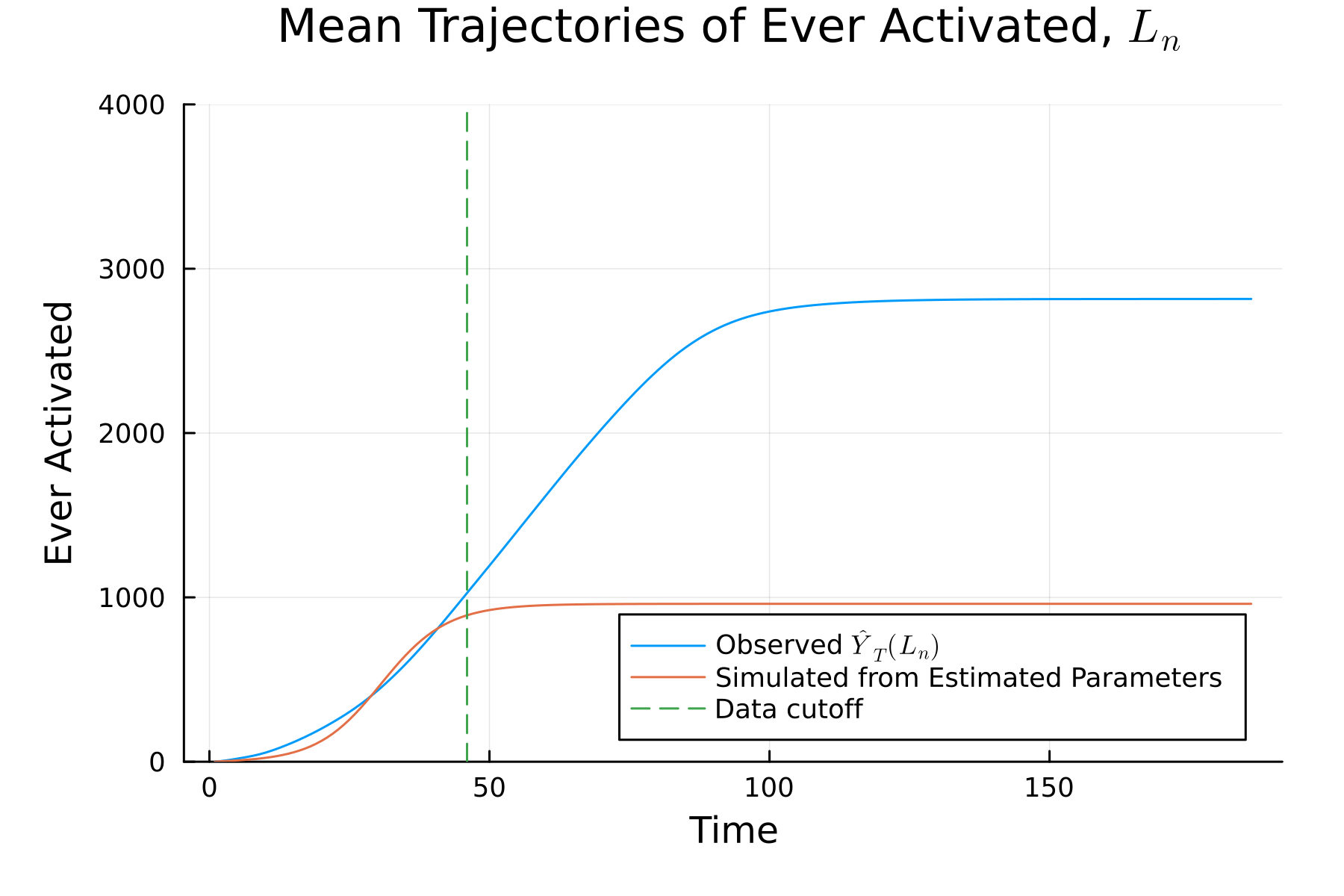

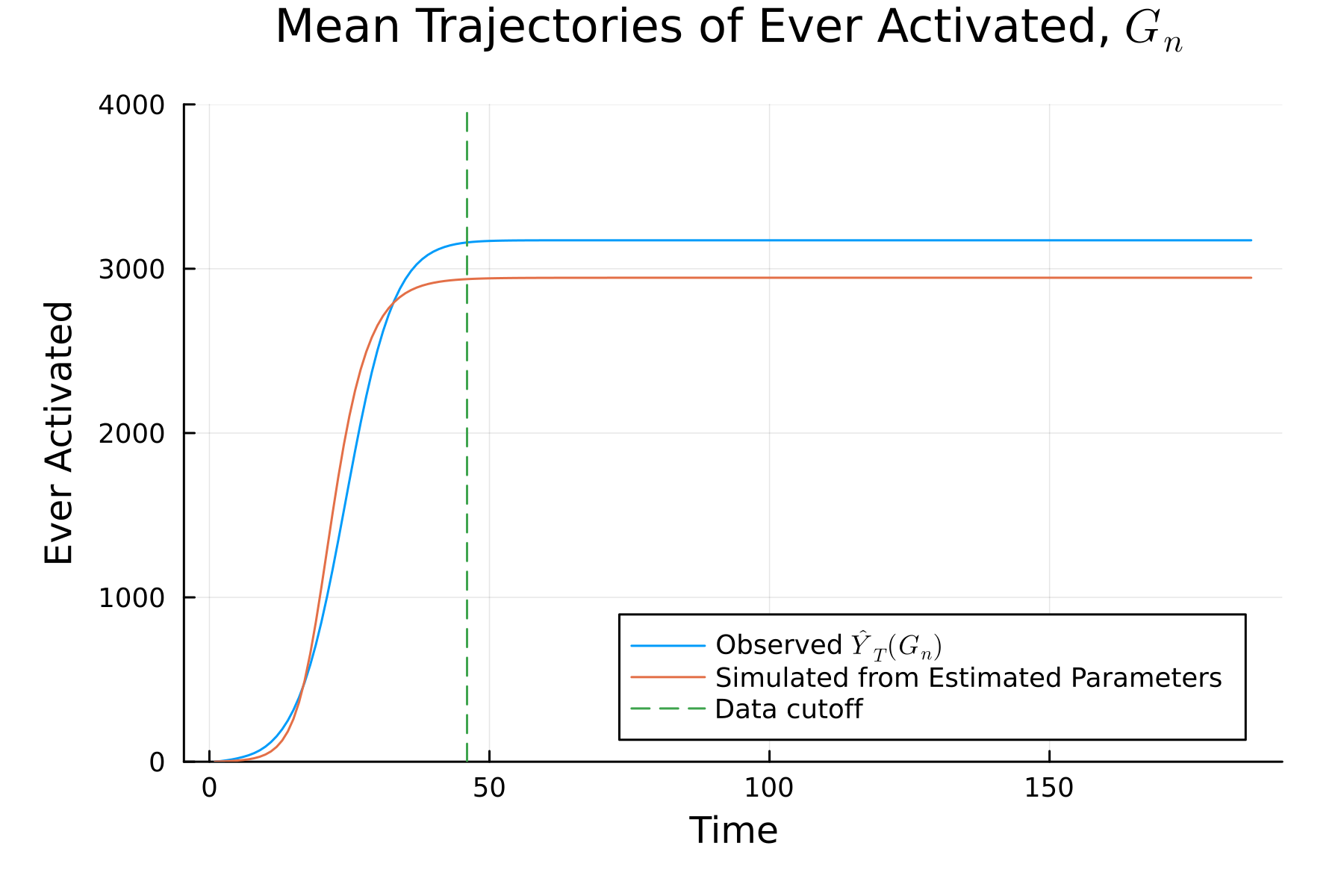

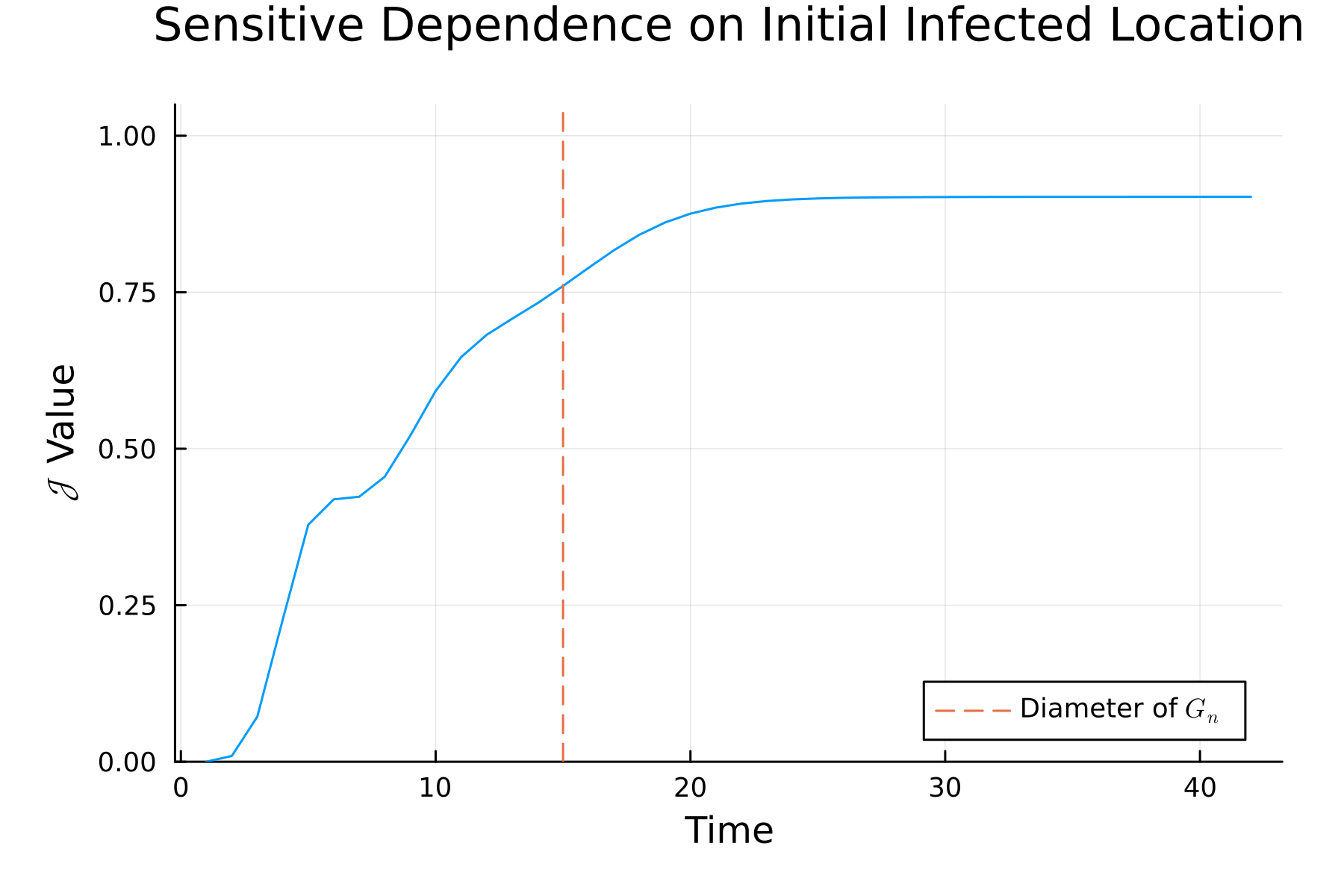

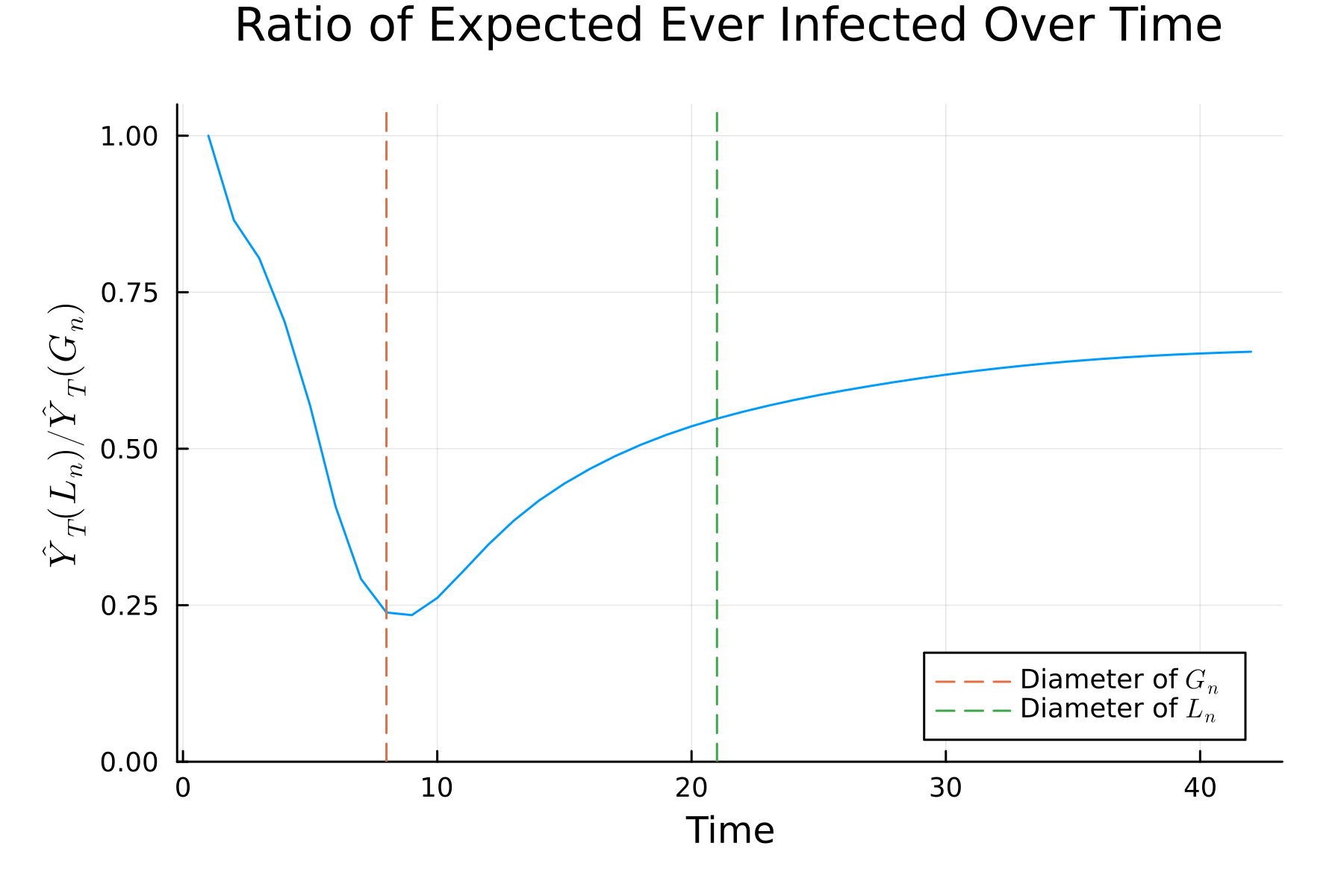

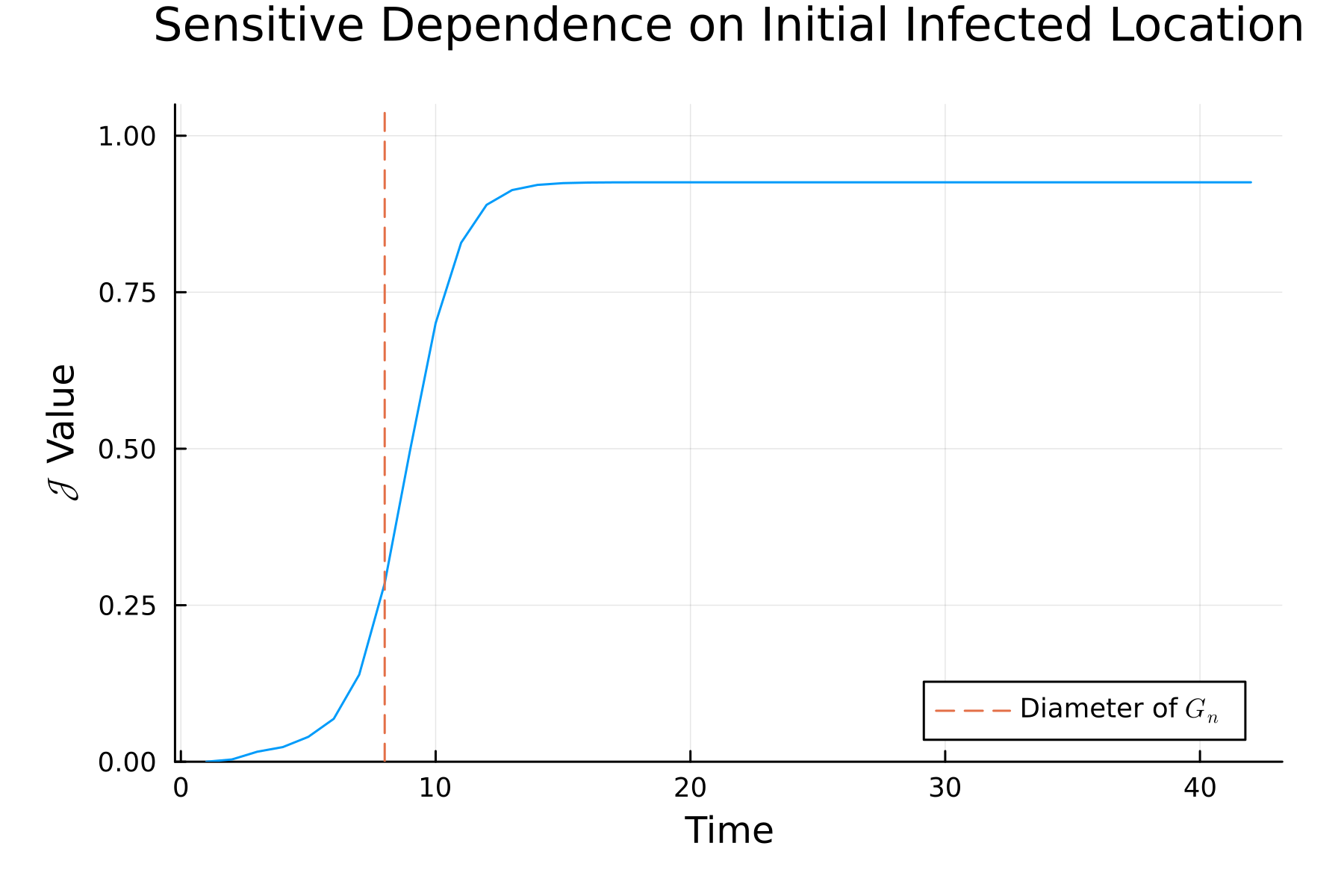

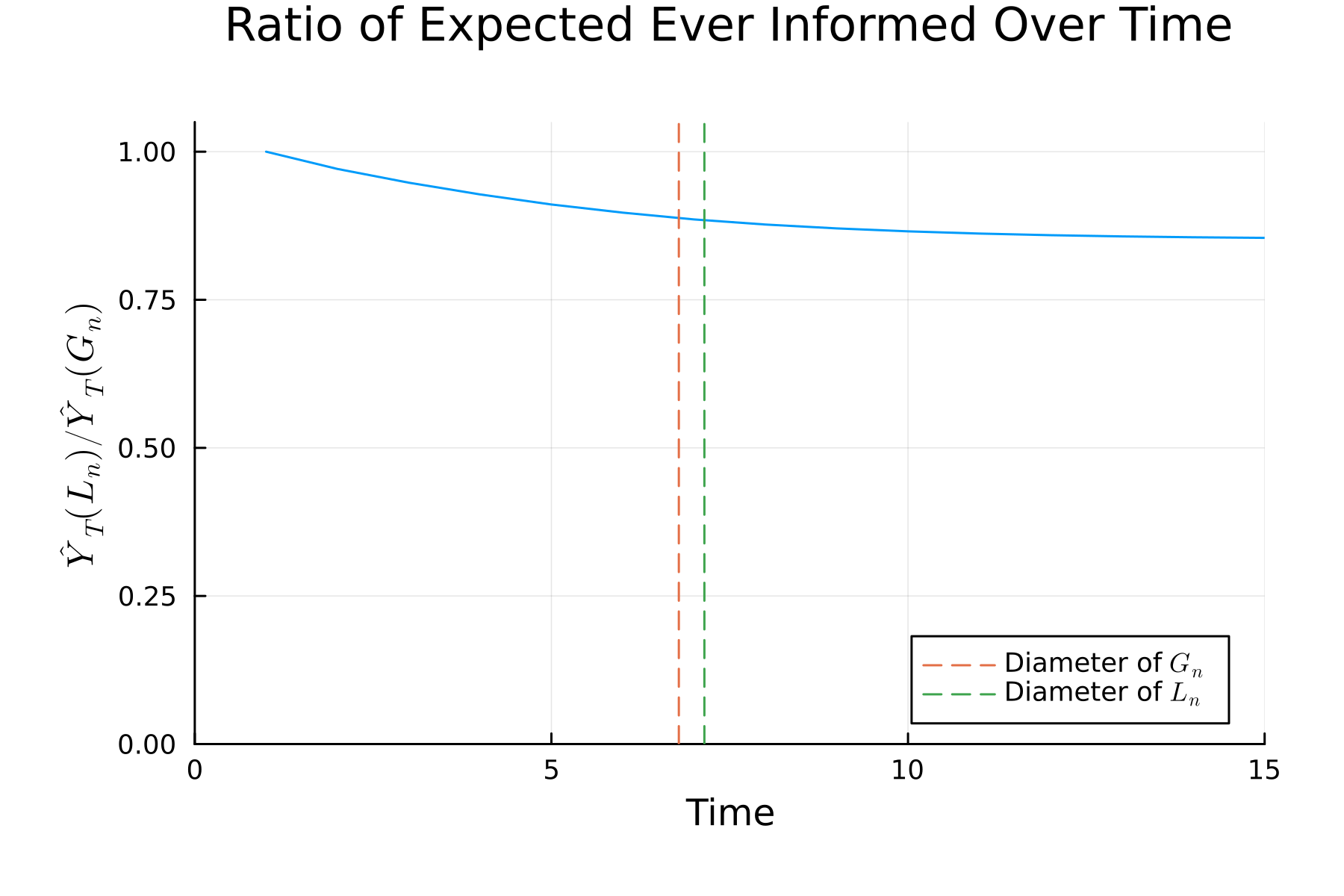

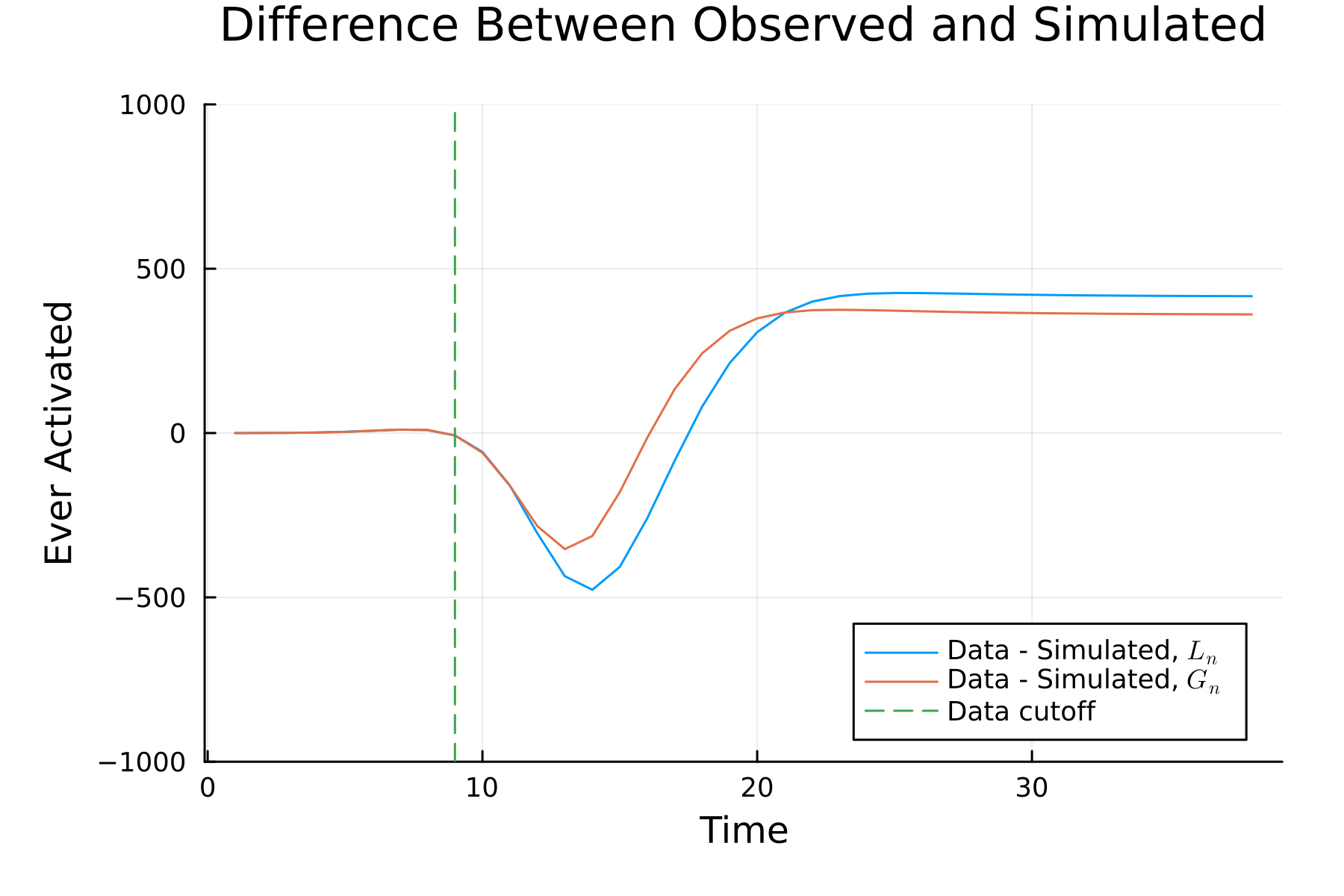

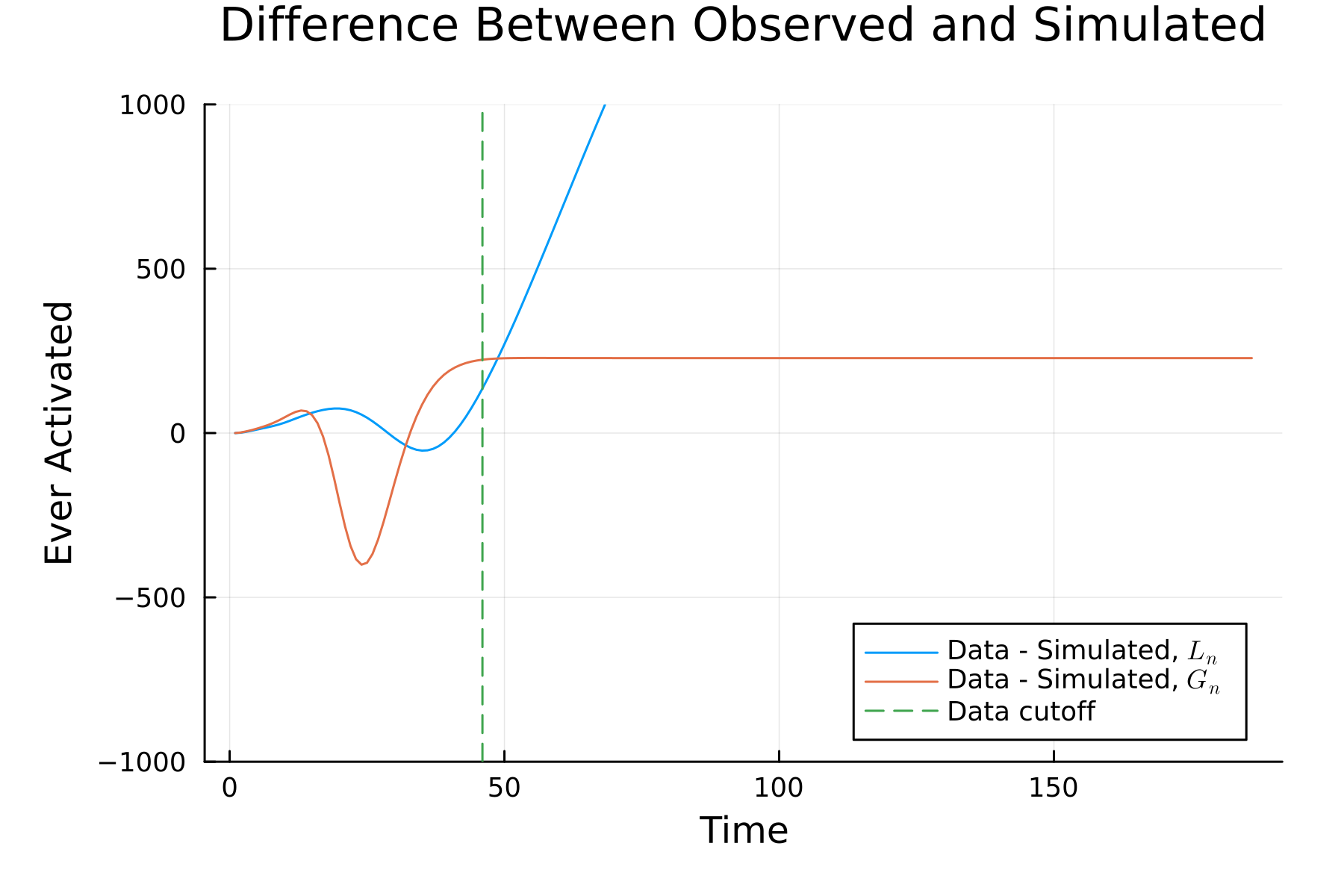

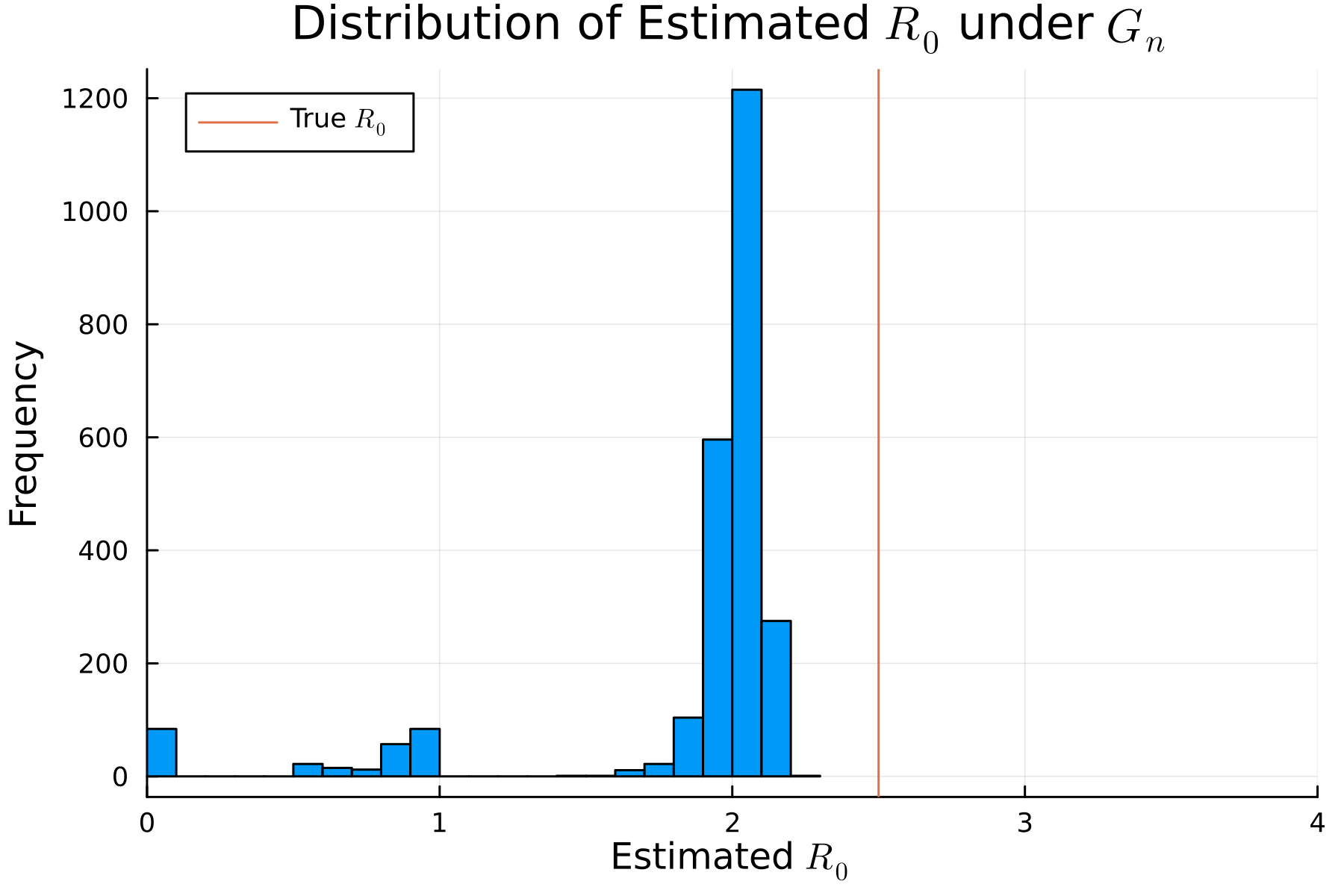

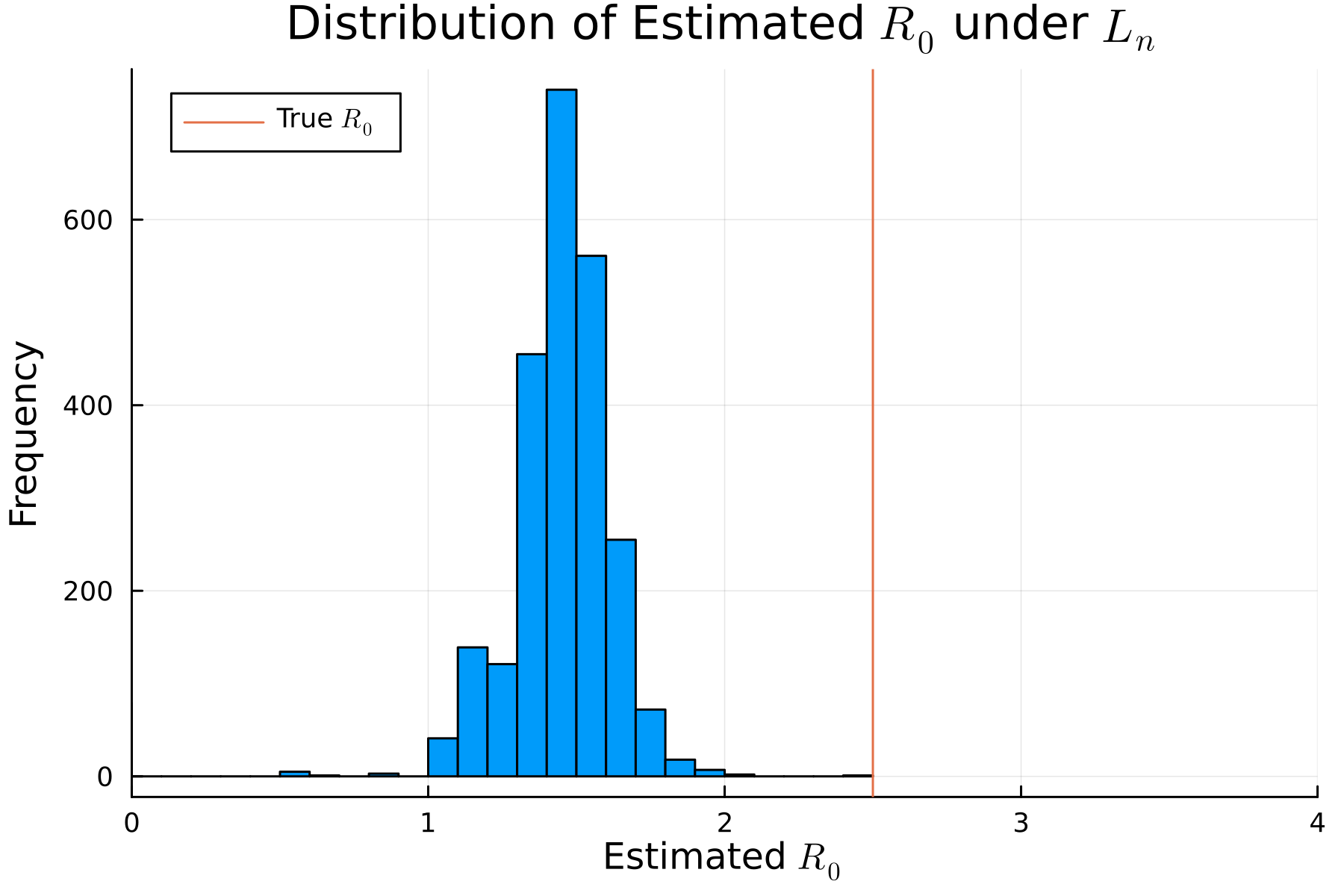

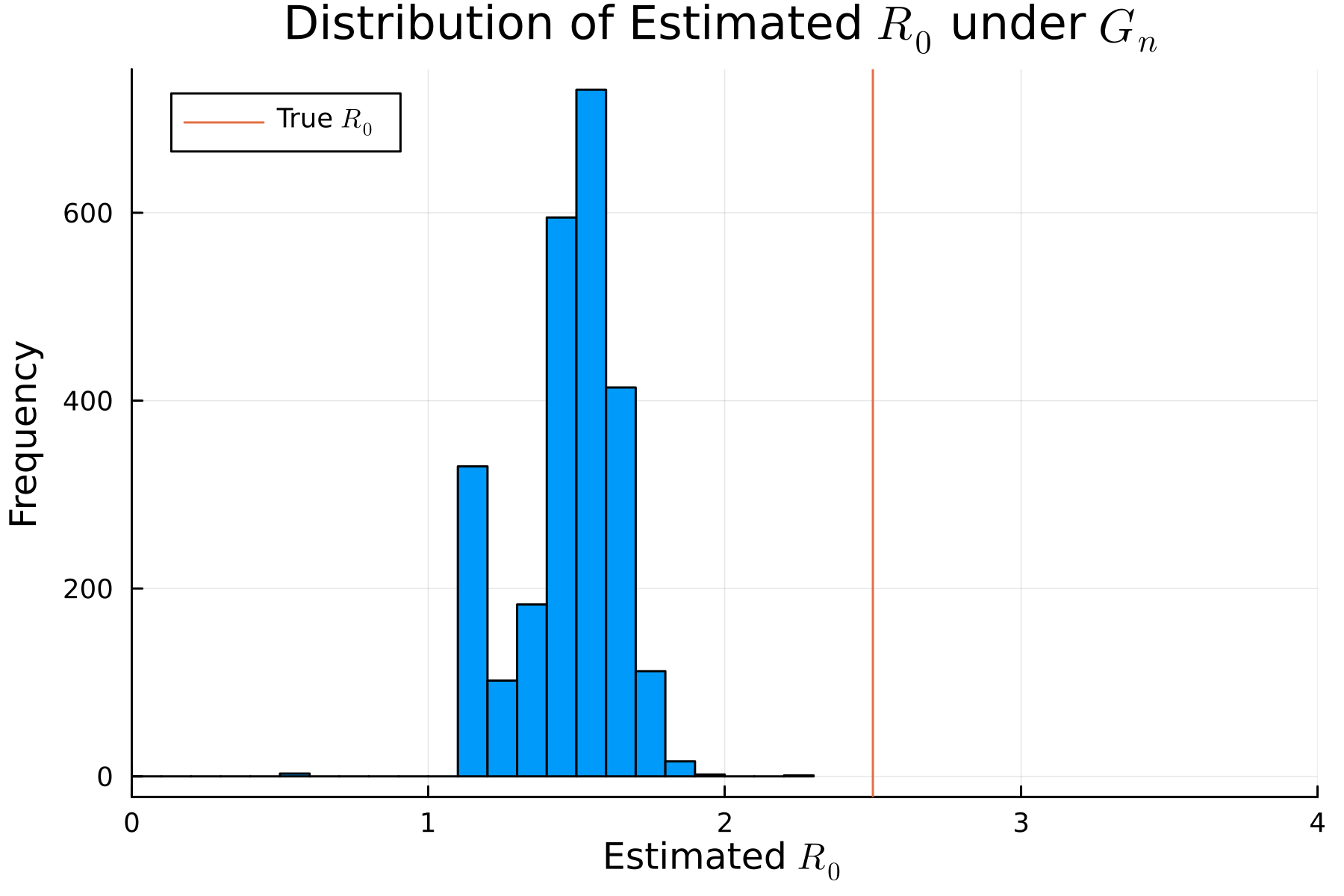

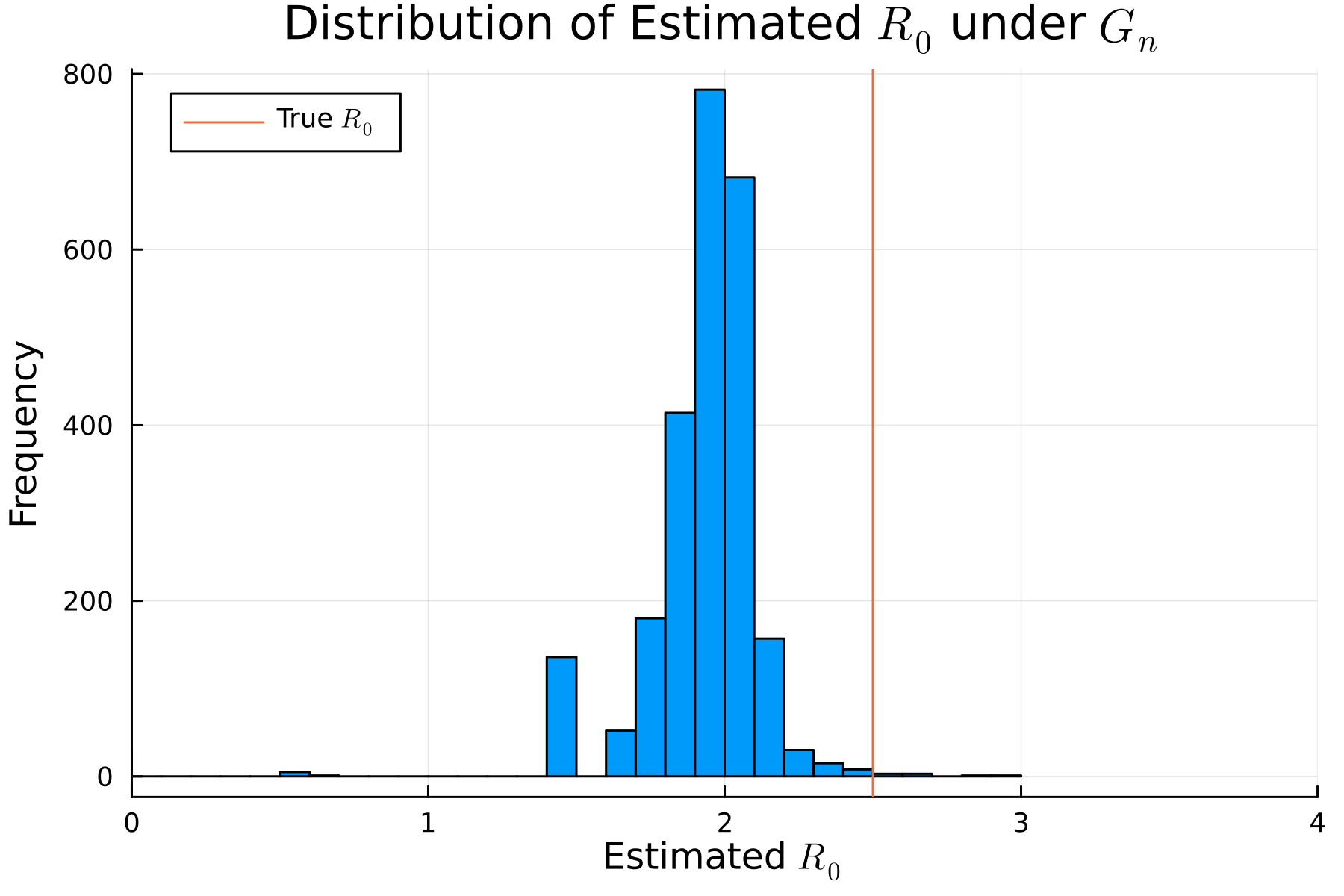

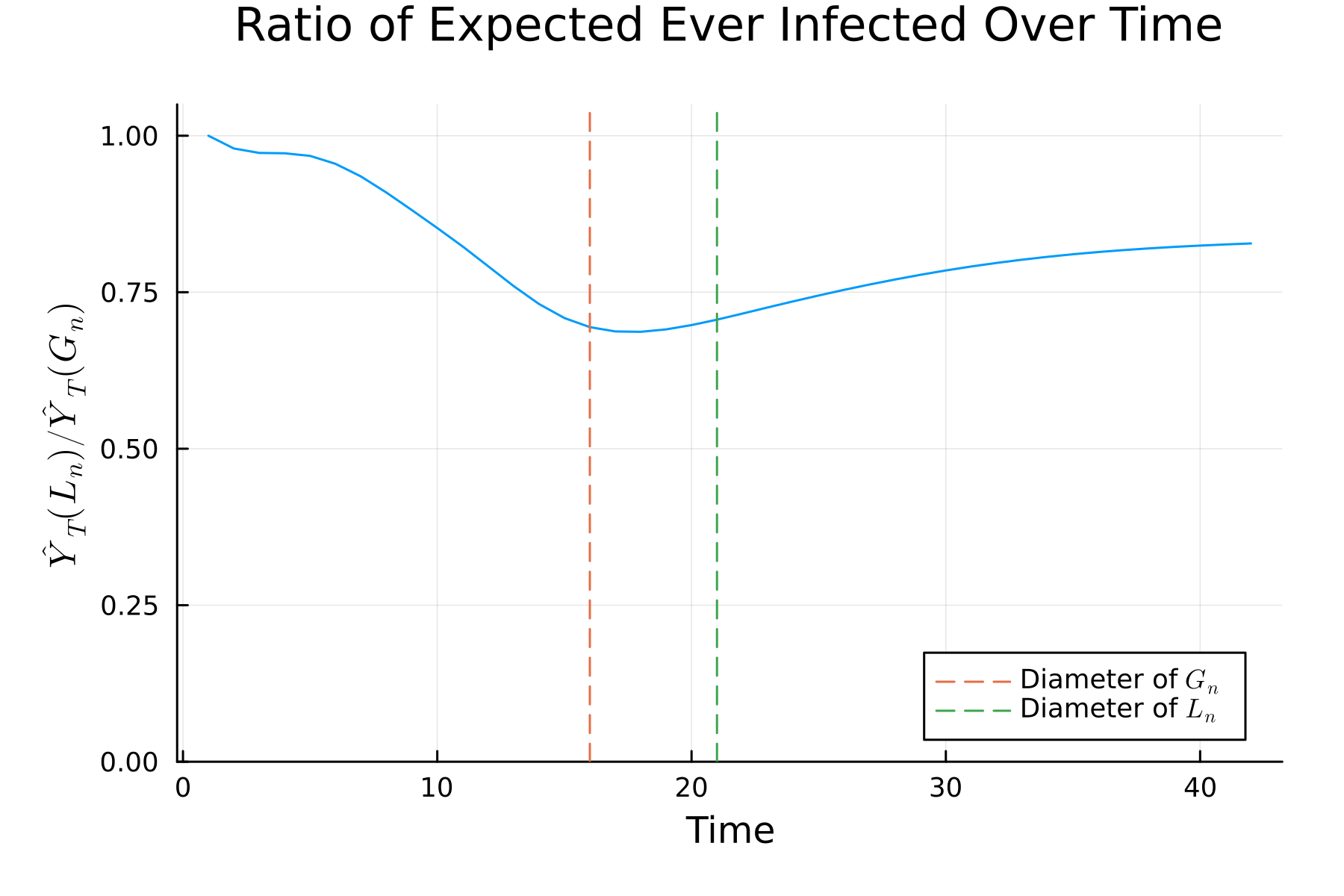

We begin by simulating a version of Theorem 1. To do so, we simulate the error network, , as an Erdos-Renyi graph with links that are i.i.d. with probability . We simulate 2,500 iterations of the SIR process on both the fixed and , with re-drawn in each simulation. We do so for the generated with both and . Average graph statistics for each are shown in Table B.1. Note that the degree distribution stays quite similar, as the average additional degree from is 0.100 for both sets of simulations. The initial seed is chosen uniformly at random and held fixed throughout the simulations. We then compute the empirical analogue of , the ratio of the expected number of ever-activated nodes under each process.

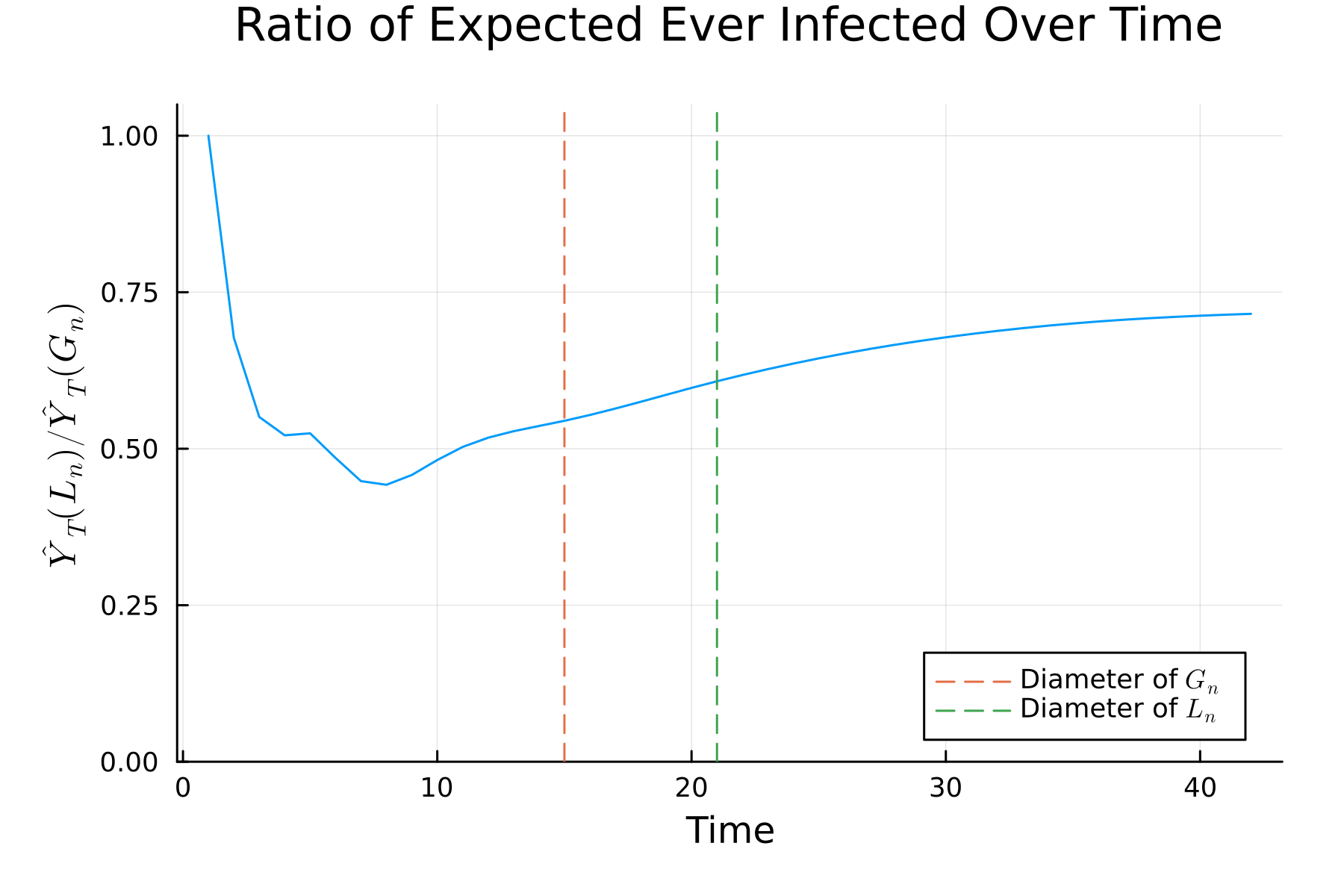

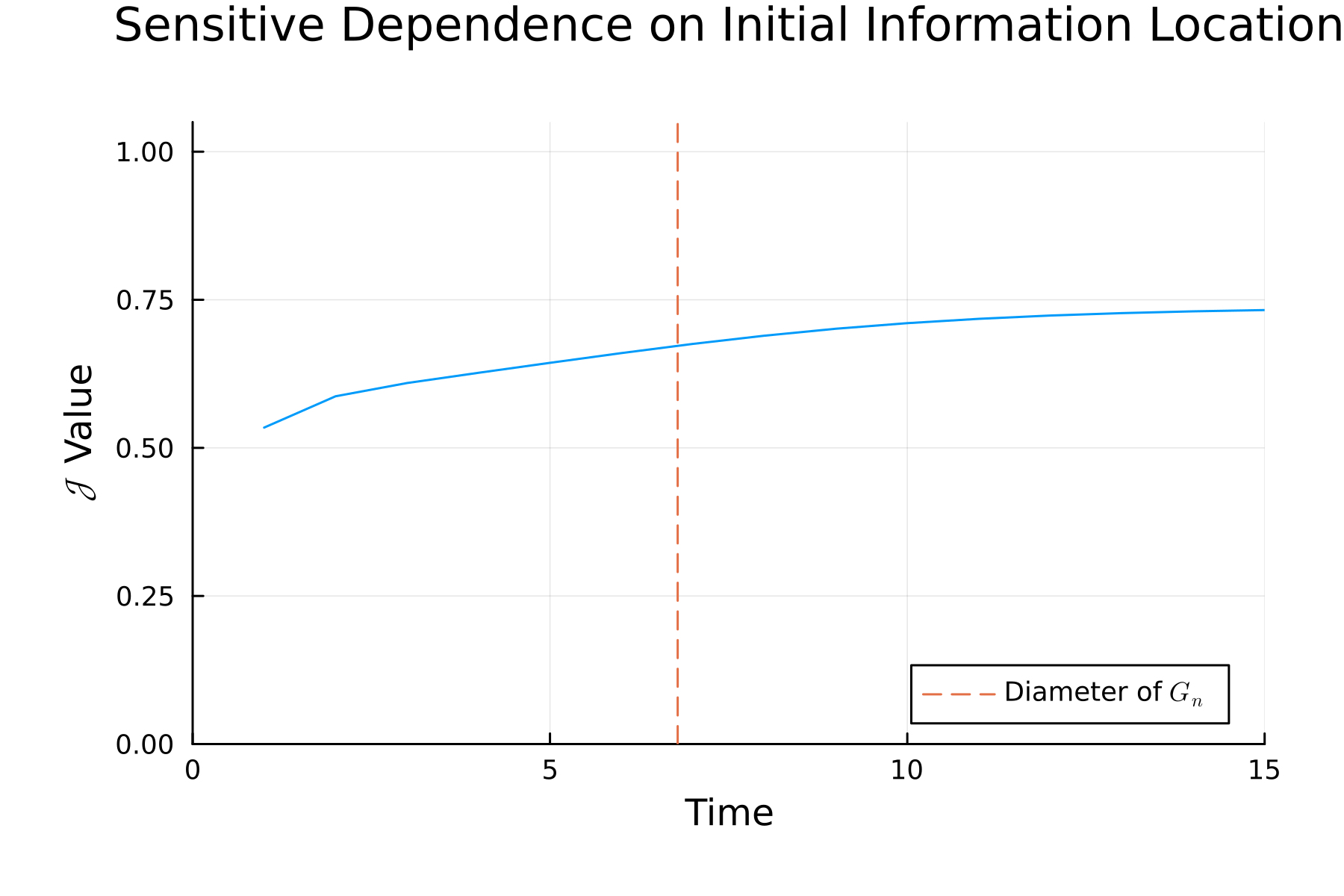

In Figures 3(a) and 3(c), we plot the simulated values of over time for each graph. For , the minimum ratio is attained at with a value of , meaning the policymaker would underestimate the extent of the diffusion by 22 percentage points. Once the diffusion on reaches the diameter of the graph, the ratio increases towards a value just below one. For , the minimum ratio is attained at , taking a value of . With a lower-dimension diffusion process, the simulations are much more sensitive to additional links in . In the Appendix B.6, we show that with and , the minimum ratio of is still much smaller than the values attained with . The shape of the curves in Figure 3(a) and 3(c) are similar to our theoretical results, since our results focus on asymptotic results where the diffusion cannot reach the edge of the network. Hence, the ratio in our theoretical results will continue to decline. Appendix Figure B.1 shows exactly this phenomenon by separating the ratio into separate curves for and – the separation between the two curves is maximized just after the diameter of is reached.181818Note that the ratio asymptotes with to a value just below 1, as the additional links in allow for there to be more overall activations in expectation than in . Consequentially, the decline in the period prior to reaching the diameter of lines up exactly with the results anticipated by Theorem 1.

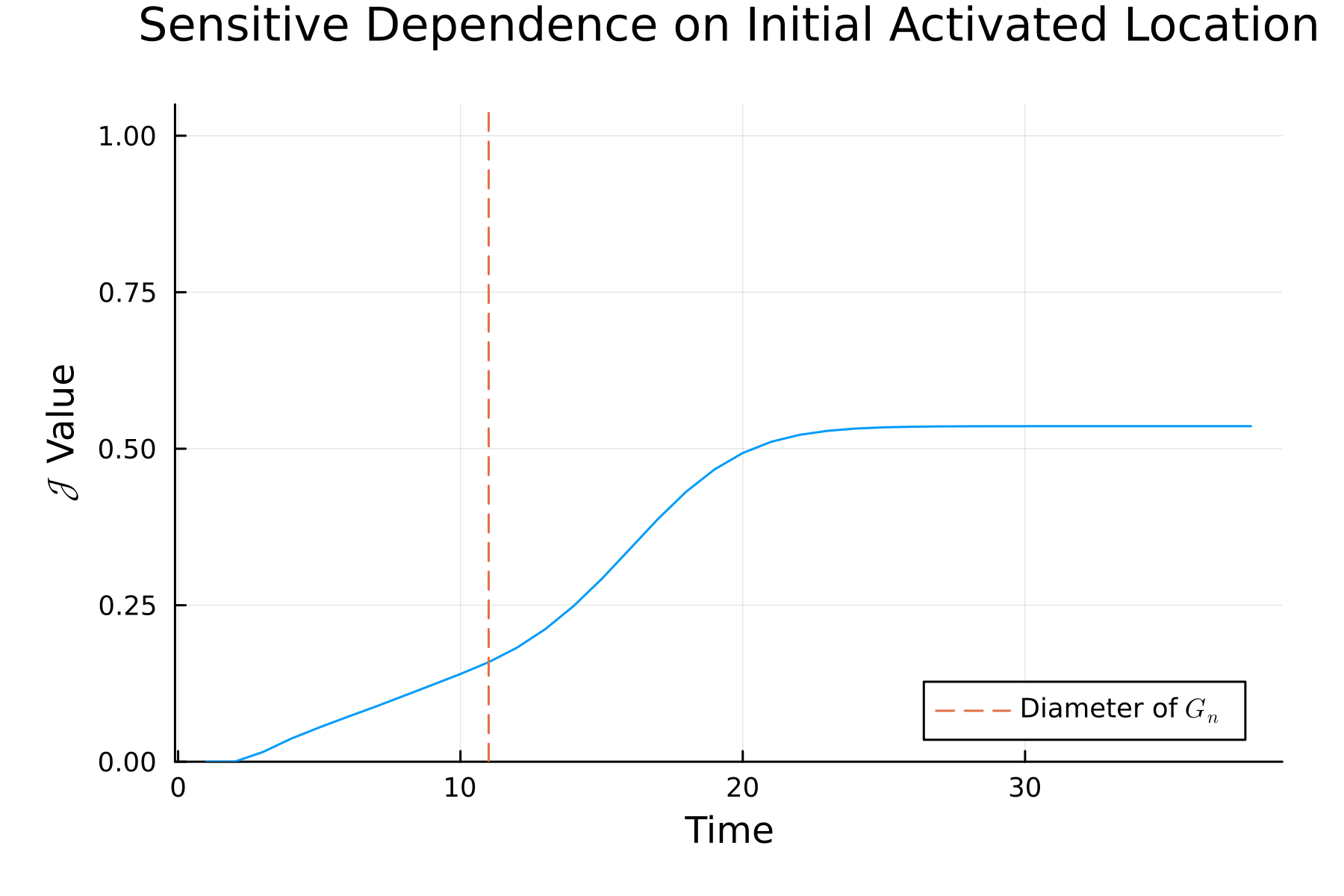

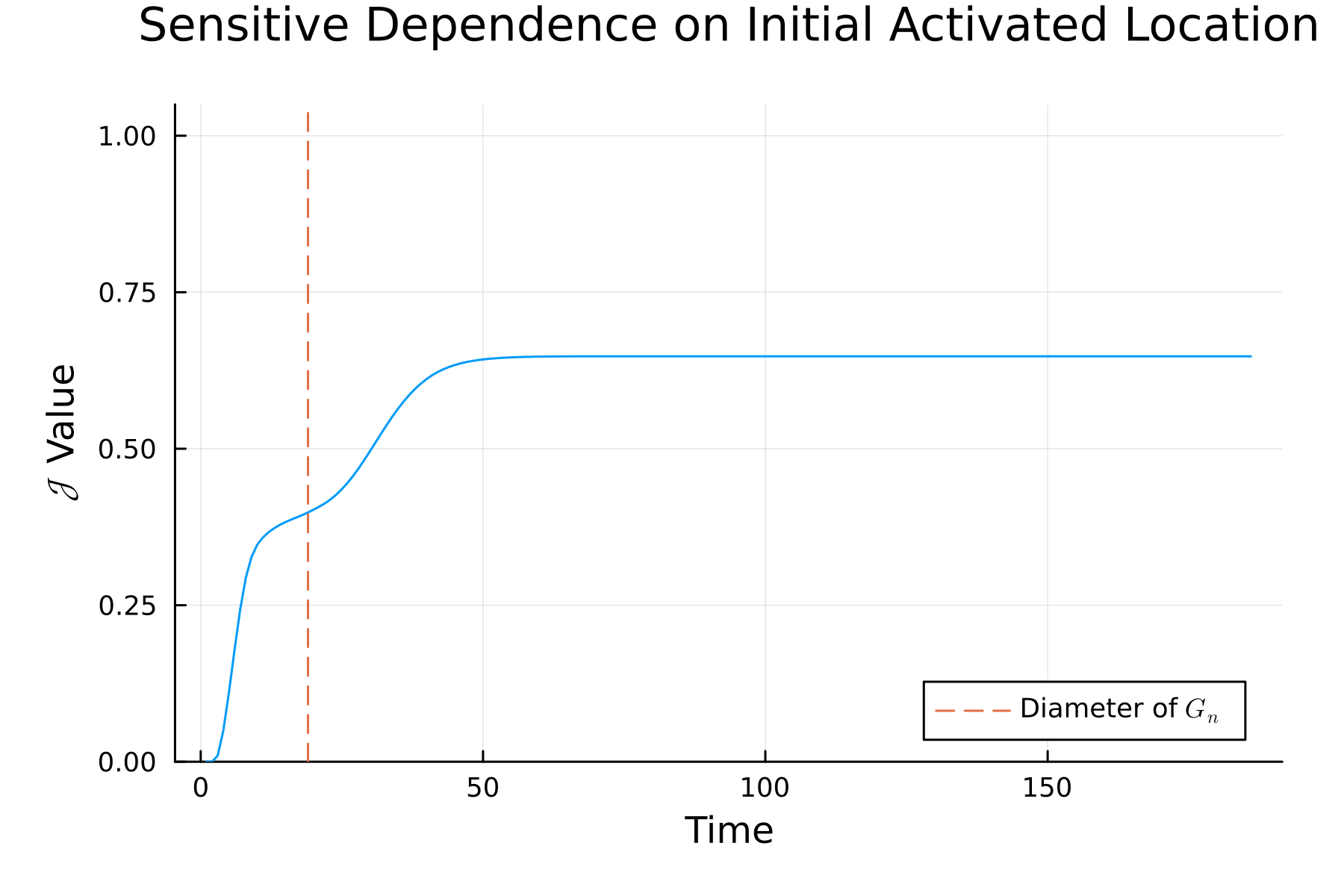

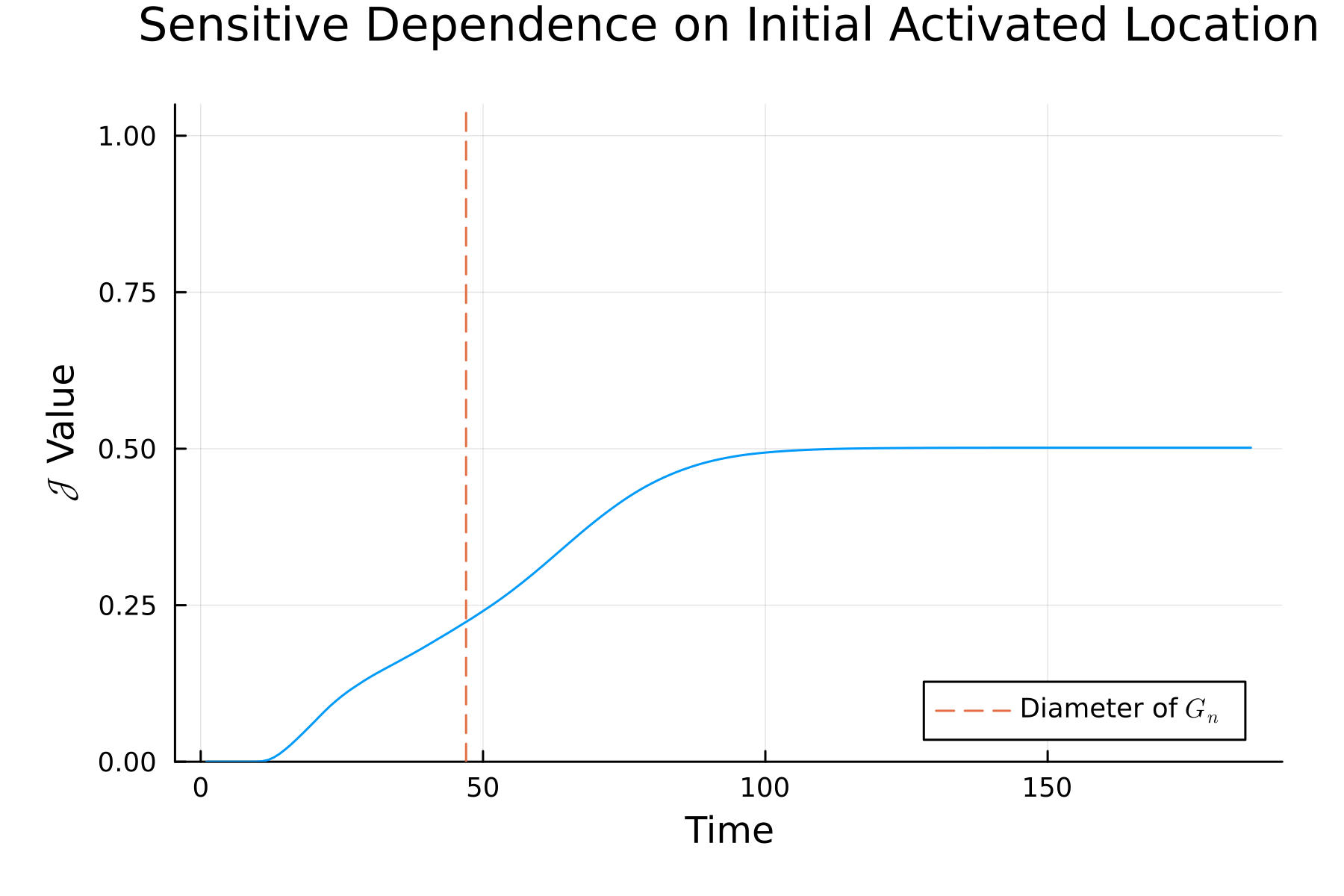

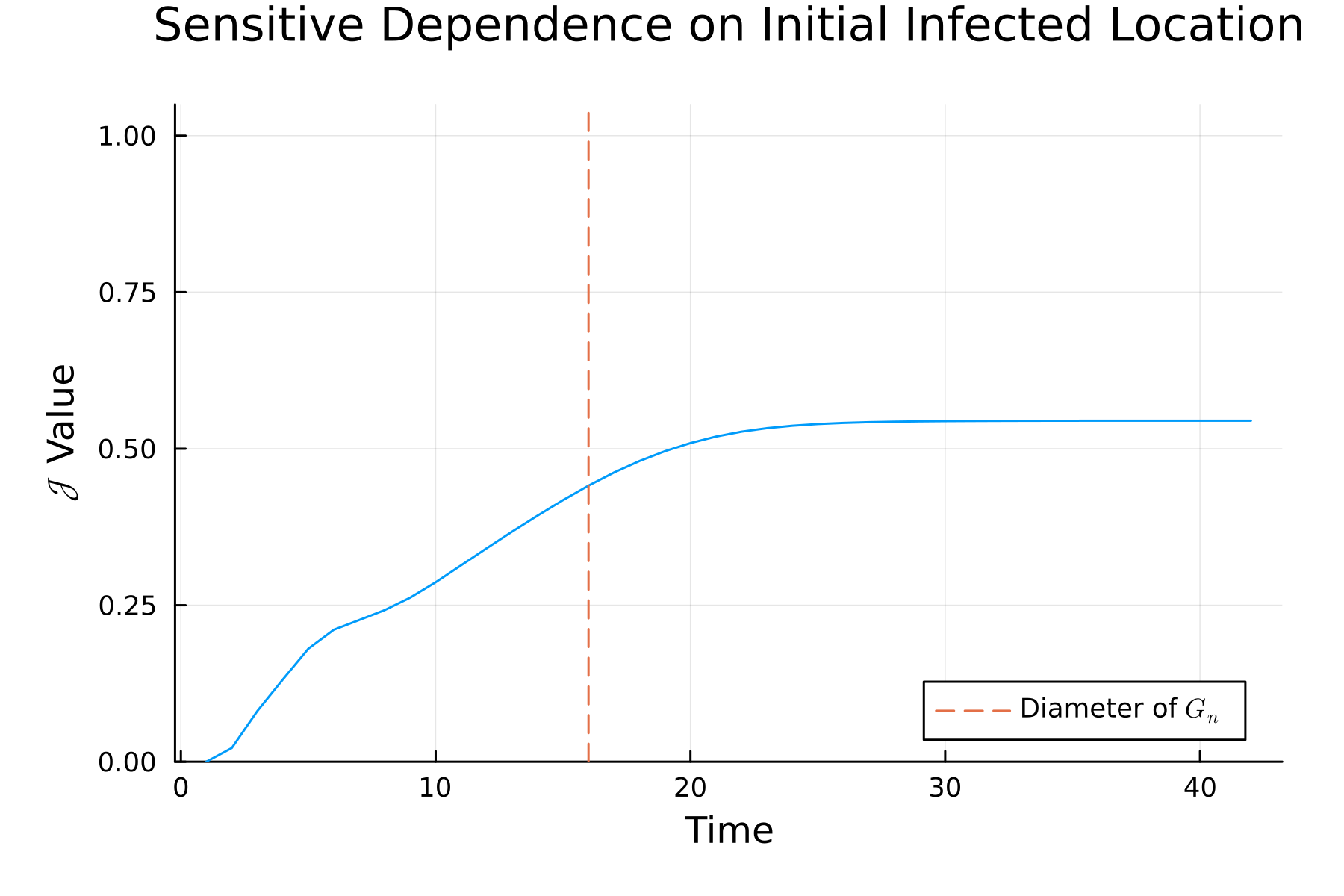

Next, we investigate Theorem 2 in simulation by looking at a perturbation of an initial seed within a local ball covering 1-5% of the overall number of nodes. We fix and a particular instance of to form , and set as the center of the lattice. Then, we construct , the set of possible alternate seeds, and choose a uniformly at random. To construct , we first find the depth of the second closest links in to – call this distance . Then, nodes are included in if they are at distance from . Empirically, for , meaning that the distance from to is 3. The local neighborhood around , (which contains all nodes at or within distance ) of this size makes up 5.3 percent of the total nodes in the graph, while makes up 64.6 percent of the local neighborhood. For , the distance from to is 4, while the local neighborhood of this size makes up 1.05 percent of the graph and the set of make up 31.0 percent of the local neighborhood.

To approximate , we fix the underlying percolation as in our theory and examine the set of ever-activated nodes infected by an epidemic that begins from and . We exploit the connection between percolations and the one-period SIR process, predetermining which links in the network will transmit. However, we do not condition on the event that there is some overlap between the diffusions (in Theorem 2, this is encoded in the object and is assumed). Therefore, when considering , the denominator can be equal to zero and thus the quantity may not be well defined. To avoid this denominator issue, we instead consider the following measure. Recall that is the set of ever-infected nodes from a diffusion started at node at time . Then we define:

Note that this re-arranges terms from – the key difference is that when is closer to 1, quantity will be close to 0. However, both measure the notion of overlap between diffusions. Note that here, we take expectations only over the percolation on , meaning we generate a single draw of and then hold it fixed. We simulate the process 2,500 times, and then take the average over simulations at each time period to get . Results are shown in Figures 3(b) and 3(d).

Figures 3(b) and 3(d) indicate that there is generally little overlap between the diffusions until the process has reached the diameter of the graph and saturated the network. Recall that when is close to zero, this implies that the share of nodes that would be activated by both starting conditions as a share of the total activations is small. Hence, this implies that the activation paths are following very different portions of the network. This lack of overlap is despite the fact that and are extremely local. For , at (the halfway point to the diameter of ), the value of indicates almost entirely distinct processes. For , at (again half of the diameter of ), the value of . These results are consistent with the theoretical results: there exist time periods early on in which the diffusions are almost entirely disjoint. Empirically, these results demonstrate that the diffusions remain disjoint for a relatively long period of time.

While it is clear that our simulations are highly sensitive to measurement error, regardless of whether or , the changes in sensitivity are instructive. Comparing to , the simulations demonstrate that the diffusion process is much more sensitive in terms of the extent of diffusion with lower dimension, rather than the location. This is because ensures that a greater fraction of connections are “local” – therefore, there can be less local perturbation. However, i.i.d. connections lead to many more activations. Nonetheless, we note that there is still severe sensitive dependence on initial conditions with – in the short run only a third of the diffusion overlaps on average.

6.2. Aggregate Patterns Are Well-Approximated by Compartmental Models

Next, we study the approximation of the diffusion process by a standard differential equations SIR compartmental model. In practice, diffusion occurs between a discrete set of agents and transmission occurs over discrete time. The compartmental differential equations model simplifies matters by using a mean field approximation, but there is a potential for error which we now explore.

We assume that the econometrician fits the following model to data which is generated by a diffusion on . Let , , and be the susceptible, infected, and removed nodes at time . Then the change in each quantity at time will be given by:

where and are parameters to be estimated using the diffusion data through some time period . Note that .

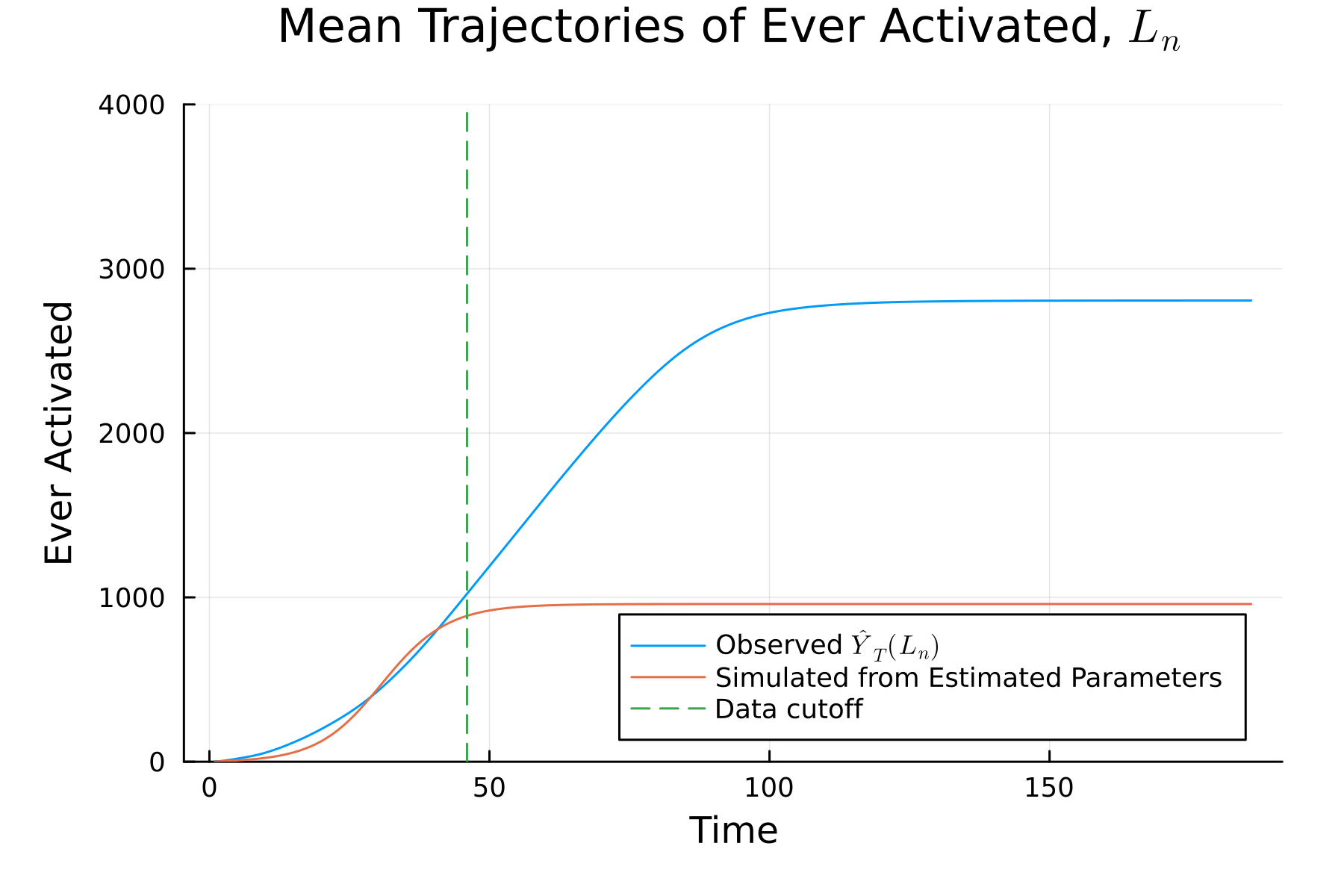

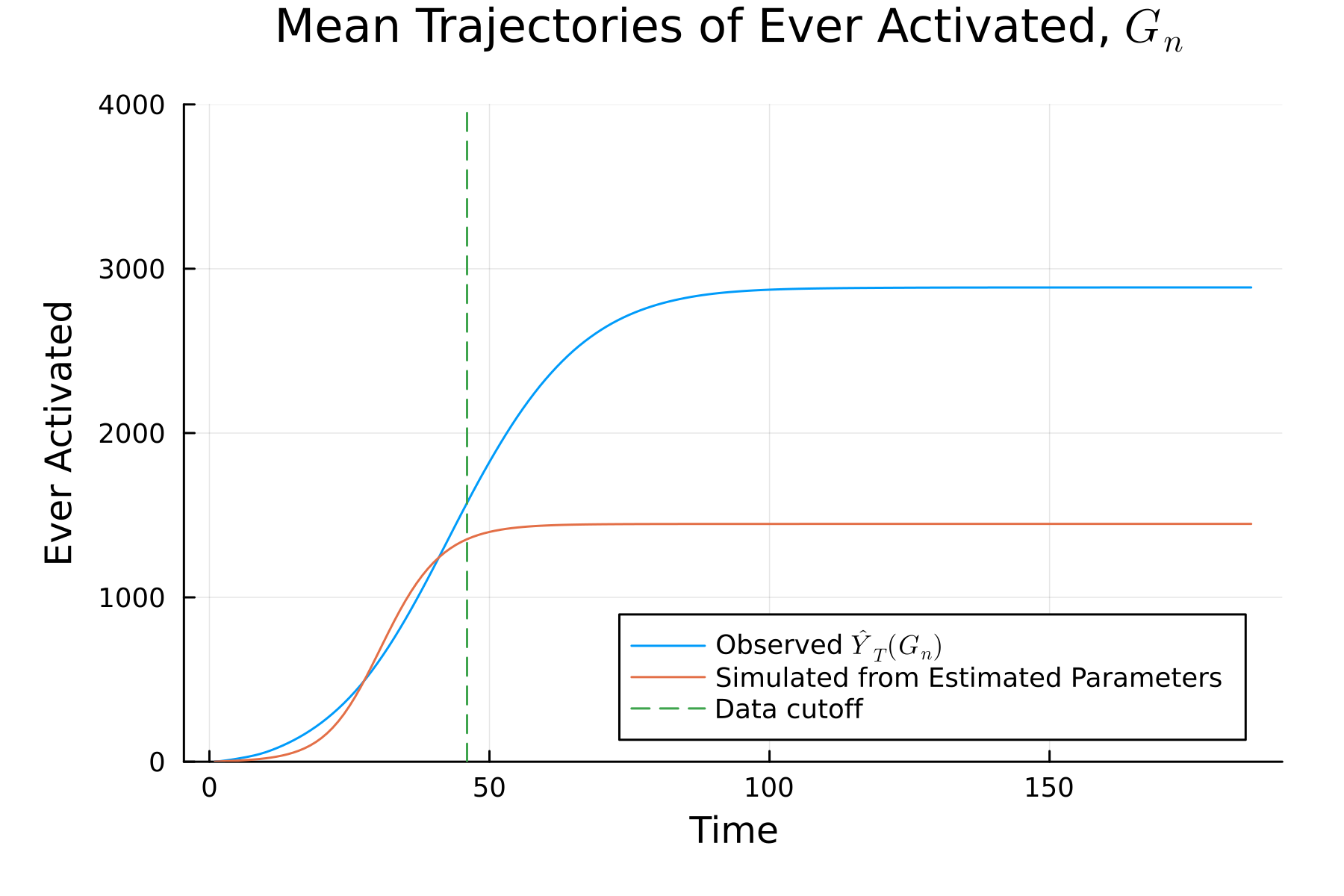

We conduct two exercises. In the first exercise, we simulate a diffusion process on for periods. We then estimate the parameters of interest, ( at and we generate forecasts from the compartmental model. We compare this to the actual diffusion trajectory. The second exercise replicates the first, with the only change being that we simulate the diffusion process on instead. Note that this is not what generates the diffusion process in the “real world”—that is diffusion on . However, together the two simulations capture two features: (a) the deviation of the mean-field model from the underlying discrete process and (b) how the deviation depends on the relative structure of to . We repeat both sets of simulations for both and .

In practice, we run a number of simulations in each configuration. We then fit for each simulation draw and then average them to produce forecasts which then can be compared to and (both of course averaged over simulation draws) which we then print below. Details are given in Appendix B.5.

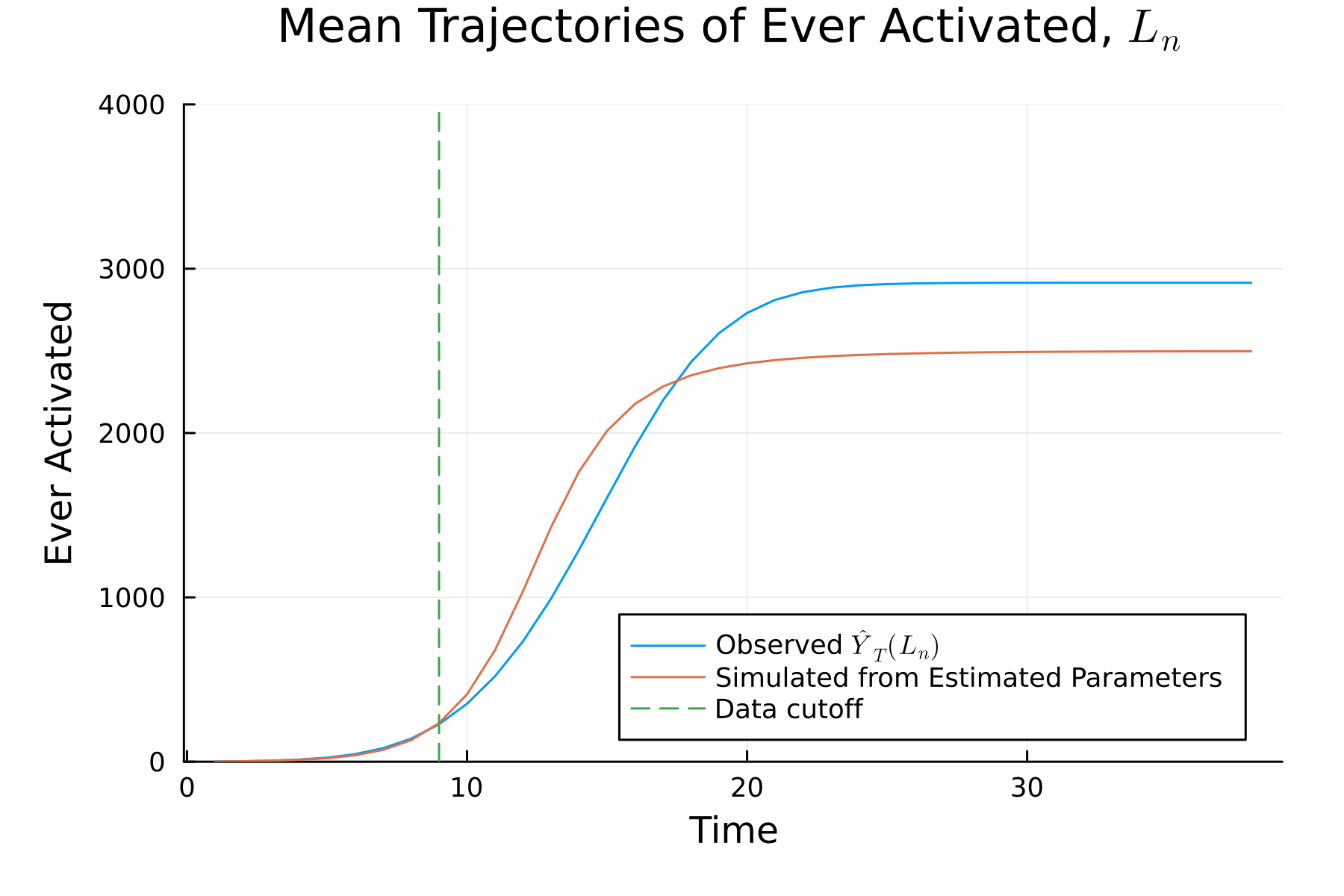

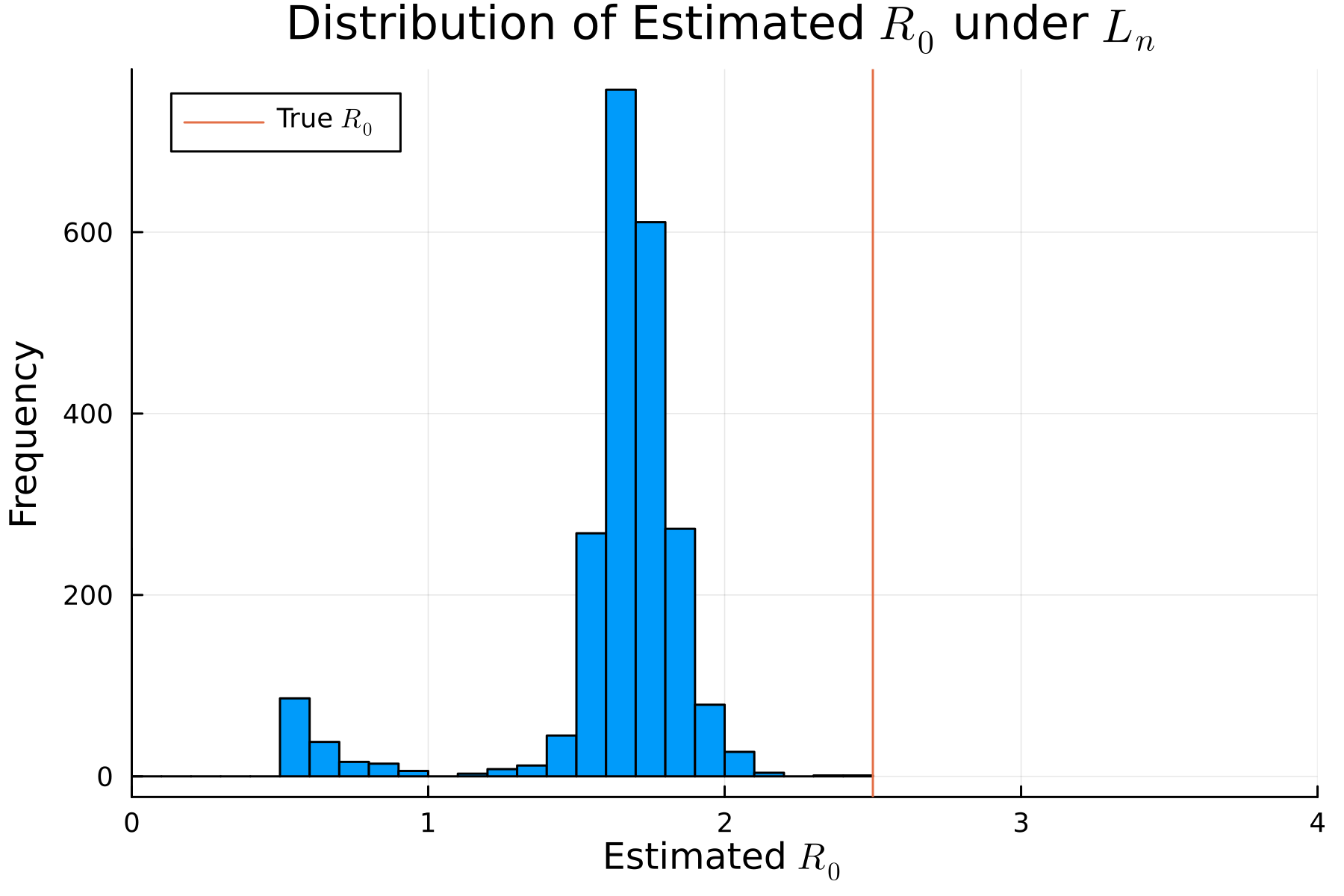

Figure 4 presents the results. We begin with and it is helpful to look to the diffusion on first in Panel 4(a). Recall that this shows how well the mean-field approach captures the dynamics on a hypothetical network structure ignoring links in . In the periods where the SIR process is fit to the simulated data, the fit is very good. The estimated , derived by taking the average across simulations of , is 1.46 under , well below the true of 2.5. Note that while Lemma 1 implies that there exists a consistent estimator of , the estimator we propose in theory uses activation-level data. Here, we base our estimate of using the aggregate diffusion pattern. The estimated forecasts (in orange) diverge quickly from the true diffusion, . Because of the initially exponential growth structure of the compartmental model, early in the medium run it overshoots, though the diffusion saturates much earlier and in fact the overall diffusion count in the long run is underestimated.

That is, in sample, the compartmental model can be made to fit well, but with a lower growth rate for the number of ever-infected nodes. However, because of the lower implied , the compartmental model dramatically underestimates the total number of expected activations out of sample. Ex-post, a policymaker could fit this type of model and do extremely well, but it would not be helpful for predicting the future trajectory.

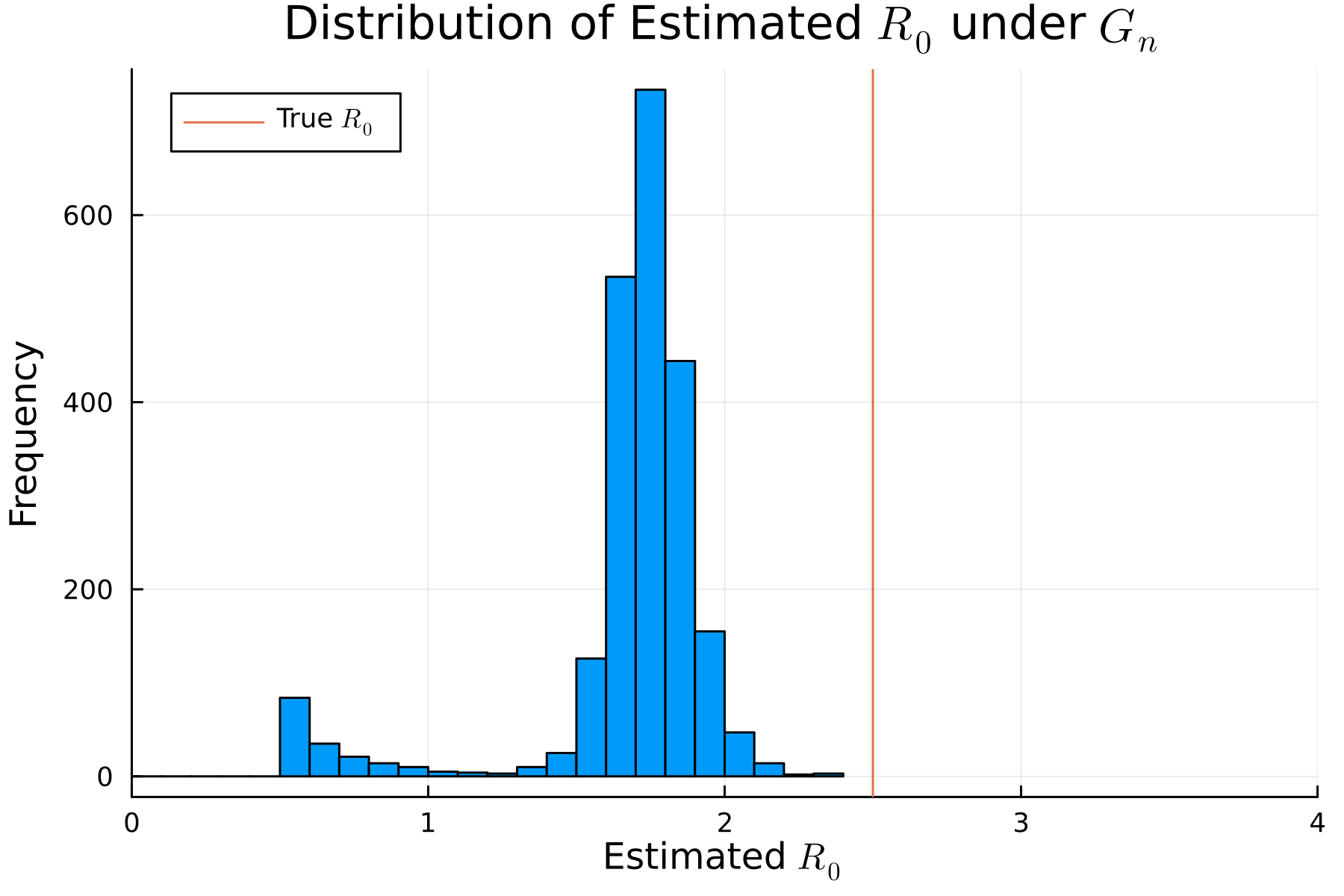

In Panel 4(b), we turn to diffusion on . The estimated , derived by taking the average across simulations of , is 1.52 under , still below the true of 2.5. We find very similar results as the case with . The principle difference is that the idiosyncratic links, , generate a slightly closer forecast curve to the true trajectory. Also of note, the implied diffusions from the compartmental model on and are also similar. While the estimates are such that the historical fit is quite good, the exponential structure makes the process run too fast and then fade too early as well, relative to a slower more persistent polynomial process (which of course could be historically fit by looking backwards).

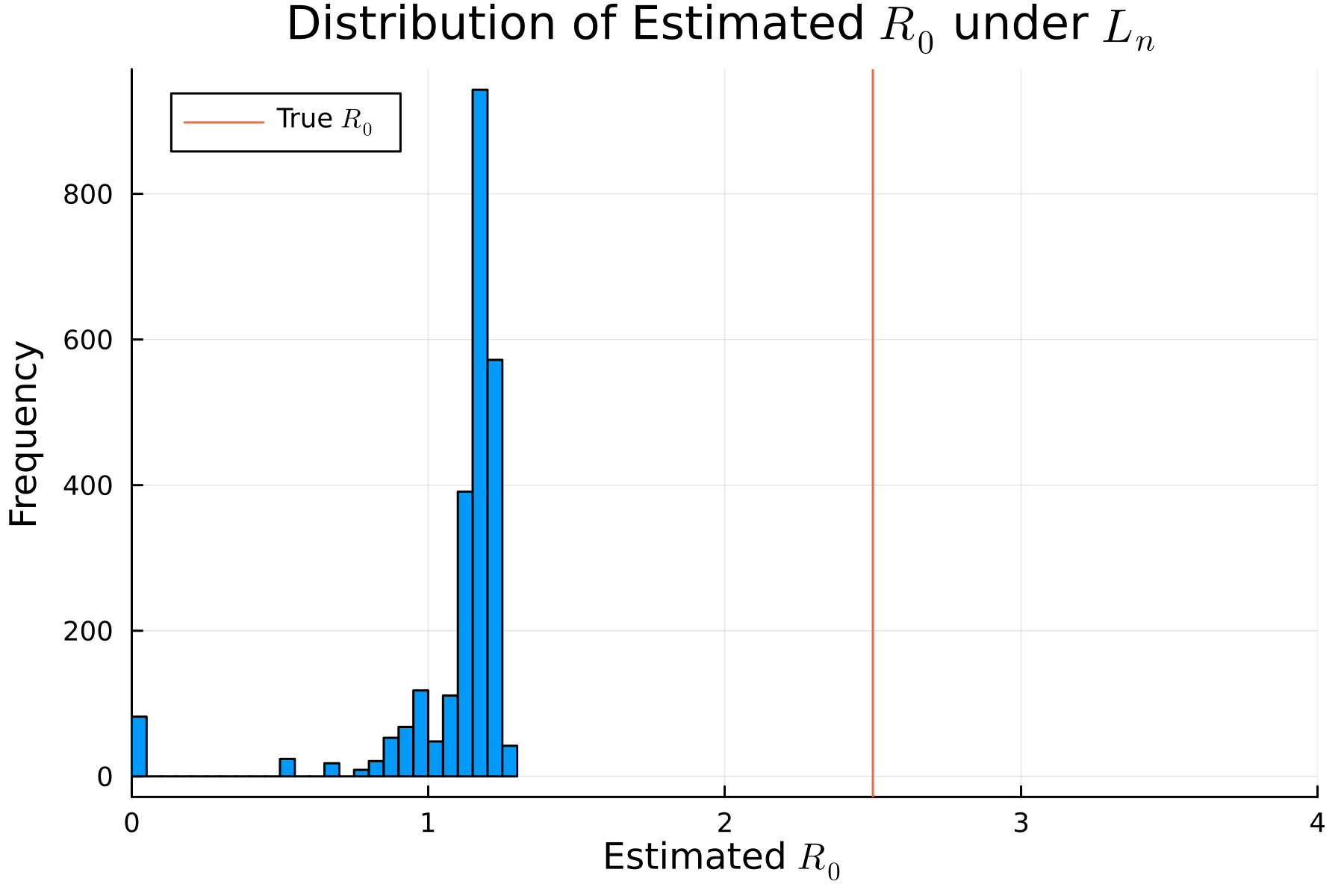

For , there is a shift between and . With and , as seen in Panel 4(c), the process cannot be well approximated by the model. The fitted compartmental SIR looks almost nothing like the true trajectory: while fitting to data the SIR model makes a complete “S” curve shape, it dramatically underestimates the total activations. Turning to the case, as seen in Panel 4(d), the compartmental SIR model is able to match the data more closely, because the diffusion moves much more quickly.

In sum, a compartmental SIR model can, in many cases, be fit well looking backwards to a polynomial diffusion process. This fit is even better the higher the dimension of , as it admits more expansive balls. But in all cases, the compartmental SIR estimates to rapid a diffusion that saturates and then stabilizes too quickly: historical aggregate fits may be excellent and at the same time they may serve as poor forecast tools.

7. Empirical Applications

We now consider three empirical applications. The first examines the COVID-19 pandemic, which showcases our results in a large scale setting. In addition, it demonstrates how only local linking can still cause errors in diffusion – though we show that the problems are much worse in the idiosyncratic case. The second example studies mobile phone marketing in India, which showcases our results in a much smaller scale setting. Here, sensitive dependence on initial location has much more dramatic results – volumes of diffusion are more robust in this setting, because the networks themselves are much smaller. Finally, we consider the diffusion of a weather insurance product in China. Here, we consider how errors in a diffusion model could impact statistical power when estimating peer effects.

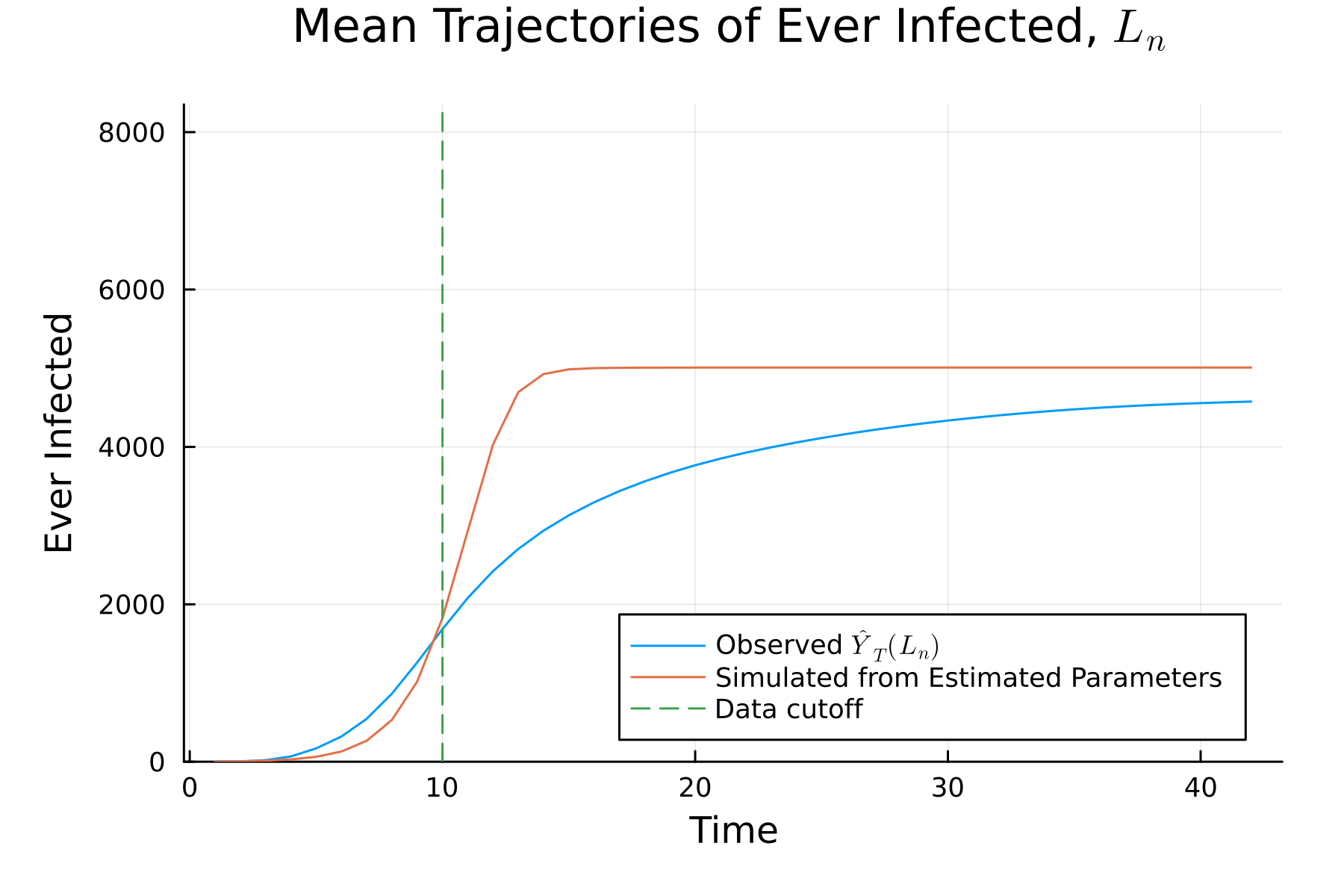

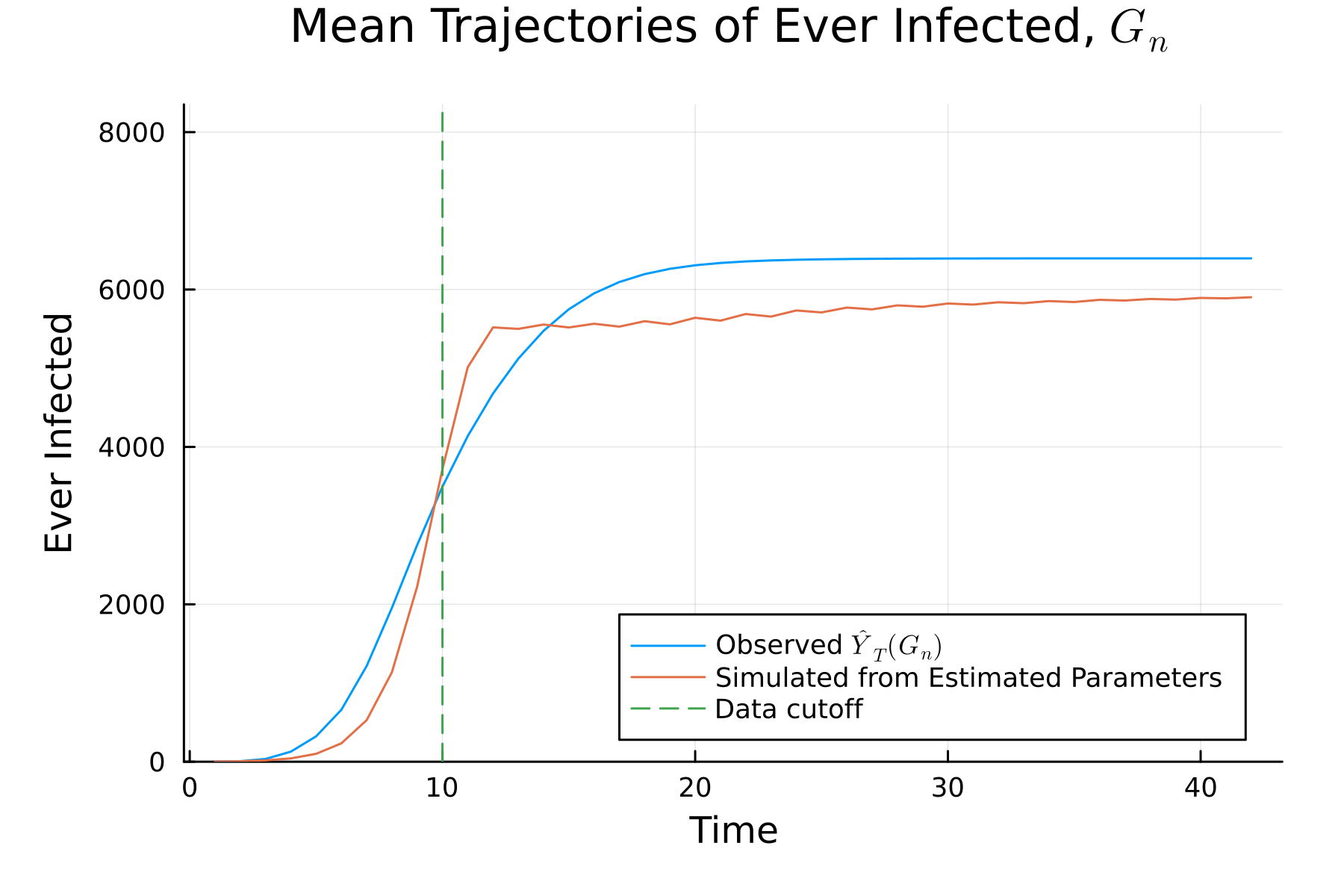

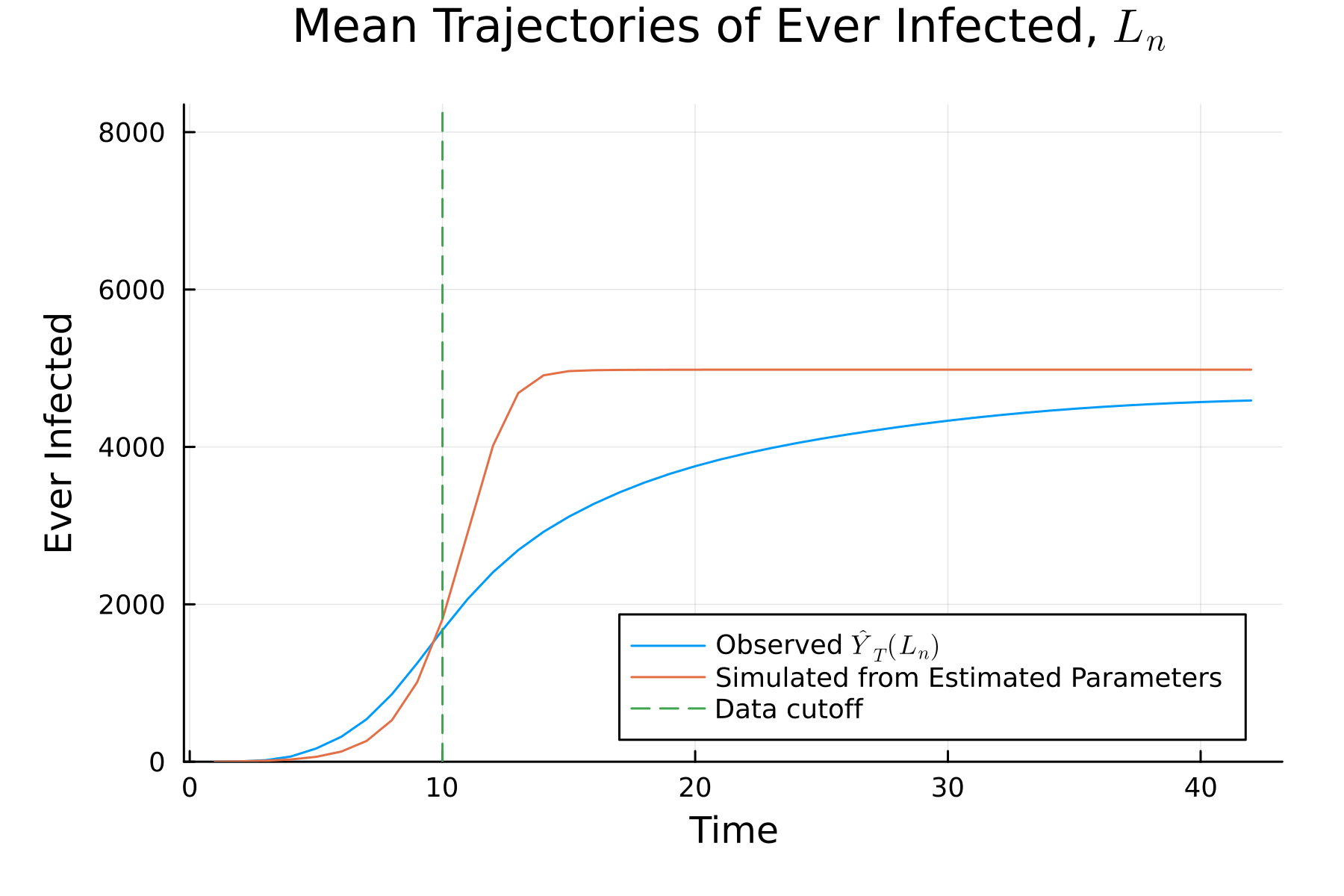

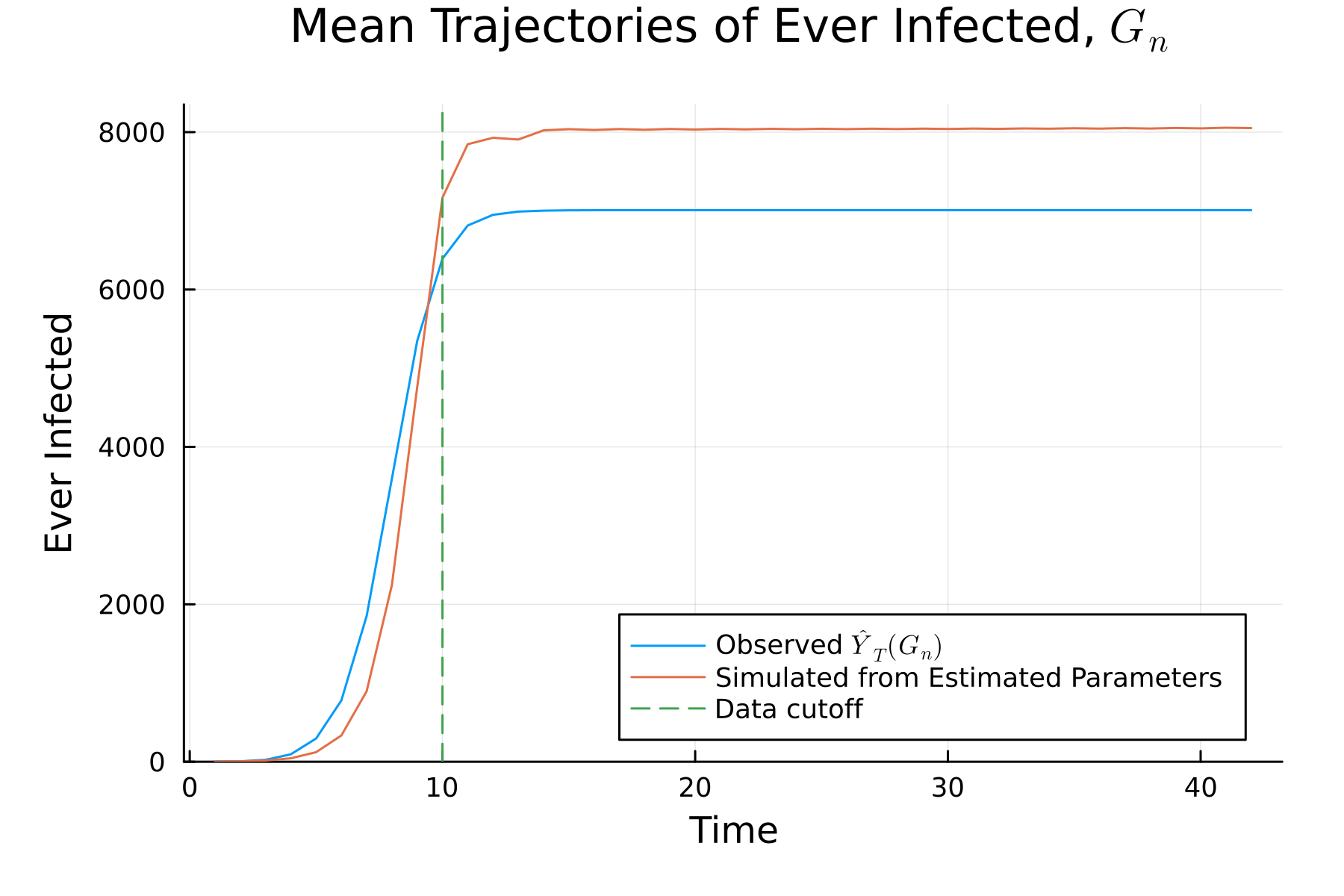

7.1. Data from the COVID-19 Pandemic

Kang et al., (2020) introduces a dynamic human mobility flow data set across the United States, with data starting from January 1st, 2019. By analyzing millions of anonymous mobile phone users’ movements to various places, the daily and weekly dynamic origin-to-destination population flows are computed at three geographic scales: census tract, county, and state. We study tract-to-tract flows on March 1st, 2020, at the start of the COVID-19 pandemic in the United States. Note that this date was before the WHO declared COVID-19 a pandemic and before the United States declared a national state of emergency. For the sake of computational tractability, we focus on a region in the Southwest of the United States that contains all of California and Nevada, along with a small portion of Arizona. A map of the region is shown in Appendix Figure C.1.