Towards Trust and Reputation as a Service in a Blockchain-based Decentralized Marketplace

Abstract

Motivated by the challenges inherent in implementing trusted services in the Society 5.0 initiative, we propose a novel trust and reputation service for a decentralized marketplace. We assume that a Smart Contract is associated with each transaction and that the Smart Contract is responsible for providing automatic feedback, replacing notoriously unreliable buyer feedback by a more objective assessment of how well the parties have fulfilled their obligations. Our trust and reputation service was inspired by Laplace’s Law of Succession, where trust in a seller is defined as the probability that she will fulfill her obligations on the next transaction. We offer three applications. First, we discuss an application to a multi-segment marketplace, where a malicious seller may establish a stellar reputation by selling cheap items, only to use their excellent reputation to defraud buyers in a different market segment. Next, we demonstrate how our trust and reputation service works in the context of sellers with time-varying performance by providing two discounting schemes wherein older reputation scores are given less weight than more recent ones. Finally, we show how to predict trust and reputation far in the future, based on incomplete information. Extensive simulations have confirmed our analytical results.

Index Terms:

Society 5.0, service-centric society, decentralized marketplace, smart contract, trust measure, reputation.I Introduction and motivation

In 2016, the Japanese Government publicized a bold initiative and a call to action for the implementation of a “Super Smart Society” announced as Society 5.0. The novelty of Society 5.0 is that it embodies a sustainable service-centric society enabled by the latest digital technologies. Society 5.0 meets the needs of its members by providing goods and services to the people who require them when they are required, and in the amount required, thus enabling its citizens to live an active and comfortable life through the provisioning of high-quality services [1, 2, 3, 4]. Society 5.0 provides a common societal infrastructure for prosperity based on an advanced service platform which turns out to be its main workhorse.

The insight behind Society 5.0 is that continued progress of ICT and digital technologies of all sorts will provide individuals and society tremendous opportunities for innovation, growth, and unprecedented prosperity and well-being through various forms of human-to-human, human-to-machine, and machine-to-machine cooperations and collaboration. Most of these forms of cooperation and collaboration between humans and machines or between autonomous machine systems have yet to be defined and understood.

Services and their effects have been studied intensely in the past two decades and most of their dynamics are now well understood [5, 6, 7, 8, 9, 10]. Recently, the emergence of Decentralized Autonomous Organizations (DAO) has motivated the study of service provisioning in decentralized blockchain-based environments fed by open networks of contributors [11, 12, 13].

Our paper was inspired and motivated by some of the challenges that will have to be overcome in order to implement Society 5.0. Key among these challenges, as pointed out by several workers, is providing trusted and secure services [14, 15, 16]. With this in mind, we set out to explore providing a trust and reputation service in recently proposed blockchain-based decentralized marketplaces. To the best of our knowledge, this is the first time such an effort has been undertaken.

Today, decentralized markets are growing at a rapid pace with all types of goods and services being transacted online. In such global markets, buyers and sellers engage in transactions with counterparts with whom they had little or no previous interaction. This introduces significant risks for both buyers and sellers. In order to assist buyers (sellers) with the process of choosing a trustworthy trading partner, marketplaces maintain individual reputation scores for each seller (buyer) [17, 18, 19, 20]. These reputation scores capture, in various forms, statistical information about the past behavior of sellers (buyers) registered with the platform.

The goal of a trust and reputation service is to provide buyers with a robust framework that allows them to select future transaction partners based on a combination of objective and subjective trust measures distilled from accumulated evidence of sellers’ past behavior in the marketplace. The quality of a trust and reputation service depends, in a fundamental way, on the quality of the feedback it receives from buyers. This is even more crucial when we consider decentralized marketplaces, where there is no centralized control, unlike marketplaces such as Amazon and eBay.

Being a subjective measure, the quality of buyer feedback is notoriously hard to assess [21, 22, 23]. The fundamental problem is that different buyers may rate a similar experience with the same seller vastly differently. When feedback is provided by buyers from around the world, who may value different aspects of the same transaction differently, it is very hard to know when a buyer provides truthful feedback.

I-A Our contributions

The first main contribution of this paper is to propose a novel blockchain-based trust and reputation service with the goal of reducing the uncertainty associated with buyer feedback in decentralized marketplaces.

The second main contribution of the paper is to illustrate three applications of the proposed blockchain-based trust and reputation service. Specifically, in Subsections VI-A and VI-B we discuss two applications of our service to a multi-segment marketplace, where a malicious seller may establish an enviable reputation by selling cheap items or providing some specific service, only to use their superb reputation score to defraud buyers in a different market segment. Next, in Subsection VI-C, we apply the results of Section IV in the context of sellers with time-varying performance due, for example, to overcome initial difficulties. We provide two discounting schemes where older reputation scores are given less weight than more recent ones, thus focusing attention on current performance. Finally, in Subsection VI-D we show how to predict trust and reputation scores far in the future, based on incomplete information.

In our work we assume that a Smart Contract (SC) is associated with each transaction. We assume that the SC in charge of the transaction is also responsible for providing feedback at the end of the transaction, replacing buyer feedback with a more objective assessment of how well the buyer and the seller have fulfilled their contractual obligations towards each other.

At the heart of any trust and reputation service must lie a trust engine, an algorithm that takes as input a seller’s reputation score and distills from it a subjective trust measure, namely the perceived probability that on the next transaction, the seller will fulfill her contractual obligations. The proposed trust and reputation engine was inspired by a classic result in probability theory, namely Laplace’s Law of Succession [24, 25]. We extend Laplace’s classic result in a way that provides a trust measure in a seller’s future performance in terms of her past reputation scores.

The remainder of this paper is organized as follows. Section II offers a succinct review of recently proposed blockchain-based trust and reputation systems. Section IV introduces the proposed Laplace trust and reputation service. This is followed by Section V which discusses how the trust measure is updated over time. Section VI offers three applications of the proposed Laplace trust and reputation service. Section VII introduces our simulation model and offers simulation results. Finally, Section VIII offers concluding remarks and directions for future work.

We wish to alert the reader that an appendix was added for some tedious mathematical derivations whose inclusion in the main paper would be distracting.

II Blockchain-based reputation systems

Trust and reputation models have long been of interest to economists [26, 27, 28, 29, 30, 31, 32, 33]. The advent of e-commerce has renewed interest in online transactions where, naturally, trust or lack thereof is a major concern.

In recent years, a steadily increasing number of workers have investigated blockchain-based reputation systems wherein SCs may or may not play a significant role. We refer the reader to the surveys of Hendrix et al. [34], Bellini et al. [11], and Hasan et al. [12] for a comprehensive discussion. With this in mind, the main goal of this section is to review some of the recently proposed blockchain-based reputation systems.

Buechler et al. [35] developed a reputation system where SCs contribute to the task of reputation scoring by analyzing the underlying network structure. Their system allows buyers and sellers to query and record the outcomes of transactions.

Lu et al. [36] proposed a blockchain-based trust model specifically designed to improve the trustworthiness of messages in Vehicular Ad-hoc Networks (VANET). However, their system does not use SCs in any capacity. Later, Javaid et al. [37] proposed a blockchain-based and a trusted Certificate-Authority-based trust and reputation model for VANET. While SCs are mentioned by the authors of [37], no specific role for SCs is mentioned in the paper, other than supporting the functionality of the blockchain. More recently, Singh et al. [38] have proposed a blockchain-based trust management system in the context of the Internet of Vehicles [39, 40], an extension of VANET. In their work, the blockchain provides trust among vehicles that have no reason to trust each other. The blockchain also manages in a reliable manner trust and reputation across the Internet of Vehicles. However, although mentioned, there is no specific role played by SCs in their scheme.

Arshad et al. [41] presented a blockchain-based reputation system that they call REPUTABLE which computes the reputation of sellers within a blockchain ecosystem through decentralized on-chain and off-chain implementations. REPUTABLE ensures privacy, reliability, integrity, and accuracy of reputation scores, all this with minimal overhead. In order to facilitate gathering buyer feedback, REPUTABLE employs SCs. However, the SCs are not entrusted with providing feedback on their own.

III The assumed blockchain-based decentralized marketplace

If a reputation system is to be successful, several conditions must be satisfied: first, the decentralized marketplace must collect, aggregate, and disseminate seller reputation scores accurately and in a timely manner; second, buyers provide truthful feedback on their buying experience; and, third, buyers base the choice of their future transaction partners (i.e. sellers) solely on reputation scores.

The first and third conditions are relatively easy to enforce or to incentivize. The second condition is far more problematic. It has been argued that if buyers consistently provide truthful feedback, isolated interactions between buyers and sellers take on attributes of long-term relationships and, as a result, the reputation scores tallied by the marketplace become a high-quality substitute for community-based reputation [42].

It is not surprisingly, therefore, that numerous authors have proposed strategies intended to incentivize truthful feedback [43, 44, 45, 46].

In this work we assume a blockchain-based marketplace similar to [47, 17, 19, 18, 20, 48], where the transactions between buyers and sellers are maintained as individual blocks that, once added to the blockchain, keep immutable information about the transaction. We maintain statistical information about the buyers’ and sellers’ performance as part of the blockchain.

IV The Laplace trust and reputation service

The main goal of this section is to introduce our trust and reputation service.

IV-A Terminology and definitions

Consider a decentralized marketplace and a new seller who just joined the marketplace at time . We associate with the seller an urn containing an unknown number, , of balls and an unknown composition, in terms of the number of black balls it contains. The intention is for the urn of unknown composition to represent the total number of transactions in which seller will be involved during her career in the marketplace. Here, each black ball represents a transaction in which seller has fulfilled her contractual obligations.

We define the reputation score of the seller at time as an ordered triple whose first and second components are, respectively, the total number of transactions in which the seller was involved up to time and the number of transactions in which the seller has fulfilled her contractual obligations up to time . The third component is or, simply, if no confusion can arise.

Each transaction in which seller is involved is associated with a ball extracted from the urn without replacement. If the extracted ball is black, we say that the seller has fulfilled her obligations in the corresponding transaction. The motivation for this is that every time a ball is extracted from the urn without replacement, the probability of obtaining a black ball on the next extraction changes. This is intended to capture, to some extent, the uncertainties and vagaries of seller behavior.

Let be the random variable denoting the initial number of black balls in the urn. Let , be the hypothesis that the initial composition of the urn is , in other words the urn contains black balls, while the remaining balls have other colors.

Since nothing is known à priori about the past history, skill level, and integrity profile of the seller, it makes sense to assume, as an initial prior, that all compositions of the urn are equiprobable (see [24] for a good discussion) and so

| (1) |

We define , the trust measure in seller at time , to be the probability that the seller will fulfill her contractual obligations on the next transaction following . In terms of the underlying urn, this means that the next ball extracted from the urn is black. For example, let be the event that on the very first transaction the seller will fulfill her contractual obligations. Equivalently, is the event that, on the first extraction a black ball will appear. For reasons that will become clear later we write for . It is clear that

| (2) | |||||

which makes intuitive sense, since we have no à prior knowledge of the seller’s past behavior in the marketplace and therefore the trust we place in her is .

IV-B Updating the prior

Now, suppose that our seller has accumulated, in the time interval , a reputation score of . Recall that this means that out of a total of transactions in which the seller was involved up to time , she has fulfilled her obligations in of them. Equivalently, this says that from the urn mentioned above, a sample of balls was extracted without replacement and that of them were observed to be black.

In order to update the trust measure in our seller, we need to update our belief in the original composition of the associated urn. For this purpose, let be the event that in a sample of balls extracted without replacement from the urn, black balls were observed. Once the event is known, we update the prior in a Bayesian fashion by setting

| (3) | |||||

To summarize, the expression of the updated prior reflects our updated belief in the initial composition of the urn, as a result of seeing black balls out of balls extracted. In terms of our seller, upon seeing that the seller has fulfilled her obligations in out of the first transactions, we update the perceived intrinsic performance profile of our seller. At the risk of mild confusion, we continue to write for the updated prior, instead of more cumbersome .

IV-C Modeling the trust measure

Recall that we define a seller’s (subjective) trust measure, , at time as the probability of the event that on the next transaction the seller will fulfill her contractual obligations.

Theorem IV.1

Assuming that seller has accumulated, in the interval , a reputation score of , the trust measure in at time is

Proof:

Consider the urn associated with seller and assume that out of the urn, a sample of balls was extracted and of them were observed to be black. Let be the event that the next ball extracted from the urn is black. In terms of our marketplace, is precisely . By the Law of Total Probability,

| (4) |

Observe that and recall that, by (3), With this, (4) can be written as

and the proof of Theorem IV.1 is complete. ∎

IV-D Illustrating Theorem IV.1

Somewhat surprisingly, the expression of the trust measure is independent of and depends only on and . It is very important to note that the expression of the trust measure specified in Theorem IV.1 is very easy to remember and to compute. Specifically, if a certain seller has accumulated a reputation score , evaluating the corresponding trust measure in the seller at time is very simple. This is one of the significant advantages of our trust and reputation service.

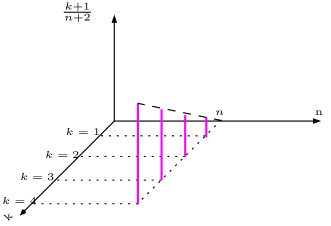

It is of interest to plot the trust measure of Theorem IV.1 for the cases where , and are fixed. First, for fixed , Figure 1 reveals that features a linear increase in . Indeed, the trust measure of a seller with a reputation score of and that of a seller with a reputation score of , differ by .

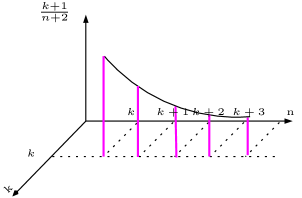

On the other hand, Figure 2 shows that for a fixed value of , , perceived as a function of , experiences a hyperbolic decline. To see this, observe that the trust measure of a seller with a reputation score of and that of a seller with a reputation score of , differ by .

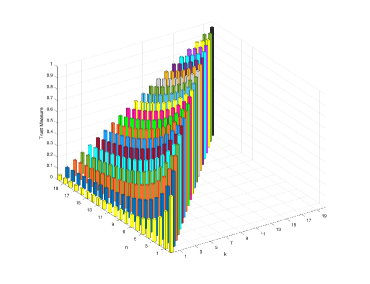

To summarize this discussion, we refer the reader to Figure 3 the trust measure for small values of and . For a better illustration, the values of for different values of are depicted in different colors. Figure 3 also reveals that , as we found in (2).

V Updating the trust measure

The main goal of this section is to show how the trust measure introduced in Section IV is updated over time.

Theorem V.1

Assume that in the time interval , seller was involved in transactions and that she has fulfilled her contractual obligations in of them. If in the time interval seller is involved in additional transactions and that she fulfills her contractual obligations in of them, then the seller’s trust measure, , at time is

| (5) |

Proof:

Let be the event that in a subsequent sample of size , balls were observed to be black. Once the event is known to have occurred, it is necessary to update our prior. Proceeding, in a Bayesian fashion, we write

| (6) | |||||

As before, in order to simplify notation, we continue to refer to as . The expression of the prior in (7) reflects our updated belief in the composition of the urn, as a result of seeing black balls out of balls in the second sample extracted.

Let be the event that the next ball extracted from the urn is black. In terms of our marketplace, is .

| (8) | |||||

∎

Notice that, in spite of the laborious derivation, the final result is extremely simple and easy to compute. This is a definite advantage of our scheme.

An interesting question is to determine under what conditions the trust measure is at least as large as . The answer to this question is provided by the following result.

Lemma V.2

Proof:

Follows by Lemma A.4 in the appendix , , and . ∎

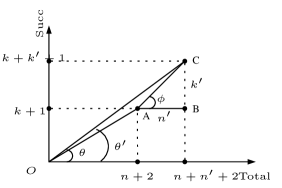

Refer to Figure 4 for a geometric illustration of Lemma V.2. Consider a two-dimensional coordinate system where the horizontal and vertical axes capture, respectively, the total number of transactions and the number of transactions in which the seller has fulfilled her contractual obligations. Consider, further, the points of coordinates . It is easy to confirm that , and . Finally, is is easy to confirm that if and only if the angle determined by the sides and of the triangle determined by the points satisfies , exactly as claimed in Lemma V.2.

Theorem V.1 can be readily generalized.

Theorem V.3

For an arbitrary positive integer , consider successive epochs , such that in epoch , our seller was involved in transactions and has fulfilled her contractual obligations in of them. Then the seller’s reputation score at time is and her associated trust measure is

| (9) |

Proof:

Assume, without loss of generality, that and let and denote, respectively, and . In the time interval the seller was involved in transactions and has fulfilled her obligations in of them. In the time interval, our seller was involved in transactions and has fulfilled her contractual obligations in of them.

Theorem V.3 has a number of consequences:

-

•

the updated trust measure is related to the updated reputation scores, exactly as specified in Theorem IV.1;

-

•

the updated trust measure does not change if

-

–

Associativity: the seller has fulfilled her obligations in of the first transactions and in out of the next transactions, provided .

-

–

Commutativity: for any choice of subscripts , with , the transactions in epoch have occurred before or after the transactions in epoch ;

-

–

Interchangeability: the seller has fulfilled her obligation in of the transactions in epoch and in of the transactions in epoch , provided that and .

-

–

VI Applications of the Laplace Trust Engine

The main goal of this section is to illustrate three applications of the trust and reputation service introduced in Section IV. Specifically, in Subsections VI-A and VI-B we discuss two applications to a multi-segment marketplace, where a malicious seller may establish a very high reputation by selling cheap items or providing some specific type of service, only to use their reputation score to defraud buyers in a different market segment.

Next, in Subsection VI-C, we apply the results of Section IV in the context of sellers with time-varying performance due to an initial learning curve. We provide two discounting schemes, wherein older reputation scores are given less weight than more recent ones. Finally, in Subsection VI-D we show how to predict trust and reputation scores far in the future, based on currently available information.

VI-A Price-range specific trust and reputation

We assume that the transactions in the marketplace are partitioned, by the monetary value of the goods transacted, into non-overlapping price ranges for some positive integer . These ranges determine market segments where market segment involves all the transactions within the price range .

In all marketplaces of which we are aware [11, 12, 15, 16, 17, 18, 19, 20, 22, 23], seller reputation is global, being established irrespective of their performance in different market segments.

However, this may lead to insecurities. For example, imagine a seller that has established an enviable reputation score by selling cheap items, all in the market segment corresponding to the range . Suppose that our seller decides to get involved in a different market segment, say corresponding to price range . Should her reputation score established in carry over to ? We believe that the answer should be in the negative. One reason is that, as pointed out by [49] and other workers, dishonest sellers establish stellar reputation scores by selling cheap items and use the resulting reputation score to hit-and-run in a different market segment.

To prevent this kind of attack from being mounted, we associate with each market segment a distinct reputation score and, consequently, a distinct trust measure. Also, with each market segment, we associate a different urn as discussed in the previous sections of this work. For example, if our seller has never transacted in the market segment corresponding to the price range , her reputation score in that market segment is and, not surprisingly, her corresponding trust measure will be , capturing the idea that nothing is known about the performance of the seller in that market segment.

Consider a generic market segment , and assume that up to time , our seller has accumulated a reputation score of in . Consistent with our definition, the trust measure that our seller enjoys in is . This trust measure is local to and is independent of the seller’s trust measure in other market segments.

It is worth noting that, as an additional benefit, our approach provides resistance to Sybil attacks. It is well known that malicious users involve their Sybils in augmenting their reputation scores [50, 51, 13, 52]. However, the fact that by assumption Smart Contracts are responsible for providing transaction feedback (including the market segment in which the transaction took place), this feedback will be, perforce, local to one market segment, minimizing the effect of the attack. Indeed, as a result of the Sybil attack, the malicious user’s reputation may well increase in one market segment, but her reputation in other market segments will not be affected. This provides for very desirable resistance to Sybil attacks.

VI-B Service-specific trust and reputation

In Subsection VI-A we argued that reputation scores and, therefore, the trust measure of a seller should not be global but should, instead, be specific to individual price ranges. Specifically, we made the point that reputation scores acquired by doing business in one market segment (by dollar amount) should not carry over to a different market segment.

In this subsection, we extend the same idea to the types of services provided. The intuition is that a service provider (i.e. seller) may behave differently when providing different services. Thus, the best indicator of how the service provider will perform in the future depends on their past performance in the context of the type of services contemplated. This motivates assessing the trustworthiness of a service provider by the type of individual service of interest.

As an illustrative example, consider a plumbing contractor who may act in the marketplace as a seller of plumbing hardware, but also as a provider of plumbing services such as repairs, installation of various equipment such a gas furnaces, electric furnaces, hot water heaters, or extended maintenance contracts, etc.

Our plumber may be inclined to provide higher quality services in areas that benefit him most (e.g. installing electric water heaters) and of lesser quality in some other areas that are less lucrative, e.g. maintenance contracts or installing gas water heaters), even though an electric water heater may cost roughly the same as a gas water heater.

The point is that the plumber’s reputation score acquired by providing one type of service should not be relevant when evaluating his/her trustworthiness in different service categories where he/she is either less competent or simply not interested in providing high-quality services.

VI-C Discounting old trust measures

Up to this point, we have assumed that seller behavior is constant over time. For various reasons, sellers may well change their attitude and behave differently from the way they acted in the past. To accommodate this imponderable, in this subsection we introduce two simple mechanisms that allow us to discount older trust measures, giving more credence to recent reputation scores.

For an arbitrary integer , consider successive time epochs with and such that in epoch , our seller was involved in transactions and has fulfilled her contractual obligations in of them. Recall that, given this information, the seller’s reputation score at time is and, by Theorem V.3, her associated trust measure is

| (10) |

VI-C1 First discounting scheme

In order to produce a weighted version of (10), consider non-negative rational numbers Assuming , define weights , where, for all ,

Assuming , define the following weighted version of (10):

| (11) | |||||

It is clear that by varying the s we can give different weights to the past versus more recent trust measures of the seller. For example, by taking for and , the past performance of the seller is ignored and the discounted trust measure reduces to the most recent trust measure. Conversely, by taking , for , and , the past is given more weight to the detriment of the more recent performance. We claim that

Lemma VI.1

| (12) |

Proof:

Assume, without loss of generality, that . The proof of the rightmost inequality in the chain above follows directly from Lemma A.3 in the appendix file by setting , , and for all , and . The leftmost inequality is followed by a mirror argument. ∎

Lemma VI.1 shows that the discounted trust measure cannot improve the overall trust measure. It can, however, focus attention to more recent performance that, in many contexts, may be more relevant.

VI-C2 Second discounting scheme

We find it useful to inherit the notation and terminology developed in the previous subsection. In order to produce a simple discounting scheme, we compute a weighted average of the seller trust measure in each of the time epochs. Indeed, consider the time interval during which a seller has been active in the marketplace. Let be an arbitrary partition of . Assume, further, that for all , in the time interval the seller has accumulated a reputation score . Define non-negative weights , with , and define the weighted trust measure of the seller in the time interval as

| (13) |

It is clear that by varying the s we can give different weights to the past versus more recent trust measure of the seller. It is also easy to see that the following result holds, mirroring (12).

Lemma VI.2

| (14) |

Proof:

We prove that . The proof that is similar and, therefore, omitted. As before, assume without loss of generality that . With this assumption, we write

| (15) | |||||

This completes the proof of Lemma VI.2. ∎

VI-D Predicting trust measure and reputation scores over the long term

It is of great theoretical interest and practical relevance to be able to extrapolate the correct performance of a seller and predict her performance, far in the future. With this in mind, consider a seller that has completed transactions and has fulfilled her obligations in of them. Let be the corresponding event. We are interested in predicting the expected reputation score of the seller by the time her total number of transactions has reached for some .

Let be the random variable that keeps track of the number of black balls among the additional balls extracted, and assume that the event has occurred.

Using the expression of from (3), the conditional probability of the event given is

| (16) | |||||

Actually, this follows directly from (25) in Subsection A-B of the Appendix by taking and .

We are interested in evaluating the conditional expectation, , of given . For this purpose, using the Law of Total Expectation, we write

The two sums will be evaluated separately. We begin by evaluating the following sum:

This implies that the second sum is . Next, to evaluate the first sum, we notice that

| (17) | |||||

Using (17), the first sum can be written as

| (18) | |||||

By combining the intermediate results developed above, the expression of becomes

| (19) | |||||

The intuition behind this simple result is as follows: since nothing is known about the future, in each of the hypothetical extractions from the urn, the success probability, is the same, namely, . Thus, by a well-known result, the expectation of the number of successes must be .

Let us translate (19) into the language of trust and reputation. Consider a seller with a current reputation score of . We are interested in predicting the reputation score of the seller by time when her total number of transactions has reached . By (19), it follows that out of a total of transactions, the predicted number of transactions in which our seller has fulfilled her obligations is .

To put it differently, the expected reputation score of the seller by time , when she was involved in transactions, is . Interestingly, as the following derivation shows, the seller’s predicted trust measure at time is still .

| (20) | |||||

VII Simulation results

The goal of this section is to present the results of our empirical evaluation of the trust and reputation service discussed, analytically, in Sections IV – VI.

VII-A Simulation model

For the purpose of empirical evaluation, we have simulated a blockchain-based decentralized marketplace with SC support. The actors in the marketplace are the buyers and the sellers. We assume that a SC is associated with each transaction and, for simplicity, that each transaction involves one buyer and one seller. The SC in charge of the transaction is responsible for providing feedback at the end of the transaction, replacing notoriously unreliable buyer feedback with a more objective assessment of how well the buyer and the seller have fulfilled their contractual obligations towards each other.

The marketplace simulation model consists of a seller who was involved in transactions with multiple buyers. Each transaction can be either successful (indicating that the seller has fulfilled her contractual obligations) or failed otherwise. In the simulation, we tracked the number of successful transactions and the total number of transactions. The probability of a successful transaction is determined based on the goals of the experiment as we explain in the following subsections. For each goal, we repeated the experiment a large number of times, as needed.

The remainder of this section is structured as follows. In Subsection VII-B we turn our attention to a multi-segment marketplace (by dollar value of the goods transacted) and illustrate, by simulation, the reputation scores and trust measure of a generic seller in these market segments. Next, in Subsection VII-C we present simulation results of seller performance in a marketplace segmented by service type, not price range. This is followed, in Subsection VII-D, by a simulation of the effect of two discounting strategies on the trust measure of a generic seller. Finally, in Subsection VII-E we predict, by simulation, the future reputation scores and trust measure of a generic seller, using currently available, incomplete information.

VII-B Trust measure in a price-range based multi-segment marketplace

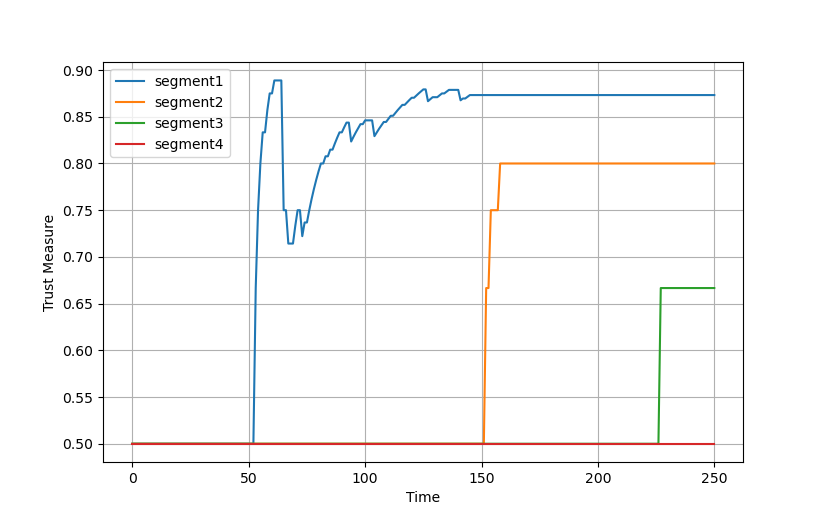

The purpose of this subsection is to illustrate, by simulation, the trust measure of a seller in different market segments defined by the dollar value of the goods transacted. For the simulation, we assume that the transactions in the marketplace are divided into four non-overlapping price ranges , and , based on the monetary value of the items transacted. These four price ranges determine four disjoint market segments—, where market segment includes all transactions falling within the price range .

We have simulated a seller that has accumulated, over a time window of 250 units, the following performance in each of the four market segments:

-

•

In market segment the seller had 85 successful transactions out of 100 total transactions;

-

•

In market segment the seller had 3 successful transactions out of 3 total transactions;

-

•

In market segment the seller had 1 successful transaction out of 1 total transaction; and,

-

•

In market segment the seller had zero transactions;

Figure 5 illustrates the seller’s trust measure in each of the four market segments using (IV.1) from Theorem IV.1.

Not surprisingly, even though the trust measure of the seller in market segment is fairly high, 86/102, her trust measure in market segment is a meager 2/3, while in market segment the seller’s performance is only 1/2, reflecting the fact that the seller has had no experience in the market segment. As a result, the seller cannot misrepresent her performance.

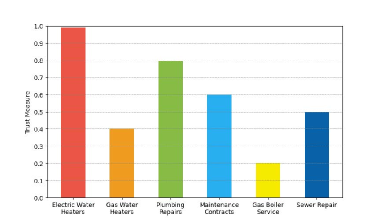

VII-C Trust measure in a service-type based multi-segment marketplace

In Subsection VI-A we argued that the reputation scores and trust measure of a seller should not be global but should, instead, be specific to individual price ranges. In Subsection VI-B we extended the same idea to various types of services and made the point that the best indicator of how the service provider will perform in the future depends on their past performance in the context of the type of services contemplated.

This motivated us to assess the trustworthiness of a service provider by the type of individual service of interest. With this in mind, we have simulated the evolution of reputation scores and trust measures of a plumbing contractor who is offering the following services: electric heater installation, gas heater installation, general plumbing repairs, long-term maintenance contracts, sewer repairs, and gas boiler service.

Some of these services are more lucrative than others and our plumber is more competent in dealing with electricity than with gas equipment installation and repairs. Thus, our plumber may be inclined to provide higher quality services in areas that benefit him most (e.g. installing electric water heaters and general plumbing repairs) and of lesser quality in some other areas that are less lucrative, e.g. installing gas water heaters or providing sewer repairs. We note that in this case, the quality of a service is not necessarily price range dependent, because an electric water heater may cost roughly the same as a gas water heater.

The point is that the plumber’s reputation score acquired by providing one type of service should not be relevant when evaluating his/her trustworthiness in different service categories where he/she is either less competent or simply not interested in providing high-quality services. In our simulations, our plumber has accumulated the following performance in each of the six service categories:

-

•

In the electric heater installation category, the plumber had 92 successful transactions out of 93 transactions;

-

•

In the gas heater installation category, the plumber had 11 successful transactions out of 29 transactions;

-

•

In the general plumbing repairs category, the plumber had 39 successful transactions out of 48 transactions;

-

•

In the maintenance contract category, the plumber had 58 successful transactions out of 98 transactions;

-

•

In the gas boiler service category, the plumber had 3 successful transactions out of 18 transactions;

-

•

In the sewer repairs category, the plumber had 0 successful transactions out of 0 transactions.

Figure 6 illustrates our plumber’s trust measure in each of the service categories above.

Thus, if a consumer wishes to hire a trustworthy plumbing contractor for gas boiler service, our plumber has nothing to recommend him in that service category, even though they have a stellar performance in electric water heater installation.

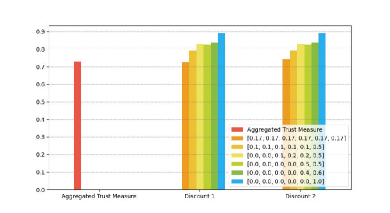

VII-D Illustrating the effect of discounting strategies

We have simulated the reputation scores and associated trust measure, of a generic seller in six time epochs, each one week long. Each epoch has its own success rate, as detailed below.

-

•

Epoch 1: time range from 0 to 250 with a success rate of 0.55;

-

•

Epoch 2: time range from 250 to 500 with a success rate of 0.65;

-

•

Epoch 3: time range from 500 to 750 with a success rate of 0.70;

-

•

Epoch 4: time range from 750 to 1000 with a success rate of 0.75;

-

•

Epoch 5: time range from 1000 to 1250 with a success rate of 0.80;

-

•

Epoch 6: time range from 1250 to 1500 with a success rate of 0.90.

Initially, the seller’s reputation scores were low, perhaps because of her lack of experience. We have simulated the effect of the two discounting strategies presented in Section VI. Table I displays the different weights utilized as discounting parameters:

| Experiment 1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.5 |

|---|---|---|---|---|---|---|

| Experiment 2 | 0.0 | 0.0 | 0.1 | 0.2 | 0.2 | 0.5 |

| Experiment 3 | 0.0 | 0.0 | 0.0 | 0.0 | 0.5 | 0.5 |

| Experiment 4 | 0.0 | 0.0 | 0.0 | 0.0 | 0.4 | 0.6 |

| Experiment 5 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 |

| Experiment 6 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 |

The results of the simulation with each experiment color-coded are summarized in Figure 7. In the figure we have plotted, side by side, the seller’s aggregate trust measure without discounting as well as her trust measure weighted as described. In the figure, it becomes obvious the effect of favoring recent performance over more remote performance. As it turns out, selecting the weights that focus attention on the performance of the seller in the last week presents her trust measure in the best light, as it is, conceivably, the most accurate reflection of her improvement.

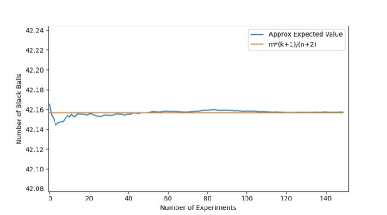

VII-E Predicting trust measure and reputation scores over the long term

In this subsection, we are presenting the results of simulating the convergence of the predicted and simulated long-term trust measure of a seller. For this purpose, we have simulated the performance of a seller in her first 100 transactions. Our goal was to see how close is the prediction of the expected number of her successful transactions among the next 100 transactions. The results of the simulation are plotted in Figure 8. The simulation was repeated between 50 and 150 times. From the figure, it is clear that the seller’s simulated long-term performance, in terms of her reputation scores (and associated trust measure) converges to the theoretically predicted performance.

VIII Concluding remarks

This paper was motivated by the multi-fold challenges inherent in implementing the vision of trusted and secure services in Society 5.0.

The first main contribution of this paper was a novel trust and reputation service with a view to reducing the uncertainty associated with buyer feedback in decentralized marketplaces. Our trust and reputation service was inspired by a classic result in probability theory that can be traced back to Laplace.

The second main contribution of the paper was to offer three applications of the proposed trust and reputation service.

Specifically, in Subsections VI-A and VI-B we discussed two applications to a multi-segment marketplace, where a malicious seller may establish a stellar reputation by selling cheap items or providing some specific service, only to use their excellent reputation score to defraud buyers in a different market segment. As we noted, our service can provide Sybil resistance is a much-desired attribute.

Next, in Subsection VI-C, we applied the results of Section IV in the context of sellers with time-varying performance due, for example, to fighting an initial learning curve or other similar impediments. We provided two discounting schemes wherein less recent reputation scores are given less weight than more recent ones. In Subsection VI-D we showed how to use or trust and reputation services to predict reputation scores far in the future, based on fragmentary information.

Last, but certainly not least, the reputation and trust service developed in this paper seems to have applications for several domains, including banking, inventory management, vehicular networks [37], peer-to-peer networking [36], and vehicular clouds [39]. Exploring these new application domains promises to be an exciting area for future work.

References

- [1] A. Deguchi, C. Hirai, H. Matsuoka, T. Nakano, K. Oshima, M. Tai, and S. Tani, What Is Society 5.0? Tokyo, Japan, 05 2020, pp. 1–23.

- [2] M. E. Gladden, “Who will be the members of society 5.0? towards an anthropology of technologically posthumanized future societies,” Social Sciences, vol. 8, no. 5, p. 148, May 2019. [Online]. Available: http://dx.doi.org/10.3390/socsci8050148

- [3] Hitachi-UTokyo Laboratory (H-UTokyo Lab), Society 5.0 – A People-centric Super-smart Society. Berlin: Springer Open, 2020.

- [4] Y. Shiroishi, K. Uchiyama, and N. Suzuki, “Society 5.0: For human security and well-being,” IEEE Computer, vol. 51, no. 7, pp. 91–95, July 2018.

- [5] H. Chesbrough and J. Spohrer, “A research manifesto for service science,” Communications of the ACM, vol. 7, no. 49, pp. 35–40, July 2006.

- [6] R. Larson, “Smart service systems: Bridging the silos,” Service Science, vol. 8, no. 4, pp. 359–367, 2016.

- [7] P. Maglio and J. Spohrer, “Fundamentals of service science,” Journal of the Academy of Marketing Science, vol. 36, no. 1, pp. 18–20, 2008.

- [8] P. Maglio, S. Vargo, N. Caswell, and J. Spohrer, “The service system is the basic abstraction of service science,” Information Systems and e-business Management, vol. 7, no. 4, pp. 395–406, 2009.

- [9] A. Medina-Borja, “Smart things as service providers: A call for convergence of disciplines to build a research agenda for the service systems of the future,” Service Science, vol. 7, no. 1, pp. ii–v, 2015.

- [10] J. Spohrer, P. Maglio, J. Bailey, and D. Gruhl, “Toward a science of service systems,” IEEE Computer, vol. 40, no. 1, pp. 71–77, January 2007.

- [11] E. Bellini, Y. Iraqi, and E. Damiani, “Blockchain-based distributed trust and reputation management systems: A survey,” IEEE Access, vol. 8, pp. 21 127–21 151, 2020.

- [12] O. Hasan, L. Brunie, and E. Bertino, “Privacy-preserving reputation systems based on blockchain and other cryptographic building blocks: A survey,” ACM Computing Surveys (CSUR), vol. 55, no. 2, pp. 1–37, 2022.

- [13] C. Santana and L. Albareda, “Blockchain and the emergence of decentralized autonomous organizations (DAO): An integrative model and research agenda,” Technological Forecasting & Social Change, vol. 182, 2022.

- [14] T. Kaji, Y. Takahashi, A. Shimura, and M. Yoshino, “Trusted and secure service system for society 5.0,” Hitachi Review, pp. 81–85, November 2021.

- [15] A. Gandini, I. Pais, and D. Beraldo, “Reputation and trust on online labor markets: the reputation economy of elance,” Work Organisation, Labour and Globalisation, vol. 16, pp. 27–43, 2016.

- [16] F. Adebesin and R. Mwalugha, “The mediating role of organizational reputation and trust in the intention to use wearable health devices: Cross-country study,” JMIR Mhealth Uhealth, vol. 20, 2020.

- [17] V. Koutsos, D. Papadopoulos, D. Chatzoloulos, S. Tarkoma, and P. Hui, “Agora: A privacy-aware data marketplace,” IEEE Transactions on Dependable and Secure Computing, 2021.

- [18] Y. Peng, M. Du, F. Li, R. Cheng, and D. Song, “FalconDB: Blockchain-based collaborative database,” in Proceedings of ACM SIGMOD’2020, Portland, Oregon, June 14-19, 2020.

- [19] K. Soska, A. Kwon, N. Christin, and S. Devadas, “Beaver: a decentralized anonymous marketplace with secure reputation,” Cryptology ePrint Archive: Report 2016/464, 2016.

- [20] M. Travizano, C. Sarraute, G. Ajzenman, and M. Minnoni, “Wibson: A decentralized data marketplace,” in Proc. ACM Workshop on Blockchain and Smart Contracts, San Francisco, CA, 2018.

- [21] D. de Siqueira Braga, M. Niemann, B. Hellingrath, and F. B. de Lima-Neto, “Survey on computational trust and reputation models,” ACM Computing Surveys, vol. 51, pp. 1 – 40, November 2018.

- [22] A. Jøsang and R. Ismail, “The beta reputation system,” in Proceedings of 15-th Bled Electronic Commerce Conference, e-Reality: Constructing the e-Economy, Bled, Slovenia, June, 17–19, 2002.

- [23] W. T. Teacy, J. Patel, N. R. Jennings, and M. Luck, “TRAVOS: Trust and reputation in the context of inaccurate information sources,” Autonomous Agents and Multi-Agent Systems, no. 2, pp. 183–198, 2006.

- [24] S. Geisser, “On prior distributions for binary trials,” The American Statistician, no. 4, pp. 244–247, November 1984.

- [25] S. L. Zabell, “The rule of succession,” Erkenntnis, pp. 283–321, 1989.

- [26] F. Bass, “A new product growth for model consumer durables,” Management Science, vol. 15, no. 5, pp. 215–227, 1969.

- [27] D. Bergemann, A. Bonatti, and A. Smolin, “The design and price of information,” American Economic Review, no. 1, pp. 1–48, 2018.

- [28] S. Frederick, G. Loewenstein, and T. O’Donoghue, “Time discounting and time preference: A critical review,” Journal of Economic Literature, vol. XL, pp. 351–401, 2002.

- [29] R. Howard, “Information value theory,” IEEE Transactions on Systems Science and Cybernetics, vol. 2, no. 1, pp. 22–26, August 1966.

- [30] D. Lucking-Reiley, “Auctions on the Internet: What’s beig auctioned and how,” Journal of Inducstrial Economics, vol. 48, pp. 227–252, 2000.

- [31] P. Resnick, R. Zeckhauser, J. Swanson, and K. Lockwood, “The value of reputation on eBay,” Experimental Economics, no. 2, pp. 79–101, 2006.

- [32] C. Shapiro, “Premiums for high quality products as returns to reputation,” Quarterly Journal of Economics, vol. 98, pp. 659–680, 1983.

- [33] K. Waehrer, “A mode of auction contracts for liquidated damages,” Journal of Economic Theory, pp. 531–555, 1995.

- [34] F. Hendrix, K. Bubendorfer, and R. Chard, “Reputation systems: A survey and taxonomy,” Journal of Parallel and Distributed Computing, vol. 75, 2014.

- [35] M. Buechler, M. Eerabathini, C. Hockenbrocht, and D. Wan, “Decentralized reputation system for transaction networks,” Technical report, University of Pennsylvania, Tech. Rep., 2015.

- [36] Z. Lu, Q. Wang, G. Qu, and Z. Liu, “Bars: A blockchain-based anonymous reputation system for trust management in vanets,” in Proc. 17th IEEE Int. Conference On Trust, Security and Privacy in Computing and Communications, 2018, pp. 98–103.

- [37] U. Javaid, M. N. Aman, and B. Sikdar, “Drivman: Driving trust management and data sharing in vanets with blockchain and smart contracts,” in 2019 IEEE 89th Vehicular Technology Conference (VTC2019-Spring), 2019, pp. 1–5.

- [38] P. K. Singh, R. Singh, S. K. Nandi, K. Z. Ghafoor, D. B. Rawat, and S. Nandi, “Blockchain-based adaptive trust management in internet of vehicles using smart contract,” IEEE Transactions on Intelligent Transportation Systems, vol. 22, no. 6, pp. 3616–3630, 2020.

- [39] S. Olariu, “A survey of vehicular cloud computing: Trends, applications, and challenges,” IEEE Transactions on Intelligent Transportation Systems, vol. 21, no. 6, pp. 2648–2663, June 2020.

- [40] ——, “Vehicular crowdsourcing for congestion support in smart cities,” Smart Cities, vol. 4, pp. 662–685, 2021.

- [41] J. Arshad, M. A. Azad, A. Prince, J. Ali, and T. G. Papaioannou, “REPUTABLE–a decentralized reputation system for blockchain-based ecosystems,” IEEE Access, vol. 10, pp. 79 948–79 961, 2022.

- [42] P. Resnick, R. Zeckhauser, E. Friedman, and K. Kuwabara, “Reputation systems,” Communications of the ACM, no. 12, pp. 45–48, 2000.

- [43] R. Jurca and B. Faltings, “An incentive-compatible reputatiion mechanism for the online hotel booking industry,” in Proc. IEEE Conference on e-commerce, Newport Beach, CA, 2003, pp. 285–292.

- [44] ——, “Confess, an incentive-compatible reputatiion mechanism for the online hotel booking industry,” in Proc. IEEE Conference on e-commerce, San Diego, CA, 2004.

- [45] ——, “Enforcing truthful strategies in incentive-compatible reputation mechanisms,” Internet and Network Economics, pp. 268–277, 2005.

- [46] H. Zhao, X. Yang, and X. Li, “WIM: A wage-based incentive mechanism for reinforcing truthful feedbacks in reputation systems,” in Proc. IEEE Globecom, San Diego, CA, 2010.

- [47] R. Dennis and G. Owen, “Rep on the block: A next generation reputation system based on the blockchain,” in 2015 10th International Conference for Internet Technology and Secured Transactions (ICITST), 2015, pp. 131–138.

- [48] Z. Zhou, M. Wang, C.-N. Yang, Z. Fu, X. Sun, and Q. J. Wu, “Blockchain-based decentralized reputation system in e-commerce environment,” Future Generation Computer Systems, vol. 124, pp. 155–167, 2021.

- [49] R. Kerr and R. Cohen, “Smart cheaters do prosper: defeating trust and repuation systems,” in Proceedings of 8-th International Conference on Autonomous Agents and Multiagent Systems, Budapest, Hungary, May 10-15, 2009.

- [50] A. Cheng and E. Friedman, “Sybilproof reputation mechanisms,” in SIGGCOM Workshops, 2005, pp. 128–132.

- [51] B. Nasrulin, G. Ishmaev, and J. Pouwelse, “MeritRank: Sybil tolerant reputation for merit-based tokenomics,” in Proc. 4-th IEEE Conference on Blockchain Research and Applications for Innovative Networks and Services (BRAINS’22), 2022, pp. 95–102.

- [52] A. Stannat, C. U. Ileri, D. Gijswijt, and J. Pouwelse, “Achieving sybil-proofness in distributed work systems,” in Proc. 20-th International Conference on Autonomous Agents and Multiagent Systems, (AAMAS’21), 2021, pp. 1261–1271.

- [53] R. L. Graham, D. E. Knuth, and O. Patashnik, Concrete Mathematics, 2nd ed. Addison-Wesley, 1994.

![[Uncaptioned image]](/html/2403.04779/assets/x8.png)

Professor Olariu received his M.Sc and PhD from McGill University, Montreal, Canada. Much of his experience has been with the design and implementation of robust protocols for wireless networks and their applications. Professor Olariu is applying mathematical modeling and analytical frameworks to the resolution of problems ranging from securing communications to predicting the behavior of complex systems to evaluating the performance of wireless networks. His most recent research interests are in the area of services computing.

![[Uncaptioned image]](/html/2403.04779/assets/figs/RaviMukkamala.jpg)

Dr. Ravi Mukkamala received his Ph.D. from the University of Iowa, Iowa City, Iowa, in 1987. He also received his M.B.A. from Old Dominion University in 1993. He joined ODU as an Assistant professor in 1987 where he is currently a Professor of Computer Science and Associate Dean for the College of Sciences. Dr. Mukkamala’s current areas of research include computer security, privacy, data mining, and modeling. He has published more than 175 research papers in refereed journals and conference proceedings. He has received more than $3 million in research grants as PI or co-PI from agencies including NASA, as well as Jefferson Lab and private industries. He received a Most Inspirational Faculty Award from ODU in 1994. He has won several best paper awards at national and international conferences over the years.

![[Uncaptioned image]](/html/2403.04779/assets/figs/Meshari.jpg)

Meshari Aljohani received the M.S. degree in computer science from California Lutheran University in 2013. He is currently pursuing the Ph.D. degree in computer science at Old Dominion University. His research interests are related to blockchain, marketplace, and reputation systems.

Appendix A Appendices

A-A Combinatorial preliminaries

Lemma A.1

For non-negative integers, , the following holds

Proof:

See [53], pp. 167–8. ∎

Lemma A.2

For all non-negative integers , with , the following equality holds

| (21) |

Proof:

See [53], p. 169. ∎

A-B Evaluating

To simplify notation, we write instead of . Obviously, Recall that by (3), and that . With this, the expression of becomes:

| (22) |

A-C Two simple algebraic inequalities

Lemma A.3

Let be an arbitrary positive integer and consider non-negative real numbers and as well as positive reals such that

| (26) |

Then,

| (27) |

Proof:

Let us evaluate the difference

| (28) | |||||

∎

Lemma A.4

Let be non-negative reals and let be positive reals. Then

| (29) |

Proof:

We write in stages

and the proof of the lemma is complete. ∎