Single-level Robust Bidding of Renewable-only Virtual Power Plant in Energy and Ancillary Service Markets for Worst-case Profit Optimization

Abstract

This paper proposes a novel single-level robust mathematical approach to model the RES-only Virtual Power Plant (RVPP) bidding problem in the simultaneous Day Ahead Market (DAM) and Secondary Reserve Market (SRM). The worst-case profit of RVPP due to uncertainties related to electricity prices, Non-dispatchable Renewable Energy Sources (ND-RES) production, and flexible demand is captured. In order to find the worst-case profit in a single-level model, the relationship between price and energy uncertainties leads to some non-linear constraints, which are appropriately linearized. The simulation results show the superiority of the proposed robust model compared to those in the literature, as well as its computational efficiency.

Index Terms:

Renewable-only virtual power plant, single-level model, robust optimization, uncertainty, worst-case profit.I Introduction

I-A Motivation

The penetration of ND-RESs has experienced a remarkable growth in the last decades. However, the stochastic nature of these sources implies that ND-RESs are less reliable when it comes to predictable and controllable power injection over a given period of time [gulotta2023short]. This makes ND-RESs participation in the energy and Ancillary Service Market (ASM) difficult, as failure to meet with the contracted energy and reserve in the market will lead to penalties if not suspension from future market activities. However, by integrating multiple portfolios of ND-RESs and other flexible assets as an RVPP, the performance and competitiveness of ND-RESs in these markets can be significantly improved [yang2023optimal].

The viability of RVPP depends on its economic performance, related to benefits and costs. Different markets bring different benefits according to the bidding/offering ability of RVPP and its ability to provide what is promised [alvaroPOSYFT]. However, in addition to the internal uncertainties of RVPP units in their production and demand, there are various external uncertainties in the markets, such as the energy and reserve electricity price uncertainties [zhang2021robust]. Therefore, the development of bidding approaches for RVPP participation in different markets taking into account the characteristics of RVPP units, market rules, and internal and external uncertainties has at most important for RVPP operators and researchers [venegas2022review].

I-B Literature Review

Many papers in the literature use mathematical optimization models to capture different uncertainties associated with Virtual Power Plant (VPP) due to ease of implementation, convergence to the global optimum, and computational efficiency of these models [gao2024review]. In this context, Robust Optimization (RO) programming is an efficient way to deal with different sets of uncertainties that vary in their possible values. The goal of RO is to find the worst case of the optimization problem to minimize the negative impact of uncertainties on the solution [naval2021virtual]. However, the definition of the worst case can vary depending on how the optimization is implemented, whether it is single-level or multi-level, and can lead to different solutions in each approach. The authors in [ZHANG2023108558, bafrani2022robust, ju2019cvar, rahimiyan2015strategic, wang2023optimal, oskouei2021strategic, silva2024light, Hadi] develop a single-level optimization problem for the VPP market bidding problem to find the worst case of energy of ND-RESs. The literature addresses VPP scheduling and bidding problems by considering different uncertainty characterizations in demand [ZHANG2023108558, bafrani2022robust, ju2019cvar, oskouei2021strategic, Hadi], ND-RES production [bafrani2022robust, ju2019cvar, rahimiyan2015strategic, wang2023optimal, oskouei2021strategic, silva2024light, Hadi], and electricity price [rahimiyan2015strategic, wang2023optimal, oskouei2021strategic, Hadi], focusing on multi-market [ZHANG2023108558, bafrani2022robust, rahimiyan2015strategic, wang2023optimal, oskouei2021strategic, silva2024light, Hadi], multi-objective [ju2019cvar], and multi-energy models [wang2023optimal, oskouei2021strategic]. The main advantages of the mentioned single-level RO programming in [ZHANG2023108558, bafrani2022robust, ju2019cvar, rahimiyan2015strategic, wang2023optimal, oskouei2021strategic, silva2024light, Hadi] are the possibility to consider multiple uncertainties, simplicity of implementation, global optimality, and calculation efficiency. However, a simplified definition of the worst case of energy for the severe scenarios is implemented. In fact, the worst case of energy defined for ND-RESs in the above papers does not lead to the worst condition of profit, considering the possibility of different values of electricity prices. For instance, in a case where the electricity price is low in a certain period, even though the energy of a ND-RES can deviate significantly in this period, the resulting loss for RVPP might not be significant compared to a period with much higher electricity price and average or low energy deviation.

Multi-level RO models provide more flexibility to find the actual worst-case of the VPP bidding problem compared to single-level models. This is due to the definition of a new level for the optimization problem that models the behavior of uncertain parameters (both electrcity price and energy uncertainties). Therefore, the objective function of this level can be defined to find the worst case of energy or profit of VPP. In addition, another level for the problem can be included to define the corrective or remedial actions after the occurrence of uncertainties.

The literature on multi-level models proposes mathematical techniques, including Adaptive [khojasteh2023novel, li2022robust] and Stochastic [zhang2021robust, baringo2018day, kong2020robust] RO to account for various uncertainties in ND-RES production [zhang2021robust, baringo2018day, khojasteh2023novel, kong2020robust, li2022robust], demand [khojasteh2023novel, kong2020robust], electricity prices [zhang2021robust, baringo2018day], and reserve deployment or dispatch order of Transmission System Operator (TSO) [zhang2021robust, baringo2018day, li2022robust]. The proposed models are implemented for the multi-market participation of VPP [zhang2021robust, baringo2018day, khojasteh2023novel] and for multi-energy VPPs [kong2020robust]. Different techniques, including Benders and other decomposition techniques [zhang2021robust, khojasteh2023novel], the Column Constraint Generation algorithm [baringo2018day], and improved versions of these algorithms [kong2020robust, li2022robust], are proposed to accelerate the solution time of the optimization problem. The main limitations of the multi-level approaches in general, and in the above works in particular, are the complexity of programming and the fact that the size of the problem grows with the number of iterations in the solving procedure. In addition, they usually imply long computational times, which can compromise applications such as sensitivity analysis.

I-C Approach and Contributions

To avoid the difficulties of implementing a multi-level model and the computational complexity for practical applications, this paper models the worst-case profit of RVPP against uncertainties by means of a novel single-level Mixed Integer Linear Programming (MILP) problem. The equations related to the uncertain parameters in the objective function of the optimization problem (equations related to the energy and reserve price uncertainties) as well as the equations related to the uncertain parameters in the constraints (equations related to the ND-RES and demand uncertainties) are defined by developing the approach in [bertsimas2004price, rahimiyan2015strategic, Hadi] and by developing on the idea from the big M method [floudas1995nonlinear]. The proposed implementation of robust constraints makes it possible to capture the relationship between different uncertain parameters in the objective and constraints of the optimization problem, and to find the exact worst case profit of RVPP. Finally, defining the relationship between uncertain parameters in order to find the worst case leads to some non-linear constraints, which are linearized by using well-established methods.

The contributions of this paper are threefold:

-

•

Modeling the worst-case profit robustness of an RVPP with a single-level Mixed Integer non-Linear Programming (MINLP) model. As opposed to other single-level models in the literature, the proposed model maximizes the expected profit of RVPP for the simultaneous DAM and SRM participation against the worst-case profit robustness of different uncertainties on prices and energy (ND-RES production and demand).

-

•

Addressing the non-linear couplings between various uncertainties within the optimization problem, and subsequently formulating an equivalent MILP problem for the initial MINLP one.

-

•

The proposed single-level MILP model has high computational efficiency and simpler implementation compared to the multi-level optimization models in the literature.

I-D Paper Organization

The reminder of the paper is organized as follows. A conceptual comparison of energy and profit robustness approaches is presented in Section II. The proposed single-level robust bidding problem of RVPP for DAM and SRM participation is formulated in Section III. An illustrative example is given in Section LABEL:sec:_Example to show the performance of the proposed robust model in finding the worst-case profit. The simulation results are presented in Section LABEL:sec:Simulation. Finally, the conclusions are drawn in Section LABEL:sec:Conclusion.

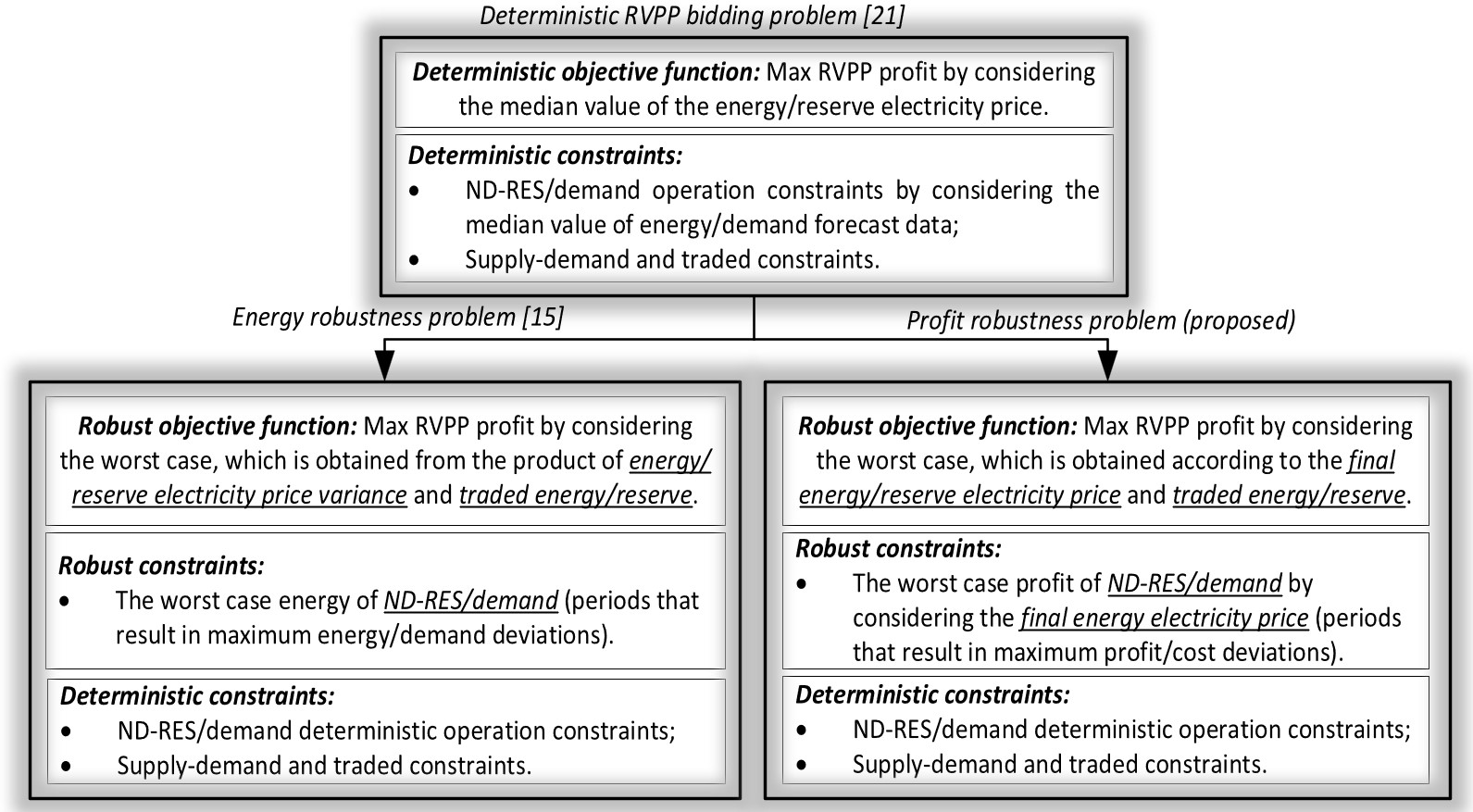

II Comparing Energy and Profit Robustness

Figure 1 shows the structure of a deterministic RVPP bidding problem and a comparison between the energy and the profit robustness approaches. In the deterministic approach, a single value (usually the median or average) of the forecast data is considered to solve the optimization problem. The constraints are related mainly to the operation of the RVPP units, and supply-demand balance [oladimeji2022optimal]. When considering the uncertainties, depending on whether the uncertainties affect the objective function or the constraints of the optimization problem, different sets of constraints need to be defined in each of the RO approaches. The uncertainties related to the energy/reserve electricity price affect the objective function of the optimization problem, whereas the uncertainties associated with the ND-RES generation and demand consumption affect the constraints.

In the energy robustness approach, those periods that result in more deviation of the energy/reserve electricity price variance multiplied by the total traded energy/reserve of RVPP are selected as the worst-case scenarios of the electricity price [Hadi]. In the energy robustness constraints, the periods that have higher deviation of energy are selected as the worst case of ND-RESs production or demand regardless of the electricity price.

In the profit robustness approach proposed in this paper and for the uncertain parameters in the objective function of the optimization problem (energy/reserve electricity price), the worst case is defined according to the final value of the energy/reserve electricity price by means of binary variables. The final value of the energy electricity price is also used to calculate the worst case of profit/cost of each unit (uncertainty of ND-RES and demand in the constraints of the optimization problem). For this purpose, the final energy electricity price is multiplied by the energy variable of ND-RES/demand and is limited by the profit reduction effect due to ND-RES/demand uncertainty.

In the following section, the proposed profit robustness approach is formulated as a single-level optimization problem. In Section LABEL:sec:_Example, these two approaches are compared using an illustrative example.

III Profit Robustness Formulation

III-A Nomenclature

This subsection presents the notation and nomenclature used in the remainder of the paper.

General Notation Concepts

-

•

An uncertain parameter with a tilde symbol denotes the median value in the forecast distribution, representing a point where half of the observations are lower ();

-

•

the hat/inverse hat symbol on uncertain parameters signifies the greatest positive/negative permitted deviation from the forecast’s median (, );

-

•

parameters with an upper/lower bar represent their upper/lower bounds of parameter (, );

-

•

upward/downward arrows indicate up/down direction of regulation in variables and parameters (, /, ).