CV@R penalized portfolio optimization with biased stochastic mirror descent

Abstract

This article studies and solves the problem of optimal portfolio allocation with CV@R penalty when dealing with imperfectly simulated financial assets. We use a Stochastic biased Mirror Descent to find optimal resource allocation for a portfolio whose underlying assets cannot be generated exactly and may only be approximated with a numerical scheme that satisfies suitable error bounds, under a risk management constraint. We establish almost sure asymptotic properties as well as the rate of convergence for the averaged algorithm. We then focus on the optimal tuning of the overall procedure to obtain an optimized numerical cost. Our results are then illustrated numerically on simulated as well as real data sets.

Keywords— Stochastic Mirror Descentbiased observationsrisk management constraintportfolio selectiondiscretization.

1 Introduction

Given a portfolio of financial assets, what is the best way to allocate resources under a risk management constraint? Without any fixed constraint, it is likely that the asset with the highest expected return would be favored, leading to a trivial optimization problem. However, ethical issues arise when this latter return possesses high variability, since even though in the long run some profits are expected, large losses can occur in between wins. This problematic is especially relevant for institutions with some large capital investments such as banks and insurances.

Hence, the necessity for regulation appears. As a matter of fact, this is precisely the point of the Basel III banking regulation that has been implemented in response to the various past financial crises. Risks can be quantified with various metrics, and policies developed using one or another metric could lead to different investment optimization problems and strategies. In this work, we consider a penalty on the conditional value at risk denoted by CV@R (also referred to as the expected shortfall in the literature) of the portfolio, which stands for a coherent measure of risk of an investment [6, 44]. We refer to Equation (1) in the next section for a formal definition. Heuristically, the CV@R measures how big the average loss is, at a given rate for worst scenarii (say for example). Our problem is therefore to optimize the expected portfolio returns while keeping the risk (measured via CV@R) under a fixed threshold.

Portfolio optimization under CV@R constraint has already been investigated in previous works, we can notably cite Rockafellar and Uryasev [43] who develop a Monte-Carlo strategy to approximate the CV@R of the portfolio. These results have been refined in subsequent works of the authors, notably in Krokhmal et al. [29], Rockafellar et Uryasev [44] and more recently in [42] , but basically the authors of these former works use the approximation of the V@R and CV@R with a batch empirical sum to feed an optimization algorithm via classical tools of convex analysis.

The approximation with a Monte-Carlo empirical mean to handle the V@R and the CV@R can be traced back to Ben Tal and Teboulle [13] and Pluf [38], who link these two quantities by a and of a convex function. This article spun a series of articles dealing with the Robbins-Monro approximation of V@R and CV@R. We can cite a series of papers by Bardou, Frikha and Pagès [10], [11], and the book [9], as well as [23] all dealing with Robbins Monro stochastic approximation. However, as in [23], a question still remains when the underlying asset’s distribution is unobtainable. A natural solution to that problem would be to approximate the underlying distribution, introducing a bias. This trend of biased stochastic approximation is very natural but presents some challenges in itself, which can be addressed in multiple ways. We can cite the works of [7] or [31] (see also the references therein) for an overview of the techniques used for biased stochastic approximation algorithms.

In mathematical finance, assets are commonly modeled using stochastic differential equations, and in general, these equations do not have any explicit solutions. A natural approach to this issue is simply to replace the SDE with a discretization scheme. However, a such discretization naturally introduces a bias in the stochastic approximation procedure, and the effect of this bias should be addressed to finely tune the optimization algorithm. Discretization for SDEs has been studied since the pioneering work of Talay and Tubaro [46], where strong regularity is assumed on the coefficients. As results developed, regularity assumptions have been dropped, and sharp bounds have been derived for both weak and strong error (see e.g. [28]) on specific stochastic models for specific discretization schemes (see e.g. [1, 2] among others).

In our paper, we assume in addition that one of the asset in our portfolio is risk-less, which allows to model debt obligations, or treasury bonds. In mathematical terms, we consider a stochastic rate, modeled by a Cox-Ingersoll-Ross (shortened as CIR below) [19] process and we use this rate for the growth ratio of one component of our portfolio (see Subsection 3.1 below the definition). It can be shown that CIR processes can be calibrated to always stay positive (which is desirable for modeling rates - but sometimes not necessary). Unfortunately, positivity is not preserved with the usual explicit Euler scheme. This fact drives us, when discretizing the CIR, to use a drift-implicit Euler scheme, introduced in [1], that is known to preserve positivity (see Section 3.2 and Proposition C.2 below for more details). Thankfully, rate of convergence for the approximation of the CIR process has been widely studied, see e.g. [21, 3] and these quantitative results may be exploited to control the bias and its propagation in the specific terms induced by some functional related to the CV@R variational formulation.

Finally, we also impose a reinvestment condition, saying that the strategy must reallocate all funds available. This means that if we have an initial capital of and elements in our portfolio, we are looking for a vector such that . Equivalently, we consider in the simplex: and and look for an optimal set of weights . Note that this is asking each weights to be positive. This prevents short selling, which is the practice of selling a stock one does not own in hopes of buying it back in the future at a lower price, and is yet another behavior that is regulated by financial institutions.

In order to determine a strategy in the simplex, one natural idea would be to derive an algorithm without the constraint , and project back the result over the simplex. However, projection over the simplex tends to favor extremal points, which slows down the convergence of algorithms while projection is itself an additional step that may be numerically costly when some high-dimensional portfolio are considered. To overcome this issue, we set up a stochastic mirror descent, as pioneered by Nemirovskii & Yudin [35]. Mirror descent (and its variants) stands for a widely used class of optimization algorithms, whose main interest is to avoid a costly projection into the set of constraints by replacing the Euclidean distance by a Bregman divergence in the second order Taylor expansions. It may be adapted to the stochastic framework with the help of carefully tuned step-size sequences, we can cite among others [36] that initiates the use of a noisy stochastic gradient in the mirror descent, [30] for specific derivations on convex optimization problems on the simplex and more recently Zhou et al [47] that derives some results on the a.s. convergence in the general case with asymptotic pseudo-trajectories, that are common tools of random dynamical systems (see e.g. [15]).

In summary, to find an investment strategy while managing risk, we will use a stochastic mirror descent with an approximation of the portfolio, combined with a fine approximation for the CV@R. The discretization of the Portfolio is handled by an implicit Euler scheme. This discretization feeds the approximation of the V@R and the CV@R, which is done through a biased Robbins-Monro algorithm, which in turn feeds a stochastic mirror descent to determine the optimal portfolio allocation. Even if every individual steps have a known (sometimes involved) solution, we show that plugging-in these solutions together yields a strategy that solves the constrained optimization problem. Our main results are as follows:

-

•

First, using some sophisticated tools of stochastic approximation (ODE method) and of mirror descent (Fenchel conjugate among others), we establish the convergence of our biased procedure towards the minimum of our penalized criterion.

-

•

Second, we establish some new sharp probabilistic upper bounds dedicated to the simulation of the CIR process that are necessary to assess the influence of the number of assets on our stochastic algorithm. These bounds are at the cornerstone of our work and of crucial importance for the fine tuning of the numerical implicit Euler scheme.

In what follows, we carefully study the influence of the number of considered assets and of the discretization step-size on the numerical cost of the overall procedure. We then use our method to construct a Markowitz portfolio envelope [33] that crosses the risk (built with the CV@R) and the expected return to identify the optimal investment strategy.

This article is organized as follows. In Section 2 we detail the optimization problem and the stochastic mirror descent that we propose. We state the almost sure convergence result as well as the non asymptotic bounds that are proved in Appendix B. Then in Section 3 we describe the structure of a portfolio of interest and the simulation strategy. In particular we highlight the link between the step size of the discretization and the bias that will be induced in the SMD algorithm. Finally, we illustrate our results in Section 4 both on simulated and on real data.

2 CV@Rαconstrained mean value optimization

2.1 Financial model and constrained optimization

We consider the relative return of a portfolio, described by a random vector , that is composed of assets whose capital at the initialization time is scaled to . We address the question of the optimal investment strategy in order to maximize the mean relative return at a fixed time horizon where , i.e. each random variable corresponds to where is the price of asset at time .

An investment strategy corresponds to an allocation of the initial capital, modeled by a collection of positive weights that belongs to the dimensional simplex denoted by and defined as:

We are interested in a constrained optimization of the mean of the random variable defined by:

The constraint we are using involves a risk measure, named the conditional value at risk, which quantifies the mean value of a loss given that a loss has occurred. More precisely, if refers to a chosen risk level, corresponds to the classical statistical quantile defined as:

while , that defines the active constraint we will use, is the mean value of the loss when is below , namely:

| (1) |

Note that here, we implicitly assume that the risk level is chosen such that the associated quantile is negative, which implies that is a positive quantity.

Then, for any fixed positive level , the optimization problem of with CV@Rα constraints we are interested in, is the problem defined by:

For our purpose, we also introduce the unconstrained penalized optimization problem: we consider for any the solution of the following (convex) optimization problem:

The (standard) following result is key for our forthcoming analysis.

Proposition 2.1.

The collection of the two convex problems and are equivalent. More precisely, for any that defines a feasible constraint, a solution exists such that:

Moreover, is a decreasing function of . Oppositely, any solution of solves with .

We emphasize that this latter result is the keystone of our forthcoming analysis: instead of solving directly , we will instead define a collection of penalized problems for several values of . Proposition 2.1 then establishes that this approach leads to optimal portfolio allocation under CV@R constraints. We also highlight that the relationship between and remains unknown and challenging to obtain. The proof of this Lagrangian formulation is deferred to Appendix A. Using the result of [43, 29] and in particular the convex representation of the , we observe that:

where is the convex coercive Lipschitz continuous and differentiable function defined by:

where .

We emphasize that despite the definition with , when has an absolutely continuous distribution with respect to the Lebesgue measure, is differentiable (we refer to [10] for further details on this remark).

Then, we deduce from Proposition 2.1 and the above representation that the collection of the optimization problems are then described equivalently by the convex unconstrained problem:

| (2) |

where the key function is defined by:

We emphasize that forms a collection of convex functions defined on , coercive w.r.t. and that enables to avoid the CV@Rαconstraint with a suitable reparametrization of the problem.

2.2 Biased stochastic Mirror Descent

To solve the minimization problem (2) we are led to use stochastic approximation theory, that originates in the pioneering works of [40] and [41] since the (convex) function is written as an expectation.

However, we encounter here specific difficulties. First we need to handle the minimization over the simplex . Second, the random variables involved in cannot generally be simulated exactly, and it will therefore be necessary to control the bias coming from the stochastic simulation. Lastly, note that even though is differentiable, it is the expectation of a non-differentiable function of which will require some specific attention in the following algorithms.

2.2.1 Deterministic case

Mirror Descent (MD below) originates from the pioneering work of [35] and permits to naturally handle constrained optimization problems especially when the mirror/proximal mapping is explicit, which is indeed the case for a convex problem constrained on (see e.g. [30],[16]). The MD approach has the nice feature to define a smooth evolution that lives inside the constrained set without adding some supplementary projection step and “pushes” the frontiers of the simplex at an infinite distance from any point strictly inside . Though we will need to encompass the stochastic framework, since is defined through an expectation which is not explicit, for the sake of clarity we describe first the deterministic version.

For this purpose, we first introduce the strongly convex negative entropy function over the simplex of probability distributions, defined by:

If refers to the standard Euclidean inner product, the Bregman divergence is defined by:

This Bregman divergence will induce the natural metric associated to the component involved in the problem . In the same way, we also introduce the standard Euclidean square distance over , which may be viewed as a Bregman divergence. It then leads to a Bregman divergence over pairs and defined as:

which is the Bregman divergence associated to the strongly convex function:

We emphasize that the strong convexity of induces the following lower bound:

| (3) |

The (deterministic) MD with a step-size sequence consists in minimizing from to the first order Taylor approximation of penalized by the Bregman divergence. To alleviate the notations , we will denote by the position of the algorithm and generally an element of . We observe that the MD iterative step corresponds to:

A remarkable feature is that this latter minimization can be made explicit :

where the first equation has to be understood within a dimensional vector structure.

For a fixed , we define the minimizer of . Following the work of [12, 35], it can be shown that an averaged version of the sequence defined by

satisfies the next error bound:

Theorem 1 (Proposition 1 in [30]).

For any , we note by

then

where .

It is possible to produce several variations around this previous result. It is also possible to assess an upper bound on , using in particular Equations (4) and (5) stated below, which implies

Nevertheless, we emphasize that we will not use this upper bound as our study will be more involved. We should only keep in mind that it is possible to finely tune the step-size sequence to obtain a upper bound. We refer to [30] for further details.

2.2.2 Stochastic Mirror Descent (SMD) using biased simulations

In our problem, and involves the computation of several expectations, which are not explicit and for which the computational time of approximation may not be reasonable. If we denote by and the partial derivatives with respect to and , and using that is expectation of a convex function, we then verify that:

| (4) |

and

| (5) |

Remark 1.

We formulated the above convergence and rate estimation results for . However, these results would stay true as soon as the key function is convex when we can access to a sub-gradient, which has been shown to be compatible with mirror descent.

We assume that we observe a sequence of mutually independent random variables that are also sampled independently from the previous positions of the algorithm. The expressions (4) and (5) lead to a natural (possibly biased) stochastic approximation of with the help of the sequence . Assuming that the algorithm is at step at position , we introduce the stochastic approximation of the sub-gradients:

| (6) |

We now describe the necessary assumptions on the sequence to build a consistent SMD algorithm.

Assumption 1.

Biased simulations

Let and denote the distributions of and respectively. We assume that the sequence satisfies both:

| (7) |

and

| (8) |

where stands for the Wasserstein-1 distance.

The sequences and translate the fact that we may observe some biased realizations of the assets at step , the perfect simulation framework being translated by for all integer . The Wasserstein distance used in is indeed an easiest way to upper bound the bias naturally involved in our approximation procedure. Indeed, Equation (23) (see below) will involve the Kolmogorov distance instead, denoted by below, which quantifies the difference between cumulative distribution function. As the discretization of S.D.E. with (implicit) Euler scheme are well understood in terms of Wasserstein-1 distance, and because of the straightfoward inequality , we prefered to introduce Assumption 1 in terms of .

We emphasize that both and might heavily depend on the dimension of the vector . A specific example will be detailed below in our work.

The method we propose is then defined with Algorithm 1.

The next result states the asymptotic almost sure convergence of the sequence constructed in Algorithm 1 towards the target point . Under a suitable assumption on the biased sequences and , we derive the next result.

Theorem 2 (Almost sure convergence of the biased SMD).

Assume that

and that the bias sequences and introduced in Assumption 1 satisfy

then:

-

-

The Cesaro average defined by

(9) is almost surely convergent and

-

Assume that:

then the sequence almost surely converges and verifies that:

The results obtained in and are rather classical in the stochastic optimization community. The difficulty here is to derive a “Lyapunov” function and then to quantify the effect of the bias induced by satisfying (7) and (8). To do so, we will follow the arguments developed in [30] in order to obtain a recursion expression but we will need to use some ad-hoc supplementary steps to handle the bias and to use the Robbins Siegmund theorem. The last item is much more difficult to obtain, roughly speaking we use the O.D.E. method introduced in [15]. Even though it is a standard tool in stochastic optimization, applying this method to our framework is challenging because of the mirror descent O.D.E. and it deserves some sophisticated additional developments that are far from being a straightforward application of [15]. In particular, we will need to use and adapt some fine results of [34] to our framework. The proof is given in Appendix B.

Asymptotic results such as the one stated in Theorem 2 are commonly criticized because algorithms are always ran within a finite number of iterations. In particular, Theorem 2 does not provide any insight on the rate of convergence of the method, which may crucially influence the practical usefulness of the algorithm. Nevertheless, it shows that Algorithm 1 converges and minimizes the function up to a Cesaro averaging procedure (see and of Theorem 2). It may be shown indeed that the algorithm converges without Cesaro averaging at the price of a more stringent condition on the terms involved in the bias of the algorithm quantified by and .

To cope with the legitimate asymptotic criticisms, we also state non asymptotic theoretical guarantees for the value of the objective function.

Theorem 3 (Finite-time guarantees).

Finally, we aim at applying these guarantees in the case of a finite horizon of computation and in this view, can be controlled using a recursion inequality (35). We consider the specific case of the SMD with a constant step-size sequence stopped at iteration :

We will also assume a constant upper bound of the bias in the simulation of the random variables : we denote by its resulting impact in the SMD. This is legitimate since we can reduce this bias with the use of an arbitrarily small discretization step-size, which of course harms the computational cost. More precisely we consider fixed values of and such that:

Corollary 2.1.

For a given , if are chosen such that

with , then there exists large enough such that:

This previous corollary is built using the optimal tuning of the parameters and derived from our proof that is detailed in Appendix B.2. Therefore, these values may be seen as purely theoretical as we do not exactly know the value of . Nevertheless, any upper bound of may be used to derive a strategy and an upper bound of the excess risk (see Equation (37) in Appendix (B.2)). In the meantime, the choice:

yields:

which is slightly worse than the upper bound stated in Corollary (2.1).

3 Portfolio hedging under constraint

We aim to apply our optimization strategy to the specific situation of portfolio hedging. As a consequence, we precise the structure of , a portfolio of financial assets, and detail the strategy of biased simulation that can be used. We will illustrate this setting using numerical simulations in Section 4. We are exactly in the field of application described in Section 2.

3.1 Description of the portfolio dynamics

In what follows, we consider the situation where contains assets: a return obtained as the baseline short-term interest rate Cox-Ingersoll-Ross process or CIR, with no drift, and a family of geometric Brownian motions that encode some risky assets in the portfolio.

Recall that the CIR has been introduced in [19] as a diffusion process and that it is commonly used for the description of the dynamics of interest rates. The CIR short rate model induces a trajectory , whose stochastic differential equation depends on a triple and is given by:

| (10) |

where stands for a standard real Brownian motion. The parameter stands for the long-time mean of the short rate while quantifies the strength of the mean-reversion effect. The volatility is multiplied by , and the condition guarantees that the interest rate remains positive with probability . We refer to [24] for further details. This almost sure positivity motivated our decision to use the CIR process instead of the Vasicek one. Moreover, the CIR model also incorporates both the mean reversion and the conditional heteroscedasticity since the volatility of the short rate process is increased when the short rate increases.

The assets are then described by the following system of stochastic differential equations:

| (11) |

where refers to a multivariate Brownian motion with correlated components. For the sake of simplicity, these components are assumed to satisfy:

but more general correlation structures could be handled in our framework with further efforts. The correlation matrix is the symmetric positive matrix, denoted by .

The first process corresponds to a neutral risk process whereas each geometric Brownian motion corresponds to a specific risky asset parametrized by known parameters and . We refer to Pitman and Yor [39] and to Gulisashvili and Stein [26] for several details on these classical processes used (among others) for portfolio modeling.

Below we also assume that all the parameters that describe the CIR evolution and the portfolio dynamics (see Equations (10) and (11)) are known and we are simply interested in the optimal hedging strategy, i.e. we are looking for the optimal associated to the optimal mean return penalized by defined in Equation (2) at time . As indicated in Section 2, we will use a Stochastic Mirror Descent strategy and we then need to sample some realizations of at time . Before detailing our sampling strategy, we summarize our assumptions on the parameters.

Assumption 2.

Assumptions on the portfolio parameters

We assume that:

-

i)

the CIR parameters satisfy and .

-

ii)

the correlation matrix of the Brownian motions in invertible.

These assumptions on the coefficients defining the CIR ensure a control of the moment of the weak error rate as well as exponential integrability of the integral of the CIR for all time (see Appendix C).

3.2 Simulation of the portfolio

We are interested in an efficient simulation method that satisfies Assumption 1: both a good approximation of the law of (7) and a bias upper bound of the form (8).

For this purpose, we emphasize that each G.B.M. used in Equation (11) may be simulated exactly since an exact representation of is available:

In the meantime, we can also observe that some exact simulation method exists for the CIR process sampled at a given fixed time. Nevertheless, the CIR process induces some numerical difficulties.

-

•

First, the SDE (10) is not explicitly solvable at any time so that the integral of the CIR between and needs to be approximated.

-

•

Second the correlations between the different Brownian components of the portfolio are hardly compatible with the existing exact simulation methods of the CIR: the presence of correlated noise, which is commonly accepted in financial modeling, is hardly tractable with the use of an exact simulation of the CIR (with the help of square distributions, see, e.g. [4]).

-

•

Third, one viable strategy to obtain an approximation could be the use of a discretization scheme as the implicit Euler or Milstein schemes with a fixed step-size for example, thanks to a recursion of the form:

where corresponds to an iterative update that uses the position and is a two dimensional Gaussian innovation with a specific covariance. Nevertheless, such an attractive point of view induces some theoretical difficulties because of the form of the function we need to approximate. This function is non-smooth and unbounded, which generates some technical difficulties when trying to use or adapt classical approaches on weak discretization errors.

We are led to develop our own ad-hoc simulation of the portfolio and prove its associated properties on the approximation.

Correlated Brownian motion

For this purpose, we introduce some independent standard Brownian paths and use the Cholesky decomposition to encode the correlations and recover correlated Brownian motions .

More precisely, the Cholesky decomposition used on yields a matrix such that:

| (12) |

We now define .

There are two important consequences of constructing for in this way. The first one is that the Cholesky method yields a lower triangular matrix whose first line is :

In particular, we see that we can take and is independent of . The components may be simply written as:

The second important and standard consequence is that these stochastic processes for are indeed Brownian motions with the desired covariance matrix.

Geometric Brownian Motion simulations

From now, we consider and we alleviate the notations by noting , and . The asset at time for all is a Geometric Brownian motion driven by , and we have:

| (13) |

since when .

Interest rate simulation

Finally we focus on a discretization method for the CIR process. We mention that discretizing the CIR process leads to some theoretical issues, as the coefficients in the SDE are not uniformly elliptic and bounded, as assumed in the seminal works of Bally and Talay [8]. Besides, a classical explicit Euler scheme generates positivity issues (because of the square root). However, many authors, notably Alfonsi [1, 2] proposed implicit Euler schemes and provided weak and strong error rates in the previously mentioned works. We choose to use an drift-implicit Euler scheme which was introduced by [1] and studied in numerous articles [21, 3] . The drift-implicit Euler scheme on a discrete time grid can be written by considering the SDE satisfied by which leads to

where . This implicit scheme can be solved explicitely on from iteration to iteration , which ensures the positivity of the scheme . In particular, the update from to is given by:

| (14) |

Convergence results for this discretization scheme will be recalled in Appendix C.

We then use the integral representation and propose to approximate with a Riemann integral approximation between and :

This leads to the definition of our approximation:

| (15) |

Overall simulation algorithm

Combining all these steps, we are led to define the following algorithm to compute a biased simulation of .

In order to propose a convergent algorithm derived from Theorem 2, we need to derive an upper bound of the bias induced by Algorithm 2 involving the CIR approximation and the Riemann approximation of its integral computed in Equation (15). The accuracy of our simulations depends on the number of discretization points sampled between and in Algorithm 2 used to build the Riemann approximation (15). It is necessary to assess the accuracy of our method in terms of the value of to make (7) and (8) explicit. The simulation given in Algorithm 2 satisfies the next statements.

Proposition 3.1.

Proposition 3.2.

Assume that the portfolio parameters satisfy Assumption 2 then for any , there exists a constant independent of and such that:

where .

The proofs of these two results is postponed to Appendix C. We emphasize that these two satellite results contain some sharp new estimations of numerical probability nature on the Euler scheme used for the simulation of our portfolio, and may be of independent interest for applications in mathematical finance. They are not so easy to obtain in particular regarding the influence of the number of assets and need some technical computations to obtain this last dependency that is crucial in our stochastic optimization procedure to design an efficient bias reduction strategy.

3.3 Stochastic Mirror Descent with sampling approximation

We finally aggregate the optimization procedure described in Algorithm 1 with our sampling scheme in Algorithm 2 and we address the problem of adapting the step size of the discretization scheme to the step size of the SMD approximation in light of Theorems 2, 3 and Propositions 3.1 and 3.2.

SMD at fixed time horizon

According to our previous results, we can now consider the choice of parameters induced by Corollary 2.1. Recall that we assume a constant step-size sequence and discretizaton step-size . Corollary 2.1 combined with Propositions 3.1 and 3.2 induce that should be chosen as:

which entails that we could choose a discretization step-size close to .

SMD with decreasing step-size sequence

Let us now choose adequate step-size sequences in order to obtain an a.s. convergent optimization algorithm (Theorem 2). Recall that the sequence scales the step-size of stochastic gradient descent and assume that

We now chose the step sequence for approximating the CIR process as:

According to Propositions 3.1 and 3.2, using the notations of Theorem 2, we deduce that:

Assumption in Theorem 2 now reads:

which is equivalent to:

With these conditions on and , we can now derive the non-asymptotic bound Theorem 3. We set , using the notations of Theorem 3, we deduce that:

Using comparisons between series and integral, we find that:

If we use the notation that denotes an inequality up to a constant which heavily depends on the number of assets in the portfolio, we then obtain that:

We point out that choosing and allows for a convergence rate which is similar to the previous case.

4 Simulations

In this brief numerical paragraph, we illustrate the behavior of our algorithm on both synthetic and real datasets. The simulations have been driven using Python 3.7.13 on a standard computer.

4.1 Description of the simulation study

Bregman divergence vs Euclidean projection

In order to assess the specificity and efficiency of our algorithm, we also consider the projected stochastic gradient optimization that is obtained after a stochastic gradient step-size + a Euclidean projection on the simplex of probability distribution. The projection has been exactly computed with the help of the standard recursive method derived from the Lagrangian formulation. Below, we will refer to SMD for the stochastic mirror descent and PSGD for the projected stochastic gradient descent (whose definition is straightforward (see [22, 32, 18]). In what follows, we have used the recent algorithm introduced in [22] to project any points into the simplex of probability measure for which a fast implementation is available in [32] and for which a complexity bound of is established in [18]. That being said, it is also shown in [18] that is the worst-case complexity of the method while in practice the observed complexity is only . A such complexity is also assessed in expectation when using a random pivot strategy as proposed in [27]. As reported in Table 1 of [18], the observed complexity of several projection methods, including the one of [18], is . We have chosen to compare SMD with PSGD with the projection method of [18] as indicated in Section 4 of [18], their state of the art algorithm generally outperforms the other methods for reasonable vectors to be projected into the simplex.

SMD vs. MC-MD

We also compare our algorithm with a batch Monte-Carlo Mirror Descent, e.g. we use a mini-batch simulation instead of a single one at each step of the algorithm. Therefore, in the Monte-Carlo Mirror Descent (MC-MD), an additional loop is included in order to perform a Monte-Carlo estimation of the gradients (4) and (5). Of course, a such strategy improves the quality of the estimation but has a supplementary cost in terms of simulation times. We present below a comparison of the two methods on synthetic data where we will compare the results of SMD and MC-MD in terms of numerical costs in seconds.

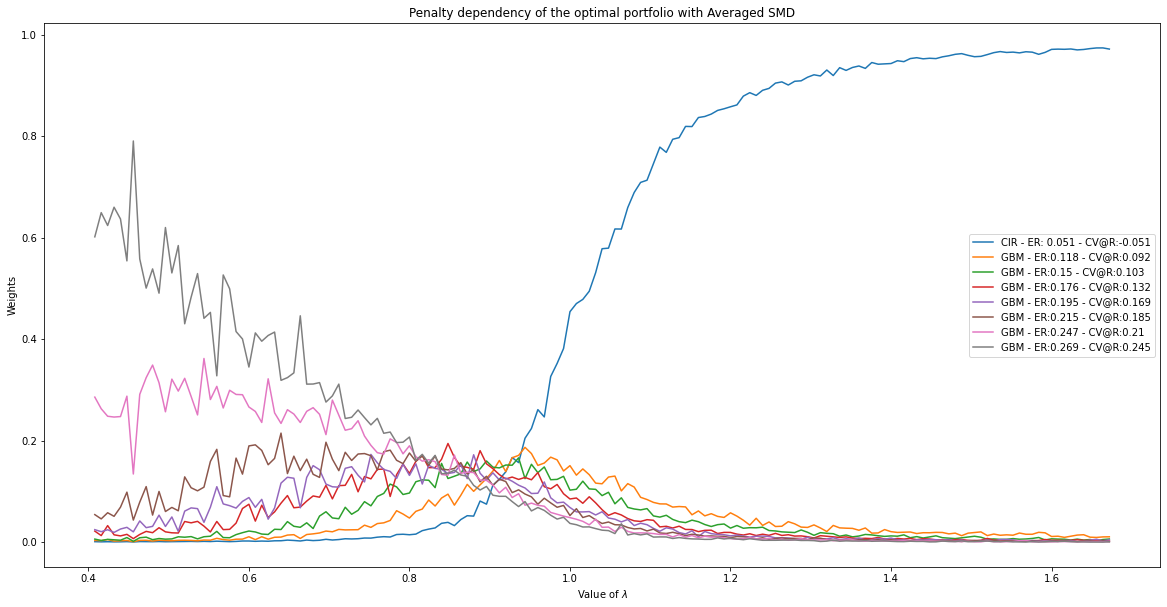

Diversification and influence of

To undertake the influence of the penalty parameter , and in particular its effect on the composition of the optimal portfolio, we vary its value in a regular grid defined with the help of a lower and upper value and a number of points in the grid. According to Proposition 2.1, it is expected that large values of essentially favor low risk portfolio composition whereas small values of allow for risky portfolio with higher expected returns.

Efficient frontier construction

Since the value of has to be determined from a practical point of view, we decided to use the Markowitz efficient frontier approach [33]. The efficient frontier was initially introduced with the standard deviation as a natural measure of the risk of the portfolio. This curve was initially obtained by representing the risk in the X-axis and the Expected Return in the Y-axis. Below, we replace the volatility by the CV@R as a natural risk measure as proposed in [29] to build our Markowitz efficient frontier. The frontier is constructed as follow, for an integer , we compute with our SMD algorithm an approximation of the optimal portfolio associated to this penalty parameter , i.e. the set of weights that approximately minimizes :

For convenience, we denote

where .

We then draw the frontier obtained that may be computed on-line all along the iterations of the SMD algorithm with a Cesaro averaging strategy: if corresponds to a random sequence built with Algorithm 1 stopped at iteration and if is the biased porfolio simulation sequence used all along Algorithm 1, then we may approximate the expected return and the risk by:

We emphasize that since this construction requires the optimization of the portfolio for each value of , it is mandatory to design an efficient and fast procedure to solve each optimization problem, which legitimates the use of our stochastic algorithm.

Finally, we propose to use the Sharpe ratio criterion (see e.g. [45]) to select the optimal portfolio among all the portfolio found on the Markowitz frontier. More precisely, if refers to the risk-free portfolio hedging , the Sharpe ratio criterion selects the portfolio that maximizes the ratio between the difference and the risk measured by .

4.2 Synthetic dataset

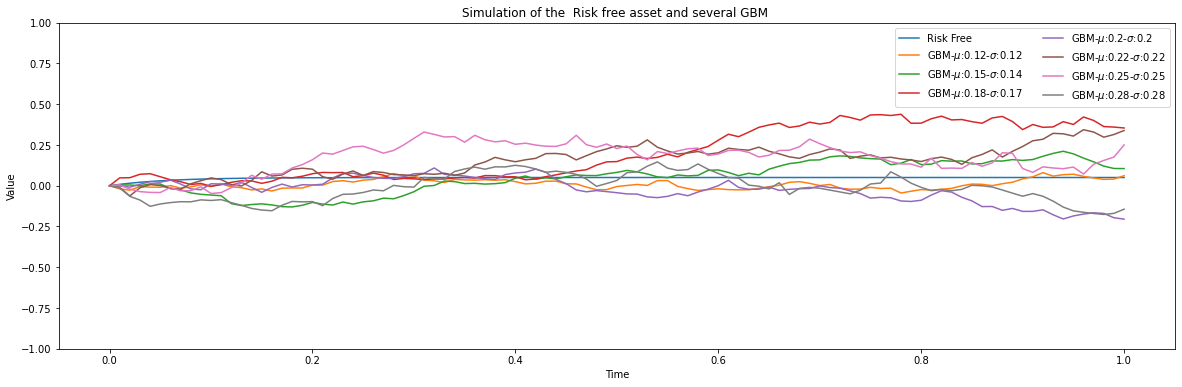

In this first set of simulations, we implement our SMD with purely artificial assets that are driven with a CIR and several GBM, whose parameters are chosen such that the mean reward / Expected Return (ER for short below) and the individual CV@R monotonically vary together. Figure 1 represents one simulation run of the assets we used. At this stage, we do not use any correlation between assets, which is of course a very simplifying assumption that is typically false for financial application purposes. In a second stage in Section 4.3, we will consider correlated assets.

Comparison between SMD and PSGD

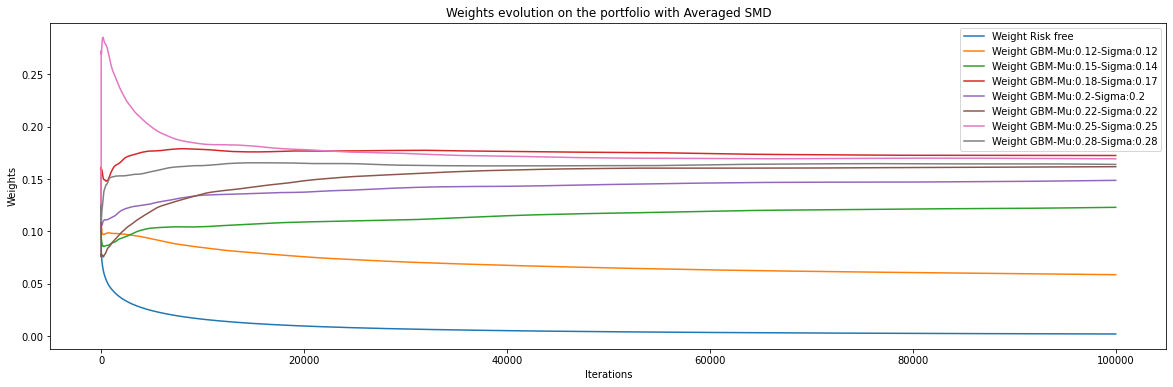

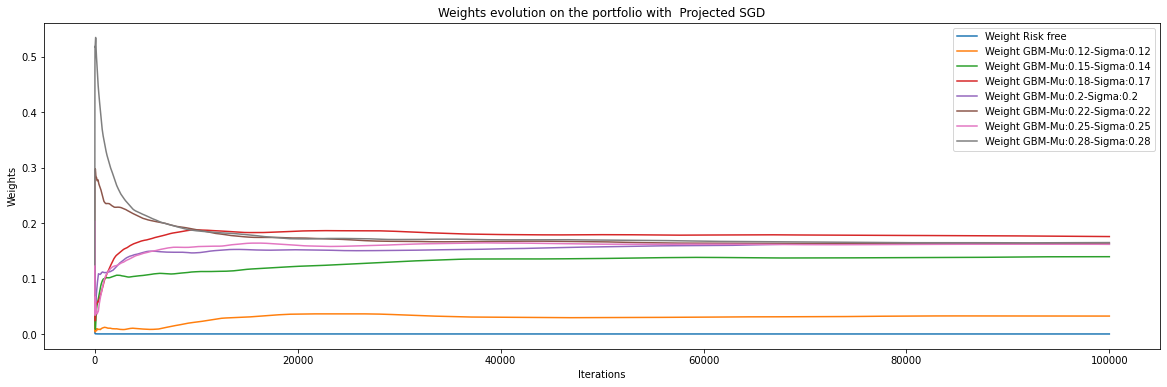

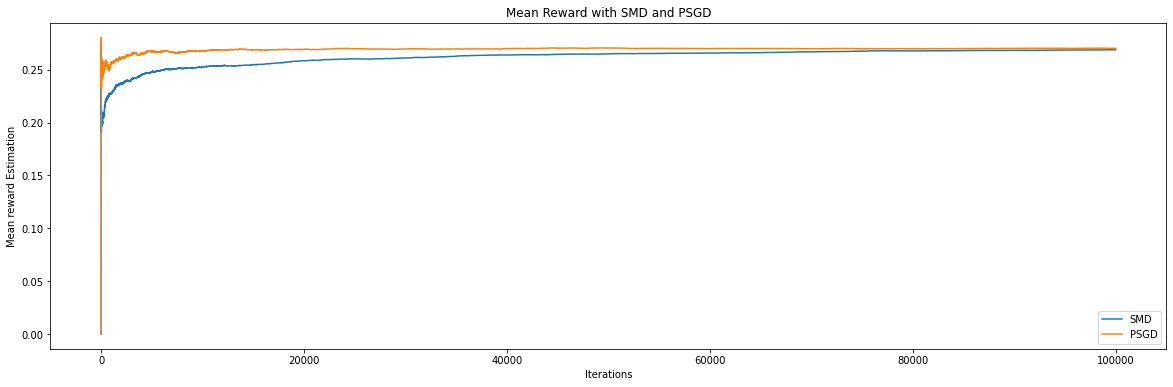

Our first experiment consists in comparing the behaviour of the SMD and the PSGD. The value of used here is .

Figure 2 shows that there is no real evidence that SMD and PSGD lead to very different results in terms of the rate of convergence of , even though as indicated in Figure 2 the limiting weights reached by the two algorithms may not be the same. As indicated in Figure 3, the performances in terms of ER and CV@R are equivalent, which indicates that the convex function may have an infinite set of minima, with a continuum of critical points. Even in this theoretically difficult situation, the trajectory of SMD (and the one of PSGD) almost surely converges as indicated in Theorem 2 and as shown in Figure 2.

Even though both algorithms achieve almost the same results in terms of weights, CV@R and ER, the numerical cost associated to the Euclidean projection is important and prevents from the use of the PSGD with a large number of assets. Table 1 provides a brief comparison of the the computational time ratio between PSGD and SMD, which demonstrates that SMD with several dozen of assets requires generally at least times less computations when compared to the update with PSGD. This phenomenon is of course amplified when increases since the projection algorithm requires more and more operations in larger dimensions.

| 2 | 3 | |

| 3 | 5 | |

| 4 | 6 | |

| 5 | 7 |

All the more, as indicated in Figure 3 (the same conclusion can be drawn from Figure 2), the speed of convergence of SMD seems fastest than the one of PSGD from a numerical point of view. Of course, this remark is purely based on empirical observations from numerical simulations and not on a mathematical results as the theoretical rates of convergence of the methods are equivalent (both rates evolve as where is the number of iterations of the algorithms and as with the supplementary Ruppert-Polyak averaging strategy). This is certainly due to the fact that the averaged SMD algorithm evolves smoothly over the simplex while the averaged PSGD approach is much more irregular due to the sequence of gradient step outside + projection inside the simplex. Finally, this last remark associated with the supplementary computational time due to the projection over the simplex (instead of the instantaneous mirror update) amplifies the benefits of SMD when compared to PSGD regarding the speed of computation. This last remark is inline with some recent observations in the machine learning community (see e.g. [47]).

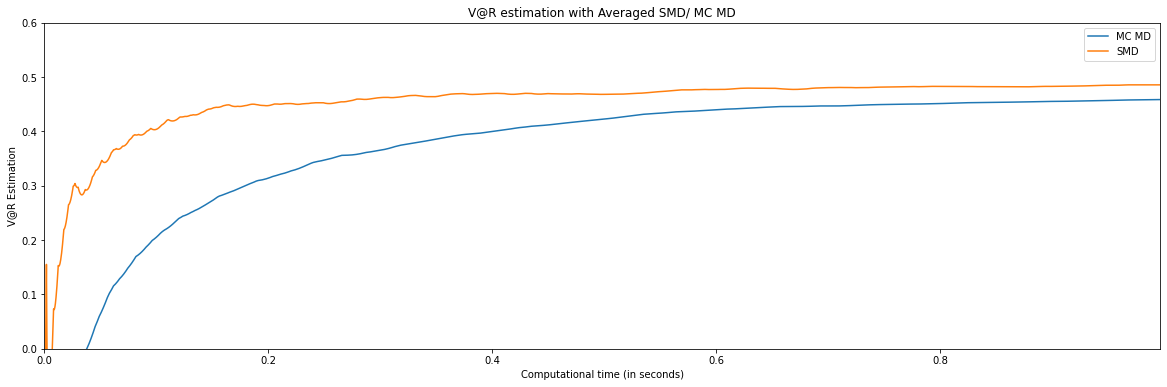

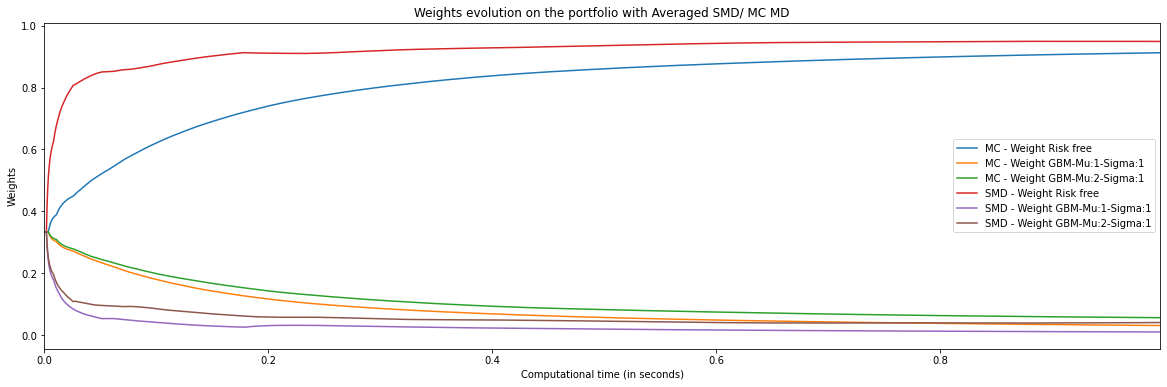

Comparison between SMD and MC-MD

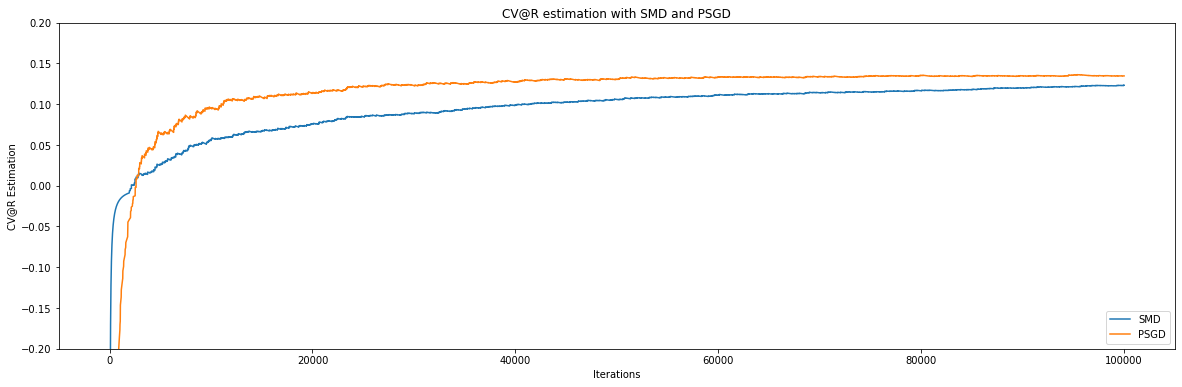

We now present the result of the comparison of SMD and MC-MD. To take into account the computational cost of the MC step, we represent the estimation of the algorithm with respect to the computational time (in second). In these simulation, we draw 10 independent realization of the portfolio in the MC step. We observe that the supplementary accuracy of the estimation of the gradient, obtained at each iteration, is not sufficient to overcome the additional supplementary cost (in terms of seconds) generated by the Monte-Carlo step. As indicated by the right hand side of Figure 4, it appears that both SMD and MC-MD converge to the same portfolio when we push the number of iterations (e.g. the computational time), which lead to the same value of the V@R of the portfolio. We have compared in Figure 4 the learning speed of SMD and of MC-MD of the optimal weights and of the optimal V@R. Our simulations seem to recommend the use of a single stochastic simulation per iteration instead of the use of a mini-batch MC strategy for the problem we are studying.

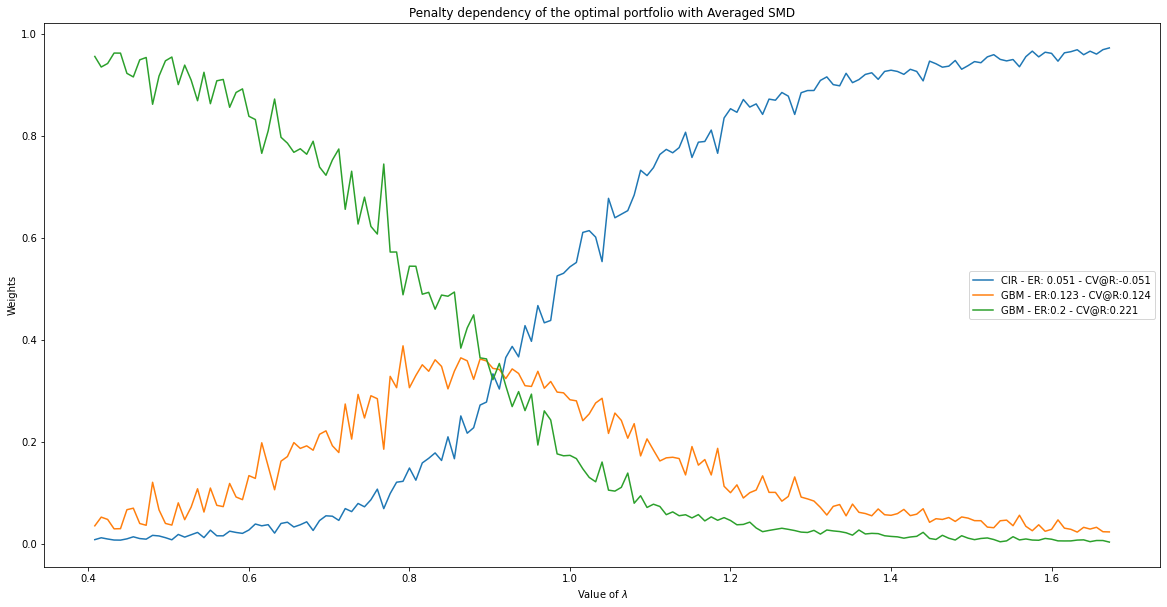

Effect of the penalty parameter

In Figure 5, we assess the influence of the penalty coefficient involved in on the optimal solutions obtained with the SMD. The experiments have been set up with 3 and 8 assets in the portfolio. The fluctuations of the curves in Figure 5 are due to the early stopping strategy we adopted to limit the computational cost, but the following conclusions are highly trustable since the evolution of each curve is rather clear. We have indicated in the legend of each subfigure in Figure 5 the ER of each individual asset that is estimated on-line with our algorithm, as well as the CV@R. We observe that for small values of , the optimal portfolio with 3 and 8 assets favor the most risky ones and do not weight the risk-free component. It is of course the opposite behaviour for large values of when essentially the CIR component gathers the essential weight of the portfolio. Finally, in the intermediary regime, the CV@R penalty generates a product diversification, which is recovered both on the left and on the right of Figure 5, which is also exactly the objective of the CV@R penalty.

4.3 Real dataset

We briefly detail how we shall use our algorithm to estimate optimal portfolio. This short numerical paragraph should be understood as a proof of concept study since we believe that it illustrates the ability of our method.

Yahoo! dataset and parameters estimation

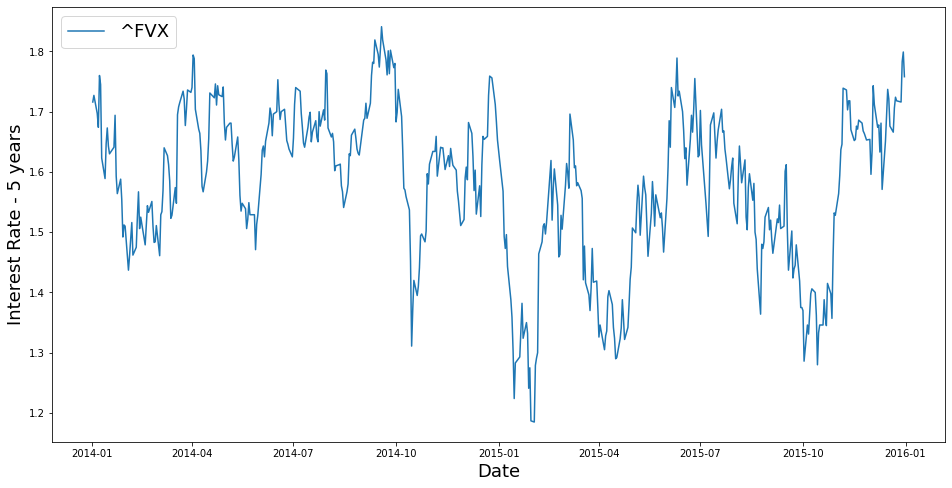

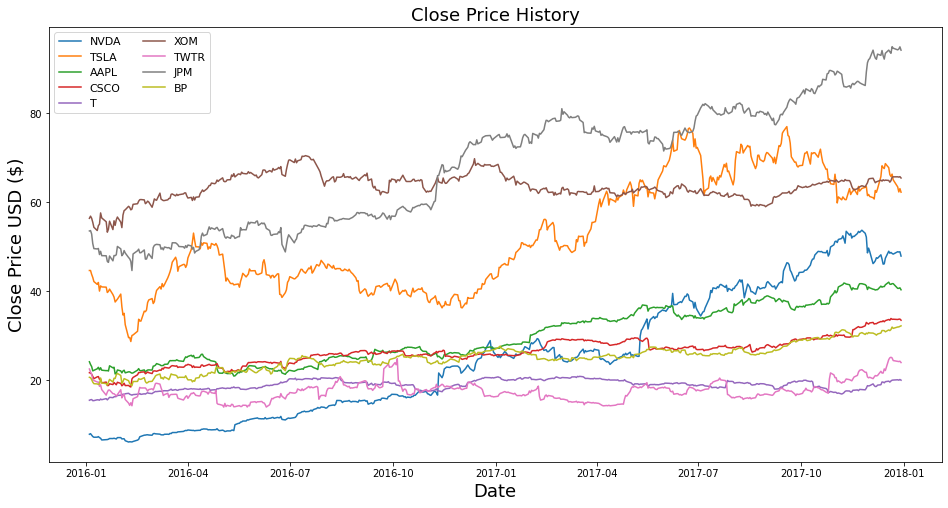

In this final study, we consider some stock prices that are daily recorded on the Yahoo! website https://finance.yahoo.com/lookup and that are freely available with the yahoo-finance API of Python [37].

We use the daily dataset of the Treasury Yield 5 Years ( FVX) to calibrate the null risk asset as well as several assets that are detailed in Figure 6, between 2014 and 2016 (to avoid the period of negative interest rates). We model the FVX time series as a daily realization of a CIR stochastic model whereas risky assets are considered as correlated GBM. Parameters are estimated following the optimal martingale method as it is reported in [25] as it outperforms the discretized log-likelihood maximization approach (for discretely observed CIR realizations). We refer to Equation 4.2 for the drift coefficients and Equation given at the end of Section 4.3 of [25].

Concerning the GBM, we estimate their coefficients ( and ) with the log-return series, which is a standard procedure described among other in Section 3.2.3 of [24] for example.

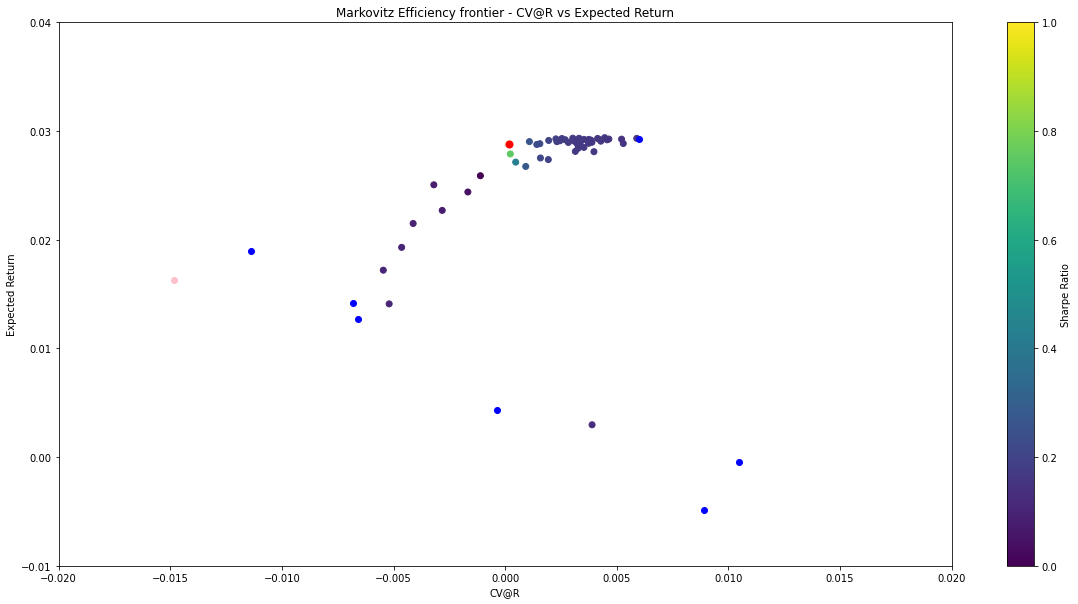

Markowitz efficient frontier with CV@R

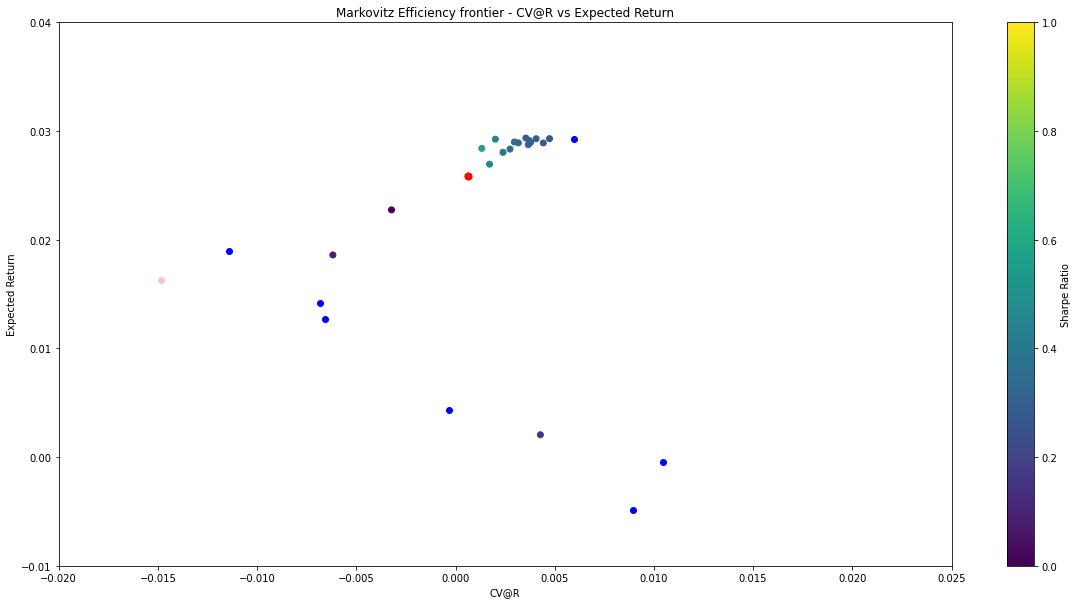

Once the parameters are estimated, we assume that their values are kept fixed for the next daily observation so that we are able to use our SMD Monte-Carlo approach to estimate the optimal portfolio associated to these financial assets. We then use our SMD to estimate the Markowitz efficient frontier, adapted with the CV@R as a measure of risk of the portfolio. We represent we obtain in Figure 7 for two different level of quantiles ( and ).

We use for the construction of our frontier a discretization of the SDE and compute the return of the portfolio for T=30 days. The red point represents the position of the "optimal" portfolio according to the Sharpe ratio. The computational cost for the construction of the Markowitz frontier with 10 assets and a time window appears to be reasonnably fast since we compute these frontiers on standard PC with Python 3.0 in less than 10 minutes each. As indicated in Figure 7, SMD produces each time an optimal portfolio that really balances the CV@R and the ER.

Competing Interests

The authors declare no competing interests.

Appendix A Lagrangian formulation

This appendix is dedicated to the proof of the Lagrangian unconstrained formulation used to deal with the CV@Rαconstraint.

Proof of Proposition 2.1.

We observe that is a continuous convex function, defined on the convex simplex and is a convex optimization problem defined with a constraint defined through a CV@Rαinequality. It is well known that CV@Rα induces a coherent measure of risk, which implies the two important properties of positive homogeneity and sub-additivity. We refer to [38] for this important remark, and to [5, 6] for seminal contributions on risk measurements in mathematical finance. The important consequence of a such coherence is the convexity of the function that defines the constraint in . We verify that :

We are led to define the convex function that induces the constraint in by:

We shall observe that the collection of functions defines a family of convex constraints and such that for all , the constraint is strictly feasible: there exists that is an interior point such that . For a such , we then define the Lagrangian function:

From the Slater condition, we deduce that the strong duality involved in holds: there is no duality gap and primal and dual optimization problems coincide. In particular, the Karush-Kuhn-Tucker conditions are satisfied: the solution of the primal problem verifies:

| (16) |

and the complementary slackness is verified for the pair :

| (17) |

We now establish the monotonous property. We consider a pair and consider and derived from the previous Lagrangian equation. We know that the complementary slackness condition holds for both and . Equations (16) and (17) entail:

| (18) |

where we used in the last line Equation (17) at point . Since Since and while and , we deduce from Equation (18) that:

It finally implies that

We now consider the penalized criterion with , we verify that:

It implies that:

Obviously, we also observe that solves for , e.g.:

∎

Appendix B Proof of the theoretical results on the SMD

B.1 Almost sure convergence of the algorithm

Below, we will use some standard results that are valid for any Bregman divergence , whose statements are given below. We refer to [35] for further details.

Lemma B.1 (Three points lemma).

For any triple of points , one has:

Lemma B.2 (Gradient of the Bregman divergence).

For any pair of points , one has:

With the help of these lemmas, we derive the proof of the almost sure convergence result stated in Theorem 2. The main issue generated by our biased simulation setting is that involved in Equations (4), (5) and (6) acts non-linearly on in our stochastic approximation term, which lead to a significant amount of theoretical difficulties.

Proof of Theorem 2.

Let us recall that throughout the proof, the position of the algorithm is and that we denote by a generic point of the set .

Proof of .

The proof is divided into three steps. We first write a biased descent inequality, and then control the size of the bias induced by our model before using the Robbins Siegmund Theorem.

Step 1: Biased descent inequality. The main point here is to obtain a recursive inequality on , where is a point that minimizes . Our starting point is the definition of :

where we recall that is the stochastic approximation of the sub-gradients:

The first order condition entails that:

Using Lemma B.2 on the second term, we deduce that:

We then apply Lemma B.1 with and and obtain that:

Using the strong convexity of stated in Inequality (3), we deduce that:

which can be written as:

| (19) |

Let us first handle the last term of the right hand side:

The Young inequality leads to:

| (20) |

where in the last line we use that

associated with (see Equation (6)).

In the same way, we also have:

| (21) |

We use Equations (20) and (21) in Inequality (19) and obtain that:

| (22) |

We need to handle the biased drift that comes from the sampled random variables involved in . We write:

with is a martingale increment and stands for the bias:

| (23) |

Now, choosing and using this decomposition into Equation (22), we obtain the main descent inequality, which will be the cornerstone of our analysis:

| (24) |

The Cauchy-Schwarz inequality entails:

| (25) |

Now, the Young inequality and Equation (3) implies that:

| (26) |

We then plug Equations (26) and (25) into (24) and obtain that:

| (27) |

Step 2: Bias upper bound. We are led to estimate the size of . For this purpose, we introduce the Kolmogorov distance , defined on real distributions and defined by:

The Kolmogorov and Wasserstein distance for real distributions (see e.g. Theorem 3.1 of [17]) are related as follows:

Using the expression of in (23), its second coordinates verifies :

Using now the variational characterization of the distance on -Lipschitz function, and using that for any , , we have: , we then deduce that:

We then obtain from Assumption 1 Equation (7) that:

We are led to study an upper bound of . We observe that:

We simply observe that in this case, the second term of the right hand side of the previous inequality is upper bounded by thanks to Assumption 1 Equation (8). We deduce that:

| (28) |

Step 3: Conclusion of the proof. We apply the Robbins-Siegmund Lemma to Equation (27): we observe that the compactness of and the existence of a second order moment for leads to the existence of such that:

| (29) |

Proof of

This result is almost straightforward starting from . We verify from that is an almost surely bounded sequence. Hence, almost surely the Cesaro average sequence is a Cauchy sequence and therefore converges towards . We then use the convexity of and observe that

The continuity of then implies that almost surely:

Proof of

The proof of this last point is more intricate and needs the introduction of more sophisticated tools of dynamical systems to obtain the convergence of the overall sequence towards a point of .

Step 1: continuous time trajectory.

We follow the roadmap of [14] that introduces the asymptotic pseudo-trajectories for stochastic algorithms, and [34] that adapts these tools to the mirror descent.

We introduce the mirror map and the Fenchel conjugate defined on by:

Note that the Fenchel coupling verifies that for any :

| (31) |

The Mirror Descent ordinary differential equation is then defined as:

| (32) |

From Equation (3), we know that is strongly convex, which implies first that is a -Lipschitz continuous function (see Proposition 2.2 of [34]). Second, is a continuous bounded function, which implies with the Cauchy-Arzela-Peano theorem that any solution of the Cauchy problem always exists.444It is not clear that is a Lipschitz continuous function, which prevents from the direct use of Theorem 2.4 of [34]. Indeed a such Lipschitz property depends on the distribution of the random variable . Nevertheless, the nature of the gradient dynamics prevents the explosion of the solutions, which compactifies the trajectories and permits to by-pass the uncertainty on this Lipschitz property. We consider any any minimizer of and a solution of (32). Following the arguments of Nemirovski and Yudin [35], we define the Fenchel coupling as:

Note that using (31), . The Fenchel inequality yields for any time . We observe that :

such that is non-increasing with time. In turn, it implies the compactness of any trajectory (and the convergence with a of the value of towards where is the Cesaro average of the trajectory). From any trajectory , we consider any adherence point. If does not belong to , then we can find a compact neighbourhood of and an increasing sequence such that . Using the continuity of we can find a second set and a radius such that

and for which we have:

We use that is -Lipschitz to obtain that:

where the last line comes from Equations (4) and (5). We can deduce that:

Finally, we write that:

This contradicts the compactness of the trajectories and leads to a contradiction. We deduce that and that any adherence point of belongs to .

Finally, we prove that the whole trajectory converges towards . The construction of holds for any in , in particular for . For this particular choice, we verify that:

because is non-increasing and larger than .

Since by construction converges to , then as , which in turn implies that as . We then conclude that the whole trajectory converges towards .

Step 2: stochastic algorithm convergence. To derive the asymptotic behaviour of the SMD, we follow the argument of Proposition 4.1 in [14] . We consider that satisfies the stochastic recursion

We then define the continuous time affine interpolation of using the natural time-scale and and introduce the stochastic process defined as

We still use the decomposition derived from (23):

where the martingale increment satisfies (see (29)):

and the bias term satisfies under Equation (28) and assumption of that:

Then, the Markov inequality and the Borel-Cantelli lemma yields

We then use Remark 4.5 and Proposition 4.2 of [14] and deduce that Assumption A1 of Proposition 4.1 [14] holds. In the meantime, Assumption A2 of Proposition 4.1 [14] is valid from the proof of and the convergence of . Since is a -Lipschitz function, we then deduce that is an aymptotic pseudo-trajectory of the deterministic mirror descent o.d.e. stated in (32). In particular, converges using Step 1 of , which concludes the proof of . ∎

B.2 Proof of the non-asymptotic behaviour (Theorem 3).

Step 1: control of .

Step 2: non-asymptotic control of the position of the SMD.

Going back again to (27), we can now use the convergence of to get:

From the convexity of , we deduce that , and taking the expectation in both sides, we deduce that:

Summing these inequalities from to , we get:

Following the convexity argument of Theorem 2 and the definition of in(9), we deduce that:

| (36) |

which ends the proof.

Proof of Corollary 2.1.

We now consider a fixed step sequence for the algorithm and the discretization stopped at a horizon . More precisely, we assume for and that (28) translates:

We aim at choosing constant values for step sequences adapted to the finite horizon .

Within this framework the step sequences and defined in (33) become

Let us now see how both and should depend on . With these choices, (35) becomes:

Appendix C Proofs associated with the simulation of the portfolio

The main goal of this section is to prove Proposition 3.1 and Proposition 3.2. To this aim, we first need technical properties on the drift-implicit Euler Scheme coupled with the Riemann integral approximation and on the density of the portfolio .

C.1 Properties of the CIR process and its discretization

Conditional moments of the CIR process

We recall some useful properties satisfied by the CIR process and on some important objects that are related to the CIR introduced in Equation (10).

Proposition C.1.

-

is a Markov process and satisfies:

-

i)

If , then remains strictly positive almost surely.

-

ii)

The (conditional) expectation and variance are given by:

(38) and

(39) -

iii)

The CIR possesses an exponential integrability:

The two first items of the previous proposition are classical, and may be found in [24]. The exponential integrability of the CIR process is more recent and may be traced back to [20] (Proposition 3.2). We emphasize that within realistic situations, the values of and for the CIR process are in general linked within a reasonable ratio of , so that the limiting support of is generally significantly larger than . Note also that this last result holds at any horizon time but it may be explicited for with a larger size of .

Proposition C.1 will be useful for deriving some important properties related to the bias of our approximation strategy.

Weak error associated to the implicit Euler scheme

We recall the following statement of [3] proved in [21], that provides an upper bound of the weak error associated to the implicit Euler scheme(14). In the previous reference, a strong error rate of order is also provided with stronger assumptions on the parameters.

Proposition C.2 (Theorem 1 in [3]).

Assume that , then for any , a constant exists such that:

Control of the error in the approximation of the integral of the CIR

Recall the definition of in (47)

Let us now prove two technical lemmas first on the estimation of then on exponential moments.

Lemma C.1.

Assume that the CIR parameters satisfy , then there exists a constant such that, for any ,

Proof of Lemma C.1.

We bound using first the Jensen inequality and then the Cauchy-Schwarz inequality, we obtain that:

Now taking the expectation and decomposing between the approximation error from the numerical scheme at time and the regularity of the CIR process we obtain that:

| (40) |

Let us start with the first term in the right hand side of the equation above. We use the explicit expression of conditional expectation and variances of the CIR stated in of Proposition C.1. Thus, for any with , the bias-variance decomposition associated with Equations (38) and (39) leads to:

We then use again Equation (38) to obtain a recursive expression of :

Therefore

From Equation (39) and a conditional expectation argument we deduce that:

We then obtain that:

We then compute that:

and

Finally we deduce that for some

| (41) |

We now turn to the second term above, that we estimate using the strong error rate of Proposition C.2 for . Assuming , we get:

Since this bound is uniform in , we deduce that :

| (42) |

Combining estimates (41) and (42) in equation (40) gives the conclusion. ∎

Lemma C.2.

For any choice of , if then:

| (43) |

Proof of Lemma C.2.

We use the Cauchy-Schwarz inequality to upper-bound the expectation:

We apply of Proposition C.1 and observe that since , then and:

For the second part, we rely on the recursive expression for stated in (C.2), that we bound using:

Thus

Choosing and , we deduce that:

Using the independence and stationarity of the Brownian motion, we set a standard Gaussian random variable such that , therefore:

where

A straightforward recursion yields:

In particular, we can use this to upper bound the sum with:

We can now bound the Laplace transform, using the independence of the and the Laplace transform of a distribution .

where the last line derives from . From our choice of and , we observe that and . We then conclude that . ∎

C.2 Results on the portfolio

Proposition C.3 (Density of the portfolio).

Assume that is positive definite, then the distribution of at time is absolutely continuous with respect to the Lebesgue measure. Moreover, the density may be written as:

where is a bounded continuous function, whose bound is independent from and .

Proof.

Let us argue first in the case of uncorrelated Brownian motions in equations (11), i.e. when is the identity matrix. The correlated case will again be dealt with using Cholesky decomposition. Note that

The density of the integral of the CIR process can be derived from Pitman and Yor [39], wherein the authors give an expression of the Laplace transform of the integral of a Bessel process. This representation can in turn be used to derive the Laplace transform of the , which upon inversion, gives its density, see e.g. Gulisashvili and Stein [26]. Next, since the assets are geometric brownian motions, their density can be computed explicitly, and we obtain the density of the vector by multiplying these densities together, thanks to the independence of the driving Brownian motions.

Furthermore, to justify the existence of a density for the pair , we can once again cite [26]. This density is denoted by and verifies for any bounded function :

Below, we denote by the marginal distribution of , whose density is bounded on (see among others e.g. [39] and [26]). To describe the other components, we introduce:

and using a conditional expectation argument, we have:

where refers to the dimensional standard centered Gaussian distribution. For a fixed value of , we consider the change of variables:

which is equivalent to and

Since is invertible, the Jacobian of the change of variable is then given by:

We observe that , which leads to:

The previous expression then guarantees that has a distribution uniformly continuous with respect to the Lebesgue measure on , whose density is of the form:

where

The Gaussian density being continuous and bounded by , we then have:

Therefore, is a bounded continuous function, whose bound is independent from and . ∎

Below, we will need to upper bound the probability of sliced events that are defined as follows. Consider a vector of the simplex and , we introduce:

From Proposition C.3, we deduce the following property.

Proposition C.4 (Sliced events).

Consider a portfolio defined by Equation (11). Assume , and that the correlation matrix is invertible. Assume that the initialization is given by . A constant exists such that for any , for any :

Proof.

We consider small enough (whose dependency with and will be precised later on) and we observe that:

| (44) |

Step 1: Let us first consider the second term in Equation (44). We then consider two separate cases.

-

•

If and considering , we then observe that since is a non-negative process, so that .

-

•

Assume now that , using the notations of Proposition C.3, we observe that:

so that

where the last line comes from standard estimation of the Gaussian tail. Choosing small enough, we then deduce that a constant exists such that:

(45) Defining , a union bound then leads to:

Step 2: We study the first term of (44) and for any vector and for any integer , we denote by the vector . For any , we can find such that , so that:

Now, we recall the joint density defined in Proposition C.3 and rewrite the previous inequality as:

We use the Cauchy-Schwarz inequality in order to bound the inner integral:

where the last line derives from . The previous inequality combined with the Jensen inequality and the Tonelli theorem yield:

The expression of obtained in Proposition C.3 yields:

where we use the fact that we integrate over and that the function is bounded. We finally obtain that for a positive constant :

| (46) |

Step 3: Final bound We now choose to balance the size of Equation (45) and Equation (46) in the decomposition (44). Fix , we choose such that , so that:

We also verify with this choice of that:

To balance both contributions, we aim at finding the smallest constant such that:

which is equivalent to

Now we consider the left hand side as a polynomial of degree in and obtain that the inequality is satisfied for any when the constant is chosen as:

Finally we obtain that:

which concludes the proof. ∎

C.3 Proof of Proposition 3.1

Proof.

Let us first rewrite the Wasserstein distance as:

Since the G.B.M. are exactly simulated and the test function is chosen among Lipschitz functions it is sufficient to bound Recall the definition of the approximation in Equation (15), we obtain

where

| (47) |

Using and a three way Holder’s inequality, we obtain that for and such that then:

Using Lemma C.1 and C.2, we deduce that for any choice of such that , we have:

| (48) |

for large enough (independent from ), which concludes the proof. ∎

C.4 Upper bound of the bias term

Proof of Proposition 3.2.

Below, we alleviate the notations and denote by , which is the return of asset at time . From the exact simulation of the G.B.M. , we have that whereas where is a biased approximation of defined in (15). We denote by the repartition of the portfolio and recall that . The goal of this section is to control the bias in terms of a function of the discretization parameter :

From the re-investment condition, we know that and the Cauchy-Schwarz inequality yields:

Since we discretize only the first component, we have that:

We can rewrite the difference as:

Taking the expectation and applying the Cauchy-Schwarz inequality in the second term we obtain that can be bounded by:

| (49) |

We apply Proposition 3.1 and deduce that the second term is of the order . We then focus on the difference of indicator functions. Let us remark that:

thus

where

These two events are handled similarly, we write:

where is given by (47). Let us fix and consider the event , then

and now, observe that:

which lead to control the probability the the portfolio belongs to a slice. Consider a vector of the simplex and , we introduce:

An upper bound for this probability was obtained in Proposition C.4. A constant exists such that for any , for any :

We finally study and write that for any , and using :

where we applied first a union bound and then the Markov and the Cauchy-Schwarz inequalities. We finally obtain from Lemma C.2 and C.1 that:

| (50) |

Combining Proposition C.4 and (50), we deduce that:

Now using this bound as well as (48) in (49) we obtain that:

| (51) |

where the parameters , , and have to be chosen. Note that the constant depends heavily on the number of assets and on the choice of . We optimize only on the two parameters and the quantity:

It is immediate to verify that should be chosen such that

In the meantime, the optimal value of satisfies:

Some straightforward computations show that , which in turn implies that a constant large enough exists such that:

It is then easy to see that the rate may be arbitrarily close to by picking large enough and close to . More precisely, for any , we can find and such that:

∎

References

- [1] A. Alfonsi. On the discretization schemes for the cir (and bessel squared) processes. Monte Carlo Methods and Applications, 11:355–384, 2005.

- [2] A. Alfonsi. High order discretization schemes for the cir process: application to affine term structure and heston models. Mathematics of Computation, 79(269):209–237, 2010.

- [3] A. Alfonsi. Strong order one convergence of a drift implicit euler scheme: Application to the cir process. Statistics & Probability Letters, 83(2):602–607, 2013.

- [4] A. Alfonsi. Affine diffusions and related processes: simulation, theory and applications, volume 6. Springer, 2015.

- [5] P. Artzner, F. Delbaen, J.M. Eber, and D. Heath. Thinking coherently. Risk, 10, 1997.

- [6] P. Artzner, F. Delbaen, J.M. Eber, and D. Heath. Coherent measures of risk. Mathematical Finance, 9:203–228, 1999.

- [7] Y. Atchadé, G. Fort, and E. Moulines. On perturbed proximal gradient algorithms. The Journal of Machine Learning Research, 18(1):310–342, 2017.

- [8] V. Bally and D. Talay. The law of the Euler scheme for stochastic differential equations. Probability theory and related fields, 104(1):43–60, 1996.

- [9] O. Bardou, N. Frikha, and G. Pagès. Recursive computation of value-at-risk and conditional value-at-risk using mc and qmc. In Pierre L’ Ecuyer and Art B. Owen, editors, Monte Carlo and Quasi-Monte Carlo Methods 2008, pages 193–208, Berlin, Heidelberg, 2009. Springer Berlin Heidelberg.

- [10] O. Bardou, N. Frikha, and G. Pagès. Cvar hedging using quantization-based stochastic approximation algorithm. Mathematical Finance, 26(1):184–229, 2016.

- [11] O. Bardou, N. Frikha, and G. Pagès. Computing var and cvar using stochastic approximation and adaptive unconstrained importance sampling. Monte Carlo Methods and Applications, 15(3):173–210, 2009.

- [12] Amir Beck and Marc Teboulle. Mirror descent and nonlinear projected subgradient methods for convex optimization. Operations Research Letters, 31(3):167–175, 2003.

- [13] A. Ben Tal and M. Teboulle. Expected utility, penalty functions and duality in stochastic nonlinear programming. Manage. Sci., 32:1445–1466, 1986.

- [14] M. Benaïm. Dynamics of stochastic approximation algorithms. Séminaire de probabilités de Strasbourg, 33:1–68, 1999.

- [15] M. Benaïm and M. Hirsch. Asymptotic pseudotrajectories and chain recurrent flows, with applications. Journal of Dynamics and Differential Equations, 8(1):141–176, 1996.

- [16] S. Bubeck. Convex optimization: Algorithms and complexity. Foundations and Trends in Machine Learning, (8), 2015.

- [17] L. Chen and Q.-M. Shao. Stein’s method for normal approximation. In An introduction to Stein’s method, volume 4 of Lect. Notes Ser. Inst. Math. Sci. Natl. Univ. Singap., pages 1–59. Singapore Univ. Press, Singapore, 2005.

- [18] L. Condat. Fast projection onto the simplex and the l1 ball. Mathematical Programming Series A, 158:575–585, 2016.

- [19] J.C. Cox, J.E. Ingersoll, and S.A. Ross. A theory of the term structure of interest rates. Econometrica, 53:385–407, 1985.

- [20] A. Cozma and C. Reisinger. Exponential integrability properties of Euler dicretization schemes for the cox-ingersoll-ross process. Discrete and continuous dynamical systems, series B, 21(10):3359–3377, 2016.

- [21] S. Dereich, A. Neuenkirch, and L. Szpruch. An Euler-type method for the strong approximation of the cox ingersoll ross process. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences, 468(2140):1105–1115, 2012.

- [22] J. Duchi, S. Shalev-Shwartz, Y. Singer, and T. Chandra. Efficient projections onto the l 1 -ball for learning in high dimensions. Int. Conf. on Machine learning (ICML), 2008.

- [23] N. Frikha and L. Huang. A multi-step richardson–romberg extrapolation method for stochastic approximation. Stochastic Processes and their Applications, 125(11):4066–4101, 2015.

- [24] P. Glasserman. Monte Carlo Methods in Financial Engineering. Stochastic Modelling and Applied Probability. Springer, 2003.

- [25] A. Going-Jaeschke. Parameter estimation and bessel processes in financial models and numerical analysis in hamiltonian dynamics. PhD dissertation of Swiss Federal Institutde of Technology of Zurich, 1998.

- [26] A. Gulisashvili and E. Stein. Asymptotic behavior of the stock price distribution density and implied volatility in stochastic volatility models. Applied Mathematics and Optimization, 61(3):287–315, 2010.

- [27] K.C. Kiwiel. Breakpoint searching algorithms for the continuous quadratic knapsack problem. Math. Program., Ser. A, 112:473–491, 2008.

- [28] P. Kloeden and E. Platen. Numerical solution of SDE. Springer Science, 1999.

- [29] P. Krokhmal, J. Palmquist, and S. Uryasev. Portfolio optimization with conditional value-at-risk objective and constraints. Journal of Risk, 4(2):43–68, 2001.

- [30] G. Lan, A. Nemirovskij, and A. Shapiro. Validation analysis of mirror descent stochastic approximation method. Math. Program., Ser. A, (134):425–458, 2012.

- [31] Sophie Laruelle and Gilles Pagès. Stochastic approximation with averaging innovation applied to finance. Monte Carlo Methods and Applications, 18(1):1–51, 2012.

- [32] A. Fujino M. Blondel and N. Ueda. Large-scale multiclass support vector machine training via euclidean projection onto the simplex. International Conference on Pattern Recognition, 2014.

- [33] H.M. Markowitz. Portfolio selection. Journal of Finance, 7:77–91, 1952.

- [34] P. Mertikopoulos and M. Staudigl. On the convergence of gradient-like flows with noisy gradient input. SIAM Journal on Optimization, 28(1):163–197, 2018.

- [35] A. Nemirovskij and D. Yudin. Problem complexity and method efficiency in optimization. Wiley-Interscience, 1983.

- [36] Y. Nesterov. Primal-dual subgradient methods for convex problems. Mathematical Programming, Serie B, 120:221–259, 2009.

- [37] [DATA] Python package pandadatareader. getdatayahoo("nvda", "tsla", "aapl", "csco", "t", "xom", "twtr", "jpm", "bp"). start="2016-01-01", end="2018-01-01".

- [38] G.Ch. Pflug. Some remarks on the value-at-risk and the conditional value-at-risk. In Probabilistic Constrained Optimization: Methodology and Applications, Ed. S. Uryasev. Kluwer Academic Publishers, 2000.

- [39] M. Pitman, J . Yor. A decomposition of bessel bridges. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 59(4):425–457, 1982.

- [40] H. Robbins and S. Monro. A stochastic approximation method. The Annals of Mathematical Statistics, 22:400–407, 1951.

- [41] H. Robbins and D. Siegmund. A convergence theorem for non negative almost supermartingales and some applications. Optimizing methods in stat., pages 233–257, 1971.

- [42] R. Rockafellar and J. Royset. Random variables, monotone relations, and convex analysis. Mathematical Programming, 148(1):297–331, 2014.

- [43] R. T. Rockafellar and S. Uryasev. Optimization of conditional value-at-risk. The Journal of Risk, 2(3):21–41, 2000.

- [44] R. T. Rockafellar and S. Uryasev. Conditional value-at-risk for general loss distributions. Journal of Banking and Finance, 26(7):1443–1471, 2002.

- [45] W. F. Sharpe. Mutual fund performance. Journal of Business, 39:119–138, 1966.

- [46] D. Talay and L. Tubaro. Expansion of the global error for numerical schemes solving stochastic differential equations. Stochastic analysis and applications, 8(4):483–509, 1990.

- [47] Z. Zhou, P. Mertikopoulos, N. Bambos, S. Boyd, and P. Glynn. Stochastic mirror descent in variationally coherent optimization problems. Advances in Neural Information Processing Systems, 30, 2017.