Regression graphs and sparsity-inducing reparametrizations

Summary.

Motivated by the important statistical role of sparsity, the paper uncovers four reparametrizations for covariance matrices in which sparsity is associated with conditional independence graphs in a notional Gaussian model. The intimate relationship between the Iwasawa decomposition of the general linear group and the open cone of positive definite matrices allows a unifying perspective. Specifically, the positive definite cone can be reconstructed without loss or redundancy from the exponential map applied to four Lie subalgebras determined by the Iwasawa decomposition of the general linear group. This accords geometric interpretations to the reparametrizations and the corresponding notion of sparsity. Conditions that ensure legitimacy of the reparametrizations for statistical models are identified. While the focus of this work is on understanding population-level structure, there are strong methodological implications. In particular, since the population-level sparsity manifests in a vector space, imposition of sparsity on relevant sample quantities produces a covariance estimate that respects the positive definite cone constraint.

Some key words: Directed acyclic graph; Exponential map; General linear group; Iwasawa decomposition; Matrix logarithm; Sparsity.

1. Introduction

Sparsity, the existence of many zeros or near-zeros in some domain, plays at least two roles in statistics depending on context: to aid interpretation of a high-dimensional interest parameter; and to prevent accumulation of estimation error associated with a high-dimensional nuisance parameter. There is now a large literature concerned with enforcing sparsity on sample quantities, having assumed that the corresponding population-level object is sparse. For an extensive account, see Wainwright (2019).

The present paper barely touches on sample quantities. It is concerned, in the specific context of covariance estimation, with the suggestion (Battey, 2023) that one might systematically induce sparsity on population-level quantities through reparametrization. A precursor to the idea, although the authors did not use this terminology, is parameter orthogonalization (Cox & Reid, 1987). The latter entails a traversal of parametrization space by solving a system of partial differential equations, constructed in such a way that interpretation of the interest parameter is retained, and such that in the new parametrization, the nuisance parameter is orthogonal to the interest parameter in the sense of e.g. Jeffreys (1948, pp. 158,184). In other words, the nuisance parameter is redefined in such a way that it induces sparsity on the relevant block of the Fisher information matrix, a population-level object, thereby reducing its role. Any interpretation of the original nuisance parameter is sacrificed in favour of a more reliable inference for the interest parameter. Inducement of population-level sparsity does not seem to have received subsequent attention until the recent examples highlighted by Battey (2023), although it could be argued that the development of Gaussian graphical models (e.g. Lauritzen, 1996; Cox & Wermuth, 1996) is in this vein, together with the important work on graphical modelling for extremes by Engelke & Hitz (2020).

The main question we seek to address is whether, for a given covariance matrix, not obviously sparse in any domain, a sparsity-inducing reparametrization can be deduced. Battey (2017) and Rybak & Battey (2021) provided a proof of concept for this idea. Their position was that covariance matrices and their inverses are often nuisance parameters, and it is therefore arguably more important that the sparsity holds to an adequate order of approximation in an arbitrary parametrization, than that the sparse parametrization has interpretable zeros. In the case of Gaussian graphical models, the precision matrix is the interest parameter by virtue of the interpretability ascribed to its zeros. Thus, both aspects are of interest and are addressed here. A third type of situation, to which the present paper does not contribute, is when the covariance matrix is a nuisance parameter that has a known structure up to a low-dimensional parameter. This situation is common in some settings, for instance in the analysis of split-plot or Latin square designs with block effects treated as random. The appropriate method of analysis is then residual maximum likelihood (Patterson & Thompson, 1971) or modifications thereof, which implicitly resolves the residual space into suitable orthogonal subspaces associated with a standard analysis of variance, when one exists; see e.g. Bailey (2008) for analysis of variance with random block effects, and McCullagh (2023, Ch. 8) for a discussion of residual maximum likelihood.

The contribution of the work to be presented is manifold. New geometric insight motivates reparametrizations of the set of covariance matrices. Specifically, since every full-rank covariance matrix is positive definite, which in turn is invertible, we associate any positive definite matrix with the equivalence class of invertible matrices that are orthogonally related. The set of such equivalence classes is thus identified with the set of positive definite ones, and the set of full-rank covariance matrices is thereby viewed as a parametrized homogeneous manifold of the general linear group of invertible matrices.

Every invertible matrix can be decomposed in many ways as (a combination of) rotation, scale and shear matrices that represent geometric rigid and non-rigid transformations of a real vector space. From the Iwasawa and Cartan decompositions of the general linear group, invertible matrices are given coordinates based on infinitesimal versions of such transformations, which, modulo the aforementioned equivalence relation, can be used to parametrize positive definite matrices. The unifying perspective so obtained recovers the examples of Battey (2017) and Rybak & Battey (2021) as special cases, while also pointing to new parametrizations whose applicability appears much broader in view of their graphical models interpretation under a notional Gaussian graphical model. Through these insights, the work uncovers an information geometry of Gaussian graphical models via the partial Iwasawa coordinates of the general linear group, which is naturally compatible with the information geometry of Gaussian models (Rao, 1945; Jeffreys, 1946); see §8.2.

While the focus of this work is deterministic, we highlight recent important work by Zwiernik (2023), whose complementary focus on estimation covers the matrix logarithmic sparsity model of Battey (2017) and, more generally, models with linear restrictions on spectral functions of the covariance matrix. While the extension of the Zwiernik (2023) work to the new parametrizations is not immediate, his framework, in respecting the geometry of covariance spaces, is extremely appealing.

Section 2.3 details the geometric insight leading to the reparametrizations of §3, and §2.2 gives a formal treatment of reparametrization. While rigour necessitates such a formalization, which repays careful reading, the key ideas of §3 are understandable from first principles and could be tackled directly, although with some relinquishment of insight. The main results and statistical insights are in §4 and §5.

2. Background

2.1. Notation

The following subsets of the vector space of real matrices are extensively referenced; most of them are matrix Lie groups with matrix multiplication as the group operation: the symmetric matrices ; the skew symmetric matrices ; the general linear group of nonsingular matrices ; the group of orthogonal matrices ; the rotation group of special orthogonal matrices with determinant ; the symmetric positive definite matrices ; the group of diagonal matrices ; the group of permutation matrices ; the group of lower triangular matrices with arbitrary diagonal entries ; the group of lower triangular matrices with unit diagonal entries ; the group of strictly lower triangular matrices . Versions of the upper triangular matrices are defined analogously, and versions of and with positive diagonal elements are differentiated using the subscript . We denote by a generic vector subspace of and by the (interior of a) convex cone within (excluding the origin), an open subset of . We denote by and , respectively, the direct sum and product of two vector spaces; we also use and for the kronecker sum and kronecker product when the context is clear.

With the vectorization map taking a symmetric matrix to a -dimensional column vector, define the half-vectorization map

where the matrix

picks out the upper triangular part of the vectorization, and is a -dimensional unit vector with 1 in position and 0 elsewhere. Its inverse

exists through the Moore-Penrose inverse of . Here and elsewhere, denote the canonical basis vectors for , where is a vector with 1 for its th component and zero elsewhere.

2.2. as a parametrized manifold and sparsity

The set of covariance matrices can be identified with the convex cone . By viewing as a submanifold of the vector space of real matrices we can construct a parametrization that makes it a parametrized manifold. Consider the injective map

that maps a point in to a positive definite matrix within . At every point , the derivative is injective where its matrix representation is of rank . Then and we say that is a parametrization of . A reparametrization of corresponds to an injective map from a domain with non-singular derivative such that there is a diffeomorphism with . The derivative condition ensures that is of dimension . The two parametrizations and are said to be equivalent since , and is a reparametrization of (and vice versa). The commutative diagram in the left half of Figure 1 illustrates the type of reparametrization used in this paper.

In contrast, the statistical model or manifold is determined via an injective map that maps a covariance matrix to a parametric probability measure on some sample space. Every is obtained from unique points in and , and the statistical model given by is impervious to reparametrization of the manifold . Reparametrization of the statistical model amounts to applying a diffeomorphism such that correspondences change but not the image . This form of reparametrization is not considered in the present work.

A sparse matrix with respect to the parametrization is the image under of a sparse vector coordinatized in the standard basis of : zero components of manifest as zero elements in . The structure of sparsity in with respect to the domain depends on how is coordinatized and the map . We will use sparsity to refer to the domain or to the range of a parametrization interchangeably, with context disambiguating the two.

2.3. as a homogeneous space of

Crucial to our approach to reparametrization is the close relationship between the general linear group of invertible matrices and . Concepts from group theory relevant to this paper can be found in Appendix A. Note that is positive definite for every , and the map is invariant to the action for of the orthogonal group. A positive definite matrix can be transformed to any other under the transitive action

of , and is hence a homogeneous space: a differentiable manifold with a transitive differentiable action of . For example, between any pair the invertible matrix transforms to under the above action. The orthogonal group is the stabilizer of and fixes , and we thus obtain the identification with via the group isomorphism

where is the set of equivalence classes or orbits of elements .

The advantage in linking with lies in the use of the Cartan and Iwasawa decompositions of to define new parametrizations of ; they are more familiarly known, respectively, as the Singular Value Decomposition (SVD) and the LDU decomposition of . The Iwasawa decomposition of determines a unique triple such that (see e.g. Terras, 1988, Ch. 4). Since is lower triangular with positive diagonal entries, we also recover the well-known QR decomposition. From the Iwasawa decomposition we have , and we recover the LDU decomposition of the positive definite matrix , which is unique (Golub & Van Loan, 2013). The Cartan decomposition of determines the triple such that ; it can be made unique when elements of are distinct (see Proposition 3.4). Geometrically, the decompositions describe how combinations of rotational, scaling, and shearing transformations of vectors in can be carried out via a single invertible transformation from , and vice versa.

We will focus on the Iwasawa decomposition for the following reason. Triangular matrices in fix a nested sequence of subspaces (called a flag) of with . Triangular matrices in with ones along the diagonal represent a shear transformation in :

that fixes a subspace , where is a linear operator ; in the matrix representation the map is block triangular and belongs to :

Every -dimensional rotation can be expressed a compositions of shears and scaling. For example, when , we have

with a scaling transformation bookended by two shear transformations. Effectively, the rotational component of a positive definite transformation in represented as a positive definite matrix in can be captured through a combination of scaling and shear transformations.

We will see in the sequel that the couple in the Iwasawa decomposition of can be used to parametrize not only a positive definite matrix but also just its rotational component. The Cartan decomposition can thus be derived from the Iwasawa decomposition, and the latter is taken as the fundamental representation for the purpose of this work. A group theoretic justification that relates the corresponding Lie algebras can be found in (Terras, 1988, Lemma 3, p.288).

The Iwasawa decomposition into , and at the group level () has a corresponding Iwasawa decompomposition at the Lie algebra level ()

| (2.1) |

where , and are the Lie algebras of , and , respectively. The four parametrizations considered in this work are based on the constituent terms of (2.1).

3. Reparametrization

3.1. Broad question and solution strategy

The set is the natural parameter domain for parametrizing . Referring to Figure 1, the question we seek to address is whether there is another parameter domain , that is perhaps less natural, but in which a population-level sparsity is present, encapsulating the relevant set of multivariate dependencies. In other words, we seek a reparametrization that induces sparsity on the covariance matrix . The problem is addressed from the opposite direction, by first considering the parameter domains in which sparsity can be fruitfully represented, and then studying the form of multivariate dependencies that are implied by such sparsity. The deduced structures are found to be both necessary and sufficient, so that the direction of interest is recovered through this route.

3.2. Four parametrizations suggested by the Iwasawa decomposition

We take as our object of study for the parameter domain in Figure 1, a -dimensional subset of obtained from judicious combinations of the Lie algebras and . This is enabled by Proposition 3.1 in §3.7 that asserts the existence of a diffeomorphism and thus a unique smooth inverse . From an initial parametrization of in terms of , the discussion above suggests four such maps of the form or , each of which results in a map , since the matrix exponential can be interpreted as the exponential map from the Lie algebra of the Lie group to (Appendix A). In certain cases, non-injectivity of , especially when restricted to certain Lie subalgebras, means that only when restricted to an appropriate subset of does qualify as a legitimate reparameteziation.

With , we consider the four maps

The subscripts on indicate which of the matrix sets, , , and respectively, parametrized in terms of , are represented as the image of the exponential map. In each case belongs to one of the Lie algebras or a direct sum/product of two of them in the decomposition (2.1), and depends on through the basis expansion , where are the canonical basis matrices of dimension , with . The particular form of is given in §§3.3–3.6, and is part of the definition of the reparametrization maps (see Remark 3.1). The maps relate to, and are compatible with, the identification of PD as a quotient manifold. Since is subspace of spanned by the canonical basis matrices of the considered Lie subalgebras, zeros in or correspond directly to zeros in .

A geometrical interpretation of sparsity can be given to the structure induced on through sparsity of and using the Iwasawa decomposition (2.1) of the Lie algebra of and the discussion of §6; a statistical interpretation is available using the partial Iwasawa coordinates for (Terras, 1988, Chapter 4), and is presented in §5 in the context of a notional Gaussian model. We investigate the structure induced on the original scale, i.e. in or equivalently in under the canonical parametrization , through sparsity constraints on , and establish that the uncovered structure is both necessary and sufficient for sparsity of . Importantly, the matrix on the transformed scale can be considerably sparser than , a conclusion with strong statistical implications. We revisit this point in §7 and §8.1. Although many unresolved issues remain in the statistical exploitation of the sparsity, which is ancillary to our present focus, we anticipate the work will stem further developments in this vein.

3.3. The parametrization

The matrix logarithm of a covariance matrix was considered by Leonard & Hsu (1992) for covariance estimation and by Chiu et al. (1996) as a tool to incorporate dependence on covariates. Battey (2017) exploited the vector-space properties of and examined the structure induced on through sparsity of in an expansion of using the canonical basis for , where consists of non-diagonal matrices of the form for and diagonal matrices from of the form .

The commutative diagram (Figure 2) depicts the most relevant directed paths for reparametrization of from a statistical modelling perspective.

Starting from the natural parametrization , where , the same is reached via the more circuitous route involving the composition of three maps. A diffeomorphism that takes to is not available in closed form, however, Proposition 3.1 in §3.7 confirms its existence. The bijective map maps a vector to a symmetric matrix given by the linear combination

Injectivity of , inferred as a special case of Propositions 3.2 and 3.3 in §3.7, then ensures that is a legitimate reparametrization as described in Figure 1 with and .

The use of can be interpreted in three complementary ways. The first arises from Arsigny et al. (2017) who endow with a Lie group structure with as the corresponding Lie algebra. The second interpretation subsumes the first and is geometric; it rests on the fact that the tangent space at in the homogeneous manifold equipped with a Riemannian structure can be identified with , and the matrix exponential coincides with the Riemannian exponential map , where is the tangent bundle. The third interpretation uses the Iwasawa decomposition (2.1) via the decomposition

of as a direct sum of two of the constituent Lie subalgebras of that appear in the Iwasawa decomposition, which implies that where . Every matrix can be expressed as the sum of its symmetric and skew-symmetric parts. The identification implies that the orthogonal component of can be ignored in this parametrization, and the Lie algebra of the orthogonal group containing the skew-symmetric parts of is thus unused.

3.4. The parametrization

Rybak & Battey (2021) considered a spectral decomposition , where is an orthonormal matrix of eigenvectors and is a diagonal matrix of corresponding eigenvalues. As seen in §2.3, the parametrization relates more directly to the Cartan decomposition of via the SVD. However, since every skew symmetric can be decomposed as with , can also be generated from the Lie algebra , which represents the shear transformation of a positive definite matrix defined using the invariant map , where . Additionally, it can be shown that , where is the adjoint representation of the orthogonal matrix in the spectral decomposition of , which links the Cartan and Iwasawa decompositions.

Without loss of generality Rybak and Battey (2021) took the representation in which and considered the map , yielding a different vector space from that in in which to study sparsity. This was done via in the two canonical bases for consisting of matrices of the form for and the diagonal basis in §3.3. In fact, only the component was considered sparse. Allowance for additional sparsity via can be easily incorporated and corresponds to further structure. The new parametrization here is , where is the vector of log-transformed eigenvalues of .

Figure 3 summarizes the two routes to from the initial parametrization . A diffeomorphism is again available, but not in closed form, from Proposition 3.1 in §3.7. The map maps to the two matrices

The map in Figure 1 is then . The situation regarding invertibility of the maps is more nuanced than for the parametrization owing to the aforementioned non-uniqueness of the decomposition and multivaluedness of the matrix logarithm of . For the purpose of the present paper, the implications are negligible, as we can make the parametrization injective under some conditions in . This is clarified in Proposition 3.4 in §3.7. The vector space as the parameter domain in Figure 1 is identified with the direct product of two of the constituent Lie subalgebras in the Iwasawa decomposition of in (2.1).

3.5. The parametrization

The parametrizations in Battey (2017) and Rybak & Battey (2021) made only partial use of the Iwasawa decomposition of . The decomposition 2.1 points to two further parametrizations discussed here and in §3.6. The map is based on the sum of two constituent Lie subalgebras from (2.1), which coincides with another Lie subalgebra of consisting of all lower triangular matrices. The canonical basis for consists of matrices of the form , . Equivalently, the construction can be expressed in terms of upper triangular matrices with an analogous parametrization and there are no substantive differences in the conclusions of §4 and §5.

In the diagram, a diffeomorphism exists by Proposition 3.1 in §3.7. The map maps to

The matrix exponential maps to the unique Cholesky factor of so that , and in Figure 1. As with , invertibility of is not guaranteed without further constraints on since is not injective. This point is revisited in Proposition 3.4 of §3.7.

3.6. The parametrization

This parametrization represents a full use of the Iwasawa decomposition (2.1), and enjoys invertibility without any restrictions on its domain. The so-called LDU decomposition of is , where . Analogously to the previous cases, the matrix logarithm is applied to and the canonical basis , with off-diagonal basis matrices of the form with and diagonal matrices from defined in §3.3, is used to represent in terms of coefficients . To complete the parametrization, consists of the log-transformed diagonal entries of .

The diffeomorphism exists from Proposition 3.1 in §3.7. The map maps to the two matrices

so that . The exponential is injective (in fact, bijective) so that in Figure 1 is a legitimate reparametrization with domain .

As seen in §2.3, a combination of shearing and scaling can mimic a rotation, and a combination of two shearing transforms mimics a symmetric operator. Consequently, the parametrization in essence encompasses the previous three, and this manifests in the sparsity-induced structure in a positive definite matrix under . Specifically, §4, which establishes the structure induced on through sparsity of in the four maps or , ascertains that, in terms of the induced structure, is a generalization of both and . Rybak and Battey (2021) showed that is a generalization of . Thus, is, in this sense, an encompassing formulation, a conclusion that is not apparent from inspection of the forms of the four parametrizations. In §5 these inclusions are clarified further and given a probabilistic interpretation using a notional Gaussian model.

Remark 3.1.

A change of a matrix basis is achieved by the action of a nonsingular as . The group acts equivariantly on the map , since for every and . Hence,

owing to the transitive action of on , and the preimages of and is the same . The four maps are well-defined only upon fixing a basis for the considered Lie subalgebra.

3.7. Injectivity of the four maps

Proposition 3.1, the proof of which is in Appendix B.1, establishes existence of the diffeomorphisms introduced in §3.

Proposition 3.1.

The convex set is diffeomorphic to .

The inverses determine precisely how sparsity in or manifests in a point in the convex cone, and thus, quite straightforwardly, in the covariance matrix . However, they are difficult to determine in closed form. The maps prescribe a path from to (and similarly for ) and can be viewed as suitable surrogates, but need not be diffeomorphisms even when injectivity is guaranteed.

Injectivity of and hinge on injectivity of the matrix exponential, and uniqueness of eigen, Cholesky and LDU decompositions for the latter three. We first consider the matrix exponential.

Propositions 3.2 and 3.3 describe conditions for existence and uniqueness of the matrix logarithm, which affect invertibility of the four reparametrizations in §3.

Proposition 3.2 (Culver (1966)).

Let . There exists an such that if and only if and each Jordan block of corresponding to a negative eigenvalue occurs an even number of times.

Proposition 3.3 (Culver (1966)).

Let and suppose that a matrix logarithm exists. Then has a unique real solution if and only if all eigenvalues of are positive and real, and no elementary divisor (Jordan block) of corresponding to any eigenvalue appears more than once.

Proposition 3.2 covers all four logarithm maps , , and . Conditions that ensures uniqueness in Proposition 3.3 are satisfied only by and . A geometric version of the sufficient condition (“if” part) in Proposition 3.3 claims uniqueness if lies in the ball around , where is the spectral norm of given by its largest singular value. This provides a sufficient (not necessary) condition to ensure that .

Relatedly, perhaps more appropriate from the perspective of reparametrization of , are conditions that ensure injectivity of the matrix exponential . As a consequence of Proposition 3.3, is injective when restricted to Lie subalgebras and , but not and . The geometric version of the sufficient condition in Proposition 3.3 then asserts that the matrix exponential is injective when restricted to the ball around the origin (zero matrix) within (e.g. Baker, 2001, Proposition 2.4). This provides a sufficient (not necessary) condition to ensure that . The condition is close to being necessary for and . For example, with maps

to the identity ; thus, for any fixed . The issue arises because skew-symmetric matrices of the form considered comprise the kernel of . We see that and thus violates the sufficient condition.

Moving on to the decompositions, the following proposition elucidates on conditions that ensure injectivity of the four maps from §3 and legitimize them as reparametrizations of .

Proposition 3.4.

-

(i)

The maps and are injective on .

-

(iii)

Assume that the elements of are distinct. The map is injective when is restricted to such that the image within , and upon choosing for a particular permutation of and combination of signs for the columns of and a permutation of elements of , where is as in §3.4.

-

(ii)

The map is injective when restricted to such that the image within , where is as in §3.5.

4. Structure of when is sparse

Consider the matrices of §3, all of which can be written in terms of a canonical basis of dimension as . Suppose now that is sparse in the sense that . Corollaries 4.1–4.4 to be presented specify the structure induced on each of , , and through sparsity of .

The identification of equivalence classes of with , when coupled with the Iwasawa decomposition of and its Lie algebra (2.1), leads to a geometric interpretation in §6 of parameters and and their sparsity. In terms of the images of the maps and , a statistical interpretation of the sparsity-induced structure is discussed in §5.

Corollary 4.1 for the map was derived by Battey (2017) using elementary arguments. Specifically, this entailed showing that for a matrix , represented in terms of the canonical basis , a basis for is provided both by the eigenvectors of corresponding to the non-unit eigenvalues, and by , the set of unique non-zero column vectors of the basis matrices picked out from by the non-zero elements of . It follows that the rank of , i.e. the dimension of , is the equal to . The precise value of depends on the configuration of , but can be specified in expectation if the support of is taken as a simple random sample of size from . Since the column space and the row space of a symmetric matrix coincide, the non-trivial eigenvectors of have only non-zero entries, which corresponds to a very specific structure on , summarized in Corollary 4.1.

The analogous study of by Rybak & Battey (2021) required considerable technical modification, using a representation of normal operators in terms of block-diagonal matrices, which simplifies calculations involving the matrix logarithm. The analysis to be presented for and is more involved still, since triangular matrices are not necessarily normal.

Lemma 4.1 and Theorem 4.1 are general results applying in different ways to the four cases discussed in §3. They are specialized to these cases of interest in Corollaries 4.1–4.4 to expound the structure induced on or through sparsity of . While the statements of Corollaries 4.1 and 4.2 are not new, new proofs in Appendix C are presented in terms of the general formulation rather than the more elementary proofs provided by Battey (2017) and Rybak and Battey (2021).

For a matrix possessing a matrix logarithm , Lemma 4.1 refers to the real Jordan decomposition (e.g. Horn and Johnson, 2012, p. 202) , where consists of eigenvectors or generalized eigenvectors of and , where the kronecker sum is a block-diagonal matrix with blocks and , and is the th Jordan block whose superdiagonal entries are 1 and whose diagonal entries are , an eigenvalue of with geometric multiplicity equal to the dimension of . Let denote the set of indices for columns of corresponding to eigenvectors whose eigenvalues are not equal to one. Thus, the cardinality of the complementary set is the geometric multiplicity of the unit eigenvalue of , and . Let and denote the indices for the non-zero rows and columns of respectively, and . The sizes of these sets are , and respectively, each of which is strongly related to when is sparse. A bound which is always valid is , although can be considerably smaller than this, as it depends on the configuration of basis elements picked out by the sparse . Indeed, it can arise that even when exceeds , provided that the configuration of non-zero elements of produces zero rows or columns of .

Lemma 4.1.

Let . With and , a vector space of dimension , .

For normal matrices in , i.e. those satisfying , so that Lemma 4.1 recovers Lemma 2.1 of Battey (2017) and Proposition 3.1 of Rybak and Battey (2021). Theorem 4.1 establishes general conditions for logarithmic sparsity of a matrix . In this and subsequent results, the dependence of and on is implicit and suppressed in the notation.

Theorem 4.1.

Consider where , a vector space with canonical basis of dimension . The matrix is logarithmically sparse in the sense that , with if and only if has rows of the form for some , all distinct, and columns of the form . Of these, coincide after transposition. If is normal, .

While arbitrary constraints on the value of are avoided in Theorem 4.1 and in subsequent formal statements, a small value e.g. is guaranteed both to generate, and to be implied by, a simplification in the underlying conditional independence graph, under a notional Gaussian model. However, relatively large values of also entail a graphical reduction in many cases, as discussed below.

The importance of Theorem 4.1 lies in its implications for the four parametrizations of interest. Specifically, for all four, the form of induced by a sparse , established in corollaries 4.1–4.4, follows immediately from Theorem 4.1. An example at the end of this section illustrates these results. For each of the parametrizations studied here, the induced structure for is necessary and sufficient for sparsity of .

Corollary 4.1.

The image of the map is logarithmically sparse in the sense that in the basis representation for if and only if is of the form , where is a permutation matrix and with of maximal dimension, in the sense that it is not possible to find another permutation such that the dimension of the identity block is larger than .

To return to the discussion of the permissible value of , there are basis elements for . For to induce some pattern of zeros in , needs to have a zero row, which requires only zero coefficients in the basis expansion of , thus can be as large as in this case.

Corollary 4.2.

The image of the map is logarithmically sparse in the sense that in the basis representation for if and only if is of the form , where is a permutation matrix and , where and is of maximal dimension, in the sense that it is not possible to find another permutation such that the dimension of the diagonal block is larger than .

Corollary 4.3.

The image of the map is logarithmically sparse in the sense that in the basis representation for if an only if is of the form , where and has zero rows and zero columns, of which coincide.

Corollary 4.4.

The image of the map is logarithmically sparse in the sense that in the basis representation for if an only if is of the form , where , and has zero rows and zero columns, of which coincide.

To make a comparison between different structures of more explicit, we consider a simple stylised example with . For parametrizations and we set , corresponding to and respectively. For we consider two cases, , for which , (this serving as the definition of ), and , for which , with in both cases. The structure of the resulting covariance matrices is displayed in Figure 7.

Figure 7 suggests that, unlike a with zero rows, with zero columns can generate a dense covariance matrix. Intuitively, for the same restriction on the sparsity of , the corresponding covariance matrices and should represent relationships of similar complexity. The following lemma confirms this intuition. Specifically, Lemma 4.2 shows that although can be fully sparse, the sparsity restriction on induces a low-rank structure on a submatrix of .

Lemma 4.2.

Consider a random vector , with covariance matrix . Let denote the length of the subvector . Then, columns of in Corollary 4.4 corresponding to are zero if and only if the submatrix

of has rank .

If the map is instead replaced by an essentially equivalent representation in terms of upper triangular matrices, the analogous structures and are the same as for and respectively.

There is a relationship between the two parametrizations and if zeros in are allowed. To see this, write

where and . On writing , where and using the properties of matrix exponential,

which recovers the LTU decomposition with . Thus if is allowed to have zeros, there is an exact relationship between the coefficients of the expansion of and those of .

5. Statistical interpretation in a notional Gaussian model

The basis coefficients and the structures expounded in Corollaries 4.1–4.4 are directly interpretable. Those of Corollaries 4.1 and 4.2 were discussed by Battey (2017) and Rybak & Battey (2021) respectively. The more interesting structures of Corollaries 4.3 and 4.4 are elucidated here from a graphical modelling perspective, assuming for some of the latter statements an underlying Gaussian model.

5.1. Interpretation of basis coefficients

With , let and be disjoint subsets of variable indices, and in a departure from previous notation aligning with graphical modelling convention, let denote the identity matrix of dimension . As a consequence of a block-diagonalization identity for symmetric matrices (Cox & Wermuth, 1993; Wermuth & Cox, 2004),

| (5.1) |

The matrix identity (5.1) holds independently of any distributional assumptions on the underlying random variables. The components , and are the so-called partial Iwasawa coordinates for based on a two-component partition of (Terras, 1988, Chapter 4). For a statistical interpretation, let be a mean-centred random vector with covariance matrix , is the matrix of regression coefficients of in a linear regression of on and is the residual covariance matrix, i.e. and . More explicitly, on fixing a component and , the corresponding component of is

| (5.2) |

The conditional expectation indicates conditioning on observed values of with as a free variable. Although the ordering in Corollary 4.4 is immaterial, it is notationally convenient to order the underlying random variables as and apply the block-diagonalization identity recursively with, say , , , . There results a block diagonalization in blocks, recovering the LDU decomposition. In this representation, the th entry of from Corollary 4.4 is given by , a mean-squared error from the linear projection of on , and the th entry of the lower-triangular matrix , for , is given by , that is, the coefficient of in a regression of on .

Further interpretation for the entries of is obtained by considering an upper-triangular decomposition of the precision matrix. For an arbitrary partition , let be partitioned accordingly as

The block upper-triangular decomposition takes the form,

where . Then,

An alternative expression for the matrix of regression coefficients of in a regression of on is thus (Wermuth & Cox, 2004), which corresponds to the non-zero off-diagonal block of .

By partitioning recursively until is upper-triangular, we obtain that the th row of contains minus the regression coefficients of on . Let , where is a strictly lower-triangular matrix, and let . In particular, for , namely, the coefficient of in a regression of on . Then,

where we used that, for a nilpotent matrix of degree , .

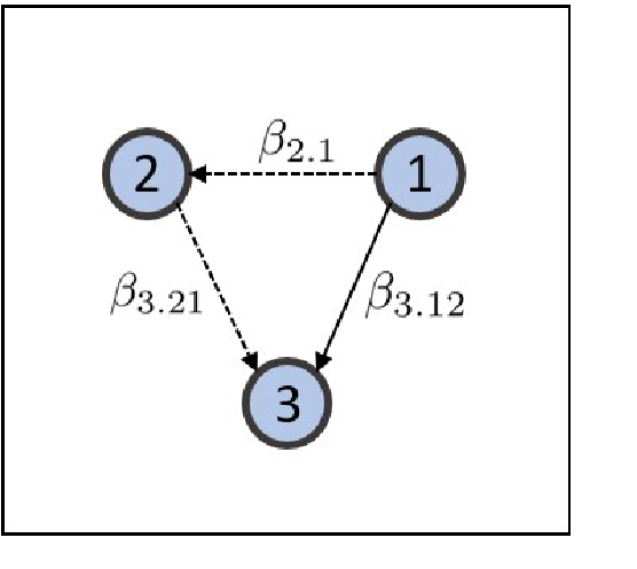

For a set of three variables , the marginal effect of on is related to the conditional effects through Cochran’s recursion (Cochran,, 1938),

| (5.3) |

which generalizes to an arbitrary number of variables in the manner indicated below. The right-hand side of equation (5.3) corresponds to tracing the effects of on along two paths connecting the nodes in a notional recursive system of random variables , with edge weights set equal to the corresponding regression coefficients. A directed edge in a recursive system can exist from node to node only if . Thus, there are two possible paths from to , namely and , which correspond to the first and second term in (5.3) respectively.

The lower-triangular matrices and have the form,

| (5.4) |

The entry for thus corresponds to the sum of effects of on along all paths connecting the two nodes. When the joint distribution of is Gaussian, linear regression coefficients correspond to conditional dependencies, and the trivariate system can be represented by a directed acyclic graph, as shown in Figure 8(A).

For a system of four variables, with a corresponding directed acyclic graph of the form shown in Figure 8(B), we have,

| (5.5) |

Again, for corresponds to the sum of effects of on along all directed paths connecting the two nodes, with edge weights given by regression coefficients, i.e. the marginal effect of on via Cochran’s recursion.

Using the properties of matrix logarithm,

Thus, the element of , and, by extension, the corresponding coefficient in the basis expansion of , is equal to the weighted sum of effects of on along all paths connecting the two nodes, with weights inversely proportional to the length of a given path. Estrada & Higham, (2010) and Kloster & Gleich, (2014) present some applications in which shorter paths are more important than longer ones, leading to length-based weighted averages of paths between nodes.

5.2. Interpretation of sparsity structures

Using the natural ordering in equation (5.2), the entries of encapsulate dependencies between each pair of variables, , , , conditional on other variables among , and marginalizing over the remaining variables .

In the terminology of e.g. Cox & Wermuth (1996), marginalization over a variable indicated by in the depiction below, induces an edge between and if the marginalized variable is a transition node or a source node in a parent graph. No direction in the induced edge is implied if the marginalized variable is a source node, which is indicated by ----.

By contrast, if and are separated by a sink node in , then conditioning on such a variable, indicated by below, is edge inducing, with no direction implied.

The entry for is zero if the effects of on cancel out. This happens, for example, when in equation (5.3). Alternatively, when no cancellations are present, , , implies an absence of a directed path from to in the notional directed acyclic graph. In addition, nodes cannot be sink nodes, and nodes cannot be transition or source nodes.

An assumption that is Gaussian of mean zero and covariance allows the zeros in to be interpreted as conditional independencies. If the th row of consists entirely of zeros, the dependence between and any can be explained away by conditioning on the remaining variables . This can happen for all only if for all , i.e., there are no direct edges between and , and the only connecting nodes, if any, are sink nodes .

Suppose that from Corollary 4.4 has a zero th column. This implies that for every , the only source or transition nodes connecting and are in the conditioning sets (otherwise dependence is induced through marginalization), and that there are no sink nodes among these conditioning variables (as conditioning on sink-nodes is edge-inducing). Consequently, the examples from Figure 7 can be represented by directed acyclic graphs presented in Figure 9.

More generally, suppose that a random vector is partitioned into four blocks of variables and that the lower-triangular matrix in the statements of corollaries 4.3 and 4.4 has zero columns corresponding to and zero rows corresponding to , that is, is of dimension and is of a dimension . The directed acyclic graph of the random vector is presented in Figure 10. Each square corresponds to a group of random variables/nodes. No connections are present among groups of variables represented by white squares, while arbitrary connections can be present within groups represented by white squares. A directed edge between groups of variables denotes a directed edge between each pair of nodes in the two groups. Double-headed arrow indicates that either of the directions can be present.

6. Geometric insight

Our approach of §3 can be intuited geometrically through the action of a positive definite matrix : the condition for every implies that the angle between a vector and is smaller than , and they both lie on the same side of the hyperplane to which is perpendicular; alternatively, in the coordinate system given by the orthogonal eigenvectors of , the vector is merely stretched along the same direction by a positive factor determined by the eigenvalues of . The same-sidedness of the action of can thus be decomposed into rotations that preserve orientations (i.e., ), restricted shearing (i.e., ), and scaling (i.e., ).

The parameter domains considered in §3 are subsets of that correspond to infinitesimal versions of such transformations. For example, elements of are infinitesimal rotations in in the following sense: for every curve with we have for some such that is approximately a rotation for small . In similar fashion, elements of and are infinitesimal scale and shear transformations in , respectively. The vector space structure of the Lie algebras allows us to combine infinitesimal rotation, scale and shear transformations via vector addition and scale operations, which then allows us to quantify and interpret sparsity in the ensuing positive definite matrix. Thus each parametrization of uses as coordinates for the domain a combination of geometrically interpretable transformations, which when put together constitutes a positive definite transformation. Section 4 details the structure of subsets of to which sparse subsets of map.

The geometric interpretation of sparsity in is as a quantification of the amount of shear and scaling that the positive definite applies to a vector .

The Lie group exponential map, given by the matrix exponential (see Appendix A), is surjective for with corresponding , but not for the general linear group , unless the (field) of entries are complex. This ensures, for example, that every rotation matrix and upper triangular matrix with positive or unit diagonal is available for constructing a positive definite matrix in the images of and , respectively. With this in mind, we can interpret the sparsity level as the dimension of a submanifold of that corresponds to a combination of scale, rotation, and shear transformation, which when put together in some proportion results in a positive definite transformation given by .

For example, consider the map with numbers of non-zero coefficients in and , respectively, with . The image of is an -dimensional connected submanifold of comprising an dimensional submanifold of and -dimensional submanifold of ; the image of need not be a subgroup of since the subspace spanned by the subset of corresponding to non-zero coefficients need not be a Lie subalgebra of ; the same applies to the map . In this case, the sparsity levels and in the new domain relates to dimensions of the rotation and scaling submanifolds of , and configuration of the non-zero coefficients relates to the choice of -dimensional submanifold of . Evidently, such geometric interpretation are available for the other reparametrization maps as well with respect to shear and scale submanifolds of .

7. Sparsity comparisons

7.1. Exact zeros

Section 4 studied the structure induced on , in terms of exact zeros, through sparsity of . An aspect not discussed in detail there is the observation of Battey (2017) and Rybak & Battey (2021) that may be considerably sparser than , both in terms of exact zeros and approximate zeros. This is most clearly illustrated through the parametrization . As shown by Battey (2017) and as is implicit in Corollary 4.1, the number of non-unit eigenvalues of when is and the number non-zero entries of any eigenvector associated with a non-unit eigenvalue of is also . Thus, with , the th entry of the matrix logarithm is . If , then and for . However is still feasible by cancellation in the sum even if . Suppose that . If or then by Corollary 4.1. However if and , then by construction, illustrating the possibility that may be substantially sparser than . A random sparse is necessarily sparser in terms of exact zeros than . However a random dense with the structure specified by Corollary 4.1 almost surely has a matrix logarithm with the same degree of sparsity in terms of exact zeros as . Notwithstanding, it is often the case that is much sparser than under more general notions of sparsity. A similar phenomenon applies in the other parametrizations. The relative sparsity levels in the four parametrizations are explored in §7.2.

7.2. Approximate zeros

A more general notion of sparsity suitable for the four cases is -sparsity. Defined for and as

and for and as

A comparable definition of -sparsity for is

In the simulations to follow, sparsity after reparametrization is compared to sparsity on the original scale via the ratio, .

We consider both directions of the discussion in §7.1 by simulation for . With as one of the constituent Lie subalgebras in the Iwasawa decomposition (2.1), in one direction, we generate a sparse or and compare their -sparsity level to that of the corresponding covariance matrix . For the converse question, we generate a dense and compare its -sparsity level to that of or after reparametrization.

7.2.1. Simulations for sparse

Figure 11 was obtained by generating 250 realizations of a random, sparse with by taking the support of to be random samples of size from the index set for and or from the index set for and . This was done for different values of as indicated in Figure 1. The values of the nonzero basis coefficients were then drawn from a uniform distribution on . The positive elements of the diagonal matrices in the decompositions and are obtained from and distributions, as indicated.

, ,

, ,

7.2.2. Simulations for dense

Rather than constructing from a sparse , we now sample covariance matrices directly, and construct the corresponding tranformation on the logarithmic scale. A random dense is obtained from the representation by generating uniformly over according to Haar measure and by generating the positive of the diagonal matrix from a gamma distribution of shape and scale , written . The results are reported in Figure 12.

8. Discussion and open problems

8.1. Methodological implications: some provisional remarks

As emphasized throughout, the focus of this work is on elucidating population-level structure, thereby pointing to an interpretation of sparsity after reparametrization and also facilitating the assessment of assumptions. In particular, a key aspect is whether sparsity assumptions, required to prevent the accumulation of estimation error and thereby provide statistical guarantees for many multivariate procedures of interest, are likely to be in reasonable accord with reality.

From a methodological point of view, two broad approaches are to assume a plausible set of graphical structures, leading to a reparametrization in which the subsumed structure is sparse, or to seek to deduce the sparsest representation empirically.

There are numerous open challenges associated with these two broad possibilities, which we do not take up here. Perhaps primary among these is the existence and uniqueness of the constrained maximum likelihood estimator under the relevant constraints, analogous to the discussion of Zwiernik et al. (2017) for Gaussian models with linear constraints on the covariance matrix. Zwiernik (2023) has highlighted further difficulties in using the log-likelihood function to estimate a covariance matrix when there are linear restrictions on its matrix logarithm, and proposed to instead use the Bregman divergence as a loss function. Open questions are whether his analysis extends to the other parametrizations considered here, and whether model adequacy can be assessed. A further set of methodological questions emerges once consideration is given to which sparsity constraints should be allowed for , i.e. whether each coefficient should be treated on an equal footing, or whether preference should be given to configurations that generate the most interesting structures according to e.g. Corollary 4.4 and the discussion of §5.

Since the matrix logarithms in each of the four parametrizations of §3 belong to different spaces, there are difficulties in traversing reparametrization space to find the most convenient representation empirically. One conceivable resolution is based on the observation that all four sparse parametrizations are representable in terms of a strictly lower triangular matrix and a diagonal matrix . With the canonical basis for described in §3.6, and with the canonical basis for with elements , the four cases of interest can be represented in terms of a common basis on noting that

where and have basis expansions in and . In principle, this provides a means of parametrizing a ‘path’ (actually a hypersurface) through parametrization space by writing

where , and

| (8.1) |

This hypersurface through model space, while parametrized, is not a parametrization in the formal sense discussed in Appendix B, as the presence of the sign function violates injectivity. Both sign functions can be dropped at the expense of the positive definiteness of . This is similar in spirit to the encompassing model formulation for regression transformation of Box & Cox (1964), who required a single parameter to traverse outcome-transformation space, and thereby model space. Similarly to the representation above, only certain values of the transformation parameter give reasonable models, as discussed by Box & Cox (1982).

8.2. Further exploration of the partial Iwasawa decomposition

In equation (5.1), the matrix

belongs to a restricted subset of and the matrix

is block diagonal with positive definite blocks. This suggests a version of the parametrization in which sparsity is imposed on and on the blocks of after reparametrization. This is likely to induce a range of further structures on the original domain, with corresponding graphical interpretation.

Conversely, for every positive definite there exists a unique triple and (Terras, 1988, Chapter 4) such that

the partial Iwasawa decomposition, and hence the parametrization with the two-block structure corresponding to the partition of , can conceivably be used to parametrize several other statistically interesting graphical models with appropriate restrictions on and . Indeed, this can be further generalized to any partition of with , which then offers additional possibilities.

Interestingly, information geometry of the zero-mean multivariate Gaussian (Skovgaard, 1984) induced by the Fisher Information metric tensor coincides with the quotient geometry of under a Riemannian metric that is invariant to the transitive action of . Upon representing a positive definite covariance matrix in the partial Iwasawa coordinates , the metric is endowed with an interpretation compatible with a suitable graphical model and a corresponding parametrization. We will develop this connection elsewhere.

Appendix A Matrix groups

We restrict attention to only those concepts from group theory that bear direct relevance to the exposition and proofs. An excellent source of reference for matrix groups is Baker (2001). The action of a group on a set is a continuous map . The orbit of is the equivalence class , and the set of orbits is a partition of known as the quotient of under the action of . A group action is said to be transitive if between any pair there exists a such that ; in other words, orbits of all coincide. The subset of that fixes is known as the isotropy group of and if equals the identity element for every , the group action is said to be free.

For every subgroup we can consider the (right) coset, or the quotient, consisting of equivalence classes of , where if for some . For groups that act transitively on , the map is a bijection, where is the isotropy group of the identity element.

A group that is also a differential manifold is a Lie group. Lie groups thus enjoy a rich structure given by both algebraic and geometric operations. The tangent space at the identity element, denoted by , has a special role in that, together with the group operation, it generates the entire group, i.e. every element can be accessed through elements of and the group operation. It is referred to as the Lie algebra and is a vector subspace of the same dimension as the group. Relevant to the matrices introduced in §2.1, we have:

-

(i)

If with matrix multiplication as the group action, then .

-

(ii)

If or with matrix multiplication as the group action, then , the set of skew-symmetric matrices.

-

(iii)

If with matrix multiplication as the group action, then is the set of lower triangular matrices.

-

(iv)

If with matrix multiplication as the group action, then is the set of lower triangular matrices with zeros along the diagonal.

-

(iv)

If with logarithmic addition as the group action (Arsigny et al., 2017) then .

When is a matrix Lie group, the usual matrix exponential can be related to the map such that . Properties of (e.g., injectivity) will depend on that of the matrix exponential, and hence on the topology of . If is compact and connected then is surjective. If it is injective in a small neighbourhood around the origin in , then it bijective. Since is also a differentiable manifold, a geometric characterisation of the matrix exponential is that it will coincide with the Riemannian exponential map under a bi-invariant Riemannian metric on .

Appendix B Parametrizations of

B.1. Proof of Proposition 3.1

Proof.

The set is a symmetric space of dimension of noncompact type and can thus has nonpositive (sectional) curvature when equipped with a Riemannian structure (Helgason, 2001). The map is injective, and we can thus pullback the metric from to making it non-positively curved. The set , by virtue of being the interior of the convex cone of positive semidefinite matrices, is simply connected and complete. By the Cartan-Hadamard theorem (Helgason, 2001) it is thus diffeomorphic to . ∎

B.2. Proof of Proposition 3.4

Proof.

Injectivity of follows from Proposition 3.3. It is well-known that the Cholesky and LDU decompositions as used in the definitions of and respectively are unique (Golub & Van Loan, 2013). Uniqueness of the LDU decomposition also stems from uniqueness of the Iwasawa decomposition of (Terras, 1988) through the identification . The maps and are thus injective. When combined with injectivity of the exponential map from Proposition 3.4, the parameterisation is injective.

The situation concerning uniqueness of the eigen decomposition is involved, even after restriction to a subset of that renders the exponential injective. First note that under our parameterisation using the exponential map. Then, observe that for any , and thus pairs map to the same for every for which , since . Indeed, fixes and is the isotropy subgroup in (see Appendix A). In addition to , another source of indeterminacy comes from permutations and , with and so that . Put together, this implies that every pair maps to the same as long as and .

The situation can be salvaged if the positive elements of are all distinct so that reduces to the set of diagonal rotation matrices with entries (Grossier et al., 2021, Theorem 3.3). In this case, the map is a covering map with fibers consisting of matrices obtained by permutations of elements of , and a similar permutation of eigenvectors of , and matrices in the set of diagonal matrices mentioned above with unit determinant, which determine signs of the eigenvectors of ; there are such diagonal matrices and not owing to the unit determinant constraint.

Uniqueness can be ensured upon identifying a global cross section that picks out one element from every fiber such that is a singleton for every . For example, can be defined by selecting a particular permutation and of the eigenvalues and eigenvectors of (e.g., elements of arranged in a decreasing order); since , a fixed rule for choosing signs of the eigenvectors determines a unique . Then, contains pairs for a fixed permutation . The cross section is bijective with the quotient under the equivalence relation that identifies any two pairs that map to the same .

The proof for injectivity of follows upon noting that the exponential map is injective when restricted to the given ball within . This completes the proof.

∎

Appendix C Proofs for Section 4

C.1. Auxiliary results

Lemma C.1 (Axler, 2015).

Let V be a real inner-product space and let be a linear operator on V with matrix representation . The following are equivalent: (i) is normal; (ii) there exists an orthonormal basis of V with respect to which where the blocks of the block-diagonal matrix are either or of the form

| (C.1) |

where , , and . Each block is an eigenvalue of , and for each block (C.1), and are eigenvalues of .

The representation C.1 in terms of polar coordinates is convenient for subsequent calculations involving the matrix logarithm.

Lemma C.2.

Let be a normal matrix. The matrix logarithm , if it exists, takes the form , where is orthonormal and is block diagonal with blocks of the form described in Lemma C.1.

Proof.

By Lemma C.1, , where is orthonormal and is block diagonal. Let be an eigenvalue of . From Proposition 3.2, existence of a logarithm requires that any negative real eigenvalues have associated with them an even number of blocks. By Lemma C.1 negative eigenvalues appear in blocks, since blocks correspond to complex conjugate pairs of eigenvalues. It follows that the matrix logarithm of a normal matrix exists if and only if negative eigenvalues have even multiplicity, in which case, we can without loss of generality construct blocks of size for a negative eigenvalue of the form . Then , and since and commute, , where

Thus

which is of the form in Lemma C.1. For blocks corresponding to complex conjugate pairs of eigenvalues of , a similar argument together with

shows that

which is also of the form of Lemma C.1. ∎

Lemma C.3.

Let . Then is normal if and only if is normal.

Proof.

Suppose that is normal, that is . By the Jordan decomposition , normality of implies normality of . The matrix exponential is normal if and only if . Two general properties of the matrix exponential are that for matrices such that , and . Thus showing that is normal. The converse statement follows by Lemmas C.1 and C.2. ∎

Lemma C.4 (Weierstrass’s M-test, e.g. Whittaker and Watson, 1965, p.49).

Let be a sequence of functions such that, for all within some region , , where are independent of and is a positive convergent sequence. Then converges to some limit, say, uniformly over .

Lemma C.5.

For , define . Then for any operator norm , provided that is bounded, . Additionally, for any .

Proof.

Let and let be such that . Since the operator norm is subadditive and submultiplicative

as . Lemma C.4 applies with .

For the second statement, it suffices by the Jordan decomposition of to show that where is an eigenvalue of . For , by definition, whereas for , , . ∎

Lemma C.6.

Consider where , a vector space with canonical basis of dimension . The matrix is logarithmically sparse in the sense that , with if and only if , where is a permutation matrix and

| (C.2) |

where and , . Moreover, if is normal, is also normal and in (C.2).

Proof.

Suppose first that is logarithmically sparse. By definition, has zero rows. Assume without loss of generality that is in canonical form, so that the last rows are zero. Thus write as a partitioned matrix with blocks upper blocks , of dimensions and , the remaining blocks being zero. On taking the Taylor expansion of the matrix exponential,

which is of the form given in equation (C.2) with .

To prove the reverse direction, we need to construct such that

| (C.3) |

where the number of zero rows of is greater or equal to . Let and . Set , which exists by assumption since eigenvalues of are eigenvalues of . Clearly, by the Taylor series of matrix exponential,

It thus remains to be shown that some matrix . Let . By Lemma C.5, is invertible, and we can take . Note that the matrix logarithm of is not unique. However, for a real eigenvalue of , logarithm of the Jordan block has periodicity , (Culver, 1966). Thus, for , every real matrix , will have the form (C.3) in the sense of the last rows being equal to canonical basis vectors, with a non-zero diagonal element. The result follows by observing that for , .

∎

C.2. Proof of Lemma 4.1

Proof.

Recall that indexes the columns of corresponding to non-unit eigenvalues.

Suppose that . Since , the geometric multiplicities of the unit eigenvalues of and are equal. Thus, and therefore .

To prove that , consider the real Jordan decomposition . Let denote the th column of . We show that by establishing containment on both sides. Let . Then there exist coefficients such that

where the final equality follows since for all , so the th diagonal entry of is zero. It follows that ..

For the converse containment, suppose for a contradiction that there exists such that . Since has full rank, its columns are linearly independent and there exist coefficients , each in such that . Since for by the previous argument,

By definition of , for any , thus the equality implies for all , a contraction, since the columns , are linearly independent. ∎

C.3. Proof of Theorem 4.1

Proof.

From Lemma C.6, rows of are of the canonical form , and since zero columns of are zero rows of , it is also true by Lemma C.6 applied to that columns of are of canonical form . If rows and columns of are of the canonical form, then , where and . The matrix logarithm of is . The converse direction follows by applying the exponential map to and invoking Lemma C.6 in the converse direction. ∎

C.4. Proof of Lemma 4.2

Proof.

Consider a random vector with the corresponding covariance matrix

where the matrices and are lower triangular with unit entries on the diagonal. Then

since is full-rank by definition. Consider a submatrix

Since is invertible, and for any two matrices , , with compatible dimensions , the result follows. ∎

Acknowledgements

KB thanks Sergey Oblezin for helpful discussions on Lie group decompositions, and acknowledges support from grants EPSRC EP/V048104/1, EP/X022617/1, NSF 2015374 and NIH R37-CA21495. HB acknowledges support from an EPSRC research fellowship under grant number EP/T01864X/1.

References

- Amari (1985) Amari, S. (1985). Differential Geometric Methods in Statistics, Springer-Verlag.

- Arsigny et al. (2017) Arsigny, V., Fillard, P., Pennac, X. and Ayache, N. (2017). Geometric means in a novel vector space structure on symmetric positive-definite matrices. SIAM J. Matrix Analy. Applic., 29, 328–347.

- Bailey (2008) Bailey, R. A. (2008). Design of Comparative Experiments, Cambridge University Press.

- Baker (2001) Baker, A(2001). Matrix Groups: an introduction to Lie group theory, Springer.

- Barndorff-Nielsen et. al (1986) Barndorff-Nielsen, O. E., Cox, D. R. and Reid, N. (1986). The role of differential geometry in statistical theory. International Statistical Review, 54, 83–96.

- Battey (2017) Battey, H. S. (2017). Eigen structure of a new class of structured covariance and inverse covariance matrices. Bernoulli, 23, 3166–3177.

- Battey (2023) Battey, H. S. (2023). Inducement of population sparsity Canad. J. Statist. (special issue in honour of Nancy Reid), to appear.

- Box & Cox (1964) Box, G. E. P. and Cox, D. R. (1964). An analysis of transformations (with discussion). J. Roy. Statist. Soc. B, 26, 211–252.

- Box & Cox (1982) Box, G. E. P. and Cox, D. R. (1982). An analysis of transformations revisited, rebutted. J. Amer. Statist. Assoc., 77, 209–210.

- Chiu et al. (1996) Chiu, T. Y. M., Leonard, T. and Tsui, K-W.(1996). The matrix-logarithmic covariance model. J. Amer. Statist. Assoc., 91, 198-210.

- Cochran, (1938) Cochran, W. G. (1938). The omission or addition of an independent variate in multiple linear regression. Supplement to the J. Roy. Statist. Soc., 5, 171–176.

- Cox (1961) Cox, D. R. (1961). Tests of separate families of hypotheses. In Proceedings of the fourth Berkeley Symposium on Mathematical Statisticsand Probability, 1, 105–123.

- Cox (1962) Cox, D. R. (1962). Further results on tests of separate families of hypotheses. J. Roy. Statist. Soc. B, 24, 406–424.

- Cox & Reid (1987) Cox, D. R. and Reid, N. (1987). Parameter orthogonality and approximate conditional inference (with discussion). J. Roy. Statist. Soc. B, 49, 1–39.

- Cox & Wermuth (1993) Cox, D. R. and Wermuth, N. (1993). Linear dependencies represented by chain graphs. Statist. Sci., 8, 204–218.

- Cox & Wermuth (1996) Cox, D. R. and Wermuth, N. (1996). Multivariate Dependencies. Chapman & Hall, London.

- Culver (1966) Culver, W. J.(1966). On the existence and uniqueness of the real logarithm of a matrix. Proc. Am. Math. Soc., 17, 1146-1151.

- Drton et al. (2008) Drton, M. Strumfels, B. and Sullivant, S.(2008). Lectures on algebraic statistics. Birkhäuser.

- Engelke & Hitz (2020) Engelke, S. and Hitz, A. S. (2020). Graphical models for extremes (with discussion). J. Roy. Statist. Soc. B, 82, 871–932.

- Estrada & Higham, (2010) Estrada, E. and Higham, D. J. (2014). Network properties revealed through matrix functions. SIAM review, 52, 696–714.

- Golub & Van Loan (2013) Golub, G. H. and Van Loan, C. F.(2013). Matrix Computations. Fourth edition. The Johns Hopkins University Press.

- Grossier et al. (2021) Grossier, D., Jung, S. and Schwartzman, A.(2021). Uniqueness questions in a scaling-rotation geometry on the space of symmetric positive-definite matrices. Differ. Geom. Appl., 79, 101798.

- Helgason (2001) Helgason, S.(2001). Differential geometry, Lie groups, and symmetric spaces. American Mathematical Society .

- Horn & Johnson (2012) Horn, R. A. and Johnson, C. R. (2012). Matrix Analysis. Cambridge University Press.

- Jeffreys (1946) Jeffreys, H. (1946). An invariant form for the prior probability in estimation problems. Proc. Roy. Soc. London, A., 186, 453–461.

- Jeffreys (1948) Jeffreys, H. (1948). Theory of Probability, 2nd ed. Oxford.

- Kloster & Gleich, (2014) Kloster, K. and Gleich, D. F. (2014). Heat kernel based community detection. Proceedings of the 20th ACM SIGKDD international conference on Knowledge discovery and data mining, 1386–1395.

- Lauritzen (1996) Lauritzen, S. L. (1996). Graphical Models. Oxford University Press.

- Leonard & Hsu (1992) Leonard, T an Hsu, J. S. J.(1992). Bayesian inference for a covariance matrix. Ann. Statist., 20, 1669-1696.

- McCullagh (2023) McCullagh, P. (2023). Ten Projects in Applied Statistics, Springer.

- Patterson & Thompson (1971) Patterson, H. D. and Thompson, R. (1971). Recovery of inter-block information when block sizes are unequal. Biometrika, 58, 545–554.

- Rao (1945) Rao, C. R. (1945) Information and the accuracy attainable in the estimation of statistical parameters. Bull. Calcutta Math. Soc., 37, 81–89.

- Rybak & Battey (2021) Rybak, J. and Battey, H. S. (2021). Sparsity induced by covariance transformation: some deterministic and probabilistic results. Proc. Roy. Soc. London, A., 477, 20200756.

- Skovgaard (1984) Skovgaard, L. T.(1984). A Riemannian geometry of the multivariate normal model. Scand J Statist, 11, 211-223.

- Terras (1988) Terras, A. (1988). Harmonic Analysis on Symmetric Spaces and Applications II. Springer.

- Wainwright (2019) Wainwright, M. (2019). High-dimensional statistics: a non-asymptotic viewpoint. Cambridge University Press.

- Wermuth & Cox (2004) Wermuth, N. and Cox, D. R. (2004). Joint response graphs and separation induced by triangular systems. J. Roy. Statist. Soc. B, 66, 687–717.

- Whittaker & Watson (1965) Whittaker, E. T. and Watson, G. N. (1965). A Course of Modern Analysis. Cambridge University Press, London.

- Zwiernik et al. (2017) Zwiernik, P., Uhler, C. and Richards, D. (2017). Maximum likelihood estimation for linear Gaussian covariance models. J. Roy. Statist. Soc. B, 79, 1269–1292.

- Zwiernik (2023) Zwiernik, P. (2023). Entropic covariance models. arXiv:2306.03590.