Conformal Predictive Programming for Chance Constrained Optimization

Abstract

Motivated by the advances in conformal prediction (CP), we propose conformal predictive programming (CPP), an approach to solve chance constrained optimization (CCO) problems, i.e., optimization problems with nonlinear constraint functions affected by arbitrary random parameters. CPP utilizes samples from these random parameters along with the quantile lemma – which is central to CP – to transform the CCO problem into a deterministic optimization problem. We then present two tractable reformulations of CPP by: (1) writing the quantile as a linear program along with its KKT conditions (CPP-KKT), and (2) using mixed integer programming (CPP-MIP). CPP comes with marginal probabilistic feasibility guarantees for the CCO problem that are conceptually different from existing approaches, e.g., the sample approximation and the scenario approach. While we explore algorithmic similarities with the sample approximation approach, we emphasize that the strength of CPP is that it can easily be extended to incorporate different variants of CP. To illustrate this, we present robust conformal predictive programming to deal with distribution shifts in the uncertain parameters of the CCO problem.

Index terms— Conformal prediction; chance constrained optimization; robust uncertainty quantification.

1 Introduction

Chance constrained optimization (CCO) problems arise in many different domains such as robot navigation [1, 2, 3], portfolio optimization [4, 5], power systems design [6, 7], and learning [8, 9]. CCO problems are of the form

where is the decision variable, is a cost function, is a constraint function, are random parameters, and is the maximum probability of constraint violation. The existence of chance constraints makes CCO problems hard to solve [10]. In fact, without strong assumptions on , , and (e.g., and being linear and being Gaussian), CCO problems are computationally intractable due to the need to solve multi-dimensional integrals. Even if we had the technical ability to solve such complex integrals, we usually lack information about the distribution of which makes the integral unknown; for instance, in robotics the functions and are nonlinear and follows an unknown distribution. A common approach is hence to sample the random parameter and to solve an approximate optimization problem over the samples while providing probabilistic feasibility guarantees for the CCO problem. These approaches include the sample approximation approach (SAA) [11] and the scenario approach (SA) [12]. We also follow a sampling-based approach, but our algorithms and feasibility guarantees are derived through the lens of conformal prediction (CP) [13, 14].

In this paper, we propose conformal predictive programming (CPP) as a new method for solving CCO problems. CPP utilizes conformal prediction, a statistical technique that has recently gained attention as it enables efficient uncertainty quantification for predictions from machine learning models, see [15, 16]. The main idea behind CPP is to transform the CCO problem into a deterministic optimization problem by using the quantile lemma which central to the idea of CP. Using a CP argument, we can then relate the solution of this problem to the CCO problem. We make the following contributions.

-

•

We present CPP as a new algorithm for solving general CCO problems. We present CPP-KKT and CPP-MIP as computationally tractable reformulations of CPP. We further extend CPP to deal with multiple chance constraints.

-

•

We provide marginal probabilistic feasibility guarantees for the CCO problem which are conceptually different from feasibility guarantees provided by SA and SAA.

-

•

To illustrate the versatility of CPP, which can seamlessly incorporate different variants of CPP, we present robust CPP that can deal with distribution shifts in .

-

•

We illustrate the efficacy and validity of CPP on a set of case studies. While a theoretical comparison with SA and SAA is difficult, we provide a numerical comparison.

Related Work

CCO problems have been extensively studied with early studies in [17]. Earlier works make assumptions on the distribution of the random parameter such as being Gaussian or log-concave [18, 19, 20]. In practice, however, these assumptions usually do not hold and is generally unknown [6]. More recent approaches do not make such limiting assumptions and solve the CCO problem approximately by sampling the random variable . We next review sampling-based approaches.

Scenario Approach (SA): Here, i.i.d. samples (or scenarios) are drawn from the distribution of , and the chance constraint is reformulated as to approximate the solution to the CCO problem in (3) [21, 22, 23]. By assuming convexity of the nominal problem, the SA solution can be shown to be a feasible solution for the CCO problem with a probability of at least where depends on [12]. We note that these guarantees are different from the marginal probabilitistic feasibility guarantees that we derive, which do not require any convexity assumptions. Recent attempts to lift the convexity assumption are presented in [24, 25, 26, 27]. The approach with least assumptions that is most similar to our work is [23], which generates feasibility guarantees for the CCO problem using an additional dataset.

Sample Average Approximation (SAA): In SAA [11, 28], an empirical distribution from the set of sampled scenarios is used to approximate the chance constraint by instead imposing the constraint

| (1) |

where . Feasibility guarantees of the SAA solution for the CCO problem can be obtained if the domain of is finite. In [11], under relaxed assumptions, feasibility guarantees are provided empirically with an additional dataset but without formal guarantees. We later show that CPP shares algorithmic similarities with SAA but that it allows to obtain feasibility guarantees with no assumptions on the optimization problem.

As discussed, solutions to SA and SAA reformulations are not guaranteed to be feasible for the CCO problem (3) with probability one. In robust optimization approaches [29, 30], the idea of a safe approximation allows feasibility to be preserved. A method that lies in between robust optimization and sampling-based methods is presented in [31]. To the best of our knowledge, there has been little work on bridging the gap between the optimality of solutions obtained from the approximate feasibility region (approximated using risk measures) and the feasibility region of the CCO problem. In [29], a general method for evaluating feasibility guarantees of a candidate solution to a CCO problem is proposed, arriving at similar guarantees than the scenario approach.

2 Background: Conformal Prediction

Conformal prediction (CP) is a statistical tool for uncertainty quantification that can generate probabilistically valid prediction sets for complex machine learning models, see [14, 15, 16] for an overview. Consider a set of exchangeable111Exchangeability of is a weaker assumption than being independent and identically distributed (i.i.d.). random variables , then CP aims to find a probabilistic upper bound for based on . In practice, can be a test datapoint while is a calibration dataset. The idea is now to compute the quantile over the distribution of at a desired confidence level , which reduces to checking the rank of . The next result summarizes the central idea behind CP where we denote by the product measure222 follows where the probability measures of are . generated by .

Lemma 2.1.

Quantile Lemma [Lemma 1 in [41]] Let be exchangeable random variables where . For a failure probability , it holds that

where with and

| (2) |

with being a random variable with a unit point mass at . Further, if almost surely there are no ties between , then it holds that

If are sorted in nondecreasing order, it holds that where , which makes it easy to compute in practice. The variable is referred to as the nonconformity score and is often the result of a function composition, e.g., in regression a common choice is the prediction error where a predictor predicts an output from an input . In this setting, we obtain the prediction region with . The guarantees in (2) are marginal over the randomness in , as indicated by . The conditional probability is known to be a random variable that follows a Beta distribution centered around with decreasing variance as increases, see [16] for details. We are hence inspired by the results in Lemma 2.1 in the remainder to find a solution to the CCO problem, which we formally define next.

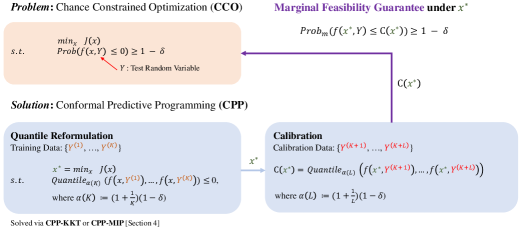

3 Conformal Predictive Programming

Chance Constraint Optimization (CCO). Consider a probability space with the sample space , the -algebra , and the probability measure . Let be a -dimensional random vector defined over . We denote the distribution of as , i.e., . For , we define the CCO problem as

| (3a) | ||||

| s.t. | (3b) | |||

| (3c) | ||||

| (3d) | ||||

where is a measurable function defined over a decision variable and the random vector . We denote by the pushforward measure of , and we refer to (3b) as an individual chance constraint (or simply chance constraint). Further, let and denote inequality and equality constraints and denote the cost function. We emphasize that is a user-defined failure probability. We note that CPP can be extended to deal with joint chance constraints of the form as we show in Appendix A, which we recommend reading after Sections 3-4. We denote the feasible region and the optimal solution of (3) as and , respectively. As standard in the literature, we assume that is non-empty (i.e., exists) and is bounded from below.

Conformal Predictive Programming (CPP). In this section, we present CPP which consists of two main steps. We first approximate the optimization problem in equation (3) by replacing the chance constraint in (3b) with a new constraint defined over the quantile in equation (2). For reasons discussed later, we then use Lemma 2.1 to conformalize the optimal solution of this optimization problem, called , to certify its feasibility. Following these steps, we present two tractable reformulations of CPP in Section 4 which we call CPP-KKT and CPP-MIP. To start, we note that CPP requires two separate training and calibration datasets. We summarize our assumptions on these datasets next.

Assumption 3.1.

We have access to a training dataset of random variables where is such that . We further have access to a calibration dataset of random variables such that are independent and where is such that .

Note that are assumed to be independent for our main results to hold, while are not required to be independent. The reason is that will, for reasons we elaborate on further below, not be independent even if is. However, we recommend using an independent training dataset, as we do in our experiments.

Quantile Reformulation. The motivation of our algorithm is based on Lemma 2.1. Specifically, we observe that, for a fixed parameter independent of test and training data , it holds that if are independent. We thus approximate the optimization problem in (3) as

| (4a) | ||||

| s.t. | (4b) | |||

| (4c) | ||||

We denote the feasible region of the optimization problem in (4) as . Note that the feasible region depends on , which we indicate by the input argument in . Due to the quantile constraint in equation (4b), it is not obvious at this point how to solve the optimization problem (4). We will defer solving this challenge to Section 4 and denote the optimal solution by for now, again stressing the dependence on . Note in this regard that and are random variables themselves given the randomness of the training dataset. For simplicity, we will often drop the dependence of on .

Feasibility Guarantees. As the optimal solution depends on , we note that the random variables are no longer exchangeable. While may be a feasible solution, this loss of exchangeability means that we cannot apply Lemma 2.1 to make any formal statements about . We thus conformalize the solution using the calibration dataset . In essence, we perform a conformal prediction step with the nonconformity score for and we compute

so that is a probabilistically valid upper bound on . We summarize this result in Theorem 3.2, and we provide a short proof in Appendix B.1 for completeness.

Theorem 3.2.

How do these feasibility guarantees now relate to the feasibility of the CCO problem in equation (3)? Ideally, we want that in which case we expect to provide a feasible solution to the CCO problem in (3). In the way we use the quantile constraint in equation (4b) and in the way we have defined , one can expect that the distribution of is centered around zero with small variance. This is confirmed by our experiments in Section 6. In practice, this hence motivates us to repeatedly draw training and calibration datasets and solve (4) until . We remark that another way of reducing is to enforce instead of (4b) for a tightening parameter .

Finally, we would like to provide another connection to the CCO problem in (3). From equation (5a) it follows that with , see [16] for details. In other words, we know that the conditional probability of given the calibration dataset is Beta distributed and centered around . As noted in [42], the cumulative distribution function corresponding to this Beta distribution evaluated at is where is the regularized incomplete beta function evaluated at . This implies that

holds with a probability of at least over the randomness in .

4 Computational Encodings of the Quantile

We next present two approaches through which the quantile in equation (4b) can be computed efficiently. The first approach is based on representing the quantile within the optimization problem (4) as a linear optimization problem. This leads to a bilevel optimization problem in which we rewrite the inner optimization problem with its KKT conditions. We call this approach CPP-KKT and show that a feasible solution to CPP-KKT is also a feasible solution to (4), but not vice versa. Our second approach, which is an equivalent reformulation, is based on mixed-integer programming (MIP) and called CPP-MIP. The idea is to reformulate the quantile within the optimization problem (4) with a set of mixed integer constraints. A feasible solution to CPP-MIP is also a feasible solution to (4), and vice versa.

Quantile Encoding and Bilevel Optimization. Following ideas presented [43, 44], we first rewrite the quantile in equation (4b) for a fixed by the linear program

| (6a) | ||||

| (6b) | ||||

| (6c) | ||||

where are decision variables and where we use instead of for simplicity. Intuitively, the optimization problem in (6) minimizes a weighted sum of the distance between the quantile and each sample . Before we continue, we show how is related to (4b) in Lemma 4.1, with the proof provided in Appendix B.2

As shown in Appendix B.2, the upper bound is in general not conservative and exact when . We can now use the linear program in (6) to replace equation (4b), which results in the following optimization problem

| (7a) | ||||

| s.t. | (7b) | |||

| (7c) | ||||

| (7d) | ||||

| (7e) | ||||

| (7f) | ||||

Using Lemma 4.1, we immediately see that a feasible solution to (7) is necessarily a feasible solution to (4).

Corollary 4.2.

Note that the inner optimization problem in equation (7) is composed of equations (7d), (7e), and (7f). For any fixed value of the decision variable from the outer optimization problem, the inner optimization problem is linear in . We can hence rewrite the inner optimization problem with its KKT conditions [45]. This results in the optimization problem

| (8a) | ||||

| s.t. | (8b) | |||

| (8c) | ||||

| (8d) | ||||

| (8e) | ||||

| (8f) | ||||

| (8g) | ||||

| (8h) | ||||

| (8i) | ||||

| (8j) | ||||

| (8k) | ||||

where are new decision variables. Specifically, (8b)-(8c) denote constraints from the outer optimization problem, while (8d)-(8f) represent the stationarity condition, (8g)-(8h) denote primal feasibility conditions, (8i) denotes dual feasibility condition, and (8j)-(8k) denote complementary slackness condition. We summarize our main result next and provide a proof in Appendix B.3.

Theorem 4.3.

An optimal solution to (8) is a feasible solution to (4), but not necessarily its optimal solution . However, we expect this optimal solution to be close to (see Lemma 4.1).

Note that (8) is a nonconvex optimization problem even when , , are convex and is an affine function due to constraints (8j) and (8k). However, in this case (8) is a linear complimentarity program, efficient solvers exist [46]. We next propose an alternative approach to exactly reformulate the quantile in equation (4b). We empirically compare the approaches in Section 6.

Quantile Encoding with Mixed Integer Programming.

We rewrite the quantile in equation (4b) using mixed integer programming (MIP). First recall from Section 2 that where when are sorted in non-decreasing order. Note hence that the quantile constraint in (4b) requires that at least out of the constraints are satisfied, i.e., that

| (9) |

where is the indicator function. We proceed by introducing binary variables for that encode the satisfaction of along with a set of mixed integer linear constraints. Specifically, let

| (10a) | |||

| (10b) | |||

where is a small positive constant, e.g., machine precision, and and are sufficiently large positive and small negative constants, respectively (details below). The constraints in (10) enforce that if and only if , see [47] for details. By replacing the quantile in (4b) with the set of mixed integer linear constraints in (10) we obtain

| (11a) | ||||

| s.t. | (11b) | |||

| (11c) | ||||

| (11d) | ||||

| (11e) | ||||

where , , and . Note that an over(under)-estimate of suffices for our purpose [47], and and exist when is continuous and is a compact set. The next result establishes the equivalence between the optimization problems in equations (4) and (11). It follows immediately from the previous construction and is provided without proof.

Solving MIP problems is in general NP-hard, which makes solving (11) NP-hard. However, these problems can usually be solved efficiently in practice, e.g., using optimization solvers such as SCIP [48], rarely encountering the worst case complexity, as we demonstrate in Section 6. Note also that the optimization problem in (11) reduces to a mixed integer linear program when , , , and are affine functions.

Remark 1.

SAA and CPP-MIP (and thus CPP) share algorithmic similarities for the special choice of in equation (1) which makes equation (1) equivalent to equation (9). While this observation is intuitive, we arrived at this conclusion from independent starting points. To the best of our knowledge, unlike in [11] and other SAA variants, we need to make no assumptions on the form of the CCO problem in (3) to obtain the feasibility results in Theorem 3.2. We also emphasize that CPP provides marginal probabilistic feasibility guarantees as opposed to SA and SAA.

5 Robust Conformal Predictive Programming

CP has been an active research area over the last years with developments in adaptive CP [49, 50], robust CP [51, 52], conformalized quantile regression [53, 54], outlier detection [55, 56], and many more. We believe that the strength of our approach is that CPP can easily be extended to incorporate different versions and extensions of CP. To illustrate this point, we present robust conformal predictive programming (RCPP) in this section.

RCPP can deal with distribution shifts in , i.e., when the datapoint is not following the distribution where the training and calibration datasets are drawn from. This may be the case when training and deployment conditions are different and when there is a sim2real gap. RCPP is based on robust conformal prediction as presented in [51], which we summarize in Appendix C. It is assumed that instead follows a distribution from the ambiguity set where denotes the size of the distribution shift and is an f-divergence measure. In essence, robust CP follows the same procedure as CP but it uses a modified failure probability of (see Lemma C.1 in Appendix C) which is such that .

Robust Conformal Predictive Programming (RCPP). We demonstrate the use of robust CP in solving robust chance constraint optimization (RCCO) problems of the form

| (12a) | ||||

| s.t. | (12b) | |||

| (12c) | ||||

The difference between the RCCO in (12) and the CCO in (3) is that is no longer drawn from the distribution , but is instead drawn from a distribution within the ambiguity set . Our robust extension of CPP to solve the RCCO uses robust CP and requires the next assumption.

Assumption 5.1.

We make the same assumptions on training and calibration datasets as in Assumption 3.1, but require now that and .

Note here that is defined in Lemma C.1 and can be obtained by solving a set of convex optimization programs. Similar to CPP, RCPP consists of a quantile reformulation and a feasibility analysis. We summarize RCPP and its guarantees next and provide a proof in Appendix B.4.

Theorem 5.2.

As in CPP, the quantile can be encoded by either a bilevel program with the KKT conditions, with replaced with , or by MIP as illustrated in Section 4, where from (11d) is replaced with .

6 Numerical Experiments

In this section, we validate CPP on a general nonlinear CCO problem and an optimal control problem. We then validate RCCP on a portfolio optimization problem. We further compare CPP with SA and SAA in Appendix D.2 and provide results for CCO problems with joint chance constraints in Appendix D.5. All experiments are conducted in Python 3 on a MacBook Air (2022) with M2 and 16GB memory using SCIP as an optimization solver.

Experimental Procedure. Our experimental evaluation proceeds in two steps. In the first step, we validate the solution of the CPP-KKT formulation in (8) and the CPP-MIP formulation in (11). Let denote the number of experiments, and again denote the size of the training and calibration sets, and denote the size of an additional test dataset. Specifically, we perform the following procedure for CPP-KKT and CPP-MIP. For each experiment , we sample a training dataset where is problem specific. We then compute the solution of (8) (or (11)) and evaluate the optimal value . We set a time limit of seconds for the computation of and report the number of timeouts in the appendix. For each solution , we sample a test dataset and compute the empirical coverage

to evaluate how well the CCO problem in (3) is solved.

In the second step, we validate the feasibility guarantees of CPP. Specifically, we perform the following procedure for CPP-KKT and CPP-MIP. For each experiment , we sample a calibration dataset . We then compute the upper bound to validate the feasibility guarantees in Theorem 3.2. Using the test dataset , we compute

to evaluate the feasibility guarantees in Theorem 3.2. We will provide plots of the histograms of and .

6.1 Case Study 1: General Nonlinear CCO Problem

Problem Statement. We consider the CCO problem

| (14) | ||||

| s.t. | ||||

with failure probability and where is a long-tailed exponential distribution.

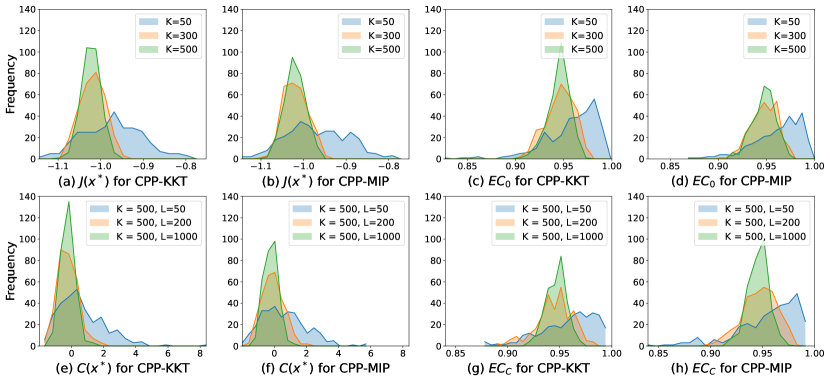

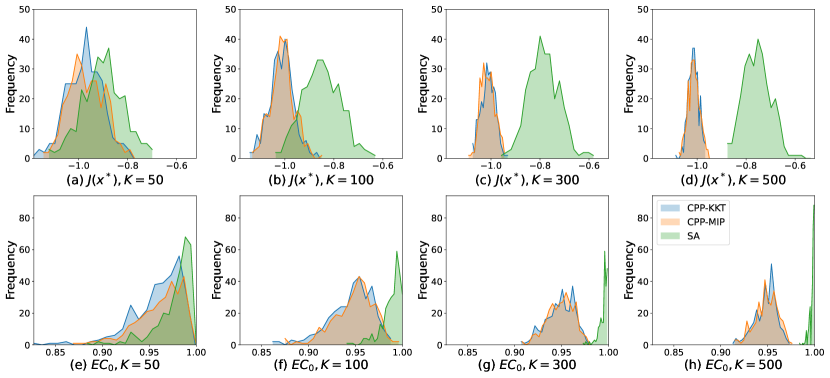

Results. For now, we fix and . In the first validation step, we vary the value of . We show the empirical distributions of for CPP-KKT in Figure 2(a) and for CPP-MIP in Figure 2(b). In both cases, we see that the distributions of the cost has decreasing variance for larger values of , and that the distribution for is centered at approximately , while the center of for is slightly bigger. Intuitively, this makes sense since more training data is expected to increase the optimality of the solution and to decrease the variance. We next show the empirical distribution of for CPP-KKT in Figure 2(c) and for CPP-MIP in Figure 2(d). Both distributions are centered at with decreasing variance for larger values of . For the value of , this is exactly the behavior that we expect and would like to see. In the second validation step, we fix and vary the value of . We show the empirical distributions of for CPP-KKT in Figure 2(f) and for CPP-MIP in Figure 2(g). Both distributions are centered at (as we argued before) with decreasing variance as we increase . We next plot the distributions of the empirical coverage for CPP-KKT in Figure 2(g) and for CPP-MIP in Figure 2(h). Again, these are centered at with decreasing variance as increases, confirming our theoretical results in Theorem 3.2. We provide additional experimental results for different values of and in Appendix D.1. There, we also provide a table where we record the average statistics attained with varying and including the solver time for CPP-KKT and CPP-MIP in Table LABEL:table:average_statistics. We observe that CPP-MIP is faster on average than CPP-KKT, and no timeout nor infeasible solution was observed in Case Study 1. We compare CPP to SA and SAA in this setting in Appendix D.2.

6.2 Case Study 2: Optimal Control Problem

Problem Statement. We demonstrate the effectiveness and utility of the CPP algorithm in solving a stochastic optimal control problem. Consider a robot operating in a two-dimensional Euclidean space, e.g, a mobile service robot. The state of the robot is where and represent position and velocity at time in each dimension. We describe the robot dynamics by discrete-time double integrator dynamics

with , and where is the control input and is system noise. Specifically, in this setting we let each entry of be drawn from a Laplace Distribution, , and we let to be a user-specified time horizon.

We are interested in synthesizing control inputs for times that allow the robot to reach a region centered around the target location at time with high probability. Specifically, for parameters and , we want to solve the control problem

| (15) | ||||

| s.t. | ||||

Results. We repeat the experimental procedure as previously outlined, but now with fixed parameters , , , and . We perform the same validation as in Case Study 1 and we report the same plots for CPP-KKT and CPP-MIP in Figure 6 in Appendix D.3. We observe the same pattern as before and specifically note that CPP provides the desired coverage of %. It is also worth mentioning that, in this case study, CPP-KKT outperforms CPP-MIP in terms of solve time, which is 5.15 seconds and 16.75 seconds on average, respectively. We postulate that, in this case study, the NP-hardness of the MIP solver plays a role so that the solver has to branch more in the solve tree while KKT conditions appear more efficient.

6.3 Case Study 3: Portfolio Optimization Problem

In this case study, we demonstrate RCPP in solving a RCCO problem in the setting of portfolio optimization. We specifically compare RCPP to CPP as a baseline model.

Problem Statement.

We consider an investment portfolio optimization problem consisting of three assets.

The weight of each assets (i.e., our investment) in the portfolio is represented by the vector where each asset should be larger than the minimum permissible asset and the total investment should be constrained by a limit . The return rate of each of the three assets, denoted by the vector , are assumed to follow a normal distribution. Specifically, we describe the distribution from which we draw training and calibration datasets as . The test data is drawn from the distribution which simulates a distribution shift from . We explain how we calculate the size of the distribution shift in Appendix D.4. The inter-asset risk association is captured by a risk weight matrix ,

and the portfolio’s overall risk tolerance is quantified by a threshold .

Additionally, this problem includes a chance constraint, ensuring that the portfolio’s return exceeds a lower-bound with high probability.

The objective of this problem is to maximize .

Specifically, we want to solve the CCO problem

| (16) | ||||

| s.t. | ||||

where , , , , and .

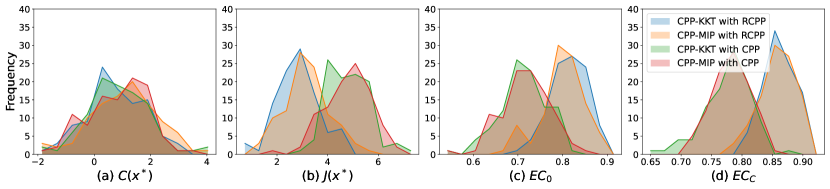

Results. We again follow the experimental procedure outlined before. However, we now apply CPP and RCPP each with the KKT and the MIP variants with parameters , , , and . We show the results in Fig. 7 in Appendix D.4. In summary, we observe that RCPP (both with KKT and MIP) achieve the desired coverage of % while CPP (both with KKT and MIP) achieves a lower coverage as it does not account for the distribution shift between and .

7 Conclusion

We presented CPP as a new algorithm for solving general CCO problems. CPP is based on the quantile lemma from conformal prediction which allows us to provide marginal probabilistic feasibility guarantee for the CCO problem. We also presented two tractable reformulations and extended CPP to deal with multiple chance constraints and distribution shifts. We experimentally evaluated our method on three extensive case studies. For future work, we will analyze probabilistic optimality of CPP, and we will focus on exploring theoretical connections with other sampling-based approaches such as SA and SAA.

8 Acknowledgements

The National Science Foundation supported this work through the following grants: CAREER award (SHF-2048094), CNS-1932620, CNS-2039087, FMitF-1837131, CCF-SHF-1932620, the Airbus Institute for Engineering Research, and the funding by Toyota R&D and Siemens Corporate Research through the USC Center for Autonomy and AI.

References

- [1] C. Dawson, A. Jasour, A. Hofmann, and B. Williams, “Chance-constrained trajectory optimization for high-dof robots in uncertain environments,” arXiv preprint arXiv:2302.00122, 2023.

- [2] Y. K. Nakka and S.-J. Chung, “Trajectory optimization of chance-constrained nonlinear stochastic systems for motion planning under uncertainty,” IEEE Transactions on Robotics, vol. 39, no. 1, pp. 203–222, 2022.

- [3] L. Blackmore, M. Ono, and B. C. Williams, “Chance-constrained optimal path planning with obstacles,” IEEE Transactions on Robotics, vol. 27, no. 6, pp. 1080–1094, 2011.

- [4] R. N. Sengupta and R. Kumar, “Robust and reliable portfolio optimization formulation of a chance constrained problem,” Foundations of Computing and Decision Sciences, vol. 42, no. 1, pp. 83–117, 2017.

- [5] B. K. Pagnoncelli, S. Ahmed, and A. Shapiro, “Computational study of a chance constrained portfolio selection problem,” Journal of Optimization Theory and Applications, vol. 142, no. 2, pp. 399–416, 2009.

- [6] X. Geng and L. Xie, “Data-driven decision making in power systems with probabilistic guarantees: Theory and applications of chance-constrained optimization,” Annual reviews in control, vol. 47, pp. 341–363, 2019.

- [7] T. Summers, J. Warrington, M. Morari, and J. Lygeros, “Stochastic optimal power flow based on convex approximations of chance constraints,” in 2014 Power Systems Computation Conference. IEEE, 2014, pp. 1–7.

- [8] H. Xu, C. Caramanis, and S. Mannor, “Robust regression and lasso,” Advances in neural information processing systems, vol. 21, 2008.

- [9] S. Pfrommer, T. Gautam, A. Zhou, and S. Sojoudi, “Safe reinforcement learning with chance-constrained model predictive control,” in Learning for Dynamics and Control Conference. PMLR, 2022, pp. 291–303.

- [10] A. Prékopa, Stochastic programming. Springer Science & Business Media, 2013, vol. 324.

- [11] J. Luedtke and S. Ahmed, “A sample approximation approach for optimization with probabilistic constraints,” SIAM Journal on Optimization, vol. 19, no. 2, pp. 674–699, 2008.

- [12] M. C. Campi and S. Garatti, “The exact feasibility of randomized solutions of uncertain convex programs,” SIAM Journal on Optimization, vol. 19, no. 3, pp. 1211–1230, 2008.

- [13] V. Vovk, A. Gammerman, and G. Shafer, Algorithmic learning in a random world. Springer, 2005, vol. 29.

- [14] G. Shafer and V. Vovk, “A tutorial on conformal prediction.” Journal of Machine Learning Research, vol. 9, no. 3, 2008.

- [15] V. Balasubramanian, S.-S. Ho, and V. Vovk, Conformal prediction for reliable machine learning: theory, adaptations and applications. Newnes, 2014.

- [16] A. N. Angelopoulos and S. Bates, “A gentle introduction to conformal prediction and distribution-free uncertainty quantification,” arXiv preprint arXiv:2107.07511, 2021.

- [17] A. Charnes and W. W. Cooper, “Chance-constrained programming,” Management science, vol. 6, no. 1, pp. 73–79, 1959.

- [18] C. Van de Panne and W. Popp, “Minimum-cost cattle feed under probabilistic protein constraints,” Management Science, vol. 9, no. 3, pp. 405–430, 1963.

- [19] S. Kataoka, “A stochastic programming model,” Econometrica: Journal of the Econometric Society, pp. 181–196, 1963.

- [20] A. Prékopa, “Logarithmic concave measures with application to stochastic programming,” Acta Scientiarum Mathematicarum, vol. 32, pp. 301–316, 1971.

- [21] G. C. Calafiore and M. C. Campi, “The scenario approach to robust control design,” IEEE Transactions on automatic control, vol. 51, no. 5, pp. 742–753, 2006.

- [22] M. C. Campi, S. Garatti, and M. Prandini, “The scenario approach for systems and control design,” Annual Reviews in Control, vol. 33, no. 2, pp. 149–157, 2009.

- [23] M. C. Campi, S. Garatti, and F. A. Ramponi, “A general scenario theory for nonconvex optimization and decision making,” IEEE Transactions on Automatic Control, vol. 63, no. 12, pp. 4067–4078, 2018.

- [24] S. Grammatico, X. Zhang, K. Margellos, P. Goulart, and J. Lygeros, “A scenario approach for non-convex control design,” IEEE Transactions on Automatic Control, vol. 61, no. 2, pp. 334–345, 2015.

- [25] G. C. Calafiore, D. Lyons, and L. Fagiano, “On mixed-integer random convex programs,” in 2012 IEEE 51st IEEE Conference on Decision and Control (CDC). IEEE, 2012, pp. 3508–3513.

- [26] M. C. Campi and S. Garatti, “Wait-and-judge scenario optimization,” Mathematical Programming, vol. 167, pp. 155–189, 2018.

- [27] Y. Yang and C. Sutanto, “Chance-constrained optimization for nonconvex programs using scenario-based methods,” ISA transactions, vol. 90, pp. 157–168, 2019.

- [28] J. Luedtke, S. Ahmed, and G. L. Nemhauser, “An integer programming approach for linear programs with probabilistic constraints,” Mathematical programming, vol. 122, no. 2, pp. 247–272, 2010.

- [29] A. Nemirovski and A. Shapiro, “Convex approximations of chance constrained programs,” SIAM Journal on Optimization, vol. 17, no. 4, pp. 969–996, 2007.

- [30] A. Nemirovski, “On safe tractable approximations of chance constraints,” European Journal of Operational Research, vol. 219, no. 3, pp. 707–718, 2012.

- [31] K. Margellos, P. Goulart, and J. Lygeros, “On the road between robust optimization and the scenario approach for chance constrained optimization problems,” IEEE Transactions on Automatic Control, vol. 59, no. 8, pp. 2258–2263, 2014.

- [32] S. Peng, “Chance constrained problem and its applications,” Ph.D. dissertation, Université Paris Saclay (COmUE); Xi’an Jiaotong University, 2019.

- [33] G. C. Calafiore and L. E. Ghaoui, “On distributionally robust chance-constrained linear programs,” Journal of Optimization Theory and Applications, vol. 130, pp. 1–22, 2006.

- [34] E. Delage and Y. Ye, “Distributionally robust optimization under moment uncertainty with application to data-driven problems,” Operations research, vol. 58, no. 3, pp. 595–612, 2010.

- [35] J. Cheng, E. Delage, and A. Lisser, “Distributionally robust stochastic knapsack problem,” SIAM Journal on Optimization, vol. 24, no. 3, pp. 1485–1506, 2014.

- [36] Z. Chen, D. Kuhn, and W. Wiesemann, “Data-driven chance constrained programs over wasserstein balls,” Operations Research, 2022.

- [37] A. R. Hota, A. Cherukuri, and J. Lygeros, “Data-driven chance constrained optimization under wasserstein ambiguity sets,” in 2019 American Control Conference (ACC). IEEE, 2019, pp. 1501–1506.

- [38] R. Ji and M. A. Lejeune, “Data-driven distributionally robust chance-constrained optimization with wasserstein metric,” Journal of Global Optimization, vol. 79, no. 4, pp. 779–811, 2021.

- [39] R. Jiang and Y. Guan, “Data-driven chance constrained stochastic program,” Mathematical Programming, vol. 158, no. 1-2, pp. 291–327, 2016.

- [40] Z. Hu and L. J. Hong, “Kullback-leibler divergence constrained distributionally robust optimization,” Available at Optimization Online, vol. 1, no. 2, p. 9, 2013.

- [41] R. J. Tibshirani, R. Foygel Barber, E. Candes, and A. Ramdas, “Conformal prediction under covariate shift,” Advances in neural information processing systems, vol. 32, 2019.

- [42] A. Lin and S. Bansal, “Verification of neural reachable tubes via scenario optimization and conformal prediction,” arXiv preprint arXiv:2312.08604, 2023.

- [43] R. Koenker and G. Bassett Jr, “Regression quantiles,” Econometrica: journal of the Econometric Society, pp. 33–50, 1978.

- [44] M. Cleaveland, I. Lee, G. J. Pappas, and L. Lindemann, “Conformal prediction regions for time series using linear complementarity programming,” arXiv preprint arXiv:2304.01075, 2023.

- [45] S. P. Boyd and L. Vandenberghe, Convex optimization. Cambridge university press, 2004.

- [46] A. Fischer, “A newton-type method for positive-semidefinite linear complementarity problems,” Journal of Optimization Theory and Applications, vol. 86, pp. 585–608, 1995.

- [47] A. Bemporad and M. Morari, “Control of systems integrating logic, dynamics, and constraints,” Automatica, vol. 35, no. 3, pp. 407–427, 1999.

- [48] T. Achterberg, “Scip: solving constraint integer programs,” Mathematical Programming Computation, vol. 1, pp. 1–41, 2009.

- [49] I. Gibbs and E. Candes, “Adaptive conformal inference under distribution shift,” Advances in Neural Information Processing Systems, vol. 34, pp. 1660–1672, 2021.

- [50] M. Zaffran, O. Féron, Y. Goude, J. Josse, and A. Dieuleveut, “Adaptive conformal predictions for time series,” in International Conference on Machine Learning. PMLR, 2022, pp. 25 834–25 866.

- [51] M. Cauchois, S. Gupta, A. Ali, and J. C. Duchi, “Robust validation: Confident predictions even when distributions shift,” arXiv preprint arXiv:2008.04267, 2020.

- [52] A. Gendler, T.-W. Weng, L. Daniel, and Y. Romano, “Adversarially robust conformal prediction,” in International Conference on Learning Representations, 2021.

- [53] Y. Romano, E. Patterson, and E. Candes, “Conformalized quantile regression,” Advances in neural information processing systems, vol. 32, 2019.

- [54] M. Sesia and E. J. Candès, “A comparison of some conformal quantile regression methods,” Stat, vol. 9, no. 1, p. e261, 2020.

- [55] J. Lei, A. Rinaldo, and L. Wasserman, “A conformal prediction approach to explore functional data,” Annals of Mathematics and Artificial Intelligence, vol. 74, pp. 29–43, 2015.

- [56] L. Guan and R. Tibshirani, “Prediction and outlier detection in classification problems,” Journal of the Royal Statistical Society Series B: Statistical Methodology, vol. 84, no. 2, pp. 524–546, 2022.

- [57] W. Xie, S. Ahmed, and R. Jiang, “Optimized bonferroni approximations of distributionally robust joint chance constraints,” Mathematical Programming, vol. 191, no. 1, pp. 79–112, 2022.

- [58] L. Lindemann, M. Cleaveland, G. Shim, and G. J. Pappas, “Safe planning in dynamic environments using conformal prediction,” IEEE Robotics and Automation Letters, 2023.

- [59] V. Raman, A. Donzé, M. Maasoumy, R. M. Murray, A. Sangiovanni-Vincentelli, and S. A. Seshia, “Model predictive control with signal temporal logic specifications,” in 53rd IEEE Conference on Decision and Control. IEEE, 2014, pp. 81–87.

- [60] A. K. Kuchibhotla, “Exchangeability, conformal prediction, and rank tests,” arXiv preprint arXiv:2005.06095, 2020.

- [61] R. Koenker, Quantile regression. Cambridge university press, 2005, vol. 38.

- [62] Y. Zhao, B. Hoxha, G. Fainekos, J. V. Deshmukh, and L. Lindemann, “Robust conformal prediction for stl runtime verification under distribution shift,” arXiv preprint arXiv:2311.09482, 2023.

- [63] L. Devroye, A. Mehrabian, and T. Reddad, “The total variation distance between high-dimensional gaussians with the same mean,” arXiv preprint arXiv:1810.08693, 2018.

Appendix

Appendix A Conformal Predictive Programming for Joint Chance Constrained Optimization

In practice, we often require the simultaneous satisfaction of multiple chance constraints with high probability. Specifically, in such cases, we are interested in solving the optimization problem

| (17a) | ||||

| s.t. | (17b) | |||

| (17c) | ||||

| (17d) | ||||

to which we refer to as a joint chance constraint optimization (JCCO) problem. Here, indicates the number of chance constraints as defined by the functions . We emphasize that the only difference between the optimization problems in equations (17) and (3) is in the joint chance constraint in equation (17b). Starting off from CPP as introduced in the main part of the paper, we next present two extensions of CPP through which we can solve JCCO problems in (17).

Joint Chance Constrained Optimization via Union Bounding. The first method is based on Boole’s inequality which has been employed in prior work to provide conformal prediction guarantees [57, 6, 58]. The main idea here is to dissect the joint chance constraint in (17b) into individual chance constraints that we instead enforce with a confidence of . Specifically, we solve the optimization problem

| (18a) | ||||

| s.t. | (18b) | |||

| (18c) | ||||

| (18d) | ||||

by rewriting each of the individual chance constraints in equation (18b) with one of the two quantile reformulations presented before. We describe the relationship between (17) and (18) in Theorem A.1.

Theorem A.1.

Proof.

Let be a feasible solution to (18). It trivially holds that and . By Boole’s inequality, . Equivalently, it holds that . ∎

Subsequently, we can encode each chance constraint in (18b) either by following the CPP-KKT or the CPP-MIP approach introduced in Section 4, but now with ). As we noted before, a feasible solution to (18) via the CPP-KKT or the CPP-MIP is also a feasible solution to (17). Similar to Theorem 3.2 but now with , we compute the probabilistic upper bound

for each individual chance constraint such that . We can find an upper bound again via Boole’s inequality such that , formally summarized next.

Theorem A.2.

Let , then it holds that .

Proof.

Since we know that for all , it holds by Boole’s inequality that . Equivalently, it holds that . ∎

As emphasized before Theorem A.1, the optimal solution of (18) may not be the optimal solution of (17). In fact, we expect an optimal solution of (18) to be more conservative. However, by means of we obtain interpretability of the individual chance constraints , i.e., we obtain information in how far the corresponding constraint may be violated or satisfied. Next, we further present an equivalent and nonconservative encoding by again using mixed integer programming. This solution may have higher computational cost than the encoding presented in this section.

Joint Chance Constrained Optimization via Mixed Integer Programming. The second method that we present to solve the JCCO problem in (17) is by computing the maximum over the chance constraint functions . Motivated by standard formulations used in [6], we thus first rewrite (17) into

| (19a) | ||||

| s.t. | (19b) | |||

| (19c) | ||||

| (19d) | ||||

We can trivially see that the optimization problems in (19) and (17) are equivalent. Next, we can encode the max operator in equation (19b) with a mixed integer program (MIP) using the Big-M method [47]. Suppose we want to encode the maximum as for a given index . We can introduce a set of binary variables for , and any satisfying the following set of constraints

| (20a) | |||

| (20b) | |||

| (20c) | |||

| (20d) | |||

encodes the maximum exactly, see e.g., [59]. Intuitively, denotes if is the maximum.

We can now use this MIP encoding to solve the JCCO problem in (19). We first do so by following the CPP-MIP approach. By substituting with in the optimization problem (11), we arrive at (21).

| (21a) | ||||

| s.t. | (21b) | |||

| (21c) | ||||

| (21d) | ||||

| (21e) | ||||

| (21f) | ||||

| (21g) | ||||

| (21h) | ||||

that is equivalent to (19). Note here again that . In (21), and follow the same intuition as in (11).

The same MIP encoding of the operator can be taken for the CPP-KKT approach, which results in

| (22a) | ||||

| s.t. | (22b) | |||

| (22c) | ||||

Suppose now that we attain a solution from solving (21) or (22). We can then again certify its feasibility similar to Theorem 3.2 by computing

such that , or equivalently, . We emphasize that comparing to the aforementioned union bound approach to solve the JCCO problem, the solution to (19) is nonconservative. However, due to the introduction of new binary variables, it is computationally more costly and it lacks interpretability as discussed before. We empirically illustrate our results with a case study in Appendix D.5.

Appendix B Proofs for Technical Theorems and Lemmas

B.1 Proof for Theorem 3.2

B.2 Proof for Lemma 4.1

Proof.

Consider the function and the optimization problem

| (23) |

From Chapter 1 in [61], we know that the solution of (23) is equivalent to as defined in equation (2) if . If , however, the solution of (23) can be any value belonging to the set where is the empirical distribution over . Since is monotone, it is easy to see that the solution to (23) is an upper bound of the quantile . Therefore, it is sufficient to show that (6) is equivalent to (23). We see this as follows. Note that , which is equivalent to (6) by variable splitting. ∎

B.3 Proof for Theorem 4.3

Proof.

A linear program has zero duality gap [45]. This implies that the optimal solution of the inner problem in equations (7d), (7e), and (7f) is equivalent to the KKT conditions in (8d)-(8k). Hence, (8) is equivalent to (7). Due to Corollary 4.2, we conclude that a feasible solution to (8) is a feasible solution to (4). ∎

B.4 Proof for Theorem 5.2

Proof.

Recall that , and let denote the pushforward measure of under , i.e., . Note that are independent and identically distributed since is independent of . Let now be any distribution from and let . Let also where is the pushforward measure of under . By the data processing inequality, it follows that . Therefore, by Lemma C.1, . ∎

Appendix C Robust Conformal Prediction

Recall from Section 2 that are assumed to be exchangeable. In practice, however, this assumption is usually violated, e.g., we may have calibration data from a simulator while the data observed during deployment is different. Nonetheless, we would like to provide guarantees when and are statistically close. Let and denote calibration and deployment distributions, respectively, and let while . To capture their distance, we use the -divergence which is defined as

| (24) |

where is the support of and where is the Radon-Nikodym derivative. It is hence assumed that is absolutely continuous with respect to . The function needs to be convex with and for all . If , we attain the total variation distance where and represent the probability density functions corresponding to and . The next result is mainly taken from [51] and is presented as summarized in [62].

Lemma C.1 (Corollary 2.2 in [51]).

Let and be independent random variables such that . For a failure probability of , assume that with

Then, it holds that with

| (25) |

We emphasize that and in Lemma C.1 are convex optimization problems and can thus be computed efficiently.

Appendix D Supplementary Experimental Results

D.1 General Nonlinear CCO Problem: Results with Varying Training and Calibration Size

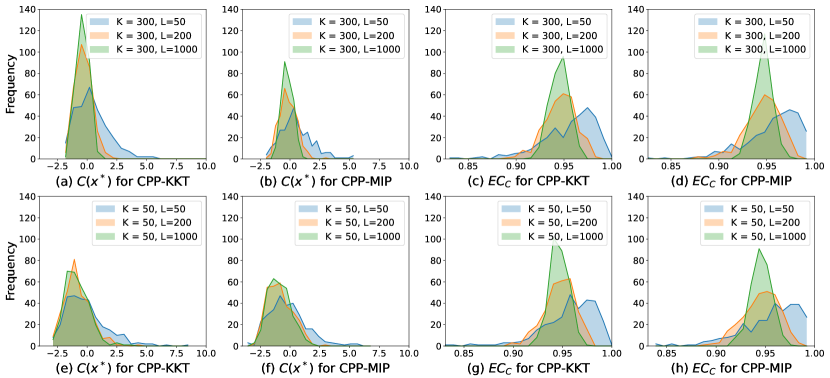

Supplementary Results for Feasibility Guarantees. We showcase the effect of the size of the training dataset and the calibration dataset on the guarantee in Theorem 3.2 by repeating the second step in the Experimental Procedure from the case study in Section 6. We let . We first fix and vary . We show the empirical distribution of the upper bound for CPP-KKT in Figure 3(a) and for CPP-MIP in Figure 3(b). We demonstrate the empirical distribution of the empirical coverage for CPP-KKT in Figure 3(c) and for CPP-MIP in Figure 3(d). Now, we choose and vary . Similarly, we show the empirical distribution of the upper bound for CPP-KKT in Figure 3(e) and for CPP-MIP in Figure 3(f). We demonstrate the empirical distribution of the empirical coverage for CPP-KKT in Figure 3(g) and for CPP-MIP in Figure 3(h). From the figures, one can infer as expected that the coverage in Theorem 3.2 benefits from a large training and a large calibration size.

Supplementary Results for Average Statistics. We showcase the effect of size of the training dataset and the calibration dataset on the computation times by repeating the experimental procedure from the case study in Section 6. We fix and and show in Table LABEL:table:average_statistics the average statistics of the experimental results with and .

| Solver Time (s) | ||||||

|---|---|---|---|---|---|---|

| K = 50, L = 50 | CPP-KKT | 0.211 | -0.964 | 0.963 | 0.961 | 0.649 |

| CPP-MIP | 0.105 | -0.959 | 0.964 | 0.959 | 0.114 | |

| K = 50, L = 200 | CPP-KKT | -0.49 | -0.964 | 0.963 | 0.951 | 0.649 |

| CPP-MIP | -0.565 | -0.959 | 0.964 | 0.949 | 0.114 | |

| K = 50, L = 500 | CPP-KKT | -0.546 | -0.964 | 0.963 | 0.95 | 0.649 |

| CPP-MIP | -0.62 | -0.959 | 0.964 | 0.949 | 0.114 | |

| K = 50, L = 750 | CPP-KKT | -0.523 | -0.964 | 0.963 | 0.951 | 0.649 |

| CPP-MIP | -0.603 | -0.959 | 0.964 | 0.95 | 0.114 | |

| K = 50, L = 1000 | CPP-KKT | -0.541 | -0.964 | 0.963 | 0.951 | 0.649 |

| CPP-MIP | -0.618 | -0.959 | 0.964 | 0.95 | 0.114 | |

| K = 100, L = 50 | CPP-KKT | 0.838 | -1.007 | 0.949 | 0.96 | 1.394 |

| CPP-MIP | 0.767 | -1.003 | 0.952 | 0.962 | 0.134 | |

| K = 100, L = 200 | CPP-KKT | 0.036 | -1.007 | 0.949 | 0.949 | 1.394 |

| CPP-MIP | 0.027 | -1.003 | 0.952 | 0.951 | 0.134 | |

| K = 100, L = 500 | CPP-KKT | -0.009 | -1.007 | 0.949 | 0.949 | 1.394 |

| CPP-MIP | -0.035 | -1.003 | 0.952 | 0.951 | 0.134 | |

| K = 100, L = 750 | CPP-KKT | -0.01 | -1.007 | 0.949 | 0.95 | 1.394 |

| CPP-MIP | -0.025 | -1.003 | 0.952 | 0.951 | 0.134 | |

| K = 100, L = 1000 | CPP-KKT | 0.007 | -1.007 | 0.949 | 0.95 | 1.394 |

| CPP-MIP | -0.107 | -1.003 | 0.952 | 0.949 | 0.134 | |

| K = 200, L = 50 | CPP-KKT | 0.883 | -1.007 | 0.951 | 0.963 | 7.273 |

| CPP-MIP | 0.866 | -1.008 | 0.95 | 0.962 | 0.186 | |

| K = 200, L = 200 | CPP-KKT | 0.044 | -1.007 | 0.951 | 0.95 | 7.273 |

| CPP-MIP | 0.026 | -1.008 | 0.95 | 0.949 | 0.186 | |

| K = 200, L = 500 | CPP-KKT | -0.062 | -1.007 | 0.951 | 0.949 | 7.273 |

| CPP-MIP | -0.003 | -1.008 | 0.95 | 0.95 | 0.186 | |

| K = 200, L = 750 | CPP-KKT | 0.01 | -1.007 | 0.951 | 0.951 | 7.273 |

| CPP-MIP | 0.007 | -1.008 | 0.95 | 0.951 | 0.186 | |

| K = 200, L = 1000 | CPP-KKT | -0.043 | -1.007 | 0.951 | 0.95 | 7.273 |

| CPP-MIP | -0.03 | -1.008 | 0.95 | 0.95 | 0.186 | |

| K = 300, L = 50 | CPP-KKT | 0.757 | -1.008 | 0.951 | 0.959 | 6.476 |

| CPP-MIP | 0.739 | -1.009 | 0.951 | 0.96 | 0.225 | |

| K = 300, L = 200 | CPP-KKT | 0.048 | -1.008 | 0.951 | 0.95 | 6.476 |

| CPP-MIP | 0.048 | -1.009 | 0.951 | 0.95 | 0.225 | |

| K = 300, L = 500 | CPP-KKT | 0.017 | -1.008 | 0.951 | 0.951 | 6.476 |

| CPP-MIP | -0.028 | -1.009 | 0.951 | 0.95 | 0.225 | |

| K = 300, L = 750 | CPP-KKT | -0.023 | -1.008 | 0.951 | 0.95 | 6.476 |

| CPP-MIP | -0.012 | -1.009 | 0.951 | 0.95 | 0.225 | |

| K = 300, L = 1000 | CPP-KKT | -0.046 | -1.008 | 0.951 | 0.95 | 6.476 |

| CPP-MIP | -0.016 | -1.009 | 0.951 | 0.95 | 0.225 | |

| K = 500, L = 50 | CPP-KKT | 0.874 | -1.012 | 0.95 | 0.962 | 15.093 |

| CPP-MIP | 0.827 | -1.01 | 0.95 | 0.961 | 0.326 | |

| K = 500, L = 200 | CPP-KKT | 0.018 | -1.012 | 0.95 | 0.948 | 15.093 |

| CPP-MIP | 0.111 | -1.01 | 0.95 | 0.951 | 0.326 | |

| K = 500, L = 500 | CPP-KKT | 0.014 | -1.012 | 0.95 | 0.95 | 15.093 |

| CPP-MIP | 0.011 | -1.01 | 0.95 | 0.95 | 0.326 | |

| K = 500, L = 750 | CPP-KKT | 0.034 | -1.012 | 0.95 | 0.951 | 15.093 |

| CPP-MIP | 0.037 | -1.01 | 0.95 | 0.951 | 0.326 | |

| K = 500, L = 1000 | CPP-KKT | 0.003 | -1.012 | 0.95 | 0.95 | 15.093 |

| CPP-MIP | -0.004 | -1.01 | 0.95 | 0.95 | 0.326 |

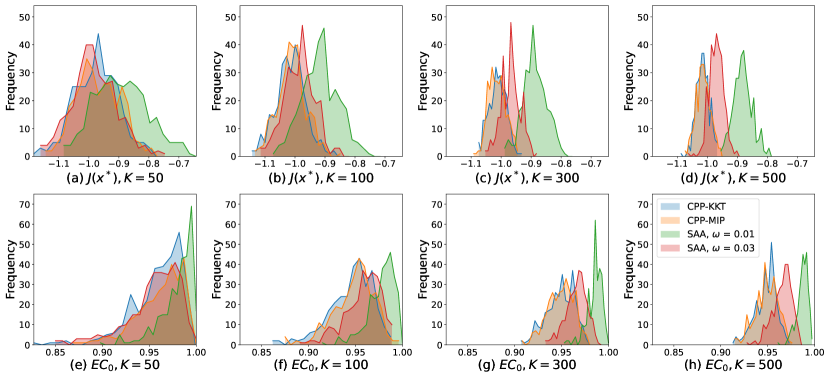

D.2 General Nonlinear CCO Problem: Comparison between CPP, SA, and SAA

We empirically compare our method with the scenario approach (SA) for general nonconvex problems from [23] and the sample average approximation (SAA) approach from [11] on the general nonlinear CCO problem from Section 6. We emphasize that CPP provides marginal probabilistic feasibility guarantees which are different from the feasibility guarantees of SA and SAA making a theoretical comparison difficult. In our comparison, we thus solve the CPP, SA, and SAA problems with the same number of training data . For SA, this may result in conservative solutions.

Recall that in SAA, we approach the CCO problem by enforcing equation (1). In [11], for the approximation in (1), it is shown that for the choice of a feasibility guarantee can be provided conditioned on the domain of . Under Lipschitz continuity of , this can also be guaranteed by the chance constraint

| (26) |

for any where can be arbitrarily small. As mentioned in Remark (1), CPP shares algorithmic similarities with SAA for the special choice of . To show the similarity, we compare in Figure 4 the results attained by CPP and by SAA (with the choices of and ) for the general nonlinear CCO problem from Section 6 again with and and for varying . We omit in our comparison, since setting a small will have no practical impact to our experimental results. For a fair comparison, we use the equivalence-preserving MIP encoding introduced in Section 4 for the SAA. In Figure 4, we see that attains similar results to both CPP-KKT and CPP-MIP, especially when , where the selected is closed to .

In SA, recall that we require all scenarios to satisfy the constraint for the decision variable . We compare SA and CPP, again on the general nonlinear CCO problem from Section 6, with varying in Figure 5 with and . As we expect, we see SA attains more conservative results than CPP, since CPP only requires a portion of the constraints on the scenarios to be satisfied. We remark that a feasibility guarantee exists for SA [23], but we will refrain from comparing to it in this paper since our feasibility guarantees are, as said before, marginal and with respect to .

D.3 Optimal Control Problem: Plots

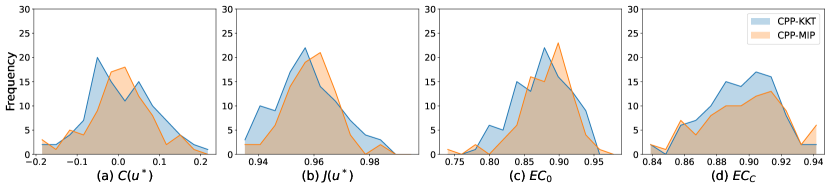

We show the results for the optimal control case study in Figure 6. The number of timeouts for CPP-KKT and CPP-MIP are and respectively. None of the methods have infeasible solution.

D.4 Portfolio Optimization Problem: Plots

To calculate the distribution shift, we use the KL divergence as our choise of f-divergence where . We estimate the distribution shift as by computing following [63], where a closed-form expression for the KL-divergence is given as

| (27) |

where are the mean and covariance of and are the mean and convariance of . We show the results for the portfolio optimization case study in Figure 7, where we see that our RCPP achieves the expected coverage and , while CPP undercovers and does not account for distribution shift. No timeouts of infeasible solutions are observed for all four methods. The average computation time for CPP-KKT with RCPP, CPP-MIP with RCPP, CPP-KKT with CPP, and CPP-MIP with CPP are 3.05s, 2.28s, 9.26s, 2.54s, respectively.

D.5 Case Study for JCCO

Problem Statement. In this section, we showcase how to use CPP to solve JCCO problems as explained in Appendix A. We are interested in solving the JCCO problem

| (28) | ||||

| s.t. | ||||

where is the decision variable, , ,

and is a random vector where we fix (a Student’s t-distribution) and . Note that we can use the linear JCCO program in (28) to encode practical problems including the probability set coverage problem [11].

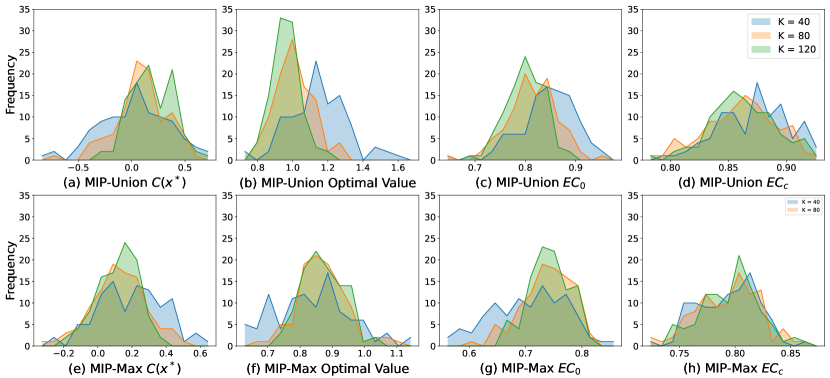

Results. We repeat the experimental procedure from Section 6 with with CPP-MIP using both the union bound (which we refer to as MIP-Union) and the maximum operator (which we refer to as MIP-Max) as introduced in Section D.5. We remark that we do not show the results for CPP-KKT due to the number of timeouts that we observed with the maximum operator encoding while the results for the union bound showed similar results as MIP-Union.

We observe no timeout nor infeasible solution with CPP-MIP. We show the empirical distribution of for MIP-Union in Figure 8(a) and for MIP-Max in Figure 8(e) where both distributions are centered near zero. We highlight that MIP-Union, as expected, is more conservative in terms of the distribution of optimal values, which we show in Figure 8(b), as compared to MIP-Max, shown in Figure 8(f). Since the union bound is more conservative, we see the same trend on their corresponding distributions of and in Figure 8, where MIP-Union attains better coverage results. However, for both distributions, we observe the expected distributions of , both of which center above 0.8.