Asymptotic Equivalency of

Two Different Approaches of -statistics

Chudamani Poudyal111

Chudamani Poudyal, PhD, ASA,

is an Assistant Professor

in the Department of Mathematical Sciences,

University of Wisconsin-Milwaukee,

P.O. Box 413,

Milwaukee, WI 53201, USA.

E-mail: cpoudyal@uwm.edu

There are several ways to establish

the asymptotic normality of -statistics,

depending upon the selection of the weights

generating function and the cumulative

distribution function of the underlying model.

Here, in this paper it is shown that the

two of the asymptotic approaches are

equivalent/equal for a particular

choice of the weights generating function.

For a positive integer ,

let be an iid sample

from an unknown true underlying cumulative

distribution function with the parameter vector

.

The motivation of most of the statistical inference

is to estimate the parameter vector

from the available sample dataset.

The corresponding order statistic

of the sample is denoted by

.

In order to estimate the

parameter vector ,

the statistics we are interested

here is a linear combination

of the order values,

so the name -statistics,

in the form

(1)

where

represents a weights-generating.

Both and

are specially chosen functions,

(see, e.g., Poudyal, 2021, Poudyal and Brazauskas, 2022)

and are known that are specified

by the statistician.

The corresponding population qualities

are then given by

(2)

Like classical method of moments,

-estimators are found by matching sample

-moments, Eq. (1),

with population -moments,

Eq. (2),

for ,

and then solving the system of equations

with respect to .

The obtained solutions,

which we denote by

,

, are, by definition,

the -estimators of

.

Note that the functions are such that

Further,

define

(3)

Consider

Ideally,

we expect that the statistics vector

converges in distribution

to the population vector .

As mentioned by

Serfling (1980, §8.2 and references therein),

there are several approaches of

establishing asymptotic normality

of

depending upon the various

scenarios of the weights generating

function and the underlying cdf .

This paper focuses only on a

specific weights generating function .

In particular,

Chernoff et al. (1967, Remark 9)

established that the -variate vector

,

converges in distribution to the

-variate normal random vector

with mean and

the variance-covariance matrix

with the entries

(4)

(5)

(6)

where the function is defined as

(7)

For given

,

and with the specific

weights-generating function

(10)

the sample -moments, Eq. (1),

and the population -moments, Eq. (2)

are simply the sample and population

trimmed moments, respectively.

For these specific weights-generating

functions,

Brazauskas et al. (2007, 2009) independently

established an equivalent simplified

expression for ,

which can be written as

(11)

The motivation of this paper is

to show the equivalency of the Eqs.

(4),

(5),

(6), and

(11).

2 Preliminaries

In order to establish the equivalency of

the different approaches mentioned

in Section 1,

we summarize essential measure theoretic

preliminaries in this section.

Let and

are Lebesgue measurable set and function,

respectively.

Then,

following Folland (1999, p. 65),

we define

(12)

(13)

It is well known that,

Fubini’s Theorem provides

a crucial link between

multiple integrals and iterated integrals,

assuming the function involved is integrable.

Essentially, it enables evaluation of double integrals

by swapping the order of integration

(and, by extension, multiple integrals)

as iterated one dimensional integrals.

Here, we state the Fubini’s Theorem

without introducing the concept of product measure.

Theorem 1(Fubini’s Theorem - Folland (1999), p. 67).

Let ,

s.t. and ,

is a rectangular region.

Consider a function

then the Fubini’s Theorem states that

(14)

(15)

An immediate application of the

Fubini’s Theorem is the following corollary.

Corollary 1.

Let and

are two integrable functions

in the finite interval

with such that

Here, we establish the equivalency

of the two asymptotic approaches

for the weights-generating function

given by Eq. (10).

That is, we establish the equivalency of the Eqs.

(4),

(5),

(6), and

(11).

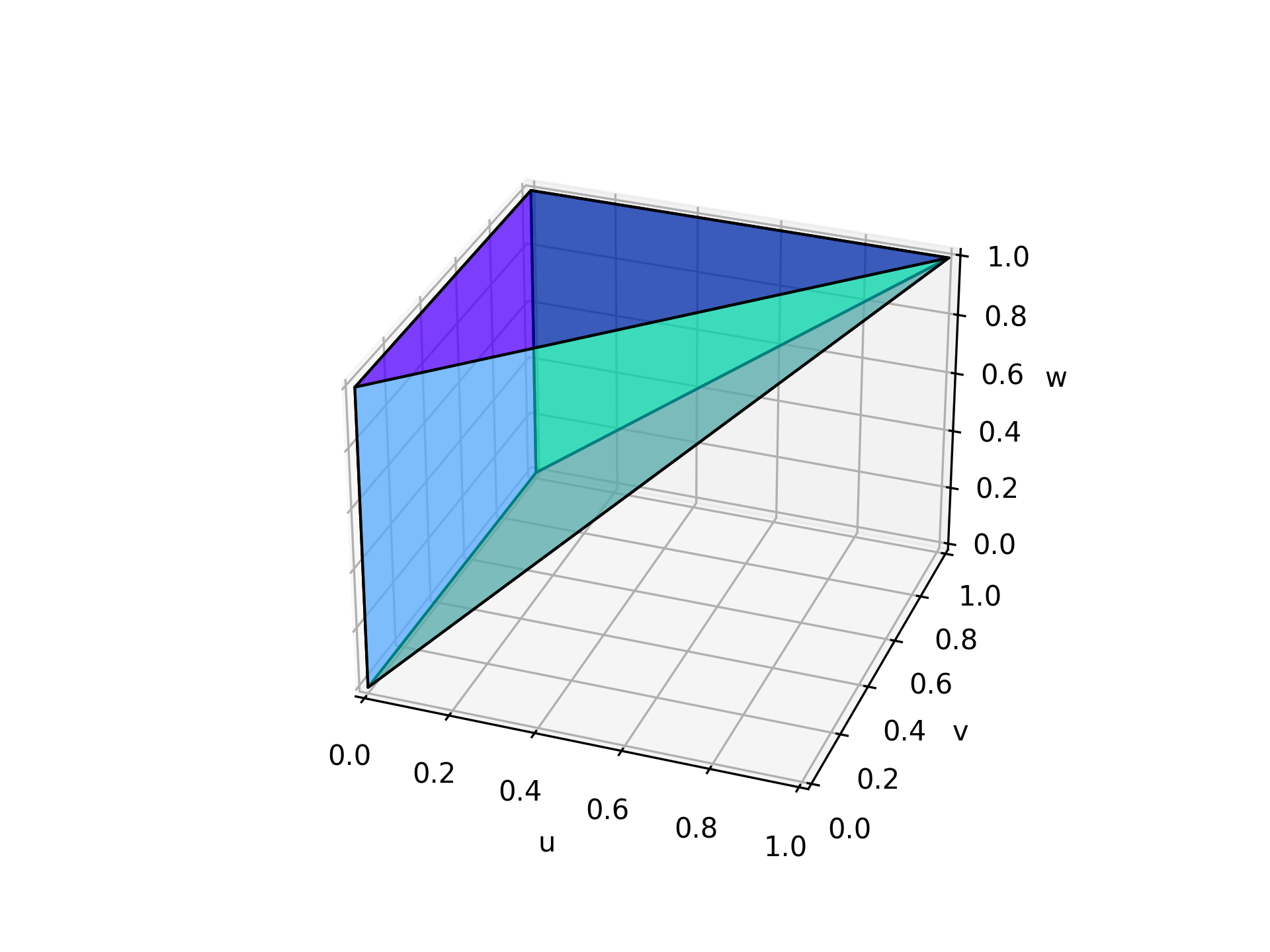

where the domain of integration,

,

in Eq. (20),

is defined as

(21)

Figure 1: Visualization of the set .

It is clear that

–

a rectangular pyramid as shown

in Figure 1,

is a measurable subset of the unit

cube .

That is,

the Lebesgue measure of

is simply the

volume of which is 1/3.

Also, note that

,

, and

.

Since is measurable

and assuming the functions

involved in Eq. (20)

satisfy the conditions for Fubini’s Theorem,

then the order of integration in

Eq. (20) can be changed.

That is,

(22)

As observed in Eq. (22),

in order to establish

Eq. (5)

Eq. (6),

it simply remains to show that

(23)

To establish this equality,

we investigate in two scenarios.

Brazauskas et al. (2007)

Brazauskas, V., Jones, B.L., and Zitikis, R. (2007).

Robustification and performance evaluation of empirical risk measures

and other vector-valued estimators.

METRON–International Journal of Statistics, 65(2),

175–199.

Brazauskas et al. (2009)

Brazauskas, V., Jones, B.L., and Zitikis, R. (2009).

Robust fitting of claim severity distributions and the method of

trimmed moments.

Journal of Statistical Planning and Inference,

139(6), 2028–2043.

Chernoff et al. (1967)

Chernoff, H., Gastwirth, J.L., and Johns, Jr., M.V. (1967).

Asymptotic distribution of linear combinations of functions of order

statistics with applications to estimation.

Annals of Mathematical Statistics, 38(1), 52–72.

Folland (1999)

Folland, G.B. (1999).

Real Analysis: Modern Techniques and Their Applications.

Second edition. John Wiley & Sons, New York.

Poudyal (2021)

Poudyal, C. (2021).

Robust estimation of loss models for lognormal insurance payment

severity data.

ASTIN Bulletin. The Journal of the International Actuarial

Association, 51(2), 475–507.

Poudyal and Brazauskas (2022)

Poudyal, C. and Brazauskas, V. (2022).

Robust estimation of loss models for truncated and censored severity

data.

Variance – The scientific journal of the Casualty Actuarial

Society, 15(2), 1–20.

Serfling (1980)

Serfling, R.J. (1980).

Approximation Theorems of Mathematical Statistics.

John Wiley & Sons, New York.