Risk-Sensitive Multi-Agent Reinforcement Learning in Network Aggregative Markov Games

Abstract.

Classical multi-agent reinforcement learning (MARL) assumes risk neutrality and complete objectivity for agents. However, in settings where agents need to consider or model human economic or social preferences, a notion of risk must be incorporated into the RL optimization problem. This will be of greater importance in MARL where other human or non-human agents are involved, possibly with their own risk-sensitive policies. In this work, we consider risk-sensitive and non-cooperative MARL with cumulative prospect theory (CPT), a non-convex risk measure and a generalization of coherent measures of risk. CPT is capable of explaining loss aversion in humans and their tendency to overestimate/underestimate small/large probabilities. We propose a distributed sampling-based actor-critic (AC) algorithm with CPT risk for network aggregative Markov games (NAMGs), which we call Distributed Nested CPT-AC. Under a set of assumptions, we prove the convergence of the algorithm to a subjective notion of Markov perfect Nash equilibrium in NAMGs. The experimental results show that subjective CPT policies obtained by our algorithm can be different from the risk-neutral ones, and agents with a higher loss aversion are more inclined to socially isolate themselves in an NAMG.111Code available at https://github.com/hafezgh/risk-sensitive-marl-namg

1. Introduction

Markov game (MG) is a common framework for studying multi-agent systems (MAS), and it is the main theoretical framework for multi-agent reinforcement learning (MARL) (Shapley, 1953; Littman, 1994). In classical MARL, each agent is assumed to have a risk-neutral objective, i.e., it tries to maximize a notion of expected return without taking into account subjective preferences of itself or of the other agents in the MAS. Risk-neutral MARL in MGs has seen great advances in recent years, especially in specific types of MGs, such as zero-sum MGs (Sayin et al., 2021; Zhang et al., 2020; Alacaoglu et al., 2022; Perolat et al., 2015; Qiu et al., 2021b) and Markov potential games (Ding et al., 2022; Fox et al., 2022; Maheshwari et al., 2022; Mguni et al., 2021; Leonardos et al., 2021). However, the risk-neutral RL objective often falls short when representing agents with distinct subjective preferences, such as internal cognitive biases of themselves or of other agents. Thus, to address these preferences, agents integrate a risk measure into their RL objective, ushering into the realm of risk-sensitive reinforcement learning (RSRL). In general, the literature on risk-sensitive MARL is more sparse compared to single-agent RSRL. The majority of the works that consider risk-sensitive multi-agent MDPs are concerned not with an RL setting but either with theoretically proving the existence of Markov perfect Nash equilibria, or finding these equilibria using iterative algorithms given complete information of the game in a centralized setting for MDPs with specific constraints (Ghosh et al., 2023; Zhong et al., 2022; Ghosh et al., 2022; Pal and Pradhan, 2021; Başar, 2021; Zhang et al., 2021).

Risk in RL can be categorized into two main types based on the risk-sensitive objective, as delineated by Prashanth and Fu (Prashanth et al., 2022). The first category, explicit risks, involves directly incorporating the risk measure into the objective function. In contrast, implicit risks are integrated by imposing a constraint on the RL stochastic optimization problem. Notably, in practice, implicit risk-sensitive objectives are often transformed into explicit objectives. This is achieved by formulating a Lagrangian and computing its gradient to employ algorithms founded on policy gradient (PG) methods (Prashanth et al., 2022). Within the spectrum of implicit risk measures in RL and MDPs, notable examples include variance as risk ((Tamar et al., 2012, 2013; Prashanth and Ghavamzadeh, 2016) in single-agent RSRL, and (Reddy et al., 2019) in risk-sensitive MARL), and chance constraints ((Chow et al., 2017) in single-agent RSRL). On the other hand, explicit risk measures encompass entropic risk measures predicated on exponential return ((Borkar, 2001; Fei et al., 2021; Moharrami et al., 2022) in single-agent RSRL and (Noorani and Baras, 2022; Soorki et al., 2021) in risk-sensitive MARL), coherent risk measures, and cumulative prospect theory (CPT).

Coherent risk measures (Artzner et al., 1999; Delbaen, 2002), such as the well-known conditional value at risk (CVaR), mean semi-deviation (Shapiro et al., 2021), and spectral risk (Acerbi, 2002), are widely used in the fields of economy and operations research. Their application has also been explored within MDPs as dynamic risk measures. Osogami et al. (Osogami, 2012) showed that risk-sensitive MDPs governed by Markov coherent risk measures can be classified under the domain of robust MDPs. Subsequently, dynamic programming methodologies have been suggested for this type of MDPs (Ruszczyński, 2010; Cavus and Ruszczynski, 2014). Building on these works, PG-based techniques and actor-critic (AC) algorithms have also been developed for RSRL with coherent risk measures, as detailed in (La and Ghavamzadeh, 2013; Tamar et al., 2014; Chow and Ghavamzadeh, 2014; Tamar et al., 2015) for single-agent RSRL, and in (Zhu et al., 2022; Munir et al., 2021; Qiu et al., 2021a) for risk-sensitive MARL.

CPT Background.

The concept of Prospect Theory (PT) emerged as an alternative model to expected utility theory, providing a more accurate model of human decision-making under uncertainty (Kahneman and Tversky, 1979). To enhance the applicability of PT, Cumulative Prospect Theory (CPT) was subsequently introduced (Tversky and Kahneman, 1992). Unlike PT, CPT applies weighting functions to cumulative probabilities, addressing them separately for positive and negative outcomes. By integrating these probability weighting functions and a non-linear utility function, CPT successfully illustrates varying human attitudes towards potential gains and losses against a subjective reference point. Central to CPT is the idea that humans typically exhibit aversion to losses, i.e., they generally take more risks when facing potential gains and take fewer risks when confronted with potential losses. Additionally, CPT’s framework elucidates human inclinations to overestimate small probabilities and underestimate large ones during uncertain decision-making. When we consider CPT in the context of either static or dynamic Markov risk measures, it meets only two of the four requirements that define a coherent risk measure. A risk measure, when applied to a random variable (r.v.) representing potential outcomes, is deemed coherent if it has the following four characteristics: convexity, monotonicity, translation invariance, and positive homogeneity (Artzner et al., 1999). Among these, the CPT risk measure only possesses monotonicity and positive homogeneity, and is neither translation invariant nor convex. The non-coherent nature of CPT makes it more challenging to work with mathematically. CPT can be seen as a generalization of coherent risk measures, i.e., by appropriate selection of CPT probability weighting functions, one can derive various coherent risk measure formulations (Lin and Marcus, 2013; Jie et al., 2018).

Contributions.

In this work, we consider risk-sensitive MARL with CPT risk measure in network aggregative Markov games (NAMGs), and propose a distributed actor-critic algorithm to find risk-sensitive policies for each agent. We derive a policy gradient theorem for CPT MARL based on a subjective steady-state distribution of the MDP from each agent’s prespective, and provide a sampling-based approach to estimate the value functions with asymptotic consistency. Since CPT is a generalization of coherent risk measures, our PG theorem generalizes the previous PG works for static and dynamic coherent risk measures (Chow and Ghavamzadeh, 2014; Tamar et al., 2015). Under a set of assumptions, we prove the convergence of our algorithm to a subjective and risk-sensitive notion of Markov perfect Nash equilibrium (MPNE) which we show is unique given the aforementioned assumptions. Experimentally, we also demonstrate that a higher loss aversion can make agents more conservative and increase their tendency for social isolation in an NAMG.

Remark 1.

(Application) A potential application of the proposed framework is calculating CPT risk-sensitive policies of human agents in real-world settings, such as driving scenarios or financial markets, that can be modeled by NAMGs. Subsequently, these policies can serve dual purposes: guiding agents towards strategies optimized for their individual preferences or facilitating social or economic changes in the environment to steer agents in a direction that aligns with desired outcomes.

2. Related Works

In the context of Markov risk measures in MDPs, CPT is articulated through two distinct formulations. The first formulation is the nested structure, wherein the CPT operator is applied to the cumulative return after each step (action taken) (Lin and Marcus, 2013; Lin, 2013; Lin et al., 2018). An important advantage of this formulation is that it ensures the existence of a Bellman optimality equation. Recently, Tian et al. (Tian et al., 2021) extended this nested formulation to a multi-agent setting with agents that are characterized by bounded rationality and operating under quantal level- strategies (Wright and Leyton-Brown, 2017). Restricting their approach to deterministic policies, they propose a centralized value iteration algorithm to determine optimal risk-sensitive policies given a complete model of the environment and the reward functions.

In the second formulation, the CPT operator is applied solely to the agent’s final cumulative return at the end of every episode (Prashanth et al., 2016; Jie et al., 2018). Contrary to the nested formulation, this formulation does not have a Bellman equation. However, it can be approached from a stochastic optimization perspective, allowing policy optimization through a gradient-based method akin to PG techniques (Jie et al., 2018). This PG method has also been implemented by considering neural networks for policy approximation (Markowitz et al., 2021). It is important to emphasize that the absence of the Bellman equation in this context necessitates policy optimization exclusively through offline Monte Carlo sampling constrained by a finite time horizon.

To date, no cognitive research has been conducted to ascertain which of the two CPT RSRL formulations best represents the dynamic risk behavior exhibited by humans, whether in single-agent or multi-agent environments. Nonetheless, the following can be said about the two formulations:

-

•

The nested formulation benefits from the presence of a Bellman equation, enabling the use of online actor-critic algorithms and a recursively defined value function. This advantage is absent in the non-nested formulation, where it is only plausible to use PG techniques using offline Monte Carlo sampling.

- •

-

•

The non-nested formulation aligns well with finite-horizon episodic tasks where the agent is rewarded at the end of each episode. However, its applicability is limited when considering infinite-horizon tasks. Conversely, the nested formulation and its Bellman equation are suitable for tasks where the agent is rewarded at every timestep.

-

•

In scenarios without complete information of the model, the reward function, or the policies of other agents, both formulations necessitate a strategy for estimating the CPT value given that we have access to a simulator of the MDP or a large enough experience dictionary (replay buffer). Such an estimation technique tailored for the non-nested formulation has been introduced by Jie et al. (Jie et al., 2018).

Remark 2.

(Motivation) Given the above considerations, in risk-sensitive MARL with CPT, in a setting where the agents interact in an online infinite-horizon MDP with limited information about other agents’ policies, the nested CPT formulation is the viable option to adopt. Due to the possibility of non-deterministic optimal policies for each agent in MARL, we opt for actor-critic style algorithms using parameterized policies. Furthermore, we consider NAMGs as our MARL framework due to three reasons. First, because they are inherently suited to distributed algorithms. Second, given a set of assumptions, NAMG, and its risk-sensitive version can be shown to have a unique Markov perfect Nash equilibrium which our algorithm converges to. And third, because NAMGs are a suitable framework to show the tangible effect of loss aversion in human-like agents and on their tendency for social isolation and conservatism.

3. Preliminaries

3.1. Cumulative Prospect Theory

Given a real-valued r.v. with distribution , a reference point , two monotonically non-decreasing weighting functions, , utility functions , and given appropriate integrability assumptions, we can define the CPT value using Choquet integrals as

| (1) |

where we denote and . For a discrete r.v., we can define the CPT value similarly as

| (2a) | |||

| (2b) | |||

| (2c) |

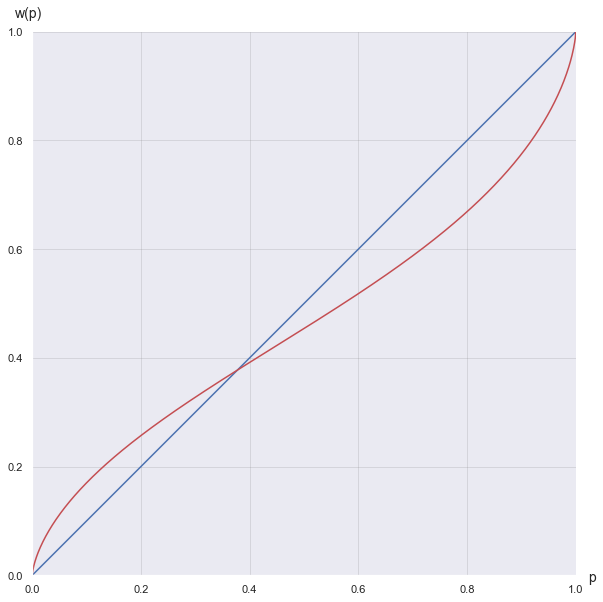

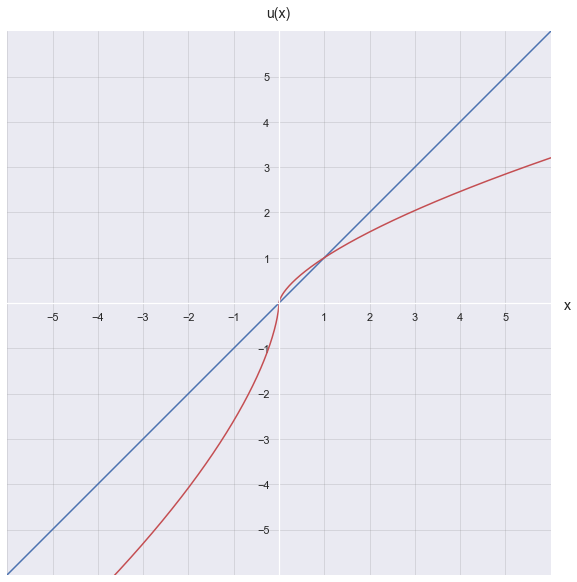

where serves as a reference point that separates gains and losses. Without loss of generality, we assume throughout this paper. Conventional representations of CPT weighting functions include and (Tversky and Kahneman, 1992), or and (Prelec, 1998). Note that by setting and equal to , the definition of expected utility is recovered which shows that CPT is a generalization of expected utility theory. Furthermore, and are usually concave functions ( is convex) to reflect the higher sensitivity of humans towards losses compared to gains (Kahneman and Tversky, 1979). As a result, the utility function can have analytical representations if , and if . The parameters and are subjective model parameters that can differ from person to person based on their level of risk-aversion and individual characteristics. The conventional representations of weighting and utility functions given a set of subjective parameters are plotted in Figures 1 and 2.

3.2. Network Aggregative Markov Games

Throughout this paper, we assume that agents are interacting in an ergodic network aggregative Markov game with a discounted infinite-horizon criterion. An NAMG with players is an MG denoted by , where is the state space, is the joint action space; is a joint reward function bounded in where ; is the MDP transition probability distribution; is a graph with edge set on which each agent interacts with its neighbors; is the MDP’s discount factor; and is the initial state distribution. In NAMG, for each agent , the reward function is a function of its own action and an aggregative function of other agents’ actions,

| (3) |

where we have,

| (4) |

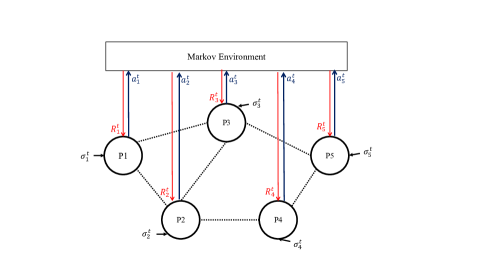

where are the edge weights of the communication graph , with denoting the weight of the edge from to . Therefore, given the graph, and by observing its neighbors’ actions, agent is able to calculate . Figure 3 shows a schematic of an NAMG.

Previously, in various domains, such as resource allocation (Deng, 2019), social networks (Zhu et al., 2013), electrical microgrids (Tan et al., 2021), and power systems (Deng, 2021), either single-state network aggregative games (NAGs), or dynamic network aggregative games have been studied in risk-neutral setting. Furthermore, most of the theoretical works in this domain have focused on studying convergence to the Markov perfect Nash or Stackelberg equilibrium in single-state or dynamic NAGs with quadratic cost/reward functions that ensure the uniqueness of the equilibrium (Parise et al., 2020; Cenedese et al., 2020; Shokri and Kebriaei, 2020; Saffar et al., 2017). In this paper, for the first time, we consider risk-sensitive NAMGs.

3.3. CPT Risk-Sensitive MARL Objective in NAMGs

Using the nested formulation, the objective of the risk-sensitive agent in an NAMG will be equivalent to

| (5) | ||||

where and , respectively. Using the properties of NAMGs, and considering as the probability that occurs at state for agent , we can rewrite the objective as

| (6) |

Therefore, by observing the actions of neighboring agents and calculating the aggregative term , agent can treat as a probability distribution similar to the transition probabilities for each state.

4. Distributed Nested CPT Policy Gradient

In this section, we derive a gradient expression for the Markov dynamic CPT risk measure in NAMGs, represented by the gradient of the initial state’s value function in an ergodic CPT risk-sensitive NAMG, . Before presenting the PG theorem, we state the following assumption,

Assumption 1.

The weight functions are double differentiable, and the derivatives are Lipschitz continuous with common constant . Furthermore, the utility functions are differentiable (denoted by ) for all agents.

The above assumption may seem strict at first. However, conventional forms of the CPT utility functions, specifically and , along with the weighting functions and , depicted in Figures 1 and 2, satisfy this assumption.

Theorem 1.

(Nested CPT Policy Gradient)

Given Assumption 1, the gradient of the CPT return for agent , , with respect to the policy parameter is

| (7) |

where, and represent the CPT cumulative weighting and utility functions of the agent from (2) (superscript is dropped). The distribution is a subjective steady-state probability distribution of the MDP in which , where is a subjective measure of time spent in each state and can be obtained by solving the following system of linear equations,

| (8) |

where denotes the probability that the Markov chain starts in state , and and are the utility cumulative weighting functions of agent from (2) ( and are chosen according to the sign of ).

Proof.

Considering agent , we drop the subscript and denote as and as . Furthermore, used below, where is equivalent to , is the more general case of joint policies in Markov games, which encompasses in an NAMG. The gradient of the CPT risk-sensitive return considering its recursive definition can be written as

| (9) |

We define

| (10) |

as the subjective (distorted) visitation probability of right after following policy . Note that since is a non-decreasing function with positive derivatives everywhere and is a function that maps to , this term is always positive. By defining , by recursion, we can write the subjective probability of visiting state after steps, starting from and following policy as

| (11) |

Therefore, after repeated unrolling, we can write (9) as

| (12) |

Similar to a risk-neutral MDP, given and the state value function corresponding to this policy, the function is an inherent property of the CPT risk-sensitive MDP (this function can be compared with the function in the proof of risk-neutral policy gradient theorem in (Sutton and Barto, 2018), Section 13.2). Therefore, we let , which can be considered a subjective (perceived) measure of time that the CPT risk-sensitive agent spends in state when following policy and starting from state . In a similar fashion as in risk-neutral ergodic MDPs (see (Sutton and Barto, 2018), Section 9.2), can be calculated by solving the following system of linear equations,

| (13) |

where is the probability distribution of the starting state. Therefore, we can write (9) as

| (14) |

As is positive for all , we can define as the subjective limiting (steady-state) distribution of the CPT risk-sensitive MDP, and therefore, we have

| (15) |

It is interesting to compare (15) with the similar expression in risk-neutral policy gradient theorem, . Due to the non-linear CPT operator (compared to the linear expectation operator), the policy is entangled with the transition probabilities inside the gradient of the cumulative weighting function, and therefore, in the risk-sensitive case, it is not possible to define a stand-alone Q-function as a function of state and action to measure the quality of an action in a given state. As noted by Lin (Lin, 2013), this complication has the consequence that the optimal risk-sensitive policy even in the single-agent setting can be stochastic. To further expand the above expression, we can use the chain rule of calculus and write,

| (16) |

This is the general case of PG in CPT risk-sensitive MARL. Given the aggregative term in NAMGs, we can rewrite this equation as (7).

∎

We now provide an algorithm to estimate the above gradient using samples from a simulator of the environment or a large enough experience dictionary. This approximation scheme which is later used to also estimate the value function is Algorithm 1 is proposed by Jie et al. (Jie et al., 2018) to estimate the CPT value of an r.v., , using samples from its distribution. The following Assumption (A2 in (Jie et al., 2018)) is needed to guarantee the asymptotic consistency of this estimation algorithm.

Assumption 2.

The utility functions and are continuous and non-decreasing on their support and , respectively.

The above assumption also holds for conventional forms of weighting and utility functions in Figures 1 and 2 (Jie et al., 2018). Given Assumptions 1 and 2, Proposition 4 in (Jie et al., 2018) is verified and for a given r.v. , Algorithm 1 is guaranteed to have asymptotic consistency, i.e., it converges to asymptotically as the number of samples, , approaches infinity.

Gradient estimation.

To have a estimate of the gradient in (7), we need estimates of CPT values corresponding to

and (which we denote by ). Note that Assumption 1 states that are Lipschitz and therefore, they can be used as independent CPT weighting functions with corresponding cumulative weighting functions . Given the transition probabilities and repeated distributed sampling of rewards and transitions by agents from the environment or the experience dictionaries, the term in brackets corresponding to each state can be estimated using Algorithm (1). Furthermore, using these samples and solving a linear system of equations resulting from (13), the subjective steady-state distribution can be found. We note that this estimation algorithm is model-based and requires transition probabilities, however, it does not assume any knowledge of the reward function or the policies of other agents, and is therefore privacy-preserving. Having a policy gradient theorem and a corresponding gradient approximation scheme, we can now develop our distributed actor-critic algorithm.

5. Distributed Nested CPT Actor-Critic

Algorithm (2) lays out the pseudocode for Distributed Nested CPT Actor-Critic. As can be seen, the critic’s value function is estimated using the sampling strategy in Algorithm 1, and we use the samples from the simulator for bootstrapping (by adding them to the experience dictionary for later use). Although sampling from the simulator for gradient and value function approximation can be computationally intensive, it can become less so as we build the experience dictionary and do away with the simulator. We now prove the asymptotic convergence of the proposed algorithm.

5.1. Convergence of the Critic

In order to calculate the state value function corresponding to the current policy, we define the following CPT operator (note that the agent’s superscript has been dropped),

| (17) |

The following assumption is needed to ensure that the operator in (17) is a sup-norm contraction.

Assumption 3.

The utility functions and are invertible (denoted by and ) and differentiable (denoted by and ), and we have . Further, there exists such that holds for any and any non-negative real-valued r.v. , where is the discount factor of the MDP.

Similar to Assumptions 1 and 2, the above assumption can also be verified to hold for typical analytical forms of and in Figures 2 and 1 as shown by Lin et al. (Lin et al., 2018). Under this assumption, based on Theorem 6 in (Lin et al., 2018), the operator (17) is a sup-norm contraction on a Banach space defined over the MDP’s state space that includes all possible state value functions . Therefore, for every , there exists such that

| (18) |

Remark 3.

(Applicability of linear function approximation) The contraction of the operator (7) has only been validated for a tabular representation of the state-value function (Lin et al., 2018). We also assessed the possibility of approximating the state value function using linear functions for scaling up the proposed actor-critic algorithm to large or continuous state spaces. The traditional proof of convergence for a critic with linear function approximation requires the contraction of this operator with respect to the norm defined over the steady-state distribution of the MDP (Lemma in Tsitsiklis and Van Roy (Tsitsiklis and Van Roy, 1997)). However, via counterexample, it can be seen that this property does not necessarily hold for the operator (7).

Remark 4.

The previous remark and the fact that we were required to limit ourselves to tabular representations implies that mathematical properties of CPT-sensitive MDPs do not allow them to belong to the family of robust MDPs (Osogami, 2012) and enjoy properties such as linear approximation for the state value function and a convenient gradient estimation scheme as with coherent risk measures (Tamar et al., 2015). It would be interesting to study and look at this limitation from a cognitive perspective and to see whether dealing with dynamic CPT risk-sensitive continuous control is cognitively cumbersome for humans in behavioral experiments.

5.2. Convergence of the Actor

For notational simplicity, we denote by . We prove the convergence of our AC algorithm to a subjective MPNE of the game if the following assumptions are satisfied.

Assumption 4.

For each agent , is convex with respect to . Also, the gradient is uniformly bounded, i.e., for each agent there exists such that,

| (19) |

Assumption 5.

The pseudo-gradient mapping value function, , is strongly monotone with respect to , i.e., for every , there exists such that

Furthermore, this mapping is Lipschitz continuous, i.e.,

Theorem 1.

(Convergence of the actor) Given Assumptions 4 and 5 and a critic and an actor with learning steps such that,

| (20) |

algorithm (2) converges to the unique subjective Markov perfect Nash equilibrium of the NAMG, asymptotically.

Proof.

We prove that the actor update will converge to the unique Nash policy of the Markov game, which exists if Assumptions 4 and 5 are satisfied, starting from any initial condition. We rewrite the actor update for agent below,

Under Assumptions 4 and 5, based on Theorem 2 in Rosen (Rosen, 1965), there exists a unique MPNE for the NAMG. Note that this CPT-sensitive (subjective) MPNE can be different from the MPNE of the game when the agents are risk-neutral. Consider the parameter vector as the vector that constructs this unique Nash policy, for which we have for all . Per Assumption 4 and by defining , we have

| (21) | ||||

By summing the above equation over different and defining , we have

| (22) |

where . We also know that . Therefore, according to assumption 5,

| (23) | ||||

Finally, with telescopic summation,

| (24) | ||||

Since , . Therefore, as is bounded, is bounded as well. Consequently, as , converges to as and as a result converges to . ∎

Given the asymptotic proof of convergence for the actor and the critic and considering the conditions of the learning step sequences in Theorem 1, we can apply Theorem 1.1 of Borkar (Borkar, 1997), which shows the asymptotic convergence of the AC algorithm to the unique MPNE of the NAMG. Note that if Assumptions 4 and 5 do not hold, given the actor’s gradient expression, we can only ensure the convergence of the AC algorithm to a locally optimal policy parameter for each agent.

6. Numerical Experiment

To examine the empirical convergence of Distributed Nested CPT AC, we constructed a risk-sensitive NAMG with an interpretable design for measuring the effect of loss aversion in risk-sensitive agents on the converged policies. Note that due to the CPT operator, Assumptions 4 and 5 are hard to verify in any experimental setup and we did not expect the algorithm to converge to the subjective MPNE (which may not be unique if the aforementioned assumptions are not satisfied). In the constructed NAMG, there are four agents, five states, and three possible actions , and the communication graph is fully-connected. The reward function is defined as

| (25) |

where the first term is the reward solely affected by the agent’s action, and the second term is the reward that is affected by the actions of the neighboring of the agent. The aggregative term is

| (26) |

which indicates a communication graph with equal weights among the neighbors. The reward coefficient for agent is randomly generated from

| (27) |

Also, the reward coefficients is randomly generated form

| (28) |

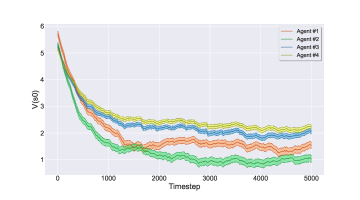

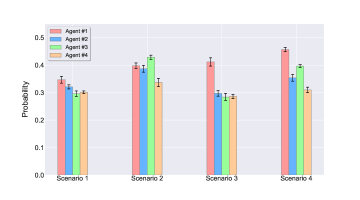

The above setup implies a high risk for the agent if it decides to take an action greater than and become involved with its neighboring community, e.g., take a financial risk in an interactive market. Thus, it can be said that each agent in this non-cooperative environment chooses by its action how much risk it wants to take and to what degree it wants to interact with the community (other agents who could, for instance, be economic, political, or social competitors), and ties its received reward to their actions. If the agent chooses the action , it will settle for a low, but risk-free profit. However, when choosing another action, depending on the actions of the other agents, it can make a significant profit or loss that is also affected by stochasticity of the environment. Our objective is to study the agents’ risk-aversion levels based on the parameter in the cumulative perspective theory utility function (Figure 2). The higher the value of this parameter, the more loss-averse the agent is. We expect that in the designed non-cooperative environment, a more loss-averse agent will choose the action with a higher probability and have a tendency to become socially isolated or conservative. To evaluate this hypothesis, we run the proposed algorithm for this risk-sensitive NAMG and for four different loss-aversion scenarios. In the first scenario, all agents are risk-neutral (corresponding to a vanilla AC algorithm with linear function approximation). In the second scenario, all agents have the same level of loss aversion (). In the third scenario, only Agent 1 is risk-sensitive (), and other agents are risk-neutral. Finally, in the last scenario, all agents are risk-sensitive, but Agent one has a higher loss aversion coefficient (), while others have . Figure 4 shows the convergence of the value functions corresponding to one of the states in the second scenario. Figure 5 shows the probability of choosing action (a quantitative indicator of social conservatism) in the converged policies of agents in each scenario. As observed, the level of social isolation and the probability of choosing the conservative action is proportional to the risk-aversion level of the agents in the community.

7. Conclusion and Future Works

In this work, we proposed a distributed risk-sensitive MARL algorithm in NAMGs with theoretical convergence guarantees based on cumulative prospect theory, a cognitive risk measure that broadens the scope of the traditionally adopted coherent risk measure. We empirically showed the positive correlation between loss aversion and social isolation of agents. We observed that scaling the proposed algorithm to larger environments and continuous control is not compatible with theoretical convergence gurantees. However, a plausible direction of future work is the appropriate use of function approximation and deep RL methods to tackle the curse of dimensionality for large state and action spaces in CPT-sensitive RL, and in general risk-averse RL (Urpí et al., 2021), in an empirical framework, albeit without theoretical convergence gurantees.

References

- (1)

- Acerbi (2002) Carlo Acerbi. 2002. Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking & Finance 26, 7 (2002), 1505–1518.

- Alacaoglu et al. (2022) Ahmet Alacaoglu, Luca Viano, Niao He, and Volkan Cevher. 2022. A natural actor-critic framework for zero-sum Markov games. In International Conference on Machine Learning. PMLR, 307–366.

- Artzner et al. (1999) Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. 1999. Coherent measures of risk. Mathematical finance 9, 3 (1999), 203–228.

- Başar (2021) Tamer Başar. 2021. Robust designs through risk sensitivity: An overview. Journal of Systems Science and Complexity 34 (2021), 1634–1665.

- Borkar (1997) Vivek S Borkar. 1997. Stochastic approximation with two time scales. Systems & Control Letters 29, 5 (1997), 291–294.

- Borkar (2001) Vivek S Borkar. 2001. A sensitivity formula for risk-sensitive cost and the actor–critic algorithm. Systems & Control Letters 44, 5 (2001), 339–346.

- Cavus and Ruszczynski (2014) Ozlem Cavus and Andrzej Ruszczynski. 2014. Risk-averse control of undiscounted transient Markov models. SIAM Journal on Control and Optimization 52, 6 (2014), 3935–3966.

- Cenedese et al. (2020) Carlo Cenedese, Giuseppe Belgioioso, Sergio Grammatico, and Ming Cao. 2020. Time-varying constrained proximal type dynamics in multi-agent network games. In 2020 European Control Conference (ECC). IEEE, 148–153.

- Chow and Ghavamzadeh (2014) Yinlam Chow and Mohammad Ghavamzadeh. 2014. Algorithms for CVaR optimization in MDPs. Advances in neural information processing systems 27 (2014).

- Chow et al. (2017) Yinlam Chow, Mohammad Ghavamzadeh, Lucas Janson, and Marco Pavone. 2017. Risk-constrained reinforcement learning with percentile risk criteria. The Journal of Machine Learning Research 18, 1 (2017), 6070–6120.

- Delbaen (2002) Freddy Delbaen. 2002. Coherent risk measures on general probability spaces. Advances in finance and stochastics: essays in honour of Dieter Sondermann (2002), 1–37.

- Deng (2019) Zhenhua Deng. 2019. Distributed algorithm design for resource allocation problems of second-order multiagent systems over weight-balanced digraphs. IEEE Transactions on Systems, Man, and Cybernetics: Systems 51, 6 (2019), 3512–3521.

- Deng (2021) Zhenhua Deng. 2021. Distributed algorithm design for aggregative games of Euler–Lagrange systems and its application to smart grids. IEEE Transactions on Cybernetics 52, 8 (2021), 8315–8325.

- Ding et al. (2022) Dongsheng Ding, Chen-Yu Wei, Kaiqing Zhang, and Mihailo Jovanovic. 2022. Independent policy gradient for large-scale markov potential games: Sharper rates, function approximation, and game-agnostic convergence. In International Conference on Machine Learning. PMLR, 5166–5220.

- Fei et al. (2021) Yingjie Fei, Zhuoran Yang, Yudong Chen, and Zhaoran Wang. 2021. Exponential bellman equation and improved regret bounds for risk-sensitive reinforcement learning. Advances in Neural Information Processing Systems 34 (2021), 20436–20446.

- Fox et al. (2022) Roy Fox, Stephen M Mcaleer, Will Overman, and Ioannis Panageas. 2022. Independent natural policy gradient always converges in Markov potential games. In International Conference on Artificial Intelligence and Statistics. PMLR, 4414–4425.

- Ghosh et al. (2022) Mrinal K Ghosh, Subrata Golui, Chandan Pal, and Somnath Pradhan. 2022. Nonzero-sum risk-sensitive continuous-time stochastic games with ergodic costs. Applied Mathematics & Optimization 86, 1 (2022), 6.

- Ghosh et al. (2023) Mrinal K Ghosh, Subrata Golui, Chandan Pal, and Somnath Pradhan. 2023. Discrete-time zero-sum games for Markov chains with risk-sensitive average cost criterion. Stochastic Processes and their Applications 158 (2023), 40–74.

- Jie et al. (2018) Cheng Jie, LA Prashanth, Michael Fu, Steve Marcus, and Csaba Szepesvári. 2018. Stochastic optimization in a cumulative prospect theory framework. IEEE Trans. Automat. Control 63, 9 (2018), 2867–2882.

- Kahneman and Tversky (1979) DANIEL Kahneman and Amos Tversky. 1979. Prospect theory: An analysis of decision under risk. Econometrica 47, 2 (1979), 363–391.

- La and Ghavamzadeh (2013) Prashanth La and Mohammad Ghavamzadeh. 2013. Actor-critic algorithms for risk-sensitive MDPs. Advances in neural information processing systems 26 (2013).

- Leonardos et al. (2021) Stefanos Leonardos, Will Overman, Ioannis Panageas, and Georgios Piliouras. 2021. Global convergence of multi-agent policy gradient in markov potential games. arXiv preprint arXiv:2106.01969 (2021).

- Lin (2013) Kun Lin. 2013. Stochastic systems with cumulative prospect theory. Ph.D. Dissertation. University of Maryland, College Park.

- Lin et al. (2018) Kun Lin, Cheng Jie, and Steven I Marcus. 2018. Probabilistically distorted risk-sensitive infinite-horizon dynamic programming. Automatica 97 (2018), 1–6.

- Lin and Marcus (2013) Kun Lin and Steven I Marcus. 2013. Dynamic programming with non-convex risk-sensitive measures. In 2013 American Control Conference. IEEE, 6778–6783.

- Littman (1994) Michael L Littman. 1994. Markov games as a framework for multi-agent reinforcement learning. In Machine learning proceedings 1994. Elsevier, 157–163.

- Maheshwari et al. (2022) Chinmay Maheshwari, Manxi Wu, Druv Pai, and Shankar Sastry. 2022. Independent and decentralized learning in markov potential games. arXiv preprint arXiv:2205.14590 (2022).

- Markowitz et al. (2021) Jared Markowitz, Marie Chau, and I-Jeng Wang. 2021. Deep CPT-RL: Imparting Human-Like Risk Sensitivity to Artificial Agents.. In SafeAI@ AAAI.

- Mguni et al. (2021) David H Mguni, Yutong Wu, Yali Du, Yaodong Yang, Ziyi Wang, Minne Li, Ying Wen, Joel Jennings, and Jun Wang. 2021. Learning in nonzero-sum stochastic games with potentials. In International Conference on Machine Learning. PMLR, 7688–7699.

- Moharrami et al. (2022) Mehrdad Moharrami, Yashaswini Murthy, Arghyadip Roy, and Rayadurgam Srikant. 2022. A Policy Gradient Algorithm for the Risk-Sensitive Exponential Cost MDP. arXiv preprint arXiv:2202.04157 (2022).

- Munir et al. (2021) Md Shirajum Munir, Sarder Fakhrul Abedin, Nguyen H Tran, Zhu Han, Eui-Nam Huh, and Choong Seon Hong. 2021. Risk-aware energy scheduling for edge computing with microgrid: A multi-agent deep reinforcement learning approach. IEEE Transactions on Network and Service Management 18, 3 (2021), 3476–3497.

- Noorani and Baras (2022) Erfaun Noorani and John S Baras. 2022. Risk-attitudes, Trust, and Emergence of Coordination in Multi-agent Reinforcement Learning Systems: A Study of Independent Risk-sensitive REINFORCE. In 2022 European Control Conference (ECC). IEEE, 2266–2271.

- Osogami (2012) Takayuki Osogami. 2012. Robustness and risk-sensitivity in Markov decision processes. Advances in neural information processing systems 25 (2012).

- Pal and Pradhan (2021) Chandan Pal and Somnath Pradhan. 2021. Zero-sum games for pure jump processes with risk-sensitive discounted cost criteria. Journal of Dynamics and Games 9, 1 (2021), 13–25.

- Parise et al. (2020) Francesca Parise, Sergio Grammatico, Basilio Gentile, and John Lygeros. 2020. Distributed convergence to Nash equilibria in network and average aggregative games. Automatica 117 (2020), 108959.

- Perolat et al. (2015) Julien Perolat, Bruno Scherrer, Bilal Piot, and Olivier Pietquin. 2015. Approximate dynamic programming for two-player zero-sum Markov games. In International Conference on Machine Learning. PMLR, 1321–1329.

- Prashanth et al. (2022) LA Prashanth, Michael C Fu, et al. 2022. Risk-Sensitive Reinforcement Learning via Policy Gradient Search. Foundations and Trends® in Machine Learning 15, 5 (2022), 537–693.

- Prashanth and Ghavamzadeh (2016) LA Prashanth and Mohammad Ghavamzadeh. 2016. Variance-constrained actor-critic algorithms for discounted and average reward MDPs. Machine Learning 105 (2016), 367–417.

- Prashanth et al. (2016) LA Prashanth, Cheng Jie, Michael Fu, Steve Marcus, and Csaba Szepesvári. 2016. Cumulative prospect theory meets reinforcement learning: Prediction and control. In International Conference on Machine Learning. PMLR, 1406–1415.

- Prelec (1998) Drazen Prelec. 1998. The probability weighting function. Econometrica (1998), 497–527.

- Qiu et al. (2021b) Shuang Qiu, Xiaohan Wei, Jieping Ye, Zhaoran Wang, and Zhuoran Yang. 2021b. Provably efficient fictitious play policy optimization for zero-sum Markov games with structured transitions. In International Conference on Machine Learning. PMLR, 8715–8725.

- Qiu et al. (2021a) Wei Qiu, Xinrun Wang, Runsheng Yu, Rundong Wang, Xu He, Bo An, Svetlana Obraztsova, and Zinovi Rabinovich. 2021a. RMIX: Learning risk-sensitive policies for cooperative reinforcement learning agents. Advances in Neural Information Processing Systems 34 (2021), 23049–23062.

- Reddy et al. (2019) D Sai Koti Reddy, Amrita Saha, Srikanth G Tamilselvam, Priyanka Agrawal, and Pankaj Dayama. 2019. Risk averse reinforcement learning for mixed multi-agent environments. In Proceedings of the 18th international conference on autonomous agents and multiagent systems. 2171–2173.

- Rosen (1965) J Ben Rosen. 1965. Existence and uniqueness of equilibrium points for concave n-person games. Econometrica: Journal of the Econometric Society (1965), 520–534.

- Ruszczyński (2010) Andrzej Ruszczyński. 2010. Risk-averse dynamic programming for Markov decision processes. Mathematical programming 125 (2010), 235–261.

- Saffar et al. (2017) Mohsen Saffar, Hamed Kebriaei, and Dusit Niyato. 2017. Pricing and rate optimization of cloud radio access network using robust hierarchical dynamic game. IEEE Transactions on Wireless Communications 16, 11 (2017), 7404–7418.

- Sayin et al. (2021) Muhammed Sayin, Kaiqing Zhang, David Leslie, Tamer Basar, and Asuman Ozdaglar. 2021. Decentralized Q-learning in zero-sum Markov games. Advances in Neural Information Processing Systems 34 (2021), 18320–18334.

- Shapiro et al. (2021) Alexander Shapiro, Darinka Dentcheva, and Andrzej Ruszczynski. 2021. Lectures on stochastic programming: modeling and theory. SIAM.

- Shapley (1953) Lloyd S Shapley. 1953. Stochastic games. Proceedings of the national academy of sciences 39, 10 (1953), 1095–1100.

- Shokri and Kebriaei (2020) Mohammad Shokri and Hamed Kebriaei. 2020. Leader–follower network aggregative game with stochastic agents’ communication and activeness. IEEE Trans. Automat. Control 65, 12 (2020), 5496–5502.

- Soorki et al. (2021) Mehdi Naderi Soorki, Walid Saad, Mehdi Bennis, and Choong Seon Hong. 2021. Ultra-reliable indoor millimeter wave communications using multiple artificial intelligence-powered intelligent surfaces. IEEE Transactions on Communications 69, 11 (2021), 7444–7457.

- Sutton and Barto (2018) Richard S Sutton and Andrew G Barto. 2018. Reinforcement learning: An introduction. MIT press.

- Tamar et al. (2015) Aviv Tamar, Yinlam Chow, Mohammad Ghavamzadeh, and Shie Mannor. 2015. Policy gradient for coherent risk measures. Advances in neural information processing systems 28 (2015).

- Tamar et al. (2012) Aviv Tamar, Dotan Di Castro, and Shie Mannor. 2012. Policy gradients with variance related risk criteria. In Proceedings of the twenty-ninth international conference on machine learning. 387–396.

- Tamar et al. (2013) Aviv Tamar, Dotan Di Castro, and Shie Mannor. 2013. Temporal difference methods for the variance of the reward to go. In International Conference on Machine Learning. PMLR, 495–503.

- Tamar et al. (2014) Aviv Tamar, Shie Mannor, and Huan Xu. 2014. Scaling up robust MDPs using function approximation. In International conference on machine learning. PMLR, 181–189.

- Tan et al. (2021) Shaolin Tan, Yaonan Wang, and Athanasios V Vasilakos. 2021. Distributed population dynamics for searching generalized nash equilibria of population games with graphical strategy interactions. IEEE Transactions on Systems, Man, and Cybernetics: Systems 52, 5 (2021), 3263–3272.

- Tian et al. (2021) Ran Tian, Liting Sun, and Masayoshi Tomizuka. 2021. Bounded risk-sensitive markov games: Forward policy design and inverse reward learning with iterative reasoning and cumulative prospect theory. In Proceedings of the AAAI Conference on Artificial Intelligence, Vol. 35. 6011–6020.

- Tsitsiklis and Van Roy (1997) John Tsitsiklis and Benjamin Van Roy. 1997. An analysis of temporal-difference learning with function approximation. IEEE Trans. Automat. Control 42, 5 (1997), 674–690.

- Tversky and Kahneman (1992) Amos Tversky and Daniel Kahneman. 1992. Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and uncertainty 5 (1992), 297–323.

- Urpí et al. (2021) Núria Armengol Urpí, Sebastian Curi, and Andreas Krause. 2021. Risk-averse offline reinforcement learning. arXiv preprint arXiv:2102.05371 (2021).

- Wright and Leyton-Brown (2017) James R Wright and Kevin Leyton-Brown. 2017. Predicting human behavior in unrepeated, simultaneous-move games. Games and Economic Behavior 106 (2017), 16–37.

- Zhang et al. (2020) Kaiqing Zhang, Sham Kakade, Tamer Basar, and Lin Yang. 2020. Model-based multi-agent rl in zero-sum markov games with near-optimal sample complexity. Advances in Neural Information Processing Systems 33 (2020), 1166–1178.

- Zhang et al. (2021) Kaiqing Zhang, Xiangyuan Zhang, Bin Hu, and Tamer Basar. 2021. Derivative-free policy optimization for linear risk-sensitive and robust control design: Implicit regularization and sample complexity. Advances in Neural Information Processing Systems 34 (2021), 2949–2964.

- Zhong et al. (2022) Hai Zhong, Yutaka Shimizu, and Jianyu Chen. 2022. Chance-Constrained Iterative Linear-Quadratic Stochastic Games. IEEE Robotics and Automation Letters 8, 1 (2022), 440–447.

- Zhu et al. (2013) Kun Zhu, Ekram Hossain, and Dusit Niyato. 2013. Pricing, spectrum sharing, and service selection in two-tier small cell networks: A hierarchical dynamic game approach. IEEE Transactions on Mobile Computing 13, 8 (2013), 1843–1856.

- Zhu et al. (2022) Ziqing Zhu, Ka Wing Chan, Siqi Bu, Bin Zhou, and Shiwei Xia. 2022. Nash Equilibrium Estimation and Analysis in Joint Peer-to-Peer Electricity and Carbon Emission Auction Market With Microgrid Prosumers. IEEE Transactions on Power Systems (2022).