Dynamic Coalition Portfolio Selection with Recursive Utility

Abstract. In this paper, we consider a dynamic coalition portfolio selection problem, with each agent’s objective given by an Epstein–Zin recursive utility. To find a Pareto optimum, the coalition’s problem is formulated as an optimization problem evolved by a multi-dimensional forward-backward SDE. Since the evolution system has a forward-backward structure, the problem is intrinsically time-inconsistent. With the dynamic-game point of view, we rigorously develop an approach to finding the equilibrium Pareto investment-consumption strategy. We find that the relationship between risk aversion and EIS has more influence on the coalition’s problem than that on the one-agent problem. More interestingly, we show that the equilibrium Pareto consumption strategy associated with the recursive utility is much more effective than that associated with the CRRA expected utility, which highlights the feature of recursive utility that the marginal benefit of consumption can depend on the future consumption.

Keywords. Portfolio selection, recursive utility, coalition optimization, cooperation game, time-inconsistency, forward-backward SDE, equilibrium Pareto strategy.

AMS subject classifications. 91B10, 91B51, 91B70, 93E20, 49L12.

1 Introduction

Since the pioneering work by von Neumann and Morgenstern [41], coalitions have occupied the center stage for research within game theory. In the social sciences, a minimal requirement on allocative efficiency is the so-called Pareto optimality (see Aziz, Brandt, and Harrenstein [2], for example). A well-known approach of finding Pareto optima is to solve a new optimization problem with the subjective given by some convex combination of each agent’s subjective. Then the optimum (if it exists) of the new problem is exactly a Pareto optimum of the coalition.

On the other hand, it is well recognized that the recursive utility developed by Epstein and Zin [21] and Duffie and Epstein [12] is a milestone in macroeconomics and quantitative finance, because it provides a simple but very useful tool to separate investor’s risk aversion and elasticity of intertemporal substitution (EIS, for short). From an economic theory view of point, this is much more reasonable than the standard constant relative risk aversion (CRRA, for short) expected utility. Since then, the recursive utility has been widely applied on the study of asset pricing and portfolio selection problems. Another important feature of recursive utility is that the marginal benefit of consumption depends not only on current consumption but also (through the value function) on the trajectory of future consumption. Such a property is playing a crucial role in the fast-growing green portfolios, because one has to consider some sustainable development issues when modeling the performances of environmental, social, and governance (ESG) investing; see Pindyck and Wang [38] and Hong, Wang, and Yang [25], for example.

Motivated by the above, we study a coalition portfolio selection problem, with each agent’s performance described by an Epstein–Zin recursive utility . We use , , and to describe each agent’s risk aversion, EIS, and discount factor, respectively. The main feature of our model is that the discount factor of each agent is allowed to be different from each each. Indeed, since the discount rate is not only due to the interest rate, it is more like a subjective preference for the time cost, and then each agent should have an individual discount rate (see Dumas, Uppal, and Wang [16] and Borovička [6]). For example (see Gârleanu and Panageas [23]), the old and the young in a family usually have different preferences for the time risk (or the time cost), due to which forcing them to use the same discount rate is really unreasonable.

The purpose of this paper is to study the coalition’s investment-consumption performance when the model involves heterogeneous discount rates. Some interesting phenomenons produced by the heterogeneous discount rates and the recursive utility are revealed.

The main contribution of this paper can be briefly summarized as follows.

(i) It is well-known (see EI Karoui, Peng, and Quenez [20]) by now that the recursive utility is exactly the solution of some (nonlinear) backward stochastic differential equation (BSDE, for short). Combining this with the wealth equation, the coalition’s problem (denoted by Problem (C)) is reformulated as a maximizing problem with the controlled dynamics described by a system of a forward SDE and a multi-dimensional BSDE. We find that Problem (C) is intrinsically time-inconsistent, due to the appearance of backward state equations. With the dynamic-game point of view introduced by Strotz [40], we rigorously develop an approach to constructing the equilibrium Pareto investment-consumption strategy.

(ii) We show that by applying the recursive utility, the effectiveness of equilibrium Pareto consumption strategy (EPCS, for short) associated with CRRA utility can be significantly improved in the following sense:

| Consumption strategy | Time-consistency | Heterogeneity |

|---|---|---|

| Pre-committed, CRRA utility | No | Yes |

| Equilibrium, CRRA utility | Yes | No |

| Equilibrium, recursive utility | Yes | Yes |

Table 1: Comparison between recursive utility and CRRA utility

In the CRRA utility case, the EPCS of agent takes the following form:

where can be uniquely determined by solving some ordinary differential equations (ODEs, for short). Note that the above EPCS does not depend on the parameter . Since the agents’ discount rates are heterogeneous, such a consumption strategy is unrealistic from an economic point of view. Thus, it is not very effective to use the CRRA utility to model a dynamic coalition portfolio selection problem. However, this inadequacy can be improved by replacing the CRRA utility by a recursive one. Indeed, in the recursive case, the EPCS reads:

It is noteworthy to point out that this phenomenon is similar to the equilibrium investment performance in dynamic mean-variance portfolio choices, in which the equilibrium investment strategy is independent of current wealth for the standard criterion (see Basak and Chabakauri [3]), but is proportional to current wealth for the log return (see Dai, Jin, Kou, and Xu [10]).

(iii) We find that the relationship between risk aversion and EIS has more influence on the coalition’s problem than that on the one-agent problem.

Let be the optimal consumption strategy associated with the discount rate in the one-agent problem, and be the equilibrium consumption strategy associated with the discount rate in the coalition’s problem. Let , then we have

| Consumption strategy with | Relationship between and |

|---|---|

| One-agent problem | |

| Coalition’s problem |

Table 2: Comparison between one-agent and coalition’s problems with

| Consumption strategy with | Relationship between and |

|---|---|

| One-agent problem | |

| Coalition’s problem |

Table 3: Comparison between one-agent and coalition’s problems with

This shows that the coalition’s problem is more sensitive with the relationship between risk aversion and EIS than the one-agent problem.

(iv) We show that the coalition manager only needs to decide the whole coalition’s investment strategy, but has to make a decision for each agent’s consumption strategy. This predicts that distributing the wealth in a coalition is much more complicated than making money, because it is the common aim of each agent to make as much money as possible, but how to spend money is nobody else’s business but one’s own.

1.1 Literature review on recursive coalition problem

The coalition problem (also called a corporation game, a social planner problem, a group decision maker problem, or a multi-agent problem) has been studied for a long history in economics and social sciences. Some newest results can be found in Morellec and Schsrhoff [34], Aziz, Brandt, and Harrenstein [2], Jackson and Yariv [28], Garlappi, Giammarino, and Lazrak [22], and the references cited therein. After the pioneering works [12, 13], the coalition problem with recursive utility has been studied by Dana and LeVan [9], Ma [33], Duffie, Geoffard, and Skiadas [14], Kan [29], Dumas, Uppal, and Wang [16], Anderson [1], Gârleanu and Panageas [23], and Borovička [6], to mention a few. However, the solutions obtained in these works are pre-committed, and we are going to find a sophisticated solution in the paper, since the coalition’s problem is intrinsically time-inconsistent (see Jackson and Yariv [28]).

More importantly, most of the above works focus on generalizing the CRRA model to the recursive case, but the consequence of the separation advantage between risk aversion and EIS in recursive utility is not very clear. We will clarify this crucial issue and provides a strong evidence to support the effectiveness of introducing recursive utility in the paper.

1.2 Literature review on optimal control theory for FBSDEs

In the control theory, the optimal control problem for foward-backward SDEs (FBSDEs, for short) was initially studied by Peng [35], and has been developed by Dokuchaev and Zhou [11], Lim and Zhou [32], Yong [44], Cvitanić and Zhang [8], Wang, Wu, and Xiong [42], Hu, Ji, and Xue [26], and Sun, Wang, and Wen [39], etc. All these results are essentially concerned with the Pontryagin’s maximum principle, using a variation method. In the paper, we focus on the time-consistency, which corresponds to Bellman’s dynamical programming principle approach.

1.3 Literature review on time-inconsistent control theory

The seminal paper [40] by Strotz was the first to formalize the consistent planning problem with a dynamic-game point of view. Since then, the equilibrium approach by sophisticated agents has received very strong attention; see, for example, Pollak [37], Laibson [31], Harris and Laibson [24], Basak and Chabakauri [3], Cao and Werning [7], and Dai, Jin, Kou, and Xu [10] on the economic side, and Ekeland and Pirvu [19], Ekeland and Lazrak [17], Hu, Jin, and Zhou [27], Yong [45, 46], Björk, Murgoci, and Zhou [5], Björk, Khapko, and Murgoci [4] on the mathematical side. However, these existing approaches cannot be applied in our coalition model with recursive utility, because the coalition’s dynamic contains a multi-dimensional backward SDE (2.3). Roughly speaking, the time-inconsistency of our model is caused purely by the backward state, rather than by the non-exponential discount [40, 37, 19, 17, 45, 46] or by the conditional expectation operator [3, 27, 5, 4]. We will overcome this mathematical difficulty by modifying the approach developed in our recent work [43].

The rest of this paper is organized as follows. In Section 2, we formulate the problem. The time-inconsistency of the model is shown in Section 3. The main results are presented in Section 4. In Section 5, we provide some numerical results and make some comparisons. The proofs are collected in Section 6.

2 The model and problem formulation

Consider the following forward SDE for the coalition’s wealth process driven by a one-dimensional Brownian motion :

| (2.1) |

where is the riskless interest rate, is the appreciation rate of one stock, is the volatility, is agent ’s proportion of dollar amount invested in the stock, and is the consumption of agent . Here, the space is defined by

For simplicity, we use the following notations of the investment-consumption strategies from now on:

Naturally, agent wants to maximize his/her utility functional

| (2.2) |

where , called an Epstein–Zin recursive utility (see [12, 13, 15, 20], for example), is determined by

| (2.3) |

with

and

The parameter controls the risk aversion of the agents, with gives the agents’ EIS, and is the subjective discount factor of agent (which can be different for the different ). If , we have the additively separable aggregator:

| (2.4) |

and then

| (2.5) |

which is exactly the standard CRRA expected utility. Unlike the CRRA utility (2.5), the recursive utility as defined by (2.3) disentangles risk aversion from the EIS.

Since our model is formulated in a Markovian framework, we only focus on the following Markovian solution to (2.3) for simplicity.

Proposition 2.1.

Under the assumptions presented above, the following ODE admits a unique positive solution:

| (2.6) |

Moreover,

| (2.7) |

is a solution to (2.3).

In our model, each agent concerns with not only his/her own consumption but also the coalition’s whole wealth . This is very natural in a coalition problem; for example, each family member usually hopes to maximize both his/her own consumption amount and the whole wealth possessed by the family.

The minimal requirement on allocative efficiency is the so-called Pareto optimality (see Aziz, Brandt, and Harrenstein [2]), which is defined as follows:

Definition 2.2.

A pair is called a Pareto optimal investment-consumption strategy if there exists no other pair such that

and at least one of the above inequalities is strict.

To find a Pareto optimal investment-consumption strategy, we introduce the following new problem: Maximize the following objective

| (2.8) |

By the standard results in game theory (see Yong [47, Proposition 3.2.1], for example), we know that the optimal investment-consumption strategy of the new problem is a Pareto optimum of the coalition. Since we focus on clarifying the performance of heterogeneous discount rates, we take for to reduce the additional heterogeneous terms. In economic languages, all the agents are treated by the coalition equally. Then the coalition problem’s objective (2.8) can be rewritten as follows:

| (2.9) |

3 Time-inconsistency of the model

In this section, we shall show that the Pareto optimum of the coalition is time-inconsistent in general.

For simplicity, we consider a special case of the model with , by which the recursive utility reduces to a CRRA one. It follows that

| (3.1) |

For any fixed initial time , we introduce the following dynamic problem over : For any given , maximize

subject to

Note that the above is a standard optimal control problem, because is fixed in (3.1) and only plays a role as a parameter. In the literature, such type of problems is usually called an auxiliary problem of the original problem. By the standard DPP approach, the optimal investment-consumption strategy with initial time can be explicitly obtained:

| (3.2) | |||

| (3.3) |

in which is the unique positive solution to the following ODE:

Since the relationship does not hold in general, it is easily shown that there exists at least an such that depends on . Indeed, without loss of generality, we can suppose that there exist two indexes such that , and does not depend on . Then

Note that does not depend on and contains a parameter , so the product must depend on . Thus, the problem is time-inconsistent and the strategy given by (3.2) is a pre-committed optimum.

We remark that since in general, we cannot simplify the above problem as a one-agent investment-consumption problem with a CRRA utility and a quasi-exponential discount, as studied by Ekeland, Mbodji, and Pirvu [18]. By the equilibrium HJB equation approach (see Yong [45, 46], for example) or the extended HJB equation approach (see Björk, Khapko, and Murgoci [4], for example), the time-consistent equilibrium investment-consumption strategy (which is also called a sophisticated solution) associated with (2.1) and (3.1) can be obtained. However, for the general case with , the situation of controlled backward state equation is not avoidable, and then the approach developed in [45, 46, 4] cannot be applied.

4 The main result

In finance, time-consistency is an essential requirement of the practicable strategies. When the problem is time-inconsistent, it is no longer clear what we mean by the word “optimal”, because a strategy which is optimal for one choice of starting point in time will generically not be optimal at a later point in time (see Björk, Murgoci, and Zhou [5]). Thus, instead of finding a Pareto optimum, we are going to find an equilibrium Pareto strategy for the coalition, with the dynamic-game theoretic framework introduced by Strotz [40].

4.1 Equilibrium Pareto strategy

Inspired by [27, 45, 4], we introduce the following definition, which gives the Pareto optimality in a dynamic-game sense.

Definition 4.1.

We call an equilibrium Pareto investment-consumption strategy (EPICS, for short) of the coalition, if the following holds:

| (4.1) |

for any and , with

| (4.2) |

and

| (4.3) |

Remark 4.2.

We only consider the closed-loop strategy in the paper. The intuition behind 4.1 is similar to that in [27, 45, 4]. At any given time , the controller is playing a game with all his/her incarnations in the future by maximizing his/her utility functional on , and knowing that he/she will lose the control of the system beyond . This can be regarded a leader-follower game with infinitely many players.

Remark 4.3.

We remark that there are two games in our model. The agents not only play against their incarnations in the future, but also play a cooperation game with each other.

4.2 Equilibrium HJB equation: Verification theorem and well-posedness

From Section 3, we see that the pre-committed optimal strategy in the CRRA utility case can be obtained by introducing an auxiliary problem. However, extending this approach to the recursive utility case is challenge. In other words, it is not easy to find a pre-committed optimal strategy for the coalition in recursive utility case, due to the appearance of controlled multi-dimensional BSDEs. Thus, with the equilibrium strategy having been obtained on , the optimization problem on , which is the sophisticated problem of the original, still cannot be solved by the DPP approach. This brings some new difficulties to finding the equilibrium strategy (i.e., the sophisticated solution) in our model comparing with Yong [45, 46] and Björk, Khapko, and Murgoci [4].

Motivated by our recent work [43] with Yong, we introduce the following equilibrium HJB equation (or called an extended HJB equation):

in which the equilibrium investment-consumption strategy (if it exists) is determined by the following Hamiltonian:

| (4.4) |

with

| (4.5) |

Clearly, if the equilibrium strategy exists, then we have

| (4.6) |

and

| (4.7) |

Now we make the ansatz:

| (4.8) |

Then

The equilibrium investment strategy (4.6) and the equilibrium consumption strategy (4.7) become

| (4.9) |

and

| (4.10) |

respectively, with

| (4.11) |

We call (4.11) an equilibrium ODE.

Theorem 4.4.

To guarantee the well-posedness of (4.11), we introduce the following conditions.

(A1) The coefficients , , and satisfy

| (4.12) |

or

| (4.13) |

Theorem 4.5.

Let (A1) hold. Then the equilibrium ODE (4.11) admits a unique positive solution.

Combining Theorem 4.4 and Theorem 4.5 together, we have the following result immediately.

5 Interpretation and numerics

The equilibrium investment strategy is given by

It is independent of the discount rate , which coincides with the case of one-agent optimal investment-consumption problem. We remark that the coalition only needs to decide the sum of each agent’s investment strategy.

The equilibrium consumption strategy is given by

It shows that the coalition needs to choose an explicit consumption strategy for each agent. Thus, although the agents are playing a cooperation game, how to share the wealth is still much more troublesome than making money itself.

5.1 Monotonic property of equilibrium consumption strategy

Proposition 5.1.

Let (A1) hold. Then for any two given discount rates , the corresponding equilibrium consumption strategies and satisfy if , and if .

Proof.

Recall that the agents’ equilibrium consumption strategies are given by

From the proof of Theorem 4.5, we know that

If , we have , and then . Similarly, we have if . ∎

The parameter controls the risk aversion of the agents. If the risk aversion coefficient is smaller than the reciprocal of the EIS , the agent with a smaller discount factor will be distributed more rewards than the one with a bigger discount factor. However, when the risk aversion coefficient is bigger than the reciprocal of the EIS, the agent with a smaller discount factor will be distributed less rewards than the one with a bigger discount factor. Thus, the relation between the risk aversion and the EIS has an important influence on the coalition’s taste of the discount factors.

5.2 Comparison with one-agent model

In the one-agent model, the wealth equation and the objective are given by

and

respectively, with

and

By the recursive DPP established by Peng [36], the optimal investment-consumption strategy is given by

| (5.1) |

with being the unique positive solution of the following ODE:

| (5.2) |

We denote the optimal investment-consumption strategy associated with by . It is well-known that for the one-agent problem, we always have if . But for the multi-agent problem, if , we can have for . This is a new feature of our model.

5.3 Comparison with CRRA model

In this subsection, we shall compare the equilibrium strategy derived in our model with that derived in the CRRA utility case.

Pre-committed strategy with CRRA utility. When , the recursive utility reduces to a CRRA utility. Recall from (3.3) that at time , the pre-committed optimal consumption strategy of agent reads:

| (5.3) |

which depends on . Since this strategy is time-inconsistent, it is not flexible.

Equilibrium strategy with CRRA utility. Taking in (4.10), we see that the equilibrium consumption strategy of agent with CRRA utility is given by:

| (5.4) |

It is time-consistent, but it is surprising that does not depend on . In other words, the agents take the same consumption strategy as each other, which is unreasonable from a economic view of point.

Equilibrium strategy with recursive utility. The equilibrium consumption strategy of agent in our model is given by

| (5.5) |

which is time-consistent and also depends on . Thus, the equilibrium consumption strategy in our model appears more reasonable than that associated with the CRRA utility.

Analysis for the above phenomena

From (4.2) and (4.2), with the ansatz (4.8), we see that the equilibrium investment-consumption strategy is determined by maximizing the following Hamiltonian:

| (5.6) |

with

| (5.7) |

and

| (5.8) |

Note that in the recursive utility case, the marginal benefit of agent ’s consumption at time is given by

| (5.9) |

which depends not only on agent ’s current consumption but also (through the value function ) on the trajectory of coalition’s future consumptions . It leads to that , given by

| (5.10) |

depends on both coalition’s value function and agent ’s value function . Thus, the corresponding equilibrium consumption strategy of agent depends on the parameter .

In the CRRA utility case, the aggregator becomes an additively separable one:

| (5.11) |

and then the marginal benefit of agent ’s consumption at time reduces to

| (5.12) |

which only depends on agent ’s current consumption . Then,

| (5.13) |

Thus, in this case the equilibrium consumption strategy of agent is given by coalition’s value function , which is independent of the parameter .

The more essential reason is that the time-inconsistent problem is an optimization problem on the local time horizon . For the model with CRRA utility, the utility is affected by the discount factor only through the discounting function . When is small enough, over for each . Then the agents face almost the same problem as each other over . However, for the model with recursive utility, the discount factor affects the utility not only by the discounting function but also by the value function . Thus, the agents’ problems can be still different from each other, even if is very small.

5.4 Numerics

The setting

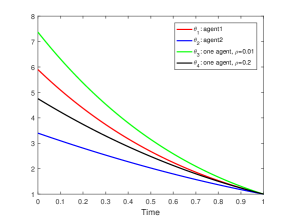

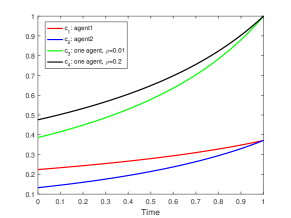

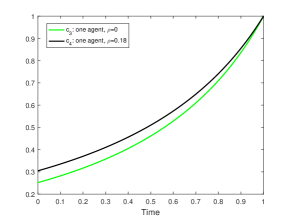

Figure 1: We set , , , , , , , , , and . Note that in this setting, the relation holds. In Figure 1 (a), is the solution of the equilibrium HJB equation (4.11); the functions and are the solutions of the HJB equation (5.2) in the one-agent model associated with and , respectively. In Figure 1 (b), are the equilibrium consumption strategies (4.10) of agent and agent in the two-agent model, respectively; the functions and are the optimal consumption strategies (5.1) in the one-agent model associated with and , respectively.

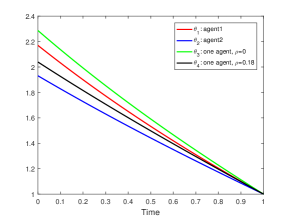

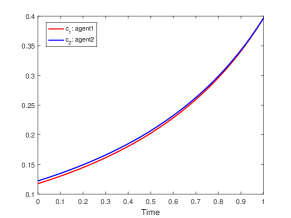

Figure 2: We set , , , , , , , , , and . In this setting, we have . The meaning of and is similar to that in Figure 1.

From Figure 1 (a) and Figure 2 (a), we see that and for both and . From Figure 1 (b) and Figure 2 (c), we see that holds for both and in the one-agent model. But in the multi-agent model, from Figure 2 (b) and Figure 2 (c) we see that for and for . Thus, the numerics coincides with our theoretical results.

6 Appendix: Proof of the main results

Appendix A: Proof of 2.1

If (2.6) admits a unique positive solution, then (2.7) can be obtained by applying the Itô formula directly. The uniqueness of positive solutions to (2.6) can be obtained by a standard method. Thus, we only need to prove that (2.6) really admits a positive solution. This suffices to show that if is a positive solution of (2.6) on , then

for some positive constants independent of . Let be the unique solution to the following linear ODE:

Clearly, . By the comparison theorem of ODEs, we have

| (6.1) |

Now we establish the upper bound estimate of . If , then

Let be the unique positive solution to the following linear ODE:

By the comparison theorem of ODEs again, we have

| (6.2) |

If , then

in which is given by (6.1). Let be the unique positive solution to the following linear ODE:

By the comparison theorem of ODEs again, we have

| (6.3) |

Combining (6.1), (6.2), and (6.3) together, we complete the proof.

Appendix B: Proof of Theorem 4.4

Let be defined as (4.2) and (4.3). Then the corresponding state and utility are given by

and

| (6.4) |

respectively. By applying the Itô formula to the mapping on , we get

where is the solution to (4.11). Substituting the above into (6.4) yields that

Next, by applying the Itô formula to the mapping on , we have

| (6.5) |

By 2.1, the following ODE admits a unique positive soluiton :

Then

which implies that

Substituting the above into (6.5) yields that

| (6.6) |

Then, by the standard estimates of SDEs, we have

Noting that and the derivatives and are bounded, we get

where is a constant which depends on the fixed and , but is independent of . Thus, we have

It follows that

where

Note that

and

Then it is easilly checked that (4.1) holds, which completes the proof.

Appendix C: Proof of Theorem 4.5

Similar to the proof of 2.1, it suffices to show that if is a postive solution of (4.11) on , then

for some positive constants independent of .

Step 1. Monotonicity of in . Without loss of generality, we let for . Denote . Then

Clearly, the above is a linear ODE with the unknown and the nonhomogeneous term . Using the fact

we have , which implies that

| (6.7) |

We first prove the result under the assumption (4.12). Denote

Note that

and

Then there exists an such that on . Let

| (6.8) |

If , then the desired result is proved with . Thus, we assume that . By the continuity of , we get . Note that

we have

Thus for some , we have

which contradicts (6.8). This completes the proof under the assumption (4.12).

We next prove the result under the assumption (4.13). Note that

Using the fact , we have

Under (4.13), we have . Then,

Thus,

which completes the proof under the assumption (4.13).

Acknowledgement

Hanxiao Wang is supported by NSFC Grant 12201424, Guangdong Basic and Applied Basic Research Foundation 2023A1515012104, and Research Team Cultivation Program of Shenzhen University (2023QNT011). Chao Zhou is supported by NSFC Grant 11871364 and Singapore MOE AcRF Grants A-800453-00-00, R-146-000-271-112, R-146-000-284-114. The authors would like to thank Prof. Jiongmin Yong (of UCF) for some suggestive comments and Dr. Luchan Zhang (of SZU) for some help on numerics.

References

- [1] E. W. Anderson, The dynamics of risk-sensitive allocations, Journal of Economic theory, 125 (2005), 93–150.

- [2] H. Aziz, F. Brandt, and P. Harrenstein, Pareto optimality in coalition formation, Games and Economic Behavior, 82 (2013), 562–581.

- [3] S. Basak and G. Chabakauri, Dynamic mean-variance asset allocation, The Review of Financial Studies, 23 (2010), 2970–3016.

- [4] T. Björk, M. Khapko, and A. Murgoci, On time-inconsistent stochastic control in continuous time, Finance and Stochastics, 21 (2017), 331–360.

- [5] T. Björk, A. Murgoci, and X. Y. Zhou, Mean-variance portfolio optimization with state-dependent risk aversion, Mathematical Finance, 24 (2014), 1–24.

- [6] J. Borovička, Survival and long-run dynamics with heterogeneous beliefs under recursive preferences, Journal of Political Economy, 128 (2020), 206–251.

- [7] D. Cao and I. Werning, Saving and dissaving with hyperbolic discounting Econometrica, 86 (2018), 805–857.

- [8] J. Cvitanić and J. Zhang, Contract theory in continuous-time models, Springer Science and Business Media, 2012.

- [9] R. A. Dana and C. LeVan, Structure of Pareto optima in an infinite-horizon economy where agents have recursive preferences, Journal of Optimaztion Theory and Applications, 64 (1990), 269–292.

- [10] M. Dai, H. Jin, S. Kou, and Y. Xu, A dynamic mean-variance analysis for log returns, Management Science, 67 (2021), 1093–1108.

- [11] M. Dokuchaev and X. Y. Zhou, Stochastic controls with terminal contingent conditions, Journal of Mathematical Analysis and Applications, 238 (1999), 143–165.

- [12] D. Duffie and L. G. Epstein, Stochastic differential utility, Econometrica, 60 (1992), 353–394.

- [13] D. Duffie and L. G. Epstein, Asset pricing with stochastic differential utility, The Review of Financial Studies, 5 (1992), 411–436.

- [14] D. Duffie, P. Y. Geoffard, and C. Skiadas, Efficient and equilibrium allocations with stochastic differential utility, Journal of Mathematical Economics, 23 (1994), 133–146.

- [15] D. Duffie and P. L. Lions, PDE solutions of stochastic differential utility, Journal of Mathematical Economics, 21 (1992), 577–606.

- [16] B. Dumas, R. Uppal, and T. Wang, Efficient Intertemporal Allocations with Recursive Utility, Journal of Economic Theory, 93 (2000), 240–259.

- [17] I. Ekeland and A. Lazrak, The golden rule when preferences are time inconsistent, Mathematics and Financial Economics, 4 (2010), 29–55.

- [18] I. Ekeland, O. Mbodji, and T. A. Pirvu, Time-consistent portfolio management, SIAM Journal on Financial Mathematics, 3 (2012), 1–32.

- [19] I. Ekeland and T. A. Pirvu, Investment and consumption without commitment, Mathematics and Financial Economics, 2 (2008), 57–86.

- [20] N. EI Karoui, S. Peng, and M. C. Quenez, Backward stochastic differential equations in finance, Mathematical Finance, 7 (1997), 1–71.

- [21] L. Epstein and S. Zin, Substitution, Risk Aversion and the Temporal Behavior of Consumption and Asset Returns: A Theoretical Framework, Econometrica, 57 (1989), 937–969.

- [22] L. Garlappi, R. Giammarino, and A. Lazrak, Ambiguity and the corporation: Group disagreement and underinvestment, Journal of Financial Economics, 125 (2017), 417–433.

- [23] N. Gârleanu and S. Panageas, Young, old, conservative, and bold: The implications of heterogeneity and finite lives for asset pricing, Journal of Political Economy, 123 (2015), 670–685.

- [24] C. Harris and D. Laibson, Dynamic choices of hyperbolic consumers, Econometrica, 69 (2001), 935–957.

- [25] H. Hong, N. Wang, and J. Yang, Welfare consequences of sustainable finance, National Bureau of Economic Research, 2021

- [26] M. Hu, S. Ji, and X. Xue, A global stochastic maximum principle for fully coupled forward-backward stochastic systems, SIAM Journal on Control and Optimization, 56 (2018), 4309–4335.

- [27] Y. Hu, H. Jin, and X. Y. Zhou, Time-inconsistent stochastic linear–quadratic control, SIAM Journal on Control and Optimization, 50 (2012), 1548–1572.

- [28] M. O. Jackson and L. Yariv, Collective dynamic choice: the necessity of time inconsistency, American Economic Journal: Microeconomics, 7 (2015), 150–178.

- [29] R. Kan, Structure of Pareto optima when agents have stochastic recursive preferences, Journal of Economic Theory, 64 (1995), 626–631.

- [30] P. Krusell and A. A. Smith Jr, Consumption and saving decisions with quasi-geometric discounting, Econometrica, 71 (2003), 366–375.

- [31] D. Laibson, Golden eggs and hyperbolic discounting, Quarterly Journal of Economics, 112 (1997), 443–477.

- [32] A. E. B. Lim and X. Y. Zhou, Linear-quadratic control of backward stochastic differential equations, SIAM Journal on Control and Optimization, 40 (2001), 450–474.

- [33] C. Ma, Market equilibrium with heterogeneous recursive-utility-maximizing agents, Economic Theory, 3 (1993), 243–266.

- [34] E. Morellec and N. Schš¹rhoff, Corporate investment and financing under asymmetric information, Journal of Financial Economics, 99 (2011), 262–288.

- [35] S. Peng, Backward stochastic differential equations and applications to optimal control, Applied Mathematics and Optimization, 27 (1993), 125–144.

- [36] S. Peng, Backward stochastic differential equations and stochastic optimizations, Topics in Stochastic Analysis, J. Yan, S. Peng, S. Fang, and L. Wu, eds., Science Press, Beijing, 1997 (in Chinese).

- [37] R. A. Pollak, Consistent planning, The Review of Economic Studies, 35 (1968), 185–199.

- [38] R. S. Pindyck and N. Wang, The economic and policy consequences of catastrophes, American Economic Journal: Economic Policy, 5 (2013), 306–339.

- [39] J. Sun, H. Wang, and J. Wen, Zero-sum Stackelberg stochastic linear-quadratic differential games, SIAM Journal on Control and Optimization, 61 (2023), 250–282.

- [40] R. H. Strotz, Myopia and inconsistency in dynamic utility maximization, The Review of Economic Studies, 23 (1955), 165–180.

- [41] J. von Neumann and O. Morgenstern, Theory of games and economic behavior, New York: John Wiley & Sons, 1944.

- [42] G. Wang, Z. Wu, and J. Xiong, Maximum principles for forward-backward stochastic control systems with correlated state and observation noises, SIAM Journal on Control and Optimization, 51 (2013), 491–524.

- [43] H. Wang, J. Yong, and C. Zhou, Optimal controls for forward-backward stochastic differential equations: Time-inconsistency and time-consistent solutions, preprint arXiv:2209.08994, 2022.

- [44] J. Yong, Optimality variational principle for controlled forward-backward stochastic differential equations with mixed initial-terminal conditions, SIAM Journal on Control and Optimization, 48 (2010), 4119–4156.

- [45] J. Yong, Time-inconsistent optimal control problems and the equilibrium HJB equation, Mathematical Control and Related Fields, 2 (2012), 271–329.

- [46] J. Yong, Time-inconsistent optimal control problems, Proceedings of 2014 ICM, Section 16. Control Theory and Optimization, (2014), 947–969.

- [47] J. Yong, Differential games: a concise introduction, World scientific, 2014.