On the minimax robustness against correlation and heteroscedasticity of ordinary least squares among generalized least squares estimators of regression

Abstract

We present a result according to which certain functions of covariance matrices are maximized at scalar multiples of the identity matrix. In a statistical context in which such functions measure loss, this says that the least favourable form of dependence is in fact independence, so that a procedure optimal for i.i.d. data can be minimax. In particular, the ordinary least squares (ols) estimate of regression is minimax, in the class of generalized least squares estimates, when the maximum is taken over certain classes of error covariance structures and the loss function possesses a natural monotonicity property. An implication is that it can be safe to ignore such departures – whose precise form is typically unknown – from the usual assumption of i.i.d. errors. We then consider regression models in which the response function is possibly misspecified, and show that, depending on the design, ols can fail to be minimax. We argue that the gains from a minimax estimate are however often outweighed by the simplicity of ols. We go on to investigate the interplay between minimax precision matrices and minimax designs. We find that the design has by far the major influence on efficiency and that, when the two are combined, ols is generally at least ‘almost’ minimax, and often exactly so.

keywords:

design , induced matrix norm , Loewner ordering , particle swarm optimization , robustness.MSC:

[2010] Primary 62G35 , Secondary 62K051 Introduction and summary

When carrying out a study, whether observational or designed, calling for a regression analysis the investigator may be faced with questions regarding possible correlations or heteroscedasticity within the data. If there are such departures from the assumptions underlying the use of the ordinary least squares (ols) estimates of the regression parameters, then the use of generalized least squares (gls) might be called for. In its pure form, as envisioned by Aitken (1935), this calls for the use of the inverse of the covariance matrix , i.e. the precision matrix, of the random errors. This is inconvenient, since is rarely known and, even if there is some prior knowledge of its structure, before the study is carried out there are no data from which accurate estimates of its elements might be made. If a consistent estimate of the precision matrix does exist, then one can employ ‘feasible generalized least squares’ estimation - see e.g. Fomby, Johnson & Hill (1984). Otherwise a positive definite ‘pseudo precision’ matrix might be employed. With data and design matrix this leads to the estimate

| (1) |

In Wiens (2024) a similar problem was addressed, pertaining to designed experiments whose data are to be analyzed by ols. A lemma, restated below as Lemma 1, was used to show that certain commonly employed loss functions, taking covariance matrices as their arguments and increasing with respect to the Loewner ordering by positive semidefiniteness, are maximized at scalar multiples of the identity matrix. This has the somewhat surprising statistical interpretation that the least favourable form of dependence is in fact independence. The lemma was used to show that the assumption of independent and homoscedastic errors at the design stage of an experiment is in fact a minimax strategy, within broad classes of alternate covariance structures.

In this article we study the implications of the lemma in the problem of choosing between ols and gls. We first show that, when the form of the regression response is accurately modelled, then it can be safe – in a minimax sense – to ignore possible departures from independence and homoscedasticity, varying over certain large classes of such departures. This is because the common functions measuring the loss incurred by gls, when the covariance matrix of the errors is , are maximized when is a multiple of the identity matrix. But in that case the best gls estimate is in fact ols, i.e. ols is a minimax procedure.

We then consider the case of misspecified regression models, in which bias becomes a component of the integrated mean squared prediction error (imspe). The imspe is maximized over and over the departures from the fitted linear model. We show that, if a gls with (pseudo) precision matrix is employed, then the variance component of this maximum continues to be minimized by , i.e. by ols, but the bias generally does not and, depending upon the design, ols can fail to be a minimax procedure. This is in contrast to the findings in Wiens (2024), where incorrectly assuming that at the design stage did not affect the bias, and so designing for independence remained a minimax procedure.

We present an algorithm allowing us to determine the minimax choice of numerically, and study this for a large number of designs. It turns out that, if a sensible design is chosen, then is ‘almost’ a minimax choice. When a minimax design – minimizing the maximum imspe over the design as well as over – is also chosen, then is often exactly minimax. We conclude that, for Loewner-increasing loss functions, and for covariance matrices varying over the classes covered by Lemma 1, the simplicity of ols makes it a safe and attractive alternative to gls.

The computations for this article were carried out in matlab; the code is available on the author’s personal website.

2 A useful lemma

Suppose that is a matrix norm, induced by the vector norm , i.e.

We use the subscript ‘’ when referring to an arbitrary matrix norm, but adopt special notation in the following cases:

(i) For the Euclidean norm , the matrix norm is denoted and is the spectral radius, i.e. the root of the maximum eigenvalue of . This is the maximum eigenvalue of if is a covariance matrix, i.e. is symmetric and positive semidefinite.

(ii) For the sup norm , the matrix norm is , the maximum absolute row sum.

(iii) For the 1-norm , the matrix norm is , the maximum absolute column sum. For symmetric matrices, .

Now suppose that the loss function in a statistical problem is , where is an covariance matrix and is non-decreasing in the Loewner ordering:

Here means that , i.e. is positive semidefinite.

The following lemma is established in Wiens (2024).

Lemma 1.

For , covariance matrix and induced norm , define

| (2) |

For the norm an equivalent definition is

Then:

(i) In any such class , .

(ii) If and , then .

A consequence of (i) of this lemma is that if one is carrying out a statistical procedure with loss function , then a version of the procedure which minimizes is minimax as varies over . The procedures discussed in this article do not depend on the particular value of – its only role is to ensure that is large enough to contain the departures of interest.

3 Generalized least squares regression estimates when the response is correctly specified

Consider the linear model

| (3) |

for of rank . Suppose that the random errors have covariance matrix . If is known then the ‘best linear unbiased estimate’ is . In the more common case that the covariances are at best only vaguely known, an attractive possibility is to use the generalized least squares estimate (1) for a given positive definite (pseudo) precision matrix . If then the blue is returned. A diagonal gives ‘weighted least squares’ (wls). For brevity we drop the ‘pseudo’ and call a precision matrix. Since is invariant under multiplication of by a scalar, we assume throughout that

| (4) |

The covariance matrix of is

Viewed as a function of this is non-decreasing in the Loewner ordering, so that if a function is non-decreasing in this ordering, then

is also non-decreasing and the conclusions of the lemma hold:

But this last expression is minimized by , i.e. by the ols estimate , with minimum value

This follows from the monotonicity of and the inequality

which uses the fact that is idempotent, hence positive semidefinite.

It is well-known that if then the th largest eigenvalue of dominates that of , for all . It follows that is non-decreasing in the Loewner ordering in the cases:

(i) ;

(ii) ;

(iii) ;

(iv) for .

Thus if loss is measured in any of these ways and then is minimax for in the class of gls estimates.

In each of the following examples, we posit a particular covariance structure for , a norm , a bound and a class for which . In each case , so that statement (ii) of the lemma applies and is minimax for (and for all of as well) and with respect to any of the criteria (i) – (iv).

Example 1: Independent, heteroscedastic errors. Suppose that . Then the discussion above applies if is the subclass of diagonal members of for .

Example 2: Equicorrelated errors. Suppose that the researcher fears that the observations are possibly weakly correlated, and so considers , with . If then , and we take . If is the subclass of or or defined by the equicorrelation structure, then minimaxity of for any of these classes follows. If then this continues to hold for , and for if .

Example 3: ma errors. Assume first that the random errors are homoscedastic but are possibly serially correlated, following an ma model with corr and with . Then , and in the discussion above we may take to be the subclass – containing – defined by if . If the errors are instead heteroscedastic, then is replaced by .

Example 4: ar errors. It is known – see for instance Trench (1999, p. 182) – that the eigenvalues of an ar autocorrelation matrix with autocorrelation parameter are bounded, and that the maximum eigenvalue has . Then, again under homoscedasticity, the covariance matrix has , and the discussion above applies when is the subclass defined by the autocorrelation structure.

3.1 Inference from GLS estimates when

In the next section we consider biased regression models, and investigate the performance of the gls estimate (1) with when in fact is a multiple of the identity matrix. A caveat to the use of this estimate in correctly specified models (3) is given by the following result. It was established in Wiens (2000) for wls estimates, but holds for gls estimates as well.

Theorem 1.

The projector will typically have rank when , and so degrees of freedom are lost in the estimation of and subsequent normal-theory inferences.

4 Minimax precision matrices in misspecified response models

Working in finite design spaces , and with -dimensional regressors , Wiens (2018) studied design problems for possibly misspecified regression models

with the unknown contaminant ranging over a class and satisfying, for identifiability of , the orthogonality condition

| (5) |

as well as a bound

| (6) |

For designs placing mass on , he took , loss function imspe:

and found designs minimizing the maximum, over , of .

In Wiens (2018) the random errors were assumed to be i.i.d.; now suppose that they instead have covariance matrix and take with precision matrix . Using (5), and emphasizing the dependence on and , decomposes as

| (7) |

Here is the bias. Denote by the vector consisting of the values of corresponding to the rows of , so that .

To express these quantities in terms of the design, define a set of indicator matrices

There is a one-one correspondence between and the set of -point designs on . Given , with , the th column of contains ones, specifying the number of occurrences of in a design, which thus has design vector . Conversely, a design determines by .

Define to be the matrix with rows . Then and, correspondingly, for .

The proof of the following theorem is in the appendix.

Theorem 2.

For as at (2) and as at (6), define ; this is the relative importance to the designer of errors due to bias rather than to variation. Then for a design and precision matrix , the maximum of as varies over and varies over is

| (8) |

where

Here the columns of form an orthogonal basis for the column space , is the indicator matrix of the design , and denotes the maximum eigenvalue of a matrix.

In (8), var and bias are the components of the imspe due to variation and to bias, respectively. That is minimized by for any design was established in §3. If ols is to be a minimax procedure for a particular design, then for each any increase in bias must be outweighed by a proportional decrease in var. We shall present numerical evidence that for many designs this is not the case, and then ols is not minimax.

To find minimizing (8) we note that any positive definite matrix can be represented as , for a lower triangular . We thus express as a function of the vector consisting of the elements in the lower triangle of , and minimize over using a nonlinear constrained minimizer. The constraint – recall (4) – is that .

Of course we cannot guarantee that these methods yield an absolute minimum, but the numerical evidence is compelling. In any event, the numerical results give a negative answer to the question of whether or not ols is necessarily minimax for any design – the minimizing is often, but not always, the identity.

To assess these precision matrices we carried out a simulation study. We set the design space to be , with the equally spaced. We chose regressors , or , corresponding to linear, quadratic, or cubic regression. For various values of and we first randomly generated probability distributions and then generated a multinomial vector; this is . For each such design we computed the minimizing , and both components of the minimized value of . This was done for . We took equal to five times the number of regression parameters. Denote by the minimizing . Of course . In each case we compared three quantities:

The means, and standard errors based on 100 runs, of these performance measures using these ‘multinomial’ designs are given in Table 1. When the percent reduction in the bias, i.e. in , can be significant, but is accompanied by an often sizeable increase in the variance (). When the reduction in is typically quite modest.

| Table 1. Minimax precision matrices; multinomial designs: | ||||||||

|---|---|---|---|---|---|---|---|---|

| means of performance measures standard error. | ||||||||

| Response | ||||||||

| linear | ||||||||

| quadratic | ||||||||

| cubic | ||||||||

| Table 2. Minimax precision matrices; symmetrized designs: | ||||||||

|---|---|---|---|---|---|---|---|---|

| means of performance measures standard error. | ||||||||

| Response | ||||||||

| linear | ||||||||

| quadratic | ||||||||

| cubic | ||||||||

These multinomial designs, mimicking those which might arise in observational studies, are not required to be symmetric. We re-ran the simulations after symmetrizing the designs by averaging them with their reflections across and then applying a rounding mechanism which preserved symmetry. The resulting designs gave substantially reduced losses both for (ols) and (gls). The differences between the means of and were generally statistically insignificant, and the values of , and showed only very modest benefits to gls. See Table 2.

A practitioner might understandably conclude that, even though is minimax, its benefits are outweighed by the computational complexity of its implementation. This is bolstered by Theorem 1, which continues to hold with the modification that now follows a scaled non-central distribution, with a non-centrality parameter depending on .

5 Minimax precision matrices and minimax designs

| Table 3. Minimax designs and precision matrices: | ||||||||

|---|---|---|---|---|---|---|---|---|

| performance measures ( if ). | ||||||||

| Response | ||||||||

| linear | ||||||||

| quadratic | ||||||||

| cubic | ||||||||

We investigated the interplay between minimax precision matrices and minimax designs. To this end (8) was minimized over both and . To minimize over we employed particle swarm optimization (Kennedy and Eberhart 1995). The algorithm searches over continuous designs , and so each such design to be evaluated was first rounded so that had integer values. Then , and the corresponding minimax precision matrix were computed and the loss returned. The final output is an optimal pair . Using a genetic algorithm yielded the same results but was many times slower.

The results, using the same parameters as in Tables 1 and 2, are shown in Table 3. We note that in all cases the use of the minimax design gave significantly smaller losses, both using ols and gls. In eight of the twelve cases studied it turned out that the choice was in fact minimax; in the remaining cases minimax precision resulted in only a marginal improvement. Of the two factors – and – explaining the decrease in , the design is by far the greater contributor.

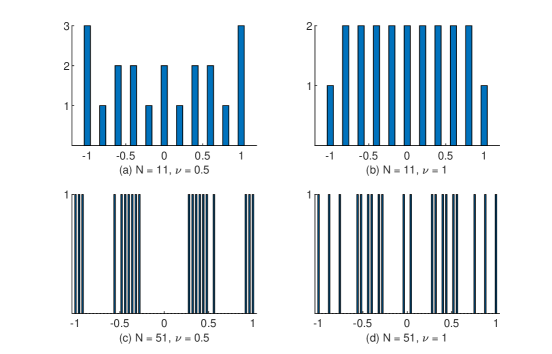

See Figure 1 for some representative plots of the minimax designs for a cubic response. These reflect several common features of robust designs. One is that the designs using , i.e. aimed at minimization of the bias alone, tend to be more uniform than those using . This reflects the fact – following from (5) – that if a uniform design on all of could be implemented, then the bias using ols would vanish. As well, when the design space is sufficiently rich as to allow for clusters of nearby design points to replace replicates, then this tends to take place. See Wiens (2023), Fang and Wiens (2000) and Heo et al. (2001) for examples and discussions. Such clusters form near the support points of the classically I-optimal designs, minimizing variance alone.

In their study of random design strategies on continuous design spaces, Waite and Woods (2022) also recommend designs with clusters chosen near the I-optimal design points. See Studden (1977) who showed that the I-optimal design for cubic regression places masses , at each of , - a situation approximated by the design in (c) of Figure 1, whose clusters around these points account for masses of and each.

Appendix: Proof of Theorem 2

In the notation of the theorem, (7) becomes

| (A.1) | |||||

As in §3, and taking in (iv) of that section, for the trace in (A.1) is maximized by , with

| (A.2) |

Extend the orthogonal basis for by appending to the matrix , whose columns form an orthogonal basis for the orthogonal complement . Then is an orthogonal matrix and we have that for a non-singular . If the construction is carried out by the Gram-Schmidt method, then is upper triangular.

Constraint (5) dictates that lie in . A maximizing will satisfy (6) with equality, hence for some with unit norm. Combining these observations along with (A.1) and (A.2) yields that is given by

| (A.3) |

Here and elsewhere we use that , and that such products have the same non-zero eigenvalues. Then (A.3) becomes times , given by

| (A.4) |

The maximum eigenvalue is also that of

Acknowledgements

This work was carried out with the support of the Natural Sciences and Engineering Research Council of Canada.

References

-

Aitken, A. C. (1935), “On Least Squares and Linear Combinations of Observations,” Proceedings of the Royal Society of Edinburgh, 55: 42-48.

-

Fang, Z., and Wiens, D. P. (2000), “Integer-Valued, Minimax Robust Designs for Estimation and Extrapolation in Heteroscedastic, Approximately Linear Models,” Journal of the American Statistical Association, 95, 807-818.

-

Fomby, T.B., Johnson, S.R., Hill, R.C. (1984), “Feasible Generalized Least Squares Estimation,” in: Advanced Econometric Methods, Springer, New York, NY.

-

Heo, G., Schmuland, B., and Wiens, D. P. (2001), “Restricted Minimax Robust Designs for Misspecified Regression Models,” The Canadian Journal of Statistics, 29, 117-128.

-

Kennedy, J., Eberhart, R. (1995), “Particle Swarm Optimization,” Proceedings of IEEE International Conference on Neural Networks, 1942-1948.

-

Studden, W.J. (1977), “Optimal Designs for Integrated Variance in Polynomial Regression,” Statistical Decision Theory and Related Topics II, ed. Gupta, S.S. and Moore, D.S. New York: Academic Press, pp. 411-420.

-

Trench, W. F. (1999), “Asymptotic distribution of the spectra of a class of generalized Kac-Murdock-Szegö matrices,” Linear Algebra and Its Applications, 294, 181-192.

-

Waite, T.W., and Woods, D.C. (2022),“Minimax Efficient Random Experimental Design Strategies With Application to Model-Robust Design for Prediction,” Journal of the American Statistical Association, 117, 1452-1465.

-

Wiens, Douglas P. (2000), “Robust Weights and Designs for Biased Regression Models: Least Squares and Generalized M-Estimation,” Journal of Statistical Planning and Inference, 83, 395-412.

-

Wiens, Douglas P. (2018), “I-Robust and D-Robust Designs on a Finite Design Space,” Statistics and Computing, 28, 241-258.

-

Wiens, Douglas P. (2023),“ Jittering and Clustering: Strategies for the Construction of Robust Designs,” arXiv preprint arXiv:2309.08538.

-

Wiens, D. P. (2024), “A Note on Minimax Robustness of Designs Against Correlated or Heteroscedastic Responses,” Biometrika, in press. https://doi.org/10.1093/biomet/asae001.