Similarity and Comparison Complexity††thanks: We are indebted to Benjamin Enke, Matthew Rabin, Joshua Schwartzstein, and Tomasz Strzalecki for their excellent supervision and guidance. We also thank Katie Coffman, Thomas Graeber, Yannai Gonczarowski, Jerry Green, David Laibson, Shengwu Li, Gautam Rao, Andrei Shleifer, and Harvard PhD workshop participants for helpful comments and suggestions. Shubatt: Department of Economics, Harvard University. cshubatt@g.harvard.edu. Yang: Department of Economics, Harvard University. jeffrey_yang@g.harvard.edu.

Abstract

Some choice options are more difficult to compare than others. This paper develops a theory of what makes a comparison complex, and how comparison complexity generates systematic mistakes in choice. In our model, options are easier to compare when they 1) share similar features, holding fixed their value difference, and 2) are closer to dominance. We show how these two postulates yield tractable measures of comparison complexity in the domains of multiattribute, lottery, and intertemporal choice. Using experimental data on binary choices, we demonstrate that our complexity measures predict choice errors, choice inconsistency, and cognitive uncertainty across all three domains. We then show how canonical anomalies in choice and valuation, such as context effects, preference reversals, and apparent probability weighting and present bias in the valuation of risky and intertemporal prospects, can be understood as responses to comparison complexity.

Keywords: Complexity, multi-attribute choice, choice under risk, intertemporal choice, cognitive uncertainty, experiments

1 Introduction

Some choice options are hard to compare, and this difficulty leads to errors in decision-making. Individuals choose health insurance plans, savings vehicles, and cell phone plans that are in reality financially dominated. Even in settings where objective choice errors cannot be identified, introspection reveals that we often face difficult comparisons: how should one choose between job offers that differ in salary and equity compensation, mortgages with different repayment schedules, or housecats of varying size and temperament? We worry or even agonize over choosing incorrectly in such contexts, and these mistakes not only have private welfare costs for market participants, but may also shape how markets function.

While a growing economic literature on complexity considers what makes choices difficult, most theories of complexity operate at the option level — that is, they tell us what makes a choice option difficult to value (e.g., Enke and Graeber,, 2023; Enke et al.,, 2023; Puri,, 2023; Khaw et al.,, 2021). While this difficulty may shape behavior in certain contexts, people often choose by comparing options directly rather than by producing absolute valuations, and there are important differences between what makes options hard to compare vs. hard to value. For instance, two lotteries may be difficult to value in the sense of having many states, yet easy to compare if one lottery transparently dominates the other.

In this paper, we seek to answer two questions. First, what makes choice options hard to compare? We develop a theory of comparison complexity applicable to the domains of multiattribute, lottery, and intertemporal choice, which formalizes the intuition that options are harder to compare when they require the decision-maker to aggregate trade-offs across option features. We then test our theory using rich experimental data on binary choices across all three domains, and demonstrate its predictive power relative to benchmark models. Second, what are the behavioral consequences of comparison complexity? We embed our theory of comparison complexity into a stochastic choice model in which the decision-maker chooses based on noisy signals of how options compare, the precision of which are governed by our theory of comparison complexity. We use our choice model to shed light on various systematic anomalies in choice and valuation, including context effects, preference reversals, and apparent probability weighting and hyperbolic discounting in the valuation of risky and intertemporal prospects. Through the lens of our model, these phenomena can all be understood as a response to the cognitive difficulty of making comparisons.

Theory of comparison complexity. We develop a theory of comparison complexity, which we formalize as the difficulty of identifying one’s preferred option from a binary menu. We consider a decision-maker who is uncertain about the values of two options and , and chooses based on a noisy signal of how the values compare. The precision of this signal, , captures the ease of comparison between and , and governs the decision-maker’s likelihood of choosing the higher value option. We propose a theory of how depends on the features of choice options, applicable to the domains of multiattribute, lottery, and intertemporal choice.

Much previous work argues that complexity arises when decision-makers must aggregate different problem features to reach a conclusion. Our theory is motivated by the simple observation that comparisons involve aggregating trade-offs across option features, and that not all comparisons require the same degree of aggregation. To illustrate, consider the three choice environments in Figure 1. Notice that across these domains, the comparison between and is easy — there is little need to make trade-offs across option features to see that is in fact better than . On the other hand, the comparison between and is less obvious, as the DM now must engage with non-trivial trade-offs across different option features: 1a) involves a trade-off between the monthly fee vs. usage fee, 1b) involves trading off a higher maximum payout against a lower payout probability, and 1c) involves a trade-off between payout amount and delay.

Our theory is built on two formal principles that capture this notion of trade-off complexity: similarity and dominance. First, we posit that holding fixed their value difference, options are easier to compare if they are more similar — that is, that the ease of comparison is an increasing transformation of the value-dissimilarity ratio:

where the numerator contains the value difference between the two options and the denominator is a distance metric measuring their dissimilarity. Intuitively, similar options require less aggregation of trade-offs to compare, as the DM can divert attention from features that are similar across options and so more easily assess their differences. This intuition echoes work in psychology (Tversky and Edward Russo,, 1969) and in economics (Rubinstein,, 1988; He and Natenzon,, 2023) which has stressed the role of similarity in governing the ease of comparison.

| Domain | Representation for | Distance Metric |

| Multiattribute | ||

| Lottery | ||

| Intertemporal |

denotes the cumulative payoff function of a payoff flow .

To pin down the specific dissimilarity measure, we appeal to our second principle: that options are maximally easy to compare in the presence of dominance. Dominance eliminates the need to aggregate trade-offs across features, and to the extent decision-makers find this aggregation difficult, comparisons involving dominance relationships should be more accurate than comparisons that do not. The relevant dominance notions in each of our domains — attribute-wise dominance in multiattribute choice, first-order stochastic dominance in lottery choice, and temporal dominance in intertemporal choice111We say an intertemporal payoff flow temporally dominates if at any point in time, will have paid off more in total than . — give rise to the appropriate dissimilarity measure in each domain, summarized in Table 1; for each of these measures, options are maximally easy to compare when they share a dominance relationship.

The postulates of similarity and dominance are not only satisfied by our representations, but also are key in characterizing them; we show that axioms on binary choice behavior corresponding to the postulates of similarity and dominance, in tandem with other easily understood axioms, characterize our representations of in each domain.

Tests of complexity measures. Our theory predicts that in binary choice, the prevalence of 1) choice errors, 2) within-individual choice inconsistency, and 3) subjective uncertainty over choices should be decreasing in the value-dissimilarity ratio. Using three experimental datasets on binary choices corresponding to our three domains of interest, we show that the value-dissimilarity ratio is strongly predictive of each of these behavioral indicators of choice complexity. We collect datasets on multiattribute and intertemporal choice ourselves and draw lottery choice data from Peterson et al., (2021) and Enke and Shubatt, (2023). In each set of experiments, subjects face a sequence of binary choice problems: in total we study 662 choice problems between multiattribute goods with induced values; 10,923 lottery choice problems; and 1100 choice problems between time-dated payoff streams. All three datasets contain repeat instances of the same choice problem for a given subject, allowing for the estimation of choice inconsistency rates, as well as a measure of subjects’ cognitive uncertainty — their subjective probability of choosing the lower-value option.

We find that the value-dissimilarity ratio is strongly predictive of choice “error" rates in all three domains, where we define an error as a) choosing the lower-value option in multiattribute choice and b) choosing the less-preferred option according to a best-fit model of risk and time preferences in lottery and intertemporal choice, respectively. This relationship is quantitatively large — in multiattribute choice, for instance, error rates range from 5% for choice problems with the highest value-dissimilarity ratio to more than 30% for choice problems with the lowest ratio. As we see in Figure 2, similarly pronounced relationships hold in intertemporal and lottery choice.

We also find that within-subject choice inconsistency is decreasing in the value-dissimilarity ratio across all three domains. In multi-attribute choice, inconsistency rates range from less than 5% for choice problems with the highest value-dissimilarity ratio to over 20% for choice problems with the lowest ratio, and we find similar relationships in lottery and intertemporal choice. Finally, we document that the value-dissimilarity ratio predicts not only comparison complexity revealed in choice behavior, but also captures subjective complexity, i.e., how hard comparisons actually feel to subjects. We find a strong decreasing relationship between cognitive uncertainty and the value-dissimilarity ratio.

Benchmarking predictive power. Using our experimental choice data, we benchmark the predictive power of our theory against existing models in all three domains. We structurally estimate a choice model in which choice rates depend only on the value-dissimilarity ratio.222Our structural model contains two free parameters for multiattribute choice, and three parameters for lottery and intertemporal choice. In multiattribute choice, our model delivers predictive power comparable to that of leading behavioral choice models while using fewer free parameters, and importantly explains a substantial amount of variation in choice that is not captured by existing models. In lottery and intertemporal choice, our model substantially outperforms leading behavioral choice models. In these domains, our model explains 10-28% more variation than the best alternative models without using any additional parameters (and in the case of lottery choice, actually using fewer parameters).

Multinomial choice model and behavioral implications. Having developed and tested our theory of comparison complexity, we embed the theory in a multinomial choice model to study its behavioral implications beyond binary choice. In our choice model, the decision-maker faces a menu of options, and chooses based on noisy signals on how each pair of options in the menu compares. In particular, for each comparison in the menu, the decision-maker generates a signal on the value comparison between the two options with precision , where is governed by the value-dissimilarity ratio; the DM then chooses the option with the highest posterior expected value according to these signals.

Our choice model straightforwardly accounts for documented context effects in multinomial choice, such as the decoy and asymmetric dominance effects. Furthermore, we show that in lottery and intertemporal choice, our model rationalizes documented instabilities and biases in valuations, where here we formalize valuations within our choice model as a set of comparisons between an option and different amounts of money in a multiple price list. The core insight is that some risky or intertemporal prospects are easier to compare to money than others, which leads to systematic biases in valuations. Through this mechanism, our model predicts apparent probability weighting and hyperbolic discounting in valuations even in the absence of such distortions in direct choice, rationalizing documented preference reversals. The model also makes the novel testable prediction that one can reverse the direction of these biases by changing the numeraire in valuation: asking subjects to value lotteries using probability-equivalents, and intertemporal payments using time-equivalents.

Contribution and relation to prior work.

Our paper builds upon a growing literature on complexity and cognitive uncertainty in choice. These papers have documented how complexity can lead to noisy choice and/or systematically biased valuations (Enke and Shubatt,, 2023; Puri,, 2023, etc.), but typically focus on a single choice domain. Our unifying measure of complexity can be computed across several choice domains and experimental settings, offering a framework to tie together these disparate findings.

We also formalize insights from a more conceptual Psychology and Economics literature on similarity in choice. These papers (Rubinstein,, 1988; Tversky and Edward Russo,, 1969) use illustrative examples to argue that when agents choose between dissimilar objects, we may expect more violations of standard choice axioms. We both introduce an explicit similarity measure and formally model how similarity affects choice.

Finally, we bring cognitive insights and empirical evidence to a recently developing literature on stochastic choice. Our model belongs to a general class of moderate utility models axiomatized in He and Natenzon, (2023), wherein binary choice probabilities are a function of the value difference between two options normalized by their distance according to a metric. We make three contributions to this literature. First, we propose specific distance metrics in the domains of multiattribute, lottery, and intertemporal choice, motivated by the idea that the need to aggregate tradeoffs across option features governs the difficulty of comparison. Second, we provide a series of experimental tests of the model’s predictions, quantifying the tight relationship between the complexity measure and cognitive uncertainty, choice inconsistency, and choice errors. Third, we provide a novel and flexible framework for extending this class of binary choice models to multinomial choice.

Section 2 lays out the binary choice model and discusses the psychological motivation for the complexity measure. Section 3 describes the binary choice experiment design and results. Section 4 introduces the extension to multinomial choice, and applies the model to study context effects and valuations. Section 5 concludes. Proofs of all formal results are relegated to Appendix C.

2 Theory of Comparison Complexity

2.1 Binary Choice Framework

Let denote the set of options, and let denote the value of each . We consider a decision-maker (DM) who is uncertain over the value of each option in , and when faced with a binary choice , chooses based on a noisy signal on how and compare.

In particular, the DM has continuous, i.i.d. priors over for all distributed according to a symmetric distribution , and observes a signal on the ordinal value comparison between and , given by

and chooses the option with the highest posterior expected value. Here, the precision parameter governs the ease of comparison between and . Letting denote the likelihood of choosing over 333In particular, , where the DM uniformly randomizes if ., this signal structure implies that , for some continuous, strictly increasing, with .444In particular, , where is the standard normal CDF. That is, the decision-maker’s likelihood of correctly choosing the higher-valued option is increasing in the ease of comparison . In what follows, we propose a theory of how depends on the structure of choice options in the domains of multiattribute, lottery, and intertemporal choice.

2.2 Comparison Complexity: General Principles

Our theory of formalizes the intuition that the difficulty of a comparison is governed by the degree to which it requires the DM to aggregate tradeoffs. The theory is grounded in two principles that capture this intuition: similarity and dominance.

First, we posit holding fixed the value difference, options are easier to compare when they are more similar. Echoing previous work in psychology (Tversky and Edward Russo,, 1969) and in economics (Rubinstein,, 1988; He and Natenzon,, 2023), this property reflects the intuition that if options are more similar, the DM can divert attention from the features that are similar across the options and so more easily assess the differences between them, thereby reducing the need to aggregate tradeoffs. As such, we propose a representation of the ease of comparison that is an increasing transformation of the value-dissimilarity ratio:

where the numerator contains the value difference between the two options and the denominator is a distance metric measuring their dissimilarity.

Second, we posit options are maximally easy to compare when there is a dominance relationship between them. In the presence of dominance, the DM does not need to engage with trade-offs to see which option is better, and so we should expect comparisons that involve dominance to be easier those that do not. As formalized in the sections below, this principle gives rise to a specific distance metric in each domain, depending on the domain-relevant notion of dominance.

2.3 Multiattribute Choice

Consider the domain of multiattribute choice, where each option is defined on real-valued attributes, where . Utility is linear in attributes, where the value of each option is given by for attribute weights .555In Appendix B.1, we show how the model can be generalized to allow for additively separable preferences that are not necessarily linear in attributes, and provide an axiomatic characterization of the generalized model. We propose that the ease of comparison in this domain is governed by the following representation:

Definition 1.

Say that has an -complexity representation, denoted , if there exists , for all , such that

for continuous, strictly increasing with , where is the distance between and in value-transformed attribute space.

In words, under the -complexity representation, the ease of comparison between two options is governed by their value-dissimilarity ratio: their integrated value difference, normalized by a distance metric equal to their feature-by-feature value difference.

Note that our proposed complexity representation satisfies the properties of similarity and dominance. Holding fixed the value difference between two options, the ease of comparison is increasing in the similarity between and , as measured by a distance metric on the space of alternatives. Moreover, if there is an attribute-by-attribute dominance relationship between and ; i.e. for all , the ease of comparison takes on its maximal value of .

-complexity also satisfies a simplification property, wherein reducing the number of active attributes — that is, attributes along which there is a value difference — increases the ease of comparison. To take an example, suppose , , and consider the following comparisons:

Note that is formed by eliminating the value difference along the first attribute and redistributing that value to the second attribute. Our complexity representation predicts that the DM finds easier to compare than , i.e. . More generally, our model predicts that eliminating a value difference along some attribute and redistributing it to another attribute makes options easier to compare.666That is, given any , for satisfying , for all , with , we have . This property again reflects tradeoff complexity: if individuals find it difficult to aggregate tradeoffs across features, we should expect that a simplification operation of the kind above, where some of that aggregation is done for the decision-maker, makes the comparison easier.

2.3.1 Axiomatic Foundations

The above properties are not only satisfied by our complexity representation, but are also key properties in its characterization. Our representation for is characterized by axioms on binary choice behavior corresponding to the properties of similarity, dominance, and attribute simplification, along with three other easily understood axioms.

Let denote the set of all pairs of distinct options. Consider a binary choice rule satisfying for all ; here, denotes the likelihood of choosing over . In our binary choice framework, has an -Complexity representation if and only if binary choice probabilities take the form below.

Definition 2.

Say that a binary choice rule has an -Complexity Representation if there exists , , such that

for some continuous, strictly increasing.

That is, under our representation for , the likelihood of choosing over is an increasing function of the signed value difference between the two options, normalized by their distance.

We now characterize our representation. Let denote the option obtained by replacing the th attribute of with 777That is and for all .. Say that dominates , written , if for all with a strict inequality for at least one . Say that attribute is null if for all . Consider the following axioms:

-

M1.

Continuity: is continuous on its domain.

-

M2.

Linearity: .

-

M3.

Moderate Transitivity: If , , then either or .

-

M4.

Dominance: If , then for any , where the inequality is strict if .

-

M5.

Simplification: For any , satisfying for

for some : if and , then .

Continuity and Linearity are standard axioms, and the latter reflects the fact that both preferences and the distance in our model are linear in attributes. Moderate Transitivity is a transitivity condition on binary choice that allows for choice probabilities to depend on features of choice options other than their value difference – and specifically allows for choice probabilities to depend on a notion of similarity between choice probabilities.888In particular, He and Natenzon (2023) show that a binary choice rule acting on a finite domain satisfies Moderate Transitivity if and only if is increasing in the value difference between and , normalized by the distance between and according to some distance metric . While this equivalence does not hold in our choice domains as they are not finite, our other axioms can be thought of as adding structure to this distance metric.

Dominance and Simplification are the exact counterparts of the properties of discussed earlier, stated in terms of choice probabilities. Dominance says that if is revealed better than on every attribute, then the likelihood of correctly choosing takes on its maximal value. Simplification says that if we eliminate the value difference between and along some attribute and redistribute that value to another attribute of , the likelihood of correctly choosing increases.

The following theorem says that when there are 3 or more attributes, M1–M5 characterize the behavioral implications of our representation for binary choice data, and that the parameters of our representation can be identified from binary choice data.999In Appendix B.1, we show that the two attribute case is characterized by adding an Exchangeability axiom, which says that swapping attribute labels (while making the appropriate adjustments to account for attribute weights) will not affect choice.

Theorem 1.

Suppose that all attributes are non-null and . has a -complexity representation if and only if it satisfies M1–M5. Moreover, if also has a -complexity representation , then and for .

2.4 Risky and Intertemporal Choice

2.4.1 Lotteries

Consider the lottery domain, where each option is a finite-support lottery over ; that is each is described by the mass function where for finitely many . Let and denote the CDF and quantile function of . Preferences are given by expected utility, with for strictly increasing.

Definition 3.

has an CDF-complexity representation, denoted , if for strictly increasing,

for continuous, strictly increasing with , where the CDF distance is given by

As with the -complexity representation, the ease of comparison between two options under the CDF-complexity representation is governed by their value-dissimilarity ratio — that is, the value difference between the two options normalized by a measure of their dissimilarity. The specific dissimilarity measure in our representation, , is a metric equal to the area between the utility-valued CDFs of and , and so captures how similarly the payoffs in and are distributed.101010 is a special case of the Wasserstein metric, a distance notion defined on probability distributions over a metric space.

This measure provides a formal foundation for existing empirical work which documents a tight connection between the CDF distance and choice rates. In particular, both Enke and Shubatt, (2023) and Erev et al., (2002) show that the performance of stochastic choice models over lotteries dramatically improves when decision noise is allowed to vary with the a special case of the CDF distance, with .

2.4.2 Intertemporal Payoff Flows

Now consider the intertemporal domain, where each option is a finite stream of time-dated payoffs; each is described by the payoff function where for finitely many ; describes how much pays off at time . Let denote the cumulative payoff function of , which describes how much money pays in total up until time . Preferences are given by exponential discounting, with , for .111111In Appendix B.1 we show how the theory can be generalized to allow for a general decreasing discount function , and provide an axiomatic characterization of this generalized model.

Definition 4.

has an CPF-complexity representation, denoted , if there exists such that

for continuous, strictly increasing with , where the CPF distance is given by

As with our previous complexity measures, the ease of comparison between two options under the CPF-complexity representation is governed by their value-dissimilarity ratio, where the dissimilarity measure is a metric that is proportional to the present value of the difference between the cumulative payoff functions of and , and captures how similarly and distribute their payoffs across time.

2.4.3 Shared Properties

Like our multiattribute complexity measure, and satisfy our core properties of similarity and dominance. Holding fixed the value difference, and are increasing in the similarity between and , as measured by a distance metric on the space of alternatives, where this distance metric is chosen to so that takes on its maximal value when there is a dominance relationship between and . In particular, say that a lottery first-order stochastically dominates when for all , and say that a payoff flow temporally dominates if if for all — that is, if will have paid out more in total than at any point in time. Notice that takes on its maximal value of when there is a first-order stochastic dominance relationship between lotteries and , and takes on their maximal value of when there is a temporal dominance relationship between payoff flows and .

and also satisfy analogs of the simplification property for , which says that aggregating value differences across different features into the same feature makes options easier to compare. As formally stated in Appendix B.1, concentrating value differences from different percentile regions in the distribution of two lotteries , into the same region increases the ease of comparison according to , and concentrating value differences from different time periods of two payoff flows into the same time period increases the ease of comparison according to .

2.4.4 Axiomatic Foundations

The binary choice behavior implied by and can be characterized using axioms analogous to M1—M5. In Appendix B.1, we show how the binary choice rules corresponding to and are characterized by five axioms: direct translations of Continuity, Linearity, Moderate Transitivity, and Dominance, and an analog of Simplification.

2.4.5 Connection to Complexity

Our complexity measures for risk and time not only share the same properties of our multiattribute measure, but can also be interpreted as extensions of complexity. We relegate discussion of the connection between CPF and complexity to the appendix, and discuss the connection between CDF and complexity below. CDF complexity is equivalent to complexity when applied to a common attribute representation of lotteries — specifically, the attribute representation that maximizes the ease of comparison according to complexity.

Consider the set of possible couplings of lotteries — that is, the set of joint distributions over payoffs such that and for all . Note that each coupling induces an attribute representation of and , in which the attributes are given by the set of joint utility-transformed payoff realizations in the support of , weighted by the likelihoods of those payoff realizations under .121212Such attribute representations of lotteries have been used in previous work, such as Bordalo, et al. (2012).

To take an example, consider a lottery which pays $18 w.p. , and which pays $12 w.p. , and consider the attribute structures induced by two different couplings:

The attribute structure on the left corresponds to a coupling in which the lotteries are uncorrelated, and the attribute structure on the right corresponds to a coupling that imposes positive correlation between the lotteries. For each attribute structure induced by , we can compute the ease of comparison under complexity, given by131313For example, in the risk neutral case where , the ease of comparison is given by for the leftmost attribute representation and for the rightmost attribute representation

Proposition 1 says that the attribute structure that maximizes the ease of comparison according to gives rise to exactly the CDF complexity representation.

Proposition 1.

.

Proposition 1 points to the following two-stage cognitive interpretation of our CDF complexity measure: in a “representation stage", the DM first represents the lotteries using a common set of attributes, and then compares the lotteries along these attributes in an “evaluation stage". In particular, Proposition 1 says that if the DM represents the lotteries using an attribute structure that maximizes their comparability in the evaluation stage, where this ease of comparison is governed by -complexity, the overall ease of comparison will be given by CDF complexity.

As with our lottery complexity measure, CPF complexity can be seen as an extension of complexity to intertemporal choice. In Appendix B.2, we show how the CPF complexity representation can be similarly derived as the complexity for the common attribute representation of intertemporal payoff flows that maximizes their ease of comparison.

2.5 Parameterizing the Model

In each of our domains, our model predicts that the the probability of choosing option over is given by

where the signed value-dissimilarity ratio is specified in each domain according to Definitions 1,3, and 4, and is a strictly increasing transformation that is symmetric around , with .141414There is a one-to-one correspondence between , which maps the signed value-dissimilarity ratio into choice probabilities , and , which maps the value-dissimilarity ratio into signal precisions . In particular, for , , where is the standard normal CDF. To obtain quantitative predictions, the analyst needs to specify the preference parameters that enter the value-dissimilarity ratio — the attribute weights in multiattribute choice, the Bernoulli utility function in lottery choice, and the discount factor in intertemporal choice — as well as the transformation . In each domain, these objects can identified from binary choice data, as demonstrated in Theorem 1 for multiattribute choice, and in Appendix B.1 for our other two domains.

When fitting our model to data, as in Section 3, our preferred specification of is given by the two-parameter functional form

| (1) |

Here is a tremble parameter that governs the DM’s error rate at dominance, and governs the curvature in the relationship between choice probabilities and the value-dissimilarity ratio. Note that for , error rates will be concave in , which captures the possibility that the difficulty of a comparison may be steeply increasing away from dominance.

Note that also implies that choice rates will be relatively insensitive to the value-dissimilarity ratio at indifference (i.e. at ) whereas psychometric evidence typically finds that accuracy rates are -shaped in the difference between stimuli in unidimensional stimulus comparison tasks, and are therefore most sensitive to the differences between stimuli when they are close to equality (Woodrow,, 1933; Gescheider,, 2013).151515Our model can be seen as capturing the influence of both the integrated stimulus difference (the numerator in the value-dissimilarity ratio) as well as the complexity of comparing multidimensional stimuli (the denominator in the value-dissimilarity ratio) on accuracy rates. As such, we will also consider a three parameter functional form,

| (2) |

where the additional parameter governs the sensitivity of choice rates to around indifference. Note that when , (2) reduces to (1).

3 Experimental Tests

We test our proposed representations of comparison complexity against data from three analogous binary choice experiments in multiattribute, intertemporal, and lottery choice. We first provide an overview of the goals and design features shared across the three experiments, and then present domain-specific details along with results.

3.1 Overview

The goals of these experiments are two-fold. First, we want to show that our proposed complexity ratios capture the difficulty of comparisons. In particular, our theory predicts that (1) choice errors, (2) choice inconsistency, and (3) subjective uncertainty, three natural indicators of choice complexity, should all be decreasing in the value-dissimilarity ratio. We show that our ratios are highly predictive of all three. Second, we want to show that even in relatively simple decision contexts, our model captures quantitatively important features of choice that are missed by standard models. We show that despite having a comparable number of or in some cases far fewer free parameters, our structurally estimated choice model is able to explain observed choice rates 20-30% better than leading behavioral models in the domains of lottery and intertemporal choice, and predicts variation in choice not captured by the best-fit behavioral model in multiattribute choice.

We address these questions in three parallel experimental datasets. We run new experiments in multi-attribute and intertemporal choice and compile existing data from Enke and Shubatt, (2023) and Peterson et al., (2021) to study risky choice. In our experiments, we recruit participants through an online survey platform to make 50 incentivized binary choice problems. For each problem, we elicit participants’ subjective certainty in their response. In order to measure choice consistency, 10 of these problems are randomly repeated throughout the survey. We collect an average of 37 choices for each of 662 multi-attribute choice problems and 1,100 intertemporal problems – a total of more than 66,000 individual decisions. Our compiled risk dataset includes nearly 10,000 problems (over 1 million decisions) and includes similar measures of cognitive uncertainty and consistency.161616Cognitive uncertainty is elicited only for the 500 problems from Enke and Shubatt, (2023). Problems are only repeated in the Peterson et al., (2021) experiment. Unlike our experiments, subjects see these repeated problems immediately after giving an initial response.

3.2 Multiattribute Choice

We ask participants to identify the cheaper of two hypothetical phone plans characterized by either two, three, or four attributes. These attributes include a device cost, a monthly flat fee, a data usage fee, and a quarterly wi-fi fee. Participants learn about a fictional consumer with a fixed budget and are asked to choose the plan that will save the consumer the most money over one year. The consumer’s data usage is known, and so each problem has an objectively payoff-maximizing answer, allowing us to perfectly observe choice errors. For three-attribute problems, the budget is $700 and the average plan costs $621.171717The majority of our problems involve three attributes. For two-attribute problems, the budget is $480 (average cost $410). For four-attribute problems, the budget is $760 (average cost $688). We fix the plans’ value difference at one of two values ($46 or $69) so that variation in the ratio mostly reflects variation in option similarity. If a participant is selected to earn a bonus (1 in 2 chance), we select one of their choices at random and pay them 1/12 of the money they saved. These payments range between $4 and $9. For more detail on the design and pre-registration, see Appendix D.

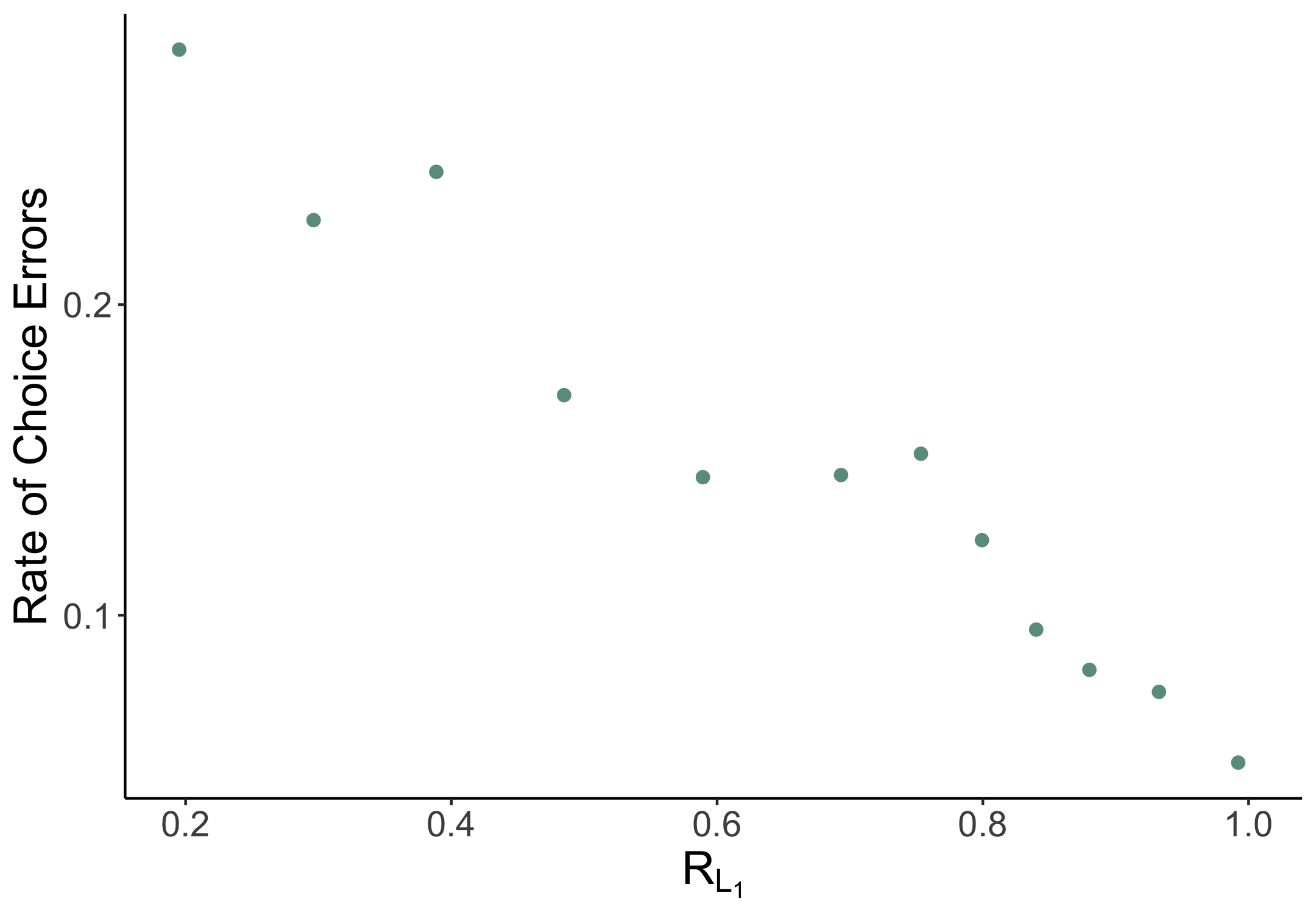

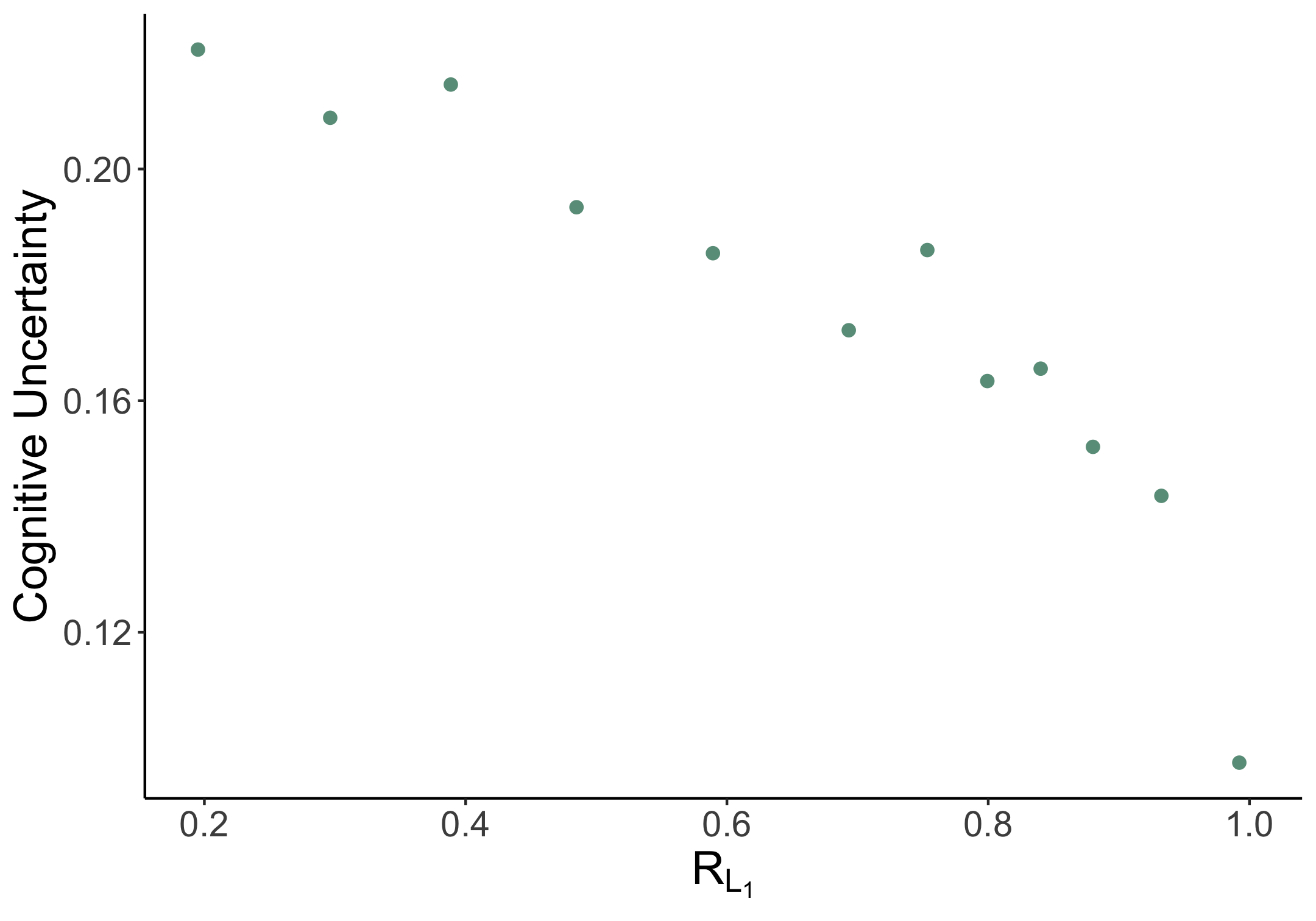

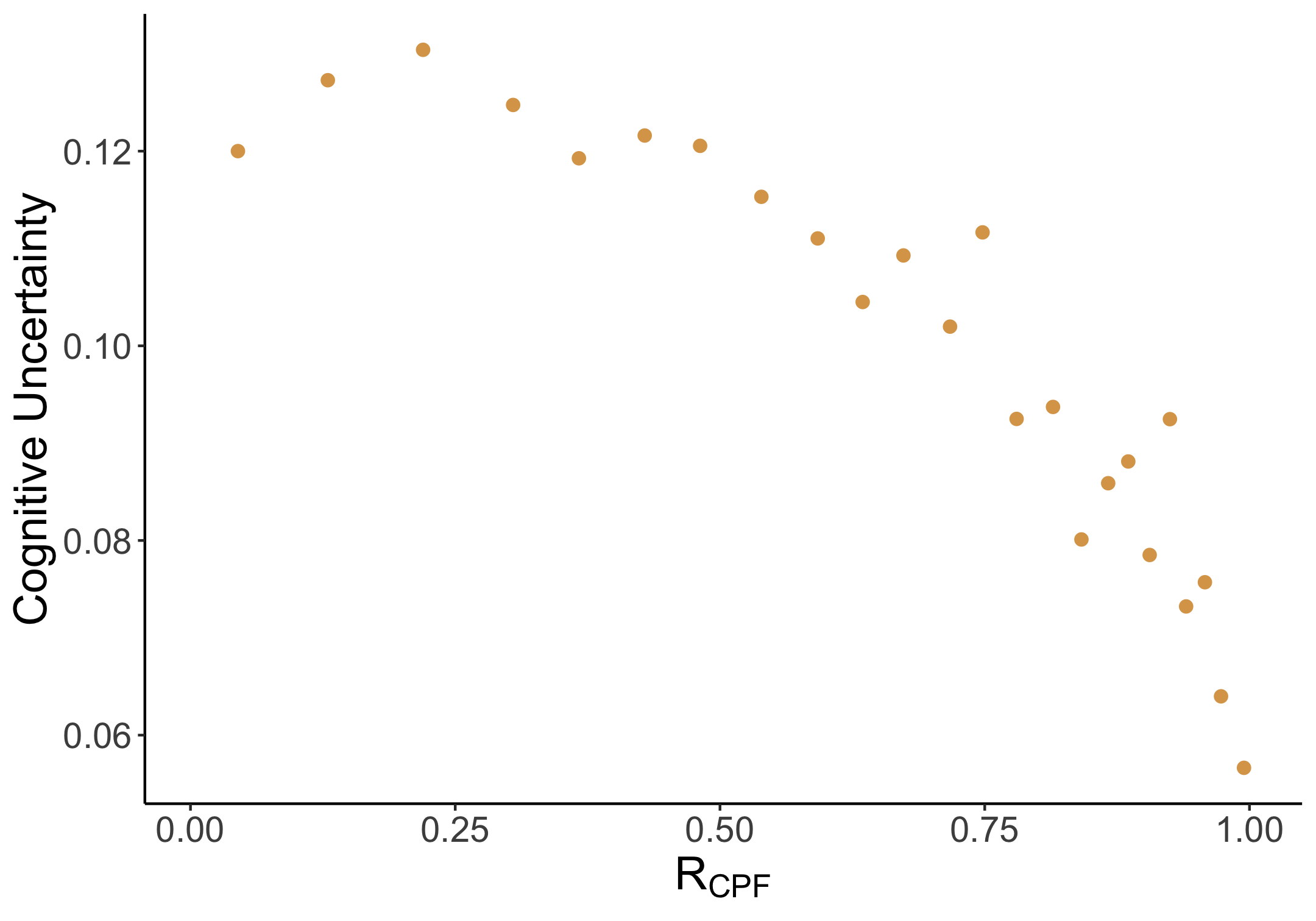

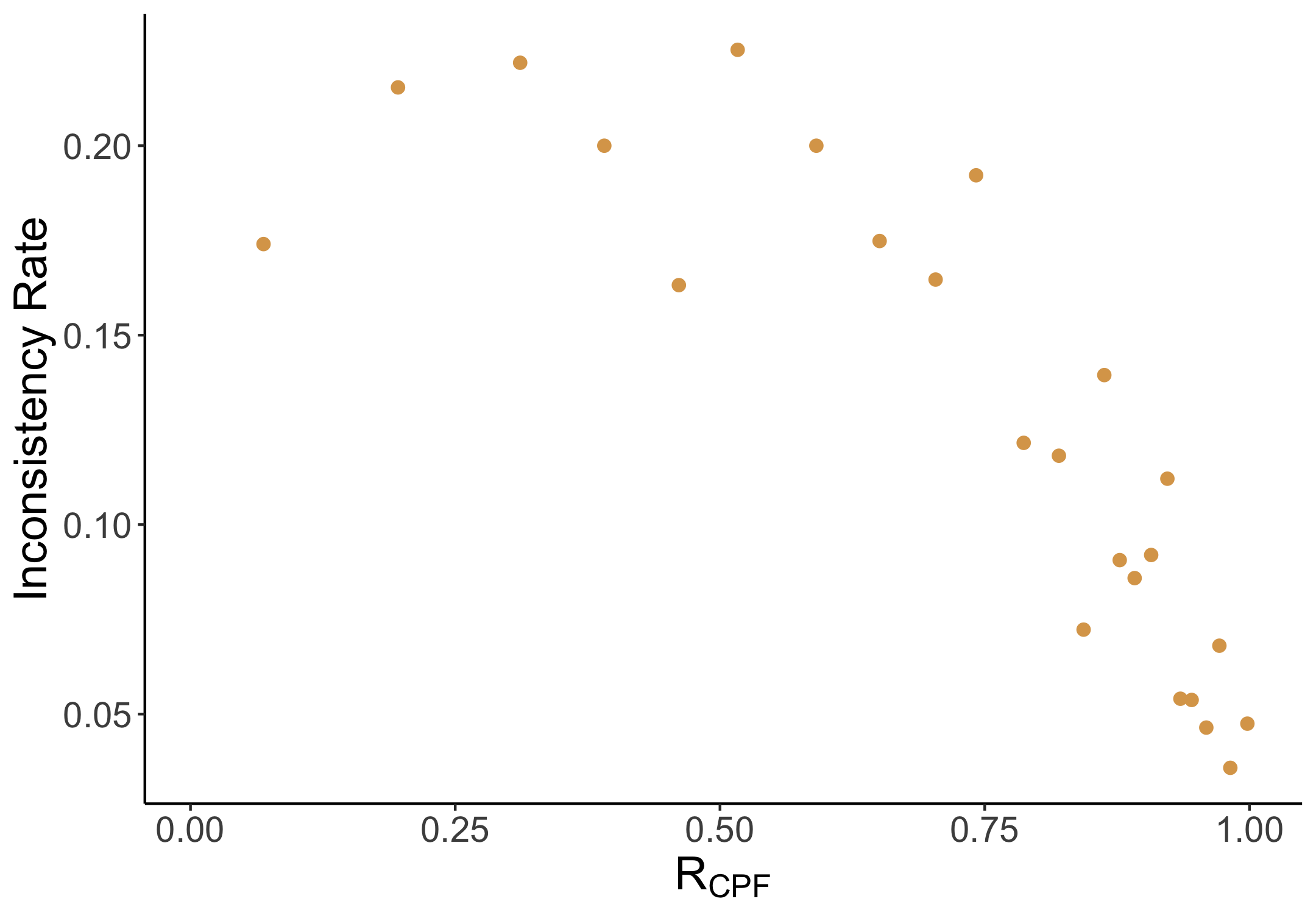

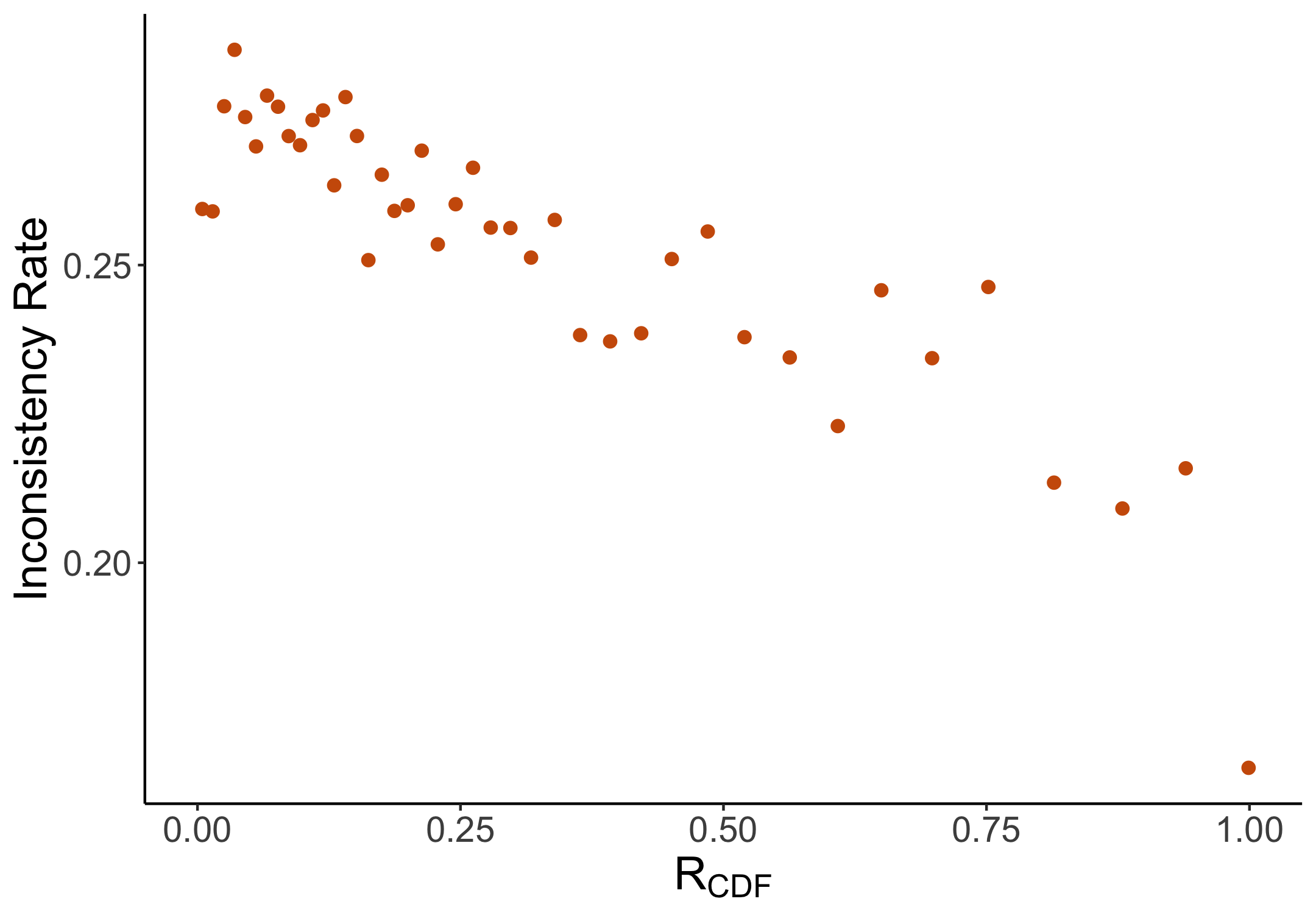

Figure 3 shows binned scatter plots relating the ratio (x-axis) to choice errors, cognitive uncertainty, and inconsistency. We see that all three are strongly decreasing in the ratio. The average error rate, only around 5% for problems near-dominance, increases five-fold for problems with the lowest values of the ratio (). We take this as strong evidence that (1) the ratio indeed captures cognitive complexity, and (2) decision-makers respond to this complexity by making more random choices.

Importantly, these relationships are not driven by variation in the value difference alone, but instead by variation in the ratio, which we varied independently of the value difference when constructing the choice problems. The regression evidence in Appendix Table 2 shows that the relationships above are unchanged when including controls for the value difference.181818Due to the concern of calculator usage in our experiment, we pre-registered analyses for the subsample of subjects who do not report using a calculator in the experiment, in addition to the full sample. Appendix Table 3 reports analyses restricting to this subsample of 407 subjects (82.5% of the full sample). The quantitative relationships in this subsample are virtually unchanged.

3.2.1 Benchmarking Performance

To study whether our theory explains variation in choice patterns that are not captured by existing behavioral models of multiattribute choice, we conduct a benchmarking exercise in which we structurally estimate our choice model, using the parameter specifications in (1) and (2), and compare its performance to leading behavioral multiattribute choice models, which we also structurally estimate on our data. We estimate three such models, each of which deliver accounts of how various biases lead to under- or overweighting of attributes in choice: salience-weighting (Bordalo et al.,, 2013), focusing (Kőszegi and Szeidl,, 2013), and relative thinking (Bushong et al.,, 2021), each with logit errors (see Appendix E.1 for details on the structural models).

Appendix Table 4 summarizes the estimation results. In predicting choice rates at the problem level, the fitted salience, focusing, and relative thinking models achieve values of .001, .001, and 0.35, respectively. Despite having one fewer free parameter than the relative thinking model, the two-parameter version of our choice model delivers a comparable of 0.29.191919As Table 5 documents, the three parameter version of our choice model yields an of 0.32. Importantly, our model explains a substantial amount of variation in choice data not captured by the relative thinking model; as Appendix Table 5 documents, when regressing actual choice rates vs. fitted choice rates under the relative thinking model, including the fitted choice rates under our choice model as an additional predictor results in an increase in from 0.35 to 0.41, a 19% increase in variance explained.

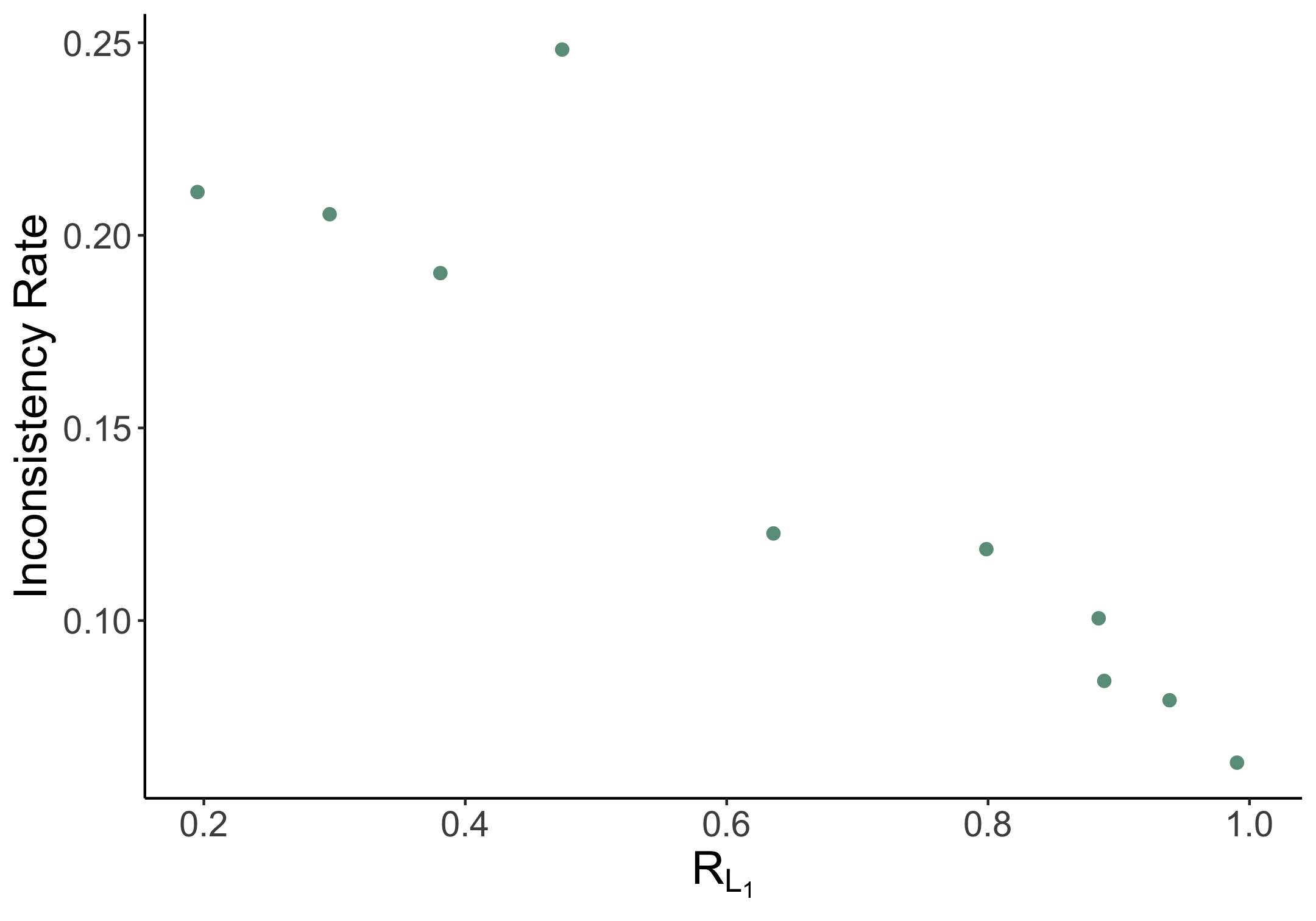

3.3 Intertemporal Choice

We ask participants to choose which of two time-dated payoff streams they would prefer to receive. Each option has one or two payoffs, ranging between $1 and $40, to be received at delays ranging between the present and 2 years in the future. If the subject wins a bonus (1 in 5 chance), they will actually receive one of the payment streams they selected on the specified dates. For more details on the design and pre-registration, see Appendix D.

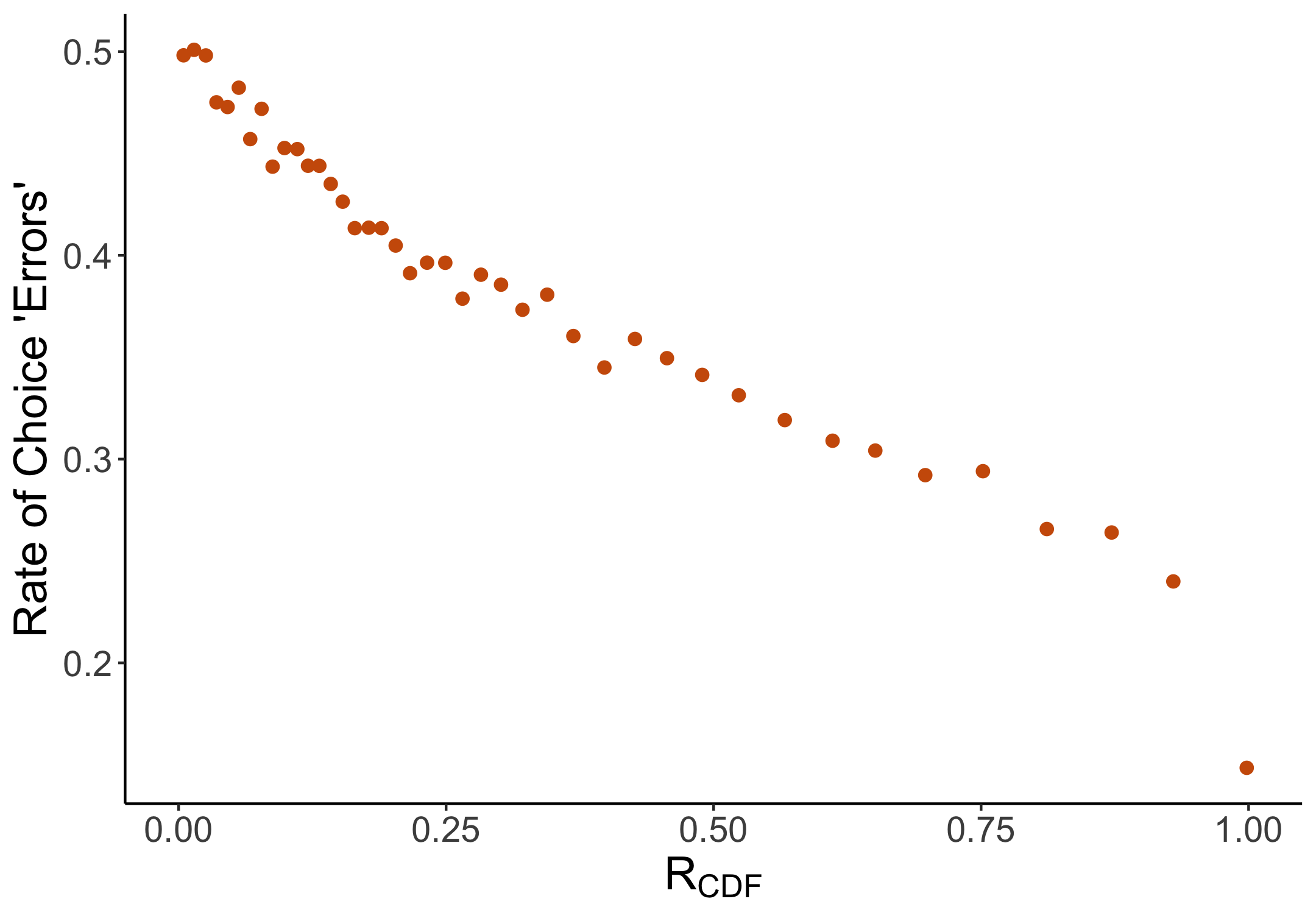

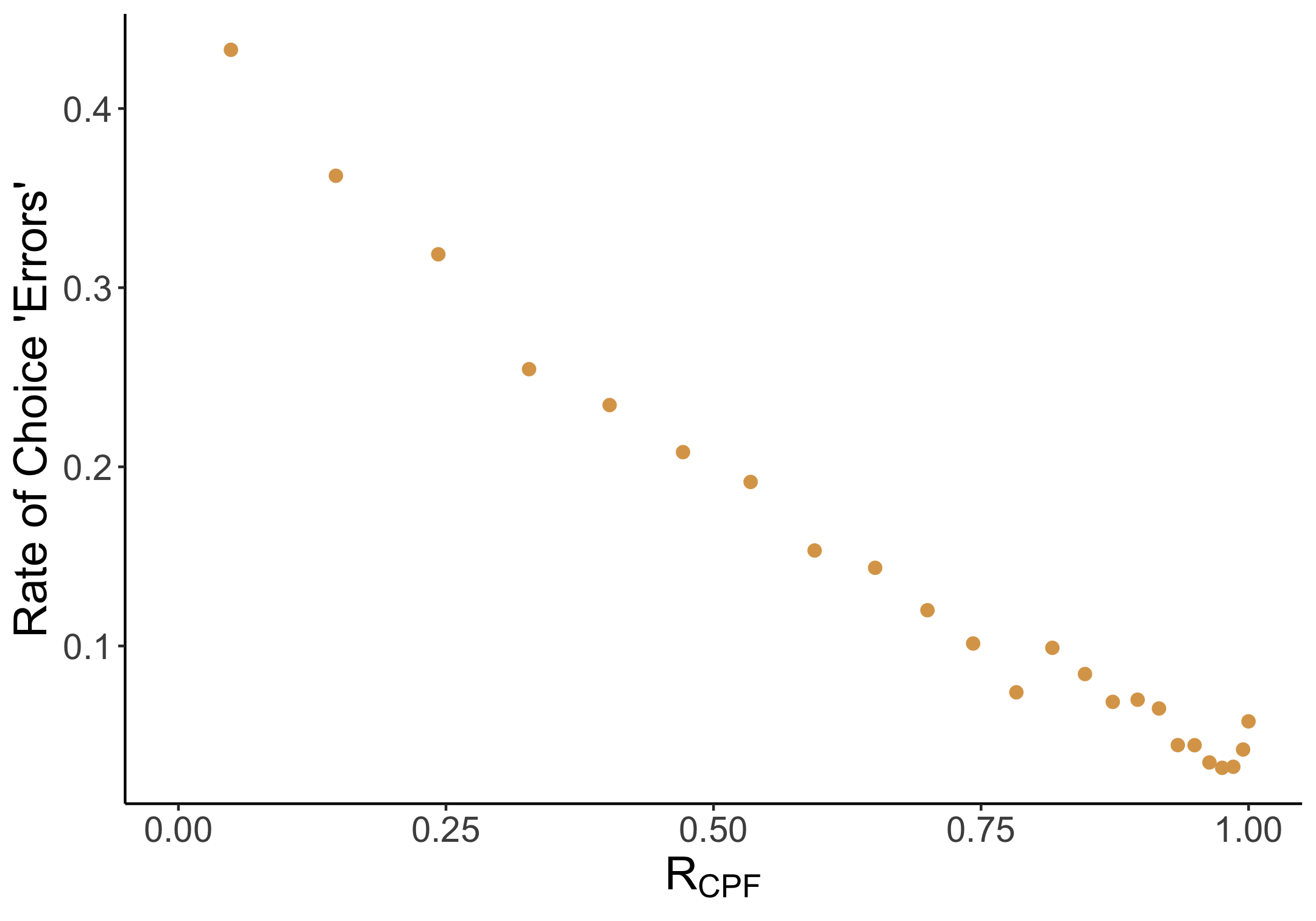

Unlike in multi-attribute choice, we cannot observe choice errors here – the definition of an “error” depends on the decision-maker’s discount function, which is unknown. The CPF ratio also depends on this discount function, so we proceed by experimentally estimating a representative agent exponential discount factor from the choice data. We estimate the choice model with additive logit errors, which yields a monthly discount factor of 0.93. For details on the specification, see Appendix E.1. In Figure 4, we present the main results from the intertemporal experiment. Here, a choice is coded as an “error” if an individual chooses the option with lower present value according to the estimated discount factor. As in our multiattribute choice data, we find very strong relationships between the CPF ratio and choice “errors,” cognitive uncertainty, and inconsistency. The average "error" rate ranges from around 5% for problems with the highest value of the CPF ratio to 50% for problems with the lowest value of the CPF ratio (. As the regression evidence in Appendix Table 6 documents, these relationships are virtually quantitatively unchanged when controlling for the value difference, which indicates that the ratio between the value difference and our proposed dissimilarity measure — as opposed to the value difference alone — is driving these relationships.

3.3.1 Heterogeneity

In principle, the “errors” plotted in Figure 4(a) could reflect heterogeneous preferences. The inconsistency and cognitive uncertainty results suggest that this cannot be the entire story, as these measures are all within-subject, and do not depend on estimated preferences. Moreoever, we can perform the error analysis using individual-level discount factors , which we estimate using the 50 choices observed for each subject. Using these individually estimated discount factors, we find a similarly pronounced relationship between the CPF ratio and apparent errors (see Appendix Figure 10 and Table 7).

3.3.2 Benchmarking Performance

While Figure 4 indicates that our model is a good descriptor of choice, but leaves open the question over whether the value-dissimilarity ratio explains meaningful variation in choice behavior that is not captured by other models. To this end, we conduct a benchmarking exercise analogous to that in Section 3.2.1 in which we structurally estimate our choice model, using the parameterization specified in (1), and compare its performance to leading intertemporal choice models. We estimate two such models: standard exponential discounting and hyperbolic discounting, both with logit errors (see Appendix E.2 for details on the structural models). In predicting choice rates at the problem level, these models achieve values of 0.75 and 0.78 respectively. In contrast, our model achieves an of 0.88 – a 13% improvement in variance explained over hyperbolic discounting, using the same number of parameters. Appendix Table 8 summarizes the estimation results.

3.4 Lottery Choice

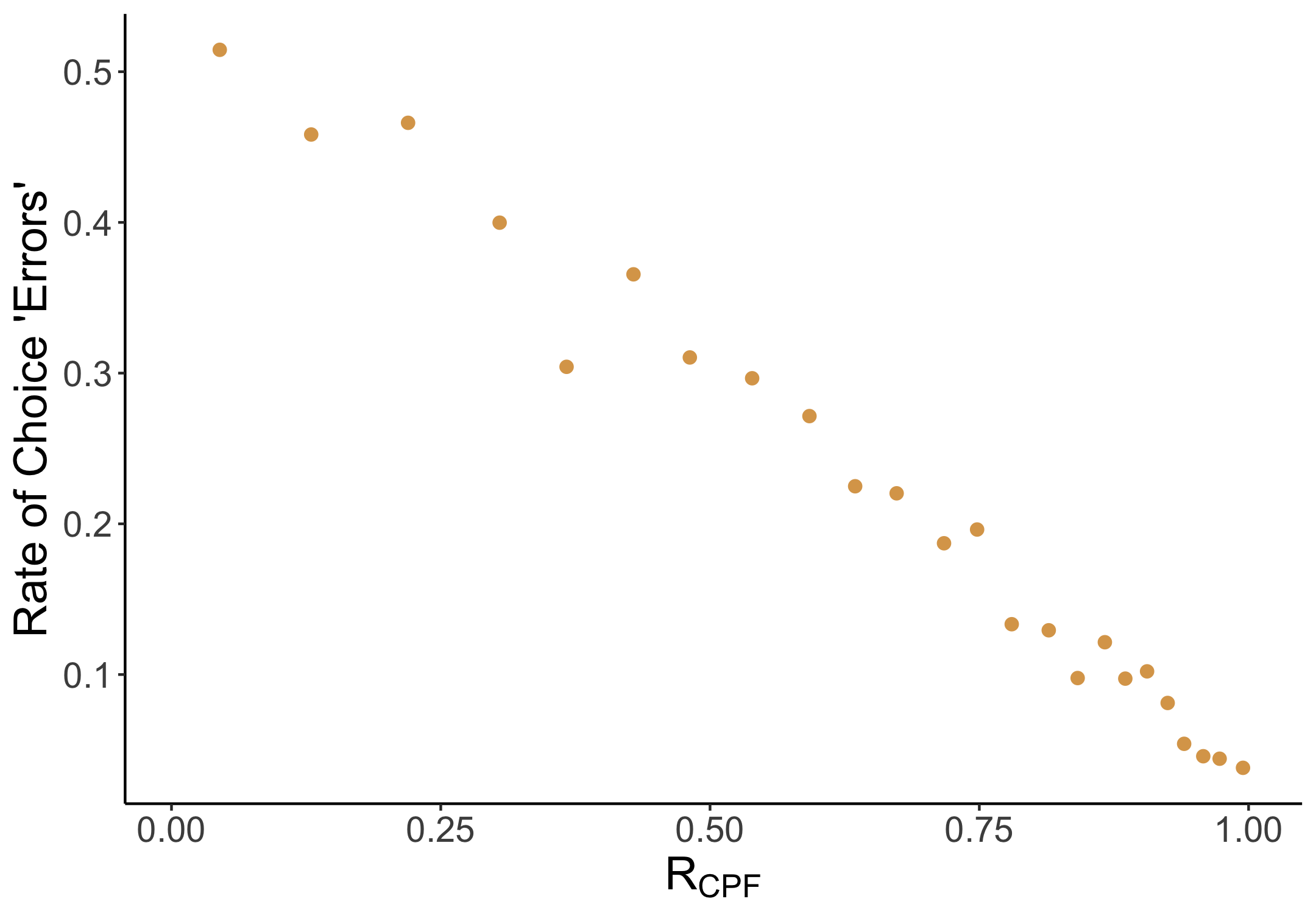

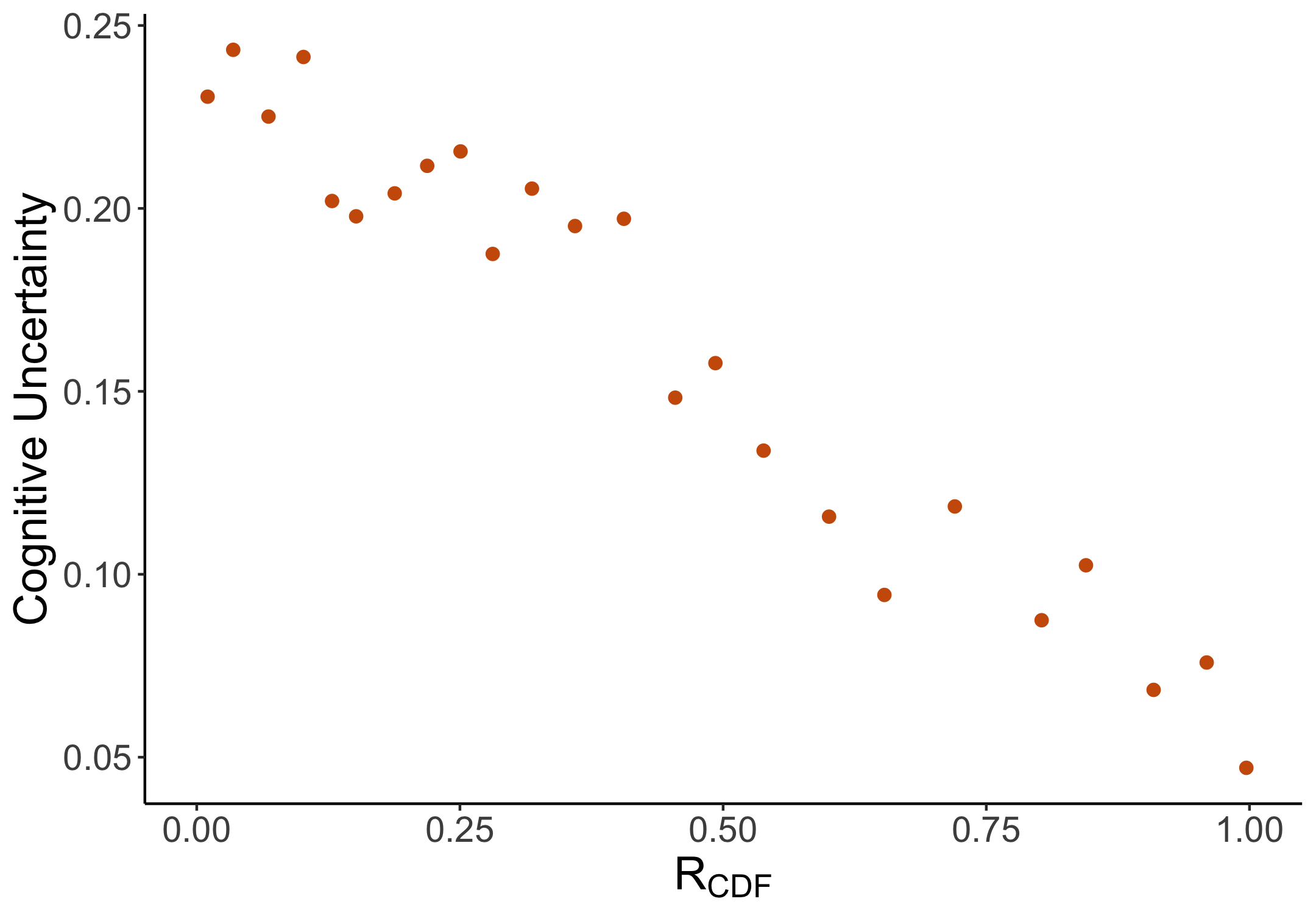

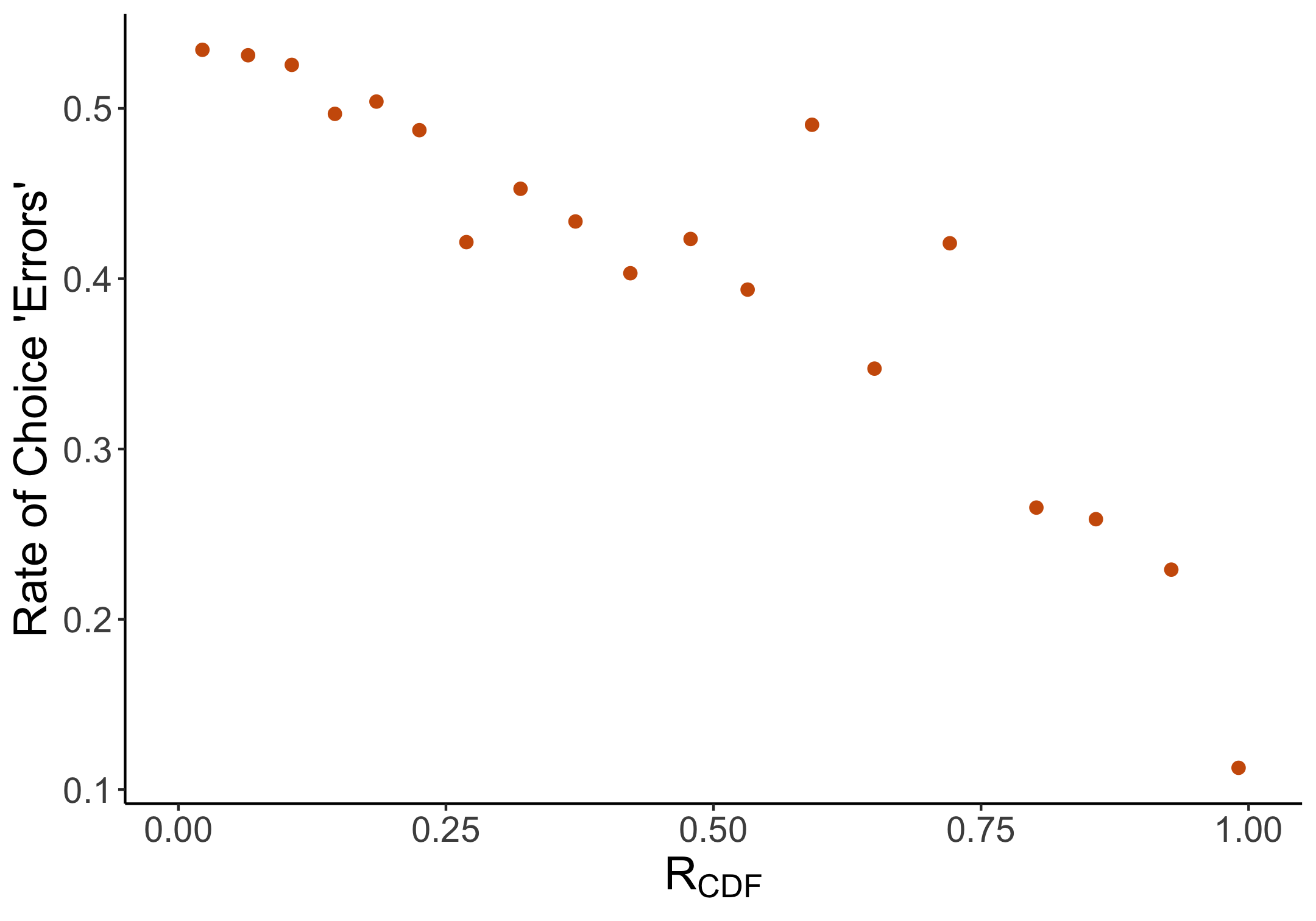

In both lottery choice experiments, participants were asked to choose between two lotteries which pay off different amounts with known probabilities. If participants were selected to receive a bonus, the computer would simulate one of their chosen lotteries and actually pay out the simulated value. As in intertemporal choice, both the CDF ratio and our notion of choice “errors” depend on an unknown preference parameter – the Bernoulli utility function. We proceed by estimating a representative-agent model of CRRA utility with additive logit errors (see Appendix E.3 for details), and code “errors” as departures from this estimated model. Figure 5 shows the results. Once again, all three outcomes are strongly decreasing in the ratio; in particular, the CDF ratio achieves an of 0.45 in variance explained over error rates. Consistent with our results in our other two domains, these relationships are driven by the value-dissimilarity ratio, as opposed to the value difference alone: as Appendix Table 9 demonstrates, the relationships below are quantitatively similar when including controls for the value difference.

3.4.1 Heterogeneity

As in intertemporal choice, we can recreate the error analysis using individual-level risk aversion parameters , which we estimate using the 50 lottery choices observed for each individual in the data collected in Enke and Shubatt, (2023).202020We restrict this analysis to the data in Enke and Shubatt, (2023) since the data in Peterson et al., (2021) contains too few unique choice problems for each subject to allow for estimation of individual-level risk preferences. Using these individually estimated risk aversion parameters, we find if anything a stronger relationship between the CPF ratio and apparent errors (see Appendix Figure 11 and Table 10).

3.4.2 Benchmarking Performance

As with intertemporal choice, our model explains significant variation in choice rates uncaptured by existing rational and behavioral choice models. To benchmark performance, we estimate a standard reference-dependent expected utility model as well as a full prospect theory model with loss aversion (see Appendix E.3 for details). We compare the performance of these models to two versions of our CDF complexity model, both of which use the paramterization of specified in (1): one that assumes risk neutral preferences, and one that allows for utility curvature, jointly estimated along with the parameters for (see Appendix E.3 for details).

Appendix Table 11 summarizes the estimation results. In predicting choice rates at the problem level, reference dependent expected utility and prospect theory achieve values of 0.56 and 0.59 respectively. Despite having four fewer parameters than prospect theory, the risk-neutral version of our model achieves an of 0.66 – a 12% improvement in variance explained over prospect theory. This is in line with results from Enke and Shubatt (2023), who find that allowing complexity to enter the noise term of a logit choice model substantially improves performance over standard models.212121The “complexity index” developed by Enke and Shubatt loads heavily on “excess dissimilarity,” which is tightly connected to our ratio: it is exactly equal to the denominator of the CDF ratio minus the numerator, assuming risk-neutral preferences. Adding an additional parameter to capture utility curvature in our model yields an of 0.73 – a 24% improvement in variance explained over prospect theory.

4 Multinomial Choice

We have thus far focused on comparison complexity in binary choice. We now extend our model to multinomial choice and show how comparison complexity can rationalize a range of documented anomalies in choice and valuation, such as context effects, preference reversals, and apparent biases in the valuation of risky and intertemporal prospects.

4.1 Multinomial Choice Extension

Consider the same setting as in our binary choice framework. There is a set of options , and the DM has continuous, iid priors over for all , distributed according to a symmetric distribution . Let denote the collection of finite subsets of , and let denote the set of finite menus. The DM faces a choice problem , comprised of a menu of options and a choice context – a set of options the DM observes but cannot choose, i.e. phantom options. The DM chooses from based on signals on how each pair of options in compare.

In particular, for each pair of distinct options , the DM observes a signal of the form

Letting denote the collection of these signals, the DM chooses the option with the maximal posterior expected value . We are interested in the resulting choice probabilities in a choice problem, which are given by222222This formulation for holds when ties in posterior expectations occur with probability 0. In the case of ties, we assume a symmetric tiebreaking rule. See Appendix B.3 for details.

Note that the restriction of this choice model to binary choice problems, i.e. such that and , is exactly the binary choice model studied in Section 2. With some abuse of notation, we will let denote binary choice probabilities, and let denote binary choice probabilities given a choice context .

Discussion of model properties.

As this model extends our binary choice framework, it delivers the prediction that binary choices are unbiased – that is, the DM always picks the higher-valued option weakly more often in binary choice problems.232323In particular, our model satisfies the Weak Transitivity condition, which says if , then In choice from larger menus, however, the presence of comparisons to other options in the menu or choice context can lead to systematic distortions in choice.

To illustrate, consider an example where , with and where , . That is, the DM has no idea how compares to and , but knows that is better than . Here, the model predicts that – the presence of in the choice context provides additional information that rules out posterior beliefs over in which , thus distorting the the DM’s choice in favor of the inferior option . In Section 4.2, we show how the model can rationalize a number of documented context effects using this logic.

To apply the choice model in a given domain, the analyst needs to specify the ranking of the choice options according to as well as the precision parameters . While these primitives can be identified using binary choice behavior, as we show in Appendix B.4, our approach in the remainder of this section will be to discipline the model using our theory of comparison complexity, which pins down the primitives and in the domains of multiattribute, lottery, and intertemporal choice.

Relationship to Existing Models.

Our model belongs to class of menu-dependent learning models

(e.g. Safonov,, 2022; Natenzon,, 2019), in which the DM chooses based on a signal that depends on the menu that she faces. One model in this class that warrants discussion is the Bayesian Probit model in Natenzon, (2019). In this model, the DM has

i.i.d. Gaussian priors over , and chooses based on signals received for each option in the menu, where the are jointly normal across options. The pairwise correlations of allow the model to capture a notion of the ease of comparability between choice options, where choice options are more easily comparable if are more highly correlated.

Recall that in our model, the DM only receives information on ordinal value comparisons. In Bayesian Probit, the DM learns about the cardinal value differences between choice options, which rules out certain intuitive choice patterns. For instance, consider the the following choice options in the multiattribute domain:

Since is dominated by both and , we might expect that and also ; that is, the DM does not err in the presence of dominance but finds tradeoffs across attributes difficult. Bayesian Probit cannot rationalize this choice data; implies that ,242424This analysis assumes that the global precision parameter . If instead , we will also have the prediction that . which implies . This yields the counterfactual prediction .

Intuitively, in Bayesian Probit the DM receives information on the cardinal value difference between choice options. As such, when the Bayesian Probit DM perfectly learns the cardinal value differences and , they also learn the value difference . In our model, on the other hand, the DM only receives information on the ordinal value comparison between choice options, which allows for situations in which the DM perfectly learns that and , yet remains uncertain regarding the ranking between and .

4.2 Context Effects

In our model, the presence of other options in the choice context can generate information that distorts choice, even if these options are never chosen. The following proposition summarizes this prediction.

Proposition 2.

Let . If , there exists such that if , .

Proposition 2 says that when an inferior option is easier to compare to than to , the presence of in the choice context will distort choice in favor of if and are sufficiently hard to compare.252525In Appendix C, we also consider the analogous result that the addition of a superior option to the choice context can bias choice in favor of if . Intuitively, if the DM does not know how compares to or , but learns that is in fact better than , the presence of can push choice in favor of – even when is strictly better than . When combined with our theory of comparison complexity in the multiattribute domain, the above result rationalizes familiar decoy and asymmetric dominance effects.

Corollary 2.1.

Consider options from , with and let have an -complexity representation. Let .

-

(i)

If , then implies .

-

(ii)

For any value difference , there exists such that if , there exists with such that .

Part (i) says that if and are indifferent, then introducing an inferior phantom option that is more similar to than distorts choice in favor of . Part (ii) says this distortion does not just arise at indifference: if and are sufficiently dissimilar relative to their value difference, there exists a decoy that distorts choice in favor of .

Example 1.

(Classic decoy effects). Consider a setting where options have two attributes, where , and where has an complexity representation. Consider two indifferent choice options , , and consider the effect of including a phantom option on choice shares between and .

Case 1: . Since , we have . We recover the classic asymmetric dominance effect: the addition of an option that is dominated by the target option but not by the competitor distorts choice in favor of .

Case 2: . We again have , we have . Here, the model predicts a “good deal" effect – is not dominated by either or , but its proximity to makes the target option seem like a “good deal" relative to , whereas its distance to prevents the DM from drawing the same inference about the competing option.

Case 3: . Here, , and so Corollary 2.1 implies that . That is, the model predicts that the addition of a mutually dominated option does not affect choice shares.

Comparison to other context-dependence models. Though each of the choice patterns above can be explained by familiar models, our model is distinct in simultaneously explaining all three. The salience (Bordalo et al.,, 2013) and focusing models (Kőszegi and Szeidl,, 2013) cannot rationalize the decoy effects in Cases 1 and 2. The relative thinking model (Bushong et al.,, 2021), in which the DM weighs a given change along an attribute by less when there is a larger range of values along that attribute, can rationalize the decoy effect in Case 1 as a result of option extending the range of attribute 2 more than attribute 1, but not Case 2, where has no effect on attribute ranges. The pairwise normalization model (Landry and Webb,, 2021) predicts that increases the relative of relative to whenever is closer to than it is to , and so can rationalize the decoy effects in both Cases 1 and 2, but also delivers the counterfactual prediction that the addition of a mutually dominated option will also distort choice in favor of . Furthermore, all of these models are formulated in multi-attribute choice, which means they cannot easily explain documented decoy effects in lottery choice (Soltani et al.,, 2012) or other domains. Our choice framework straightforwardly applies to lottery and intertemporal choice.

We also make an important conceptual distinction from these existing models. In our model, biased choice does not arise from a behavioral bias, but instead as a rational response to imperfect comparability. We only expect decoy options to distort choice between and when their binary comparison is challenging. This is consistent with the fact that the attraction effect is muted when consumers face familiar choice contexts or have clear prior preferences (Huber et al.,, 2014) – an empirical phenomenon that is not well-explained by existing models.

4.3 Biases and Instabilities in Valuation

Consider the classic preference reversal phenomenon in risky choice. Lottery pays a high amount with a low probability, while pays a modest sum with a high probability, e.g.

We consistently see that most subjects choose over in direct choice between the two, but state a higher certainty equivalent for when valuing the two lotteries independently. A number of explanations for these apparent preference reversals have been put forth in the literature, such as intransitive preferences or violations of independence (see Seidl, (2002) for a review). Our model makes two simple predictions which together rationalize preference reversals. First, valuations are systematically biased when options are difficult to compare to money; and second, some options are easier to compare to money than others.

4.3.1 Modeling Valuations

To model valuations, we extend our multinomial choice framework as follows. The DM now faces a finite menu sequence in a choice context , generates a set of signals for each pairwise comparison in and chooses the option from each menu with the highest posterior expected value, yielding the joint choice frequencies262626As before, this formulation for choice probabilities holds when ties in posterior expectations occur with probability 0. In the case of ties, we assume a symmetric tiebreaking rule; See Appendix B.3 for details.

where records the frequency of choosing for .

We model valuations within this extended choice framework as follows. There is an option to be valued, and a price list : a set of options for which the ranking is unambiguous, i.e. for all . The DM faces a valuation task : a sequence of binary choices between and each price in the price list: that is DM faces a menu sequence given the choice context . Note that this choice procedure corresponds to a multiple price list, a workhorse procedure for eliciting valuations in experimental economics.

Since the DM perfectly learns the ranking of prices, this choice procedure yields a single switching point: that is, for any signal realization there is an index for which the DM chooses the option for all , and the price for all . Just as the switching point in a multiple price list is taken to reveal the subject’s valuation of , this switching point reveals where the DM believes the object falls within the ranking of prices. We will be interested in the distribution over these switching points induced by , which we denote by .272727Given a signal , the DM’s posterior switching point is computed by calculating and for all , and finding the unique index such that and (in the case of ties, we assume the DM randomizes as described in Appendix B.3).

For notational convenience, let and denote the value of and ease of comparison between and , respectively.

Constant comparability. Our model predicts that when is hard to compare to prices, valuations will exhibit a “pull-to-center” effect – they will in general be systematically biased towards the middle of the price list. To illustrate, consider a case where the ease of comparison between and prices is constant in . For ease of exposition, assume that is not indifferent to any price in , so that there is a true ranking such that if and otherwise.

Proposition 3.

Given a valuation task , where and for all , we have the following:

-

(i)

If , .

-

(ii)

As , converges in distribution to .

Proposition 3 says that i) when is incomparable to prices, valuations are compressed to the middle of the price list, and that ii) as becomes increasingly comparable to prices, valuations converge to the truth. Intuitively, if , the DM receives no information on where falls within the ranking of prices – her posterior puts equal probability on each possible ranking, and so she values in the middle of the price list. However, as increases, the DM’s valuation of becomes increasingly accurate, and eventually converges to the truth. When combined with our theory of comparison complexity, this “pull-to-center” force can rationalize documented preference reversals and apparent biases in valuation.

4.3.2 Classic Preference Reversals

Lottery Choice. Consider the lottery domain, where for strictly increasing, and where has a CDF-complexity representation for which ; that is, the DM perfectly learns the ranking between two lotteries that have a dominance relationship. We show how our how our model can rationalize documented preference reversals.

Example 2.

(Classic preference reversals). Suppose the DM is weakly risk-averse, i.e. is concave, and consider the lotteries

First, consider a DM tasked with choosing directly between these two lotteries. Since any risk-averse DM weakly prefers to , our choice model predicts that : the DM is more likely to choose over in direct choice.

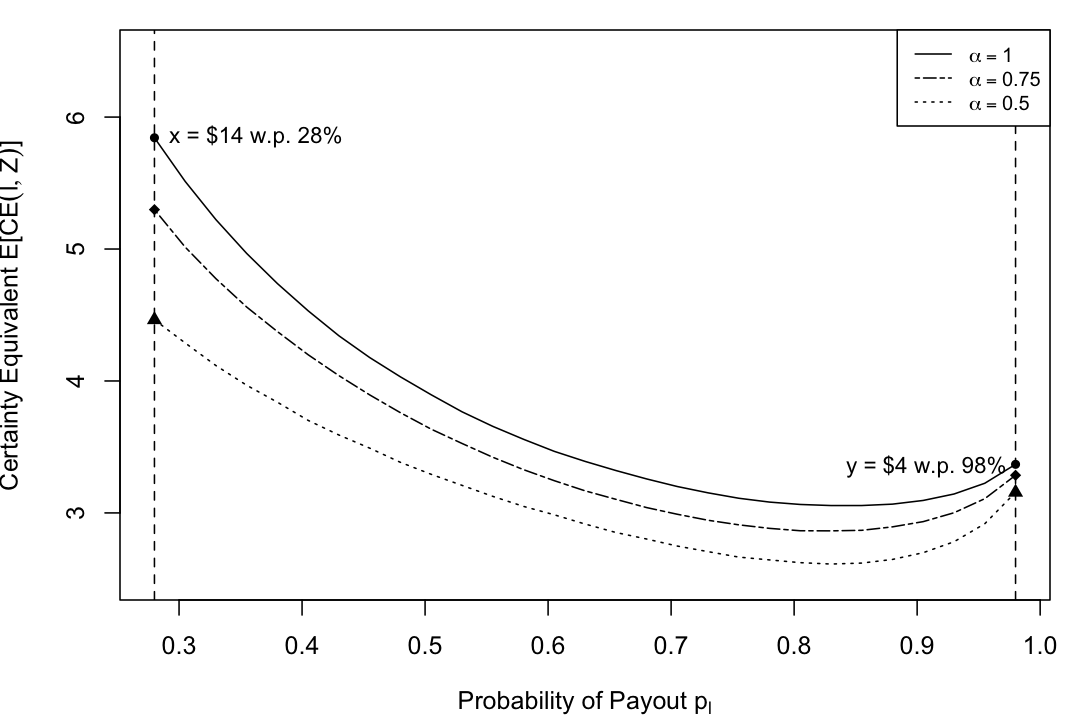

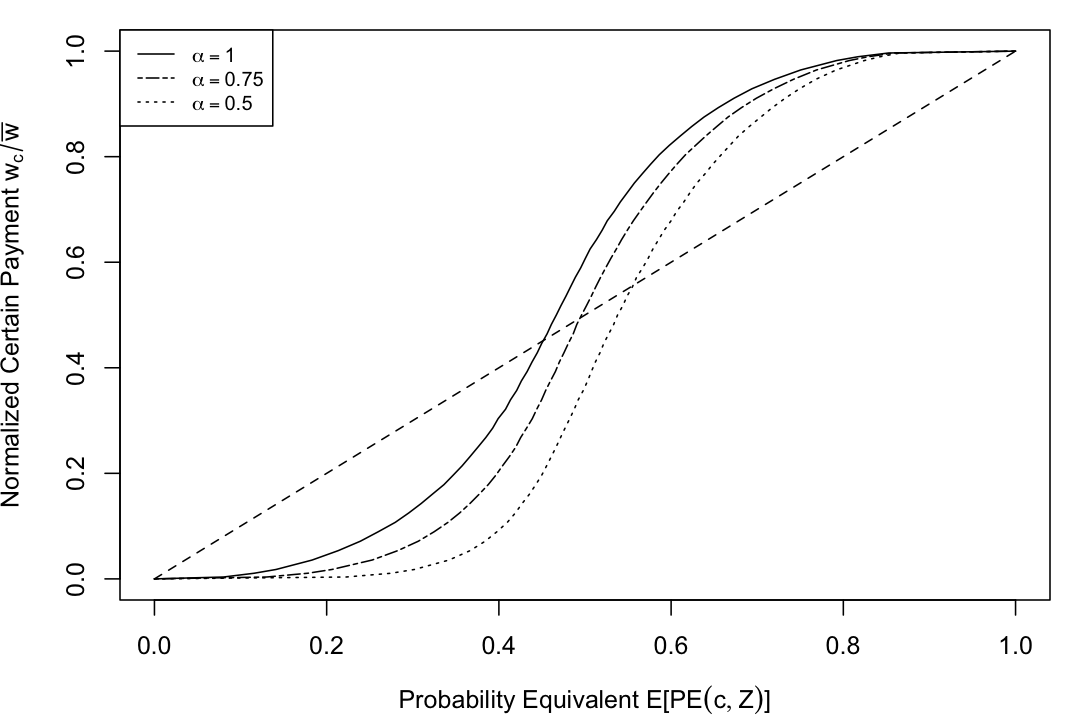

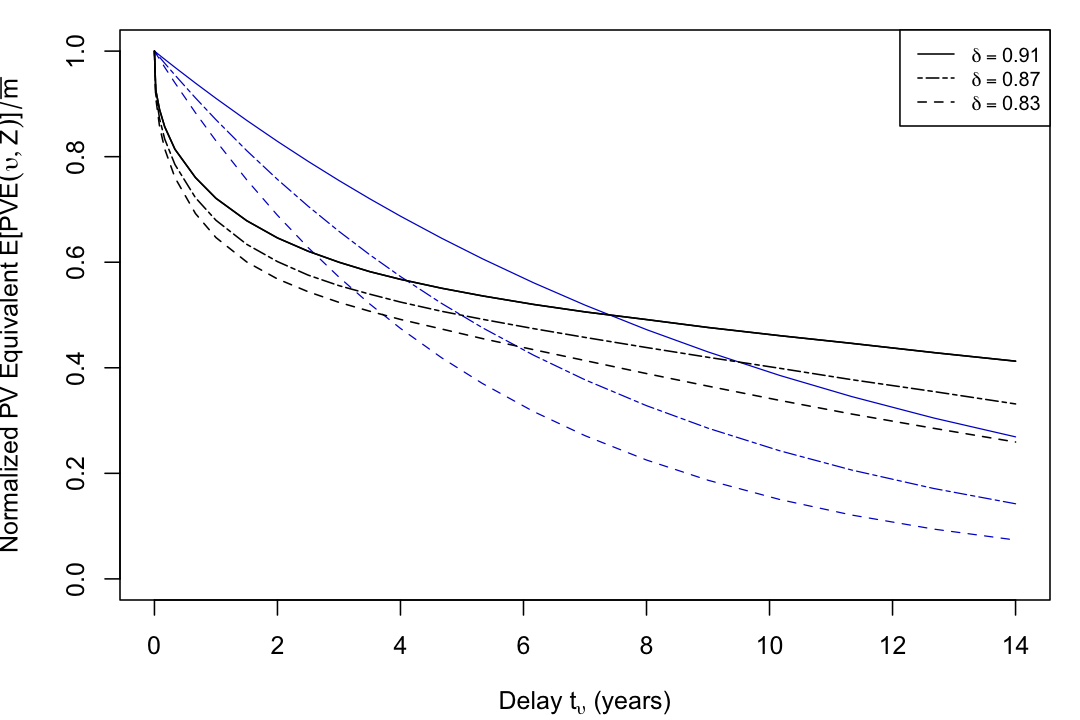

Now consider a DM tasked with producing a certainty equivalent for each lottery. Note that under , the two lotteries differ in their ease of comparison to money: , which is more dissimilar to a certain payment than , is harder to compare to money than . This differential ease of comparison, in conjunction with the pull-to-center effects described in Proposition 3, result in distortions that can cause to be valued higher than .

Formally, the DM faces a valuation task , where is a simple lottery that pays out with probability , to be valued against a price list , where each is a degenerate simple lottery. We make restrictions on that are commonly employed in the experimental literature: call a price list adapted to a simple lottery if is composed of composed of equal-sized steps, i.e. is constant in , and also contains the minimal and maximal support points of , i.e. and . Recall that each valuation task produces a distribution of switching points . Let denote the distribution over the DM’s certainty equivalents obtained from assigning each realized switching point to a valuation at the midpoint of the adjacent prices.282828Since we assumed , it is never the case that or , i.e. the DM never values the lottery below 0, or above the maximal price, and so is well-defined.

Figure 6 plots the expected certainty equivalents for simple lotteries with the same expected value as and , simulated from our model with CRRA preferences.

First consider the certainty equivalents of and , which correspond to the intersection of each curve with the vertical dashed lines in Figure 6: although is weakly preferred to since the DM is risk-averse, the model predicts that is valued higher than on average. The intuition is as follows: since the low-probability lottery is dissimilar to and therefore difficult to compare to money, its valuation is pulled to the midpoint of the undominated range of prices , and so the valuation of is inflated. On the other hand, since the high-probability lottery is easier to compare to money its valuation will exhibit a lower level of bias and if anything will be distorted downwards towards the midpoint of undominated prices . As such, our model rationalizes preference reversals, where and yet .

The entirety of the figure traces our model’s predictions for preference reversals in general: for with a modest payoff probability and with a high payoff probability, we will have for with a high payoff probability — despite the fact that is in truth preferred to , and so .

In our model, preference reversals result from the differential ease of comparing lotteries to money. This suggests that one may be able to eliminate or even reverse the direction of these effects by changing the numeraire: the currency against which the lotteries are valued.

Example 3.

(Reversals with probability equivalents). For instance, consider the same lotteries and from Example 2, and imagine that instead of valuing and in terms of money, the DM is asked to assess the probability-equivalents of the lotteries: the probability that makes the lottery indifferent to and .

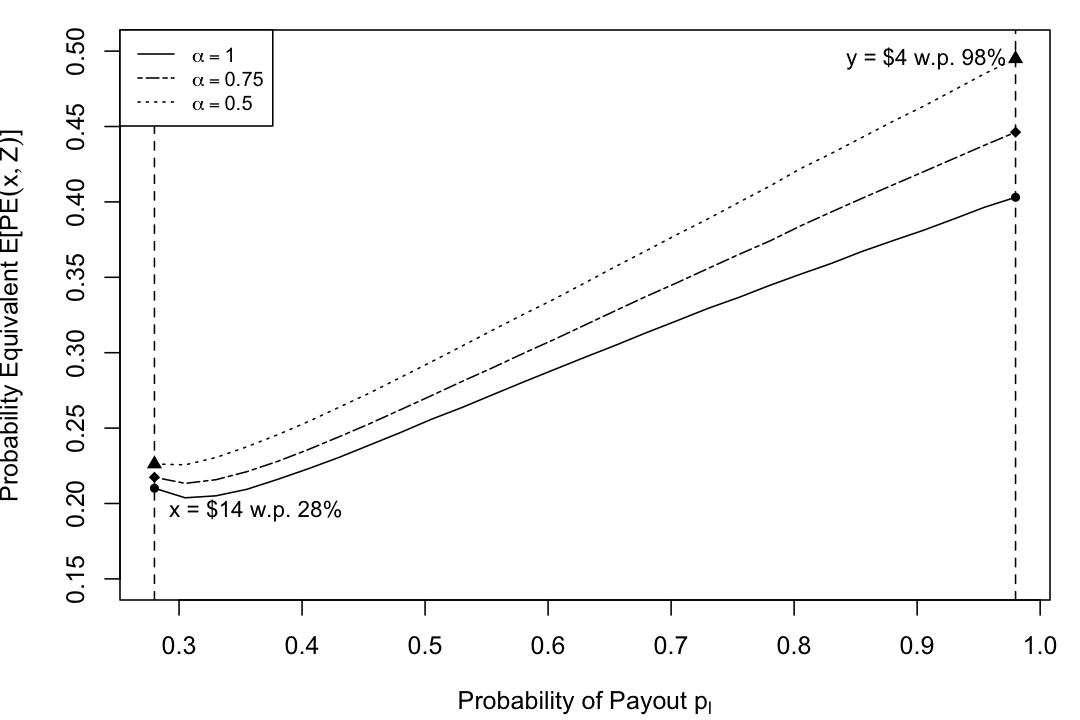

Whereas was easier to compare to money, is now easier to compare to the new numeraire. Our model predicts that this change in numeraire reverses the distortion in the valuation of and .

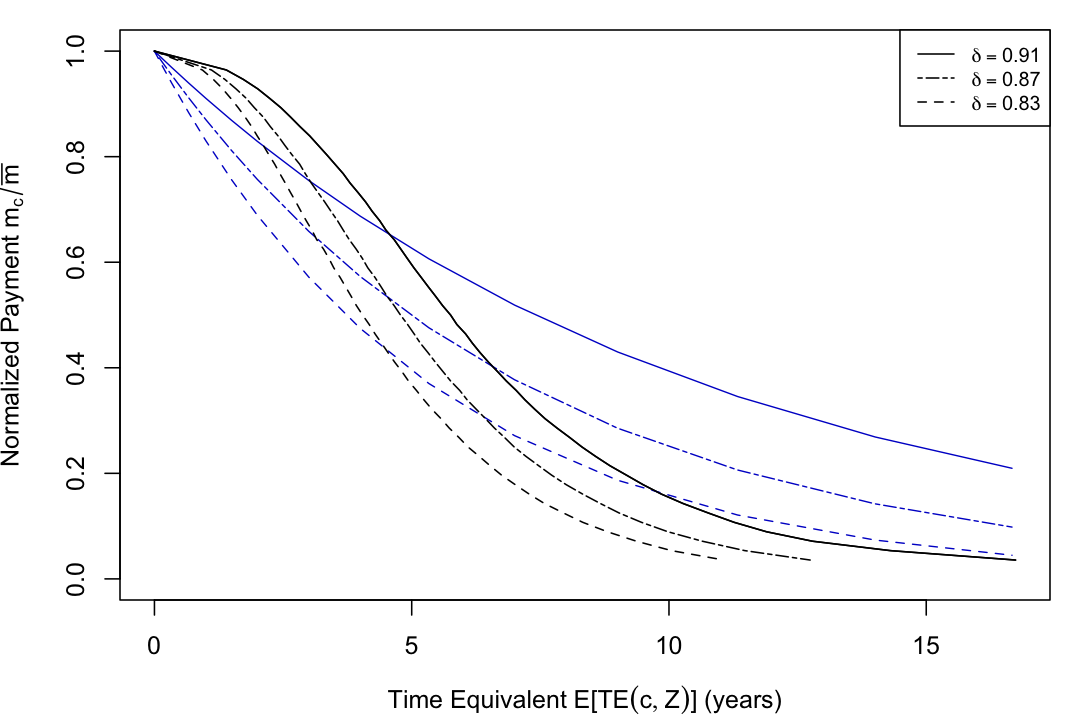

Formally, rather than valuing a simple lottery against a price list, the decision-maker now values against a probability list , where each .292929We assume that . Analogous to the restriction made in Example 2, call a probability list adapted to if is constant in and , . Analogous to before, let denote the distribution over the DM’s probability equivalents, obtained from assigning each switching point to a probability equivalent at the midpoint of the adjacent probabilities.

Figure 7 plots the expected probability equivalents , simulated from our model with CRRA preferences, for the same set of lotteries as in Figure 6: simple lotteries with the same expected value as and ,

Consider the probability equivalents of and , given by the intersection of each curve with the vertical dashed lines in Figure 7. Whereas was valued higher than on average when valued in terms of certainty equivalents, our model predicts that the distortion in valuations reverses when the lotteries are valued in terms of probability equivalents: we have . Intuitively, is hard to compare to the , so its valuation is compressed upward towards the middle of the range of undominated probabilities , whereas is easy to compare to , and so its valuation will be close to the truth.

Importantly, even though valuation using probability equivalents reverses the distortions responsible for preference reversals in this example, our model does not predict that valuations using probability equivalents are systematically more accurate than certainty equivalents. To see this, focus on the predictions of the model in the case of risk neutral preferences. Here, both methods of valuation are subject to bias: and are indifferent in truth, and yet we have and .

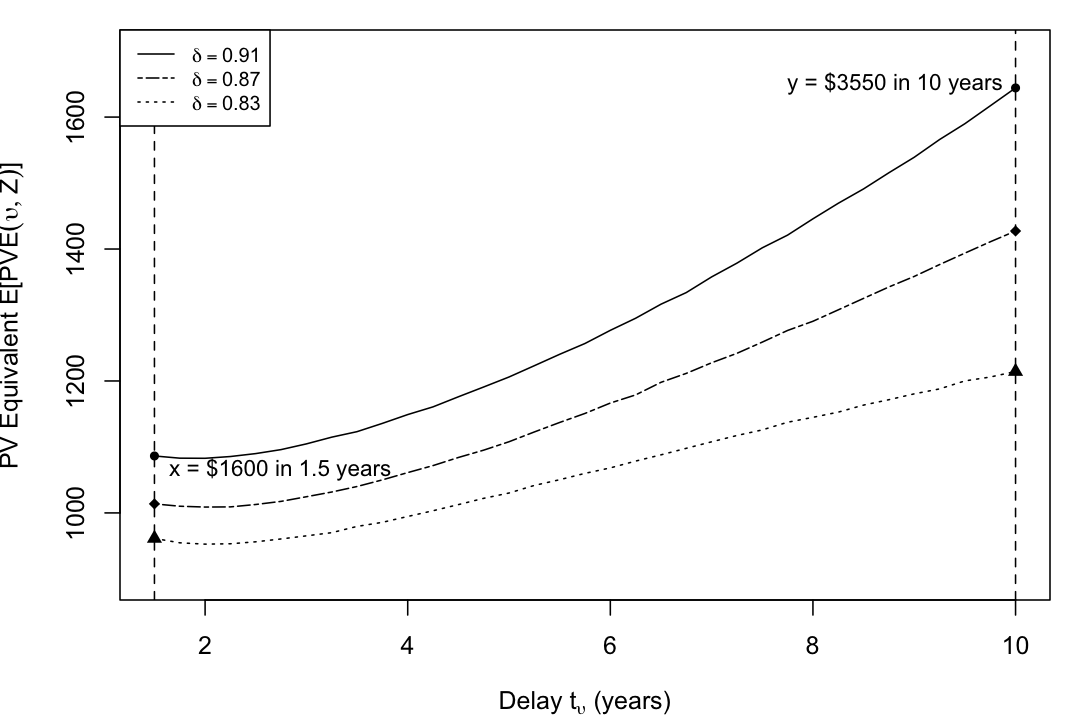

Intertemporal Choice. The logic above, which shows the differential ease of comparing options to the numeraire can rationalize preference reversals, is not limited to risky choice.

Consider the following example of a preference reversal in intertemporal choice, documented by Tversky et al., (1990) using choice vignettes:

The authors find that in direct choice, a majority of subjects choose the earlier payment , but that when tasked with valuing the options in terms of money today, most subjects value the more delayed payment higher than .

In Appendix B.5, we show how our model applied to the intertemporal domain rationalizes such preference reversals as the consequence of being more similar to and therefore easier to compare to money today than .

4.3.3 Biases in Valuation of Risk and Time

The pattern of biased valuation presented in Figure 6 also generates apparent probability-weighting in certainty equivalents. To see why this is true, suppose we have a risk-neutral agent and we elicit certainty equivalents on simple lotteries to measure the agent’s probability weighting function. Previously, we argued that low-probability lotteries will be over-valued and high-probability lotteries will be under-valued. Thus, if we estimated the agent’s probability weighting function based on her valuations, we would conclude the agent is overweighting small probabilities and underweighting large probabilities.

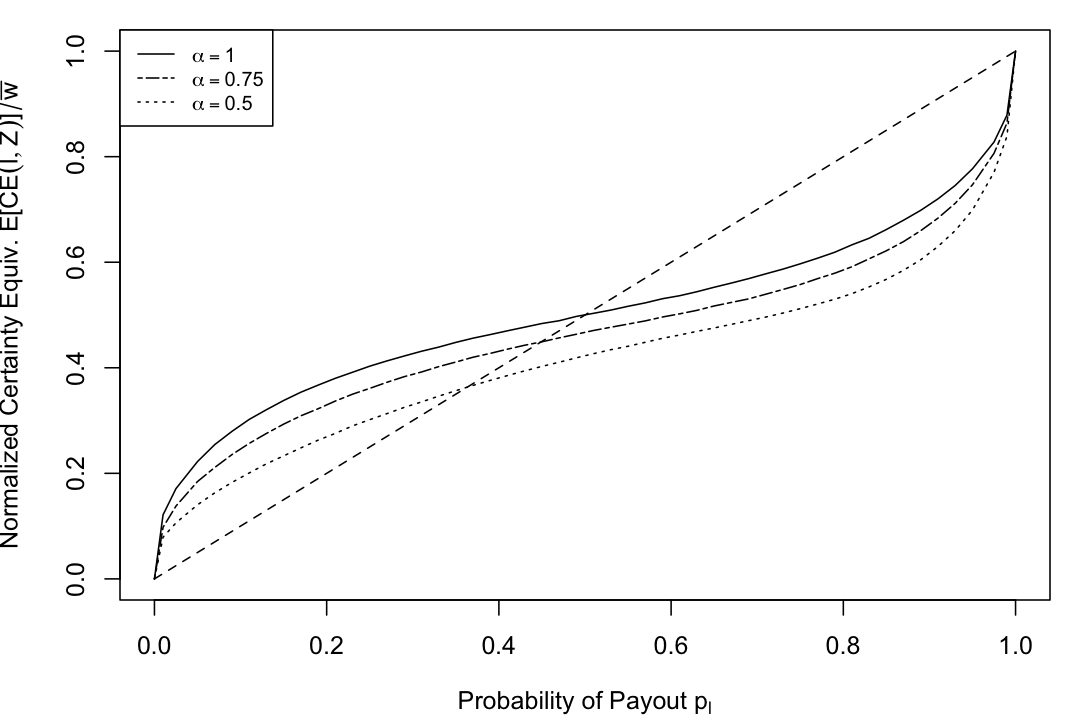

To illustrate this, consider the standard paradigm used to estimate the probability weighting function, in which the DM provides certainty equivalents of simple lotteries . Figure 8 plots the predicted normalized certainty equivalents as a function of for a DM with CRRA preferences. The weights implied by these certainty equivalents reproduce the familiar inverse S-shaped pattern of probability weighting.

In our model, this apparent probability weighting does not reflect a true preference, but instead a bias resulting from the complexity of comparing a lottery to a price list. This is important for two reasons. First, we do not predict probability weighting in binary choice, which is consistent with evidence that the inverse S-shaped probability weighting function is far more prominent in valuation tasks than in direct choice (Harbaugh et al.,, 2010; Bouchouicha et al.,, 2023). Second, we predict that these seeming patterns of probability weighting will be highly sensitive to the units against which the lotteries are valued. In particular, we predict that it is possible to reverse the pattern of apparent probability-weighting with an appropriate choice of price list currency.

Consider an alternative paradigm for estimating the probability weighting function, in which the DM provides probability equivalents of a certain payout: the probability that makes the lottery indifferent to a certain payment . Tracing out the probability equivalents as a function of the normalized certain payments should — assuming no complexity-driven distortions — recover the same preference information as the certainty equivalents discussed above. Figure 9 plots the predicted relationship between the certain payment amount (y-axis) and the associated probability equivalent (x-axis), in which the certain payment is valued against a probability list , for . Here we see a reversal of the inverse S-shaped pattern: the difficulty of comparing sure payments against the numeraire good causes probability equivalents to be compressed towards the middle of the price list, generating apparent underweighting of small probabilities and overweighting over large probabilities. This is an empirical prediction which could be tested experimentally.

Importantly, we do not claim that distorted probability weighting functions do not exist – instead, our model offers a potential explanation for why canonical valuation tasks over simple lotteries may overstate the degree of any true probability weighting.

We can consider a similar exercise in the context of valuing intertemporal payment streams, where we see that complexity-driven noise generates apparent hyperbolic discounting even in the absence of hyperbolicity in preferences. We work out this exercise in full in Appendix B.6, but the logic is much the same as probability-weighting. In traditional price-list elicitations, payments dated close to the present will be undervalued, as valuations are pulled down towards the center of the price list; and payments further in the future will be overvalued, as valuations are pulled up towards the center of the price list. This produces a pattern of complexity-driven hyperbolic discounting, which is consistent with evidence from (Enke et al.,, 2023). We further predict that this pattern persists when front-end delays are incorporated, since the apparent hyperbolicity predicted by our model is not driven by a preference for the present. This is also supported by evidence from (Enke et al.,, 2023).

Importantly, our model predicts that these distortions are not generic, but instead arise specifically from the difficulty of comparing delayed payments to the numeraire good of money today. As with lotteries, our model predicts that we can reverse the pattern of hyperbolic discounting by instead eliciting valuations in time-equivalents rather than money-equivalents, as discussed in B.6. Once again, we do not claim that real present-biased preferences do not exist; rather, our model suggests a mechanism for why canonical valuation tasks may overstate the true degree of hyperbolic discounting.

5 Conclusion

This paper presents a new theory of comparison-based complexity in multiattribute, lottery, and intertemporal choice, in which comparisons are easier when two options are more similar along their features (holding value difference fixed); and easiest when two options have a dominance relationship. We provide experimental evidence that our measures of comparison complexity predict choice errors, choice inconsistency, and cognitive uncertainty. Finally, we show how comparison complexity can generate systematically biased choices and valuations. In particular, our choice model rationalizes familiar context effects like the decoy and asymmetric dominance; classic preference reversals; and probability weighting and hyperbolic discounting in risk and time respectively. Furthermore, our model predicts that it is possible to reverse the standard patterns of probability weighting and hyperbolic discounting, depending on how the researcher chooses the currency against which options are valued.

References

- Bordalo et al., (2013) Bordalo, P., Gennaioli, N., and Shleifer, A. (2013). Salience and Consumer Choice. Journal of Political Economy, 121(5):803–43.

- Bouchouicha et al., (2023) Bouchouicha, R., Wu, J., and Vieider, F. M. (2023). Choice lists and standard patterns of risk-taking.

- Bushong et al., (2021) Bushong, B., Rabin, M., and Schwartzstein, J. (2021). A Model of Relative Thinking. The Review of Economic Studies, 88(1):162–191.

- Debreu, (1983) Debreu, G. (1983). Topological methods in cardinal utility theory. In Mathematical Economics, pages 120–132. Cambridge University Press.

- Enke and Graeber, (2023) Enke, B. and Graeber, T. (2023). Cognitive Uncertainty*. The Quarterly Journal of Economics, 138(4):2021–2067.

- Enke et al., (2023) Enke, B., Graeber, T., and Oprea, R. (2023). Complexity and Time. Technical report, National Bureau of Economic Research.

- Enke and Shubatt, (2023) Enke, B. and Shubatt, C. (2023). Quantifying Lottery Choice Complexity.

- Erev et al., (2002) Erev, I., Roth, A. E., Slonim, R., and Barron, G. (2002). Combining a Theoretical Prediction with Experimental Evidence. SSRN Electronic Journal.

- Gescheider, (2013) Gescheider, G. A. (2013). Psychophysics: the fundamentals. Psychology Press.

- Gilboa, (2009) Gilboa, I. (2009). Theory of decision under uncertainty, volume 45. Cambridge university press.

- Gonzalez and Wu, (1999) Gonzalez, R. and Wu, G. (1999). On the Shape of the Probability Weighting Function. Cognitive Psychology, 38(1):129–166.

- Harbaugh et al., (2010) Harbaugh, W. T., Krause, K., and Vesterlund, L. (2010). The Fourfold Pattern of Risk Attitudes in Choice and Pricing Tasks. The Economic Journal, 120(545):595–611.

- He and Natenzon, (2023) He, J. and Natenzon, P. (2023). Moderate Utility. American Economic Review: Insights.

- Huber et al., (2014) Huber, J., Payne, J. W., and Puto, C. P. (2014). Let’s be Honest about the Attraction Effect. Journal of Marketing Research, 51(4):520–525.

- Khaw et al., (2021) Khaw, M. W., Li, Z., and Woodford, M. (2021). Cognitive Imprecision and Small-Stakes Risk Aversion. The Review of Economic Studies, 88(4):1979–2013.

- Kőszegi and Szeidl, (2013) Kőszegi, B. and Szeidl, A. (2013). A Model of Focusing in Economic Choice. The Quarterly Journal of Economics, 128(1):53–104.

- Landry and Webb, (2021) Landry, P. and Webb, R. (2021). Pairwise normalization: A neuroeconomic theory of multi-attribute choice. Journal of Economic Theory, 193:105221.

- Loewenstein and Prelec, (1992) Loewenstein, G. and Prelec, D. (1992). Anomalies in intertemporal choice: Evidence and an interpretation. The Quarterly Journal of Economics, 107(2):573–597. Publisher: MIT Press.

- Natenzon, (2019) Natenzon, P. (2019). Random Choice and Learning. Journal of Political Economy. Publisher: University of Chicago PressChicago, IL.

- Peterson et al., (2021) Peterson, J. C., Bourgin, D. D., Agrawal, M., Reichman, D., and Griffiths, T. L. (2021). Using large-scale experiments and machine learning to discover theories of human decision-making. Science, 372(6547):1209–1214. Publisher: American Association for the Advancement of Science.

- Puri, (2023) Puri, I. (2023). Simplicity and Risk.

- Rubinstein, (1988) Rubinstein, A. (1988). Similarity and decision-making under risk (is there a utility theory resolution to the Allais paradox?). Journal of Economic Theory, 46(1):145–153.

- Safonov, (2022) Safonov, E. (2022). Random Choice with Framing Effects: a Bayesian Model.

- Seidl, (2002) Seidl, C. (2002). Preference reversal. Journal of Economic Surveys, 16(5):621–655. Publisher: Wiley Online Library.

- Soltani et al., (2012) Soltani, A., De Martino, B., and Camerer, C. (2012). A Range-Normalization Model of Context-Dependent Choice: A New Model and Evidence. PLoS Computational Biology, 8(7):e1002607.

- Tversky and Edward Russo, (1969) Tversky, A. and Edward Russo, J. (1969). Substitutability and similarity in binary choices. Journal of Mathematical Psychology, 6(1):1–12.

- Tversky and Kahneman, (1992) Tversky, A. and Kahneman, D. (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty, 5(4):297–323.

- Tversky et al., (1990) Tversky, A., Slovic, P., and Kahneman, D. (1990). The Causes of Preference Reversal. The American Economic Review, 80(1):204–217.

- Vallender, (1974) Vallender, S. S. (1974). Calculation of the Wasserstein distance between probability distributions on the line. Theory of Probability & Its Applications, 18(4):784–786. Publisher: SIAM.

- Woodrow, (1933) Woodrow, H. (1933). Weight-discrimination with a varying standard. The American Journal of Psychology, 45(3):391–416. Publisher: JSTOR.

APPENDIX

Appendix A Appendix: Tables and Figures