Contracting with a Learning Agent††thanks: This work is funded by the European Union (ERC grant No. 101077862, Project: ALGOCONTRACT, PI: Inbal Talgam-Cohen, and ERC grant No. 740282, under the European Union’s Horizon 2020 Research and Innovation Programme, PI: Noam Nisan), a Google Research Scholar award, a Foundations of Data Science Institute (FODSI) fellowship, the Israel Science Foundation (ISF grants No. 336/18 and No. 505/23 ), the Binational Science Foundation (BSF grant No. 2021680), and the National Science Foundation (NSF CAREER Grant CCF-1942497, PI: S. Matthew Weinberg).

Abstract

Many real-life contractual relations differ completely from the clean, static model at the heart of principal-agent theory. Typically, they involve repeated strategic interactions of the principal and agent, taking place under uncertainty and over time. While appealing in theory, players seldom use complex dynamic strategies in practice, often preferring to circumvent complexity and approach uncertainty through learning. We initiate the study of repeated contracts with a learning agent, focusing on agents who achieve no-regret outcomes.

Optimizing against a no-regret agent is a known open problem in general games; we achieve an optimal solution to this problem for a canonical contract setting, in which the agent’s choice among multiple actions leads to success/failure. The solution has a surprisingly simple structure: for some , initially offer the agent a linear contract with scalar , then switch to offering a linear contract with scalar . This switch causes the agent to “free-fall” through their action space and during this time provides the principal with non-zero reward at zero cost. Despite apparent exploitation of the agent, this dynamic contract can leave both players better off compared to the best static contract. Our results generalize beyond success/failure, to arbitrary non-linear contracts which the principal rescales dynamically.

Finally, we quantify the dependence of our results on knowledge of the time horizon, and are the first to address this consideration in the study of strategizing against learning agents.

1 Introduction

Classic and repeated contracts.

In a classic contract setting, a principal (she) incentivizes an agent (he) to invest effort in a project. The project’s success depends stochastically on the effort invested. The incentive scheme, a.k.a. contract, is performance-based — it determines the agent’s payment based on the project’s outcome, rather than directly on the agent’s effort. This gap between the agent’s costly effort and the stochastic outcome creates moral hazard, and makes contract design a challenging problem.

Due to their immense importance in practice, the design of contracts has long been studied in Economics, forming a rich literature recognized by a Nobel prize in 2016. Recently, there has been a surge of interest in computational aspects of contract design, leading to the ongoing development of a new algorithmic theory of contracts (see, e.g., [6, 7, 32, 47, 33, 27, 38, 19, 52, 57, 28, 1, 20, 39, 29, 61]). Much of the computational research has focused on the classic, one-shot contract setting – the principal and agent share a single interaction, in which the principal offers a contract and the agent chooses a best-response action.111Another setting that has been considered is a series of one-shot interactions with multiple agents, which enables the principal to learn the best contract for the agent population (see, e.g., [43, 22, 63, 31]). An exception is the work of [51], which studies a novel long-term principal-agent model tailored to afforestation. In their model, the principal pays whenever a tree’s state – a Markov chain – progresses, and the agent responds based on the state (not on learning). Yet, this overlooks the fact that in reality, “most principal-agent relationships are repeated or long-term,” i.e., the same agent exerts effort for the principal repeatedly over time [13]. The goal of this paper is to extend algorithmic contract theory beyond the basic single-shot setting, and into the realm of repeated contracts.

Repeated contracts have been studied extensively in Economics. The literature explores many possible variations of how outcomes, actions and contracts evolve over time as the principal and agent interact (see, e.g., [58] and references therein; for surveys see [23], [13, Chapter 10], and [50, Chapter 8]). The main theme of this literature is that the incentive problem grows significantly in complexity with repetition. First, the agent’s action set becomes extremely rich, and optimizing over it is highly non-trivial. Second, the optimal contract itself typically becomes excessively complex – “too complex to be descriptive or prescriptive for incentive contracting in reality” [13].

In light of this complexity, one line of work turns to identifying classes of settings under which a simple contract suffices, most notably the famous work of [44], which assumes constant absolute risk aversion (CARA) utilities and Brownian motion of the output.222The work of [44] studies a single payment at the end of the contractual relationship, based on all outcomes. Another line of work studies contracts that circumvent complexity by being deliberately vague, leaving the agent uncertain about his performance-based compensation (see, e.g., [3, 10, 30]). Our algorithmic perspective yields a new, learning-based approach with which to tackle the complexity of repeated contracts.

Learning to respond to your new boss.

Consider some motivating examples: A worker joins a new team, a student starts an internship, or a junior professor joins a committee. These agents are all initially uncertain of the amount of effort required of them, and what outcomes will be considered good performance. They face a potentially-complex choice of when to exert more effort, and when to step back and lower their effort. Part of their performance assessment is often done by their peers, introducing more uncertainty and noise. The environment is also dynamic, with some outcomes highly valued at one time period but less appreciated in the next period. In effect, each of the agents encounters an implicit and changing system of incentives, to which he is expected to gradually adapt over the course of the repeated interaction. In fact, this pattern is prevalent in many real-life contractual relationships.333For an aforementioned example, the interested reader can see [37] along with the references cited therein. More broadly, in some settings like credit scoring, an evaluation system creates incentives for an agent, while remaining deliberately opaque so as to avoid gaming. The agent thus has no choice but to pick an action “in the dark” [36].

A naturally arising question, then, is: how should an agent choose his actions in a contractual relation that involves uncertainty and recurrent interactions? Inspired by the work of [14] on algorithmic mechanism design, we argue that applying a learning method is a natural way for the agent to respond. In practice, agents tend to react to repeated strategic interactions in a way that is consistent with no-regret learning [55, 56]. No-regret learning has been extensively studied in the context of general repeated games (see, e.g., [11, 15, 34, 42, 53, 60, 2, 49, 62]), repeated auctions and other economic interactions (see, e.g., [24, 18, 48]), and Stackelberg security games (see, e.g., [8]). See [59] for a comprehensive exposition. By assuming that agents apply no-regret learning rather than complex strategic reasoning, we initiate a new approach to repeated contracting.

1.1 Our Model and Contribution

Optimizing against a no-regret learner.

We revisit the classic question of optimal contract design in a repeated setting, this time considering a no-regret learning agent. The main question we address is: if the principal knows that the agent is a no-regret learner, what contract sequence should she offer? We refer to the best sequence as the optimal dynamic contract.

We study the optimal dynamic contract in the following model: A principal and agent interact over time steps for some large . In each step , the agent takes a costly action as recommended by the no-regret learning algorithm, and the principal pays the agent according to the current contract and the action’s outcome. The contracts can be modified by the principal over time dynamically (and adaptively). A simple benchmark is achieved by not modifying them, that is, simply repeating the optimal one-shot contract in each round. We refer to this as the optimal static contract. It is not hard to see that the principal’s revenue in this case against a no-regret agent will essentially be the optimal static revenue (A.1 in Appendix A).

Our main focus is on “mean-based” learning agents, who apply simple, natural and common learning algorithms, such as multiplicative weights [4], follow the perturbed leader [41, 46], or EXP3 [5]. Intuitively, mean-based algorithms consider the cumulative payoffs from each of the actions, and play actions which performed sub-optimally in the past with a low probability (see Section 2 for a precise definition, taken from [14]).

We also briefly consider more sophisticated agents, who apply no-swap-regret rather than mean-based learning (e.g., [12]). Against such agents, a crisp optimal strategy is immediate from previous work on general repeated games against learners [26, 54]: It is known that the best static solution is also the best dynamic one. In our context this means that no dynamic contract can achieve better than the optimal static contract (A.2 in Appendix A). Interestingly, we show that both players can be better off if the agent applies more naïve, mean-based learning (although, as expected, there are also many cases where the agent is worse off due to this interaction).

What is known.

In general games, finding an optimal dynamic strategy against a mean-based learner is an open problem. The work of [26] shows an equivalence between this problem and an -dimensional control problem, where is the number of actions among which the agent chooses. So far, it is known how to non-trivially (i.e., with a non-trivial dynamic contract) optimize against a mean-based learner only for the setting of repeated auctions, in which [14] show that the designer can extract full welfare as revenue. The works of [25, 17] extend this result to prior-free auction settings and multiple agents. However, even with a single agent, the optimal auction against a mean-based learner turns out to be fairly impractical. It alternates between running second-price auctions and charging the winner huge payments, and is thus “not meant to guide practice” [17]. The work of [18] studies mechanisms for a no-regret agent where in addition there is learning on behalf of the principal, as a means to dispense with the common prior assumption present in many economic design problems.

Our contribution.

In this paper we give a clean, tractable answer to our main question as follows. When the agent’s choice among actions can lead to success/failure of the project, the principal’s optimal dynamic contract is surprisingly simple (especially in comparison to the optimal dynamic auction): Offer the agent one carefully-designed contract for a certain fraction of the rounds (both contract and fraction are poly-time computable), then switch to the zero contract (that is, pay the agent nothing always) for the remaining rounds. Previous works on the canonical contract setting with success/failure outcomes include [6, 27, 28, 51]. In this setting, simple linear (single-parameter) contracts are optimal, and this is actually the only property required for our result – our result generalizes to any setting where the principal utilizes only linear contracts.

Unlike the optimal dynamic auction, the optimal dynamic contract divides the welfare among the principal and agent. In fact, it can increase the utility of both players (and thus also the total welfare) in comparison to the optimal static contract. One interpretation of this result is that, while a no-swap-regret algorithm is better for the agent against any fixed behavior of the principal, an agent who commits to a mean-based algorithm can be overall better off against a dynamic principal. A similar advantage of simple no-regret learning over no-swap-regret was noted in a different context by [15].

Our main result also generalizes to settings with a rich set of outcomes beyond success/failure, as long as the principal changes the contract dynamically by scaling it (“single-dimensional scaling”). However, we also show that absent this single-dimensional scaling restriction, there exist principal-agent instances where the optimal dynamic contract does not take this form: it is possible for the principal to do strictly better than offering the same contract for several rounds and then switching to the zero contract.

Implicit in all our positive results, as well as in all known results in the literature on optimizing against a learner, is the assumption that the optimizer knows the time horizon . We show that when there is (even limited) uncertainty about , the principal’s ability to use dynamic contracts to guarantee more revenue than the optimal static contract diminishes. We achieve this by characterizing the optimal dynamic contract under uncertainty of , and showing that the principal’s added value from being dynamic sharply degrades with an appropriate measure of uncertainty.

More related work.

The work of [40] shows how to learn an agent’s private type (rather than to maximize revenue) through online principal-agent interaction using menus of contracts. Ben-Porat et al., [9] study principal-agent problems over MDPs, where the (budgeted) principal offers an additional reward to the agent, and the agent picks the MDP policy selfishly, without learning.

1.2 Illustrative Example

| “Failure” outcome | “Success” outcome | |

|---|---|---|

| Action 1 () | 1 | 0 |

| Action 2 () | 1/2 | 1/2 |

| Action 3 () | 0 | 1 |

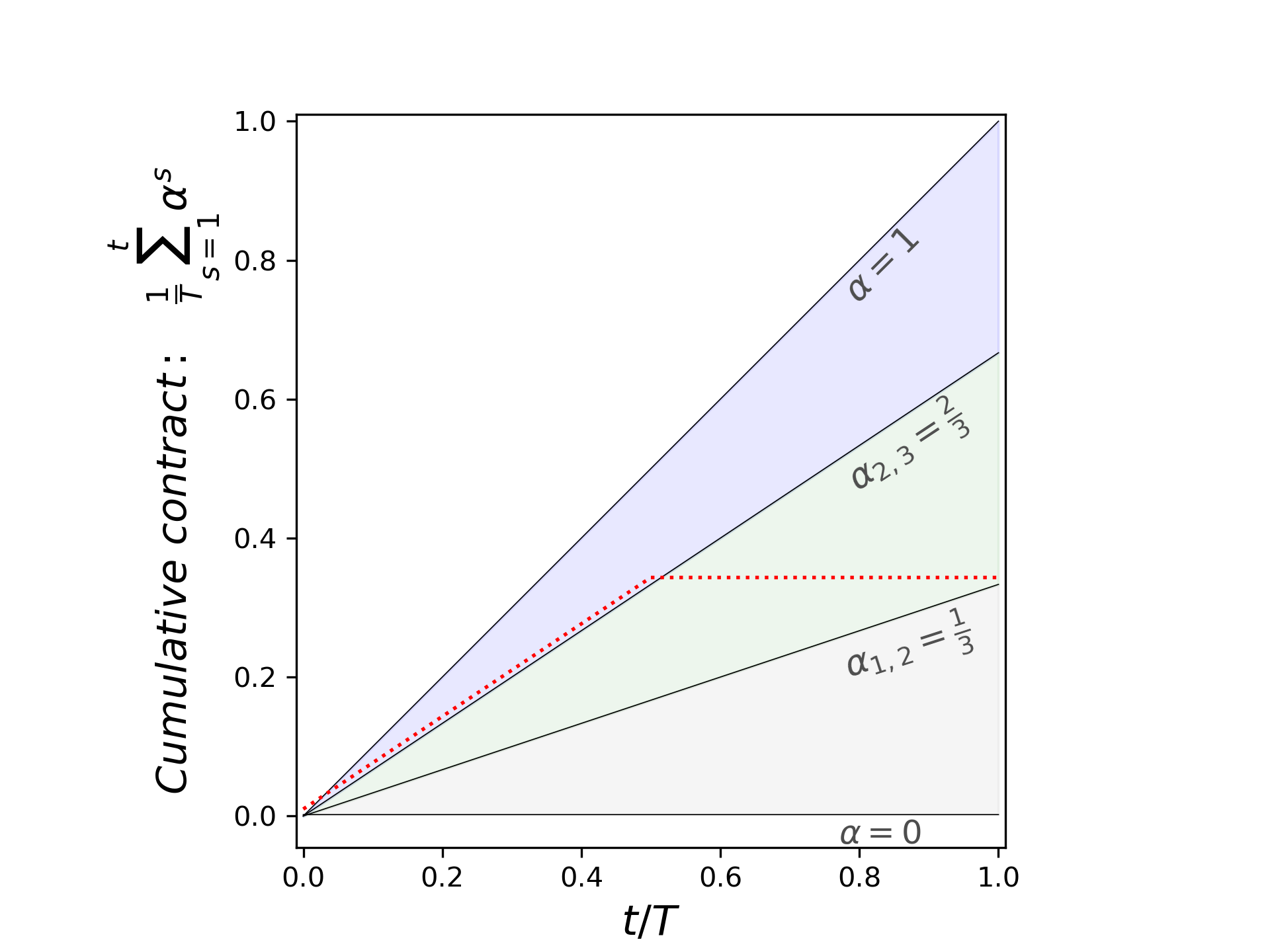

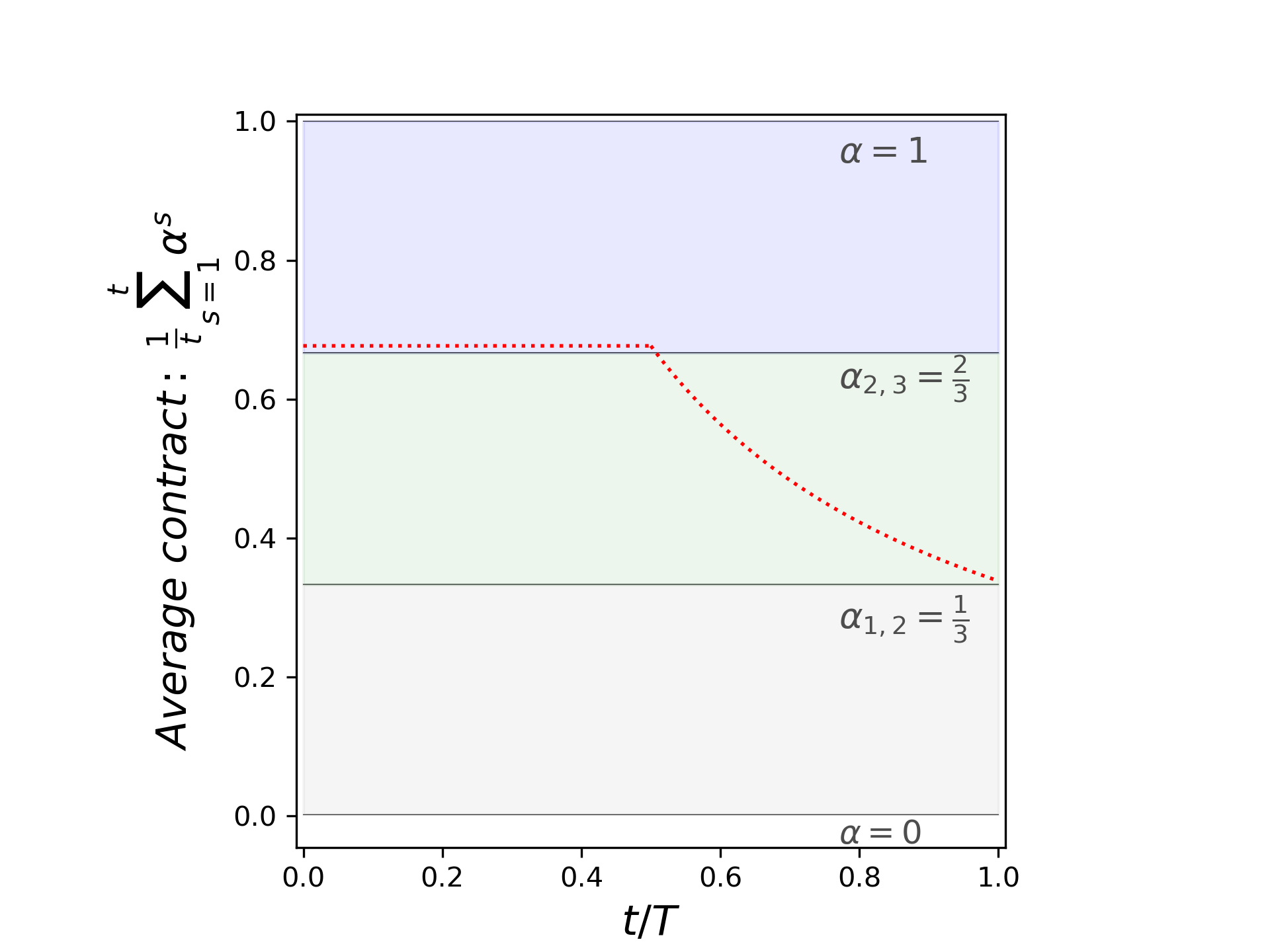

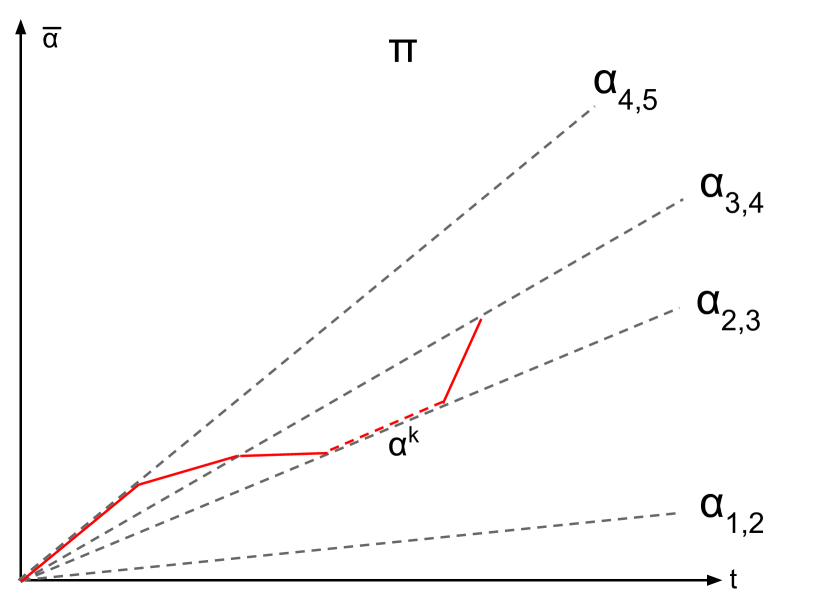

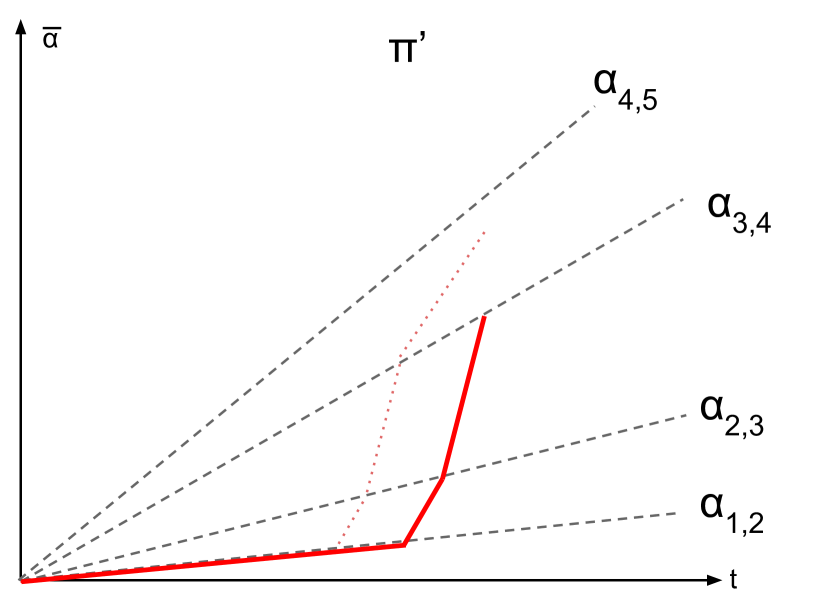

To demonstrate our model and findings, we show an example where a simple dynamic contract yields higher revenue than the best static contract. The analysis requires some familiarity with the basics of contract settings, which appear in the first paragraphs of Section 2 for completeness. Consider the setting in Figure 1: There are three actions with costs for the agent, leading with the probabilities shown in the figure to two outcomes “failure” and “success” with rewards and for the principal. Since there are two outcomes, w.l.o.g. we can consider only linear contracts, i.e., contracts that pay the agent for success (leaving the principal with ).

Under an optimal static linear contract, the agent must be indifferent either between actions and or between actions and (otherwise, the principal is overpaying for incentivizing an action). The indifference contracts are denoted by and , respectively. These lead to the same expected utility for the principal, where the expectation is over the probability of success: . That is, both and are optimal static contracts.

Now consider a principal interacting with a mean-based learning agent. The principal initially offers the contract for time steps. The agent follows his mean-based strategy and plays action (in a fraction of the time with high probability), which yields a utility of roughly per step for the agent and per step for the principal. Subsequently, the principal switches to the zero contract for the remaining time steps. From the perspective of the agent, at the time of the switch the cumulative utilities of actions and are roughly (compared to from action ). But in every step of the subsequent stage, the cumulative utility of action is degraded by an amount of and the cumulative utility of action is degraded by an amount of . Thus the agent “falls” to action and plays it until the last period . The overall utility for the agent is , and for the principal . The principal thus improves her utility by a factor of compared to the optimal static contract.

Figure 2 shows a graphical representation of the above dynamic contract. It turns out that this simple “free-fall” contract (see Definition 2.1) is also an optimal dynamic strategy for the principal, and in fact, this is not a a special property of the current example. In Section 3 we show that for any linear contract game, there exists an optimal strategy with this form: offer a fixed contract for a period of steps and then switch to the zero contract. Moreover, in Section 4 we show that, surprisingly, this simple structure remains optimal also for general non-linear contracts, as long as their dynamics are characterized by a single scalar parameter.

1.3 Summary of Results and Roadmap

We initiate the study of repeated principal-agent problems with a learning agent; the key takeaways from our work are as follows:

Theorem (See Theorem 3.1 in Section 3.1, combined with the reduction in Theorem 2.4).

In success/failure settings, as well as in arbitrary contract settings where the principal restricts to linear contracts, the optimal dynamic contract against a mean-based agent is a free-fall contract. This optimal dynamic contract can be efficiently computed.

Theorem (See Theorem 3.7 in Section 3.2).

Consider the space of repeated principal-agent problems; in a subset of this space of positive measure, both the principal and agent achieve unboundedly better expected utilities from the principal’s optimal dynamic contract compared to the optimal static contract.

One takeaway from the previous theorem is that the principal and agent can both benefit when the agent commits to mean-based rather than no-swap-regret learning, in stark contrast to auctions (where a buyer committing to a mean-based strategy is left with zero payoff, because the auctioneer can extract the full surplus). We generalize our findings on the optimality of free-fall contracts among any dynamic contract with single-dimensional scaling.

Theorem (See Theorem 4.1 in Section 4, combined with the reduction in Theorem 2.4).

In arbitrary contract settings, there is a free-fall contract that is optimal among dynamic contracts. A dynamic contract has single-dimensional scaling if it starts from an arbitrary contract , and at every time step plays for some scalar .

In Section 4.1 we demonstrate that in absence of single-dimensional scaling, there may not exist a free-fall contract that is optimal among dynamic contracts.

Finally, we are the first to investigate the impact of not knowing the time horizon when optimizing against a no-regret learner. Of course, the learning agent can guarantee no-regret without knowing the time horizon (see e.g., [21], Section 2.3). We show that even mild uncertainty of the principal about the time horizon significantly degrades her ability to outperform the best static contract, and we quantify this degradation as follows:

Theorem (See Theorems 5.2-5.3 in Section 5).

For any contract problem and error-tolerance parameter , there exists is some minimum time uncertainty parameter so that for any minimum time horizon , no randomized dynamic contract can guarantee the principal a -multiplicative advantage over the optimal static contract simultaneously for every time horizon in the range . Conversely, for any contract problem and time uncertainty parameter , there is some nonzero error-tolerance parameter such that for a sufficiently large time horizon minimum , there is a randomized dynamic contract that can guarantee the principal a -multiplicative advantage over the optimal static contract simultaneously for every time horizon in the range .

The computational study of repeated contracts, in particular with learning, raises many open questions, e.g.: What is the optimal dynamic contract when the principal does not restrict to one-dimensional dynamics, and what is the computational complexity of finding it? What is the optimal dynamic contract against a learning agent with a hidden type (unifying our contract model with the auction model of [14]), or against a team of multiple learning agents? What is the effect on welfare and utilities when, rather than a learner and optimizer, we have two learning players?

2 Model

We first present basic (non-repeated) contracts, and the class of linear contracts; a familiar reader may wish to skip to Sections 2.1-2.2 on repeated contract settings (discrete and continuous).

Single-shot contract setting. There are two players, a principal and an agent. The agent has a finite set of actions, among which it chooses an action and incurs a corresponding cost (in addition to we will use to index actions). W.l.o.g. the actions are sorted by cost () and the cost of the first (null) action is zero (). There is a finite set of possible outcomes, and every action is associated with a probability distribution over the outcomes. The null action leads with probability 1 to the first (null) outcome. Every outcome is associated with a finite reward for the principal (in addition to we will use to index rewards). We assume w.l.o.g. that and . We denote the expected reward by for action . As is standard we assume no dominated actions: i) if then ; ii) for every action there exists a contract that uniquely incentivizes it. The contract setting (a.k.a. principal-agent problem) is known to both players.

The game. The game in the basic (non-repeated) setting has the following steps: (1) The principal commits to a contract , , where is the non-negative amount the principal will pay the agent if outcome is realized.444The non-negativity of the contractual payments is known as limited liability [45]. Without it – or some other form of risk averseness of the agent – he could simply “buy the project” from the principal and enjoy the rewards directly. In particular, can be the zero contract in which for all . (2) The agent selects an action , unobservable to the principal, and incurs a cost . (3) An observable outcome is realized according to distribution . The principal receives reward and pays the agent . The principal thus derives a utility (payoff) of , and the agent of .

Expected utilities and optimality. In expectation over the outcomes, the utilities from contract and action are for the principal, and for the agent. Summing these up we get the expected welfare from the agent’s chosen action . For a given contract , let be the set of actions incentivized by this contract, i.e., maximizing the agent’s expected utility (usually this will be a single element, but in the case of ties we include all actions in ).555The standard tie-breaking assumption, according to which the agent breaks ties in favor of the principal, is less relevant here since we want our analysis to apply to all learning algorithms, regardless of the way they break ties. The goal of the contract designer is to maximize the principal’s expected utility, also known as revenue. Such a contract is referred to as optimal.

Linear contracts. In a linear contract with parameter , the principal commits to paying the agent a fixed fraction (commission) of any obtained reward. Thus by choosing action , the agent gets expected utility , and the principal gets . As is raised from to , the agent’s expected utility is affected less by the action cost, and the agent’s incentives align more with the principal’s and with social welfare. This intuition is formalized by [32], showing that as increases, the agent responds with actions that have increasing costs, increasing expected rewards, and increasing expected welfares.666We assume w.l.o.g. that for every action there is a linear contract which uniquely incentivizes it (otherwise when focusing on linear contracts we may omit this action from the setting). The critical at which the agent switches from action to action (for ) is denoted by , and is also referred to as an indifference point or breakpoint. For we define . Using this notation, for every linear contract , the agent plays action . In the linear contract setting, the focus is on linear contracts and only such contracts are allowed.

2.1 Repeated Contract Setting: Discrete Version

We study a repeated contract setting , in which the above game is repeated for discrete rounds between the same principal and agent. The number of rounds is called the time horizon. The setting is known to both players,777In Section 5 we consider what happens when is unknown to the principal. The other parameters of the setting, if unknown, can be easily learned via sampling. who update the contracts and actions in each round. The outcomes of the actions are drawn independently per round (past outcomes affect future outcomes only through learning). Denote the contract, action, realized outcome and reward at time by , respectively. The agent’s payoff at time is . The sequence of contracts is called a dynamic contract, and the pairs form the trajectory of play. We define the following class:

Definition 2.1.

A free-fall contract is a dynamic contract in which the principal offers a (single-shot) contract for the first rounds, and then offers the zero contract for the remaining rounds.

Learning agent. The agent’s approach to choosing an action is learning-based, by applying a no-regret algorithm (rather than based on myopic best-responding, as in the one-shot setting). Our analysis applies with full feedback on the performance of each action, where the agent observes the expected payoffs of all actions (whether taken or not — e.g. by observing someone else take that action), or with bandit feedback, where the agent observes only the achieved payoff of the action taken. A delicate issue is that, unlike the standard scenario of learning in games, the payments for each action are stochastic. Thus, the agent must not only learn which action to take, but also the expected payment from each action. When is large enough, the extra learning has a vanishing impact, and does not affect the analysis of players’ utilities and strategies.

Our main focus is on the prominent family of mean-based algorithms. The idea behind mean-based algorithms is that they rarely pick an action whose current mean is significantly worse than the current best mean. There exist such algorithms with both full and bandit feedback that are mean-based and achieve no-regret. In our setting, let be the expected utility the agent would achieve from taking action at round , and let represent the cumulative utility achievable from action up to time given the principal’s trajectory of play. Then:

Definition 2.2 ([14]).

A learning algorithm is -mean-based if whenever , then the probability that the algorithm takes action in round is at most . We say an algorithm is mean-based if it is -mean-based for some .888Some small changes need to be made to this definition for the partial-information (bandits) setting – see Definition B.4 in Appendix B.3.

Optimal dynamic contract. The design goal in the repeated setting is to find an optimal dynamic contract: a sequence that maximizes the total expected revenue against a learning agent (whether mean-based or no-swap-regret, where in either case we assume the worst-case such learning algorithm). In the linear contract setting, the sequence is composed of linear contracts. If it maximizes the total expected revenue among all linear contract sequences, we say it is the optimal dynamic linear contract. We remark that it is without loss of generality to consider only linear contracts with .999This is a non-trivial consequence of our proof machinery. The proof appears as Observation A.3 in Appendix A for completeness.

Note that, as described here, the contract sequence is fixed by the principal at the beginning of the game. We refer to such a principal as oblivious. If the principal can choose as a function of the agent’s previous actions, we say the principal is adaptive. Our positive results (showing the principal can guarantee at least some amount of utility) hold even for oblivious principals, and our negative results hold even for adaptive principals.

Optimal static contract. In a repeated setting, a static contract is a sequence of contracts in which the same one-shot contract is played repeatedly. The repeated game with a static contract and a regret-minimizing agent is, in the limit, equivalent to the classic one-shot contract game with a best-responding agent (Observation A.1). A natural benchmark for dynamic contracts is thus the optimal static contract, in which the optimal one-shot contract is played repeatedly.

2.2 Repeated Contract Setting: Continuous Version

To simplify the technical analysis, we now present a continuous version of our repeated contracts model. For the remainder of the paper we will primarily work in the continuous-time model.

Reduction to continuous time. In [26], the authors consider the problem of strategizing against a mean-based learner in a repeated bi-matrix game, and show it reduces to designing dynamic strategies for a simplified continuous-time analogue (note that the choice of continuous-time analogue is tailored to mean-based learning – it is not intended to be a special case of a general discrete-continuous reduction against any learner). We pursue a similar reduction here, and show (in Theorem 2.4) how to reduce the problem of designing dynamic contracts in the discrete-time setting (Section 2.1), to a simpler problem in a continuous-time setting. We later extend the reduction to settings with an unknown time horizon (see Theorem 5.4 in Section 5).

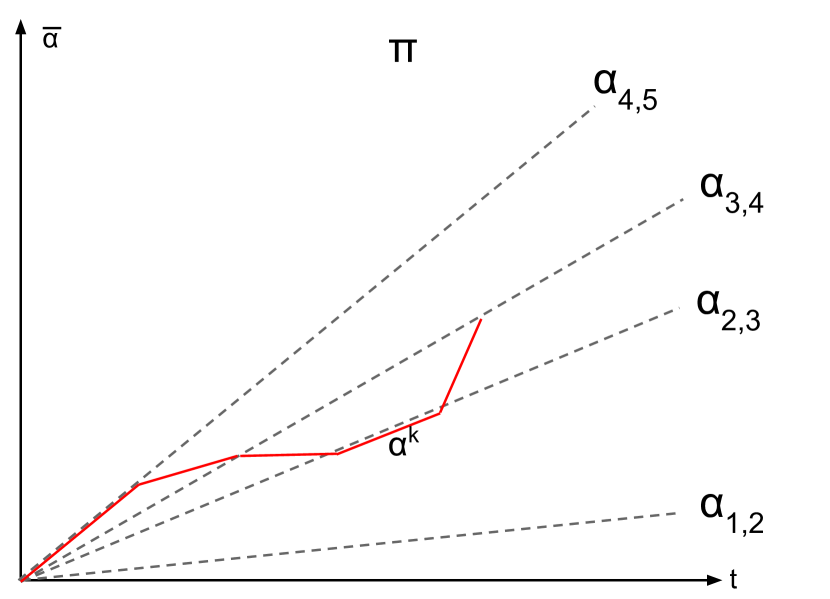

Trajectories of continuous play. In the continuous setting, rather than specifying the trajectory of play by a sequence of contracts and responses, we instead specify it by a finite sequence of tuples , each representing a “segment” of play where the principal plays a constant contract and the agent responds with a constant action. Here, each represents an arbitrary contract, each represents the (fractional) amount of time that the principal presents this contract to the agent, and each represents the action the agent takes during this time. In the linear contract setting, we use the notation instead of . We sometimes refer to as a contract, by which we mean the dynamic contract composed of for segments of length .

To form what we call a valid trajectory of play against a mean-based learner, the responses of the agent must satisfy certain constraints. Let

be the total duration of the first segments, and the average contract offered by the principal for the first segments, respectively. Then each (for ) must satisfy and . In words, must be a best-response to the historical average contract at both the beginning and end of segment (and therefore also throughout segment ).

The following is a continuous analogue of Definition 2.1.

Definition 2.3.

A free-fall trajectory is a game trajectory in which for all .

Optimal trajectory. The average expected utility of the principal along trajectory is given by

Let , where the runs over all valid trajectories of arbitrary finite length. We can think of as the maximum possible expected utility of the principal in the continuous setting game. The following theorem (a direct analogue of Theorem 9 in [26]) connects to what is achievable by the principal in our original discrete-time game.

Theorem 2.4.

Fix any repeated principal-agent problem with rounds, and let denote the optimal expected utility of a principal in the continuous analogue. Then:

-

1.

For any , there exists an oblivious strategy for the principal that gets at least expected utility for the principal against an agent running any mean-based algorithm .

-

2.

For any , there exists a mean-based algorithm such that no (even adaptive101010In the partial-information (bandits) setting, this result only holds for deterministic adaptive principals and not for randomized adaptive principals (in the full-information setting, it holds for either); see Appendix B.3 for further discussion.) principal can get more than expected utility against an agent running .

One important thing to note about Theorem 2.4 is that the first part is highly constructive – in fact, the discrete-time strategy for the principal corresponding to a trajectory is essentially the straightforward extrapolation, which plays each contract for rounds (although a slight perturbation of this is necessary to account for segments that do not have a unique best-response). This means that when we show, in Theorem 3.1, that the utility-optimizing for takes the form of a free-fall trajectory, we are simultaneously showing that a free-fall dynamic contract is asymptotically optimal in the original discrete-time setting.

Finally, note that all the above definitions (and the reduction of Theorem 2.4) extend to the specific case where the learner is only allowed to use linear contracts. In this setting, we will write in place of .

3 Linear Contracts

In this section we focus on the case where the principal restricts to using only linear contracts in every step of the interaction with the agent (one example is when there are outcomes, such as success and failure. In this case, arbitrary contracts can be described as linear contracts). We begin by showing that without loss of generality, optimal dynamic contracts take the form of free-fall contracts. We begin by showing a in Section 3.1, and in Section 3.2 we analyze the implications of optimal contracts on the welfare and on the agent’s utility. In particular, we show that dynamic contracts that are optimal for the principal can improve the utilities for both players compared to their utilities under the best static contract.

3.1 Free-Fall Contracts are Optimal

The following theorem shows that in the linear contract setting, free fall contracts are optimal dynamic contracts. We state our theorem in the language of the continuous-time reduction of Theorem 2.4.

Theorem 3.1.

Let be any linear dynamic contract. Then, there exists a free-fall linear contract where , and which can be computed in time polynomial in the problem size.

Proof overview.

We will present a series of “rewriting” rules, which will allow us to replace a given dynamic contract with a simpler, more constrained, dynamic contract with utility at least as large as . At the conclusion of our sequence of rewriting steps, we will see that our contract takes the form of a free-fall contract, thus implying that there is an optimal free-fall contract.

We begin not with a rewriting rule, but instead a general observation about the structure of dynamic linear contracts — namely, that it is impossible for an agent to “skip over” an action. That is, if an agent is playing action at some point, and action at some later point, there must exist segments of non-zero duration where the agent plays each of the intermediate actions between and . Formally, we can write this as follows.

Lemma 3.2.

If is a dynamic linear contract, then for any , (i.e., in any two consecutive segments, the learner’s action can change by at most one).

Proof.

Note that and must both be best responses to the average historical contract , i.e., . Since is always of the form or , the conclusion follows. ∎

Note that the proof of Lemma 3.2 relies on the “linear topology” of the best-response regions in Figure 2 (i.e., any non-zero boundary between best-response regions connects two consecutive actions of the agent). This property is not true for general contracts or general games; however, we will later see that Lemma 3.2 also holds for the class of -scaled contracts introduced in Section 4.

We now proceed to introduce our rewriting rules. The first rewriting rule we present is very general (and in fact applies to any game): we will show that without loss of generality, no two consecutive segments of a dynamic contract induce the same action for the learner. Intuitively, for any time interval in which a mean-based agent plays a single action, we can replace the contracts in this interval with their average and obtain overall a revenue-equivalent dynamic contract. Formally, we can phrase this as follows.

Lemma 3.3.

Let be any linear dynamic contract. Then there exists a linear dynamic contract such that and no two consecutive segments of share the same agent action ().

Proof.

Let be any linear dynamic contract. Assume that for some , . Then the linear dynamic contract formed by replacing the two segments and with the single segment has the property that . To see this, observe that the same action is played throughout the entire interval, and the average payout to the agent is the same. Therefore, in fact we have . It only remains to confirm that this is still a valid dynamic contract (i.e., that each prescribed action is still a best response in the corresponding segment).

To see this, observe first that the cumulative contract at the start (respectively, end) of the merged segment in is the same as the start of segment (respectively, end of segment ) in . Therefore, all segments before and after the merged segment are still correct. To confirm the merged segment, we need only confirm that is a best response on the merged segment in using the fact that it was a best response in both segments and in .

For this, let denote the cumulative contract after the first segments, denote the cumulative contract after the first segments, denote the cumulative contract of during a time in the merged segment, and denote the cumulative contract of during a time in segments or . Observe first that for every between and , there is some such that . Because is a best response on the entire segments and , this means that is a best response to for all between and . Moreover, observe that lies between and for all . Therefore, is indeed a best response to for all in the merged segment, and the dynamic contract is valid.

By repeatedly applying this merging of segments, we can obtain a linear dynamic contract satisfying the constraints of the lemma. ∎

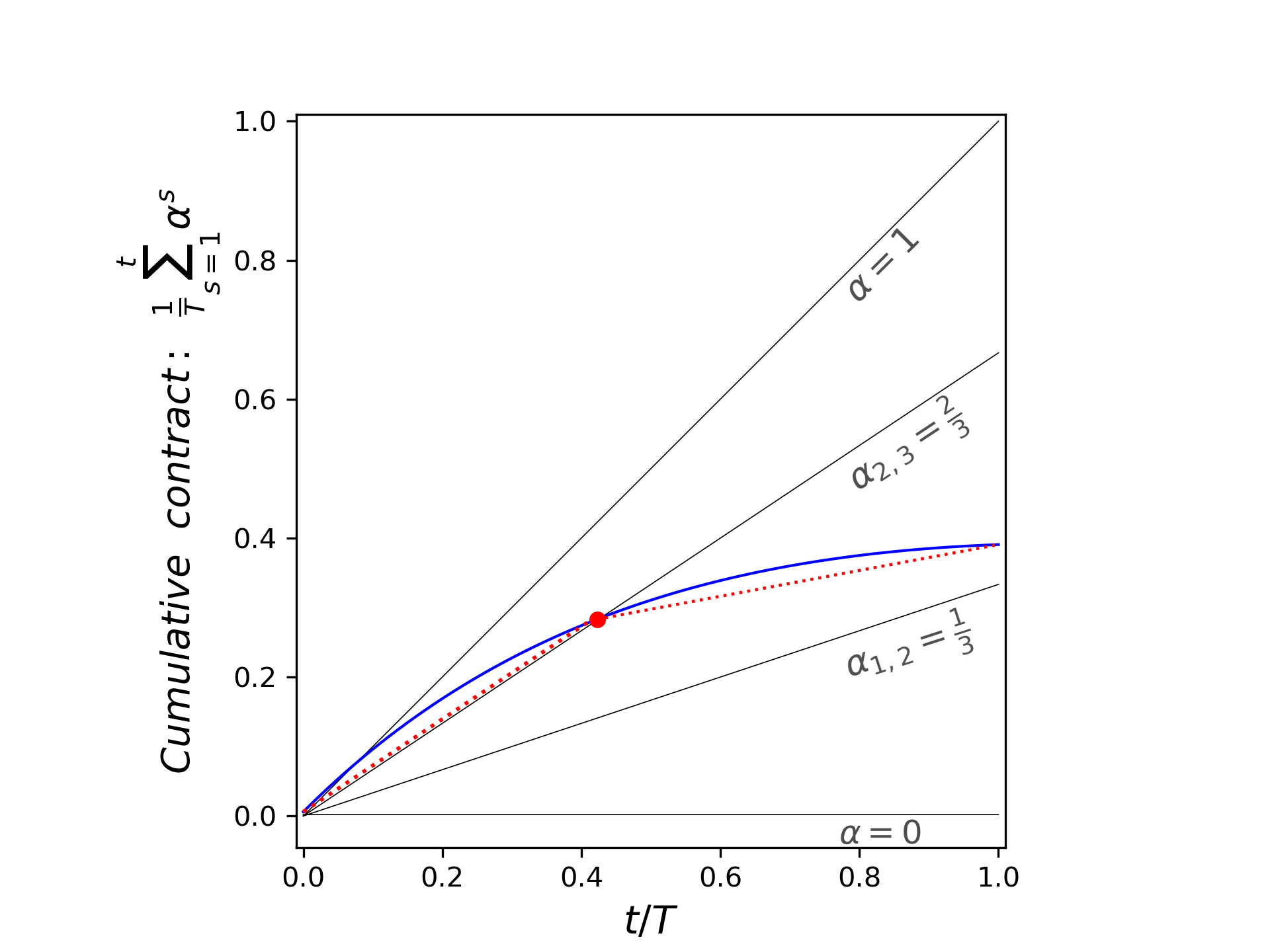

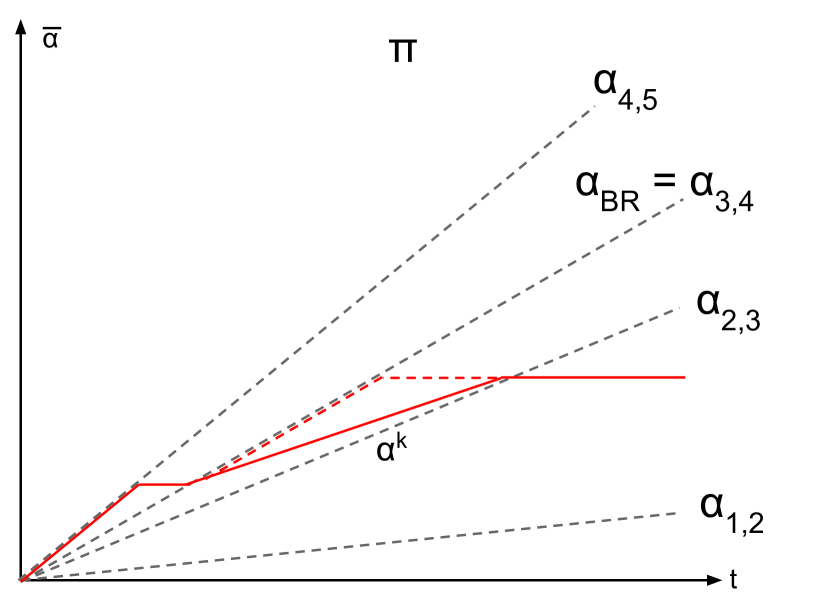

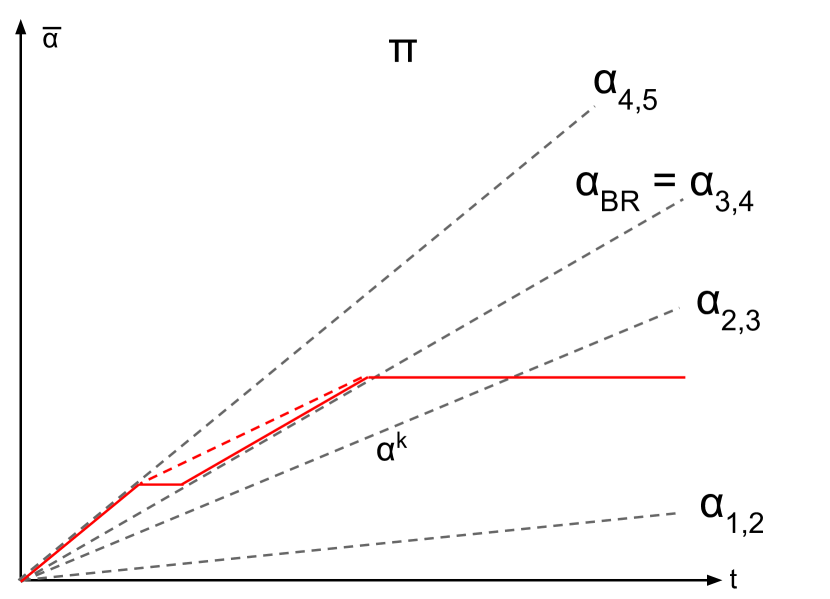

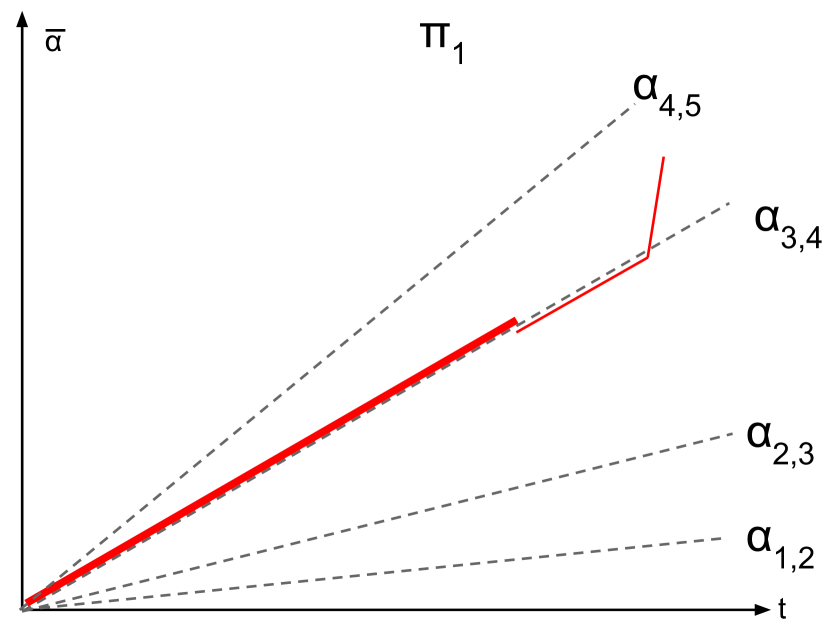

Figure 3 illustrates the above lemma graphically. The figure displays the cumulative contract over time for the contract game depicted in Figure 1. The blue curve represents the trajectory of an arbitrary dynamic contract strategy under which the agent’s best response is to take action until time , and then take action in the remaining time. The crossing point between the best response regions is marked with a red dot. Lemma 3.3 demonstrates that we can replace the blue trajectory with the simpler trajectory depicted in red. In this red trajectory, every region between two consecutive values is crossed by a single linear segment (i.e., a piecewise-stationary trajectory), resulting in the same behavior by the agent and the same revenue.

Our second rewriting rule is specific to linear contracts. It shows that for every linear contract in which the agent is indifferent between two actions, it is beneficial for the principal to shift the contract infinitesimally so that the agent prefers the action with the higher expected reward.

Lemma 3.4.

Let be a dynamic linear contract where during segment the agent is indifferent between actions and (i.e., ), but . If we form by replacing with , then (the principal always prefers that the agent plays the action with higher expected reward).

Proof.

Since actions in the linear contract setting are sorted by increasing value of expected reward, we have that ∎

Note that the principal can implement the change in the agent’s action in Lemma 3.4 by simply increasing their payment to the agent by an arbitrarily small amount – this incentivizes the agent to break ties in favor of the action with larger expected reward (which is the action labeled with a larger number). The fact that the principal can implement this change also follows as a direct consequence of the discrete-to-continuous reduction of Theorem 2.4.

By applying the above two rewriting rules (Lemmas 3.3 and 3.4) along with our observation in Lemma 3.2, we can establish our third rewriting rule: it is always possible to rewrite a dynamic contract so that the sequence of actions is a consecutively decreasing sequence.

Lemma 3.5.

Let be any dynamic linear contract. Then there exists a dynamic linear contract with and where is a decreasing sequence of consecutive actions (i.e., ).

Proof.

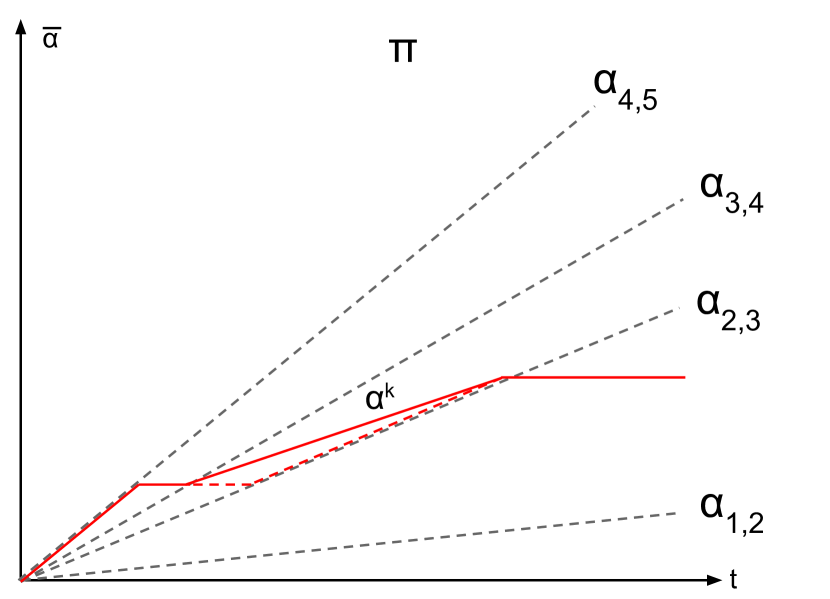

Apply the two rewriting rules in Lemmas 3.3 and 3.4 to until it satisfies the post-conditions of both lemmas (so, no two consecutive segments incentivize the same action, and any segment on a best-response boundary incentivizes the higher-reward action). Since Lemma 3.2 implies that consecutive segments cannot skip over an action, this means that every two consecutive actions under are consecutive: either the agent switches to the next higher action or the next lower action each time step. We therefore just must show that any dynamic contract where the agent increases their action can be rewritten as a decreasing contract with at least same payoff.

Consider the first segment in where the agent switches to a larger action, that is, the smallest such that . Let (so ). Note that the agent must be indifferent between actions and at the end of the th segment (i.e., ).

Now, there are two cases: either segments and are the first two segments of the dynamic contract (i.e., ), or there exists a st segment. In the first case, the agent is indifferent between actions and for the entire first segment (from time to ), but plays action . This contradicts the fact that cannot be reduced further by Lemma 3.4.

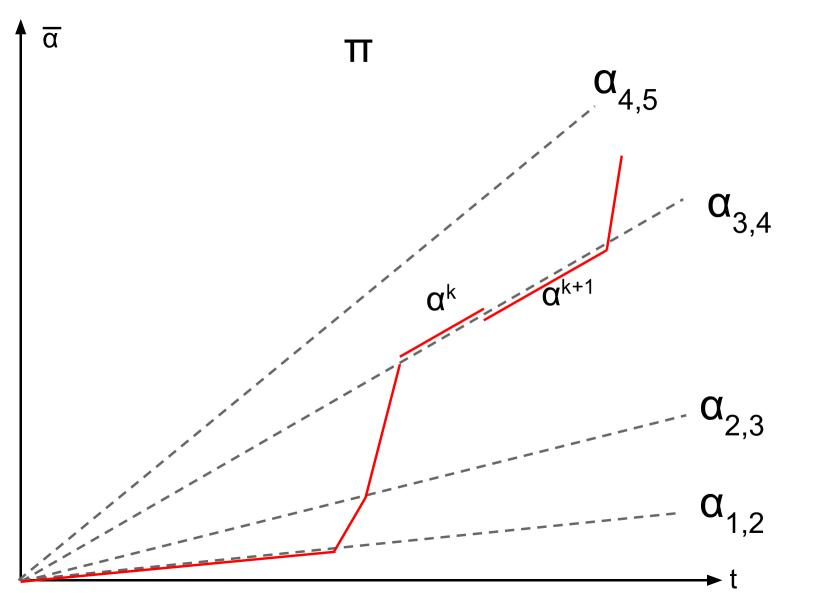

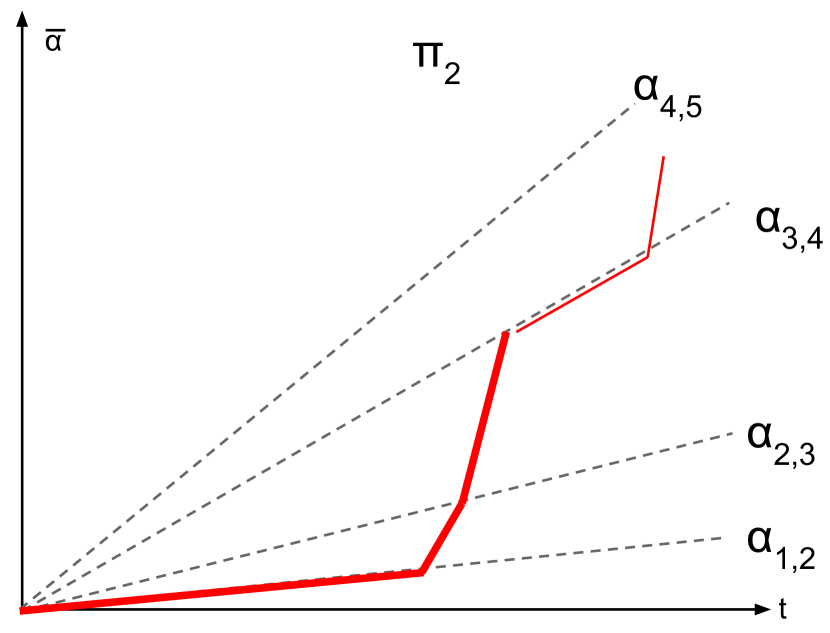

In the second case, the st segment must incentivize action for the learner (since the sequence of actions is decreasing up until segment ). But this means that the agent must be indifferent between actions and also after the st segment, and thus for the entirety of the th segment (). Since the agent plays during the th segment, this also contradicts the fact that cannot be reduced further by Lemma 3.4 (see Figure 4 for an example of this reduction). ∎

We are now almost done – Lemma 3.5 shows we can rewrite any dynamic contract so that the agent descends through their action space. We now need only show that the principal should abruptly switch to offering the zero contract after the first segment (instead of slowing the rate of descent through these regions by offering a positive contract). We do this in our final rewriting lemma.

Lemma 3.6.

Let be a dynamic linear contract where the agent plays a decreasing sequence of actions. Then there exists a free-fall linear contract with .

Proof.

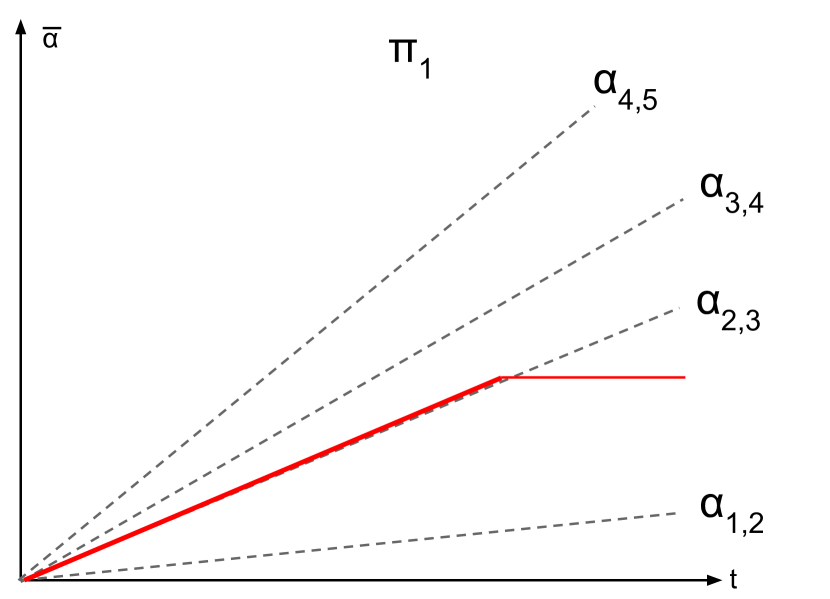

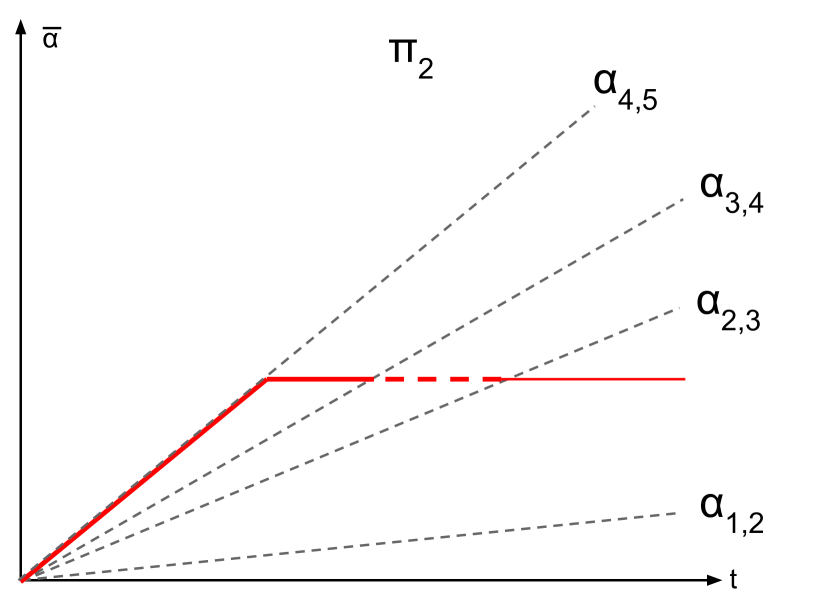

Let (with decreasing), and consider the last non-free-fall segment , i.e., is the maximal for which . Assume that (if not, then is already a free-fall contract).

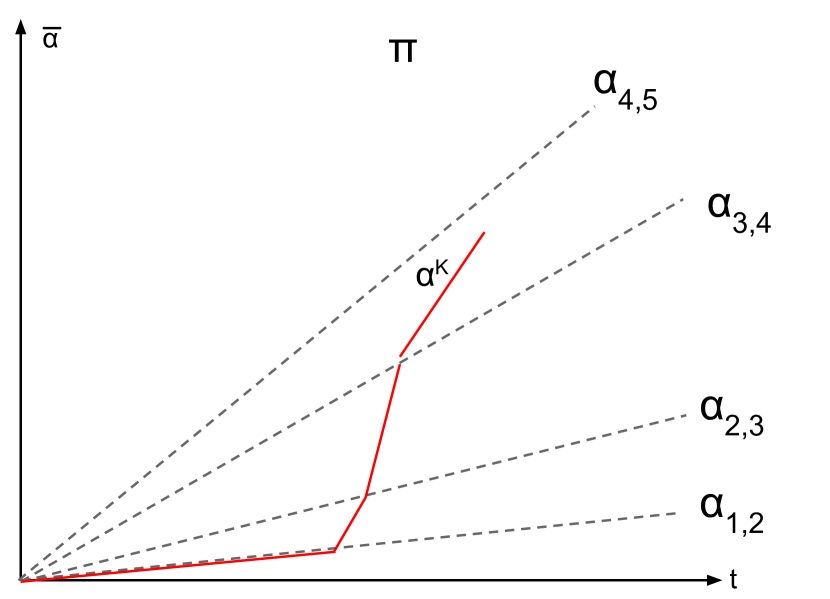

Let be the indifference contract for the best-response boundary separating the current action from the previously incentivized action. Consider replacing this segment with the two consecutive segments , . In doing so we essentially are doing the inverse of the first rewriting rule in Lemma 3.3 – replacing a single segment with two segments that average to the original segment – and because of this, the resulting dynamic contract is valid and has the same utility as our original contract (the construction also guarantees both segments stay within this region). But now we have a segment that lies along the best-response boundary , so by Lemma 3.4 we can replace it with the segment and strictly increase the utility of our dynamic contract (see Figure 5).

We can then merge this segment with the previous segment in (which also incentivizes action ) to obtain a new dynamic contract with strictly greater utility than and whose first non-free-fall action occurs strictly earlier. Repeating this process, we obtain a free-fall contract with at least the same utility as . ∎

We can now prove our original theorem.

Proof of Theorem 3.1.

From Lemmas 3.5 and 3.6 the first part of this theorem (that there exists a free-fall linear contract with ) immediately follows.

To show that we can efficiently compute this free-fall contract, note that the optimal free-fall linear contract might as well start with a segment of the form for some indifference contract (if it does not start by offering some indifference contract, we can apply the rewriting rule of Lemma 3.3 to merge this segment with the following segment, which would incentivize the same action).

It is also true that the optimal free-fall linear contract might as well end at an indifference contract: that is, for some . To see this, consider a free-fall linear contract that does not end on an indifference contract. It ends with a segment of the form for some agent action . Consider the contract formed by replacing the duration of the last segment with ; this operation is valid for all in some interval . Note that is a convex function of (it is of the form ) so it is maximized when equals one of the endpoints of this interval. But at both endpoints, lies on a best-response boundary (for , , for , ).

Since our optimal contract is completely characterized by its start and end points, it can be computed in polynomial time in by testing all the pairs of indifference points with as candidates for the start and end points of the optimal initial contract (this pair of indifference points also uniquely specifies the fraction of time that must be spent in free-fall). Note that in the case where in the optimal free-fall contract , the optimal contract is the best static contract. ∎

3.2 Implication to Welfare and Agent’s Utility

In the example shown in Section 1.2, the dynamic manipulation that the principal made degraded the overall welfare, and all the added profits for the principal were at the expense of the agent. We demonstrate that this is not always the case; there are other scenarios where dynamic manipulations by the principal, which are optimal for maximizing their revenue, can actually be Pareto improvements over the best static contract, increasing the overall welfare.

Example.

(Welfare improvement): Consider the setting depicted in Figure 1 with a slight variation where the cost of action is , with . In this case, the best static contract incentivizes action and yields a utility of for the principal and zero for the agent. However, the best dynamic contract remains the same as in the previous analysis: it starts by incentivizing action for a period of steps and then transitions to action by offering zero payments for the remaining time. This results in a utility of for the principal and zero for the agent, thereby increasing welfare by a factor of without altering the agent’s utility.

Next, we show the existence of “win-win” scenarios where optimal dynamic contracts can enhance the payoffs for both the principal and the agent compared to the best static contract. The improvement in welfare can be substantial, reaching as much as , essentially achieving full welfare. Specifically, we establish that the multiplicative gap between the utilities of the best static contract and those of the best dynamic contract can be for the principal’s utility and for the agent’s utility.

Theorem 3.7.

There exist repeated contract settings where an optimal dynamic contract improves expected welfare by a multiplicative factor compared to the best static contract, and where the agent’s expected utility improves by a factor of . Moreover, these settings have a positive measure.

Proof.

The idea of the proof is to look at games where the values for the principal when incentivizing each action are similar, but the actions differ significantly in terms of welfare. Then, by investing a small amount of additional payment in the early stages of the game (compared to the best static contract), the principal can incentivize the agent to substantially improve welfare, initially in the form of higher profits for the agent. This added welfare is then shared between the players during the free-fall stage of the dynamic. Consider the following contract game.111111 In this example we shift the rewards with an additive constant such that the reward for the principal when the agent takes the null action equals some constant instead of zero. This simplifies the following analysis and is without loss of generality: as utility functions are, in general, defined up to affine transformations, one can reduce this constant form the principal’s utility without changing the incentives in the game. There are actions, with expected reward for some . Concretely, we let . The cost of the action are specified recursively by and for , yielding . The resulting indifference contracts are thus for . In this game, the principal has the same utility (of one unit) for all the indifference contracts. The agent’s utility under the contract , as the reader can verify, is given by . Notably, this utility is higher for the higher actions. The welfare of action is thus . Next, we slightly alter this game by increasing the payoff of action by a small amount such that the optimal static contract is now , which yields a utility of for the principal, and the agent is still indifferent under this contract between action and the null action. In the following analysis, we are mainly interested in large (but finite) . Notice that the optimal static contract is extremely inefficient for large , getting an arbitrarily low (independent of ) fraction of the optimal welfare.

Now consider an optimal dynamic strategy; by Theorem 3.1, there is an optimal strategy of a free-fall form. We will construct a free-fall contract p that starts at , so action is played initially, where the duration of that stage is chosen such that the final action at time is action . Specifically, we require , and so . We show that this free-fall strategy bounds the utilities of both players from below.

Claim 3.8.

In an optimal free-fall contract, the utilities for both players are at least those obtained in the contract described above.

The proof for this claim is deferred to the appendix. It consists of three parts: first, we show that an optimal free-fall contract must start at . This is done directly by way of contradiction. Then, the proof shows that the last action that is played by the agent in an optimal free-fall contract must be higher than . The intuition for this part of the proof is that as the principal continues to free fall through lower and lower actions, the marginal gain from each action (which is the expected reward of that action because we are free falling) continues to diminish. At some point, the marginal gain is outweighed by the current average principal utility, which we show should occur at action (since we know the principal can get an average utility of and the expected reward of action is ). Lastly, we compare the utilities of both players in a free-fall strategy that begins at action and ends at action to those of the optimal free-fall strategy and observe that the utilities in the former case bound the respective utilities in the latter case from below. The principal’s utility is clearly bounded from below by her utility in our strategy due to optimality. For the agent, the total utility is determined by the stopping point. Since the agent’s utility at is increasing with in our game, we conclude that the agent’s utility in an optimal contract is at least .

Now let us calculate the average utilities for the players under our dynamic strategy, averaged over the whole sequence of play. The agent’s average utility at the last step is the same as the utility that would have been obtained under the average contract at that time, which is . To calculate the utility for the principal, we define to be the time when the agent switches from action to action . We know that the transition from action to happens at time , and until that time the principal gains a utility of one per time unit. After that time, the average contract at time is the weighted average until of the contract with weight and zero contract with weight . Therefore, the transition times from each action are given by . After time , the principal pays zero and extracts the full welfare from the agents actions, and so the overall utility for the principal is .

Claim 3.9.

The utility for the principal in the free-fall contract is

Proof.

The utility from region is . The time intervals are

The utility for the principal from region and large is thus:

Summing over such terms yields a utility of ∎

The above arguments hold similarly also for perturbed versions of this game. For example, shifting the rewards by arbitrary and independent values in the range , as well as re-scaling the reward parameter , yielding a positive measure in the parameter space. ∎

One interesting point about the example presented in the proof above is that if the agent had used a “smarter” learning algorithm that guaranties low swap regret, then the outcome of the best static contract would have been obtained (see Observation A.2 in the appendix, following the analysis of [26]). The agent in this case would have had lower utility. That is, using a better algorithm leads to a worse outcome! The explanation for this counter-intuitive result is that a mean-based regret-minimizing algorithm is only guaranteed to approach the set of Coarse Correlated Equilibria (CCE),121212In fact, for mean-based algorithms there is a stricter characterization of the set of equilibria to which they may converge [48], but the above explanation still holds. whereas no-swap-regret dynamics must approach the set of Correlated Equilibria (CE, a subset of the set of CCE’s). There are games in which some CCE distributions of play give higher utilities to the players than all CE distributions (see e.g., [35, 48] for examples in auctions, and [15] for a related example in general games). In other words – committing to use an algorithm with weaker worst-case guarantees allows, in some cases, obtaining better (non-worst-case) results.

4 General Contracts with Single-Dimensional Scaling

Next, we consider general contracts and generalize the result of Theorem 3.1 to families of one-dimensional (yet non-linear) dynamic contracts for which free-fall contracts are optimal.

Given any contract , the set of -scaled contracts are the one-dimensional family of contracts of the form for some . We will consider a principal that is restricted to only play -scaled contracts. In the continuous-time formulation of Section 2.2, this means that each contract must be -scaled. We will let , and we will often abuse notation and write as shorthand for this contract (e.g., we will specify segments of the trajectory in the form ). Recall that a free-fall contract denotes such a dynamic contract for the principal where for all .

As with linear contracts, note that as increases from , the contract incentivizes the agent to play an action in (which is unique except for at most “breakpoint” values of , where the agent is indifferent between two actions). This induces an ordering on over the actions; we will relabel the actions so that actions 1 (the null action), 2, 3, are incentivized for increasing values of . Formally, if the agent has actions, we have “breakpoints” , where action belongs to iff (with ).

The goal of this section is to prove the following analogue of Theorem 3.1, that free-fall -scaled contracts are optimal -scaled dynamic contracts.

Theorem 4.1.

Let be any -scaled dynamic contract. Then there exists a free-fall -scaled contract where .

Our proof of Theorem 4.1 will parallel our previous proof of 3.1 in the sense that we will demonstrate how to gradually transform a general -scaled contract into a free-fall -scaled contract while increasing utility for the principal. The main difficulty in applying the proof of Theorem 4.1 directly is that the rewriting rule in Lemma 3.4 no longer holds – for -scaled contracts, it is not the case that segments along a best-response boundary should always incentivize the larger action for the agent. In the proof below, we forego the use of this rewriting rule by instead using the weaker condition that we cannot have two consecutive segments along a best-response boundary (Lemma 4.3). Note that since linear contracts are a specific case of -scaled contracts, this also provides an alternate proof of Theorem 3.1.

To prove Theorem 4.1, we will establish a sequence of lemmas constraining the potential geometry of an optimal -scaled dynamic contract. We begin with some general observations on the structure of -scaled contracts and the underlying state space of the dynamic contract problem.

We begin our proof with the observation that, similar to linear contracts, -scaled contracts cannot “skip over” actions for the agent (c.f. Lemma 3.2, which has an essentially identical proof).

Lemma 4.2.

If is a -scaled dynamic contract, then for any , .

Proof.

Note that and both must be best-responses to the average historical contract after segment , which is a -scaled contract with parameter . In other words, and belong to . Since is always of the form or the conclusion follows. ∎

Now, recall that in Lemma 3.3 we show that (for general contract problems) we can restrict our attention to trajectories where no two consecutive segments have the same agent best response (i.e., for any ). The following lemma proves a strengthening of this fact specific to -scaled contracts.

Lemma 4.3.

Let be any -scaled dynamic contract. Then there exists a -scaled dynamic contract with the property that for all , and , and that .

Proof.

The fact that we can rewrite into an equivalent contract where follows from the proof of Lemma 3.3. Therefore, assume without loss of generality that already has this form. We will show how to rewrite it into a new dynamic contract with the additional property that .

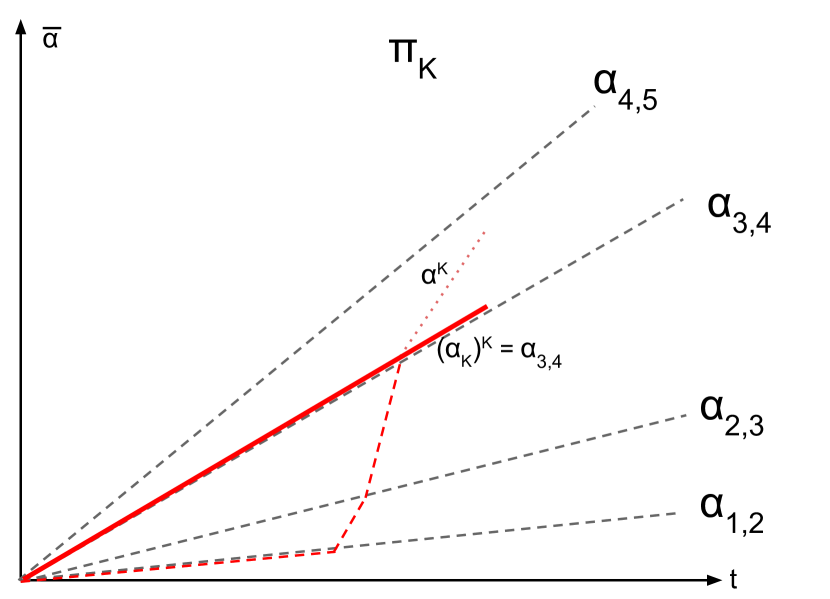

We will induct on the number of segments in the path (it is obviously true when there is only segment). Assume that for some , has the property that . This implies that . Since there is a unique value of for which (namely, one of the breakpoints ), this can only happen if , which in turn means that . Pictorially, this is because if a dynamic contract spends only one segment in a best-response region, this segment must lie along the boundary of the best-response region (see Figure 6).

Now, consider the following two modifications of :

-

1.

In , we replace the first segments of with a scaled up version of the st segment. That is, remove the first segments of and replace them with . To see that this is a valid contract, note that since , incentivizes action so the first segment of this contract is valid. Moreover, after time units have elapsed, both and resume the same sequence of segments from the same state .

-

2.

In , we replace the first segments of with a scaled up version of the first segments. That is, remove the segment , and scale up (for each ) to . Again, this is a valid dynamic contract because scaling up a (prefix of a) dynamic contract results in a valid dynamic contract, and and both resume the remainder of segments at the same time and from the same state .

Finally, note that is a convex combination of and – specifically, – and so is less than or equal to one of them. But both and have strictly fewer segments than , so by applying the inductive hypothesis, we are finished. ∎

As a consequence of Lemmas 4.2 and 4.3, we can restrict ourselves to dynamic contracts whose sequences of actions are either consecutively increasing () or consecutively decreasing (). We show that we can ignore the first case – such contracts can never be better than static contracts.

Lemma 4.4.

Let be a -scaled dynamic contract where the are consecutively increasing. Then there exists a static -scaled contract (i.e., a single segment dynamic contract of the form ) where .

Proof.

As in the proof of Lemma 4.3, we will again induct on the number of segments of . If has one segment, we are done.

Now consider a with segments, whose last segment is . Recall that for any , is the smallest value of for which incentivizes action . Note that if , we can improve the utility of the principal by decreasing to (this pays strictly less to the agent but still incentivizes the same action ). We’ll therefore assume the last segment is of the form ; note that this segment by itself is a valid static -scaled contract, as incentivizes action . Call this contract .

Let be the dynamic contract formed by the first segments of (see Figure 7 for examples of and ). But now, is a convex combination of and , so it is at most the maximum of these two quantities. If this maximum is , we are done ( is a static contract); if it is , we are also done by the inductive hypothesis ( has segments). ∎

Finally, we show that in the case where the sequence of actions are consecutively decreasing, such a contract is no better than some free-fall contract.

Lemma 4.5.

Let be a -scaled dynamic contract where the are consecutively decreasing. Then there exists a free-fall -scaled contract where .

Proof.

Assume that is not a free-fall contract. We will show we can rewrite in a way so that either the first agent action strictly decreases or the first non-free-fall occurs strictly later. Since the number of segments in is bounded (by , since the actions are consecutively decreasing), this implies the theorem statement.

Let be the first segment in with where (so, the dynamic contract is not free-falling here). Note that since this segment ends on the boundary between the best-response regions for and , .

The main observation of this proof is that we can rewrite this segment as a combination of a free-fall segment (with ) and a segment along the boundary of these two best-response regions (with ). Specifically, form a new dynamic contract by replacing in with the two consecutive segments and , where is chosen so that . Note that by doing this now has segments, where segments and are this new free-fall and boundary segment respectively. Note that we will let quantities like , , and still refer to the relevant quantities for , not .

This allows us to proceed via a similar technique as in Lemma 4.3. Consider the following two modifications of (see Figure 8 for examples):

-

1.

In , we replace the first segments of with a scaled-up version of the boundary segment of the form .

-

2.

In , we replace the first segments of with a scaled up version of the first segments (the first segments of and the free-fall segment, but not the boundary segment). Specifically, let . Then the first segments of are of the form , and the th segment of is of the form .

As in the proof of Lemma 4.3, we can check that both and are valid dynamic contracts: in particular, after units of time, they are both in the state , so the remaining suffix of is a valid extension for both contracts.

Again, can be written as a convex combination of and , specifically,

But starts at a later action than (since ), and is a free-fall contract for one further step than (since , and the th segment in also has ). This completes the proof. ∎

We can now conclude the proof of Theorem 4.1.

Proof of Theorem 4.1.

4.1 General Contracts and Free-Fall

Unlike in the linear contract setting and the single-dimensional scaling setting, free-fall contracts are not optimal in the general contract setting. In this section, we give a general contract instance with actions (3 non-null actions) and outcomes (3 non-null outcomes), where the best dynamic contract provably outperforms the best free-fall dynamic contract. The instance in question is defined as follows:

-

•

The cost vector .

-

•

The reward vector .

-

•

The forecast matrix is given by

This instance was found by a programmatic search131313The code verifying this example can be found at: https://colab.sandbox.google.com/gist/jschnei/4d067ac2892d6b7c215dcea909577c53/optimal-dynamic-contracts-minimal-example.ipynb over a large collection of instances. For this instance, we can (again, pragmatically) compute that the best free-fall dynamic contract achieves a net asymptotic utility for the principal of at most per round. At the same time, we can exhibit a non-free-fall dynamic contract for this instance that achieves a utility of at least per round.

At a high level, the verification of this example relies on the following fact: given a sequence of actions , we can construct a polynomial-sized linear program to find the optimal continuous-time dynamic (general or free-fall) contract with this specific action sequence.

The variables of this LP are the and corresponding to each action . The constraints follow from the definition of a valid trajectory of play in Section 2.2 and are as follows:

-

•

(Non-negativity) .

-

•

(Time normalization) . We normalize the total duration of the trajectory to 1.

-

•

(Beginning of segment is best response) for any . This represents the constraint .

-

•

(End of segment is best response) for any . This represents the constraint .

The objective of the LP is the optimizer utility . If we want to further impose that the contract is a free-fall contract, we can add the constraint that for .

For free-fall contracts, we have an additional constraint on what sequences of actions are possible. Note that a free-fall contract will never repeat an action – in particular, after the initial segment, the cumulative utility of each action decreases by per round, so the sequence of actions a free-fall contract passes through must be sorted in decreasing order of cost. This means there are at most sequences of actions to check, and by checking all of them we can provably compute the optimal free-fall contract for a given general contract instance.

On the other hand, it’s not clear if there are any constraints on how complex the sequence of actions for the optimal general dynamic contract can be – it is an interesting open question whether there exists any efficient (or even computable) algorithm for computing for a general contract instance. Luckily, in order to show this separation, we need only exhibit a single general contract which outperforms the best free-fall contract. In the example above, we compute the best general contract for the same action sequence that the optimal free-fall contract passes through, and observe that the general contract obtains strictly larger utility.

5 Unknown Time Horizon

Up until now, the principal has been able to take advantage of precisely knowing the time horizon. In this section, we explore what happens when the principal only approximately knows this parameter. We will consider the case where the principal knows that the time horizon falls into some range , and wants to guard against a worst-case choice of time horizon from that range. What are the trade-offs between the time uncertainty and how much additional principal utility we can get over the best static contract? To explore these concepts precisely, we make the following definition:

Definition 5.1.

Suppose we have a principal-agent problem . Let be the single-round profit of the optimal static linear contract for this problem. We say that a pair is feasible with respect to if for all sufficiently large time horizons , there exists a (potentially randomized) principal algorithm such that the (expected) profit of at any time is at least (and infeasible with respect to otherwise).

Our main result in this section is Theorem 5.2: for every principal-agent problem and any error-tolerance , it is impossible to indefinitely maintain an advantage over the optimal static contract. To be more precise, when is we know that the instance has become infeasible (for some instances, the infeasibility transition may occur much earlier). To do this we use a novel potential function argument, which shows that in order to stay a constant factor ahead of the optimal static contract, the principal must be constantly sacrificing potential (which means lowering the average historical linear contract is has offered). To complement this result, in Theorem 5.3, we show that all time ratios permit some tiny advantage over the optimal static contract. We manage to achieve at least for all problems where the optimal dynamic contract (with known time horizon) outperforms the optimal static contract. These ideas are captured in the theorems below:

Theorem 5.2.

Suppose we have a principal-agent problem . For every , there exists a such that is infeasible with respect to for all .

Theorem 5.3.

Suppose we have a principal-agent problem . If there exists a such that for any and , is infeasible, then there are no dynamic strategies that outperform the optimal static linear contract.

5.1 Extending Discrete-to-Continuous Reduction to Unknown Time Horizon

As a first step, we present a generalized version of our result that lets us convert between discrete and continuous settings, Theorem 2.4. One of the biggest differences is the introduction of this parameter which equals the multiplicative ratio . Instead of a trajectory being solely evaluated at its end time , we now care about its performance over its final interval of multiplicative width , namely .

This introduction of an interval causes another consideration: the principal might gain from appropriately randomizing over trajectories , e.g. combining a trajectory that does well in the first half with another trajectory that does well in the second half. This was not previously an issue when evaluating trajectories at a single point because some trajectory in the support must attain at least the expectation. Hence we generalize to analyzing distributions .

Finally, in order to quantify the performance of a trajectory at a certain time , we will introduce some corresponding parenthetical superscript notation. In particular, will denote the cumulative expected principal utility of trajectory from time zero to , and is formally defined as

Then the worst-case (under possible time horizons) expected (under drawing from the distribution and actions producing random outcomes) utility of the principal for distribution is given by

where each is according to the drawn trajectory .

Finally, let , where the sup runs over all distributions of valid trajectories of arbitrary finite length. We can think of as the maximum possible worst-case utility of the principal in the unknown time horizon continuous setting game.

Theorem 5.4.

Fix any principal-agent problem and . We have the following two results:

-

1.

For any , there exists an oblivious strategy for the principal that gets at least utility for the principal for all for sufficiently large .

-

2.

For any , there exists a mean-based algorithm such that no (even adaptive141414As with the known time-horizon result, this only holds against adaptive principals in the full-information setting, or if the principal is deterministic. See Appendix B.3 for details.) principal can get more than utility against an agent running for all for any .

The proof of Theorem 5.4 is also deferred to Appendix B. Given this result, questions about feasibility boil down to questions about the value of .

5.2 Proof of Theorem 5.2

Proof of Theorem 5.2.

Due to Theorem 5.4, it suffices to show that there exists some such that . This lets us focus on the continuous-time setting.

The high-level plan from here is to focus on a particular continuous trajectory apply a potential argument to it. We will then show our analysis extends to distributions for free. We will define a potential function that maps time-averaged linear contracts to potentials in . This potential is based only on the principal-agent problem . There are some peculiarities about our potential argument, relating to the passage of time. Consider a principal managing to produce a time-averaged linear contract of after units of time, and compare that with a principal that has managed to arrive a time-averaged linear contract of after units of time instead, i.e. twice the time. In terms of absolute (not time-averaged) units of profit we can extract from this point, it is twice as good to be in the latter situation. With this in mind, our proof will carefully distinguish between the raw potential and the time-weighted potential . If a principal maintains a steady time-averaged linear contract, then the raw potential will remain constant while the time-weighted potential will grow.

The purpose of the time-weighted potential is to model the ability of a principal to extract additional profit by gradually lowering time-averaged linear contract. It will be used to demonstrate that this extra profit produced by using up a finite resource, which will imply the desired theorem result.

We now give our raw potential function . We begin by writing down the linear contract breakpoints of ; without loss of generality151515Implicitly, this step prunes away all actions which cannot be incentivized by a linear contract. they are , where the linear contract leaves the agent indifferent between actions and . For notational convenience, we also define an as the minimum linear contract to incentivize the first action. We also denote the expected reward of action with . With this notation in place, our raw potential function is the following piecewise-linear function. Note that we can assume without loss of generality that the average linear contract never exceeds , because capping it to this quantity only improves principal utility at all moments in time.

The potential above is depicted in Figure 9 and can be seen as the product of the following thought experiment: what if the principal was allowed to offer unbounded payments (in particular, payments can be negative and can exceed the payment bound )? In our continuous-time setting, this gives the principal the ability to produce segments of play which have near-instantaneous times while using large-magnitude cumulative contracts to move between the boundaries between actions. If these near-instantaneous actions are used at time , then the time-weighted potential captures the necessary payments to alter the time-averaged linear contract. One interesting aside about this thought experiment is that the necessary payment to near-instantaneously move up from to the next , namely , is equal to the payout received for near-instantaneously using a negative contract to move down from to .

Potential function in hand, we return to the original problem where payments are bounded and nonnegative. Let us consider the segment of play and relate the total profit generated during this segment of play with the change in potential.

For notational convenience we define shorthand for the cumulative linear contract offered.

We will also use to denote the (time-weighted) principal utility for segment and to denote the corresponding amount of principal utility that the optimal static contract obtains over time. Using this notation, we can compute an upper bound on how much additional principal utility this segment manages to achieve over the optimal static contract.

At the same time, this contract has shifted the time-averaged linear contract and hence altered the time-weighted potential.

Interestingly, the expression for time-weighted potential has a term that perfectly cancels with our bound for how much additional principal utility this segment produces over the optimal static contract.

The right-hand side expression above is just the integral of the current raw potential as this segment advances the time from to . Conveniently, this upper bound still works out to the same amount even if we subdivide our segment into two sub-segments such that and (and re-index the other segments appropriately). This means we can sum this bound to get an overall bound for any time , just by splitting the last segment appropriately. To formalize this, we introduce some more parenthetical superscript notation to denote the corresponding objects when considering time from zero to . In particular, denotes the optimal static contract’s principal utility for units of time, denotes the cumulative linear contract for units of time.

Recall our notation where denotes the optimal static contract’s principal utility. For , we know that the excess principal utility needs to be at least , which implies the following.

With this bound in mind, we can view every trajectory that manages to successfully beat the optimal static contract by in terms of how much raw potential it has as a function of time. Note that this bound controls the current raw potential based on the average raw potential up to this point (minus a constant). As a result, if we just consider trajectories that obey this bound, the worst case for us would be a function that satisfies it with equality everywhere since greedily picking the maximum value for the function early on allow for higher values later on (greedy stays ahead). We now solve for this function which simultaneously maximizes raw potential everywhere.

At time , we know the raw potential can be at most . We want to choose and hence so that is negative in order to create a contradiction. Because yields the maximum possible function value attainable at time , this means that our actual raw potential will also be negative at . We now solve for the largest value of that does not actually create a contradiction.

Hence it suffices to pick a . This demonstrates that it is impossible for a deterministic trajectory to beat the optimal static contract by a multiplicative factor.

What about randomized dynamic contracts ? We can just take the appropriate convex combination of our bounds according to drawing . In particular, this yields:

We can then re-execute the remainder of the proof in the same way, replacing the deterministic additional principal utility with expected additional principal utility and deterministic raw potential with expected raw potential. The expected potential function is still bounded everywhere by the same function and we reach the same conclusions about . This completes the proof. ∎

Remark.