Synthetic Data Applications in Finance

Synthetic Data Applications in Finance

Vamsi K. Potluru, Daniel Borrajo, Andrea Coletta††thanks: work done while at AI Research, Niccolò Dalmasso, Yousef El-Laham, Elizabeth Fons, Mohsen Ghassemi, Sriram Gopalakrishnan, Vikesh Gosai, Eleonora Kreačić, Ganapathy Mani, Saheed Obitayo, Deepak Paramanand, Natraj Raman, Mikhail Solonin,

Srijan Sood, Svitlana Vyetrenko, Haibei Zhu, Manuela Veloso, Tucker Balch

J.P. Morgan AI Research

{vamsi.k.potluru, first.last}@jpmchase.com

Synthetic data has made tremendous strides in various commercial settings including finance, healthcare, and virtual reality. We present a broad overview of prototypical applications of synthetic data in the financial sector and in particular provide richer details for a few select ones. These cover a wide variety of data modalities including tabular, time-series, event-series, and unstructured arising from both markets and retail financial applications. Since finance is a highly regulated industry, synthetic data is a potential approach for dealing with issues related to privacy, fairness, and explainability. Various metrics are utilized in evaluating the quality and effectiveness of our approaches in these applications. We conclude with open directions in synthetic data in the context of the financial domain.

1 Introduction

Synthetic data has been receiving increased attention in the research community and beyond with the wide-spread popularity of generative models such as DALL-E [RPG+21] and GPT4 [Ope23] for the domains of image and text generation, respectively. The use of synthetic data in finance is still in an early phase and typically involves tabular, time-series, and text datasets [ADM+20]. In this work, we will primarily focus on tabular and time-series synthetic data which have wide applicability in the retail and investment banking applications such as marketing, trading, and anti-money laundering. Also, we will briefly touch upon modalities involving images and text as can be seen in applications such as check fraud and document understanding. The latter has seen tremendous uptick in financial use-cases with the introduction of chatGPT.

Synthetic data applications in finance can be primarily tagged into the following use-cases.

Data Liberation:

Data use and sharing within and outside the financial institutions is highly restrictive due to internal policies designed to protect the important relationship of trust between consumers and financial institutions and to ensure compliance with the various regulatory regimes across the globe. These are mostly concerned about the privacy and legal aspects of the customer data and they in turn lead to limits or bureaucracy for data use. Other risks include leakage of institutional knowledge which could pose a competitive risk for the bank [LWSF23, TBV23]. Certain types of synthetic data may potentially alleviate this issue and thereby speed up the adoption of AI and model development process in the firm [ADM+20]. There are many criteria for evaluating the quality of synthetic data and one such notion is that of epistemic parity [RHR+22] where the findings on the original dataset match those that are found on the synthetic dataset. Other applications include explanations where instead of using samples from the real datasets, we can generate private synthetic data [PSZ22].

Augmentation:

We can also utilize synthetic data to augment our training data for improving the performance of downstream classifiers. Intuitively, synthetic data can help robustify our training samples when the generated samples are sufficiently diverse from the original dataset. The benefits of synthetic data in image domains have been clearly established [CSK+22]. It is an open question as to in which regimes does synthetic data provide a lift for training machine learning (ML) models in tabular regimes [XSC22, MA23]. Other applications include fairness, where synthetic data can be utilized to the datasets in such a manner that the downstream fairness metrics are improved while preserving classification performance [LRD22].

Counterfactual Scenarios and Testing:

Learning machine learning (ML) models which are robust to distributional shifts is a challenging problem and synthetic data offers a way of modeling counterfactual scenarios to benchmark these models [CELT+22]. Testing robustness of ML systems is a big challenge in operations due to the wider variability of real-world data than the training data that was used to build these production systems (Section 3.4.1).

| Modalities | Models | Applications |

|---|---|---|

| Tabular | CTGAN [XSCIV19] | Fraud, AML (section 4 ) |

| Event series | Hawkes [ZJL+20] | Multi-touch attribution (section 5) |

| Automated Planning [GNT04] | Customer Journeys (section 5) | |

| Time series | TimeGAN [YJvdS19a] | Market counterfactuals (section 6) |

| Discrete time-series | Bayes Net [S+10] [TGG+22] | Asset allocation (section 2) |

| Images | ScrabbleGAN [FAEC+20] | Check OCR (section 7.1 ) |

| Documents | Bayes Network [RSV22] | Layout generation (section 7.2.1) |

The paper is structured as follows: we provide a brief review to the various synthetic data generation techniques in the literature (Section 2). This includes simulation based techniques (Section 2.1.1), various metrics for measuring the quality of the synthetic data as well as publicly available libraries for the generation. Privacy is a huge requirement in many applications and we provide a novel framework for categorizing all synthetic data into six levels (Section 3). We then consider data arising from various modalities and tackle them one by one. We start with various applications of synthetic data in the tabular settings (Section 4) and follow it up by providing succinct applications for event-series in the case of customer journeys and multi-touch attribution (Section 5). Time series is another modality which is widely prevalent in many financial applications and we provide compelling synthetic data use-cases in generation, imputation, constraint satisfaction among others (Section 6). Finally, we consider applications in unstructured data such as images and text (Section 7.2.1) for check processing and document understanding. We conclude with some of the open questions in the field.

2 Background and Related Work

Availability of data is a crucial factor for decision making in the finance domain. However, the sensitive nature of information in this domain makes access to shared data difficult. Although synthetic data offers a route to mitigate this limitation, synthetic data per se is not automatically private [JSH+22]. We devote Section 3 to discuss this important issue. In this section, we will provide a high-level overview of the various generation techniques that are available in the literature and the metrics to evaluate the quality of the synthetic data that is generated. Additional modality-specific generation models and metrics will be discussed in greater detail in the corresponding Sections 4 5 6, 7. Finally, we briefly review some popular packages for generating synthetic data.

2.1 Generation techniques

The classical method (SMOTE) for generating synthetic data for imbalanced datasets is by interpolating between the samples [CBHK02]. With the recent success of deep learning techniques in various ML tasks, it is no surprise that they work exceedingly well even for generation. In particular, models such as generative adversarial networks (GANs) [GPAM+14b], diffusion models [SDWMG15], and energy based models (EBMs) [TWOH03, DM19] have been widely successful in a wide variety of synthetic data generation tasks. They gain their flexibility from the fact that they are universal function approximators [HSW89], as well as their high capacity arising from over-parameterization. GANs have been quite successful for tabular [PWV16a], time [YJvdS19a], and image data [FAEC+20]. Recently, diffusion based models have been performing increasingly well in a variety of generation tasks, avoiding some of the training pitfalls associated with GANs [KBRB23].

Financial data can also be generated using simulators, which can be powerful for a multitude of reasons including helping with data privacy concerns, generating rare data, and their ability to incorporate expert knowledge. Simulators can be built by: (1) encoding domain knowledge into models [Cho95]; (2) learning the model directly from data (eg: deep generative models [OE18]); or (3) a hybrid method that includes expert knowledge into the model and then fine-tunes the model with data (e.g. with Bayesian Networks [AMAF19]). In this work, when we refer to simulators, we mean a program that rolls out the state of a system (its variables) over time or steps. So, simulation-based methods are mostly pertinent for time series or event-series data in finance.

2.1.1 Model-Based Simulation methods

Model-based simulation is a powerful approach for generating synthetic time series data which can leverage domain knowledge of predefined rules, and helpful assumptions for effective simulation [FHMR88]. One advantage of using such simulators to generate data is the ability to explicitly represent the underlying mechanism of data generation by incorporating domain knowledge [ATLO17]. This allowssimulators to generate data for rare or extreme scenarios [RT+09] that may not be present in the data. Rare events play an important role in financial applications [EKM13]. Such simulators also have the advantage of control and reproducibility by design, allowing researchers to replicate data generation, analyze the effect of small parameter changes, and ensure consistency.

Model-based simulators are also helpful for generating realistic datasets for downstream ML models in cases where private data cannot be released; this can be due to privacy and or regulatory constraints in finance [VL18]. With respect to privacy levels, using a simulator can offer us the highest level of data privacy, as the model can be programmed by a domain expert without referencing the data. However, if the model used in a simulator was built referencing (for example) statistical properties or cases from a dataset, then information leakage can occur and the privacy level is reduced.

As stated, simulators can be helpful in simulating potential (unseen) scenarios in markets, and also useful for testing various strategies or policies in finance. The effectiveness and realism of simulators will depend on how accurate (fidelity) the model used in the simulator captures the dynamics of the target features. This often involves a trade off between model accuracy and simplicity (affects speed and comprehensibility). A simulator needs not be highly accurate (lower fidelity) to be useful [SKB23]; as the statistician George Box put it, ”Essentially, all models are wrong, but some are useful” [BD19].

For generating such synthetic data in finance using model-based simulators, we will discuss a set of approaches that include Markov models, automated planning, and agent-based simulators [ATLO17].

Using Markov models:

The Markov assumption [Put14a, Cin13] is often used in modeling systems. By this assumption, the successor state of a system is only dependent on the current state of a system. Markov models have been extensively used to model real-world systems [Whi85, BVD17], including finance [BR11].

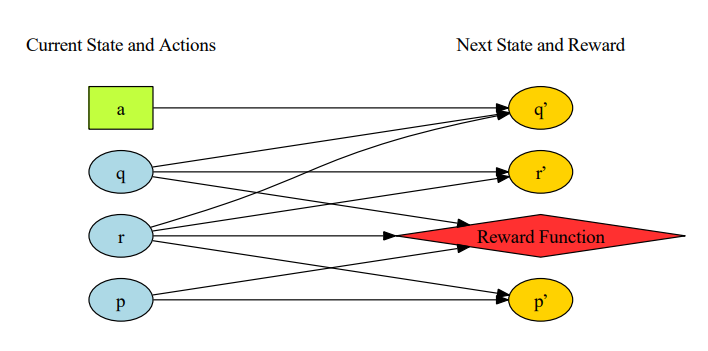

A Markov process is one in which the state evolves over time based on the current state alone, based on dynamics defined by the modeler. These processes can be used directly to simulate financial scenarios and generate data [Bra14, I+08]. Data can also be generated by including one or more agents and their behavior, or a policy of actions, in the Markov process. Agents would act in the environment (described by the model) to optimize their objectives. The data generated would then be reflective of system dynamics as well as of dynamics that emerge from the policies (actions) of agents in the environment. How these agents behave need not be explicitly modeled, and can be learned after specifying a reward function; this is what defines Markov Decision Processes (MDPs) [Put14b] and their variants. Such models are used in reinforcement learning. In addition to data generation, one can also test (investment) policies on such models and simulate unseen situations by appropriately modifying the model.

In order to define Markov models for generating synthetic data, one popular language is the Resource Domain Definition Language (RDDL) [S+10, TGG+22] which allows one to define MDPs as well as Partially Observable Markov Decision Processes (POMDPs) [Kri16]. POMDPs are a type of MDP that includes the ability to reason about state information that is not fully specified. Using RDDL to define a Markov model involves defining how the dynamics of the environment evolves over time, actions an agent may take, and a reward function. However, if one is interested in generating data purely by simulation using a particular model (a Markov process), and not by including or wanting agent behavior data, then the actions and reward function can be made irrelevant. The RDDL simulator111RDDL simulator code: https://github.com/ssanner/rddlsim222RDDL simulator in python: https://github.com/ataitler/pyRDDLGym (which runs an RDDL model) can be run to generate data. If one ignores actions and rewards, an RDDL model is essentially a dynamic Bayes net [Mur02] model. In [PMG+23] the authors give an example of using RDDL to model the problem of asset allocation and optimal trade execution.

Agent-based models:

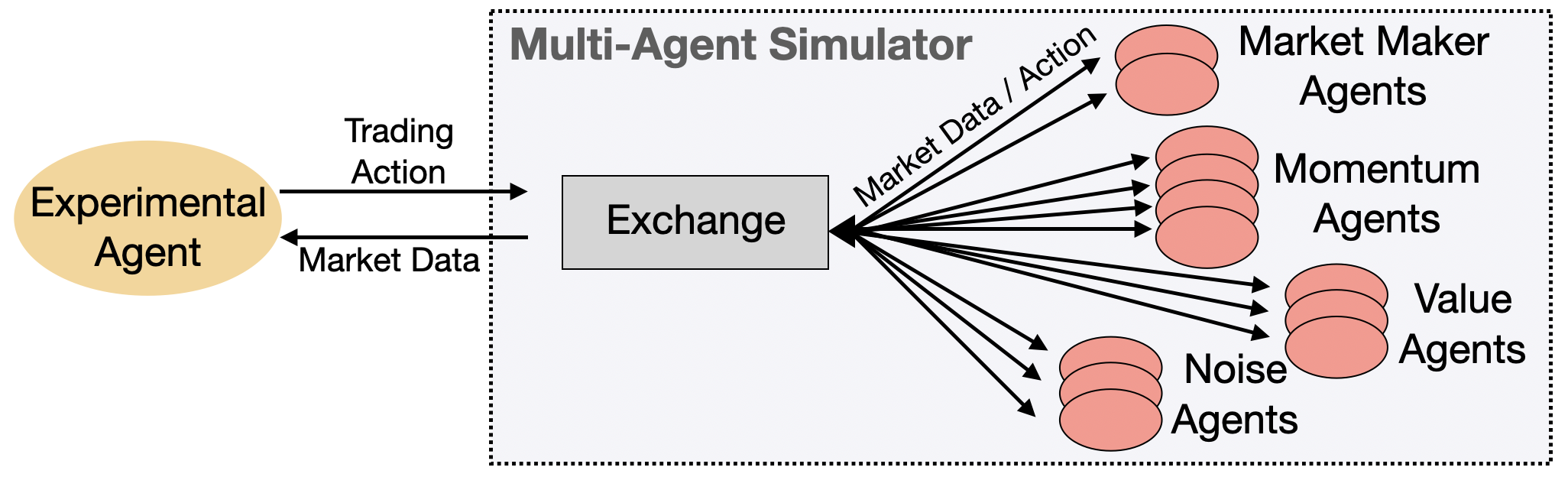

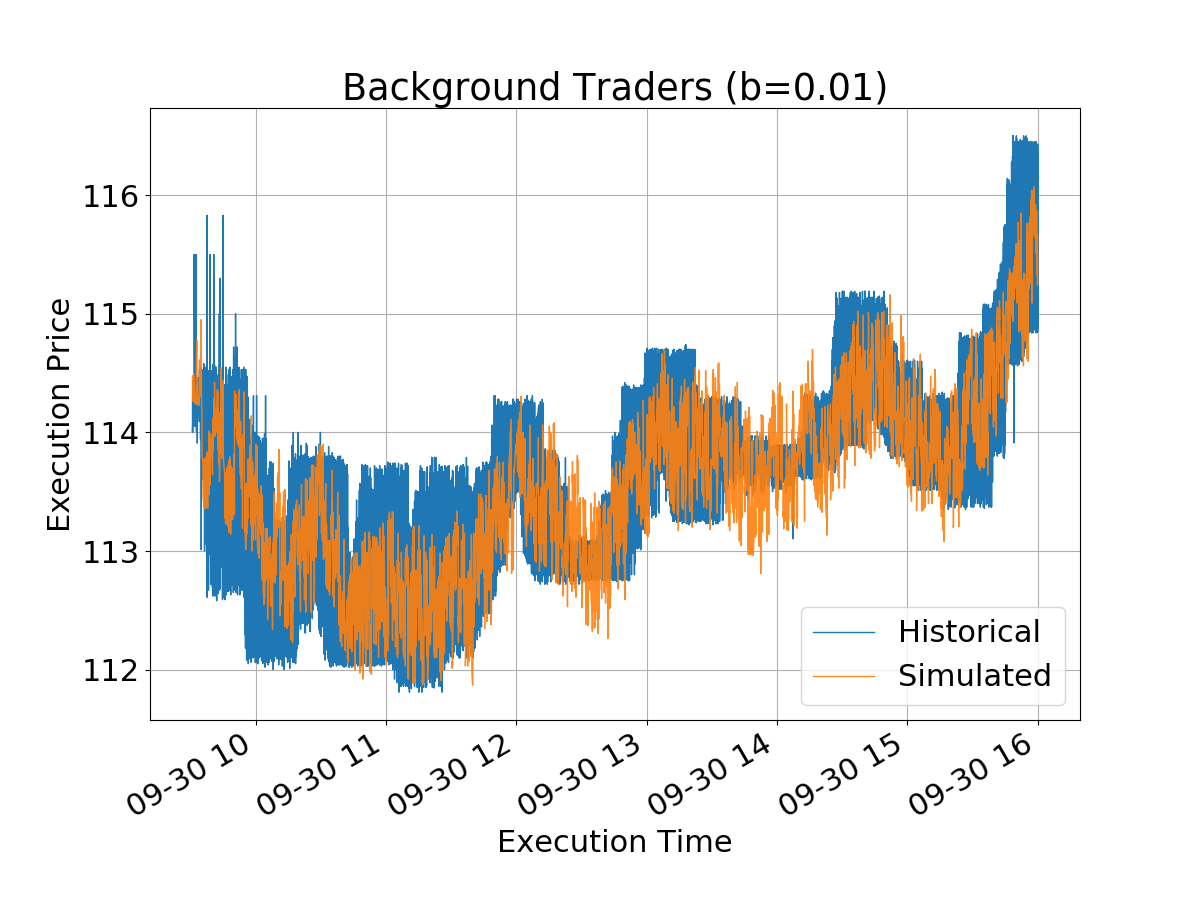

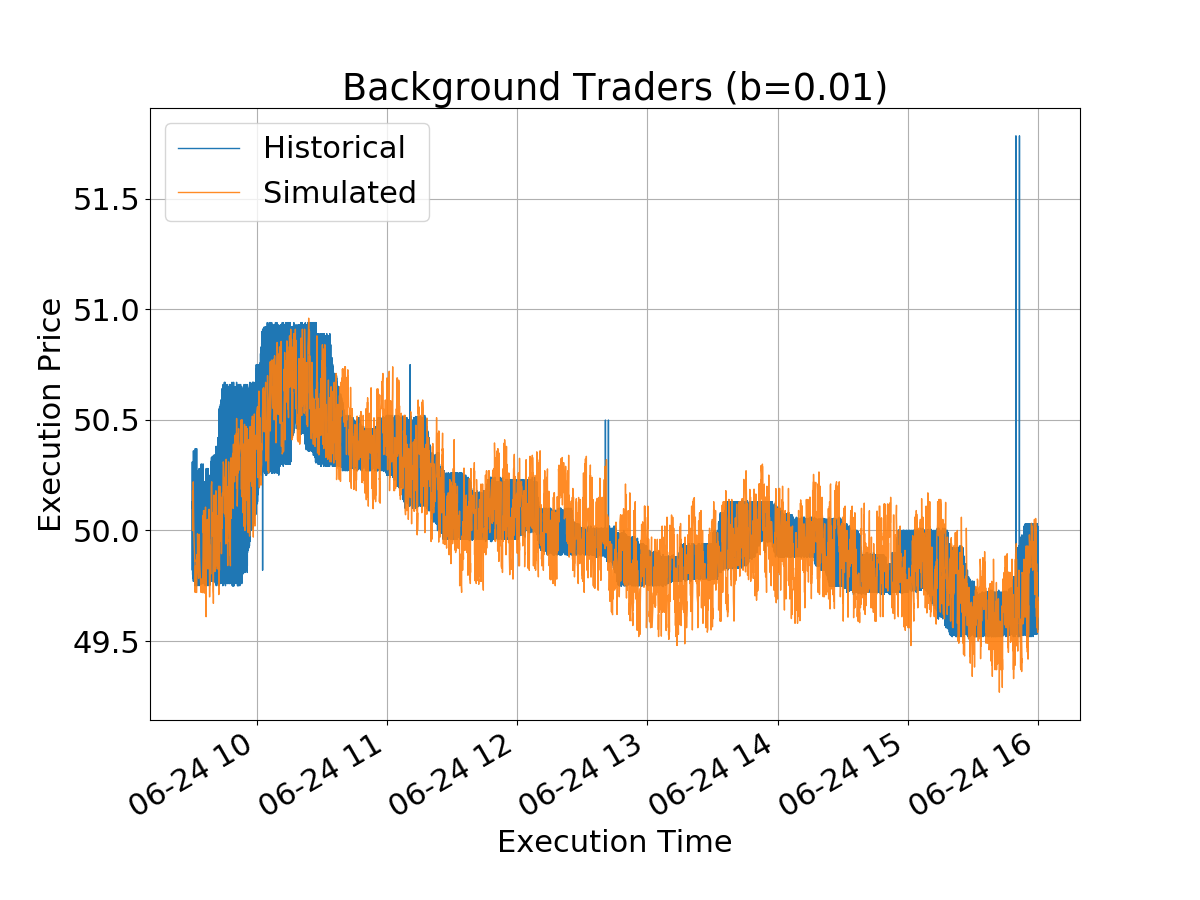

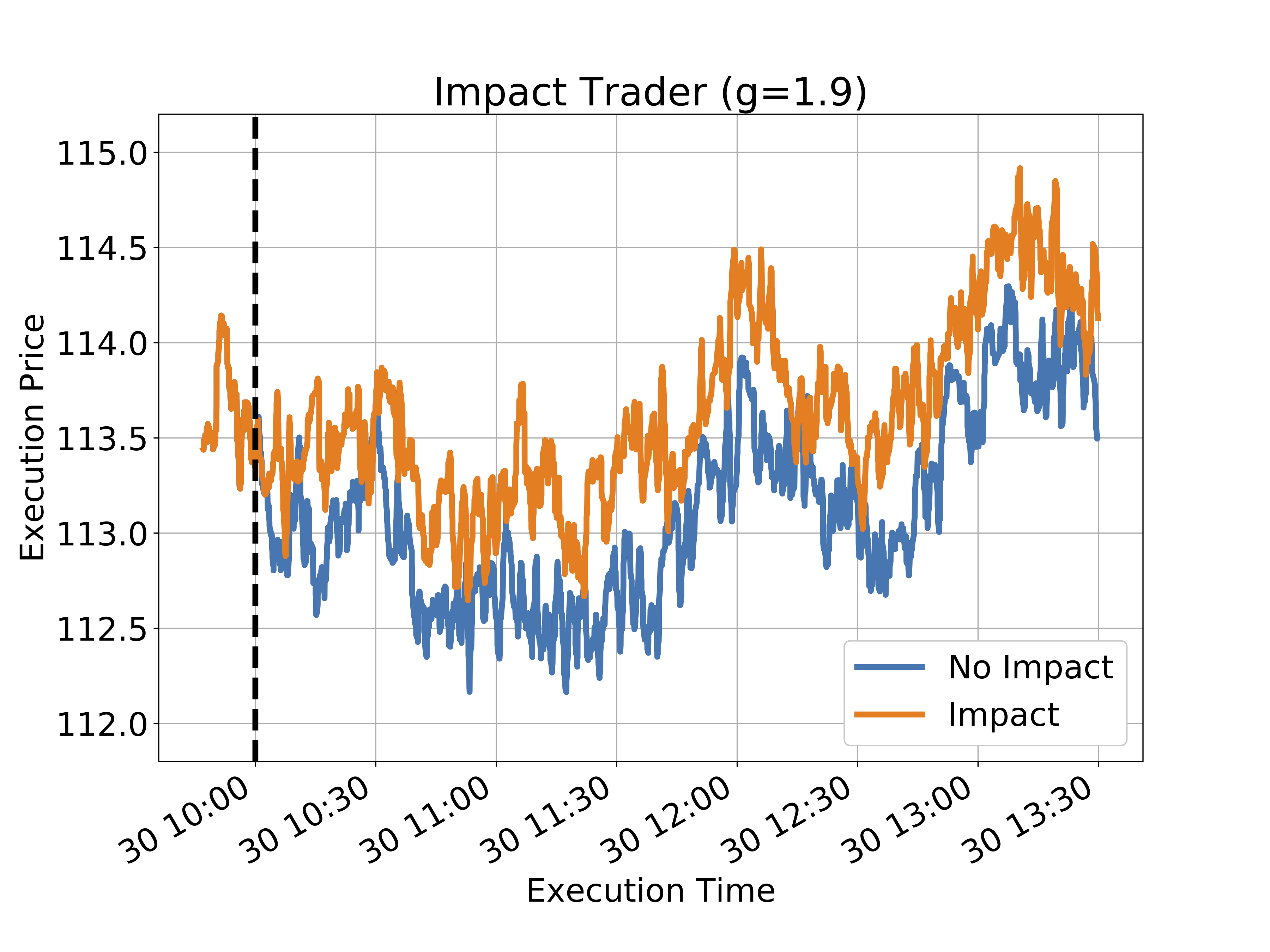

It is often necessary to test trading algorithms against the hypothetical market stress scenarios in order to ensure their robustness before deploying them in real settings. For that purpose, financial price time series are commonly simulated by stochastic processes (for instance, by an Ornstein-Uhlenbeck process as in [CK11]). However, such approaches suffer from an inability to explicitly model interactions among market agents. The knowledge of those interactions is often required to understand scenario nuances. In contrast, agent-based simulation presents a natural bottom-up approach to modeling agent interaction in financial markets [BHB19, AVG+22, Miz16]. A schematic example of multi-agent marked simulator, called ABIDES (which stands for Agent-Based Interactive Discrete Event Simulator) [BHB19], is shown in Figure 2. To emulate the real market, ABIDES defines a pool of heterogeneous agents (i.e., traders) with different strategies to mimic the real market traders. Multi-agent simulators, such as ABIDES, can be used in a forward simulation mode - i.e., to test how a trading strategy interacts with the simulated market [VBP+19]; as well as to generate synthetic series data that contains agent identity/market regime labels. For example, in [CELT+22] the synthetic time series benchmark dataset with volatility regime labels, that was generated using ABIDES, was provided to test the robustness of forecasting algorithms to distributional shifts.

2.2 Metrics

In order to evaluate the quality of our synthetic data generators, we consider various metrics utilizing both the real and synthetic samples. They can be mainly divided into three main categories:

Fidelity:

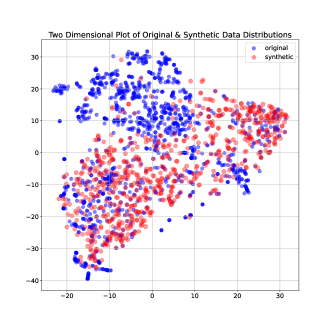

These metrics capture the distributional aspects of the synthetic data with respect to the real samples. Typical metrics include the Kolmogorov-Smirnov (KS) test statistic and Chi-Squared (CS) test which measure for the similarity for continuous and categorical variables (columns) respectively. Other distributional divergence measures include Jensen-Shannon distance, MMD, and Wasserstein distance. Specialized metrics of distributional similarity such as stylized fact comparison (e.g., similarity of price returns between real and synthetic time series) are used for financial time series [VBP+19]. Additionally, T-SNE plots provide a common way to visually check the distributional similarity between real and synthetic data in a two dimensional projection [vdMH08].

Utility:

These metrics evaluate the quality of the synthetic data as an effective proxy for real data in classification and regression tasks among others. The various downstream tasks are typically solved by using XGBoost [CG16], neural nets, or logistic regression among others. The Training on Synthetic data and Testing on Real data (TSTR) approach allows us to evaluate the usefulness of synthetic data by training a prediction or classification model on synthetic data and testing its performance on a real downstream task [EHR17b].

Privacy:

These metrics provide a measure of risk mitigation across the various types of potential attacks on the released synthetic data such as membership inference [SSS16], attribute inference [NS07], and property inference[LWSF23]. Privacy metrics such as -anonymity and -diversity, in addition to reidentification scores such as delta-presence and identifiability score attempt to quantify privacy risk.

Recently, metrics have also been introduced to account for diversity and authenticity of the generated samples [ACvdS20]. We will review additional domain-specific metrics in the corresponding data modality section.

2.3 Synthetic Data Generation with Python Libraries

There are several Python libraries available for synthetic data generation, each with its distinct capabilities and features. This section provides a detailed overview of five of these libraries—SynthCity, SDV, DataSynthesizer, Faker, and Metadata to Data—and compares them on various metrics. Each library has its own strengths, weaknesses, and unique features. Here, we provide a detailed description of each major Python library for synthetic data generation, including the aforementioned five libraries using common Python libraries like pandas, NumPy, and scikit-learn. A comparison of these libraries can be found in Exhibit 3.

-

•

SynthCity: It is tailored for the generation and evaluation of synthetic tabular data. The package has a pluginable architecture, and it encompasses a wide array of reference models, ranging from GAN-based methods to Bayesian Networks, with specialized tools for time series, survival analysis, and privacy-centric synthesis.

-

•

SDV (Synthetic Data Vault): A Python framework focused on the generation and evaluation of synthetic tabular, multi-table, and time series data. Harnessing a combination of state-of-the-art machine learning models, SDV provides capabilities and data synthesis across diverse use-cases while ensuring that generated datasets closely resemble original data in structure and statistical properties.

-

•

DataSynthesizer: This Python-based tool designed for the creation of synthetic datasets, with an emphasis on preserving data structure while ensuring privacy. Leveraging differential privacy and other techniques, it offers a balance between data utility and privacy, making it an optimal choice for researchers and practitioners concerned with data anonymization.

-

•

TGAN (TableGAN): A specialized generative adversarial network (GAN) tailored for generating synthetic tabular data. Merging the capabilities of deep learning with the nuances of structured data, TableGAN enables the creation of high-quality synthetic datasets, preserving intricate data patterns and relationships while offering an alternative to traditional data augmentation methods.

-

•

Faker: A lightweight library primarily used for creating fake data for testing purposes. It can rapidly generate large volumes of data in a variety of formats. While Faker does support complex data types, it does not provide advanced features like data anonymization, or correlation modeling.

-

•

Metadata to Data (using Python libraries like pandas, NumPy, scikit-learn): This approach involves generating synthetic data based on the metadata of a given dataset. It uses common Python libraries, making it highly flexible and customizable to specific needs. The functionality of this approach heavily depends on the specific implementation, but it can potentially support all functionalities, including complex data types, correlation modeling, and data anonymization. It also provides the freedom to optimize performance based on the specific requirements and computational resources available.

| SynthCity | SDV | Data Synthesizer | TGAN | Faker | Metadata to Data | |

| Spatially Aware Data | ✓ | Variable | ||||

| Data Anonymization | ✓ | ✓ | Variable | |||

| Supports Complex Data Types | ✓ | ✓ | ✓ | Variable | ||

| Statistical Similarity | ✓ | ✓ | ✓ | ✓ | Variable | |

| Advanced ML Models | ✓ | ✓ | Variable | |||

| Correlation Modeling | ✓ | ✓ | ✓ | Manual | ✓ | |

| Performance | High | Variable | Variable | Variable | High | Variable |

3 Privacy

We begin this section by discussing risks posed by data sharing that are specific to the financial domain. We next review privacy attacks studied in machine learning literature. We then discuss the relationship between the privacy risks in the financial domain and the privacy attacks. Finally, we discuss various levels of (privacy) defense that can be applied to the original data or embedded into the synthetic data generation process, and the protection these provide in the context of privacy attacks. We refer to these levels as privacy levels.

3.1 Privacy risks in the finance domain

In financial institutions, data sharing between various lines of businesses within the institution as well as externally is governed by various regulations and internal guidelines that are put in place to protect clients’ sensitive information and protect firms from MNPI (Material Non-Public Information), litigation, reputation, and competitive risks. In this section, we review some prominent risks and relevant regulations in this space.

Fair Credit Reporting Act (FCRA)

This act requires that information collected by consumer reporting agencies (e.g. credit bureaus) cannot be provided to anyone who does not have a purpose specified by the FCRA. In particular, it is not enough to only remove from the data fields that identify an individual. In addition, one needs to ensure that the identity cannot be revealed using other data fields, outcome of an algorithm used on the data, and/or publicly available information.

Regulation on Unfair, Deceptive or Abusive Acts or Practices (UDAAP)

Sharing and certain uses of identifiable data may be sensitive to consumer or a client, and it thus represents potential UDAAP risks if used or shared in a manner contrary to elections made by, or representations made to, consumers or clients. In particular, in many settings sharing identifiable data is subject to privacy elections made by consumers.

Litigation risks

Inappropriate release of data or functions of data (e.g., models trained on data, insights from data, or synthetic data resembling these datasets) that reveal personally identifying information or statistics (a.k.a. global characteristics) of the data, may pose litigation risks. This is particularly prominent in the context of data sourced from external vendors: use of such data is typically bounded by contracts that precisely define the scope of the use.

Competitive risks

Publishing data that resembles characteristics of a firm’s client base or industries and publicly traded companies the firm has interest in, may pose competitive, antitrust and increased insider trading risks. This holds even if the published data is synthetic.

3.2 Privacy attacks in machine learning literature

ML models and their outputs are vulnerable to various privacy attacks [SZZ+23]. The basic assumption of a privacy attack is the existence of a maliciously intentioned adversary who aims to elicit some private information based on the model output. In this paper, we focus on the model output in the form of synthetic data. Privacy attacks come in various flavors. Each distinct attack is characterized by a set of assumptions; e.g. what information is available to the adversary, what information needs to be protected, what is the goal of the attack, etc. Here, we briefly overview some of the most relevant attacks, in the context of privacy risks in the domain of finance (see Table 4).

Membership inference attacks (MIAs)

In many cases, the presence of an individual’s data in a dataset by itself can reveal sensitive information. The adversary’s task in MIA [SSS16] is to successfully infer whether an individual was present in the training dataset or not, based on the output of a data processing procedure (e.g. an ML classifier or a synthetic data generator). Moreover, an adversary with the knowledge of an individual’s presence in the dataset can further use linkage attacks (reconstruction attacks) to identify sensitive attributes of that individual. For example, if all data columns matching public information of an individual correspond to an entry in the dataset with a given private attribute, the presence of the individual in the dataset reveals that private attribute for that individual. Thus, MIA can be used as a stepping stone to launch other types of attack.

Reconstruction attacks (attribute inference attacks)

Reconstruction attacks are characterized by an adversary who is in possession of partial knowledge of a set of features with the aim to recover sensitive features or the full data sample. A notable example of an attribute inference attack is the one where an adversary relies on a public set of (non-sensitive) attributes in order to infer values of a sensitive attribute [NS07].

Property inference attacks

Property inference represents the ability to extract properties of the original dataset based on the corresponding synthetic data. In general, property inference covers learning of any summary statistic of the original data (e.g. mean value, quantiles, histograms, etc.) under the assumption of the access to synthetic data. Preventing property inference attack necessarily degrades fidelity of the synthetic data [LWSF23].

| FCRA | UDAAP | Litigation Risk | Competitive Risk | |

| Membership Inference Attack | Applicable | Applicable | Applicable | N/A |

| Attribute Inference Attack | Applicable | Applicable | Applicable | N/A |

| Property Inference Attack | N/A | N/A | Applicable | Applicable |

| Model Inference Attack | Applicable | Applicable | Applicable | Applicable |

3.3 Defences against privacy attacks

In this section, we review some defenses against privacy attacks. Note that the list is non exhaustive. Moreover, we propose a novel hierarchy of defenses against privacy attacks we refer to as privacy levels.

Anonymization/PII obscuration

There is a wide range of techniques that rely on personal identifiable information (PII) obscuration or anonymization of sensitive fields (e.g. full or partial masking of characters, mapping of categories into codes, etc.). These are however generally prone to linkage attacks, and thus they do not provide formal guarantees against privacy attacks [NS07].

Randomization

Randomization is a data swapping technique that aims to provide plausible deniability by making it impossible for an adversary to infer any information regarding the data with absolute certainty. It involves swapping values of certain (or all) data points between unique individuals in the dataset. Randomization often aims to provide privacy while preserving the utility of the downstream task (or the accuracy of a query from the dataset) to an acceptable degree.

Differential privacy

Differential privacy [DR+14, ABG+23] as defence belongs to the family of randomization techniques. It provides theoretical guarantees that a potential adversary with the knowledge of an algorithm’s output (e.g. synthetic data) is not able to distinguish with certainty whether a particular individual was present in the input dataset (e.g. original data). More precisely, let represent the universe of datasets consisting of entries. We say that two datasets are neighbouring if they differ in exactly one data entry, i.e. individual. Let represent a mechanism that takes as an input a dataset from and provides an output, e.g. a synthetic dataset. We say that is -differentially private if for any two neighbouring datasets and and any set of outcomes of mechanism we have

| (1) |

For and small values of , -differential privacy guranatees that for any run of the mechanism, any output is almost equally likely to be observed on any neighbouring database. On the other hand, -differential privacy guarantees that for all neighbouring datasets the absolute value of privacy loss is bounded by , with probability at least . We are now ready to introduce our privacy framework.

3.4 Privacy levels: synthetic data generation techniques as privacy defenses

In this section, we propose a six-level privacy defense hierarchy and discuss the privacy attacks, utility implications, and potential privacy guarantees for each level. Each level corresponds to a category of defense mechanisms. This is important when reviewing what individuals and businesses want to do with existing data. In practice, we would look to apply the corresponding privacy level to the specific use case in order to achieve the business goal, with security and speed being the two primary benefits to the business. Note that there is still not a widely accepted definition of synthetic data [JSH+22].

| Level 1 | Level 2 | Level 3 | Level 4 | Level 5 | Level 6 | |||||||||||||

| Obscure PII |

|

|

|

|

|

|||||||||||||

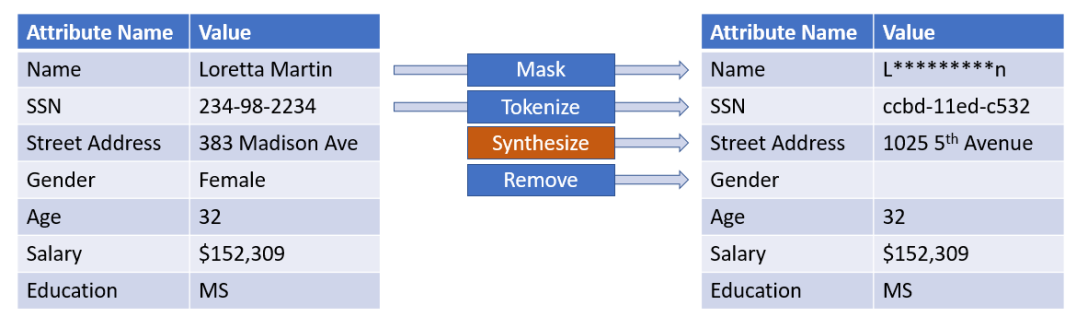

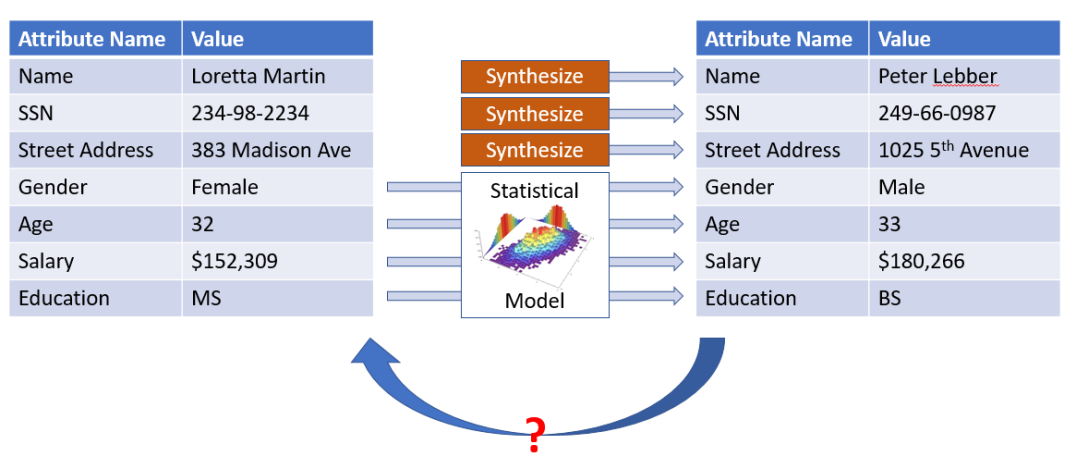

Level 1: Obscure PII

Examples of mechanisms at this level include dropping, replacing, masking, or anonymizing of the PII attributes. Since this approach does not modify non-PII attributes in any way, it will not impact the utility of downstream tasks and thus there is no utility degradation. This however represents weak privacy protection as data remains vulnerable to linkage attacks (see Figure 6 for an illustrative example).

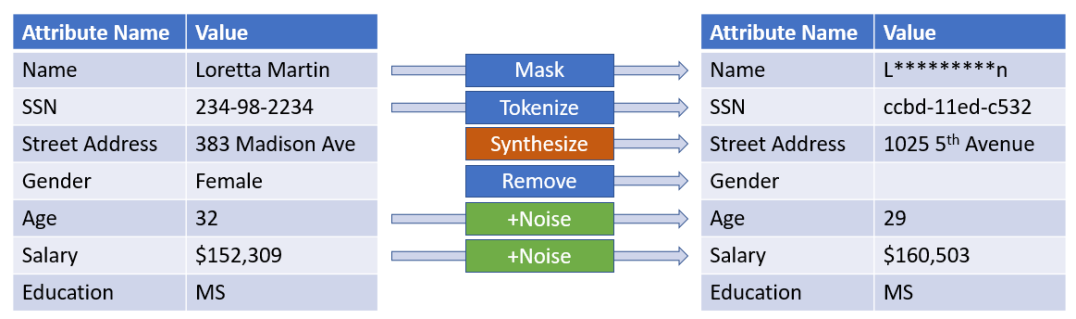

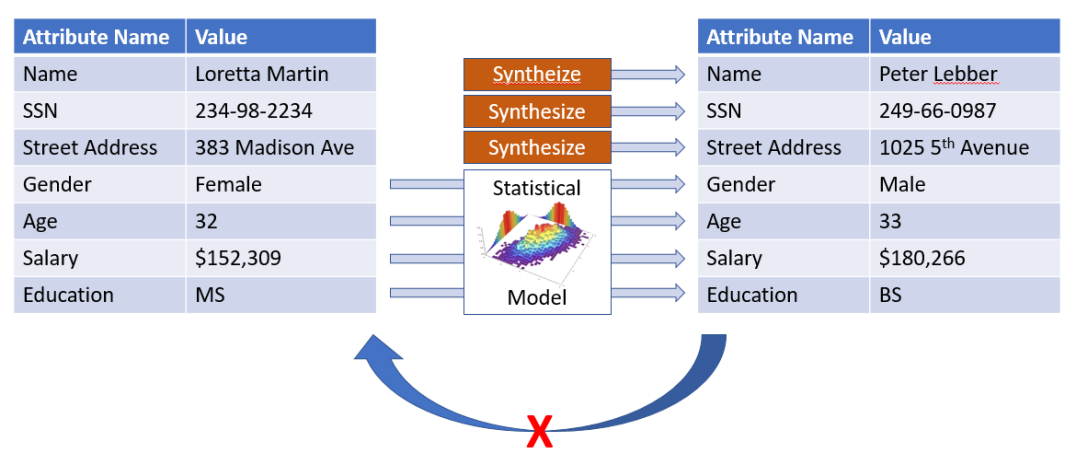

Level 2: Obscure PII + Randomization

In addition to obscuring PII columns, we add deliberate noise to other attributes or carefully randomize the algorithm applied to the data (algorithm could be a query from the dataset, train a machine learning algorithm, etc.). Depending on the amount of noise and the downstream task, some degree of utility degradation is expected (see Figure 7 for an illustrative example).

Level 3: Generative modeling

Many ML-based synthetic data generation approaches such as Gaussian copula, GAN copula, etc. fall in this category [PWV16b, GPAM+14b, PMG+18]. These methods typically do not have strong privacy guarantees (see Figure 8 for an illustrative example).

Level 4: Generative modeling + Randomization

Randomizing the synthetic data generation process by adding deliberate noise to the input data (the real data), the synthetic data generation algorithm, or the output (synthetic data). Utility degradation depends on the synthetic data generation approach, the amount of injected noise, and the downstream task. This approach has the potential to achieve strong protection against MIA. In particular, synthetic data generation methods that provide DP guarantees belong to this class [ADR+19, XLW+18, YJvdS19b] (see Figure 9 for an illustrative example).

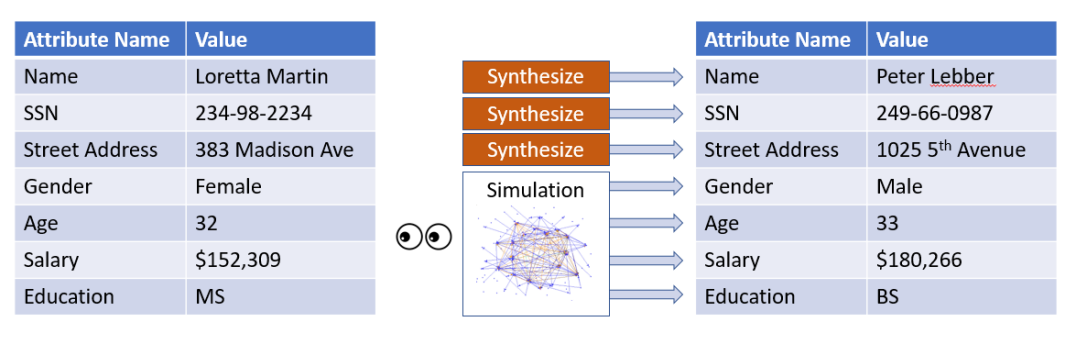

Level 5: Simulation-based synthetic data generation calibrated on real data

In this approach the data generation model is not trained on real data. In fact, there is no learning in this approach. This approach relies on simulations governed by rules to generate synthetic data. These rules, however, are calibrated such that the generated data follows some statistical properties of the original, real dataset. Utility degradation depends on the downstream task and the simulation framework. This approach generally represents a strong defence, except in the context of PIA attacks, since the simulator is calibrated with respect to statistical properties of the real dataset (see Figure 10 for an illustrative example).

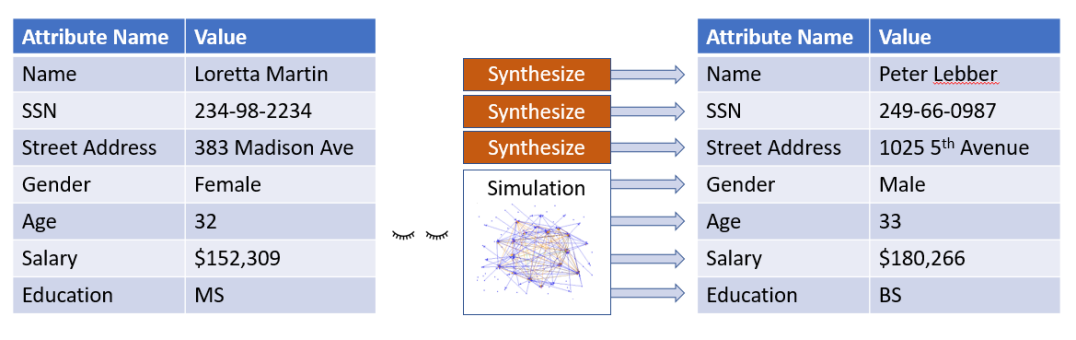

Level 6: Uncalibrated simulation-based synthetic data generation

Uncalibrated simulation has no related statistical properties to the original real dataset, meaning that the population-level statistics from the original dataset are not revealed. In general, this method yields a strong privacy guarantee given the severe utility degradation. This method of data creation requires the user to define the metadata of the original data, describing the column names and the values in those columns. Given the uncalibrated nature of this level, different data distributions to that of the original dataset are used, strengthening the defence of the synthetic data. This approach remediates one of the consequences of level 5 generation of defence against PIA attacks, given that the statistical properties of the data are uncalibrated to the real dataset (see Figure 11 for an illustrative example).

3.4.1 Privacy Levels to Guide Synthetic Data Use Cases

The creation of these privacy levels has the benefit of being transposed across business use-cases. Levels one and two lend themselves to use cases around sharing data after removing the confidential elements of the original dataset. Levels three and four translate well to improving AI models, be that through augmenting the original data, or testing AI models. Finally, levels five and six can support software engineers in testing applications among others. We will see additional level five synthetic data applications in the time-series Section 6 using ABIDES. Level 6 data in particular can be utilized for software testing, proof of concepts, hackathons, stress testing business rules in applications, and data migrations among others.

Case Study: Stress Testing Software Applications

A common challenge in the software engineering space is stress testing applications to better understand performance. For financial systems, market volatility can cause unexpected increases in the volumes traded, when unexpected events occur, such as Brexit or the outbreak of Covid-19, which saw abnormal increases in the volume of trades. To better understand how the supporting technology will function when such events occur, it is important to test these types of scenarios before they occur to ensure stability of these systems. Using production data for testing is not feasible due to privacy concerns.

We created level calibrated simulation-based synthetic data to contain similar statistical properties, while removing all records of confidential data in the generated dataset. Millions of rows of data were generated in order to test the application if a sudden spike in trades were to occur. This enabled a streamlined approach to stress testing that had previously not existed.

4 Tabular Data

In this section, we focus on one of the most ubiquitous type of financial data, namely tabular data, and in particular synthetic data generation, privacy, fairness and robustness of downstream classifiers.

4.1 Generation

Real-world domains are often described by what we call tabular data, i.e., data that can be structured and organized in a table-like format. Synthetic data generation of these types of datasets is vital as it resolves data scarcity and quality concerns by providing synthetic data that preserves the overall statistical properties and relationships among the attributes of the original dataset (Figure 12). Synthetic data enables testing new ideas without compromising real data, blending multiple sources, and protecting individual privacy when sharing [VVdB17, TWB+21]. However, major questions arise from the use of synthetic data. Particularly, is there a major cost that comes with replacing the original training data with the synthetic data we generated? To address this question, the development of a framework to mitigate performance degradation is indispensable.

Recent work [ET08] shows that there are various approaches to model tabular data distribution: statistical-based [LZF20], machine learning-based [CR10], Bayesian network-based [GBR21], neural network-based [PMG+18]. Each of these methods for synthetic data generation possesses unique capabilities and features. The appropriate method depends on many factors such as the distribution of the observed data or the objective of generating the synthetic data. For instance, statistical-based approaches prove advantageous when dealing with known marginal distributions. Due to this, reaching consensus on which method we should use for a specific dataset and use-case remains challenging. Recently, a potential solution for model selection was proposed by using Bayesian optimization [HNSOP23].

We review three popular neural network-based models namely, TVAE, conditional tabular GAN (CTGAN) and CopulaGAN. Since the original GAN formulation [GPAM+14b], ongoing research has proposed new optimization strategies and modifications to address limitations found on GANs. One of these GAN models, that builds on the success attained by previous architectures, is CTGAN. It uses mode-specific normalization to capture non-Gaussian and multimodal distributions [XSCIV19]. This model also introduces a conditional generator and training by sampling to deal with challenges imposed by highly imbalanced categorical columns and sparsity of one-hot-encoded vectors, which is a limitation of previous GAN architectures. CopulaGAN is a variation of CTGAN which takes advantage of the cumulative distribution function (CDF)-based transformation. The other neural network approach called TVAE [XSCIV19] is based on variational autoencoders (VAE). Synthetic data generation can also be achieved by treating each table column as a random variable, modeling a multivariate probability distribution, and sampling from it using statistical-based methods. This approach, known as GaussianCopula [MV12], is based on copula functions which are mathematical functions that allow us to describe the joint distribution of multiple random variables by analyzing the dependencies among their marginal distributions [PWV16a]. This is used to model the covariances among features in addition to the distributions [LM22]. Beyond these approaches, synthetic data can also be synthesized by inferring the domain of each attribute, deriving a description of the distribution of attributes in the dataset and sampling from the probabilistic model in the dataset description. This method is called DataSynthesizer (DS) [PSH17].

4.1.1 Optimization Method

Most of synthetic generation approaches mentioned earlier are “unsupervised” in the sense that they do not take into account the downstream task. Most of the approaches discussed earlier treat the label variable like other covariates. The primary focus of these approaches is to create models that are “similar” to original datasets. This creates a conflict in some use cases where the primary objective is optimizing for downstream predictions as opposed to achieving similarity to the original data. We propose a novel synthetic data generation framework, Supervised and Composed Generative Optimization Approach for Tabular data (SC-GOAT) [HNSOP23], which incorporates a supervised component and optimizes directly on the downstream loss function to address the aforementioned issues. This approach comprises of two steps. In the first step, we incorporate a supervised component customized for the specific downstream task leveraging a Bayesian optimization approach to fine-tune the hyperparameters related to the neural networks. For the second step, we adopt a meta-learning approach to identify the optimal mixture distribution of the existing synthetic data generation approaches. Therefore, the SC-GOAT approach generates synthetic data based on the mixture of multiple synthetic data generation approaches we mentioned earlier.

| Data set | Label | Observation | Continuous | Binary | Multi-class | Label = 0 | Label = 1 |

|---|---|---|---|---|---|---|---|

| Credit Balanced | ’Class’ | 50,000 | 30 | 1 | 0 | 66.70%% | 33.3% |

4.2 Application: Credit Card Fraud

In this section, we investigate our generative models in terms of the utility of using machine learning for fraud detection.

Data:

To showcase the usefulness of synthetic tabular data, we use the credit card fraud dataset333Data available on the Kaggle platform at https://www.kaggle.com/datasets/mlg-ulb/creditcardfraud. The dataset contains transactions collected in the span of two days made by European cardholders for the month of September 2013. The dataset is highly imbalanced, containing 492 frauds out of 284807 total transactions, a 0.172% of all transactions. The credit card fraud dataset contains only numerical input variables with a total of 31 features. With respect to confidentiality and privacy, 28 of the features - V1 to V28 are principal components obtained by using PCA. ’Time’, ’Amount’, and ’Class’ are the only features not to be transformed with PCA. ’Time’ contains the seconds elapsed between each transaction and the first transaction in the dataset. ’Class’ is the target variable which takes the value of 0 for cases of no fraud and 1 for cases of fraud. And ’Amount’ is the transaction amount. Given the class imbalance ratio of the credit fraud dataset, we processed the dataset by oversampling the minority class with random undersampling of the majority class, leading to a more balanced dataset. This involved duplicating examples in the minority class in order to reach an equal balance between the minority and majority class. We used Synthetic Minority Oversampling Technique (SMOTE) [CBHK02]. The dataset descriptions are summarized in Table 13.

| Synthesizer | Class Frauds (1) | Class No Frauds (0) |

|---|---|---|

| Original | 33.33% | 66.67% |

| GaussianCopula | 41.9% | 58.1% |

| CopulaGAN | 74.76% | 25.24% |

| CTGAN | 74.76% | 25.24% |

| TVAE | 40.07% | 59.93% |

| EmpiricalCopula | 33.81% | 66.19% |

| DS 0 | 0.173% | 99.83% |

| DS 0.1 | 45.47% | 54.53% |

| SC-GOAT | 36.10% | 63.90% |

Evaluation:

To evaluate the synthetic data generated, various benchmarking approaches are available allowing flexibility in adapting the loss function to suit the specific objectives of synthetic data generation. In this paper, we will adopt a downstream approach to evaluate the generative models. We will use our generative models to generate synthetic data from the original dataset, train and test our datasets on fraud detection models, and evaluate this via the AUROC metric. This serves as a well-rounded metric to assess the models’ overall performance. From this analysis, we can decide on the best synthetic data generative models, and select the best fraud detection models.

| Untuned | Tuned | |||||||

|---|---|---|---|---|---|---|---|---|

| Method | average | std | test statistic | p-value | average | std | test statistic | p-value |

| Gaussian Copula | 94.45% | 0.01 | 14.10 | 0 | 94.45% | 0.01 | 14.31 | 0 |

| CTGAN | 95.34% | 0.01 | 16.21 | 0 | 95.93% | 0.01 | 13.15 | 0 |

| CopulaGAN | 95.50% | 0.01 | 14.18 | 0 | 96.41% | 0.01 | 7.80 | 0 |

| TVAE | 98.52% | 0.00 | 0.00 | 0.5 | 98.48% | 0.00 | 0.00 | 0.5 |

| SC-GOAT | 98.52% | 0.00 | - | - | 98.48% | 0.00 | - | - |

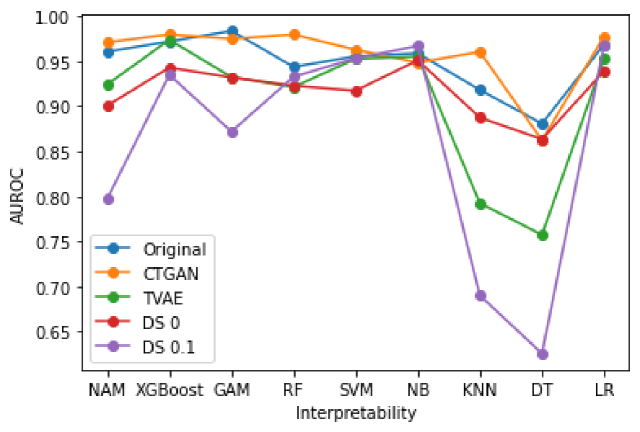

Table 14 reports the level of balance of various synthetic datasets generated from different approaches without conditional sampling for one experiment. The datasets generated by CTGAN and CopulaGAN synthesize a more imbalanced dataset that is dissimilar from the original dataset. The other approaches, TVAE, GaussianCopula and EmpiricalCopula synthesize datasets that are more similar to the original dataset in terms of class balance. Figure 15 shows a comparison among the performance of the original data and the synthetic data. This chart shows the AUROC results of different models for the data generated with different approaches. The original dataset performs the best for GAM and decision tree models. CTGAN and TVAE, which happen to be neural-network based generative models, improve the results for XGBoost. Therefore, in the fraud detection scenario, when training data synthesized by neural network approaches, XGBoost performs better at distinguishing between fraudulent and non-fraudulent cases.

Given the positive results of using the XGBoost model, another experiment was performed solely by training an XGBoost classifier [CG16] on the training data set and subsequently evaluating its performance on a separate validation data set. Table 16 shows the AUROC results between the various approaches. The results are reported based on 10 runs of the experiment with 70% of the real data used for training, 20% for validation, and the remaining 10% for testing. The SC-GOAT [HNSOP23] approach outperforms all other approaches by identifying the optimal mixture distribution of existing synthetic data generation methods.

4.3 Privacy

As previously discussed, privacy preservation of data in the financial domain is crucial in order to assure compliance with the relevant privacy regulations. A vast body of financial data is presented in tabular format, and thus privacy-preserving generation of synthetic tabular data is a particularly relevant topic in ML for finance.

Privacy considerations in the tabular setting typically assume that the data consists of a number of independent individuals represented by rows of the table, each of which is characterized by a number of attributes contained within the columns of the table. There are various angles of privacy concerns in this setting, and we review the most prominent ones. Often one requires protection of sensitive attributes represented by values within a subset of columns [SSW11]. This is relevant not only in the context of publishing the original dataset, but also any output based on the original dataset input (in particular its synthetic data counterpart) that would enable learning of sensitive attributes [NS07]. Another usual requirement is to protect global statistics of the datasets, such as quantiles or correlations [LWSF23]. Finally, most literature on privacy in tabular data quantifies it with respect to its ability to successfully perform MIA, i.e. correctly identify which individuals were present in the original dataset [SSS16]. As previously discussed, a de facto standard differential privacy represents a defense against MIA. In the remainder of this section, we review existing approaches for differentially private generation of tabular synthetic data.

In the space of statistical-based methods for tabular data, differential privacy is typically achieved by employing perturbation with the use of e.g. the Laplace mechanism [LXJ14, ADR+19]. Marginal-based methods [TMH+22] rely on low order marginals in order to fit a graphical model, e.g. PrivBayes [ZCP+17] and PrivSyn [ZWL+21]. Recent work in the area of private synthetic data generation mainly focused on deep generative models which utilize the DP-SGD framework in order to achieve privacy [ACG+16]. Some prominent examples of this line of work are DPGAN [XLW+18], PATE [PAE+17], PATEGAN [YJvdS19b], DPCTGAN and PATECTGAN [RLP+20]. These approaches however lack interpretability which is of crucial importance in the finance domain. Some recent works that focus on interpretability rely on space partitioning techniques together with noise perturbation in order to achieve differentially-private synthetic data [KNP+23]. We have also explored privacy in diffusion models for tabular data [WKW+23]

4.3.1 Privacy in Credit Card Fraud Use case

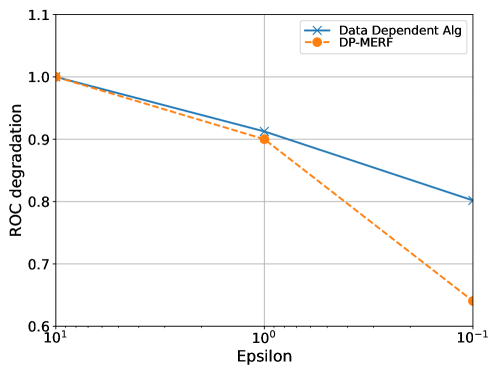

Our goal is to demonstrate the trade-off between the extent of privacy protection (measured by the scale of noisy perturbation) and the utility of synthetic data in the context of a downstream task. We consider two algorithms that output DP synthetic data based on the original data input: the data-dependent algorithm from [KNP+23] which relies on space partitioning and noisy perturbation, and deep learning based DP-MERF [HAP21].

Dataset:

We use a credit card fraud dataset (see discussion above), and use all features except time. We use of input data for synthetic data generation, for various privacy budgets . Synthetic data is then used to train classifiers (see [KNP+23] for a detailed setup), which are tested on the remaining of the original input data.

Evaluation:

We present degradation of average ROC (area under the receiver operating curve) over repetitions. The algorithm introduced in [KNP+23] does not outperform DP-MERF in terms of ROC values. This is not surprising as it does not rely on deep generative models. However, their performance degrades slower as privacy increases compared to the DP-MERF (Figure 17).

4.4 Fairness

As synthetic data generation is a powerful tool to both augment and correct automatic decision-making tools, more recent developments have explored and analysed the biases inherited in synthetic data and their downstream effects. This is particularly relevant to commercial banking, where machine learning algorithms are directly used for tasks such as auto loans or credit card applications decisions. Most of recent work revolves around diagnosing and improving generative models [XYZW18, SHCV19, XWY+19, XYZW19, vBKBvdS21, LRD22], while other approaches tackle the problem from a transfer learning [TAC23] or optimization [XDP+23] perspective. We refer the reader to [MMS+21] for a high-level overview.

4.5 Robustness

Recent years saw the surge of interest in utilizing synthetic data in order to improve model robustness. [CRS+19] show that training a classifier with additional unlabelled data from the same distribution improves adversarial robustness, i.e. robustness against adversarial attacks that are launched by manipulating features of the test instances. [DZGZ21] explore how data from a different domain/distribution affects adversarial robustness in the original domain. [SMH+22] investigate how adversarial robustness of a classifier trained on synthetic data from a proxy distribution translates to the robustness on the real data. In comparison to data arising from a related domain/proxy distribution, the advantage of relying on a synthetic data generator trained on real data is that control over the distance between real and synthetic distribution often comes for free as a consequence of theoretical guarantees on the fidelity of the chosen generator [GPAM+14a, ACB17, LCC+17].

We have reviewed various aspects of synthetic tabular data and there are many open questions. Some of them include: can we generate high quality synthetic data which match the performance of real datasets, differentially private explanations for customer decisions as opposed to utilizing real data, distinguishing synthetic data from real data. We continue our discussion on tabular data with event series which has an additional temporal component that needs to be taken into account.

5 Event series data

Event series data record sequences of events, including associated time and related features. In general, a sequence of event series data is composed of multiple events of different types, in which the occurrence of any event at time might depend on the history (i.e., the sequence of past events) up to time . Unlike time series data, in which a continuously occurring phenomenon is sampled at different resolutions, time interval between two events is usually not predetermined, so event series data are asynchronous. Event series data are ubiquitous in many financial domains. In commercial banking, “customer journeys” log the interactions of customers with the bank. In trading, limit order books record buy or sell orders on a security at a specific price or better. In marketing applications, customer impressions record when a specific ad was served to the customer and whether the customer eventually purchased the advertised product. Outside of financial applications, infectious diseases patterns [CLM22], earthquake logs [Oga98], social media interactions [RLMX17], and crime modeling [RG18] are among other examples of event series data. Graphs are typically used to model the rich interaction structures between entities such as customers [LLS+23] but this makes the generation process much more involved. Diffusion models have been recently explored for the generation of these large-scale graphs [LKPL23].

The literature on modeling sequential data encompasses a broad spectrum of techniques. Traditional approaches include Hidden Markov Models [BP66, RJ86], Kalman filters [Kal60, WB+95], dynamic Bayesian networks [Gha97] and sequential mining patterns algorithms [ME10, FVLK+17]. More recently, deep learning approaches such as recurrent neural networks [HS97, YSHZ19], deep autoregressive models [ODZ+16, VdOKE+16] and transformer-based architectures [VSP+17, LWLQ22] have proven highly effective in sequential data prediction. Within this diverse landscape of sequential data models, a powerful set of tools to model the occurrence of events in event series data are temporal point processes [CI80, DVJ+03]. Temporal point processes model the probability of occurrence of an event of a given type at any time (possibly as a function of the history up to time t). Hawkes processes (self-exciting point processes) are a common class of temporal point processes [Haw71, IW79, Rei18] that model sequential event series in which the occurrence of an event may increase the probability of occurrence of future events. Temporal point processes are particularly useful as, once trained, one can directly generate synthetic event series data with the same dynamics of the training data; one of the most popular algorithms is the thinning algorithm [Oga81], (see [DZ13] and [XFY+17] for more recent simulation-based approaches). Recent works have focused on improving the Hawkes model capacity by estimating the event dynamics more flexibly beyond self-excitation or for different data types [LXZ+15, ZLKY19, ZJL+20, PH22, GDL+22, ZDG+22], while other approaches have focused on the privacy properties of Hawkes processes [GKD+22, ZLZZ22]. Additionally, point processes have been extended to incorporate a stochastic process as intensity function (Cox processes [Cox55]) or to assume a probability distribution which can be expressed as a functional determinant (determinantal point processes [Mac75]). Finally, goodness-of-fit evaluation is usually conducted by looking at the integral of the estimated intensity between out-of-sample events, which is known to follow an exponential distribution with rate under the ground truth intensity [DVJ+03]. Other goodness-of-fit approaches include the difference between the empirical and estimated intensity [XFY+17] as well as non-parametric two sample tests [WZZX21].

5.1 Using Automated Planning

A way of generating synthetic event series data assumes there is a model of the underlying environment and perform a simulation using the model on different scenarios. The different events that appear in the simulation are converted into data points of the output dataset. An example of such technique [BV20, BVS20] uses classical automated planning [GNT04]. The assumption is that most data that financial institutions keep on clients, come from client’s interaction with the bank. Each interaction can be seen as an action that the client executes and that is observable by the bank. Examples are opening accounts, making wire transfers, or withdrawing money from ATMs. At each time step, a clients state can be described in terms of some facts, such as the accounts they opened, the balance on their accounts, or their regular payments (e.g. monthly rent, yearly taxes, utility bills). Also, at each time step, clients have short-term financial goals, such as paying the rent, buying a product, or receiving the payroll from their employer. Given that we can define clients’ interactions in terms of actions, states and goals, we can use an automated planning framework to randomly generate goals for clients, generate plans that achieve those goals from the current state of clients, and execute the actions in those plans. Each action execution leaves a trace that can be logged into a record of a dataset that defines that interaction. Data generated using this method has been used in several papers for purposes ranging from reasoning on entanglements [MCV+23] to goal recognition [EVY+23]. In particular, this approach generated datasets that described money laundering activities, fraudulent transactions, or customer journeys [BV20].

Figure 18 shows an excerpt of a customer journey dataset generated from a simulated trace using planning. Events are usually described by a date-time tag, a label for the executed event, and a client id. The event description includes the channel used by the client, mobile in this case and the corresponding action.

| Date and time | Event | Customer ID |

|---|---|---|

| 2021-05-24 21:22:14 | mobile : logon | ID-22522 |

| 2021-05-24 21:25:14 | mobile : transaction summary business | ID-22522 |

| 2021-05-24 21:26:14 | mobile : transaction history prepaid account | ID-22522 |

| 2021-05-24 21:28:14 | mobile : ultimate rewards info | ID-22522 |

| 2021-05-24 21:31:14 | mobile : ultimate rewards activity | ID-22522 |

| 2021-05-24 21:36:14 | mobile : logoff | ID-22522 |

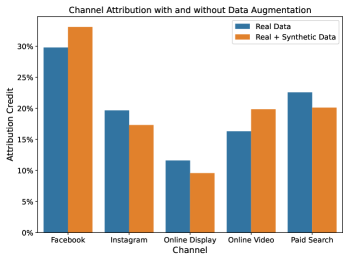

5.2 Application: Marketing spending insight via synthetic customer journeys

In this section, we show how data augmentation with synthetic customer journeys can help downstream tasks related to marketing campaigns. In marketing, customer journeys are composed of the customer interactions with different advertising channels, such as search, social media or television ads. Post mortem spending insight is usually conducted by identifying the importance of different channels in terms of customer conversions, i.e., in terms of the number of customers who purchased the advertised product after seeing the ad. Multi-Touch Attribution (MTA) models measure this importance by assigning credit to each channel to drive future budget allocation. Unlike more traditional approaches, where all the credit was assigned to the last customer touch point, MTA models take into account the entirety of the customer journeys; see [YSS15, ADR17, ADY+18] for examples of MTA models. Temporal point processes can be used to learn the customer journey dynamics, enrich the available training data, and improve the downstream MTA model insights.

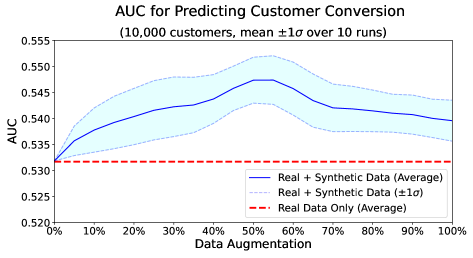

To showcase the usefulness of synthetic event series data, we use a public MTA dataset444Data available on the Kaggle platform at https://www.kaggle.com/code/hughhuyton/multitouch-attribution-modelling/notebook. The data cover a month-long campaign with the ads channels available in the data being Facebook, Instagram, Paid Search, Online display and Paid Search. We extract customer journeys with a conversion rate from the campaign, and use a Markov chain MTA model [KBRF18]. We train an XGBoost [CG16] model trained on features extracted from customer journeys data to predict the customer conversion. An improvement in prediction performance would indicate that synthetic event series data do indeed capture the dynamics within the real data. We use a mixture of 4 Hawkes processes for augmentation, conducting a separate hyper-parameter optimization across the number of mixtures and the decay parameters. Figure 19 (left) reports the XGBoost model AUC as a function of the percentage of data augmentation used in training (shaded bands indicate one standard deviation computed over 10 runs). We see that the addition of synthetic customer journeys improves the classifier performance, although the increase saturates after 50% augmentation. Figure 19 (right) shows the MTA credit assignments when using 50% of the synthetic customer journeys. The synthetic journeys do not radically change the credit assignment, but increase the importance of online video advertisement, which gains credit and ranking.

6 Time series data

Synthetic time series (TS) data refers to artificially generated time series data that emulate the statistical properties and patterns observed in the real world. Synthetic time series are useful when only limited number of historical observations are available. They are also needed to simulate specific scenarios (for instance, market crashes). Such data finds utility in the finance domain in multiple ways, including back-testing investment strategies, evaluating trading algorithm performance for robustness, and simulating market stress scenarios for risk management. Additionally, synthetic time series data can be combined with historically observed data to make model training datasets larger as well as to enhance the representation of minority classes in imbalanced datasets – both of which typically lead to better generalization capabilities of machine learning models.

Approaches to synthetic time-series

We can divide the existing methods for synthetic time-series generation and simulation in three major classes [Goo16]:

-

•

Parametric models assume a specific parametric form for the underlying distribution of the data, and they have a fixed number of parameters that are usually estimated from the training data. Once their parameters are estimated, we can generate synthetic samples by sampling directly from the learned distribution. A Gaussian distribution is an example of parametric model, where the mean and variance are the parameters. For time series data, suitable models include probabilistic variants of vector autoregression [New83], or state-space models. In terms of financial time series, stochastic differential equations (SDEs) [PEK21, JB19] are among the most popular class of models due to their ability to explicitly model time series data as a continuous time stochastic process with an underlying drift (i.e., trend) and diffusion (i.e., noise). Common SDEs employed to model price time series include geometric Brownian motion and the Ornstein–Uhlenbeck (OU) [MMS09] process, where the OU process captures the mean-reversion property typically observed in financial time series [BBDG18].

-

•

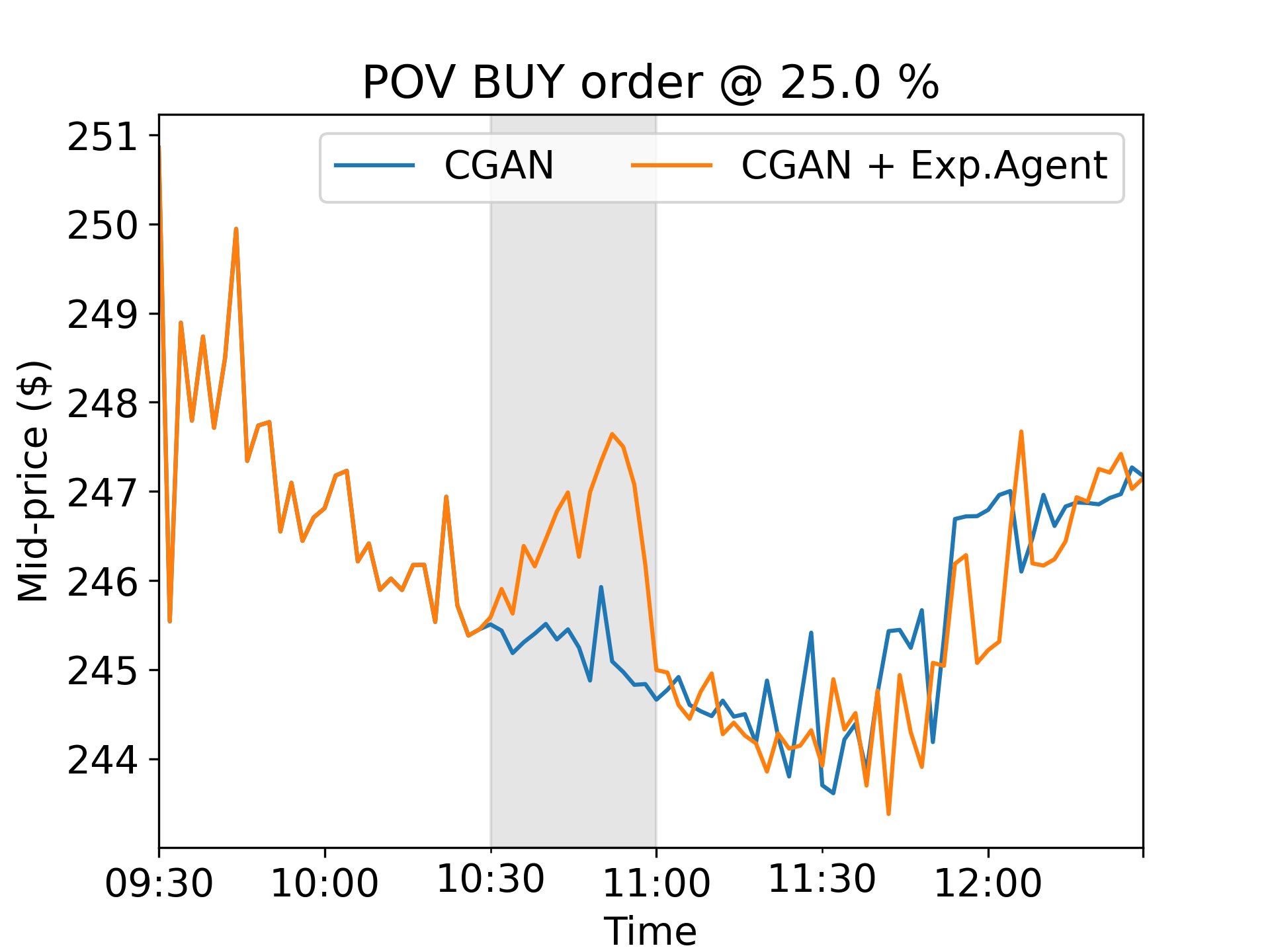

Non-Parametric models do not take any parametric assumptions, i.e., they do not make strong assumptions about the form of the underlying distribution. Instead, these models aim at estimating the data distribution directly from the training samples, often without specifying a set of fixed parameters. Example of non-parametric models are GANs [Goo16] and VAEs [Doe16]. Among non-parametric models we can distinguish between: implicit models which do not need to make any assumption on the density function form, but they rather train and sample directly the samples (e.g., GANs); and explicit models which make an explicit assumption on the form of density function from which they sample the synthetic samples (e.g,. VAEs). A recent work using an implicit model is shown in Section 6.2, where a conditional generative network (cGAN) is used to generated synthetic order books [CMVB22].

-

•

Agent-based models provide a natural bottom-up approach to model the underlying system dynamics (e.g., traders) and to simulate and generate synthetic markets. Agent-based models have been widely used in the economic literature to replicate complex processes, and perform ”what-if” studies [LeB06]. In Section 6.2 we discuss ABIDES [BHB19] a state-of-art Multi-Agent Simulator for high-fidelity market data.

Metrics:

Fidelity and utility metrics described in Section 2.2 are widely used for assessing the quality of generic (i.e., not necessarily financial) synthetic time series data. Properties of financial time series that are repeated across a wide range of instruments, venues, and time periods are referred to as stylized facts [VBP+19]. For instance, it is a well known fact that the distribution of daily stock price returns shows fat tails and that distribution is time-invariant. Evaluating the stylized facts of generated financial time series such as distributions of asset returns, order volumes, order arrival times, order cancellations, etc., and comparing them to those derived from real historical data allows us to infer the level of fidelity of a time series generation process.

Related Work:

Realistic time series generation has been previously studied in the literature by using the generative adversarial networks (GANs). In the TimeGAN architecture [YJvdS19a], realistic generation of temporal patterns was achieved by jointly optimizing with both supervised and adversarial objectives to learn an embedding space. QuantGAN [WKKK20] consists of a generator and discriminator functions represented by temporal convolutional networks, which allows it to synthesize long-range dependencies such as the presence of volatility clusters that are characteristic of financial time series. TimeVAE [DFWB21] was recently proposed as a variational autoencoder alternative to GAN-based time-series generation. GANs and VAEs are typically used for creating statistical replicas of the training data, and not the distributionally new scenarios needed for data augmentation. Recently, neural SDEs have also been proposed for realistic time series generation. Neural SDEs assume that the time series data follow some underlying latent SDE, where the drift and diffusion of the SDE are modelled via a deep neural network.

Data augmentation is well established in computer vision tasks due to the simplicity of label-preserving geometric image transformation techniques, but it is still not widely used for time series with some early work being discussed in the literature [IU21, WSS+20]. For example, simple augmentation techniques applied to financial price time series, such as adding noise or time warping, were shown to improve the quality of next day price prediction model [FDZ+20, FDZ+21]. However, such transformations were not required to produce realistic synthetic time series. Furthermore, some augmentation methods might work in certain domain-specific time series, but not in others. For example, if noise is added to a sample, what scale of noise should be used? Given a certain dataset, what set of transformations would work best? Therefore, a major challenge in data augmentation is how to search over the space of possible transformations, which can be prohibitive given the large number of possible transformations and their associated hyperparameters. This issue motivated the investigation of several automated data augmentation algorithms [CZM+19]. Previous methods perform the search by using proxy tasks with small models and training subsets [LKK+19, ZWZZ20, HLC+19], which might not give optimal results in the final task. More recently, RandAugment [CZSL20] proposes to sample augmentations uniformly with the same shared magnitude, where the number of augmentations and magnitude can be tuned with a grid search. A similar approach is proposed for time series in [FDjZ+21] where all possible augmentations are weighted with a learnable parameter, while in [OMI22] a neural network that dynamically selects the best combination of data augmentation methods is proposed, using a feature consistency loss.

6.1 Generation

Application: Realistic Generation of Financial Time Series

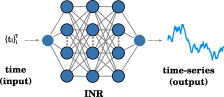

Time series data often presents unique challenges due to its potentially irregular sampling or presence of missing values. These issues can significantly affect the performance of certain deep learning models, leading to inaccurate predictions or flawed insights. Given the crucial role time series data plays across various scientific and economic domains, researchers have focused on the development and deployment of robust deep learning models capable of accommodating these inconsistencies. In recent years, Implicit Neural Representations (INRs) have gained popularity as an accurate and flexible method to parameterize signals from diverse sources, including images, videos, audio, and 3D scenes [RSGZ+21, CLW21, SMB+20]. Traditional methods primarily use discrete representations like data grids that often grapple with limited spatial resolution and inherent discretization issues. Instead, INRs encode data in terms of continuous functional relationships. Thus, they are are resolution-independent, offering a novel framework for data representation. Furthermore, modifications to INRs, such as SIREN’s periodic activations [SMB+20] and NeRFs’ positional encodings [MST+20], have successfully mitigated the spectral bias commonly faced by traditional neural networks. Therefore, the resolution free nature of INRs, in combination with their capacity for accurate spectral reconstruction makes them particularly useful in time series applications, where data irregularities and missing values are prevalent.

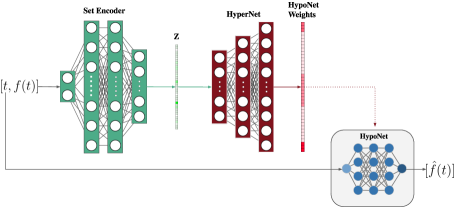

In particular, [FSEL+22] proposes HyperTime that leverages INRs with hypernetworks for time series generation. Given that each time series is represented by an INR, the hypernetwork allows it to learn a prior over the time series dataset, which generates a compressed latent representation of the entire time series dataset. The embeddings can then be interpolated to generate novel time series. The method was evaluated using two quantitative metrics: 1) the predictive score, which measures the usefulness of the generated data by using a train on synthetic, test on real (TSRT) approach where a model is trained using the synthetic data to predict the next step in a sequence, and then it is evaluated using the real data; and 2) the discriminative score which serves as a measurement of fidelity of the generated data, where the aim is to assess if the synthetic data is indistinguishable from real data. A discriminative model is trained to classify real and fake samples, and then used to test whether the original and generated data are correctly classified. The discriminative score is computed as , where a low value means that the classification is challenging, and therefore, the model cannot tell which samples are real and which are generated. Results for multiple lengths of Google stock data are shown in Table 21 where HyperTime outperforms all other benchmarks with regards to the predictive score and shows competitive performance with regards to the discriminative score.

| Method | Stock24 | Stocks72 | Stock360 | |

|---|---|---|---|---|

| Predictive Score | ||||

| iHT | .037 .000 | .188 .000 | .168 .000 | |

| GT-GAN | .040 .000 | .207 .000 | .188 .000 | |

| TimeGAN | .038 .001 | .226 .002 | .206 .000 | |

| RCGAN | .040 .001 | .192 .001 | .189 .000 | |

| DiffTime | .038 .001 | .213 .000 | .215 .000 | |

| LS4 | .103 .001 | .194 .000 | .168 .000 | |

| FF | .076 .001 | .191 .000 | .169 .000 | |

| Original | .036 .001 | .186 .001 | .167 .001 | |

| Discriminative Score | ||||

| iHT | .044 .011 | .014 .009 | .018 .015 | |

| GT-GAN | .077 .031 | .058 .017 | .085 .064 | |

| TimeGAN | .102 .021 | .073 .047 | .042 .074 | |

| RCGAN | .196 .027 | .012 .09 | .014 .007 | |

| DiffTime | .097 .016 | .097 .012 | .101 .018 | |

| LS4 | .363 .027 | .089 .081 | .088 .081 | |

| FF | .349 .113 | .016 .018 | .015 .014 |

Application: Imputation of Financial Time Series

Addressing time series imputation is crucial across different domains including finance, climate modelling, and healthcare, given the potentially vast differences in the type of data under study. Classic strategies, such as averaging and regression, are generally too simplistic and fail to sufficiently encapsulate the underlying behavior. Although modern methods, like iterative imputation and maximum likelihood procedures, allow for a higher degree of algorithmic complexity and performance improvement, the assumptions they often make can introduce biases that are detrimental to intricate cases (refer to [JCL+22] or [CWL+18] for examples). Inspired by the success of [FSEL+22] to generate time series that can be irregularly sampled, [BFELV23] proposes Modulated Auto-Decoding SIREN (MADS) for multivariate time series imputation. MADS utilises the capabilities of SIRENs for high fidelity reconstruction of signals and irregular data handling and combines the SIREN parameterizations with hypernetworks in order to learn a prior over the space of time series. Experimental results across three real-world time series datasets from different domains are shown in Table 22, where MADS shows best performance in the majority of the datasets. Interestingly, in all cases, the best performance is achieved by INR-based methods. For details of the performance metrics and additional results, we refer to the original paper [BFELV23].

| Air Quality | HAR () | HAR () | PhysioNet | ||||||||||

| Family | Method | MSE | Max MSE | W2 | MSE | Max MSE | W2 | MSE | Max MSE | W2 | MSE | Max MSE | W2 |

| Classic | Mean | 0.091 | 0.470 | 0.260 | 0.027 | 0.332 | 0.078 | 0.028 | 0.358 | 0.182 | 0.024 | 0.386 | 0.029 |

| (0.000) | (0.000) | (0.000) | (0.001) | (0.004) | (0.001) | (0.000) | (0.004) | (0.004) | (0.001) | (0.018) | (0.001) | ||

| Median | 0.091 | 0.480 | 0.260 | 0.029 | 0.332 | 0.215 | 0.029 | 0.362 | 0.180 | 0.026 | 0.428 | 0.086 | |

| (0.000) | (0.000) | (0.000) | (0.000) | (0.004) | (0.305) | (0.000) | (0.004) | (0.000) | (0.001) | (0.022) | (0.125) | ||

| Deep learning | BRITS | 0.224 | 0.880 | 0.388 | 0.308 | 0.952 | 0.284 | 0.312 | 0.988 | 0.666 | 0.522 | 0.986 | 0.144 |

| (0.015) | (0.016) | (0.022) | (0.004) | (0.004) | (0.005) | (0.004) | (0.004) | (0.005) | (0.011) | (0.011) | (0.005) | ||

| CSDI | 0.075 | 0.844 | 1.220 | 0.010 | 0.280 | 0.122 | 0.020 | 0.436 | 0.168 | 0.037 | 0.506 | 0.422 | |

| (0.012) | (0.015) | (0.045) | (0.002) | (0.021) | (0.017) | (0.006) | (0.056) | (0.031) | (0.005) | (0.035) | (0.029) | ||

| GP-VAE | 0.083 | 0.772 | 0.764 | 0.035 | 0.374 | 0.280 | 0.038 | 0.416 | 0.302 | 0.024 | 0.386 | 0.352 | |

| (0.003) | (0.013) | (0.015) | (0.007) | (0.027) | (0.020) | (0.007) | (0.025) | (0.026) | (0.001) | (0.019) | (0.013) | ||

| INR | SIREN+ | 0.085 | 0.504 | 0.226 | 0.007 | 0.178 | 0.106 | 0.008 | 0.270 | 0.123 | 0.017 | 0.368 | 0.270 |

| (0.009) | (0.034) | (0.030) | (0.002) | (0.090) | (0.018) | (0.003) | (0.023) | (0.035) | (0.001) | (0.019) | (0.014) | ||

| HN+SIREN | 0.077 | 0.516 | 0.210 | 0.010 | 0.266 | 0.119 | 0.013 | 0.354 | 0.138 | 0.024 | 0.418 | 0.332 | |

| (0.009) | (0.011) | (0.029) | (0.005) | (0.077) | (0.035) | (0.006) | (0.070) | (0.043) | (0.002) | (0.026) | (0.023) | ||

| Mod-SIREN | 0.070 | 0.480 | 0.214 | 0.007 | 0.210 | 0.100 | 0.010 | 0.276 | 0.121 | 0.018 | 0.378 | 0.286 | |

| (0.007) | (0.016) | (0.036) | (0.002) | (0.010) | (0.016) | (0.010) | (0.047) | (0.072) | (0.002) | (0.029) | (0.023) | ||

| MADS | 0.072 | 0.458 | 0.202 | 0.005 | 0.186 | 0.072 | 0.006 | 0.252 | 0.082 | 0.018 | 0.372 | 0.276 | |

| (0.012) | (0.016) | (0.028) | (0.000) | (0.005) | (0.003) | (0.001) | (0.011) | (0.005) | (0.001) | (0.018) | (0.013) | ||

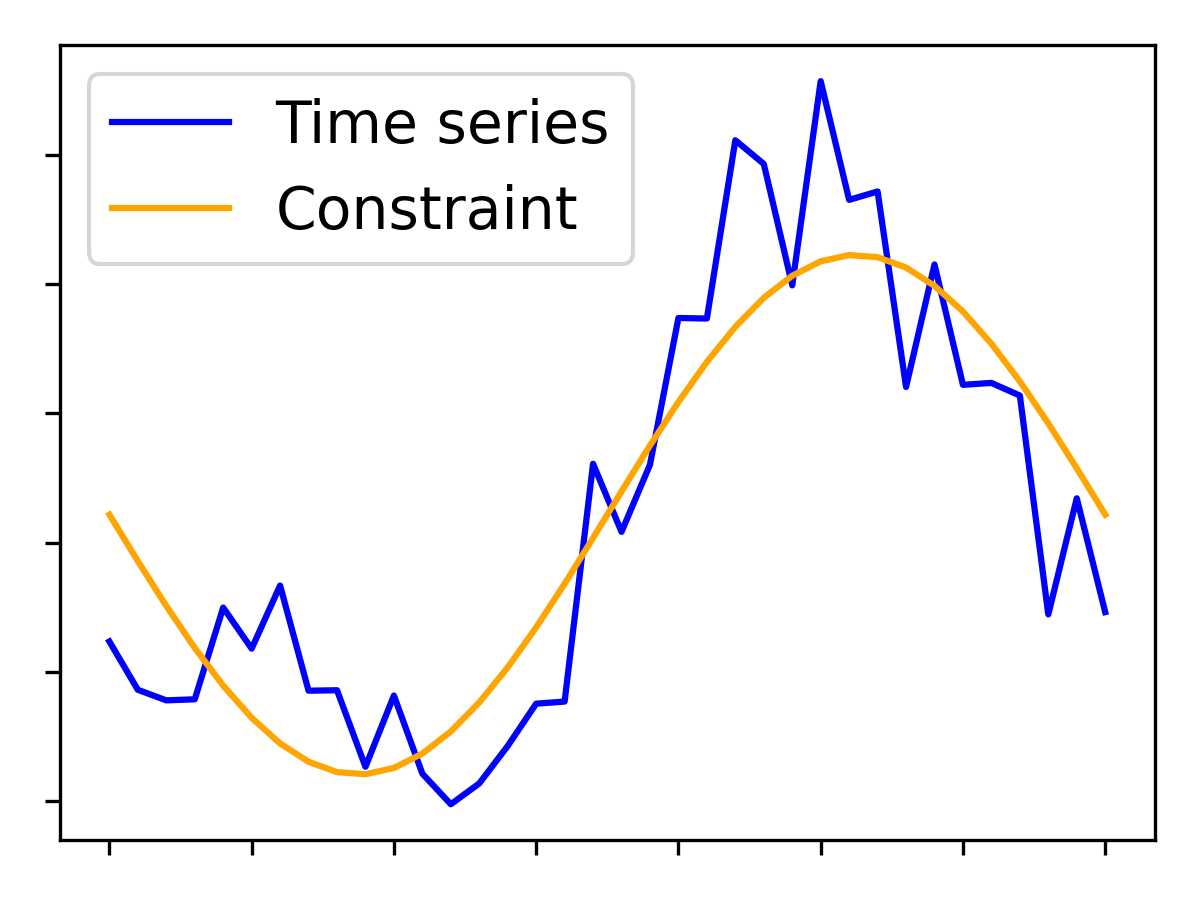

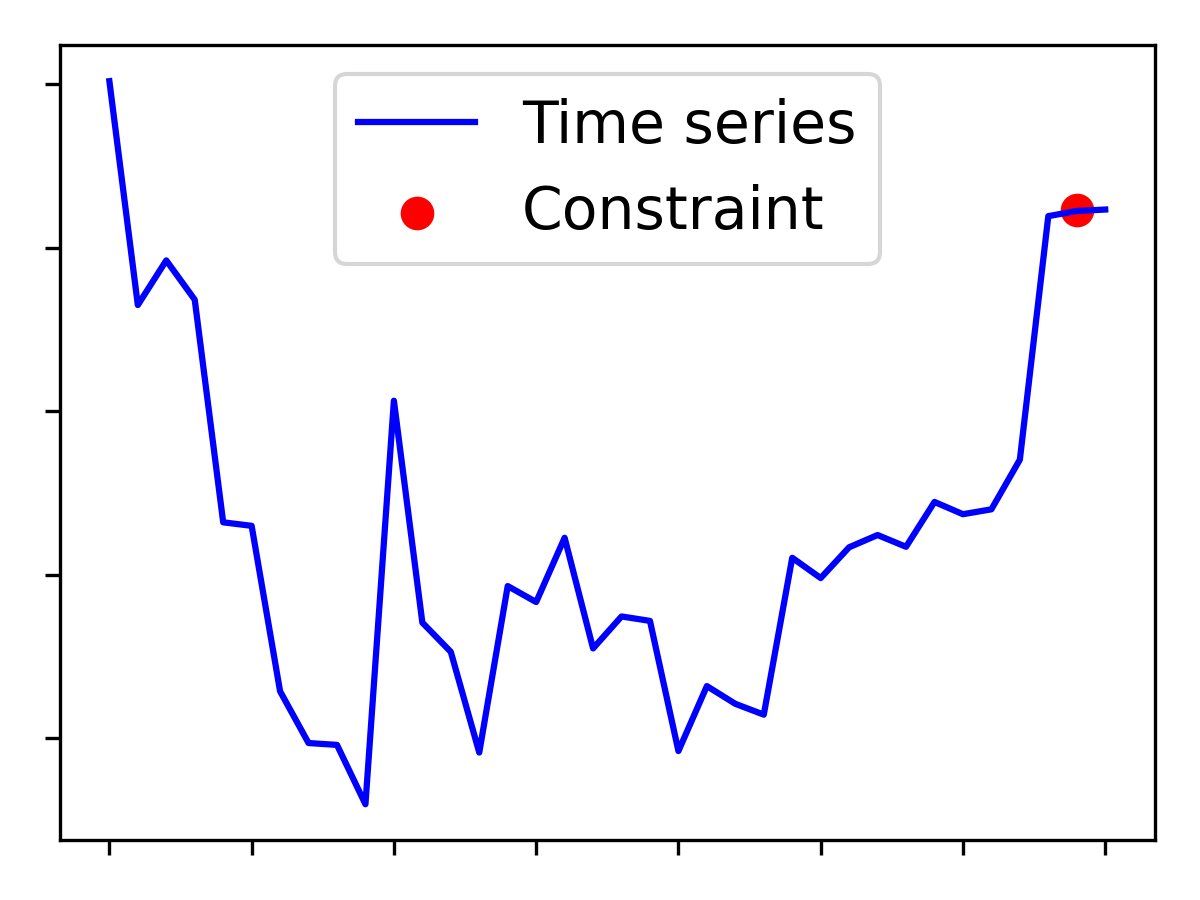

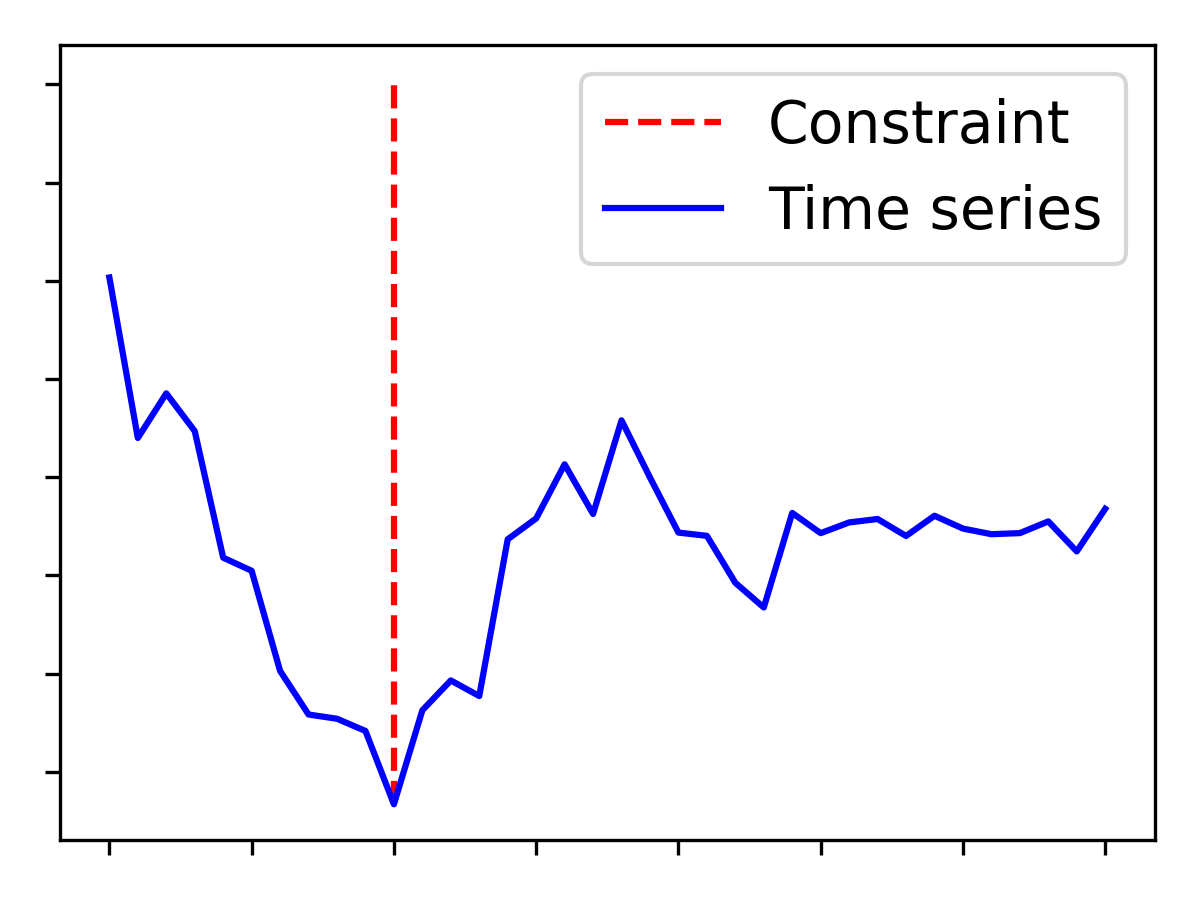

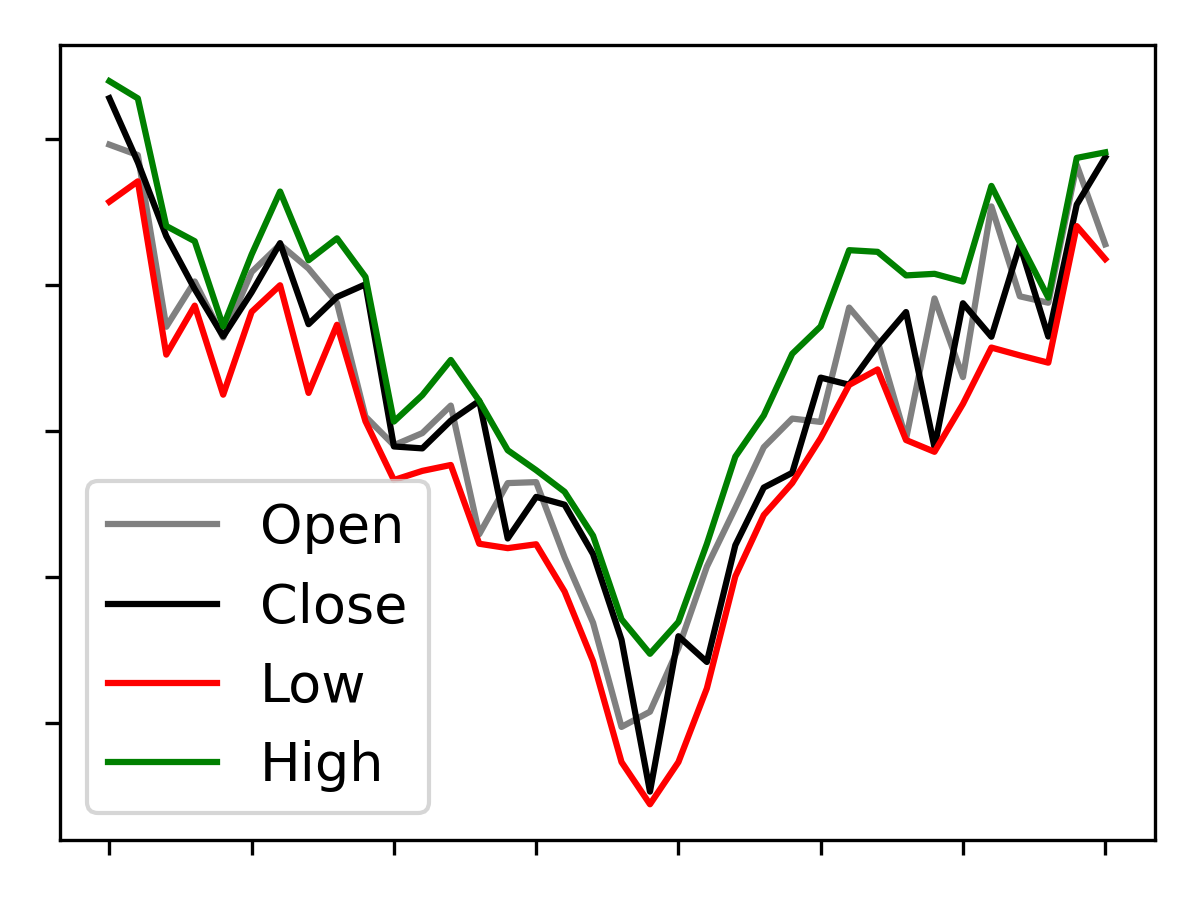

Application: Constrained Market Scenarios Generation

Synthetic time-series are extremely useful to test hypotheses and algorithms before employing them in real settings, especially for unseen and counterfactual scenarios. For instance, the US Federal Reserve publishes synthetic market stress scenarios given by the constrained time series for financial institutions to assess their performance in hypothetical recessions [fed]. We refer to the constrained time-series generation problem as the problem of generating synthetic time-series that are statistically similar to historical times series while matching some input constraints [DLAG+20, XZF+18, GSLO+17].

Existing work that employs deep generative models attempts to capture the statistical data properties and temporal dynamics of time-series, neglecting additional requirements, such as input constraints. These constraints are often introduced by re-training the existing generative models, and penalizing them proportionally to the mass they allocate to invalid data [TK21, DLAG+20, GSLO+17, XZF+18]. Other works consider unconstrained generative models to generate synthetic markets while rejecting and re-sampling time-series that do not match the constraints [PWV16b].

A formal definition of constrained time-series generation is introduced in [CGBV23]. This work divides the constraints in Soft and Hard constraints, and additionally it divides them between Global and Local constraints. Soft constraints optimize the time-series to minimize a constraint score (i.e., minimize the distance between the time-series and the constraint), and do not require sample rejection. Hard constraints require the time-series to exactly match the input-constraints, and a time-series can be rejected if it does not respect a constraint. Additional, Global constraints compare across all the points in the time-series, while Local constraints focus on specific sub-sections of the input time-series. This work proposes four different approaches to tackle the constrained generative problem. It starts from a constrained-optimization (COP) framework, and then it proposes three different variant of denoising diffusion models. The COP framework provides to the user the possibility to specify any constraints, and generate synthetic time-series starting from random noise or existing time-series. This method explicitly includes also all the statistical data properties as constraints, e.g., auto-correlation and returns for financial time-series. Thus, it enables the users to constrain the time-series and also to control their statistical properties. Instead, the diffusion models learn the statistical data properties directly from input data, and they can integrate additional constraints during training or inference. In particular, one promising diffusion model, called Guided-DiffTime, shows the ability to incorporate any differentiable constraints into the sampling procedure. This model does not require to be re-trained when incorporating new constraints. The proposed approach outperform existing state-of-art benchmarks under different quantitative and qualitative metrics.