X-Vine Models for Multivariate Extremes

Abstract

Regular vine sequences permit the organisation of variables in a random vector along a sequence of trees. Regular vine models have become greatly popular in dependence modelling as a way to combine arbitrary bivariate copulas into higher-dimensional ones, offering flexibility, parsimony, and tractability. In this project, we use regular vine structures to decompose and construct the exponent measure density of a multivariate extreme value distribution, or, equivalently, the tail copula density. Although these densities pose theoretical challenges due to their infinite mass, their homogeneity property offers simplifications. The theory sheds new light on existing parametric families and facilitates the construction of new ones, called X-vines. Computations proceed via recursive formulas in terms of bivariate model components. We develop simulation algorithms for X-vine multivariate Pareto distributions as well as methods for parameter estimation and model selection on the basis of threshold exceedances. The methods are illustrated by Monte Carlo experiments and a case study on US flight delay data.

Key words: exponent measure, graphical model, multivariate Pareto distribution, pair copula construction, regular vine, tail copula

1 Introduction

For multivariate extremes, margin-free tail dependence models based on max-stable distributions arise from classical limit theory for sample extremes (de Haan and Resnick, 1977). A question of high interest is the construction of such models that are flexible, parsimonious, and computationally tractable, and scale well as the dimension grows (Engelke and Ivanovs, 2021). To do so, we propose a novel approach based on regular vine tree sequences (Bedford and Cooke, 2001, 2002), called X-vines. The models can easily be built in arbitrary dimension by combining bivariate components only. The latter can be chosen independently from one another, giving great flexibility. The pairs are grouped in trees, the number of which determines the complexity of the model. Computations proceed by recursive algorithms.

For copula-based dependence modelling, outside the context of extreme value analysis, vine constructions have grown into a versatile and widely applied approach (Czado, 2019; Czado and Nagler, 2022; Nagler and Vatter, 2023). Our contribution is to make vine-based methods operational, in theory and practice, for densities of exponent measures of multivariate extreme value distributions. The challenge to overcome is that these densities do not integrate to one but to infinity. A change of margin transforms exponent measure densities into tail copula densities, which still have infinite mass, but with structural properties that resemble copula densities more closely.

Figure 1 shows a regular vine sequence in dimension . The structure consists of four trees , in which the edges of one tree become nodes in the next one. Each of the pairs of variables appears as the leading pair before the semicolon on exactly one edge. The numbers behind the semicolons refer to conditioning variables. The first tree represents a Markov tree, while the subsequent trees add higher-order dependence relations.

An X-vine specification consists of a regular vine sequence , together with, for each edge in the first tree, a bivariate exponent measure or tail copula density, and, for each edge of the subsequent trees, a bivariate copula density, not necessarily stemming from extreme value theory. For the example in Fig. 1, four bivariate exponent measure densities () and six bivariate copula densities () would be required. These bivariate components can be chosen independently from another, without any constraints. Our main result shows how to combine bivariate building blocks into a single multivariate exponent measure or tail copula density. Further, we show that commonly used parametric models in extreme value analysis are actually examples of such X-vine models. We leverage the recursive nature of regular vine sequences both in theory and computations.

The models constructed in this way turn out to be the tail limits of regular vine copulas. For the special case of D-vine copulas, such tail limits were already computed in Joe (1996) and Joe et al. (2010), focusing on tail dependence functions rather than densities. In Simpson et al. (2021), tails of D-vine and C-vine copulas were investigated from the perspective of the limiting shapes of sample clouds.

X-vine constructions are related to but different from recently proposed graphical models for extremes, either for directed or undirected graphs (Gissibl and Klüppelberg, 2018; Engelke and Hitz, 2020; Engelke et al., 2022). Markov trees (Segers, 2020; Hu et al., 2023) are a special case in the intersection of graphical and X-vine models.

After reviewing background on multivariate extremes and regular vine sequences in Section 2, we state a version of Sklar’s theorem for tail copula densities in Section 3. Some well-known parametric examples are worked out in Section 4, with a focus on the simplifying assumption that the conditional copula densities only depend on the values of the conditioning variables through their indices, but not their actual values. Section 5 contains the paper’s main results, showing on the one hand how a general tail copula density can be decomposed along any regular vine sequence, and, on the other hand, how to construct a tail copula density from a regular vine sequence and bivariate building blocks. The so-called X-vine models arising in this way are put to work in the subsequent sections, covering simulation algorithms (Section 6), parameter estimation and model selection (Section 7), simulation studies (Section 8), and a case study on US flight delay data (Section 9) taken from Hentschel et al. (2022). Section 10 concludes. The appendices contain a detailed example to illustrate the theory of regular vine sequences and X-vine models, the proofs of the paper’s results, additional theory on Sklar’s theorem, exponent measure densities and the connection with regular vine copulas, as well as additional numerical results. The methods are implemented in R (R Core Team, 2023), relying in particular on packages graphicalExtremes (Engelke et al., 2022) and VineCopula (Nagler et al., 2023); a dedicated software package is under construction.

2 Background

We write for the index set of the variables. Bold symbols refer to multivariate quantities. For a point and a subset , write subvectors as and . Mathematical operations on vectors such as addition, multiplication and comparison are considered component-wise.

2.1 Multivariate extreme value theory: tail copulas and their densities

Tail copulas

Classical extreme value theory starts from the assumption that the distribution function of a random vector is in the max-domain of attraction of a multivariate extreme value distribution. This assumption comprises two parts: (i) all univariate marginal distributions are in the domains of attraction of some univariate extreme value distributions; (ii) after reduction of the univariate margins to a common scale, the joint distribution of the random vector is multivariate regularly varying. We refer to Beirlant et al. (2004) and de Haan and Ferreira (2007) for textbook treatments of multivariate extreme value theory.

The focus in this paper is on part (ii), which concerns the tail dependence of , that is, the probabilities of high values occurring jointly among the variables . To describe the mathematical theory behind tail dependence, let be the survival copula of : under the standing assumption that the marginal distribution functions are continuous, is the distribution function of the random vector with uniformly distributed components for . Our interest is in high values of and thus in low outcomes of .

Definition 2.1 (Tail copula and tail copula measure).

The (lower) tail copula of is the function on defined by

| (2.1) |

provided the limit exists. If it does, then the tail copula measure, denoted by the same symbol , is the Borel measure on determined by for .

The term ‘tail copula’ stems from Schmidt and Stadtmüller (2006) in the bivariate case; Joe et al. (2010) call it ‘tail dependence function’. The tail copula measure already appears in Einmahl et al. (2001), where it is denoted by . It is closely linked to the exponent measure in Eq. (2.9) below, introduced in de Haan and Resnick (1977) and which constitutes a fundamental notion in multivariate extreme value theory.

The total mass of the tail copula measure equals infinity but is finite for Borel sets contained in for some . Its univariate margins are equal to the one-dimensional Lebesgue measure:

| (2.2) |

Equation (2.1) implies that is homogeneous of order one, both as a function and as a measure: for , Borel sets , and ,

| (2.3) |

Any Borel measure on satisfying (2.2) and (2.3) is a tail copula measure, i.e., is the limit in (2.1) for some copula .

Tail copula densities

Throughout, we assume that the tail copula measure has no mass on the hyperplanes through infinity, that is, for all , so that is concentrated on . Furthermore, we assume that is absolutely continuous with respect to the -dimensional Lebesgue measure with continuous density , that is, for all Borel sets . Choosing for , we recover from by for all . The marginal constraint (2.2) implies

| (2.4) |

In view of (2.3), is homogeneous of order :

| (2.5) |

Properties (2.4) and (2.5) characterise the set of -variate tail copula densities; see Section 4 for some well-known parametric families.

By Scheffé’s lemma from measure theory, if the copula has density and the tail copula measure has density , then (2.1) is implied by for all . A word of caution: for a given copula density , the limit may exist for all but not be a tail copula density, as the marginal constraint (2.4) may fail; a case in point is the independence copula, with density , in which case the said limit is zero.

Margins of tail copulas

For a non-empty set , let denote the coordinate projection and let denote the -th marginal measure of ,

| (2.6) |

for Borel sets . The choice for shows that is the tail copula measure of the copula of , as in Definition 2.1. For , we have

The density of the measure is

| (2.7) |

for and, provided , is obtained from by integrating out the variables with indices .

Relations between tail copulas and other concepts in multivariate extremes

For later reference, we review a number of related terms from multivariate extreme value theory. This paragraph can be skipped at first reading, as the contributions in Sections 3 and 5 do not depend on it.

Equation (2.1) is equivalent to the assumption that the random vector with for satisfies

| (2.8) |

that is, is in the max-domain of attraction of a multivariate extreme value (or max-stable) distribution defined in terms of the stable tail dependence function for . The margins of are unit-Pareto, for , while those of are unit-Fréchet, for . Equivalently, the distribution of is multivariate regularly varying (de Haan and Resnick, 1977; Resnick, 2007) with limit measure

| (2.9) |

on , that is, as for Borel sets contained in for some and satisfying , with the boundary of . The measure is called exponent measure because of the identity for .

Another statement equivalent to (2.1) is that the conditional distribution of given is asymptotically multivariate Pareto for high threshold , that is, we have the weak convergence relation

| (2.10) |

where is a random vector supported on with distribution equal to the restriction of in (2.9) to and normalized to a probability measure,

| (2.11) |

for Borel sets and normalizing constant . For , we also have .

Up to a location shift, multivariate Pareto distributions are a special case of multivariate generalised Pareto distributions introduced in Rootzén and Tajvidi (2006). They play a prominent role in the theory of graphical models for extremes (Engelke and Hitz, 2020). In the context of tail copula measures, it is more convenient to take component-wise reciprocals in (2.10) leading to inverted multivariate Pareto distributions, introduced in Section 6.

If the tail copula measure is concentrated on and has density , the exponent measure and the multivariate Pareto distribution have densities too. The exponent measure is concentrated on and has density

| (2.12) |

while the multivariate Pareto vector has probability density for .

By (2.3) and (2.9), the exponent measure is homogeneous of order and thus determined by the angular measure on the unit simplex via

for and Borel sets , with for . Under the above smoothness assumption, the angular measure is concentrated on the relative interior of the unit simplex and its density satisfies for (Dombry et al., 2016), see also Lemma B.1 in Appendix B.

2.2 Regular vine sequences and the vine telescoping product formula

Informally, a regular vine sequence on elements consists of a linked set of trees, where the edges in tree become nodes in tree , joined by an edge only if they share a common node as edges in tree , for (Bedford and Cooke, 2002). Regular vine copulas, also called pair copula constructions, allow for flexible high-dimensional modelling using parametric families of bivariate copulas as building blocks for the edges of each tree. For recent overviews, see, for example, the monograph by Czado (2019) or the survey article by Czado and Nagler (2022). Our objective is to do the same for tail copula densities.

Recall that a tree is a connected, acyclic graph comprising a node set and an edge set . Any two distinct nodes in a tree are connected by a unique path.

Definition 2.2 (Regular vine tree sequence).

An ordered set of trees is a regular vine tree sequence on elements if is a tree with node set , while for , the tree has node set and the proximity condition holds: for any , we have , that is, two nodes in can be connected only if, as edges in , they share a common node.

For brevity, we also use the term regular vine sequence. The proximity condition and other concepts defined below are illustrated via a five-dimensional example in Appendix A.

Definition 2.3 (Complete union, conditioning set, conditioned set).

Let be a regular vine sequence. For any edge , the complete union of is if and if and ; informally, is the subset of nodes in reachable from by the membership relation. The conditioning set of an edge with is and the conditioned set of is with and ; if , we have , , and .

Clearly, . Further, , and are disjoint subsets of ; and are singletons while has elements; and , a node set with elements. If , then ; indeed, by proximity, with , and ; similarly . Further, the conditioned sets are related by and . To see this, note that, by proximity, we have and for three distinct elements , and . Since both the left- and right-hand side are singletons, we must have ; similarly .

The edge is also written as and, since and are singletons, and , say, we abbreviate , with and the convention that , that is, and . Similarly, for , the convention is that . In Fig. 1, for instance, the edge labelled in has , , and . Appendix A contains a fully worked out example to illustrate these concepts.

For positive scalars with , the identity is known as a telescoping product. Regular vine sequences enjoy a similar property that will be key to Theorem 5.1 and which, to the best of our knowledge, has not yet been stated in the literature.

Lemma 2.4 (Vine telescoping product).

Let be an integer and let for every non-empty with for every . Given a regular vine sequence on , we have

| (2.13) |

With the notation , the last factor in (2.13) is

| (2.14) |

The formula (2.13) is spelled out in Eq. (A.1) in Appendix A for a five-dimensional regular vine sequence.

Remark 2.5 (Edge-wise vine telescoping product).

Given an edge for some in a regular vine sequence on , we can consider the sub-vine induced by on the node set in the natural way: we have where and for . Applying Lemma 2.4 to , we obtain the seemingly more general formula

| (2.15) |

3 Sklar’s theorem for tail copula densities

Let be a -variate tail copula density, that is, properties (2.4) and (2.5) hold. Recall its multivariate margins in (2.7). For non-empty, disjoint subsets and for and such that , define

Viewing the “conditional” tail copula density as an -variate probability density, we can decompose it into univariate probability densities and a copula density.

Proposition 3.1 (Sklar’s theorem: direct part).

Let be a -variate tail copula density and let be non-empty and disjoint. For such that , the function

is a probability density on . For , it has marginal probability density and cumulative distribution function

with quantile function . If , then the copula density of is

| (3.1) |

The homogeneity property (2.5) induces certain scaling properties.

Lemma 3.2 (Scale equi- and invariance).

In Proposition 3.1, for such that , the family of probability densities is a scale family: if the random vector has probability density then the random vector has probability density . As a consequence, for all , , and , we have

| (3.2) |

In particular, if for some , then does not depend on the value of .

Remark 3.3 (Conditional independence).

Let be the multivariate Pareto vector in (2.11), suppose , and let be distinct elements in , with . Provided is positive and continuous, and are conditionally independent given in the sense of Definition 1 in Engelke and Hitz (2020) if and only if for all and , the density of the independence copula. This statement follows by combining the factorization property in Proposition 1 in Engelke and Hitz (2020) with equations (2.12) and (3.1); see also (D.1) in Appendix D for an expression of directly in terms of the exponent measure density .

Definition 3.4 (Simplifying assumption).

The family of copula densities in (3.1) satisfies the simplifying assumption if the copula densities do not depend on , that is, there exists a single copula density such that for all and .

If is a singleton, , the scale invariance (3.2) implies that always satisfies the simplifying assumption. In Section 4, we will see that the copula families induced by many commonly used parametric exponent measure models satisfy the simplifying assumption for all and .

Sklar’s theorem for tail copula densities (Proposition 3.1) admits a converse part, stating how to combine several tail copula densities along a scale-invariant family of copula densities to form a tail copula density in a higher dimension. Proposition C.1 in Appendix C gives a precise statement. In the remainder of the paper, we will not use this result as such, although the X-vine construction in Section 5 is in the same spirit.

4 Parametric families of tail copula densities

We will compute the copula densities in (3.1) for tail copula densities arising from two parametric families: the scaled extremal Dirichlet model (Section 4.1) due to Belzile and Nešlehová (2017), encompassing the logistic, negative logistic and Dirichlet max-stable models, and the Hüsler–Reiss model (Section 4.2). For both families, the simplifying assumption (Definition 3.4) is satisfied for all choices of and , and the copula densities take on known parametric forms. This section can be skipped at first reading.

4.1 Scaled extremal Dirichlet model

In dimension , consider parameters and with . The angular measure density of the scaled extremal Dirichlet model is introduced in Belzile and Nešlehová (2017, Proposition 5). By Eq. (2.12) and Lemma B.1, the corresponding tail copula density is

| (4.1) |

for , where and . The model is closed under marginalisation: for with , the marginal tail copula density in (2.7) is of the same form in dimension and with parameters and . The model unites and extends several well-known parametric families in multivariate extreme value analysis:

In McNeil and Nešlehová (2010, Definition 3), the family of Liouville copulas is defined as the collection of survival copulas of random vectors of the form , where has a Dirichlet distribution on the unit simplex and is independent of the positive random variable , whose distribution is referred to as the radial distribution. The special case where is uniformly distributed on the unit simplex yields the family of Archimedean copulas (McNeil and Nešlehová, 2009).

Proposition 4.1.

Let be the scaled extremal Dirichlet tail copula density in (4.1) in dimension . For every pair of disjoint, non-empty subsets with , the copula densities in (3.1) satisfy the simplifying assumption (Definition 3.4). If , then is equal to density the -variate Liouville copula with Dirichlet parameters and with radial density on proportional to

If , then is equal to the density of the survival copula of the above Liouville copula.

In special cases, the copula densities can be identified more explicitly (calculations in Appendix B.3):

-

•

if and , then is the density of the -variate Clayton copula with parameter with ;

-

•

if and , then is the density of the -variate Clayton survival copula with parameter with .

In both cases, the dependence decreases as the number of conditioning variables increases.

4.2 Hüsler–Reiss model

Let be the set of symmetric, strictly conditionally negative definite matrices, that is, all matrices of the form for a -variate random vector with positive definite covariance matrix, i.e., is a variogram matrix. Fix and consider the -dimensional positive definite covariance matrix

| (4.2) |

for as in the previous sentence, we have . The -variate Hüsler–Reiss tail copula density is

| (4.3) |

where is the centered -dimensional Gaussian density with the stated covariance matrix and . The exponent measure density associated to via (2.12) appears in Engelke et al. (2015), where it is shown that it does not depend on the choice of . The corresponding max-stable distribution in (2.8) goes back to Hüsler and Reiss (1989), who studied maxima of triangular arrays of Gaussian random vectors.

For a matrix and for index sets and , write . Let denote the standard normal distribution function and recall that the -variate Gaussian copula density with -dimensional positive definite correlation matrix evaluated in is

| (4.4) |

Proposition 4.2.

Let be a variogram with and let be the Hüsler–Reiss tail copula density in (4.3). For every pair of disjoint, non-empty subsets with , the copula densities in (3.1) satisfy the simplifying assumption (Definition 3.4). The common copula density is equal to the -variate Gaussian copula density (4.4) with correlation matrix for any , where is the diagonal matrix with the same diagonal as

The expression of the correlation matrix in Proposition 4.2 depends on the choice of , although the actual matrix does not. This is because the proof is based on identity (4.3) for the tail copula density. In Hentschel et al. (2022), a formula for the exponent measure density is derived that does not require the choice of such an index . The formula involves what is called the Hüsler–Reiss precision matrix, denoted by . It remains to be investigated how to express the correlation matrix in terms of .

5 Vine decompositions of tail copula densities

In this section, we show that any tail copula density in dimension can be decomposed along any regular vine sequence (Definition 2.2) on elements into bivariate tail copula densities and bivariate copula densities. Moreover, the copula densities depending on a single conditioning variable satisfy the simplifying assumption (Definition 3.4). Conversely, starting from any regular vine sequence on elements, any collection of bivariate tail copula densities and any collection of bivariate copula densities, a -variate tail copula density can be assembled. We coin tail copula densities constructed in this way as X-vines. By exploiting connection (2.12) between tail copula densities and exponent measure densities, all results carry over to the latter too. For the reader’s convenience, the main formulas are spelled out in terms of exponent measure densities in Appendix D.

Theorem 5.1 (Tail copula density decomposition along a regular vine).

Let be a -variate () tail copula density and let with be a regular vine sequence on . For , we have

| (5.1) |

where, for , the pair-copula density is

with and for .

Remark 5.2.

The decomposition (5.1) is based on the vine telescoping product formulas (2.13)–(2.14) in Lemma 2.4. By applying the more general formula (2.15) in Remark 2.5, we find, for every edge with , a decomposition of the marginal tail copula density on the complete union , with cardinality : for , we have

| (5.2) |

The decomposition (5.2) is true only for subsets of the form for some edge in the regular vine sequence.

For the pair copula associated to the edge in the regular vine sequence, consider the first-order partial derivatives

| (5.3) |

Theorem 5.3 (Recursion and uniqueness).

In the setting of Theorem 5.1, for any , we have

| (5.4) |

As a consequence, is determined uniquely by the bivariate tail copula densities for and the bivariate copula densities for and .

Equation (5.4) is effectively a recursive relation, allowing to reduce the number of conditioning variables until there is only one conditioning variable left. The reason is that each of the indices and in (5.4) is itself of the form or for an edge in , i.e., one level lower than .

Definition 5.4 (X-vine tail copula density).

A -variate tail copula density is an X-vine along a regular vine sequence if for each edge , the pair copula densities do not depend on the value of . The -variate exponent measure density in (2.12) is called an X-vine if the tail copula density is an X-vine.

Example 5.5 (Trivariate case).

By Lemma 3.2, a trivariate tail copula density is always an X-vine, and this along any of the three possible regular vine sequences on . Indeed, for the vine sequence determined by , we can for instance write

featuring the copula density

The function is thus completely specified by the two bivariate tail copula densities and and the bivariate copula density . In Theorem 5.7 below, this construction principle is lifted to higher dimensions.

By Propositions 4.1 and 4.2, the scaled extremal Dirichlet model (including the logistic, negative logistic and extremal Dirichlet models) and the Hüsler–Reiss family have conditional copula densities that always satisfy the simplifying assumption. As a consequence, they are examples of X-vine tail copula densities too, and this along any regular vine sequence.

Definition 5.6 (X-vine specification).

The triplet is an X-vine specification on elements () if:

-

1.

with is a regular vine sequence on ;

-

2.

is a family of bivariate tail copula densities;

-

3.

is a family of bivariate copula densities.

Fig. 2 in Section 8 shows an example of an X-vine specification involving a mix of parametric models for the bivariate (tail) copula densities.

Theorem 5.7 (X-vine tail copula density construction).

Let be an X-vine specification on elements. Then the function defined by

| (5.5) |

with the functions defined recursively by

| (5.6) |

is a -variate tail copula density and its multivariate margins are the ones implied by the notation. In particular, is an X-vine.

Remark 5.8 (Link with regular vine copulas).

X-vine tail copula densities arise as the lower tail dependence limits of regular vine copula densities provided the pair copula densities at the edges of the first tree have the corresponding bivariate tail copula densities as lower tail dependence limits. In the passage to the limit, the regular vine sequence is preserved and so are the pair copulas at all trees starting from the second one. Max-stable dependence structures based on X-vines thus arise naturally from the max-domain of attraction condition of regular vine copulas, and the X-vine limit is particularly easy to calculate. These properties are worked out in Appendix E.

If the bivariate copula density associated with an edge is equal to the independence one, , the corresponding factor drops out in (5.1) and the recursive formulas in (5.4) and (5.6) simplify to

Sparse X-vine specifications arise when for many edges . Model selection of sparse vine copulas in high dimensions has been investigated in Müller and Czado (2019) and Nagler et al. (2019). The case where all pair copulas are equal to the independence one for all edges starting from a given tree is of practical importance (Brechmann et al., 2012; Brechmann and Joe, 2015).

Definition 5.9.

A truncated regular vine tree sequence on elements with truncation level is an ordered set of trees for which there exists a regular vine tree sequence on elements such that for all .

Definition 5.10.

The triplet is a truncated X-vine specification on elements () with truncation level if:

-

1.

is a truncated regular vine tree sequence on ;

-

2.

is a family of bivariate tail copula densities;

-

3.

is a family of bivariate copula densities; in case , we have .

By definition, any truncated X-vine specification can be completed to a full X-vine specification by completing the truncated regular vine tree sequence to a full one as in Definition 5.9 and by setting for all . The resulting X-vine copula density does not depend on the way in which the truncated regular vine tree sequence is completed, since the factorisation in (5.1) simplifies anyway to

with an empty second product in case . A truncated X-vine specification involves bivariate tail copula densities and bivariate copula densities, yielding bivariate components in total. The truncation level allows to tune the trade-off between sparsity and flexibility. If , the model is a Markov tree as in Engelke and Hitz (2020) and Segers (2020). Increasing and adding trees (‘layers’) yield more complex dependence structures. Truncated X-vine specifications will be shown at work in the case study in Section 9.

6 Sampling from X-vine Pareto distributions

6.1 Inverted multivariate Pareto distributions

In Section 2, we introduced the multivariate Pareto distribution (2.11) as a limit model for high threshold excesses in (2.10). In the context of tail copula measures, it is more convenient to work with their reciprocals.

Definition 6.1.

The -variate random vector has an inverted multivariate Pareto distribution if there exists a -variate tail copula measure such that

for Borel sets , with ; equivalently, if there exists a multivariate Pareto random vector such that .

If is concentrated on and has density , then has probability density . In general, for , the conditional distribution of given is uniform on ; this is a consequence of the marginal constraint (2.2). More generally, for Borel sets , we have

| (6.1) |

where the set has -measure one. Hence, on , the probability density of coincides with the tail copula density .

For the random vector in Definition 2.1, the inverted multivariate Pareto vector is the weak limit in

| (6.2) |

For non-empty , we have

The conditional marginal has a -variate inverted multivariate Pareto distribution associated with the marginal tail copula measure in (2.6). In contrast, the random vector does not necessarily have an inverted multivariate Pareto distribution, as is not guaranteed.

6.2 Random sampling from (inverted) multivariate Pareto distributions

Through equations (2.10) and (6.2), the (inverted) multivariate Pareto distribution serves as a model for a random vector conditionally on the event that at least one variable takes a value far in the tail of its respective marginal distribution. The L-shaped support of the (inverted) multivariate Pareto distribution makes direct random sampling from it a little awkward. Lemma 2 in Engelke and Hitz (2020) provides an ingenious algorithm that reduces the task of simulating from a multivariate Pareto random vector to random sampling from the conditional distributions for every . Below, we will study the equivalent problem of simulating from the conditional distribution of in case the tail copula density is an X-vine as in Definition 5.4.

We will do so by inverting the Rosenblatt transformation (Rosenblatt, 1952), applying conditional quantile functions with an increasing number of conditioning variables successively to independent uniform random variables. A judicious choice of the ordering of the variables permits to compute the required conditional quantile functions recursively in terms of the bivariate ingredients of the X-vine specification. This ordering is encoded in the permutation constructed in the next lemma.

Lemma 6.2.

Let be a regular vine sequence on elements. For every , there exists a permutation of such that (i) and (ii) there exist edges such that and for each .

Let be an X-vine tail copula density. For each edge and for fixed , let be the inverse of the distribution function , with defined in (5.3). Similarly for . Recall from Proposition 3.1 that for , non-empty , and such that , the quantile function is the inverse of the distribution function . Inverting (5.4) yields the recursive relations

| (6.3) |

Let be independent random variables, all uniformly distributed on . For , let be a permutation of satisfying the two requirements in Lemma 6.2. Define a random vector recursively as follows:

| (6.4) |

Proposition 6.3.

Let be an inverted multivariate Pareto random vector associated with the X-vine tail copula density . For , the distribution of in (6.4) is equal to the one of conditionally on . For every , the conditional quantile function is of the form or for some edge and can thus be computed recursively via (6.3).

7 Estimation and model selection

Let for be an independent random sample from a distribution function with continuous but unspecified margins and whose survival copula has lower tail copula (Definition 2.1). Suppose that the tail copula density is an X-vine with specification (Definitions 5.4 and 5.6 and Theorem 5.7). We propose a procedure to estimate from the excesses over a high multivariate threshold.

The regular vine sequence with trees may be known or not. The bivariate tail copulas for edges in the first tree and the bivariate copula densities for edges in trees are assumed to belong to prespecified (lists of) parametric families. The X-vine specification may be truncated (Definition 5.10), leading to a simpler model.

The basis of the method is a link between the conditional copula densities in Sklar’s theorem (Proposition 3.1) on the one hand and the inverted multivariate Pareto distribution (Definition 6.1) on the other hand (Section 7.1). In Section 7.2, we propose parameter estimates, supposing that is given and that parametric families of (tail) copula densities have been specified for all edges. In Section 7.3, finally, we treat model selection, which comprises the selection of the parametric families of the bivariate model components, the selection of the regular vine sequence , and the selection of the truncation level .

7.1 Copulas and inverted multivariate Pareto distributions

Let be a -variate copula tail copula density, not necessarily an X-vine. In Sklar’s theorem (Proposition 3.1), suppose that the copula density satisfies the simplifying assumption (Definition 3.4). The following proposition shows how to transform an inverted multivariate Pareto random vector associated to into a random vector with density .

Proposition 7.1.

Let be a -variate tail copula density and let be an inverted multivariate Pareto random vector associated to . Let be non-empty and disjoint.

-

(i)

For such that and , the conditional density of given is .

-

(ii)

Suppose . If satisfies the simplifying assumption (Definition 3.4), then, conditionally on the event , the random vector is independent of and its density is .

By statement (ii), the density of given is equal to for any non-empty set . For estimation, we will use this property for , requiring in effect that all variables (rather than at least one) in exceed a high threshold. We do so in order to avoid a potential bias stemming from including too many non-extreme values in the procedure. An alternative would be to opt for a censored likelihood approach (Ledford and Tawn, 1996), but this seems difficult to implement beyond dimensions two or three.

7.2 Sequential maximum likelihood estimation of X-vines

Let the -variate tail copula density be an X-vine specified by as in Theorem 5.7. Assume that the bivariate tail copula densities () and bivariate copula densities () belong to specified parametric families. Let denote the parameter vector associated with . Here, contains the parameters (or parameter vectors) associated with each pairwise tail copula density for , while for denotes the vector of parameters (or parameter vectors) associated with each bivariate copula density for . While it is possible to derive the full-likelihood of an X-vine (inverted) multivariate Pareto distribution, performing parameter estimation with the full model in high dimensions becomes challenging in extremes. Instead, using the X-vine decomposition into bivariate components and recursively defined quantities (Theorem 5.7), we outline a sequential procedure for parameter estimation, starting from to tree by tree. This approach is inspired by the one for regular vine copulas (see, e.g., Czado, 2019), but with suitable adaptations to the extreme value context.

(1) Standardising the margins and selecting sub-samples

Recall from the beginning of the section that , with , is an independent random sample from the unknown -variate distribution , whose survival copula is assumed to have tail copula with tail copula density . Set

| (7.1) |

where denotes any estimator of the marginal distribution function . One possibility is the empirical distribution function, and to avoid boundary effects, we set

| (7.2) |

where is the (maximal) rank of among . We view the points as pseudo-observations from the survival copula .

By Eq. (6.2), for large , the rescaled points for such that constitute pseudo-observations from a distribution that approximates the inverted multivariate Pareto distribution associated with . We set where is such that is ‘large’ and is ‘small’; in the usual large-sample setting in extreme value theory, we have with and . For , let

| (7.3) |

be the set of indices corresponding to observations whose the th component is ‘large’; for the rank-based definition of in the previous paragraph, this set of indices corresponds to the largest observations for the th variable. Further, put

which are, respectively the set of indices corresponding to large observations in all variables in simultaneously and the set of indices with large observations in at least one variable. Write where . In view of Eq. (6.2), we treat as a sample of pseudo-observations of the inverted multivariate Pareto distribution associated with . The sample size is random, and in the rank-based definition above, we have . For non-empty and , we write .

(2) Estimating the tail copula parameters in

For each edge , we estimate the parameter (vector) associated with the bivariate tail copula density . By Eq. (6.1), for , the conditional density of given is . As one out of many possibilities, we use maximum pseudo-likelihood estimation to fit this density to the sub-samples for both and , with as in Eq. (7.3), More precisely, we maximise each of the two pseudo-likelihoods

| (7.4) |

over , yielding estimates and , respectively. The final estimate is . The idea of averaging maximum pseudo-likelihood estimators on product spaces has already been suggested for the Hüsler–Reiss model in (Engelke et al., 2015), and implemented for multivariate Pareto distributions in the graphicalExtremes package (Engelke et al., 2022). Other approaches for parameter estimation can be considered: censored likelihoods (Ledford and Tawn, 1996; de Haan et al., 2008) or the empirical stable tail dependence functions (Einmahl et al., 2008, 2018).

(3) Estimating the copula parameters in

Start with an edge , i.e., such that is a singleton, , say. Then and are edges in . By Proposition 7.1(ii), the density of the random pair

is . The tail copula density parameters and have been estimated in the previous step, yielding estimates and . Define pseudo-observations for from by

We estimate the parameter (vector) by maximising the pseudo-likelihood

| (7.5) |

Other estimators are possible based on parametric relationships between the dependence coefficients such as Kendall’s tau and Spearman’s rho in relation to the parameters of corresponding bivariate copula densities (Czado, 2019).

Parameters (or parameter vectors) associated with edges in for layers can be estimated similarly, proceeding recursively. Suppose that all parameters associated with edges in have already been estimated; let denote the parameters and their estimate. By Proposition 7.1(i), the density of the random pair

is . Define pseudo-observations for from by

| (7.6) |

In this definition, the conditional distribution functions and are calculated recursively via Eq. (5.6) with in that formula replaced by the edges that are joined by , that is, such that . The parameter (vector) is then obtained by maximising the pseudo-likelihood in (7.5).

7.3 Model selection for X-vines

Model selection for X-vines based on a random sample from as in Section 7.2 involves two steps:

-

(1)

selecting a regular vine sequence ;

-

(2)

given the regular vine sequence obtained in (1), choosing adequate bivariate parametric (tail) copula families, and .

In fact, the two procedures are executed together sequentially, progressing from one tree to the next tree. First, we describe step (2) given the regular vine sequence .

Selecting parametric (tail) copula families given a truncated regular vine sequence

We first consider the specification of in Definition 5.6 in tree . Let be the list of candidate bivariate tail copula families. For each edge , specifying involves choosing the bivariate tail copula family among . Similar to the idea of averaged maximum pseudo-likelihood estimates in Section 7.2, we use the averaged-AIC value for selecting bivariate tail copula families. For each edge and each , , we obtain two maximum pseudo-likelihood estimates and , derived through the maximisation of log-likelihood functions on product spaces; see (7.4). The averaged-AIC value is

where is the number of parameters in . We select the bivariate tail copula family with the lowest averaged-AIC among .

Similarly, we specify in Definition 5.6 in for . Let denote the list of candidate bivariate parametric copula families, including the independence copula (without parameters). Specifying involves selecting the bivariate parametric copula family among for each edge . We do so by maximising the AIC, following the common practice in vine copula modelling; see Brechmann (2010) and (Czado, 2019, Section 8.1). For each edge , we estimate the associated parameter (vector) by maximising the log-likelihood (7.5), and we calculate the corresponding AIC over the list of the bivariate parametric copula families , ,

where is the number of parameters in , and if contains only the independence copula. We then choose the bivariate parametric copula family with the lowest value among .

It is worthwhile to note that when implementing the model selection step for an edge in , only the trees need to have been selected, but not the trees . This sequential approach aligns well with the vine learning procedure in the next paragraph.

Selecting the regular vine sequence

Morales-Napoles (2010) showed that the number of different regular vine sequences is equal to , making it impossible to go through all possible vine structures. We adopt the model selection approach similar to the one in Dissmann et al. (2013), choosing trees sequentially from to .

To select the first tree, , on the node set , we follow a procedure as in Engelke and Volgushev (2022) and Hu et al. (2023). For every pair of distinct elements in , let be a nonnegative weight derived from the data. We will be using an empirical version of the tail dependence coefficient , namely we will set equal to

where and are defined as in (7.2). Another possible edge weight would be the empirical extremal variogram as in Engelke and Volgushev (2022). The first tree is then selected as the maximum-spanning tree based on the edge weights , that is,

For each edge in , we then select parametric tail copula densities and estimate their parameters as previously explained.

Next we describe, for , how to select the tree given the already selected trees and the parametric families and parameter estimates for edges . The edge set of is necessarily . Let be the set of pairs of elements of that satisfy the proximity condition (Definition 2.2); that is, every element of is a pair of distinct elements in so that is a singleton. For such , we can then consider the conditioning set and the conditioned set as before and, by recursion, compute and for as in (7.6). Based on these, we compute an edge weight ; we will take the absolute value of the empirical Kendall’s tau, . We then select as the maximum spanning tree on the node set with edges restricted to , that is,

For each edge , we further select the parametric copula families and estimate their parameters as before.

Selecting truncated regular vine tree sequences

The model selection procedure described above may set all pair-copulas to the independence copula in the subsequent trees from to for a truncation level . In this case, the resulting model corresponds to the truncated X-vine model in Definition 5.10. Besides an information criterion, we consider two additional criteria for selecting the independence copula at an edge : when the effective sample size falls below a certain low value, and when the absolute value of the empirical Kendall’s tau is close to zero. Sparsity, induced by a smaller effective sample size, is more likely when the total sample size is relatively smaller than the dimension ; recall that we condition on variables being extreme in tree as explained in Section 7.2.

Even when the above criteria are not met, when is large, it is natural to limit the number of model parameters by considering truncated X-vines, since Dissmann’s algorithm captures as much dependence as possible in the first few trees. We use a modified Bayesian information (mBIC) to determine the truncation level, inspired by the one for regular vine copulas in Nagler et al. (2019). This modified version adjusts the prior probability in the BIC to penalise dependence copulas more severely in trees at higher levels. More specifically, assuming that for any edge for , the parametric family has a single parameter and that a value of corresponds to the independence copula, the mBIC includes independent Bernoulli variables with mean for and a hyperparameter : set and, for , put

| (7.7) |

with as in (7.5). The selected truncation level is the value of in that minimises . In practice, we will set as in Nagler et al. (2019).

8 Simulation study

We conduct three simulation studies, evaluating the proposed procedures for parameter estimation, selection of bivariate parametric (tail) copula families, and vine truncation.

8.1 Parameter estimation

We first consider the -dimensional X-vine model in Fig. 2. The bivariate tail copula densities in the first tree are chosen from the Hüsler–Reiss model, the negative logistic, logistic, and Dirichlet families (Section 4), while the bivariate copula densities in the subsequent trees for are taken from the Clayton, Gumbel, and Gaussian copula families. We specify the parameter values for the bivariate parametric families as follows, including the tail dependence coefficient or Kendall’s for comparison: , , , ; , , ; , ; and . The formulas connecting the parameters of the families of tail copula densities with the value of are given in Appendix F.2.

Implementing simulation algorithms as detailed in Section 6 and Appendix A, we generate multivariate inverted Pareto random samples associated with in Section 6. Rather than using these directly, we perform a rank transformation as defined in (7.1) with , where denotes the rank of among for . We then take sub-samples with and as in (7.3) to investigate simulation results with respect to threshold exceedances.

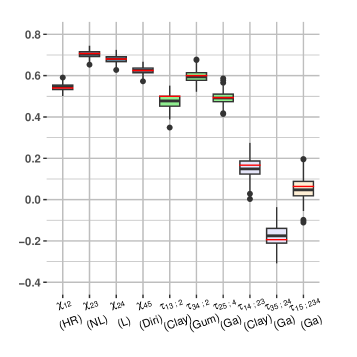

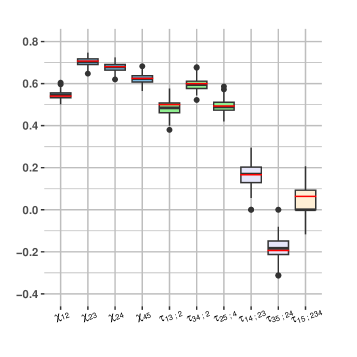

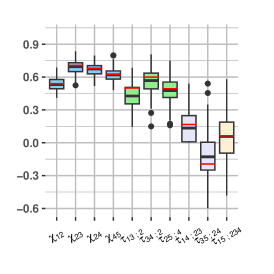

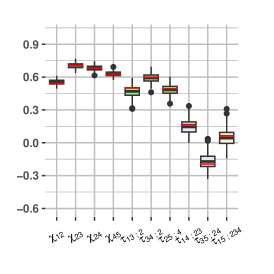

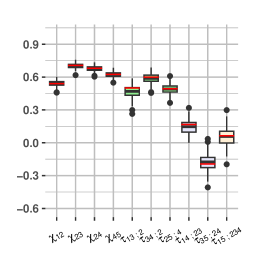

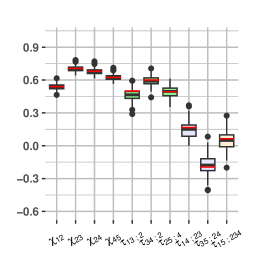

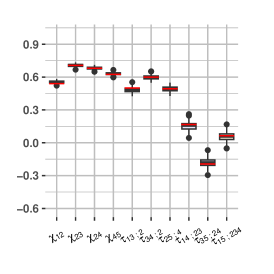

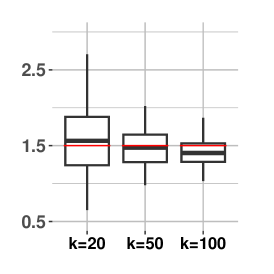

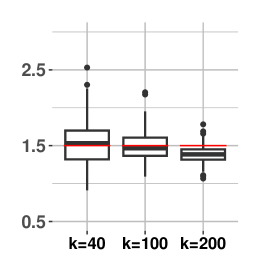

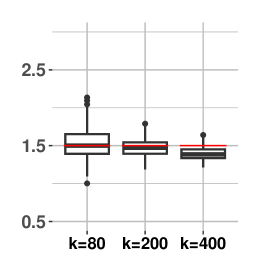

We set and perform sequential parameter estimation as in Section 7.2 over 200 repetitions. We obtain maximum pseudo-likelihood estimates and the model-based dependence measures, and , using the parametric relations in Appendix F.2 for each of the ten edges in the vine. In Fig. LABEL:fig:boxplot_SPE, box-plots present dependence measure estimates from specified parametric families based on the X-vine specification in Fig. 2. The four left-most box-plots () show the tail dependence coefficient estimates for the four edges , and the remaining plots display Kendall’s tau estimates for the six edges . Appendix F.2 includes additional box-plots: first, of dependence measures with varying sample sizes and threshold exceedances, and second, of maximum likelihood estimates of tail copula densities for a specific edge with varying .

8.2 Selecting parametric (tail) copula families

We assess algorithm effectiveness in selecting bivariate parametric families for each edge in each tree, using the same X-vine specification as in Fig. 2. While the flexibility of X-vine models allows us to consider any bivariate parametric family, we simplify the process by considering a catalogue of four candidate tail copula models for : the Hüsler–Reiss, negative logistic, logistic model, and Dirichlet model, along with a catalogue of nine candidate pair-copula families for : Independence, Gaussian, Clayton, Survival Clayton, Gumbel, Survival Gumbel, Frank, Joe, and Survival Joe copulas, as implemented in the VineCopula software package (Nagler et al., 2023).

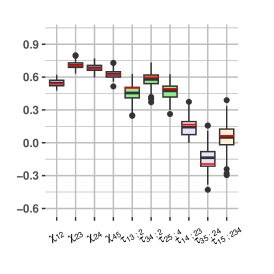

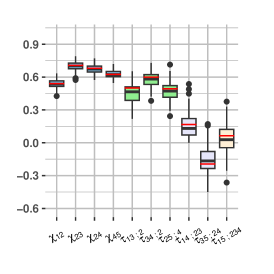

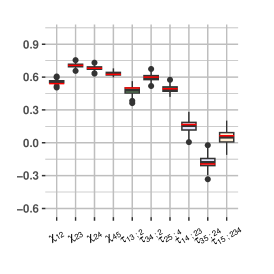

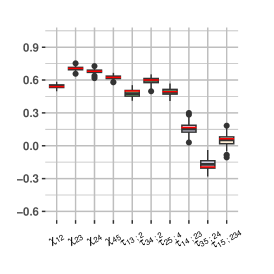

Using again 200 repetitions with , we assess the accuracy of the (averaged) AIC in Section 7.3 in selecting bivariate parametric families. The overall proportion of correctly selected families across all tree levels is 60%. For individual trees, the proportions are as follows: 62% for , 78% for , 55% for , and 10% for . The specific proportions for each edge in each tree are presented in Table 1(a). The lower proportions observed for and in result from the challenge in distinguishing between the negative logistic and logistic models. Overall, the proportion of accurately selected families decreases with declining effective sample size and Kendall’s tau estimate across tree levels. We observe the lowest proportion for the deepest edge where the corresponding pair-copula exhibits weak dependence; the algorithm selects the independence copula for this edge 110 times out of 200. Additionally, box-plots of dependence measure estimates from sequentially selected bivariate parametric families over 200 repetitions are presented in Fig. LABEL:fig:boxplot_Fam.

We also investigate how effective sample sizes change over tree levels shown in Table 1(b). We calculate averaged-effective sample size over 200 repetitions for each edge in each tree and express it as a percentage of the sample size . The overall averaged-effective sample size decreases in the first level tree when considering stronger extremal structures (result is omitted). This reduction is due to the fact that, for a high threshold , the probability decreases as the tail dependence between and increases. For the second level tree , the averaged-effective sample is , since the use of the rank transform implies (in the absence of ties) the identity for all .

| 99% | 40% | 60% | 49% | |

| 58% | 93% | 82% | ||

| 42% | 68% | |||

| 11% |

| 7.30% | 6.47% | 6.60% | 6.87% | |

| 5.00% | 5.00% | 5.00% | ||

| 3.52% | 3.38% | |||

| 3.12% |

8.3 Tree selection and truncation

We consider a higher dimensional X-vine model where residual dependence weakens with increasing tree level. Specifically, for we consider a -dimensional C-vine, that is, in each tree , there is a single node such that belongs to the conditioned set of all edges . The first tree includes the Hüsler–Reiss models and negative logistic models with randomly assigned parameter values for . Subsequent trees contain bivariate Gaussian copulas with partial correlations for and , and for with . This X-vine specification allows us to explore truncated X-vine models by setting pair-copulas with weak dependence to independence copulas.

We directly use inverted multivariate Pareto samples of size from the X-vine model for a later comparison of model-based tail dependence coefficients. Using the procedures explained in Sections 7.2 and 7.3, we sequentially select trees using for and for , , as edge weights. For each selected tree, we choose the bivariate parametric families with the lowest (averaged) AIC for each edge and estimate the associated parameters. Additionally, the independence copulas in subsequent trees are chosen if either or for each edge.

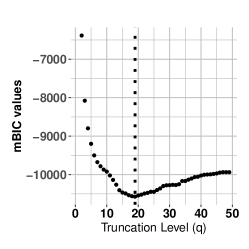

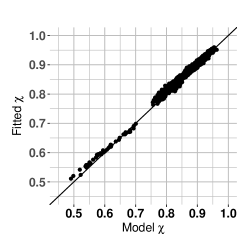

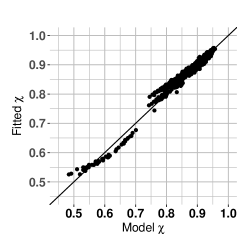

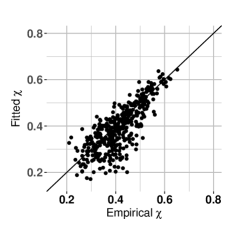

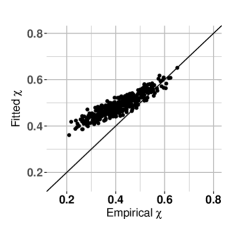

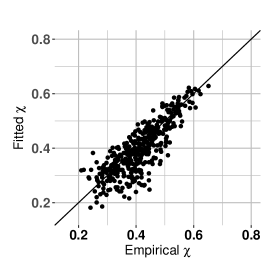

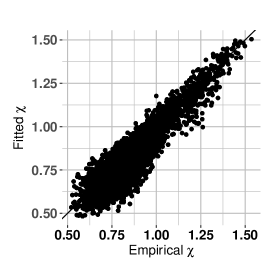

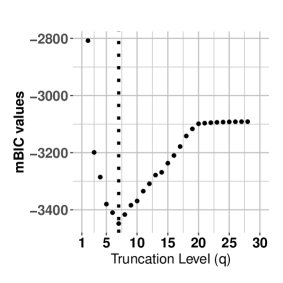

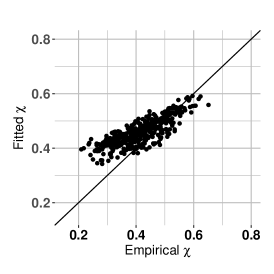

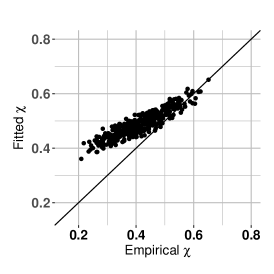

To explore truncated X-vine models, we use the mBIC with as in Nagler et al. (2019). For a specific iteration, we select the mBIC-optimal truncation level of , indicated as a dotted line in Fig. LABEL:fig:mBIC50dim. We assess the goodness of fit by comparing pairwise -values from the specified 50-dimensional X-vine model with those obtained from the fitted truncated X-vine model via Monte Carlo simulations in Fig. LABEL:fig:Chi50dim (for bivariate tail copula densities, closed-form expressions of are available for most well-known parametric tail copula density families; see Appendix F). In the case of the truncated X-vine model, the chi-plot in Fig. LABEL:fig:Chi50Trunc resembles that of the full model but exhibits more variability, particularly for lower values.

9 Application: US flight delay data

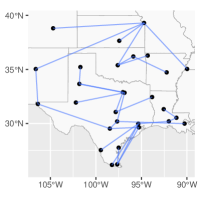

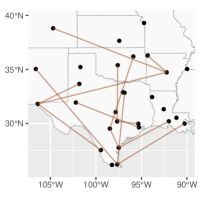

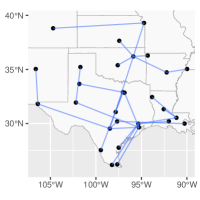

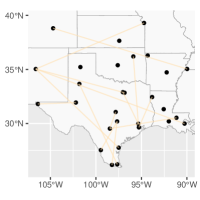

We apply X-vine models to investigate extremal dependence among large flight delays in the US flight network. The raw data-set is accessible through the US Bureau of Transportation Statistics111https://www.bts.dot.gov. These flight delay data were analysed by Hentschel et al. (2022) who first selected airports with a minimum of 1 000 flights per year and applied a -medoids clustering algorithm to identify homogeneous clusters in terms of extremal dependence. This clustering approach not only makes the analysis suitable for modelling extremal dependence but also reveals shared frequent flight connections between airports and similar geographical characteristics in each cluster. Focusing on the Hüsler–Reiss family, Hentschel et al. (2022) fitted an extremal graphical model to large flight delays of airports in the Texas cluster to investigate conditional independence.

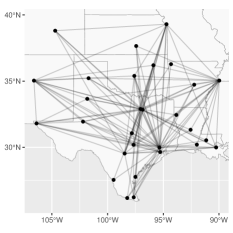

For the purpose of model comparison, we also analyse daily total delays (in minutes) in the Texas cluster. The cluster comprises airports and counts days from 2005 to 2020, during which all airports have recorded measurements. This pre-processed data is available through the R-package graphicalExtremes (Engelke et al., 2022). A graphical representation of the actual flight connections between airports is presented in Fig. LABEL:fig:FlightGraphDomain. While the graph derived from flight connections does not guarantee the optimal graph in terms of extremal behavior, it offers valuable insights into the flight network.

Let denote the observed measurements. Following the standardisation process with the rank transformation as in Section 7.2, we take sub-samples for where is the threshold of the uniform margin . We choose such that in order to have a large enough effective sample size in relation to the number of variables.

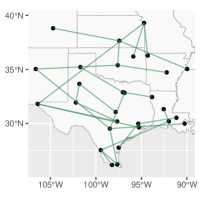

Assigning for and for , , as edge weights, we select the vine tree structure sequentially as in Section 7.3. The first maximum spanning tree is obtained with a range of estimated tail dependence coefficients between and and a mean of in Fig. 9 in Appendix F.3. Out of the edges in , selected bivariate tail copula families include the Hüsler–Reiss ( edges), negative logistic ( edges) and Dirichlet models ( edges). Subsequent trees with a total of edges are then chosen with the following pair-copula families (the number of edges inside parentheses): Independence (201), Gaussian (31), Clayton (8), Gumbel (26), Frank (34), Joe (36), Survival Clayton (31), Survival Gumbel (9), and Survival Joe (2). As the tree level rises, we observe a decline in residual dependence and an increase in the number of independence copulas. The X-vine algorithm sets all pair copulas to the independence copula from tree level , that is, the vine is truncated at level .

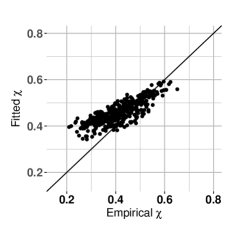

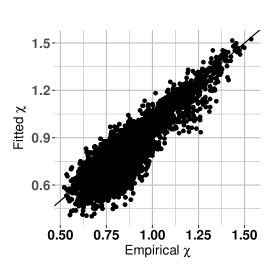

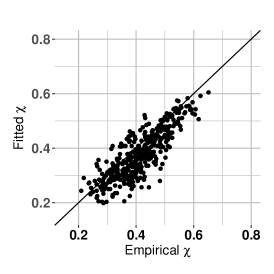

To evaluate the X-vine model’s efficacy in capturing extremal dependence for large flight delays between airports in the Texas cluster, we estimate bivariate and trivariate tail dependence coefficients. We compare empirical pairwise tail dependence coefficients for with those from the fitted X-vine model in Fig. LABEL:fig:ChiflightFullXvine. Additionally, Fig. LABEL:fig:Chi3FlightFull in Appendix F.3 compares trivariate empirical tail dependence coefficients for with those obtained from the fitted X-vine model. Both assessments indicate a satisfactory fit for the large flight delays data.

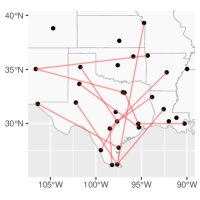

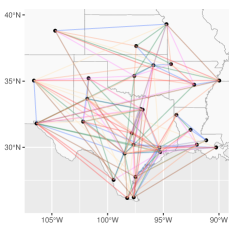

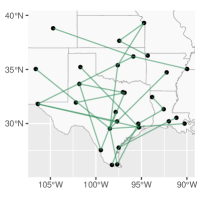

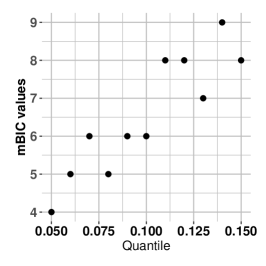

To further explore truncated X-vine models with a lower truncation level, we use the mBIC in Eq. (7.7). Fig. LABEL:fig:mBICFlight illustrates the mBIC-optimal truncation level of , which corresponds to 113 dependence copulas [Gaussian (17), Clayton (3), Gumbel (23), Frank (16), Joe (25), Survival Clayton (22), Survival Gumbel (6), and Survival Joe (1)] out of the 147 total edges from to . The total number of bivariate model components is thus . Additionally, we investigate how the truncation level changes over the threshold range of in Fig. LABEL:fig:mBICvsQuan in Appendix F.3. It appears that the mBIC-optimal truncation levels are not overly sensitive to the choice of the threshold. The superimposed graph of the first seven vine trees is shown in Fig. LABEL:fig:FlightGraphXvineTrunc, showing for to only the 113 out of 147 edges for which a copula other than the independence one is selected. The level by level vine tree sequence from to is presented in Fig. 9 in Appendix F.3.

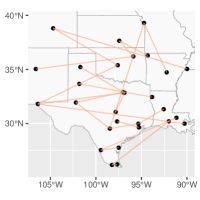

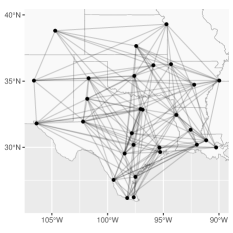

Returning attention to model comparison, we consider extremal graphical models with the Hüsler–Reiss distribution, another sparse model for extremes, detailed in Engelke et al. (2021) and Hentschel et al. (2022). Hentschel et al. (2022) obtained the sparse Hüsler–Reiss graphical model through a structure learning method, using the EGlearn algorithm of Engelke et al. (2021) for the sequential estimation of extremal graphical structure from data. The tuning parameter controls sparsity, and the empirical extremal variogram matrix is used as edge weight for the minimum spanning tree with smaller elements in indicating stronger extremal dependence.

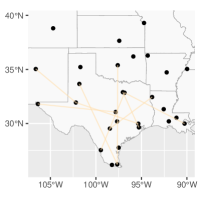

Following the vignette in Engelke et al. (2022), the data set is split in half: a training set for model fitting and a test set for tuning parameter selection. We determine the optimal tuning parameter, , by evaluating the Hüsler–Reiss log-likelihood values across tuning parameter values from the test set. The resulting sparse extremal graph with 148 edges at is shown in Fig. LABEL:fig:FlightGraphEGlearn.

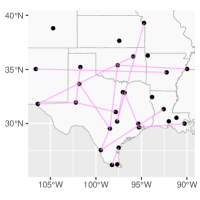

We assess the goodness of fit using the entire sub-samples and compare empirical tail dependence coefficients to those obtained from the fitted graphical models: the Hüsler–Reiss extremal graphical model for the flight graph in Fig. LABEL:fig:ChiFlightDomain, the truncated X-vine model with in Fig. LABEL:fig:ChiFlightTruncXvine, and the extremal Hüsler–Reiss graphical model with in Fig. LABEL:fig:ChiFlightEGlearn, respectively.

The flexibility of a regular vine structure allows the selection of various (tail) copula families with the lowest AIC. Recall from Section 4.2 that the Hüsler–Reiss model arising from the X-vine specification is constructed using bivariate Hüsler–Reiss tail copula densities in the first tree and bivariate Gaussian copulas in subsequent trees. In the truncated X-vine model, 8 out of 28 edges prefer Hüsler–Reiss models in , while in trees for , 96 out of 113 edges favour copula families other than the Gaussian one. However, uncertainty in sequential parameter estimation tends to accumulate across tree levels. Consequently, the -plot of the truncated X-vine model shows a better fit but more variability. In contrast, the -plot of the extremal Hüsler–Reiss graphical model has less variability but seems to biased towards higher tail dependence.

Similarly, focusing exclusively on the Hüsler–Reiss model, Fig. 12 presents a model comparison between the extremal Hüsler–Reiss graphical model based on the flight graph, the Hüsler–Reiss model derived from the X-vine structure, and the extremal Hüsler–Reiss graphical model from the EGlearn algorithm. Additional details about the fitted models and model comparison are provided in Appendix F.3.

10 Discussion

We have opened the door to the construction and the use of extremal dependence models based on regular vine tree sequences. For (ordinary) copulas, the methodology has been extensively developed in the literature since its inception more than two decades ago. Our contribution is to deliver the theoretical and methodological advances required to apply vine machinery in the extreme value context too. The key consists of a version of Sklar’s theorem applied to tail copula densities, which stand in one-to-one relation to exponent measure densities, together with a telescoping product formula for regular vines. For many popular parametric families of tail dependence models, the resulting conditional copula densities satisfy a simplifying assumption. Tail copula densities with this property, called X-vines, are specified by a triple consisting of a regular vine sequence, a vector of bivariate tail copula densities and a vector of bivariate copula densities. These bivariate building blocks can be chosen independently from another, yielding great flexibility. At the same time, the recursive properties of regular vines ensure that all computations can be reduced to operations involving the bivariate building blocks only. Further, we have studied the inverted multivariate Pareto distributions associated to these X-vines, as dependence models for excesses over high multivariate thresholds. A recursive algorithm serves to sample from such distributions, and we have developed a statistical methodology on them, in order to learn an X-vine from data. The method comprises parameter estimation, model selection, and vine structure learning, all proceeding sequentially, tree by tree. In large dimensions, truncating the vine sequence produces models with fewer parameters. We have illustrated the performance of the various methods on simulated and real data.

While the proposed methodology is fully operational, it is clearly open to improvement, while many open questions remain, just as for ordinary regular vine copulas. We name just a few. The vine structure learning method inspired by Dissmann et al. (2013) aims to capture dependence by the first several trees in the sequence, but there is no guarantee that it retrieves the true structure. The regular vine atlas of Morales-Nápoles et al. (2023) can serve as a test bed for evaluating vine learning approaches. While the parameter estimators were shown to perform well in simulations, their large-sample theory remains to be developed, in line with Hobæk Haff (2013). For the Hüsler–Reiss model, the precise connection between the variogram matrix and the correlation parameters of the bivariate Gaussian copulas remains to be elucidated and the effect of truncation on the Hüsler–Reiss precision matrix (Hentschel et al., 2022) to be uncovered. The relation between X-vines and graphical models for extremes as in Engelke and Hitz (2020) deserves further investigation, perhaps leveraging results of Zhu and Kurowicka (2022). Finally, as our approach is limited to dependence structures generated from max-stable distributions, a completely open question is whether it can be extended to other settings in multivariate extreme value analysis, such as the conditional extremal dependence model (Heffernan and Tawn, 2004) or the geometric sample-cloud approach (Nolde, 2014; Simpson et al., 2021).

Acknowledgments

This work is supported in part by funds from the Fonds de la Recherche Scientifique – FNRS, Belgium (grant number T.0203.21).

References

- Bedford and Cooke (2001) Bedford, T. and R. M. Cooke (2001). Probability density decomposition for conditionally dependent random variables modeled by vines. Annals of Mathematics and Artificial intelligence 32, 245–268.

- Bedford and Cooke (2002) Bedford, T. and R. M. Cooke (2002). Vines–a new graphical model for dependent random variables. The Annals of Statistics 30(4), 1031–1068.

- Beirlant et al. (2004) Beirlant, J., Y. Goegebeur, J. Segers, and J. L. Teugels (2004). Statistics of Extremes: Theory and Applications, Volume 558. John Wiley & Sons.

- Belzile and Nešlehová (2017) Belzile, L. R. and J. G. Nešlehová (2017). Extremal attractors of Liouville copulas. Journal of Multivariate Analysis 160, 68–92.

- Brechmann (2010) Brechmann, E. (2010). Truncated and simplified regular vines and their applications. Master’s thesis, Technische Universität Muünchen.

- Brechmann et al. (2012) Brechmann, E. C., C. Czado, and K. Aas (2012). Truncated regular vines in high dimensions with application to financial data. Canadian journal of statistics 40(1), 68–85.

- Brechmann and Joe (2015) Brechmann, E. C. and H. Joe (2015). Truncation of vine copulas using fit indices. Journal of Multivariate Analysis 138, 19–33.

- Coles and Tawn (1991) Coles, S. G. and J. A. Tawn (1991). Modelling extreme multivariate events. Journal of the Royal Statistical Society: Series B (Methodological) 53(2), 377–392.

- Czado (2019) Czado, C. (2019). Analyzing dependent data with vine copulas, Volume 222 of Lecture Notes in Statistics. Springer, Cham. A practical guide with R.

- Czado and Nagler (2022) Czado, C. and T. Nagler (2022). Vine copula based modeling. Annual Review of Statistics and Its Application 9, 453–477.

- de Haan and Ferreira (2007) de Haan, L. and A. Ferreira (2007). Extreme Value Theory: An Introduction. Springer Science & Business Media.

- de Haan et al. (2008) de Haan, L., C. Neves, and L. Peng (2008). Parametric tail copula estimation and model testing. Journal of Multivariate Analysis 99(6), 1260–1275.

- de Haan and Resnick (1977) de Haan, L. and S. I. Resnick (1977). Limit theory for multivariate sample extremes. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete 40(4), 317–337.

- Dissmann et al. (2013) Dissmann, J., E. C. Brechmann, C. Czado, and D. Kurowicka (2013). Selecting and estimating regular vine copulae and application to financial returns. Computational Statistics & Data Analysis 59, 52–69.

- Dombry et al. (2016) Dombry, C., S. Engelke, and M. Oesting (2016). Asymptotic properties of the maximum likelihood estimator for multivariate extreme value distributions. arXiv preprint arXiv:1612.05178.

- Einmahl et al. (2018) Einmahl, J. H., A. Kiriliouk, and J. Segers (2018). A continuous updating weighted least squares estimator of tail dependence in high dimensions. Extremes 21, 205–233.

- Einmahl et al. (2008) Einmahl, J. H., A. Krajina, and J. Segers (2008). A method of moments estimator of tail dependence. Bernoulli 14(4), 1003–1026.

- Einmahl et al. (2001) Einmahl, J. H. J., V. I. Piterbarg, and L. de Haan (2001). Nonparametric estimation of the spectral measure of an extreme value distribution. The Annals of Statistics 29(5), 1401–1423.

- Engelke et al. (2022) Engelke, S., A. Hitz, N. Gnecco, and M. Hentschel (2022). graphicalExtremes: Statistical methodology for graphical extreme value models. R package version 0.2.0.

- Engelke and Hitz (2020) Engelke, S. and A. S. Hitz (2020). Graphical models for extremes. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 82(4), 871–932.

- Engelke and Ivanovs (2021) Engelke, S. and J. Ivanovs (2021). Sparse structures for multivariate extremes. Annual Review of Statistics and Its Application 8, 241–270.

- Engelke et al. (2022) Engelke, S., J. Ivanovs, and K. Strokorb (2022). Graphical models for infinite measures with applications to extremes and Lévy processes. arXiv preprint arXiv:2211.15769.

- Engelke et al. (2021) Engelke, S., M. Lalancette, and S. Volgushev (2021). Learning extremal graphical structures in high dimensions. arXiv preprint arXiv:2111.00840.

- Engelke et al. (2015) Engelke, S., A. Malinowski, Z. Kabluchko, and M. Schlather (2015). Estimation of Hüsler–Reiss distributions and Brown–Resnick processes. Journal of the Royal Statistical Society Series B: Statistical Methodology 77(1), 239–265.

- Engelke and Volgushev (2022) Engelke, S. and S. Volgushev (2022). Structure learning for extremal tree models. Journal of the Royal Statistical Society Series B: Statistical Methodology 84(5), 2055–2087.

- Gissibl and Klüppelberg (2018) Gissibl, N. and C. Klüppelberg (2018). Max-linear models on directed acyclic graphs. Bernoulli 24(4A), 2693–2720.

- Gumbel (1960) Gumbel, E. J. (1960). Distributions des valeurs extrêmes en plusieurs dimensions. Publ. Inst. Statist. Univ. Paris 9, 171–173.

- Heffernan and Tawn (2004) Heffernan, J. E. and J. A. Tawn (2004). A conditional approach for multivariate extreme values (with discussion). Journal of the Royal Statistical Society Series B: Statistical Methodology 66(3), 497–546.

- Hentschel et al. (2022) Hentschel, M., S. Engelke, and J. Segers (2022). Statistical inference for Hüsler–Reiss graphical models through matrix completions. arXiv preprint arXiv:2210.14292.

- Hobæk Haff (2013) Hobæk Haff, I. (2013). Parameter estimation for pair-copula constructions. Bernoulli 19(2), 462–491.

- Hu et al. (2023) Hu, S., Z. Peng, and J. Segers (2023). Modelling multivariate extreme value distributions via markov trees. Scandinavian Journal of Statistics n/a(n/a), https://doi.org/10.1111/sjos.12698.

- Hüsler and Reiss (1989) Hüsler, J. and R.-D. Reiss (1989). Maxima of normal random vectors: Between independence and complete dependence. Statistics & Probability Letters 7(4), 283–286.

- Joe (1990) Joe, H. (1990). Families of min-stable multivariate exponential and multivariate extreme value distributions. Statistics & Probability Letters 9(1), 75–81.

- Joe (1996) Joe, H. (1996). Families of -variate distributions with given margins and bivariate dependence parameters. In Distributions with fixed marginals and related topics (Seattle, WA, 1993), Volume 28 of IMS Lecture Notes Monogr. Ser., pp. 120–141. Inst. Math. Statist., Hayward, CA.

- Joe et al. (2010) Joe, H., H. Li, and A. K. Nikoloulopoulos (2010). Tail dependence functions and vine copulas. Journal of Multivariate Analysis 101(1), 252–270.

- Ledford and Tawn (1996) Ledford, A. W. and J. A. Tawn (1996). Statistics for near independence in multivariate extreme values. Biometrika 83(1), 169–187.

- McNeil and Nešlehová (2010) McNeil, A. J. and J. Nešlehová (2010). From Archimedean to Liouville copulas. Journal of Multivariate Analysis 101(8), 1772–1790.

- McNeil and Nešlehová (2009) McNeil, A. J. and J. Nešlehová (2009). Multivariate Archimedean copulas, -monotone functions and -norm symmetric distributions. The Annals of Statistics 37(5B), 3059–3097.

- Morales-Napoles (2010) Morales-Napoles, O. (2010). Counting vines. In Dependence modeling: Vine copula handbook, pp. 189–218. World Scientific.

- Morales-Nápoles et al. (2023) Morales-Nápoles, O., M. Rajabi-Bahaabadi, G. A. Torres-Alves, and C. M. P. ’t Hart (2023). Chimera: An atlas of regular vines on up to 8 nodes. Scientific Data 10(1), 337.

- Müller and Czado (2019) Müller, D. and C. Czado (2019). Selection of sparse vine copulas in high dimensions with the lasso. Statistics and Computing 29(2), 269–287.

- Nagler et al. (2019) Nagler, T., C. Bumann, and C. Czado (2019). Model selection in sparse high-dimensional vine copula models with an application to portfolio risk. Journal of Multivariate Analysis 172, 180–192.

- Nagler et al. (2023) Nagler, T., U. Schepsmeier, J. Stoeber, E. C. Brechmann, B. Graeler, and T. Erhardt (2023). VineCopula: Statistical Inference of Vine Copulas. R package version 2.4.5.

- Nagler and Vatter (2023) Nagler, T. and T. Vatter (2023). rvinecopulib: High Performance Algorithms for Vine Copula Modeling. R package version 0.6.3.1.1.

- Nolde (2014) Nolde, N. (2014). Geometric interpretation of the residual dependence coefficient. Journal of Multivariate Analysis 123, 85–95.

- R Core Team (2023) R Core Team (2023). R: A Language and Environment for Statistical Computing. Vienna, Austria: R Foundation for Statistical Computing.

- Resnick (2007) Resnick, S. I. (2007). Heavy-tail phenomena: probabilistic and statistical modeling. Springer Science & Business Media.

- Rootzén and Tajvidi (2006) Rootzén, H. and N. Tajvidi (2006). Multivariate generalized Pareto distributions. Bernoulli 12(5), 917–930.

- Rosenblatt (1952) Rosenblatt, M. (1952). Remarks on a multivariate transformation. The Annals of Mathematical Statistics 23(3), 470–472.

- Schmidt and Stadtmüller (2006) Schmidt, R. and U. Stadtmüller (2006). Non-parametric estimation of tail dependence. Scandinavian Journal of Statistics 33(2), 307–335.

- Segers (2020) Segers, J. (2020). One-versus multi-component regular variation and extremes of Markov trees. Advances in Applied Probability 52(3), 855–878.

- Simpson et al. (2021) Simpson, E. S., J. L. Wadsworth, and J. A. Tawn (2021). A geometric investigation into the tail dependence of vine copulas. Journal of Multivariate Analysis 184, 104736.

- Zhu and Kurowicka (2022) Zhu, K. and D. Kurowicka (2022). Regular vines with strongly chordal pattern of (conditional) independence. Computational Statistics & Data Analysis 172, 107461.

SUPPLEMENTARY MATERIAL

In Appendix A, we provide detailed illustrations of a number of concepts, results and methods for a particular five-dimensional regular vine sequence. Appendix B contains the proofs of all results in the paper. A converse to Sklar’s theorem in Proposition 3.1 is stated and proved in Appendix C. For readers more familiar with exponent measure densities than with tail copula densities, a number of theoretical results are reformulated in terms of exponent measure densities in Appendix D. In Appendix E, it is shown that X-vine models are the tail limits of regular vine copula models in the sense of Definition 2.1. Finally, Appendix F.2 contains additional numerical results, both for the Monte Carlo simulations in Section 8 and the US flight data case study in Section 9.

Appendix A Example in dimension five

Consider the regular vine sequence on nodes specified by the following trees for :

In tree , consider the edge , which is also a node in tree . The proximity condition is satisfied since : note that is indeed a singleton, the unique element of which is the set . The edge has complete union , which is the union of the conditioning sets and . Further, has conditioning set , and conditioned set , which is itself the union of and . Writing this edge in its conditioned form gives better readability: . Fig. 6 shows the regular vine sequence, where the nodes and edges have been labeled using the conditioned forms.

Vine telescoping product

Given are scalars for non-empty such that for every . Also, write for disjoint and non-empty . Developing the product formula in Lemma 2.4 along the given regular vine sequence gives

| (A.1) |

Tail copula density decomposition

By Theorem 5.1, any 5-variate tail copula density can be decomposed along the given regular vine sequence as

| (A.2) |

where, for brevity, we write for and . The bivariate copula densities in the decomposition are given by formula (3.1) in Sklar’s theorm for tail copula densities (Proposition 3.1). The copulas associated with the edges in tree necessarily satisfy the simplifying assumption (see the paragraph right after Definition 3.4): for instance, the value of does not depend on , which is why we write rather than on the second line of (A.2).

Recursion

To completely specify the tail copula density in terms of bivariate components, we can calculate the arguments of the pair copulas through the recursive formula of Theorem 5.3, as explained also in the paragraph after that theorem. For example, in Eq. (A.2), starting from the first argument of the copula associated with the deepest edge, the conditional distribution function can be expressed in terms of the conditional distribution functions and and the bivariate copula via

| (A.3) |

where . Eq. (A.3) is the first identity in Eq. (5.4) applied to with , , and . In turn, the conditional distribution function can be expressed as (similarly for ),

where , and , i.e., in terms of bivariate (tail) copula densities , and only.

Unique-edge property

Proofs involving regular vine sequences often operate via a recursive argument in which a node and the edges that contain it are peeled off, leaving a regular vine sequence on elements; see for instance the proof of Theorem 5.3, which relies on Lemma B.2 below. Let us illustrate the latter for the regular vine sequence in Figure 6. The conditioned set of the deepest edge is . For each of the latter two nodes and for each level , there is a unique edge that contains this node in its complete union. For instance, for node these are the edges , , and ; moreover, node belongs to the conditioned set of each of these edges. Removing node and these four edges leaves a regular vine sequence on the four remaining elements , which is the sub-vine induced by on the node set .

Simulation